Exhibit 99.2

FOURTH QUARTER EARNINGS CALL February 9, 2018

Forward Looking Statements This slide presentation contains statements regarding management’s expectations and objectives for future periods as well as forecasts and estimates regarding the impact of the Tax Cuts and Jobs Act of 2017, 2018 IIC guidance, 2017-2019 capital expenditures, 2017-2019 weighted average ratebase, equity needs and sources, and general earnings sensitivities. It also includes assumptions regarding capital expenditures, authorized rate base, authorized cost of capital, and certain other factors. These statements and other statements that are not purely historical constitute forward-looking statements that are necessarily subject to various risks and uncertainties. Actual results may differ materially from current expectations. PG&E Corporation and the Utility are not able to predict all the factors that may affect future results. Factors that could cause actual results to differ materially include, but are not limited to: ï,· the impact of the Northern California wildfires, including the costs of restoration of service to customers and repairs to the Utility’s facilities, and whether the Utility is able to recover such costs through CEMA; the timing and outcome of the wildfire investigations; whether the Utility may have liability associated with these fires; if liable for one or more fires, whether the Utility would be able to recover all or part of such costs through insurance or through regulatory mechanisms, to the extent insurance is not available or exhausted; and potential liabilities in connection with fines or penalties that could be imposed on the Utility if the CPUC or any other law enforcement agency brought an enforcement action and determined that the Utility failed to comply with applicable laws and regulations;ï,· the impact of the Tax Cuts and Jobs Act of 2017, and the timing and outcome of the CPUC decision related to the Utility’s future filings in connection with the impact of the Tax Cuts and Jobs Act of 2017 on the Utility’s rate cases and its implementation plan;ï,· the Utility’s ability to efficiently manage capital expenditures and its operating and maintenance expenses within the authorized levels of spending and timely recover its costs through rates, and the extent to which the Utility incurs unrecoverable costs that are higher than the forecasts of such costs; ï,· the timing and outcomes of the TO18 and TO19 rate cases and other ratemaking and regulatory proceedings; ï,· the timing and outcomes of the ex parte OII and the safety culture OII;ï,· the timing and outcome of the Butte fire litigation; the timing and outcome of any proceeding to recover costs in excess of insurance from customers, if any; the effect, if any, that the SED’s $8.3 million citations issued in connection with the Butte fire may have on the Butte fire litigation; and whether additional investigations and proceedings in connection with the Butte fire will be opened and any additional fines or penalties imposed on the Utility;ï,· whether the CPUC approves the Utility’s application to establish a WEMA to track wildfire expenses and to preserve the opportunity for the Utility to request recovery of wildfire costs in excess of insurance at a future date, and the outcome of any potential request to recover such costs; ï,· whether the Utility can continue to obtain insurance and whether insurance coverage is adequate for future losses or claims;ï,· the outcome of the probation and the monitorship, the timing and outcomes of the debarment proceeding, the SED’s unresolved enforcement matters relating to the Utility’s compliance with naturalgas-related laws and regulations, and other investigations that have been or may be commenced, and the ultimate amount of fines, penalties, and remedial and other costs that the Utility may incur as a result;ï,· the ability of PG&E Corporation and the Utility to access capital markets and other sources of debt and equity financing in a timely manner on acceptable terms;ï,· changes in credit ratings which could, among other things, result in higher borrowing costs and fewer financing options, especially if PG&E Corporation or the Utility were to lose their investment grade credit ratings; andï,· the other factors disclosed in PG&E Corporation and the Utility’s joint annual report on Form10-K for the year ended December 31, 2017 and other reports filed with the SEC, which are available on PG&E Corporation’s website at www.pgecorp.com and on the SEC website at www.sec.gov. This presentation is not complete without the accompanying statements made by management during the webcast conference call held on February 9, 2018. The statements in this presentation are made as of February 9, 2018. PG&E Corporation undertakes no obligation to update information contained herein. This presentation, including Appendices, and the accompanying press release were attached to PG&E Corporation’s Current Report on Form8-K that was furnished to the SEC on February 9, 2018 and, along with the replay of the conference call, is also available on PG&E Corporation’s website at www.pgecorp.com. 2

Inverse Condemnation Strategies Regulatory Requested rehearing of CPUC’s decision in San Diego Gas & Electric’s wildfire cost recovery proceeding Legal Asked trial court in Butte fire case to reconsider interpretation of the application of inverse condemnation Legislative Informing lawmakers on impacts of climate change and the need for comprehensive solutions

Tax Cuts and Jobs Act Expected Impact Annual reduction in customer revenue driven ~$500M Lower Customer Bills by lower corporate tax rate annual revenue reduction Faster net operating loss amortization and 2020 Cash Tax Payments ~1 year acceleration of federal tax payments estimated year federal tax payments begin Higher ratebase growth and increased earnings primarily driven by elimination of ~$800M Ratebase Growth bonus depreciation; $500M in 2018 and an incremental ratebase additional $300M in 2019 in 2019 Higher financing needs driven by incremental ~$400M Financing Needs ratebase growth; additional equity needs of incremental equity ~$200M in 2018 and 2019 needs through 2019 Tax Cuts and Jobs Act results in lower customer bills and higher ratebase growth Tax reform implementation is subject to CPUC review. See the Forward Looking Statements for factors that could cause actual results to differ materially from the guidance presented and underlying assumptions. 4

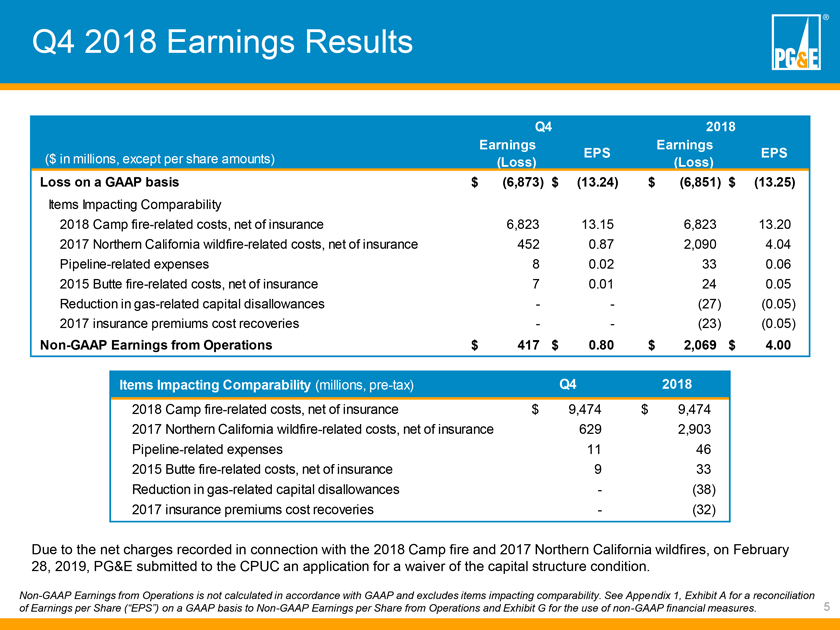

Q4 2017 Earnings Results Q4 2017 Earnings Earnings EPS EPS (millions) (millions) Earnings on a GAAP basis $ 114 $ 0.22 $ 1,646 $ 3.21 Items Impacting Comparability Tax Cuts and Jobs Act transition impact (1) 147 0.29 147 0.29 Northern California wildfire-related costs 49 0.09 49 0.09 Butte fire-related costs, net of insurance 9 0.02 36 0.07 Pipeline related expenses 7 0.01 52 0.10 Legal and regulatory related expenses 1 — 6 0.01 Fines and penalties — — 47 0.09 Diablo Canyon settlement-related disallowance — — 32 0.06 GT&S revenue timing impact — — (88) (0.17) Net benefit from derivative litigation settlement — — (38) (0.07) Earnings from Operations $ 327 $ 0.63 $ 1,889 $ 3.68 Items Impacting Comparability (millions,pre-tax) Q4 2017 Northern California wildfire-related costs $ 82 $ 82 Butte fire-related costs, net of insurance 15 60 Pipeline related expenses 12 89 Legal and regulatory related expenses 2 10 Fines and penalties — 71 Diablo Canyon settlement-related disallowance — 47 GT&S revenue timing impact — (150) Net benefit from derivative litigation settlement — (65) (1) Tax Cuts and Jobs Act transition impact reflects anafter-tax amount. Earnings from Operations is not calculated in accordance with GAAP and excludes items impacting comparability. See Appendix 2, Exhibit A for a reconciliation of Earnings per Share (“EPS”) on a GAAP basis to Earnings from Operations and Exhibit G for the use ofnon-GAAP financial measures. 5

Q4 2017: Quarter over Quarter Comparison Earnings per Share from Operations $1.40 ($0.33) $1.20 ($0.18) $1.00 ($0.09) $0.80 ($0.06) ($0.02) ($0.02) $1.33 ($0.05) $0.05 $0.60 $0.40 $0.63 $0.20 $0.00 Q4 2016 EPS Timing of 2015 Timing of Impact of 2017 Timing of CEE Incentive Increase in Miscellaneous Growth in Rate Q4 2017 EPS from GT&S Taxes GRC Decision Operational Award Shares Base Earnings from Operations Revenue Spend Outstanding Operations Impact Earnings from Operations is not calculated in accordance with GAAP and excludes items impacting comparability. See Appendix 2, Exhibit A for a reconciliation of Earnings per Share (“EPS”) on a GAAP basis to Earnings from Operations and Exhibit G for the use ofnon-GAAP financial measures. 6

2018 Assumptions Capital Expenditures Authorized Ratebase (weighted average) ($ millions) ($ billions) 2018 2018 General Rate Case 3,900 General Rate Case 26.1 Gas Transmission and Storage 1,000 Gas Transmission and Storage 3.8 Transmission Owner 19 1,400 Transmission Owner 7.1 Total Cap Ex $6.3 billion Total Ratebase $37.0 billion Other Factors Affecting Authorized Cost of Capital* Earnings from Operations Return on Equity: 10.25% + Incentive revenues, efficiencies and other benefits—GT&S amounts not requested Equity Ratio: 52% - Ex parte settlement GT&S revenue adjustment—Insurance premiums *CPUC authorized CWIP earnings: offset bybelow-the-line costs See the Forward Looking Statements for factors that could cause actual results to differ materially from the guidance presented and underlying assumptions. 7

2018 Items Impacting Comparability Guidance ($ millions,pre-tax) 2018 Pipeline-related expenses (1) 35—60 Butte fire-related costs (2) 30—60 Northern California wildfire-related costs, net of insurance (3) 35—50 Estimated 2018 Items Impacting Comparability Guidance Total $100—170 (1) Total cost ofrights-of-way program expected to range from $450 million to $475 million. (2) Butte fire-related costs reflect legal costs associated with the Butte fire. Range excludes any potential claims-related impacts. (3) Northern California wildfire-related costs, net of insurance reflects legal and other costs associated with the Northern California wildfires. Range excludes any potential claims-related impacts. See the Forward Looking Statements for factors that could cause actual results to differ materially from the guidance presented and underlying assumptions. See Appendix 2, Exhibit E for PG&E Corporation’s 2018 Items Impacting Comparability Guidance and Exhibit G for Use ofNon-GAAP Financial Measures. 8

Robust Cap Ex Supports Strong Returns Capital Expenditures ($ in B) 2017-2019 $6.3B ~$6B $5.8B 2017 Recorded 2018 2019 General Rate Case Gas Transmission & Storage Electric Transmission Owner Range See the Forward Looking Statements for factors that could cause actual results to differ materially from the guidance presented and underlying assumptions. 9

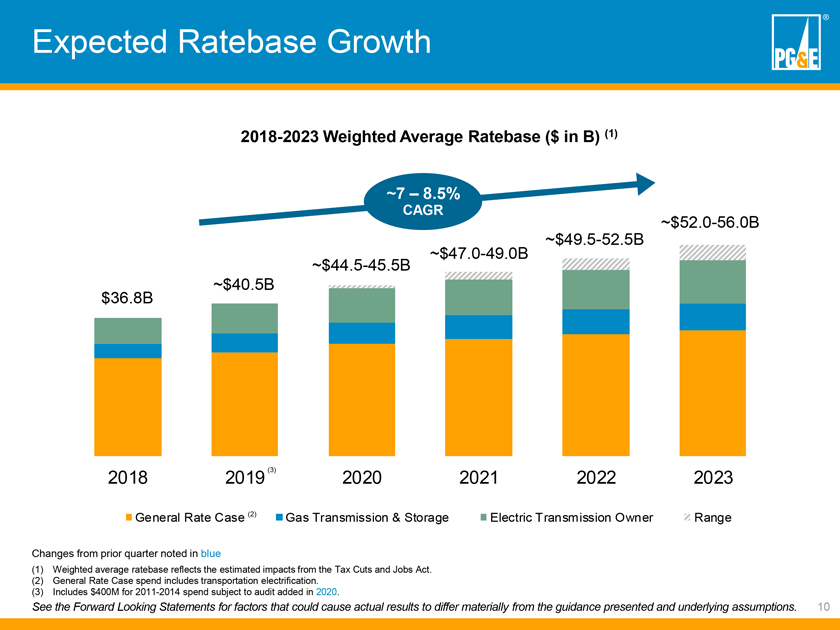

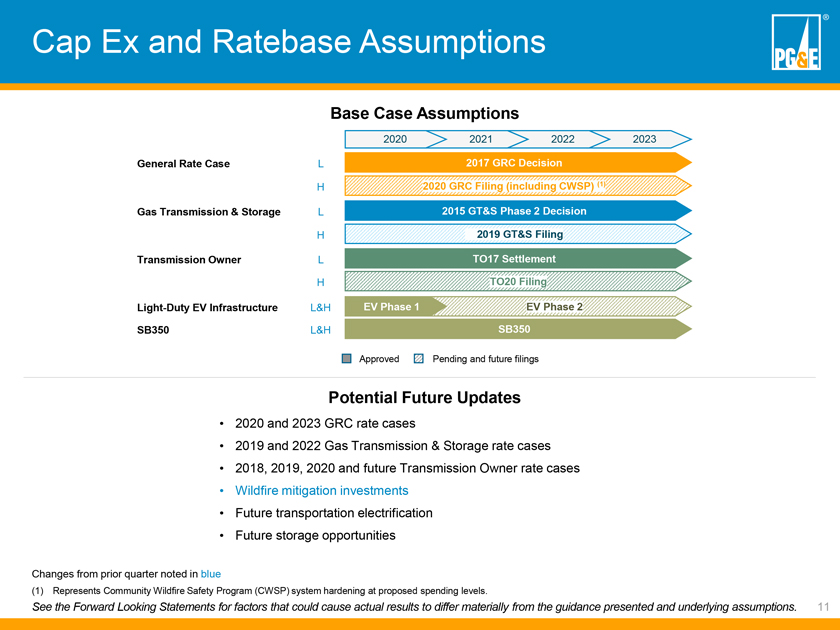

Ratebase Supports Strong Returns 2017-2019 Weighted Average Ratebase ($ in B) (1) ~7.5—8% CAGR $37.0B ~$40B $34.4B 2017 2018 2019 General Rate Case Gas Transmission & Storage Electric Transmission Owner Range Base Case Assumptions Potential Future Updates 2018 2019 • 2019 Gas Transmission & Storage rate case GRC L 2017 GRC Decision • 2018 and 2019 Transmission Owner rate cases H 2017 GRC Decision • Future transportation electrification (e.g., January 2017 GT&S L 2015 GT&S Phase 2 Decision medium and heavy duty vehicle filing) H 2015 GT&S Phase 2 Decision 2019 GT&S Filing • State infrastructure modernization (e.g., rail and water TO L TO19 Filing TO17 Settlement projects) H TO19 Filing • Future storage opportunities Other Light-Duty Electric Vehicle Infrastructure Program Approved Pending and future filings (1) Weighted average ratebase in 2018 and 2019 reflect the estimated impacts from the Tax Cuts and Jobs Act. Changes from prior quarter noted in blue See the Forward Looking Statements for factors that could cause actual results to differ materially from the guidance presented and underlying assumptions. 10

Equity Needs and Sources Needs Sources Previous Guidance (Internal Programs) Internal Programs (Excluding DRP (1)) + Tax Reform + Cash from Dividend Suspension + Items Impacting Comparability December 31, 2017 shares outstanding: ~515 million (1) Dividend Reinvestment Plan. See the Forward Looking Statements for factors that could cause actual results to differ materially from the guidance presented and underlying assumptions. 11

Appendix

Appendix 1 – Incremental Equity Factors Incremental Equity Factors for Unrecovered Costs Equity Impacting Event MultiplierNon-deductible cash charges 100% Cash expenses 72%Non-cash charges (1) 36% (1) Multiplier applies at time of accrual; additional 36% applies at time of cash charge. 13

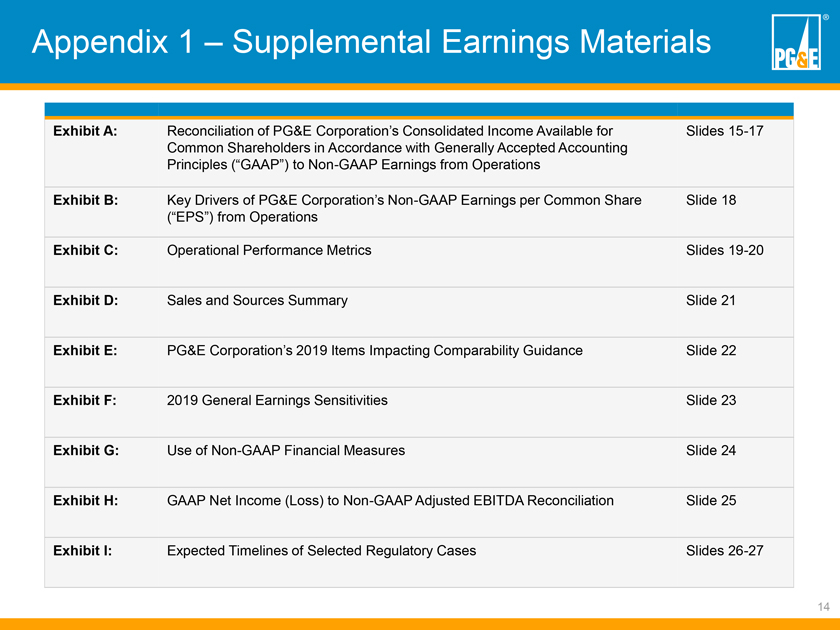

Appendix 2 – Supplemental Earnings Materials Exhibit A: Reconciliation of PG&E Corporation’s Consolidated Income Available Slides15-16 for Common Shareholders in Accordance with Generally Accepted Accounting Principles to Earnings from Operations Exhibit B: Key Drivers of PG&E Corporation’s Earnings per Common Share Slide 17 from Operations Exhibit C: Operational Performance Metrics Slides18-19 Exhibit D: Sales and Sources Summary Slide 20 Exhibit E: PG&E Corporation’s 2018 Items Impacting Comparability Guidance Slides 21 Exhibit F: 2018 General Earnings Sensitivities Slide 22 Exhibit G: Use ofNon-GAAP Financial Measures Slide 23 Exhibit H: Expected Timelines of Selected Regulatory Cases Slides24-28 14

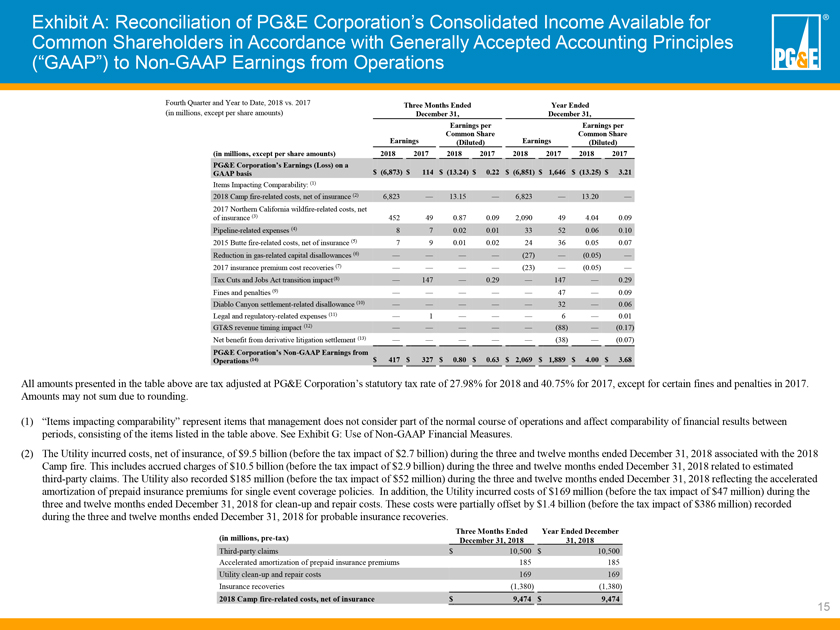

Exhibit A: Reconciliation of PG&E Corporation’s Consolidated Income Available for Common Shareholders in Accordance with Generally Accepted Accounting Principles (“GAAP”) to Earnings from Operations Page 1 of 2 Fourth Quarter and Year to Date, 2017 vs. 2016 Three Months Ended December 31, Twelve Months Ended December 31, (in millions, except per share amounts) Earnings per Earnings per Earnings Common Share Earnings Common Share (Diluted) (Diluted) 2017 2016 2017 2016 2017 2016 2017 2016 PG&E Corporation’s Earnings on a GAAP basis $ 114 $ 692 $ 0.22 $ 1.36 $ 1,646 $ 1,393 $ 3.21 $ 2.78 Items Impacting Comparability: (1) Tax Cuts and Jobs Act transition impact (2) 147 — 0.29 — 147 — 0.29 -Northern California wildfire-related costs (3) 49 — 0.09 — 49 — 0.09 -Butte fire-related costs, net of insurance (4) 9 27 0.02 0.05 36 137 0.07 0.27 Pipeline related expenses (5) 7 20 0.01 0.04 52 67 0.10 0.13 Legal and regulatory related expenses (6) 1 11 — 0.02 6 43 0.01 0.09 Fines and penalties (7) — 101 — 0.20 47 307 0.09 0.61 Diablo Canyon settlement-related disallowance (8) — — — — 32 — 0.06-GT&S revenue timing impact (9) — (193) — (0.38) (88) (193) (0.17) (0.38) Net benefit from derivative litigation settlement (10) — — — — (38) — (0.07)-GT&S capital disallowance — 17 — 0.04 — 130 — 0.26 PG&E Corporation’s Earnings from Operations (11) $ 327 $ 675 $ 0.63 $ 1.33 $ 1,889 $ 1,884 $ 3.68 $ 3.76 All amounts presented in the table above are tax adjusted at PG&E Corporation’s statutory tax rate of 40.75 percent, except as indicated below. (1) “Items impacting comparability” represent items that management does not consider part of the normal course of operations and affect comparability of financial results between periods. See Exhibit G: Use ofNon-GAAP Financial Measures. (2) PG&E Corporation, on a consolidated basis, incurred aone-time charge of $147 million during the three and twelve months ended December 31, 2017, as a result of the Tax Cuts and Jobs Act, which was signed into law on December 22, 2017. The Utility’s charge of $64 million was related to deferred tax assets not reflected in authorized revenue requirements, such as deferred tax assets associated with disallowed plant, and PG&E Corporation’s charge of $83 million was primarily related to net operating loss carryforwards and compensation-related deferred tax assets. (3) The Utility incurred costs of $82 million (before the tax impact of $33 million) during the three and twelve months ended December 31, 2017, associated with the Northern California wildfires. This includes charges of $64 million (before the tax impact of $26 million) for the three and twelve months ended December 31, 2017, for the reinstatement of liability insurance coverage and $18 million (before the tax impact of $7 million) during the three and twelve months ended December 31, 2017, for legal and other expenses. Three Months Ended Twelve Months Ended (in millions,pre-tax) December 31, 2017 December 31, 2017 Liability Insurance $ 64 $ 64 Legal and Other 18 18 Northern California wildfire-related costs $ 82 $ 82 (4) The Utility incurred costs, net of insurance, of $15 million (before the tax impact of $6 million) and $60 million (before the tax impact of $24 million) during the three and twelve months ended December 31, 2017, respectively, associated with the Butte fire. This includes accrued charges of $350 million (before the tax impact of $143 million) during the twelve months ended December 31, 2017, related to estimated third-party claims. The Utility also incurred charges of $15 million (before the tax impact of $6 million) and $60 million (before the tax impact of $25 million) during the three and twelve months ended December 31, 2017, respectively, for legal costs. These costs were partially offset by $350 million (before the tax impact of $143 million) recorded during the twelve months ended December 31, 2017, for expected insurance recoveries. 15

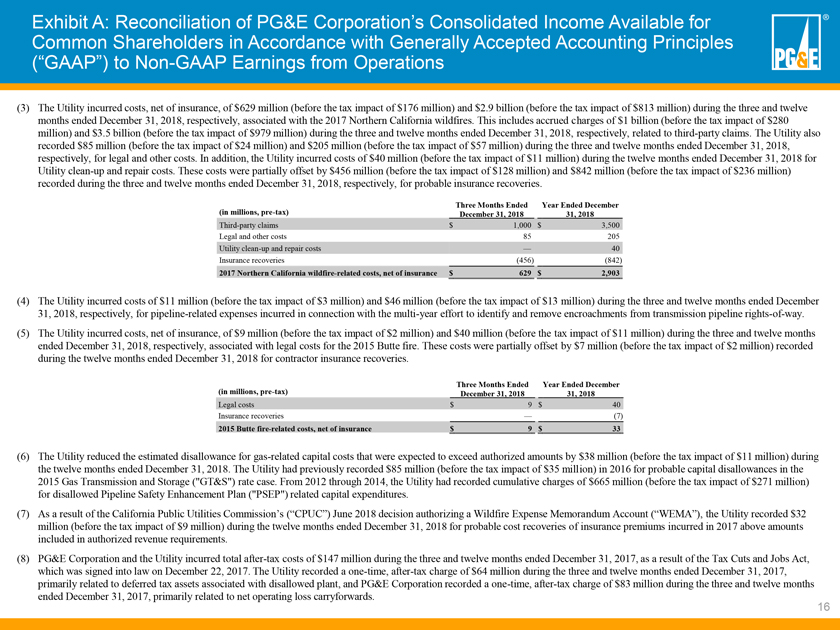

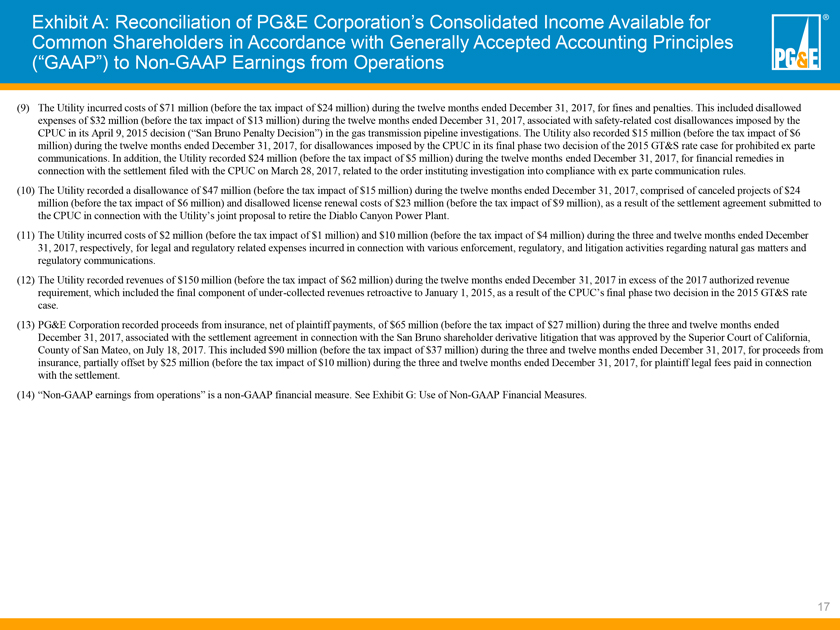

Exhibit A: Reconciliation of PG&E Corporation’s Consolidated Income Available for Common Shareholders in Accordance with Generally Accepted Accounting Principles (“GAAP”) to Earnings from Operations Page 2 of 2 Three Months Ended Twelve Months Ended (in millions,pre-tax) December 31, 2017 December 31, 2017 Third-party claims $— $ 350 Legal costs 15 60 Insurance recoveries— (350) Butte fire-related costs, net of insurance $ 15 $ 60 (5) The Utility incurred costs of $12 million (before the tax impact of $5 million) and $89 million (before the tax impact of $37 million) during the three and twelve months ended December 31, 2017, respectively, for pipeline related expenses incurred in connection with the multi-year effort to identify and remove encroachments from transmission pipelinerights-of-way. (6) The Utility incurred costs of $2 million (before the tax impact of $1 million) and $10 million (before the tax impact of $4 million) during the three and twelve months ended December 31, 2017, respectively, for legal and regulatory related expenses incurred in connection with various enforcement, regulatory, and litigation activities regarding natural gas matters and regulatory communications. (7) The Utility incurred costs of $71 million (before the tax impact of $24 million) during the twelve months ended December 31, 2017, for fines and penalties. This includes costs of $32 million (before the tax impact of $13 million) during the twelve months ended December 31, 2017, associated with safety-related cost disallowances imposed by the California Public Utilities Commission (“CPUC”) in its April 9, 2015 decision (“San Bruno Penalty Decision”) in the gas transmission pipeline investigations. The Utility also recorded $15 million (before the tax impact of $6 million) during the twelve months ended December 31, 2017, for penalty imposed by the CPUC in its final phase two decision of the 2015 Gas Transmission and Storage (“GT&S”) rate case for prohibited ex parte communications. In addition, the Utility recorded $24 million (before the tax impact of $5 million) during the twelve months ended December 31, 2017, in connection with the proposed decision (“PD”) in the Order Instituting an Investigation into Compliance with Ex Parte Communication Rules (“ex parte OII”). Three Months Ended Twelve Months Ended (in millions,pre-tax) December 31, 2017 December 31, 2017 Charge for disallowed expense $— $ 32 GT&S ex parte penalty — 15 Ex parte OII PD (tax deductible) — 12 Ex parte OII PD (not tax deductible) — 12 Fines and penalties $— $ 71 (8) Consistent with the CPUC decision adopted on January 11, 2018 in connection with the retirement of the Diablo Canyon Power Plant, the Utility recorded a disallowance of $47 million (before the tax impact of $15 million) during the twelve months ended December 31, 2017, comprised of cancelled projects of $24 million (before the tax impact of $6 million) and disallowed license renewal costs of $23 million (before the tax impact of $9 million). (9) As a result of the CPUC’s final phase two decision in the 2015 GT&S rate case, during the twelve months ended December 31, 2017, the Utility recorded revenues of $150 million (before the tax impact of $62 million) in excess of the 2017 authorized revenue requirement, which includes the final component of under-collected revenues retroactive to January 1, 2015. (10) PG&E Corporation recorded proceeds from insurance, net of plaintiff payments, of $65 million (before the tax impact of $27 million) during the twelve months ended December 31, 2017, associated with the settlement agreement in connection with the shareholder derivative litigation that was approved by the court on July 18, 2017. This includes $90 million (before the tax impact of $37 million) for insurance recoveries partially offset by $25 million (before the tax impact of $10 million) for plaintiff legal fees paid in connection with the settlement during the twelve months ended December 31, 2017. (11) “Earnings from operations” is anon-GAAP financial measure. See Exhibit G: Use ofNon-GAAP Financial Measures. 16

Exhibit B: Key Drivers of PG&E Corporation’s Earnings per Common Share (“EPS”) from Operations Fourth Quarter and Year to Date, 2017 vs. 2016 (in millions, except per share amounts) Three Months Ended Twelve Months Ended December 31, 2017 December 31, 2017 Earnings per Earnings Common Common Share Share Earnings (Diluted) Earnings (Diluted) 2016 Earnings from Operations (1) $ 675 $ 1.33 $ 1,884 $ 3.76 Timing of 2015 GT&S revenue impact (2) (172) (0.33) — Timing of taxes (3) (90) (0.18) — Impact of 2017 GRC decision (4) (47) (0.09) (139) (0.27) Timing of operational spend (5) (31) (0.06) — CEE Incentive Award (6) (10) (0.02) (10) (0.02) Increase in shares outstanding— (0.02) —(0.08) Tax benefit on stock compensation (7)—— 31 0.06 Miscellaneous (23) (0.05) 20 0.03 Growth in rate base earnings (8) 25 0.05 103 0.20 2017 Earnings from Operations (1) $ 327 $ 0.63 $ 1,889 $ 3.68 (1) See Exhibit A for a reconciliation of EPS on a GAAP basis to EPS from Operations. All amounts presented in the table above are tax adjusted at PG&E Corporation’s statutory tax rate of 40.75 percent, except for tax benefits on stock compensation. See Footnote 3 below. (2) Represents the impact in 2016 of the delay in the Utility’s 2015 GT&S rate case. The CPUC issued its final phase two decision on December 1, 2016, delaying recognition of the full 2016 revenue increase until the fourth quarter of 2016. (3) Represents the timing of taxes reportable in quarterly statements in accordance with Accounting Standards Codification 740 and results from variances in the percentage of quarterly earnings to annual earnings. (4) Represents the impact of lower tax repair benefits as a result of the CPUC’s final decision in the 2017 GRC proceeding. (5) Represents timing of operational expense spending during the three months ended December 31, 2017 as compared to the same period in 2016. (6) Represents the Customer Energy Efficiency (“CEE”) incentive award received during the fourth quarter of 2016, with no similar amount in 2017. The 2017 award of $21.9 million was fully offset by the reduction approved by the CPUC related to the rehearing of the 2006 – 2008 CEE incentive awards. (7) Represents the excess tax benefit related to share-based compensation awards that vested during the twelve months ended December 31, 2017. Pursuant to ASU2016-09, Compensation – Stock Compensation (Topic 718), which PG&E Corporation and the Utility adopted in 2016, excess tax benefits associated with vested awards are reflected in net income. (8) Represents the impact of the increase in rate base authorized in various rate cases, including the 2017 General Rate Case (“2017 GRC”), during the three and twelve months ended December 31, 2017 as compared to the same periods in 2016. 17

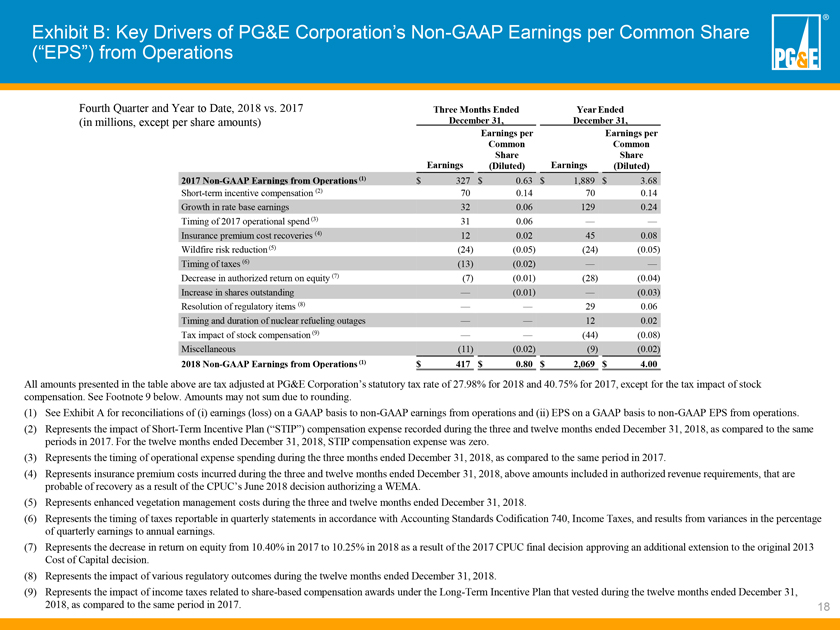

Exhibit B: Key Drivers of PG&E Corporation’s Non-GAAP Earnings per Common Share (“EPS”) from Operations Fourth Quarter and Year to Date, 2018 vs. 2017 Three Months Ended Year Ended (in millions, except per share amounts) December 31, December 31, Earnings per Earnings per Common Common Share Share Earnings (Diluted) Earnings (Diluted) 2017 Non-GAAP Earnings from Operations (1) $ 327 $ 0.63 $ 1,889 $ 3.68 Short-term incentive compensation (2) 70 0.14 70 0.14 Growth in rate base earnings 32 0.06 129 0.24 Timing of 2017 operational spend (3) 31 0.06 — — Insurance premium cost recoveries (4) 12 0.02 45 0.08 Wildfire risk reduction (5) (24) (0.05) (24) (0.05) Timing of taxes (6) (13) (0.02) — — Decrease in authorized return on equity (7) (7) (0.01) (28) (0.04) Increase in shares outstanding — (0.01) — (0.03) Resolution of regulatory items (8) — — 29 0.06 Timing and duration of nuclear refueling outages — — 12 0.02 Tax impact of stock compensation (9) — — (44) (0.08) Miscellaneous (11) (0.02) (9) (0.02) 2018 Non-GAAP Earnings from Operations (1) $ 417 $ 0.80 $ 2,069 $ 4.00 All amounts presented in the table above are tax adjusted at PG&E Corporation’s statutory tax rate of 27.98% for 2018 and 40.75% for 2017, except for the tax impact of stock compensation. See Footnote 9 below. Amounts may not sum due to rounding. (1) See Exhibit A for reconciliations of (i) earnings (loss) on a GAAP basis to non-GAAP earnings from operations and (ii) EPS on a GAAP basis to non-GAAP EPS from operations. (2) Represents the impact of Short-Term Incentive Plan (“STIP”) compensation expense recorded during the three and twelve months ended December 31, 2018, as compared to the same periods in 2017. For the twelve months ended December 31, 2018, STIP compensation expense was zero. (3) Represents the timing of operational expense spending during the three months ended December 31, 2018, as compared to the same period in 2017. (4) Represents insurance premium costs incurred during the three and twelve months ended December 31, 2018, above amounts included in authorized revenue requirements, that are probable of recovery as a result of the CPUC’s June 2018 decision authorizing a WEMA. (5) Represents enhanced vegetation management costs during the three and twelve months ended December 31, 2018. (6) Represents the timing of taxes reportable in quarterly statements in accordance with Accounting Standards Codification 740, Income Taxes, and results from variances in the percentage of quarterly earnings to annual earnings. (7) Represents the decrease in return on equity from 10.40% in 2017 to 10.25% in 2018 as a result of the 2017 CPUC final decision approving an additional extension to the original 2013 Cost of Capital decision. (8) Represents the impact of various regulatory outcomes during the twelve months ended December 31, 2018. (9) Represents the impact of income taxes related to share-based compensation awards under the Long-Term Incentive Plan that vested during the twelve months ended December 31, 2018, as compared to the same period in 2017. 18

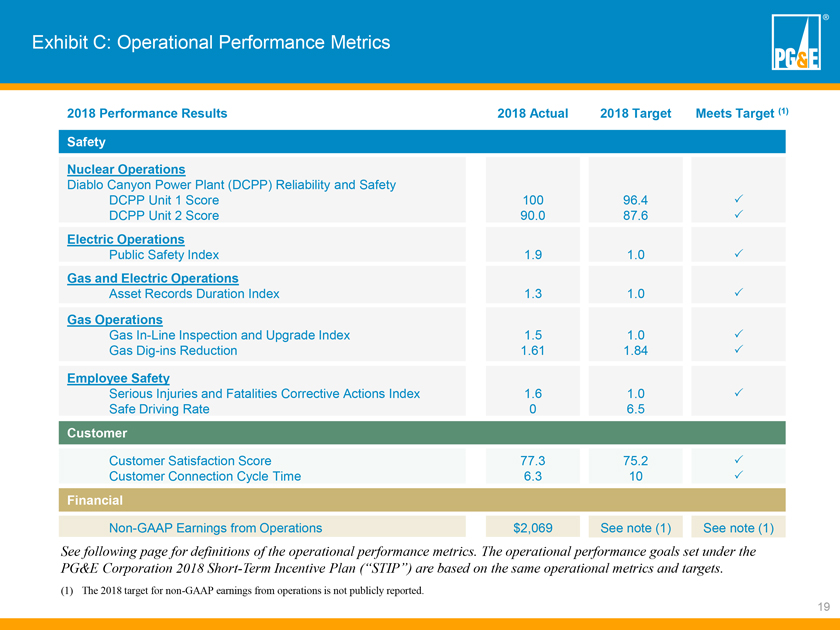

Definitions of 2017 Operational Performance Metrics from Exhibit C Safety Public and employee safety are measured in four areas: (1) Nuclear Operations Safety, (2) Electric Operations Safety, (3) Gas Operations Safety, and (4) Employee Safety. 1. The safety of the Utility’s nuclear power operations, Unit 1 and Unit 2, is an index comprised of 11 performance indicators for nuclear power generation that are regularly benchmarked against other nuclear power generators. 2. The safety of the Utility’s electric operations is represented by (a) work that supports the safe reliable operations of the overhead electric system, and (b) the percentage of time that Utility personnel are on site within 60 minutes after receiving a 911 call of a potential Utility electric hazard. 3. The safety of the Utility’s natural gas operations is represented by (a) the ability to complete plannedin-line inspections and pipeline retrofit projects, measured by two equally weighted components ofIn-Line Inspections andIn-Line Upgrades; (b) the number of third party“dig-ins” (i.e., damage resulting in repair or replacement of underground facility) to Utility gas assets per 1,000 Underground Service Alert tickets; and (c) the timeliness (measured in minutes) ofon-site response to gas emergency service calls. 4. The safety of the Utility’s employees is represented by (a) measuring the timely and quality completion of planned actions in response to Serious Injuries and Fatalities (SIF), (b) the number of serious preventable motor vehicle incidents that the driver could have reasonably avoided, per one million miles driven, and (c) the percentage of work-related injuries reported to the 24/7 Nurse Report Line within one day of the incident. Customer Customer satisfaction and service reliability are measured by: 1. The overall satisfaction (measured as a score of zero to 100) of customers with the products and services offered by the Utility, as measured through a quarterly survey performed by an independent third-party research firm. 2. The total time (measured in minutes) the average customer is without electric power during a given time period. Financial Earnings from Operations (shown in millions of dollars) measures PG&E Corporation’s earnings power from ongoing core operations. This allows investors to compare the underlying financial performance of the business from one period to another, exclusive of items that management believes do not reflect the normal course of operations (items impacting comparability). Earnings from Operations are not calculated in accordance with GAAP. For a reconciliation of Consolidated Income Available for Common Shareholders as reported in accordance with GAAP to Earnings from Operations, see Exhibit A.

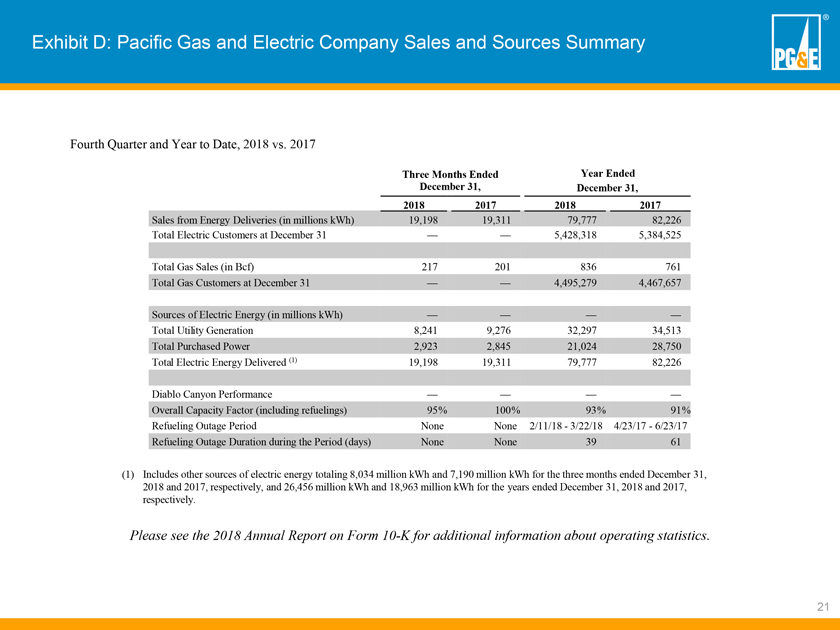

Exhibit D: Pacific Gas and Electric Company Sales and Sources Summary Fourth Quarter and Year to Date, 2017 vs. 2016 Three Months Ended December 31, Twelve Months Ended December 31, 2017 2016 2017 2016 Sales from Energy Deliveries (in millions kWh) 19,311 19,531 82,226 83,017 Total Electric Customers at December 31 5,384,525 5,349,691 Total Gas Sales (in Bcf) 201 189 761 782 Total Gas Customers at December 31 4,467,657 4,442,379 Sources of Electric Energy (in millions kWh) Total Utility Generation 9,276 8,504 34,513 32,916 Total Purchased Power 2,845 8,999 28,750 41,324 Total Electric Energy Delivered (1) 19,311 19,531 82,226 83,017 Diablo Canyon Performance Overall Capacity Factor (including refuelings) 100% 99% 91% 96% Refueling Outage Period None None4/23-6/234/30-6/2 Refueling Outage Duration during the Period None None 61 33 (1) Includes other sources of electric energy totaling 7,190 million kWh and 2,028 million kWh for the three months ended December 31, 2017 and 2016, respectively, and 18,963 million kWh and 8,777 million kWh for the twelve months ended December 31, 2017 and 2016, respectively. Please see the 2017 Annual Report on Form10-K for additional information about operating statistics.

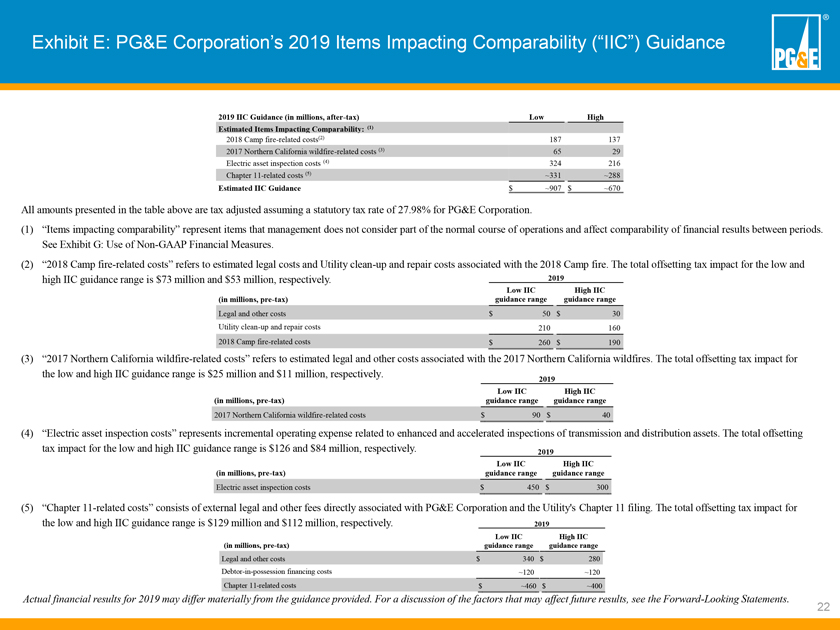

Exhibit E: PG&E Corporation’s 2018 Items Impacting Comparability (“IIC”) Guidance 2018 IIC Guidance (in millions,after-tax) Low High Estimated Items Impacting Comparability: (1) Pipeline-related expenses (2) $ 43 $ 25 Butte fire-related costs (3) $ 43 22 Northern California wildfire-related costs, net of insurance (4) $ 36 25 Estimated IIC Guidance $ 122 $ 72 All amounts presented in the table above are tax adjusted at PG&E Corporation’s statutory tax rate of 27.98 percent, except as indicated below. (1) “Items impacting comparability” represent items that management does not consider part of the normal course of operations and affect comparability of financial results between periods. See Exhibit G: Use ofNon-GAAP Financial Measures. (2) “Pipeline-related expenses” includes costs incurred to identify and remove encroachments from transmission pipelinerights-of-way. Thepre-tax range of estimated costs is shown below. The offsetting tax impact for the low and high earnings guidance range is $17 million and $10 million, respectively. 2018 Low earnings High earnings (in millions,pre-tax) guidance range guidance range Pipeline-related expenses $ 60 $ 35 (3) “Butte fire-related costs” refers to legal costs associated with the Butte fire. Thepre-tax range of estimated costs is shown below. The offsetting tax impact for the low and high earnings guidance range is $17 million and $8 million, respectively. 2018 Low earnings High earnings (in millions,pre-tax) guidance range guidance range Butte fire-related costs $ 60 $ 30 (4) “Northern California wildfire-related costs, net of insurance” refers to the legal and other costs associated with the Northern California wildfires, net of insurance. The totalpre-tax range of estimated costs is shown below. The total offsetting tax impact for the low and high earnings guidance range is $13 million and $10 million, respectively. 2018 Low earnings High earnings (in millions,pre-tax) guidance range guidance range Legal and Other $ 150 $ 100 Insurance recoveries (100) (65) Northern California wildfire-related costs, net of insurance $ 50 $ 35 Actual financial results for 2018 may differ materially from the guidance provided. For a discussion of the factors that may affect future results, see the Forward-Looking Statements. 21

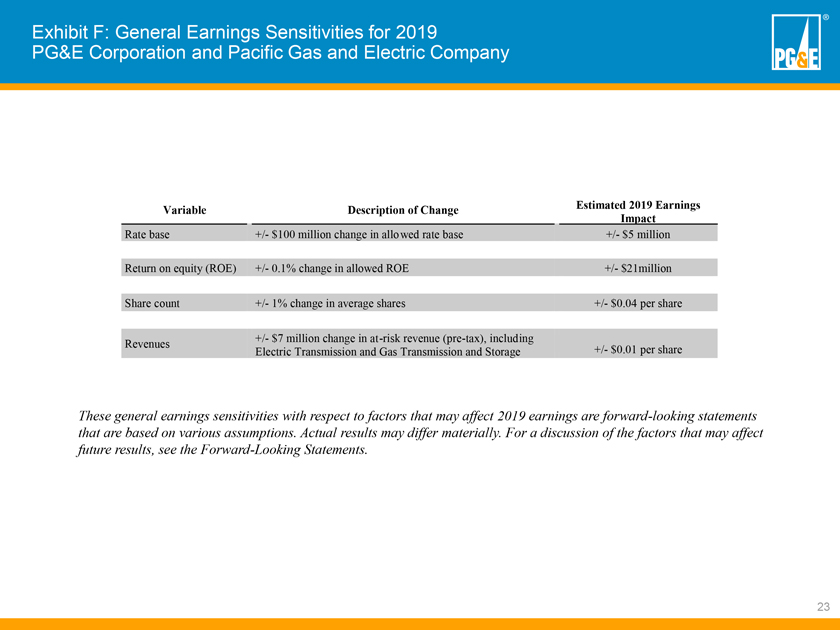

Exhibit F: 2018 General Earnings Sensitivities PG&E Corporation and Pacific Gas and Electric Company Variable Description of Change Estimated 2018 Earnings Impact Rate base +/- $100 million change in allowed rate base +/- $5 million Return on equity (ROE) +/- 0.1% change in allowed ROE +/- $19 million Share count +/- 1% change in average shares +/- $0.04 per share +/- $7 million change inat-risk revenue(pre-tax), including Revenues +/- $0.01 per share Electric Transmission and Gas Transmission and Storage These general earnings sensitivities with respect to factors that may affect 2018 earnings are forward-looking statements that are based on various assumptions. Actual results may differ materially. For a discussion of the factors that may affect future results, see the Forward-Looking Statements.

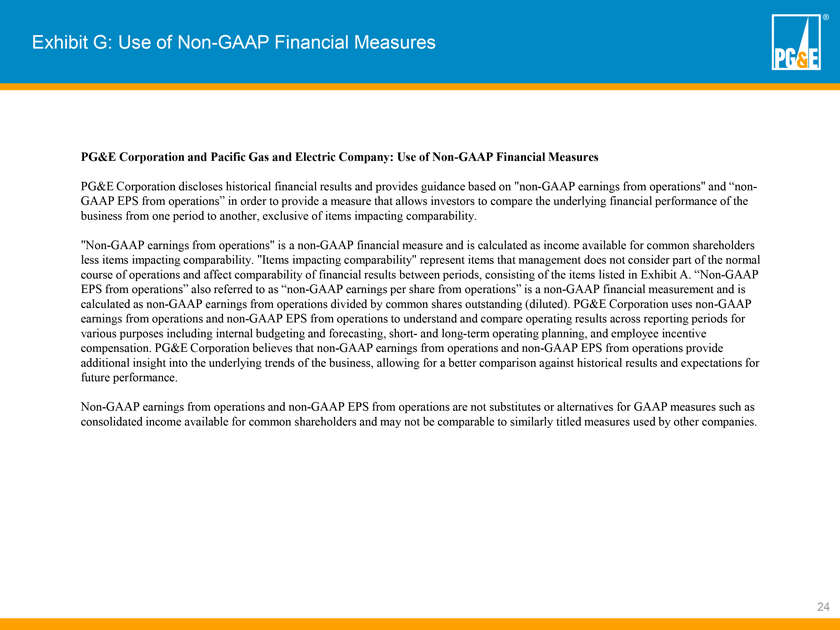

Exhibit G: Use ofNon-GAAP Financial Measures PG&E Corporation and Pacific Gas and Electric Company: Use ofNon-GAAP Financial Measures PG&E Corporation discloses historical financial results and provides guidance based on “earnings from operations” in order to provide a measure that allows investors to compare the underlying financial performance of the business from one period to another, exclusive of items impacting comparability. “Earnings from operations” is anon-GAAP financial measure and is calculated as income available for common shareholders less items impacting comparability. “Items impacting comparability” represent items that management does not consider part of the normal course of operations and affect comparability of financial results between periods, including certain pipeline related expenses, certain legal and regulatory related expenses, fines and penalties, Butte fire-related costs and insurance recoveries, net benefits from the derivative litigation settlement, impacts of the 2015 GT&S rate case, the Diablo Canyon settlement-related disallowance, costs and insurance recoveries related to the Northern California wildfires, and the transition impact of the Tax Cuts and Jobs Act. PG&E Corporation uses earnings from operations to understand and compare operating results across reporting periods for various purposes including internal budgeting and forecasting, short- and long-term operating planning, and employee incentive compensation. PG&E Corporation believes that earnings from operations provide additional insight into the underlying trends of the business allowing for a better comparison against historical results and expectations for future performance. Earnings from operations are not a substitute or alternative for GAAP measures such as consolidated income available for common shareholders and may not be comparable to similarly titled measures used by other companies.

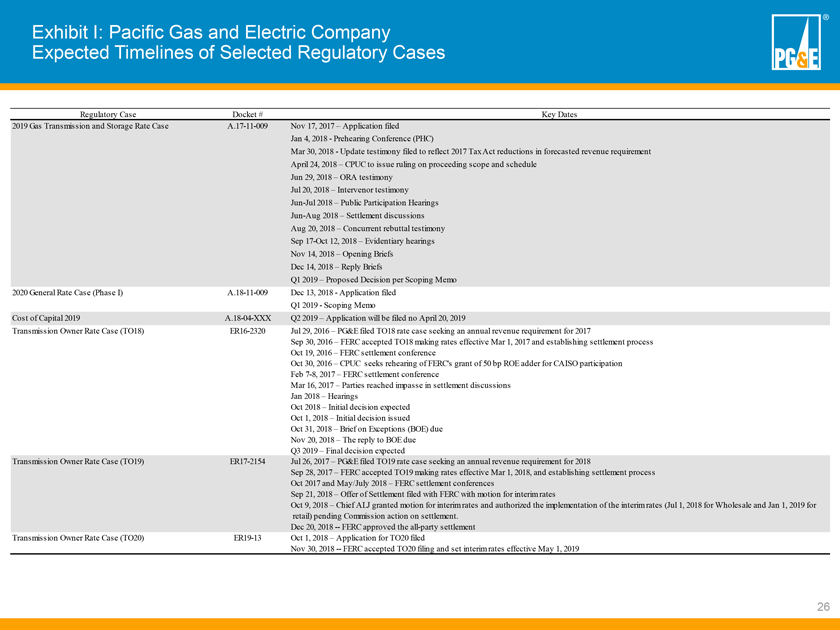

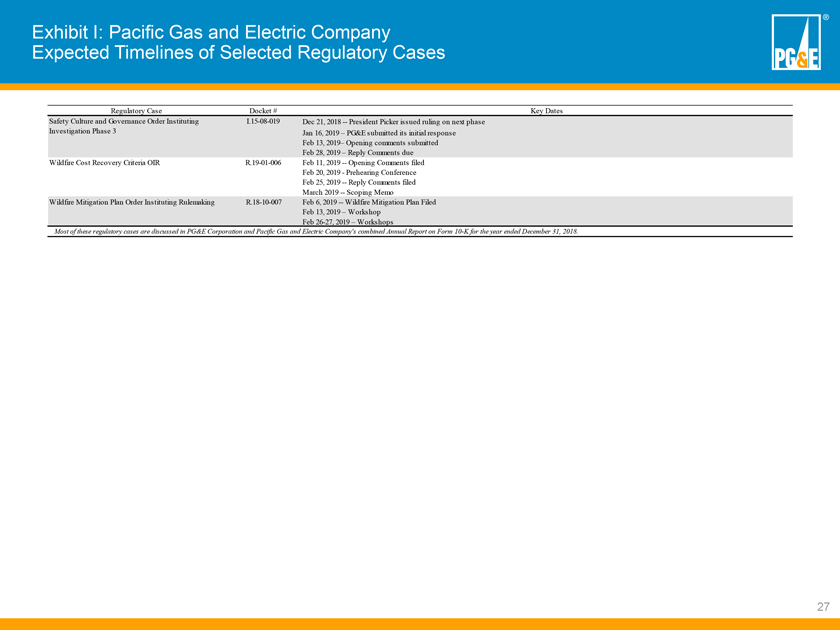

Exhibit H: Pacific Gas and Electric Company Expected Timelines of Selected Regulatory Cases Regulatory Case Docket # Key Dates 2017 General Rate Case (Phase I) A.15-09-001 Sep 1, 2015 – Application Filed Oct 29, 2015 – Prehearing conference Jan 22, 2016 – PG&E Supplemental Testimony on gas distribution recordkeeping Feb 22, 2016 – PG&E Supplemental Testimony on updated tax forecast, labor escalation Apr 8, 2016 – ORA testimony Apr 29, 2016 – Intervenor testimonyMay-Jun, 2016 – Settlement discussions May 2016 – Public participation hearings May 27, 2016 – Rebuttal testimony Aug 3, 2016 – Settlement with all parties that filed testimony submitted Feb 27, 2017 – Proposed decision issued May, 2017 – Final decision issued Transmission Owner Rate Case (TO19) ER17-2154 Jul 26, 2017 – PG&E filed TO19 rate case seeking an annual revenue requirement for 2018 Sep 28, 2017 – FERC accepted TO19 making rates effective Mar 1, 2018, and establishing settlement process Oct 23, 2017 – FERC settlement conference May 2018 – Additional FERC settlement conference anticipated Transmission Owner Rate Case (TO18) ER16-2320 Jul 29, 2016 – PG&E filed TO18 rate case seeking an annual revenue requirement for 2017 Sep 30, 2016 – FERC accepted TO18 making rates effective Mar 1, 2017 and establishing settlement process Oct 19, 2016 – FERC settlement conference Oct 30, 2016 – CPUC seeks rehearing of FERC’s grant of 50 bp ROE adder for CAISO participation Feb7-8, 2017 – FERC settlement conference Mar 16, 2017 – Parties reached impasse in settlement discussions Jan 9, 2018 – Hearings begin Jun 1, 2018 – Initial decision expected Safety Culture and Governance OrderI.15-08-019 Sep 2, 2015 – OII issued Instituting Investigation Oct 30, 2015 – PG&E submits discovery responses to SED Dec 15, 2015 – PG&E submits discovery responses to SED Jan 25, 2016 – PG&E submits discovery responses to SED Apr 2016 – CPUC hires NorthStar as consultant for investigation Apr26-27, May10-12, 2016 – Orientation presentations with SED and NorthStar staff May2016-Mar 2017 – Ongoing discovery (data requests, interviews, site visits, and demos) from NorthStar May 8, 2017 – President Picker Phase II Scoping Memo and NorthStar Assessment Report Issued Aug 1, 2017 – Prehearing Conference Scheduled Nov 17, 2017—President Picker issued Assigned Commissioner Ruling on Schedule and Scope of Testimony Jan 8, 2018 – PG&E Prepared Testimony submitted Jan 24, 2018 – President Picker Ruling on Procedural Schedule for Comments on Hearings Jan 24, 2018 – Proceeding Reassigned to ALJ Allen Jan 26, 2018 – Procedural Schedule Suspended Jan 29, 2018 – ALJ Ruling on Modified Procedural Schedule Feb 16 2018 – Parties Prepared Testimony Due Feb 23, 2018 – PG&E Rebuttal Testimony Due Mar 2, 2018 – Comments on Evidentiary Hearings Due

Exhibit H: Pacific Gas and Electric Company Expected Timelines of Selected Regulatory Cases Regulatory Case Docket # Key Dates 2015 Electric Distribution Resources PlanA.15-07-006, Aug 13, 2014 – Commission issues OIR directing utilities to file Electric Distribution Resources Plans (DRP)R.14-08-013 Sep 5, 2014 – Comments on OIR Sep 17, 2014 – Workshop I Sep 22, 2014 – Reply Comments on OIR Nov 17, 2014 – Draft Guidance Issued Dec 12, 2014 – Comments on Draft Guidance Jan 8, 2015 – Workshop II Feb 6, 2015 – Final Guidance Ruling issued Apr 13, 2015 – Workshop III Jul 1, 2015 – PG&E files Electric Distribution Resources Plan Aug 31, 2015 – Protests/comments due Sep 15, 2015 – Replies to protests due Sep 30, 2015 – Prehearing Conference Nov 6, 2015 – Joint IOU/CAISO Workshop Nov9-10, 2015 – Integration Capacity Analysis (ICA) Workshop Dec 3, 2015 – ICA Workshop Report filed Jan 8, 2016 – ALJ Ruling invitingpre-workshop comments to Locational Net Benefits Analysis (LNBA) methodologies and Demonstration Project (Demo) B Jan 26, 2016 –Pre-LNBA Workshop Comments Filed Jan 27, 2016 – ACR/ALJ Ruling issuing Scope and Schedule Feb 1, 2016 – LNBA, Alternate Proposal and Related Demo B Workshop Feb 4, 2016 – Case reassigned to ALJ Kelly Mar 2016 – Workshop on Field DemosC-F Apr 2016 – DRP/IDER workshop to discuss sourcing mechanisms in Field DemosC-F May 2016 – Comments on Field DemosC-F and alternatives Jul 2016 – Proposed Decision on Field DemosC-F Aug 2016 – Final Decision on Field DemosC-F Sep 2016 – Begin Field DemosC-F Jan 24, 2017 – Grid Modernization Workshop Feb 9, 2017 – Decision on Field Demos C and D Feb 27, 2017 – Decision on DER Growth Scenario and Distribution Load Forecasting schedule Mar 4, 2017 – PG&E filed updated Demo C project Mar 8, 2017 – LNBA Working Group Final Report issued Mar 15, 2017 – ICA Working Group Final Report issued Apr 7, 2017 – PG&E filed DER forecasting methodology and assumptions Apr 19, 2017 – Decision on scope of long–term refinements to ICA and LNBA May 15, 2017 – Working group on ICA and LNBA long–term refinements May 16, 2017 – CPUC Staff whitepaper on Grid Modernization Jun 5, 2017 – Grid Modernization workshop

Exhibit H: Pacific Gas and Electric Company Expected Timelines of Selected Regulatory Cases Regulatory Case Docket # Key Dates 2015 Electric Distribution Resources PlanA.15-07-006, Jun 15, 2017 – Decision on PG&E’s revised Field Demo D (DRP)R.14-08-013 Jun 19, 2017 – PG&E filed comments on CPUC Staff’s Grid Modernization Whitepaper Jun 22, 2017 – Decision requiring IOUs to file assumptions and framework details on DER growth forecasting and disaggregation Jun 28, 2017 – PG&E filed assumptions and framework details on DER growth forecasting and disaggregation Jun 30, 2017 – Decision requesting IOU comments on Energy Division staff proposal on the Distribution Investment Deferral Framework Mid Jul, 2017 – Comments on CPUC Decision approving Field Demo C Late Jul 2017 – Decision on IOU DER Growth Scenarios for distribution planning Late Jul 2017 – Comments due on Energy Division’s Distribution Investment Deferral Framework whitepaper Aug 2017 – Reply Comments on Energy Division’s Distribution Investment Deferral Framework whitepaper Aug 2017 – Reply Comments on CPUC Decision approving Field Demo C Oct 6, 2017 – Decision on ICA and LNBA use cases Q3 2017 – Proposed Decision on DER Growth scenarios assumptions and framework Q1 2018 – Proposed Decision on ICA and LNBA long–term refinements Catastrophic Event Memorandum Account A.16-10-019 Oct 31, 2016 – Application filed and testimony served (CEMA) 2016 Dec 5, 2016 – Protests or responses Dec 12, 2016 – Reply to protests or responses Dec 19, 2016 – Prehearing conference Oct 3, 2017 – Intervenor testimony Oct 24, 2017 – Rebuttal testimony Nov6-9 , 2017 – Hearings Dec 5, 2017 – Opening Briefs Dec 22, 2017 – Reply Briefs Jan 4, 2018 – All Party Settlement Agreement filed Q1, 2018 – Proposed Decision Q2, 2018 – Final Decision 2017 Integrated Resource Plan / Long TermR.16-02-007 Feb 11, 2016 – CPUC opens Order Instituting Rulemaking Procurement Plan Mar 14, 2016 – Comments due on OIR May 26, 2016 – Scoping Memo Issued Jun 14, 2016 – Workshop on E3’s Pathways Study hosted by State Agencies Jun 23, 2016 – CPUC transfers significant modeling issues from legacy LTPP proceeding toR.16-02-007 proceeding(D.16-06-042) Aug 11, 2016 – Staff Preliminary Proposal for an Integrated Resource Plan (IRP) Process Issued Aug 23, 2016 – California Air Resources Board and CPUC Joint Workshop on ARB’s 2030 Scoping Plan Update for the Energy Sector Aug 31, 2016 – Parties submit comments on Staff’s Preliminary Proposal for an IRP Process Sep 26, 2016 – Workshop on Staff’s Preliminary Proposal for an IRP Process Oct 5, 2016 – Technical Advisory Group formed on modeling-related activities Dec 2016 – Final Proposal for an IRP Process Issued by Staff Sep 19, 2017 – Draft Reference System Plan issued Dec 28, 2017 – Proposed Decision issued 1Q 2018 – Decision adopting Reference System Plan 3Q 2018 – Load Serving Entities file individual Integrated Resource Plans

Exhibit H: Pacific Gas and Electric Company Expected Timelines of Selected Regulatory Cases Regulatory Case Docket # Key Dates Integration of Distributed EnergyR.14-10-003 Sep 22, 2015 – Decision to expand scope to include distributed energy resources (DERs) on system side of customer’s meter Resources Mar 24, 2016 – Working Group established to focus on contracting of DER products and services Apr 4, 2016 – Assigned Commissioner Ruling (ACR) introducing a regulatory incentive proposal for DER deployment Sep 1, 2016 – Amended Scoping Memo and Rulingre-categorizing all activities as rate-setting Sep 22, 2016 – Workshop to begin considering societal cost test for DERs, including values of avoided societal costs Dec, 2016 – Final Decision on competitive solicitation framework and regulatory incentives. Mar 23, 2017 – PG&E and other IOUs filed opening comments on a ruling on Energy Division’s Societal Cost Test (SCT) proposal. Apr 6, 2017 – PG&E filed joint IOU reply comments on Energy Division’s SCT proposal Apr 17, 2017 – PG&E files comments on interim greenhouse gas adder for SCT Apr 24, 2017 – PG&E filed joint IOU reply comments interim greenhouse gas adder for SCT May 16, 2017 – Joint IOUs filed motion for hearing on the SCT proposals Jun 16, 2017 – Ruling denying IOU’s request for hearings on the SCT proposals and instead establishing a Workshop Jun 22, 2017 – Proposed Decision to allow a 1–year waiver to updating the Avoided Cost Calculator Jul 2017 – filed Advice Letter for DER Incentive Pilot Aug 8, 2017 – Workshop on Energy Division’s SCT proposal Aug 10, 2017 – Expected decision allowing a 1–year waiver to updated the Avoided Cost Calculator Diablo Canyon Retirement Joint ProposalA.16-08-006 Aug 11, 2016 – Application Filed Application Sep 15, 2016 – Intervenor Protests Oct 6, 2016 – Prehearing Conference Oct 20, 2016 – Public Participation Hearings in San Luis Obispo Dec 8, 2016 – Workshop at CPUC Dec 28, 2016 – Community Impact Mitigation Settlement Filed with CPUC Jan 27, 2017 – Intervenor Testimony & Comments On CIMP Settlement Mar 17, 2017 – Rebuttal Testimony & PG&E’s Response To Comments On CIMP Settlement Apr18-28, 2017 – Evidentiary Hearings May 23, 2017—License Renewal Project and Future Cancelled Project Settlement Agreement Filed May 26, 2017 – Opening Briefs Jun 16, 2017 – Reply Briefs Jun 22, 2017 – Opening Comments on the License Renewal Project and Future Cancelled Project Settlement Agreement Jul 7, 2017 – Reply Comments on the License Renewal Project and Future Cancelled Project Settlement Agreement Sep 14, 2017 – Public Participation Hearings Nov 28, 2017 – Final Oral Argument Jan 11, 2018 – Final Decision issued Ex Parte Order Instituting Investigation andI.15-11-015 Nov 23, 2015 – OII issued Order to Show Cause Dec 3, 2015 – City of San Bruno, City of San Carlos and TURN comments on need for evidentiary hearings, issues and schedule in the proceeding Jan 8, 2016 – ALJ Bushey orders meet and confer among parties and sets prehearing conference date Jan 27, 2016 – Parties meet to discuss issues for hearing and briefing Jan 28, 2016 – PG&E (on behalf of parties) submits joint report on meet and confer to determine hearing issues Feb 26, 2016 – Status report on resolving hearing issues due to Commission Mar 1, 2016 – Prehearing conference

Exhibit H: Pacific Gas and Electric Company Expected Timelines of Selected Regulatory Cases Regulatory Case Docket # Key Dates Ex Parte Order Instituting Investigation andI.15-11-015 Apr 18, 2016 – Joint meet and confer report filed by parties Order to Show Cause Apr 20, 2016 – Prehearing conference May 20, 2016 – Opening briefs on inclusion of additional emails (“Category 3”) Jun 10, 2016 – Reply briefs on inclusion of Category 3 emails Jul 12, 2016 – Revised scoping memo Sep 2016 – Status conference to set schedule for rest of proceeding Jan 2017 – Commission grants two month extension to allow for additional settlement discussions Mar 28, 2017 – PG&E, Cities of San Bruno and San Carlos, ORA, SED, and TURN submit joint settlement agreement Jun 23, 2017 – Per an ALJ Ruling, PG&E submits supplemental briefing on joint settlement agreement Sep 1, 2017 – Proposed Decision Sep 21, 2017 – PG&E’s Comments on Proposed Decision and Motion to File Under Seal Sep 29, 2017 – Parties Request for Extension of Time to Respond to PG&E Motion Oct 2, 2017 – PG&E Status Report to ALJ Mason Oct 18, 2017 – PG&E Second Status Report to ALJ Mason Nov 1, 2017 – PG&E’s Third Status Report to ALJ Mason Nov 1, 2017 – Parties Comments Adopting the Proposed Modified Settlement Nov 11, 2017 – PG&E Comments on Proposed Decision Modifying the Adopted Settlement Dec 14, 2017 – Commission Decision Extending the Statutory Deadline Most of these regulatory cases are discussed in PG&E Corporation and Pacific Gas and Electric Company’s combined Annual Report on Form10-K for the year ended December 31, 2017.

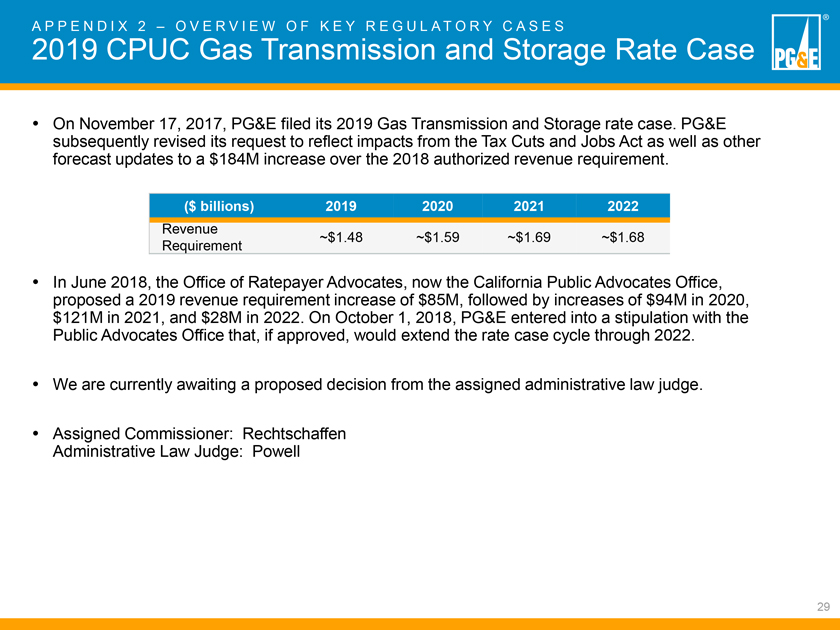

A P P E N D I X 2 – O V E R V I E W O F K E Y R E G U L A T O R Y C A S E S 2019 CPUC Gas Transmission and Storage Rate Case On November 17, 2017, PG&E filed its 2019 Gas Transmission and Storage rate case. PG&E subsequently revised its request to reflect impacts from the Tax Cuts and Jobs Act as well as other forecast updates to a $184M increase over the 2018 authorized revenue requirement. ($ billions) 2019 2020 2021 2022 Revenue ~$1.48 ~$1.59 ~$1.69 ~$1.68 Requirement In June 2018, the Office of Ratepayer Advocates, now the California Public Advocates Office, proposed a 2019 revenue requirement increase of $85M, followed by increases of $94M in 2020, $121M in 2021, and $28M in 2022. On October 1, 2018, PG&E entered into a stipulation with the Public Advocates Office that, if approved, would extend the rate case cycle through 2022. We are currently awaiting a proposed decision from the assigned administrative law judge. Assigned Commissioner: Rechtschaffen Administrative Law Judge: Powell

A P P E N D I X 2 – O V E R V I E W O F K E Y R E G U L A T O R Y C A S E S FERC Transmission Owner Rate Case TO18 (2017 Revenues) • July 29, 2016 – Filed TO18 with FERC requesting $1.7 billion revenue requirement, an ROE (inclusive of 50 basis point adder) of 10.90% • A final decision is expected in the second half of 2019 TO19 (2018 Revenues) • On August 24, 2018 the Parties reached a settlement-in-principle on all issues tying the TO19 settlement RRQ to the final FERC decision in TO18 by applying a settlement factor of 98.85% to the final TO18 authorized RRQ • On December 20, 2019, the FERC issued a letter approving the settlement, but rates will be subject to refund until resolution of TO18 TO20 (2019 Revenues) • On October 1, 2018, PG&E filed its TO20 rate case, requesting both a conversion to formula rates, a revenue requirement of ~$1.96B and an ROE of 12.5% (inclusive of 50 basis point incentive adder)