Energy Transfer Partners, L.P. Barclays CEO Energy – Power Conference September 4, 2012 Filed by Energy Transfer Partners, L.P. pursuant to Rule 425 under the Securities Act of 1933 and deemed filed pursuant to Rule 14a-12 under the Securities Exchange Act of 1934 Subject Company: Sunoco, Inc. Commission File No.: 1-06841 |

2 Legal Disclaimer SAFE HARBOR FOR FORWARD-LOOKING STATEMENTS This document may include certain statements concerning expectations for the future that are forward-looking statements as defined by federal law. Such forward-looking statements are subject to a variety of known and unknown risks, uncertainties, and other factors that are difficult to predict and many of which are beyond ETP management’s control. An extensive list of factors that can affect future results are discussed in the Annual Reports on Form 10-K and other documents filed by ETP and Energy Transfer Equity, L.P. (“ETE”) from time to time with the Securities and Exchange Commission (“SEC”). Statements in this document regarding the proposed transaction between ETP and Sunoco, Inc. (“Sunoco”) the expected timetable for completing the proposed transaction, future financial and operating results, benefits and synergies of the proposed transaction, future opportunities for the combined company, and any other statements about ETP, ETE, Sunoco Logistics Partners, L.P. (“SXL”) or Sunoco managements’ future expectations, beliefs, goals, plans or prospects constitute forward looking statements within the meaning of the Private Securities Litigation Reform Act of 1995. Any statements that are not statements of historical fact (including statements containing the words “believes,” “plans,” “anticipates,” “expects,” estimates and similar expressions) should also be considered to be forward looking statements. There are a number of important factors that could cause actual results or events to differ materially from those indicated by such forward looking statements, including: the ability to consummate the proposed transaction; the ability to obtain the requisite regulatory approvals, Sunoco shareholder approval and the satisfaction of other conditions to consummation of the transaction; the ability of ETP to successfully integrate Sunoco’s operations and employees; the ability to realize anticipated synergies and cost savings; the potential impact of announcement of the transaction or consummation of the transaction on relationships, including with employees, suppliers, customers and competitors; the ability to achieve revenue growth; national, international, regional and local economic, competitive and regulatory conditions and developments; technological developments; capital and credit markets conditions; inflation rates; interest rates; the political and economic stability of oil producing nations; energy markets, including changes in the price of certain commodities; weather conditions; environmental conditions; business and regulatory or legal decisions; the pace of deregulation of retail natural gas and electricity and certain agricultural products; the timing and success of business development efforts; terrorism; and the other factors described in the Annual Reports on Form 10-K for the year ended December 31, 2011 and subsequent quarterly reports on Form 10-Q filed with the SEC by ETP, ETE, SXL and Sunoco. ETP, ETE, SXL and Sunoco disclaim any intention or obligation to update any forward looking statements as a result of developments occurring after the date of this document. |

Energy Transfer Overview |

4 Energy Transfer Overview • Energy Transfer Partners, L.P. (ETP) is one of the largest and most diversified investment grade MLPs – Enterprise value of $17.2 billion 1,2 • Recent strategic transactions combined with organic growth projects have transformed Energy Transfer into a geographically diversified midstream logistics platform with “best in class” natural gas, crude oil, NGL and refined product capabilities – Strategic transactions resulted from a need to diversify both operationally and geographically and our customers’ desire for fully integrated midstream capabilities • In addition, ETP has announced more than $3.0 billion of growth projects since late 2010, with a focus on liquids-rich opportunities in the Eagle Ford, Permian, and Woodford areas – In excess of $1.0 billion of additional capex will be spent on new projects to be placed into service by Q1 2013 – These transactions and growth projects have transformed Energy Transfer into a much larger and more diversified midstream energy partnership well positioned for future growth 1 As of August 30, 2012. Excludes the value of the general partner interest and incentive distribution rights (IDRs) held by ETE. 2 Includes net debt as of June 30, 2012. |

ETP Has Rapidly Evolved… • ETP has undertaken several initiatives to expand the services we can provide to our customers with an emphasis on geographic and fee-based diversification –Joint acquisition of LDH Energy (“LDHE”) in May 2011 with Regency Energy Partners LP (“RGP”) • Diversified into natural gas liquids and enhanced NGL capabilities with emphasis on fee based income –Contribution of propane business to AmeriGas in January 2012 • Minimized exposure to weather sensitive non-core business and deleveraged balance sheet through tender offer –ETE’s acquisition of Southern Union (“SUG”) and drop down of a 50% interest in Citrus to ETP in March 2012 • Expanded geographic reach with emphasis on fee based income –Announced the pending acquisition of Sunoco, Inc. (“SUN”) in April 2012; scheduled to close October 2012 • Creates “best in class” natural gas, crude oil, NGL and refined product logistics and transportation platform –Announced the pending dropdown of a portion of SUG to ETP HoldCo Corp, a new ETP-controlled entity to be jointly owned by ETP and ETE, in June 2012 • Transfers operational control of SUG assets to ETP and begins simplification of overall structure 2004 – 2007 2008 – 2009 2010 – 2011 2012 Acquired TUFCO Pipeline, Houston Pipeline and Transwestern Interstate Pipeline Completed the first 42-inch diameter natural gas pipeline in the state of Texas in 2007 Initiated open season for new interstate gas pipeline, Midcontinent Express Pipeline (“MEP”), a 50/50 joint venture with Kinder Morgan Energy Partners (“KMP”) MEP completed and placed in- service Completed Phoenix and San Juan projects, expanding Transwestern Pipeline Initiated open season for new interstate gas pipeline, Tiger Pipeline Initiated open season for new interstate gas pipeline, Fayetteville Express Pipeline (“FEP”), a 50/50 joint venture with KMP FEP and Tiger completed ahead of schedule and significantly under budget ETP and Regency acquired LDHE and formed Lone Star NGL JV Lone Star NGL JV announced new Mont Belvieu fractionation plant and West Texas NGL pipeline projects to significantly expand liquids platform Expansion of Eagle Ford shale projects with the Rich Eagle Ford Mainline (“REM”) pipeline and new processing facility in Jackson County, TX Completed contribution of propane business to AmeriGas Partners, L.P. ETP acquired 50% interest in Citrus, which owns Florida Gas Transmission Announced a second Mont Belvieu fractionation plant and expansion of Eagle Ford projects supported by long-term fee- based contracts ETP announces acquisition of SUN, expanding into crude oil, NGLs and refined product logistics and transportation 5 |

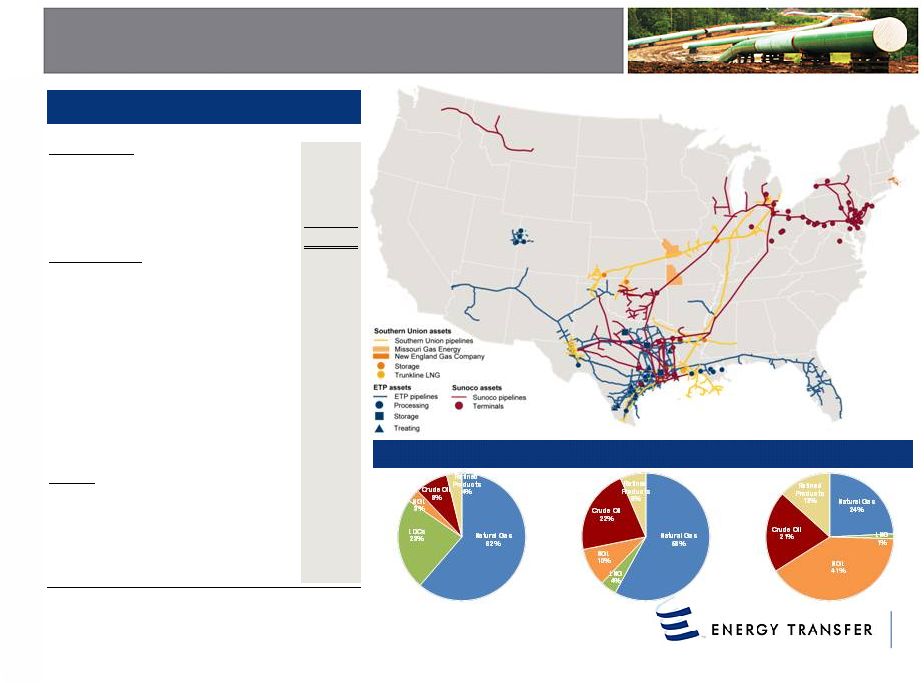

…Creating a More Diversified and Integrated Asset Footprint… 6 Note: Joint venture assets shown on consolidated basis; Includes previously announced projects under construction. Pro forma for Sunoco Pro Forma Summary Asset Overview * Throughput and storage capacity converted on a 6:1 Mcf:Bbl basis. acquisition and Southern Union dropdown. Consolidates Sunoco Logistics. Mileage Asset Composition Throughput* Storage* Pipelines (miles): Natural Gas 39,994 Natural Gas Distribution (LDCs) 15,173 NGL 2,150 Crude Oil 5,400 Refined Products 2,500 Total 65,217 Operating Metrics: Natural Gas Throughput (Bcf/d) 28 NGL Throughput (Mbbl/d) 784 LNG Throughput (Bcf/d) 2 Crude Oil Throughput (Mbbl/d) 1,747 Refined Products Throughput (Mbbl/d) 522 Natural Gas Processing Capacity (MMcf/d) 3,417 Natural Gas Treating Capacity (MMcf/d) 2,570 Natural Gas Conditioning Capacity (MMcf/d) 846 NGL Processing Capacity (Mbbl/d) 251 Natural Gas Storage (Bcf) 176 NGL Storage (Mbbl) 48,000 LNG Storage Capacity (Bcf) 9 Crude Oil Storage (Mbbl) 25,000 Refined Products Storage (Mbbl) 16,000 Facilities: Natural Gas Storage Facilities 9 NGL Storage Facilities 3 Crude Oil Storage Facilities 4 Refined Products Storage Facilities 44 Natural Gas Process., Treat., Cond. Facilities 45 NGL Processing Facilities 4 Retail Marketing Outlets 4,900 |

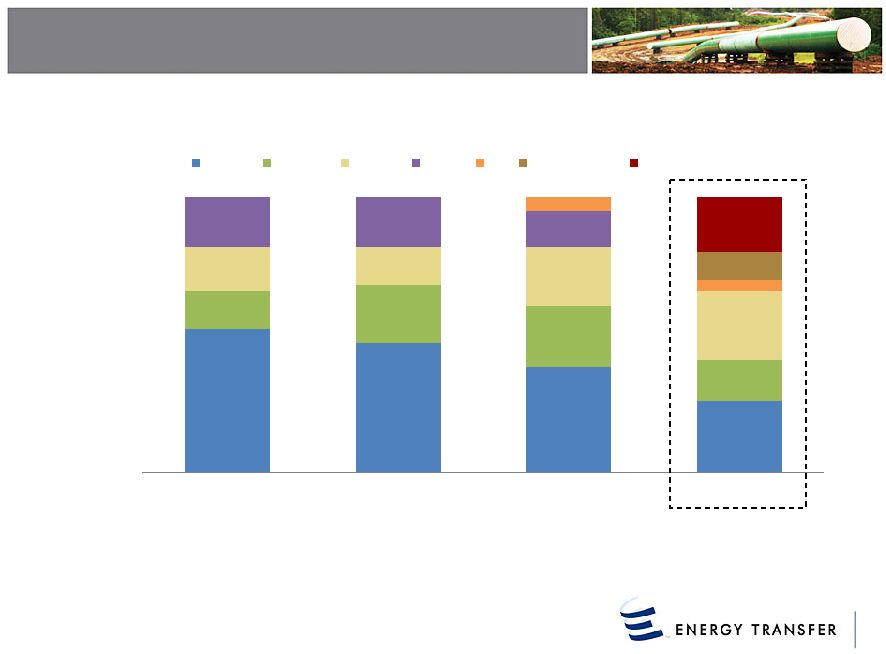

52% 47% 38% 26% 14% 21% 22% 15% 16% 14% 21% 25% 18% 18% 13% 5% 4% 10% 20% 0% 25% 50% 75% 100% 2009 2010 2011 Pro Forma 2011 Intrastate Midstream Interstate Propane NGL Retail Marketing Crude/Refined Products 1 7 …With an Enhanced Business Profile… Business Performance by Operating Segment Note: Adjusted EBITDA reconciliation in appendix. ETP adjusted EBITDA excludes “Other”; 2011 ETP pro forma for contribution of propane to AmeriGas Partners, L.P. and Citrus acquisition. Excludes distributions from AmeriGas Partners, L.P. Assumes full consolidation of SXL. |

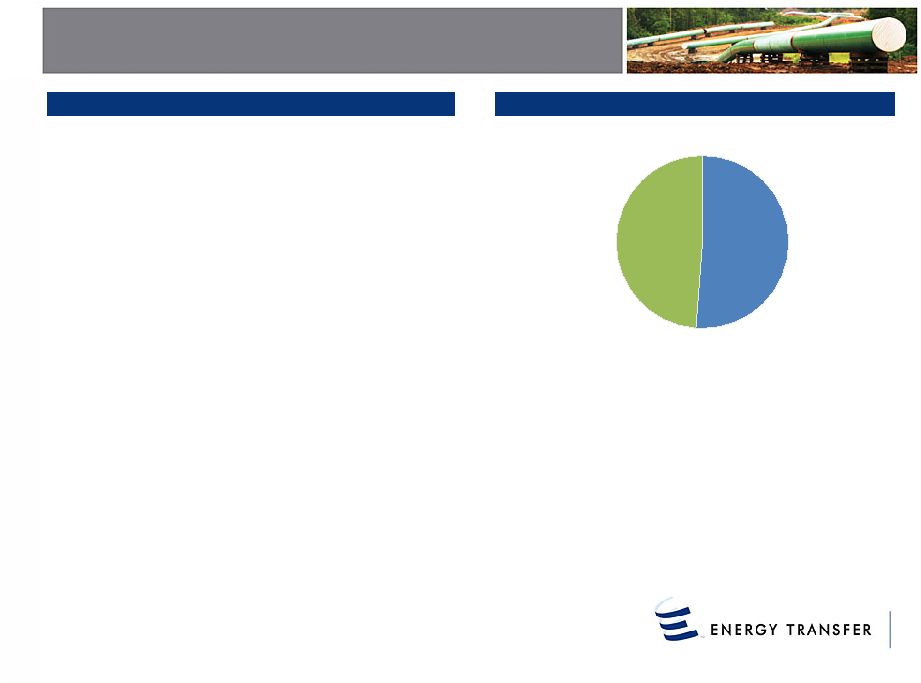

8 …Better Positioned to Deliver on Our Financial Objectives… • Retain an attractive cash flow profile Financial Objectives Capital Deployed 2005 – June 2012 Equity & Excess Cash Flow 51% Debt 49% Total = $16.0 billion 2 1 Excludes maintenance capex. – Achieve and maintain a 1.05x distribution coverage • Grow distributable cash flow – Target Debt/Adjusted EBITDA ratio of 4.00x – 4.25x – Preserve financial flexibility to successfully manage • Maintain a strong balance sheet – Generate stable cash flows from a diversified of return and that are complementary to our existing asset base – Target projects/assets that provide for attractive rates ratio growth projects and acquisitions – Manage commodity price exposure based contracts – Support growth projects with long-term fee- asset base 2 See page 19 for reconciliation. 1 |

9 …With a Robust Portfolio of Attractive Organic Growth Projects • Announced more than $3.0 billion of investment in midstream and NGL projects –The remaining projects are proceeding on time and on budget with a majority of the projects schedule to be in service over the next 6-9 months • $900 million - $1.1 billion remaining to be spent in 2012 • $1.5 billion - $1.7 billion to be spent in 2013 and beyond on announced projects • Projects further diversify the business mix and expand service offerings across the midstream value chain –Allow us to offer a full scope of services to our customers • Acquisitions have created numerous incremental commercial opportunities for further growth 2012 Growth Capex Announced Growth Projects Since Q4 2010 Lone Star 38% Midstream 50% NGL 12% Total = $3,077 million ($ millions) 2012 YTD (Q1 - Q2) 2012 2 Half (Q3 - Q4) Growth Capital Expenditures Intrastate / Midstream 551 $ $ 450 - 500 Interstate 3 - NGL 670 700 - 800 Propane & Other 2 - Total 1,226 $ $ 1,150 - 1,300 Contributions from Noncontrolling 1 (151) (200 - 250) Total (net) 1,075 $ $ 900 - 1,100 nd Interest in Lone Star 1 Represents Regency’s 30% noncontrolling interest in Lone Star. |

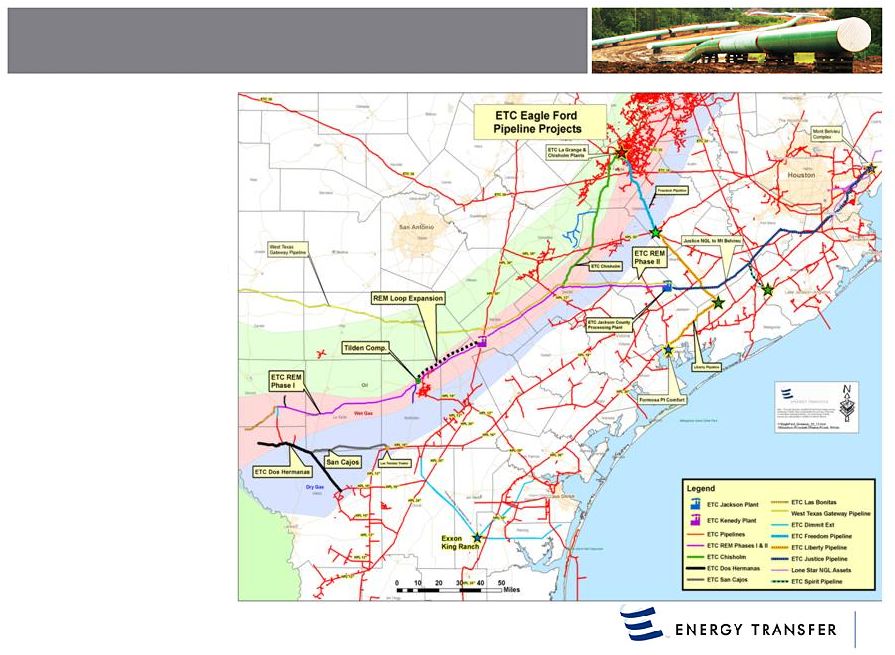

Eagle Ford Shale Projects 10 • In Q1 2012, the Chisholm natural gas processing plant was completed on time and on budget • The Chisholm plant, along with the Dos Hermanas, Chisholm, and REM Phase I pipelines, which were already in-service, represent more than $400 million of Eagle Ford projects that are now generating cash flow • Phase II of the REM pipeline, phase I of the Jackson County processing plant, and the Karnes County processing plant are scheduled for completion in Q4 2012 and/or 1st quarter 2013 |

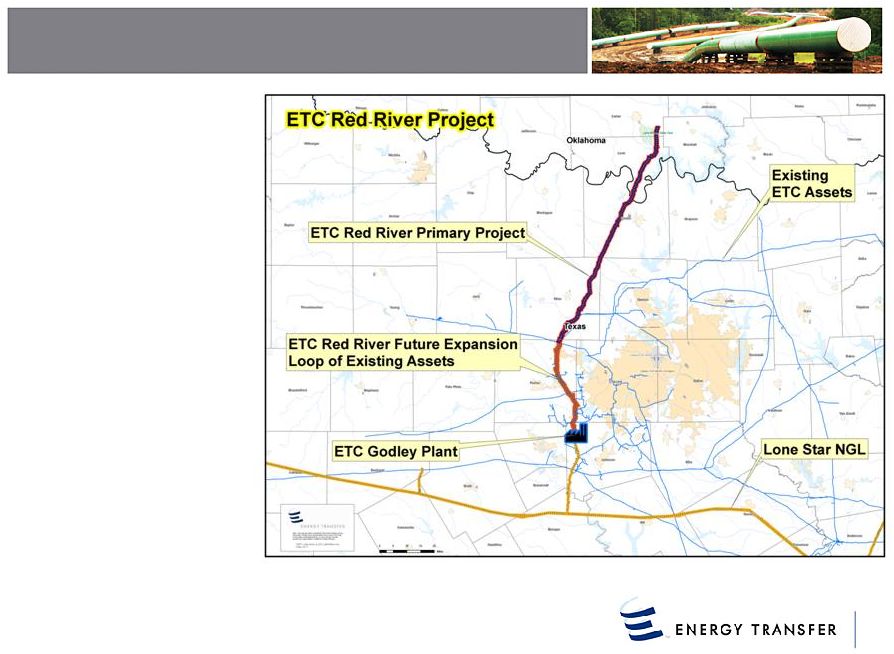

Woodford Shale Project 11 • 117 miles of 30-inch pipe and 22 miles of 24-inch loop of existing system • 450 MMcf/d of initial pipeline capacity • Originating in Carter County, OK and terminating in Johnson County at the Godley Plant • 200 MMcf/d Cryo plant at Godley • Expected pipeline in-service by Q4 2012 • Expected Godley expansion in- service by Q3 2013 • Estimated cost ~$360 million • Supported by long-term agreement with XTO/Exxon |

ETP NGL and Lone Star Pipeline Projects 12 Approximately 570 miles of 16-inch pipe with an initial capacity of 200,000 Bbl/d Originating in Winkler County and terminating in Jackson County, Texas Lone Star has secured capacity through ETP’s Justice NGL pipeline from Jackson County to Mont Belvieu Estimated cost (100%) ~$917 million Expected in-service Q4 2012 130 mile 20-inch NGL pipeline 340,000 Bbl/d design capacity Expected in-service Q4 2012 Project cost ~$300 million West Texas Gateway Project (NGL) Pipeline Justice Pipeline |

13 • Two 100,000 Bbl/d NGL fractionators to be constructed at Mont Belvieu • A substantial amount of the fractionation capacity will be utilized for NGLs from ETP’s Justice Pipeline • Estimated cost (100%): Frac I ~$390 million Frac II ~$350 million • Expected in-service: Frac I – Q1 2013 (100% contracted) Lone Star Fractionation Projects Frac II – Q1 2014 (~70% contracted) |

14 Investment Considerations Well Positioned For Future Growth • Attractive portfolio of organic growth projects with an emphasis on fee-based opportunities in liquids rich emerging shale plays • Majority of the projects scheduled to be in service over the next 6-9 months • Recent transactions provide numerous incremental commercial opportunities with a complementary asset base Balanced Business Profile • Operating model with businesses across the midstream value chain diversifies and strengthens overall cash flow profile • Significant portion of operating income derived from fee-based sources with long-term contracts anchored by a high-quality customer base with strong credit profile • Hedge positions provide for further cash flow stability in commodity price sensitive areas Strong Balance Sheet • Recent transactions viewed as favorable by the rating agencies and further strengthens overall credit profile • Track record of a balanced approached to funding organic growth projects • Demonstrated commitment to maintaining investment grade credit metrics Diversified And Complementary Asset Footprint • Pro forma asset base will be a “best in class” natural gas, crude oil, NGL and refined products logistics platform • Integrated and complementary asset network will provide connections to multiple end markets for natural gas, crude oil and refined products • A full suite of NGL capabilities to meet the needs of liquids rich shale production |

Supplemental Information |

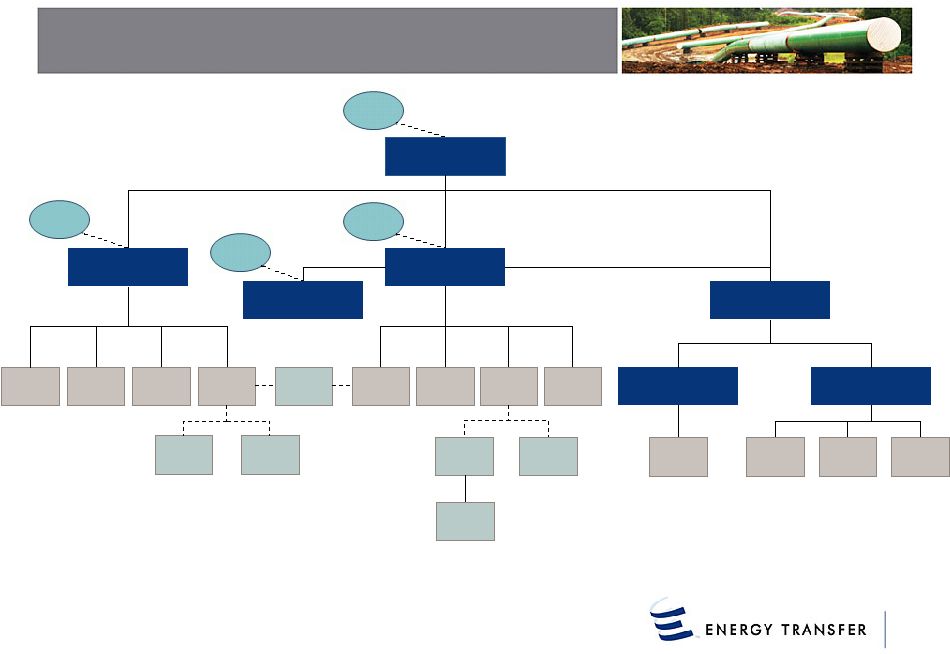

Pro Forma Organizational Structure Southern Union Company Southern Union Gas Services Panhandle Energy LDC Divisions Energy Transfer Equity, L.P. (NYSE: ETE) Public LP unitholders Lone Star NGL LLC 30% interest 70% interest 50% interest 49.99% interest HPC Midcontinent Express Pipeline Gathering & Processing Regency Energy Partners LP (NYSE: RGP) NGL Interstate Fayetteville Express Pipeline 50% interest Citrus Corp 50% interest Public LP unitholders Energy Transfer Partners, L.P. (NYSE: ETP) FGT ETP HoldCo Corp Sunoco Logistics Partners L.P. (NYSE: SXL) LP Interest GP Interest IDRs Public LP unitholders Sunoco, Inc. Retail & Marketing LP Interest GP Interest IDRs LP Interest GP Interest IDRs 60% Ownership 40% Ownership (Board Majority) Intrastate Midstream Contract Treating Contract Compression JVs 16 Public LP unitholders |

17 Announced Projects Project Description Capacity Expected Completion ($ mm) Midstream Dos Hermanas Pipeline 50-mile, 24-inch pipeline originating in northwest Webb County and extending to ETP's existing Houston Pipeline rich gas gathering system in eastern Webb County 400 MMcf/d In-service Q4 2010 $43 Chisholm Pipeline 83 mile, 20-inch pipeline extending from DeWitt County to ETP's La Grange Processing Plant in Fayette County 100 MMcf/d, expandable to 300 MMcf/d In-service Q2 2011 $68 REM Phase I 160-mile, 30-inch pipeline originating in Dimmitt County and extending to the Chisholm Pipeline for ultimate delivery to ETP’s processing plants 400 MMcf/d, expandable to 800 MMcf/d In-service Q4 2011 $220 Chisholm Plant Natural gas processing plant located adjacent to ETP's existing La Grange Plant in Fayette County 120 MMcf/d In-service Q1 2012 $70 REM Phase II 70 mile, 42-inch pipeline expansion, which will extend from the Chisholm Pipeline in DeWitt County east into Jackson County 800 MMcf/d Q4 2012 $170 400 MMcf/d, Phase I Q1 2013 $420 200 MMcf/d, Phase II Q1 2014 200 MMcf/d, Phase III Q1 2014 Red River Gathering Pipeline 117-mile, 24- and 30-inch pipeline from Carter County, Oklahoma to ETP's Godley Plant in Johnson County, Texas 450 MMcf/d, expandable to 550 MMcf/d Q4 2012 $360 Godley Plant Expansion Cryogenic processing plant to be constructed at the Godley processing facility in Johnson County, Texas 200 MMcf/d Q3 2013 Karnes County Processing Plant Natural gas processing plant located in Karnes County 200 MMcf/d Q4 2012 $210 REM Expansion 37 mile, 30-inch pipeline expansion Q4 2013 Sub-total $1,561 NGL (ETP) Freedom Pipeline 43-mile, 8-inch NGL pipeline connecting the Liberty pipeline to ETP's La Grange & Chisholm plants 40 Mbbl/d In-service Q3 2011 $30 Liberty Pipeline 93-mile, 12-inch NGL pipeline owned through a 50/50 JV with Copano. Connects the Freedom pipeline to the Formosa plant 90 Mbbl/d In-service Q3 2011 $26 Justice Pipeline 130-mile, 20-inch NGL pipeline from the Jackson Plant to Mont Belvieu 340 Mbbl/d Q4 2012 $300 Sub-total $356 NGL (100%) West Texas Gateway 570-mile, 16-inch NGL pipeline originating in Winkler County and terminating in Jackson County 200 Mbbl/d Q4 2012 $917 Frac I Mont Belvieu NGL fractionator 100 Mbbl/d Q1 2013 $390 Frac II Mont Belvieu NGL fractionator 100 Mbbl/d Q1 2014 $350 Contribution from Regency for its 30% interest ($497) Sub-total $1,160 Total announced ETP growth projects since Q4 2010 (including 70% of Lone Star) $3,077 Jackson Plant Natural gas processing plant located in Jackson County Estimated Cost |

18 Adjusted EBITDA Reconciliation The Partnership has disclosed in this press release EBITDA, as adjusted, and distributable cash flow which are non-GAAP financial measures. Management believes Adjusted EBITDA is a non-GAAP financial measure. Management believes Adjusted EBITDA provides useful information to investors as measure of comparison with peer companies, including companies that may have different financing and capital structures. The presentation of Adjusted EBITDA also allows investors to view our performance in a manner similar to the methods used by management and provides additional insight to our operating results. There are material limitations to using measures such as Adjusted EBITDA, including the difficulty associated with using it as the sole measure to compare the results of one company to another, and the inability to analyze certain significant items that directly affect a company’s net income or loss or cash flows. In addition, our calculation of Adjusted EBITDA may not be consistent with similarly titled measures of other companies and should be viewed in conjunction with measurements that are computed in accordance with GAAP, such as gross margin, operating income, net income, and cash flow from operating activities. Definition of Adjusted EBITDA The Partnership defines Adjusted EBITDA as total partnership earnings before interest, taxes, depreciation, amortization, and other non-cash items, such as non-cash compensation expense, gains and losses on disposals of assets, the allowance for equity funds used during construction, unrealized gains and losses on commodity risk management activities, non-cash impairment charges, and other non-operating income or expense items. Unrealized gains and losses on commodity risk management activities includes unrealized gains and losses on commodity derivatives and inventory fair value adjustments (excluding lower of cost or market adjustments). LTM + 2008-2011 Annual Years Ended December 31, ($ millions) 2008 2009 2010 2011 6/30/2012 Net income 866.0 $ 791.5 $ 617.2 $ 697.2 $ 1,543.2 $ Interest expense, net of interest capitalized 265.7 394.3 412.6 474.1 521.5 Income tax expense 6.7 12.8 15.5 18.8 16.6 Depreciation and amortization 262.2 312.8 343.0 430.9 431.0 Non-cash compensation expense 23.5 24.0 27.2 37.5 37.7 (Gains) losses on deconsolidation/disposals of assets 1.3 1.6 5.0 3.2 (1,054.9) Gains on non-hedged interest rate derivatives 51.0 (39.2) (4.6) 77.4 89.3 Unrealized (gains) losses on commodity risk management activities (35.5) (30.0) 78.3 11.4 90.0 Goodwill impairment loss 11.4 - - - - Impairment of investment in affiliate - - 52.6 5.4 5.4 Proportionate share of unconsolidated affiliates' interest, depreciation and allowance for equity funds used during construction - 22.3 22.5 30.0 155.4 Adjusted EBITDA attributable to non-controlling interest - - - (37.8) (58.3) Other, net (includes allowance for equity funds used during construction) (73.3) (12.7) (28.5) (5.4) (6.4) Loss on extinguishment of debt - - - - 115.0 Adjusted EBITDA 1,378.9 $ 1,477.4 $ 1,540.9 $ 1,742.6 $ 1,885.5 $ Last Twelve Months Ended |

19 Reconciliation of Capital Deployed and Funding Sources Fiscal Years Ended 8/31 Four Months Years Ended 12/31 YTD 6/30 ($ millions) 2005 2006 2007 Ended 12/31/07 2008 2009 2010 2011 2012 Net cash used in investing activities 1,133.7 $ 1,244.4 $ 2,158.1 $ 995.9 $ 2,015.6 $ 1,345.8 $ 1,493.8 $ 3,552.4 $ 1,402.4 $ Proceeds from sale of assets and discontinued operations 196.9 6.9 23.1 21.5 19.4 21.5 27.9 9.3 1,455.8 Non-cash activity 2.5 4.0 - 1.4 2.2 63.3 (588.7) - 105.0 Maintenance capital expenditures (41.0) (51.8) (89.2) (49.0) (141.0) (102.7) (99.3) (134.2) (54.3) Capital deployed 1,292.1 $ 1,203.5 $ 2,092.0 $ 969.8 $ 1,896.2 $ 1,327.9 $ 833.8 $ 3,427.5 $ 2,909.0 $ Net cash provided by operating activities 169.4 $ 543.9 $ 1,112.7 $ 245.7 $ 1,258.1 $ 826.9 $ 1,202.3 $ 1,344.4 $ 599.5 $ Maintenance capital expenditures (41.0) (51.8) (89.2) (49.0) (141.0) (102.7) (99.3) (134.2) (54.3) Distributions paid (207.0) (343.8) (622.5) (176.0) (879.2) (957.3) (1,066.0) (1,159.5) (646.0) Net proceeds from sale of assets and discontinued operations² 196.9 6.9 23.1 21.5 19.4 21.5 27.9 9.3 705.8 Excess cash flow 118.3 $ 155.2 $ 424.1 $ 42.2 $ 257.3 $ (211.6) $ 64.9 $ 60.0 $ 605.1 $ Net proceeds from issuance of common units 507.7 $ 132.4 $ 1,200.0 $ 234.9 $ 373.1 $ 936.3 $ 1,152.2 $ 1,467.0 $ 93.6 $ Capital contributions from general partner 10.4 2.8 24.5 - 8.0 3.4 8.9 - - Capital contributions from noncontrolling interest - - - - - - - 645.3 151.3 Non-cash activity¹ 2.5 4.0 - 1.4 2.2 63.3 (588.7) - 105.0 Equity issued 520.6 $ 139.2 $ 1,224.5 $ 236.3 $ 383.3 $ 1,003.0 $ 572.5 $ 2,112.2 $ 349.9 $ 1 1 Non-cash activity comprises issuances of common units in connection with certain acquisitions (2012, 2009, 2008, four months ended 12/31/07, 2006 and 2006) and redemption of common units in connection with the transfer of the investment in MEP (year ended 12/31/10). 2 YTD 6/30/2012, net proceeds from sale of assets and discontinued operations is net of repayment of debt in January 2012. |

20 ETP Debt Capitalization 1 Net proceeds from the July 2012 equity offering were $671 million.. ($ millions) 6/30/2012 July 2012 Equity Offering 1 August 2012 Maturity Pro Forma 6/30/2012 ETP Revolver ($2.5bn) 493 $ (493) $ 108 $ 108 $ ETP Senior Notes: 5.65% due 2012 108 - (108) - 6.00% due 2013 350 - - 350 8.50% due 2014 292 - - 292 5.95% due 2015 750 - - 750 6.13% due 2017 400 - - 400 6.70% due 2018 600 - - 600 9.70% due 2019 400 - - 400 9.00% due 2019 450 - - 450 4.65% due 2021 800 - - 800 5.20% due 2022 1,000 - - 1,000 6.63% due 2036 400 - - 400 7.50% due 2038 550 - - 550 6.05% due 2041 700 - - 700 6.50% due 2042 1,000 - - 1,000 Total ETP Senior Notes 7,800 - (108) 7,692 ETP Other Long-Term Debt: Transwestern Senior Notes 870 - - 870 Other (12) - - (12) Total ETP Other Long-Term Debt 858 - - 858 Total Debt 9,151 $ (493) $ - $ 8,658 $ |

21 Definitions The following is a list of certain acronyms and terms generally used in the energy industry and throughout this presentation : /d per day Bbl barrels Btu British thermal unit, an energy measurement Capacity capacity of a pipeline, processing plant or storage facility refers to the maximum capacity under normal operating conditions and, with respect to pipeline transportation capacity, is subject to multiple factors (including natural gas injections and withdrawals at various delivery points along the pipeline and the utilization of compression) which may reduce the throughout capacity from specified capacity levels. gpm gallons per minute Mcf thousand cubic feet MMBtu million British thermal units MMcf million cubic feet Bcf billion cubic feet NGL natural gas liquid, such as propane, butane and natural gasoline NYMEX New York Mercantile Exchange |

22 In connection with the proposed business combination transaction between ETP and Sunoco, Inc. (“Sunoco”), ETP filed with the U.S. Securities and Exchange Commission (the “SEC”) a registration statement on Form S-4 that included a proxy statement/prospectus. The registration statement was declared effective on August 24, 2012. Sunoco mailed the definitive proxy statement/prospectus to the Sunoco shareholders on or about August 29, 2012. THE REGISTRATION STATEMENT AND THE PROXY STATEMENT/PROSPECTUS CONTAIN IMPORTANT INFORMATION ABOUT ETP, SUNOCO, THE PROPOSED TRANSACTION AND RELATED MATTERS. INVESTORS AND SECURITY HOLDERS ARE URGED TO READ THE REGISTRATION STATEMENT AND THE PROXY/PROSPECTUS CAREFULLY. Investors and security holders may obtain free copies of the registration statement and the proxy statement/prospectus and other documents filed with the SEC by ETP and Sunoco through the web site maintained by the SEC at www.sec.gov. In addition, investors and security holders may obtain free copies of the registration statement and the proxy statement/prospectus by phone, e-mail or written request by contacting the investor relations department of ETP or Sunoco at the following: Energy Transfer Partners, L.P. Sunoco, Inc. 3738 Oak Lawn Ave. 1818 Market Street, Suite 1500 Dallas, TX 75219 Philadelphia, PA 19103 Attention: Investor Relations Attention: Investor Relations Phone: (214) 981-0795 Phone: (215) 977-6764 Email: InvestorRelations@energytransfer.com Email: SunocoIR@sunocoinc.com ETP and Sunoco, and their respective directors and executive officers, may be deemed to be participants in the solicitation of proxies in respect of the proposed transactions contemplated by the merger agreement. Information regarding directors and executive officers of ETP’s general partner is contained in ETP’s Form 10-K for the year ended December 31, 2011, which has been filed with the SEC. Information regarding Sunoco’s directors and executive officers is contained in Sunoco’s definitive proxy statement dated March 16, 2012, which is filed with the SEC. A more complete description is available in the registration statement and the proxy statement/prospectus. Important Additional Information Filed with the SEC |