| FREE WRITING PROSPECTUS | ||

| FILED PURSUANT TO RULE 433 | ||

| �� | REGISTRATION FILE NO.: 333-226943-06 | |

January 21, 2020

FREE WRITING PROSPECTUS

STRUCTURAL AND COLLATERAL TERM SHEET

$899,096,873

(Approximate Total Mortgage Pool Balance)

$762,321,000

(Approximate Offered Certificates)

BENCHMARK 2020-B16 |

Deutsche Mortgage & Asset Receiving Corporation

Depositor

German American Capital Corporation

JPMorgan Chase Bank, National Association

Citi Real Estate Funding Inc.

Sponsors and Mortgage Loan Sellers

| Deutsche Bank Securities | Citigroup | J.P. Morgan |

| Co-Lead Managers and Joint Bookrunners | ||

| Academy Securities | Drexel Hamilton |

| Co-Managers | |

The depositor has filed a registration statement (including the prospectus) with the Securities and Exchange Commission (File No. 333-226943) for the offering to which this communication relates. Before you invest, you should read the prospectus in the registration statement and other documents the depositor has filed with the Securities and Exchange Commission for more complete information about the depositor, the issuing entity and this offering. You may get these documents for free by visiting EDGAR on the Securities and Exchange Commission website at www.sec.gov. Alternatively, the depositor or Deutsche Bank Securities Inc., any other underwriter, or any dealer participating in this offering will arrange to send you the prospectus if you request it by calling toll-free 1-800-503-4611 or by emailing: prospectus.cpdg@db.com. The offered certificates referred to in these materials, and the asset pool backing them, are subject to modification or revision (including the possibility that one or more classes of certificates may be split, combined or eliminated at any time prior to issuance or availability of a final prospectus) and are offered on a “when, as and if issued” basis. You understand that, when you are considering the purchase of these certificates, a contract of sale will come into being no sooner than the date on which the relevant class has been priced and we have verified the allocation of certificates to be made to you; any “indications of interest” expressed by you, and any “soft circles” generated by us, will not create binding contractual obligations for you or us. This free writing prospectus does not contain all information that is required to be included in the prospectus.

| Capitalized terms used but not defined herein have the meanings assigned to them in the Preliminary Prospectus expected to be dated January 21, 2020 relating to the offered certificates (hereinafter referred to as the “Preliminary Prospectus”). |

| KEY FEATURES OF SECURITIZATION |

| Offering Terms: | ||

| Co-Lead Managers and Joint Bookrunners: | Deutsche Bank Securities Inc., J.P. Morgan Securities LLC and Citigroup Global Markets Inc. | |

| Co-Managers: | Academy Securities, Inc. and Drexel Hamilton, LLC | |

| Sponsors and Mortgage Loan Sellers: | German American Capital Corporation* (“GACC”) (27.5%), JPMorgan Chase Bank, National Association (“JPMCB”) (45.2%) and Citi Real Estate Funding Inc. (“CREFI”) (27.2%)*An indirect wholly owned subsidiary of Deutsche Bank AG | |

| Master Servicer: | Midland Loan Services, a Division of PNC Bank, National Association | |

| Operating Advisor: | Park Bridge Lender Services LLC | |

| Asset Representations Reviewer: | Park Bridge Lender Services LLC | |

| Special Servicer: | KeyBank National Association | |

| Certificate Administrator: | Wells Fargo Bank, National Association | |

| Trustee: | Wells Fargo Bank, National Association | |

| Rating Agencies: | Fitch Ratings, Inc. (“Fitch”), Kroll Bond Rating Agency, Inc. (“KBRA”), and Moody’s Investors Service, Inc. (“Moody’s”). | |

| Credit Risk Retention: | For a discussion on the manner in which the U.S. credit risk retention requirements are being satisfied by GACC, as retaining sponsor, see “Credit Risk Retention” in the Preliminary Prospectus. Note that this securitization transaction is not being structured to satisfy EU risk retention and due diligence requirements. | |

| Determination Date: | 11thday of each month, or if such 11th day is not a business day, the immediately following business day, commencing in March 2020. | |

| Distribution Date: | 4thbusiness day following the Determination Date in each month, commencing in March 2020. | |

| Cut-off Date: | With respect to each mortgage loan, the later of the related payment date of such mortgage loan in February 2020 (or, in the case of any mortgage loan that has its first due date subsequent to February 2020, the date that would have been its due date in February 2020 under the terms of that mortgage loan if a monthly payment were scheduled to be due in that month) and the date of origination of such mortgage loan. Unless otherwise noted, all mortgage loan statistics are based on balances as of the Cut-off Date. | |

| Closing Date: | On or about February 12, 2020 | |

| Settlement Terms: | DTC, Euroclear and Clearstream, same day funds, with accrued interest. | |

| ERISA Eligible: | All of the Offered Certificates are expected to be ERISA eligible. | |

| SMMEA Eligible: | None of the Offered Certificates will be SMMEA eligible. | |

| Day Count: | 30/360 | |

| Tax Treatment: | REMIC | |

| Rated Final Distribution Date: | February 2053 | |

| Minimum Denominations: | $10,000 (for each class of offered principal balance certificates) and $100,000 (for each class of offered interest-only certificates) and in each case in multiples of $1 thereafter. | |

| Clean-up Call: | 1% (with certain exceptions described under“Pooling and Servicing Agreement—Termination; Retirement of Certificates”in the Preliminary Prospectus) | |

| Distribution of Collateral by Property Type |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

2

| TRANSACTION HIGHLIGHTS |

| Mortgage Loan Sellers | Number of Mortgage Loans | Number of Mortgaged Properties | Aggregate Cut-off Date Balance | % of Initial Outstanding Pool Balance |

| German American Capital Corporation | 7 | 39 | $225,200,000 | 25.0% |

| JPMorgan Chase Bank, National Association | 13 | 14 | $354,301,873 | 39.4% |

| Citi Real Estate Funding Inc. | 11 | 22 | $214,595,000 | 23.9% |

| JPMorgan Chase Bank, National Association/Citi Real Estate Funding Inc.(1) | 1 | 1 | $60,000,000 | 6.7% |

| German American Capital Corporation/JPMorgan Chase Bank, National Association(2) | 1 | 1 | $45,000,000 | 5.0% |

| Total: | 33 | 77 | $899,096,873 | 100.0% |

Collateral Facts | ||||

| Initial Outstanding Pool Balance: | $899,096,873 | |||

| Number of Mortgage Loans: | 33 | |||

| Number of Mortgaged Properties: | 77 | |||

| Average Mortgage Loan Cut-off Date Balance: | $27,245,360 | |||

| Weighted Average Mortgage Rate: | 3.6060% | |||

| Weighted Average Mortgage Loan Original Term to Maturity Date or ARD (months): | 118 | |||

| Weighted Average Mortgage Loan Remaining Term to Maturity Date or ARD (months): | 116 | |||

| Weighted Average Mortgage Loan Seasoning (months): | 1 | |||

| % of Mortgaged Properties Leased to a Single Tenant: | 18.9% | |||

Credit Statistics(3) | ||||

| Weighted Average Mortgage Loan U/W NCF DSCR: | 3.20x | |||

| Weighted Average Mortgage Loan Cut-off Date LTV(4)(5): | 52.8% | |||

| Weighted Average Mortgage Loan Maturity Date or ARD LTV(4): | 51.9% | |||

| Weighted Average U/W NOI Debt Yield(5): | 12.1% | |||

Amortization Overview | ||||

| % Mortgage Loans with Amortization through Maturity Date or ARD: | 3.8% | |||

| % Mortgage Loans which pay Interest Only through Maturity or ARD Date: | 88.6% | |||

| % Mortgage Loans which pay Interest Only followed by Amortization through Maturity Date or ARD: | 7.5% | |||

| Weighted Average Remaining Amortization Term (months)(6): | 360 | |||

Amortization Overview | ||||

| % Mortgage Loans with Upfront or Ongoing Tax Reserves: | 38.0% | |||

| % Mortgage Loans with Upfront or Ongoing Replacement Reserves(7): | 37.4% | |||

| % Mortgage Loans with Upfront or Ongoing Insurance Reserves: | 25.1% | |||

| % Mortgage Loans with Upfront or Ongoing TI/LC Reserves(8): | 44.1% | |||

| % Mortgage Loans with In Place Hard Lockboxes: | 73.1% | |||

| % Mortgage Loans with Cash Traps Triggered at DSCR Levels ≥ 1.10x: | 67.6% | |||

| % Mortgage Loans with Cash Traps Triggered at Debt Yield Levels ≥ 5.75%: | 32.4% | |||

| Prepayment Provisions | ||||

| % Mortgage Loans with Defeasance Only After a Lockout Period and Prior to an Open Period: | 59.7% | |||

| % Mortgage Loans with Prepayment Only After a Lockout Period and Prior to an Open Period with a Yield Maintenance Charge: | 23.2% | |||

| % Mortgage Loans with Prepayment with Yield Maintenance Charge or with Defeasance or Yield Maintenance Charge Prior to an Open Period: | 10.6% | |||

| % Mortgage Loans with Prepayment Only After a Lockout Period and Prior to an Open Period with Defeasance or a Yield Maintenance Charge: | 6.6% | |||

| (1) | Includes the $60.0 millionpari passu portion of the Bellagio Hotel and Casino mortgage loan, as to which JPMCB is acting as mortgage loan seller of the $30.0 million Note A-3-C2 and CREFI is acting as the mortgage loan seller of the $30.0 million Note A-2-C2. |

| (2) | Includes the $45.0 millionpari passu portion of the 1633 Broadway mortgage loan, as to which GACC is acting as mortgage loan seller of the $22.5 million Note A-2-C-1-B and JPMCB is acting as the mortgage loan seller of the $22.5 million Note A-3-C-1-B. |

| (3) | The LTV, DSCR and Debt Yield calculations include any relatedpari passu companion loan(s) and exclude any related subordinate companion loan(s) and/or mezzanine loan(s). |

| (4) | With respect to 5 mortgage loans (18.1%) (including Bellagio Hotel and Casino, 650 Madison Avenue, 181 West Madison, Fairfield Inn & Suites Spokane and Springhill Suites Florence), the Cut-off Date LTV and Maturity Date or ARD LTV have been calculated using a value other than the “As Is” appraised values. For additional information please see the footnotes to Annex A-1 in the Preliminary Prospectus. |

| (5) | With respect to the Landing Square mortgage loan (4.0%) the Cut-off Date LTV and U/W NOI Debt Yield is calculated based on the Cut-off Date Balance net of a capex holdback reserve. |

| (6) | Excludes mortgage loans which are interest only for the full loan term. |

| (7) | Includes FF&E reserves. |

| (8) | Represents the percent of the allocated Initial Outstanding Pool Balance of office, retail and mixed use properties only structured with TI/LC reserves. |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

3

Benchmark 2020-B16 Mortgage Trust |

| STRUCTURE SUMMARY |

OFFERED CERTIFICATES

| Class(1) | Ratings (Moody’s/Fitch/KBRA) | Initial Certificate Balance or Notional | Initial Subordination | Weighted (years)(4) | Principal (months)(4) | Certificate Principal to Value Ratio(5) | Certificate NOI Debt Yield(6) | |

| Class A-1 | Aaa(sf)/AAAsf/AAA(sf) | $4,592,000 | 30.000%(7) | 3.07 | 1 – 58 | 37.0% | 17.3% | |

| Class A-2 | Aaa(sf)/AAAsf/AAA(sf) | $10,098,000 | 30.000%(7) | 4.84 | 58 – 58 | 37.0% | 17.3% | |

| Class A-3 | Aaa(sf)/AAAsf/AAA(sf) | $40,849,000 | 30.000%(7) | 6.84 | 82 – 82 | 37.0% | 17.3% | |

| Class A-SB | Aaa(sf)/AAAsf/AAA(sf) | $9,800,000 | 30.000%(7) | 7.47 | 58 – 118 | 37.0% | 17.3% | |

| Class A-4 | Aaa(sf)/AAAsf/AAA(sf) | (8) | 30.000%(7) | (8) | (8) | 37.0% | 17.3% | |

| Class A-5 | Aaa(sf)/AAAsf/AAA(sf) | (8) | 30.000%(7) | (8) | (8) | 37.0% | 17.3% | |

| Class X-A(9) | Aa1(sf)/AAAsf/AAA(sf) | $691,854,000(10) | N/A | N/A | N/A | N/A | N/A | |

| Class A-M | Aa2(sf)/AAAsf/AAA(sf) | $93,955,000 | 19.000% | 9.93 | 119 – 119 | 42.8% | 14.9% | |

| Class B | NR/AA-sf/AA(sf) | $36,301,000 | 14.750% | 9.93 | 119 – 119 | 45.0% | 14.2% | |

| Class C | NR/A-sf/A-(sf) | $34,166,000 | 10.750% | 9.93 | 119 – 119 | 47.1% | 13.6% | |

NON-OFFERED CERTIFICATES

| Class(1) | Ratings (Moody’s/Fitch/KBRA) | Initial Certificate Balance or Notional | Initial Subordination | Weighted Average Life | Principal (months)(4) | Certificate Principal to Value Ratio(5) | Certificate NOI Debt Yield(6) | |

| Class X-B(9) | NR/A-sf/AAA(sf) | $70,467,000(10) | N/A | N/A | N/A | N/A | N/A | |

| Class X-D(9) | NR/BBB-sf/BBB-(sf) | $40,572,000(10) | N/A | N/A | N/A | N/A | N/A | |

| Class X-F(9) | NR/BB-sf/BB-(sf) | $16,015,000(10) | N/A | N/A | N/A | N/A | N/A | |

| Class X-G(9) | NR/B-sf/B-(sf) | $8,541,000(10) | N/A | N/A | N/A | N/A | N/A | |

| Class X-H(9) | NR/NR/NR | $26,692,872(10) | N/A | N/A | N/A | N/A | N/A | |

| Class D | NR/BBBsf/BBB+(sf) | $23,489,000 | 8.000% | 9.93 | 119 – 119 | 48.6% | 13.2% | |

| Class E | NR/BBB-sf/BBB-(sf) | $17,083,000 | 6.000% | 9.98 | 119 – 120 | 49.6% | 12.9% | |

| Class F | NR/BB-sf/BB-(sf) | $16,015,000 | 4.125% | 10.01 | 120 – 120 | 50.6% | 12.6% | |

| Class G | NR/B-sf/B(sf) | $8,541,000 | 3.125% | 10.01 | 120 – 120 | 51.1% | 12.5% | |

| Class H | NR/NR/NR | $26,692,872 | 0.000% | 10.01 | 120 – 120 | 52.8% | 12.1% | |

NON-OFFERED VERTICAL RISK RETENTION INTEREST

| Non-Offered Vertical Risk Retention Interest | Ratings (Moody’s/Fitch/KBRA) | Initial Certificate Balance or Notional | Initial Subordination | Weighted Average Life | Principal (months)(11) | Certificate Principal to Value Ratio | Certificate NOI Debt Yield |

| VRR Interest(12)(13) | NR/NR/NR | $44,955,000 | N/A | 9.62 | 1 - 120 | N/A | N/A |

| (1) | The pass-through rates for the Class A-1, Class A-2, Class A-3, Class A-SB, Class A-4, Class A-5, Class A-M, Class B, Class C, Class D, Class E, Class F, Class G and Class H certificates (collectively, the “Principal Balance Certificates”) in each case, will be one of: (i) a fixedper annum rate, (ii) the weighted average of the net mortgage rates on the mortgage loans (in each case, adjusted, if necessary, to accrue on the basis of a 360-day year consisting of twelve 30-day months) as of their respective due dates in the month preceding the month in which such Distribution Date occurs (the “WAC Rate”), (iii) a rate equal to the lesser of a specified pass-through rate and the WAC Rate or (iv) the WAC Rate less a specified rate. |

| (2) | Approximate; subject to a permitted variance of plus or minus 5%. The Certificate Balance of the VRR Interest is not included in the Certificate Balance or Notional Amount of any Class of Certificates set forth under “Offered Certificates” or “Non-Offered Certificates” in the table above. |

| (3) | The initial subordination levels are calculated based on the initial Certificate Balance. The approximate initial credit support percentages shown in the table above do not take into account the VRR Interest. However, losses incurred on the mortgage loans will be allocated between the VRR Interest and the Principal Balance Certificates,pro ratain accordance with their respective outstanding Certificate Balances. See “Credit Risk Retention” and “Description of the Certificates” in the Preliminary Prospectus. |

| (4) | The weighted average life and principal window during which distributions of principal would be received as set forth in the table with respect to each class of Principal Balance Certificates are based on (i) modeling assumptions described in the Preliminary Prospectus and (ii) assumptions that there are no prepayments, modifications or losses in respect of the mortgage loans and there are no extensions or forbearances of maturity dates of the mortgage loans. The weighted average life and principal window of the Class A-4 and Class A-5 certificates are subject to change as described in footnote (8) below. |

| (5) | “Certificate Principal to Value Ratio” for any class of Principal Balance Certificates is calculated as the product of (a) the weighted average mortgage loan Cut-off Date LTV of the mortgage loans, multiplied by (b) a fraction, the numerator of which is the total initial Certificate Balance of the related class of Principal Balance Certificates and all other classes of Principal Balance Certificates, if any, that are senior to such class, and the denominator of which is the total initial Certificate Balance of all classes of Principal Balance Certificates. The Certificate Principal to Value Ratios of the Class A-1, Class A-2, Class A-3, Class A-SB, Class A-4 and Class A-5 certificates are calculated in the aggregate for those classes as if they were a single class. |

| (6) | “Certificate Underwritten NOI Debt Yield” for any class of Principal Balance Certificates is calculated as the product of (a) the weighted average Underwritten NOI Debt Yield for the mortgage loans, multiplied by (b) a fraction, the numerator of which is the total initial Certificate Balance of all classes of Principal Balance Certificates and the denominator of which is the total initial Certificate Balance of such class of Principal Balance Certificates and all other classes of Principal Balance Certificates, if any, that are senior to such class. The Underwritten NOI Debt Yields of the Class A-1, Class A-2, Class A-3, Class A-SB, Class A-4 and Class A-5 certificates are calculated in the aggregate for those classes as if they were a single class. |

| (7) | The initial subordination levels for the Class A-1, Class A-2, Class A-3, Class A-SB, Class A-4 and Class A-5 certificates are represented in the aggregate. |

| (8) | The exact initial Certificate Balances of the Class A-4 and Class A-5 certificates are unknown and will be determined based on the final pricing of those classes of certificates. However, the respective initial Certificate Balances, weighted average lives and principal windows of the Class A-4 and Class A-5 certificates are expected to be within the applicable ranges reflected in the following chart. The aggregate initial Certificate Balance of the Class A-4 and Class A-5 certificates is expected to be approximately $532,560,000, subject to a variance of plus or minus 5.0%. |

| Class of Certificates | Expected Range of Initial Certificate Balance | Expected Range of Weighted Avg. Life (years)(4) | Expected Range of Principal Window (months)(4) | |||

| Class A-4 | $0 - $266,000,000 | NAP - 9.84 | NAP / 118-118 | |||

| Class A-5 | $266,560,000 - $532,560,000 | 9.87 - 9.86 | 118-119 / 118-119 |

| (9) | As further described in the Preliminary Prospectus, the pass-through rate applicable to the Class X-A, Class X-B, Class X-D, Class X-F, Class X-G and Class X-H certificates (collectively, the “Class X Certificates” and, together with the Principal Balance Certificates, the “Regular Certificates”) for each Distribution Date will generally be equal to the excess of (i) the WAC Rate over (ii)(A) with respect to the Class X-A certificates, the weighted average of the pass-through rates of the Class A-1, Class A-2, Class A-3, Class A-SB, Class A-4, Class A-5 and Class A-M certificates (based on their respective Certificate Balances immediately prior to such Distribution Date), (B) with respect to the Class X-B certificates, the weighted average of the pass-through rates of the Class B and Class C certificates (based on their respective Certificate Balances immediately prior to such Distribution Date), (C) with respect to the Class X-D certificates, the weighted average of the pass-through rates of the Class D and Class E certificates (based on their respective Certificate Balances immediately prior to such Distribution Date), (D) with respect to the Class X-F certificates, the pass-through rate of the Class F certificates, (E) with respect to the Class X-G certificates, the pass-through rate of the Class G certificates and (F) with respect to the Class X-H certificates, the pass-through rate of the Class H certificates. |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

4

Benchmark 2020-B16 Mortgage Trust |

| STRUCTURE SUMMARY |

| (10) | The Class X Certificates will not have Certificate Balances. None of the Class X Certificates will be entitled to distributions of principal. The interest accrual amounts on the Class X-A certificates will be calculated by reference to a notional amount equal to the aggregate Certificate Balances of the Class A-1, Class A-2, Class A-3, Class A-SB, Class A-4, Class A-5 and Class A-M certificates. The interest accrual amounts on the Class X-B certificates will be calculated by reference to a notional amount equal to the aggregate Certificate Balances of the Class B and Class C certificates. The interest accrual amounts on the Class X-D certificates will be calculated by reference to a notional amount equal to the aggregate Certificate Balances of the Class D and Class E certificates. The interest accrual amounts on the Class X-F certificates will be calculated by reference to a notional amount equal to the Certificate Balance of the Class F certificates. The interest accrual amounts on the Class X-G certificates will be calculated by reference to a notional amount equal to the Certificate Balance of the Class G certificates. The interest accrual amounts on the Class X-H certificates will be calculated by reference to a notional amount equal to the Certificate Balance of the Class H certificates. The notional amount of each class of Class X Certificates is subject to change depending upon the final pricing of the Principal Balance Certificates, as follows: (1) if as a result of such pricing the pass-through rate of any class of Principal Balance Certificates whose Certificate Balance comprises such notional amount is equal to the WAC Rate, the Certificate Balance of such class of Principal Balance Certificates may not be part of, and will reduce accordingly, such notional amount of such class of Class X Certificates (or, if as a result of such pricing the pass-through rate of such class of Class X Certificates is equal to zero, such class of Class X Certificates may not be issued on the Closing Date), and/or (2) if as a result of such pricing the pass-through rate of any class of Principal Balance Certificates that does not comprise such notional amount of such class of Class X Certificates is less than the WAC Rate, such class of Principal Balance Certificates may become a part of, and will increase accordingly, such notional amount of such class of Class X Certificates. |

| (11) | The weighted average life and principal window during which distributions of principal would be received as set forth in the foregoing table with respect to the VRR Interest (as defined below) are based on the assumptions set forth under “Yield and Maturity Considerations—Weighted Average Life” in the Preliminary Prospectus and on the assumptions that there are no prepayments, modifications or losses in respect of the mortgage loans and that there are no extensions or forbearances of maturity dates of the mortgage loans. |

| (12) | German American Capital Corporation, as the retaining sponsor, is expected to acquire from the depositor, on the Closing Date, an “eligible vertical interest” (as defined in Regulation RR) in the form of a single vertical security (the “VRR Interest”), representing approximately 5% of all classes of Principal Balance Certificates and the VRR Interest. The VRR Interest will be retained by certain retaining parties in accordance with the credit risk retention rules applicable to this securitization transaction. See “Credit Risk Retention” in the Preliminary Prospectus. The VRR Interest is a class of Certificates. |

| (13) | Although it does not have a specified pass-through rate (other than for tax reporting purposes), the effective interest rate for the VRR Interest will be the WAC rate. |

| Class A-2 Principal Paydown(1) |

| Class | Mortgage Loan Seller | Mortgage Loan | Property Type | Cut-off Date Balance | Remaining Term to Maturity (Mos.) | Cut-off Date LTV Ratio | U/W NCF DSCR | U/W NOI Debt Yield | |

| A-2 | JPMCB | 300-314 North College Street | Retail | $10,630,000 | 58 | 67.5% | 2.07x | 9.3% | |

| (1) | This table reflects the mortgage loans whose balloon payments will be applied to pay down the Class A-2 certificates, assuming (i) that none of the mortgage loans experience prepayments, defaults or losses, (ii) there are no extensions of maturity dates and (iii) each mortgage loan is paid in full on its stated maturity date. See “Yield and Maturity Considerations—Yield Considerations” in the Preliminary Prospectus. |

| Class A-3 Principal Paydown(1) |

| Class | Mortgage Loan Seller | Mortgage Loan | Property Type | Cut-off Date Balance | Remaining Term to Maturity (Mos.) | Cut-off Date LTV Ratio | U/W NCF DSCR | U/W NOI Debt Yield | |

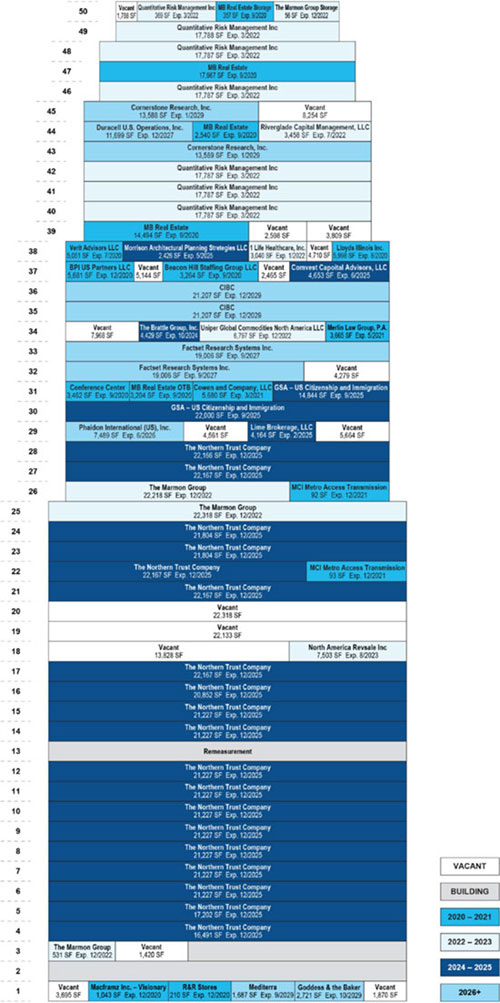

| A-3 | JPMCB | 181 West Madison | Office | $43,000,000 | 82 | 28.8% | 4.67x | 20.4% | |

| (1) | This table reflects the mortgage loans whose balloon payments will be applied to pay down the Class A-3 certificates, assuming (i) that none of the mortgage loans experience prepayments, defaults or losses, (ii) there are no extensions of maturity dates and (iii) each mortgage loan is paid in full on its stated maturity date. See “Yield and Maturity Considerations—Yield Considerations” in the Preliminary Prospectus. |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

5

Benchmark 2020-B16 Mortgage Trust

|

| OVERVIEW OF MORTGAGE POOL CHARACTERISTICS |

| Ten Largest Mortgage Loans | |||||||||

| Mortgage Loan | Mortgage Loan Seller | City, State | Property Type | Mortgage Loan Cut-off Date | % of Initial Outstanding Pool Balance | Cut-off Date Balance per NRA/Room(1) | Cut-off Date LTV(1)(2) | U/W NCF DSCR after | U/W NOI Debt Yield(1) |

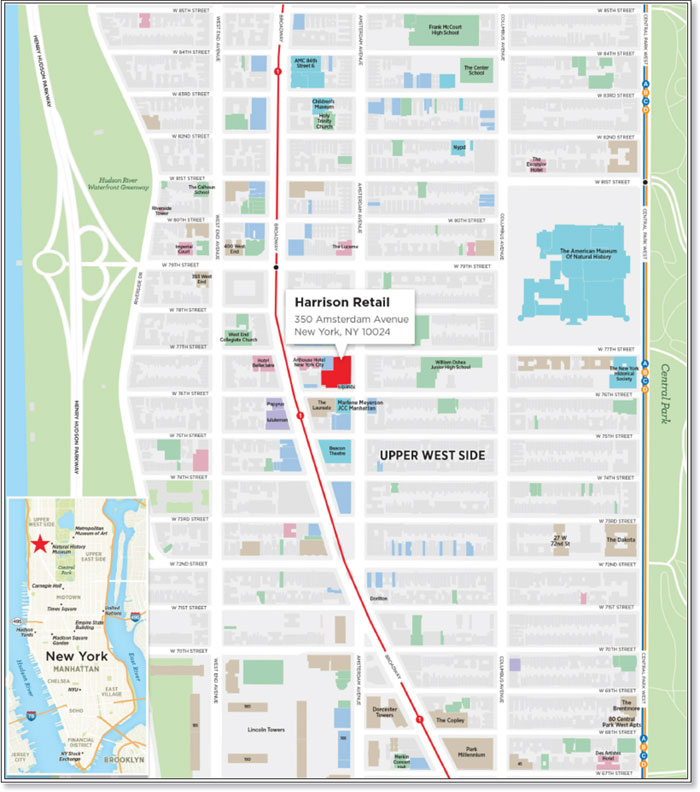

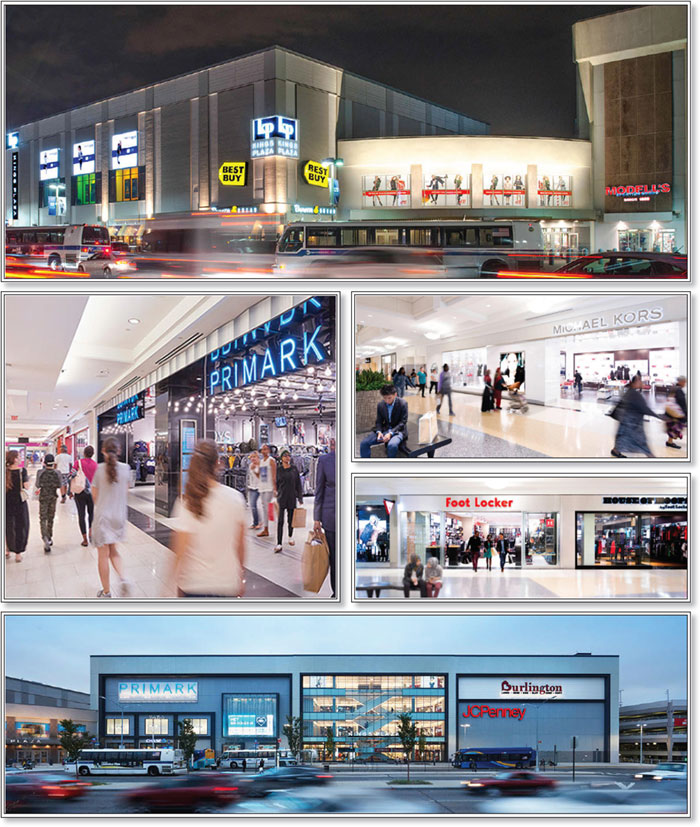

| Harrison Retail | GACC | New York, NY | Retail | $65,000,000 | 7.2% | $737 | 65.0% | 2.20x | 8.2% |

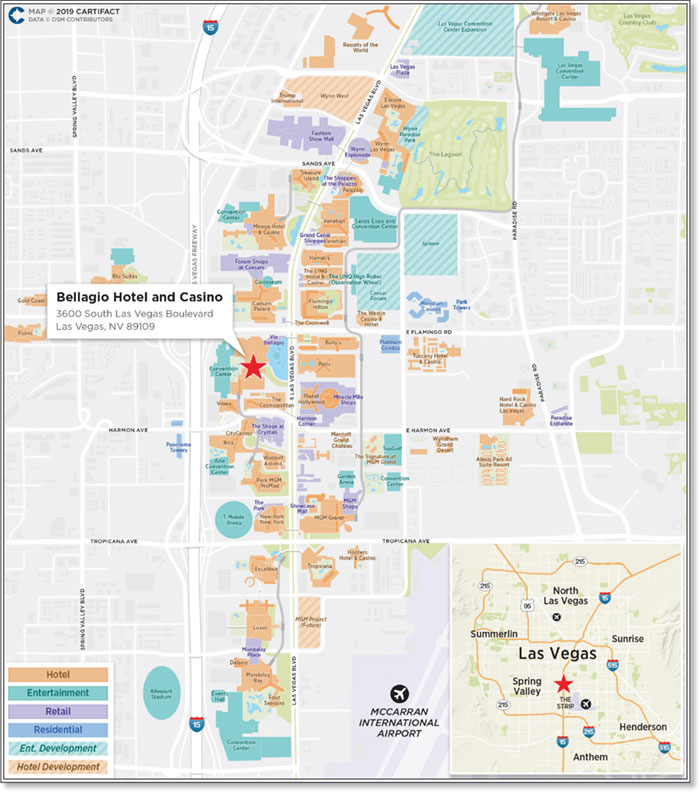

| Bellagio Hotel and Casino | JPMCB/CREFI | Las Vegas, NV | Hospitality | 60,000,000 | 6.7% | $426,189 | 39.3% | 8.42x | 28.3% |

| Kings Plaza | JPMCB | Brooklyn, NY | Retail | 50,000,000 | 5.6% | $600 | 54.1% | 3.07x | 10.7% |

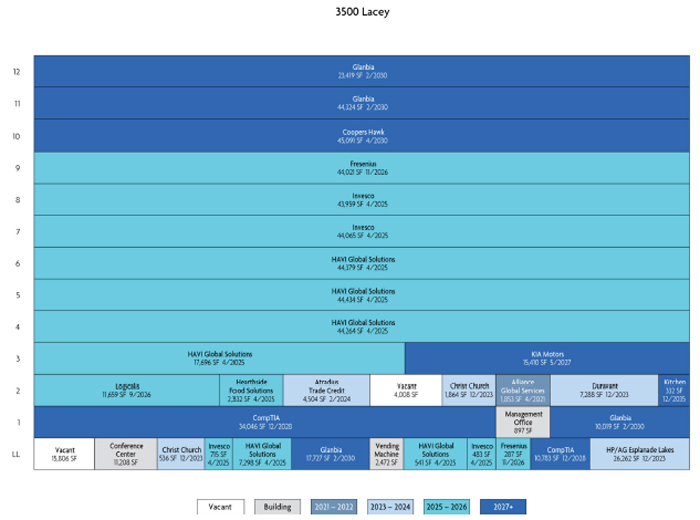

| 3500 Lacey | JPMCB | Downers Grove, IL | Office | 50,000,000 | 5.6% | $147 | 66.5% | 2.38x | 11.3% |

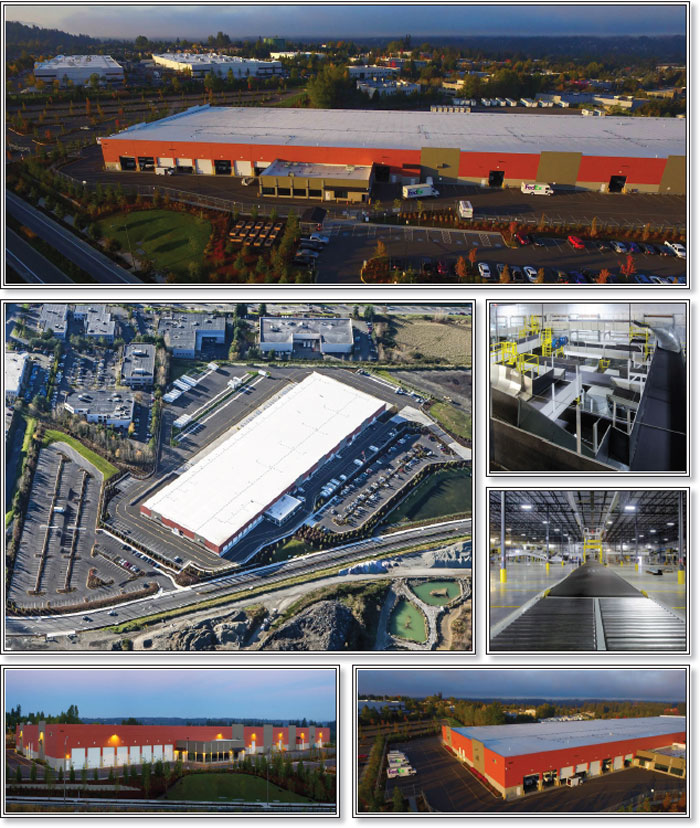

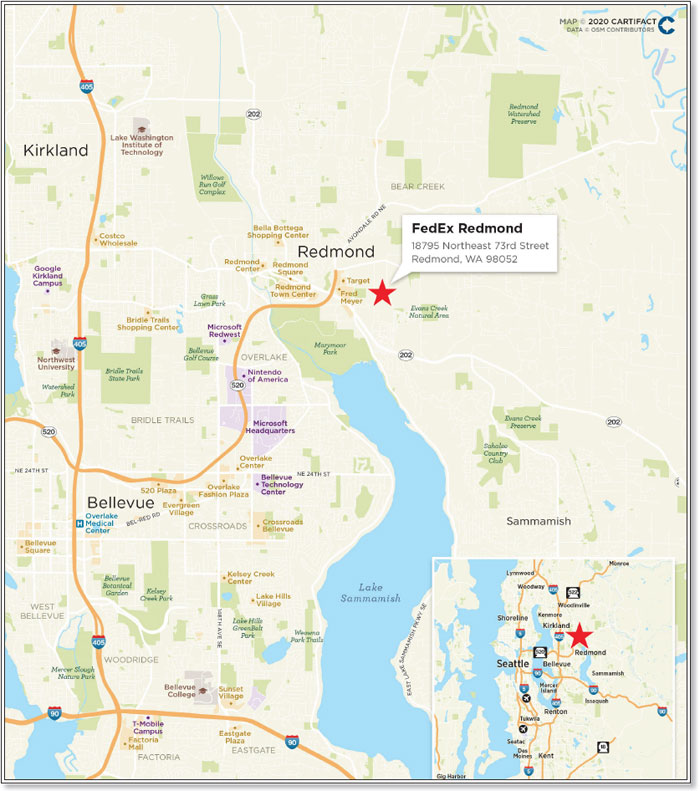

| FedEx Redmond | JPMCB | Redmond, WA | Industrial | 45,140,000 | 5.0% | $215 | 55.4% | 2.15x | 8.6% |

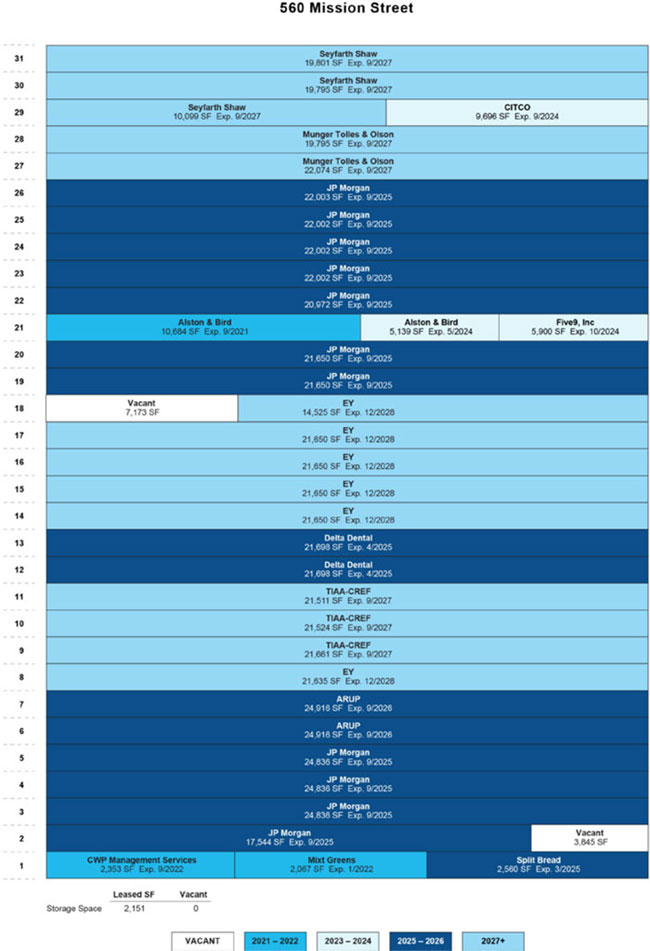

| 560 Mission Street | GACC | San Francisco, CA | Office | 45,000,000 | 5.0% | $449 | 35.6% | 5.23x | 14.2% |

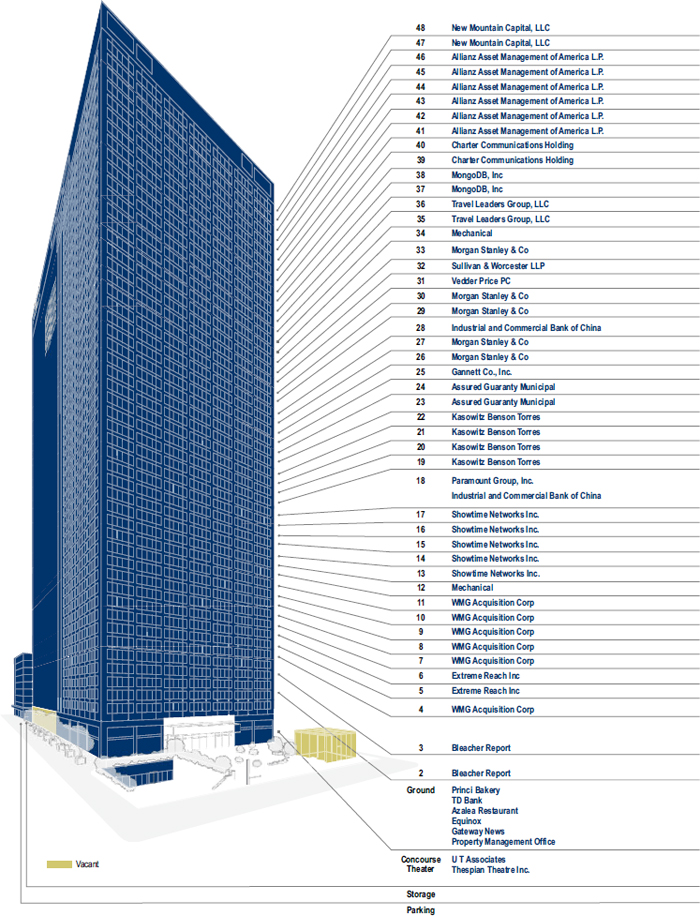

| 1633 Broadway | GACC/JPMCB | New York, NY | Office | 45,000,000 | 5.0% | $391 | 41.7% | 3.84x | 11.9% |

| Starwood Industrial Portfolio | GACC | Various, Various | Industrial | 45,000,000 | 5.0% | $36 | 45.2% | 3.67x | 13.1% |

| 650 Madison Avenue | CREFI | New York, NY | Mixed Use | 45,000,000 | 5.0% | $977 | 48.5% | 2.74x | 10.0% |

| 181 West Madison | JPMCB | Chicago, IL | Office | 43,000,000 | 4.8% | $114 | 28.8% | 4.67x | 20.4% |

| Total/Weighted Average | $493,140,000 | 54.8% | 48.8% | 3.88x | 13.8% | ||||

| (1) | The Cut-off Date Balance per NRA/Room Cut-off Date LTV, U/W NCF DSCR after IO and U/W NOI Debt Yield calculations include any relatedpari passu companion loan(s) and exclude any related subordinate companion loan(s) and/or mezzanine loan(s). |

| (2) | With respect to the Bellagio Hotel and Casino, 650 Madison Avenue and 181 West Madison mortgage loans, the Cut-off Date LTV have been calculated based on the appraised values other than “As Is”. For additional information please see the footnotes to Annex A-1 in the Preliminary Prospectus. |

| Existing Mezzanine Debt Summary | ||||||||||

| Mortgage Loan | Mortgage Loan Cut-off Date Balance | Pari Passu/ | Mezzanine Debt Cut-off Date Balance | Trust U/W NCF DSCR | Total Debt U/W NCF DSCR(1)(2) | Trust Cut-off Date LTV | Total Debt Cut-off Date LTV(1) | Trust U/W NOI Debt Yield | Total Debt U/W NOI Debt Yield(1) | |

| Kings Plaza(2) | $50,000,000 | $437,000,000 | $53,000,000 | 3.07x | 1.73x | 54.1% | 60.0% | 10.7% | 9.6% | |

| 510 East 14th Street | $35,000,000 | $50,000,000 | $75,000,000 | 3.62x | 1.36x | 29.5% | 55.6% | 10.9% | 5.8% | |

| 490-504 Myrtle Avenue | $35,000,000 | $50,000,000 | $20,000,000 | 1.92x | 1.28x | 60.2% | 74.3% | 7.4% | 6.0% | |

| (1) | Total Debt U/W NCF DSCR, Total Debt Cut-off Date LTV and Total Debt U/W NOI Debt Yield calculations include any relatedpari passu companion loan(s), any related subordinate companion loan(s) and/or any related mezzanine loan(s). |

| (2) | The Kings Plaza mezzanine loan is interest only for the first five years of the loan term then fully amortizing based on a five-year schedule. Total Debt U/W NCF DSCR is based on the first 12 month period of the amortization period of the loan. |

| Subordinate Debt Summary | |||||||||

| Mortgage Loan | Mortgage Cut-off Date Balance | Pari Passu | Subordinate Debt Cut-off Date Balance | Trust U/W NCF DSCR | Total Debt U/W NCF DSCR(1) | Trust Cut-off Date LTV(2) | Total Debt Cut-off Date LTV(1)(2) | Trust U/W NOI Debt Yield | Total Debt U/W NOI Debt Yield(1) |

| Bellagio Hotel and Casino | $60,000,000 | $1,616,200,000 | $1,333,800,000 | 8.42x | 4.06x | 39.3% | 70.7% | 28.3% | 15.7% |

| 1633 Broadway | $45,000,000 | $956,000,000 | $249,000,000 | 3.84x | 3.08x | 41.7% | 52.1% | 11.9% | 9.5% |

| Starwood Industrial Portfolio | $45,000,000 | $99,500,000 | $65,527,072 | 3.67x | 2.53x | 45.2% | 65.7% | 13.1% | 9.0% |

| 650 Madison Avenue | $45,000,000 | $541,800,000 | $213,200,000 | 2.74x | 2.01x | 48.5% | 66.1% | 10.0% | 7.3% |

| 181 West Madison | $43,000,000 | $64,900,000 | $132,100,000 | 4.67x | 2.10x | 28.8% | 64.0% | 20.4% | 9.2% |

| (1) | Total Debt U/W NCF DSCR, Total Debt Cut-off Date LTV and Total Debt U/W NOI Debt Yield calculations include any relatedpari passu companion loan(s), related subordinate companion loan(s) and/or related mezzanine loan(s). |

| (2) | With respect to the Bellagio Hotel and Casino, 650 Madison Avenue and 181 West Madison mortgage loans, the Trust Cut-off Date LTV and Total Debt Cut-off Date LTV have been calculated based on the appraised values other than “As Is”. For additional information please see the footnotes to Annex A-1 in the Preliminary Prospectus. |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

6

Benchmark 2020-B16 Mortgage Trust

|

| OVERVIEW OF MORTGAGE POOL CHARACTERISTICS |

| Companion Loan Summary | |||||||||

| Loan No. | Mortgage Loan | Note(s) | Original Balance ($) | Cut-off Date Balance ($) | Holder of Note(1) | Lead Servicer for Whole Loan (Y/N) | Master Under Lead | Special | |

| 2 | Bellagio Hotel and Casino | A-1-C1 | $100,000,000 | $100,000,000 | BANK 2020-BNK25 | No | |||

| A-2-C1 | $60,000,000 | $60,000,000 | GSMS 2020-GC45 | No | |||||

| A-1-S1, A-1-S2, A-2-S1, A-2-S2, A-3-S1, A-3-S2 | $716,000,000 | $716,000,000 | BX 2019-OC11 | Yes (A-1-S1) | KeyBank | Situs | |||

| A-2-C2, A-3-C2 | $60,000,000 | $60,000,000 | Benchmark 2020-B16 | No | |||||

| A-1-RL, A-2-RL, A-3-RL | $360,200,000 | $360,200,000 | Third party investor | No | |||||

| A-1-C2, A-1-C3, A-1-C4, A-1-C5 | $200,000,000 | $200,000,000 | MSNBA | No | |||||

| A-2-C3 | $60,000,000 | $60,000,000 | CREFI | No | |||||

| A-3-C1, A-3-C3, A-3-C4, A-3-C5, A-3-C6 | $120,000,000 | $120,000,000 | JPMCB | No | |||||

| Total Senior Notes | $1,676,200,000 | $1,676,200,000 | |||||||

| B-1-S, B-2-S, B-3-S | $510,700,000 | $510,700,000 | BX 2019-OC11 | No | |||||

| B-1-RL, B-2-RL, B-3-RL | $139,800,000 | $139,800,000 | Third party investor | No | |||||

| C-1-S, C-2-S, C-3-S | $683,300,000 | $683,300,000 | BX 2019-OC11 | No | |||||

| Total | $3,010,000,000 | $3,010,000,000 | |||||||

| 3 | Kings Plaza | A-1-1 | $70,000,000 | $70,000,000 | JPMCB | Yes(2) | Midland | KeyBank | |

| A-1-2 | $50,000,000 | $50,000,000 | Benchmark 2020-B16 | No | |||||

| A-1-3, A-1-4 | $51,108,108 | $51,108,108 | JPMCB | No | |||||

| A-2-1, A-2-2, A-2-3, A-2-4 | $157,945,946 | $157,945,946 | SGFC | No | |||||

| A-3-1 | $50,000,000 | $50,000,000 | BANK 2020-BNK25 | No | |||||

| A-3-2, A-3-3 | $82,945,946 | $82,945,946 | WF | No | |||||

| A-3-4 | $25,000,000 | $25,000,000 | BANK 2020-BNK25 | No | |||||

| Total | $487,000,000 | $487,000,000 | |||||||

| 4 | 3500 Lacey | Note A-1 | $50,000,000 | $50,000,000 | Benchmark 2020-B16 | Yes | Midland | KeyBank | |

| Note A-2 | $35,800,000 | $35,800,000 | JPMCB | No | |||||

| Total | $85,800,000 | $85,800,000 | |||||||

| 6 | 560 Mission Street | A-1 | $60,000,000 | $60,000,000 | GSMS 2020-GC45 | No | |||

| A-1-2-A, A-1-4 | $45,000,000 | $45,000,000 | Benchmark 2020-B16 | Yes | Midland | KeyBank | |||

| A-1-2-B, A-1-3 | $45,000,000 | $45,000,000 | DBRI | No | |||||

| A-2-1 | $100,000,000 | $100,000,000 | BANK 2020-BNK25 | No | |||||

| A-2-2 | $50,000,000 | $50,000,000 | BANA | No | |||||

| Total | $300,000,000 | $300,000,000 | |||||||

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

7

Benchmark 2020-B16 Mortgage Trust

|

| OVERVIEW OF MORTGAGE POOL CHARACTERISTICS |

| Loan No. | Mortgage Loan | Note(s) | Original Balance ($) | Cut-off Date Balance ($) | Holder of Note | Lead Servicer for Whole Loan (Y/N) | Master Servicer Under Lead Securitization | Special Servicer Under Lead Securitization |

| 7 | 1633 Broadway | A-1-S-1, A-2-S-1, A-3-S-1, A-4-S-1 | $1,000,000 | $1,000,000 | BWAY 2019-1633 | No | ||

| A-1-C-1, A-1-C-3, A-1-C-4, A-1-C-5, A-1-C-6, A-1-C-7 | $205,000,000 | $205,000,000 | GS Bank | No(3) | ||||

| A-1-C-2, A-2-C-5 | $60,000,000 | $60,000,000 | GSMS 2020-GC45 | No | ||||

| A-2-C-1-A, A-2-C-2, A-2-C-3, A-2-C-4, A-2-C-6, A-2-C-7 | $212,500,000 | $212,500,000 | DBRI | No | ||||

| A-2-C-1-B, A-3-C-1-B | $45,000,000 | $45,000,000 | Benchmark 2020-B16 | No | ||||

| A-3-C-1-A, A-3-C-2, A-3-C-3, A-3-C-4, A-3-C-5, A-3-C-6, A-3-C-7 | $227,500,000 | $227,500,000 | JPMCB | No | ||||

| A-4-C-1, A-4-C-2 | $100,000,000 | $100,000,000 | BANK 2020-BNK25 | No | ||||

| A-4-C-3, A-4-C-4, A-4-C-5, A-4-C-6, A-4-C-7 | $150,000,000 | $150,000,000 | WFB | No | ||||

| Total Senior Notes | $1,001,000,000 | $1,001,000,000 | ||||||

| B-1, B-2, B-3, B-4 | $249,000,000 | $249,000,000 | BWAY 2019-1633 | Yes(3) | KeyBank | Situs | ||

| Total | $1,250,000,000 | $1,250,000,000 | ||||||

| 8 | Starwood Industrial Portfolio | A-1, A-2-2 | $60,000,000 | $60,000,000 | GSMS 2020-GC45 | No | ||

| A-2-1, A-3-1 | $45,000,000 | $45,000,000 | Benchmark 2020-B16 | No | ||||

| A-3-2, A-4 | $39,500,000 | $39,500,000 | DBRI | |||||

| Total Senior Notes | $144,500,000 | $144,500,000 | ||||||

| B-1 | $65,527,072 | $65,527,072 | GSMS 2020-GC45 | Yes(4) | Midland | Midland | ||

| Total | $210,027,072 | $210,027,072 | ||||||

| 9 | 650 Madison Avenue | A-1-1 | $50,000,000 | $50,000,000 | CGCMT 2019-C7 | No(5) | ||

| A-1-2-1 | $40,000,000 | $40,000,000 | CCRE | No | ||||

| A-1-3, A-2-1 | $50,000,000 | $50,000,000 | GSMS 2020-GC45 | No | ||||

| A-1-4, A-1-6 | $137,900,000 | $137,900,000 | CREFI | No | ||||

| A-1-5 | $45,000,000 | $45,000,000 | Benchmark 2020-B16 | No | ||||

| A-2-2, A-2-3, A-2-4, A-2-5, A-2-6, A-2-7, A-2-8 | $116,450,000 | $116,450,000 | GSBI | No | ||||

| A-3-1, A-3-2, A-3-3 | $146,450,000 | $146,450,000 | BCREI | No | ||||

| A-4, A-5, A-6, A-7 | $1,000,000 | $1,000,000 | MAD 2019-650M | No | ||||

| Total Senior Notes | $586,800,000 | $586,800,000 | ||||||

| B-1, B-2, B-3, B-4 | $213,200,000 | $213,200,000 | MAD 2019-650M | Yes(5) | KeyBank | LNR | ||

| Total | $800,000,000 | $800,000,000 | ||||||

| 10 | 181 West Madison | A-1 | $1,000,000 | $1,000,000 | JPMCC 2020-LOOP | No | ||

| A-2 | $43,000,000 | $43,000,000 | Benchmark 2020-B16 | No(6) | ||||

| A-3, A-4 | $63,900,000 | $63,900,000 | JPMCB | No | ||||

| Total Senior Notes | $107,900,000 | $107,900,000 | ||||||

| B-1 | $132,100,000 | $132,100,000 | JPMCC 2020-LOOP | Yes(6) | KeyBank | Situs | ||

| Total | $240,000,000 | $240,000,000 | ||||||

| 13 | 510 East 14th Street | A-1-1 | $35,000,000 | $35,000,000 | Benchmark 2020-B16 | No | ||

| A-1-2 | $15,000,000 | $15,000,000 | CREFI | No | ||||

| A-2 | $35,000,000 | $35,000,000 | GSMS 2020-GC45 | Yes | Midland | Midland | ||

| Total | $85,000,000 | $85,000,000 |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

8

Benchmark 2020-B16 Mortgage Trust

|

| OVERVIEW OF MORTGAGE POOL CHARACTERISTICS |

| Loan No. | Mortgage Loan | Note(s) | Original Balance ($) | Cut-off Date Balance ($) | Holder of Note | Lead Servicer for Whole Loan (Y/N) | Master Servicer Under Lead Securitization | Special Servicer Under Lead Securitization |

| 14 | 490-504 Myrtle Avenue | A-1 | $50,000,000 | $50,000,000 | CGCMT 2019-C7 | Yes | Wells Fargo | LNR |

| A2 | $35,000,000 | $35,000,000 | Benchmark 2020-B16 | No | ||||

| Total | $85,000,000 | $85,000,000 | ||||||

| 24 | Giant Anchored Portfolio | A-1-A | $38,500,000 | $38,500,000 | CGCMT 2019-C7 | Yes | Wells Fargo | LNR |

| A-1-B | $10,000,000 | $10,000,000 | Benchmark 2020-B16 | No | ||||

| A-2-A | $30,000,000 | $30,000,000 | BANK 2019-BNK24 | No | ||||

| A-2-B | $18,500,000 | $18,500,000 | WFB | No | ||||

| Total | $97,000,000 | $97,000,000 |

| (1) | The identification of a securitization trust means we have identified another securitization trust that has closed or as to which a preliminary prospectus (or preliminary offering circular) or final prospectus (or final offering circular) has printed that has or is expected to include the identified Mortgage Note(s). |

| (2) | Prior to the servicing shift securitization date, the related whole loan will be serviced under the pooling and servicing agreement for this transaction. From and after the related servicing shift securitization date, the related servicing shift whole loan will be serviced under the related servicing shift pooling and servicing agreement. |

| (3) | With respect to the 1633 Broadway Whole Loan, the initial Control Notes are Note B-1, Note B-2, Note B-3 and Note B-4. During the continuance of a control shift event related to the BWAY 2019-1633 securitization transaction (i.e., when the most senior class of certificates in such transaction have been control appraised out), Note A-1-C1 will be the Control Note; provided, however, that the 1633 Broadway Whole Loan will continue to be serviced by the master servicer, and if necessary, the special servicer, under the BWAY 2019-1633 trust and servicing agreement. See “Description of the Mortgage Pool—The Whole Loans—The Non-Serviced AB Whole Loans—The 1633 Broadway Whole Loan” in the Preliminary Prospectus. |

| (4) | With respect to the Starwood Industrial Portfolio Whole Loan, the initial Control Note is Note B-1. During the continuance of a control appraisal period related to the Starwood Industrial Portfolio Whole Loan, Note A-2-1 will be the Control Note; provided, however, that the Starwood Industrial Portfolio Whole Loan will continue to be serviced by the master servicer, and if necessary, the special servicer, under the GSMS 2020-GC45 pooling and servicing agreement. See “Description of the Mortgage Pool—The Whole Loans—The Non-Serviced AB Whole Loans—The Starwood Industrial Portfolio Whole Loan” in the Preliminary Prospectus. |

| (5) | With respect to the 650 Madison Avenue Whole Loan, the initial Control Note is Note B-1. During the continuance of a control appraisal period related to the 650 Madison Avenue Whole Loan, Note A-1-1 will be the Control Note; provided, however, that the 650 Madison Avenue Whole Loan will continue to be serviced by the master servicer, and if necessary, the special servicer, under the MAD 2019-650M trust and servicing agreement. See “Description of the Mortgage Pool—The Whole Loans—The Non-Serviced AB Whole Loans—The 650 Madison Avenue Whole Loan” in the Preliminary Prospectus. |

| (6) | With respect to the 181 West Madison Whole Loan, the initial Control Note is Note B-1. During the continuance of a trust loan control event relating to the JPMCC 2020-LOOP securitization transaction (i.e., when the class G certificates in such transaction have been control appraised out, but the class C certificates in such transaction have not been control appraised out), a specified percentage of the certificateholders of such transaction will be entitled to exercise the rights of the Control Note to replace the special servicer (but no certificateholder will have any other rights of the Control Note). During the control shift event relating to the JPMCC 2020-LOOP securitization transaction (i.e., when the class C certificates in such transaction have been control appraised out), Note A-2 will be the Control Note; provided however, that the 181 West Madison Whole Loan will continue to be serviced by the master servicer, and if necessary, the special servicer, under the JPMCC 2020-LOOP trust and servicing agreement See “Description of the Mortgage Pool—The Whole Loans—The Non-Serviced AB Whole Loans—The 181 West Madison Whole Loan” in the Preliminary Prospectus. |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

9

Benchmark 2020-B16 Mortgage Trust

|

| OVERVIEW OF MORTGAGE POOL CHARACTERISTICS |

| Distribution of Cut-off Date Balances(1) | ||||||||||

| Range of Cut-off Date Balances | Number of Mortgage Loans | Aggregate Cut-off Date Balance | % of Initial Pool Balance | Weighted Averages | ||||||

| Mortgage Rate | Stated Remaining Term (Mos.) | U/W NCF DSCR | Cut-off Date LTV(2) | Maturity Date LTV(2) | ||||||

| $3,725,000 | - | $7,499,999 | 7 | $40,395,000 | 4.5% | 4.0210% | 119 | 2.09x | 63.7% | 58.9% |

| $7,500,000 | - | $14,999,999 | 6 | $66,461,873 | 7.4% | 3.8547% | 109 | 2.39x | 67.8% | 65.2% |

| $15,000,000 | - | $24,999,999 | 3 | $59,350,000 | 6.6% | 3.6773% | 120 | 2.87x | 52.0% | 52.0% |

| $25,000,000 | - | $49,999,999 | 13 | $507,890,000 | 56.5% | 3.5444% | 115 | 3.04x | 48.7% | 47.7% |

| $50,000,000 | - | $65,000,000 | 4 | $225,000,000 | 25.0% | 3.5782% | 119 | 4.09x | 56.1% | 56.1% |

| Total/Weighted Average | 33 | $899,096,873 | 100.0% | 3.6060% | 116 | 3.20x | 52.8% | 51.9% | ||

| Distribution of Mortgage Rates(1) | ||||||||||

| Range of Mortgage Rates | Number of Mortgage Loans | Aggregate Cut-off Date Balance | % of Initial Pool | Weighted Averages | ||||||

| Mortgage Rate | Stated Remaining Term (Mos.) | U/W NCF DSCR | Cut-off Date LTV(2) | Maturity Date LTV(2) | ||||||

| 2.5890% | - | 2.9999% | 3 | $125,000,000 | 13.9% | 2.8260% | 118 | 4.28x | 36.1% | 36.1% |

| 3.0000% | - | 3.4999% | 5 | $215,000,000 | 23.9% | 3.3026% | 118 | 4.66x | 46.4% | 46.4% |

| 3.5000% | - | 3.9999% | 15 | $401,567,000 | 44.7% | 3.7617% | 115 | 2.56x | 56.3% | 56.1% |

| 4.0000% | - | 4.3500% | 10 | $157,529,873 | 17.5% | 4.2421% | 115 | 1.99x | 66.2% | 61.1% |

| Total/Weighted Average | 33 | $899,096,873 | 100.0% | 3.6060% | 116 | 3.20x | 52.8% | 51.9% | ||

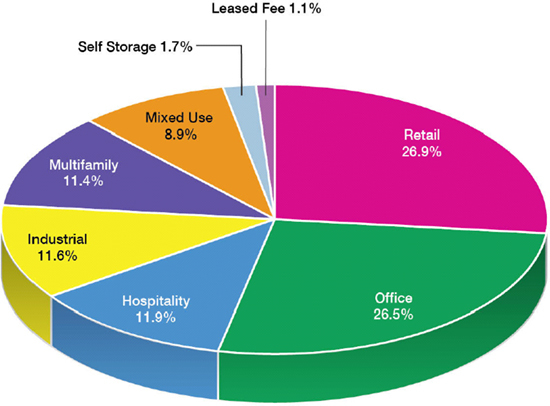

| Property Type Distribution(1)(3)(4) | |||||||||||

| Property Type | Number of Mortgaged Properties | Aggregate Cut-off Date Balance | % of Initial Outstanding Pool Balance | Number of NRA/Units/Rooms | Weighted Averages | ||||||

Cut-off Date NRA/Units/Rooms | Mortgage Rate | Stated Remaining Term (Mos.) | Occupancy | U/W NCF DSCR | Cut-off Date LTV(2) | Maturity LTV(2) | |||||

| Retail | 18 | $242,055,000 | 26.9% | 2,815,754 | $406 | 3.5987% | 116 | 98.8% | 2.58x | 59.0% | 58.7% |

| Anchored(5) | 17 | $231,425,000 | 25.7% | 2,779,143 | $411 | 3.5773% | 119 | 98.8% | 2.60x | 58.6% | 58.3% |

| Unanchored | 1 | $10,630,000 | 1.2% | 36,611 | $290 | 4.0650% | 58 | 100.0% | 2.07x | 67.5% | 67.5% |

| Office | 7 | $238,032,000 | 26.5% | 5,014,134 | $284 | 3.5301% | 112 | 95.9% | 3.68x | 46.1% | 46.1% |

| CBD | 4 | $166,500,000 | 18.5% | 4,251,283 | $346 | 3.2756% | 109 | 96.0% | 4.13x | 37.8% | 37.8% |

| Suburban | 3 | $71,532,000 | 8.0% | 762,851 | $140 | 4.1226% | 118 | 95.9% | 2.65x | 65.5% | 65.5% |

| Hospitality | 5 | $107,199,873 | 11.9% | 4,409 | $290,300 | 3.5798% | 119 | 82.4% | 5.79x | 47.5% | 43.3% |

| Full Service | 3 | $92,700,000 | 10.3% | 4,230 | $322,692 | 3.4858% | 119 | 82.9% | 6.38x | 44.6% | 41.5% |

| Select Service | 1 | $7,999,873 | 0.9% | 84 | $95,237 | 4.2760% | 118 | 77.8% | 2.09x | 67.8% | 54.5% |

| Limited Service | 1 | $6,500,000 | 0.7% | 95 | $68,421 | 4.0640% | 119 | 80.2% | 1.94x | 64.4% | 55.8% |

| Industrial | 35 | $104,245,000 | 11.6% | 4,410,567 | $125 | 3.5915% | 118 | 99.4% | 2.82x | 52.3% | 52.3% |

| Warehouse/Distribution | 33 | $102,448,944 | 11.4% | 4,238,472 | $126 | 3.5978% | 118 | 99.4% | 2.80x | 52.4% | 52.4% |

| Cold Storage | 2 | $1,796,056 | 0.2% | 172,095 | $34 | 3.2310% | 118 | 100.0% | 3.67x | 45.2% | 45.2% |

| Multifamily | 4 | $102,800,000 | 11.4% | 604 | $373,444 | 4.0355% | 119 | 96.0% | 1.62x | 66.0% | 63.9% |

| Mid Rise | 3 | $66,600,000 | 7.4% | 282 | $515,321 | 3.8837% | 118 | 98.0% | 1.83x | 61.7% | 61.7% |

| Garden | 1 | $36,200,000 | 4.0% | 322 | $112,422 | 4.3150% | 119 | 92.2% | 1.22x | 73.9% | 68.1% |

| Mixed Use | 2 | $80,000,000 | 8.9% | 600,575 | $232,971 | 3.2384% | 118 | 98.5% | 3.13x | 40.2% | 40.2% |

| Office/Retail | 1 | $45,000,000 | 5.0% | 600,415 | $977 | 3.4860% | 118 | 97.4% | 2.74x | 48.5% | 48.5% |

| Multifamily/Retail | 1 | $35,000,000 | 3.9% | 160 | $531,250 | 2.9200% | 118 | 100.0% | 3.62x | 29.5% | 29.5% |

| Self-Storage | 5 | $15,175,000 | 1.7% | 271,983 | $58 | 4.1598% | 118 | 84.7% | 1.47x | 69.5% | 60.4% |

| Leased Fee | 1 | $9,590,000 | 1.1% | 131,802 | $73 | 3.7100% | 119 | NAP | 2.52x | 70.0% | 70.0% |

| Total/Weighted Average | 77 | $899,096,873 | 100.0% | 3.6060% | 116 | 95.5% | 3.20x | 52.8% | 51.9% | ||

| Geographic Distribution(1)(3) | ||||||||

| State/Location | Number of Properties | Aggregate Cut-off Date Balance | % of Initial Outstanding Pool Balance | Weighted Averages | ||||

| Mortgage Rate | Stated Remaining Term (Mos.) | U/W NCF DSCR | Cut-off Date LTV(2) | Maturity Date LTV(2) | ||||

| New York | 10 | $332,900,000 | 37.0% | 3.4254% | 118 | 2.78x | 52.6% | 52.6% |

| New York City | 9 | $321,600,000 | 35.8% | 3.4183% | 119 | 2.79x | 52.3% | 52.3% |

| New York State | 1 | $11,300,000 | 1.3% | 3.6300% | 118 | 2.62x | 59.4% | 59.4% |

| Illinois | 9 | $122,717,194 | 13.6% | 4.0182% | 106 | 3.26x | 51.3% | 51.3% |

| California | 3 | $85,000,000 | 9.5% | 3.1605% | 118 | 3.91x | 41.7% | 41.7% |

| Northern | 2 | $78,500,000 | 8.7% | 3.0973% | 118 | 4.00x | 40.4% | 40.4% |

| Southern | 1 | $6,500,000 | 0.7% | 3.9240% | 118 | 2.86x | 57.0% | 57.0% |

| Nevada | 1 | $60,000,000 | 6.7% | 3.1702% | 118 | 8.42x | 39.3% | 39.3% |

| North Carolina | 4 | $59,230,000 | 6.6% | 3.9160% | 108 | 2.50x | 58.2% | 53.4% |

| Washington | 2 | $53,139,873 | 5.9% | 3.9311% | 119 | 2.14x | 57.3% | 55.3% |

| Other | 48 | $186,109,806 | 20.7% | 3.8097% | 119 | 2.43x | 60.8% | 58.3% |

| Total/Weighted Average | 77 | $899,096,873 | 100.0% | 3.6060% | 116 | 3.20x | 52.8% | 51.9% |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

10

Benchmark 2020-B16 Mortgage Trust

|

| OVERVIEW OF MORTGAGE POOL CHARACTERISTICS |

| Distribution of Cut-off Date LTVs(1)(2) | ||||||||||

| Range of Cut-off Date LTVs | Number of Mortgage Loans | Aggregate Cut-off Date Balance | % of Initial Outstanding Pool Balance | Weighted Averages | ||||||

| Mortgage Rate | Stated Term | U/W NCF DSCR | Cut-off Date LTV | Maturity Date LTV(2) | ||||||

| 28.8% | - | 54.9% | 12 | $463,700,000 | 51.6% | 3.3348% | 115 | 4.19x | 42.4% | 41.8% |

| 55.0% | - | 59.9% | 5 | $106,110,000 | 11.8% | 3.7786% | 119 | 2.42x | 57.6% | 57.6% |

| 60.0% | - | 64.9% | 5 | $110,587,000 | 12.3% | 3.8213% | 119 | 2.17x | 62.3% | 61.8% |

| 65.0% | - | 69.9% | 6 | $154,534,873 | 17.2% | 3.9343% | 114 | 2.21x | 65.9% | 64.8% |

| 70.0% | - | 74.3% | 5 | $64,165,000 | 7.1% | 4.1190% | 119 | 1.50x | 73.0% | 67.4% |

| Total/Weighted Average | 33 | $899,096,873 | 100.0% | 3.6060% | 116 | 3.20x | 52.8% | 51.9% | ||

| Distribution of Maturity Date or ARD LTVs(1)(2) | ||||||||||

| Range of Maturity Date or ARD LTVs | Number of Mortgage Loans | Aggregate Cut-off Date Balance | % of Initial Outstanding Pool Balance | Weighted Averages | ||||||

| Mortgage Rate | Stated Term | U/W NCF DSCR | Cut-off Date LTV(2) | Maturity Date or ARD LTV | ||||||

| 28.8% | - | 49.9% | 11 | $413,700,000 | 46.0% | 3.3319% | 115 | 4.32x | 40.9% | 40.3% |

| 50.0% | - | 54.9% | 2 | $57,999,873 | 6.5% | 3.4853% | 119 | 2.93x | 56.0% | 54.2% |

| 55.0% | - | 59.9% | 7 | $119,410,000 | 13.3% | 3.8244% | 119 | 2.34x | 58.5% | 57.6% |

| 60.0% | - | 70.0% | 13 | $307,987,000 | 34.3% | 3.9123% | 117 | 2.08x | 66.0% | 64.9% |

| Total/Weighted Average | 33 | $899,096,873 | 100.0% | 3.6060% | 116 | 3.20x | 52.8% | 51.9% | ||

| Distribution of Underwritten NCF Debt Service Coverages(1) | ||||||||||

| Range of Underwritten NCF Debt Service Coverages | Number of Mortgage Loans | Aggregate Cut-off Date Balance | % of Initial Outstanding Pool Balance | Weighted Averages | ||||||

| Mortgage Rate | Stated Remaining Term (Mos.) | U/W NCF DSCR | Cut-off Date LTV(2) | Maturity Date or ARD LTV(2) | ||||||

| 1.22x | - | 1.49x | 2 | $43,000,000 | 4.8% | 4.3142% | 119 | 1.24x | 72.9% | 66.6% |

| 1.50x | - | 1.74x | 4 | $49,975,000 | 5.6% | 3.9740% | 119 | 1.66x | 66.8% | 63.8% |

| 1.75x | - | 2.49x | 11 | $296,049,873 | 32.9% | 3.8726% | 117 | 2.21x | 61.0% | 60.5% |

| 2.50x | - | 3.49x | 9 | $222,072,000 | 24.7% | 3.6265% | 119 | 2.82x | 54.6% | 53.4% |

| 3.50x | - | 8.42x | 7 | $288,000,000 | 32.0% | 3.1466% | 113 | 5.07x | 37.7% | 37.7% |

| Total/Weighted Average | 33 | $899,096,873 | 100.0% | 3.6060% | 116 | 3.20x | 52.8% | 51.9% | ||

| Original Terms to Maturity or ARD(1) | |||||||||||

| Original Terms to Maturity or ARD | Number of Mortgage Loans | Aggregate Cut-off Date Balance | % of Initial Outstanding Pool Balance | Weighted Averages | |||||||

| Mortgage Rate | Stated Remaining Term (Mos.) | U/W NCF DSCR | Cut-off Date LTV(2) | Maturity Date or ARD LTV(2) | |||||||

| 60 | - | 60 | 1 | $10,630,000 | 1.2% | 4.0650% | 58 | 2.07x | 67.5% | 67.5% | |

| 84 | - | 84 | 1 | $43,000,000 | 4.8% | 3.9000% | 82 | 4.67x | 28.8% | 28.8% | |

| 119 | - | 120 | 31 | $845,466,873 | 94.0% | 3.5853% | 119 | 3.14x | 53.9% | 52.9% | |

| Total/Weighted Average | 33 | $899,096,873 | 100.0% | 3.6060% | 116 | 3.20x | 52.8% | 51.9% | |||

| Distribution of Remaining Terms to Maturity or ARD(1) | ||||||||||

| Range of Remaining Terms to Maturity or ARD | Number of Mortgage Loans | Aggregate Cut-off Date Balance | % of Initial Outstanding Pool Balance | Weighted Averages | ||||||

| Mortgage Rate | Stated Remaining Term (Mos.) | U/W NCF DSCR | Cut-off Date LTV(2) | Maturity Date or ARD LTV(2) | ||||||

| 58 | - | 58 | 1 | $10,630,000 | 1.2% | 4.0650% | 58 | 2.07x | 67.5% | 67.5% |

| 82 | - | 82 | 1 | $43,000,000 | 4.8% | 3.9000% | 82 | 4.67x | 28.8% | 28.8% |

| 118 | - | 120 | 31 | $845,466,873 | 94.0% | 3.5853% | 119 | 3.14x | 53.9% | 52.9% |

| Total/Weighted Average | 33 | $899,096,873 | 100.0% | 3.6060% | 116 | 3.20x | 52.8% | 51.9% | ||

| Distribution of Underwritten NOI Debt Yields(1)(4) | ||||||||||

| Range of Underwritten NOI Debt Yields | Number of Mortgage Loans | Aggregate Cut-off Date Balance | % of Initial Outstanding Pool Balance | Weighted Averages | ||||||

| Mortgage Rate | Stated Remaining Term (Mos.) | U/W NCF DSCR | Cut-off Date LTV Ratio(2) | Maturity Date or ARD LTV(2) | ||||||

| 7.1% | - | 8.9% | 9 | $242,395,000 | 27.0% | 3.8685% | 119 | 1.91x | 63.7% | 62.4% |

| 9.0% | - | 9.9% | 7 | $133,970,000 | 14.9% | 3.7598% | 114 | 2.35x | 59.7% | 58.8% |

| 10.0% | - | 12.4% | 8 | $261,394,873 | 29.1% | 3.5263% | 118 | 3.03x | 49.9% | 49.5% |

| 12.5% | - | 14.9% | 7 | $158,337,000 | 17.6% | 3.2909% | 118 | 3.81x | 47.0% | 44.9% |

| 15.0% | - | 28.3% | 2 | $103,000,000 | 11.5% | 3.4748% | 103 | 6.85x | 34.9% | 34.9% |

| Total/Weighted Average | 33 | $899,096,873 | 100.0% | 3.6060% | 116 | 3.20x | 52.8% | 51.9% | ||

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

11

Benchmark 2020-B16 Mortgage Trust

|

| OVERVIEW OF MORTGAGE POOL CHARACTERISTICS |

| Amortization Types(1) | ||||||||

| Amortization Type | Number of Mortgage Loans | Aggregate Cut-off Date Balance | % of Initial Outstanding Pool Balance | Weighted Averages | ||||

| Mortgage Rate | Stated Term | U/W NCF DSCR | Cut-off Date LTV Ratio(2) | Maturity Date or ARD LTV(2) | ||||

| Interest Only | 25 | $797,022,000 | 88.6% | 3.5332% | 116 | 3.39x | 51.0% | 51.0% |

| Interest Only, then Amortizing | 6 | $67,875,000 | 7.5% | 4.1907% | 119 | 1.39x | 72.1% | 65.1% |

| Amortizing Balloon | 2 | $34,199,873 | 3.8% | 4.1412% | 120 | 2.46x | 56.8% | 45.4% |

| Total/Weighted Average | 33 | $899,096,873 | 100.0% | 3.6060% | 116 | 3.20x | 52.8% | 51.9% |

Footnotes:

| (1) | The U/W NCF DSCR, Cut-off Date LTV Ratio, Maturity Date or ARD LTV, Underwritten NOI Debt Yield and Cut-off Date Balance per # of NRA/Units/Rooms calculations include any relatedpari passu companion loan(s) and exclude any related subordinate companion loan(s) and/or mezzanine loan(s). |

| (2) | With respect to 5 mortgage loans (18.1%) (including Bellagio Hotel and Casino, 650 Madison Avenue, 181 West Madison, Fairfield Inn & Suites Spokane and Springhill Suites Florence), the Cut-off Date LTV and Maturity Date or ARD LTV have been calculated using a value other than the “As Is” appraised values. For additional information please see the footnotes to Annex A-1 in the Preliminary Prospectus. |

| (3) | Reflects allocated loan amount for properties securing multi-property Mortgage Loans. |

| (4) | With respect to the Landing Square mortgage loan (4.0%) the Cut-off Date LTV and U/W NOI Debt Yield is calculated based on the Cut-off Date Balance net of a capex holdback reserve. |

| (5) | Anchored retail includes specialty retail, other, super-regional mall, single tenant and shadow anchored properties. |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

12

Benchmark 2020-B16 Mortgage Trust

|

STRUCTURE OVERVIEW |

| The aggregate amount available for distribution to holders of the Certificates (including the VRR Interest) on each Distribution Date will be: (i) the gross amount of interest, principal, yield maintenance charges and prepayment premiums collected with respect to the Mortgage Loans in the applicable one-month collection period, net of specified expenses of the issuing entity, including fees payable therefrom to, and losses, liabilities, costs and expenses reimbursable or indemnifiable therefrom to, the Master Servicer, the Special Servicer, the Certificate Administrator, the Trustee, the Operating Advisor, the Asset Representations Reviewer and CREFC®; and (ii) allocated to amounts available for distribution to the holders of the VRR Interest, on the one hand, and amounts available for distribution to the holders of the remaining Certificates (the “Non-VRR Certificates”), on the other hand. On each Distribution Date, the portion of such aggregate available funds allocable to: (a) the VRR Interest will be the product of such aggregate available funds multiplied by a fraction, expressed as a percentage, the numerator of which is the initial Certificate Balance of the VRR Interest, and the denominator of which is the aggregate initial Certificate Balance of the Principal Balance Certificates and the initial Certificate Balance of the VRR Interest (the “VRR Percentage”); and (b) the Non-VRR Certificates will at all times be the product of such aggregate available funds multiplied by the difference between 100% and the VRR Percentage (such difference, the “Non-VRR Percentage”). See “Credit Risk Retention” and “Description of the Certificates” in the Preliminary Prospectus.

| |

| Payments in respect of the Non-VRR Percentage of principal on the Non-VRR Certificates will be distributed, first, to the Class A-SB certificates, until the Certificate Balance of such class is reduced to the planned principal balance for the related Distribution Date set forth on Annex F to the Preliminary Prospectus, then, to the Class A-1, Class A-2, Class A-3, Class A-4, Class A-5, Class A-SB, Class A-M, Class B, Class C, Class D, Class E, Class F, Class G and Class H certificates, in that order, until the Certificate Balance of each such class is reduced to zero. Notwithstanding the foregoing, if the total Certificate Balance of the Class A-M, Class B, Class C, Class D, Class E, Class F, Class G and Class H certificates have been reduced to zero as a result of loss allocation, payments in respect of principal of the certificates will be distributed, first, to the Class A-1, Class A-2, Class A-3, Class A-SB, Class A-4 and Class A-5 certificates, on a pro rata basis, based on the Certificate Balance of each such class, then, to the extent of any recoveries on realized losses, to the Class A-M, Class B, Class C, Class D, Class E, Class F, Class G and Class H certificates, in that order, in each case until the Certificate Balance of each such class is reduced to zero (or previously allocated realized losses have been fully reimbursed).

Each class of Class X Certificates will not be entitled to receive distributions of principal; however, (i) the notional amount of the Class X-A certificates will be reduced by the aggregate amount of principal distributions and realized losses allocated to the Class A-1, Class A-2, Class A-3, Class A-SB, Class A-4, Class A-5 and Class A-M certificates; (ii) the notional amount of the Class X-B certificates will be reduced by the aggregate amount of principal distributions and realized losses allocated to the Class B and Class C certificates; (iii) the notional amount of the Class X-D certificates will be reduced by the aggregate amount of principal distributions and realized losses allocated to the Class D and Class E certificates; (iv) the notional amount of the Class X-F certificates will be reduced by the principal distributions and realized losses allocated to the Class F certificates; (v) the notional amount of the Class X-G certificates will be reduced by the principal distributions and realized losses allocated to the Class G certificates; and the notional amount of the Class X-H certificates will be reduced by the principal distributions and realized losses allocated to the Class H certificates.

| |

Interest Payments: | On each Distribution Date, interest accrued for each class of Non-VRR Certificates at the applicable pass-through rate will be distributed in the following order of priority, to the extent of the Non-VRR Percentage of the aggregate available funds (exclusive of any portion thereof that represents the Non-VRR Percentage of any yield maintenance charges and prepayment premiums): first, to the Class A-1, Class A-2, Class A-3, Class A-SB, Class A-4, Class A-5, Class X-A, Class X-B, Class X-D, Class X-F, Class X-G and Class X-H certificates, on a pro rata basis, based on the accrued and unpaid interest on each such class and then, to the Class A-M, Class B, Class C, Class D, Class E, Class F, Class G and Class H certificates, in that order, in each case until the interest payable to each such class is paid in full. |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

13

Benchmark 2020-B16 Mortgage Trust

|

STRUCTURE OVERVIEW |

| The pass-through rates applicable to the Class A-1, Class A-2, Class A-3, Class A-SB, Class A-4, Class A-5, Class A-M, Class B, Class C, Class D, Class E, Class F, Class G and Class H certificates for each Distribution Date will equal one of: (i) a fixed per annum rate, (ii) the WAC Rate, (iii) a rate equal to the lesser of a specified pass-through rate and the WAC Rate or (iv) the WAC Rate less a specified rate.

As further described in the Preliminary Prospectus, the pass-through rates applicable to the Class X Certificates for each Distribution Date will generally be equal to the excess of (i) the WAC Rate over (ii) (A) with respect to the Class X-A certificates, the weighted average of the pass-through rates of the Class A-1, Class A-2, Class A-3, Class A-SB, Class A-4, Class A-5 and Class A-M certificates (weighted based on their respective Certificate Balances immediately prior to that Distribution Date), (B) with respect to the Class X-B certificates, the weighted average of the pass-through rates of the Class B and Class C certificates (weighted based on their respective Certificate Balances immediately prior to that Distribution Date), (C) with respect to the Class X-D certificates, the weighted average of the pass-through rates of the Class D and Class E certificates (weighted based on their respective Certificate Balances immediately prior to that Distribution Date), (D) with respect to the Class X-F certificates, the pass-through rate of the Class F certificates, (E) with respect to the Class X-G certificates, the pass-through rate of the Class G certificates and (F) with respect to the Class X-H certificates, the pass-through rate of the Class H certificates.

| |

| Prepayment interest shortfalls will be allocated pro rata based on interest entitlements, in reduction of the interest otherwise payable with respect to each of the interest-bearing classes of certificates.

| |

| The Non-VRR Percentage of losses on the Mortgage Loans will be allocated to each class of Non-VRR Certificates entitled to principal in reverse alphabetical order starting with Class H through and including Class A-M and then to Class A-1, Class A-2, Class A-3, Class A-SB, Class A-4 and Class A-5 certificates on a pro rata basis based on the Certificate Balance of each such class. The notional amount of any class of Class X Certificates will be reduced by the aggregate amount of realized losses allocated to the class(es) of certificates that are component(s) of the notional amount of such class of Class X Certificates.

| |

Prepayment Premiums:

|

| A percentage of the Non-VRR Percentage of all prepayment premiums (either fixed prepayment premiums or yield maintenance amounts) collected on the Mortgage Loans will be allocated to each of the Class A-1, Class A-2, Class A-3, Class A-SB, Class A-4, Class A-5, Class A-M, Class B, Class C, Class D and Class E certificates (the “YM P&I Certificates”) then entitled to principal distributions, which percentage will be equal to the product of (a) a fraction, not greater than one, the numerator of which is the amount of principal distributed to such class on such Distribution Date and the denominator of which is the total amount of principal distributed to the holders of the Class A-1, Class A-2, Class A-3, Class A-SB, Class A-4, Class A-5, Class A-M, Class B, Class C, Class D, Class E, Class F, Class G and Class H certificates on such Distribution Date, and the Base Interest Fraction.

The “Base Interest Fraction” for any principal prepayment on any Mortgage Loan and for:

(A) any of the Class A-1 through Class E certificates with a Pass-Through Rate equal to either the WAC Rate or the WAC Rate less a specified rate, will be a fraction (not greater than one)(a) whose numerator is the greater of zero and the amount, if any, by which (i) the Pass-Through Rate on such class of certificates exceeds (ii) the yield rate (as provided by the master servicer) used in calculating the prepayment premium or yield maintenance charge, as applicable, with respect to such principal prepayment and (b) whose denominator is the amount, if any, by which (i) the Net Mortgage Rate on such Mortgage Loan during the related interest accrual period exceeds (ii) the yield rate (as provided by the master servicer) used in calculating the prepayment premium or yield maintenance charge, as applicable, with respect to such principal prepayment; provided, however, that if such yield rate is greater than or equal to the Net Mortgage Rate on such Mortgage Loan during the related interest accrual period, then the respective Base Interest Fraction will be zero; provided, further, that if such yield rate is greater than or equal to the Net Mortgage Rate on such Mortgage Loan during the related interest accrual period, but less than the Pass-Through Rate described in clause (a)(i) above, then the respective Base Interest Fraction will be one; and

|

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

14

Benchmark 2020-B16 Mortgage Trust

|

STRUCTURE OVERVIEW |

|

| (B) any of the Class A-1 through Class E certificates with a Pass-Through Rate equal to a fixed per annum rate, will be a fraction (not greater than one)(a) whose numerator is the greater of zero and the amount, if any, by which (i) the Pass-Through Rate on such class of certificates exceeds (ii) the yield rate (as provided by the master servicer) used in calculating the prepayment premium or yield maintenance charge, as applicable, with respect to such principal prepayment and (b) whose denominator is the amount, if any, by which (i) the Mortgage Rate on such Mortgage Loan (without regard to any increase in the interest rate of any ARD Loan after the related Anticipated Repayment Date, and net of the Administrative Cost Rate) during the related interest accrual period multiplied by 365/360 exceeds (ii) the yield rate (as provided by the master servicer) used in calculating the prepayment premium or yield maintenance charge, as applicable, with respect to such principal prepayment; provided, however, that if such yield rate is greater than or equal to the amount set forth in clause (b)(i) above, then the respective Base Interest Fraction will be zero; provided, further, that if such yield rate is greater than or equal to the amount set forth in clause (b)(i) above, but less than the Pass-Through Rate described in clause (a)(i) above, then the respective Base Interest Fraction will be one.

The remaining percentage of the Non-VRR Percentage of prepayment premiums will be allocated to the Class X-A, Class X-B and Class X-D certificates in the manner described in the Preliminary Prospectus. In general, this formula provides for an increase in the percentage of prepayment premiums allocated to the YM P&I Certificates then entitled to principal distributions relative to the Class X-A, Class X-B and Class X-D certificates as Discount Rates decrease and a decrease in the percentage allocated to such classes as Discount Rates rise.

|

Whole Loans: |

| The mortgaged properties identified on Annex A-1 to the Preliminary Prospectus as Bellagio Hotel and Casino, Kings Plaza, 3500 Lacey, 560 Mission Street, 1633 Broadway, Starwood Industrial Portfolio, 650 Madison Avenue, 181 West Madison, 510 East 14th Street, 490-504 Myrtle Avenue and Giant Anchored Portfolio each secure both a mortgage loan to be included in the trust fund and one or more other companion loans that will not be included in the trust fund, each of which will be pari passu and/or subordinate in right of payment with the mortgage loan included in the trust fund. We refer to each such group of related loans as a “whole loan”.

As of the Closing Date, the pari passu companion loans and the subordinate companion loans are expected to be held by the party identified in “—Companion Loan Summary” above and the table titled “Whole Loan Control Notes and Non-Control Notes” in “Description of the Mortgage Pool—The Whole Loans—General” in the Preliminary Prospectus.

|

Control Rights and Directing Holder: |

| Controlling Class Certificateholders will generally have certain control rights over servicing matters with respect to each Serviced Mortgage Loan and any related Serviced Companion Loans. The majority owner or appointed representative of the class of Control Eligible Certificates that is the Controlling Class (such owner or representative, the “Directing Holder”) will be entitled to direct the Special Servicer to take, or refrain from taking certain actions with respect to each Serviced Mortgage Loan and any related Serviced Companion Loans. Furthermore, the Directing Holder will also have the right to receive notice and consent to certain material actions that the Master Servicer and the Special Servicer proposes to take with respect to each Serviced Mortgage Loan and any related Serviced Companion Loans.

It is expected that Ellington Management Group, LLC or its affiliate will be the initial Directing Holder with respect to each Serviced Mortgage Loan and any related Serviced Companion Loans.

For a description of the directing holder for each Non-Serviced Whole Loan, see “Description of the Mortgage Pool—The Whole Loans” and “Pooling and Servicing Agreement—The Directing Holder” in the Preliminary Prospectus.

|

Control Eligible Certificates: |

| Class F, Class G and Class H certificates.

|

| The Controlling Class will be the most subordinate class of Control Eligible Certificates then outstanding that has an aggregate Certificate Balance, as notionally reduced by any appraisal reduction amounts and any collateral deficiency amounts allocable to such class, equal to at least 25% of the initial Certificate Balance of such class; provided that if at any time the Certificate Balances of all Control Eligible Certificates, as notionally reduced by any appraisal reduction amounts (but without regard to any collateral deficiency amounts) allocable to such classes, have been reduced to zero, then the “Controlling Class” will be the most subordinate class of Control Eligible Certificates that has an aggregate principal balance greater than zero;

|

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

15

Benchmark 2020-B16 Mortgage Trust

|

STRUCTURE OVERVIEW |

| provided, further that if at any time the Certificate Balances of the Class A-1, Class A-2, Class A-3, Class A-SB, Class A-4, Class A-5, Class A-M, Class B, Class C, Class D and Class E certificates have been reduced to zero as a result of the allocation of principal payments on the Mortgage Loans, then the Controlling Class will be the most subordinate class of Control Eligible Certificates that has an aggregate Certificate Balance greater than zero (without regard to the application of appraisal reduction amounts or any collateral deficiency amounts to notionally reduce the Certificate Balance of such class).

The Controlling Class as of the Closing Date will be the Class H certificates.

| |

| Any class of Control Eligible Certificates that has been determined, as a result of appraisal reductions amounts and collateral deficiency amounts allocable to such class, to no longer be the Controlling Class.

| |

| Holders of the majority of any class of Control Eligible Certificates that is determined at any time of determination to no longer be the Controlling Class as a result of an allocation of appraisal reduction amounts and collateral deficiency amounts in respect of such class will have the right, at their sole expense, to require the Special Servicer to order a second appraisal for any Serviced Mortgage Loan for which an appraisal reduction event has occurred or as to which there exists a collateral deficiency amount. Upon receipt of the second appraisal, the Special Servicer will be required to send the appraisal to the Master Servicer, who will be required to recalculate the appraisal reduction amount or collateral deficiency amount based on the second appraisal, and if required by such recalculation, the Special Servicer will reinstate the Appraised-Out Class as the Controlling Class. The Holders of an Appraised-Out Class requesting a second appraisal will not be entitled to exercise any rights of the Controlling Class until such time, if any, as the class is reinstated as the Controlling Class.

| |

Control Termination Event: |

| Will occur with respect to any Mortgage Loan, Serviced Whole Loan or the Starwood Industrial Portfolio Whole Loan when the Class F certificates have a Certificate Balance (taking into account the application of any appraisal reduction amounts and collateral deficiency amounts to notionally reduce the Certificate Balance of such class) reduced to less than 25% of the initial Certificate Balance of that class; provided that a Control Termination Event will not be deemed to be continuing in the event the Certificate Balances of all Classes of Principal Balance Certificates other than the Control Eligible Certificates have been reduced to zero. With respect to an excluded loan relating to the Directing Holder, a Control Termination Event will be deemed to exist.

Upon the occurrence and the continuance of a Control Termination Event, the Directing Holder will no longer have any control rights. The Directing Holder will no longer have the right to direct certain actions of the Special Servicer and will no longer have consent rights with respect to certain material actions that the Master Servicer or Special Servicer proposes to take with respect to a Serviced Mortgage Loan and any related Serviced Companion Loans.

Upon the occurrence and continuation of a Control Termination Event, the Directing Holder will retain non-binding consultation rights with respect to certain material actions that the Special Servicer proposes to take with respect to a Serviced Mortgage Loan and any related Serviced Companion Loans. Such consultation rights will continue until the occurrence of a Consultation Termination Event.

|

| Will occur with respect to any Mortgage Loan, Serviced Whole Loan or Starwood Industrial Portfolio Whole Loan when there is no class of Control Eligible Certificates that has a then-outstanding Certificate Balance equal to at least 25% of the initial Certificate Balance of that class, in each case, without regard to the application of any appraisal reduction amounts and collateral deficiency amounts; provided that a Consultation Termination Event will not be deemed to be continuing in the event the Certificate Balances of all Classes of Principal Balance Certificates other than the Control Eligible Certificates have been reduced to zero. With respect to an excluded loan relating to the Directing Holder, a Consultation Termination Event will be deemed to exist.

Upon the occurrence and continuance of a Consultation Termination Event, the Directing Holder will have no rights under the PSA other than those rights that all Certificateholders have.

|