| FREE WRITING PROSPECTUS | |

| FILED PURSUANT TO RULE 433 | |

| REGISTRATION FILE NO.: 333-226123-05 | |

| October 29, 2019 | Benchmark 2019-B14 |

Free Writing Prospectus Structural and Collateral Term Sheet | ||

BENCHMARK 2019-B14

| ||

$1,322,249,369 (Approximate Mortgage Pool Balance) | ||

$1,144,205,000 (Approximate Offered Certificates) | ||

J.P. Morgan Chase Commercial Mortgage Securities Corp. Depositor | ||

| ||

BENCHMARK 2019-B14 mORTGAGE TRUST, Commercial Mortgage Pass-Through Certificates Series 2019-B14

| ||

| JPMorgan Chase Bank, National Association Citi Real Estate Funding Inc. German American Capital Corporation | ||

| Sponsors and Mortgage Loan Sellers | ||

| J.P. Morgan | Citigroup | Deutsche Bank Securities |

Co-Lead Managers and Joint Bookrunners | ||

| Drexel Hamilton |

Co-Managers

| Academy Securities |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

| October 29, 2019 | Benchmark 2019-B14 |

This material is for your information, and none of J.P. Morgan Securities LLC (“JPMS”), Citigroup Global Markets Inc. (“CGMI”), Deutsche Bank Securities Inc. (“DBSI”), Drexel Hamilton, LLC (“Drexel”) or Academy Securities, Inc. (“Academy Securities”) (each individually, an “Underwriter”, and together, the ‘‘Underwriters’’) are soliciting any action based upon it. This material is not to be construed as an offer to sell or the solicitation of any offer to buy any security in any jurisdiction where such an offer or solicitation would be illegal.

The Depositor has filed a registration statement (including a prospectus) with the SEC (SEC File no. 333-226123) for the offering to which this free writing prospectus relates. Before you invest, you should read the prospectus in the registration statement and other documents the Depositor has filed with the SEC for more complete information about the Depositor, the issuing entity and this offering. You may get these documents for free by visiting EDGAR on the SEC Website at www.sec.gov. Alternatively, the Depositor or any Underwriter or any dealer participating in the offering will arrange to send you the prospectus if you request itby calling (800) 408-1016 or by emailing the ABS Syndicate Desk at abs_synd@jpmorgan.com.

Neither this document nor anything contained in this document shall form the basis for any contract or commitment whatsoever. The information contained in this document is preliminary as of the date of this document, supersedes any previous such information delivered to you and will be superseded by any such information subsequently delivered prior to the time of sale. These materials are subject to change, completion or amendment from time to time.

This document has been prepared by the Underwriters for information purposes only and does not constitute, in whole or in part, a prospectus for the purposes of Regulation (EU) 2017/1129 (as amended) and/or Part VI of the Financial Services and Markets Act 2000 (as amended) or other offering document.

The attached information contains certain tables and other statistical analyses (the “Computational Materials”) that have been prepared in reliance upon information furnished by the Mortgage Loan Sellers. Numerous assumptions were used in preparing the Computational Materials, which may or may not be reflected in this document. The Computational Materials should not be construed as either projections or predictions or as legal, tax, financial or accounting advice. You should consult your own counsel, accountant and other advisors as to the legal, tax, business, financial and related aspects of a purchase of these certificates. Any weighted average lives, yields and principal payment periods shown in the Computational Materials are based on prepayment and/or loss assumptions, and changes in such prepayment and/or loss assumptions may dramatically affect such weighted average lives, yields and principal payment periods. In addition, it is possible that prepayments or losses on the underlying assets will occur at rates higher or lower than the rates shown in the Computational Materials. The specific characteristics of the certificates may differ from those shown in the Computational Materials due to differences between the final underlying assets and the preliminary underlying assets used in preparing the Computational Materials. The principal amount and designation of any certificate described in the Computational Materials are subject to change prior to issuance. None of the Underwriters nor any of their respective affiliates make any representation or warranty as to the actual rate or timing of payments or losses on any of the underlying assets or the payments or yield on the certificates.

This information is based upon management forecasts and reflects prevailing conditions and management’s views as of this date, all of which are subject to change.

This document contains forward-looking statements. Those statements are subject to certain risks and uncertainties that could cause the success of collections and the actual cash flow generated to differ materially from the information set forth in this document. While such information reflects projections prepared in good faith based upon methods and data that are believed to be reasonable and accurate as of their dates, the Depositor undertakes no obligation to revise these forward-looking statements to reflect subsequent events or circumstances. Investors should not place undue reliance on forward-looking statements and are advised to make their own independent analysis and determination with respect to the forecasted periods, which reflect the Depositor’s view only as of the date of this document.

J.P. Morgan is the marketing name for the investment banking businesses of JPMorgan Chase & Co. and its subsidiaries worldwide. Securities, syndicated loan arranging, financial advisory and other investment banking activities are performed by JPMS and its securities affiliates, and lending, derivatives and other commercial banking activities are performed by JPMorgan Chase Bank, National Association and its banking affiliates. JPMS is a member of SIPC and the NYSE. Securities and investment banking activities in the United States are performed by Deutsche Bank Securities Inc., a member of NYSE, FINRA and SIPC, and its broker-dealer affiliates. Lending and other commercial banking activities in the United States are performed by Deutsche Bank AG, acting through its New York Branch.

Capitalized terms used in this material but not defined herein shall have the meanings ascribed to them in the Preliminary Prospectus (as defined below).

THE CERTIFICATES REFERRED TO IN THESE MATERIALS ARE SUBJECT TO MODIFICATION OR REVISION (INCLUDING THE POSSIBILITY THAT ONE OR MORE CLASSES OF CERTIFICATES MAY BE SPLIT, COMBINED OR ELIMINATED AT ANY TIME PRIOR TO ISSUANCE OR AVAILABILITY OF A FINAL PROSPECTUS) AND ARE OFFERED ON A “WHEN, AS AND IF ISSUED” BASIS.

THE UNDERWRITERS MAY FROM TIME TO TIME PERFORM INVESTMENT BANKING SERVICES FOR, OR SOLICIT INVESTMENT BANKING BUSINESS FROM, ANY COMPANY NAMED IN THESE MATERIALS. THE UNDERWRITERS AND/OR THEIR AFFILIATES OR RESPECTIVE EMPLOYEES MAY FROM TIME TO TIME HAVE A LONG OR SHORT POSITION IN ANY CERTIFICATE OR CONTRACT DISCUSSED IN THESE MATERIALS.

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

|  |  |

2 of 156

| Structural and Collateral Term Sheet | Benchmark 2019-B14 | |

| Indicative Capital Structure | ||

Publicly Offered Certificates

| Class | Expected Ratings (S&P / Fitch / KBRA) | Approximate Initial Certificate Balance or Notional Amount(1) | Approximate Initial Credit Support(2) | Expected Weighted Avg. Life (years)(3) | Expected Principal Window(3) | Certificate Principal to Value Ratio(4) | Underwritten NOI Debt Yield(5) |

| A-1 | AAA(sf) / AAAsf / AAA(sf) | $22,760,000 | 30.000% | 2.64 | 12/2019 – 8/2024 | 42.0% | 14.1% |

| A-2 | AAA(sf) / AAAsf / AAA(sf) | $249,620,000 | 30.000% | 4.94 | 8/2024 – 11/2024 | 42.0% | 14.1% |

| A-3 | AAA(sf) / AAAsf / AAA(sf) | $55,480,000 | 30.000% | 6.98 | 11/2026 – 11/2026 | 42.0% | 14.1% |

| A-4 | AAA(sf) / AAAsf / AAA(sf) | (6) | 30.000% | (6) | (6) | 42.0% | 14.1% |

| A-5 | AAA(sf) / AAAsf / AAA(sf) | (6) | 30.000% | (6) | (6) | 42.0% | 14.1% |

| A-SB | AAA(sf) / AAAsf / AAA(sf) | $37,040,000 | 30.000% | 7.39 | 11/2024 – 6/2029 | 42.0% | 14.1% |

| X-A | AA-(sf) / AAAsf / AAA(sf) | $1,029,785,000(7) | N/A | N/A | N/A | N/A | N/A |

| X-B | NR / A-sf / AAA(sf) | $114,420,000(7) | N/A | N/A | N/A | N/A | N/A |

| A-S | AA-(sf) / AAAsf / AAA(sf) | $127,315,000 | 20.125% | 9.98 | 11/2029 – 11/2029 | 47.9% | 12.4% |

| B | NR / AA-sf / AA-(sf) | $61,240,000 | 15.375% | 9.98 | 11/2029 – 11/2029 | 50.8% | 11.7% |

| C | NR / A-sf / A-(sf) | $53,180,000 | 11.250% | 9.98 | 11/2029 – 11/2029 | 53.2% | 11.2% |

Privately Offered Certificates(8)

| Class | Expected Ratings (S&P / Fitch / KBRA) | Approximate Initial Certificate Balance or Notional Amount(1) | Approximate Initial Credit Support(2) | Expected Weighted Avg. Life (years)(3) | Expected Principal Window(3) | Certificate Principal to Value Ratio(4) | Underwritten NOI Debt Yield(5) |

| X-D | NR / BBB-sf / BBB-(sf) | $59,630,000(7) | N/A | N/A | N/A | N/A | N/A |

| D | NR / BBBsf / BBB(sf) | $33,845,000 | 8.625% | 9.98 | 11/2029 – 11/2029 | 54.8% | 10.8% |

| E | NR / BBB-sf / BBB-(sf) | $25,785,000 | 6.625% | 9.98 | 11/2029 – 11/2029 | 56.0% | 10.6% |

| F-RR | NR / BB-sf / BB-(sf) | $24,175,000 | 4.750% | 9.98 | 11/2029 – 11/2029 | 57.1% | 10.4% |

| G-RR | NR / B-sf / B-(sf) | $12,890,000 | 3.750% | 9.98 | 11/2029 – 11/2029 | 57.7% | 10.3% |

| NR-RR | NR / NR / NR | $48,349,368 | 0.000% | 9.98 | 11/2029 – 11/2029 | 60.0% | 9.9% |

Privately Offered Loan-Specific Certificates(8)(9)

| Class | Expected Ratings (KBRA) | Approximate Initial Certificate Balance or Notional Amount(1) | Approximate Initial Credit Support(2) | Expected Weighted Avg. Life (years)(3) | Expected Principal Window(3) | Certificate Principal to Value Ratio(10) | Underwritten NOI Debt Yield(11) |

| 225B-A | A-(sf) | $11,595,000 | 38.341% | 4.98 | 11/2024 - 11/2024 | 36.6% | 12.7% |

| 225B-B | BBB-(sf) | $33,958,000 | 28.128% | 4.98 | 11/2024 - 11/2024 | 42.7% | 10.9% |

| 225B-C | BB-(sf) | $35,434,000 | 17.472% | 4.98 | 11/2024 - 11/2024 | 49.0% | 9.5% |

| 225B-D | B-(sf) | $48,723,000 | 2.818% | 4.98 | 11/2024 - 11/2024 | 57.7% | 8.0% |

| 225B-E | NR | $9,370,000 | 0.000% | 4.98 | 11/2024 - 11/2024 | 59.4% | 7.8% |

Non-Offered Vertical Risk Retention Interest(8)

| Non-Offered Vertical Risk Retention Interest | Expected Ratings (S&P / Fitch / KBRA) | Approximate Initial Certificate Balance(1) | Approximate Initial Credit Support(2) | Expected Weighted Avg. Life (years)(3)(12) | Expected Principal Window(3)(12) | Certificate Principal to Value Ratio(4) | Underwritten NOI Debt Yield(5) |

| VRR Interest(13)(14) | NR / NR / NR | $33,000,000 | N/A | 8.62 | 12/2019 – 11/2029 | N/A | N/A |

| 225B-VRR Interest(15)(16) | NR / NR / NR | $7,320,000 | N/A | 4.98 | 11/2024 - 11/2024 | N/A | N/A |

| (1) | In the case of each such Class, subject to a permitted variance of plus or minus 5%. The certificate balance of each of the VRR Interest and the 225B-VRR Interest is not included in the certificate balance or notional amount of any class of certificates set forth under “Publicly Offered Certificates”, “Privately Offered Certificates” or “Privately Offered Loan-Specific Certificates” in the table above, and neither the VRR Interest nor the 225B-VRR Interest is offered by this Term Sheet. In addition, the notional amounts of the Class X-A, Class X-B and Class X-D Certificates may vary depending upon the final pricing of the Classes of Pooled Principal Balance Certificates whose Certificate Balances comprise such notional amounts, and, if as a result of such pricing the pass-through rate of any Class of the Class X-A, Class X-B and Class X-D Certificates, as applicable, would be equal to zero at all times, such Class of Certificates will not be issued on the closing date of this securitization. |

| (2) | The credit support percentages set forth for Class A-1, Class A-2, Class A-3, Class A-4, Class A-5 and Class A-SB Certificates represent the approximate initial credit support for the Class A-1, Class A-2, Class A-3, Class A-4, Class A-5 and Class A-SB Certificates in the aggregate. The approximate initial credit support percentages shown in the table above for the Pooled Principal Balance Certificates do not take into account the VRR Interest. However, losses incurred on the mortgage loans will be allocated between the VRR Interest, on the one hand, and the Pooled Non-VRR Certificates (exclusive of the Class X and Class R certificates), on the other hand,pro rata in accordance with their respective outstanding certificate balances. The approximate initial credit support percentages show in the table above for the Pooled Principal Balance Certificates do not include the subordination provided by the 225 Bush subordinate companion loan (the “Trust Subordinate Companion Loan”) to the 225 Bush mortgage loan. Privately Offered the Loan-Specific Certificates will not provide credit support to any class of Pooled Certificates except to the extent of the subordination of the Trust Subordinate Companion Loan (in which the Loan-Specific Certificates each represent an interest) to the 225 Bush mortgage loan included in the mortgage pool. |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

| | |

3 of 156

| Structural and Collateral Term Sheet | Benchmark 2019-B14 | |

| Indicative Capital Structure | ||

| (3) | Assumes 0% CPR / 0% CDR and a November 21, 2019 closing date. Based on modeling assumptions as described in the Preliminary Prospectus dated October 29, 2019 (the “Preliminary Prospectus”). |

| (4) | The “Certificate Principal to Value Ratio” for any Class of Pooled Principal Balance Certificates (other than the Class A-1, Class A-2, Class A-3, Class A-4, Class A-5 and Class A-SB Certificates) is calculated as the product of (a) the weighted average Cut-off Date LTV for the mortgage loans, multiplied by (b) a fraction, the numerator of which is the total initial Certificate Balance of such Class of Certificates and all Classes of Pooled Principal Balance Certificates senior to such Class of Certificates and the denominator of which is the total initial Certificate Balance of all of the Pooled Principal Balance Certificates. The Class A-1, Class A-2, Class A-3, Class A-4, Class A-5 and Class A-SB Certificate Principal to Value Ratios are calculated in the aggregate for those Classes as if they were a single class. Investors should note, however, that excess mortgaged property value associated with a mortgage loan will not be available to offset losses on any other mortgage loan. |

| (5) | The “Underwritten NOI Debt Yield” for any Class of Pooled Principal Balance Certificates (other than the Class A-1, Class A-2, Class A-3, Class A-4, Class A-5 and Class A-SB Certificates) is calculated as the product of (a) the weighted average UW NOI DY for the mortgage loans and (b) the total initial Certificate Balance of all of the Classes of Pooled Principal Balance Certificates divided by the total initial Certificate Balance for such Class and all Classes of Pooled Principal Balance Certificates senior to such Class of Certificates. The Underwritten NOI Debt Yield for each of the Class A-1, Class A-2, Class A-3, Class A-4, Class A-5 and Class A-SB Certificates is calculated in the aggregate for those Classes as if they were a single Class. Investors should note, however, that net operating income from any mortgaged property supports only the related mortgage loan and will not be available to support any other mortgage loan. |

| (6) | The exact initial certificate balances of the Class A-4 and Class A-5 certificates are unknown and will be determined based on the final pricing of those classes of certificates. However, the respective initial certificate balances, weighted average lives and expected principal windows of the Class A-4 and Class A-5 certificates are expected to be within the applicable ranges reflected in the following chart. The aggregate initial offered certificate balance of the Class A-4 and Class A-5 certificates is expected to be approximately $537,570,000, subject to a variance of plus or minus 5%. |

| Class of Certificates | Expected Range of Initial Certificate Balance | Expected Range of Weighted Avg. Life (Yrs.) | Expected Range of Principal Window |

| A-4 | $100,000,000 – $187,000,000 | 9.67 – 9.76 | 6/2029-9/2029 / 6/2029-10/2029 |

| A-5 | $350,570,000 – $437,570,000 | 9.92 – 9.91 | 10/2029-11/2029 / 9/2029-11/2029 |

| (7) | The Class X-A, Class X-B and Class X-D Notional Amounts are defined in the Preliminary Prospectus. |

| (8) | The Classes of Certificates set forth under “Privately Offered Certificates”, “Non-Offered Vertical Risk Retention Interest” and “Privately Offered Loan-Specific Certificates” in the tables above are not being offered by the Preliminary Prospectus or this Term Sheet. The Class R Certificates are not shown above. |

| (9) | The loan-specific certificates will only be entitled to receive distributions from, and will only incur losses with respect to, the Trust Subordinate Companion Loan. The Trust Subordinate Companion Loan will be included as an asset of the issuing entity but will not be part of the mortgage pool backing the pooled certificates. No class of pooled certificates will have any interest in the Trust Subordinate Companion Loan. See “Description of the Mortgage Pool—The Whole Loans—The AB Whole Loans—225 Bush Whole Loan”. |

| (10) | The “Certificate Principal to Value Ratio” for any Class of Loan-Specific Principal Balance Certificates is calculated as the product of (a) the Cut-off Date LTV for the 225 Bush Whole Loan, multiplied by (b) a fraction, the numerator of which is the sum of (i) the initial Certificate Balance of such class of Loan-Specific Certificates and all other classes of Loan-Specific Certificates, if any, that are senior to such class (including any portions of the 225B-VRR Interest that is considered to bepari passu or senior to such class) and (ii) the principal balance as of the Cut-off Date of the 225 Bush senior mortgage loan, and the denominator of which is the total initial Certificate Balance of all classes of Loan-Specific Certificates (including any portions of the 225B-VRR Interest that is considered to bepari passu or senior to such class) and the principal balance as of the Cut-off Date of 225 Bush senior mortgage loan. |

| (11) | The “Underwritten NOI Debt Yield” for any class of Loan-Specific Certificates is calculated as the product of (a) the NOI Debt Yield for the 225 Bush Whole Loan, multiplied by (b) a fraction, the numerator of which is the total initial Certificate Balance of all classes of Loan-Specific Certificates (including any portions of the 225B-VRR Interest that is considered to bepari passu or senior to such class) and the principal balance as of the Cut-off Date of 225 Bush senior mortgage loan and the denominator of which is the total initial Certificate Balance of such class of Loan-Specific Certificates (including any portions of the 225B-VRR Interest that is considered to bepari passuor senior to such class) and all other classes of Loan-Specific Certificates, if any, that are senior to such class as well as the 225 Bush senior mortgage loan. |

| (12) | The weighted average life and principal window during which distributions of principal would be received as set forth in the foregoing table with respect to the VRR interest are based on the assumptions set forth under “Yield and Maturity Considerations—Weighted Average Life” in the Preliminary Prospectus and on the assumptions that there are no prepayments, modifications or losses in respect of the mortgage loans and that there are no extensions or forbearances of maturity dates or anticipated repayments dates of the mortgage loans. |

| (13) | German American Capital Corporation, as the retaining sponsor for the securitization transaction constituted by the issuance of the Pooled Certificates, is expected to acquire from the depositor, on the Closing Date, an “eligible vertical interest” (as defined in Regulation RR) in the form of a single vertical security with an expected aggregate initial Certificate Balance of $33,000,000 (the “VRR Interest”), which is expected to represent approximately 2.50% of all Pooled Principal Balance Certificates and the VRR Interest. A portion of the VRR Interest will be retained by each of German American Capital Corporation or its “majority-owned affiliate”, JPMorgan Chase Bank, National Association and Citi Real Estate Funding Inc., in accordance with the U.S. credit risk retention rules applicable to the pooled securitization. See “Credit Risk Retention” in the Preliminary Prospectus. |

| (14) | Although it does not have a specified pass-through rate (other than for tax reporting purposes), the effective interest rate for the VRR Interest will be the WAC rate. |

| (15) | German American Capital Corporation, as the retaining sponsor with respect to the securitization transaction constituted by the issuance of the Loan-Specific Certificates, is expected to acquire from the depositor, on the Closing Date, an “eligible vertical interest” (as defined in Regulation RR) in the form of a single vertical security with an expected aggregate initial Certificate Balance of $7,320,000 (the “225B-VRR Interest”), which is expected to represent approximately 5.0% of all Loan-Specific Principal Balance Certificates and the 225B-VRR Interest. The 225B-VRR Interest will be retained by German American Capital Corporation or its “majority-owned affiliate”, in accordance with the U.S. credit risk retention rules applicable to the loan-specific securitization. |

| (16) | Although it does not have a specified pass-through rate (other than for tax reporting purposes), the effective interest rate for the 225B-VRR Interest will be the net mortgage rate on the Trust Subordinate Companion Loan. |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

| | |

4 of 156

| Structural and Collateral Term Sheet | Benchmark 2019-B14 | |

| Summary of Transaction Terms | ||

| Securities Offered: | $1,144,205,000 monthly pay, multi-class, commercial mortgage REMIC Pass-Through Certificates. |

| Co-Lead Managers and Joint Bookrunners: | J.P. Morgan Securities LLC, Citigroup Global Markets Inc. and Deutsche Bank Securities Inc. |

| Co-Managers: | Drexel Hamilton, LLC and Academy Securities, Inc. |

| Mortgage Loan Sellers: | JPMorgan Chase Bank, National Association (“JPMCB”) (47.2%), Citi Real Estate Funding Inc. (“CREFI”) (30.6%) and German American Capital Corporation (“GACC”) (22.2%). |

| Master Servicer: | Midland Loan Services, a Division of PNC Bank, National Association. |

| Special Servicer: | Midland Loan Services, a Division of PNC Bank, National Association. |

| Directing Certificateholder: | KKR Real Estate Credit Opportunity Partners II L.P. |

| Trustee: | Wells Fargo Bank, National Association. |

| Certificate Administrator: | Wells Fargo Bank, National Association. |

| Operating Advisor: | Pentalpha Surveillance LLC. |

| Asset Representations Reviewer: | Pentalpha Surveillance LLC. |

| Rating Agencies: | S&P Global Ratings, acting through Standard and Poor’s Financial Services LLC (“S&P”), Fitch Ratings, Inc. (“Fitch”) and Kroll Bond Rating Agency, Inc. (“KBRA”). |

| U.S. Credit Risk Retention: | GACC is expected to act as the “retaining sponsor” for the securitization constituted by the issuance of the Pooled Certificates, and intends to satisfy the U.S. credit risk retention requirement by (i) acquiring (either through itself or through one or more of its “majority owned affiliates” (as defined in Regulation RR)) from the depositor, on the Closing Date, an “eligible vertical interest” which will be comprised of the VRR Interest and a portion of which will be transferred by GACC to each of JPMCB and CREFI and (ii) the purchase by KKR CMBS II Aggregator Type 1 L.P., as “third-party purchaser” (as defined in Regulation RR), from the depositor, on the Closing Date, of an “eligible horizontal residual interest”, which will be comprised of the Class F-RR, G-RR and NR-RR Certificates.

GACC is also expected to act as the “retaining sponsor” for the securitization constituted by the issuance of the Loan-Specific Certificates, and intends to satisfy the U.S. credit risk retention requirement by acquiring (either through itself or through one or more of its “majority owned affiliates” (as defined in Regulation RR)) from the depositor, on the Closing Date, an “eligible vertical interest” which will be comprised of the 225B-VRR Interest. The 225B-VRR Interest will be at least equal to 5% of the aggregate certificate balance of all Loan-Specific Certificates issued by the issuing entity.

The restrictions on hedging and transfer under the U.S. credit risk retention rules as in effect on the closing date of this transaction will expire on and after the date that is the latest of (i) the date on which the aggregate principal balance of the mortgage loans has been reduced to 33% of the aggregate principal balance of the mortgage loans as of the Cut-off Date; (ii) the date on which the total unpaid principal obligations under the Certificates has been reduced to 33% of the aggregate total unpaid principal obligations under the Certificates as of the Closing Date; or (iii) two years after the Closing Date.

The restrictions on hedging and transfer under the U.S. credit risk retention rules as in effect on the closing date of the loan-specific securitization transaction securitization transaction will expire on and after the date that is the latest of (i) the date on which the principal balance of the Trust Subordinate Companion Loan has been reduced to 33% of the principal balance of the Trust Subordinate Companion Loan as of the Cut-off Date; (ii) the date on which the total unpaid principal obligations under the Loan Specific Certificates has been reduced to 33% of the aggregate total unpaid principal obligations under Loan Specific Certificates as of the Closing Date; or (iii) two years after the Closing Date.

The Pooling and Servicing Agreement (as defined below) will include the required provisions applicable to an operating advisor necessary for the pooled securitization to comply with the credit risk retention rules utilizing the “third-party purchaser” option. See “Operating Advisor” below.

Notwithstanding any references in this term sheet to the credit risk retention rules, the Regulation RR, the retaining sponsor and other risk retention related matters, in the event the credit risk retention rules and/or Regulation RR (or any relevant portion thereof) are repealed or determined by applicable regulatory agencies to be no longer applicable to the pooled securitization transaction or the loan-specific securitization transaction, none of the retaining sponsor or any other party will be required to comply with or act in accordance with the U.S. credit risk retention rules and/or Regulation RR (or such relevant portion thereof).

For additional information, see “Credit Risk Retention” in the Preliminary Prospectus.

|

| EU Credit Risk Retention: | The transaction is not structured to satisfy the EU risk retention and due diligence requirements. |

| Pricing Date: | On or about November 4, 2019. |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

| | |

5 of 156

| Structural and Collateral Term Sheet | Benchmark 2019-B14 | |

| Summary of Transaction Terms | ||

| Closing Date: | On or about November 21, 2019. |

| Cut-off Date: | With respect to each mortgage loan, the related due date in November 2019 or with respect to any mortgage loan that has its first due date in December 2019, the date that would otherwise have been the related due date in November 2019. |

| Distribution Date: | The 4th business day after the Determination Date in each month, commencing in December 2019. |

| Determination Date: | 11th day of each month, or if the 11th day is not a business day, the next succeeding business day, commencing in December 2019. |

| Assumed Final Distribution Date: | The Distribution Date in November 2029, which is the latest anticipated repayment date of the Certificates. |

| Rated Final Distribution Date: | The Distribution Date in December 2062. |

| Tax Treatment: | The Publicly Offered Certificates are expected to be treated as REMIC “regular interests” for U.S. federal income tax purposes. |

| Form of Offering: | The Class A-1, Class A-2, Class A-3, Class A-4, Class A-5, Class A-SB, Class X-A, Class X-B, Class A-S, Class B and Class C Certificates (the “Publicly Offered Certificates”) will be offered publicly. The Class X-D, Class D, Class E, Class F-RR, Class G-RR, Class NR-RR and Class R Certificates (the “Privately Offered Certificates”) and the Class 225B-A, Class 225B-B, Class 225B-C, Class 225B-D and Class 225B-E Certificates (the “Privately Offered Loan-Specific Certificates”) will be offered domestically to Qualified Institutional Buyers and to Institutional Accredited Investors (other than the Class R Certificates) and to institutions that are not U.S. Persons pursuant to Regulation S. |

| SMMEA Status: | The Publicly Offered Certificates will not constitute “mortgage related securities” for purposes of SMMEA. |

| ERISA: | The Publicly Offered Certificates are expected to be ERISA eligible. |

| Optional Termination: | On any Distribution Date on which the aggregate principal balance of the pool of mortgage loans and the Trust Subordinate Companion Loan is less than 1% of the aggregate principal balance of the mortgage loans and the Trust Subordinate Companion Loan as of the Cut-off Date, certain entities specified in the Preliminary Prospectus will have the option to purchase all of the remaining mortgage loans and the Trust Subordinate Companion Loan (and all property acquired through exercise of remedies in respect of any mortgage loan) at the price specified in the Preliminary Prospectus. Refer to “Pooling and Servicing Agreement—Termination; Retirement of Certificates” in the Preliminary Prospectus. |

| Minimum Denominations: | The Publicly Offered Certificates (other than the Class X-A and Class X-B Certificates) will be issued in minimum denominations of $10,000 and integral multiples of $1 in excess of $10,000. The Class X-A and Class X-B Certificates will be issued in minimum denominations of $1,000,000 and in integral multiples of $1 in excess of $1,000,000. |

| Settlement Terms: | DTC, Euroclear and Clearstream Banking. |

| Analytics: | The transaction is expected to be modeled by Intex Solutions, Inc. and Trepp, LLC and is expected to be available on Bloomberg L.P., Blackrock Financial Management, Inc., Interactive Data Corporation, CMBS.com, Inc., Markit Group Limited, Moody’s Analytics, MBS Data, LLC, RealINSIGHT and Thomson Reuters Corporation. |

| Risk Factors: | THE CERTIFICATES INVOLVE CERTAIN RISKS AND MAY NOT BE SUITABLE FOR ALL INVESTORS. REFER TO “RISK FACTORS” IN THE PRELIMINARY PROSPECTUS. |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

| | |

6 of 156

| Structural and Collateral Term Sheet | Benchmark 2019-B14 | |

| Collateral Characteristics | ||

| Loan Pool | ||

| Initial Pool Balance (“IPB”): | $1,322,249,369 | |

| Number of Mortgage Loans: | 53 | |

| Number of Mortgaged Properties: | 112 | |

| Average Cut-off Date Balance per Mortgage Loan: | $24,948,101 | |

| Weighted Average Current Mortgage Rate: | 3.79106% | |

| 10 Largest Mortgage Loans as % of IPB: | 39.9% | |

| Weighted Average Remaining Term to Maturity: | 106 months | |

| Weighted Average Seasoning: | 1 months | |

| Credit Statistics | ||

| Weighted Average UW NCF DSCR(1): | 2.30x | |

| Weighted Average UW NOI DY(1)(2): | 9.9% | |

| Weighted Average Cut-off Date Loan-to-Value Ratio (“LTV”)(1)(3): | 60.0% | |

| Weighted Average Maturity Date LTV(1)(3): | 56.8% | |

| Other Statistics | ||

| % of Mortgage Loans with Additional Debt: | 20.2% | |

| % of Mortgaged Properties with Single Tenants: | 11.9% | |

| Amortization | ||

| Weighted Average Original Amortization Term(4): | 362 months | |

| Weighted Average Remaining Amortization Term(4): | 362 months | |

| % of Mortgage Loans with Interest-Only: | 62.8% | |

| % of Mortgage Loans with Partial Interest-Only followed by Amortizing Balloon: | 21.8% | |

| % of Mortgage Loans with Amortizing Balloon: | 14.8% | |

| % of Mortgage Loans with Fully Amortizing: | 0.6% | |

| Lockbox / Cash Management(5) | ||

| % of Mortgage Loans with In-Place, Hard Lockboxes: | 62.5% | |

| % of Mortgage Loans with Springing Lockboxes: | 28.5% | |

| % of Mortgage Loans with In-Place, Soft Lockboxes: | 3.9% | |

| % of Mortgage Loans with In-Place, Soft (Multifamily) / Hard (Office) Lockboxes: | 3.6% | |

| % of Mortgage Loans with Springing, Soft (Multifamily) / Hard (Retail) Lockboxes: | 1.5% | |

| % of Mortgage Loans with Springing Cash Management: | 88.6% | |

| % of Mortgage Loans with In-Place Cash Management: | 11.4% | |

| Reserves | ||

| % of Mortgage Loans Requiring Monthly Tax Reserves: | 81.3% | |

| % of Mortgage Loans Requiring Monthly Insurance Reserves: | 42.4% | |

| % of Mortgage Loans Requiring Monthly CapEx Reserves(6): | 78.6% | |

| % of Mortgage Loans Requiring Monthly TI/LC Reserves(7): | 45.9% | |

| (1) | In the case of Loan Nos. 2, 3, 4, 5, 6, 7, 9, 10, 11, 12, 19, 20, 23, 28, 29 and 30, the UW NCF DSCR, UW NOI DY, Cut-off Date LTV and Maturity Date LTV calculations include the relatedPari Passu Companion Loan(s). In the case of Loan Nos. 2, 4, 5, 9, 19 and 21, the UW NCF DSCR, UW NOI DY, Cut-off Date LTV and Maturity Date LTV calculations exclude the related Subordinate Companion Loan(s) and/or mezzanine loan(s). |

| (2) | In the case of Loan Nos. 36 and 49, the UW NOI DY are calculated net of a holdback reserve. |

| (3) | In the case of Loan Nos. 3, 7, 11, 12, 20, 21, 24, 29, 32, 35, 39, 41 and 50, the Cut-off Date LTV and the Maturity Date LTV are calculated by using an appraised value based on certain hypothetical assumptions. Refer to “Description of the Mortgage Pool—Assessments of Property Value and Condition” and “—Appraised Value” in the Preliminary Prospectus for additional details. |

| (4) | Excludes 28 mortgage loans that are interest-only for the entire term or until the related anticipated repayment date. |

| (5) | For a more detailed description of Lockbox / Cash Management, refer to “Description of the Mortgage Pool—Certain Terms of the Mortgage Loans—Mortgaged Property Accounts” in the Preliminary Prospectus. |

| (6) | CapEx Reserves include FF&E reserves for hotel properties. |

| (7) | Calculated only with respect to the Cut-off Date Balance of mortgage loans secured or partially secured by retail, office, industrial and mixed use properties. |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

| | |

7 of 156

| Structural and Collateral Term Sheet | Benchmark 2019-B14 | |

| Collateral Characteristics | ||

Mortgage Loan Seller | Number of Mortgage Loans | Number of Mortgaged Properties | Aggregate | % of IPB |

| JPMCB(1) | 23 | 43 | $624,759,959 | 47.2% |

| CREFI | 19 | 53 | 404,497,000 | 30.6 |

| GACC(2) | 11 | 16 | 292,992,410 | 22.2 |

| Total | 53 | 112 | $1,322,249,369 | 100.0% |

| (1) | In the case of loan No. 4, the whole loan was co-originated by JPMCB and Goldman Sachs Bank USA. In the case of Loan No. 10, the whole loan was co-originated by JPMCB and Wells Fargo Bank, National Association. In the case of Loan No. 19, the whole loan was co-originated by JPMCB, Morgan Stanley Bank, N.A., Wells Fargo Bank, National Association and Goldman Sachs Bank USA. In the case of Loan No. 20, the whole loan was co-originated by JPMCB, Wells Fargo Bank, National Association and Bank of America, N.A. In the case of Loan No. 29, the whole loan was co-originated by JPMCB and Wells Fargo Bank, National Association. |

| (2) | Nine of the mortgage loans (15.5%) being sold by German American Capital Corporation (“GACC”) were originated or co-originated by an affiliate thereof, DBR Investments Co. Limited, and will be transferred to GACC on or prior to the closing date. Two of the mortgage loans (6.7%) being sold by GACC were originated or co-originated by an affiliate thereof, Deutsche Bank AG, New York Branch (“DBNY”). DBNY on the origination date transferred such mortgage loans to DBRI, and DBRI will transfer such mortgage loans to GACC on or prior to the closing date. |

| Ten Largest Mortgage Loans | |||||||||||

| No. | Loan Name | Mortgage Loan Seller | No. of Prop. | Cut-off Date Balance | % of IPB | SF / Units | Property Type | UW NCF DSCR(1) | UW NOI DY(1) | Cut-off Date LTV(1)(2) | Maturity Date LTV(1)(2) |

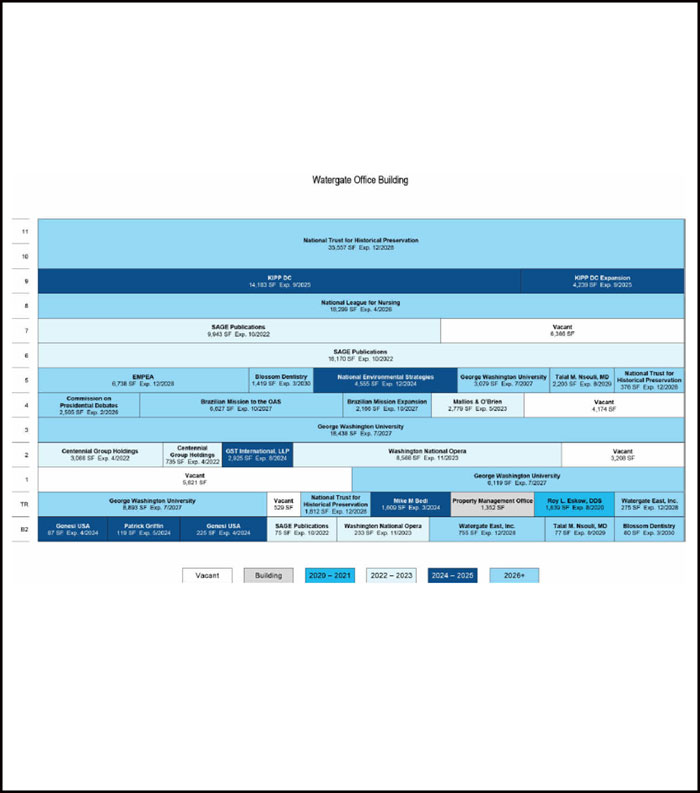

| 1 | Watergate Office Building | CREFI | 1 | $73,000,000 | 5.5% | 215,200 | Office | 2.04x | 8.2% | 69.5% | 69.5% |

| 2 | 225 Bush | GACC | 1 | $60,000,000 | 4.5% | 579,987 | Office | 3.85x | 13.4% | 34.6% | 34.6% |

| 3 | Innovation Park | JPMCB | 1 | $60,000,000 | 4.5% | 1,854,729 | Office | 2.96x | 11.6% | 68.8% | 68.8% |

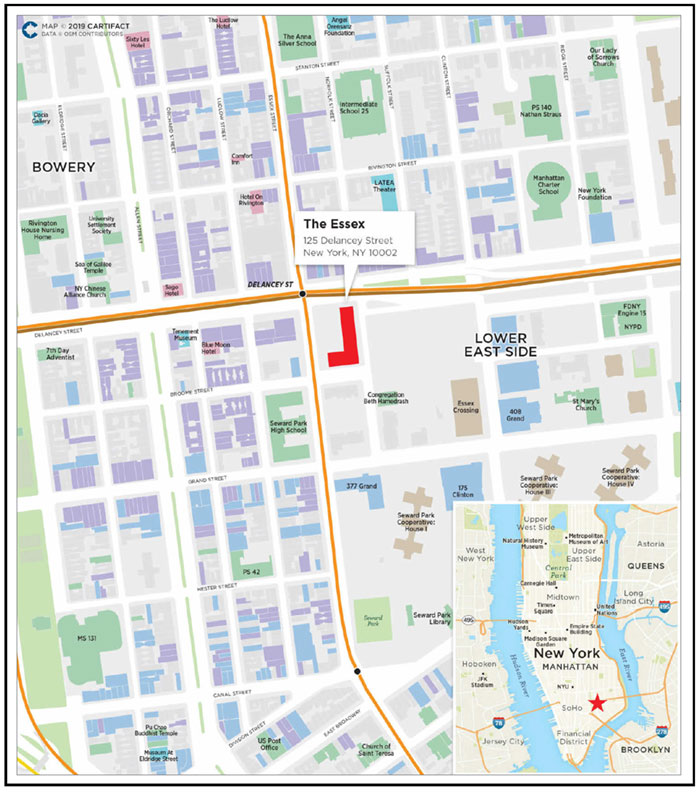

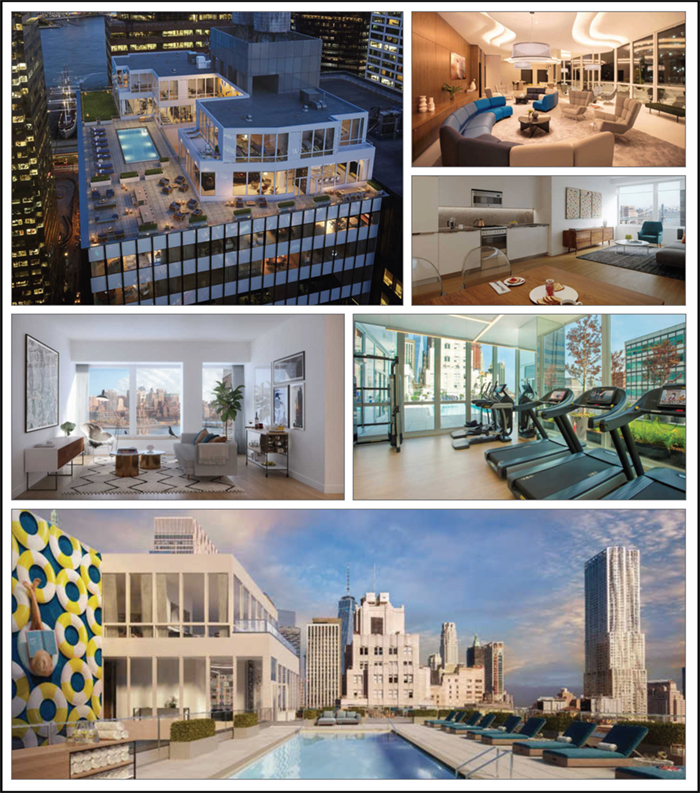

| 4 | The Essex | JPMCB | 1 | $56,900,000 | 4.3% | 195 | Mixed Use | 3.66x | 10.3% | 39.9% | 39.9% |

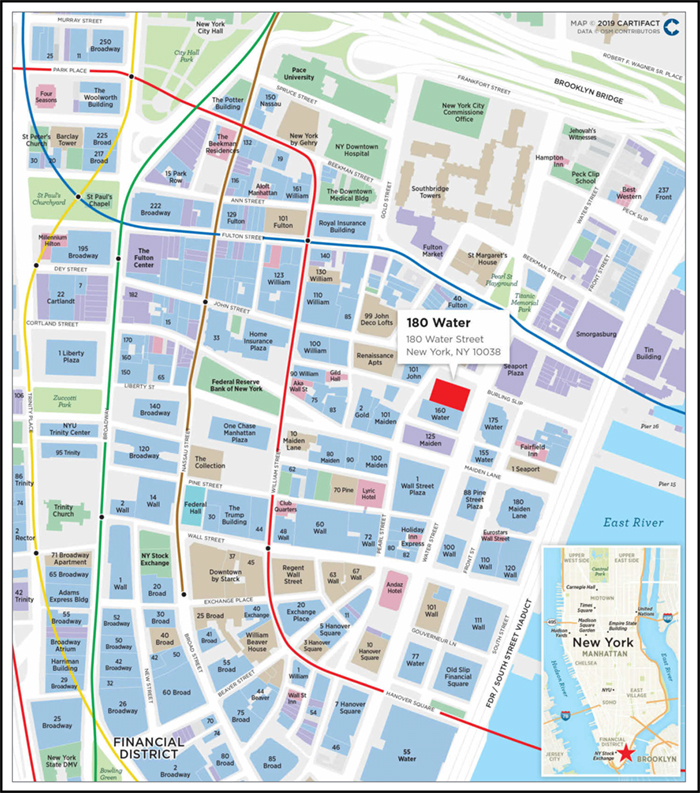

| 5 | 180 Water | GACC | 1 | $50,000,000 | 3.8% | 573 | Multifamily | 3.15x | 11.0% | 30.5% | 30.5% |

| 6 | Harvey Building Products | CREFI | 30 | $50,000,000 | 3.8% | 2,046,119 | Various | 1.51x | 9.1% | 69.4% | 62.8% |

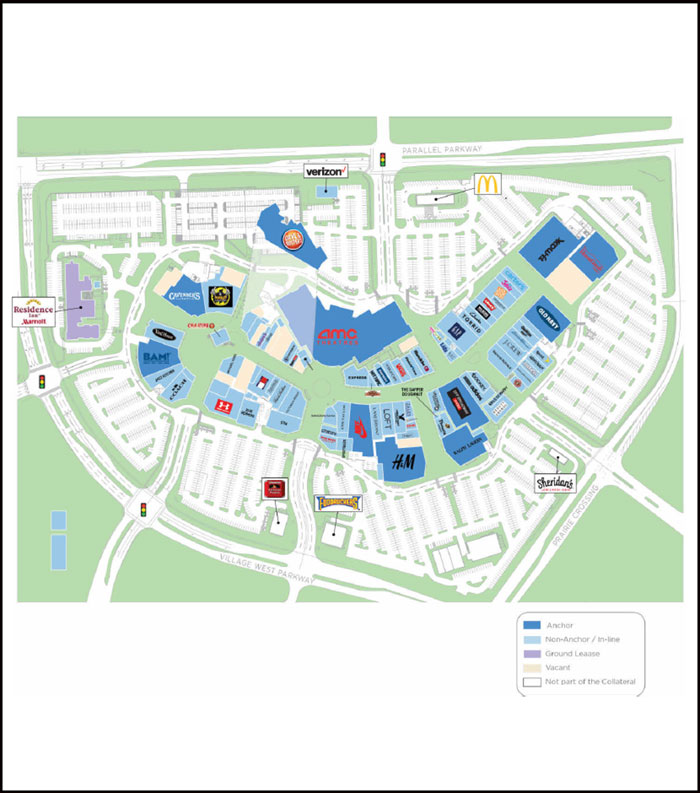

| 7 | Legends at Village West | CREFI | 1 | $50,000,000 | 3.8% | 702,750 | Retail | 1.67x | 9.5% | 53.3% | 48.3% |

| 8 | 80 on the Commons | GACC | 1 | $47,300,000 | 3.6% | 296,190 | Mixed Use | 3.50x | 11.0% | 64.4% | 64.4% |

| 9 | Osborn Triangle | JPMCB | 3 | $40,000,000 | 3.0% | 676,947 | Mixed Use | 3.12x | 12.5% | 37.1% | 37.1% |

| 10 | Tysons Tower | JPMCB | 1 | $40,000,000 | 3.0% | 528,730 | Office | 3.07x | 11.0% | 52.1% | 52.1% |

| Top 3 Total/Weighted Average | 3 | $193,000,000 | 14.6% | 2.89x | 10.9% | 58.4% | 58.4% | ||||

| Top 5 Total/Weighted Average | 5 | $299,900,000 | 22.7% | 3.08x | 10.8% | 50.3% | 50.3% | ||||

| Top 10 Total/Weighted Average | 41 | $527,200,000 | 39.9% | 2.84x | 10.7% | 52.8% | 51.7% | ||||

| (1) | In the case of Loan Nos. 2, 3, 4, 5, 6, 7, 9 and 10, the UW NCF DSCR, UW NOI DY, Cut-off Date LTV and LTV Ratio at Maturity calculations include the relatedPari Passu Companion Loan(s). In the case of Loan Nos. 2, 4, 5 and 9, the UW NCF DSCR, UW NOI DY, Cut-off Date LTV and Maturity Date LTV calculations exclude the related Subordinate Companion Loan(s). |

| (2) | In the case of Loan Nos. 3 and 7, the Cut-off Date LTV and the Maturity Date LTV are calculated by using an appraised value based on certain hypothetical assumptions. Refer to “Description of the Mortgage Pool—Assessments of Property Value and Condition” and “—Appraised Value” in the Preliminary Prospectus for additional details. |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

| | |

8 of 156

| Structural and Collateral Term Sheet | Benchmark 2019-B14 | |

| Collateral Characteristics | ||

| Companion Loan Summary | ||||||||

| Loan No. | Mortgage Loan | Note(s) | Original Balance ($) | Cut-off Date Balance ($) | Holder of Note | Lead Servicer for Whole Loan (Y/N) | Master Servicer Under Lead Securitization | Special Servicer Under Lead Securitization |

| 2 | 225 Bush | A-1, A-6 | $60,000,000 | $60,000,000 | BMARK 2019-B14 | Yes(2) | Midland | Midland |

| A-2, A-3, A-4, A-5 | $143,600,000 | $143,600,000 | DBRI | No | ||||

| B-1(1) | $146,400,000 | $146,400,000 | BMARK 2019-B14 | No(2) | ||||

| Total | $350,000,000 | $350,000,000 | ||||||

| 3 | Innovation Park

| A-1 | $60,000,000 | $60,000,000 | BMARK 2019-B14 | No(3) | ||

| A-2 | $70,000,000 | $70,000,000 | JPMCB | Yes | (3) | (3) | ||

| A-3 | $52,250,000 | $52,250,000 | JPMCB | No | ||||

| Total | $182,250,000 | $182,250,000 | ||||||

| 4 | The Essex | A-1-1, A-1-3 | $56,900,000 | $56,900,000 | BMARK 2019-B14 | Yes | Midland | Midland |

| A-1-2 | $25,000,000 | $25,000,000 | JPMCB | No | ||||

| A-1-4 | $35,100,000 | $35,100,000 | GS | No | ||||

| B-1(1) | $40,600,000 | $40,600,000 | JPMCB(4) | No | ||||

| B-2(1) | $17,400,000 | $17,400,000 | GS(4) | No | ||||

| Total | $175,000,000 | $175,000,000 | ||||||

| 5 | 180 Water | A-1 | $50,000,000 | $50,000,000 | BMARK 2019-B14 | No(5) | ||

| A-2 | $40,000,000 | $40,000,000 | DBRI | Yes | (5) | (5) | ||

| A-3, A-4, A-5 | $47,500,000 | $47,500,000 | DBRI | No | ||||

| B-1(1) | $127,500,000 | $127,500,000 | DBRI | No(5) | ||||

| Total | $265,000,000 | $265,000,000 | ||||||

| 6 | Harvey Building Products | A-1 | $60,000,000 | $60,000,000 | CREFI | No | ||

| A-2 | $50,000,000 | $50,000,000 | BMARK 2019-B14 | Yes | Midland | Midland | ||

| A-3 | $50,000,000 | $50,000,000 | CREFI | No | ||||

| Total | $160,000,000 | $160,000,000 | ||||||

| 7 | Legends at Village West | A-1 | $50,000,000 | $50,000,000 | BMARK 2019-B14 | Yes | Midland | Midland |

| A-2 | $40,000,000 | $40,000,000 | CREFI | No | ||||

| A-3 | $30,000,000 | $30,000,000 | CREFI | No | ||||

| Total | $120,000,000 | $120,000,000 | ||||||

| 9 | Osborn Triangle | A-1 | $250,000,000 | $250,000,000 | JPMCC 2019-OSB | Yes | KeyBank | Situs |

| A-2 | $50,000,000 | $50,000,000 | BMARK 2019-B12 | No | ||||

| A-3 | $50,000,000 | $50,000,000 | BMARK 2019-B13 | No | ||||

| A-4 | $40,000,000 | $40,000,000 | BMARK 2019-B14 | No | ||||

| A-5 | $20,000,000 | $20,000,000 | JPMCB | No | ||||

| A-6-1 | $20,000,000 | $20,000,000 | CCRE | No | ||||

| B-1(1) | $145,000,000 | $145,000,000 | JPMCC 2019-OSB | No | ||||

| Total | $575,000,000 | $575,000,000 | ||||||

| 10 | Tysons Tower | A-1 | $50,000,000 | $50,000,000 | BANK 2019-BNK21 | Yes | Rialto | Wells |

| A-2, A-3 | $45,000,000 | $45,000,000 | WFB | No | ||||

| A-4 | $40,000,000 | $40,000,000 | BMARK 2019-B14 | No | ||||

| A-5, A-6, A-7 | $55,000,000 | $55,000,000 | JPMCB | No | ||||

| Total | $190,000,000 | $190,000,000 | ||||||

| 11 | 900 & 990 Stewart Avenue | A-1 | $45,000,000 | $45,000,000 | BMARK 2019-B13 | Yes | Midland | CWCapital |

| A-2 | $39,000,000 | $39,000,000 | BMARK 2019-B14 | No | ||||

| Total | $84,000,000 | $84,000,000 | ||||||

| 12 | Hilton Cincinnati Netherland Plaza | A-1 | $35,500,000 | $35,500,000 | BMARK 2019-B14 | Yes | Midland | Midland |

| A-2 | $17,000,000 | $17,000,000 | JPMCB | No | ||||

| A-3 | $20,000,000 | $20,000,000 | JPMCB | No | ||||

| Total | $72,500,000 | $72,500,000 | ||||||

| (1) | Each note represents a subordinate companion loan. |

| (2) | In the case of Loan No. 2, the initial control note is Note B-1. During the continuance of a 225 Bush Control Appraisal Period, Note A-1 will be the Control Note. See “Description of the Mortgage Pool—The Whole Loans—The Non-Serviced AB Whole Loans—225 Bush Whole Loan” in the Preliminary Prospectus. |

| (3) | In the case of Loan No. 3, the whole loan is expected to be serviced under the BMARK 2019-B14 pooling and servicing agreement until such time the controlling note has been securitized, at which point such whole loan will be serviced under the pooling and servicing agreement related to such securitization. JPMCB holds the related controllingpari passu companion loan and is entitled to exercise control rights until the securitization of such controllingpari passu companion loan. |

| (4) | In the case of Loan No. 4, Note B-1 and B-2 are expected to be sold to an unrelated third party. The initial control note is Note B-1. During the continuance of The Essex Control Appraisal Period, Note A-1-1 will be the Control Note. The whole loan will be serviced under the BMARK 2019-B14 pooling and servicing agreement. JPMCB holds the related controlling subordinate companion loan and is entitled to exercise control rights of such controlling subordinate companion loan. See “Description of the Mortgage Pool--The Whole Loans--The Serviced AB Whole Loans--The Essex Whole Loan” in the Preliminary Prospectus. |

| (5) | In the case of Loan No. 5, the initial control note is Note B-1. During the continuance of a 180 Water Control Appraisal Period, Note A-1 will be the Control Note. The whole loan is expected to be serviced under the BMARK 2019-B14 pooling and servicing agreement until such time both another Note A and Note B-1 have been securitized, at which point such whole loan will be serviced under the pooling and servicing agreement related to such securitization. DBRI holds the related controlling subordinate companion loan and is entitled to exercise control rights until the securitization of such controlling subordinate companion loan. See “Description of the Mortgage Pool—The Whole Loans—The Non-Serviced AB Whole Loans—180 Water Whole Loan” in the Preliminary Prospectus. |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

| | |

9 of 156

| Structural and Collateral Term Sheet | Benchmark 2019-B14 | |

| Collateral Characteristics | ||

| Loan No. | Mortgage Loan | Note(s) | Original Balance ($) | Cut-off Date Balance ($) | Holder of Note | Lead Servicer for Whole Loan (Y/N) | Master Servicer Under Lead Securitization | Special Servicer Under Lead Securitization |

| 19 | Grand Canal Shoppes | A-1-1, A-1-6 | $70,000,000 | $70,000,000 | MSC 2019-H7 | Yes(2) | Midland | LNR |

| A-1-2, A-2-1 | $100,000,000 | $100,000,000 | BANK 2019-BNK19 | No | ||||

| A-3-1 | $50,000,000 | $50,000,000 | BMARK 2019-B12 | No | ||||

| A-3-2 | $50,000,000 | $50,000,000 | BMARK 2019-B13 | No | ||||

| A-4-1 | $60,000,000 | $60,000,000 | CGCMT 2019-GC41 | No | ||||

| A-4-3 | $20,000,000 | $20,000,000 | GSMS 2019-GC42 | No | ||||

| A-1-7, A-1-8, A-2-2-1 | $40,000,000 | $40,000,000 | BANK 2019-BNK20 | No | ||||

| A-2-2-2 | $30,000,000 | $30,000,000 | CSAIL 2019-C17 | No | ||||

| A-2-3, A-2-5 | $50,384,615 | $50,384,615 | UBS 2019-C17 | No | ||||

| A-1-4 | $40,000,000 | $40,000,000 | BANK 2019-BNK21 | No | ||||

| A-3-3-1, A-3-5 | $30,384,615 | $30,384,615 | BMARK 2019-B14 | No | ||||

| A-1-3, A-1-5 | $53,846,154 | $53,846,154 | MSNBA | No | ||||

| A-3-3-2 | $20,000,000 | $20,000,000 | JPMCB | No | ||||

| A-3-4 | $25,000,000 | $25,000,000 | CCRE | No | ||||

| A-4-2, A-4-4, A-4-5 | $95,384,615 | $95,384,615 | GSBI | No | ||||

| A-2-4 | $25,000,000 | $25,000,000 | UBS AG | No | ||||

| B-1(1) | $215,000,000 | $215,000,000 | CPPIB Credit Investment II Inc. | No(2) | ||||

| Total | $975,000,000 | $975,000,000 | ||||||

| 20 | 230 Park Avenue South

| A-1, A-4 | $110,000,000 | $110,000,000 | BANK 2019-BNK21 | Yes | Rialto | Wells |

| A-2, A-3 | $55,000,000 | $55,000,000 | WFB | No | ||||

| A-5, A-6 | $55,000,000 | $55,000,000 | BAML | No | ||||

| A-7 | $30,000,000 | $30,000,000 | BMARK 2019-B14 | No | ||||

| Total | $250,000,000 | $250,000,000 | ||||||

| 23 | 8 West Centre | A-1 | $26,000,000 | $26,000,000 | BMARK 2019-B14 | Yes | Midland | Midland |

| A-2 | $18,200,000 | $18,200,000 | JPMCB | No | ||||

| Total | $44,200,000 | $44,200,000 | ||||||

| 29 | 600 & 620 National | A-1-1 | $38,950,000 | $38,950,000 | UBSCM 2019-C17 | Yes | Midland | CWCapital |

| A-2-1-A | $20,000,000 | $20,000,000 | BMARK 2019-B14 | No | ||||

| A-1-2 | $30,000,000 | $30,000,000 | WFM | No | ||||

| A-2-1-B, A-2-2-A, A-2-2-B, A-2-3 | $48,950,000 | $48,950,000 | JPMCB | No | ||||

| Total | $137,900,000 | $137,900,000 | ||||||

| 28 | Sunset North | A-1 | $75,000,000 | $75,000,000 | BMARK 2019-B13 | Yes | Midland | CWCapital |

| A-2 | $20,000,000 | $20,000,000 | BMARK 2019-B14 | No | ||||

| A-3 | $39,500,000 | $39,500,000 | JPMCB | No | ||||

| A-4 | $15,500,000 | $15,500,000 | JPMCB | No | ||||

| Total | $150,000,000 | $150,000,000 | ||||||

| 30 | City Hyde Park | A-1 | $45,000,000 | $45,000,000 | BMARK 2019-B13 | Yes | Midland | CWCapital |

| A-2-A | $20,000,000 | $20,000,000 | BMARK 2019-B14 | No | ||||

| A-2-B | $20,000,000 | $20,000,000 | JPMCB | No | ||||

| A-3 | $27,000,000 | $27,000,000 | JPMCB | No | ||||

| Total | $112,000,000 | $112,000,000 |

| (1) | Each note represents a subordinate companion loan. |

| (2) | In the case of Loan No. 19, the initial control note is Note B-1. During the continuance of a Grand Canal Shoppes Control Appraisal Period, Note A-1-1 will be the Control Note. See “Description of the Mortgage Pool—The Whole Loans—The Non-Serviced AB Whole Loans—Grand Canal Shoppes Whole Loan” in the Preliminary Prospectus. |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

| | |

10 of 156

| Structural and Collateral Term Sheet | Benchmark 2019-B14 | |

| Collateral Characteristics | ||

| Additional Debt Summary |

No. | Loan Name | Trust | Subordinate | Total Debt | Mortgage | Total | Mortgage | Total | Mortgage | Total |

| 2 | 225 Bush | $60,000,000 | $146,400,000 | $350,000,000 | 3.85x | 2.24x | 34.6% | 59.4% | 13.4% | 7.8% |

| 4 | The Essex | $56,900,000 | $98,000,000 | $215,000,000 | 3.66x | 1.33x | 39.9% | 73.4% | 10.3% | 5.6% |

| 5 | 180 Water | $50,000,000 | $227,500,000 | $365,000,000 | 3.15x | 0.85x | 30.5% | 80.8% | 11.0% | 4.1% |

| 9 | Osborn Triangle | $40,000,000 | $145,000,000 | $575,000,000 | 3.12x | 2.33x | 37.1% | 49.7% | 12.5% | 9.3% |

| 19 | Grand Canal Shoppes | $30,384,615 | $215,000,000 | $975,000,000 | 2.46x | 1.67x | 46.3% | 59.5% | 9.6% | 7.5% |

| 21 | Villas on Nueces | $30,000,000 | $7,000,000 | $37,000,000 | 2.04x | 1.49x | 52.7% | 65.0% | 9.6% | 7.8% |

| (1) | In the case of Loan Nos. 2, 9 and 19 Subordinate Debt Cut-off Date Balance represents one or more Subordinate Companion Loans. In the case of Loan Nos. 4 and 5, Subordinate Debt Cut-off Date Balance represents one or more Subordinate Companion Loans and one or more mezzanine loans. In the case of Loan No. 21, Subordinate Debt Cut-off Date Balance represents one or more mezzanine loans. |

| (2) | In the case of Loan Nos. 2, 4, 5, 9 and 19, the Mortgage Loan UW NCF DSCR, Mortgage Loan Cut-off Date LTV and Mortgage Loan UW NOI DY calculations include the relatedPari Passu Companion Loan(s). In the case of Loan Nos. 2, 4, 5, 9, 19 and 21 the Mortgage Loan UW NCF DSCR, Mortgage Loan Cut-off Date LTV and Mortgage Loan UW NOI DY, calculations exclude the related Subordinate Companion Loan(s) and/or related mezzanine loan(s). |

| (3) | In the case of Loan No. 21, the Mortgage Loan Cut-off Date LTV and Total Debt Cut-off Date LTV is calculated using an appraised value based on certain hypothetical assumptions. Refer to “Description of the Mortgage Pool—Assessments of Property Value and Condition” and “—Appraised Value” in the Preliminary Prospectus for additional details. |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

| | |

11 of 156

| Structural and Collateral Term Sheet | Benchmark 2019-B14 | |

| Collateral Characteristics | ||

| Mortgaged Properties by Type(1) |

| Weighted Average | |||||||||

| Property Type | Property Subtype | Number of Properties | Cut-off Date Principal Balance | % of IPB | Occupancy | UW NCF DSCR(2) | UW NOI DY(2)(3) | Cut-off Date LTV(2)(4) | Maturity Date LTV(2)(4) |

| Office | Suburban | 9 | $268,898,438 | 20.3% | 96.7% | 2.49x | 10.5% | 65.1% | 62.7% |

| CBD | 3 | 163,000,000 | 12.3 | 93.5% | 2.82x | 10.2% | 53.2% | 53.2% | |

| Subtotal: | 12 | $431,898,438 | 32.7% | 95.5% | 2.61x | 10.4% | 60.6% | 59.2% | |

| Multifamily | Garden | 28 | $125,672,343 | 9.5% | 95.9% | 1.53x | 8.2% | 70.8% | 66.0% |

| High-Rise | 2 | 82,500,000 | 6.2 | 96.5% | 2.42x | 9.2% | 46.3% | 42.9% | |

| Student Housing | 2 | 50,053,000 | 3.8 | 97.5% | 1.94x | 10.0% | 56.9% | 54.5% | |

| Mid-Rise | 3 | 39,150,000 | 3.0 | 98.1% | 1.65x | 6.8% | 66.1% | 66.1% | |

| Subtotal: | 35 | $297,375,343 | 22.5% | 96.6% | 1.86x | 8.6% | 61.0% | 57.7% | |

| Retail | Anchored | 6 | $152,694,410 | 11.5% | 91.1% | 1.96x | 9.8% | 62.7% | 57.1% |

| Specialty Retail | 1 | 30,384,615 | 2.3 | 94.0% | 2.46x | 9.6% | 46.3% | 46.3% | |

| Single Tenant | 2 | 22,770,000 | 1.7 | 100.0% | 1.88x | 8.1% | 61.9% | 61.9% | |

| Unanchored | 2 | 22,250,000 | 1.7 | 95.4% | 1.45x | 9.3% | 64.7% | 48.5% | |

| Shadow Anchored | 1 | 13,475,000 | 1.0 | 94.9% | 1.53x | 9.3% | 74.4% | 61.2% | |

| Freestanding | 2 | 8,600,000 | 0.7 | 100.0% | 2.11x | 13.1% | 59.9% | 51.5% | |

| Subtotal: | 14 | $250,174,025 | 18.9% | 93.2% | 1.95x | 9.7% | 61.3% | 55.5% | |

| Mixed use | Multifamily/Retail | 2 | $76,900,000 | 5.8% | 99.1% | 2.98x | 9.4% | 48.7% | 47.1% |

| Office/Multifamily | 1 | 47,300,000 | 3.6 | 95.1% | 3.50x | 11.0% | 64.4% | 64.4% | |

| Office/Laboratory | 3 | 40,000,000 | 3.0 | 100.0% | 3.12x | 12.5% | 37.1% | 37.1% | |

| Retail/Office | 1 | 12,400,000 | 0.9 | 97.2% | 3.11x | 11.6% | 57.7% | 57.7% | |

| Subtotal: | 7 | $176,600,000 | 13.4% | 98.1% | 3.16x | 10.7% | 50.9% | 50.2% | |

| Industrial | Warehouse/Distribution | 22 | $25,368,750 | 1.9% | 100.0% | 1.51x | 9.1% | 69.4% | 62.8% |

| Manufacturing | 2 | 15,281,250 | 1.2 | 100.0% | 1.51x | 9.1% | 69.4% | 62.8% | |

| Flex | 1 | 12,500,000 | 0.9 | 92.7% | 1.58x | 9.9% | 58.1% | 53.0% | |

| Warehouse | 6 | 12,451,563 | 0.9 | 100.0% | 1.48x | 15.3% | 49.7% | 22.6% | |

| Subtotal: | 31 | $65,601,563 | 5.0% | 98.6% | 1.52x | 10.4% | 63.5% | 53.3% | |

| Self Storage | Self Storage | 9 | $51,300,000 | 3.9% | 82.6% | 2.28x | 9.3% | 62.7% | 60.7% |

| Subtotal: | 9 | $51,300,000 | 3.9% | 82.6% | 2.28x | 9.3% | 62.7% | 60.7% | |

| Hotel | Full Service | 1 | $35,500,000 | 2.7% | 74.8% | 1.62x | 10.9% | 68.7% | 63.7% |

| Extended Stay | 2 | 7,000,000 | 0.5 | 92.3% | 4.59x | 17.0% | 51.9% | 51.9% | |

| Subtotal: | 3 | $42,500,000 | 3.2% | 77.7% | 2.11x | 11.9% | 65.9% | 61.8% | |

| Manufactured Housing | Manufactured Housing | 1 | $6,800,000 | 0.5% | 94.4% | 1.56x | 9.1% | 73.1% | 63.2% |

| Subtotal: | 1 | $6,800,000 | 0.5% | 94.4% | 1.56x | 9.1% | 73.1% | 63.2% | |

| Total / Weighted Average: | 112 | 1,322,249,369 | 100.0% | 94.7% | 2.30x | 9.9% | 60.0% | 56.8% | |

| (1) | Because this table presents information relating to the mortgaged properties and not mortgage loans, the information for mortgage loans secured by more than one mortgaged property is based on allocated loan amounts. |

| (2) | In the case of Loan Nos. 2, 3, 4, 5, 6, 7, 9, 10, 11, 12, 19, 20, 23, 28, 29 and 30, the UW NCF DSCR, UW NOI DY, Cut-off Date LTV and Maturity Date LTV calculations include the relatedPari Passu Companion Loan(s). In the case of Loan Nos. 2, 4, 5, 9, 19 and 21, the UW NCF DSCR, UW NOI DY, Cut-off Date LTV and Maturity Date LTV calculations exclude the related Subordinate Companion Loan(s) and/or mezzanine loan(s). |

| (3) | In the case of Loan Nos. 36 and 49, the UW NOI DY are calculated net of a holdback reserve. |

| (4) | In the case of Loan Nos. 3, 7, 11, 12, 20, 21, 24, 29, 32, 35, 39, 41 and 50, the Cut-off Date LTV and the Maturity Date LTV are calculated using an appraised value based on certain hypothetical assumptions. Refer to “Description of the Mortgage Pool—Assessments of Property Value and Condition” and “—Appraised Value” in the Preliminary Prospectus for additional details. |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

| | |

12 of 156

| Structural and Collateral Term Sheet | Benchmark 2019-B14 | |

| Collateral Characteristics | ||

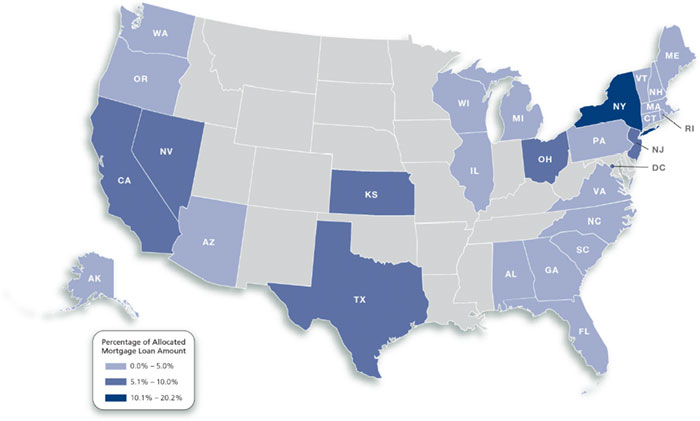

| Mortgaged Properties by Location(1) | ||||||||

Weighted Average | ||||||||

State | Number of Properties | Cut-off Date Principal Balance | % of IPB | Occupancy | UW NCF DSCR(2) | UW NOI DY(2)(3) | Cut-off Date LTV(2)(4) | Maturity Date LTV(2)(4) |

| New York | 10 | $267,750,000 | 20.2% | 97.0% | 2.46x | 9.2% | 52.2% | 50.0% |

| California | 5 | 120,700,000 | 9.1 | 97.1% | 2.79x | 10.5% | 49.5% | 49.0% |

| New Jersey | 21 | 101,160,000 | 7.7 | 93.8% | 1.47x | 8.6% | 73.7% | 66.9% |

| Ohio | 3 | 89,600,000 | 6.8 | 87.0% | 2.61x | 10.8% | 66.8% | 64.0% |

| Texas | 7 | 85,552,343 | 6.5 | 97.2% | 1.90x | 10.5% | 60.6% | 53.9% |

| District of Columbia | 2 | 83,570,000 | 6.3 | 88.9% | 2.07x | 8.3% | 68.6% | 68.6% |

| Kansas | 2 | 70,053,000 | 5.3 | 92.6% | 1.70x | 9.8% | 56.2% | 50.9% |

| Nevada | 3 | 69,735,115 | 5.3 | 91.9% | 2.71x | 10.2% | 56.6% | 56.6% |

| North Carolina | 2 | 63,914,200 | 4.8 | 95.4% | 2.93x | 11.5% | 68.4% | 68.4% |

| Florida | 5 | 63,406,680 | 4.8 | 95.0% | 1.93x | 9.9% | 65.3% | 57.2% |

| Massachusetts | 14 | 61,243,750 | 4.6 | 100.0% | 2.56x | 11.3% | 48.3% | 46.0% |

| Virginia | 1 | 40,000,000 | 3.0 | 100.0% | 3.07x | 11.0% | 52.1% | 52.1% |

| Arizona | 1 | 35,250,000 | 2.7 | 85.8% | 1.52x | 9.0% | 66.3% | 57.2% |

| Wisconsin | 1 | 34,000,000 | 2.6 | 100.0% | 2.87x | 10.1% | 65.3% | 65.3% |

| Illinois | 2 | 25,600,000 | 1.9 | 97.4% | 1.33x | 8.4% | 71.3% | 64.3% |

| Washington | 1 | 20,000,000 | 1.5 | 98.8% | 2.63x | 9.1% | 66.1% | 66.1% |

| Michigan | 6 | 18,510,000 | 1.4 | 94.6% | 3.55x | 14.9% | 53.9% | 53.9% |

| New Hampshire | 5 | 15,187,500 | 1.1 | 100.0% | 1.51x | 9.1% | 69.4% | 62.8% |

| Alabama | 1 | 13,475,000 | 1.0 | 94.9% | 1.53x | 9.3% | 74.4% | 61.2% |

| Georgia | 3 | 11,879,120 | 0.9 | 79.8% | 2.52x | 9.3% | 62.2% | 62.2% |

| Oregon | 1 | 11,593,910 | 0.9 | 93.4% | 1.69x | 10.2% | 74.8% | 59.1% |

| Connecticut | 7 | 8,075,000 | 0.6 | 100.0% | 1.51x | 9.1% | 69.4% | 62.8% |

| Alaska | 1 | 3,500,000 | 0.3 | 82.9% | 3.34x | 12.7% | 44.9% | 44.9% |

| South Carolina | 1 | 3,000,000 | 0.2 | 100.0% | 1.78x | 10.2% | 55.6% | 50.2% |

| Pennsylvania | 3 | 2,256,250 | 0.2 | 100.0% | 1.51x | 9.1% | 69.4% | 62.8% |

| Rhode Island | 2 | 2,071,875 | 0.2 | 100.0% | 1.51x | 9.1% | 69.4% | 62.8% |

| Maine | 1 | 843,750 | 0.1 | 100.0% | 1.51x | 9.1% | 69.4% | 62.8% |

| Vermont | 1 | 321,875 | 0.0 | 100.0% | 1.51x | 9.1% | 69.4% | 62.8% |

| Total / Weighted Average: | 112 | $1,322,249,369 | 100.0% | 94.7% | 2.30x | 9.9% | 60.0% | 56.8% |

| (1) | Because this table presents information relating to the mortgaged properties and not mortgage loans, the information for mortgage loans secured by more than one mortgaged property is based on allocated loan amounts. |

| (2) | In the case of Loan Nos. 2, 3, 4, 5, 6, 7, 9, 10, 11, 12, 19, 20, 23, 28, 29 and 30 , the UW NCF DSCR, UW NOI DY, Cut-off Date LTV and Maturity Date LTV calculations include the relatedPari Passu Companion Loan(s). In the case of Loan Nos. 2, 4, 5, 9, 19 and 21, the UW NCF DSCR, UW NOI DY, Cut-off Date LTV and Maturity Date LTV calculations exclude the related Subordinate Companion Loan(s) and/or mezzanine loan(s). |

| (3) | In the case of Loan Nos. 36 and 49, the UW NOI DY are calculated net of a holdback reserve. |

| (4) | In the case of Loan Nos. 3, 7, 11, 12, 20, 21, 24, 29, 32, 35, 39, 41 and 50, the Cut-off Date LTV and the Maturity Date LTV are calculated using an appraised value based on certain hypothetical assumptions. Refer to “Description of the Mortgage Pool—Assessments of Property Value and Condition” and “—Appraised Value” in the Preliminary Prospectus for additional details. |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

| | |

13 of 156

| Structural and Collateral Term Sheet | Benchmark 2019-B14 | |

| Collateral Characteristics | ||

| Cut-off Date Principal Balance |

Weighted Average | |||||||||||

| Range of Cut-off Date Principal Balances | Number of Loans | Cut-off Date Principal Balance | % of IPB | Mortgage Rate | Remaining Loan Term | UW NCF DSCR(1) | UW NOI DY(1)(2) | Cut-off Date LTV(1)(3) | Maturity Date LTV(1)(3) | ||

| $3,000,000 | - | $9,999,999 | 10 | $54,724,843 | 4.1% | 3.95537% | 119 | 2.12x | 12.4% | 59.1% | 47.7% |

| $10,000,000 | - | $19,999,999 | 13 | 173,153,410 | 13.1 | 4.02067% | 110 | 1.92x | 9.7% | 65.4% | 59.6% |

| $20,000,000 | - | $24,999,999 | 6 | 125,176,500 | 9.5 | 3.74034% | 119 | 2.11x | 8.7% | 66.9% | 64.9% |

| $25,000,000 | - | $49,999,999 | 17 | 569,294,615 | 43.1 | 3.93399% | 111 | 2.20x | 9.6% | 61.9% | 58.7% |

| $50,000,000 | - | $73,000,000 | 7 | 399,900,000 | 30.2 | 3.48156% | 91 | 2.71x | 10.4% | 53.0% | 51.6% |

Total / Wtd. Avg: | 53 | $1,322,249,369 | 100.0% | 3.79106% | 106 | 2.30x | 9.9% | 60.0% | 56.8% | ||

| Mortgage Interest Rates |

Weighted Average | |||||||||||

| Range of Mortgage Interest Rates | Number of Loans | Cut-off Date Principal Balance | % of IPB | Mortgage Rate | Remaining Loan Term | UW NCF DSCR(1) | UW NOI DY(1)(2) | Cut-off Date LTV(1)(3) | Maturity Date LTV(1)(3) | ||

| 2.75900% | - | 3.99999% | 38 | $1,038,302,025 | 78.5% | 3.57420% | 107 | 2.51x | 10.2% | 57.5% | 54.7% |

| 4.00000% | - | 4.49999% | 8 | 112,499,843 | 8.5 | 4.27968% | 91 | 1.71x | 9.1% | 68.3% | 63.9% |

| 4.50000% | - | 4.99999% | 6 | 135,947,500 | 10.3 | 4.63591% | 120 | 1.37x | 7.7% | 70.0% | 65.6% |

| 5.00000% | - | 5.35000% | 1 | 35,500,000 | 2.7 | 5.35000% | 60 | 1.62x | 10.9% | 68.7% | 63.7% |

| Total / Wtd. Avg: | 53 | $1,322,249,369 | 100.0% | 3.79106% | 106 | 2.30x | 9.9% | 60.0% | 56.8% | ||

| Original Term to Maturity in Months |

Weighted Average | |||||||||

| Original Term to Maturity in Months | Number of Loans | Cut-off Date Principal Balance | % of IPB | Mortgage Rate | Remaining Loan Term | UW NCF DSCR(1) | UW NOI DY(1)(2) | Cut-off Date LTV(1)(3) | Maturity Date LTV(1)(3) |

| 60 | 7 | $262,827,000 | 19.9% | 3.96300% | 60 | 2.52x | 10.8% | 50.1% | 48.2% |

| 84 | 1 | 56,900,000 | 4.3 | 2.75900% | 84 | 3.66x | 10.3% | 39.9% | 39.9% |

| 120 | 45 | 1,002,522,369 | 75.8 | 3.80456% | 119 | 2.17x | 9.6% | 63.8% | 60.0% |

Total / Wtd. Avg: | 53 | $1,322,249,369 | 100.0% | 3.79106% | 106 | 2.30x | 9.9% | 60.0% | 56.8% |

| Remaining Term to Maturity in Months | |||||||||

| Weighted Average | |||||||||||

| Range of Remaining Term to Maturity in Months | Number of Loans | Cut-off Date Principal Balance | % of IPB | Mortgage Rate | Remaining Loan Term | UW NCF DSCR(1) | UW NOI DY(1)(2) | Cut-off Date LTV(1)(3) | Maturity Date LTV(1)(3) | ||

| 57 | - | 84 | 8 | $319,727,000 | 24.2% | 3.74873% | 64 | 2.72x | 10.7% | 48.3% | 46.7% |

| 85 | - | 119 | 23 | 500,634,369 | 37.9 | 3.76333% | 118 | 2.23x | 9.6% | 61.4% | 58.6% |

| 120 | - | 120 | 22 | 501,888,000 | 38.0 | 3.84568% | 120 | 2.11x | 9.7% | 66.2% | 61.4% |

| Total / Wtd. Avg: | 53 | $1,322,249,369 | 100.0% | 3.79106% | 106 | 2.30x | 9.9% | 60.0% | 56.8% | ||

| (1) | In the case of Loan Nos. 2, 3, 4, 5, 6, 7, 9, 10, 11, 12, 19, 20, 23, 28, 29 and 30, the UW NCF DSCR, UW NOI DY, Cut-off Date LTV and Maturity Date LTV calculations include the relatedPari Passu Companion Loan(s). In the case of Loan Nos. 2, 4, 5, 9, 19 and 21, the UW NCF DSCR, UW NOI DY, Cut-off Date LTV and Maturity Date LTV calculations exclude the related Subordinate Companion Loan(s) and/or mezzanine loan(s). |

| (2) | In the case of Loan Nos. 36 and 49, the UW NOI DY are calculated net of a holdback reserve. |

| (3) | In the case of Loan Nos. 3, 7, 11, 12, 20, 21, 24, 29, 32, 35, 39, 41 and 50, the Cut-off Date LTV and the Maturity Date LTV are calculated by using an appraised value based on certain hypothetical assumptions. Refer to “Description of the Mortgage Pool—Assessments of Property Value and Condition” and “—Appraised Value” in the Preliminary Prospectus for additional details. |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

| | |

14 of 156

| Structural and Collateral Term Sheet | Benchmark 2019-B14 | |

| Collateral Characteristics | ||

| Original Amortization Term in Months |

| Weighted Average | |||||||||||

| Original Amortization Term in Months | Number of Loans | Cut-off Date Principal Balance | % of IPB | Mortgage Rate | Remaining Loan Term | UW NCF DSCR(1) | UW NOI DY(1)(2) | Cut-off Date LTV(1)(3) | Maturity Date LTV(1)(3) | ||

| Interest Only | 28 | $829,955,115 | 62.8% | 3.57053% | 105 | 2.77x | 10.2% | 55.7% | 55.7% | ||

| 120 | - | 324 | 2 | 26,500,000 | 2.0 | 3.90811% | 120 | 1.44x | 12.1% | 56.9% | 32.5% |

| 360 | - | 480 | 23 | 465,794,253 | 35.2 | 4.17733% | 107 | 1.53x | 9.3% | 67.9% | 60.2% |

| Total / Wtd. Avg: | 53 | $1,322,249,369 | 100.0% | 3.79106% | 106 | 2.30x | 9.9% | 60.0% | 56.8% | ||

| Remaining Amortization Term in Months |

| Weighted Average | |||||||||||

| Range of Remaining Amortization Term in Months | Number of Loans | Cut-off Date Principal Balance | % of IPB | Mortgage Rate | Remaining Loan Term | UW NCF DSCR(1) | UW NOI DY(1)(2) | Cut-off Date LTV(1)(3) | Maturity Date LTV(1)(3) | ||

Interest Only | 28 | $829,955,115 | 62.8% | 3.57053% | 105 | 2.77x | 10.2% | 55.7% | 55.7% | ||

| 120 | - | 359 | 4 | 47,818,753 | 3.6 | 3.97705% | 119 | 1.52x | 11.2% | 63.3% | 43.3% |

| 360 | - | 480 | 21 | 444,475,500 | 33.6 | 4.18283% | 106 | 1.52x | 9.2% | 67.8% | 60.4% |

| Total / Wtd. Avg: | 53 | $1,322,249,369 | 100.0% | 3.79106% | 106 | 2.30x | 9.9% | 60.0% | 56.8% | ||

| Amortization Types |

Weighted Average | |||||||||

| Amortization Types | Number of Loans | Cut-off Date Principal Balance | % of IPB | Mortgage Rate | Remaining Loan Term | UW NCF DSCR(1) | UW NOI DY(1)(2) | Cut-off Date LTV(1)(3) | Maturity Date LTV(1)(3) |

| Interest Only | 28 | $829,955,115 | 62.8% | 3.57053% | 105 | 2.77x | 10.2% | 55.7% | 55.7% |

| IO-Balloon | 16 | 287,975,500 | 21.8 | 4.15819% | 120 | 1.48x | 9.1% | 70.7% | 63.1% |

| Balloon | 8 | 196,318,753 | 14.8 | 4.17835% | 90 | 1.59x | 9.6% | 63.6% | 54.6% |

| Fully Amortizing | 1 | 8,000,000 | 0.6 | 3.95000% | 120 | 1.46x | 18.7% | 38.8% | 0.2% |

| Total / Wtd. Avg: | 53 | $1,322,249,369 | 100.0% | 3.79106% | 106 | 2.30x | 9.9% | 60.0% | 56.8% |

| Underwritten Net Cash Flow Debt Service Coverage Ratios(1) |

| Weighted Average | |||||||||||

| Range of Underwritten Net Cash Flow Debt Service Coverage Ratios | Number of Loans | Cut-off Date Principal Balance | % of IPB | Mortgage Rate | Remaining Loan Term | UW NCF DSCR(1) | UW NOI DY(1)(2) | Cut-off Date LTV(1)(3) | Maturity Date | ||

| 1.06x | - | 1.49x | 8 | $158,310,000 | 12.0% | 4.28087% | 120 | 1.22x | 7.7% | 71.6% | 61.9% |

| 1.50x | - | 1.74x | 15 | 295,781,253 | 22.4 | 4.16949% | 100 | 1.59x | 9.1% | 65.1% | 59.0% |

| 1.75x | - | 1.99x | 8 | 171,153,000 | 12.9 | 4.02942% | 105 | 1.87x | 9.9% | 66.7% | 61.7% |

| 2.00x | - | 2.24x | 2 | 103,000,000 | 7.8 | 3.98291% | 119 | 2.04x | 8.6% | 64.6% | 64.6% |

| 2.25x | - | 4.59x | 20 | 594,005,115 | 44.9 | 3.37014% | 103 | 3.12x | 11.1% | 51.7% | 51.6% |

| Total / Wtd. Avg: | 53 | $1,322,249,369 | 100.0% | 3.79106% | 106 | 2.30x | 9.9% | 60.0% | 56.8% | ||

| (1) | In the case of Loan Nos. 2, 3, 4, 5, 6, 7, 9, 10, 11, 12, 19, 20, 23, 28, 29 and 30, the UW NCF DSCR, UW NOI DY, Cut-off Date LTV and Maturity Date LTV calculations include the relatedPari Passu Companion Loan(s). In the case of Loan Nos. 2, 4, 5, 9, 19 and 21, the UW NCF DSCR, UW NOI DY, Cut-off Date LTV and Maturity Date LTV calculations exclude the related Subordinate Companion Loan(s) and/or mezzanine loan(s). |

| (2) | In the case of Loan Nos. 36 and 49, the UW NOI DY are calculated net of a holdback reserve. |

| (3) | In the case of Loan Nos. 3, 7, 11, 12, 20, 21, 24, 29, 32, 35, 39, 41 and 50, the Cut-off Date LTV and the Maturity Date LTV are calculated by using an appraised value based on certain hypothetical assumptions. Refer to “Description of the Mortgage Pool—Assessments of Property Value and Condition” and “—Appraised Value” in the Preliminary Prospectus for additional details. |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

| | |

15 of 156

| Structural and Collateral Term Sheet | Benchmark 2019-B14 | |

| Collateral Characteristics | ||

| LTV Ratios as of the Cut-off Date(1)(3) |

| Weighted Average | |||||||||||

| Range of Cut-off Date LTVs | Number of Loans | Cut-off Date Principal Balance | % of IPB | Mortgage Rate | Remaining Loan Term | UW NCF DSCR(1) | UW NOI DY(1)(2) | Cut-off Date LTV(1)(3) | Maturity Date LTV(1)(3) | ||

| 30.5% | - | 39.9% | 5 | $214,900,000 | 16.3% | 3.29998% | 79 | 3.41x | 12.1% | 35.7% | 34.2% |

| 40.0% | - | 49.9% | 2 | 33,884,615 | 2.6 | 3.73555% | 116 | 2.55x | 9.9% | 46.2% | 46.2% |

| 50.0% | - | 59.9% | 9 | 198,900,000 | 15.0 | 3.76401% | 101 | 2.45x | 10.5% | 53.3% | 51.6% |

| 60.0% | - | 69.9% | 28 | 690,535,843 | 52.2 | 3.83582% | 112 | 2.16x | 9.7% | 66.4% | 63.2% |

| 70.0% | - | 78.6% | 9 | 184,028,910 | 13.9 | 4.23603% | 119 | 1.36x | 7.6% | 74.2% | 66.9% |

Total / Wtd. Avg: | 53 | $1,322,249,369 | 100.0% | 3.79106% | 106 | 2.30x | 9.9% | 60.0% | 56.8% | ||

| LTV Ratios as of the Maturity Date(1)(3) |

Weighted Average | |||||||||||

| Range of Maturity Date LTVs | Number of Loans | Cut-off Date Principal Balance | % of IPB | Mortgage Rate | Remaining Loan Term | UW NCF DSCR(1) | UW NOI DY(1)(2) | Cut-off Date LTV(1)(3) | Maturity Date LTV(1)(3) | ||

| 0.2% | - | 39.9% | 5 | $214,900,000 | 16.3% | 3.29998% | 79 | 3.41x | 12.1% | 35.7% | 34.2% |

| 40.0% | - | 49.9% | 4 | 102,384,615 | 7.7 | 3.82423% | 89 | 1.92x | 9.6% | 53.0% | 47.2% |

| 50.0% | - | 54.9% | 10 | 177,824,843 | 13.4 | 3.81290% | 115 | 2.48x | 11.0% | 55.4% | 52.0% |

| 55.0% | - | 59.9% | 7 | 111,046,910 | 8.4 | 3.84976% | 119 | 1.86x | 10.6% | 65.9% | 57.4% |

| 60.0% | - | 72.0% | 27 | 716,093,000 | 54.2 | 3.91917% | 112 | 2.05x | 8.9% | 68.6% | 66.0% |

Total / Wtd. Avg: | 53 | $1,322,249,369 | 100.0% | 3.79106% | 106 | 2.30x | 9.9% | 60.0% | 56.8% | ||

| Prepayment Protection |

Weighted Average | |||||||||

| Prepayment Protection | Number of Loans | Cut-off Date Principal Balance | % of IPB | Mortgage Rate | Remaining Loan Term | UW NCF DSCR(1) | UW NOI DY(1)(2) | Cut-off Date LTV(1)(3) | Maturity Date LTV(1)(3) |

Defeasance | 41 | $979,084,025 | 74.0% | 3.77113% | 104 | 2.27x | 9.7% | 60.1% | 56.5% |

Yield Maintenance | 10 | 263,165,343 | 19.9 | 3.91910% | 110 | 2.55x | 10.9% | 58.9% | 57.5% |

| Defeasance or Yield Maintenance | 2 | 80,000,000 | 6.1 | 3.61375% | 119 | 1.94x | 9.0% | 62.5% | 58.4% |

Total / Wtd. Avg: | 53 | $1,322,249,369 | 100.0% | 3.79106% | 106 | 2.30x | 9.9% | 60.0% | 56.8% |

| Loan Purpose |

Weighted Average | |||||||||

| Loan Purpose | Number of Loans | Cut-off Date Principal Balance | % of IPB | Mortgage Rate | Remaining Loan Term | UW NCF DSCR(1) | UW NOI DY(1)(2) | Cut-off Date LTV(1)(3) | Maturity Date LTV(1)(3) |

| Refinance | 30 | $709,971,459 | 53.7% | 3.87617% | 99 | 2.26x | 9.7% | 56.3% | 52.6% |

| Acquisition | 21 | 561,707,910 | 42.5 | 3.71935% | 113 | 2.31x | 10.1% | 65.3% | 62.4% |

| Recapitalization | 2 | 50,570,000 | 3.8 | 3.39271% | 119 | 2.90x | 10.5% | 54.2% | 54.2% |

| Total / Wtd. Avg: | 53 | $1,322,249,369 | 100.0% | 3.79106% | 106 | 2.30x | 9.9% | 60.0% | 56.8% |

| (1) | In the case of Loan Nos. 2, 3, 4, 5, 6, 7, 9, 10, 11, 12, 19, 20, 23, 28, 29 and 30, the UW NCF DSCR, UW NOI DY, Cut-off Date LTV and Maturity Date LTV calculations include the relatedPari Passu Companion Loan(s). In the case of Loan Nos. 2, 4, 5, 9, 19 and 21, the UW NCF DSCR, UW NOI DY, Cut-off Date LTV and Maturity Date LTV calculations exclude the related Subordinate Companion Loan(s) and/or mezzanine loan(s). |

| (2) | In the case of Loan Nos. 36 and 49, the UW NOI DY are calculated net of a holdback reserve. |

| (3) | In the case of Loan Nos. 3, 7, 11, 12, 20, 21, 24, 29, 32, 35, 39, 41 and 50, the Cut-off Date LTV and the Maturity Date LTV are calculated by using an appraised value based on certain hypothetical assumptions. Refer to “Description of the Mortgage Pool—Assessments of Property Value and Condition” and “—Appraised Value” in the Preliminary Prospectus for additional details. |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

| | |

16 of 156

| Structural and Collateral Term Sheet | Benchmark 2019-B14 | |

| Collateral Characteristics | ||

| Previous Securitization History(1) |

| No. | Mortgaged Property | Cut-off Date Principal Balance | % of IPB | Location | Property Type | Previous Securitization |

| 2 | 225 Bush | $60,000,000 | 4.5% | San Francisco, CA | Office | GSMS 2017-GS5 |

| 6 | Harvey Building Products | $50,000,000 | 3.8% | Various | Various | COMM 2015-LC23 |

| 15.01 | Compass Self Storage Bloomfield | $13,000,000 | 1.0% | Bloomfield, NJ | Self Storage | CGCMT 2013-GC11 |

| 15.02 | Compass Self Storage Smyrna | $4,668,040 | 0.4% | Smyrna, GA | Self Storage | CGCMT 2013-GC11 |

| 15.03 | Compass Self Storage Port Richey | $4,206,680 | 0.3% | New Port Richey, FL | Self Storage | GSMS 2013-GC16 |

| 15.05 | Compass Self Storage Duluth | $3,676,480 | 0.3% | Duluth, GA | Self Storage | CGCMT 2013-GC11 |

| 15.06 | Compass Self Storage Kennesaw | $3,534,600 | 0.3% | Kennesaw, GA | Self Storage | CGCMT 2013-GC11 |

| 17 | Jersey City Group 1 | $32,050,000 | 2.4% | Jersey City, NJ | Multifamily | TRTX 2018-FL1 |

| 18 | Jersey City Group 3 | $31,110,000 | 2.4% | Jersey City, NJ | Multifamily | TRTX 2018-FL1 |

| 19 | Grand Canal Shoppes | $30,384,615 | 2.3% | Las Vegas, NV | Retail | GSMS 2012-SHOP |

| 24 | Florham Park Corporate Center | $25,000,000 | 1.9% | Florham Park, NJ | Office | RSO 2015-CRE4 |

| 25 | Sparks Galleria | $23,523,500 | 1.8% | Sparks, NV | Retail | Prime 2014-1 |