Exhibit 99.1

OceanFirst Financial Corp.

John R. Garbarino, Chairman, President & CEO

Michael J. Fitzpatrick, Executive Vice President & CFO

INVESTOR PRESENTATION

SEPTEMBER 27, 2005

NASDAQ: OCFC 1

OceanFirst Financial Corp.

This presentation contains certain forward-looking statements which are based on certain assumptions and describe future plans, strategies and expectations of the Company. These forward-looking statements are generally identified by use of the words “believe”, “expect”, “intend”, “anticipate”, “estimate”, “project”, or similar expressions. The Company’s ability to predict results or the actual effect of future plans or strategies is inherently uncertain. Factors which could have a material adverse effect on the operations of the Company and the subsidiaries include, but are not limited to, changes in interest rates, general economic conditions, legislative/regulatory changes, monetary and fiscal policies of the U.S. Government, including policies of the U.S. Treasury and the Federal Reserve Board, the quality or composition of the loan or investment portfolios, demand for loan products, deposit flows, competition, demand for financial services in the Company’s market area and accounting principles and guidelines. These risks and uncertainties should be considered in evaluating forward-looking statements and undue reliance should not be placed on such statements. The Company does not undertake – and specifically disclaims any obligation – to publicly release the result of any revisions which may be made to any forward-looking statements to reflect events or circumstances after the date of such statements or to reflect the occurrence of anticipated or unanticipated events.

NASDAQ: OCFC 2

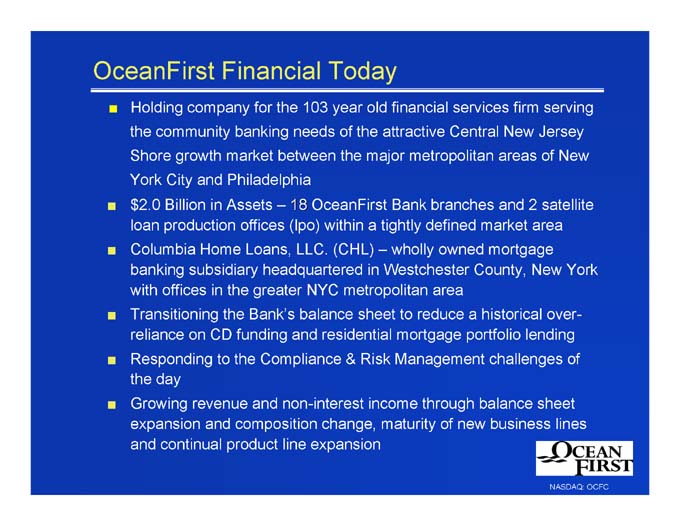

OceanFirst Financial Today

Holding company for the 103 year old financial services firm serving the community banking needs of the attractive Central New Jersey Shore growth market between the major metropolitan areas of New York City and Philadelphia

$2.0 Billion in Assets – 18 OceanFirst Bank branches and 2 satellite loan production offices (lpo) within a tightly defined market area

Columbia Home Loans, LLC. (CHL) – wholly owned mortgage banking subsidiary headquartered in Westchester County, New York with offices in the greater NYC metropolitan area

Transitioning the Bank’s balance sheet to reduce a historical over-reliance on CD funding and residential mortgage portfolio lending

Responding to the Compliance & Risk Management challenges of the day

Growing revenue and non-interest income through balance sheet expansion and composition change, maturity of new business lines and continual product line expansion

NASDAQ: OCFC 3

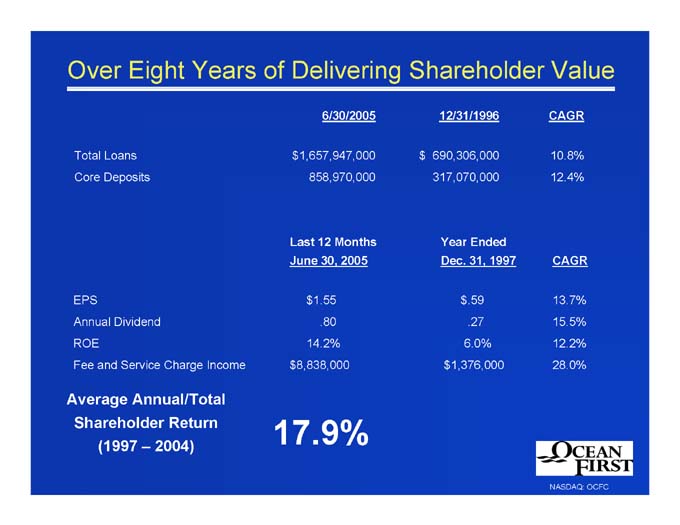

Over Eight Years of Delivering Shareholder Value

6/30/2005 12/31/1996 CAGR

Total Loans $1,657,947,000 $ 690,306,000 10.8%

Core Deposits 858,970,000 317,070,000 12.4%

Last 12 Months Year Ended

June 30, 2005 Dec. 31, 1997 CAGR

EPS $1.55 $.59 13.7%

Annual Dividend .80 .27 15.5%

ROE 14.2% 6.0% 12.2%

Fee and Service Charge Income $8,838,000 $1,376,000 28.0%

Average Annual/Total

Shareholder Return

(1997 – 2004)

17.9%

NASDAQ: OCFC 4

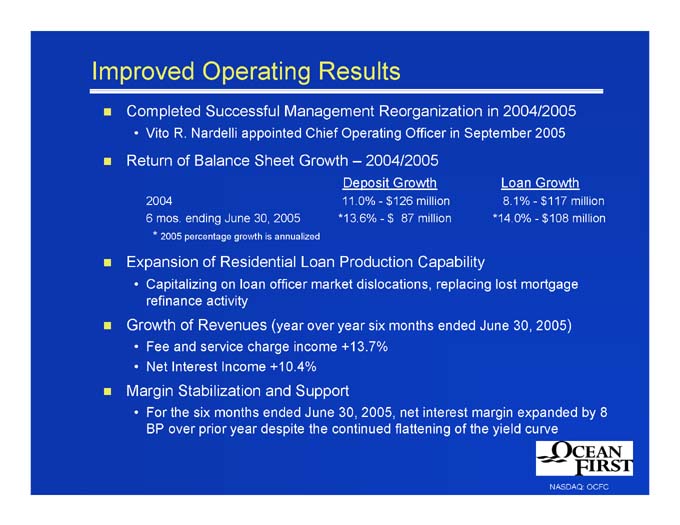

Improved Operating Results

Completed Successful Management Reorganization in 2004/2005

Vito R. Nardelli appointed Chief Operating Officer in September 2005

Return of Balance Sheet Growth – 2004/2005

Deposit Growth Loan Growth

2004 11.0% - $126 million 8.1% - $117 million

6 mos. ending June 30, 2005 *13.6% - $ 87 million *14.0% - $108 million

* 2005 percentage growth is annualized

Expansion of Residential Loan Production Capability

Capitalizing on loan officer market dislocations, replacing lost mortgage refinance activity

Growth of Revenues (year over year six months ended June 30, 2005)

Fee and service charge income +13.7%

Net Interest Income +10.4%

Margin Stabilization and Support

For the six months ended June 30, 2005, net interest margin expanded by 8 BP over prior year despite the continued flattening of the yield curve

NASDAQ: OCFC 5

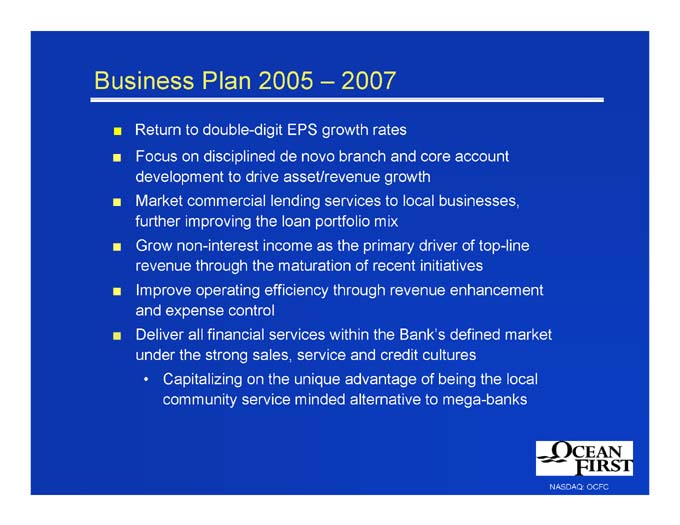

Business Plan 2005 – 2007

Return to double-digit EPS growth rates

Focus on disciplined de novo branch and core account development to drive asset/revenue growth

Market commercial lending services to local businesses, further improving the loan portfolio mix

Grow non-interest income as the primary driver of top-line revenue through the maturation of recent initiatives

Improve operating efficiency through revenue enhancement and expense control

Deliver all financial services within the Bank’s defined market under the strong sales, service and credit cultures

Capitalizing on the unique advantage of being the local community service minded alternative to mega-banks

NASDAQ: OCFC 6

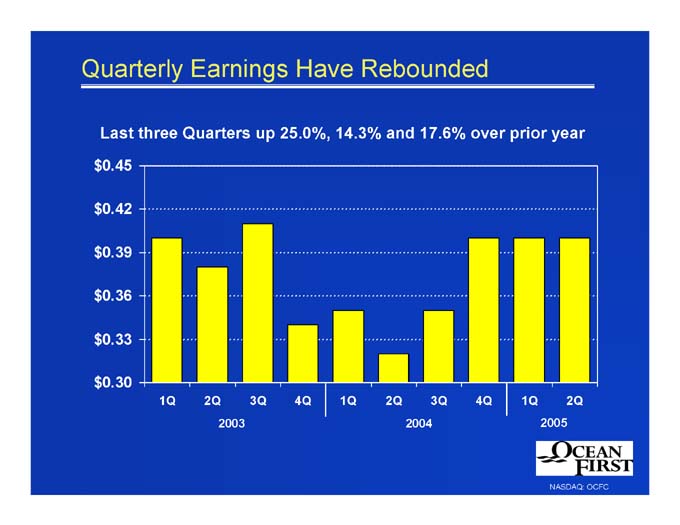

Quarterly Earnings Have Rebounded

Last three Quarters up 25.0%, 14.3% and 17.6% over prior year

$0.45

$0.42

$0.39

$0.36

$0.33

$0.30

1Q

4Q

3Q

2Q

1Q

4Q

3Q

2Q

1Q

2Q

2004

2003

2005

NASDAQ: OCFC 7

Retail Branch In-Market Growth

18 Branches in tightly defined market

provide significant presence, market share

Successful de novo branching and core deposit generation

From 1996 through 2Q ‘05, 10 branches were opened with an average core deposit mix of 73%

Additional current branch activity in our growth market

Freehold branch opened March 2005

Whiting branch to be relocated to a more convenient, prominent location (1Q ‘06)

New Little Egg Harbor branch scheduled to open (2Q ‘06)

New Wall branch scheduled to open 1Q ‘07

NASDAQ: OCFC 8

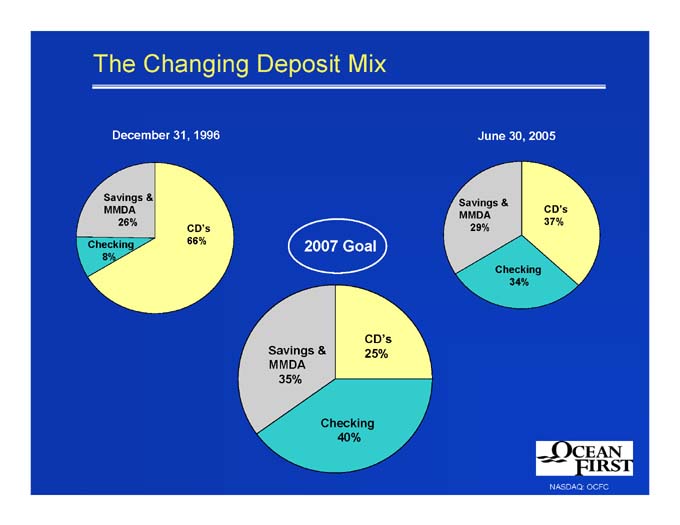

The Changing Deposit Mix

June 30, 2005

December 31, 1996

Savings &

MMDA

29%

Savings &

MMDA

26%

CD’s

37%

CD’s

66%

Checking

8%

2007 Goal

Checking

34%

CD’s

25%

Savings &

MMDA

35%

Checking

40%

NASDAQ: OCFC 9

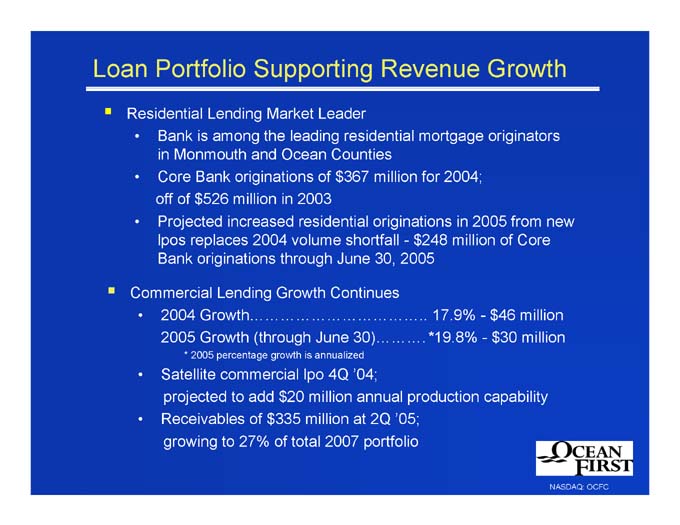

Loan Portfolio Supporting Revenue Growth

Residential Lending Market Leader

Bank is among the leading residential mortgage originators in Monmouth and Ocean Counties

Core Bank originations of $367 million for 2004;

off of $526 million in 2003

Projected increased residential originations in 2005 from new lpos replaces 2004 volume shortfall - $248 million of Core Bank originations through June 30, 2005

Commercial Lending Growth Continues

2004 Growth 17.9% - $46 million

2005 Growth (through June 30) *19.8% - $30 million

* 2005 percentage growth is annualized

Satellite commercial lpo 4Q ‘04;

projected to add $20 million annual production capability

Receivables of $335 million at 2Q ’05;

growing to 27% of total 2007 portfolio

NASDAQ: OCFC 10

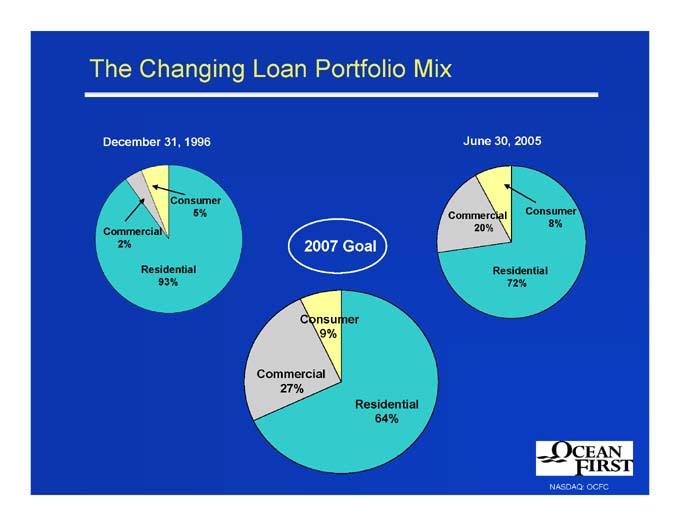

The Changing Loan Portfolio Mix

December 31, 1996

June 30, 2005

Consumer

5%

Commercial

20%

Consumer

8%

Commercial

2%

2007 Goal

Residential

72%

Residential

93%

Consumer

9%

Commercial

27%

Residential

64%

NASDAQ: OCFC 11

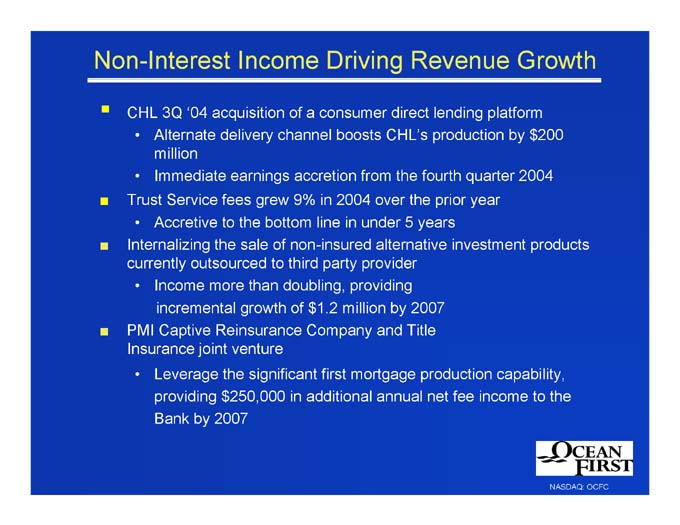

Non-Interest Income Driving Revenue Growth

CHL 3Q ‘04 acquisition of a consumer direct lending platform

Alternate delivery channel boosts CHL’s production by $200 million

Immediate earnings accretion from the fourth quarter 2004

Trust Service fees grew 9% in 2004 over the prior year

Accretive to the bottom line in under 5 years

Internalizing the sale of non-insured alternative investment products currently outsourced to third party provider

Income more than doubling, providing

incremental growth of $1.2 million by 2007

PMI Captive Reinsurance Company and Title Insurance joint venture

Leverage the significant first mortgage production capability, providing $250,000 in additional annual net fee income to the Bank by 2007

NASDAQ: OCFC 12

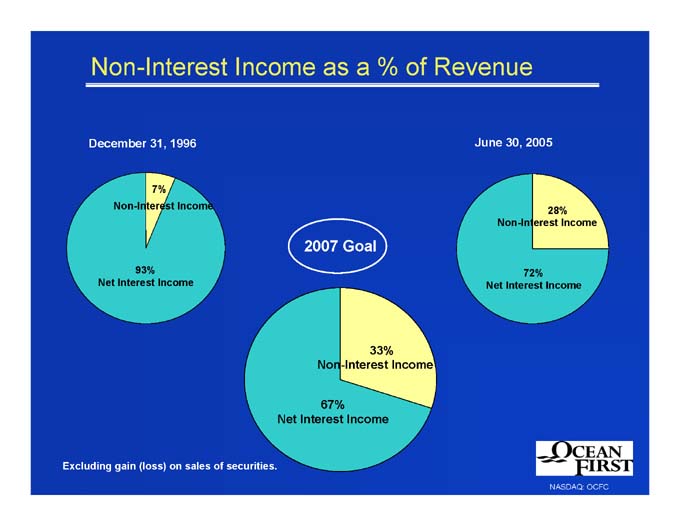

Non-Interest Income as a % of Revenue

December 31, 1996

June 30, 2005

7%

Non-Interest Income

28%

Non-Interest Income

2007 Goal

72%

Net Interest Income

93%

Net Interest Income

33%

Non-Interest Income

67%

Net Interest Income

Excluding gain (loss) on sales of securities.

NASDAQ: OCFC 13

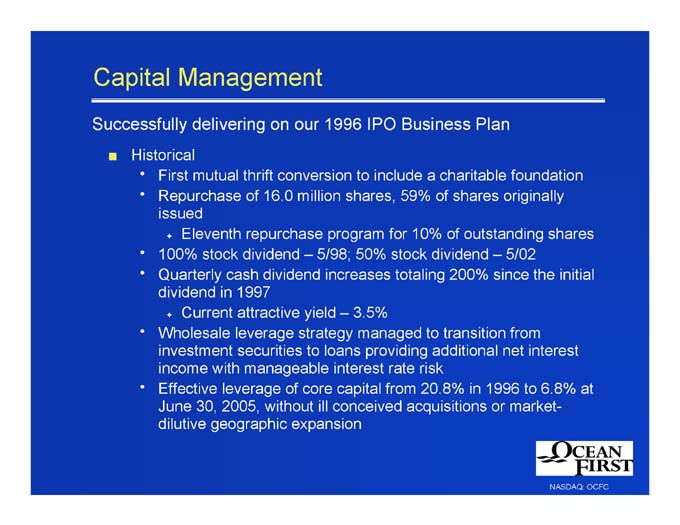

Capital Management

Successfully delivering on our 1996 IPO Business Plan

Historical

First mutual thrift conversion to include a charitable foundation

Repurchase of 16.0 million shares, 59% of shares originally issued

Eleventh repurchase program for 10% of outstanding shares

100% stock dividend – 5/98; 50% stock dividend – 5/02

Quarterly cash dividend increases totaling 200% since the initial dividend in 1997

Current attractive yield – 3.5%

Wholesale leverage strategy managed to transition from investment securities to loans providing additional net interest income with manageable interest rate risk

Effective leverage of core capital from 20.8% in 1996 to 6.8% at June 30, 2005, without ill conceived acquisitions or market-dilutive geographic expansion

NASDAQ: OCFC 14

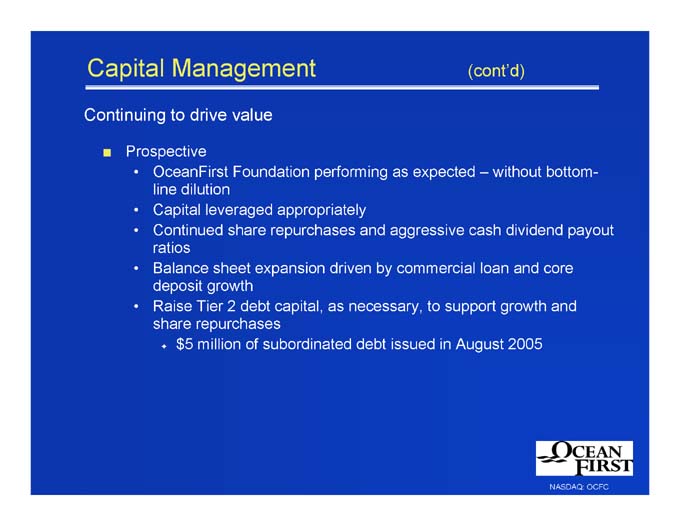

Capital Management (cont’d)

Continuing to drive value

Prospective

OceanFirst Foundation performing as expected – without bottom-line dilution

Capital leveraged appropriately

Continued share repurchases and aggressive cash dividend payout ratios

Balance sheet expansion driven by commercial loan and core deposit growth

Raise Tier 2 debt capital, as necessary, to support growth and share repurchases

$5 million of subordinated debt issued in August 2005

NASDAQ: OCFC 15

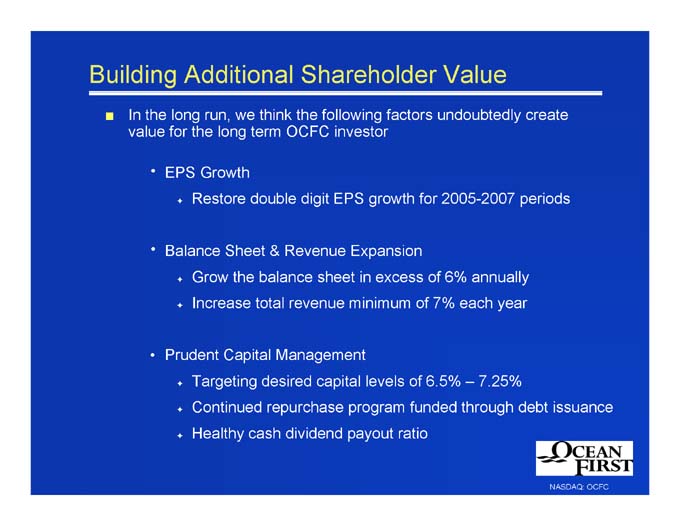

Building Additional Shareholder Value

In the long run, we think the following factors undoubtedly create value for the long term OCFC investor

EPS Growth

Restore double digit EPS growth for 2005-2007 periods

Balance Sheet & Revenue Expansion

Grow the balance sheet in excess of 6% annually

Increase total revenue minimum of 7% each year

Prudent Capital Management

Targeting desired capital levels of 6.5% – 7.25%

Continued repurchase program funded through debt issuance

Healthy cash dividend payout ratio

NASDAQ: OCFC 16

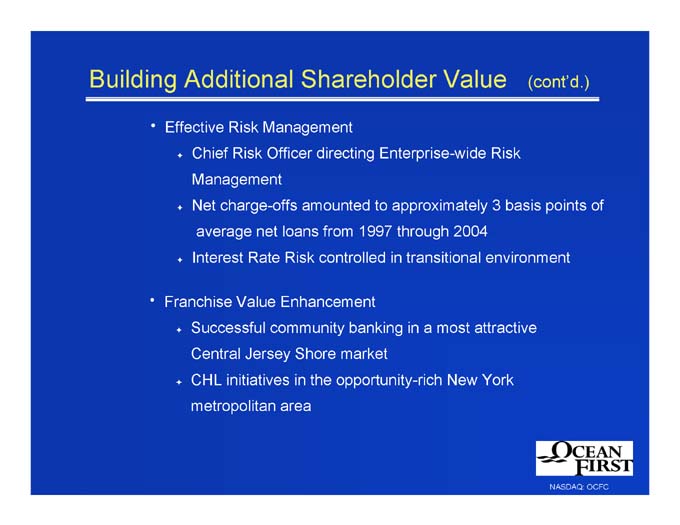

Building Additional Shareholder Value (cont’d.)

Effective Risk Management

Chief Risk Officer directing Enterprise-wide Risk

Management

Net charge-offs amounted to approximately 3 basis points of

average net loans from 1997 through 2004

Interest Rate Risk controlled in transitional environment

Franchise Value Enhancement

Successful community banking in a most attractive

Central Jersey Shore market

CHL initiatives in the opportunity-rich New York

metropolitan area

NASDAQ: OCFC 17

Thank you for your interest in

OceanFirst

Financial Corp.

NASDAQ: OCFC 18