Exhibit 99.2

MD&A Management’s Discussion and Analysis | | | | This management’s discussion and analysis (MD&A) contains information to help you understand our business and financial performance. Information is as of March 1, 2019. This MD&A focuses on our Consolidated Financial Statements and Notes and includes a discussion of known risks and uncertainties relating to our business and the oilfield services sector. You should read this MD&A with the accompanying audited Consolidated Financial Statements and Notes, which have been prepared in accordance with International Financial Reporting Standards (IFRS) and with the information in Cautionary Statement About Forward-Looking Information and Statements on page 2. The terms we, us, our, Precision Drilling and Precision mean Precision Drilling Corporation and our subsidiaries and include any partnerships that we are part. All amounts are in Canadian dollars unless otherwise stated. |

| | | |

| | Precision Drilling Corporation 2018 | |

| | | |

1 | Management’s Discussion and Analysis |

CAUTIONARY STATEMENT ABOUT FORWARD-LOOKING INFORMATION AND STATEMENTS

We disclose forward-looking information to help current and prospective investors understand our future prospects.

Certain statements contained in this MD&A, including statements that contain words such as could, should, can, anticipate, estimate, intend, plan, expect, believe, will, may, continue, project, potential and similar expressions and statements relating to matters that are not historical facts constitute forward-looking information within the meaning of applicable Canadian securities legislation and forward-looking statements within the meaning of the safe harbor provisions of the United States Private Securities Litigation Reform Act of 1995 (collectively, forward-looking information and statements).

Our forward-looking information and statements in this MD&A include, but are not limited to, the following:

| ▪ | our outlook on oil and natural gas prices |

| ▪ | our expectations about drilling activity in North America and the demand for drilling rigs |

| ▪ | our capital expenditure plans for 2019 |

| ▪ | our 2019 strategic priorities |

| ▪ | the potential impact liquefied natural gas export development could have on North American drilling activity |

| ▪ | our expectations that new or newer rigs will enter the markets we currently operate in |

| ▪ | our ability to remain compliant with our senior secured credit facility financial debt covenants. |

The forward-looking information and statements are based on certain assumptions and analysis made by Precision in light of our experience and our perception of historical trends, current conditions and expected future developments as well as other factors we believe are appropriate in the circumstances. These include, among other things:

| ▪ | our ability to react to customer spending plans as a result of changes in oil and natural gas prices |

| ▪ | the status of current negotiations with our customers and vendors |

| ▪ | customer focus on safety performance |

| ▪ | existing term contracts are neither renewed or terminated prematurely |

| ▪ | continued market demand for drilling rigs |

| ▪ | our ability to deliver rigs to customers on a timely basis |

| ▪ | the general stability of the economic and political environment in the jurisdictions we operate in |

| ▪ | the impact of an increase/decrease in capital spending. |

Undue reliance should not be placed on forward-looking information and statements. Whether actual results, performance or achievements will conform to our expectations and predictions is subject to a number of known and unknown risks and uncertainties which could cause actual results to differ materially from our expectations. Such risks and uncertainties include, but are not limited to:

| ▪ | volatility in the price and demand for oil and natural gas |

| ▪ | fluctuations in the level of oil and natural gas exploration and development activities |

| ▪ | fluctuations in the demand for contract drilling, directional drilling, well servicing and ancillary oilfield services |

| ▪ | our customers’ inability to obtain adequate credit or financing to support their drilling and production activity |

| ▪ | changes in drilling and well servicing technology, which could reduce demand for certain rigs or put us at a competitive advantage |

| ▪ | shortages, delays and interruptions in the delivery of equipment supplies and other key inputs |

| ▪ | liquidity of the capital markets to fund customer drilling programs |

| ▪ | availability of cash flow, debt and equity sources to fund our capital and operating requirements, as needed |

| ▪ | the impact of weather and seasonal conditions on operations and facilities |

| ▪ | competitive operating risks inherent in contract drilling, directional drilling, well servicing and ancillary oilfield services |

| ▪ | ability to improve our rig technology to improve drilling efficiency |

| ▪ | general economic, market or business conditions |

| ▪ | the availability of qualified personnel and management |

| ▪ | a decline in our safety performance which could result in lower demand for our services |

| ▪ | changes in laws or regulations, including changes in environmental laws and regulations such as increased regulation of hydraulic fracturing or restrictions on the burning of fossil fuels and greenhouse gas emissions, which could have an adverse impact on the demand for oil and natural gas |

| ▪ | terrorism, social, civil and political unrest in the foreign jurisdictions where we operate |

Precision Drilling Corporation 2018 Annual Report | 2 |

| ▪ | fluctuations in foreign exchange, interest rates and tax rates, and |

| ▪ | other unforeseen conditions which could impact the use of services supplied by Precision and our ability to respond to such conditions. |

Readers are cautioned that the foregoing list of risk factors is not exhaustive. You can find more information about these and other factors that could affect our business, operations or financial results in reports on file with securities regulatory authorities from time to time, including but not limited to our annual information form (AIF) for the year ended December 31, 2018, which you can find in our profile on SEDAR (www.sedar.com) or in our profile on EDGAR ( www.sec.gov).

All of the forward-looking information and statements made in this MD&A are expressly qualified by these cautionary statements. There can be no assurance that actual results or developments that we anticipate will be realized. We caution you not to place undue reliance on forward-looking information and statements. The forward-looking information and statements made in this MD&A are made as of the date hereof. We will not necessarily update or revise this forward-looking information as a result of new information, future events or otherwise, unless we are required to by securities law.

NON-GAAP MEASURES

In this MD&A, we reference additional generally accepted accounting principles (GAAP) measures that are not defined terms under IFRS to assess performance because we believe they provide useful supplemental information to investors.

Adjusted EBITDA

We believe that adjusted EBITDA (earnings before income taxes, loss or gain on redemption and repurchase of unsecured senior notes, finance charges, foreign exchange, impairment of property, plant and equipment, impairment of goodwill and depreciation and amortization), as reported in our Consolidated Statement of Loss, is a useful measure, because it gives an indication of the results from our principal business activities prior to consideration of how our activities are financed and the impact of foreign exchange, taxation and depreciation and amortization charges.

Covenant EBITDA

Covenant EBITDA, as defined in our Senior Credit Facility agreement, is used in determining the Corporation’s compliance with its covenants. Covenant EBITDA differs from Adjusted EBITDA by the exclusion of bad debt expense, restructuring costs and certain foreign exchange amounts.

Operating Loss

We believe that operating loss is a useful measure because it provides an indication of the results of our principal business activities before consideration of how those activities are financed and the impact of foreign exchange and taxation. Operating loss is calculated as follows:

Year ended December 31 (thousands of dollars) | | 2018 | | | 2017 | | | 2016 | |

Revenue | | | 1,541,189 | | | | 1,321,224 | | | | 951,411 | |

Expenses: | | | | | | | | | | | | |

Operating | | | 1,067,871 | | | | 926,171 | | | | 607,295 | |

General and administrative | | | 112,387 | | | | 90,072 | | | | 110,287 | |

Restructuring | | | - | | | | - | | | | 5,754 | |

Other recoveries | | | (14,200 | ) | | | - | | | | - | |

Depreciation and amortization | | | 365,660 | | | | 377,746 | | | | 391,659 | |

Impairment of goodwill | | | 207,544 | | | | - | | | | - | |

Impairment of property, plant and equipment | | | - | | | | 15,313 | | | | - | |

Gain on re-measurement of property, plant and equipment | | | - | | | | - | | | | (7,605 | ) |

Operating loss | | | (198,073 | ) | | | (88,078 | ) | | | (155,979 | ) |

Foreign exchange | | | 4,017 | | | | (2,970 | ) | | | 6,008 | |

Finance charges | | | 127,178 | | | | 137,928 | | | | 146,360 | |

Loss (gain) on redemption and repurchase of unsecured senior notes | | | (5,672 | ) | | | 9,021 | | | | 239 | |

Income taxes | | | (29,326 | ) | | | (100,021 | ) | | | (153,031 | ) |

Net loss | | | (294,270 | ) | | | (132,036 | ) | | | (155,555 | ) |

| |

3 | Management’s Discussion and Analysis |

Funds Provided by (Used In) Operations

We believe that funds provided by (used in) operations, as reported in our Consolidated Statements of Cash Flow, is a useful measure because it provides an indication of the funds our principal business activities generate prior to consideration of working capital, which is primarily made up of highly liquid balances.

Working Capital

We define working capital as current assets less current liabilities as reported in our Consolidated Statement of Financial Position.

Precision Drilling Corporation 2018 Annual Report | 4 |

| | | | | |

| About Precision | | Management’s Discussion and Analysis | | |

| | | | | |

Precision Drilling Corporation provides onshore drilling and completion and production services to exploration and production companies in the oil and natural gas industry.

Headquartered in Calgary, Alberta, Canada, we are a large oilfield services company with broad geographic scope in North America. We also have operations in the Middle East. Our common shares trade on the Toronto Stock Exchange, under the symbol PD, and on the New York Stock Exchange, under the symbol PDS. | | Vision Our vision is to be globally recognized as the High Performance, High Value provider of land drilling services. You can read about our strategic priorities for 2019 on page 24. |

COMPETITIVE ADVANTAGE

From our founding as a private oilfield drilling contractor in the 1950s, Precision has grown to become one of the most active drillers in North America. Our competitive advantage is underpinned by five distinguishing features:

| ▪ | a competitive operating model that drives efficiency, quality and cost discipline |

| ▪ | a culture focused on safety and performance |

| ▪ | size and scale of operations that provide higher margins and better service capabilities |

| ▪ | high quality standardized equipment and control system with process automation control and advanced digital backbone systems to deliver efficient, consistent and safe drilling services, and |

| ▪ | a capital structure that provides long-term stability, flexibility and liquidity that allows us to take advantage of business cycle opportunities. |

CORPORATE GOVERNANCE

At Precision, we believe that a transparent culture of corporate governance and ethical behaviour in decision-making is fundamental to the way we do business.

We have a diverse and experienced Board of Directors (Board). Our directors have a history of achievement and an effective mix of skills, knowledge, and business experience. The directors oversee the conduct of our business, provide oversight in support of future operations and monitor regulatory developments and governance best practices in Canada and the U.S. Our Board also reviews our governance charters, guidelines, policies and procedures to make sure they are appropriate and that we maintain high governance standards.

Our Board has established three standing committees, comprised of independent directors, to help it carry out its responsibilities effectively:

| ▪ | Corporate Governance, Nominating and Risk Committee, and |

| ▪ | Human Resources and Compensation Committee. |

The Board may also create special ad hoc committees from time to time to deal with important matters that arise.

You can find more information about our approach to governance in our management information circular, available on our website (www.precisiondrilling.com).

| |

5 | Management’s Discussion and Analysis |

TWO BUSINESS SEGMENTS

We operate our business in two segments, supported by vertically integrated business support systems.

Precision Drilling Corporation |

| | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | |

| Contract Drilling Services | | | | Completion and Production Services |

| | | | | | | | | | | | | | | | |

| ● | Drilling rig operations | | | | | ● | Canada and U.S. |

| | – | Canada | | | | | | | | | – | Service rigs | | | |

| | – | U.S. | | | | | | | | | | | | | |

| | – | International | | | | | | | | ● | Canada |

| ● | Directional drilling operations | | | | | – | Snubbing | | | |

| | – | Canada | | | | | | | | | – | Camps and catering | | | |

| | – | U.S. | | | | | | | | | – | Equipment Rentals | | | |

| | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | |

| Business support systems | | | | | | | | | | |

| | | | | | | | | | | | | | | | |

| ● | Sales and marketing | ● | Procurement and distribution | ● | Manufacturing | ● | Equipment maintenance and certification | ● | Engineering | |

| | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | |

| Corporate support | | | | | | | | |

| | | | | | | | | | | | | | | | |

| ● | Information systems | ● | Health, safety and environment | ● | Human resources | ● | Finance | ● | Legal and enterprise risk management |

| | | | | | | | | | | | | | | | |

Precision Drilling Corporation 2018 Annual Report | 6 |

Contract Drilling Services

We provide onshore drilling services to exploration and production companies in the oil and natural gas industry, operating in Canada, the U.S. and internationally.

We are a large, multi-basin oilfield operator servicing approximately 26% of the active land drilling market in Canada and 7% of the active U.S. market. We also have an international presence with operations in the Middle East and Mexico.

At December 31, 2018, our Contract Drilling Services segment consisted of:

| ▪ | 236 land drilling rigs, including: |

| – | 2 in the Kurdistan region of Iraq |

| – | 1 in the country of Georgia |

| ▪ | directional drilling services in Canada and the U.S. |

| ▪ | engineering, manufacturing and repair services, primarily for Precision’s operations |

| ▪ | centralized procurement, inventory and distribution of consumable supplies for our global operations |

| ▪ | 18 Canadian and four U.S. land drilling rigs designated as held for sale . |

At December 31, 2018, we had 236 Super Series drilling rigs. Our Super Series rigs are highly mobile and mechanized, which make them safer and more efficient in drilling directional and horizontal wells than older generation drilling rigs. Our Super Series rigs have a broad range of features to meet a diverse range of customer needs with a focus on high efficiency development drilling applications, from drilling shallow- to medium-depth wells to deeper, extended reach horizontal well bores and all depths of conventional wells. Available features include alternating current (AC) power, digital control systems, integrated top drive, omni-directional pad walking systems for multi-pad well drilling, highly mechanized pipe handling, and high capacity mud pumps.

| |

7 | Management’s Discussion and Analysis |

Completion and Production Services

We provide well completion, workover, abandonment, and re-entry preparation services, as well as snubbing units for pressure control services and equipment rentals to oil and natural gas exploration and production companies in Canada and the U.S.

On an operating hour basis in 2018, we serviced approximately 12% of the well completion and workover service rig market demand in Canada and less than 1% in the U.S.

At December 31, 2018, our Completion and Production Services segment consisted of:

| ∎ | 198 well completion and workover service rigs, including: |

| ∎ | 12 snubbing units in Canada |

| ∎ | approximately 1,700 oilfield rental items, including surface storage, small-flow wastewater treatment, power generation, and solids control equipment, primarily in Canada |

| ∎ | 132 wellsite accommodation units in Canada |

| ∎ | 43 drill camps and four base camps in Canada |

| ∎ | 10 large-flow wastewater treatment units, 22 pumphouses and eight potable water production units in Canada. |

Precision Drilling Corporation 2018 Annual Report | 8 |

| | | | | |

| 2018 Highlights and Outlook | | Management’s Discussion and Analysis | | |

| | | | | |

Adjusted EBITDA, funds provided by operations and working capital are Non-GAAP measures. See page 3 for more information.

Financial Highlights

Year ended December 31 (thousands of dollars, except where noted) | | 2018 | | | % increase/ (decrease) | | | 2017 | | | % increase/ (decrease) | | | 2016 | | | % increase/ (decrease) | |

Revenue | | | 1,541,189 | | | | 16.6 | | | | 1,321,224 | | | | 31.7 | | | | 1,003,233 | | | | (38.6 | ) |

Adjusted EBITDA | | | 375,131 | | | | 23.0 | | | | 304,981 | | | | 33.7 | | | | 228,075 | | | | (51.9 | ) |

Adjusted EBITDA % of revenue | | | 24.3 | % | | | | | | | 23.1 | % | | | | | | | 22.7 | % | | | | |

Net loss | | | (294,270 | ) | | | 122.9 | | | | (132,036 | ) | | | (15.1 | ) | | | (155,555 | ) | | | (57.2 | ) |

Cash provided by operations | | | 293,334 | | | | 151.7 | | | | 116,555 | | | | (4.9 | ) | | | 122,508 | | | | (76.3 | ) |

Funds provided by operations | | | 311,214 | | | | 69.2 | | | | 183,935 | | | | 74.6 | | | | 105,375 | | | | (70.5 | ) |

Investing activities | | | | | | | | | | | | | | | | | | | | | | | | |

Capital spending | | | | | | | | | | | | | | | | | | | | | | | | |

Expansion | | | 35,444 | | | | 196.7 | | | | 11,946 | | | | (92.0 | ) | | | 148,887 | | | | (58.8 | ) |

Upgrade | | | 30,757 | | | | (17.1 | ) | | | 37,086 | | | | 86.7 | | | | 19,862 | | | | (59.0 | ) |

Maintenance and infrastructure | | | 48,375 | | | | 87.6 | | | | 25,791 | | | | (25.7 | ) | | | 34,723 | | | | (28.8 | ) |

Intangibles | | | 11,567 | | | | (50.1 | ) | | | 23,179 | | | n/m | | | | — | | | | — | |

Proceeds on sale | | | (24,457 | ) | | | 64.8 | | | | (14,841 | ) | | | 89.3 | | | | (7,840 | ) | | | (19.9 | ) |

Net capital spending | | | 101,686 | | | | 22.3 | | | | 83,161 | | | | (57.5 | ) | | | 195,632 | | | | (56.4 | ) |

Business acquisition | | | — | | | | — | | | | — | | | (100.0 | ) | | | 12,200 | | | n/m | |

Loss per share ($) | | | | | | | | | | | | | | | | | | | | | | | | |

Basic and diluted | | | (1.00 | ) | | | 122.2 | | | | (0.45 | ) | | | (15.1 | ) | | | (0.53 | ) | | | (57.3 | ) |

n/m – calculation not meaningful.

Operating Highlights

Year ended December 31 | | 2018 | | | % increase/ (decrease) | | | 2017 | | | % increase/ (decrease) | | | 2016 | | | % increase/ (decrease) | |

Contract drilling rig fleet | | | 236 | | | | (7.8 | ) | | | 256 | | | | 0.4 | | | | 255 | | | | 1.6 | |

Drilling rig utilization days | | | | | | | | | | | | | | | | | | | | | | | | |

Canada | | | 18,617 | | | | (1.4 | ) | | | 18,883 | | | | 48.4 | | | | 12,722 | | | | (26.2 | ) |

U.S. | | | 26,714 | | | | 30.4 | | | | 20,479 | | | | 80.5 | | | | 11,343 | | | | (46.4 | ) |

International | | | 2,920 | | | | - | | | | 2,920 | | | | 4.8 | | | | 2,786 | | | | (31.8 | ) |

Revenue per utilization day | | | | | | | | | | | | | | | | | | | | | | | | |

Canada (Cdn$) | | | 21,644 | | | | 2.4 | | | | 21,143 | | | | (13.7 | ) | | | 24,509 | | | | (9.1 | ) |

U.S. (US$) | | | 21,864 | | | | 10.1 | | | | 19,861 | | | | (24.0 | ) | | | 26,145 | | | | (2.2 | ) |

International (US$) | | | 50,469 | | | | 0.5 | | | | 50,240 | | | | 9.8 | | | | 45,753 | | | | 5.2 | |

Operating cost per utilization day | | | | | | | | | | | | | | | | | | | | | | | | |

Canada (Cdn$) | | | 14,493 | | | | 10.3 | | | | 13,140 | | | | (7.8 | ) | | | 14,258 | | | | (4.2 | ) |

U.S. (US$) | | | 14,337 | | | | 3.5 | | | | 13,846 | | | | (10.9 | ) | | | 15,547 | | | | (0.5 | ) |

| | | | | | | | | | | | | | | | | | | | | | | | |

Service rig fleet | | | 210 | | | | - | | | | 210 | | | | 1.4 | | | | 207 | | | | 27.0 | |

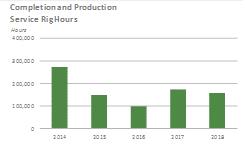

Service rig operating hours | | | 157,467 | | | | (8.9 | ) | | | 172,848 | | | | 73.8 | | | | 99,451 | | | | (33.5 | ) |

Revenue per operating hour (Cdn$) | | | 709 | | | | 11.3 | | | | 637 | | | | (1.4 | ) | | | 646 | | | | (17.6 | ) |

| |

9 | Management’s Discussion and Analysis |

Financial Position and Ratios

(thousands of dollars, except ratios) | | December 31, 2018 | | | December 31, 2017 | | | December 31, 2016 | |

Working capital(1) | | | 240,539 | | | | 232,121 | | | | 230,874 | |

Working capital ratio | | | 1.9 | | | | 2.1 | | | | 2.0 | |

Long-term debt | | | 1,706,253 | | | | 1,730,437 | | | | 1,906,934 | |

Total long-term financial liabilities | | | 1,723,350 | | | | 1,754,059 | | | | 1,946,742 | |

Total assets | | | 3,636,043 | | | | 3,892,931 | | | | 4,324,214 | |

Enterprise value(2) | | | 2,305,890 | | | | 2,782,596 | | | | 3,937,737 | |

Long-term debt to long-term debt plus equity(3) | | | 0.5 | | | | 0.5 | | | | 0.5 | |

Long-term debt to cash provided by operations | | | 5.8 | | | | 14.8 | | | | 15.6 | |

Long-term debt to enterprise value | | | 0.7 | | | | 0.6 | | | | 0.5 | |

(1) | See NON-GAAP MEASURES on page 3 of this report. |

(2) | Share price multiplied by the number of shares outstanding plus long-term debt minus cash. See page 39 for more information. |

(3) | Net of unamortized debt issue costs. |

2018 OVERVIEW

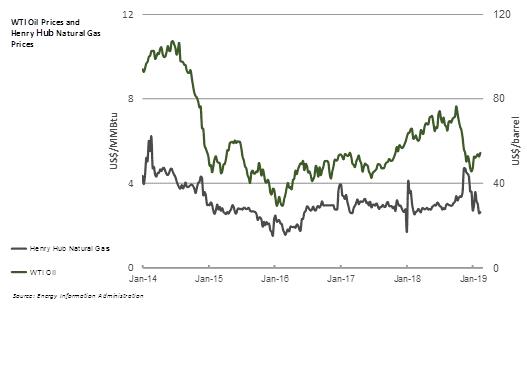

While global commodity prices strengthened in 2018, the year was beleaguered with extreme volatility, particularly in the Canadian market. In the U.S., West Texas Intermediate (WTI) oil prices averaged US$65 per barrel and Henry Hub natural gas prices averaged US$3.07 per MMBtu, levels supportive of unconventional resource development. However, a volatile and uncertain oil price outlook and renewed focus on free cash flow has encouraged conservatism in customer spending. In Canada, acute pipeline takeaway shortfalls and growing uncertainty in regulatory policy caused immense pressure on regional commodity prices and subsequent activity levels, particularly towards the end of the year. In early December the Alberta government instituted mandatory oil production curtailments as a vehicle to address regional oil price differentials relative to WTI oil prices.

For the year ended December 31, 2018, our net loss was $294 million, or $1.00 per diluted share, compared with a net loss of $132 million, or $0.45 per diluted share in 2017. During 2018 we incurred a goodwill impairment charge of $208 million related to our Canada contract drilling and U.S. directional drilling businesses, that after tax, increased our net loss by $199 million and net loss per diluted share by $0.68.

Revenue in 2018 was $1,541 million, or 17% higher than in 2017, mainly due to higher activity and day rates in our U.S. contract drilling operations. Contract Drilling Services revenue was up 19%, while Completion and Production Services revenue was down 2%. Our U.S. drilling activity increased 30% in 2018 while Canadian and international drilling activity remained consistent with 2017.

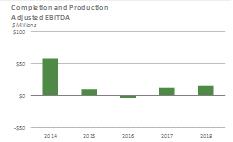

Adjusted EBITDA in 2018 was $375 million, or 23% higher than in 2017. Our Adjusted EBITDA margin was 24%, slightly higher than 2017. Adjusted EBITDA improved in 2018 primarily due to increased U.S. drilling activity and day rates. Adjusted EBITDA as a percentage of segment revenue for the year in our Contract Drilling Services segment was 30%, compared with 29% in the prior year, while Adjusted EBITDA as a percentage of segment revenue from our Completion and Production Services segment was 10%, compared to 8% in 2017. The improved percentages achieved in our Completion and Production Services segment were the result of improved day rates. Our portfolio of term customer contracts, a scalable operating cost structure, and economies achieved through vertical integration of the supply chain help us manage our Adjusted EBITDA percentages.

Capital expenditures for the purchase of property, plant and equipment were $126 million in 2018, an increase of $28 million over 2017. Capital spending for 2018 included $66 million for upgrade and expansion capital, $48 million for the maintenance of existing assets and infrastructure and $12 million for intangibles related to a new enterprise-wide resource planning (ERP) system.

In 2018 we continued to invest in our fleet adding two new-build drilling rigs in the U.S., completing 31 rig upgrades, and commencing the build of our sixth Kuwait rig, all of which were backed by long-term contracts and within a constrained expansion and upgrade capital spend of approximately $66 million.

Under IFRS, we are required to assess the carrying value of assets in our cash-generating units (CGUs) containing goodwill annually and when indicators of impairment exist. Due to the decrease in oil and natural gas well drilling in Canada and the outlook for activity in Canada and in our directional drilling division in the U.S., we recognized a $208 million goodwill impairment charge. The impairment charge represents the full amount of goodwill attributable to our Canadian contract drilling operation and our U.S. directional drilling operations.

During the year we redeemed US$80 million and repurchased and cancelled US$3 million of our 6.5% unsecured senior notes due 2021 and repurchased and cancelled US$49 million principal amount of our 5.25% unsecured senior notes due 2024.

Precision Drilling Corporation 2018 Annual Report | 10 |

OUTLOOK

Contracts

Term customer contracts provide a base level of activity and revenue. As of March 1, 2019, we had term contracts in place for an average of 54 rigs: six in Canada, 40 in the U.S. and eight internationally for 2019. In Canada, term contracted rigs normally generate 250 utilization days per rig year because of the seasonal nature of wellsite access. In most regions in the U.S. and internationally term contracts normally generate | | In 2018, approximately 49% of our total contract drilling revenue was generated from rigs under term contracts. |

365 utilization days per rig year. In 2018, we had an average of 63 drilling rigs working under term contracts and revenue from these contracts was approximately 49% of our total contract drilling revenue for the year.

Pricing, Demand and Utilization

Volatility in global crude prices remained a key theme throughout 2018, particularly towards the end of the year with concerns over the health of the global economy, ongoing trade wars, varying degrees of OPEC and non-OPEC production cuts and continued growth in U.S. production driving uncertainty in supply and demand fundamentals. The WTI oil price closed the year at US$45.41 per barrel. Since then, WTI has hovered in the mid-US$50’s per barrel range and closed at US$55.80 per barrel on March 1, 2019. A similar phenomenon played out in other grades of crude such as Western Canada Select (WCS) and Permian regional pricing whereby mid-to late 2018 differentials widened to extreme levels largely as a result of takeaway capacity constraints in each respective market. Year-to-date in 2019 differentials have narrowed and are expected to revert to more normalized levels in the Permian with incremental takeaway capacity added mid-year, while in Canada WCS differentials are expected to remain volatile but show greater stability with the province of Alberta having instituted production constraints at the end of 2018 in addition to incremental rail capacity and potential increased pipeline takeaway capacity.

Natural gas prices have remained relatively rangebound by historical standards as growth in associated gas from unconventional oil development, higher than average storage levels, infrastructure constraints and the lack of a fully developed export market from North America continue to cap pricing. Natural gas prices in the U.S., referenced by the Henry Hub price on the New York Mercantile Exchange (NYMEX), averaged US$3.07 per MMBtu in 2018, and closed the year at US$2.94 per MMBtu. In Canada, the AECO natural gas benchmark experienced price weakness and volatility in 2018 particularly in the summer months driven by plant maintenance, pipeline shut-ins, and challenges exporting natural gas as a Canadian LNG export industry has not been developed leaving a well-supplied U.S. market as the only export option for Canadian natural gas. Differences between NYMEX (U.S.) prices and AECO (Canada) prices are expected to continue if Canadian export markets remained challenged.

The rig count at March 1, 2019 was 30% lower in Canada than it was a year ago while the year-to-date rig count has averaged 48% less than 2018. Activity for the remainder of the year is expected to be determined by the strength in commodity prices and the resulting oil and natural gas customer budgets.

In the U.S., strengthening crude prices have resulted in increased drilling activity and demand for our rigs. As a result, spot market pricing and activity each increased throughout 2018 and have improved further year-to-date in 2019. As of March 1, 2019, the rig count was 5% higher than the same time last year and has averaged 10% higher year-to-date compared to 2018. Activity levels for the remainder of 2019 are expected to be dependent on commodity prices and resulting customer budgets.

The Canadian to U.S. dollar exchange rate averaged US$0.7712 (Cdn$/US$1.2966) for 2018 and closed the year at US$0.7325 (Cdn$/US$1.36521). The lower Canadian dollar relative to the U.S. dollar serves to partially offset the impact of lower U.S. dollar-denominated crude oil and natural gas prices for Canadian exploration and production companies. Year to date, the Canadian dollar has strengthened against the U.S. dollar and as of March 1, 2019, the Canadian dollar closed at US$0.7518.

International

We currently have eight rigs working on term contracts with five in Kuwait and three in the Kingdom of Saudi Arabia. During 2018, we announced the award of one new-build ST-3000 drilling rig in Kuwait under a five year take-or-pay contract with an optional one-year extension. We expect the sixth rig to commence drilling operations in the third quarter of 2019.

| |

11 | Management’s Discussion and Analysis |

Upgrading the Fleet

The industry trend toward more complex drilling programs has accelerated the retirement of older generation, less capable rigs. Over the past several years, we and some of our competitors have been upgrading the drilling rig fleet by building new rigs, upgrading existing rigs, and decommissioning lower capacity rigs. We believe this retooling of the industry-wide fleet has been making legacy rigs virtually obsolete in North America.

With the completion of our new-build rig program and upgrades of existing rigs, our fleet consisted of 236 Super Series rigs and 22 rigs identified and held for sale as at December 31, 2018.

Capital Spending

Capital spending in 2019 is expected to be $169 million and includes $53 million for sustaining and infrastructure and $116 million for upgrade and expansion, approximately $68 million of which relates to the completion of our sixth new-build rig in Kuwait. We expect that the $169 million will be split $161 million in the Contract Drilling Services segment, $6 million in the Completion and Production Services segment and $2 million to the Corporate segment.

Precision Drilling Corporation 2018 Annual Report | 12 |

| |

13 | Management’s Discussion and Analysis |

| | | | | |

| Understanding Our Business Drivers | | Management’s Discussion and Analysis | | |

| | | | | |

THE ENERGY INDUSTRY

Precision operates in the energy services business, which is an inherently challenging cyclical sector of the energy industry. We depend on oil and natural gas exploration and production companies to contract our services as part of their exploration and development activities. The economics of their businesses are dictated by the current and expected future margin between their finding and development costs and the eventual market price for the commodities they produce: crude oil, natural gas, and natural gas liquids.

Conventional / Unconventional wells

Oil and natural gas reservoirs can be conventional, where a vertical well is drilled into a highly pressurized reservoir allowing the oil and natural gas to flow freely shortly after completing the drilling process. Unconventional reservoirs are exploited by drilling a vertical section of a well followed by a horizontal section to access a large portion of the oil or natural gas formation. These “unconventional” or “shale” reservoirs are typically lower pressure and require extra stimulation to generate production. The practice of “hydraulic fracturing” follows the unconventional drilling process with high horsepower equipment pumping water and proppant down a wellbore at high pressure to frack the rock, releasing hydrocarbons. The vast majority of the wells we drill in North America are unconventional. We are not involved in the hydraulic fracturing of a well.

Commodity Prices

Cash flow to fund exploration and development is dependent on commodity prices: higher prices increase cash flow and encourage investment and when prices decline, the opposite is true.

Oil can be transported relatively easily, so it is generally priced in a global market that is influenced by an array of economic and political factors. Higher oil prices typically result in stronger demand for drilling services with funding for drilling programs directed toward the most economically attractive drilling opportunities. As the volume of unconventional oil development has dramatically increased over the past decade, generating efficiencies through industrialized processes, more capital has been directed toward unconventional oil development in North America, reflecting the region’s competitiveness globally.

Natural gas and natural gas liquids continue to be priced more regionally. In North America, natural gas demand largely depends on the weather. Colder winter temperatures, and to a lesser extent, warmer summer temperatures, result in greater natural gas demand. Other demand drivers, such as natural gas fired power generation, industrial applications, and transportation, have shown positive growth over the past several years driven by a preference for natural gas over coal, and lower prices. The planned liquefied natural gas (LNG) export from Canada and continued development in the U.S. could serve as a catalyst for natural gas directed drilling activity over the medium to long term.

The key natural gas price driver continues to be increased production from unconventional shale gas drilling. Since the winter of 2014, pricing for natural gas in North America has generally been depressed, as supplies of unconventional natural gas have increased, and current inventory levels are viewed as adequate to keep North American markets well supplied.

Precision Drilling Corporation 2018 Annual Report | 14 |

Average Oil and Natural Gas Prices

| | 2018 | | | 2017 | | | 2016 | |

Oil | | | | | | | | | | | | |

WTI (US$ per barrel) | | | 64.88 | | | | 50.95 | | | | 43.30 | |

Natural gas | | | | | | | | | | | | |

Canada | | | | | | | | | | | | |

AECO ($ per MMBtu) | | | 1.49 | | | | 2.16 | | | | 2.14 | |

U.S. | | | | | | | | | | | | |

Henry Hub (US$ per MMBtu) | | | 3.12 | | | | 2.98 | | | | 2.48 | |

Source: WTI and Henry; Hub Energy Information Administration, AECO; Gas Alberta Inc. | | | | | | | | | | | | |

New Technology

North American exploration and production companies, which comprise the majority of our customer base, have been adapting to a lower commodity price environment and are increasingly focused on drilling and completion efficiency. Most of these companies have adopted large-scale industrialization techniques, utilizing multi-well pads and high-efficiency downhole and surface drilling systems to improve efficiency. Over the past several years, drilling rig enhancements have focused on equipment upgrades, such as walking systems, AC controls and increased fluid pumping capacity. More recently, customer focus has been shifting to rig automation technologies to deliver increased efficiency, consistency and predictability of results, which customers desire in their development-style drilling programs. Exploration and production companies have an increasing appetite for these technologies as they provide an opportunity to push the limits of efficiency and consistency, common in industrialized processes.

Our technology strategy is well-aligned with customer efficiency objectives. We leverage our existing base of AC control systems installed on over 100 of our Super Series drilling rigs. These standardized control systems enable us to reliably mass deploy advanced software systems capable of delivering leading-edge digital automation, significantly boosting efficiency of the well construction process. Our technology strategy is centered around partnering with industry experts which allows us to deliver an

| |

15 | Management’s Discussion and Analysis |

extensive suite of offerings to our customers with minimal research and development capital. Our digital technology strategy is currently focused on four fundamentals:

1. | Standardized Control System Platform |

We leverage our standardized rig equipment and control system to deploy a fully integrated Process Automation Control system (PAC), which allows us to consistently implement best practices to eliminate human variance and human error, resulting in significantly improved drilling efficiency. In addition to built-in process automation routines, PAC also hosts Precision Drilling Apps (PD Apps), which leverage advanced algorithms and exploitation of various machine learning techniques to improve complex drilling processes. The standard platform is encouraging innovation in the drilling app space by attracting innovative solutions from customers and third parties inside and outside the oil and gas industry. We installed our first PAC system in late 2016 and currently have 31 PAC systems deployed in the field and more than 15 PD Apps in the trial phase or in development, making Precision an industry leader in automation technology.

2. | Data Collection and Analytics |

Our digital rig control systems with PAC are now generating well above 1 GB/min of data, versus a limited number of data channels from traditional Electronic Data Recorders, knowns as EDR systems. We have a robust data analytics strategy with a dedicated analytics team (PD Analytics) focused on improving rig performance and financial returns through commercialization of performance data.

3. | Digitally Enabled Services |

Our advanced digital infrastructure helps automate repetitive tasks for the driller, freeing up time for the driller to address more value-added responsibilities. For example, we have introduced our Directional Guidance System (DGS) aiming to either replace directional drillers on the wellsite through an advanced algorithm delivered through a PD App and remote support. To date, we have successfully drilled more than 200 wells using this technology and believe these types of solutions will eventually become industry standard.

4. | Leading-Edge Corporate-Wide Data Systems and Technology Culture |

In 2018, we successfully implemented the latest version of SAP S/4HANA to fully realize the benefits of the system’s integration with our digital service delivery platform. This robust SAP enterprise system is built to support the increased data flows from the field, provided by our PAC systems. Precision committed to a digital technology strategy nearly three years ago, enabling us to build a strong digital mindset within the company at all levels.

Our combination of High Performance standardized rig fleet, integrated PAC system, PD Apps and PD Analytics position us to help our customers achieve their efficiency goals and generate strong returns for our shareholders through service differentiation.

Precision Drilling Corporation 2018 Annual Report | 16 |

Natural gas production in Canada has been flat because of lower natural gas directed drilling due to pricing pressure and Canada’s lack of an export market other than the U.S.

| |

17 | Management’s Discussion and Analysis |

Drilling Activity

Following a decline in activity in 2015 and 2016, the North American land drilling market showed increased activity levels in 2017 and 2018, particularly in the U.S., as customer demand improved with higher oil prices.

In 2018, the industry drilled 6,781 wells in western Canada, compared with 6,959 in 2017 and 3,963 in 2016. Total industry drilling operating days were 64,491 in 2018 compared with 66,138 in 2017 and 42,391 in 2016. Average industry drilling operating days per well was 9.5, the same as in 2017 and slightly lower than 10.7 in 2016. From 2017 to 2018 the average depth of a well increased 4% compared with an increase of 5% from 2016 to 2017.

In 2018 approximately 19,300 wells were started onshore in the U.S., compared with approximately 15,800 in 2017 and 11,200 in 2016.

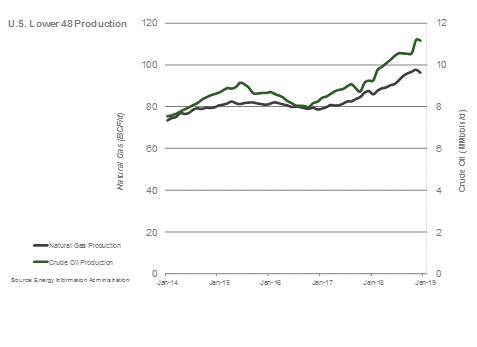

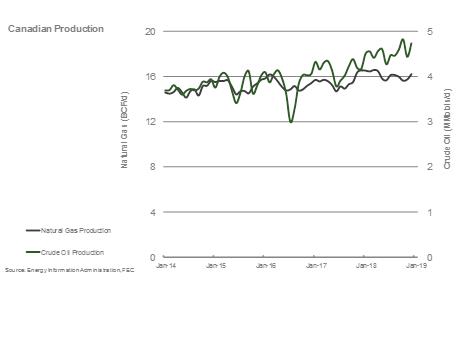

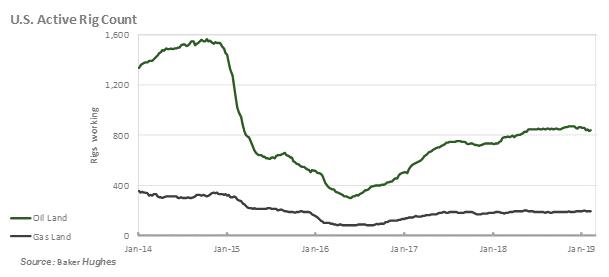

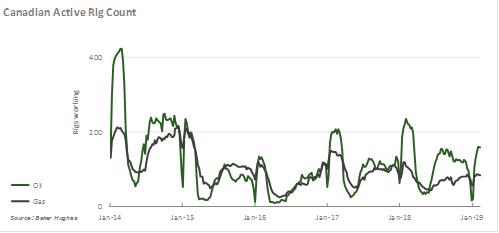

In Canada, there has been relative strength in natural gas liquids and light tight oil drilling activity in the deeper basins of northwestern Alberta and northeastern British Columbia, while in the U.S. the bias towards oil-directed drilling continues. In 2018, approximately 63% of the Canadian industry’s active rigs and 81% of the U.S. industry’s active rigs were drilling for oil targets, compared with 53% for Canada and 80% for the U.S. in 2017.

The graphs below show the shift in drilling activity to oil targets since 2014, in both the U.S. and Canada. The Canadian drilling rig activity graph also shows how Canadian drilling activity fluctuates with the seasons, a market dynamic that generally is not present in the U.S.

Precision Drilling Corporation 2018 Annual Report | 18 |

A COMPETITIVE OPERATING MODEL

The contract drilling business is highly competitive, with many industry participants. We compete for drilling contracts that are often awarded in a competitive bid process. We believe potential customers focus on pricing and rig availability when selecting a drilling contractor, but also consider many other things, including drilling capabilities, condition of rigs, quality of rig crews, breadth of service, technology offering, and safety record, among others.

Providing High Performance, High Value services to our customers is the core of our competitive strategy. We deliver High Performance through passionate people supported by quality business systems, drilling technology, equipment and infrastructure designed to optimize results and reduce risks. We create High Value by operating safely and sustainably, lowering our customers’ risks and costs while improving efficiency, developing our people, and generating superior financial returns for our investors.

Operating Efficiency

We keep customer well costs down by maximizing the efficiency of operations in several ways:

| ∎ | using innovative and advanced drilling technology that is efficient and reduces costs |

| ∎ | having equipment that is geographically dispersed, reliable and well maintained |

| ∎ | monitoring our equipment to minimize mechanical downtime |

| ∎ | managing operations effectively to keep non-productive time to a minimum |

| ∎ | staffing our rigs with well-trained crews with performance measured against defined competencies, and |

| ∎ | compensating our executives and eligible employees based on performance against safety, operational, employee retention, and financial measures. |

Efficient, Cost-Reducing Technologies

We focus on providing efficient, cost-reducing drilling technologies. Design innovations and technology improvements, such as multi-well pad capability and rapid mobility between wells, capture incremental time savings during the drilling process.

Precision has invested over $3 billion in its drilling rig fleet since 2010, adding over 120 Super Series drilling rigs during the period. With one of the newest and most technically capable fleets in North America and the Middle East, Precision’s Super Series rigs have been designed for industrial-style drilling: highly efficient; mobile; safe; controllable; upgradable; and able to act as a platform for technology delivery to the well location. Precision has completed several relatively low dollar cost upgrades over the past several years including additions of walking systems, higher pressure and capacity mud pumps, increased setback capacity and PAC technology. Precision’s Super Series drilling rig fleet has the features needed to meet essentially all the industrial-style drilling requirements of our customers in North America and deep, high-pressure drilling projects internationally.

| |

19 | Management’s Discussion and Analysis |

Broad Geographic Footprint

Geographic proximity and fleet versatility support the High Performance, High Value services we provide to our customers. Our large fleet of rigs is strategically deployed across the most active drilling regions in North America, including all major unconventional oil and natural gas basins.

Managing Downtime

Minimizing downtime is a key operating metric for us and our customers. Reliable and well-maintained equipment minimizes downtime and non-productive time during operations. We manage mechanical downtime through preventative maintenance programs, detailed inspection processes, an extensive fleet of strategically-located spare equipment, and an in-house supply chain. We minimize non-productive time (to move, rig-up and rig-out) by utilizing walking systems, reducing the number of move loads per rig, and using mechanized equipment for safer and quicker rig component connections.

Tracking Our Results

We unitize key financial information per day and per hour and compare these measures to established benchmarks and past performance. We evaluate the relative strength of our financial position by monitoring our working capital, debt ratios, and returns on capital employed. We track industry statistics to evaluate our performance against competitors.

We reward executives and eligible employees through incentive compensation plans for performance against the following measures:

| ∎ | safety performance – total recordable incident rate per 200,000 man-hours, recordable free facilities and “Triple Target Zero” days (defined on page 22 under ‘Safe Operations’). Measured against prior year performance and current year industry performance in Canada and the U.S. |

| ∎ | operational performance – rig down time for repair as measured by time not billed to the customer. Measured against a predetermined target of available billable time |

| ∎ | key field employee retention – senior field employee retention rates. Measured against predetermined target rates of retention |

| ∎ | strategic initiatives – achieving strategic operational goals. Measured against predetermined target metrics |

| ∎ | financial performance – Adjusted EBITDA, adjusted cash flow, return on capital employed and debt reduction. Measured against predetermined targets |

| ∎ | investment returns – total shareholder return performance (including dividends) against a group of industry peers, over a three-year period. The peer group consists of a predetermined group of companies with similar business operations that we compete with for investors. |

Top Tier Service

We pride ourselves on providing quality equipment operated by experienced and well-trained crews. We also strive to align our capabilities with evolving technical requirements associated with more complex well bore programs.

High Performance Rig Fleet

Our fleet of drilling rigs is well positioned to address the unconventional drilling programs of our customers. The vast majority of our drilling rigs have been designed or significantly upgraded to drill horizontal wells. With a breadth of horsepower types and drilling depth capabilities, our large fleet can address every type of onshore unconventional and conventional oil and natural gas drilling opportunity in North America.

Our service rigs provide completion, workover, abandonment, well maintenance, high pressure operations and critical sour gas well work, and well re-entry preparation across the Western Canada Sedimentary Basin and in the northern U.S. Service rigs are supported by four field locations in Alberta, two in Saskatchewan, and one each in Manitoba, British Columbia and North Dakota.

Snubbing units complement traditional natural gas well servicing by allowing customers to work on wells while they are pressurized and production has been suspended. We have two kinds of snubbing units: rig-assist and self-contained. Self-contained units do not require a service rig on site and are capable of snubbing and performing many other well servicing procedures. Included in our self-contained units are three patented L-frame units, which are more efficient in the rig up and rig out process than standard self-contained units.

Precision Drilling Corporation 2018 Annual Report | 20 |

Upgrade Opportunities

We leverage our internal manufacturing and repair capabilities and inventory of quality rigs to address market demand through upgraded drilling rigs. For drilling rigs, the upgrade is typically performed at the request of a customer and includes a term contract. Historically, certain upgrades have resulted in a change in tier classification.

Ancillary Equipment and Services

An inventory of equipment (top drives, loaders, boilers, tubulars, and well control equipment) supports our fleet of drilling and service rigs. We also maintain an inventory of key rig components to minimize downtime due to equipment failure.

We benefit from internal services for equipment certifications and component manufacturing from our manufacturing division in Canada and for standardization and distribution of consumable oilfield products through our procurement divisions in Canada and the U.S.

Precision Rentals provides specialized equipment and wellsite accommodations to customers on a rental basis. Precision Camp Services provides food and accommodation to personnel working at the wellsite, typically in remote locations in Western Canada.

Technical Centres

We operate two contract drilling technical centres, one in Nisku, Alberta and one in Houston, Texas. We also operate one completion and production services technical centre in Red Deer, Alberta. These centres accommodate our technical service and field training groups and enable us to consolidate support and training for our operations. Both of our contract drilling technical centres include fully functioning training rigs with the latest drilling technologies. In addition, our Houston facility accommodates our rig manufacturing group.

People Having an experienced, high performance crew is a competitive strength and highly valued by our customers. There are often shortages of industry manpower in peak operating periods. We rely heavily on our safety record, investment in employee development, comprehensive employee training, competency development, and reputation to attract | | Toughnecks (www.toughnecks.com) has been a highly successful field recruiting program for us since we introduced it in 2008. |

and retain employees. Our people strategies focus on initiatives that provide a safe and productive work environment, opportunity for advancement, and added wage security. We have centralized personnel, orientation, and training programs in Canada and the U.S. Our people strategies have enabled us to deliver quality field crews at all points in the industry cycle.

Systems

In 2017 we commenced an upgrade to our ERP system that was completed in the second quarter of 2018. The upgraded system fully integrates our drilling rigs with our field facilities and corporate offices increasing operating efficiencies and positioning the organization to better handle the increased data flows associated with our business. All our divisions operate using standardized business processes across marketing, equipment maintenance, procurement, manufacturing, HSE, inventory control, engineering, finance, payroll and human resources.

We continue to invest in information systems that provide competitive advantages. Electronic links between field and financial systems provide accuracy and timely processing. This repository of rig data improves response time to customer inquiries. Rig manufacturing projects also benefit from scheduling and budgeting tools, which identify and help leverage economies of scale as construction demands increase.

| |

21 | Management’s Discussion and Analysis |

Safe Operations

Safety, environmental stewardship and employee health are critical for us and for our customers and are the foundation of our culture.

Safety performance is a fundamental contributor to operating performance and the financial results we generate for our shareholders. We track safety using three separate metrics: ∎ Total Recordable Incident Rate ∎ Facilities Recordable Free ∎ Triple Target Zero Days. | | Target Zero The health and safety of our employees is a core value at Precision, and daily we work to set the standard for safety in our industry. |

Total Recordable Incident Rate (TRIR) is an industry standard and benchmarks our success and isolates areas for improvement. We have taken it to another level by tracking and measuring all injuries, regardless of severity, because they are leading indicators for the potential for more serious events. In 2018, 96% of our drilling rigs and 99% of our service rigs achieved Recordable Free Facilities. Facilities recordable free includes all of our rigs, operating centres and offices and measures how many of our facilities do not have a recordable incident during the year. In addition, we have a goal of achieving “Triple Target Zero” every day. A Triple Target Zero day is a day when we have no high potential work-related vehicle incidents, no recordable injuries and no reportable spills. For 2018 we achieved 288 Triple Target Zero days.

We foster our safety culture through strong leadership, technical and compliance training, and proven support systems. Every day, we invest in our employees to prepare them for any and every situation on the rig. Our Technical Support Centre training facilities are located in Houston, Texas, and Nisku, Alberta, where more than 6,100 employees were trained in 2018 on our culture, rig personnel and responsibilities, tools and equipment, safety and environmental protocol and procedures, leadership and team-building.

We continuously review our rig designs and components and use advanced technology to operate safely, improve the life cycle, maintain operational efficiency, reduce energy use, and maintain our energy and resources. In 2018, 20% of our fleet was configured to be powered by natural gas, which is cleaner-burning than diesel and therefore reduces our, and our customer’s, carbon footprint. Our pad-capable rig fleet has also helped our customers reduce their overall operating footprint by enabling them to drill multiple wells on a single well pad location.

Precision Drilling Corporation 2018 Annual Report | 22 |

AN EFFECTIVE STRATEGY

Precision’s vision is to be globally recognized as the High Performance, High Value provider of land drilling services. We work toward this vision by defining and measuring our results against strategic priorities we establish at the beginning of every year.

2018 Strategic Priorities | | 2018 Results |

Commercial deployment of Process Automation Controls and Directional Guidance Systems on a wide scale. | | Added ten Process Automation Control (PAC) systems with a total of 31 systems deployed in the field at year-end, a 50% increase in installed base during 2018. Equipped both training rigs in Nisku and Houston with PAC technology. Drilled 365 wells in 2018 utilizing PAC technology and drilled 119 wells utilizing its directional guidance system, over half of which were drilled without any directional drillers on location. By year-end, Precision, its partners, customers and several third parties had 15 drilling performance applications under development with several Apps in field trials. Completed ERP system upgrade to position the organization to better handle increased data flows. |

Enhance financial performance through higher utilization and improved margins. | | Consolidated utilization days increased 14% year-over-year. U.S. Drilling margins up 25%, Canadian Drilling margins up 4% and International Drilling margins remained stable. Achieved highest market share on record for Precision in the U.S. of over 7.5%. |

Reduce debt by generating free cash flow while continuing to fund only the most attractive investment opportunities. •Target $75 million to $125 million debt repayment in 2018. •Target $300 million to $500 million debt repayment by year-end 2021. | | Generated $311 million in funds provided by operations (Non-GAAP measure – see page 3 for more information) representing a 69% increase year-over-year. Precision’s 2018 debt repayments totaled $174 million, $49 million higher than the top end of Precision’s target 2018 debt repayment range. In conjunction with debt repayments, Precision grew its cash balance by $32 million throughout the year. Completed two new-build rigs in the U.S. market while continuing rig upgrade program (not exceeding $3 million in upgrade cost per rig). Precision also began construction of its sixth new-build rig in Kuwait. Capital expenditures totaled $126 million, $9 million less than planned spending. Net capital expenditures totaled $102 million with $24 million of proceeds on sale of property, plant and equipment. |

| |

23 | Management’s Discussion and Analysis |

Our Corporate and Competitive Strategies are designed to optimize resource allocation and differentiate us from the competition, generating value for investors. Unconventional drilling is the primary opportunity in the North American marketplace. Unconventional resource development requires the most efficient and technically capable drilling rigs and other highly developed services that facilitate the drilling of reliable, predictable and repeatable horizontal wells. Customer adoption of large-scale industrialization techniques and high efficiency rig systems continues to increase and Precision’s Super Series rig fleet and High Performance, High Value strategy positions the Company to benefit from that trend. The completion and production work associated with unconventional wells provides the most profitable growth opportunities for our Completion and Production Services segment.

Strategic Priorities for 2019

• | Generate strong free cash flow and utilize $100 million to $150 million to reduce debt in 2019; increased long-term debt reduction targets to $400 million to $600 million by year-end 2021 (inclusive of 2018 debt repayments). |

• | Maximize financial results by leveraging our High Performance, High Value Super Series rig fleet and scale with disciplined cost management. |

• | Full scale commercialization and implementation of our Process Automation Control platform, PD Apps and PD Analytics. |

Precision Drilling Corporation 2018 Annual Report | 24 |

| | | | | |

| 2018 Results | | Management’s Discussion and Analysis | | |

| | | | | |

Adjusted EBITDA and operating loss are Non-GAAP measures. See page 3 for more information.

Consolidated Statements of Loss Summary

Year ended December 31 (thousands of dollars) | | 2018 | | | 2017 | | | 2016 | |

Revenue | | | | | | | | | | | | |

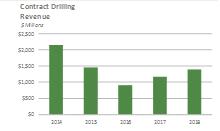

Contract Drilling Services | | | 1,396,492 | | | | 1,173,930 | | | | 907,821 | |

Completion and Production Services | | | 150,760 | | | | 154,146 | | | | 100,049 | |

Inter-segment elimination | | | (6,063 | ) | | | (6,852 | ) | | | (4,637 | ) |

| | | 1,541,189 | | | | 1,321,224 | | | | 1,003,233 | |

Adjusted EBITDA(1) | | | | | | | | | | | | |

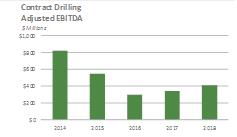

Contract Drilling Services | | | 412,134 | | | | 342,970 | | | | 296,651 | |

Completion and Production Services | | | 14,881 | | | | 11,888 | | | | (3,649 | ) |

Corporate and Other | | | (51,884 | ) | | | (49,877 | ) | | | (64,927 | ) |

| | | 375,131 | | | | 304,981 | | | | 228,075 | |

Depreciation and amortization | | | 365,660 | | | | 377,746 | | | | 391,659 | |

Impairment of goodwill | | | 207,544 | | | | — | | | | — | |

Impairment of property, plant and equipment | | | — | | | | 15,313 | | | | — | |

Gain on re-measurement of property, plant and equipment | | | — | | | | — | | | | (7,605 | ) |

Foreign exchange | | | 4,017 | | | | (2,970 | ) | | | 6,008 | |

Finance charges | | | 127,178 | | | | 137,928 | | | | 146,360 | |

Loss (gain) on redemption and repurchase of unsecured senior notes | | | (5,672 | ) | | | 9,021 | | | | 239 | |

Loss before income taxes | | | (323,596 | ) | | | (232,057 | ) | | | (308,586 | ) |

Income taxes | | | (29,326 | ) | | | (100,021 | ) | | | (153,031 | ) |

Net loss | | | (294,270 | ) | | | (132,036 | ) | | | (155,555 | ) |

(1) | See Non-GAAP Measures on page 3 of this report. |

Results by Geographic Segment

Year ended December 31 (thousands of dollars) | | 2018 | | | 2017 | | | 2016 | |

Revenue | | | | | | | | | | | | |

Canada | | | 571,640 | | | | 578,817 | | | | 418,030 | |

U.S. | | | 797,217 | | | | 568,573 | | | | 426,546 | |

International | | | 191,131 | | | | 190,401 | | | | 169,286 | |

Inter-segment elimination | | | (18,799 | ) | | | (16,567 | ) | | | (10,629 | ) |

| | | 1,541,189 | | | | 1,321,224 | | | | 1,003,233 | |

Total assets | | | | | | | | | | | | |

Canada | | | 1,269,542 | | | | 1,631,838 | | | | 1,738,853 | |

U.S. | | | 1,772,850 | | | | 1,666,368 | | | | 1,861,908 | |

International | | | 593,651 | | | | 594,725 | | | | 723,453 | |

| | | 3,636,043 | | | | 3,892,931 | | | | 4,324,214 | |

| |

25 | Management’s Discussion and Analysis |

2018 COMPARED WITH 2017

Net loss in 2018 was $294 million, or $1.00 per diluted share, compared with net loss of $132 million, or $0.45 per diluted share, in 2017. The higher net loss in 2018 was primarily the result of a $208 million goodwill impairment charge offset by higher U.S. activity and average day rates.

Revenue was $1,541 million (17% higher than 2017) because of higher U.S. activity and improved day rates.

Adjusted EBITDA in 2018 was $375 million (23% higher than 2017), mainly because of the increase in U.S. activity. Activity, as measured by drilling utilization days, increased 30% in the U.S. while remaining relatively constant in Canada and internationally compared with 2017.

Impairment

Under IFRS, we are required to assess the carrying value of assets in our CGUs containing goodwill annually and when indicators of impairment exist. Due to the decrease in oil and natural gas well drilling in Canada and the outlook for activity in Canada and in our directional drilling division in the U.S., we recognized a $208 million goodwill impairment charge. The impairment charge represents the full amount of goodwill attributable to our Canadian contract drilling and U.S. directional drilling operations.

Because of no activity in Mexico in 2017, we completed an impairment test for our Mexico contract drilling CGU as of December 31, 2017. As a result of this test it was determined that property, plant and equipment in our Mexico contract drilling business was impaired by US$12 million.

Foreign Exchange

We recognized a foreign exchange loss of $4 million in 2018 (2017 – $3 million gain) due to the devaluation of the Canadian dollar against the U.S. dollar and this affected the net U.S. dollar denominated monetary position in our Canadian dollar-based companies.

Finance Charges

Finance charges were $127 million, a decrease of $11 million compared with 2017 primarily due to a reduction in interest expense related to debt retired in 2017 and mid-2018 partially offset by higher interest income earned in the comparative period.

Gain on Redemption and Repurchase of Unsecured Senior Notes

During the year we redeemed US$80 million and repurchased and cancelled US$3 million of our 6.5% unsecured senior notes due 2021 and repurchased and cancelled US$49 million principal amount of our 5.25% unsecured senior notes due 2024 resulting in a net gain of $6 million. In comparison, during 2017, we redeemed and/or repurchased and cancelled US$442 million of our previously outstanding senior notes incurring a loss of $9 million.

Income Taxes

Income taxes were a recovery of $29 million, $71 million lower than the $100 million recovery booked in 2017. The reduced recovery in 2018 compared with 2017 was mainly due to a smaller loss prior to the non-taxable portion of the goodwill impairment.

Precision Drilling Corporation 2018 Annual Report | 26 |

2017 COMPARED WITH 2016

Net loss in 2017 was $132 million, or $0.45 per diluted share, compared with net loss of $156 million, or $0.53 per diluted share, in 2016. The reduction of net loss in 2017 was primarily the result of improved activity levels compared to 2016.

Revenue was $1,321 million (32% higher than 2016) because of higher activity in all our operations.

Adjusted EBITDA in 2017 was $305 million (34% higher than 2016), mainly because activity levels were higher in all our operations. Activity, as measured by drilling utilization days, increased 48% in Canada, 81% in the U.S., and 5% internationally compared with 2016.

Impairment

Under IFRS, we are required to assess the carrying value of assets in our CGUs containing goodwill annually and when indicators of impairment exist. Because of no activity in Mexico in 2017, we completed an impairment test for our Mexico contract drilling CGU as of December 31, 2017. The test involves determining a value in use based on a multi-year discounted cash flow using assumptions on expected future results. The resulting value in use is then compared to the carrying value of the CGU. As a result of this test it was determined that property, plant and equipment in our Mexico contract drilling business was impaired by US$12 million.

Foreign Exchange

We recognized a foreign exchange gain of $3 million in 2017 (2016 – $6 million loss) because the Canadian dollar strengthened in value against the U.S. dollar and this affected the net U.S. dollar denominated monetary position in our Canadian dollar-based companies.

Finance Charges

Finance charges were $138 million, a decrease of $8 million compared with 2016. The decrease is the result of a stronger Canadian dollar on our U.S. dollar denominated interest expense and a reduction in interest expense related to debt retired during the past two years.

Loss on Redemption and Repurchase of Unsecured Senior Notes

During 2017, we redeemed and/or repurchased and cancelled US$442 million of our previously outstanding senior notes incurring a loss of $9 million. In 2016, we redeemed and/or repurchased and cancelled $200 million and US$360 million of our previously outstanding Canadian and U.S. senior notes, respectively, incurring a slight loss.

Income Taxes

Income taxes were a recovery of $100 million, $53 million lower than the $153 million recovery booked in 2016 mainly due to a smaller loss in 2017 compared with 2016 and from the fourth quarter tax reform implemented in the U.S. reducing tax rates which reduced the benefit of our U.S. losses carried forward.

| |

27 | Management’s Discussion and Analysis |

Segmented Results

CONTRACT DRILLING SERVICES

Financial Results

Adjusted EBITDA and operating loss are Non-GAAP measures. See page 3 for more information.

Year ended December 31 (thousands of dollars, except where noted) | | 2018 | | | % of revenue | | | 2017 | | | % of revenue | | | 2016 | | | % of revenue | |

Revenue | | | 1,396,492 | | | | | | | | 1,173,930 | | | | | | | | 907,821 | | | | | |

Expenses | | | | | | | | | | | | | | | | | | | | | | | | |

Operating | | | 945,203 | | | | 67.7 | | | | 798,655 | | | | 68.0 | | | | 574,104 | | | | 63.2 | |

General and administrative | | | 39,155 | | | | 2.8 | | | | 32,305 | | | | 2.8 | | | | 34,026 | | | | 3.7 | |

Restructuring | | | — | | | | — | | | | — | | | | — | | | | 3,040 | | | | 0.3 | |

Adjusted EBITDA (1) | | | 412,134 | | | | 29.5 | | | | 342,970 | | | | 29.2 | | | | 296,651 | | | | 32.7 | |

Depreciation and amortization | | | 334,555 | | | | 24.0 | | | | 334,587 | | | | 28.5 | | | | 348,005 | | | | 38.3 | |

Impairment of goodwill | | | 207,544 | | | | 14.9 | | | | — | | | | — | | | | — | | | | — | |

Impairment of property, plant and equipment | | | — | | | | — | | | | 15,313 | | | | 1.3 | | | | — | | | | — | |

Operating loss (1) | | | (129,965 | ) | | | (9.3 | ) | | | (6,930 | ) | | | (0.6 | ) | | | (51,354 | ) | | | (5.7 | ) |

| (1) | See Non-GAAP measures on page 3 of this report. |

2018 Compared with 2017

Revenue from Contract Drilling Services was $1,396 million, 19% higher than 2017, mainly because of higher activity in our U.S. contract drilling operations and higher average day rates in each of our contract drilling operations.

In 2018, total shortfall payments in Canada and idle but contracted revenue in the U.S. were $12 million and US$0.6 million, compared with $31 million and US$6 million, respectively in 2017.

Operating expenses in 2018 were 68% of revenue and is consistent with the prior year. On a per utilization day basis, operating costs for the drilling rig division in Canada were higher than the prior year period due to timing of equipment certifications and equipment maintenance costs. In the U.S., operating costs on a per day basis were higher than the prior year period primarily due to expenses recovered through the day rate and higher turnkey activity. General and administrative expenses for 2018 were higher due to the devaluation of the Canadian dollar on our U.S. dollar denominated costs.

Our 2018 operating loss was $130 million as compared to an operating loss of $7 million in the comparable prior year period. Operating loss in 2018 increased as a result of goodwill impairment charges of $208 million offset by an increase in drilling activity in our U.S. drilling operations and improved day rates in each of our drilling operations. Our 2017 operating results include an impairment of property, plant and equipment charge of $15 million related to certain drilling rigs and spare equipment. Excluding the impairment of goodwill and property, plant and equipment impairment, operating earnings would have been $78 million in 2018 and $8 million in 2017.

Our total depreciation expense was consistent year over year.

Capital expenditures in 2018 for our Contract Drilling segment were $108 million:

| ∎ | $35 million – to expand our asset base |

| ∎ | $31 million – to upgrade existing equipment |

| ∎ | $42 million – on maintenance and infrastructure. |

Precision Drilling Corporation 2018 Annual Report | 28 |

Operating Statistics

Year ended December 31 | | 2018 | | | % increase/ (decrease) | | | 2017 | | | % increase/ (decrease) | | | 2016 | | | % increase/ (decrease) | |

Number of drilling rigs (year-end) | | | 236 | | | | (7.8 | ) | | | 256 | | | | 0.4 | | | | 255 | | | | 1.6 | |

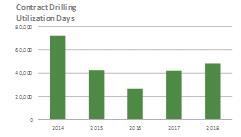

Drilling utilization days (operating and moving) | | | | | | | | | | | | | | | | | | | | | | | | |

Canada | | | 18,617 | | | | (1.4 | ) | | | 18,883 | | | | 48.4 | | | | 12,722 | | | | (26.2 | ) |

U.S. | | | 26,714 | | | | 30.4 | | | | 20,479 | | | | 80.5 | | | | 11,343 | | | | (46.4 | ) |

International | | | 2,920 | | | | - | | | | 2,920 | | | | 4.8 | | | | 2,786 | | | | (31.8 | ) |

Drilling revenue per utilization day | | | | | | | | | | | | | | | | | | | | | | | | |

Canada (Cdn$) | | | 21,644 | | | | 2.4 | | | | 21,143 | | | | (13.7 | ) | | | 24,509 | | | | (9.1 | ) |

U.S. (US$) | | | 21,864 | | | | 10.1 | | | | 19,861 | | | | (24.0 | ) | | | 26,145 | | | | (2.2 | ) |

International (US$) | | | 50,469 | | | | 0.5 | | | | 50,240 | | | | 9.8 | | | | 45,753 | | | | 5.2 | |

Drilling statistics (Canadian operations only) | | | | | | | | | | | | | | | | | | | | | | | | |

Wells drilled | | | 1,663 | | | | (3.8 | ) | | | 1,729 | | | | 79.7 | | | | 962 | | | | (28.8 | ) |

Average days per well | | | 9.9 | | | | 2.1 | | | | 9.7 | | | | (17.1 | ) | | | 11.7 | | | | 2.6 | |

Metres drilled (hundreds) | | | 4,694 | | | | 2.1 | | | | 4,597 | | | | 80.4 | | | | 2,548 | | | | (21.0 | ) |

Average metres per well | | | 2,823 | | | | 6.2 | | | | 2,659 | | | | 0.4 | | | | 2,649 | | | | 11.0 | |

Canadian Drilling

Revenue from Canadian drilling was $403 million, 1% lower than 2017. Drilling rig activity, as measured by utilization days, was down slightly by 1% while average day rates were up 2%.

Adjusted EBITDA was $124 million, 13% lower than 2017, because of lower drilling activity offset by higher average day rates.

Depreciation expense for the year was $112 million, in-line with 2017.

Drilling Statistics – Canada

In 2018, we transferred one drilling rig from Canada to the U.S. and identified 18 drilling rigs to be held for sale, bringing our Canadian 2018 year-end net rig count to 117 (2017 –136).

The industry drilling rig fleet has decreased as there were approximately 592 rigs at the end of 2018 compared with 627 at the end of 2017. Our operating day utilization was 34% (2017 – 34%), compared with industry utilization of 29% (2017 – 29%).

U.S. Drilling

Revenue from U.S. drilling was US$584 million, 43% higher than 2017. Drilling rig activity, as measured by utilization days, was up 30% while average revenue per day was up 10%.

Adjusted EBITDA was US$180 million, 70% higher than 2017, mainly because of higher activity and average day rates offset by lower idle but contracted revenue.

Depreciation expense for the year was US$120 million, US$1 million lower than 2017 because of a lower capital asset base.

Drilling Statistics – U.S.

In 2018, we completed two new-build rigs, transferred one rig from Canada and identified four drilling rigs to be held for sale, leaving our U.S. year-end net rig count at 102. In 2018, we averaged 73 rigs working, an 30% increase from 56 rigs in 2017. The industry drilling fleet increased as well, averaging 1,014 active land rigs in 2018, up 18% from 856 rigs in 2017.

Our average day rates in the U.S. increased 10% in 2018 as legacy contracts expired and newly contracted rigs were at higher day rates. Revenue from idle but contracted rigs was US$0.6 million in 2018, a reduction of $6 million from the prior year period.

| |

29 | Management’s Discussion and Analysis |

Turnkey utilization days increased 161% over 2017 and accounted for approximately 2% of our revenue compared with 2% in 2017.

Drilling Statistics – U.S.

| | 2018 | | | 2017 | | | 2016 | |

| | Precision | | | Industry (1) | | | Precision | | | Industry (1) | | | Precision | | | Industry (1) | |

Average number of active land rigs for quarters ended: | | | | | | | | | | | | | | | | | | | | | | | | |

March 31 | | | 64 | | | | 951 | | | | 47 | | | | 722 | | | | 32 | | | | 516 | |

June 30 | | | 72 | | | | 1,021 | | | | 59 | | | | 874 | | | | 24 | | | | 397 | |

September 30 | | | 76 | | | | 1,032 | | | | 61 | | | | 927 | | | | 29 | | | | 465 | |

December 31 | | | 80 | | | | 1,050 | | | | 58 | | | | 902 | | | | 39 | | | | 567 | |

Annual average | | | 73 | | | | 1,014 | | | | 56 | | | | 856 | | | | 31 | | | | 486 | |

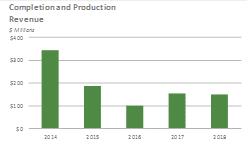

COMPLETION AND PRODUCTION SERVICES

Financial Results

Adjusted EBITDA and operating loss are Non-GAAP measures. See page 3 for more information.

Year ended December 31 (thousands of dollars, except where noted) | | 2018 | | | % of revenue | | | 2017 | | | % of revenue | | | 2016 | | | % of revenue | |

Revenue | | | 150,760 | | | | | | | | 154,146 | | | | | | | | 100,049 | | | | | |

Expenses | | | | | | | | | | | | | | | | | | | | | | | | |

Operating | | | 128,731 | | | | 85.4 | | | | 134,368 | | | | 87.2 | | | | 92,248 | | | | 93.0 | |

General and administrative | | | 7,148 | | | | 4.7 | | | | 7,890 | | | | 5.1 | | | | 9,429 | | | | 8.6 | |

Restructuring | | | — | | | | — | | | | — | | | | — | | | | 2,021 | | | | 2.0 | |