JP Morgan Chase Commercial Mortgage Securities

Filed: 15 Jun 20, 4:58pm

| FREE WRITING PROSPECTUS | ||

| FILED PURSUANT TO RULE 433 | ||

| REGISTRATION FILE NO.: 333-226123-09 | ||

June [15], 2020 | JPMDB 2020-COR7 |

Collateral Term Sheet |

JPMDB 2020-COR7

This material is for your information, and none of J.P. Morgan Securities LLC (“JPMS”), Deutsche Bank Securities Inc., Goldman Sachs & Co. LLC, Jefferies LLC and Drexel Hamilton, LLC, (each individually, an “Underwriter”, and together, the ‘‘Underwriters’’) are soliciting any action based upon it. This material is not to be construed as an offer to sell or the solicitation of any offer to buy any security in any jurisdiction where such an offer or solicitation would be illegal.

The depositor has filed a registration statement (including a prospectus) with the SEC (SEC File No. 333-226123) for the offering to which this free writing prospectus relates. Before you invest, you should read the prospectus in the registration statement and other documents the depositor has filed with the SEC for more complete information about the depositor, the issuing entity and this offering. You may get these documents for free by visiting EDGAR on the SEC Web site at www.sec.gov. Alternatively, the depositor, any underwriter or any dealer participating in the offering will arrange to send you the prospectus if you request it by calling (800) 408-1016 or by emailing the ABS Syndicate Desk atabs_synd@jpmorgan.com.

THE SECURITIES TO WHICH THIS INFORMATION RELATES WILL BE MORE FULLY DESCRIBED IN A PROSPECTUS (THE “PROSPECTUS”), WHICH IS NOT YET AVAILABLE. THE PROSPECTUS WILL CONTAIN MATERIAL INFORMATION THAT IS NOT CONTAINED IN THESE MATERIALS (INCLUDING WITHOUT LIMITATION A DETAILED DISCUSSION OF RISKS ASSOCIATED WITH AN INVESTMENT IN THE CERTIFICATES, UNDER THE HEADING“RISK FACTORS”IN THE PROSPECTUS).

Neither this document nor anything contained in this document shall form the basis for any contract or commitment whatsoever. The information contained in this document is preliminary as of the date of this document, supersedes any previous such information delivered to you and will be superseded by any such information subsequently delivered prior to the time of sale. These materials are subject to change, completion or amendment from time to time. This information is based upon management forecasts and reflects prevailing conditions and management's views as of this date, all of which are subject to change.

J.P. Morgan is the marketing name for the investment banking businesses of JPMorgan Chase & Co. and its subsidiaries worldwide. Securities, syndicated loan arranging, financial advisory and other investment banking activities are performed by JPMS and its securities affiliates, and lending, derivatives and other commercial banking activities are performed by JPMorgan Chase Bank, National Association and its banking affiliates. JPMS is a member of SIPC and the NYSE.

THE UNDERWRITERS MAY FROM TIME TO TIME PERFORM INVESTMENT BANKING SERVICES FOR, OR SOLICIT INVESTMENT BANKING BUSINESS FROM, ANY COMPANY NAMED IN THESE MATERIALS. THE UNDERWRITERS AND/OR THEIR AFFILIATES OR RESPECTIVE EMPLOYEES MAY FROM TIME TO TIME HAVE A LONG OR SHORT POSITION IN ANY CERTIFICATE OR CONTRACT DISCUSSED IN THESE MATERIALS.

|

| THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED. |

| June [15], 2020 | JPMDB 2020-COR7 |

THE REPUBLIC OF KOREA

THIS PROSPECTUS IS NOT, AND UNDER NO CIRCUMSTANCES IS THIS PROSPECTUS TO BE CONSTRUED AS, A PUBLIC OFFERING OF SECURITIES IN KOREA. NEITHER THE ISSUER NOR ANY OF ITS AGENTS MAKE ANY REPRESENTATION WITH RESPECT TO THE ELIGIBILITY OF ANY RECIPIENTS OF THIS PROSPECTUS TO ACQUIRE THE OFFERED CERTIFICATES UNDER THE LAWS OF KOREA, INCLUDING, BUT WITHOUT LIMITATION, THE FOREIGN EXCHANGE TRANSACTION LAW AND REGULATIONS THEREUNDER (THE “FETL”). THE OFFERED CERTIFICATES HAVE NOT BEEN REGISTERED WITH THE FINANCIAL SERVICES COMMISSION OF KOREA FOR PUBLIC OFFERING IN KOREA, AND NONE OF THE OFFERED CERTIFICATES MAY BE OFFERED, SOLD OR DELIVERED, DIRECTLY OR INDIRECTLY, OR OFFERED OR SOLD TO ANY PERSON FOR RE-OFFERING OR RESALE, DIRECTLY OR INDIRECTLY IN KOREA OR TO ANY RESIDENT OF KOREA EXCEPT PURSUANT TO THE FINANCIAL INVESTMENT SERVICES AND CAPITAL MARKETS ACT AND THE DECREES AND REGULATIONS THEREUNDER (THE “FSCMA”), THE FETL AND ANY OTHER APPLICABLE LAWS, REGULATIONS AND MINISTERIAL GUIDELINES IN KOREA. WITHOUT PREJUDICE TO THE FOREGOING, THE NUMBER OF OFFERED CERTIFICATES OFFERED IN KOREA OR TO A RESIDENT OF KOREA SHALL BE LESS THAN FIFTY AND FOR A PERIOD OF ONE YEAR FROM THE ISSUE DATE OF THE OFFERED CERTIFICATES, NONE OF THE OFFERED CERTIFICATES MAY BE DIVIDED RESULTING IN AN INCREASED NUMBER OF OFFERED CERTIFICATES. FURTHERMORE, THE OFFERED CERTIFICATES MAY NOT BE RESOLD TO KOREAN RESIDENTS UNLESS THE PURCHASER OF THE OFFERED CERTIFICATES COMPLIES WITH ALL APPLICABLE REGULATORY REQUIREMENTS (INCLUDING, BUT NOT LIMITED TO, GOVERNMENT REPORTING APPROVAL REQUIREMENTS UNDER THE FETL AND ITS SUBORDINATE DECREES AND REGULATIONS) IN CONNECTION WITH THE PURCHASE OF THE OFFERED CERTIFICATES.

JAPAN

THE OFFERED CERTIFICATES HAVE NOT BEEN AND WILL NOT BE REGISTERED UNDER THE FINANCIAL INSTRUMENTS AND EXCHANGE LAW OF JAPAN, AS AMENDED (THE “FIEL”), AND DISCLOSURE UNDER THE FIEL HAS NOT BEEN AND WILL NOT BE MADE WITH RESPECT TO THE OFFERED CERTIFICATES. ACCORDINGLY, EACH UNDERWRITER HAS REPRESENTED AND AGREED THAT IT HAS NOT, DIRECTLY OR INDIRECTLY, OFFERED OR SOLD AND WILL NOT, DIRECTLY OR INDIRECTLY, OFFER OR SELL ANY OFFERED CERTIFICATES IN JAPAN OR TO, OR FOR THE BENEFIT OF, ANY RESIDENT OF JAPAN (WHICH TERM AS USED IN THIS PROSPECTUS MEANS ANY PERSON RESIDENT IN JAPAN, INCLUDING ANY CORPORATION OR OTHER ENTITY ORGANIZED UNDER THE LAWS OF JAPAN) OR TO OTHERS FOR REOFFERING OR RE-SALE, DIRECTLY OR INDIRECTLY, IN JAPAN OR TO, OR FOR THE BENEFIT OF, ANY RESIDENT OF JAPAN EXCEPT PURSUANT TO AN EXEMPTION FROM THE REGISTRATION REQUIREMENTS OF, AND OTHERWISE IN COMPLIANCE WITH, THE FIEL AND OTHER RELEVANT LAWS, REGULATIONS AND MINISTERIAL GUIDELINES OF JAPAN. AS PART OF THIS OFFERING OF THE OFFERED CERTIFICATES, THE UNDERWRITERS MAY OFFER THE OFFERED CERTIFICATES IN JAPAN TO UP TO 49 OFFEREES IN ACCORDANCE WITH THE ABOVE PROVISIONS.

| THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED. | ||

|

2 of 130 |  |

| Structural and Collateral Term Sheet | JPMDB 2020-COR7 | |

| Collateral Characteristics | ||

| Loan Pool | ||

| Initial Pool Balance (“IPB”): | $909,405,614 | |

| Number of Mortgage Loans: | 37 | |

| Number of Mortgaged Properties: | 153 | |

| Average Cut-off Date Balance per Mortgage Loan: | $24,578,530 | |

| Weighted Average Current Mortgage Rate: | 3.66595% | |

| 10 Largest Mortgage Loans as % of IPB: | 54.3% | |

| Weighted Average Remaining Term to Maturity: | 106 months | |

| Weighted Average Seasoning: | 5 months | |

| Credit Statistics(1)(2)(3) | ||

| Weighted Average UW NCF DSCR(4): | 2.50x | |

| Weighted Average UW NOI Debt Yield: | 10.4% | |

| Weighted Average Cut-off Date Loan-to-Value Ratio (“LTV”)(5): | 55.7% | |

| Weighted Average Maturity Date LTV(5): | 52.5% | |

| Other Statistics | ||

| % of Mortgage Loans with Additional Debt: | 28.5% | |

| % of Mortgaged Properties with Single Tenants: | 31.6% | |

| Amortization | ||

| Weighted Average Original Amortization Term(6): | 360 months | |

| Weighted Average Remaining Amortization Term(6): | 357 Months | |

| % of Mortgage Loans with Interest-Only: | 66.6% | |

| % of Mortgage Loans with Partial Interest-Only followed by Amortizing Balloon: | 23.4% | |

| % of Mortgage Loans with Amortizing Balloon: | 10.0% | |

| Lockbox / Cash Management(7) | ||

| % of Mortgage Loans with In-Place, Hard Lockboxes: | 89.7% | |

| % of Mortgage Loans with In-Place, Soft Lockboxes: | 6.3% | |

| % of Mortgage Loans with Springing Lockboxes: | 4.0% | |

| % of Mortgage Loans with In-Place Cash Management: | 88.2% | |

| % of Mortgage Loans with Springing Cash Management: | 11.8% | |

| Reserves | ||

| % of Mortgage Loans Requiring Monthly Tax Reserves: | 56.0% | |

| % of Mortgage Loans Requiring Monthly Insurance Reserves: | 32.5% | |

| % of Mortgage Loans Requiring Monthly CapEx Reserves: | 53.4% | |

| % of Mortgage Loans Requiring Monthly TI/LC Reserves(8): | 31.6% | |

| (1) | In the case of Loan Nos. 1, 3, 4, 5, 6, 7, 8, 9, 10, 14, 17, 18, 21, 23, 26, 27, 28 and 33, the UW NCF DSCR, UW NOI Debt Yield, Cut-off Date LTV and Maturity Date LTV calculations include the related Pari Passu Companion Loan(s). In the case of Loan Nos. 3, 4, 5, 8, 10, 13 and 18, the UW NCF DSCR, UW NOI Debt Yield, Cut-off Date LTV and Maturity Date LTV calculations exclude the related Subordinate Companion Loan(s) and/or related mezzanine loan(s). |

| (2) | In the case of Loan No. 10, the BX Industrial Portfolio mortgage loan is part of a whole loan with an aggregate principal balance as of the Cut-off Date of approximately $649.428 million that is split between (i) a 17-month floating rate loan with five, one-year extension options (the “BX Industrial Portfolio Floating Rate Loan”) with an aggregate Cut-off Date principal balance of approximately $99.428 million, and (ii) a 77-month fixed rate loan (the “BX Industrial Portfolio Fixed Rate Loan”) with an aggregate Cut-off Date principal balance of $550.0 million that is comprised of comprised of (A) a senior fixed rate loan (the “BX Industrial Portfolio Senior Fixed Rate Loan”), with an aggregate Cut-off Date principal balance of $322.4 million and (B) a subordinate fixed rate loan (the “BX Industrial Portfolio Subordinate Fixed Rate Loan”), with an aggregate Cut-off Date principal balance of $227.6 million. The BX Industrial Portfolio Senior Fixed Rate Loan is senior to the BX Industrial Portfolio Subordinate Fixed Rate Loan and the BX Industrial Portfolio mortgage loan is comprised of a portion of the BX Industrial Portfolio Senior Fixed Rate Loan. The interest rate on the BX Industrial Portfolio Floating Rate Loan is LIBOR (subject to a floor of 0.000%) plus a spread of 1.450%. The BX Industrial Portfolio Fixed Rate Loan and the BX Industrial Portfolio Floating Rate Loan arepari passu,provided that voluntary prepayments are applied first to the BX Industrial Portfolio Floating Rate Loan until paid in full, and then to the BX Industrial Portfolio Fixed Rate Loan. The financial information presented in the Collateral Characteristics section above reflects the BX Industrial Portfolio Senior Fixed Rate Loan and approximately $58.283 million of the Cut-off Date principal balance of the BX Industrial Portfolio Floating Rate Loan, and excludes the remaining approximately $41.145 million of the Cut-off Date principal balance of the BX Industrial Portfolio Floating Rate Loan and the BX Industrial Portfolio Subordinate Fixed Rate Loan. For purposes of all calculations herein, LIBOR is assumed to be 0.500%. |

| (3) | In the case of Loan Nos. 3 and 4, Chase Center Tower I and the Chase Center Tower II, respectively (collectively, the “Chase Center Tower Mortgage Loans”), the mortgage loans are cross-collateralized and cross-defaulted. As such, all calculations herein are based on the aggregate Cut-off Date Balance, Maturity or ARD Balance, U/W NOI, U/W NCF and Debt Services of the Chase Center Tower Mortgage Loans. |

| (4) | With respect to Loan No. 8, the UW NCF DSCR is calculated using the sum of the first 12 whole loan principal and interest payments after the Cut-off Date based on the assumed principal and interest payment schedule set forth in Annex I of the Preliminary Prospectus. |

| (5) | In the case of Loan Nos. 3, 4, 7 and 18, the Cut-off Date LTV and the Maturity Date LTV are calculated by using an appraised value based on certain hypothetical assumptions. Refer to“Description of the Mortgage Pool—Assessments of Property Value and Condition” and“—Appraised Value” in the Preliminary Prospectus for additional details. |

| (6) | Excludes 21 mortgage loans that are interest-only for the entire term. |

| (7) | For a more detailed description of Lockbox / Cash Management, refer to“Description of the Mortgage Pool—Certain Terms of the Mortgage Loans—Mortgaged Property Accounts” in the Preliminary Prospectus. |

| (8) | Calculated only with respect to the Cut-off Date Balance of mortgage loans secured or partially secured by retail, office, industrial and mixed use properties. |

| THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED. | ||

| |

3 of 130 | |

| Structural and Collateral Term Sheet | JPMDB 2020-COR7 | |

| Collateral Characteristics | ||

Mortgage Loan Seller | Number of | Number of | Aggregate | % of IPB |

| LCM | 16 | 52 | $442,192,626 | 48.6% |

| JPMCB | 7 | 7 | 159,900,000 | 17.6 |

| GACC(1) | 6 | 75 | 129,387,500 | 14.2 |

| GSMC(2) | 7 | 18 | 120,425,488 | 13.2 |

| JPMCB/GACC/GSMC(1)(3) | 1 | 1 | 57,500,000 | 6.3 |

| Total | 37 | 153 | $909,405,614 | 100.0% |

| (1) | Seven of the mortgage loans (16.4%), or the applicable portion thereof, being sold by GACC were originated or co-originated by an affiliate thereof, DBRI or DBNY, and will be transferred to GACC on or prior to the closing date. |

| (2) | In the case of Loan No. 9, the whole loan was co-originated by Goldman Sachs Bank USA and Bank of America, N.A. In the case of Loan No. 17, the whole loan was co-originated by Goldman Sachs Bank USA and Morgan Stanley Bank, N.A. In the case of Loan No. 18, the whole loan was co-originated by Goldman Sachs Bank USA, DBR Investments Co. Limited (“DBRI”) and JPMCB. |

| (3) | In the case of Loan No. 5, the whole loan was co-originated by Goldman Sachs Bank USA, JPMCB, DBRI and Wells Fargo Bank, National Association.JPMCB will be contributing $27.5 million of the Cut-off Date Balance, GACC will be contributing $20.0 million of the Cut-Off Date Balance and GSMC will be contributing $10.0 million of the Cut-Off Date Balance. |

| Ten Largest Mortgage Loans | |||||||||||

| No. | Loan Name | Mortgage Loan Seller | No. of Prop. | Cut-off Date Balance | % of IPB | SF / Units/ Rooms / Beds | Property Type | UW NCF DSCR(1)(2)(3)(4) | UW NOI Debt Yield(1)(3) (4) | Cut-off Date LTV(1) (3)(4)(5) | Maturity Date LTV(1)(3)(4)(5) |

| 1 | 530 Broadway | LCM | 1 | $80,000,000 | 8.8% | 1,060 | Mixed Use | 2.73x | 8.4% | 53.2% | 53.2% |

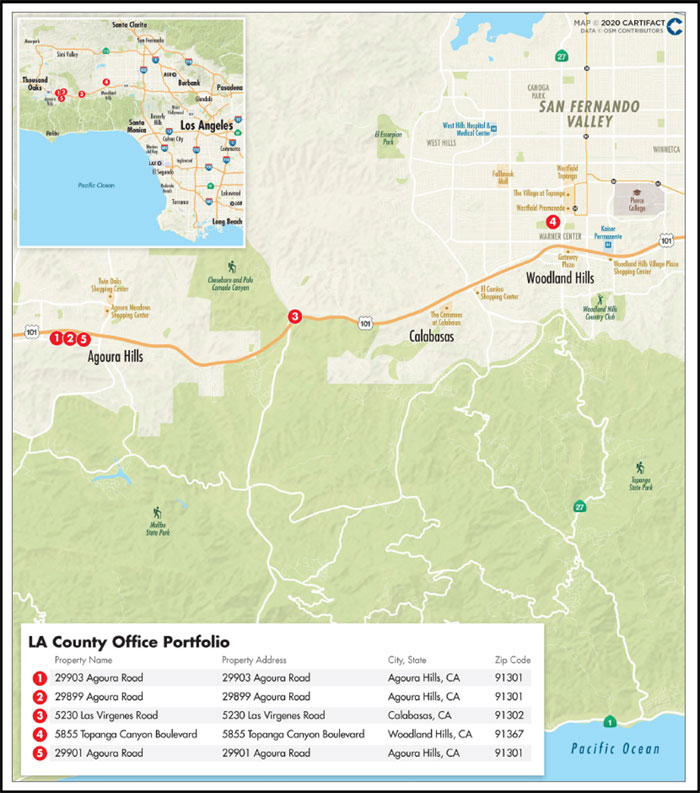

| 2 | LA County Office Portfolio | LCM | 5 | $69,000,000 | 7.6% | 199 | Office | 1.38x | 9.2% | 67.9% | 60.5% |

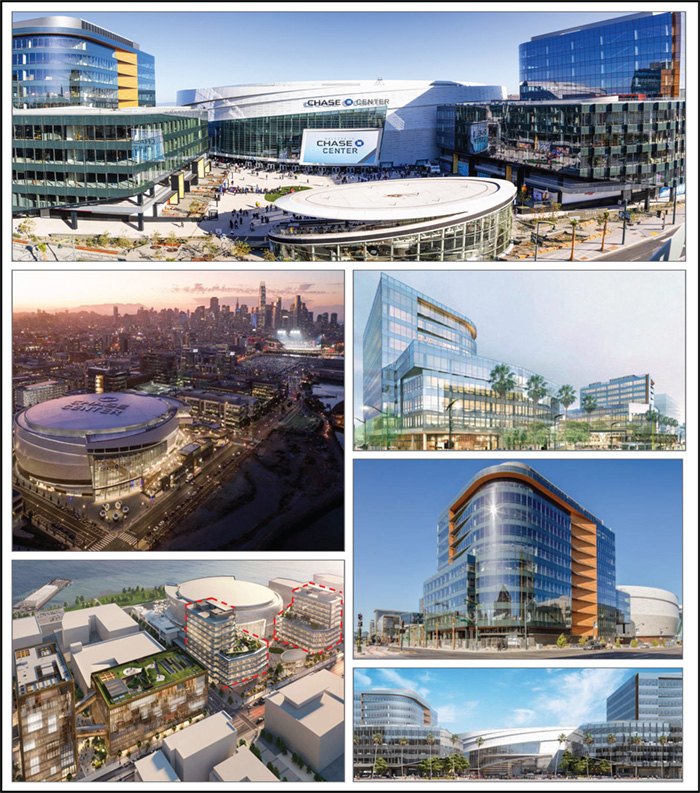

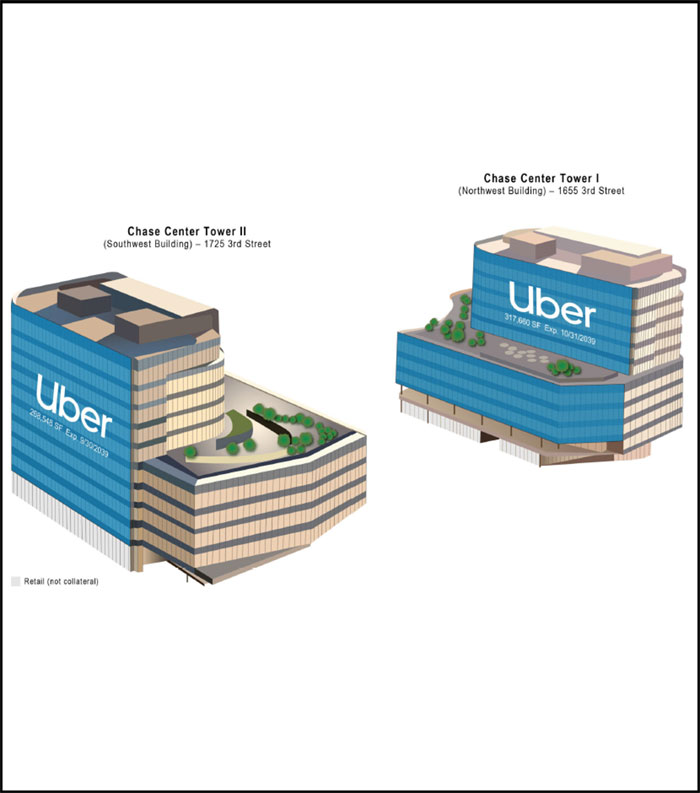

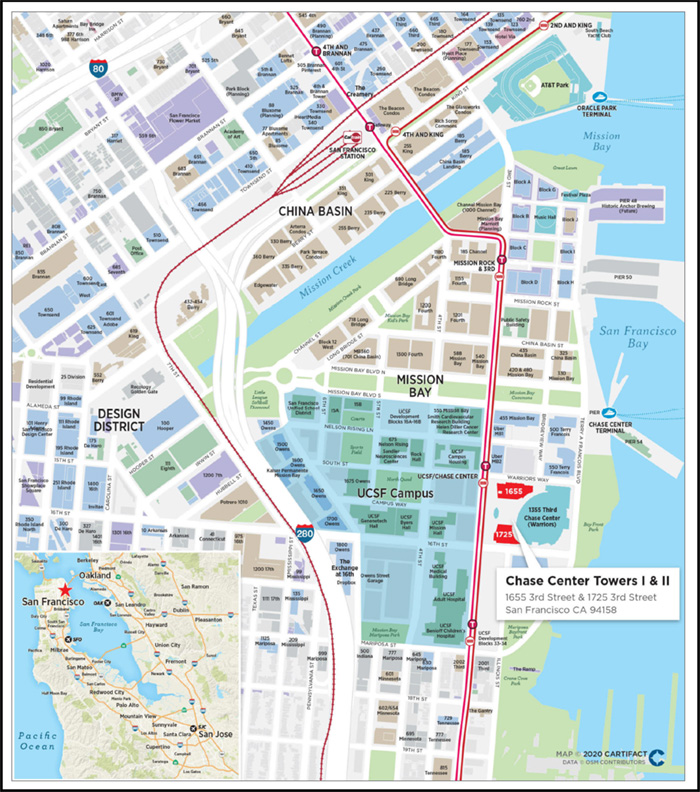

| 3 | Chase Center Tower I | JPMCB | 1 | $36,427,500 | 4.0% | 461 | Office | 3.87x | 13.9% | 31.3% | 31.3% |

| 4 | Chase Center Tower II | JPMCB | 1 | $31,072,500 | 3.4% | 461 | Office | 3.87x | 13.9% | 31.3% | 31.3% |

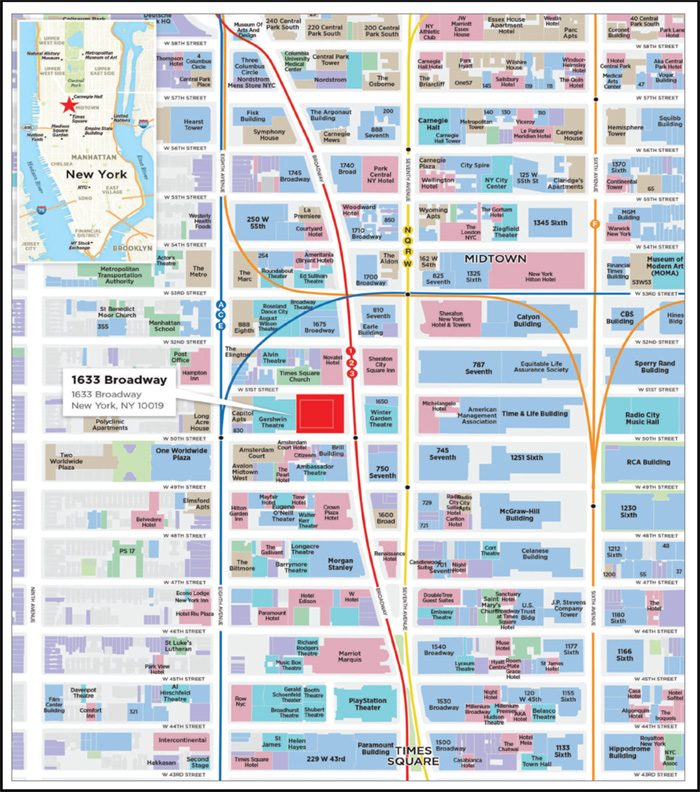

| 5 | 1633 Broadway | JPMCB / GACC / GSMC | 1 | $57,500,000 | 6.3% | 391 | Office | 3.84x | 11.9% | 41.7% | 41.7% |

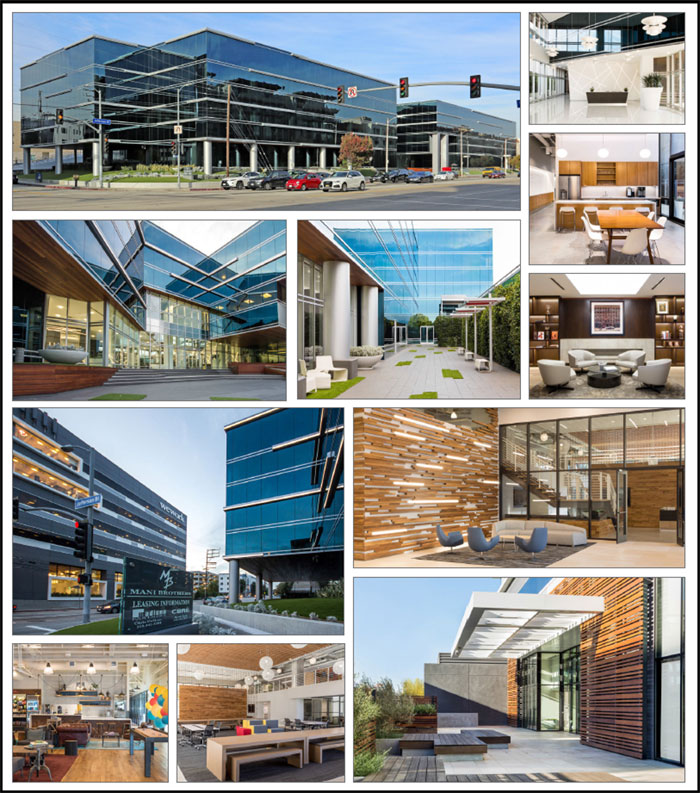

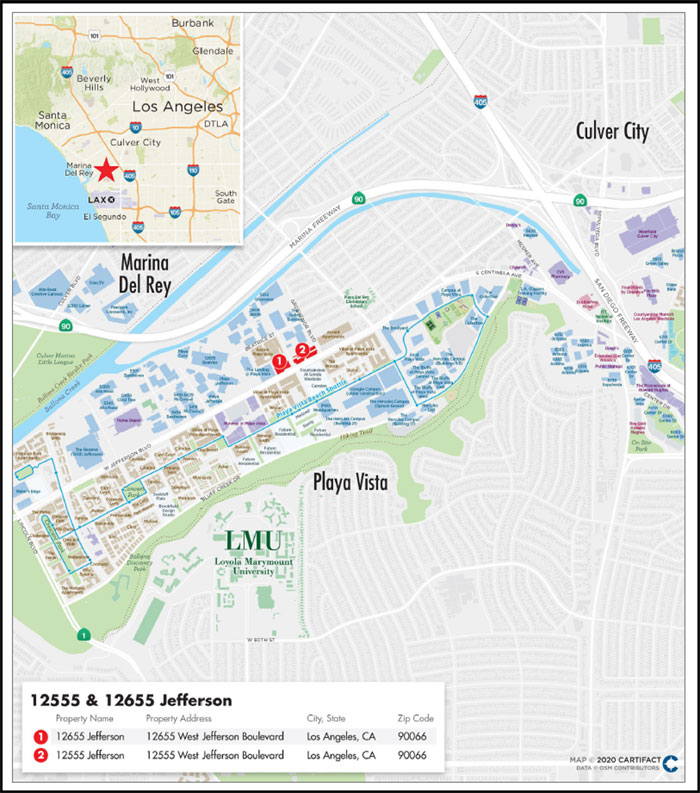

| 6 | 12555 & 12655 Jefferson | LCM | 2 | $57,000,000 | 6.3% | 572 | Office | 1.80x | 7.6% | 59.5% | 59.5% |

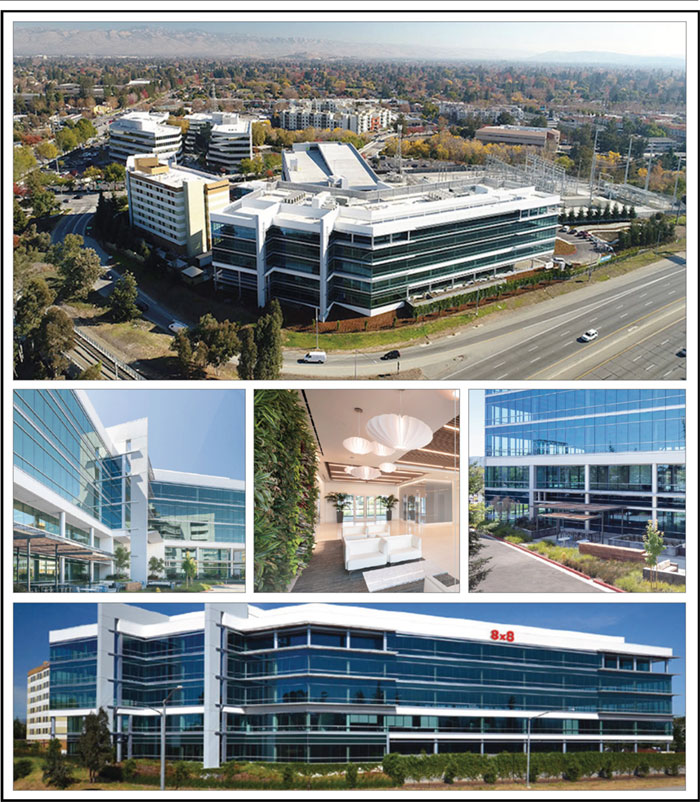

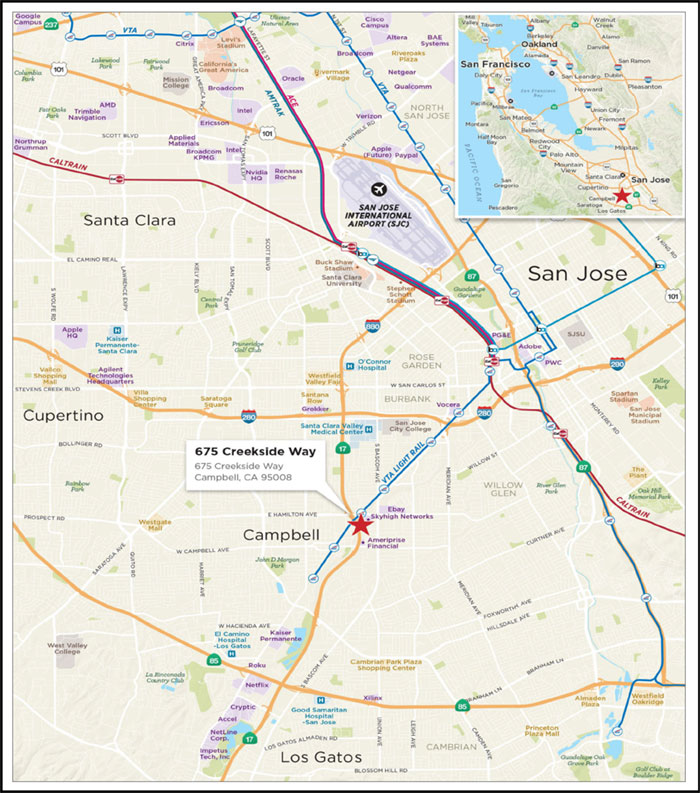

| 7 | 675 Creekside Way | GACC | 1 | $43,400,000 | 4.8% | 469 | Office | 2.52x | 9.5% | 58.3% | 58.3% |

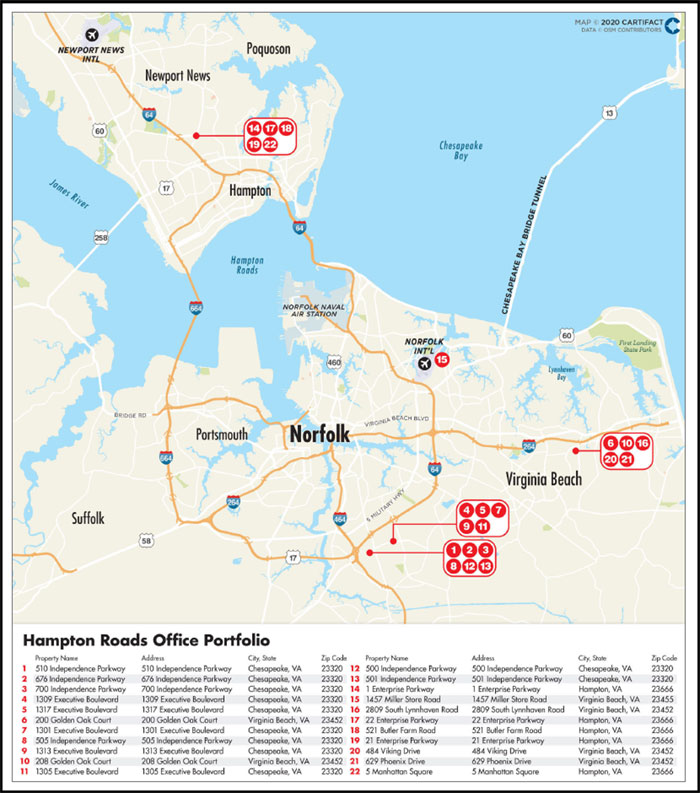

| 8 | Hampton Roads Office Portfolio | LCM | 22 | $42,387,896 | 4.7% | 99 | Office | 1.40x | 10.9% | 70.8% | 60.3% |

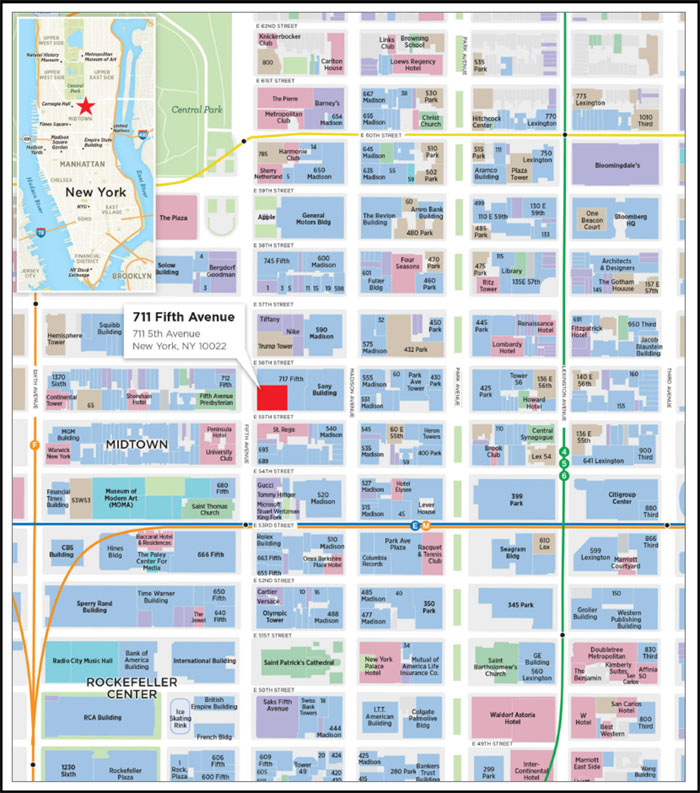

| 9 | 711 Fifth Avenue | GSMC | 1 | $40,000,000 | 4.4% | 1,603 | Mixed Use | 2.90x | 9.4% | 54.5% | 54.5% |

| 10 | BX Industrial Portfolio | GACC | 68 | $37,400,000 | 4.1% | 34 | Various | 3.57x | 12.8% | 39.6% | 39.6% |

| Top 3 Total/Weighted Average | 7 | $185,427,500 | 20.4% | 2.45x | 9.8% | 54.4% | 51.6% | ||||

| Top 5 Total/Weighted Average | 9 | $274,000,000 | 30.1% | 2.90x | 10.7% | 49.1% | 47.2% | ||||

| Top 10 Total/Weighted Average | 103 | $494,187,896 | 54.3% | 2.66x | 10.3% | 52.7% | 50.7% | ||||

| (1) | In the case of Loan Nos. 1, 3, 4, 5, 6, 7, 8, 9 and 10, the UW NCF DSCR, UW NOI Debt Yield, Cut-off Date LTV and Maturity Date LTV calculations include the related Pari Passu Companion Loan(s). In the case of Loan Nos. 3, 4, 5, 8 and 10, the UW NCF DSCR, UW NOI Debt Yield, Cut-off Date LTV and Maturity Date LTV calculations exclude the related Subordinate Companion Loan(s) and/or related mezzanine loan(s). |

| (2) | With respect to Loan No. 8, the UW NCF DSCR is calculated using the sum of the first 12 whole loan principal and interest payments after the Cut-off Date based on the assumed principal and interest payment schedule set forth in Annex I of the Preliminary Prospectus. |

| (3) | In the case of Loan No. 10, the UW NCF DSCR, UW NOI DY, Cut-off Date LTV and Maturity Date LTV calculations reflect the BX Industrial Portfolio Senior Fixed Rate Loan and approximately $58.283 million of the Cut-off Date principal balance of the BX Industrial Portfolio Floating Rate Loan, and exclude the remaining approximately $41.145 million of the Cut-off Date principal balance of the BX Industrial Portfolio Floating Rate Loan and the BX Industrial Portfolio Subordinate Fixed Rate Loan. The interest rate on the BX Industrial Portfolio Floating Rate Loan is LIBOR (subject to a floor of 0.000%) plus a spread of 1.450%. For purposes of all calculations herein regarding BX Industrial Portfolio Mortgage Loan, LIBOR is assumed to be 0.500%. |

| (4) | In the case of Loan Nos. 3 and 4, the Chase Center Tower Mortgage Loans, the mortgage loans are cross-collateralized and cross-defaulted. As such, all calculations herein are based on the aggregate Cut-off Date Balance, Maturity or ARD Balance, U/W NOI, U/W NCF and Debt Services of the Chase Center Tower Mortgage Loans. |

| (5) | In the case of Loan Nos. 3, 4 and 7, the Cut-off Date LTV and the Maturity Date LTV are calculated by using an appraised value based on certain hypothetical assumptions. Refer to “Description of the Mortgage Pool—Assessments of Property Value and Condition” and “—Appraised Value” in the Preliminary Prospectus for additional details. |

| THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED. | ||

| |

4 of 130 | |

| Structural and Collateral Term Sheet | JPMDB 2020-COR7 | |

| Collateral Characteristics | ||

| Pari Passu Companion Loan Summary |

| Loan No. | Mortgage Loan | Note(s) | Original Balance ($) | Cut-off Date Balance ($) | Holder of Note | Lead Servicer for Whole Loan (Y/N)(1) | Master Servicer Under Lead Securitization | Special Servicer Under Lead Securitization |

| 1 | 530 Broadway | A-1, A-7, A-8, A-9 | $80,000,000 | $80,000,000 | JPMDB 2020-COR7 | Yes | Midland | Midland |

| A-2, A-3, A-4, A-5, A-6 | $130,000,000 | $130,000,000 | LCM | No | ||||

| Total | $210,000,000 | $210,000,000 | ||||||

| 3 | Chase Center Tower I | A-1-A, A-1-B, A-1-C | $54,641,250 | $54,641,250 | Benchmark 2020-IG2 | No | ||

| A-1-D, A-1-E | $36,427,500 | $36,427,500 | Benchmark 2020-IG3 | No | ||||

| A-1-F, A-1-G | $36,427,500 | $36,427,500 | JPMDB 2020-COR7 | No | ||||

| A-1-H | $18,213,750 | $18,213,750 | JPMCB | No | ||||

| Total Senior Notes | $145,710,000 | $145,710,000 | ||||||

| B-1(2) | $83,637,000 | $83,637,000 | Benchmark 2020-IG2 (Loan Specific Certificates) | Yes | Midland | Midland | ||

| C-1(2) | $94,453,000 | $94,453,000 | Third Party Investor | No | ||||

| Total | $323,800,000 | $323,800,000 | ||||||

| 4 | Chase Center Tower II | A-2-A, A-2-B, A-2-C | $46,608,750 | $46,608,750 | Benchmark 2020-IG2 | No | ||

| A-2-D, A-2-E | $31,072,500 | $31,072,500 | Benchmark 2020-IG3 | No | ||||

| A-2-F, A-2-G | $31,072,500 | $31,072,500 | JPMDB 2020-COR7 | No | ||||

| A-2-H | $15,536,250 | $15,536,250 | JPMCB | No | ||||

| Total Senior Notes | $124,290,000 | $124,290,000 | ||||||

| B-2(2) | $71,363,000 | $71,363,000 | Benchmark 2020-IG2 (Loan Specific Certificates) | Yes | Midland | Midland | ||

| C-2(2) | $80,547,000 | $80,547,000 | Third Party Investor | No | ||||

| Total | $276,200,000 | $276,200,000 | ||||||

| 5 | 1633 Broadway

| A-1-S-1, A-2-S-1, A-3-S-1, A-4-S-1 | $1,000,000 | $1,000,000 | BWAY 2019-1633 | No | ||

| A-1-C-4-A | $30,000,000 | $30,000,000 | GSBI | No | ||||

| A-1-C-2, A-2-C-5 | $60,000,000 | $60,000,000 | GSMS 2020-GC45 | No | ||||

| A-1-C-1, A-1-C-5, A-2-C-1-A | $110,000,000 | $110,000,000 | CGCMT 2020-GC46 | No | ||||

| A-1-C-3, A-1-C-6 | $65,000,000 | $65,000,000 | GSMS 2020-GC47 | No | ||||

| A-2-C-3-A, A-2-C-4-B, A-2-C-4-C, A-2-C-4-D, A-2-C-6 | $90,000,000 | $90,000,000 | DBRI | No | ||||

| A-3-C-2, A-2-C-3-B | $64,650,000 | $64,650,000 | Benchmark 2020-IG1 | No | ||||

| A-3-C-3, A-2-C-2-A | $70,000,000 | $70,000,000 | Benchmark 2020-IG2 | No | ||||

| A-3-C-4, A-2-C-4-A, A-2-C-7, A-1-C-7 | $80,000,000 | $80,000,000 | Benchmark 2020-IG3 | No | ||||

| A-2-C-1-B, A-3-C-1-B | $45,000,000 | $45,000,000 | Benchmark 2020-B16 | No | ||||

| A-3-C-5, A-3-C-6 | $50,000,000 | $50,000,000 | Benchmark 2020-B17 | No | ||||

| A-3-C-7, A-1-C-4-B, A-2-C-2-B | $57,500,000 | $57,500,000 | JPMDB 2020-COR7 | No | ||||

| A-3-C-1-A | $27,850,000 | $27,850,000 | JPMCB | No | ||||

| A-4-C-1, A-4-C-2 | $100,000,000 | $100,000,000 | BANK 2020-BNK25 | No | ||||

| A-4-C-6, A-4-C-7 | $40,000,000 | $40,000,000 | BANK 2020-BNK26 | No | ||||

| A-4-C-4, A-4-C-5 | $70,000,000 | $70,000,000 | WFCM 2020-C55 | No | ||||

| A-4-C-3 | $40,000,000 | $40,000,000 | WFB | No | ||||

| Total Senior Notes | $1,001,000,000 | $1,001,000,000 | ||||||

| B-1, B-2, B-3, B-4(2) | $249,000,000 | $249,000,000 | BWAY 2019-1633 | Yes | KeyBank | Situs | ||

| Total | $1,250,000,000 | $1,250,000,000 | ||||||

| 6 | 12555 & 12655 Jefferson | A-1 | $54,000,000 | $54,000,000 | JPMDB 2019-COR6 | Yes | Midland | Midland |

| A-2, A-3 | $57,000,000 | $57,000,000 | JPMDB 2020-COR7 | No | ||||

| Total | $111,000,000 | $111,000,000 | ||||||

| 7 | 675 Creekside Way | A-1, A-4 | $43,400,000 | $43,400,000 | JPMDB 2020-COR7 | Yes | Midland | Midland |

| A-2, A-3 | $40,000,000 | $40,000,000 | DBRI | |||||

| Total | $83,400,000 | $83,400,000 | ||||||

| 8 | Hampton Roads Office Portfolio | A-1, A-5 | $50,000,000 | $49,288,251 | JPMCC 2019-COR5 | Yes | Midland | Midland |

| A-3, A-4 | $40,000,000 | $39,430,601 | JPMDB 2019-COR6 | No | ||||

| A-2, A-6 | $43,000,000 | $42,387,896 | JPMDB 2020-COR7 | No | ||||

| Total | $133,000,000 | $131,106,747 | ||||||

| 9 | 711 Fifth Avenue | A-1-1, A-1-10 | $62,500,000 | $62,500,000 | GSMS 2020-GC47 | Yes | Wells | KeyBank |

| A-1-2, A-1-3, A-1-4, A-1-5, A-1-8, A-1-9, A-1-11, A-1-12, A-1-13, A-1-14, A-1-15, A-1-16, A-1-17 | $279,000,000 | $279,000,000 | GSBI | No | ||||

| A-1-6, A-1-7 | $40,000,000 | $40,000,000 | JPMDB 2020-COR7 | No | ||||

| A-2-1, A-2-2, A-2-3, A-2-4 | $163,500,000 | $163,500,000 | BANA | No | ||||

| Total | $545,000,000 | $545,000,000 |

| THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED. | ||

| |

5 of 130 | |

| Structural and Collateral Term Sheet | JPMDB 2020-COR7 | |

| Collateral Characteristics | ||

| 10 | BX Industrial Portfolio | A-1-A-1 | $80,000,000 | $80,000,000 | Benchmark 2020-IG3 | No | ||

| A-1-A-2, A-1-A-3, A-1-A-4, A-1-A-6, A-1-A-7 | $205,000,000 | $205,000,000 | DBRI | No | ||||

| A-1-A-5, A-1-A-8 | $37,400,000 | $37,400,000 | JPMDB 2020-COR7 | No | ||||

| Total Senior Fixed Rate Notes | $322,400,000 | $322,400,000 | ||||||

| A-1-B(2) | $72,600,000 | $72,600,000 | Benchmark 2020-IG3 (Loan-Specific Certificates) | No | ||||

| A-1-C-1, A-1-C-2(2) | $110,000,000 | $110,000,000 | Third Party Investor | No | ||||

| A-1-D(2) | $45,000,000 | $45,000,000 | Third Party Investor | Yes(3) | Midland | Midland | ||

| Total Fixed Rate Notes | $550,000,000 | $550,000,000 | ||||||

| A-2 (Floating Rate Note) | $99,427,615 | $99,427,615 | Deutsche Bank AG, London Branch | No | ||||

| Total | $649,427,615 | $649,427,615 | ||||||

| 14 | Los Angeles Leased Fee Portfolio | A-1 | $61,000,000 | $61,000,000 | JPMDB 2019-COR6 | Yes | Midland | Midland |

| A-2 | $24,000,000 | $24,000,000 | JPMDB 2020-COR7 | No | ||||

| Total | $85,000,000 | $85,000,000 | ||||||

| 17 | City National Plaza

| A-1, A-2, A-3, A-4 | $330,000,000 | $330,000,000 | MSC 2020-CNP | Yes | KeyBank | KeyBank |

| A-5 | $50,000,000 | $50,000,000 | GSMS 2020-GC47 | No | ||||

| A-6 | $70,000,000 | $70,000,000 | Benchmark 2020-IG2 | No | ||||

| A-7, A-8 | $80,000,000 | $80,000,000 | Benchmark 2020-IG3 | No | ||||

| A-9 | $20,000,000 | $20,000,000 | JPMDB 2020-COR7 | No | ||||

| Total | $550,000,000 | $550,000,000 | ||||||

| 18 | Moffett Towers Buildings A, B & C | A-1-C-1, A-1-C-8 | $65,000,000 | $65,000,000 | GSMS 2020-GC47 | No(4) | ||

| A-1-C-5 | $20,000,000 | $20,000,000 | JPMDB 2020-COR7 | No | ||||

| A-1-C-2, A-1-C-3, A-1-C-6, A-1-C-7 A-1-C-9, A-1-C-10 | $128,100,000 | $128,100,000 | GSBI | No | ||||

| A-1-S-1, A-2-S-1. A-3-S-1 | $1,000,000 | $1,000,000 | MOFT 2020-ABC | No | ||||

| A-1-C-4, A-2-C-1 | $80,000,000 | $80,000,000 | Benchmark 2020-IG3 | No | ||||

| A-2-C-2, A-3-C-2, A-3-C-4 | $69,450,000 | $69,450,000 | Benchmark 2020-IG2 | No | ||||

| A-2-C-3, A-2-C-4, A-3-C-1, A-3-C-3 | $79,450,000 | $79,450,000 | Benchmark 2020-B17 | No | ||||

| Total Senior Notes | $443,000,000 | $443,000,000 | ||||||

| B-1, B-2, B-3(2) | $327,000,000 | $327,000,000 | MOFT 2020-ABC | Yes(4) | KeyBank | Situs | ||

| Total | $770,000,000 | $770,000,000 |

| THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED. | ||

| |

6 of 130 | |

| Structural and Collateral Term Sheet | JPMDB 2020-COR7 | |

| Collateral Characteristics | ||

| 21 | PCI Pharma Portfolio | A-1 | $40,000,000 | $40,000,000 | COMM 2019-GC44 | Yes | Midland | Rialto |

| A-2, A-4, A-6 | $35,000,000 | $35,000,000 | GSMS 2020-GC45 | No | ||||

| A-3 | $16,750,000 | $16,750,000 | GSMS 2020-GC47 | No | ||||

| A-5, A-7 | $16,750,000 | $16,750,000 | JPMDB 2020-COR7 | No | ||||

| Total | $108,500,000 | $108,500,000 | ||||||

| 23 | Apollo Education Group HQ Campus | A-1 | $50,000,000 | $50,000,000 | BMARK 2020-B17 | Yes | Midland | Midland |

| A-2 | $26,500,000 | $26,500,000 | JPMCB | No | ||||

| A-3 | $15,000,000 | $15,000,000 | JPMDB 2020-COR7 | No | ||||

| Total | $91,500,000 | $91,500,000 | ||||||

| 26 | Belvedere Place | A-1 | $32,750,000 | $32,750,000 | JPMDB 2019-COR6 | Yes | Midland | Midland |

| A-2 | $11,250,000 | $11,250,000 | JPMDB 2020-COR7 | No | ||||

| Total | $44,000,000 | $44,000,000 | ||||||

| 27 | Staples Headquarters | A-1 | $50,000,000 | $50,000,000 | CGCMT 2020-GC46 | Yes | Midland | CWCapital |

| A-2, A-3-1 | $30,000,000 | $30,000,000 | BMARK 2020-B17 | No | ||||

| A-3-2 | $10,000,000 | $10,000,000 | JPMDB 2020-COR7 | No | ||||

| Total | $90,000,000 | $90,000,000 | ||||||

| 28 | NOV Headquarters | A-1 | $20,000,000 | $20,000,000 | JPMCC 2019-COR5 | Yes | Midland | Midland |

| A-2 | $9,200,000 | $9,200,000 | JPMDB 2019-COR6 | No | ||||

| A-3 | $10,000,000 | $10,000,000 | JPMDB 2020-COR7 | No | ||||

| Total | $39,200,000 | $39,200,000 | ||||||

| 33 | Midland Atlantic Portfolio | A-1 | $23,000,000 | $23,000,000 | CGCMT 2020-GC46 | Yes | Midland | CWCapital |

| A-2 | $14,500,000 | $14,500,000 | GSMS 2020-GC47 | No | ||||

| A-3 | $7,500,000 | $7,500,000 | JPMDB 2020-COR7 | No | ||||

| Total | $45,000,000 | $45,000,000 |

| (1) | In the case of Loan Nos. 3, 4, 5, 10 and 18, the related Whole Loan will be serviced under the applicable controlling note securitization. During the continuance of a control appraisal period, the controlling noteholder will be the holder of the note as described further for each Whole Loan in the Preliminary Prospectus. See “Description of the Mortgage Pool—The Whole Loans” for more details. |

| (2) | Each note represents a subordinate companion loan. |

| (3) | The initial controlling note is the BX Industrial Portfolio Note A-1-D, so long as no control appraisal period with respect to the BX Industrial Portfolio Note A-1-D is continuing If and for so long as a control appraisal period with respect to the BX Industrial Portfolio Note A-1-D has occurred and is continuing, then the controlling notes will be the BX Industrial Portfolio Note A-1-C-1 and the BX Industrial Portfolio Note A-1-C-2, so long as no control appraisal period with respect to the BX Industrial Portfolio Note A-1-C-1 and the BX Industrial Portfolio Note A-1-C-2 is continuing. If and for so long as a control appraisal period with respect to the BX Industrial Portfolio Note A-1-C-1 the BX Industrial Portfolio Note A-1-C-2 has occurred and is continuing, then the controlling notes will be the BX Industrial Portfolio Note A-1-B, so long as no control appraisal period with respect to the BX Industrial Portfolio Note A-1-B is continuing. If a control appraisal period with respect to the BX Industrial Portfolio Note A-1-B has occurred and is continuing, then the controlling note will be Note A-1-A-1. See “Description of the Mortgage Pool—The Whole Loans—The Serviced AB Whole Loans—The BX Industrial Portfolio Whole Loan” in the Preliminary Prospectus. |

| (4) | The initial controlling notes are Note B-1, B-2 and B-3, so long as no Moffett Towers Buildings A, B & C control appraisal period has occurred and is continuing. If and for so long as a Moffett Towers Buildings A, B & C control appraisal period has occurred and is continuing, then the controlling note will be the Note A-1-C-1. See “Description of the Mortgage Pool—The Whole Loans—The Non-Serviced AB Whole Loans—The Moffett Towers Buildings A, B & C Whole Loan” in the Preliminary Prospectus. The Moffett Towers Buildings A, B & C Whole Loan will be serviced pursuant to the MOFT 2020-ABC trust and servicing agreement. For so long as no Moffett Towers Buildings A, B & C control appraisal period has occurred and is continuing, the control rights of the Moffett Towers Buildings A, B & C Subordinate Companion Notes will be exercisable by the controlling class under the MOFT 2020-ABC trust and servicing agreement. |

| THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED. | ||

| |

7 of 130 | |

| Structural and Collateral Term Sheet | JPMDB 2020-COR7 | |

| Collateral Characteristics | ||

| Additional Debt Summary |

No. | Loan Name | Trust | Subordinate | Total Debt | Mortgage | Total Debt | Mortgage | Total | Mortgage | Total |

| 3 | Chase Center Tower I | $36,427,500 | $178,090,000 | $323,800,000 | 3.87x | 1.36x | 31.3% | 69.5% | 13.9% | 6.2% |

| 4 | Chase Center Tower II | $31,072,500 | $151,910,000 | $276,200,000 | 3.87x | 1.36x | 31.3% | 69.5% | 13.9% | 6.2% |

| 5 | 1633 Broadway | $57,500,000 | $249,000,000 | $1,250,000,000 | 3.84x | 3.08x | 41.7% | 52.1% | 11.9% | 9.5% |

| 8 | Hampton Roads Office Portfolio | $42,387,896 | $19,715,300 | $150,822,047 | 1.40x | 1.16x | 70.8% | 81.4% | 10.9% | 9.5% |

| 10 | BX Industrial Portfolio | $37,400,000 | $268,744,955 | $649,427,615 | 3.57x | 2.09x | 39.6% | 67.6% | 12.8% | 7.5% |

| 13 | Peace Coliseum | $34,500,000 | $12,220,159 | $46,720,159 | 2.93x | 2.03x | 43.1% | 58.4% | 13.7% | 10.1% |

| 18 | Moffett Towers Buildings A, B & C | $20,000,000 | $327,000,000 | $770,000,000 | 3.63x | 2.09x | 38.7% | 67.2% | 13.1% | 7.5% |

| (1) | In the case of Loan Nos. 8 and 13, Subordinate Debt Cut-off Date Balance represents one or more mezzanine loans. In the case of Loan Nos. 3, 4, 5, 10 and 18, Subordinate Debt Cut-off Date Balance represents one or more Subordinate Companion Loans. |

| (2) | In the case of Loan Nos. 3, 4, 5, 8, 10 and 18, the UW NCF DSCR, UW NOI Debt Yield and Cut-off Date LTV calculations include the related Pari Passu Companion Loan(s). In the case of Loan Nos. 3, 4, 5, 8, 10, 13 and 18, the UW NCF DSCR, UW NOI Debt Yield and Cut-off Date LTV calculations exclude the related Subordinate Companion Loan(s) and/or related mezzanine loan(s). |

| (3) | With respect to Loan No. 8, the UW NCF DSCR is calculated using the sum of the first 12 whole loan principal and interest payments after the Cut-off Date based on the assumed principal and interest payment schedule set forth in Annex I of the Preliminary Prospectus. |

| (4) | In the case of Loan No. 10, the Mortgage Loan UW NCF DSCR, Mortgage Loan Cut-off Date LTV and Mortgage Loan UW NOI DY calculations reflect the BX Industrial Portfolio Senior Fixed Rate Loan and approximately $58.283 million of the Cut-off Date principal balance of the BX Industrial Portfolio Floating Rate Loan, and exclude the remaining approximately $41.145 million of the Cut-off Date principal balance of the BX Industrial Portfolio Floating Rate Loan and the BX Industrial Portfolio Subordinate Fixed Rate Loan. The Total Debt UW NCF DSCR, Total Debt Cut-off Date LTV and Total Debt UW NOI DY calculations reflect the $550.0 million BX Industrial Portfolio Fixed Rate Loan and the approximately $99.428 million BX Industrial Portfolio Floating Rate Loan. The interest rate on the BX Industrial Portfolio Floating Rate Loan is LIBOR (subject to a floor of 0.000%) plus a spread of 1.450%. For purposes of all calculations herein, LIBOR is assumed to be 0.500%. |

| (5) | In the case of Loan Nos. 3 and 4, the Chase Center Tower Mortgage Loans, the mortgage loans are cross-collateralized and cross-defaulted. As such, all calculations herein are based on the aggregate Cut-off Date Balance, Maturity or ARD Balance, U/W NOI, U/W NCF and Debt Services of the Chase Center Tower Mortgage Loans. |

| (6) | In the case of Loan Nos. 3, 4 and 18, the Mortgage Loan Cut-off Date LTV and Total Debt Mortgage Loan LTV are calculated by using an appraised value based on certain hypothetical assumptions. Refer to “Description of the Mortgage Pool—Assessments of Property Value and Condition” and “—Appraised Value” in the Preliminary Prospectus for additional details. |

| THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED. | ||

| |

8 of 130 | |

| Structural and Collateral Term Sheet | JPMDB 2020-COR7 | |

| Collateral Characteristics | ||

| Mortgaged Properties by Type(1) |

| Weighted Average | |||||||||

| Property Type | Property Subtype | Number of Properties | Cut-off Date Principal Balance | % of IPB | Occupancy | UW NCF DSCR(2)(3)(4)(5) | UW NOI Debt Yield(2)(4)(5) | Cut-off Date LTV(2)(4) (5)(6) | Maturity Date LTV(2)(4)(5)(6) |

| Office | Suburban | 43 | $371,227,845 | 40.8% | 97.1% | 2.14x | 10.6% | 60.5% | 55.7% |

| CBD | 7 | 237,250,000 | 26.1 | 93.3% | 3.10x | 11.2% | 47.3% | 45.5% | |

| Medical | 4 | 8,025,000 | 0.9 | 100.0% | 1.67x | 9.5% | 58.6% | 53.0% | |

| Suburban Flex | 2 | 3,310,835 | 0.4 | 100.0% | 2.61x | 9.5% | 65.4% | 65.4% | |

| Subtotal: | 56 | $619,813,681 | 68.2% | 95.7% | 2.50x | 10.8% | 55.4% | 51.9% | |

| Mixed Use | Office/Retail | 3 | $140,500,000 | 15.4% | 92.1% | 2.64x | 9.1% | 55.9% | 55.0% |

| Multifamily/Retail | 2 | 20,150,000 | 2.2 | 100.0% | 1.92x | 7.9% | 58.2% | 56.6% | |

| Subtotal: | 5 | $160,650,000 | 17.7% | 93.1% | 2.55x | 8.9% | 56.2% | 55.2% | |

| Industrial | Warehouse/Distribution | 41 | $29,725,958 | 3.3% | 93.7% | 3.40x | 12.2% | 44.2% | 44.2% |

| Flex | 13 | 10,436,859 | 1.1 | 94.4% | 2.67x | 12.0% | 53.4% | 46.5% | |

| Manufacturing | 5 | 8,573,623 | 0.9 | 98.9% | 1.85x | 9.1% | 67.5% | 57.1% | |

| R&D/Flex | 2 | 7,773,182 | 0.9 | 100.0% | 2.63x | 9.6% | 64.8% | 64.8% | |

| Warehouse/Storage | 3 | 3,203,132 | 0.4 | 21.0% | 3.57x | 12.8% | 39.6% | 39.6% | |

| Warehouse | 3 | 1,798,925 | 0.2 | 91.8% | 3.28x | 11.8% | 47.5% | 47.5% | |

| Subtotal: | 67 | $61,511,680 | 6.8% | 91.5% | 2.97x | 11.4% | 51.5% | 48.8% | |

| Retail | Anchored | 7 | $23,304,288 | 2.6% | 96.7% | 1.93x | 11.7% | 66.0% | 55.6% |

| Single Tenant | 2 | 4,537,500 | 0.5 | 100.0% | 1.38x | 8.1% | 75.0% | 61.8% | |

| Shadow Anchored | 1 | 371,200 | 0.0 | 79.7% | 1.42x | 8.9% | 70.1% | 59.0% | |

| Subtotal: | 10 | $28,212,988 | 3.1% | 97.0% | 1.83x | 11.0% | 67.5% | 56.6% | |

| Other | Leased Fee | 13 | $24,717,266 | 2.7% | 97.1% | 1.80x | 6.4% | 62.3% | 62.3% |

| Subtotal: | 13 | $24,717,266 | 2.7% | 97.1% | 1.80x | 6.4% | 62.3% | 62.3% | |

| Multifamily | Garden | 1 | $8,800,000 | 1.0% | 95.2% | 2.46x | 14.3% | 51.1% | 41.4% |

| Subtotal: | 1 | $8,800,000 | 1.0% | 95.2% | 2.46x | 14.3% | 51.1% | 41.4% | |

| Manufactured Housing | Manufactured Housing | 1 | $5,700,000 | 0.6% | 82.0% | 2.29x | 9.7% | 42.2% | 42.2% |

| Subtotal: | 1 | $5,700,000 | 0.6% | 82.0% | 2.29x | 9.7% | 42.2% | 42.2% | |

| 153 | 909,405,614 | 100.0% | 94.9% | 2.50x | 10.4% | 55.7% | 52.5% | ||

| (1) | Because this table presents information relating to the mortgaged properties and not mortgage loans, the information for mortgage loans secured by more than one mortgaged property is based on allocated loan amounts. |

| (2) | In the case of Loan Nos. 1, 3, 4, 5, 6, 7, 8, 9, 10, 14, 17, 18, 21, 23, 26, 27, 28 and 33, the UW NCF DSCR, UW NOI Debt Yield, Cut-off Date LTV and Maturity Date LTV calculations include the related Pari Passu Companion Loan(s). In the case of Loan Nos. 3, 4, 5, 8, 10, 13 and 18, the UW NCF DSCR, UW NOI Debt Yield, Cut-off Date LTV and Maturity Date LTV calculations exclude the related Subordinate Companion Loan(s) and/or related mezzanine loan(s). |

| (3) | With respect to Loan No. 8, the UW NCF DSCR is calculated using the sum of the first 12 whole loan principal and interest payments after the Cut-off Date based on the assumed principal and interest payment schedule set forth in Annex I of the Preliminary Prospectus. |

| (4) | In the case of Loan No. 10, the UW NCF DSCR, UW NOI DY, Cut-off Date LTV and Maturity Date LTV calculations reflect the BX Industrial Portfolio Senior Fixed Rate Loan and approximately $58.283 million of the Cut-off Date principal balance of the BX Industrial Portfolio Floating Rate Loan, and exclude the remaining approximately $41.145 million of the Cut-off Date principal balance of the BX Industrial Portfolio Floating Rate Loan and the BX Industrial Portfolio Subordinate Fixed Rate Loan. The interest rate on the BX Industrial Portfolio Floating Rate Loan is LIBOR (subject to a floor of 0.000%) plus a spread of 1.450%. For purposes of all calculations herein, LIBOR is assumed to be 0.500%. |

| (5) | In the case of Loan Nos. 3 and 4, the Chase Center Tower Mortgage Loans, the mortgage loans are cross-collateralized and cross-defaulted. As such, all calculations herein are based on the aggregate Cut-off Date Balance, Maturity or ARD Balance, U/W NOI, U/W NCF and Debt Services of the Chase Center Tower Mortgage Loans. |

| (6) | In the case of Loan Nos. 3, 4, 7 and 18, the Cut-off Date LTV and the Maturity Date LTV are calculated by using an appraised value based on certain hypothetical assumptions. Refer to “Description of the Mortgage Pool—Assessments of Property Value and Condition” and “—Appraised Value” in the Preliminary Prospectus for additional details. |

| THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED. | ||

| |

9 of 130 | |

| Structural and Collateral Term Sheet | JPMDB 2020-COR7 | |

| Collateral Characteristics | ||

| Mortgaged Properties by Location(1) | ||||||||

Weighted Average | ||||||||

State | Number of Properties | Cut-off Date | % of | Occupancy | UW NCF DSCR(2)(3)(4)(5) | UW NOI Debt Yield(2)(4)(5) | Cut-off Date LTV(2)(4)(5)(6) | Maturity Date LTV(2)(3)(4)(5)(6) |

| California | 30 | 374,054,288 | 41.1% | 97.2% | 2.48x | 10.1% | 54.1% | 52.4% |

| New York | 5 | 191,350,000 | 21.0 | 94.4% | 3.05x | 9.9% | 50.3% | 49.7% |

| Virginia | 41 | 51,722,175 | 5.7 | 90.6% | 1.79x | 11.2% | 65.2% | 56.6% |

| Pennsylvania | 6 | 45,935,477 | 5.1 | 78.9% | 1.94x | 10.3% | 67.6% | 58.7% |

| North Carolina | 2 | 37,824,012 | 4.2 | 95.3% | 1.68x | 10.7% | 63.9% | 50.8% |

| Illinois | 19 | 36,122,088 | 4.0 | 97.7% | 2.52x | 12.1% | 58.8% | 52.3% |

| Utah | 1 | 34,500,000 | 3.8 | 100.0% | 2.93x | 13.7% | 43.1% | 43.1% |

| Florida | 2 | 24,625,000 | 2.7 | 100.0% | 1.93x | 9.1% | 68.3% | 66.9% |

| South Carolina | 2 | 22,300,000 | 2.5 | 92.6% | 1.77x | 11.0% | 68.6% | 61.9% |

| Arizona | 1 | 15,000,000 | 1.6 | 100.0% | 4.15x | 14.9% | 47.2% | 47.2% |

| Texas | 6 | 14,416,646 | 1.6 | 96.1% | 1.99x | 9.1% | 62.8% | 61.9% |

| Nevada | 1 | 13,850,000 | 1.5 | 100.0% | 1.45x | 8.8% | 68.6% | 56.2% |

| Massachusetts | 1 | 10,000,000 | 1.1 | 100.0% | 3.98x | 12.9% | 45.5% | 45.5% |

| Alabama | 2 | 7,732,073 | 0.9 | 99.6% | 1.39x | 8.2% | 74.4% | 61.4% |

| Washington | 1 | 5,700,000 | 0.6 | 82.0% | 2.29x | 9.7% | 42.2% | 42.2% |

| Kentucky | 9 | 5,595,084 | 0.6 | 93.4% | 2.92x | 11.6% | 48.8% | 45.4% |

| Mississippi | 2 | 4,049,221 | 0.4 | 100.0% | 1.55x | 9.2% | 64.3% | 56.0% |

| New Jersey | 3 | 3,120,597 | 0.3 | 14.2% | 3.57x | 12.8% | 39.6% | 39.6% |

| Minnesota | 7 | 2,963,388 | 0.3 | 93.2% | 3.57x | 12.8% | 39.6% | 39.6% |

| Ohio | 7 | 2,536,753 | 0.3 | 78.0% | 3.26x | 12.2% | 44.1% | 42.4% |

| Georgia | 1 | 1,975,000 | 0.2 | 100.0% | 1.67x | 9.5% | 58.6% | 53.0% |

| District of Columbia | 1 | 1,912,500 | 0.2 | 100.0% | 1.38x | 8.1% | 75.0% | 61.8% |

| Indiana | 1 | 812,549 | 0.1 | 70.5% | 1.42x | 8.9% | 70.1% | 59.0% |

| Maryland | 1 | 754,603 | 0.1 | 53.5% | 3.57x | 12.8% | 39.6% | 39.6% |

| Kansas | 1 | 554,161 | 0.1 | 100.0% | 3.57x | 12.8% | 39.6% | 39.6% |

| Total / Weighted Average | 153 | $909,405,614 | 100.0% | 94.9% | 2.50x | 10.4% | 55.7% | 52.5% |

| (1) | Because this table represents information relating to the mortgaged properties and not mortgage loans, the information for the mortgage loans secured by more than one mortgaged property is based on allocated loan amounts. |

| (2) | In the case of Loan Nos. 1, 3, 4, 5, 6, 7, 8, 9, 10, 14, 17, 18, 21, 23, 26, 27, 28 and 33, the UW NCF DSCR, UW NOI Debt Yield, Cut-off Date LTV and Maturity Date LTV calculations include the related Pari Passu Companion Loan(s). In the case of Loan Nos. 3, 4, 5, 8, 10, 13 and 18, the UW NCF DSCR, UW NOI Debt Yield, Cut-off Date LTV and Maturity Date LTV calculations exclude the related Subordinate Companion Loan(s) and/or related mezzanine loan(s). |

| (3) | With respect to Loan No. 8, the UW NCF DSCR is calculated using the sum of the first 12 whole loan principal and interest payments after the Cut-off Date based on the assumed principal and interest payment schedule set forth in Annex I of the Preliminary Prospectus. |

| (4) | In the case of Loan No. 10, the UW NCF DSCR, UW NOI DY, Cut-off Date LTV and Maturity Date LTV calculations reflect the BX Industrial Portfolio Senior Fixed Rate Loan and approximately $58.283 million of the Cut-off Date principal balance of the BX Industrial Portfolio Floating Rate Loan, and exclude the remaining approximately $41.145 million of the Cut-off Date principal balance of the BX Industrial Portfolio Floating Rate Loan and the BX Industrial Portfolio Subordinate Fixed Rate Loan. The interest rate on the BX Industrial Portfolio Floating Rate Loan is LIBOR (subject to a floor of 0.000%) plus a spread of 1.450%. For purposes of all calculations herein, LIBOR is assumed to be 0.500%. |

| (5) | In the case of Loan Nos. 3 and 4, the Chase Center Tower Mortgage Loans, the mortgage loans are cross-collateralized and cross-defaulted. As such, all calculations herein are based on the aggregate Cut-off Date Balance, Maturity or ARD Balance, U/W NOI, U/W NCF and Debt Services of the Chase Center Tower Mortgage Loans. |

| (6) | In the case of Loan Nos. 3, 4, 7 and 18, the Cut-off Date LTV and the Maturity Date LTV are calculated by using an appraised value based on certain hypothetical assumptions. Refer to “Description of the Mortgage Pool—Assessments of Property Value and Condition” and “—Appraised Value” in the Preliminary Prospectus for additional details. |

| THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED. | ||

| |

10 of 130 | |

| Structural and Collateral Term Sheet | JPMDB 2020-COR7 | |

| Collateral Characteristics | ||

| Cut-off Date Principal Balance |

Weighted Average | |||||||||||

| Range of Cut-off Date Principal Balances | Number of Loans | Cut-off Date Principal Balance | % of IPB | Mortgage Rate | Remaining Loan Term | UW NCF DSCR(1)(2) (3)(4) | UW NOI Debt Yield(1)(3)(4) | Cut-off Date LTV(1)(3)(4)(5) | Maturity Date LTV(1)(3)(4)(5) | ||

| $4,954,198 | - | $9,999,999 | 9 | $62,804,687 | 6.9% | 3.82024% | 116 | 1.88x | 10.9% | 61.4% | 53.2% |

| $10,000,000 | - | $19,999,999 | 10 | 139,987,500 | 15.4 | 3.71039% | 109 | 2.38x | 10.0% | 60.7% | 57.6% |

| $20,000,000 | - | $39,999,999 | 11 | 317,325,532 | 34.9 | 3.62508% | 98 | 2.84x | 11.7% | 50.1% | 46.8% |

| $40,000,000 | - | $59,999,999 | 5 | 240,287,896 | 26.4 | 3.77402% | 107 | 2.53x | 9.9% | 56.2% | 54.3% |

| $60,000,000 | - | $80,000,000 | 2 | 149,000,000 | 16.4 | 3.47193% | 117 | 2.10x | 8.8% | 60.0% | 56.6% |

| Total / Weighted Average: | 37 | $909,405,614 | 100.0% | 3.66595% | 106 | 2.50x | 10.4% | 55.7% | 52.5% | ||

| Mortgage Interest Rates |

Weighted Average | |||||||||||

| Range of Mortgage Interest Rates | Number of Loans | Cut-off Date Principal Balance | % of IPB | Mortgage Rate | Remaining Loan Term | UW NCF DSCR(1)(2) (3)(4) | UW NOI Debt Yield(1)(3)(4) | Cut-off Date LTV(1)(3)(4)(5) | Maturity Date LTV(1)(3)(4)(5) | ||

| 2.44000% | - | 3.00000% | 3 | $157,500,000 | 17.3% | 2.84905% | 116 | 3.37x | 10.2% | 47.5% | 47.5% |

| 3.00001% | - | 3.50000% | 8 | 151,775,488 | 16.7 | 3.34391% | 109 | 2.82x | 10.5% | 55.0% | 53.5% |

| 3.50001% | - | 4.00000% | 16 | 379,754,730 | 41.8 | 3.69972% | 97 | 2.46x | 10.7% | 54.5% | 50.9% |

| 4.00001% | - | 4.50000% | 8 | 167,987,500 | 18.5 | 4.17677% | 116 | 1.82x | 10.0% | 62.4% | 57.1% |

| 4.50001% | - | 5.30000% | 2 | 52,387,896 | 5.8 | 5.17211% | 106 | 1.46x | 10.4% | 70.4% | 61.9% |

| Total / Weighted Average: | 37 | $909,405,614 | 100.0% | 3.66595% | 106 | 2.50x | 10.4% | 55.7% | 52.5% | ||

| Original Term to Maturity in Months |

| Weighted Average | |||||||||||

| Range of Original Term to Maturity in Months | Number of Loans | Cut-off Date Principal Balance | % of IPB | Mortgage Rate | Remaining Loan Term | UW NCF DSCR(1)(2) (3)(4) | UW NOI Debt Yield(1)(3)(4) | Cut-off Date LTV(1)(3)(4)(5) | Maturity Date LTV(1)(3)(4)(5) | ||

| 59 | - | 60 | 3 | $82,500,000 | 9.1% | 3.49076% | 57 | 3.92x | 14.1% | 34.2% | 34.2% |

| 77 | - | 84 | 2 | 80,800,000 | 8.9 | 3.62520% | 79 | 3.01x | 11.0% | 49.6% | 49.6% |

| 120 | - | 122 | 32 | 746,105,614 | 82.0 | 3.68974% | 115 | 2.29x | 10.0% | 58.8% | 54.8% |

| Total / Weighted Average: | 37 | $909,405,614 | 100.0% | 3.66595% | 106 | 2.50x | 10.4% | 55.7% | 52.5% | ||

| Remaining Term to Maturity in Months |

| Weighted Average | |||||||||||

| Range of Remaining Term to Maturity in Months | Number of Loans | Cut-off Date Principal Balance | % of IPB | Mortgage Rate | Remaining Loan Term | UW NCF DSCR(1)(2) (3)(4) | UW NOI Debt Yield(1)(3)(4) | Cut-off Date LTV(1)(3)(4)(5) | Maturity Date LTV(1)(3)(4)(5) | ||

| 56 | - | 84 | 5 | $163,300,000 | 18.0% | 3.55728% | 68 | 3.47x | 12.6% | 41.8% | 41.8% |

| 85 | - | 118 | 32 | 746,105,614 | 82.0 | 3.68974% | 115 | 2.29x | 10.0% | 58.8% | 54.8% |

| Total / Weighted Average: | 37 | $909,405,614 | 100.0% | 3.66595% | 106 | 2.50x | 10.4% | 55.7% | 52.5% | ||

| (1) | In the case of Loan Nos. 1, 3, 4, 5, 6, 7, 8, 9, 10, 14, 17, 18, 21, 23, 26, 27, 28 and 33, the UW NCF DSCR, UW NOI Debt Yield, Cut-off Date LTV and Maturity Date LTV calculations include the related Pari Passu Companion Loan(s). In the case of Loan Nos. 3, 4, 5, 8, 10, 13 and 18, the UW NCF DSCR, UW NOI Debt Yield, Cut-off Date LTV and Maturity Date LTV calculations exclude the related Subordinate Companion Loan(s) and/or related mezzanine loan(s). |

| (2) | With respect to Loan No. 8, the UW NCF DSCR is calculated using the sum of the first 12 whole loan principal and interest payments after the Cut-off Date based on the assumed principal and interest payment schedule set forth in Annex I of the Preliminary Prospectus. |

| (3) | In the case of Loan No. 10, the UW NCF DSCR, UW NOI DY, Cut-off Date LTV and Maturity Date LTV calculations reflect the BX Industrial Portfolio Senior Fixed Rate Loan and approximately $58.283 million of the Cut-off Date principal balance of the BX Industrial Portfolio Floating Rate Loan, and exclude the remaining approximately $41.145 million of the Cut-off Date principal balance of the BX Industrial Portfolio Floating Rate Loan and the BX Industrial Portfolio Subordinate Fixed Rate Loan. The interest rate on the BX Industrial Portfolio Floating Rate Loan is LIBOR (subject to a floor of 0.000%) plus a spread of 1.450%. For purposes of all calculations herein, LIBOR is assumed to be 0.500%. |

| (4) | In the case of Loan Nos. 3 and 4, the Chase Center Tower Mortgage Loans, the mortgage loans are cross-collateralized and cross-defaulted. As such, all calculations herein are based on the aggregate Cut-off Date Balance, Maturity or ARD Balance, U/W NOI, U/W NCF and Debt Services of the Chase Center Tower Mortgage Loans. |

| (5) | In the case of Loan Nos. 3, 4, 7 and 18, the Cut-off Date LTV and the Maturity Date LTV are calculated by using an appraised value based on certain hypothetical assumptions. Refer to “Description of the Mortgage Pool—Assessments of Property Value and Condition” and “—Appraised Value” in the Preliminary Prospectus for additional details. |

| THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED. | ||

| |

11 of 130 | |

| Structural and Collateral Term Sheet | JPMDB 2020-COR7 | |

| Collateral Characteristics | ||

| Original Amortization Term in Months |

| Weighted Average | |||||||||

| Original Amortization Term in Months | Number of Loans | Cut-off Date Principal Balance | % of IPB | Mortgage Rate | Remaining Loan Term | UW NCF DSCR(1)(2) (3)(4) | UW NOI Debt Yield(1)(3)(4) | Cut-off Date LTV(1)(3)(4)(5) | Maturity Date LTV(1)(3)(4)(5) |

| Interest Only | 21 | $605,600,000 | 66.6% | 3.46440% | 102 | 2.95x | 10.5% | 50.0% | 50.0% |

| 360 | 16 | 303,805,614 | 33.4 | 4.06771% | 115 | 1.60x | 10.2% | 67.2% | 57.6% |

| Total / Weighted Average: | 37 | $909,405,614 | 100.0% | 3.66595% | 106 | 2.50x | 10.4% | 55.7% | 52.5% |

| Remaining Amortization Term in Months |

| Weighted Average | |||||||||||

| Range of Remaining Amortization Term in Months | Number of Loans | Cut-off Date Principal Balance | % of IPB | Mortgage Rate | Remaining Loan Term | UW NCF DSCR(1)(2) (3)(4) | UW NOI Debt Yield(1)(3)(4) | Cut-off Date LTV(1)(3)(4)(5) | Maturity Date LTV(1)(3)(4)(5) | ||

| Interest Only | 21 | $605,600,000 | 66.6% | 3.46440% | 102 | 2.95x | 10.5% | 50.0% | 50.0% | ||

| 346 | - | 360 | 16 | 303,805,614 | 33.4 | 4.06771% | 115 | 1.60x | 10.2% | 67.2% | 57.6% |

| Total / Weighted Average: | 37 | $909,405,614 | 100.0% | 3.66595% | 106 | 2.50x | 10.4% | 55.7% | 52.5% | ||

| Amortization Types |

Weighted Average | |||||||||

| Amortization Types | Number of Loans | Cut-off Date Principal Balance | % of IPB | Mortgage Rate | Remaining Loan Term | UW NCF DSCR(1)(2) (3)(4) | UW NOI Debt Yield(1)(3)(4) | Cut-off Date LTV(1)(3)(4)(5) | Maturity Date LTV(1)(3)(4)(5) |

| Interest Only | 21 | $605,600,000 | 66.6% | 3.46440% | 102 | 2.95x | 10.5% | 50.0% | 50.0% |

| IO-Balloon | 12 | 212,512,500 | 23.4 | 3.92441% | 116 | 1.60x | 9.9% | 67.2% | 58.6% |

| Balloon | 4 | 91,293,114 | 10.0 | 4.40130% | 111 | 1.59x | 11.0% | 67.3% | 55.2% |

| Total / Weighted Average: | 37 | $909,405,614 | 100.0% | 3.66595% | 106 | 2.50x | 10.4% | 55.7% | 52.5% |

| Underwritten Net Cash Flow Debt Service Coverage Ratios(1)(2)(3)(4) |

| Weighted Average | |||||||||||

| Range of Underwritten Net Cash Flow Debt Service Coverage Ratios | Number of Loans | Cut-off Date Principal Balance | % of IPB | Mortgage Rate | Remaining Loan Term | UW NCF DSCR(1)(2) (3)(4) | UW NOI Debt Yield(1)(3)(4) | Cut-off Date LTV(1)(3)(4)(5) | Maturity Date LTV(1)(3)(4)(5) | ||

| 1.19x | - | 1.99x | 16 | $369,830,126 | 40.7% | 4.05633% | 114 | 1.60x | 9.3% | 66.3% | 59.1% |

| 2.00x | - | 2.99x | 13 | 312,175,488 | 34.3 | 3.49580% | 111 | 2.57x | 9.9% | 55.7% | 54.9% |

| 3.00x | - | 4.59x | 8 | 227,400,000 | 25.0 | 3.26466% | 88 | 3.88x | 13.0% | 38.5% | 38.5% |

| Total / Weighted Average: | 37 | $909,405,614 | 100.0% | 3.66595% | 106 | 2.50x | 10.4% | 55.7% | 52.5% | ||

| (1) | In the case of Loan Nos. 1, 3, 4, 5, 6, 7, 8, 9, 10, 14, 17, 18, 21, 23, 26, 27, 28 and 33, the UW NCF DSCR, UW NOI Debt Yield, Cut-off Date LTV and Maturity Date LTV calculations include the related Pari Passu Companion Loan(s). In the case of Loan Nos. 3, 4, 5, 8, 10, 13 and 18, the UW NCF DSCR, UW NOI Debt Yield, Cut-off Date LTV and Maturity Date LTV calculations exclude the related Subordinate Companion Loan(s) and/or related mezzanine loan(s). |

| (2) | With respect to Loan No. 8, the UW NCF DSCR is calculated using the sum of the first 12 whole loan principal and interest payments after the Cut-off Date based on the assumed principal and interest payment schedule set forth in Annex I of the Preliminary Prospectus. |

| (3) | In the case of Loan No. 10, the UW NCF DSCR, UW NOI DY, Cut-off Date LTV and Maturity Date LTV calculations reflect the BX Industrial Portfolio Senior Fixed Rate Loan and approximately $58.283 million of the Cut-off Date principal balance of the BX Industrial Portfolio Floating Rate Loan, and exclude the remaining approximately $41.145 million of the Cut-off Date principal balance of the BX Industrial Portfolio Floating Rate Loan and the BX Industrial Portfolio Subordinate Fixed Rate Loan. The interest rate on the BX Industrial Portfolio Floating Rate Loan is LIBOR (subject to a floor of 0.000%) plus a spread of 1.450%. For purposes of all calculations herein, LIBOR is assumed to be 0.500%. |

| (4) | In the case of Loan Nos. 3 and 4, the Chase Center Tower Mortgage Loans, the mortgage loans are cross-collateralized and cross-defaulted. As such, all calculations herein are based on the aggregate Cut-off Date Balance, Maturity or ARD Balance, U/W NOI, U/W NCF and Debt Services of the Chase Center Tower Mortgage Loans. |

| (5) | In the case of Loan Nos. 3, 4, 7 and 18, the Cut-off Date LTV and the Maturity Date LTV are calculated by using an appraised value based on certain hypothetical assumptions. Refer to “Description of the Mortgage Pool—Assessments of Property Value and Condition” and “—Appraised Value” in the Preliminary Prospectus for additional details. |

| THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED. | ||

| |

12 of 130 | |

| Structural and Collateral Term Sheet | JPMDB 2020-COR7 | |

| Collateral Characteristics | ||

| LTV Ratios as of the Cut-off Date(1)(3)(4)(5) |

| Weighted Average | |||||||||||

| Range of Cut-off Date LTVs | Number of Loans | Cut-off Date Principal Balance | % of IPB | Mortgage Rate | Remaining Loan Term | UW NCF DSCR(1)(2) (3)(4) | UW NOI Debt Yield(1)(3)(4) | Cut-off Date LTV(1)(3)(4)(5) | Maturity Date LTV(1)(3)(4)(5) | ||

| 31.3% | - | 49.9% | 10 | $267,600,000 | 29.4% | 3.40922% | 92 | 3.72x | 13.0% | 39.2% | 39.2% |

| 50.0% | - | 59.9% | 7 | 252,325,000 | 27.7 | 3.39676% | 110 | 2.43x | 8.8% | 55.9% | 55.4% |

| 60.0% | - | 64.9% | 7 | 124,351,020 | 13.7 | 3.63503% | 114 | 1.93x | 9.8% | 62.5% | 56.5% |

| 65.0% | - | 69.9% | 9 | 168,704,198 | 18.6 | 4.03435% | 114 | 1.67x | 9.4% | 67.9% | 62.2% |

| 70.0% | - | 75.0% | 4 | 96,425,396 | 10.6 | 4.47820% | 112 | 1.49x | 10.2% | 71.1% | 59.9% |

| Total / Weighted Average: | 37 | $909,405,614 | 100.0% | 3.66595% | 106 | 2.50x | 10.4% | 55.7% | 52.5% | ||

| LTV Ratios as of the Maturity Date(1)(3)(4)(5) |

Weighted Average | |||||||||||

| Range of Maturity Date LTVs | Number of Loans | Cut-off Date Principal Balance | % of IPB | Mortgage Rate | Remaining Loan Term | UW NCF DSCR(1)(2) (3)(4) | UW NOI Debt Yield(1)(3)(4) | Cut-off Date LTV(1)(3)(4)(5) | Maturity Date LTV(1)(3)(4)(5) | ||

| 31.3% | - | 39.9% | 4 | $124,900,000 | 13.7% | 3.52528% | 72 | 3.74x | 13.4% | 35.0% | 35.0% |

| 40.0% | - | 49.9% | 7 | 151,500,000 | 16.7 | 3.32752% | 110 | 3.63x | 12.8% | 43.3% | 42.8% |

| 50.0% | - | 59.9% | 14 | 375,680,218 | 41.3 | 3.49374% | 112 | 2.19x | 9.3% | 59.6% | 55.6% |

| 60.0% | - | 64.9% | 9 | 208,575,396 | 22.9 | 4.23195% | 113 | 1.59x | 9.3% | 67.5% | 61.2% |

| 65.0% | - | 68.8% | 3 | 48,750,000 | 5.4 | 3.98355% | 110 | 2.15x | 9.1% | 67.0% | 67.0% |

| Total / Weighted Average: | 37 | $909,405,614 | 100.0% | 3.66595% | 106 | 2.50x | 10.4% | 55.7% | 52.5% | ||

| Prepayment Protection |

Weighted Average | |||||||||

| Prepayment Protection | Number of Loans | Cut-off Date Principal Balance | % of IPB | Mortgage Rate | Remaining Loan Term | UW NCF DSCR(1)(2) (3)(4) | UW NOI Debt Yield(1)(3)(4) | Cut-off Date LTV(1)(3)(4)(5) | Maturity Date LTV(1)(3)(4)(5) |

| Defeasance | 31 | $764,067,718 | 84.0% | 3.62415% | 107 | 2.42x | 10.1% | 56.3% | 53.2% |

| Yield Maintenance | 2 | 79,787,896 | 8.8 | 4.47970% | 92 | 2.42x | 11.8% | 56.2% | 50.6% |

| Defeasance or Yield Maintenance | 4 | 65,550,000 | 7.2 | 3.16275% | 116 | 3.51x | 12.1% | 48.0% | 46.7% |

| Total / Weighted Average: | 37 | $909,405,614 | 100.0% | 3.66595% | 106 | 2.50x | 10.4% | 55.7% | 52.5% |

| Loan Purpose |

Weighted Average | |||||||||

| Loan Purpose | Number of Loans | Cut-off Date Principal Balance | % of IPB | Mortgage Rate | Remaining Loan Term | UW NCF DSCR(1)(2) (3)(4) | UW NOI Debt Yield(1)(3)(4) | Cut-off Date LTV(1)(3)(4)(5) | Maturity Date LTV(1)(3)(4)(5) |

| Refinance | 19 | $543,813,032 | 59.8% | 3.60009% | 104 | 2.63x | 10.6% | 53.5% | 50.0% |

| Acquisition | 17 | 331,092,582 | 36.4 | 3.71411% | 109 | 2.25x | 9.8% | 60.7% | 57.6% |

| Recapitalization | 1 | 34,500,000 | 3.8 | 4.24200% | 117 | 2.93x | 13.7% | 43.1% | 43.1% |

| Total / Weighted Average: | 37 | $909,405,614 | 100.0% | 3.66595% | 106 | 2.50x | 10.4% | 55.7% | 52.5% |

| (1) | In the case of Loan Nos. 1, 3, 4, 5, 6, 7, 8, 9, 10, 14, 17, 18, 21, 23, 26, 27, 28 and 33, the UW NCF DSCR, UW NOI Debt Yield, Cut-off Date LTV and Maturity Date LTV calculations include the related Pari Passu Companion Loan(s). In the case of Loan Nos. 3, 4, 5, 8, 10, 13 and 18, the UW NCF DSCR, UW NOI Debt Yield, Cut-off Date LTV and Maturity Date LTV calculations exclude the related Subordinate Companion Loan(s) and/or related mezzanine loan(s). |

| (2) | With respect to Loan No. 8, the UW NCF DSCR is calculated using the sum of the first 12 whole loan principal and interest payments after the Cut-off Date based on the assumed principal and interest payment schedule set forth in Annex I of the Preliminary Prospectus. |

| (3) | In the case of Loan No. 10, the UW NCF DSCR, UW NOI DY, Cut-off Date LTV and Maturity Date LTV calculations reflect the BX Industrial Portfolio Senior Fixed Rate Loan and approximately $58.283 million of the Cut-off Date principal balance of the BX Industrial Portfolio Floating Rate Loan, and exclude the remaining approximately $41.145 million of the Cut-off Date principal balance of the BX Industrial Portfolio Floating Rate Loan and the BX Industrial Portfolio Subordinate Fixed Rate Loan. The interest rate on the BX Industrial Portfolio Floating Rate Loan is LIBOR (subject to a floor of 0.000%) plus a spread of 1.450%. For purposes of all calculations herein, LIBOR is assumed to be 0.500%. |

| (4) | In the case of Loan Nos. 3 and 4, the Chase Center Tower Mortgage Loans, the mortgage loans are cross-collateralized and cross-defaulted. As such, all calculations herein are based on the aggregate Cut-off Date Balance, Maturity or ARD Balance, U/W NOI, U/W NCF and Debt Services of the Chase Center Tower Mortgage Loans. |

| (5) | In the case of Loan Nos. 3, 4, 7 and 18, the Cut-off Date LTV and the Maturity Date LTV are calculated by using an appraised value based on certain hypothetical assumptions. Refer to “Description of the Mortgage Pool—Assessments of Property Value and Condition” and “—Appraised Value” in the Preliminary Prospectus for additional details. |

| THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED. | ||

| |

13 of 130 | |

| Structural and Collateral Term Sheet | JPMDB 2020-COR7 | |

| Collateral Characteristics | ||

| Previous Securitization History(1) |

| No. | Property Name | Cut-off Date Principal Balance | % of IPB | Location | Property Type | Previous Securitization |

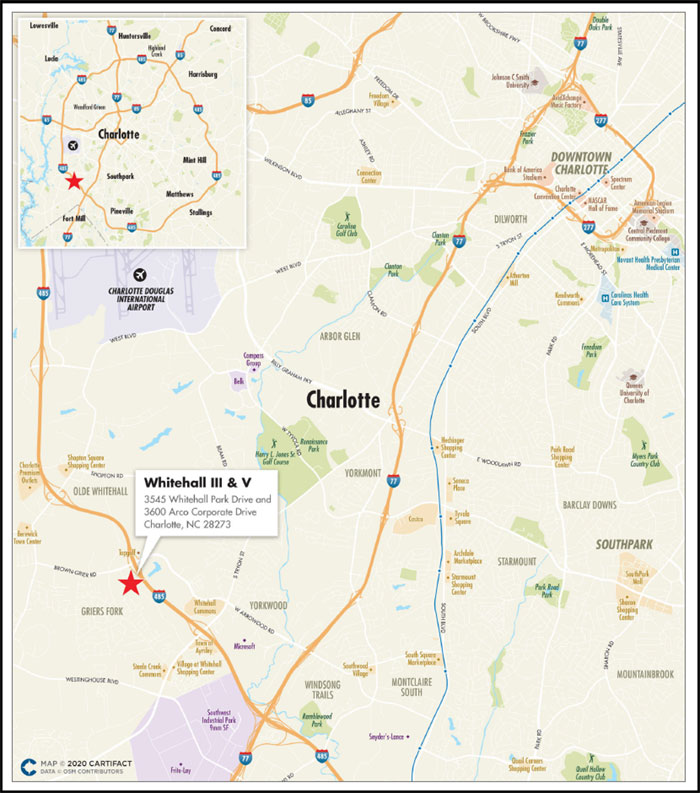

| 11 | Whitehall III & V | $36,175,532 | 4.0% | Charlotte, North Carolina | Office | LNCR 2019-CRE2; LNCR 2019-CRE3 |

| 12 | Frick Building | $35,250,000 | 3.9% | Pittsburgh, Pennsylvania | Office | WFRBS 2011-C4 |

| 18 | Moffett Towers Buildings A, B & C | $20,000,000 | 2.2% | Sunnyvale, California | Office | COMM 2013-LC6; COMM 2013-CCRE6; COMM 2013-CCRE7 |

| 23 | Apollo Education Group HQ Campus | $15,000,000 | 1.6% | Phoenix, Arizona | Office | CGCMT 2015-GC29 |

| 29 | Briarcliff Apartments | $8,800,000 | 1.0% | Depew, New York | Multifamily | UBSCM 2012-C1 |

| 33 | Midland Atlantic Portfolio | $7,500,000 | 0.8% | Various | Retail | MSBAM 2012-C5 |

| (1) | The table above represents the properties for which the previously existing debt was securitized, based on information provided by the related borrower or obtained through searches of a third-party database. |

| THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED. | ||

| |

14 of 130 | |

| Structural and Collateral Term Sheet | JPMDB 2020-COR7 | |

| Collateral Characteristics | ||

| COVID Update* |

| No. | Property Name | Mortgage Loan Seller | Information as of Date | Property Type | May Debt Service Payment Received (Yes/No) | June Debt Service Payment Received (Yes/No) | Forbearance or Other Debt Service Relief Requested (Yes/No) | Other Loan Modification Requested (Yes/No) | Lease Modification or Rent Relief Requested (Yes/No) | Occupied SF or Unit Count Making Full April Rent Payment (%) | UW Base Rent Paid (%) | Occupied SF or Unit Count Making Full May Rent Payment (%) | UW Base Rent Paid (%) |

| 1 | 530 Broadway(1) | LCM | 5/29/2020 | Mixed Use | Yes | Yes | No | No | Yes | 100.0% | 100.0% | 94.3% | 76.9% |

| 2 | LA County Office Portfolio(2) | LCM | 5/29/2020 | Office | Yes | Yes | No | No | Yes | 87.1% | 85.5% | 83.9% | 83.8% |

| 3 | Chase Center Tower I | JPMCB | 6/10/2020 | Office | Yes | Yes | No | No | No | 100.0% | 100.0% | 100.0% | 100.0% |

| 4 | Chase Center Tower II | JPMCB | 6/10/2020 | Office | Yes | Yes | No | No | No | 100.0% | 100.0% | 100.0% | 100.0% |

| 5 | 1633 Broadway | JPMCB / GACC / GSMC | 6/3/2020 | Office | Yes | Yes | No | No | Yes(3) | 86.5% | 89.9% | 86.5% | 89.9% |

| 6 | 12555 & 12655 Jefferson | LCM | 5/29/2020 | Office | Yes | Yes | No | No | No | 100.0% | 100.0% | 100.0% | 100.0% |

| 7 | 675 Creekside Way | GACC | 6/6/2020 | Office | Yes | Yes | No | No | No | 100.0% | 100.0% | 100.0% | 100.0% |

| 8 | Hampton Roads Office Portfolio(4) | LCM | 5/29/2020 | Office | Yes | Yes | No | Yes | No | 97.6% | 96.4% | 90.1% | 87.6% |

| 9 | 711 Fifth Avenue | GSMC | 6/11/2020 | Mixed Use | Yes | Yes | No | No | Yes(5) | 100.0%(6) | 81.3%(6) | 100.0%(6) | 72.4%(6) |

| 10 | BX Industrial Portfolio | GACC | 6/9/2020 | Various | NAP(7) | Yes | No | No | No | 96.5% | 97.9% | 93.8%(8) | 90.3%(8) |

| 11 | Whitehall III & V | LCM | 5/29/2020 | Office | Yes | Yes | No | No | No | 100.0% | 100.0% | 100.0% | 100.0% |

| 12 | Frick Building(9) | JPMCB | 6/1/2020 | Office | Yes | Yes | No | No | Yes | 96.9% | 96.6% | 96.8% | 96.5% |

| 13 | Peace Coliseum | LCM | 5/29/2020 | Office | Yes | Yes | No | No | No | 100.0% | 100.0% | 100.0% | 100.0% |

| 14 | Los Angeles Leased Fee Portfolio(10) | LCM | 5/29/2020 | Other | Yes | Yes | No | No | Yes | 100.0% | 100.0% | 100.0% | 100.0% |

| 15 | 1340 Concord(11) | JPMCB | 6/1/2020 | Office | Yes | Yes | No | No | No | 100.0% | 100.0% | 100.0% | 100.0% |

| 16 | 1333 Main Street(12) | LCM | 5/29/2020 | Mixed Use | Yes | Yes | No | No | No | 99.2% | 99.0% | 95.1% | 95.2% |

| 17 | City National Plaza | GSMC | 5/12/2020 | Office | Yes | Yes | No | No | Yes(13) | 92.1% | 92.3% | 91.0% | 90.8% |

| 18 | Moffett Tower A, B & C | GSMC | 5/5/2020 | Office | Yes | Yes | No | No | Yes(14) | 98.8% | 96.3% | 98.8% | 96.3% |

| 19 | Roscoe Office | GACC | 6/6/2020 | Office | Yes | Yes | No | No | No | 100.00% | 100.0% | 100.0% | 100.0% |

| 20 | Lava Ridge Business Center(15) | LCM | 5/29/2020 | Office | Yes | Yes | No | No | No | 98.4% | 98.1% | 98.4% | 98.1% |

| 21 | PCI Pharma Portfolio | GSMC | 6/8/2020 | Various | Yes | Yes | No | No | No | 100.0% | 100.0% | 100.0% | 100.0% |

| 22 | The Oliver(16) | JPMCB | 6/1/2020 | Mixed Use | Yes | Yes | No | No | Yes | 83.4% | 81.8% | 81.7% | 80.9% |

| 23 | Apollo Education Group HQ Campus | JPMCB | 6/5/2020 | Office | Yes | Yes | No | No | No | 100.0% | 100.0% | 100.0% | 100.0% |

| 24 | SHP Building IV(17) | LCM | 5/29/2020 | Office | Yes | Yes | No | No | Yes | 100.0% | 100.0% | 100.0% | 100.0% |

| 25 | GIP REIT Portfolio | GACC | 6/6/2020 | Various | Yes | Yes | No | No | No | 100.0% | 100.0% | 100.0% | 100.0% |

| 26 | Belvedere Place(18) | LCM | 5/29/2020 | Office | Yes | Yes | No | No | Yes | 100.0% | 100.0% | 97.7% | 97.5% |

| 27 | Staples Headquarters | GACC | 6/6/2020 | Office | Yes | Yes | No | No | No | 100.0% | 100.0% | 100.0% | 100.0% |

| 28 | NOV Headquarters | LCM | 5/29/2020 | Office | Yes | Yes | No | No | No | 100.0% | 100.0% | 100.0% | 100.0% |

| 29 | Briarcliff Apartments | GACC | 6/6/2020 | Multifamily | Yes | Yes | No | No | No | 98.7% | 98.8% | 97.5%(19) | 97.5%(20) |

| 30 | Stuart's Crossing | GSMC | 6/9/2020 | Retail | Yes | Yes | No | No | Yes(21) | 90.1% | 89.7% | 88.3% | 85.3% |

| 31 | KB Fresenius & DaVita Southeast Portfolio | LCM | 5/29/2020 | Office | Yes | Yes | No | No | No | 100.0% | 100.0% | 100.0% | 100.0% |

| 32 | Caton Crossings | GSMC | 6/9/2020 | Retail | Yes | Yes | No | No | Yes(22) | 98.1% | 96.6% | 88.5% | 86.1% |

| 33 | Midland Atlantic Portfolio | GSMC | 6/3/2020 | Retail | Yes | Yes | No | No | Yes(23) | 71.4% | 82.6%(24) | 78.6% | 89.5%(25) |

| 34 | Guidepost Montessori | LCM | 5/29/2020 | Office | Yes | Yes | No | No | No | 100.0% | 100.0% | 100.0% | 100.0% |

| 35 | Maple Grove RV Resort | LCM | 5/29/2020 | Manufactured Housing | Yes | Yes | No | No | No | 100.0% | 100.0% | 100.0% | 100.0% |

| 36 | 278 Court Street(26) | JPMCB | 6/1/2020 | Mixed Use | Yes | Yes | No | No | No | 100.0% | 100.0% | 100.0% | 100.0% |

| 37 | Willow Lake Tech Center(27) | LCM | 5/29/2020 | Industrial | Yes | Yes | No | Yes | No | 94.2% | 92.3% | 94.2% | 92.3% |

| * | The information in this chart is as of the date indicated and is based on information provided by the related borrowers. The information was based on reports and data aggregated from the related borrower’s existing financial and operational reporting systems and in certain circumstances was produced on an interim or ad hoc basis or was provided by the related borrower verbally. While we have no reason to believe the information presented is not accurate, we cannot assure you that it will not change or be updated in the future. |

| THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED. | ||

| |

15 of 130 | |

| Structural and Collateral Term Sheet | JPMDB 2020-COR7 | |

| Collateral Characteristics | ||

| (1) | Two tenants representing approximately 36.9% of the underwritten base rent and 30.2% of net rentable area have requested rent relief. Tenants are currently undergoing conversations with the borrower. |

| (2) | Five tenants representing approximately 39.1% of the underwritten base rent and 38.2% of net rentable area have requested rent relief. Two tenants have been granted a rent deferral and three tenants are currently undergoing conversations with the borrower. |

| (3) | One tenant, representing approximately 8% of underwritten base rent, paid reduced May rent and has signed an amendment for reduced rent through year end 2020. The difference between the underwritten contractual rent per the original lease and the reduced rent pursuant to signed amendment is required to be repaid over a 36-month period beginning January 1, 2021 at an imputed interest rate of 3.75% (from April 1, 2020) on the amount of rent deferred. One tenant, representing approximately 4.7% of the underwritten base rent, has agreed to a three month rent deferral for the months of April, May and June 2020. |

| (4) | The borrower requested an amendment to the Mortgage Loan documents and the borrower, guarantor and Midland Loan Services, a Division of PNC Bank, National Association, as master servicer for the JPMCC 2019-COR5 securitization transaction have agreed to an amendment to temporarily defer the required monthly payments into the rollover and replacement reserve accounts, which deferred amounts will be required to be repaid. |

| (5) | One retail tenant, representing approximately 4.2% of net rentable area and 37.3% of underwritten base rent, agreed with the borrower sponsor to pay 50% abated rent for April, May and June 2020 with 50% recaptured by year end 2020 and the remaining 50% recaptured by the end of the first quarter 2021. The borrower sponsor is in the process of finalizing an agreement for rent relief with respect to the Polo Bar space (7,436 square feet of the 38,638 total square feet attributable to Ralph Lauren and 1.4% of underwritten base rent attributable to Ralph Lauren) which is temporarily closed. The agreement includes a $250,000 rent abatement and $250,000 rent deferral for May 2020 and a $250,000 rent deferral for June 2020 (totaling $750,000). |

| (6) | Includes (i) one tenant, representing 4.2% of net rentable area and 37.3% of underwritten base rent, that paid their rent in accordance with an agreement to pay 50% abated rent for the month of May and (ii) one tenant, representing 11.4% of net rentable area and 41.1% of the underwritten base rent, that is in the process of executing an agreement with the borrower sponsor and is anticipated to pay May and June rent upon execution of the amendment. |

| (7) | The BX Industrial Portfolio mortgage loan was originated in May 2020 and the first due date was June 9, 2020. |

| (8) | As of the May collections period, 11 tenants, representing approximately 6.2% of net rentable area and 9.7% of the underwritten base rent, either did not pay rent or paid a portion of their scheduled rent amount. |

| (9) | Two tenants representing 6.1% of underwritten base rent have delayed rent commencement dates due to delays in tenant build-outs as result of COVID related closures. Additionally, one retail tenant, representing 0.5% of underwritten base rent has been granted temporary rent relief due to ongoing COVID related disruption. |

| (10) | One tenant representing approximately 33.7% of the underwritten base rent and 34.4% of net rentable area has been granted a rent deferral. |

| (11) | The sole tenant at the property, Ultimate Software, has taken possession of its space and commenced paying rent. However, due to COVID related closures, the build-pit pf its space has been delayed. Ultimate Software is expected to take occupancy upon completion of its build-out. |

| (12) | Two tenants representing approximately 1.7% of the underwritten base rent and 2.0% of net rentable area have requested rent relief. Tenants are currently undergoing conversations with the borrower. |

| (13) | Eight tenants, representing 13.1% of the underwritten base rent, are in discussions with the borrower sponsor with regards to lease amendments and restructures. |

| (14) | The Occupied SF or Unit Count Making Full May Rent Payment (%) and UW Base Rent Paid (%) are based on the percentage of underwritten tenant leases with rent due in May. Based on the underwritten rent roll, there are a total of six tenant leases at the Moffett Towers Buildings A, B & C Mortgaged Property and four of those tenant leases owed rent for May. Of those four tenant leases, one tenant lease, representing approximately 4% of the expected May rent collection, did not pay. Two tenants, Google and Comcast, have executed leases; however, rent was not due under those leases for May. Google is currently building-out additional leased premises and Comcast is scheduled to relocate at the Moffett Towers Buildings A, B & C Mortgaged Property. Google has executed leases for Buildings B and C, representing approximately 56% of underwritten base rent. Google is expected to take possession of Building B in January 2021. Google is expected to take possession of its premises in Building C in two phases: 96,282 square feet was taken possession of in March 2020 and 84,914 square feet is expected to be taken possession of in July 2020. Google is expected to begin paying rent for Building B and Building C in June 2021 and September 2020, respectively. Comcast has executed a lease extension and relocation for Building C and is expected to take possession of the relocation space in November 2020 and begin paying rent on both the existing space and relocation space in March 2021, representing approximately 13% of underwritten base rent. |

| (15) | One tenant, representing approximately 1.8% of the underwritten base rent and 1.6% of net rentable area, has requested rent relief. Tenant is currently undergoing conversations with the borrower. |

| (16) | The loan sponsor is currently evaluating rent relief requests with respect to a large portion of the retail component of the property, accounting for 22.3% of underwritten base rent. |

| (17) | Two tenants, representing approximately 37.2% of the underwritten base rent and 37.3% of the net rentable area, have requested rent relief. One tenant has been granted a rent deferral and one tenant is currently undergoing conversations with the borrower. |

| (18) | Two tenants, representing approximately 46.2% of the underwritten base rent and 47.3% of net rentable area, have requested rent relief. Tenants are currently undergoing conversations with the borrower. |