March 24, 2022

VIA EDGAR AND ELECTRONIC MAIL

Securities and Exchange Commission

Division of Corporation Finance

100 F Street, N.E.

Mail Stop 3233

Washington, D.C. 20549

| Attention: | Division of Corporation Finance |

| Office of Technology |

| Re: | IDT Corporation | |

| Form 10-K for the Year Ended July 31, 2021 | ||

| Filed October 14, 2021 | ||

| Form 8-K furnished March 7, 2022 | ||

| File No. 001-16371 |

Dear Ms. Blye:

We are writing to respond to the comments raised in your letter to IDT Corporation (the “Company”), dated March 11, 2022. For your convenience, we have reprinted below the comments in your letter prior to our response thereto.

Form 10-K for Fiscal Year Ended July 31, 2021 Consolidated Statements of Cash Flows, page F-8

| 1. | We note you include the change in Customer deposits at IDT Financial Services Limited (Gibraltar-based bank) within operating activities. Please tell us the specific guidance in ASC 230 you relied upon in your determination to classify the cash flows associated with this liability as operating activities. In your response, tell us about the nature and timing of the underlying cash flows and how you considered an alternative classification such as financing activities. In addition, reconcile for us the amount of the net change in Customer deposits at IDT Financial Services Limited (Gibraltar-based bank) as disclosed on your cash flow statement for fiscal 2021 to the net change in the customer deposits liability presented on your balance sheet. |

| Response: IDT Financial Services Limited (“IDTFS”) is a licensed bank authorized by the Gibraltar Financial Services Commission to conduct business as an electronic money (e-money) institution. IDTFS is an issuing only member of Mastercard and a full member of Visa Europe Limited. IDTFS’ customers offer prepaid Mastercard or VISA cards to end users. IDTFS earns a fee for providing its customers with the setup, payment service, compliance, and reporting required by Mastercard, VISA, and regulators. IDTFS may not take deposits from the public, pay interest on the holding of electronic money, or engage in lending activities. IDTFS’ customer deposit liability is the e-money customer funds, which are the aggregate balance on prepaid Mastercard or Visa cards that will be used by an end user. In contrast to a commercial bank, IDTFS’ customer deposits are not used to finance any lending or other activity of IDTFS. |

| We considered the definitions of Financing activities and Operating activities in ASC 230-10-20, and the examples of cash inflows from financing activities in ASC 230-10-45-14 and cash outflows for financing activities in ASC 230-10-45-15, as well as the examples of cash inflows from operating activities in ASC 230-10-45-16 and cash outflows for operating activities in ASC 230-10-45-17. Specifically, we note that IDTFS’ customer deposits do not meet the definition of Financing activities because they are not resources from owners, restricted resources that by donor stipulation must be used for long-term purposes, borrowed money, or other resources obtained from creditors on long-term credit. We believe the cash flows associated with IDTFS’ customer deposit liability are Operating activities because, “Operating activities include all transactions and other events that are not defined as investing or financing activities. Operating activities generally involve producing and delivering goods and providing services. Cash flows from operating activities are generally the cash effects of transactions and other events that enter into the determination of net income.” | |

| IDTFS receives cash from its customers and end users that it deposits, net of its transaction fees into restricted accounts, with an offsetting liability recorded to the customer deposit account, which will be remitted as the end user utilizes the prepaid card. We view the collection of the cash from the customer and end user, and remittance to Mastercard and VISA as the service provided to IDTFS’ customer as part of the prepaid card sales process in accordance with ASC 230-10-45-16, and thus the operating nature of the cash flows is appropriate. | |

| The following table reconciles the amount of the net change in customer deposits as disclosed in the cash flow statement to the net change in the customer deposits liability in the balance sheet: |

Customer Deposits (in thousands) | ||||||||

| Fiscal 2021 | Fiscal 2020 | |||||||

| Beginning balance sheet balance | $ | 115,992 | $ | 175,028 | ||||

| Foreign currency translation adjustment | 6,438 | 11,365 | ||||||

| Cash flow statement net change | (6,906 | ) | (70,401 | ) | ||||

| Ending balance sheet balance | $ | 115,524 | $ | 115,992 | ||||

Note 5 - Cash, Cash Equivalents, and Restricted Cash and Cash Equivalents, page F-8

| 2. | Please revise to describe the nature of the restrictions applicable to restricted cash and cash equivalents. Refer to ASC 230-10-50-7 and Rule 5-02(1) of Regulation S-X. | |

| Response: IDTFS’ restricted cash and cash equivalents consist primarily of end users’ cash plus immaterial amounts for regulatory capital reserves and cash to be paid to Mastercard and VISA. End user cash includes float amounts received from customers and end users that have not yet been added to the prepaid Mastercard and Visa cards, and e-money customer funds. Float amounts and e-money customer funds are restricted by the Gibraltar Financial Services (Electronic Money) Regulations 2020, Part 4, sections 30 and 31, that require end users’ cash to be safeguarded, segregated from any other cash that IDTFS holds, and utilized for the intended payment transaction. To clarify our existing disclosure, we will include the following additional information in future filings: | ||

| “Certain of the electronic money financial services regulations in Gibraltar require IDTFS to safeguard cash held for customer deposits, segregate cash held for customer deposits from any other cash that IDTFS holds and utilize the cash only for the intended payment transaction.” |

Form 8-K furnished March 7, 2022 Exhibit 99.1, page 1

��

| 3. | When disclosing Adjusted EBITDA, please revise to disclose the corresponding GAAP measure with equal or greater prominence. In this regard we note that you present Adjusted EBITDA in the highlighted bullet points but do not disclose the comparable GAAP measure of net (loss) income attributable to IDT. Similarly, you present Adjusted EBITDA prior to GAAP net (loss) income attributable to IDT in the tabular presentation of Consolidated Results. Also, the starting point for your reconciliations of Adjusted EBITDA should be the most directly comparable GAAP measure, which you disclose is net (loss) income attributable to IDT on a consolidated basis and income (loss) from operations for the reportable segments. Please revise and in your response provide us with the disclosures you intend to include in future filings. Refer to Item 10(e)(1)(i) of Regulation S-K and Question 102.10 of the Non-GAAP C&DIs. | |

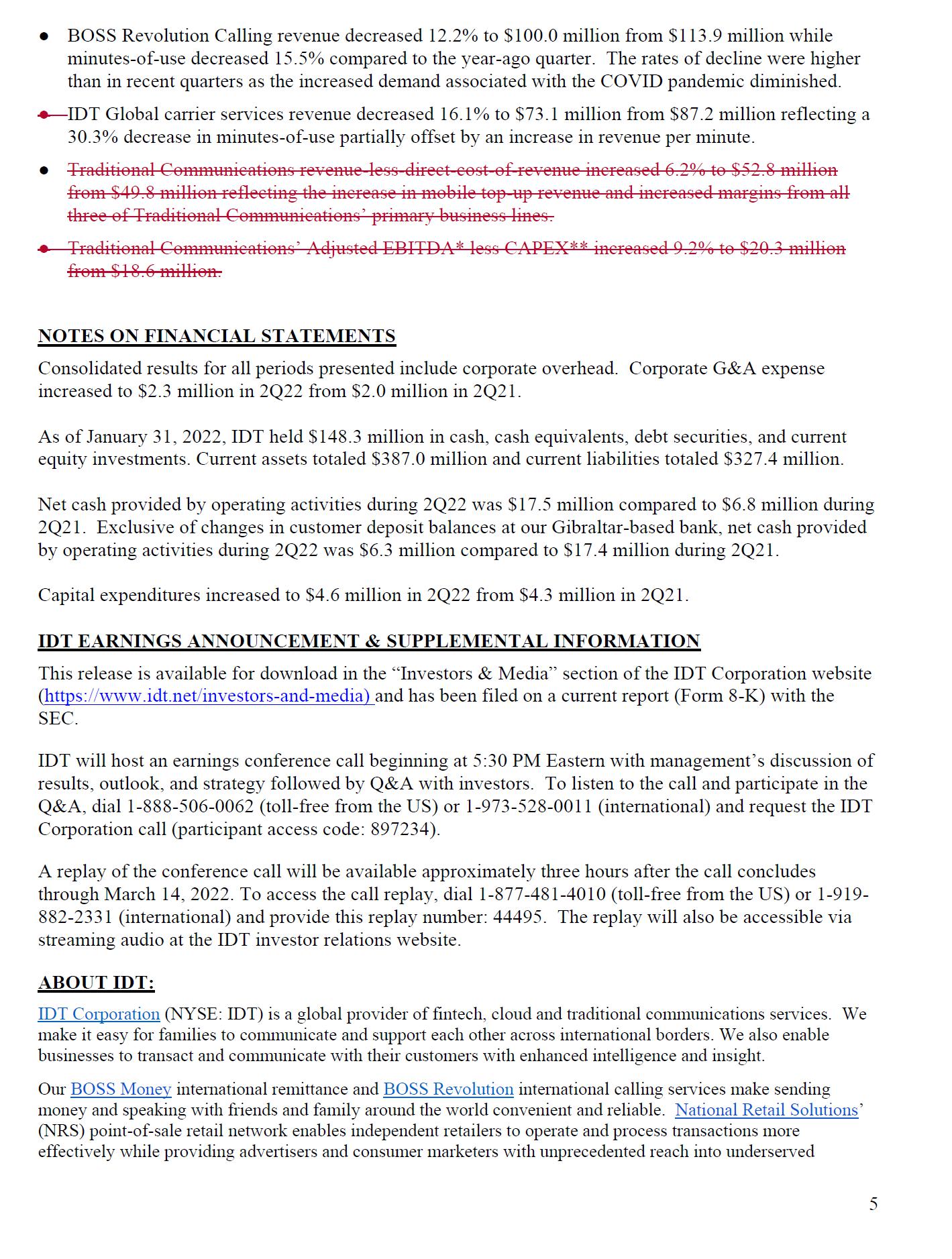

| Response: We will revise our future earnings releases to disclose the most closely corresponding GAAP measure(s) with equal or greater prominence than Adjusted EBITDA (or other Non-GAAP measures), and to start the reconciliations of Adjusted EBITDA with the most directly comparable GAAP measure. A copy of our earnings release dated March 7, 2022 marked to show the approach we intend to take in future earnings releases in response to the comments in your letter is attached to this letter as Exhibit A. |

| 4. | Your measure of Adjusted EBITDA less CAPEX appears to be a non-GAAP liquidity measure based upon your disclosure related to key performance metrics. Please revise to identify this as a non-GAAP measure, present the most directly comparable GAAP measure with equal or greater prominence, and provide a reconciliation to the comparable GAAP measure, which appears to be net cash (used in) provided by operating activities. In addition, refrain from implying that the non-GAAP measure is equivalent to or a substitute for GAAP cash flow information. In this regard, we note your disclosure that Adjusted EBITDA less CAPEX is a reasonable proxy for the cash generated by IDT’s businesses. Refer to Question 102.07 of the non-GAAP C&DIs. Please revise and in your response provide us with the disclosures you intend to include in future filings. | |

| Response: We will not include Adjusted EBITDA less CAPEX in our earnings releases going forward. A copy of our earnings release dated March 7, 2022 marked to show the approach we intend to take in future earnings releases in response to the comments in your letter is attached to this letter as Exhibit A. | ||

| 5. | We note your reference to consolidated revenue-less-direct-cost-of-revenue in the highlighted bullet points appears to present a non-GAAP measure of gross profit. Similarly, your measure of revenue-less-direct-cost-of-revenue as a percentage of revenue, which you identify as a key performance metric both here and in your Form 10-K and Form 10-Q filings, appears to be a non-GAAP measure of gross profit margin. Please revise to identify both of these as non-GAAP measures, provide the comparable GAAP measure of gross profit, including amortization and depreciation and GAAP gross profit, including amortization and depreciation, as a percentage of revenue with equal or greater prominence. Also, revise to explain how you use these measures and why you believe they are useful to investors. Refer to SAB Topic 11.B. In your response provide us with the disclosures you intend to include in future filings. | |

| Response: We do not currently have the information to include the appropriate amount of our depreciation and amortization in direct cost of revenues and selling, general and administrative expense. Therefore, we will no longer include revenue-less-direct-cost-of-revenue and revenue-less-direct-cost-of-revenue as a percentage of revenue in our earnings releases in the future. A copy of our earnings release dated March 7, 2022 marked to show the approach we intend to take in future earnings releases in response to the comments in your letter is attached to this letter as Exhibit A. | ||

| If we decide to disclose gross profit or gross profit margin measures in the future, we would only disclose GAAP measures (or, in the instance of gross profit margin, derived from a GAAP-based gross profit measure), which would conform to SAB Topic 11.B and no reconciliation to GAAP measures would be necessary. |

We acknowledge that we are responsible for the accuracy and adequacy of our disclosures, notwithstanding any review, comments, action, or absence of action by the staff of the Securities and Exchange Commission.

| Sincerely, | |||

| /s/ SHMUEL JONAS | |||

| Shmuel Jonas | |||

| Chief Executive Officer | |||

| cc: | Joyce Sweeney | ||

| Senior Staff Accountant | |||

| Kathleen Collins | |||

| Accounting Branch Chief |

Exhibit A