As filed with the Securities and Exchange Commission on September 22 , 2005

United States Securities And Exchange Commission

Washington, D.C. 20549

FORM 10-Q

(Mark One)

[X] | Quarterly Report Pursuant To Section 13 Or 15(d) Of The Securities Exchange Act Of 1934 For THE QUARTER Ended JUNE 30, 2005 Or |

[ ] | Transition Report Pursuant To Section 13 Or 15(d) Of The Securities Exchange Act Of 1934 For The Transition Period From ________ To _______ |

Commission File No. 0-24027

ENERGY EXPLORATION TECHNOLOGIES INC.

(Exact name of registrant as specified in its charter)

Alberta, Canada

(State or other jurisdiction of

incorporation or organization) | | N/A

(I.R.S. Employer

Identification No.) |

840 7th Avenue S.W., Suite 700, Calgary, Alberta, Canada T2P 3G2

(Address of principal executive offices) (Zip Code)

(403) 264–7020

(Registrant’s telephone number, including area code)

Indicate by check mark whether the registrant (1) has filed all Reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registration was required to file such Reports), and (2) has been subject to such filing requirements for the past 90 days: Yes [X] No [ ]

APPLICABLE ONLY TO ISSUERS INVOLVED IN BANKRUPTCY

PROCEEDINGS DURING THE PRECEDING FIVE YEARS:

Indicate by check mark whether the registrant has filed all documents and reports required to be filed by Sections 12, 13 or 15(d) of the Securities Exchange Act of 1934 subsequent to the distribution of securities under a plan confirmed by a court. Yes [ ] No [ ]

APPLICABLE ONLY TO CORPORATE ISSUERS:

Indicate the number of shares outstanding of each of the issuer’s classes of common stock, as of the latest practicable date:

21,317,271 common shares, no par value, as of August 31, 2005

Energy Exploration Technologies Inc.

INDEX TO THE FORM 10-Q

For the six month period ended June 30, 2005

| | | | PAGE |

| | | | |

PART I | FINANCIAL INFORMATION | |

| | ITEM 1. | FINANCIAL STATEMENTS (Unaudited) | 3 |

| |

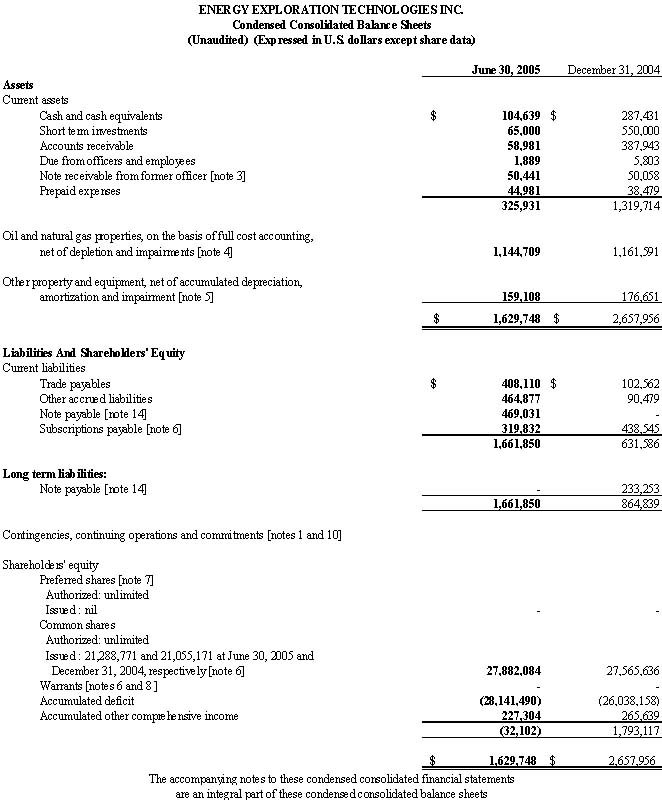

| Condensed Consolidated Balance Sheets | 3 |

| |

| Condensed Consolidated Statements of Loss and Comprehensive Loss | 4 |

| |

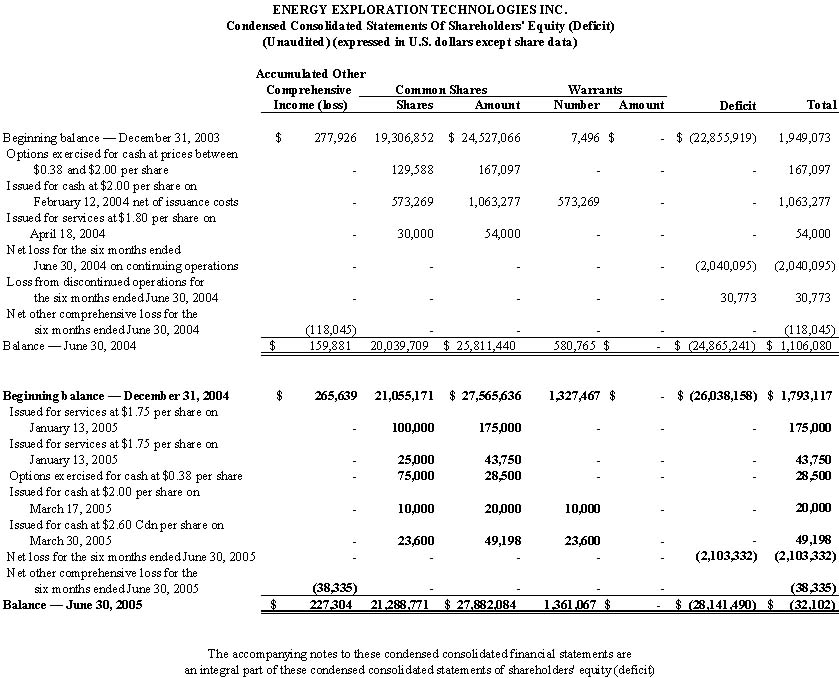

| Condensed Consolidated Statements of Shareholders’ Equity (Deficit) | 5 |

| |

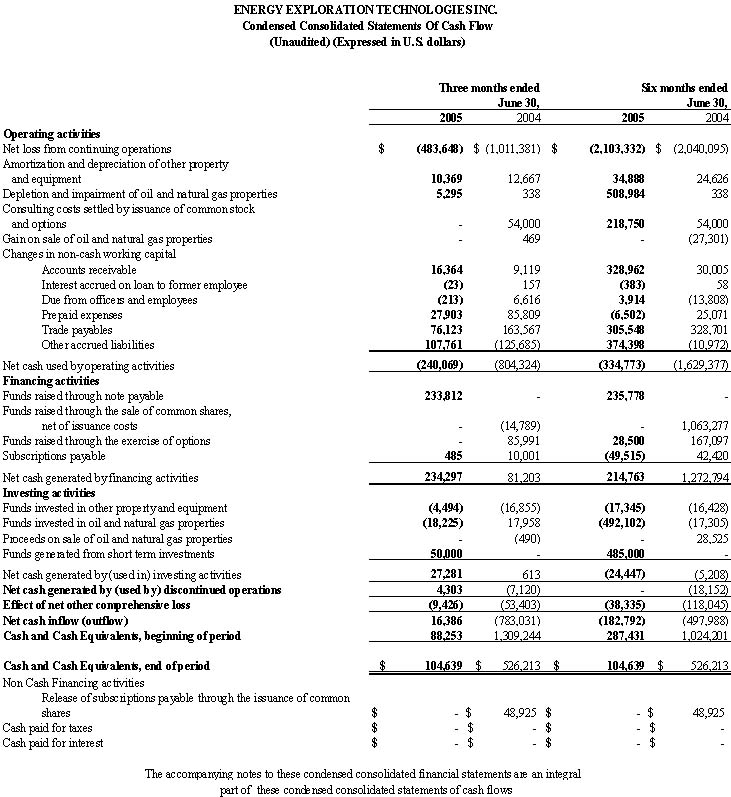

| Condensed Consolidated Statements of Cash Flow | 6 |

| |

| Notes to the Condensed Consolidated Financial Statements | 7 |

| | ITEM 2.

| MANAGEMENT'S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS | 20 |

| | ITEM 3.

| QUANTITATIVE AND QUALITATIVE DISCLOSURES ABOUT MARKET RISK | 32 |

| | ITEM 4. | CONTROLS AND PROCEDURES | 32 |

PART II | OTHER INFORMATION | |

| | ITEM 1. | LEGAL PROCEEDINGS | 33 |

| | ITEM 2. | CHANGES IN SECURITIES AND USE OF PROCEEDS | 33 |

| | ITEM 3. | DEFAULTS UPON SENIOR SECURITIES | 34 |

| | ITEM 4. | OTHER INFORMATION | 34 |

| | ITEM 5. | EXHIBITS | 35 |

| |

| SIGNATURE | 39 |

| | | | |

-2-

PART I

Item 1. Financial Information

-3-

-4-

-5-

-6-

ENERGY EXPLORATION TECHNOLOGIES INC.

Notes TO Condensed Consolidated Financial Statements

(Expressed in U.S. Dollars)

(Unaudited)

1. Organization And Ability To Continue Operations

Energy Exploration Technologies Inc. ("we","our company" or "NXT") was incorporated under the laws of the State of Nevada on September 27, 1994.

In March 2003 we divested all our U.S. properties. For reporting purposes, the results of operations and the cash flow of the U.S. properties have been presented as discontinued operations. Accordingly, prior period financial statements have been reclassified to reflect this change.

NXT was continued from the State of Nevada to the Province of Alberta, Canada on October 24, 2003. The shareholders voted on and approved this change that moved the jurisdiction of incorporation from the U.S. to Canada. The tax effects are disclosed in the proxy statement circulated to shareholders for the Special Meeting on October 24, 2003. As a result of the continuance into Canada, our common and preferred shares no longer have a par value assigned, as is the practice in the United States. Therefore the amount that was disclosed as “Additional paid-in Capital” in prior years on the consolidated balance sheets and consolidated statements of shareholders’ equity (deficit) has been added to the share issued amount. This is a legal jurisdiction reporting difference only.

We are a technology-based reconnaissance exploration company and we utilize our proprietary stress field detection (SFD) remote-sensing airborne survey technology to quickly and inexpensively identify high-grade oil and natural gas prospects.

We conduct our reconnaissance exploration activities, as well as land acquisition, drilling, completion and production activities through our wholly-owned subsidiary, NXT Energy Canada Inc. and we conduct the aerial surveys through our wholly owned subsidiary, NXT Aero Canada Inc.

NXT Energy USA Inc. and NXT Aero USA Inc. are two wholly owned subsidiaries through which we previously conducted our U.S. operations but these companies have been inactive since the sale of the U.S. properties in early 2003.

These consolidated financial statements are prepared using generally accepted accounting principles in the United States of America that are applicable to a going concern, which assumes the realization of assets and the settlement of liabilities in the normal course of operations. Our ability to continue as a going concern is dependent upon our ability to generate profitable operations in the future and obtain the necessary financing to meet our obligations and repay liabilities arising from normal business operations when they come due. The outcome of these matters cannot be predicted with any certainty at this time. These consolidated financial statements do not include any adjustments to amounts and classifications of assets and liabilities that may be necessary should we be unable to continue as going concern.

In the six months ended June 30, 2005, we incurred a comprehensive loss of $2,141,667, have an accumulated deficit of $28,141,490 and a working capital deficiency of $1,335,919 as at the end of the period.

We expect to continue incurring net losses from operations and have negative operating cash flows until we can secure revenue generating activities. NXT has identified a potential future market opportunity to sell the SFD survey as a service to third parties. NXT has not secured any contracts for this activity. These circumstances raise substantial doubt about our ability to continue as a going concern.

We have taken the following measures to ensure the ongoing viability of the company:

-7-

·

On November 3, 2004, we entered into a loan agreement with our CEO and largest shareholder, Mr. George Liszicasz, in which we borrowed $250,000 CDN. On November 16, 2004, we amended the loan agreement whereby we borrowed an additional $31,000 US. On November 17, 2004, we entered into an additional loan agreement with Mr. Liszicasz and borrowed a further $100,000 CDN. All these agreements provide that the loans accrue interest at the rate of 0.58% per month (7.0% per annum). On November 19, 2004, we entered into a Loan Agreement Amendment with Mr. Liszicasz, whereby the maturity date for all three (3) loans was extended to November 17, 2005. On February 7, 2005, we entered into another Loan Agreement Amendment, whereby the maturity date for all three (3) loans was extended further to April 15, 2006. On April 7, 2005 the principal amount of the loan agreement signed on Nov ember 17 was amended to $88,000 US. The loan was utilized on April 15, 2005.

·

On May 20, 2005 we signed a loan agreement with a family trust of one of our directors. The conditions of the loan agreement are as follows: principal amount $175,000 CDN ($140,500 US), 6.5% interest per annum and maturity date on or before June 19, 2005. The loan is secured with certain assets of the Company. $67,000 of the loan was converted into convertible promissory notes under the bridge-financing contract mentioned below on September 19, 2005. The remainder of loan is now in default and will be repaid from the proceeds of the bridge financing.

·

We have undertaken a variety of cost reduction activities including but not limited to termination of contract employees, a 50% reduction of salaries and reduction of corporate travel.

·

The company is currently negotiating a private placement of shares of common stock through an Offering Memorandum. The shares will not be registered under the Securities Act of 1933 and may not be offered or resold in the United States absent registration or pursuant to an exemption to the registration requirements. The objective of the private placement is to raise $10,000,000 on a best efforts basis to commercialize the SFD technology through obtaining a contract to provide the SFD survey as a service to third parties. The proceeds will be used to finance our marketing efforts and the necessary additional resources needed for the execution of the contract. We expect to close the private placement by December 31, 2005. There are no guarantees that the Company will be able to close the private placement. In this event, it is unlikely we will be able to meet our obligatio ns and we may be forced to cease operations and liquidate our assets.

·

We are currently finalizing a bridge-financing contract for $1,300,000 in the form of promissory notes and additional $200,000 to $700,000 is expected to close by the end of November 2005. The notes will not be registered under the Securities Act of 1933 and may not be offered or resold in the United States absent registration or pursuant to an exemption to the registration requirements. The proceeds from this financing will fund the operations of the Company until we receive the proceeds from the private placement. The conditions of the financing are as follows: the lender will receive interest bearing (10% per annum) notes, maturing 18 months from the date of issue, convertible into common shares. The number of shares to be issued on conversion shall be determined by dividing the amount of the note by the lesser of $0.70 or 85% of the lowest price of any common shares issued directly by the Company during the term of the note in connection with a public or private offering (but specifically excluding warrants or options issued to officers, directors, employees, agents, independent contractors or consultants retained by the Company). The notes are secured by the Company’s interest in gas wells and land. The lender will receive one two-year warrant for every $1.00 invested. We expect the contract to be finalized and the proceeds to be available by September 27, 2005.We can give no assurance that any or all projects in our pending programs will be commercial, or if commercial, will generate sufficient revenues to cover our operating or other costs. Should this be the case, we would be forced, unless we can raise sufficient additional working capital, to suspend our operations, and possibly even liquidate our assets and wind-up and dissolve our company. We need to raise approximately $1,000,000 to cover our normal operational expenses and finance our marketing efforts an d execution of potential contracts for the next 12 months. With funds that will be available to the company after the bridge-financing contract closes we can sustain reduced operations reflecting our cost-cutting measures for the next 12 months.

-8-

On August 2, 2005 we disposed of one of our land leases. The gain realized on the disposal was approximately $35,000.

These consolidated financial statements are prepared using generally accepted accounting principles that are applicable to a going concern, which assumes the realization of assets and the settlement of liabilities in the normal course of operations. Should this assumption not be appropriate, adjustments in the carrying amounts of the assets and liabilities to their realizable amounts and the classification thereof will be required and these adjustments and reclassifications may be material.

2. Significant Accounting Policies

Basis of Presentation

We have prepared these consolidated financial statements for our interim period as at June 30, 2005 and ended June 30, 2005 and 2004 in accordance with accounting principles generally accepted in the United States of America for interim financial reporting. While these financial statements for these interim periods reflect all normal recurring adjustments, which, in the opinion of our management, are necessary for fair presentation of the results of the interim period, they do not include all of the information and notes required by accounting principles generally accepted in the United States of America for complete financial statements. The results of operations for the six months ended June 30, 2005 are not necessarily indicative of the results to be expected for the full year. Refer to our consolidated financial statements included in our annual report on Form 10-K for our fiscal year ended December&nb sp;31, 2004.

Estimates and Assumptions

The preparation of these consolidated financial statements in accordance with accounting principles generally accepted in the United States of America requires our management to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities at the date of these consolidated financial statements and the reported amount of revenues and expenses during the reporting periods. Estimates include allowances for doubtful accounts, valuation of the note receivable, estimated useful life of assets, provisions for contingent assets and liabilities, measurement of stock based compensation and valuation of future tax assets and reflect management's best estimate. Estimates and assumptions are reviewed periodically and the effects of revisions are reflected in the period that they are determined necessary. Actual results may differ from those estimates.

Stock-Based Compensation for Employees and Directors

In accounting for the grant of our employee and director stock options, we have elected to follow Accounting Principles Board Opinion No. 25,"Accounting for Stock Issued to Employees" ("APB 25"), and related interpretations. Under APB 25, companies are not required to record any compensation expense relating to the grant of options to employees or directors where the awards are granted upon fixed terms with an exercise price equal to fair value at the date of grant and the only condition of exercise is continued employment.

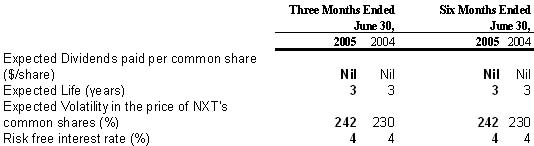

Had we elected to follow the alternative fair value accounting provided for under SFAS No. 123,“Accounting for Stock Based Compensation”,we would have recorded additional compensation expense of approximately $336,083 for the three months ended June 30, 2005 and $463,495 for the six months ended June 30, 2005 as compared to the previous year of $42,944 for the three months ended June 30, 2004 and $121,878 for the six months ended June 30, 2004. These amounts are determined using an option-pricing model with the following assumptions:

-9-

The following table illustrates the effect of net loss and loss per share if the company had applied the fair value recognition provisions of FASB Statement No. 123, “Accounting for Stock-Based Compensation”, to stock-based employee compensation.

Recent Accounting Pronouncements

In September 2004, the SEC released SAB 106, which expresses the staff’s views on the application of SFAS 143 by oil and gas producing companies following the full cost accounting method. SAB 106 provides interpretive responses related to computing the full cost ceiling to avoid double-counting the expected future cash outflows associated with asset retirement obligations, required disclosures relating to the interaction of SFAS 143 and the full cost rules, and the impact of SFAS 143 on the calculation of depreciation, depletion, and amortization. This has no impact on our company at this time.

In December 2004, the FASB issued SFAS No. 123 (revised 2004), Share-Based Payment that revised FASB Statement No. 123, Accounting for Stock-based Compensation and superseded APB Opinion No. 25, Accounting for Stock Issued to Employees, and its related implementation guidance. SFAS No. 123R focuses primarily on accounting for transactions in which an entity obtains employee services through share-based employee transactions. SFAS No. 123R requires a public entity to measure the cost of employee services received in exchange for the award of equity instruments based on the fair value of the award at the date of grant. The cost will be recognized over the period during which an employee is required to provide services in exchange for the award. SFAS No. 123R is effective as of the beginning of the first or annual reporting period that begins after June 15, 2005. The ultimate amount of increased compensat ion expense will be dependent on whether the company adopts SFAS 123R using the modified prospective or retrospective method, the number of option shares granted during the year, their timing and vesting period, and the method used to calculate the fair value of the awards, among other factors.

The company has begun, but has not completed, evaluating the impact of adopting SFAS 123R on its results of operations. The company currently determines the fair value of stock-based compensation using a Black-Scholes option-pricing model. In connection with evaluating the impact of adopting SFAS 123R, the company is also considering the potential implementation of different valuation models to determine the fair market value of stock-base compensation, although no decision has been yet made. However, the company does believe that the adoption of SFAS 123R will have a material impact on its results of operations, regardless of the valuation technique used.

To assist in the implementation of SFAS No. 123(R) the SEC issued SAB No 107, “Share-Based Payment”. While SAB No. 107 addresses a wide range of issues, the largest area of focus is valuation methodologies and the selection of assumptions. Notably, SAB No 107 lays out simplified methods for developing certain assumptions. In addition to providing the SEC staff’s interpretive guidance on SFAS No. 123(R), SAB No. 107 addresses the interaction of SFAS No. 123(R) with existing SEC guidance (e.g. the interaction with the SEC’s guidance dealing with non-GAAP

-10-

disclosures). Its intent is to clarify, not change, any of SFAS No. 123(R)’s guidance. The company is reviewing the standard and guidance to determine the potential impact, if any, on our consolidated financial statements.

In June 2005, the FASB issued FSP FIN 46(R)-5, “Implicit Variable Interests Under FASB Interpretation No.46(R), Consolidations of Variable Interest Entities” to address whether a company has an implicit variable interest in a VIE or potential VIE when specific conditions exist. The guidance describes an implicit variable interest as an implied financial interest in an entity that changes with changes in the fair market value of the entity’s net assets exclusive of variable interests. An implicit variable interest acts the same as an explicit variable interest except it involves the absorbing and/or receiving of variability indirectly from the entity (rather than directly). Restatement to the date of initial application is permitted but not required. The company is reviewing the guidance to determine the potential impact, if any, on its consolidated financial statements.

The following standards issued by the FASB do not impact us at this time:

·

In December 2004, the FASB issued SFAS No. 153, Exchanges of Non-monetary Assets, an amendment of APB Opinion No. 29 that amends Opinion 29 to eliminate the exception from fair market measurement for nonmonetary exchanges of similar productive assets and replaces it with an exception for exchanges that do not have commercial substance. The provisions of this statement are effective for all nonmonetary exchanges occurring in fiscal years beginning after June 15, 2005. The adoption of this Statement is not expected to have material effect on the results of operations or financial position of the company.

3. Note Receivable From Officer

In September 1998, we loaned the sum of CDN $54,756 (US $35,760 as of that date) to one of our officers in connection with his relocation to Calgary, Alberta. The interest rate averaged 5 ½%. Pursuant to the terms of an underlying promissory note, the officer was required to repay the loan on a monthly basis, with a balloon payment due on October 3, 2003. The officer left our company in 2002. The officer had an offsetting claim against NXT for wrongful dismissal. He has not pursued the claim and the statute of limitations applicable to his claim expired in October 2004. We are pursuing our claim now and believe that we will be successful since there no longer is any offsetting claim. The promissory note also specifies that potential legal fees in collecting this debt be borne by the former officer.

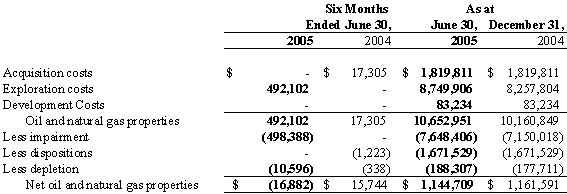

4. Oil And Natural Gas Properties

Summarized below are the oil and natural gas property costs we capitalized for the six months ended June 30, 2005 and 2004 and as at June 30, 2005 and December 31, 2004:

-11-

Net oil and natural gas property costs at June 30, 2005 and December 31, 2004 are in the majority related to Canadian unproved properties

The impairment amounts in the table above of oil and natural gas properties also include the write-down of the cost of drilling and completing wells which are either non-commercial or which we are unable to complete for technical reasons. We have written-off these individual well costs as an impairment cost since this determination was made prior to the establishment of proved reserves.

At the end of each quarter, our management performs an overall assessment of each of our unproved oil and natural gas properties to determine if any of these properties has been subject to any impairment in value. Based upon these evaluations, our management has determined that each of our oil and natural gas properties continued to have prospective commercial viability as of these dates except as described above. While we are currently conducting active exploration and development programs with respect to each of these unproved oil and natural gas properties, we anticipate that all of these properties will be evaluated and the associated costs transferred into the amortization base or be impaired over the next five years.

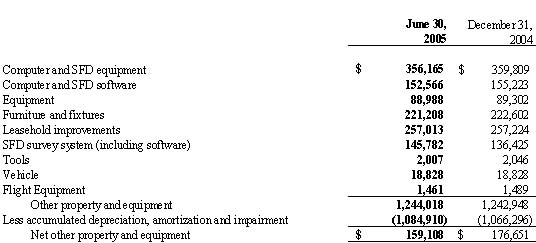

5. Other Property And Equipment

Summarized below are our capitalized costs for other property and equipment as of June 30, 2005 and December 31, 2004:

6. Common Shares

The loss per share is presented in accordance with the provisions of SFAS No. 128, Earnings Per Share (“EPS”). Basic EPS is calculated by dividing the income or loss available to common stockholders by the weighted average number of common shares outstanding for the period. Diluted EPS reflects the potential dilution that could occur if securities or other contracts to issue common stock were exercised or converted into common stock. Basic and diluted EPS were the same for the three and six months ended June 30, 2005 and 2004 because the company had losses from operations and therefore, the effect of all potential common stocks was anti-dilutive.

In calculating diluted earnings per common share for the three and six month periods ended June 30, 2005 and 2004, we excluded all options and warrants, either because the exercise price was greater than the average market price of our common shares in those quarters or the exercise of the options or warrants would have been anti-dilutive. During these periods, all outstanding stock options and warrants were the only potentially dilutive instruments.

On February 12, 2004, we raised $1,143,633 in gross proceeds through a private placement of 573,269 units. Each unit consisted of a common share at $2.00 ($2.60 CDN) per share and a warrant with a strike price of $2.75 and a one year life. Net proceeds to our company were $1,063,277 after deducting $80,356 in offering expenses and

-12-

finders’ fees. In addition, we had also received $319,832 in gross proceeds at June 30, 2005 for which shares had not been issued at June 30, 2005 and this amount is shown as subscriptions payable on the balance sheet. Also in the first quarter of 2005 we cancelled a subscription agreement and refunded $50,000 to one of our investors in the $2.00 private placement based on the shareholder’s request.

On April 18, 2004 we issued 30,000 common shares in full payment of an invoice for $54,000 for services provided by a consultant to NXT to assist us with corporate strategy and planning.

On July 22, 2004, we issued 200,000 common shares in full payment of an invoice for $400,000 for services to establish a branch office in the United Arab Emirates and market the company’s SFD Technology in the region.

On July 22, 2004, we raised $264,245 in gross proceeds through a private placement of 133,000 units. Each unit consisted of a common share at $2.00 ($2.60 CDN) per share and a warrant with a strike price of $2.75 and a one year life. Net proceeds to our company were $255,618 after deducting $8,627 in offering expenses and finder’s fees.

On December 8, 2004 NXT raised $1,000,000 from the sale of 571, 429 Units consisting of one common share and one full common share purchase warrant with an exercise price of $2.75 per common share. The transaction was completed with Dynamic Focus Resource fund of Toronto, Ontario, Canada.

On January 13, 2005 we issued 100,000 common shares valued at $1.75 per share to Pangaea Investments Inc. in exchange for general business consulting services provided.

On January 13, 2005 we issued 25,000 restricted common shares valued at $1.75 per share to CoMarConGbR Germany for investor awareness and promotion services. Another 25,000 restricted common shares are held in escrow pending CoMarCon’s fulfillment of a condition of the agreement.

During the first quarter of 2005 we issued 75,000 common shares as a result of options exercised at $0.38 per share.

On March 31, 2005 we filed the Form F-1 registration statement with the SEC requesting the registration of 3,558,998 common shares of NXT issued in private placements. The shares have not been registered at the date of this report. The company anticipates the registration within 2 months of the date of this report.

On March 17, 2005, we raised $20,000 through a private placement of 10,000 units. Each unit consisted of a common share at $2.00 ($2.60 CDN) per share and a warrant with a strike price of $2.75 and a one year life

On March 30, 2005, we raised $49,198 through a private placement of 23,600 units. Each unit consisted of a common share at $2.00 ($2.60 CDN) per share and a warrant with a strike price of $2.75 and a one year life.

7. Preferred Shares

The preferred shares are not entitled to payment of any dividends, although they are entitled under certain circumstances to participate in dividends on the same basis as if converted into common shares. Preferred shares carry liquidation preferences should our company wind-up and dissolve.

The preferred shares were all returned to treasury effective May 9, 2003 as part of the compensation received for the sale of the U.S. properties.

8. Performance Warrants

On August 1, 1996, we granted Momentum Resources Corporation a performance-based contractual right to acquire NXT warrants in connection with our use of the SFD Technology for hydrocarbon exploration. The initial term of the contract with Momentum Resources expires on December 31, 2005 and can be cancelled by NXT providing written notice to Momentum Resources no later than 60 days prior to the expiration of the pending term. Pursuant to this contractual right, Momentum Resources is entitled to a separate grant of warrants entitling it to purchase 16,000 common shares at the then current trading price for each month after December 31, 2000 in which production from SFD-identified prospects during that month exceeds 20,000 barrels of hydrocarbons. Momentum Resources has not

-13-

earned any warrants under the SFD technology license as of June 30, 2005. We terminated the contract on September 9, 2005.

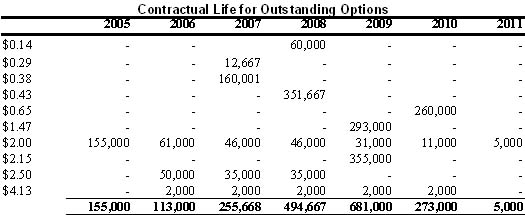

9. E mployee And Director Options

We have summarized below all outstanding options under our various stock option plans and arrangements as at June 30, 2005:

-14-

The employee and executive options outstanding as of June 30, 2005 will vest over the next three years, based upon the continued provision of services as an employee or consultant, except for the 260,000 of employee options granted on June 28, 2005, which vested immediately upon the date of the grant. The options generally vest one-third each on the first through third anniversaries of the grant date, respectively, based upon the continued provision of services. The options generally lapse, if unexercised, five years from the date of vesting.

10. Commitments and contingencies

On October 18, 2004 we signed a contract with Mr. Charles Selby under which Mr. Selby provides business support and advisory service as and when required by NXT. In consideration of services provided NXT is required to issue the total of 400,000 common shares depending on reaching certain performance milestones determined by the NXT’s board of directors and pay a retainer of $10,000 per month. The contract is renewable every 4 months based on the approval by the President and the Board. No shares have been issued as of the date of this report and the evaluation and continuation of the contract is subject to the approval by the board of directors.

We signed the extension of the sublease of the premises for our main office on November 25, 2004. The monthly minimum lease payments are $13,092 CDN and the sublease expires on January 31, 2006. The Company is commencing search for new office space to replace the existing lease when the existing contract expires.

On November 27, 2002, we were served a Statement of Claim, which had been filed on November 25, 2002, in the Court of Queen’s Bench of Alberta, Judicial District of Calgary (Action No. 0201-19820), naming Energy Exploration Technologies Inc. and George Liszicasz as defendants. Mr. Dirk Stinson, the plaintiff, alleges that NXT failed to pay him compensation of $74,750, plus interest, under a consulting agreement and further alleges that NXT, without lawful justification, obstructed Mr. Stinson from trading his shares of NXT. On December 10, 2002, we filed our Statement of Defense. Mr. Stinson is a past President and director of NXT and is currently a director and shareholder of Momentum Resources. We believe the claim against us is contentious because of the ambiguity of the arrangements and we ar e vigorously defending ourselves against the claim. No amount has been accrued for this claim in the financial statements.

On March 18, 2003, we were served a Statement of Claim which had been filed on March 14, 2003, in the Court of Queen’s Bench of Alberta, Judicial District of Calgary (Action No. 0301-04309), naming Glen Coffey, Murray’s Aviation Repairs (1980) Ltd., Energy Exploration Technologies, its wholly-owned subsidiary, NXT Energy Canada, Inc., Dennis Wolsky, as Administrator of the Estate of Jerry Wolsky, deceased and Embassy Aero Group Ltd. as defendants. Tops Aviation Ltd., Spartan Aviation Inc. and John Haskakis (the “Plaintiffs”) allege that the defendants were negligent and in breach of a Ferry Flight Contract between one or some of the defendants and one or some of

-15-

the Plaintiffs under which Mr. Jerry Wolsky was to deliver a Piper Twin Comanche aircraft to Athens, Greece. The aircraft crashed in Newfoundland enroute to Athens killing Mr. Wolsky. The Plaintiffs are seeking, among other things, damages in the amount of $450,000 CDN or loss and damages to the aircraft and cargo; and damages in respect to search and rescue expenses, salvage, storage, transportation expenses and pollution and contamination expenses.

Neither we nor our subsidiary, NXT Energy Canada, Inc., were parties to the Ferry Flight Contract. We believe the claim against us and our subsidiary is without merit and intend to vigorously defend ourselves against the claim and will seek an expeditious dismissal of the claim. No amount has been accrued for this claim in the financial statements.

On January 3, 2005, Energy Exploration Technologies, Inc signed a contract for investor awareness and promotion services in Europe. Under this contract, NXT has the obligation to pay CoMarCon, a German company, $25,000 in cash and to issue 50,000 shares. As of the date of this report the $25,000 cash has been paid, 25,000 shares have been issued and 25,000 shares are held in escrow. These shares will be released if and when CoMarCon meets a specific condition of the contract.

In March 2005 a contract was signed with Pangaea Investments under which Pangaea will provide investor relations and public relations services for a monthly fee of $5,000 CDN ($4,160 US) plus reimbursement of certain expenses, 100,000 common shares and a grant of an option to buy 100,000 additional common shares. The 100,000 common shares have been issued as of the date of this report. The contract may be terminated by either party upon 30 days notice.

In January 2005, a 12 month agreement was signed with Aware Capital under which Aware will provide investor relations and promotional services for a finders’ fee that will equal 3% of any financing arranged for by Aware and accepted and closed by NXT subject to certain limitations. As of the date of this report no fees have been paid or earned. The agreement also provides for 150,000 restricted shares of common stock to be delivered to NXT’s legal counsel and held in escrow pending Aware’s performance and completion of duties and obligations under the agreement. To the date of this report no shares have been earned or issued under this agreement.

On June 22, 2005 a contract was signed with Steedman Consultants, Inc. for provision of services with respect to miscellaneous corporate matters. The services will be provided as needed and the remuneration for the services is payable in cash or in common shares of the corporation at the option of the consultant. As of the date of this report no cash has been paid and the accrued expense as of the same date is approximately $19,000.

On June 28, 2005 an agreement was signed with Baycrest Energy Ltd. for provision of services with respect to miscellaneous corporate matters. 70,000 Energy Exploration Technologies Inc. stock options were awarded upon signing the agreement. Any other remuneration will be reviewed after the Corporation secures sufficient financing.

11. Investor Relations Options and Stock Awards

On May 15, 2001, as additional compensation to our investor relations consultant pursuant to an investor and public relations services agreement, we granted the consultant options to purchase 155,000 common shares at $2.50 per share. The underlying agreement provided that 50,000 options would vest immediately, and an additional 35,000 options would vest upon each of the first, second and third anniversary dates of the agreement, respectively, even if the agreement was not subsequently renewed so long as the agreement has not been terminated by either party prior to the end of the termination of the prior term or NXT has not terminated this agreement for "good cause" as defined in the agreement. These options lapse, to the extent vested and unexercised, five years after the date of vesting.

On January 3, 2005, Energy Exploration Technologies, Inc signed a contract for investor awareness and promotion services in Europe. Under this contract, NXT has the obligation to pay CoMarCon, a German company, $25,000 in cash and to issue 50,000 shares. As of the date of this report the $25,000 cash has been paid, 25,000 shares have been issued and 25,000 shares are held in escrow. These shares will be released if and when CoMarCon meets a specific condition of the contract.

-16-

In March 2005, NXT signed a contract with Pangaea Investments under which Pangaea will provide investor relations and public relations services for a monthly fee of $5,000 CDN ($4,160 US) plus reimbursement of certain expenses. The contract may be terminated by either party upon 30 days’ notice.

In January 2005, a 12 month agreement was signed with Aware Capital under which Aware will provide investor relations and promotional services for a finders’ fee that will equal 3% of any financing arranged for by Aware and accepted and closed by NXT subject to certain limitations. As of the date of this annual report no fees have been paid or earned. The agreement also provides for 150,000 restricted shares of common stock to be delivered to NXT’s legal counsel and held in escrow pending Aware’s performance and completion of duties and obligations under the agreement. To the date of this annual report no shares have been earned or issued under this agreement.

12. discontinued operations

In January 2003, we adopted a formal plan to divest our U.S. oil and gas properties. On May 9, 2003 we closed a sale transaction with our U.S. joint venture partner to sell the properties for total consideration of $1,450,000 with proceeds of $720,000 in cash and the return to treasury of all the outstanding preferred shares. The effective date of the transaction was March 1, 2003 and was recorded at market value. For reporting purposes, the results of operations and the financial position of the properties have been presented as discontinued operations.

In the quarter ended June 30, 2005, $4,303 gain from discontinued operations as a result of reclassification of administrative expenses booked in the first quarter of 2005. A gain on sale of aircraft equipment that had been previously written off in the amount of $ 41, 805 was recognized in the quarter ended June 30, 2004.

13. Segment Information

We operate in only one business segment, oil and natural gas exploration. We intend to develop all oil and natural gas exploration prospects identified using our proprietary SFD airborne survey technology either directly or with joint venture partners. NXT has investigated the market opportunities to sell the SFD survey as a service to third parties. We believe that opportunities will arise in the future that would permit NXT to establish this other business segment. NXT does not currently have any contracts to provide the SFD survey as a service to third parties.

Summarized below with respect to our three month and six month periods ended June 30, 2005 and 2004 is geographic information relating to:

Ÿ | revenues we have received during the period from our external customers, allocated amongst the geographic areas in which the revenue was generated; |

Ÿ | our net loss from continuing operations for the period, allocated amongst the geographic areas in which the revenue and associated expenses were generated; and |

Ÿ | our net gain (loss) loss from discontinued operations for the period, allocated amongst the geographic areas in which the revenue and associated expenses were generated. |

-17-

In preparing the above tables, we have eliminated all inter-segment revenues, expenses and assets

14. Notes Payable

As of June 30, 2005 the Company has loans outstanding in the amount of $469,031. This amount is comprised of the following:

·

$250,000 CDN borrowed from our CEO and largest shareholder, Mr. George Liszicasz on November 3, 2004 and an additional $31,000 US as a result of an amendment to the loan agreement dated November 16, 2004. On November 17, 2004, we entered into an additional loan agreement with Mr. Liszicasz for a further $100,000 CDN. The principal amount of the loan agreement signed on November 17 was later (on April 7, 2005) amended to $88,000 US. We did not utilize this loan until April 15, 2005 when the $88,000US was drawn upon. These agreements provide that the loans accrue interest at the rate of 0.58% per month (7.0% per annum). The maturity date for all three loans was amended and is now April 15, 2006.

·

$175,000 CDN and accrued interest payable to a family trust of one of our directors under a loan agreement signed on May 20, 2005. The conditions of the loan agreement are as follows: principal amount $175,000 CDN ($140,500 US), 6.5% interest per annum and original maturity date on or before June 19, 2005. The loan

-18-

is secured with certain assets of the Company. $67,000 of the loan was converted into convertible promissory notes under the bridge-financing contract on September 19, 2005. The remainder of loan is now in default and will be repaid from the proceeds of the bridge financing.

-19-

ITEM 2. MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS

Overview

Energy Exploration Technologies Inc. (referred to herein as the “Company”, NXT, “we”, “us” and “our”) is a technology company focused on using its proprietary Stress Field Detector (SFD) technology for oil and gas exploration. NXT utilizes the SFD technology invented by George Liszicasz, our CEO, President and largest shareholder. The SFD technology is a remote-sensing airborne survey technology comprised of SFD sensors, integrated electronic data acquisition, processing and interpretation subsystems and software. Our principal executive offices are located at 700, 840 - 7 Avenue SW, Calgary, Alberta, Canada and our telephone number is (403) 264-7020.

We use the airborne SFD technology to survey large exploration areas from leased aircraft at speeds of approximately 200 mph to identify and prioritize oil and gas prospects for further evaluation using conventional exploration technologies of seismic and drilling. Our SFD technology affords us the relatively inexpensive ability to acquire, analyze and interpret data on potential hydrocarbon prospects in a matter of days or weeks, as compared to months or years for other wide-area exploration activities. These advantages can dramatically reduce finding costs and the time required to identify oil and gas prospects. Once SFD prospects are identified, highly focused conventional geological and geophysical methods are employed to evaluate the potential commercial viability of the prospects. Total finding costs include SFD survey, seismic data acquisition and interpretation, purchasing mineral rights and drilling and completing exploration wells.

We now conduct our activities primarily through our wholly owned subsidiary, NXT Energy Canada Inc., which focuses on Canadian-based exploration. Survey flight activities are conducted through our subsidiary, NXT Aero Canada Inc. The parent company concentrates on improving our SFD survey system and oversees the operations of and provides management, financial and administrative services to our subsidiaries.

Corporate History

We were initially incorporated in the State of Nevada on September 27, 1994 under the name Auric Mining Corporation. In January 1996, we acquired all of the common stock of NXT Energy USA (then known as Pinnacle Oil Inc.) from its stockholders in exchange for our common stock. As a consequence of this reverse acquisition, NXT Energy USA became our wholly-owned subsidiary and its stockholders acquired a 92% controlling interest in our common stock.

Prior to this transaction, we were a corporate shell conducting no active business, and NXT Energy USA was a development stage research and development enterprise holding world-wide rights to use the SFD technology for hydrocarbon exploration purposes.

Immediately after this transaction, we changed our name to Pinnacle Oil International, Inc, and subsequently, on June 13, 2000, we changed our name to Energy Exploration Technologies.

On October 24, 2003 our shareholders, at a special shareholders’ meeting, approved the continuance of the company from the State of Nevada to the Province of Alberta, Canada. At that time we modified our name to Energy Exploration Technologies Inc.

Corporate Objective

NXT will use the proprietary SFD technology to become a technology leader in oil and gas exploration. As we enter the commercialization stage of the SFD technology development, we must acquire projects and business opportunities that build the credibility of the SFD technology and develop NXT’s ability to deliver quality oil and gas exploration Prospect Areas.

Business Strategy

Our primary objective is the achievement of profitability and self-sustaining growth:

-20-

· | through the development or sale of our current inventory of properties; |

· | by providing SFD survey services to third parties on a fee for service basis; |

· | by using the SFD survey technology to identify oil and gas prospects that have the potential to justify the acquisition of mineral rights for oil and gas developments; |

· | through the use of conventional exploration technologies to confirm the oil and gas prospects identified with the SFD survey technology; |

· | by either directly participating in the selection of drilling locations or joint venturing with partners who will earn an interest by drilling the prospects at their cost and risk; and |

· | by the monetization of the properties as they reach the development stage. |

We believe that by successfully exploiting our SFD technology we will be able to achieve market acceptance and access to additional capital to fund the exploration, land acquisition and drilling efforts that will be necessary to sustain our future growth and expansion.

Stress Field Detector Technology

Summary

The SFD sensor is a passive transducer that responds to the energy emitted by stress fields associated with significant subsurface tectonic events, which are in turn, associated with the trapping mechanisms for oil and natural gas and the presence of fluids (oil, natural gas or water) in those traps. The exact nature of the energy field, which the sensor responds to and referred to as Stress Induced Energy field is under study and is not well understood. According to the Inventor, George Liszicasz, who is also our President, CEO and largest shareholder, this naturally occurring energy field is inherently linked to materials that are subject to stresses caused by subsurface tectonic events (geomechanical stresses). We have a substantial body of empirical evidence arising from our SFD surveys in Canada and the United States that shows a strong correlation between the observed response o f the SFD Sensors with the development of oil and gas trapping mechanisms.

The following is a summary of some of the key elements of the development and status of the SFD technology.

Identification of the source of energy causing the SFD sensor response was discovered as a result of experimentation and observation.

In Petroleum Engineering technical literature there is a substantial body of research on the identification and application of stress fields associated with optimization of production operations for oil and gas. Determination of stress fields is also important in the operation of underground mines. Understanding stress fields associated with subsurface rocks is important to several industrial sectors.

The SFD sensor is the first device to our knowledge that can remotely measure the gradient of stress energy related to rocks in the subsurface. The SFD shows a measurable multiple sensor response to the presence of faults.

George Liszicasz and NXT have maintained the confidentiality of the design of the SFD to preserve the competitive advantage of the company. No patents have been sought in respect of the SFD because the technology continues to be improved and enhanced and there is a possibility that future modifications could be made to the concepts and Sensors that would not be subject to the patent thereby nullifying NXT’s competitive advantage.

-21-

SFD Development History

The observations that led to the development of the SFD technology originally occurred more than 10 years ago. George Liszicasz was conducting experiments with respect to the property of certain materials when he observed a phenomenon with respect to crystalline structures that he could not explain. Mr. Liszicasz theorized that the change in the electronic transport capability of the material was related to certain dynamic events in the environment, which he later characterized as stress events. Mr. Liszicasz tested this hypothesis through the development of successive generations of the sensor and concluded that it was responding to the redistribution of stress regimes in the subsurface primarily caused by tectonic events. With the SFD technology it is possible to measure a stress gradient. Mr. Liszicasz arrived at this conclusion after conducting numerous SFD tests against known maj or geological events such as faulting and obtaining measurable responses over significant hydrocarbon traps.

Seeing a commercial application of the SFD technology, Mr. Liszicasz focused research and development in relation to sensors that would respond to oil and gas trapping mechanisms with a higher degree of certainty. At the same time, Mr. Liszicasz commenced development of a theoretical basis for his observation. He theorized the existence of stress energy field associated with tectonic stress regime changes surrounding petroleum and natural gas accumulations and other geological events. It took a number of years to identify certain key processes taking place in the sensor and develop a remote sensing capability suitable for hydrocarbon exploration. In 1997, he moved the sensor system from a ground-based vehicle into an airplane.

Theoretical Basis

The existence of stresses in the subsurface materials associated with tectonic events is well documented in technical papers by experts in the petroleum, mining and geophysical industries. However there is essentially no data on the ability to measure stress fields directly or remotely. There is some suggestion in the geophysical science that more detailed analysis of acoustic data associated with seismic may indicate stress anomalies. The fields, which are being measured by the SFD appear to be something new. To distinguish these fields from conventional energy fields and their measurement, the SFD sensors have been subjected to nuclear radiation, electromagnetic radiation, magnetic interference, static electric fields and inertial and gravitational acceleration. The sensor’s response has been insensitive to these energy forms, indicating that the sensors are responding to some other energy field.

While we consider with interest the possible theoretical underpinnings of the SFD technology, the application of the SFD technology focuses primarily on the substantial body of empirical evidence that shows the relationship exists and it can be further developed and refined in time to provide a valuable tool for the exploration of hydrocarbons.

We hypothesize that the principal component of our SFD technology, which we refer to as the SFD sensor, is a passive transducer that creates and maintains a stress-related non-electromagnetic and non-gravitational energy field that interacts with stress-related non-electromagnetic and non-gravitational energy fields associated with subsurface conditions.

SFD Response

The evidence supporting the existence of stress gradients in the subsurface is well established. The difference between the conventional measurement techniques and the SFD method is that the former is a direct in situ measurement of strains to calculate stress and the latter measures the stress gradient remotely. The sensors respond as they pass over various stress regimes and the character of the signal response is indicative of specific geological events, such as the presence of faults and fractures and an indication of the presence of fluids in reservoirs. The SFD Technology Evaluation Survey conducted by NXT in Syria in March 2004 illustrated SFD signal responses related to known faults in the basins of Syria.

The interpretation of the SFD signals is based on pattern recognition and NXT has developed templates to qualify signal anomalies. In a SFD survey only a two dimensional line is surveyed and it is necessary to conduct the survey in a grid pattern to identify and confirm the strongest signal responses associated with structure and reservoir

-22-

development. During the SFD survey the grid pattern can be modified to re-confirm and rank prospect areas that have a high potential for petroleum and natural gas development.

SFD signal responses related to hydrocarbon trapping mechanisms have also been observed. In order for the SFD to respond to changes in stress, it must itself be in motion.

SFD Survey System

Our SFD technology is comprised of the following components, which we collectively refer to as our SFD survey system, used for the following functions:

· | Stress Field Detector—the stress field detector or SFD is a unit, which houses the SFD sensor, the principal component of our technology. As discussed above, the SFD sensor is a passive transducer that interacts with energy fields created by subsurface stresses and registers that interaction in the form of digital electronic signals. When NXT conducts SFD surveys, we use an SFD array incorporating twelve interchangeable SFD sensors, which allows us to collect twelve sets of SFD signals. The ability to collect data from multiple SFD sensors is important for several reasons. First, it facilitates repeatability and signal verification, and cuts down on the need for additional SFD survey flights. Second, we use different SFD sensor designs, which allow us to collect different qualitative information. For example, one design of SFD sensor appears to better identify anoma lies associated with subsurface structures, while another design appears to offer more information concerning faults and a third appears to offer information concerning the quality of the reservoir in the subsurface structure. Finally, the SFD sensors are extremely sensitive devices, and the operational ability of any one sensor while on an SFD survey flight may be adversely impacted. The array of twelve sensors provides a population of three of each type of sensor and ensures that the quality of data recorded remains high. |

· | Data Acquisition System—used in conjunction with the SFD sensor array on surveys, our data acquisition system is a compact, portable computer system which concurrently acquires the twelve electronic digital signals from the SFD array in two different data formats per sensor or twenty-four signal sets in total, marks each of the signal sets with their geographic location using global positioning satellite coordinates and then stores this information for subsequent processing and interpretation at our home base. |

· | Data Processing and Interpretation Systems—once returned to our home base, the SFD data collected is processed and converted into a format that can be used by our interpretive staff. All processing is performed by our staff using computer workstations and processing software, which has been developed in-house. Once the SFD data has been processed, our geological and geophysical staff review the data, plot the flight lines and produce computer-generated base maps using our processing software and industry standard mapping software and databases. |

SFD Data Interpretation

Our SFD survey system is flown over pre-selected exploration areas in a pre-set pattern using flight lines of varying altitudes and from different directions. Once SFD datasets are returned to our offices, our geological and geophysical interpretive staff process the data, plot the flight lines and produce computer-generated base maps. We then commence the following screening and interpretation process:

· | First, we screen the SFD data for anomalous signals on the flight line, which we refer to as SFDanomalies. These SFD anomalies represent the re-distribution of material stresses in the subsurface. The signal anomalies are from either known oil and natural gas pools or unknown and non-producing areas. In the course of the SFD survey significant signal anomalies are confirmed on multiple flight lines forming the survey grid pattern. The cluster of confirmed SFD anomalies form a "Prospect Area". |

-23-

· | Then our geological team puts each identified SFD "Prospect Areas” into subsurface context using available geological databases. Where we have sufficiently qualified an SFD Prospect Area it is ready for further geological and geophysical evaluation. |

· | Lastly, should the recommended SFD prospect be targeted for exploration, traditional geological and geophysical methods, usually 2D or 3D seismic, are employed to evaluate the potential commercial viability of the prospect and to pinpoint drilling sites. |

SFD Time Frames

We conduct our SFD surveys at speeds of approximately 200 mph, and survey approximately 600 linear miles in an operating day. For each operating survey day, our staff requires approximately four days to complete the data processing and initial SFD signal interpretation to sufficiently identify and recommend the SFD Prospect Areas from that survey.

As a consequence, we are able to record and interpret approximately 600 linear miles of SFD data acquired in one SFD survey flight over a period of only a few days. By way of comparison, traditional land-based seismic crews record up to five linear miles of 2D seismic per day. Two or more weeks are then required to process the data, followed by several weeks for interpretation. As a result, it can take a minimum of six months to record, process and interpret 600 linear miles of new 2D seismic data.

Analysis Of SFD Survey Results To Date

In March 2004, NXT conducted an SFD Technology Evaluation Survey in cooperation with the Syrian Ministry of Petroleum and Mineral Resources and the Syrian Petroleum Company (SPC). The Exploration Department of the Syrian Petroleum Company designed the survey flight grid over 61,000 square kilometers (23,552 square miles). This area contained subsurface structures and hydrocarbon accumulations whose location was known only to the Syrian Petroleum Company. The SFD Technology Evaluation Survey was designed to be a "blind survey" because NXT did not have any access to the geological databases of SPC or other companies operating in Syria. Using the interpretation protocol described above, NXT identified 17 Prospect Areas and 108 subsurface structures from the interpretation of the SFD sensor signals from 5,800 kilometers (3,625 miles) of SFD survey lines.

SPC had designed the SFD survey grid so that there were 137 known subsurface structures under the flight lines. With a coincidence of 108 of 137 subsurface structures the SFD technology was 79% accurate in structure identification. In addition, NXT identified 17 Prospect Areas. A Prospect Area is a cluster of SFD signal anomalies on multiple flight lines. The quality of the signal indicated that the Prospect Areas had a high potential for hydrocarbon accumulations. The staff at SPC Exploration Department reviewed the location and ranking of the Prospect Areas and confirmed that SPC had drilled 12 of the 17 Prospect Areas. To date 11 of the 12 were in commercial production at a cumulative daily rate of over 200,000 barrels of oil per day. The other drilled Prospect Area was non-commercial. Of the remaining five Prospect Areas, three had been identified by SPC on conventional seismic surveys and the last two w ere new prospects for SPC.

NXT retained the services of Dr. Nimr Arab PhD Geophysics to review the results of the SFD Technology Evaluation Survey and the data available to the Syrian Petroleum Company that was used to compare to the SFD results. The following are the results of that work.

CONCLUSIONS

The survey conducted with the SFD technology in Syria during 2004 confirms the application of the technology as a wide area reconnaissance tool that can be applied to focus conventional exploration activities.

The SFD technology can be applied to high-grade prospects that can be confirmed with conventional exploration techniques, including seismic, significantly increasing the success of exploration while materially reducing both time and costs.

SFD sensors are airborne exploration tools that employ a unique technology at a low cost to measure stress regime distributions associated with tectonic events. The tools can identify subsurface structures that have a high

-24-

likelihood of bearing hydrocarbons over a wide range of geological environments and depths, focusing and reducing the time and expense associated with conventional exploration.

NXT conducted a 5,800 km (3,635 miles) blind survey test over an area comprising 61,000 km2 (23,835 miles2) encompassing one third of the area of Syria. The survey data was acquired over a period of six days and was closely controlled by the Syrian air force personnel. The Syrian Petroleum Company (“SPC”) established the SFD flight parameters and survey grid. Using SFD interpretation protocols developed in North America, NXT evaluated the resulting data without any access to geological or production information. NXT had no opportunity to modify or calibrate interpretation protocols developed in North America and NXT was not permitted to retrace flight patterns or to cross anomalies from several directions other than when anomalies occurred at the intersection of survey lines in the preset grid.

NXT identified and submitted 17 “Prospect Areas” which are significant anomalies crossed by more than one grid line, and contain structure(s) with high potential for hydrocarbon accumulation. NXT’s Prospect Areas correctly identified 12 known drilled areas, 11 of which are cumulatively producing over 200,000 boepd and one of which is not presently economic. Three known but undrilled seismic anomalies were also identified as Prospect Areas, along with two Prospect Areas in unexplored regions that were recommended by NXT for future exploration. NXT also submitted tables identifying individual structures to SPC. By letter dated May 11th, 2004, SPC advised NXT that the survey had successfully identified 108 known structures crossed by the grid and had missed 29, a success rate of 79%. NXT has flown, acquired, processed and interpreted all SFD data and submitted all reports, maps and tab les within 32 days to the Syrian Petroleum Company and the Ministry of Petroleum and Mineral Resources of Syria.

In November 2003, NXT’s joint venture partner commenced drilling on an SFD identified prospect at Adsett in northeastern British Columbia, Canada. The subsurface structure had been confirmed with conventional seismic. In February of 2004 the operator of the drilling abandoned the well as non-commercial. The SFD interpretation predicted subsurface structure with the potential for reservoir and possible hydrocarbon accumulation. The result of the completion operations was the production of natural gas. However, the well also produced significant quantities of water along with the natural gas making future production operations uneconomical.

We now conduct our activities primarily through our wholly owned subsidiary, NXT Energy Canada Inc., which focuses on Canadian and Middle East exploration. Prior to the sale of our U.S. properties in March of 2003, we also operated through NXT Energy USA Inc., which focused on United States based exploration. Survey flight activities are conducted through our subsidiary, NXT Aero Canada Inc. The parent company concentrates on improving our SFD survey system and oversees the operations of and provides management, financial and administrative services to our subsidiaries.

Our rights to use our SFD technology arises from the technology agreement that we entered into with Momentum Resources Corporation in 1996 and the subsequent development by NXT of the second generation of operational SFD sensors. We use the SFD technology on an exclusive worldwide basis to use, possess and control the SFD data for hydrocarbon identification and exploration purposes.

Unless otherwise stated, all dollar references in this report are in U.S. dollars.

RESULTS OF OPERATIONS

Operating revenues

On February 4, 2004, a well at Entice, Alberta, in which we have a 22.5% working interest, commenced production. Our share of production averaged 26 thousand cubic feet (mcf) per day during the quarter ended June 30, 2005. Revenues, net of royalty expense, for the period were $12,987. The average price received was $5.59 per mcf and the operating cost was $0.68 per mcf. During the quarter ended June 30, 2004 our share of production averaged 28 thousand cubic feet (mcf) per day. Revenues, net of royalty expense, for the quarter ended June 30, 2004 were $4,813, the average price received was $4.63 per mcf and the operating cost was $0.57 per mcf.

-25-

Operating loss from continuing operations

We incurred an operating loss of $477,748 for the quarter ended June 30, 2005, as compared to a loss of $1,011,956 for the corresponding period in 2004, representing a $534,208 (53%) overall decrease. This decrease was attributable to the following changes:

· | Administrative costs decreased $378,451(45%) in 2005 (total of $471,111) compared to 2004 (total $849,562). This decrease was caused mainly by a decrease in general business consulting fees of $434,560 (73%) in 2005 ($162,068 in 2005 as opposed to $596,628 in 2004), decrease in insurance expense of $4,267, in communications and advertising of $6,547, in accounting and relating fees of $10,205 and investor relations expense of $14,748 partially offset by increases in office rent expense by $6,132, in legal fees of $42,686 and in salaries and wages and related costs of $76,841 ($76,310 of those salaries were reclassified to survey cost in 2004). Lower spending in the quarter ended June 30, 2005 was mainly the result of cost-cutting measures. |

· | There were no survey activity and no survey operations and support expenses in the second quarter of 2005. Survey operations and support expenses were $152,000 in the second quarter of 2004. |

· | Depletion was $5,295 in 2005, a $4,957 (1,467%) increase from $338 recorded in the same period in 2004. |

Interest income

Interest expense for the quarter ended June 30, 2005 was $5,900 compared to the 2004 income of $575 and consisted of $6,965interest on a shareholder loan partially offset by interest of $1,065 earned on short-term deposits.

Income (loss) from discontinued operations

The gain related to discontinued operations for the quarter ended June 30, 2005 was $4,303 and is a result of reclassification. The 2004 gain was $41,805 and relates to the gain on the sale of aircraft equipment that had been previously written off.

Other comprehensive income

The foreign currency exchange loss of $9,426 for the quarter ended June 30, 2005 was caused by the change in the United States – Canadian currency rates from $1.2096 at March 31, 2005 to $1.2254 at June 30, 2005. The foreign currency exchange loss of $53,403 for the same period in 2004 was due to the change in rates from $1.31 at March 31, 2004 to $1.3475 at June 30, 2004. Comprehensive gains or losses arise in consolidating our accounting records for financial reporting purposes as a result of the fluctuations during the period.

Relationships and Transactions on Terms That Would Not Be Available From Clearly Independent Third Parties

On November 3, 2004, we entered into a loan agreement with our CEO and largest shareholder, Mr. George Liszicasz, in which we borrowed $250,000 CDN. On November 16, 2004, we amended the loan agreement whereby we borrowed an additional $31,000 US. On November 17, 2004, we entered into an additional loan agreement with Mr. Liszicasz to borrow a further $100,000 CDN. On November 19, 2004, we entered into a Loan Agreement Amendment, whereby the maturity date for all three (3) loans was extended to November 17, 2005. On February 7, 2005, we entered into another Loan Agreement Amendment, whereby the maturity date for all three (3) loans was extended further to April 15, 2006. The principal amount of the loan agreement signed on November 17 was later (on April 7, 2005) amended to $88,000 US. We did not utilize this loan until April 15, 2005.

All these agreements provide that the loans accrue interest at the rate of 0.58% per month (7.0% per annum).

· | On May 20, 2005 we signed a loan agreement with a family trust of one of our directors. The conditions of the loan agreement are as follows: principal amount $175,000 CDN ($140,500 US), 6.5% interest per annum and maturity date on or before June 19, 2005. The loan is secured with certain assets of the Company. $67,000 of the loan was converted into convertible promissory notes under the bridge-financing contract on September 19, 2005. The remainder of loan is now in default and will be repaid from the proceeds of the bridge financing. |

-26-

Liquidity And Capital Resources

Sources of Cash

In the quarter ended June 30, 2005 we had net cash inflow of $16,386 compared to the second quarter of 2004 when we had net cash outflow of $783,031. The 2005 results were due to the operating activities use of cash of $240,069, cash inflow of $234,297 from financing activities, $27,281 cash generated by investing activities, $4,303 generated by discontinued operations and the effects of the fluctuations in foreign exchange of $9,426. The 2004 results were due to the operating activities use of cash of $804,324 and exchange losses of $53,403 partially offset by funds generated by financing activities of $81,203. Net cash used by our operating activities during the three month period ended June 30, 2005 of $240,069 was an decrease of $564,225 over the same period in 2004 (net cash used in operating activities in the period ended June 30, 2004 was $804,324).

Current Cash Position and Changes in Cash Position

Our cash position as of June 30, 2005 was $104,639 as compared to $287,431 as of December 31, 2004. This decrease in our cash position was attributable to the cash used in operating activities of $240,069, cash flow of $234,297 generated by financing activities, $27,281 cash generated by investing activities, $4,303 generated by discontinued operations and the effects of the fluctuations in foreign exchange of $9,426. Our cash position as of June 30, 2004 was $526,213 as compared to $1,024,201 as of December 31, 2003.

We had a working capital deficiency of $1,335,919 as of June 30, 2005. This was mainly the result of continuing operational losses, notes payable and investment in oil and natural gas properties. There was a decrease in working capital of $2,024,047 from working capital of $688,128 as of December 31, 2004. Our losses from operations will likely continue in the third quarter.

Cash used in operating activities in the quarter ended June 30, 2005 decreased by $564,225 (70%) to $240,069 for 2005 as compared to $804,324 for the same period in 2004. The decreased cash draws were attributable mainly to decreased loss from operations and changes in non-cash working capital.

Financing activities in the second quarter of 2005 generated $233,812 from the increase in notes payable and $485 from subscriptions. Financing activities in 2004 generated $85,991 from exercise of options and $10,001 from subscriptions and used $14,789 in finders’ and other fees.

Investing activities generated cash of $27,281 for the quarter ended June 30, 2005 as compared to $613 used in the quarter ended June 30, 2004. The reason for the increase was attributable mainly to cashing $50,000 of short-term investments offset by investment in oil and gas properties of $18,225 and in other property and equipment of $4,494.

Discontinued operations generated $4,303 in the quarter ended June 30, 2005. This was due to reclassification of administration expenses for the first quarter of 2005. The quarter ended June 30, 2004 used $7,120 of cash from discontinued operations.

Other comprehensive income, specifically currency exchange, was a loss of $9,426 in the quarter ended June 30, 2005 as compared to the loss $53,403 in the quarter ended June 30, 2004. The reasons for the change are explained above.

Plan of Operation and Prospective Capital Requirements

We had $104,639 in cash on hand and $65,000 in short term investments as of June 30, 2005. On September 19, 2005 we raised $1.300,000 additional capital through bridge financing and we expect to raise additional $200,000 to $700,000 by the end of November 2005. To fund our plans and to contribute toward our normal administration and increased operational requirements for the next twelve months we will be required to raise approximately

-27-

$1,000,000 additional financing through equity issues, borrowings or property dispositions. With funds available to the Company, including the proceeds from the bridge financing, we can sustain reduced operations reflecting our cost–cutting measures until August 2006.

The consolidated financial statements included with this report are prepared using generally accepted accounting principles in the United States of America that are applicable to a going concern, which assumes the realization of assets and the settlement of liabilities in the normal course of operations. Our ability to continue as a going concern is dependent upon our ability to generate profitable operations in the future and obtain the necessary financing to meet our obligations and repay liabilities arising from normal business operations when they come due. The outcome of these matters cannot be predicted with any certainty at this time. These consolidated financial statements do not include any adjustments to amounts and classifications of assets and liabilities that may be necessary should we be unable to continue as going concern.

In the six months ended June 30, 2005, we incurred a comprehensive loss of $2,141,667 and have an accumulated deficit of $28,141,490 and a working capital deficiency of $1,335,919,as at the end of the period.

We expect to continue incurring net losses from operations and have negative operating cash flows until we can secure revenue-generating activities. These circumstances raise substantial doubt about our ability to continue as a going concern.

We have taken the following measures to ensure the ongoing viability of the company:

·

On November 3, 2004, we entered into a loan agreement with our CEO and largest shareholder, Mr. George Liszicasz, in which we borrowed $250,000 CDN. On November 16, 2004, we amended the loan agreement whereby we borrowed an additional $31,000 US. On November 17, 2004, we entered into an additional loan agreement with Mr. Liszicasz and borrowed a further $100,000 CDN. On November 19, 2004, we entered into a Loan Agreement Amendment with Mr. Liszicasz, whereby the maturity date for all three (3) loans was extended to November 17, 2005. On February 7, 2005, we entered into another Loan Agreement Amendment, whereby the maturity date for all three (3) loans was extended further to April 15, 2006. The principal amount of the loan agreement signed on November 17, 2004 was amended to $88,000 US on April 7, 2005. We did not utilize this loan until April 15, 2005, when the $88,000 was drawn upon. A ll these agreements provide that the loans accrue interest at the rate of 0.58% per month (7.0% per annum).

·

On May 20, 2005 we signed a loan agreement with a family trust of one of our directors. The conditions of the loan agreement are as follows: principal amount $175,000 CDN ($140,500 US), 6.5% interest per annum and maturity date on or before June 19, 2005. The loan is secured with certain assets of the company. $67,000 of the loan was converted into convertible promissory notes under the bridge-financing contract on September 19, 2005. The remainder of loan is now in default and will be repaid from the proceeds of the bridge financing.

·

We have undertaken a variety of cost reduction activities including, but not limited to, the termination of contract employees, a 50% reduction of salaries and reduction of corporate travel.

·

The company is currently negotiating a private placement of shares of common stock through an Offering Memorandum. The shares will not be registered under the Securities Act of 1933 and may not be offered or resold in the United States absent registration or pursuant to an exemption to the registration requirements. The objective of the private placement is to raise $10,000,000 on a best efforts basis to commercialize the SFD technology through obtaining a contract to provide the SFD survey as a service to third parties. The proceeds will be used to finance our marketing efforts and the necessary additional resources needed for the execution of the contract. We expect to close the private placement by December 31, 2005. There are no guarantees that the Company will be able to close the private placement. In this event, it is unlikely we will be able to meet our obligatio ns and we may be forced to cease operations and liquidate our assets.

-28-

·