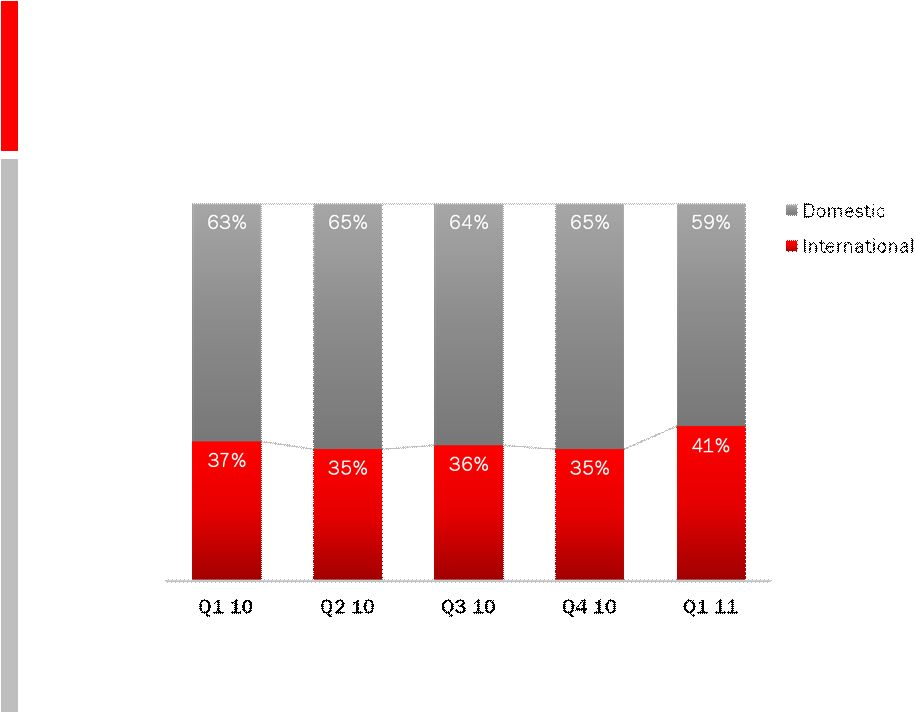

Adjusted EBITDA and Sr. Secured Leverage Ratio As defined in the term credit agreement Consolidated Senior Secured Leverage Ratio Q1 FY 10 Q2 FY 10 Q3 FY 10 Q4 FY 10 Q1 FY 11 $ Thousand Actual Actual Actual Actual Actual Consolidated Net Income $51,095 $22,380 $21,961 $23,416 $27,179 plus (i) Consolidated Interest Charges $22,073 $19,522 $22,061 $22,202 $21,546 (ii) Provision for Federal, state, local and foreign income taxes payable $1,277 $0 $0 $5,988 $0 (iii) Depreciation and amortization expense $51,012 $46,600 $50,493 $51,532 $52,522 (iv) Fees, costs and expenses incurred on or prior to the Acquisition Closing Date in connection with the Acquisition and the financing thereof $0 $0 $0 $0 $0 (v) Any cash restructuring charges and integration costs in connection with the Acquisition, in an aggregate amount not to exceed $75,000,000 $204 $0 $0 $0 $0 (vi) Non-cash restructuring charges incurred in connection with the Transaction, all as approved by Arrangers $1,502 $1,084 $1,006 $930 $848 (vii) Other non-recurring expenses reducing such Consolidated Net Income which do not represent a cash item in such period or any future period (in each case of or by the Borrower and its Subsidiaries for such Measurement Period) $8,783 ($47) $0 $574 $175 (viii) Any non-cash charges for stock compensation expense in compliance with FAS 123R and amortization of the fair value of unvested options under the Acquired Business’ employee stock option plan assumed by the Borrower $21,523 $30,146 $24,682 $25,275 $19,906 (ix) Legal fees and expenses relating to the Borrower’s indemnification obligations for the benefit of its former officers and directors in connection with its historical stock option litigation $250 724 376 $22 $15 minus (i) Federal, state, local and foreign income tax credits $0 ($840) ($15,096) $0 $5,717 (ii) All non-cash items increasing Consolidated Net Income (in each case of or by the Borrower and its Subsidiaries for such Measurement Period) ($3,036) ($3,127) ($4,026) ($2,212) $1,995 Consolidated EBITDA $154,683 $116,442 $101,457 $127,727 $114,479 4 Quarter Trailing Consolidated EBITDA $523,861 $520,429 $502,567 $500,309 $460,105 Consolidated Senior Secured Debt $1,041,483 $1,015,957 $989,803 $959,491 $919,312 Consolidated Senior Secured Leverage Ratio (x) 1.99 1.95 1.97 1.92 2.00 © 2011 Brocade Communications Systems, Inc. Page 37 of 41 |