| FREE WRITING PROSPECTUS | ||

| FILED PURSUANT TO RULE 433 | ||

| REGISTRATION FILE NO.: 333-184376-01 | ||

| January 14, 2013 | ||||

| FREE WRITING PROSPECTUS | ||||

STRUCTURAL AND COLLATERAL TERM SHEET $1,492,251,025 (Approximate Total Mortgage Pool Balance) $1,326,238,000 (Approximate Offered Certificates) | ||||

| COMM 2013-LC6 | ||||

Deutsche Mortgage & Asset Receiving Corporation Depositor German American Capital Corporation Ladder Capital Finance LLC Cantor Commercial Real Estate Lending, L.P. Sponsors and Mortgage Loan Sellers | ||||

| Deutsche Bank Securities | Cantor Fitzgerald & Co. | |||

Joint Bookrunning Managers and Co-Lead Managers | ||||

Ladder Capital Securities | CastleOak Securities, L.P. | |||

| KeyBanc Capital Markets | BofA Merrill Lynch | |||

Co-Managers | ||||

The depositor has filed a registration statement (including the prospectus) with the SEC (SEC File No. 333-184376) for the offering to which this communication relates. Before you invest, you should read the prospectus in the registration statement and other documents the depositor has filed with the SEC for more complete information about the depositor, the issuing trust and this offering. You may get these documents for free by visiting EDGAR on the SEC website at www.sec.gov. Alternatively, the depositor or Deutsche Bank Securities Inc., any other underwriter, or any dealer participating in this offering will arrange to send you the prospectus if you request it by calling toll-free 1-800-503-4611 or by email to the following address: prospectus.cpdg@db.com. The offered certificates referred to in these materials, and the asset pool backing them, are subject to modification or revision (including the possibility that one or more classes of certificates may be split, combined or eliminated at any time prior to issuance or availability of a final prospectus) and are offered on a “when, as and if issued” basis. You understand that, when you are considering the purchase of these certificates, a contract of sale will come into being no sooner than the date on which the relevant class has been priced and we have verified the allocation of certificates to be made to you; any “indications of interest” expressed by you, and any “soft circles” generated by us, will not create binding contractual obligations for you or us.

COMM 2013-LC6 Mortgage Trust

Capitalized terms used but not defined herein have the meanings assigned to them in the other Free Writing Prospectus expected to be dated January 17, 2013, relating to the offered certificates (hereinafter referred to as the “Free Writing Prospectus”).

| KEY FEATURES OF SECURITIZATION |

| Key Features: | Pooled Collateral Facts(1): | |||

| Joint Bookrunner & Co-Lead | Deutsche Bank Securities Inc. | Initial Outstanding Pool Balance: | $1,492,251,025 | |

| Managers: | Cantor Fitzgerald & Co. | Number of Mortgage Loans: | 70 | |

| Co-Managers: | Ladder Capital Securities, LLC | Number of Mortgaged Properties: | 99 | |

| CastleOak Securities, L.P. | Average Mortgage Loan Cut-off Date Balance: | $21,317,872 | ||

| KeyBanc Capital Markets Inc. | Average Mortgaged Property Cut-off Date Balance: | $15,073,243 | ||

| Merrill Lynch, Pierce, Fenner & Smith Incorporated | Weighted Avg Mortgage Loan U/W NCF DSCR: | 1.83x | ||

| Mortgage Loan Sellers: | German American Capital Corporation* (“GACC”) | Range of Mortgage Loan U/W NCF DSCR: | 1.01x – 3.33x | |

| (39.8%), Ladder Capital Finance LLC (“LCF”) | Weighted Avg Mortgage Loan Cut-off Date LTV: | 60.7% | ||

| (35.0%) and Cantor Commercial Real Estate | Range of Mortgage Loan Cut-off Date LTV: | 37.5% – 76.1% | ||

| Lending, L.P. (“CCRE”) (25.2%) | Weighted Avg Mortgage Loan Maturity Date or ARD LTV: | 51.4% | ||

| *An indirect wholly owned subsidiary of Deutsche Bank AG. | Range of Mortgage Loan Maturity Date or ARD LTV: | 0.3% – 70.8% | ||

| Master Servicer: | Midland Loan Services, a division of PNC Bank, | Weighted Avg U/W NOI Debt Yield: | 11.0% | |

| National Association | Range of U/W NOI Debt Yield: | 8.2% – 19.2% | ||

| Operating Advisor: | Park Bridge Lender Services LLC | Weighted Avg Mortgage Loan | ||

| Special Servicer: | Rialto Capital Advisors, LLC | Original Term to Maturity (months)(2): | 109 | |

| Trustee: | Wells Fargo Bank, National Association | Weighted Avg Mortgage Loan | ||

| Rating Agencies: | Moody’s Investors Service, Inc. and Standard & | Remaining Term to Maturity (months)(2): | 108 | |

| Poor’s Ratings Services | Weighted Avg Mortgage Loan Seasoning (months): | 1 | ||

| Determination Date: | The 6th day of each month, or if such 6th day is not a | % Mortgage Loans with Amortization for Full Term(3): | 55.7% | |

| business day, the following business day, | % Mortgage Loans which Fully Amortize during the loan Term: | 0.4% | ||

| commencing in February 2013. | % Mortgage Loans with Partial Interest Only: | 26.1% | ||

| Distribution Date: | 4th business day following the Determination Date in | % Mortgage Loans with Full Interest Only(4): | 17.8% | |

| each month, commencing February 2013. | % Mortgage Loans with Upfront or Ongoing Tax Reserves: | 75.9% | ||

| Cut-off Date: | Payment Date in January 2013 (or related | % Mortgage Loans with Upfront or | ||

| origination date, if later). Unless otherwise noted, all | Ongoing Replacement Reserves(5): | 62.2% | ||

| Mortgage Loan statistics are based on balances as | % Mortgage Loans with Upfront or Ongoing Insurance Reserves: | 43.2% | ||

| of the Cut-off Date. | % Mortgage Loans with Upfront or Ongoing TI/LC Reserves(6): | 70.9% | ||

| Settlement Date: | On or about January 30, 2013 | % Mortgage Loans with Upfront Engineering Reserves: | 15.3% | |

| Settlement Terms: | DTC, Euroclear and Clearstream, same day funds, | % Mortgage Loans with Upfront or Ongoing Other Reserves: | 40.4% | |

| with accrued interest. | (1) With respect to the Moffett Towers loan, the 540 West Madison Street loan and the Harmon Corner loan, LTV, DSCR and Debt Yield calculations include all related pari passu companion loans. With respect to a group of cross-defaulted and cross-collateralized mortgage loans, LTV, DSCR and Debt Yield calculations are presented in the aggregate for those mortgage loans. (2) For ARD loans, the original term to maturity and remaining term to maturity are through the anticipated repayment date. (3) Amortizing through the maturity date or, in the case of an ARD loan, through the anticipated repayment date. (4) Interest only through the maturity date or, in the case of an ARD loan, through the anticipated repayment date. (5) Includes FF&E Reserves. (6) Represents the percent of the allocated Initial Outstanding Pool Balance of retail and office properties only. | |||

| ERISA Eligible: | All of the Offered Classes are expected to be ERISA | |||

| eligible. | ||||

| SMMEA Eligible: | None of the Offered Classes will be SMMEA eligible. | |||

| Day Count: | 30/360 | |||

| Tax Treatment: | REMIC | |||

| Rated Final Distribution Date: | January 2046 | |||

| Minimum Denominations: | $10,000 (or $100,000 with respect to Class X-A) and | |||

| in each case in multiples of $1 thereafter. | ||||

| Clean-up Call: | 1% | |||

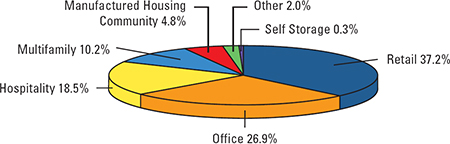

| Distribution of Collateral by Property Type |

The depositor has filed a registration statement (including the prospectus) with the SEC (SEC File No. 333-184376) for the offering to which this communication relates. Before you invest, you should read the prospectus in the registration statement and other documents the depositor has filed with the SEC for more complete information about the depositor, the issuing trust and this offering. You may get these documents for free by visiting EDGAR on the SEC website at www.sec.gov. Alternatively, the depositor or Deutsche Bank Securities Inc., any other underwriter, or any dealer participating in this offering will arrange to send you the prospectus if you request it by calling toll-free 1-800-503-4611 or by email to the following address: prospectus.cpdg@db.com. The offered certificates referred to in these materials, and the asset pool backing them, are subject to modification or revision (including the possibility that one or more classes of certificates may be split, combined or eliminated at any time prior to issuance or availability of a final prospectus) and are offered on a “when, as and if issued” basis. You understand that, when you are considering the purchase of these certificates, a contract of sale will come into being no sooner than the date on which the relevant class has been priced and we have verified the allocation of certificates to be made to you; any “indications of interest” expressed by you, and any “soft circles” generated by us, will not create binding contractual obligations for you or us.

3

COMM 2013-LC6 Mortgage Trust

| SUMMARY OF THE CERTIFICATES |

OFFERED CERTIFICATES

Class(1) | Ratings (Moody’s/S&P) | Initial Certificate Balance or Notional Amount(2) | Initial Subordination Levels(6) | Weighted Average Life (years)(3) | Principal Window (months)(3) | Certificate Principal to Value Ratio(4) | Underwritten NOI Debt Yield(5) | |||

| Class A-1 | Aaa(sf) / AAA(sf) | $93,810,000 | 30.0000% | 2.64 | 1 - 58 | 42.5% | 15.7% | |||

| Class A-2 | Aaa(sf) / AAA(sf) | $288,944,000 | 30.0000% | 4.92 | 58 - 60 | 42.5% | 15.7% | |||

| Class A-SB | Aaa(sf) / AAA(sf) | $116,999,000 | 30.0000% | 7.35 | 60 - 115 | 42.5% | 15.7% | |||

| Class A-3 | Aaa(sf) / AAA(sf) | $140,000,000 | 30.0000% | 9.69 | 112 - 118 | 42.5% | 15.7% | |||

| Class A-4 | Aaa(sf) / AAA(sf) | $404,822,000 | 30.0000% | 9.85 | 118 - 119 | 42.5% | 15.7% | |||

| Class A–M | Aaa(sf) / AAA(sf) | $134,303,000 | 21.0000% | 9.91 | 119 - 120 | 48.0% | 13.9% | |||

Class X-A(7) | Aaa(sf) / AAA(sf) | $1,178,878,000(8) | N/A | N/A | N/A | N/A | N/A | |||

| Class B | Aa3(sf) / AA-(sf) | $91,400,000 | 14.8750% | 9.94 | 120 - 120 | 51.7% | 12.9% | |||

| Class C | A3(sf) / A(sf) | $55,960,000 | 11.1250% | 9.94 | 120 - 120 | 53.9% | 12.4% | |||

NON-OFFERED CERTIFICATES

Class(1) | Ratings (Moody’s/S&P) | Initial Certificate Balance or Notional Amount(2) | Initial Subordination Levels | Weighted Average Life (years)(3) | Principal Window (months)(3) | Certificate Principal to Value Ratio(4) | Underwritten NOI Debt Yield(5) | |||

Class X–B(7) | A2(sf) / A(sf) | $147,360,000(8) | N/A | N/A | N/A | N/A | N/A | |||

Class X–C(7) | B3(sf) / NR | $104,458,024(8) | N/A | N/A | N/A | N/A | N/A | |||

| Class D | Baa3(sf) / BBB-(sf) | $61,555,000 | 7.0000% | 9.94 | 120 - 120 | 56.5% | 11.8% | |||

| Class E | Ba2(sf) / BB(sf) | $29,845,000 | 5.0000% | 9.94 | 120 - 120 | 57.7% | 11.6% | |||

| Class F | B2(sf) / B+(sf) | $27,980,000 | 3.1250% | 9.94 | 120 - 120 | 58.8% | 11.4% | |||

| Class G | NR / NR | $46,633,024 | 0.0000% | 10.47 | 120 - 144 | 60.7% | 11.0% | |||

| (1) | The pass–through rates applicable to the Class A–1, Class A–2, Class A–SB, Class A–3, Class A-4, Class A–M, Class B, Class C, Class D, Class E, Class F and Class G Certificates will equal one of: (i) a fixed per annum rate, (ii) the weighted average of the net mortgage rates on the mortgage loans (in each case, adjusted, if necessary, to accrue on the basis of a 360–day year consisting of twelve 30–day months) as of their respective due dates in the month preceding the month in which such distribution date occurs, (iii) a rate equal to the lesser of a specified pass–through rate and the weighted average of the net mortgage rates on the mortgage loans (in each case, adjusted, if necessary, to accrue on the basis of a 360–day year consisting of twelve 30–day months) as of their respective due dates in the month preceding the month in which such distribution date occurs, or (iv) the weighted average of the net mortgage rates on the mortgage loans (in each case, adjusted, if necessary, to accrue on the basis of a 360–day year consisting of twelve 30–day months) as of their respective due dates in the month preceding the month in which such distribution date occurs, less a specified rate. |

| (2) | Approximate; subject to a permitted variance of plus or minus 5%. |

| (3) | The weighted average life and principal window during which distributions of principal would be received as set forth in the table with respect to each class of certificates is based on (i) modeling assumptions and prepayment assumptions described in the Free Writing Prospectus, (ii) assumptions that there are no prepayments or losses on the mortgage loans and (iii) assumptions that there are no extensions of maturity dates and that mortgage loans with anticipated repayment dates are repaid on their respective anticipated repayment dates. |

| (4) | “Certificate Principal to Value Ratio” for any class with a Certificate Balance is calculated as the product of (a) the weighted average mortgage loan Cut–off Date LTV of the mortgage pool, multiplied by (b) a fraction, the numerator of which is the total initial Certificate Balance of the related class of Certificates and all other classes, if any, that are senior to such class, and the denominator of which is the total initial Certificate Balance of all Certificates. The Certificate Principal to Value Ratios of the Class A–1, Class A–2, Class A–SB, Class A–3 and Class A–4 Certificates are calculated in the aggregate for those classes as if they were a single class. |

| (5) | “Underwritten NOI Debt Yield” for any class with a Certificate Balance is calculated as the product of (a) the weighted average U/W NOI Debt Yield for the mortgage pool, multiplied by (b) a fraction, the numerator of which is the total initial Certificate Balance and the denominator of which is the total initial Certificate Balance of the related class of Certificates and all other classes, if any, that are senior to such class. The Underwritten NOI Debt Yields of the Class A–1, Class A–2, Class A–SB, Class A–3 and Class A–4 Certificates are calculated in the aggregate for those classes as if they were a single class. |

| (6) | The initial subordination levels for the Class A–1, Class A–2, Class A–SB, Class A–3 and Class A-4 Certificates are represented in the aggregate. |

| (7) | The pass–through rate applicable to the Class X–A, Class X–B and Class X–C Certificates for each Distribution Date will generally be equal to the excess of (i) the weighted average of the net mortgage rates on the mortgage loans (in each case, adjusted, if necessary to accrue on the basis of a 360 day year consisting of twelve 30–day months), over (ii)(A) with respect to the Class X–A Certificates, the weighted average of the pass–through rates of the Class A–1, Class A–2, Class A–SB, Class A–3, Class A-4 and Class A-M Certificates (based on their Certificate Balances), as further described in the Free Writing Prospectus, (B) with respect to the Class X–B Certificates, the weighted average of the pass–through rates of the Class B and Class C Certificates (based on their Certificate Balances), as further described in the Free Writing Prospectus and (C) with respect to the Class X–C Certificates, the weighted average of the pass–through rates of the Class E, Class F and Class G Certificates (based on their Certificate Balances), as further described in the Free Writing Prospectus. |

| (8) | The Class X–A, Class X–B and Class X–C Certificates (the “Class X Certificates”) will not have Certificate Balances. None of the Class X–A, Class X–B or Class X–C Certificates will be entitled to distributions of principal. The interest accrual amounts on the Class X–A Certificates will be calculated by reference to a notional amount equal to the sum of the total Certificate Balances of each of the Class A–1, Class A–2, Class A–SB, Class A–3, Class A-4 and Class A-M Certificates. The interest accrual amounts on the Class X–B Certificates will be calculated by reference to a notional amount equal to the sum of the total Certificate Balances of each of the Class B and Class C Certificates. The interest accrual amounts on the Class X–C Certificates will be calculated by reference to a notional amount equal to the sum of the total Certificate Balances of each of the Class E, Class F and Class G Certificates. |

The depositor has filed a registration statement (including the prospectus) with the SEC (SEC File No. 333-184376) for the offering to which this communication relates. Before you invest, you should read the prospectus in the registration statement and other documents the depositor has filed with the SEC for more complete information about the depositor, the issuing trust and this offering. You may get these documents for free by visiting EDGAR on the SEC website at www.sec.gov. Alternatively, the depositor or Deutsche Bank Securities Inc., any other underwriter, or any dealer participating in this offering will arrange to send you the prospectus if you request it by calling toll-free 1-800-503-4611 or by email to the following address: prospectus.cpdg@db.com. The offered certificates referred to in these materials, and the asset pool backing them, are subject to modification or revision (including the possibility that one or more classes of certificates may be split, combined or eliminated at any time prior to issuance or availability of a final prospectus) and are offered on a “when, as and if issued” basis. You understand that, when you are considering the purchase of these certificates, a contract of sale will come into being no sooner than the date on which the relevant class has been priced and we have verified the allocation of certificates to be made to you; any “indications of interest” expressed by you, and any “soft circles” generated by us, will not create binding contractual obligations for you or us.

4

COMM 2013-LC6 Mortgage Trust

| SUMMARY OF THE CERTIFICATES |

| Short–Term Certificate Principal Paydown Summary(1) |

| Class | Mortgage Loan Seller | Mortgage Loan | Property Type | Cut–off Date Balance | Remaining Term to Maturity (Mos.) | Cut-off Date LTV Ratio | U/W NCF DSCR | U/W NOI Debt Yield | ||

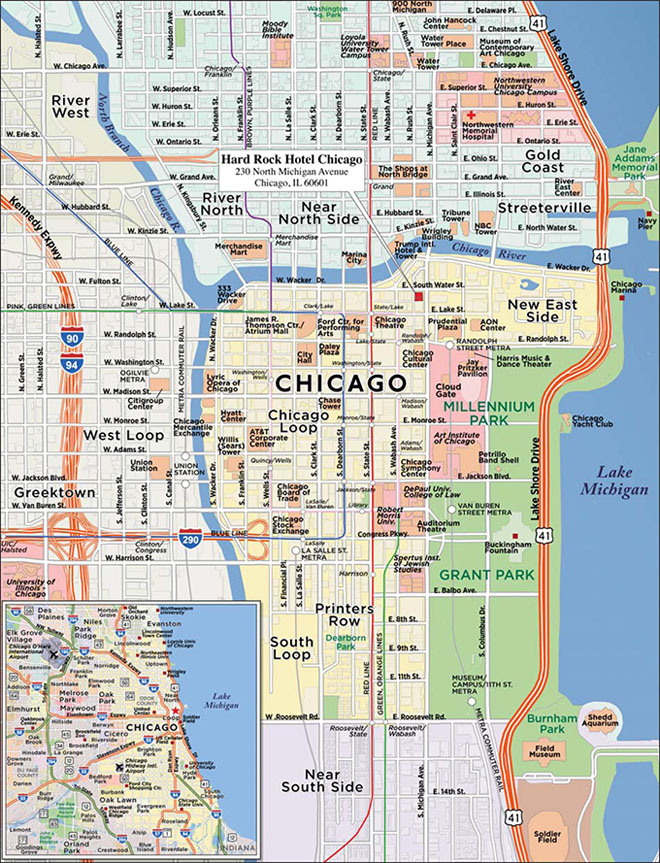

| A-2 | LCF | Hard Rock Hotel Chicago | Hospitality | $47,946,721 | 59 | 52.3% | 1.77x | 13.9% | ||

| A-2 | CCRE | Z New York Hotel | Hospitality | $18,482,342 | 59 | 49.7% | 1.76x | 13.1% | ||

| A-2 | CCRE | 1270 Gerard Avenue | Multifamily | $12,400,000 | 59 | 76.1% | 1.41x | 8.5% | ||

| A-2 | GACC | Venterra at Bradford Pointe | Multifamily | $10,087,166 | 59 | 69.2% | 1.48x | 9.4% | ||

| A-2 | CCRE | Courtyard Newark Granville | Hospitality | $4,492,697 | 59 | 57.6% | 1.62x | 13.0% | ||

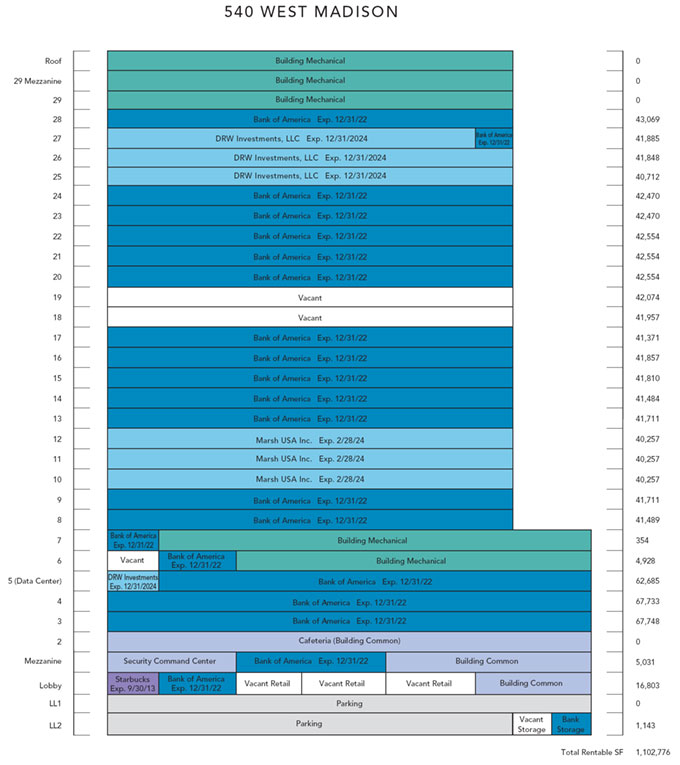

| A-2 | GACC | 540 West Madison Street | Office | $135,000,000 | 60 | 63.5% | 2.62x | 10.8% | ||

| A-2 | GACC | Renaissance Concourse Atlanta | Hospitality | $25,250,000 | 60 | 67.3% | 1.99x | 15.7% | ||

| A-2 | LCF | Holiday Inn Seattle-SeaTac | Hospitality | $21,700,000 | 60 | 61.0% | 1.72x | 13.6% | ||

| A-2 | LCF | San Pedro Crossing | Retail | $17,985,000 | 60 | 55.2% | 3.33x | 13.8% | ||

| A-2 | CCRE | Fairfield Inn and Suites - Yakima, WA | Hospitality | $3,817,000 | 60 | 57.8% | 1.72x | 14.4% | ||

| (1) | This table identifies loans with balloon payments due during the principal paydown window assuming 0% CPR and no losses on the indicated loans. See “Yield and Maturity Considerations– Yield Considerations” in the Free Writing Prospectus. |

The depositor has filed a registration statement (including the prospectus) with the SEC (SEC File No. 333-184376) for the offering to which this communication relates. Before you invest, you should read the prospectus in the registration statement and other documents the depositor has filed with the SEC for more complete information about the depositor, the issuing trust and this offering. You may get these documents for free by visiting EDGAR on the SEC website at www.sec.gov. Alternatively, the depositor or Deutsche Bank Securities Inc., any other underwriter, or any dealer participating in this offering will arrange to send you the prospectus if you request it by calling toll-free 1-800-503-4611 or by email to the following address: prospectus.cpdg@db.com. The offered certificates referred to in these materials, and the asset pool backing them, are subject to modification or revision (including the possibility that one or more classes of certificates may be split, combined or eliminated at any time prior to issuance or availability of a final prospectus) and are offered on a “when, as and if issued” basis. You understand that, when you are considering the purchase of these certificates, a contract of sale will come into being no sooner than the date on which the relevant class has been priced and we have verified the allocation of certificates to be made to you; any “indications of interest” expressed by you, and any “soft circles” generated by us, will not create binding contractual obligations for you or us.

5

COMM 2013-LC6 Mortgage Trust |

| TRANSACTION HIGHLIGHTS |

■ | $1,492,251,025 (Approximate) New–Issue Multi–Borrower CMBS: |

| – | Overview: The mortgage pool consists of 70 fixed–rate commercial and multifamily loans that have an aggregate Cut–off Date balance of $1,492,251,025 (the “Initial Outstanding Pool Balance”), have an average Cut–off Date Balance of $21,317,872 per Mortgage Loan and are secured by 99 Mortgaged Properties located throughout 27 states. |

| – | LTV: 60.7% weighted average Cut–off Date LTV and 51.4% weighted average Maturity Date or ARD LTV. |

| – | DSCR: 1.96x weighted average Debt Service Coverage Ratio, based on Underwritten NOI. 1.83x weighted average Debt Service Coverage Ratio, based on Underwritten NCF. |

| – | Debt Yield: 11.0% weighted average debt yield, based on Underwritten NOI. 10.3% weighted average debt yield, based on Underwritten NCF. |

| – | Credit Support: 30.000% credit support for the Class A–1, Class A–2, Class A–SB, Class A–3 and Class A–4 Certificates in the aggregate, which are rated Aaa(sf) / AAA(sf) by Moody’s/S&P. |

■ | Loan Structural Features: |

| – | Amortization: 82.2% of the Mortgage Loans by Cut–off Date Balance have scheduled amortization: |

■ | 55.7% of the Mortgage Loans by Cut–off Date Balance have amortization for the entire term with a balloon payment due at Maturity or ARD. |

■ | 26.1% of the Mortgage Loans by Cut–off Date Balance have scheduled amortization following a partial interest–only period with a balloon payment due at Maturity. |

■ | 0.4% of the Mortgage Loans by Cut–off Date Balance are fully amortizing for the entire term. |

| – | Hard Lockboxes: 75.6% of the Mortgage Loans by Cut–off Date Balance have Hard Lockboxes in place. |

■ | Cash Traps: 65.4% of the Mortgage Loans by Cut–off Date Balance have cash traps triggered by certain declines in net cash flow, all at levels greater than 1.05x coverage, that fund an excess cash flow reserve. |

| – | Reserves: The Mortgage Loans require amounts to be escrowed for reserves upfront or on an ongoing basis as follows: |

■ | Real Estate Taxes: 49 Mortgage Loans representing 75.9% of the total Cut–off Date Balance. |

■ | Insurance Reserves: 38 Mortgage Loans representing 43.2% of the total Cut–off Date Balance. |

■ | Replacement Reserves (Including FF&E Reserves): 46 Mortgage Loans representing 62.2% of the total Cut–off Date Balance. |

■ | Tenant Improvement / Leasing Commissions: 18 Mortgage Loans representing 70.9% of the total allocated Cut–off Date Balance of office and retail properties only. |

| – | Defeasance: 71.2% of the Mortgage Loans by Cut–off Date Balance permit defeasance only after a lockout period and prior to an open period. |

| – | Yield Maintenance: 24.7% of the Mortgage Loans by Cut–off Date Balance permit prepayment only with a Yield Maintenance Charge, following a lockout period, which may be zero, and prior to an open period. |

| – | Defeasance or Yield Maintenance: 4.1% of the Mortgage Loans by Cut–off Date Balance permit defeasance or prepayment with a Yield Maintenance Charge, following a period where each loan may be prepaid only with a Yield Maintenance charge, and prior to an open period. |

■ | Multiple–Asset Types > 5.0% of the Total Pool: |

| – | Retail: 37.2% of the Mortgaged Properties by allocated Cut–off Date Balance are retail properties (35.0% of the Mortgaged Properties are anchored retail properties, including single tenant properties). |

| – | Office: 26.9% of the Mortgaged Properties by allocated Cut–off Date Balance are office properties. |

| – | Hospitality: 18.5% of the Mortgaged Properties by allocated Cut–off Date Balance are hospitality properties. |

| – | Multifamily: 10.2% of the Mortgaged Properties by allocated Cut-off Date Balance are multifamily properties. |

■ | Geographic Diversity: The 99 Mortgaged Properties are located throughout 27 states, with only three states having greater than or equal to 10.0% by allocated Cut–off Date Balance: California (22.3%), Florida (17.5%) and Illinois (14.1%). |

The depositor has filed a registration statement (including the prospectus) with the SEC (SEC File No. 333-184376) for the offering to which this communication relates. Before you invest, you should read the prospectus in the registration statement and other documents the depositor has filed with the SEC for more complete information about the depositor, the issuing trust and this offering. You may get these documents for free by visiting EDGAR on the SEC website at www.sec.gov. Alternatively, the depositor or Deutsche Bank Securities Inc., any other underwriter, or any dealer participating in this offering will arrange to send you the prospectus if you request it by calling toll-free 1-800-503-4611 or by email to the following address: prospectus.cpdg@db.com. The offered certificates referred to in these materials, and the asset pool backing them, are subject to modification or revision (including the possibility that one or more classes of certificates may be split, combined or eliminated at any time prior to issuance or availability of a final prospectus) and are offered on a “when, as and if issued” basis. You understand that, when you are considering the purchase of these certificates, a contract of sale will come into being no sooner than the date on which the relevant class has been priced and we have verified the allocation of certificates to be made to you; any “indications of interest” expressed by you, and any “soft circles” generated by us, will not create binding contractual obligations for you or us.

6

COMM 2013-LC6 Mortgage Trust |

| STRUCTURE OVERVIEW |

| Principal Payments: | Payments in respect of principal of the Certificates will be distributed, first, to the Class A–SB Certificates, until the Certificate Balance of such Class is reduced to the planned principal balance for the related Distribution Date, as set forth on Annex A–3 to the Free Writing Prospectus, then, to the Class A–1, Class A–2, Class A–3, Class A–4, Class A-SB, Class A-M, Class B, Class C, Class D, Class E, Class F and Class G Certificates, in that order, until the Certificate Balance of each such Class is reduced to zero. Notwithstanding the foregoing, if the total Certificate Balance of the Class A–M through Class G Certificates has been reduced to zero as a result of loss allocation, payments in respect of principal of the Certificates will be distributed, first, to the Class A–1, Class A–2, Class A–3, Class A–4 and Class A–SB Certificates, on a pro rata basis, based on the Certificate Balance of each such Class, then, to the extent of any recoveries on realized losses, to the Class A-M, Class B, Class C, Class D, Class E, Class F and Class G Certificates, in that order, in each case until the Certificate Balance of each such Class is reduced to zero (or previously allocated realized losses have been fully reimbursed). The Class X–A, Class X–B and Class X–C Certificates will not be entitled to receive distributions of principal; however, (i) the notional amount of the Class X–A Certificates will be reduced by the aggregate amount of principal distributions and realized losses allocated to the Class A–1, Class A–2, Class A–SB, Class A–3, Class A–4 and the Class A–M Certificates; (ii) the notional amount of the Class X–B Certificates will be reduced by the aggregate amount of principal distributions and realized losses allocated to the Class B and Class C Certificates; and (iii) the notional amount of the Class X–C Certificates will be reduced by the aggregate amount of principal distributions and realized losses allocated to the Class E, Class F and Class G Certificates. |

| Interest Payments: | On each Distribution Date, interest accrued for each Class of the Certificates at the applicable pass–through rate will be distributed in the following order of priority, to the extent of available funds: first, to the Class A–1, Class A–2, Class A–SB, Class A–3, Class A-4, Class X–A, Class X–B and Class X–C Certificates, on a pro rata basis, based on the accrued and unpaid interest on each such Class, then, to the Class A-M, Class B, Class C, Class D, Class E, Class F and Class G Certificates, in that order, in each case until the interest payable to each such Class is paid in full. The pass–through rates applicable to the Class A–1, Class A–2, Class A–SB, Class A–3, Class A–4, Class A–M, Class B, Class C, Class D, Class E, Class F and Class G Certificates for each Distribution Date will equal one of: (i) a fixed per annum rate, (ii) the weighted average of the net mortgage rates on the mortgage loans (in each case, adjusted, if necessary, to accrue on the basis of a 360–day year consisting of twelve 30–day months) as of their respective due dates in the month preceding the month in which such distribution date occurs, (iii) a rate equal to the lesser of a specified pass–through rate and the weighted average of the net mortgage rates on the mortgage loans (in each case, adjusted, if necessary, to accrue on the basis of a 360–day year consisting of twelve 30–day months) as of their respective due dates in the month preceding the month in which such distribution date occurs, or (iv) the weighted average of the net mortgage rates on the mortgage loans (in each case, adjusted, if necessary, to accrue on the basis of a 360–day year consisting of twelve 30–day months) as of their respective due dates in the month preceding the month in which such distribution date occurs, less a specified rate. The pass–through rate applicable to the Class X–A, Class X–B and Class X–C Certificates for each Distribution Date will generally be equal to the excess of (i) the weighted average of the net mortgage rates on the mortgage loans (in each case, adjusted, if necessary to accrue on the basis of a 360 day year consisting of twelve 30–day months), over (ii)(A) with respect to the Class X–A Certificates, the weighted average of the pass–through rates of the Class A–1, Class A–2, Class A–SB, Class A–3, Class A– |

The depositor has filed a registration statement (including the prospectus) with the SEC (SEC File No. 333-184376) for the offering to which this communication relates. Before you invest, you should read the prospectus in the registration statement and other documents the depositor has filed with the SEC for more complete information about the depositor, the issuing trust and this offering. You may get these documents for free by visiting EDGAR on the SEC website at www.sec.gov. Alternatively, the depositor or Deutsche Bank Securities Inc., any other underwriter, or any dealer participating in this offering will arrange to send you the prospectus if you request it by calling toll-free 1-800-503-4611 or by email to the following address: prospectus.cpdg@db.com. The offered certificates referred to in these materials, and the asset pool backing them, are subject to modification or revision (including the possibility that one or more classes of certificates may be split, combined or eliminated at any time prior to issuance or availability of a final prospectus) and are offered on a “when, as and if issued” basis. You understand that, when you are considering the purchase of these certificates, a contract of sale will come into being no sooner than the date on which the relevant class has been priced and we have verified the allocation of certificates to be made to you; any “indications of interest” expressed by you, and any “soft circles” generated by us, will not create binding contractual obligations for you or us.

7

COMM 2013-LC6 Mortgage Trust |

| STRUCTURE OVERVIEW |

| 4 and the Class A–M Certificates (based on their Certificate Balances), as further described in the Free Writing Prospectus, (B) with respect to the Class X–B Certificates, the weighted average of the pass–through rates of the Class B and Class C Certificates (based on their Certificate Balances), as further described in the Free Writing Prospectus and (C) with respect to the Class X–C Certificates, the weighted average of the pass-through rates of the Class E, Class F and Class G Certificates (based on their Certificate Balances), as further described in the Free Writing Prospectus. |

| Prepayment Interest Shortfalls: | Net prepayment interest shortfalls will be allocated pro rata based on interest entitlements, in reduction of the interest otherwise payable with respect to each interest–bearing class of certificates. |

| Loss Allocation: | Losses will be allocated to each Class of Certificates in reverse alphabetical order starting with Class G through and including the Class A-M Certificates, and then to Class A–1, Class A–2, Class A–SB, Class A–3 and Class A–4 Certificates on a pro rata basis based on the Certificate Balance of each such class. The notional amount of any Class of Class X Certificates will be reduced by the aggregate amount of realized losses allocated to Certificates that are components of the notional amount of such Class of Class X Certificates. |

Prepayment Premiums: | A percentage of all prepayment premiums (either fixed prepayment premiums or yield maintenance amount) collected will be allocated to each of the Class A–1, Class A–2, Class A–SB, Class A–3, Class A–4, Class A–M, Class B, Class C and Class D Certificates (the “YM P&I Certificates”) then entitled to principal distributions, which percentage will be equal to the product of (a) a fraction, not greater than one, the numerator of which is the amount of principal distributed to such Class on such Distribution Date and the denominator of which is the total amount of principal distributed to the holders of the Class A–1, Class A–2, Class A–SB, Class A–3, Class A–4, Class A–M, Class B, Class C and Class D Certificates on such Distribution Date, and (b) a fraction (expressed as a percentage which can be no greater than 100% nor less than 0%), the numerator of which is the excess of the pass–through rate of such Class of Certificates currently receiving principal over the relevant Discount Rate, and the denominator of which is the excess of the Mortgage Rate of the related Mortgage Loan over the relevant Discount Rate. |

| Prepayment Premium Allocation Percentage for all YM P&I Certificates = |

| (Pass–Through Rate – Discount Rate) | X | The percentage of the principal distribution amount to such Class as described in (a) above | |

(Mortgage Rate – Discount Rate) |

| The remaining percentage of the prepayment premiums will be allocated to the Class X Certificates in the manner described in the Free Writing Prospectus. In general, this formula provides for an increase in the percentage of prepayment premiums allocated to the YM P&I Classes then entitled to principal distributions relative to the Class X Certificates as Discount Rates decrease and a decrease in the percentage allocated to such Classes as Discount Rates rise. | |

| Sale of Defaulted Loans: | Defaulted loans will be sold in a process similar to the sale process for REO property, as described under “The Pooling and Servicing Agreement—Sale of Defaulted Mortgage Loans and Serviced REO Properties” in the Free Writing Prospectus. There will be no “fair market value purchase option” and the Controlling Class Representative will have no right of first refusal with respect to the sale of defaulted loans. |

The depositor has filed a registration statement (including the prospectus) with the SEC (SEC File No. 333-184376) for the offering to which this communication relates. Before you invest, you should read the prospectus in the registration statement and other documents the depositor has filed with the SEC for more complete information about the depositor, the issuing trust and this offering. You may get these documents for free by visiting EDGAR on the SEC website at www.sec.gov. Alternatively, the depositor or Deutsche Bank Securities Inc., any other underwriter, or any dealer participating in this offering will arrange to send you the prospectus if you request it by calling toll-free 1-800-503-4611 or by email to the following address: prospectus.cpdg@db.com. The offered certificates referred to in these materials, and the asset pool backing them, are subject to modification or revision (including the possibility that one or more classes of certificates may be split, combined or eliminated at any time prior to issuance or availability of a final prospectus) and are offered on a “when, as and if issued” basis. You understand that, when you are considering the purchase of these certificates, a contract of sale will come into being no sooner than the date on which the relevant class has been priced and we have verified the allocation of certificates to be made to you; any “indications of interest” expressed by you, and any “soft circles” generated by us, will not create binding contractual obligations for you or us.

8

COMM 2013-LC6 Mortgage Trust |

| STRUCTURE OVERVIEW |

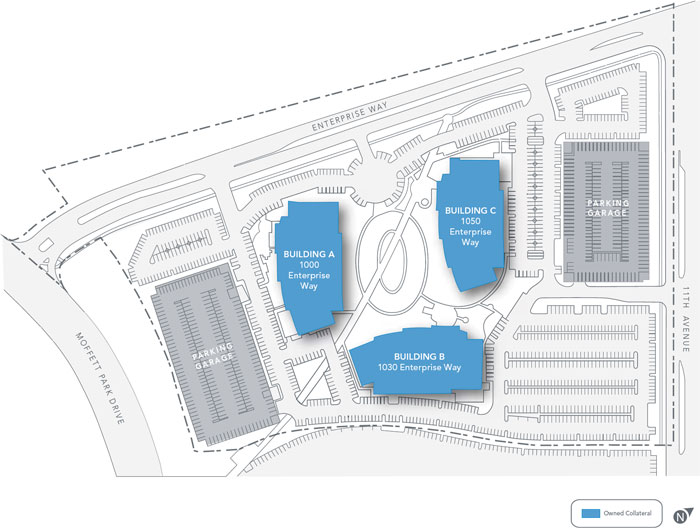

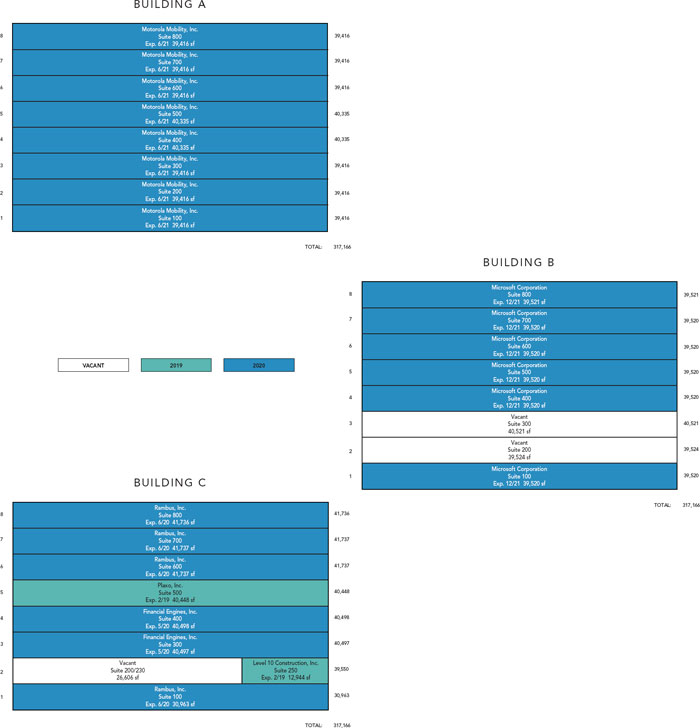

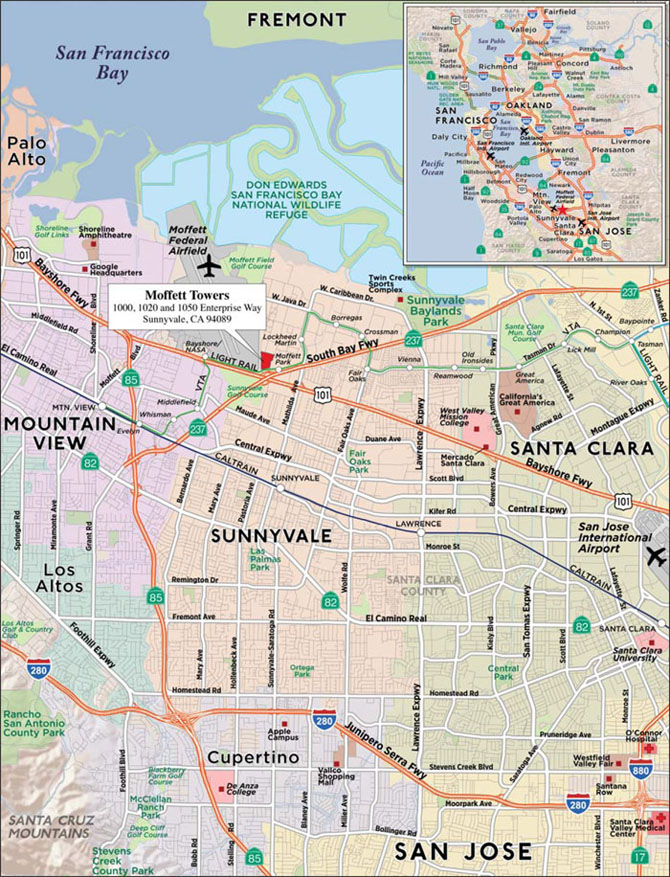

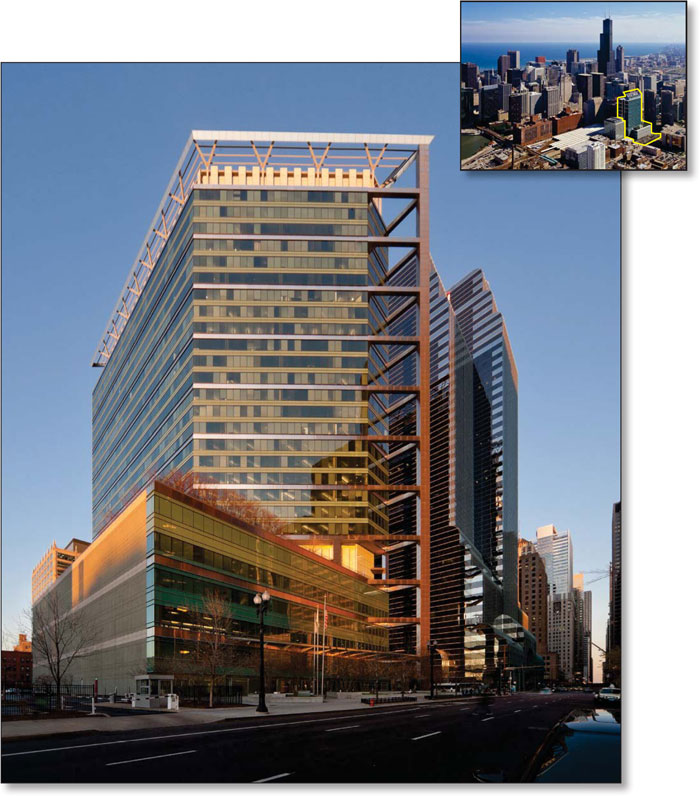

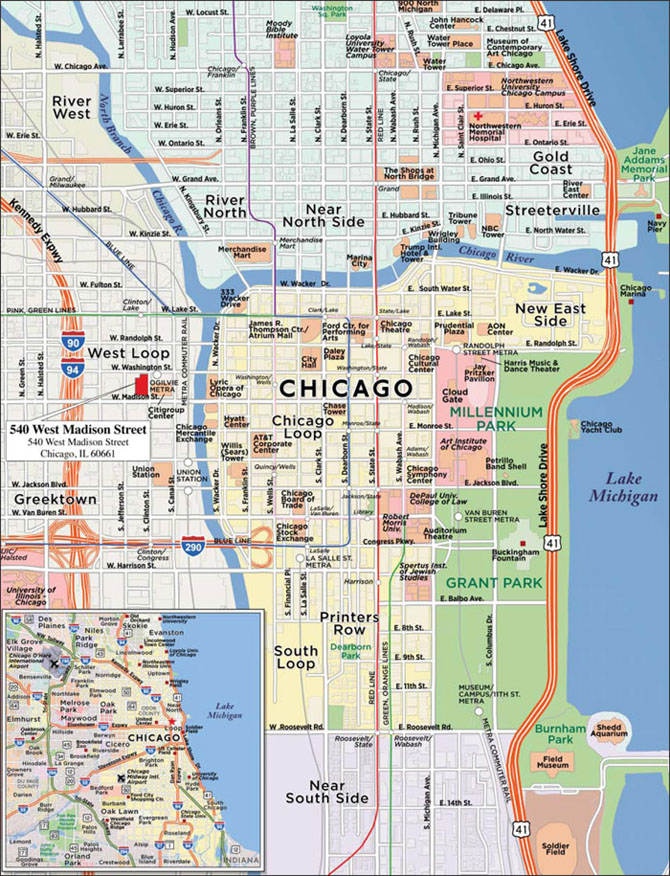

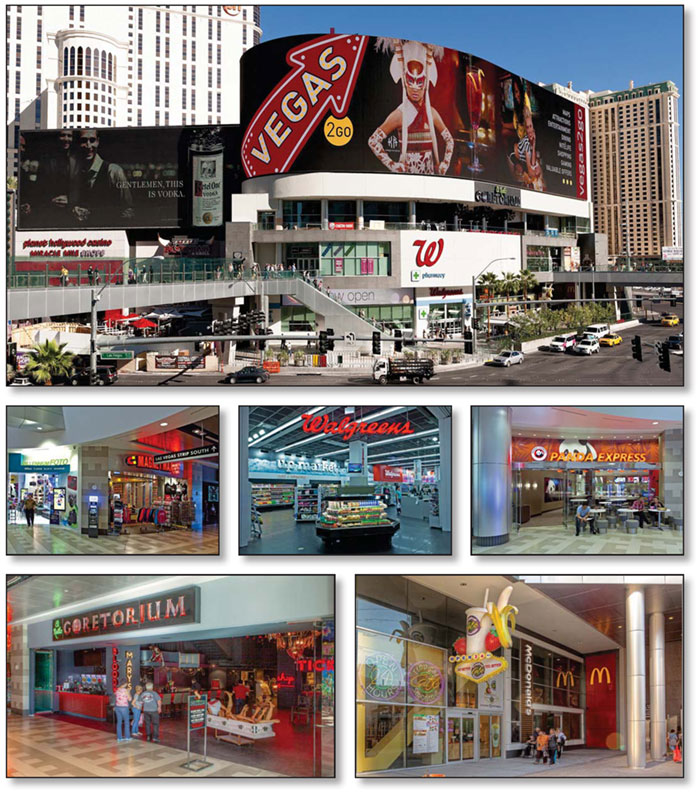

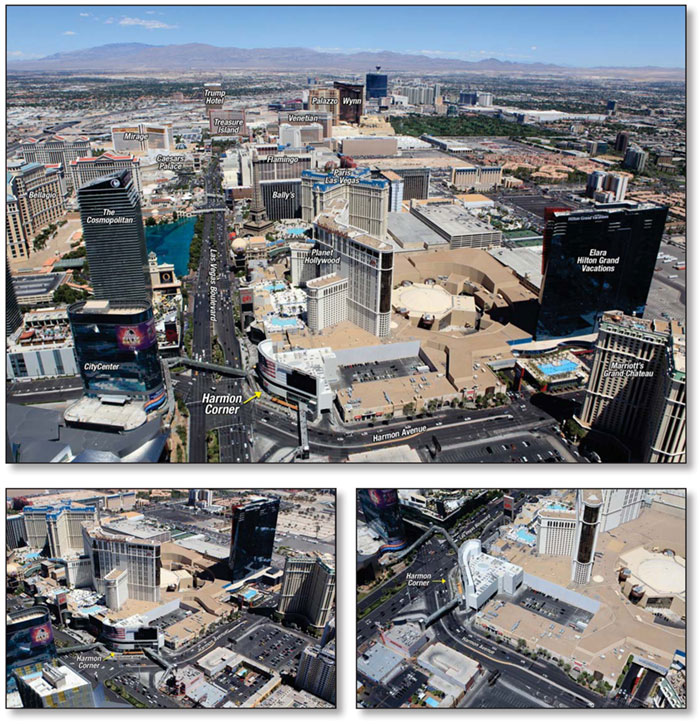

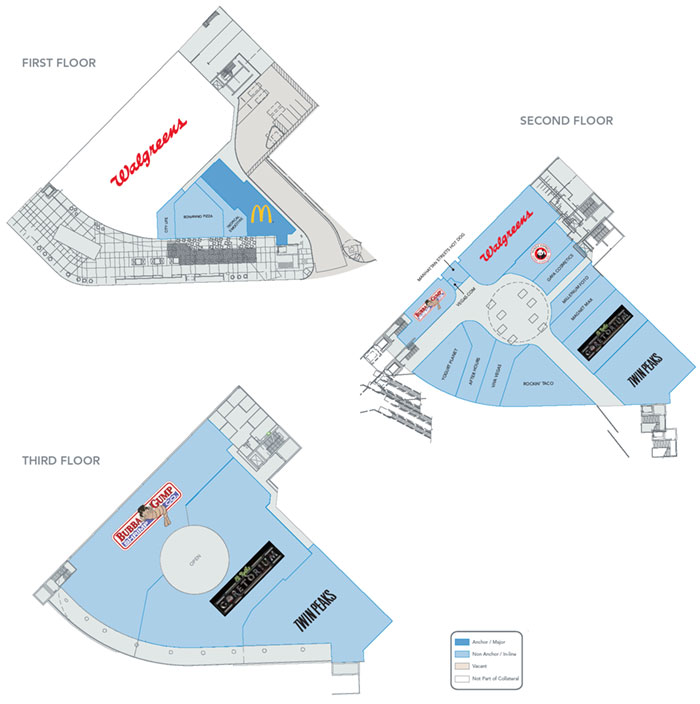

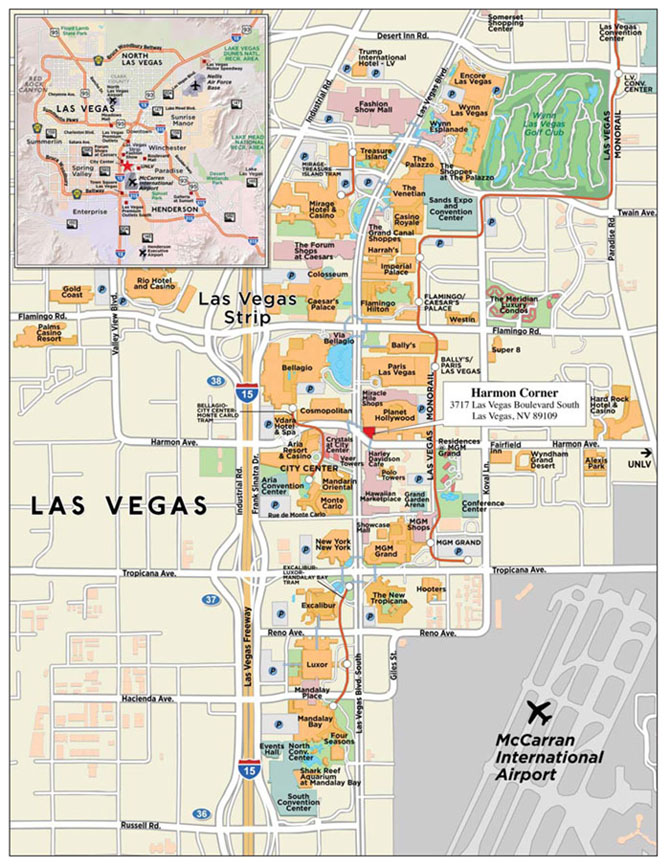

| Loan Combinations: | The Mortgaged Property identified on Annex A–1 to the Free Writing Prospectus as Moffett Towers secures a Mortgage Loan (the “Moffett Towers Mortgage Loan”) with an outstanding principal balance as of the Cut–off Date of $175,000,000, representing approximately 11.7% of the Initial Outstanding Pool Balance, and is secured on a pari passu basis with two companion loans that have an aggregate outstanding principal balance as of the Cut-off Date of $160,000,000, are not part of the mortgage pool and are currently held by German American Capital Corporation. The Moffett Towers Mortgage Loan and related companion loans are pari passu in right of payment and are referred to herein as the “Moffett Towers Loan Combination.” The Moffett Towers pari passu companion loans may be sold or further divided at any time (subject to compliance with the terms of the related intercreditor agreement). The Mortgaged Property identified on Annex A–1 to the Free Writing Prospectus as 540 West Madison Street secures a Mortgage Loan (the “540 West Madison Street Mortgage Loan”) with an outstanding principal balance as of the Cut–off Date of $135,000,000, representing approximately 9.0% of the Initial Outstanding Pool Balance, and is secured on a pari passu basis with a companion loan that has an outstanding principal balance as of the Cut-off Date of $100,000,000, is not part of the mortgage pool and is currently held by German American Capital Corporation. The 540 West Madison Street Mortgage Loan and related companion loan are pari passu in right of payment and are referred to herein as the “540 West Madison Street Loan Combination.” The 540 West Madison Street pari passu companion loan may be sold or further divided at any time (subject to compliance with the terms of the related intercreditor agreement). The Moffett Towers Loan Combination and 540 West Madison Street Loan Combination will be serviced pursuant to the pooling and servicing agreement related to this transaction (the “Pooling and Servicing Agreement”) and the related intercreditor agreements. For additional information regarding the Moffett Towers Loan Combination and the 540 West Madison Street Loan Combination, see “Description of the Mortgage Pool—Loan Combinations—The Moffett Towers Loan Combination” and “—The 540 West Madison Street Loan Combination” in the Free Writing Prospectus. The Mortgaged Property identified on Annex A–1 to the Free Writing Prospectus as Harmon Corner secures a Mortgage Loan (the “Harmon Corner Mortgage Loan”) with an outstanding principal balance as of the Cut–off Date of $34,906,374, representing approximately 2.3% of the Initial Outstanding Pool Balance, and is secured on a pari passu basis with a companion loan that has an outstanding principal balance as of the Cut–off Date of $74,799,373, is not part of the mortgage pool and is currently held by the COMM 2012–CCRE5 Mortgage Trust. The Harmon Corner Mortgage Loan and related companion loan are pari passu in right of payment and are collectively referred to herein as the “Harmon Corner Loan Combination.” The Harmon Corner Loan Combination is being serviced pursuant to the pooling and servicing agreement related to the COMM 2012-CCRE5 transaction and the related intercreditor agreement. For additional information regarding the Harmon Corner Loan Combination, see “Description of the Mortgage Pool—Loan Combinations—The Harmon Corner Loan Combination” in the Free Writing Prospectus. |

Control Rights: | Other than with respect to the Harmon Corner Loan Combination, certain Classes of Certificates (the “Control Eligible Certificates”) will have certain control rights over servicing matters with respect to each Mortgage Loan. The majority owner or appointed representative of the Class of Control Eligible Certificates that is the Controlling Class (such owner or representative, the “Directing Holder”), will be entitled to direct the Special Servicer to take, or refrain from taking certain actions with respect to a Mortgage Loan. |

The depositor has filed a registration statement (including the prospectus) with the SEC (SEC File No. 333-184376) for the offering to which this communication relates. Before you invest, you should read the prospectus in the registration statement and other documents the depositor has filed with the SEC for more complete information about the depositor, the issuing trust and this offering. You may get these documents for free by visiting EDGAR on the SEC website at www.sec.gov. Alternatively, the depositor or Deutsche Bank Securities Inc., any other underwriter, or any dealer participating in this offering will arrange to send you the prospectus if you request it by calling toll-free 1-800-503-4611 or by email to the following address: prospectus.cpdg@db.com. The offered certificates referred to in these materials, and the asset pool backing them, are subject to modification or revision (including the possibility that one or more classes of certificates may be split, combined or eliminated at any time prior to issuance or availability of a final prospectus) and are offered on a “when, as and if issued” basis. You understand that, when you are considering the purchase of these certificates, a contract of sale will come into being no sooner than the date on which the relevant class has been priced and we have verified the allocation of certificates to be made to you; any “indications of interest” expressed by you, and any “soft circles” generated by us, will not create binding contractual obligations for you or us.

9

COMM 2013-LC6 Mortgage Trust |

| STRUCTURE OVERVIEW |

| Furthermore, the Directing Holder will also have the right to receive notice and consent to certain material actions that the Master Servicer and the Special Servicer proposes to take with respect to such Mortgage Loan. | |

The directing holder of the Harmon Corner Loan Combination is the directing holder of the COMM 2012-CCRE5 Mortgage Trust. Prior to the occurrence and continuance of a Consultation Termination Event, the Directing Holder of this transaction will have consultation rights (but not control rights) with respect to certain material actions to be taken by the master servicer and the special servicer of the Harmon Corner Loan Combination. The directing holder of the Harmon Corner Loan Combination is referred to herein as a “Loan Combination Directing Holder”. See also “Description of the Mortgage Pool—Loan Combinations” in the Free Writing Prospectus. |

| Control Eligible Certificates: | Class E, Class F and Class G Certificates. |

| Controlling Class: | The Controlling Class will be the most subordinate Class of Control Eligible Certificates then outstanding that has an aggregate Certificate Balance, as notionally reduced by any Appraisal Reduction Amounts allocable to such Class, equal to no less than 25% of the initial Certificate Balance of such Class. |

| The Controlling Class as of the Settlement Date will be the Class G Certificates. | |

| The holder of the control rights with respect to the Harmon Corner Loan Combination will be the related Loan Combination Directing Holder. |

| Appraised–Out Class: | Any Class of Control Eligible Certificates that has been determined, as a result of Appraisal Reductions Amounts allocable to such Class, to no longer be the Controlling Class. |

Remedies Available to Holders of an Appraised–Out Class: | Holders of the majority of any Class of Control Eligible Certificates that is determined at any time of determination to no longer be the Controlling Class as a result of an allocation of an Appraisal Reduction Amounts in respect of such Class will have the right, at their sole expense, to require the Special Servicer to order a second appraisal for any Mortgage Loan for which an Appraisal Reduction Event has occurred. Upon receipt of the second appraisal, the Special Servicer will be required to determine, in accordance with the Servicing Standard, whether, based on its assessment of the second appraisal, a recalculation of the Appraisal Reduction Amount is warranted. If warranted, the Special Servicer will direct the Master Servicer to recalculate the Appraisal Reduction Amount based on the second appraisal, and if required by such recalculation, the Special Servicer will reinstate the Appraised–Out Class as the Controlling Class. The Holders of an Appraised–Out Class requesting a second appraisal will not be entitled to exercise any rights of the Controlling Class until such time, if any, as the Class is reinstated as the Controlling Class. |

| Directing Holder: | It is expected that an entity controlled by Rialto Real Estate Fund, L.P., will be the initial Directing Holder (for each Mortgage Loan other than the Harmon Corner Mortgage Loan) and will also own 100% of the Class E, Class F and Class G Certificates as of the Settlement Date. The directing holder with respect to the Harmon Corner Loan Combination will be the related Loan Combination Directing Holder. The Loan Combination Directing Holder of the Harmon Corner Loan Combination will initially be the directing holder of the COMM 2012-CCRE5 Mortgage Trust. |

The depositor has filed a registration statement (including the prospectus) with the SEC (SEC File No. 333-184376) for the offering to which this communication relates. Before you invest, you should read the prospectus in the registration statement and other documents the depositor has filed with the SEC for more complete information about the depositor, the issuing trust and this offering. You may get these documents for free by visiting EDGAR on the SEC website at www.sec.gov. Alternatively, the depositor or Deutsche Bank Securities Inc., any other underwriter, or any dealer participating in this offering will arrange to send you the prospectus if you request it by calling toll-free 1-800-503-4611 or by email to the following address: prospectus.cpdg@db.com. The offered certificates referred to in these materials, and the asset pool backing them, are subject to modification or revision (including the possibility that one or more classes of certificates may be split, combined or eliminated at any time prior to issuance or availability of a final prospectus) and are offered on a “when, as and if issued” basis. You understand that, when you are considering the purchase of these certificates, a contract of sale will come into being no sooner than the date on which the relevant class has been priced and we have verified the allocation of certificates to be made to you; any “indications of interest” expressed by you, and any “soft circles” generated by us, will not create binding contractual obligations for you or us.

10

COMM 2013-LC6 Mortgage Trust |

| STRUCTURE OVERVIEW |

| Control Termination Event: | Will occur when no Class of Control Eligible Certificates has a Certificate Balance (as notionally or actually reduced by any Appraisal Reduction Amounts and Realized Losses) equal to or greater than 25% of the Certificate Balance as of the Settlement Date. |

| Upon the occurrence and the continuance of a Control Termination Event, the Controlling Class will no longer have any Control Rights. The Directing Holder will no longer have the right to direct certain actions of the Special Servicer and will no longer have consent rights with respect to certain material actions that the Master Servicer or Special Servicer proposes to take with respect to a Mortgage Loan. | |

Upon the occurrence and continuation of a Control Termination Event, the Directing Holder (i.e., the majority owner or representative of the senior most Class of Control Eligible Certificates) will retain non–binding consultation rights with respect to certain material actions that the Special Servicer proposes to take with respect to a Mortgage Loan. Such consultation rights will continue until the occurrence of a Consultation Termination Event. With respect to the Harmon Corner Loan Combination, the related Loan Combination Directing Holder will retain its control rights as specified under the related intercreditor agreement, without regard to whether a Control Termination Event has occurred and is continuing under the Pooling and Servicing Agreement. |

| Consultation Termination Event: | Will occur when, without giving regard to the application of any Appraisal Reduction Amounts (i.e., giving effect to principal reduction through Realized Losses only), there is no Class of Control Eligible Certificates that has an aggregate Certificate Balance equal to 25% or more of the initial Certificate Balance of such Class. |

Upon the occurrence and continuance of a Consultation Termination Event, the Directing Holder will have no rights under the Pooling and Servicing Agreement other than those rights that all Certificateholders have. With respect to the Harmon Corner Loan Combination, the related Loan Combination Directing Holder will retain its control rights as specified under the related intercreditor agreement, without regard to whether a Consultation Termination Event has occurred and is continuing under the Pooling and Servicing Agreement. |

Appointment and Replacement of Special Servicer: | The Directing Holder will appoint the initial Special Servicer as of the Settlement Date. Prior to the occurrence and continuance of a Control Termination Event, the Special Servicer may generally be replaced at any time by the Directing Holder. |

| Upon the occurrence and during the continuance of a Control Termination Event, the Directing Holder will no longer have the right to replace the Special Servicer and such replacement will occur based on a vote of holders of all voting eligible Classes of Certificates as described below. |

Replacement of Special Servicer by Vote of Certificateholders: | Other than with respect to the Harmon Corner Loan Combination, if a Control Termination Event has occurred and is continuing, upon (i) the written direction of holders of Certificates evidencing not less than 25% of the voting rights of all Classes of Certificates entitled to principal (taking into account the application of Appraisal Reduction Amounts to notionally reduce the Certificate Balances of Classes to which such Appraisal Reduction Amounts are allocable) requesting a vote to replace the Special Servicer with a replacement Special Servicer, (ii) payment by such requesting holders to the Certificate Administrator of all reasonable fees and expenses to be incurred by the Certificate Administrator in connection with administering such vote and (iii) delivery by such holders to the Certificate Administrator of written confirmations from each Rating Agency that the appointment of the replacement Special Servicer will not result in a downgrade of the Certificates, the Certificate Administrator will be required to promptly provide written |

The depositor has filed a registration statement (including the prospectus) with the SEC (SEC File No. 333-184376) for the offering to which this communication relates. Before you invest, you should read the prospectus in the registration statement and other documents the depositor has filed with the SEC for more complete information about the depositor, the issuing trust and this offering. You may get these documents for free by visiting EDGAR on the SEC website at www.sec.gov. Alternatively, the depositor or Deutsche Bank Securities Inc., any other underwriter, or any dealer participating in this offering will arrange to send you the prospectus if you request it by calling toll-free 1-800-503-4611 or by email to the following address: prospectus.cpdg@db.com. The offered certificates referred to in these materials, and the asset pool backing them, are subject to modification or revision (including the possibility that one or more classes of certificates may be split, combined or eliminated at any time prior to issuance or availability of a final prospectus) and are offered on a “when, as and if issued” basis. You understand that, when you are considering the purchase of these certificates, a contract of sale will come into being no sooner than the date on which the relevant class has been priced and we have verified the allocation of certificates to be made to you; any “indications of interest” expressed by you, and any “soft circles” generated by us, will not create binding contractual obligations for you or us.

11

COMM 2013-LC6 Mortgage Trust |

| STRUCTURE OVERVIEW |

| notice to all certificateholders of such request and conduct the solicitation of votes of all Certificates in such regard. Upon the written direction (within 180 days) of (i) Holders of at least 75% of the aggregate voting rights of all Classes of Certificates entitled to principal (taking into account Realized Losses and the application of Appraisal Reduction Amounts to notionally reduce the Certificate Balances of Classes to which such Appraisal Reduction Amounts are allocable) or (ii) the Holders of more than 50% of the voting rights of each Class of Non–Reduced Certificates, the Trustee will immediately replace the Special Servicer with the replacement Special Servicer. In addition, after the occurrence of a Consultation Termination Event, if the Operating Advisor determines that the Special Servicer is not performing its duties in accordance with the Servicing Standard, the Operating Advisor will have the right to recommend the replacement of the Special Servicer. The Operating Advisor’s recommendation to replace the Special Servicer must be confirmed by a majority of the voting rights of all Classes of Certificates (taking into account the application of Appraisal Reduction Amounts to notionally reduce the Certificate Balances of Classes to which such Appraisal Reduction Amounts are allocable) within 180 days from the time such recommendation is posted to the Certificate Administrator website and is subject to the receipt of written confirmations from each Rating Agency that the appointment of the replacement Special Servicer will not result in a downgrade of the Certificates. With respect to the Harmon Corner Loan Combination, none of the Directing Holder, the Trustee or any Certificateholders will have the right to replace the special servicer. | |

Cap on Workout and Liquidation Fees: | The workout fees and liquidation fees payable to a Special Servicer will be an amount equal to the lesser of: (1) 1.0% of each collection of interest and principal following a workout or liquidation and (2) $1,000,000 per workout or liquidation. All Modification Fees actually paid to the Special Servicer in connection with a workout or liquidation or in connection with any prior workout or partial liquidation that occurred within the prior 18 months will be deducted from the total workout and/or liquidation fees payable (other than Modification Fees earned while the Mortgage Loan was not in special servicing). In addition, the total amount of workout and liquidation fees actually payable by the Trust will be capped in the aggregate at $1,000,000 for each Mortgage Loan. If a new special servicer begins servicing the Mortgage Loan, all amounts paid to the prior special servicer will be disregarded for purposes of calculating the cap. |

| Special Servicer Compensation: | The special servicing fee will equal 0.25% per annum of the stated principal balance of the related specially serviced loan or REO property. The Special Servicer and its affiliates will be prohibited from receiving or retaining any compensation or any other remuneration (including in the form of commissions, brokerage fees, rebates, or as a result of any other fee–sharing arrangement) from any person (including the issuing entity, any borrower, any manager, any guarantor or indemnitor in respect of a Mortgage Loan or Serviced Loan Combination, if any, and any purchaser of any Mortgage Loan, Serviced Companion Loan or REO Property) in connection with the disposition, workout or foreclosure of any Mortgage Loan or Serviced Loan Combination, the management or disposition of any REO Property, or the performance of any other special servicing duties under the Pooling and Servicing Agreement, other than as expressly permitted in the Pooling and Servicing Agreement and other than commercially reasonable treasury management fees, banking fees and insurance commissions or fees received or retained by the Special Servicer or any of its Affiliates in connection with any services performed by such party with respect to any mortgage loan. The Special Servicer will also be required to report any compensation or other remuneration the Special Servicer or its affiliates have received from any person and such information will be disclosed in the Certificateholders’ monthly distribution date statement. |

The depositor has filed a registration statement (including the prospectus) with the SEC (SEC File No. 333-184376) for the offering to which this communication relates. Before you invest, you should read the prospectus in the registration statement and other documents the depositor has filed with the SEC for more complete information about the depositor, the issuing trust and this offering. You may get these documents for free by visiting EDGAR on the SEC website at www.sec.gov. Alternatively, the depositor or Deutsche Bank Securities Inc., any other underwriter, or any dealer participating in this offering will arrange to send you the prospectus if you request it by calling toll-free 1-800-503-4611 or by email to the following address: prospectus.cpdg@db.com. The offered certificates referred to in these materials, and the asset pool backing them, are subject to modification or revision (including the possibility that one or more classes of certificates may be split, combined or eliminated at any time prior to issuance or availability of a final prospectus) and are offered on a “when, as and if issued” basis. You understand that, when you are considering the purchase of these certificates, a contract of sale will come into being no sooner than the date on which the relevant class has been priced and we have verified the allocation of certificates to be made to you; any “indications of interest” expressed by you, and any “soft circles” generated by us, will not create binding contractual obligations for you or us.

12

COMM 2013-LC6 Mortgage Trust |

| STRUCTURE OVERVIEW |

| Operating Advisor: | With respect to the Mortgage Loans and prior to the occurrence of a Control Termination Event, the Operating Advisor will have access to any final asset status report and all information available with respect to the transaction on the Certificate Administrator’s website but will not have any approval or consultation rights. After the occurrence and during the continuance of a Control Termination Event, the Operating Advisor will have consultation rights with respect to certain major decisions and will have additional monitoring responsibilities on behalf of the entire trust. The Operating Advisor will be subject to termination if holders of at least 15% of the aggregate voting rights of the Certificates (in connection with termination and replacement relating to the Mortgage Loans), vote to terminate and replace the Operating Advisor and such vote is approved by holders of more than 50% of the applicable voting rights that exercise their right to vote, provided that holders of at least 50% of the applicable voting rights have exercised their right to vote. The holders initiating such vote will be responsible for the fees and expenses in connection with the vote and replacement. The Operating Advisor will not have consultation rights in respect of the Harmon Corner Loan Combination. |

| Liquidated Loan Waterfall: | On liquidation of any Mortgage Loan, all net liquidation proceeds will be applied so that amounts allocated as a recovery of accrued and unpaid interest will not, in the first instance, include any amount by which the interest portion of P&I Advances previously made was reduced as a result of Appraisal Reduction Amounts. After the adjusted interest amount is so allocated, any remaining net liquidation proceeds will be allocated to pay principal on the Mortgage Loan until the unpaid principal amount of the Mortgage Loan has been reduced to zero. Any remaining liquidation proceeds would then be allocated as a recovery of accrued and unpaid interest corresponding to the amount by which the interest portion of P&I Advances previously made was reduced as a result of Appraisal Reduction Amounts. |

The depositor has filed a registration statement (including the prospectus) with the SEC (SEC File No. 333-184376) for the offering to which this communication relates. Before you invest, you should read the prospectus in the registration statement and other documents the depositor has filed with the SEC for more complete information about the depositor, the issuing trust and this offering. You may get these documents for free by visiting EDGAR on the SEC website at www.sec.gov. Alternatively, the depositor or Deutsche Bank Securities Inc., any other underwriter, or any dealer participating in this offering will arrange to send you the prospectus if you request it by calling toll-free 1-800-503-4611 or by email to the following address: prospectus.cpdg@db.com. The offered certificates referred to in these materials, and the asset pool backing them, are subject to modification or revision (including the possibility that one or more classes of certificates may be split, combined or eliminated at any time prior to issuance or availability of a final prospectus) and are offered on a “when, as and if issued” basis. You understand that, when you are considering the purchase of these certificates, a contract of sale will come into being no sooner than the date on which the relevant class has been priced and we have verified the allocation of certificates to be made to you; any “indications of interest” expressed by you, and any “soft circles” generated by us, will not create binding contractual obligations for you or us.

13

COMM 2013-LC6 Mortgage Trust |

OVERVIEW OF MORTGAGE POOL CHARACTERISTICS |

Distribution of Cut–off Date Balances(1) |

| Weighted Averages | ||||||||||||||

| Range of Cut–off Date Balances | Number of Mortgage Loans | Aggregate Cut–off Date Balance | % of Initial Outstanding Pool Balance | Mortgage Rate | Stated Remaining Term (Mos.)(2) | U/W NCF DSCR | Cut–off Date LTV Ratio | LTV Ratio at Maturity or ARD | ||||||

| $801,000 | - | $9,999,999 | 30 | $160,851,170 | 10.8% | 4.7301% | 116 | 1.72x | 66.3% | 53.8% | ||||

| $10,000,000 | - | $24,999,999 | 23 | $378,832,533 | 25.4% | 4.3674% | 107 | 1.79x | 62.8% | 53.4% | ||||

| $25,000,000 | - | $39,999,999 | 10 | $307,726,442 | 20.6% | 4.4123% | 116 | 1.82x | 60.0% | 48.3% | ||||

| $40,000,000 | - | $54,999,999 | 3 | $136,293,835 | 9.1% | 4.5921% | 98 | 1.87x | 59.0% | 49.8% | ||||

| $55,000,000 | - | $69,999,999 | 1 | $68,925,010 | 4.6% | 4.9040% | 119 | 1.67x | 54.7% | 44.9% | ||||

| $70,000,000 | - | $175,000,000 | 3 | $439,622,035 | 29.5% | 3.9048% | 101 | 1.93x | 58.7% | 52.3% | ||||

| Total/Weighted Average | 70 | $1,492,251,025 | 100.0% | 4.3248% | 108 | 1.83x | 60.7% | 51.4% | ||||||

Distribution of Mortgage Rates(1) |

| Range of Mortgage Rates | Number of Mortgage Loans | Aggregate Cut–off Date Balance | % of Initial Outstanding Pool Balance | Weighted Averages | ||||||||||

| Mortgage Rate | Stated Remaining Term (Mos.)(2) | U/W NCF DSCR | Cut–off Date LTV Ratio | LTV Ratio at Maturity or ARD | ||||||||||

| 3.6700% | - | 4.2499% | 22 | $843,620,571 | 56.5% | 3.9750% | 106 | 1.90x | 60.0% | 51.9% | ||||

| 4.2500% | - | 4.4999% | 13 | $174,307,000 | 11.7% | 4.2877% | 115 | 2.02x | 61.7% | 53.2% | ||||

| 4.5000% | - | 4.7499% | 10 | $136,390,086 | 9.1% | 4.6103% | 117 | 1.64x | 66.7% | 51.0% | ||||

| 4.7500% | - | 5.9180% | 25 | $337,933,368 | 22.6% | 5.1020% | 105 | 1.64x | 59.4% | 49.1% | ||||

| Total/Weighted Average | 70 | $1,492,251,025 | 100.0% | 4.3248% | 108 | 1.83x | 60.7% | 51.4% | ||||||

Property Type Distribution(1)(3) |

| Property Type | Number of Mortgaged Properties | Aggregate Cut–off Date Balance | % of Initial Outstanding Pool Balance | Number of Units, Rooms, Beds, Pads or NRA | Weighted Averages | ||||||||||||||||

Cut–off Date Balance per Unit/Room/ Bed/Pad/NRA | Mortgage Rate | Stated Remaining Term (Mos.)(2) | Occupancy | U/W NCF DSCR | Cut–off Date LTV Ratio | LTV Ratio at Maturity or ARD | |||||||||||||||

| Retail | 45 | $555,405,032 | 37.2% | 3,910,258 | $285 | 4.2043% | 117 | 96.8% | 1.92x | 59.2% | 49.1% | ||||||||||

Anchored(4) | 43 | $521,905,032 | 35.0% | 3,717,554 | $288 | 4.1925% | 117 | 96.9% | 1.86x | 60.1% | 49.8% | ||||||||||

| Unanchored | 2 | $33,500,000 | 2.2% | 192,704 | $245 | 4.3889% | 114 | 94.5% | 2.71x | 43.9% | 38.8% | ||||||||||

| Office | 8 | $400,883,439 | 26.9% | 2,583,768 | $282 | 4.0312% | 99 | 91.1% | 1.91x | 60.6% | 55.3% | ||||||||||

| Suburban | 5 | $223,313,956 | 15.0% | 1,319,633 | $308 | 4.0860% | 119 | 90.6% | 1.56x | 59.5% | 51.9% | ||||||||||

| CBD | 3 | $177,569,482 | 11.9% | 1,264,135 | $250 | 3.9623% | 74 | 91.6% | 2.35x | 61.9% | 59.7% | ||||||||||

| Hospitality | 28 | $276,441,771 | 18.5% | 4,197 | $99,982 | 4.7508% | 93 | 74.5% | 1.83x | 58.2% | 49.3% | ||||||||||

| Full Service | 7 | $191,304,073 | 12.8% | 1,730 | $122,603 | 4.7946% | 84 | 72.9% | 1.78x | 56.7% | 49.4% | ||||||||||

| Extended Stay | 15 | $52,100,000 | 3.5% | 1,989 | $31,491 | 4.4999% | 120 | 81.4% | 2.08x | 60.1% | 47.7% | ||||||||||

| Limited Service | 6 | $33,037,697 | 2.2% | 478 | $77,008 | 4.8934% | 105 | 73.3% | 1.72x | 64.2% | 51.2% | ||||||||||

| Multifamily | 12 | $152,703,296 | 10.2% | 4,367 | $43,478 | 4.2834% | 111 | 93.0% | 1.48x | 69.8% | 58.8% | ||||||||||

| Manufactured Housing Community | 4 | $71,817,488 | 4.8% | 2,441 | $29,491 | 4.6679% | 119 | 89.9% | 1.72x | 65.8% | 53.6% | ||||||||||

| Other | 1 | $30,300,000 | 2.0% | NAP | NAP | 5.9180% | 144 | 99.1% | 1.30x | 51.4% | 14.7% | ||||||||||

| Self Storage | 1 | $4,700,000 | 0.3% | 625 | $7,520 | 4.3635% | 120 | 83.5% | 1.64x | 72.3% | 58.2% | ||||||||||

| Total/Weighted Average | 99 | $1,492,251,025 | 100.0% | 4.3248% | 108 | 90.4% | 1.83x | 60.7% | 51.4% | ||||||||||||

Geographic Distribution(1)(3) |

| State/Location | Number of Mortgaged Properties | Aggregate Cut–off Date Balance | % of Initial Outstanding Pool Balance | Weighted Averages | ||||||||||||

| Mortgage Rate | Stated Remaining Term (Mos.)(2) | U/W NCF DSCR | Cut–off Date LTV Ratio | LTV Ratio at Maturity or ARD | ||||||||||||

| California | 9 | $333,269,482 | 22.3% | 4.2525% | 122 | 1.58x | 56.1% | 45.2% | ||||||||

Northern(5) | 3 | $214,469,482 | 14.4% | 4.0330% | 119 | 1.59x | 56.3% | 48.4% | ||||||||

Southern(5) | 6 | $118,800,000 | 8.0% | 4.6489% | 126 | 1.54x | 55.8% | 39.4% | ||||||||

| Florida | 8 | $261,418,113 | 17.5% | 4.3396% | 118 | 1.80x | 55.7% | 45.4% | ||||||||

| Illinois | 5 | $209,693,971 | 14.1% | 4.1916% | 67 | 2.27x | 62.2% | 59.3% | ||||||||

| Texas | 14 | $119,905,122 | 8.0% | 4.2056% | 105 | 2.14x | 64.6% | 56.6% | ||||||||

| New York | 8 | $83,650,374 | 5.6% | 4.7882% | 97 | 1.67x | 62.7% | 54.8% | ||||||||

| Other | 55 | $484,313,962 | 32.5% | 4.3736% | 113 | 1.78x | 64.5% | 53.5% | ||||||||

| Total/Weighted Average | 99 | $1,492,251,025 | 100.0% | 4.3248% | 108 | 1.83x | 60.7% | 51.4% | ||||||||

| (1) | With respect to the Moffett Towers loan, the 540 West Madison Street loan and the Harmon Corner loan, LTV, DSCR and Cut–off Date Balance per Unit/Room/Bed/Pad/NRA calculations include all related pari passu companion loans. With respect to a group of cross-defaulted and cross-collateralized mortgage loans, LTV, DSCR and Cut–off Date Balance per Unit/Room/Bed/Pad/NRA calculations are presented in the aggregate for those mortgage loans. |

| (2) | In the case of 13 Mortgage Loans with an Anticipated Repayment Date, Stated Remaining Term (Mos.) is through the related Anticipated Repayment Date. |

| (3) | Reflects allocated loan amount for properties securing multi–property Mortgage Loans. |

| (4) | Includes anchored and single tenant properties. |

| (5) | Northern California properties have a zip code greater than 93600. Southern California properties have a zip code less than or equal to 93600. |

The depositor has filed a registration statement (including the prospectus) with the SEC (SEC File No. 333-184376) for the offering to which this communication relates. Before you invest, you should read the prospectus in the registration statement and other documents the depositor has filed with the SEC for more complete information about the depositor, the issuing trust and this offering. You may get these documents for free by visiting EDGAR on the SEC website at www.sec.gov. Alternatively, the depositor or Deutsche Bank Securities Inc., any other underwriter, or any dealer participating in this offering will arrange to send you the prospectus if you request it by calling toll-free 1-800-503-4611 or by email to the following address: prospectus.cpdg@db.com. The offered certificates referred to in these materials, and the asset pool backing them, are subject to modification or revision (including the possibility that one or more classes of certificates may be split, combined or eliminated at any time prior to issuance or availability of a final prospectus) and are offered on a “when, as and if issued” basis. You understand that, when you are considering the purchase of these certificates, a contract of sale will come into being no sooner than the date on which the relevant class has been priced and we have verified the allocation of certificates to be made to you; any “indications of interest” expressed by you, and any “soft circles” generated by us, will not create binding contractual obligations for you or us.

14

COMM 2013-LC6 Mortgage Trust |

OVERVIEW OF MORTGAGE POOL CHARACTERISTICS |

Distribution of Cut–off Date LTV Ratios(1) |

| Range of Cut–off Date LTV Ratios | Number of Mortgage Loans | Aggregate Cut–off Date Balance | % of Initial Outstanding Pool Balance | Weighted Averages | ||||||||||||||

| Mortgage Rate | Stated Remaining Term (Mos.)(2) | U/W NCF DSCR | Cut–off Date LTV Ratio | LTV Ratio at Maturity or ARD | ||||||||||||||

| 37.5% | - | 49.9% | 3 | $68,951,825 | 4.6% | 4.5229% | 101 | 2.20x | 44.6% | 39.1% | ||||||||

| 50.0% | - | 54.9% | 7 | $220,921,731 | 14.8% | 4.6961% | 110 | 1.81x | 53.5% | 42.2% | ||||||||

| 55.0% | - | 59.9% | 10 | $456,611,924 | 30.6% | 3.9794% | 116 | 1.83x | 56.8% | 47.7% | ||||||||

| 60.0% | - | 64.9% | 18 | $305,388,887 | 20.5% | 4.3216% | 89 | 2.14x | 62.6% | 58.1% | ||||||||

| 65.0% | - | 69.9% | 18 | $253,760,011 | 17.0% | 4.3852% | 111 | 1.64x | 66.9% | 54.1% | ||||||||

| 70.0% | - | 76.1% | 14 | $186,616,648 | 12.5% | 4.5799% | 115 | 1.47x | 73.0% | 61.0% | ||||||||

| Total/Weighted Average | 70 | $1,492,251,025 | 100.0% | 4.3248% | 108 | 1.83x | 60.7% | 51.4% | ||||||||||

Distribution of LTV Ratios at Maturity or ARD(1) |

Range of LTV Ratios at Maturity or ARD | Number of Mortgage Loans | Aggregate Cut–off Date Balance | % of Initial Outstanding Pool Balance | Weighted Averages | ||||||||||||||

| Mortgage Rate | Stated Remaining Term (Mos.)(2) | U/W NCF DSCR | Cut–off Date LTV Ratio | LTV Ratio at Maturity or ARD | ||||||||||||||

| 0.3% | - | 49.9% | 22 | $576,761,112 | 38.7% | 4.4019% | 113 | 1.76x | 55.3% | 42.3% | ||||||||

| 50.0% | - | 54.9% | 13 | $368,678,453 | 24.7% | 4.2452% | 114 | 1.72x | 60.8% | 51.8% | ||||||||

| 55.0% | - | 59.9% | 18 | $221,425,679 | 14.8% | 4.3165% | 115 | 1.86x | 65.4% | 56.9% | ||||||||

| 60.0% | - | 70.8% | 17 | $325,385,782 | 21.8% | 4.2840% | 86 | 2.07x | 66.8% | 63.1% | ||||||||

| Total/Weighted Average | 70 | $1,492,251,025 | 100.0% | 4.3248% | 108 | 1.83x | 60.7% | 51.4% | ||||||||||

Distribution of Underwritten NCF Debt Service Coverage Ratios(1) |

| Range of Underwritten NCF Debt Service Coverage Ratios | Number of Mortgage Loans | Aggregate Cut–off Date Balance | % of Initial Outstanding Pool Balance | Weighted Averages | ||||||||||||||

| Mortgage Rate | Stated Remaining Term (Mos.)(2) | U/W NCF DSCR | Cut–off Date LTV Ratio | LTV Ratio at Maturity or ARD | ||||||||||||||

| 1.01x | - | 1.10x | 1 | $6,095,191 | 0.4% | 4.5000% | 119 | 1.01x | 55.4% | 0.3% | ||||||||

| 1.11x | - | 1.20x | 1 | $15,725,000 | 1.1% | 4.0310% | 120 | 1.20x | 65.8% | 26.8% | ||||||||

| 1.21x | - | 1.30x | 3 | $65,118,616 | 4.4% | 5.7076% | 130 | 1.28x | 63.6% | 40.3% | ||||||||

| 1.31x | - | 1.40x | 5 | $44,502,302 | 3.0% | 4.6056% | 119 | 1.36x | 69.2% | 58.5% | ||||||||

| 1.41x | - | 1.50x | 7 | $110,603,296 | 7.4% | 4.4447% | 107 | 1.44x | 68.5% | 56.8% | ||||||||

| 1.51x | - | 1.99x | 34 | $878,006,106 | 58.8% | 4.2913% | 111 | 1.67x | 59.7% | 49.9% | ||||||||

| 2.00x | - | 3.33x | 19 | $372,200,513 | 24.9% | 4.1021% | 95 | 2.53x | 59.0% | 56.1% | ||||||||

| Total/Weighted Average | 70 | $1,492,251,025 | 100.0% | 4.3248% | 108 | 1.83x | 60.7% | 51.4% | ||||||||||

Distribution of Original Terms to Maturity or ARD(1) |

Range of Original Terms to Maturity or ARD | Number of Mortgage Loans | Aggregate Cut–off Date Balance | % of Initial Outstanding Pool Balance | Weighted Averages | ||||||||||||

| Mortgage Rate | Stated Remaining Term (Mos.)(2) | U/W NCF DSCR | Cut–off Date LTV Ratio | LTV Ratio at Maturity or ARD | ||||||||||||

| 60 | 10 | $297,160,926 | 19.9% | 4.2701% | 60 | 2.24x | 61.0% | 58.5% | ||||||||

| 120 | 59 | $1,164,790,099 | 78.1% | 4.2973% | 119 | 1.74x | 60.8% | 50.5% | ||||||||

| 144 | 1 | $30,300,000 | 20.0% | 5.9180% | 144 | 1.30x | 51.4% | 14.7% | ||||||||

| Total/Weighted Average | 70 | $1,492,251,025 | 100.0% | 4.3248% | 108 | 1.83x | 60.7% | 51.4% | ||||||||

Distribution of Remaining Terms to Maturity or ARD(1) |

Range of Remaining Terms to Maturity or ARD | Number of Mortgage Loans | Aggregate Cut–off Date Balance | % of Initial Outstanding Pool Balance | Weighted Averages | ||||||||||||||

| Mortgage Rate | Stated Remaining Term (Mos.)(2) | U/W NCF DSCR | Cut–off Date LTV Ratio | LTV Ratio at Maturity or ARD | ||||||||||||||

| 59 | - | 60 | 10 | $297,160,926 | 19.9% | 4.2701% | 60 | 2.24x | 61.0% | 58.5% | ||||||||

| 112 | - | 120 | 59 | $1,164,790,099 | 78.1% | 4.2973% | 119 | 1.74x | 60.8% | 50.5% | ||||||||

| 144 | - | 144 | 1 | $30,300,000 | 20.0% | 5.9180% | 144 | 1.30x | 51.4% | 14.7% | ||||||||

| Total/Weighted Average | 70 | $1,492,251,025 | 100.0% | 4.3248% | 108 | 1.83x | 60.7% | 51.4% | ||||||||||

| (1) | With respect to the Moffett Towers loan, the 540 West Madison Street loan and the Harmon Corner loan, LTV, DSCR and Cut–off Date Balance per Unit/Room/Bed/Pad/NRA calculations include all related pari passu companion loans. With respect to a group of cross-defaulted and cross-collateralized mortgage loans, LTV, DSCR and Cut–off Date Balance per Unit/Room/Bed/Pad/NRA calculations are presented in the aggregate for those mortgage loans. |

| (2) | In the case of 13 Mortgage Loans with an Anticipated Repayment Date, Stated Remaining Term (Mos.) is through the related Anticipated Repayment Date. |