Exhibit (a)(5)K)

EFiled: Nov 22 2013 12:19PM EST Transaction ID 54601762 Case No. 9113- |  |

IN THE COURT OF CHANCERY OF THE STATE OF DELAWARE

| SALVATORE BONGIOVANNI, On Behalf of Himself | ) | |||

| and All Others Similarly Situated, | ) | |||

| ) | ||||

Plaintiff, | ) | |||

| ) | C.A. No. ______ | |||

v. | ) | |||

| ) | ||||

| SANTARUS, INC., DAVID F. HALE, MICHAEL G. | ) | |||

| CARTER, TED W. LOVE, GERALD T. PROEHL, | ) | |||

| ALESSANDRO E. DELLA CHÀ, KENT SNYDER, | ) | |||

| DANIEL D. BURGESS, MICHAEL E. HERMAN, | ) | |||

| SALIX PHARMACEUTICALS, LTD., SALIX | ) | |||

| PHARMACEUTICALS, INC., and WILLOW | ) | |||

| ACQUISITION SUB CORPORATION, | ) | |||

| ) | ||||

Defendants. | ) | |||

| ) |

VERIFIED CLASS ACTION COMPLAINT

Plaintiff Salvatore Bongiovanni (the “Plaintiff”), on behalf of himself and all others similarly situated, by his attorneys, alleges the following upon information and belief, except as to those allegations pertaining to Plaintiff which are alleged upon personal knowledge:

NATURE AND SUMMARY OF THE ACTION

1. This is a shareholder class action brought by Plaintiff on behalf of holders of the common stock of Santarus, Inc. (“Santarus” or the “Company”) against the board of directors of Santarus (the “Board” or “Individual Defendants”), and other persons and entities (collectively, the “Defendants”), to enjoin the acquisition (the “Proposed Transaction”) of Santarus by Salix Pharmaceuticals, Ltd. (“Salix”) and its wholly-owned subsidiaries Salix Pharmaceuticals, Inc. and Willow Acquisition Sub Corporation (“Merger Sub”).

2. On November 7, 2013, Santarus and Salix issued a joint press release announcing that they had entered into a definitive merger agreement (“Merger Agreement”) for Salix to acquire Santarus, via a tender offer (the “Tender Offer”), in an all cash transaction worth

approximately $2.6 billion. Under the terms of the Proposed Transaction, Santarus shareholders will receive $32.00 for each share of Santarus common stock that is tendered (the “Proposed Transaction”). Following the consummation of the Proposed Transaction, Santarus will become a wholly-owned subsidiary of Salix.

3. Pursuant to Delaware General Corporation Law Section 251(h), after at least 50% of the Company’s common stock is tendered to Salix, Salix, Inc. and Merger Sub and their subsidiaries through the Tender Offer, Salix will then execute a short form merger for the remaining shares of Santarus, which will not require the consent of the Company’s stockholders.

4. Santarus is a California-based specialty biopharmaceutical company that acquires, develops, and commercializes drugs for the treatment of gastroenterology and endocrinology related issues. The Company’s gastroenterology portfolio includes drugs such as Uceris (inflammatory bowel disease) and Zegerid (gastroesophageal reflux disease or GERD), while its endocrinology portfolio includes flagship drug Glumetza (type 2 diabetes), as well as Cycloset (type 2 diabetes) and Fenoglide (high cholesterol). Santarus also has at least three investigational drugs that the Company is trying to advance. Through strategic alliances with the likes of Merck & Co. and GlaxoSmithKline the Company also develops and sells certain over the counter products.

5. In facilitating the Proposed Transaction with Salix, the Board has breached their fiduciary duties by agreeing to the Proposed Transaction for inadequate consideration. Given Santarus’ recent strong performance as well as its future growth prospects, the consideration shareholders will receive is inadequate and undervalues the Company. While shareholders are expected to collect a 36% premium on the closing price in the Tender Offer, the transaction

2

premium is significantly below that of comparable transactions in the industry. In fact, in just the previous year, the Company’s stock price had increased by an astronomical 166%. Moreover, the Proposed Transaction appears purposely timed to forestall a surge in the Company’s share price, as it was announced simultaneously with the Company’s third quarter 2013 results whereby total revenues grew 81% and non-GAAP adjusted earnings were up over 189%.

6. As alleged in further detail below, both the value to Santarus’ shareholders contemplated in the Proposed Transaction and the process by which Defendants propose to consummate the Proposed Transaction are fundamentally unfair to Plaintiff and the other public shareholders of the Company.

7. Compounding the failure to provide adequate consideration, Defendants locked-up the Proposed Transaction by agreeing to certain deal-protection devices that unfairly favor Salix and discourage potential bidders from submitting a superior bid for the Company. Most notably, the Merger Agreement includes an array of deal protection devices that include (i) a non-solicitation or “no-shop” provision that prohibits the Company from seeking superior bids; (ii) a matching rights provision allowing Salix to match any superior bid for Santarus; and (iii) a termination fee of $80 million.

8. As described below, both the value to Santarus shareholders contemplated in the Proposed Transaction and the process by which Defendants propose to consummate the Proposed Transaction are fundamentally unfair to Plaintiff and the other public shareholders of the Company.

9. The Proposed Transaction is designed to preclude other potential bidders to emerge with superior offers while also precluding shareholders from voicing opposition. Defendants are working to close the deal absent judicial intervention, the initial closing of the Tender Offer is expected to consummate first quarter 2014.

3

10. For these reasons and as set forth in detail herein, Plaintiff seeks to enjoin Defendants from taking any steps to consummate the Proposed Transaction or, in the event the Proposed Transaction is consummated, recover damages resulting from the Individual Defendants’ violations of their fiduciary duties of loyalty, good faith and due care as well as violations of the Exchange Act.

THE PARTIES

11. Plaintiff is, and has been at all relevant times, a shareholder of Santarus common stock.

12. Defendant Santarus is a corporation organized and existing under the laws of Delaware, with its principal executive offices located at 3611 Valley Centre Drive, Suite 400, San Diego, CA 92130. Santarus is a specialty biopharmaceutical company focused on acquiring, developing and commercializing products that address the needs of patients treated by physician specialists. As of December 31, 2012, the Company’s marketed and approved products included Uceris (budesonide), Zegerid (omeprazole/sodium bicarbonate), Glumetza (metformin hydrochloride extended release tablets), Cycloset (bromocriptine mesylate) tablets and Fenoglide (fenofibrate) tablets. As of December 31, 2012, the Company’s investigational drugs included Ruconest (recombinant human C1 esterase inhibitor), Rifamycin SV MMX, and SAN-300 (anti- VLA-1 antibody). Santarus’ shares are traded on the NASDAQ under the ticker symbol “SNTS.”

13. Defendant David F. Hale (“Hale”) has served as a director of Santarus since June 2000 and has served as Chairman of the Board since February 2004.

14. Defendant Michael G. Carter (“Carter”) has served as a director of Santarus since February 2005.

4

15. Defendant Ted W. Love (“Love”) has served as a director of Santarus since March 2005.

16. Defendant Gerald T. Proehl (“Proehl”) has served as President of Santarus since March 2000 and as Chief Executive Officer (“CEO”) and a director since January 2002.

17. Defendant Alessandro E. Della Chà (“Della Chà”) has served as a director of Santarus since April 2012.

18. Defendant Kent Snyder (“Snyder”) has served as a director of Santarus since September 2004.

19. Defendant Daniel D. Burgess (“Burgess”) has served as a Santarus director since July 2004.

20. Defendant Michael E. Herman (“Herman”) has served as a Santarus director since September 2003 and is the Chair of the Compensation Committee and a member of the Nominating and Corporate Governance Committee.

21. Defendant Salix is a specialty pharmaceutical company dedicated to acquiring, developing and commercializing prescription drugs and medical devices used in the treatment of a variety of gastrointestinal disorders, which are those affecting the digestive tract. As of December 31, 2012, the Company’s products included XIFAXAN, MOVIPREP, APRISO, RELISTOR, OSMOPREP, SOLESTA, DEFLUX, FULYZAQ, GIAZO, METOZOLV ODT, AZASAN, ANUSOL-HC, PROCTOCORT, PEPCID, DIURIL and COLAZAL. Salix’s principle executive offices are located at 8510 Colonnade Center Drive, Raleigh, NC 27615.

22. Defendant Salix Pharmaceuticals, Inc. (“Salix, Inc.”), is a California corporation and wholly-owned subsidiary of Salix.

5

23. Defendant Merger Sub is a Delaware corporation and wholly-owned subsidiary of Salix formed solely for the purpose of entering into the Merger Agreement and consummating the Proposed Transaction.

THE FIDUCIARY DUTIES OF THE INDIVIDUAL DEFENDANTS

24. By reason of the Individual Defendants’ positions with the Company as officers and/or directors, said individuals are in a fiduciary relationship with Plaintiff and the other public shareholders of Santarus and owe Plaintiff and all other Santarus public shareholders (the “Class”) the duties of good faith, fair dealing and loyalty. By virtue of their positions as directors and/or officers of Santarus, the Individual Defendants, at all relevant times, had the power to control and influence and did control, influence and cause Santarus to engage in the practices complained of herein.

25. Each of the Individual Defendants is required to act in good faith, in the best interests of the Company’s shareholders and with due care, including reasonable inquiry. In a situation where the directors of a publicly traded company undertake a transaction that may result in a change in corporate control, the directors must take all steps reasonably required to maximize the value shareholders will receive rather than use a change of control to benefit themselves. To diligently comply with this duty, the directors of a corporation may not take any action that:

a. Adversely affects the value provided to the corporation’s shareholders;

b. Contractually prohibits them from complying with or carrying out their fiduciary duties;

c. Discourages or inhibits alternative offers to purchase control of the corporation or its assets;

6

d. Will otherwise adversely affect their duty to search for and secure the best value reasonably available under the circumstances for the corporation’s shareholders; or

e. Will provide the directors and/or officers with preferential treatment at the expense of, or separate from, the public shareholders.

26. Plaintiff alleges herein that the Individual Defendants, separately and together, in connection with the Proposed Transaction, violated duties owed to Plaintiff and the other shareholders of Santarus, including their duties of loyalty, good faith and independence, insofar as they,inter alia, engaged in self-dealing and obtained for themselves personal benefits, including personal financial benefits, not shared equally by Plaintiff or the other shareholders of Santarus common stock.

CLASS ACTION ALLEGATIONS

27. Plaintiff brings this action on his own behalf and as a class action pursuant to Rule 23 of the Delaware Court of Chancery and on behalf of all holders of Santarus common stock who are being and will be harmed by Defendants’ actions described below (the “Class”). Excluded from the Class are Defendants herein and any person, firm, trust, corporation or other entity related to or affiliated with any of the Defendants.

28. This action is properly maintainable as a class action for the following reasons:

| a. | The Class is so numerous that joinder of all members is impracticable. While the exact number of members of the Class is unknown to Plaintiff at this time and can be ascertained through appropriate discovery, as of October 31, 2013, approximately 67,128,949 shares of the Company were outstanding. The holders of these shares are believed to be geographically dispersed throughout the United States. |

7

| b. | There are questions of law and fact which are common to the Class and which predominate over questions affecting any individual Class member. The common questions include,inter alia, the following: |

| i. | Whether the Individual Defendants have breached their fiduciary duties of undivided loyalty, independence or due care with respect to Plaintiff and the other members of the Class in connection with the Proposed Transaction; |

| ii. | Whether the Individual Defendants have breached their fiduciary duty by failing to maximize the value Plaintiff and the other members of the Class will receive in connection with the Proposed Transaction; |

| iii. | Whether the Individual Defendants have breached any of their fiduciary duties to Plaintiff and to the other members of the Class in connection with the Proposed Transaction, including the duties of good faith, diligence and fair dealing; |

| iv. | Whether the Individual Defendants, in bad faith and for improper motives, have impeded or erected barriers to discourage other offers for the Company or its assets; and |

| v. | Whether Plaintiff and the other members of the Class would suffer irreparable injury were the transactions complained of herein consummated. |

8

| c. | Plaintiff is an adequate representative of the Class, has retained competent counsel experienced in litigation of this nature and will fairly and adequately protect the interests of the Class; |

| d. | Plaintiff’s claims are typical of the claims of the other members of the Class, and Plaintiff does not have any interests adverse to the Class; |

| e. | The prosecution of separate actions by individual members of the Class would create a risk of inconsistent or varying adjudications with respect to individual members of the Class which would establish incompatible standards of conduct for the party opposing the Class; and |

| f. | Defendants have acted on grounds generally applicable to the Class with respect to the matters complained of herein, thereby making appropriate the relief sought herein with respect to the Class as a whole. |

SUBSTANTIVE ALLEGATIONS

A. Background

29. California-based Santarus is a pharmaceutical company focused on acquiring, developing and commercializing proprietary products for patients treated by gastroenterologists and other physicians. The Company currently markets products for the treatment of upper GI diseases and disorders and type 2 diabetes, and is developing drugs for the treatment of lower GI disorders. The Company’s gastroenterology portfolio includes drugs such as Uceris (inflammatory bowel disease) and Zegerid (gastroesophageal reflux disease or GERD), while its endocrinology portfolio includes flagship drug Glumetza (type 2 diabetes), as well as Cycloset (type 2 diabetes) and Fenoglide (high cholesterol). Santarus also has at least three investigational drugs that the Company is trying to advance. Through strategic alliances with the likes of Merck & Co. and GlaxoSmithKline the Company also develops and sells certain over the counter products.

9

30. Recently, Santarus’ financial performance has been impressive. In the Company’s press release filed with the United States Securities and Exchange Commission (“SEC”) on November 7, 2013, the Company reported exceptional third quarter results. Specifically, the Company reported total revenues of $98.8 million which were 81% higher than the $54.7 million reported for the third quarter of 2012 and net income of $0.38 diluted earnings per share (EPS) for the third quarter of 2013, nearly triple the amount as compared to $0.13 diluted EPS for the third quarter of 2012. Cash, cash equivalents and short-term investments were reported at $168.7 million as of September 30, 2013, an increase of approximately $74.0 million compared with $94.7 million reported at December 31, 2012.

31. Despite these promising future prospects, the Company’s shareholders face the prospect of being excluded from this upside potential due to the intervening tender-offer proposal made by Salix. Rather than allowing the public shareholders to reap the benefits of the exciting opportunities on Santarus’ horizon, the Individual Defendants have acted for their own benefit and the benefit of Salix, and to the detriment of Santarus’ public shareholders by entering into the Proposed Transaction.

B. The Proposed Transaction

32. On November 7, 2013, Santarus and Salix issued a joint press release announcing the Proposed Transaction, which stated, in relevant part, the following:

RALEIGH, NC and SAN DIEGO, CA, November 7, 2013 – Salix Pharmaceuticals, Ltd. (NASDAQ:SLXP) and Santarus, Inc. (NASDAQ:SNTS) today announced that the companies have entered into a definitive merger agreement under which Salix will acquire all of the outstanding common stock of Santarus for $32.00 per share in cash (without interest). The all-cash transaction values Santarus at approximately $2.6 billion. The $32.00 per share price represents an approximately 36% premium over Santarus’ November 6, 2013

10

closing price of $23.53 per share and an approximately 39% premium over Santarus’ average closing stock price for the prior 30-trading day period. The proposed transaction has been unanimously approved by the Boards of Directors of Salix and Santarus. The companies expect to close the transaction in the first quarter of 2014.

Salix President and Chief Executive Officer, Carolyn Logan, stated, “We are extremely pleased with the Santarus acquisition, which is transformative for Salix both commercially and financially, fulfilling many of our strategic needs while providing immediate and significant accretion in 2014 and beyond. We are very pleased to be able to merge our sales forces, combine two complementary product portfolios, expand our pipeline, diversify revenue, access health care providers in primary care, add a significant number of health care prescribers to our called-on universe and to better position Salix for success in the present as well as the future. Additionally we look forward to all of our stakeholders – patients, healthcare providers, employees and stockholders – benefiting from the increased scale created by a larger, even stronger Salix.”

Gerald T. Proehl, President and Chief Executive Officer, Santarus, stated, “Our employees have worked very hard to build Santarus into a premier specialty biopharmaceutical company. I would like to thank all of our employees for their contributions to making Santarus the successful company it is today.” Mr. Proehl added, “We believe the timing is right for this strategic combination with Salix, a highly respected company that is uniquely positioned to expand the commercialization of Santarus’ marketed products and to continue to advance the development of our pipeline products. We welcome the opportunity Salix will provide to build on Santarus’ success.”

* * *

Under the terms of the definitive merger agreement, Salix intends to commence a cash tender offer to acquire all of the outstanding common stock of Santarus for $32.00 per share. Following successful completion of the tender offer, Salix will acquire all remaining shares of Santarus common stock not tendered in the offer through a second step merger at the same price per share paid in the tender offer. The consummation of the tender offer is subject to various conditions, including a minimum tender of at least a majority of the outstanding shares of Santarus common stock on a fully diluted basis, the expiration or termination of the waiting period under the Hart Scott Rodino Antitrust Improvements Act and other customary closing conditions. The tender offer is not subject to a financing condition. Certain directors and officers of Santarus, who, as of November 6, 2013, beneficially owned or had options to acquire a number of shares of Santarus’ common stock equal to approximately 12 percent of Santarus’ total outstanding shares of common stock, have entered into a tender and support agreement pursuant to which such persons have agreed to tender their shares into the tender offer and, if applicable, vote their shares against certain matters, including third party proposals to acquire Santarus. The Board of Directors of Santarus unanimously recommends that Santarus stockholders tender their shares in the tender offer.

11

In connection with the merger agreement, Salix and Santarus entered into an agreement with Santarus’ licensor Cosmo Technologies Limited restructuring certain aspects of Santarus’ relationship with Cosmo. Under the terms of the agreement, Salix will be returning rifamycin SV MMX® to Cosmo Technologies Limited effective with the closing of Salix’s acquisition of Santarus.

Salix intends to finance the transaction with a combination of approximately $800 million cash on hand and $1.95 billion in committed financing from Jefferies Finance LLC. Jefferies Finance LLC also has committed to provide an additional $150 million revolving credit facility. The commitment from Jefferies Finance LLC to provide financing is subject to the satisfaction of customary conditions.

33. The consideration offered to Santarus public stockholders in the Proposed Transaction is unfair and inadequate because, among other things, the intrinsic value of Santarus’ common shares are materially in excess of the consideration being offered in the Proposed Transaction given the Company’s prospects for future growth and earnings. The Board has breached their fiduciary duties to Santarus stockholders by failing to take steps to obtain the best price possible under the circumstances before entering into this transaction pursuant to which Salix is underpaying for Santarus shares, thus unlawfully harming Santarus stockholders.

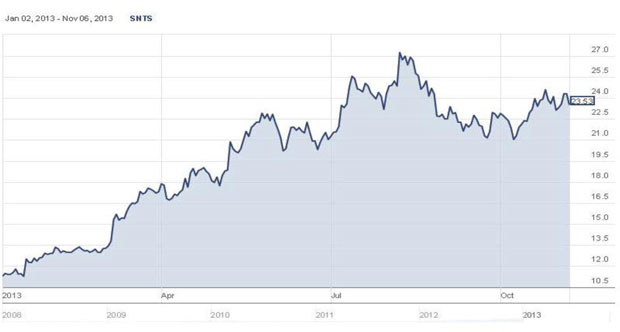

34. Given Santarus’ recent strong performance as well as its future growth prospects, the consideration shareholders will receive is inadequate and undervalues the Company. While shareholders are expected to collect a 36% premium on the closing price, this transaction premium is significantly below that of comparable transactions in the industry. In fact, in just the previous year, the Company’s stock price had increased by an astronomical 166% as demonstrated in the chart below:

12

35. Moreover, the Proposed Transaction appears purposely timed to forestall a surge in the Company’s share price, as it was announced simultaneously with the Company’s third quarter 2013 results whereby total revenues grew 81% and non-GAAP adjusted earnings were up over 189%. The timing of the transaction eliminates the market’s ability to respond to the glowing quarterly results, announced concurrently with the merger after the close of the market on November 7, 2013. As such, it appears that the proposed offer price provides an insufficient premium to shareholders.

C. The Burdensome Deal Protection Devices

36. On November 7, 2013, the Company filed a Form 8-K with the SEC that disclosed the terms of its Merger Agreement. To the detriment of Santarus stockholders, as part of the Merger Agreement, the Individual Defendants agreed to certain deal protection devices that operate conjunctively to lock-up the Proposed Transaction and ensure that no competing offers will emerge for the Company.

13

37. First, the Merger Agreement contains a strict “no-solicitation” provision prohibiting the Company or the Individual Defendants from taking any affirmative action to comply with their fiduciary duties to obtain the best price possible under the circumstances. Pointedly, the Merger Agreement at section 7.8(a) requires that the Company and the Individual Defendants shall not, “directly or indirectly, (i) solicit, initiate, propose or take any action to knowingly encourage (including by way of furnishing information) any inquiries or the submission of any proposal that constitutes, or could reasonably be expected to lead to, an Acquisition Proposal or otherwise knowingly facilitate any effort or attempt to make an Acquisition Proposal.”

38. Similarly, sections 7.8(b) and 7.8(d) of the Merger Agreement provides for “information right” and “matching right” provisions pursuant to which the Company must promptly notify Salix within twenty-four (24) hours should it receive an unsolicited competing Acquisition Proposal. The Company must notify Salix of the bidder’s identity and the terms of the bidder’s offer. Thereafter, if the Board determines that the competing acquisition proposal constitutes a “Superior Proposal,” section 7.8(d) requires the Board to grant Salix four (4) business days to amend the terms of the Merger Agreement to make a counter-offer that the Company must consider in determining whether the competing bid still constitutes a “Superior Proposal.”

39. The effect of these provisions is to prevent the Board from entering discussions or negotiations with other potential purchasers unless the Board can first determine that the competing acquisition proposal is, in fact, “superior,” and even then, the Company must give Salix an opportunity to match the competing takeover proposal. Consequently, this provision prevents the Individual Defendants from exercising their fiduciary duties and precludes an opportunity for a potential purchaser to emerge.

14

40. Additionally, the Merger Agreement provides that Santarus must pay to Salix a termination fee of $80 million pursuant to section 9.3 in the event the Company decides to pursue any competing offer. This unreasonable termination fee will ensure that no competing offer will appear, as any competing bidder would essentially pay a naked premium for the right to provide the stockholders with a superior offer.

41. Ultimately, these deal protection provisions restrain the Company’s ability to solicit or engage in negotiations with any third party regarding a proposal to acquire all or a significant interest in the Company. The circumstances under which the Board may respond to an unsolicited written bona fide proposal for an alternative acquisition that constitutes or would reasonably be expected to constitute a “Superior Proposal” are too narrowly circumscribed to provide an effective “fiduciary out” under the circumstances.

FIRST CAUSE OF ACTION

Claim For Breach Of Fiduciary

Duties Against The Individual Defendants

42. Plaintiff repeats and realleges each allegation set forth herein.

43. The Individual Defendants have violated fiduciary duties of care, loyalty and good faith owed to public shareholders of Santarus.

44. By the acts, transactions and courses of conduct alleged herein, the Individual Defendants, individually and acting as a part of a common plan, are attempting to unfairly deprive Plaintiff and other members of the Class of the true value of their investment in Santarus.

45. As demonstrated by the allegations above, the Individual Defendants failed to exercise the care required, and breached their duties of loyalty, good faith and independence owed to Santarus’ public shareholders because, among other reasons, they failed to take steps to maximize the value of Santarus to its public shareholders.

15

46. The Individual Defendants dominate and control the business and corporate affairs of Santarus. Thus, there exists an imbalance and disparity of knowledge and economic power between them and the public shareholders of Santarus which makes it inherently unfair for them to benefit their own interests to the exclusion of maximizing shareholder value.

47. By reason of the foregoing acts, practices and course of conduct, the Individual Defendants have failed to exercise ordinary care and diligence in the exercise of their fiduciary obligations toward Plaintiff and the other members of the Class.

48. As a result of the actions of Defendants, Plaintiff and the Class will suffer irreparable injury in that they have not and will not receive their fair portion of the value of Santarus’ assets and businesses and have been and will be prevented from obtaining a fair price for their common stock.

49. Unless the Individual Defendants are enjoined by the Court, they will continue to breach their fiduciary duties owed to Plaintiff and the members of the Class, all to the irreparable harm of the members of the Class.

50. Plaintiff and the members of the Class have no adequate remedy at law. Only through the exercise of this Court’s equitable powers can Plaintiff and the Class be fully protected from the immediate and irreparable injury which the Individual Defendants’ actions threaten to inflict.

16

SECOND CAUSE OF ACTION

On Behalf Of Plaintiff And The Class

Against Salix, Salix Inc. and Merger Sub For Aiding And Abetting

The Individual Defendants’ Breaches Of Fiduciary Duty

51. Plaintiff incorporates by reference and realleges each and every allegation contained above, as though fully set forth herein.

52. Salix, Salix, Inc. and Merger Sub have acted and are acting with knowledge of, or with reckless disregard to, the fact that the Individual Defendants are in breach of their fiduciary duties to Santarus’ public shareholders and have participated in such breaches of fiduciary duties.

53. Salix, Salix, Inc. and Merger Sub knowingly aided and abetted the Individual Defendants’ wrongdoing alleged herein. In so doing, Salix, Salix, Inc. and Merger Sub rendered substantial assistance in order to effectuate the Individual Defendants’ plan to consummate the Proposed Transaction in breach of their fiduciary duties.

54. Plaintiff has no adequate remedy at law.

PRAYER FOR RELIEF

WHEREFORE, Plaintiff demands injunctive relief in his favor and in favor of the Class and against Defendants as follows:

A. Declaring that this action is properly maintainable as a Class action and certifying Plaintiff as Class representative and his attorneys as class counsel;

B. Enjoining Defendants, their agents, counsel, employees and all persons acting in concert with them from consummating the Proposed Transaction, unless and until the Company adopts and implements a procedure or process to obtain a merger agreement providing the best possible terms for shareholders;

C. Rescinding, to the extent already implemented, the Proposed Transaction or any of the terms thereof, or granting Plaintiff and the Class rescissory damages;

17

D. Directing the Individual Defendants to account to Plaintiff and the Class for all damages suffered as a result of the Individual Defendants wrongdoing;

E. Awarding Plaintiff the costs and disbursements of this action, including reasonable attorneys’ and experts’ fees; and

F. Granting such other and further equitable relief as this Court may deem just and proper.

| DATED: November 22, 2013 | FARUQI & FARUQI, LLP | |||||

| By: | /s/ Peter B. Andrews | |||||

Peter B. Andrews (#4623) Craig J. Springer (#5529) 20 Montchanin Road, Suite 145 Wilmington, DE 19807 Tel: (302) 482-3182 Email: pandrews@faruqilaw.com Email: cspringer@faruqilaw.com | ||||||

| Counsel for Plaintiff | ||||||

Of Counsel:

FARUQI & FARUQI, LLP

Juan E. Monteverde

369 Lexington Ave., Tenth Floor

New York, NY 10017

Tel: (212) 983-9330

18