Exhibit 99.1

ROBERT W. BAIRD & CO.’S 2006 BUSINESS SOLUTIONS CONFERENCE

ICT GROUP, INC.

NASDAQ: ICTG

John Brennan, Chairman & CEO

March 1, 2006

Company Statements

This presentation contains certain forward-looking statements that are subject to risks and uncertainties. Forward-looking statements include without limitation certain information relating to the effect of competition in the telemarketing industry, ICT Group’s ability to execute its business strategy, the development of alliances upon terms acceptable to ICT Group and the achievement of the anticipated benefits of such alliances, as well as statements that are preceded by, followed by or include the words “believes,” “expects,” “estimates,” “anticipates,” “plans,” “should,” or similar expressions. For such statements, ICT Group claims the protection of the safe harbor for forward-looking statements contained in the Private Securities Litigation Reform Act of 1995. Actual events or results may differ materially from those discussed in the forward-looking statements as a result of various factors, including without limitation, those discussed in ICT Group’s annual report on Form 10-K for the year ended December 31, 2004 and other documents filed by ICT Group with the Securities and Exchange Commission. ICT Group makes no undertaking and disclaims any obligation to update such forward-looking statements.

This presentation shows net income for 1996, 2002, 2003, 2004 and 2005 exclusive of special charges. In 1996 the Company reported a pre-tax, nonrecurring, non-cash charge of $12.7M which was primarily associated with the granting of options, concurrent with the Company’s IPO, to replace certain previously granted expiring options. In 2002 the Company incurred special charges of $12.6M, pre-tax. This included charges of $8.9M, pre-tax, associated with the closing and scaling back of facilities and staff in the U.S. and Europe. It also included $3.7M, pre-tax, of additional charges, including a $1.4M charge for a client claim, a $1.7M charge for the costs associated with the defense of a class action litigation and a $0.6M charge for costs associated with a postponed underwritten public offering. In 2003, the Company incurred special charges of $4.0M, pre-tax associated with a class action litigation which were partially offset by a $0.7M partial reversal of the 2002 restructuring charge. In 2004, the Company incurred special charges of $10.3M, pre-tax associated with costs incurred to defend and the settlement of a class action litigation.

In 2005, the Company received $4.2M of insurance recoveries and incurred $0.6M, pre-tax associated with the class action litigation.

Company Overview

Leading global provider of outsourced customer management and related marketing/BPO solutions Focus on mid-sized opportunities within Fortune 500 Target select group of high-growth vertical industries Extensive offshore operations supported from U.S. 41 service centers in U.S. and 7 foreign countries 16,200 employees—820 full-time LTM Revenues: $401M

March 1, 2006

U.S. Customer Interaction Services ($B) $40.0 $30.0 $20.0 $10.0 $0.0 $20.4 $23.1 $26.3 $30.0 $34.3 $38.7

2004 2005 2006 2007 2008 2009

CAGR 13.7%

Customer Service

Sales

Marketing

Technical Support/Help Desk

Source: IDC

March 1, 2006

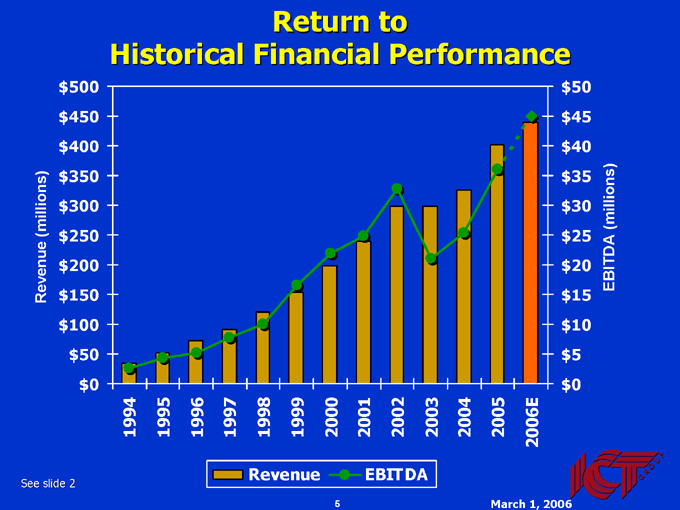

Return to

Historical Financial Performance $500 $450 $400 $350 $300 $250 $200 $150 $100 $50 $0

Revenue (millions)

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006E

EBITDA (millions) $50 $45 $40 $35 $30 $25 $20 $15 $10 $5 $0

See slide 2

Revenue EBITDA

March 1, 2006

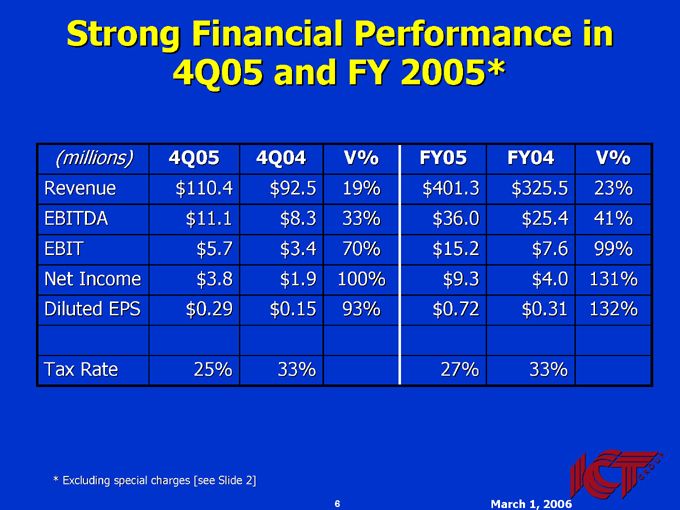

Strong Financial Performance in 4Q05 and FY 2005*

(millions) | | 4Q05 4Q04 V% FY05 FY04 V% |

Revenue | | $110.4 $92.5 19% $401.3 $325.5 23% |

EBITDA | | $11.1 $8.3 33% $36.0 $25.4 41% |

EBIT | | $5.7 $3.4 70% $15.2 $7.6 99% |

Net | | Income $3.8 $1.9 100% $9.3 $4.0 131% |

Diluted | | EPS $0.29 $0.15 93% $0.72 $0.31 132% |

* | | Excluding special charges [see Slide 2] |

March 1, 2006

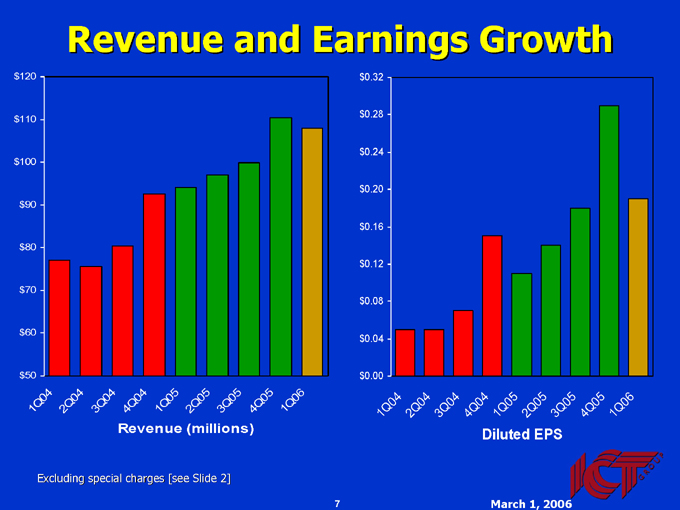

Revenue and Earnings Growth $120 $110 $100 $90 $80 $70 $60 $50

1Q04 2Q04 3Q04 4Q04 1Q05 2Q05

3Q 05

4Q 05

1Q06

Revenue (millions) $0.32 $0.28 $0.24 $0.20 $0.16 $0.12 $0.08 $0.04 $0.00

1Q04 2Q04 3Q04 4Q04 1Q05 2Q05 3Q05 4Q05 1Q06

Diluted EPS

Excluding special charges [see Slide 2]

March 1, 2006

Key Growth Drivers

Shifted to more consistent services business while improving operating performance of sales business Focused on select verticals while diversifying customer base Developed and implemented successful offshore strategy Added higher margin marketing and technology services

March 1, 2006

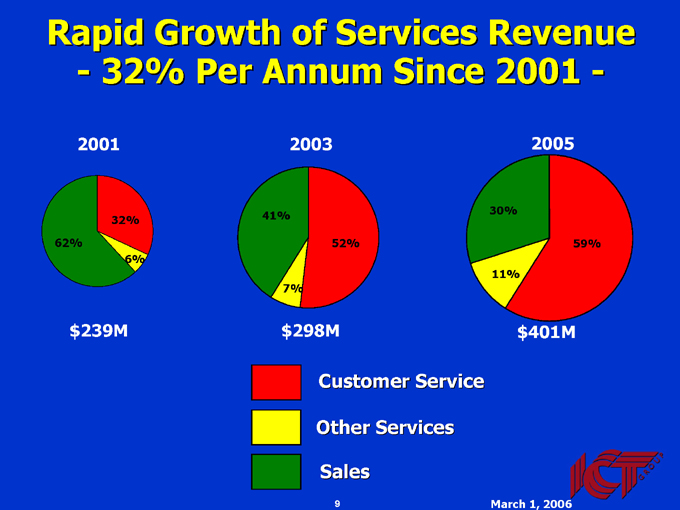

Rapid Growth of Services Revenue

- 32% Per Annum Since 2001 -

2001

32% 62% 6% $239M

2003

41%

52%

7% $298M

2005

30%

59%

11% $401M

Customer Service

Other Services

Sales

9

March 1, 2006

Focusing Resources on Select Markets

ICT differentiates itself through its vertical marketing expertise and application knowledge base Have become an industry leader in financial services and health care sectors: account for 65% of revenue Improved our sales close rate and enabled cross-selling of additional services to existing clients Now applying vertical strategy to expand into new markets: government, technology and energy services

10

March 1, 2006

Key Clients in Major Verticals

11

March 1, 2006

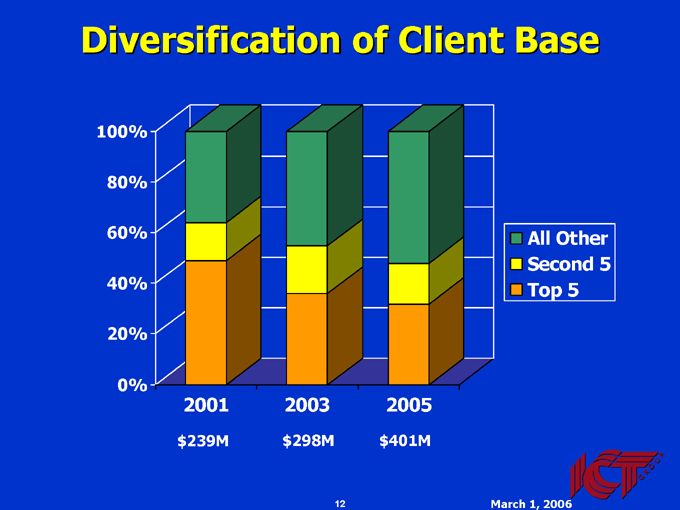

Diversification of Client Base

100%

80%

60%

40%

20%

0%

2001 2003 2005

$239M $298M $401M

All Other Second 5 Top 5

March 1, 2006

12

Global Capabilities

Based on proven international expertise Initially supported local country markets Expanded to provide low cost near-shore and offshore solutions Launched home shoring alternative in 2H05 Evaluating additional expansion for 2006

13

March 1, 2006

Global Strategy: Markets & Operations

U.K. Canada Ireland

U.S.

Philippines Mexico Caribbean India

Argentina

Australia

Served Market

Served Market with External Production External Production

Under Evaluation

Consistent Technology Platform Worldwide

Best-in-class technology platform:

Centralized architecture for reliability/flexibility VoIP telephony to reduce costs Redundant private network for voice & data communications

Intense focus on quality

All centers are ISO 9001:2000 certified

15

March 1, 2006

Leveraging Offshore Operations to Target New BPO Opportunities

Use offshore operations during off-peak hours to support other BPO services for new and existing clients Amortize infrastructure over expanded business base Raise utilization rates resulting in higher revenue and margin per workstation and higher ROIC

Add services through internal expansion, strategic relationships and acquisitions

16

March 1, 2006

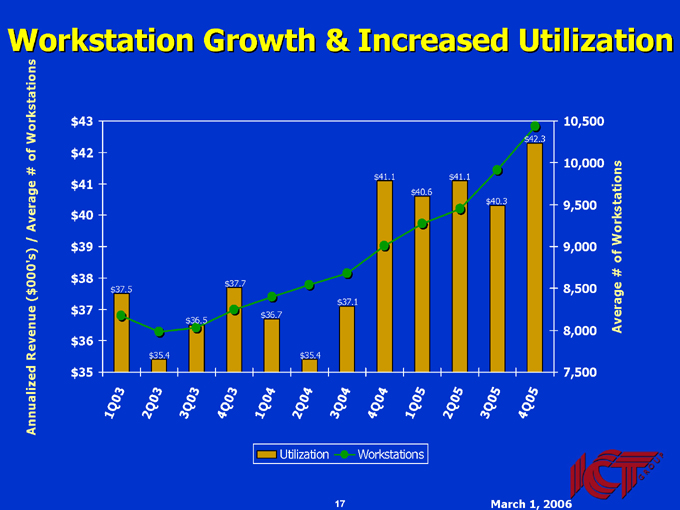

Workstation Growth & Increased Utilization

Annualized Revenue ($000’s) / Average # of Workstations $43 $42 $41 $40 $39 $38 $37 $36 $35 $37.7 $37.5

$36.5

$35.4

$37.1

$36.7

$35.4 $41.1 $41.1 $40.6 $40.3 $42.3

1Q03

2Q03

3Q03

4Q03

1Q04

2Q04

3Q04

4Q04

1Q05

2Q05

3Q05

4Q05

10,500 10,000 9,500 9,000 8,500 8,000 7,500

Average # of Workstations

Utilization Workstations

17

March 1, 2006

Margin Enhancement from CRM Technology Services

Expanded service offerings now include:

Hosted CRM, e-mail and knowledge-base software Hosted ACD, IVR and message alert services

Small but growing part of business achieving operating margins in excess of 25%

Strong pipeline for message alert services across multiple applications

Added management and sales staff

Establishing strategic alliances to target key markets

18

March 1, 2006

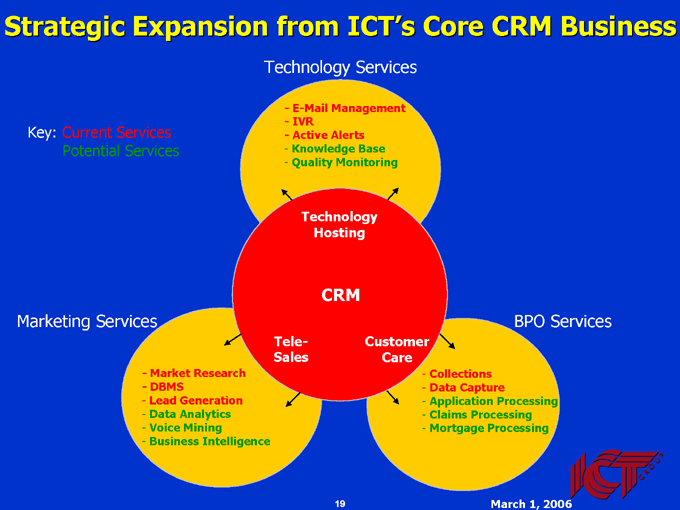

Strategic Expansion from ICT’s Core CRM Business

Technology Services

E-Mail Management IVR

Active Alerts Knowledge Base Quality Monitoring

Key: Current Services Potential Services

Marketing Services

Technology Hosting

CRM

Tele-Sales

Customer Care

Market Research DBMS

Lead Generation Data Analytics Voice Mining Business Intelligence

Collections Data Capture

Application Processing Claims Processing Mortgage Processing

BPO Services

19

March 1, 2006

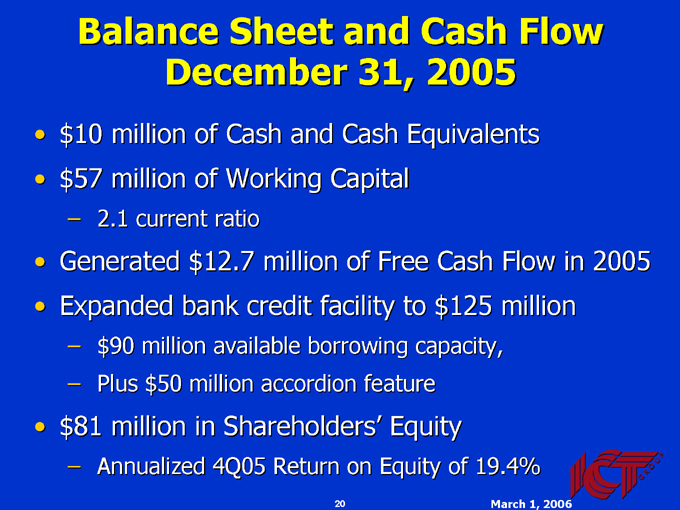

Balance Sheet and Cash Flow December 31, 2005 $10 million of Cash and Cash Equivalents $57 million of Working Capital

2.1 current ratio

Generated $12.7 million of Free Cash Flow in 2005 Expanded bank credit facility to $125 million $90 million available borrowing capacity, Plus $50 million accordion feature $81 million in Shareholders’ Equity

Annualized 4Q05 Return on Equity of 19.4%

20

March 1, 2006

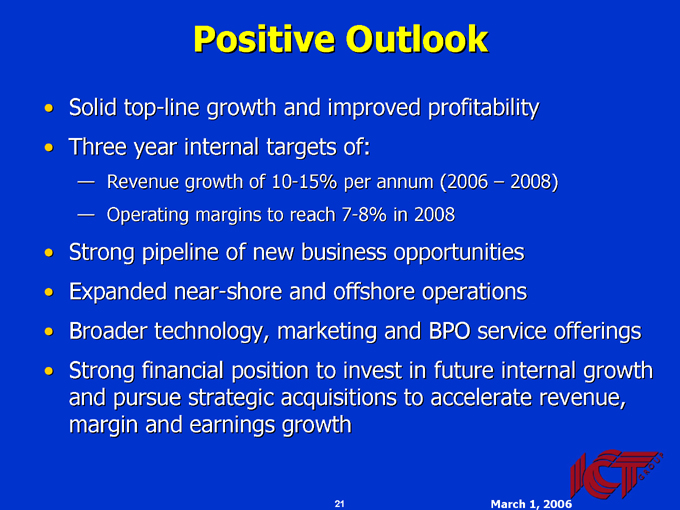

Positive Outlook

Solid top-line growth and improved profitability Three year internal targets of:

Revenue growth of 10-15% per annum (2006 – 2008) Operating margins to reach 7-8% in 2008

Strong pipeline of new business opportunities Expanded near-shore and offshore operations

Broader technology, marketing and BPO service offerings Strong financial position to invest in future internal growth and pursue strategic acquisitions to accelerate revenue, margin and earnings growth

21

March 1, 2006

NASDAQ: ICTG

March 1, 2006