Banc of America Merrill Lynch Commercial Mortgage

Filed: 4 Feb 16, 12:00am

| FREE WRITING PROSPECTUS | ||

| FILED PURSUANT TO RULE 433 | ||

| REGISTRATION FILE NO.: 333-206847-01 | ||

|  |

Morgan Stanley Bank of America Merrill Lynch Trust 2016-C28

Free Writing Prospectus

Structural and Collateral Term Sheet

$955,648,355

(Approximate Total Mortgage Pool Balance)

$813,496,000

(Approximate Offered Certificates)

Banc of America Merrill Lynch Commercial Mortgage Inc.

as Depositor

Bank of America, National Association

Morgan Stanley Mortgage Capital Holdings LLC

CIBC Inc.

Starwood Mortgage Funding III LLC

as Sponsors and Mortgage Loan Sellers

Commercial Mortgage Pass-Through Certificates

Series 2016-C28

February 4, 2016

| BofA MERRILL LYNCH | MORGAN STANLEY | |

| Co-Lead Bookrunning Manager | Co-Lead Bookrunning Manager | |

CIBC World Markets | Drexel Hamilton | |

| Co-Manager | Co-Manager | |

STATEMENT REGARDING THIS FREE WRITING PROSPECTUS

The depositor has filed a registration statement (including a prospectus) with the SEC (File No. 333-206847) for the offering to which this communication relates. Before you invest, you should read the prospectus in that registration statement and other documents the depositor has filed with the SEC for more complete information about the depositor, the issuing entity and this offering. You may get these documents for free by visiting EDGAR on the SEC web site atwww.sec.gov. Alternatively, the depositor or any underwriter or any dealer participating in the offering will arrange to send you the prospectus if you request it by calling toll free 1-800-294-1322 or by email todg.Prospectus_Requests@baml.com.

| This is not a research report and was not prepared by any Underwriter’s research department. It was prepared by the Underwriters’ sales, trading, banking or other non-research personnel. Please see additional important information and qualifications at the end of this Term Sheet. |

Neither this Term Sheet nor anything contained herein shall form the basis for any contract or commitment whatsoever.The information contained herein is preliminary as of the date hereof.This Term Sheet is subject to change, completion or amendment from time to time.The information contained herein will be superseded by similar information delivered to you as part of the Preliminary Prospectus.The information contained herein supersedes any such information previously delivered.The information contained herein should be reviewed only in conjunction with the entire Preliminary Prospectus.All of the information contained herein is subject to the same limitations and qualifications contained in the Preliminary Prospectus.The information contained herein does not contain all relevant information relating to the underlying mortgage loans or mortgaged properties.Such information is described in the Preliminary Prospectus.The information contained herein will be more fully described in the Preliminary Prospectus.The information contained herein should not be viewed as projections, forecasts, predictions or opinions with respect to value.Prior to making any investment decision, prospective investors are strongly urged to read the Preliminary Prospectus in its entirety.Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or determined if this Term Sheet is truthful or complete.Any representation to the contrary is a criminal offense.

IMPORTANT NOTICE RELATING TO AUTOMATICALLY GENERATED EMAIL DISCLAIMERS

Any legends, disclaimers or other notices that may appear at the bottom of, or attached to, the email communication to which this Term Sheet may have been attached are not applicable to this Term Sheet and should be disregarded. Such legends, disclaimers or other notices have been automatically generated as a result of this Term Sheet having been sent via Bloomberg or another email system.

IMPORTANT NOTICE REGARDING THE CONDITIONS FOR THIS OFFERING OF ASSET-BACKED SECURITIES

THE ASSET-BACKED SECURITIES REFERRED TO IN THIS TERM SHEET ARE BEING OFFERED WHEN, AS AND IF ISSUED. IN PARTICULAR, YOU ARE ADVISED THAT THE ASSET-BACKED SECURITIES, AND THE ASSET POOL BACKING THEM, ARE SUBJECT TO MODIFICATION OR REVISION (INCLUDING, AMONG OTHER THINGS, THE POSSIBILITY THAT ONE OR MORE CLASSES OF SECURITIES MAY BE SPLIT, COMBINED OR ELIMINATED), AT ANY TIME PRIOR TO ISSUANCE OR AVAILABILITY OF A FINAL PROSPECTUS. AS A RESULT, YOU MAY COMMIT TO PURCHASE SECURITIES THAT HAVE CHARACTERISTICS THAT MAY CHANGE, AND YOU ARE ADVISED THAT ALL OR A PORTION OF THE SECURITIES MAY NOT BE ISSUED THAT HAVE THE CHARACTERISTICS DESCRIBED IN THIS TERM SHEET. OUR OBLIGATION TO SELL SECURITIES TO YOU IS CONDITIONED ON THE SECURITIES AND THE UNDERLYING TRANSACTION HAVING THE CHARACTERISTICS DESCRIBED IN THIS TERM SHEET. IF WE DETERMINE THAT THE FOREGOING CONDITION IS NOT SATISFIED IN ANY MATERIAL RESPECT, WE WILL NOTIFY YOU, AND NEITHER THE ISSUING ENTITY NOR ANY UNDERWRITER WILL HAVE ANY OBLIGATION TO YOU TO DELIVER ALL OR ANY PORTION OF THE SECURITIES WHICH YOU HAVE COMMITTED TO PURCHASE, AND THERE WILL BE NO LIABILITY BETWEEN US AS A CONSEQUENCE OF THE NON-DELIVERY.

| This is not a research report and was not prepared by the Underwriters’ research departments. Please see additional important information and qualifications at the end of this Term Sheet. |

| T-1 |

| MSBAM 2016-C28 | Structural Overview |

Offered Certificates

| Class | Expected Ratings (DBRS/Fitch/Moody’s)(1) | Approximate Initial Certificate Balance or Notional Amount(2) | Approximate Initial Credit Support(3) | Pass-Through Rate Description | Expected Weighted Average Life (Years)(5) | Principal Window (Months)(5) | Certificate Principal UW NOI Debt Yield(6) | Certificate Principal to Value Ratio(7) | |||||||||

| A-1 | AAA(sf)/AAAsf/Aaa(sf) | $25,700,000 | 30.000% | (4) | 2.90 | 1-58 | 16.3% | 42.6% | |||||||||

| A-2 | AAA(sf)/AAAsf/Aaa(sf) | $43,800,000 | 30.000% | (4) | 4.85 | 58-60 | 16.3% | 42.6% | |||||||||

| A-SB | AAA(sf)/AAAsf/Aaa(sf) | $59,300,000 | 30.000% | (4) | 6.93 | 60-110 | 16.3% | 42.6% | |||||||||

| A-3 | AAA(sf)/AAAsf/Aaa(sf) | $215,000,000 | 30.000% | (4) | 9.59 | 110-117 | 16.3% | 42.6% | |||||||||

| A-4 | AAA(sf)/AAAsf/Aaa(sf) | $325,154,000 | 30.000% | (4) | 9.81 | 117-119 | 16.3% | 42.6% | |||||||||

| X-A | AAA(sf)/AAAsf/Aaa(sf) | $668,954,000 | (8) | N/A | Variable IO(9) | N/A | N/A | N/A | N/A | ||||||||

| X-B | AAA(sf)/AA-sf/Aa3(sf) | $97,954,000 | (8) | N/A | Variable IO(9) | N/A | N/A | N/A | N/A | ||||||||

| A-S | AAA(sf)/AAAsf/Aa1(sf) | $47,782,000 | 25.000% | (4) | 9.89 | 119-119 | 15.2% | 45.6% | |||||||||

| B | AA(sf)/AA-sf/Aa3(sf) | $50,172,000 | 19.750% | (4) | 9.89 | 119-119 | 14.2% | 48.8% | |||||||||

| C | A(sf)/A-sf/A3(sf) | $46,588,000 | 14.875% | (4) | 9.89 | 119-119 | 13.4% | 51.8% | |||||||||

Privately Offered Certificates(10)

| Class | Expected Ratings (DBRS/Fitch/Moody’s)(1) | Approximate Initial Certificate Balance or Notional Amount(2) | Approximate Initial Credit Support(3) | Pass-Through Rate Description | Expected Weighted Average Life (Years)(5) | Principal Window (Months)(5) | Certificate Principal UW NOI Debt Yield(6) | Certificate Principal to Value Ratio(7) | |||||||||

| X-D | AAA(sf)/BBB-sf/NR | $52,560,000 | (8) | N/A | Variable IO(9) | N/A | N/A | N/A | N/A | ||||||||

| D | BBB(sf)/BBB-sf/NR | $52,560,000 | 9.375% | (4) | 9.89 | 119-119 | 12.6% | 55.1% | |||||||||

| E-1(11)(17)(23) | BBB(sf)/BBsf/NR | $14,335,000 | (12)(18)(24) | 7.875% | (4) | 9.92 | 119-120 | 12.4% | 56.0% | ||||||||

| E-2(11)(17)(23) | BBB(low)(sf)/BB-sf/NR | $14,335,000 | (12)(18)(24) | 6.375% | (4) | 9.97 | 120-120 | 12.2% | 56.9% | ||||||||

| E(11) | BBB(low)(sf)/BB-sf/NR | $28,670,000 | (12) | 6.375% | N/A(13) | 9.95 | 119-120 | 12.2% | 56.9% | ||||||||

| F-1(14)(17)(23) | BB(sf)/NR/NR | $4,778,000 | (1*5)(18)(24) | 5.875% | (4) | 9.97 | 120-120 | 12.1% | 57.2% | ||||||||

| F-2(14)(17)(23) | BB(sf)/NR/NR | $4,778,000 | (15)(18)(24) | 5.375% | (4) | 9.97 | 120-120 | 12.0% | 57.5% | ||||||||

| F(14) | BB(sf)/B-sf/NR | $9,556,000 | (15) | 5.375% | N/A(16) | 9.97 | 120-120 | 12.0% | 57.5% | ||||||||

| EF(17) | BB(sf)/B-sf/NR | $38,226,000 | (18) | 5.375% | N/A(19) | 9.95 | 119-120 | 12.0% | 57.5% | ||||||||

| G-1(20)(23) | B(high)(sf)/NR/NR | $11,348,500 | (21)(24) | 4.188% | (4) | 9.97 | 120-120 | 11.9% | 58.3% | ||||||||

| G-2(20)(23) | B(low)(sf)/NR/NR | $11,348,500 | (21)(24) | 3.000% | (4) | 9.97 | 120-120 | 11.8% | 59.0% | ||||||||

| G(20) | B(low)(sf)/NR/NR | $22,697,000 | (21) | 3.000% | N/A(22) | 9.97 | 120-120 | 11.8% | 59.0% | ||||||||

| EFG(23) | B(low)(sf)/NR/NR | $60,923,000 | (24) | 3.000% | N/A(25) | 9.96 | 119-120 | 11.8% | 59.0% | ||||||||

| H-1(26) | NR/NR/NR | $14,334,677 | (27) | 1.500% | (4) | 11.44 | 120-144 | 11.6% | 59.9% | ||||||||

| H-2(26) | NR/NR/NR | $14,334,677 | (27) | 0.000% | (4) | 11.97 | 144-144 | 11.4% | 60.8% | ||||||||

| H(26) | NR/NR/NR | $28,669,354 | (27) | 0.000% | N/A(28) | 11.71 | 120-144 | 11.4% | 60.8% | ||||||||

| (1) | Ratings shown are those of DBRS, Inc. (“DBRS”), Fitch Ratings, Inc. (“Fitch”) and Moody’s Investors Service, Inc. (“Moody’s”). Certain nationally recognized statistical rating organizations that were not hired by the depositor may use information they receive pursuant to Rule 17g-5 under the Securities Exchange Act of 1934, as amended, or otherwise to rate the certificates. There can be no assurance as to what ratings a non-hired nationally recognized statistical rating organization would assign. See “Risk Factors—Other Risks Relating to the Certificates—Nationally Recognized Statistical Rating Organizations May Assign Different Ratings to the Certificates; Ratings of the Certificates Reflect Only the Views of the Applicable Rating Agencies as of the Dates Such Ratings Were Issued; Ratings May Affect ERISA Eligibility; Ratings May Be Downgraded” and “Ratings” in the Preliminary Prospectus, expected to be dated February 5, 2016 (the “Preliminary Prospectus”). Capitalized terms used but not defined herein have the meanings assigned to such terms in the Preliminary Prospectus. |

| (2) | Approximate, subject to a permitted variance of plus or minus 5%. In addition, the notional amounts of the Class X-A, Class X-B and Class X-D certificates may vary depending upon the final pricing of the classes of principal balance certificates whose certificate balances comprise such notional amounts, and, if as a result of such pricing the pass-through rate of the Class X-A, Class X-B or Class X-D certificates, as applicable, would be equal to zero, such class of certificates will not be issued on the closing date of this securitization. |

| (3) | The approximate initial credit support percentages set forth for the certificates are approximate and, for the Class A-1, Class A-2, Class A-3, Class A-4 and Class A-SB certificates, are represented in the aggregate. The approximate initial credit support percentage set forth for the Class E certificates represents the approximate initial credit support for the underlying Class E-2 trust component. The approximate initial credit support percentage set forth for the Class F certificates represents the approximate initial credit support for the underlying Class F-2 trust component. The approximate initial credit support percentage set forth for the Class EF certificates represents the approximate initial credit support for the underlying Class F-2 trust component. The approximate initial credit support percentage set forth for the Class G certificates represents the approximate initial credit support for the underlying Class G-2 trust component. |

The approximate initial credit support percentage set forth for the Class EFG certificates represents the approximate initial credit support for the underlying Class G-2 trust component. The approximate initial credit support percentage set forth for the Class H certificates represents the approximate initial credit support for the underlying Class H-2 trust component.

| This is not a research report and was not prepared by the Underwriters’ research departments. Please see additional important information and qualifications at the end of this Term Sheet. |

| T-2 |

| MSBAM 2016-C28 | Structural Overview |

| (4) | The pass-through rates for the Class A-1, Class A-2, Class A-SB, Class A-3, Class A-4, Class A-S, Class B, Class C, Class D, Class E-1, Class E-2, Class F-1, Class F-2, Class G-1, Class G-2, Class H-1 and Class H-2 certificates will be one of the following: (i) a fixed rateper annum, (ii) a variable rateper annum equal to the weighted average of the net mortgage interest rates on the mortgage loans for the related distribution date, (iii) a variable rateper annum equal to the lesser of (a) a fixed rate and (b) the weighted average of the net mortgage interest rates on the mortgage loans for the related distribution date or (iv) a variable rateper annum equal to the weighted average of the net mortgage interest rates on the mortgage loans for the related distribution date minus a specified percentage. For purposes of the calculation of the weighted average of the net mortgage interest rates on the mortgage loans for each distribution date, the mortgage interest rates will be adjusted as necessary to a 30/360 basis. |

| (5) | The Expected Weighted Average Life (Years) and Principal Window (Months) during which distributions of principal would be received as set forth in the foregoing table with respect to each class of certificates having a certificate balance are based on the assumptions set forth under “Yield and Maturity Considerations—Weighted Average Life” in the Preliminary Prospectus and on the assumptions that there are no prepayments, modifications or losses in respect of the mortgage loans and that there are no extensions or forbearances of maturity dates or anticipated repayment dates of the mortgage loans. |

| (6) | Certificate Principal UW NOI Debt Yield for any class of principal balance certificates (other than the Exchangeable Certificates and the Exchangeable Combined Certificates) is calculated as the product of (a) the weighted average UW NOI Debt Yield for the mortgage pool, multiplied by (b) a fraction, the numerator of which is the total initial principal balance of all the principal balance certificates (other than the Exchangeable Certificates and the Exchangeable Combined Certificates) and trust components, and the denominator of which is the total initial principal balance of the subject class of principal balance certificates and all other classes of principal balance certificates (other than the Exchangeable Certificates and the Exchangeable Combined Certificates) and trust components, if any, that are senior to such class. The Certificate Principal UW NOI Debt Yields of the Class A-1, Class A-2, Class A-SB, Class A-3 and Class A-4 certificates are calculated in the aggregate for those classes as if they were a single class. |

| Certificate Principal UW NOI Debt Yield for each class of the Class E-1, Class E-2, Class F-1, Class F-2, Class G-1, Class G-2, Class H-1 and Class H-2 certificates is calculated as the product of (a) the weighted average UW NOI Debt Yield for the mortgage pool, multiplied by (b) a fraction, the numerator of which is the total initial principal balance of all the principal balance certificates (other than the Exchangeable Certificates and the Exchangeable Combined Certificates) and trust components, and the denominator of which is the total initial principal balance of the trust component with the same alphanumeric designation and all other classes of principal balance certificates (other than the Exchangeable Certificates and the Exchangeable Combined Certificates) and trust components that are senior to such trust component. The Certificate Principal UW NOI Debt Yield for the Class E certificates is equal to the Certificate Principal UW NOI Debt Yield for the Class E-2 trust component. The Certificate Principal UW NOI Debt Yield for each class of the Class F and Class EF certificates is equal to the Certificate Principal UW NOI Debt Yield for the Class F-2 trust component. The Certificate Principal UW NOI Debt Yield for each class of the Class G and Class EFG certificates is equal to the Certificate Principal UW NOI Debt Yield for the Class G-2 trust component. The Certificate Principal UW NOI Debt Yield for the Class H certificates is equal to the Certificate Principal UW NOI Debt Yield for the Class H-2 trust component. |

| (7) | Certificate Principal to Value Ratio for any class of principal balance certificates (other than the Exchangeable Certificates and the Exchangeable Combined Certificates) is calculated as the product of (a) the weighted average Cut-off Date LTV Ratio of the mortgage pool, multiplied by (b) a fraction, the numerator of which is the total initial certificate balance of the subject class of principal balance certificates and all other classes of principal balance certificates (other than the Exchangeable Certificates and the Exchangeable Combined Certificates) and trust components that are senior to such class, and the denominator of which is the total initial certificate balance of all the principal balance certificates (other than the Exchangeable Certificates and the Exchangeable Combined Certificates) and trust components. The Certificate Principal to Value Ratios of the Class A-1, Class A-2, Class A-SB, Class A-3 and Class A-4 certificates are calculated in the aggregate for those classes as if they were a single class. Certificate Principal to Value Ratio for each class of the Class E-1, Class E-2, Class F-1, Class F-2, Class G-1, Class G-2, Class H-1 and Class H-2 certificates is calculated as the product of (a) the weighted average Cut-off Date LTV Ratio of the mortgage pool, multiplied by (b) a fraction, the numerator of which is the total initial principal balance of the trust component with the same alphanumeric designation and all other classes of principal balance certificates (other than the Exchangeable Certificates and the Exchangeable Combined Certificates) and trust components that are senior to such trust component, and the denominator of which is the total initial principal balance of all the principal balance certificates (other than the Exchangeable Certificates and the Exchangeable Combined Certificates) and trust components. The Certificate Principal to Value Ratio for the Class E certificates is equal to the Certificate Principal to Value Ratio for the Class E-2 trust component. The Certificate Principal to Value Ratio for each class of the Class F and Class EF certificates is equal to the Certificate Principal to Value Ratio for the Class F-2 trust component. The Certificate Principal to Value Ratio for each class of the Class G and Class EFG certificates is equal to the Certificate Principal to Value Ratio for the Class G-2 trust component. The Certificate Principal to Value Ratio for the Class H certificates is equal to the Certificate Principal to Value Ratio for the Class H-2 trust component. |

| (8) | The Class X-A, Class X-B and Class X-D certificates (collectively, the “Class X Certificates”) will not have certificate balances and will not be entitled to receive distributions of principal. Interest will accrue on the Class X-A, Class X-B and Class X-D certificates at their respective pass-through rates based upon their respective notional amounts. The notional amount of the Class X-A certificates will equal the aggregate certificate balance of the Class A-1, Class A-2, Class A-SB, Class A-3 and Class A-4 certificates outstanding from time to time. The notional amount of the Class X-B certificates will equal the aggregate certificate balance of the Class A-S and Class B certificates outstanding from time to time. The notional amount of the Class X-D certificates will equal the certificate balance of the Class D certificates outstanding from time to time. |

| (9) | The pass-through rate for the Class X-A certificates for any distribution date will be aper annum rate equal to the excess, if any, of (a) the weighted average of the net mortgage interest rates on the mortgage loans for the related distribution date, over (b) the weighted average of the pass-through rates on the Class A-1, Class A-2, Class A-SB, Class A-3 and Class A-4 certificates for the related distribution date, weighted on the basis of their respective aggregate certificate balances outstanding immediately prior to that distribution date. The pass-through rate for the Class X-B certificates for any distribution date will be aper annum rate equal to the excess, if any, of (a) the weighted average of the net mortgage interest rates on the mortgage loans for the related distribution date, over (b) the weighted average of the pass-through rates on the Class A-S and Class B certificates for the related distribution date, weighted on the basis of their respective aggregate certificate balances outstanding immediately prior to that distribution date. The pass-through rate for the Class X-D certificates for any distribution date will be aper annum rate equal to the excess, if any, of (a) the weighted average of the net mortgage interest rates on the mortgage loans for the related distribution date, over (b) the pass-through rate on the Class D certificates for the related distribution date. For purposes of the calculation of the weighted average of the net mortgage interest rates on the mortgage loans for each distribution date, the mortgage interest rates will be adjusted as necessary to a 30/360 basis. |

| (10) | Not offered pursuant to the Preliminary Prospectus or this Term Sheet. Information provided in this Term Sheet regarding the characteristics of these certificates is provided only to enhance your understanding of the offered certificates. The privately offered certificates also include the Class V and Class R certificates, which do not have a certificate balance, notional amount, pass-through rate, rating or rated final distribution date, and which are not shown in the chart. The Class V certificates represent a beneficial ownership interest held through the grantor trust in certain excess interest in respect of mortgage loans having anticipated repayment dates, if any. The Class R certificates represent the beneficial ownership of the residual interest in each of the real estate mortgage investment conduits, as further described in the Preliminary Prospectus. |

| (11) | A holder of Class E-1 and Class E-2 certificates may exchange such classes of certificates (on an aggregate basis) for a related amount of Class E certificates, and a holder of Class E certificates may exchange that class for a ratable portion of each class of the Class E-1 and Class E-2 certificates. |

| This is not a research report and was not prepared by the Underwriters’ research departments. Please see additional important information and qualifications at the end of this Term Sheet. |

| T-3 |

| MSBAM 2016-C28 | Structural Overview |

| (12) | On the closing date, the issuing entity will issue the Class E-1 and Class E-2 trust components (collectively, the “Class E Trust Components”), which will have outstanding certificate balances on the closing date of $14,335,000 and $14,335,000, respectively. The Class E-1 and Class E-2 certificates and the Class E certificates will, at all times, represent undivided beneficial ownership interests in a grantor trust that will hold such trust components. Each class of the Class E-1, Class E-2 and Class E certificates will, at all times, represent a beneficial interest in a percentage of the outstanding certificate balance of the Class E-1 and Class E-2 trust components. Following any exchange of Class E-1 and Class E-2 certificates for Class E certificates or any exchange of Class E certificates for Class E-1 and Class E-2 certificates, the percentage interest of the outstanding certificate balances of the Class E-1 and Class E-2 trust components that is represented by the Class E-1 and Class E-2 certificates and the Class E certificates will be increased or decreased accordingly. The initial balance of each class of the Class E-1 and Class E-2 certificates shown in the table above represents the maximum principal balance of such class without giving effect to any issuance of Class E certificates (and assuming no Class EF or Class EFG certificates are issued). The initial certificate balance of the Class E certificates shown in the table above is equal to the aggregate of the maximum initial certificate balances of the Class E-1 and Class E-2 certificates, representing the maximum certificate balance of the Class E certificates that could be issued in an exchange. The principal balance of the Class E-1 and Class E-2 certificates to be issued on the closing date will be reduced, in required proportions, by an amount equal to the principal balance of the Class E certificates issued on the closing date. |

| (13) | The Class E certificates will not have a pass-through rate, but will be entitled to receive the sum of the interest distributable on its percentage interests in the Class E-1 and Class E-2 trust components. The pass-through rates on the Class E-1 and Class E-2 trust components will at all times be the same as the pass-through rates of the Class E-1 and Class E-2 certificates, respectively. Any distribution of interest to the Class E certificates on the first distribution date is expected to be in an amount that would produce an effective pass-through rate equal to the weighted average of the pass-through rates of the Class E-1 and Class E-2 trust components for the first distribution date. |

| (14) | A holder of Class F-1 and Class F-2 certificates may exchange such classes of certificates (on an aggregate basis) for a related amount of Class F certificates, and a holder of Class F certificates may exchange that class for a ratable portion of each class of the Class F-1 and Class F-2 certificates. |

| (15) | On the closing date, the issuing entity will issue the Class F-1 and Class F-2 trust components (collectively, the “Class F Trust Components”), which will have outstanding certificate balances on the closing date of $4,778,000 and $4,778,000, respectively. The Class F-1 and Class F-2 certificates and the Class F certificates will, at all times, represent undivided beneficial ownership interests in a grantor trust that will hold such trust components. Each class of the Class F-1, Class F-2 and Class F certificates will, at all times, represent a beneficial interest in a percentage of the outstanding certificate balance of the Class F-1 and Class F-2 trust components. Following any exchange of Class F-1 and Class F-2 certificates for Class F certificates or any exchange of Class F certificates for Class F-1 and Class F-2 certificates, the percentage interest of the outstanding certificate balances of the Class F-1 and Class F-2 trust components that is represented by the Class F-1 and Class F-2 certificates and the Class F certificates will be increased or decreased accordingly. The initial balance of each class of the Class F-1 and Class F-2 certificates shown in the table above represents the maximum principal balance of such class without giving effect to any issuance of Class F certificates (and assuming no Class EF or Class EFG certificates are issued). The initial certificate balance of the Class F certificates shown in the table above is equal to the aggregate of the maximum initial certificate balances of the Class F-1 and Class F-2 certificates, representing the maximum certificate balance of the Class F certificates that could be issued in an exchange. The principal balance of the Class F-1 and Class F-2 certificates to be issued on the closing date will be reduced, in required proportions, by an amount equal to the principal balance of the Class F certificates issued on the closing date. |

| (16) | The Class F certificates will not have a pass-through rate, but will be entitled to receive the sum of the interest distributable on its percentage interests in the Class F-1 and Class F-2 trust components. The pass-through rates on the Class F-1 and Class F-2 trust components will at all times be the same as the pass-through rates of the Class F-1 and Class F-2 certificates, respectively. Any distribution of interest to the Class F certificates on the first distribution date is expected to be in an amount that would produce an effective pass-through rate equal to the weighted average of the pass-through rates of the Class F-1 and Class F-2 trust components for the first distribution date. |

| (17) | A holder of Class E-1, Class E-2, Class F-1 and Class F-2 certificates may exchange such classes of certificates (on an aggregate basis) for a related amount of Class EF certificates, and a holder of Class EF certificates may exchange that class for a ratable portion of each class of the Class E-1, Class E-2, Class F-1 and Class F-2 certificates. |

| (18) | Each class of the Class E-1, Class E-2, Class F-1, Class F-2 and Class EF certificates will, at all times, represent a beneficial interest in a percentage of the outstanding certificate balance of the Class E-1, Class E-2, Class F-1 and Class F-2 trust components. Following any exchange of Class E-1, Class E-2, Class F-1 and Class F-2 certificates for Class EF certificates or any exchange of Class EF certificates for Class E-1, Class E-2, Class F-1 and Class F-2 certificates, the percentage interest of the outstanding certificate balances of the Class E-1, Class E-2, Class F-1 and Class F-2 trust components that is represented by the Class E-1, Class E-2, Class F-1 and Class F-2 certificates and the Class EF certificates will be increased or decreased accordingly. The initial balance of each class of the Class E-1, Class E-2, Class F-1 and Class F-2 certificates shown in the table above represents the maximum principal balance of such class without giving effect to any issuance of Class EF certificates (and assuming no Class E, Class F or Class EFG certificates are issued). The initial certificate balance of the Class EF certificates shown in the table above is equal to the aggregate of the maximum initial certificate balances of the Class E-1, Class E-2, Class F-1 and Class F-2 certificates, representing the maximum certificate balance of the Class EF certificates that could be issued in an exchange. The principal balance of the Class E-1, Class E-2, Class F-1 and Class F-2 certificates to be issued on the closing date will be reduced, in required proportions, by an amount equal to the principal balance of the Class EF certificates issued on the closing date. |

| (19) | The Class EF certificates will not have a pass-through rate, but will be entitled to receive the sum of the interest distributable on its percentage interests in the Class E-1, Class E-2, Class F-1 and Class F-2 trust components. Any distribution of interest to the Class EF certificates on the first distribution date is expected to be in an amount that would produce an effective pass-through rate equal to the weighted average of the pass-through rates of the Class E-1, Class E-2, Class F-1 and Class F-2 trust components for the first distribution date. |

| (20) | A holder of Class G-1 and Class G-2 certificates may exchange such classes of certificates (on an aggregate basis) for a related amount of Class G certificates, and a holder of Class G certificates may exchange that class for a ratable portion of each class of the Class G-1 and Class G-2 certificates. |

| (21) | On the closing date, the issuing entity will issue the Class G-1 and Class G-2 trust components (collectively, the “Class G Trust Components”), which will have outstanding certificate balances on the closing date of $11,348,500 and $11,348,500, respectively. The Class G-1 and Class G-2 certificates and the Class G certificates will, at all times, represent undivided beneficial ownership interests in a grantor trust that will hold such trust components. Each class of the Class G-1, Class G-2 and Class G certificates will, at all times, represent a beneficial interest in a percentage of the outstanding certificate balance of the Class G-1 and Class G-2 trust components. Following any exchange of Class G-1 and Class G-2 certificates for Class G certificates or any exchange of Class G certificates for Class G-1 and Class G-2 certificates, the percentage interest of the outstanding certificate balances of the Class G-1 and Class G-2 trust components that is represented by the Class G-1 and Class G-2 certificates and the Class G certificates will be increased or decreased accordingly. The initial balance of each class of the Class G-1 and Class G-2 certificates shown in the table above represents the maximum principal balance of such class without giving effect to any issuance of Class G certificates (and assuming no Class EFG certificates are issued). The initial certificate balance of the Class G certificates shown in the table above is equal to the aggregate of the maximum initial certificate balances of the Class G-1 and Class G-2 certificates, representing the maximum certificate balance of the Class G certificates that could be issued in an exchange. The principal balance of the Class G-1 and |

| This is not a research report and was not prepared by the Underwriters’ research departments. Please see additional important information and qualifications at the end of this Term Sheet. |

| T-4 |

| MSBAM 2016-C28 | Structural Overview |

| Class G-2 certificates to be issued on the closing date will be reduced, in required proportions, by an amount equal to the principal balance of the Class G certificates issued on the closing date. |

| (22) | The Class G certificates will not have a pass-through rate, but will be entitled to receive the sum of the interest distributable on its percentage interests in the Class G-1 and Class G-2 trust components. The pass-through rates on the Class G-1 and Class G-2 trust components will at all times be the same as the pass-through rates of the Class G-1 and Class G-2 certificates, respectively. Any distribution of interest to the Class G certificates on the first distribution date is expected to be in an amount that would produce an effective pass-through rate equal to the weighted average of the pass-through rates of the Class G-1 and Class G-2 trust components for the first distribution date. |

| (23) | A holder of Class E-1, Class E-2, Class F-1, Class F-2, Class G-1 and Class G-2 certificates may exchange such classes of certificates (on an aggregate basis) for a related amount of Class EFG certificates, and a holder of Class EFG certificates may exchange that Class EFG for a ratable portion of each class of the Class E-1, Class E-2, Class F-1, Class F-2, Class G-1 and Class G-2 certificates. |

| (24) | Each class of the Class E-1, Class E-2, Class F-1, Class F-2, Class G-1, Class G-2 and Class EFG certificates will, at all times, represent a beneficial interest in a percentage of the outstanding certificate balance of the Class E-1, Class E-2, Class F-1, Class F-2, Class G-1 and Class G-2 trust components. Following any exchange of Class E-1, Class E-2, Class F-1, Class F-2, Class G-1 and Class G-2 certificates for Class EFG certificates or any exchange of Class EFG certificates for Class E-1, Class E-2, Class F-1, Class F-2, Class G-1 and Class G-2 certificates, the percentage interest of the outstanding certificate balances of the Class E-1, Class E-2, Class F-1, Class F-2, Class G-1 and Class G-2 trust components that is represented by the Class E-1, Class E-2, Class F-1, Class F-2, Class G-1 and Class G-2 certificates and the Class EFG certificates will be increased or decreased accordingly. The initial balance of each class of the Class E-1, Class E-2, Class F-1, Class F-2, Class G-1 and Class G-2 certificates shown in the table above represents the maximum principal balance of such class without giving effect to any issuance of Class EFG certificates (and assuming no Class E, Class F, Class EF or Class G certificates are issued). The initial certificate balance of the Class EFG certificates shown in the table above is equal to the aggregate of the maximum initial certificate balances of the Class E-1, Class E-2, Class F-1, Class F-2, Class G-1 and Class G-2 certificates, representing the maximum certificate balance of the Class EFG certificates that could be issued in an exchange. The principal balance of the Class E-1, Class E-2, Class F-1, Class F-2, Class G-1 and Class G-2 certificates to be issued on the closing date will be reduced, in required proportions, by an amount equal to the principal balance of the Class EFG certificates issued on the closing date. |

| (25) | The Class EFG certificates will not have a pass-through rate, but will be entitled to receive the sum of the interest distributable on its percentage interests in the Class E-1, Class E-2, Class F-1, Class F-2, Class G-1 and Class G-2 trust components. Any distribution of interest to the Class EFG certificates on the first distribution date is expected to be in an amount that would produce an effective pass-through rate equal to the weighted average of the pass-through rates of the Class E-1, Class E-2, Class F-1, Class F-2, Class G-1 and Class G-2 trust components for the first distribution date. |

| (26) | A holder of Class H-1 and Class H-2 certificates may exchange such classes of certificates (on an aggregate basis) for a related amount of Class H certificates, and a holder of Class H certificates may exchange that class for a ratable portion of each class of the Class H-1 and Class H-2 certificates. |

| (27) | On the closing date, the issuing entity will issue the Class H-1 and Class H-2 trust components (collectively, the “Class H Trust Components”), which will have outstanding certificate balances on the closing date of $14,334,677 and $14,334,677, respectively. The Class H-1 and Class H-2 certificates and the Class H certificates will, at all times, represent undivided beneficial ownership interests in a grantor trust that will hold such trust components. Each class of the Class H-1, Class H-2 and Class H certificates will, at all times, represent a beneficial interest in a percentage of the outstanding certificate balance of the Class H-1 and Class H-2 trust components. Following any exchange of Class H-1 and Class H-2 certificates for Class H certificates or any exchange of Class H certificates for Class H-1 and Class H-2 certificates, the percentage interest of the outstanding certificate balances of the Class H-1 and Class H-2 trust components that is represented by the Class H-1 and Class H-2 certificates and the Class H certificates will be increased or decreased accordingly. The initial balance of each class of the Class H-1 and Class H-2 certificates shown in the table above represents the maximum principal balance of such class without giving effect to any issuance of Class H certificates. The initial certificate balance of the Class H certificates shown in the table above is equal to the aggregate of the maximum initial certificate balances of the Class H-1 and Class H-2 certificates, representing the maximum certificate balance of the Class H certificates that could be issued in an exchange. The principal balance of the Class H-1 and Class H-2 certificates to be issued on the closing date will be reduced, in required proportions, by an amount equal to the principal balance of the Class H certificates issued on the closing date. |

| (28) | The Class H certificates will not have a pass-through rate, but will be entitled to receive the sum of the interest distributable on its percentage interests in the Class H-1 and Class H-2 trust components. The pass-through rates on the Class H-1 and Class H-2 trust components will at all times be the same as the pass-through rates of the Class H-1 and Class H-2 certificates, respectively. Any distribution of interest to the Class H certificates on the first distribution date is expected to be in an amount that would produce an effective pass-through rate equal to the weighted average of the pass-through rates of the Class H-1 and Class H-2 trust components for the first distribution date. |

| This is not a research report and was not prepared by the Underwriters’ research departments. Please see additional important information and qualifications at the end of this Term Sheet. |

| T-5 |

| MSBAM 2016-C28 | Structural Overview |

| Offered Certificates: | $813,496,000 (approximate) monthly pay, multi-class, commercial mortgage pass-through certificates, consisting of eight principal balance classes (Class A-1, Class A-2, Class A-SB, Class A-3, Class A-4, Class A-S, Class B and Class C) and two interest-only classes (Class X-A and Class X-B) | |

| Co-Lead Bookrunning Managers: | Merrill Lynch, Pierce, Fenner & Smith Incorporated and Morgan Stanley & Co. LLC | |

| Co-Managers: | CIBC World Markets Corp. and Drexel Hamilton, LLC | |

| Mortgage Loan Sellers: | Bank of America, National Association, Morgan Stanley Mortgage Capital Holdings LLC, CIBC Inc. and Starwood Mortgage Funding III LLC | |

| Rating Agencies: | DBRS, Inc., Fitch Ratings, Inc. and Moody’s Investors Service, Inc. | |

| Master Servicer: | Wells Fargo Bank, National Association | |

| Special Servicer: | C-III Asset Management LLC | |

| Certificate Administrator/ Certificate Registrar/Custodian: | Wells Fargo Bank, National Association | |

| Trustee: | Wilmington Trust, National Association | |

| Operating Advisor: | Park Bridge Lender Services LLC | |

| Asset Representations Reviewer: | Park Bridge Lender Services LLC | |

| Initial Directing Certificateholder: | C-III High Yield Real Estate Debt Fund IV Tier Holdings Inc. or an affiliate thereof | |

| Cut-off Date: | The mortgage loans will be considered part of the trust fund as of their respective cut-off dates. The cut-off date with respect to each mortgage loan is the respective due date for the monthly debt service payment that is due in February 2016 (or, in the case of any mortgage loan that has its first due date in March 2016, the date that would have been its due date in February 2016 under the terms of that mortgage loan if a monthly debt service payment were scheduled to be due in that month). | |

| Expected Pricing Date: | Week of February 8, 2016 | |

| Expected Closing Date: | Week of February 22, 2016 | |

| Determination Dates: | The 11th day of each month or, if the 11th day is not a business day, then the business day immediately following such 11th day. | |

| Distribution Dates: | The 4th business day following each determination date. The first distribution date will be in March 2016. | |

| Rated Final Distribution Date: | The distribution date in January 2049 | |

| Interest Accrual Period: | Preceding calendar month | |

| Payment Structure: | Sequential pay | |

| Tax Treatment: | REMIC | |

| Optional Termination: | 1.00% clean-up call | |

| Minimum Denominations: | $10,000 for each class of Offered Certificates (other than Class X-A and Class X-B certificates); $1,000,000 for the Class X-A and Class X-B certificates | |

| Settlement Terms: | DTC, Euroclear and Clearstream | |

| Legal/Regulatory Status: | Each class of Offered Certificates is expected to be eligible for exemptive relief under ERISA. No class of Offered Certificates is SMMEA eligible. | |

| Analytics: | The certificate administrator is expected to make available all distribution date statements, CREFC® reports and supplemental notices received by it to certain modeling financial services as described in the Preliminary Prospectus. | |

| Bloomberg Ticker: | MSBAM 2016-C28 <MTGE><GO> | |

| Risk Factors: | THE CERTIFICATES INVOLVE CERTAIN RISKS AND MAY NOT BE SUITABLE FOR ALL INVESTORS. SEE THE “RISK FACTORS” SECTION OF THE PRELIMINARY PROSPECTUS. |

| This is not a research report and was not prepared by the Underwriters’ research departments. Please see additional important information and qualifications at the end of this Term Sheet. |

| T-6 |

| MSBAM 2016-C28 | Structural Overview |

| Accrual: | Each class of Offered Certificates will accrue interest on a 30/360 basis. | |

| Amount and Order of Distributions: | On each distribution date, funds available for distribution from the mortgage loans, net of (i) specified expenses of the issuing entity, including fees payable to, and costs and expenses reimbursable to, the master servicer, the special servicer, the certificate administrator, the trustee, the operating advisor, the asset representations reviewer and CREFC®, (ii) any yield maintenance charges and prepayment premiums and (iii) any excess interest distributable to the Class V certificates, will be distributed in the following amounts and order of priority:

First, to the Class A-1, Class A-2, Class A-SB, Class A-3, Class A-4, Class X-A, Class X-B and Class X-D certificates, in respect of interest, up to an amount equal to, and pro rata in accordance with, the interest entitlements for those classes;

Second, to the Class A-1, Class A-2, Class A-SB, Class A-3 and Class A-4 certificates as follows, to the extent of funds allocated to principal and available for distribution: (i) (a) first, to principal on the Class A-SB certificates, until the certificate balance of the Class A-SB certificates is reduced to the planned principal balance for the related distribution date set forth in Annex E to the Preliminary Prospectus, (b) second, to principal on the Class A-1 certificates, until the certificate balance of the Class A-1 certificates has been reduced to zero, (c) third, to principal on the Class A-2 certificates, until the certificate balance of the Class A-2 certificates has been reduced to zero, (d) fourth, to principal on the Class A-3 certificates until the certificate balance of the Class A-3 certificates has been reduced to zero, (e) fifth, to principal on the Class A-4 certificates until the certificate balance of the Class A-4 certificates has been reduced to zero, and (f) sixth, to principal on the Class A-SB certificates, until the certificate balance of the Class A-SB certificates has been reduced to zero, or (ii) if the certificate balance of each class of certificates other than the Class A-1, Class A-2, Class A-SB, Class A-3 and Class A-4 certificates has been reduced to zero as a result of the allocation of mortgage loan losses to those certificates, funds available for distributions of principal will be distributed to the Class A-1, Class A-2, Class A-SB, Class A-3 and Class A-4 certificates, pro rata, without regard to the distribution priorities described above or the planned principal balance of the Class A-SB certificates;

Third, to the Class A-1, Class A-2, Class A-SB, Class A-3 and Class A-4 certificates, to reimburse the Class A-1, Class A-2, Class A-SB, Class A-3 and Class A-4 certificates, first, up to an amount equal to, and pro rata, based on, any previously unreimbursed losses on the mortgage loans allocable to principal that were previously borne by each such class, and second, up to an amount equal to, and pro rata based on, interest on such unreimbursed losses previously allocated to each such class at the pass-through rate for such class from the date the related loss was allocated to such class;

Fourth, to the Class A-S certificates as follows: (a) to interest on the Class A-S certificates in the amount of its interest entitlement; (b) to the extent of funds allocable to principal remaining after distributions in respect of principal to each class with a higher priority (as set forth in prior enumerated clauses set forth above), to principal on the Class A-S certificates until its certificate balance has been reduced to zero; and (c) to reimburse the Class A-S certificates first for any previously unreimbursed losses on the mortgage loans that were previously allocated to those certificates, and second, for interest on such unreimbursed loss amount at the pass-through rate for such class;

Fifth, to the Class B certificates as follows: (a) to interest on the Class B certificates in the amount of its interest entitlement; (b) to the extent of funds allocable to principal remaining after distributions in respect of principal to each class with a higher priority (as set forth in prior enumerated clauses set forth above), to principal on the Class B certificates until its certificate balance has been reduced to zero; and (c) to reimburse the Class B certificates first, for any previously unreimbursed losses on the mortgage loans that were previously allocated to those certificates, and second, for interest on such unreimbursed loss amount at the pass-through rate for such class;

Sixth, to the Class C certificates as follows: (a) to interest on the Class C certificates in the amount of its interest entitlement; (b) to the extent of funds allocable to principal remaining after distributions in respect of principal to each class with a higher priority (as set forth in prior enumerated clauses set forth above), to principal on the Class C certificates until its certificate balance has been reduced to zero; and (c) to reimburse the Class C certificates first for any previously unreimbursed losses on the mortgage loans that were previously allocated to those certificates, and second, for interest on such unreimbursed loss amount at the pass-through rate for such class;

Seventh, to the non-offered certificates (other than the Class X-D certificates and other than the Class R and Class V certificates) in the amounts and order of priority described under “Description of the Certificates—Distributions” in the Preliminary Prospectus; and

Eighth, to the Class R certificates, any remaining amounts.

| |

| Exchangeable Certificates | The Class E-1, Class E-2, Class F-1, Class F-2, Class G-1, Class G-2, Class H-1 and Class H-2 certificates are collectively referred to herein as the “Exchangeable Certificates”, and the Class E, Class F, Class EF, Class G, Class EFG and Class H certificates are collectively referred to herein as the “Exchangeable Combined Certificates.” On the closing date, the upper-tier REMIC of the issuing entity will issue the Class E-1, Class E-2, Class F-1, Class F-2, Class G-1, Class G-2, Class H-1 and Class H-2 trust components (each a “trust component”), which will have outstanding balances on the closing date set forth in the table below and |

| This is not a research report and was not prepared by the Underwriters’ research departments. Please see additional important information and qualifications at the end of this Term Sheet. |

| T-7 |

| MSBAM 2016-C28 | Structural Overview |

| will be held in the grantor trust for the benefit of the holders of the Exchangeable Certificates and the Exchangeable Combined Certificates. Exchangeable Certificates will at all times represent undivided beneficial ownership interests, held through the grantor trust, in one or more of such trust components, as further described in the Preliminary Prospectus. |

| Trust Component | Closing Date Balance | |||

| Class E-1 trust component | $ | 14,335,000 | ||

| Class E-2 trust component | $ | 14,335,000 | ||

| Class F-1 trust component | $ | 4,778,000 | ||

| Class F-2 trust component | $ | 4,778,000 | ||

| Class G-1 trust component | $ | 11,348,500 | ||

| Class G-2 trust component | $ | 11,348,500 | ||

| Class H-1 trust component | $ | 14,334,677 | ||

| Class H-2 trust component | $ | 14,334,677 | ||

Each class of Exchangeable Combined Certificates may be exchanged for the corresponding classes of Exchangeable Certificates set forth next to such class in the table below, and vice versa. The Exchange Percentage set forth next to each class of Exchangeable Certificates in the table below represents the percentage of the aggregate certificate balance of the Exchangeable Certificates involved in an exchange that is represented by the certificate balance of such class of Exchangeable Certificates that is required to be surrendered to receive the corresponding Exchangeable Combined Certificates (or that will be received if Exchangeable Combined Certificates are surrendered). |

| Class of Exchangeable Combined Certificates | Corresponding Classes of Exchangeable Certificates | Exchange Percentage | |

| Class E | Class E-1 Class E-2 | 50% 50% | |

| Class F | Class F-1 Class F-2 | 50% 50% | |

| Class EF | Class E-1 Class E-2 Class F-1 Class F-2 | 37.5006540051274% 37.5006540051274% 12.4993459948726% 12.4993459948726% | |

| Class G | Class G-1 Class G-2 | 50% 50% | |

| Class EFG | Class E-1 Class E-2 Class F-1 Class F-2 Class G-1 Class G-2 | 23.5297014263907% 23.5297014263907% 7.84268667005893% 7.84268667005893% 18.6276119035504% 18.6276119035504% | |

| Class H | Class H-1 Class H-2 | 50% 50% |

No class of Exchangeable Combined Certificates will have a pass-through rate; instead, each such class of Exchangeable Combined Certificates be entitled to receive the sum of the interest that would otherwise be distributable in respect of the percentage interest in each related trust component evidenced by such class of Exchangeable Combined Certificates. The various amounts distributable on a class of Exchangeable Combined Certificates on each distribution date in respect of Interest Accrual Amounts, Interest Distribution Amounts, principal distribution amounts, reimbursements of Realized Losses and yield maintenance charges allocated to any of the related trust components evidenced by such class of Exchangeable Combined Certificates will be so distributed in a single, aggregate distribution to the holders of such class of Exchangeable Combined Certificates on such distribution date. In addition, each class of Exchangeable Combined Certificates will be allocated the aggregate amount of Realized Losses, Interest Shortfalls, and any other shortfalls in respect of the percentage interest in each related trust component evidenced by such class of Exchangeable Combined Certificates.

For the avoidance of doubt, no fee will be required with respect to any exchange of Exchangeable Certificates.

| ||

| Interest and Principal Entitlements: | The interest entitlement of each class of Offered Certificates on each distribution date generally will be the interest accrued during the related interest accrual period on the related certificate balance or notional amount at the related pass-through rate, net of any prepayment interest shortfalls allocated to that class for such |

| This is not a research report and was not prepared by the Underwriters’ research departments. Please see additional important information and qualifications at the end of this Term Sheet. |

| T-8 |

| MSBAM 2016-C28 | Structural Overview |

distribution date as described below. If prepayment interest shortfalls arise from voluntary prepayments on serviced mortgage loans during any collection period, the master servicer is required to make a compensating interest payment to offset those shortfalls. See “Description of the Certificates—Prepayment Interest Shortfalls” in the Preliminary Prospectus. The remaining amount of prepayment interest shortfalls will be allocated to reduce the interest entitlement on all classes of certificates,pro rata, based on their respective amounts of accrued interest for the related distribution date. If a class receives less than the entirety of its interest entitlement on any distribution date, then the shortfall, excluding any shortfall due to prepayment interest shortfalls, will be added to its interest entitlement for the next succeeding distribution date.

The principal distribution amount for each distribution date generally will be the aggregate amount of principal received or advanced in respect of the mortgage loans, net of any non-recoverable advances and interest thereon that are reimbursed to the master servicer, the special servicer or the trustee during the related collection period. Non-recoverable advances and interest thereon are reimbursable from principal collections before reimbursement from other amounts.

| ||

Special Servicer Compensation: | The principal compensation to be paid to the special servicer in respect of its special servicing activities will be the special servicing fee, the workout fee and the liquidation fee.

The special servicing fee for each distribution date is calculated based on the outstanding principal balance of each mortgage loan (other than any non-serviced mortgage loan) that is a specially serviced mortgage loan (and any related serviced companion loan) or as to which the related mortgaged property has become an REO property at the special servicing fee rate, which will be a rate equal to the greater of 0.25%per annum and theper annum rate that would result in a special servicing fee of $3,500 for the related month. The special servicing fee will be payable monthly,first, from liquidation proceeds, insurance and condemnation proceeds, and collections in respect of the related specially serviced mortgage loan or REO property and,then, from general collections on all the mortgage loans (other than a non-serviced mortgage loan) and any REO properties.

The special servicer will also be entitled to (i) liquidation fees generally equal to 1.0% of liquidation proceeds in respect of a specially serviced mortgage loan (and any related serviced companion loan) or related REO property and (ii) workout fees generally equal to 1.0% of interest and principal payments made in respect of a rehabilitated mortgage loan (and any related serviced companion loan), subject to a cap with respect to each such fee of $1,000,000 with respect to any mortgage loan, whole loan or related REO property and subject to certain adjustments and exceptions as described in the Preliminary Prospectus under “Pooling and Servicing Agreement—Servicing and Other Compensation and Payment of Expenses—Special Servicer Compensation”.

With respect to any non-serviced mortgage loan, the related special servicer under the related other pooling and servicing agreement pursuant to which such mortgage loan is being serviced will be entitled to similar compensation as that described above with respect to such non-serviced mortgage loan under such other pooling and servicing agreement as further described in the Preliminary Prospectus, although any related fees may accrue at a different rate and there may be a higher (or no) cap on liquidation and workout fees. | |

| Prepayment Premiums/Yield Maintenance Charges: | If any yield maintenance charge or prepayment premium is collected during any particular collection period with respect to any Mortgage Loan, then on the Distribution Date corresponding to that collection period, the certificate administrator will pay to the holders of each class of the Class A-1, Class A-2, Class A-SB, Class A-3, Class A-4, Class A-S, Class B, Class C and Class D certificates, the product of (a) such yield maintenance charge or prepayment premium, (b) the related Base Interest Fraction (as defined below) for such class, and (c) a fraction, the numerator of which is equal to the amount of principal distributed to such class for that distribution date, and the denominator of which is the total amount of principal distributed to the principal balance certificates (other than the Control Eligible Certificates) for that distribution date. Any yield maintenance charge or prepayment premium that is collected during any particular collection period with respect to any mortgage loan and remaining after the distributions in the preceding sentence (as to the applicable distribution date, the “Class X YM Distribution Amount”) will be distributed to the holders of the Class X certificates as follows: (1) first, to the Class X-A and Class X-B certificates, in each case in an amount equal to the product of (i) a fraction, the numerator of which is equal to the amount of principal distributed on the applicable distribution date with respect to the class(es) of principal balance certificates whose certificate balances comprise the notional amount of the applicable class of Class X certificates, and the denominator of which is the total amount of principal distributed on the applicable distribution date with respect to the principal balance certificates, multiplied by (ii) the Class X YM Distribution Amount for the applicable distribution date, and (2) second, to the Class X-D certificates, in an amount equal to the portion of the Class X YM Distribution Amount remaining after the distributions to the holders of the Class X-A and Class X-B certificates. “Base Interest Fraction” means, with respect to any principal prepayment of any mortgage loan that provides for the payment of a yield maintenance charge or prepayment premium, and with respect to any class of principal balance certificates, a fraction (A) the numerator of which is the greater of (x) zero and (y) the difference between (i) the pass-through rate on that class, and (ii) the applicable discount rate and (B) the denominator of which is the difference between (i) the mortgage interest rate on the related mortgage loan and (ii) the applicable discount rate; provided, however, that: under no circumstances will the Base Interest Fraction be greater than one; if the discount rate referred to above is greater than or equal to the mortgage interest rate on the related mortgage loan and is greater than or equal to the pass-through rate on that class, then the Base Interest Fraction will equal zero; and if the discount rate referred to above is greater than or equal to the mortgage interest rate on the related mortgage loan and is less than the pass-through rate on that |

| This is not a research report and was not prepared by the Underwriters’ research departments. Please see additional important information and qualifications at the end of this Term Sheet. |

| T-9 |

| MSBAM 2016-C28 | Structural Overview |

| class, then the Base Interest Fraction will be equal to 1.0. Consistent with the foregoing, the Base Interest Fraction is equal to: | ||||

| (Pass-Through Rate – Discount Rate) | ||||

| (Mortgage Rate – Discount Rate) | ||||

| Realized Losses: | On each distribution date, immediately following the distributions to be made to the certificateholders on that date, the certificate administrator is required to calculate the amount, if any, by which (i) the aggregate stated principal balance of the mortgage loans, including any successor REO loans expected to be outstanding immediately following that distribution date is less than (ii) the then aggregate certificate balance of the principal balance certificates (other than the Exchangeable Certificates and the Exchangeable Combined Certificates) and trust components after giving effect to distributions of principal on that distribution date (any such deficit, a “Realized Loss”).

first, to the Class H-2 Trust Component (and correspondingly, to the Class H-2 certificates and the Class H certificates,pro rata based on their respective percentage interests in the Class H-2 Trust Component);

second, to the Class H-1 Trust Component (and correspondingly, to the Class H-1 certificates and the Class H certificates,pro rata based on their respective percentage interests in the Class H-1 Trust Component);

third, to the Class G-2 Trust Component (and correspondingly, to the Class G-2 certificates, the Class G certificates and the Class EFG certificates,pro rata based on their respective percentage interests in the Class G-2 Trust Component);

fourth, to the Class G-1 Trust Component (and correspondingly, to the Class G-1 certificates, the Class G certificates and the Class EFG certificates,pro rata based on their respective percentage interests in the Class G-1 Trust Component);

fifth, to the Class F-2 Trust Component (and correspondingly, to the Class F-2 certificates, the Class F certificates, the Class EF certificates and the Class EFG certificates,pro rata based on their respective percentage interests in the Class F-2 Trust Component);

sixth, to the Class F-1 Trust Component (and correspondingly, to the Class F-1 certificates, the Class F certificates, the Class EF certificates and the Class EFG certificates,pro rata based on their respective percentage interests in the Class F-1 Trust Component);

seventh, to the Class E-2 Trust Component (and correspondingly, to the Class E-2 certificates, the Class E certificates, the Class EF certificates and the Class EFG certificates,pro rata based on their respective percentage interests in the Class E-2 Trust Component);

eighth, to the Class E-1 Trust Component (and correspondingly, to the Class E-1 certificates, the Class E certificates, the Class EF certificates and the Class EFG certificates,pro rata based on their respective percentage interests in the Class E-1 Trust Component),

ninth, to the Class D certificates;

tenth, to the Class C certificates;

eleventh, to the Class B certificates; and

twelfth, to the Class A-S certificates.

Following the reduction of the certificate balances of all such classes of certificates (and, in turn, the related trust components) to zero, the certificate administrator will be required to allocate Realized Losses among the Class A-1, Class A-2, Class A-SB, Class A-3 and Class A-4 certificates,pro rata, based upon their respective certificate balances, until their respective certificate balances have been reduced to zero.

| |||

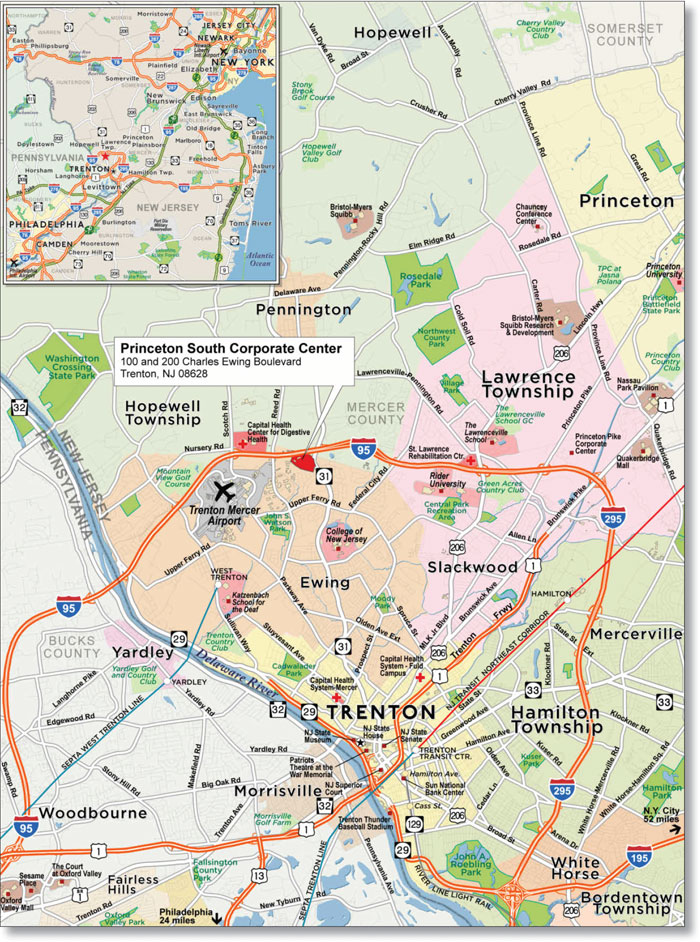

| Serviced Whole Loans: | The mortgaged property identified on Annex A-1 to the Preliminary Prospectus as Princeton Pike Corporate Center secures (i) a mortgage loan (the “Princeton Pike Corporate Center mortgage loan”) with an outstanding principal balance as of the Cut-off Date of $50,000,000, representing approximately 5.2% of the initial pool balance, and (ii) two (2)pari passu promissory notes that are not part of the mortgage pool (collectively referred to as the “Princeton Pike Corporate Centerpari passu companion loan” and a “servicedpari passu companion loan”), with an aggregate outstanding principal balance as of the Cut-off Date of $80,000,000. The Princeton Pike Corporate Centerpari passu companion loan is expected to be held by Morgan Stanley Bank, N.A. or an affiliate thereof on the closing date and may be contributed to one or more future securitization transactions or may be otherwise transferred at any time. The Princeton Pike Corporate Center mortgage loan and the Princeton Pike Corporate Centerpari passu companion loan are collectively referred to as the “Princeton Pike Corporate Center whole loan” and a “servicedpari passu whole loan” and will be serviced pursuant to the related intercreditor agreement and the pooling and servicing agreement for this transaction. With respect to the Princeton Pike Corporate Center mortgage loan, any holder of the Princeton Pike Corporate Centerpari passu companion loan will have certain consultation rights under the pooling and servicing agreement with respect to certain major decisions and other matters related to the Princeton Pike Corporate Center whole loan. | |||

| This is not a research report and was not prepared by the Underwriters’ research departments. Please see additional important information and qualifications at the end of this Term Sheet. |

| T-10 |

| MSBAM 2016-C28 | Structural Overview |

| The mortgaged property identified on Annex A-1 to the Preliminary Prospectus as Le Meridien Cambridge MIT secures (i) a mortgage loan (the “Le Meridien Cambridge MIT mortgage loan”) with an outstanding principal balance as of the Cut-off Date of $30,000,000, representing approximately 3.1% of the initial pool balance, and (ii) two (2)pari passu promissory notes that are not part of the mortgage pool (collectively referred to as the “Le Meridien Cambridge MITpari passu companion loan” and a “servicedpari passu companion loan”), with an aggregate outstanding principal balance as of the Cut-off Date of $42,200,000. The Le Meridien Cambridge MITpari passu companion loan is expected to be held by Bank of America, National Association or an affiliate thereof on the closing date and may be contributed to one or more future securitization transactions or may be otherwise transferred at any time. The Le Meridien Cambridge MIT mortgage loan and the Le Meridien Cambridge MITpari passu companion loan are collectively referred to as the “Le Meridien Cambridge MIT whole loan” and a “servicedpari passu whole loan” and will be serviced pursuant to the related intercreditor agreement and the pooling and servicing agreement for this transaction. With respect to the Le Meridien Cambridge MIT mortgage loan, any holder of the Le Meridien Cambridge MITpari passu companion loan will have certain consultation rights under the pooling and servicing agreement with respect to certain major decisions and other matters related to the Le Meridien Cambridge MIT whole loan. | ||

| There are no other “servicedpari passu whole loans,” and there are no “serviced AB whole loans,” related to the issuing entity. See “Description of the Mortgage Pool—The Whole Loans” in the Preliminary Prospectus. | ||

| With respect to any mortgage loan that is part of a serviced whole loan, unless otherwise indicated, all LTV, DSCR and Debt Yield calculations herein include the related servicedpari passu companion loan. | ||

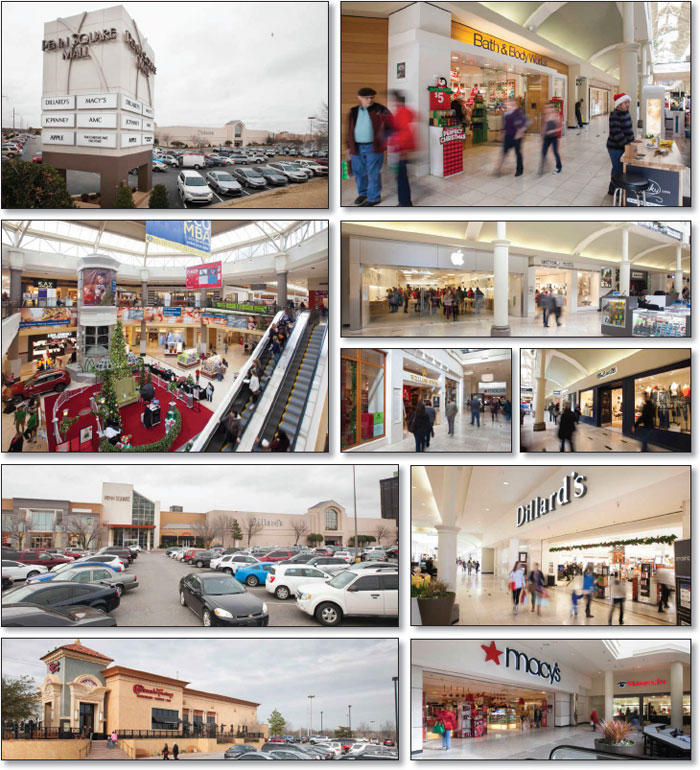

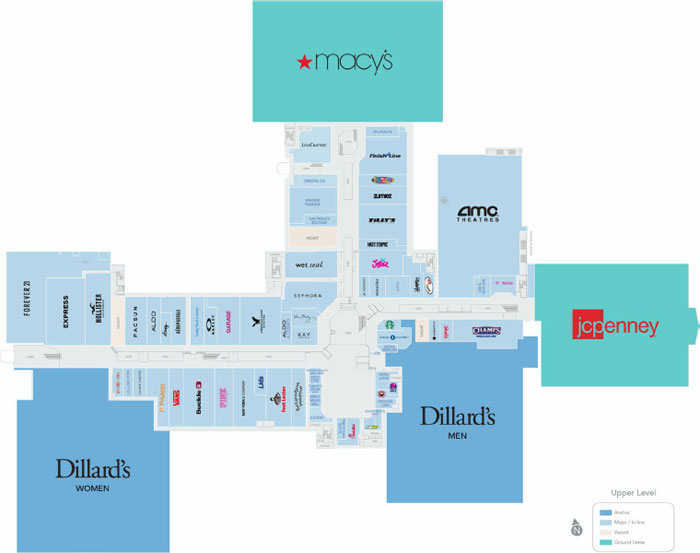

| Non-Serviced Whole Loans: | The mortgaged property identified on Annex A-1 to the Preliminary Prospectus as Penn Square Mall secures (1) on a generally seniorpari passu basis (a) a mortgage loan (the “Penn Square Mall mortgage loan”) with an outstanding principal balance as of the Cut-off Date of $90,000,000, representing approximately 9.4% of the initial pool balance, and (b) two (2)pari passu promissory notes that have an aggregate outstanding principal balance as of the Cut-off Date of $116,500,000 (collectively referred to as the “Penn Square Mall non-servicedpari passu companion loan” and a “non-servicedpari passu companion loan”), which promissory notes are not included in the issuing entity and are currently held by the MSCI 2016-PSQ securitization trust and by Morgan Stanley Bank, N.A., and (2) one (1) subordinate promissory note with an outstanding principal balance as of the Cut-off Date of $103,500,000 (the “Penn Square Mall non-serviced subordinate companion loan” and a “subordinate companion loan”), which promissory note is generally subordinate in right of payment to the Penn Square Mall mortgage loan and the Penn Square Mall non-servicedpari passu companion loan, is not included in the issuing entity and is currently held by the MSCI 2016-PSQ securitization trust. The promissory note held by Morgan Stanley Bank, N.A. may be contributed to one or more future securitization transactions or may be otherwise transferred at any time. The Penn Square Mall mortgage loan, the Penn Square Mall non-servicedpari passu companion loan and the Penn Square Mall non-serviced subordinate companion loan are collectively referred to herein as the “Penn Square Mall whole loan” and a “non-serviced whole loan”. The Penn Square Mall whole loan will be serviced pursuant to the related intercreditor agreement and the MSCI 2016-PSQ trust and servicing agreement. The holder of the controlling portion of the Penn Square Mall non-servicedpari passu companion loan (or, so long as such portion is included in the MSCI 2016-PSQ securitization trust, the controlling class representative thereunder (or other party designated to exercise the rights of such control note)) will be entitled to direct the servicing of the Penn Square Mall whole loan and will have the right to replace the special servicer with respect to the Penn Square Mall whole loan with or without cause. | |

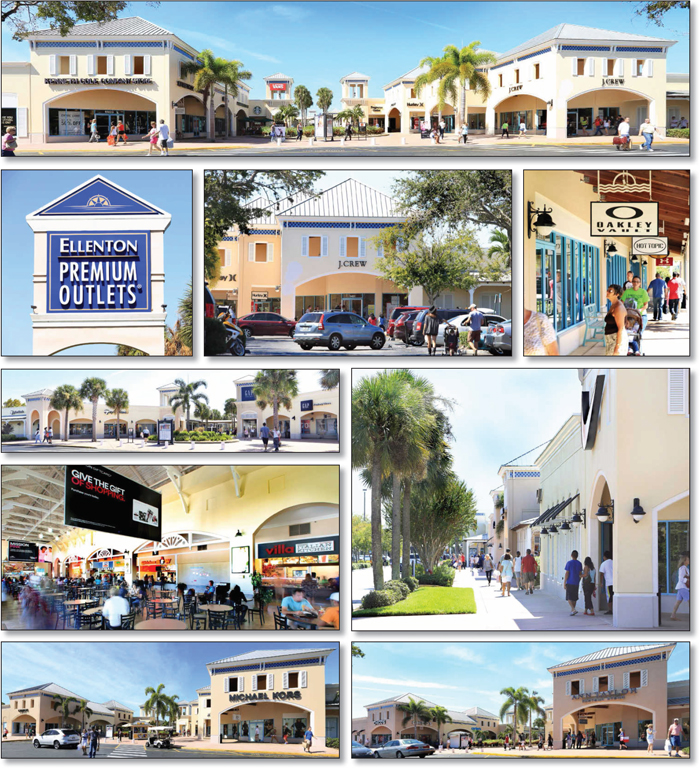

| The mortgaged property identified on Annex A-1 to the Preliminary Prospectus as Ellenton Premium Outlets secures on apari passu basis (i) a mortgage loan (the “Ellenton Premium Outlets mortgage loan”) with an outstanding principal balance as of the Cut-off Date of $71,200,000, representing approximately 7.5% of the initial pool balance, and (ii) threepari passu promissory notes that are not part of the mortgage pool (collectively referred to as the “Ellenton Premium Outlets non-servicedpari passu companion loan” and a “non-servicedpari passu companion loan”), with an aggregate outstanding principal balance as of the Cut-off Date of $106,800,000. The Ellenton Premium Outlets non-servicedpari passu companion loan is not included in the issuing entity: a portion thereof (represented by promissory Note A-1 and Note A-3) is currently held by the MSCI 2015-UBS8 securitization trust, and a portion thereof (represented by promissory Note A-2) is currently held by UBS Real Estate Securities Inc., which may sell such portion at any time, subject to compliance with the related intercreditor agreement. The Ellenton Premium Outlets mortgage loan and the Ellenton Premium Outlets non-servicedpari passu companion loan are collectively referred to herein as the “Ellenton Premium Outlets whole loan” and a “non-serviced whole loan” and will be serviced pursuant to the related intercreditor agreement and the pooling and servicing agreement for the MSCI 2015-UBS8 securitization. The holder of the portion of the Ellenton Premium Outlets non-servicedpari passu companion loan represented by promissory Note A-1 (or, so long as such portion is included in the MSCI 2015-UBS8 securitization trust, the controlling class representative thereunder (or other party designated to exercise the rights of such control note)) will be entitled to direct the servicing of the Ellenton Premium Outlets whole loan and will have the right to replace the special servicer with respect to the Ellenton Premium Outlets whole loan with or without cause. | ||

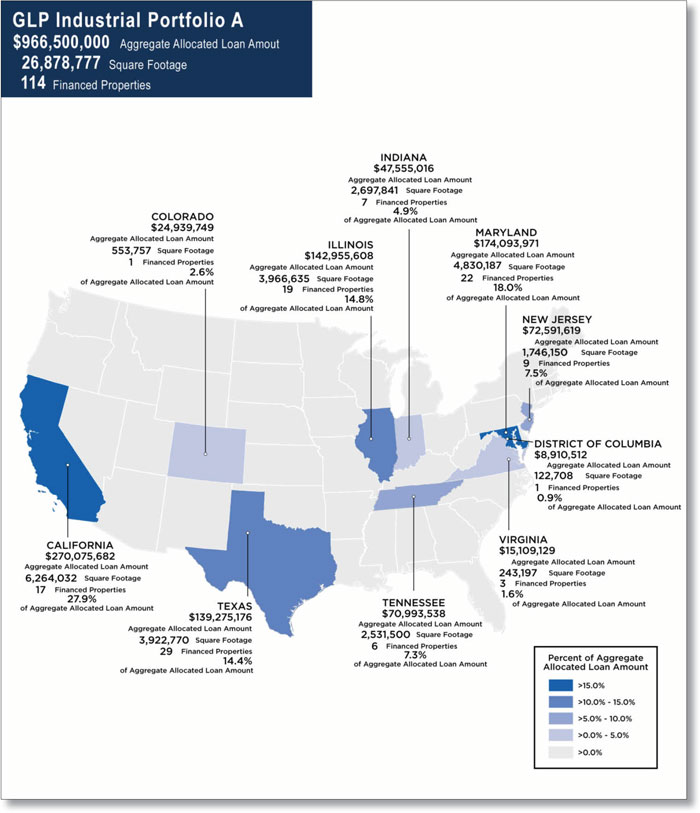

| The portfolio of mortgaged properties identified on Annex A-1 to the Preliminary Prospectus as GLP Industrial Portfolio A secures (1) on a generally seniorpari passu basis (a) a mortgage loan (the “GLP Industrial Portfolio A mortgage loan”) with an outstanding principal balance as of the Cut-off Date of $70,000,000, representing approximately 7.3% of the initial pool balance, and (b) four (4)pari passu promissory notes that have an aggregate outstanding principal balance as of the Cut-off Date of $567,600,000 (collectively referred to as the “GLP Industrial Portfolio A non-servicedpari passucompanion loan” and a “non-serviced pari passu |

| This is not a research report and was not prepared by the Underwriters’ research departments. Please see additional important information and qualifications at the end of this Term Sheet. |

| T-11 |

| MSBAM 2016-C28 | Structural Overview |

companion loan”), which promissory notes are not included in the issuing entity and are currently held by the CSMC 2015-GLPA securitization trust, the CSAIL 2016-C5 securitization trust and Column Financial, Inc. or an affiliate thereof, and (2) two (2) subordinate promissory notes with an aggregate outstanding principal balance as of the Cut-off Date of $328,900,000 (the “GLP Industrial Portfolio A non-serviced subordinate companion loan” and a “subordinate companion loan”), which promissory notes are generally subordinate in right of payment to the GLP Industrial Portfolio A mortgage loan and the GLP Industrial Portfolio A non-servicedpari passu companion loan, are not included in the issuing entity and are currently held by the CSMC 2015-GLPA securitization trust. The promissory note held by Column Financial, Inc. or an affiliate thereof may be contributed to one or more future securitization transactions or may be otherwise transferred at any time. The GLP Industrial Portfolio A mortgage loan, the GLP Industrial Portfolio A non-servicedpari passu companion loan and the GLP Industrial Portfolio A non-serviced subordinate companion loan are collectively referred to herein as the “GLP Industrial Portfolio A whole loan” and a “non-serviced whole loan”. The GLP Industrial Portfolio A whole loan will be serviced pursuant to the related intercreditor agreement and the CSMC 2015-GLPA trust and servicing agreement. The holder of the controlling portion of the GLP Industrial Portfolio A non-servicedpari passu companion loan (or, so long as such portion is included in the CSMC 2015-GLPA securitization trust, the controlling class representative thereunder (or other party designated to exercise the rights of such control note)) will be entitled to direct the servicing of the GLP Industrial Portfolio A whole loan and will have the right to replace the special servicer with respect to the GLP Industrial Portfolio A whole loan with or without cause.

The mortgaged property identified on Annex A-1 to the Preliminary Prospectus as University West Apartments secures on apari passu basis (i) a mortgage loan (the “University West Apartments mortgage loan”) with an outstanding principal balance as of the Cut-off Date of $18,000,000, representing approximately 1.9% of the initial pool balance, and (ii) onepari passu promissory note that is not part of the mortgage pool (referred to as the “University West Apartments non-servicedpari passu companion loan” and a “non-servicedpari passu companion loan”), with an outstanding principal balance as of the Cut-off Date of $27,000,000. Thepari passu promissory note evidencing the University West Apartments non-servicedpari passu companion loan is currently held by the MSBAM 2015-C27 securitization trust. The University West Apartments mortgage loan and the University West Apartments non-servicedpari passu companion loan are collectively referred to herein as the “University West Apartments whole loan” and a “non-serviced whole loan” and will be serviced pursuant to the related intercreditor agreement and the pooling and servicing agreement for the MSBAM 2015-C27 securitization. The holder of the University West Apartments non-servicedpari passu companion loan (or, so long as such companion loan is included in the MSBAM 2015-C27 securitization trust, the controlling class representative thereunder (or other party designated to exercise the rights of such control note)) will be entitled to direct the servicing of the University West Apartments whole loan and will have the right to replace the special servicer with respect to the University West Apartments whole loan with or without cause.