UNITED STATES SECURITIES AND EXCHANGE COMMISSION

Washington D.C. 20549

____________

FORM 10-Q

x Quarterly Report Pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934

For the quarterly period ended March 31, 2015

OR

o Transition Report Pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934

For the transition period from to

Commission File Number 001-31668

INTEGRATED BIOPHARMA, INC.

(Exact name of registrant, as specified in its charter)

| Delaware | 22-2407475 |

| (State or other jurisdiction of | (I.R.S. Employer |

| incorporation or organization) | Identification No.) |

| 225 Long Ave., Hillside, New Jersey | 07205 |

| (Address of principal executive offices) | (Zip Code) |

(888) 319-6962

(Registrant’s telephone number, including Area Code)

Not Applicable

(Former name, former address and former fiscal year, if changed since last report)

Indicate by check mark whether the Registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities and Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the Registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one):

| | | | | | | |

| Large accelerated filer | | Accelerated filer | | Non-accelerated filer | | Smaller reporting company þ |

Indicate by check whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act).

Applicable only to Corporate Issuers:

The number of shares outstanding of each of the issuer’s class of common stock, as of the latest practicable date:

| Class | Outstanding at May 14, 2015 |

| Common Stock, $0.002 par value | 21,105,174 Shares |

INTEGRATED BIOPHARMA, INC. AND SUBSIDIARIES

FORM 10-Q QUARTERLY REPORT

For the Nine Months Ended March 31, 2015

INDEX

| | | Page |

| | Part I. Financial Information | |

| Item 1. | Condensed Consolidated Statements of Operations for the Three and Nine Months Ended March 31, 2015 and 2014 (unaudited) | 2 |

| | Condensed Consolidated Balance Sheets as of March 31, 2015 and June 30, 2014 (unaudited) | 3 |

| | Condensed Consolidated Statements of Cash Flows for the Nine Months ended March 31, 2015 and 2014 (unaudited) | 4 |

| | Notes to Condensed Consolidated Statements | 5 |

| | | |

| Item 2. | Management’s Discussion and Analysis of Financial Condition and Results of Operations | 18 |

| | | |

| Item 3. | Quantitative and Qualitative Disclosures about Market Risk | 26 |

| | | |

| Item 4. | Controls and Procedures | 26 |

| | | |

| | Part II. Other Information | |

| | | |

| Item 1. | Legal Proceedings | 26 |

| | | |

| Item 1A. | Risk Factors | 26 |

| | | |

| Item 2. | Unregistered Sales of Equity Securities and Use of Proceeds | 26 |

| | | |

| Item 3. | Defaults Upon Senior Securities | 27 |

| | | |

| Item 4. | Mine Safety Disclosure | 27 |

| | | |

| Item 5. | Other Information | 27 |

| | | |

| Item 6. | Exhibits | 27 |

| | Other | |

| Signatures | | 28 |

| | | |

| | | |

| | | |

Cautionary Statement Regarding Forward-Looking Statements

Certain statements in this Quarterly Report on Form 10-Q may constitute “forward-looking” statements as defined in Section 27A of the Securities Act of 1933, as amended (the “Securities Act”), Section 21E of the Securities Act of 1934, as amended (the “Exchange Act”), the Private Securities Litigation Reform Act of 1995 (the “PSLRA”) or in releases made by the Securities and Exchange Commission (“SEC”), all as may be amended from time to time. Such forward-looking statements involve known and unknown risks, uncertainties and other important factors that could cause the actual results, performance or achievements of Integrated BioPharma, Inc. and its subsidiaries (the “Company”) or industry results, to differ materially from any future results, performance or achievements expressed or implied by such forward-looking statements. Such factors including, among others, changes in general economic and business conditions; loss of market share through competition; introduction of competing products by other companies; the timing of regulatory approval and the introduction of new products by the Company; changes in industry capacity; pressure on prices from competition or from purchasers of the Company's products; regulatory changes in the pharmaceutical manufacturing industry and nutraceutical industry; regulatory obstacles to the introduction of new technologies or products that are important to the Company; availability of qualified personnel; the loss of any significant customers or suppliers; and other factors both referenced and not referenced in the Company’s Annual Report on Form 10-K for the fiscal year ended June 30, 2014 (“Form 10-K”), as filed with the SEC. Statements that are not historical fact are forward-looking statements. Forward-looking statements can be identified by, among other things, the use of forward-looking language, such as the words, “plan”, “believe”, “expect”, “anticipate”, “intend”, “estimate”, “project”, “may”, “will”, “would”, “could”, “should”, “seeks”, or “scheduled to”, or other similar words, or the negative of these terms or other variations of these terms or comparable language, or by discussion of strategy or intentions. These cautionary statements are being made pursuant to the Securities Act, the Exchange Act and the PSLRA with the intention of obtaining the benefits of the “safe harbor” provisions of such laws. The Company cautions investors that any forward-looking statements made by the Company are not guarantees or indicative of future performance. Important assumptions and other important factors that could cause actual results to differ materially from those forward-looking statements with respect to the Company, include, but are not limited to, the risks and uncertainties affecting its businesses described in Item 1 of the Company’s Annual Report filed on Form 10-K for the year ended June 30, 2014 and in other securities filings by the Company. Although the Company believes that its plans, intentions and expectations reflected in or suggested by such forward-looking statements are reasonable, actual results could differ materially from a projection or assumption in any of the forward-looking statements. The Company’s future financial condition and results of operations, as well as any forward-looking statements, are subject to change and inherent risks and uncertainties. The forward-looking statements contained in this Quarterly Report on Form 10-Q are made only as of the date hereof and the Company does not have or undertake any obligation to update or revise any forward-looking statements whether as a result of new information, subsequent events or otherwise, unless otherwise required by law.

1

ITEM 1. FINANCIAL STATEMENTS

2

3

4

INTEGRATED BIOPHARMA, INC. AND SUBSIDIARIES

NOTES TO THE CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

(in thousands, except share and per share amounts)

Note 1. Principles of Consolidation and Basis of Presentation

Basis of Presentation of Interim Financial Statements

The accompanying condensed consolidated financial statements for the interim periods are unaudited and include the accounts of Integrated BioPharma, Inc., a Delaware corporation (together with its subsidiaries, the “Company”). The interim condensed consolidated financial statements have been prepared in conformity with Rule 10-01 of Regulation S-X of the Securities and Exchange Commission (“SEC”) and therefore do not include information or footnotes necessary for a complete presentation of financial position, results of operations and cash flows in conformity with accounting principles generally accepted in the United States of America. However, all adjustments (consisting only of normal recurring adjustments) which are, in the opinion of management, necessary for a fair presentation of the financial position and operating results for the periods presented have been included. These condensed consolidated financial statements should be read in conjunction with the financial statements and notes thereto, together with Management’s Discussion and Analysis of Financial Condition and Results of Operations, contained in the Company’s Annual Report on Form 10-K for the fiscal year ended June 30, 2014 (“Form 10-K”), as filed with the SEC. The June 30, 2014 balance sheet was derived from audited financial statements, but does not include all disclosures required by accounting principles generally accepted in the United States of America. The results of operations for the three and nine months ended March 31, 2015 are not necessarily indicative of the results for the full fiscal year ending June 30, 2015 or for any other period.

Nature of Operations

The Company is engaged primarily in manufacturing, distributing, marketing and sales of vitamins, nutritional supplements and herbal products. The Company’s customers are located primarily in the United States, Luxembourg and Canada. The Company was previously known as Integrated Health Technologies, Inc. and, prior to that, as Chem International, Inc. The Company was reincorporated in its current form in Delaware in 1995. The Company continues to do business as Chem International, Inc. with certain of its customers and certain vendors.

The Company’s business segments include: (a) Contract Manufacturing operated by InB:Manhattan Drug Company, Inc. (“MDC”), which manufactures vitamins and nutritional supplements for sale to distributors, multilevel marketers and specialized health-care providers; (b) Branded Proprietary Products operated by AgroLabs, Inc. (“AgroLabs”), which distributes healthful nutritional products for sale through major mass market, grocery, drug and vitamin retailers, under the following brands: Naturally Noni, Coconut Water, Aloe Pure, Peaceful Sleep, Green Envy, ACAI Extra, ACAI Cleanse, Wheatgrass and other products which are being introduced into the market (these are referred to as our branded proprietary nutraceutical business and/or products); and (c) Other Nutraceutical Businesses which includes the operations of (i) The Vitamin Factory (the “Vitamin Factory”), which sells private label MDC products, as well as our AgroLabs products, through the Internet, (ii) IHT Health Products, Inc. (“IHT”) a distributor of fine natural botanicals, including multi minerals produced under a license agreement and (iii) Chem International, Inc., a distributor of certain raw materials for DSM Nutritional Products, LLC.

Significant Accounting Policies

There have been no material changes during fiscal year 2015 in the Company’s significant accounting policies to those previously disclosed in the Company’s Annual Report on Form 10-K for the fiscal year ended June 30, 2014.

Investment in iBio, Inc. The Company accounts for its investment in iBio, Inc. (“iBio”) common stock on the cost basis as it initially retained approximately 6% of its interest in iBio (1,266,706 common shares) (the “iBio Stock”) at the time of the spin-off of this subsidiary in August 2008. The Company reviews its investment in iBio for impairment and records a loss when there is deemed to be an impairment of the investment. To date, there were cumulative impairment charges of $298. The market value of the iBio Stock as of March 31, 2015 was approximately $1.0 million.

5

INTEGRATED BIOPHARMA, INC. AND SUBSIDIARIES

NOTES TO THE CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

(in thousands, except share and per share amounts)

Pursuant to the Company’s Loan Agreement with PNC Bank, National Association (“PNC”), the Company is required to sell the iBio Stock when the trading price of the iBio Stock is less than $0.88 per share for a period of fifteen (15) consecutive trading days on the applicable exchange and utilize all proceeds from such sale to prepay the outstanding principal of the term loan outstanding under the Loan Agreement at such time. During certain periods in the fiscal years ended June 30, 2014 and 2013, the trading price of the iBio Stock was less than $0.88 for a period of fifteen (15) consecutive trading days and continued to have a trading price less than $0.88 during certain periods through April 8, 2015. (See Note 5. Senior Credit Facility, Subordinated Convertible Note, net - CD Financial, LLC and other Long Term Debt).

As of May 14, 2015, PNC has not required the Company to sell any of the iBio Stock but reserves the right to do so at any time in the future. Although not required to do so, on or about April 30, 2015, the Company sold 60,000 shares of iBio Stock providing net trading proceeds of approximately $64 which were used to prepay principal outstanding under the Term Loan. (See Note 5. Senior Credit Facility, Subordinated Convertible Note, net - CD Financial, LLC and other Long Term Debt).

Earnings Per Share. Basic earnings per common share amounts are based on the weighted average number of common shares outstanding. Diluted earnings per share amounts are based on the weighted average number of common shares outstanding, plus the incremental shares that would have been outstanding upon the assumed exercise of all potentially dilutive stock options, warrants, and convertible debt subject to anti-dilution limitations using the treasury stock method

The following stock options and potentially dilutive shares for convertible notes payable, were not included in the computation of weighted average diluted common shares outstanding as the effect of doing so would be anti-dilutive for the three and nine months ended March 31, 2015 and 2014:

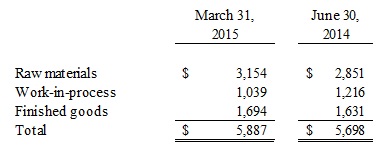

Note 2. Inventories

Inventories are stated at the lower of cost or market using the first-in, first-out method and consist of the following as of:

6

INTEGRATED BIOPHARMA, INC. AND SUBSIDIARIES

NOTES TO THE CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

(in thousands, except share and per share amounts)

Note 3. Intangible Assets, net

Intangible assets consist of trade names, license fees from the Branded Proprietary Products Segment, and unpatented technology from the Other Nutraceutical Businesses Segment. The carrying amount of intangible assets, net is as follows as of:

Amortization expense recorded on intangible assets for each of the three and nine months ended March 31, 2015 and 2014 was $34 and $103, respectively. Amortization expense is recorded on the straight-line basis over periods ranging from 13 years to 20 years based on contractual or estimated lives and is included in selling and administrative expenses. Tests for impairment or recoverability are performed at least annually and require significant management judgment and the use of estimates which the Company believes are reasonable and appropriate at the time of the impairment test. Future unanticipated events affecting cash flows and changes in market conditions could affect such estimates and result in the need for an impairment charge. The Company also re-evaluates the periods of amortization to determine whether circumstances warrant revised estimates of current useful lives. No impairment losses were identified or recorded in the three and nine months ended March 31, 2015 and 2014 on the Company’s intangible assets.

The estimated annual amortization expense for intangible assets for the five succeeding fiscal years is as follows:

7

INTEGRATED BIOPHARMA, INC. AND SUBSIDIARIES

NOTES TO THE CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

(in thousands, except share and per share amounts)

Note 4. Property and Equipment, net

Property and equipment, net consists of the following as of:

Depreciation and amortization expense recorded on property and equipment was $71 and $60 for the three months ended March 31, 2015 and 2014, respectively and $202 and $195 for the nine months ended March 31, 2015 and 2014, respectively. In the nine months ended March 31, 2015, the Company traded in property and equipment with an original cost of $115 for a cash discount of $6 on the replacement property, resulting in a gain on disposal of $3. In the nine months ended March 31, 2014, the Company traded in property and equipment with an original cost of $72 for a cash discount of $4 on the replacement property, resulting in a gain on disposal of $4. Additionally, the Company disposed of fully depreciated property of $58 in the nine months ended March 31, 2015.

8

INTEGRATED BIOPHARMA, INC. AND SUBSIDIARIES

NOTES TO THE CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

(in thousands, except share and per share amounts)

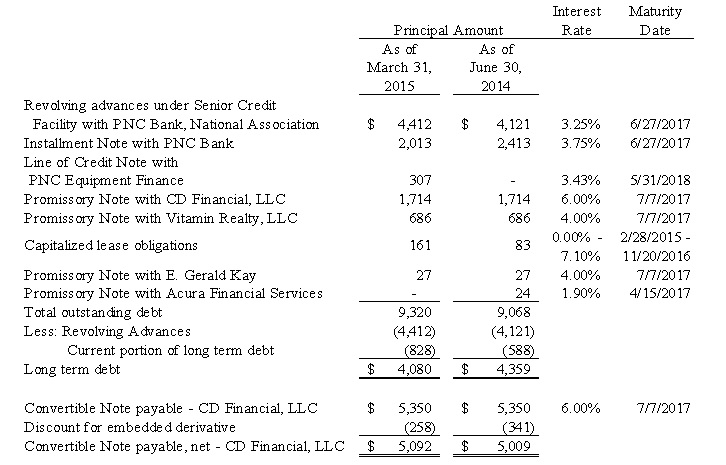

Note 5. Senior Credit Facility, Subordinated Convertible Note, net - CD Financial, LLC and other Long Term Debt

As of March 31, 2015 and June 30, 2014, the Company had the following debt outstanding:

SENIOR CREDIT FACILITY

On June 27, 2012, the Company, MDC, AgroLabs, IHT, IHT Properties Corp. (“IHT Properties”) and Vitamin Factory (collectively, the “Borrowers”) entered into a Revolving Credit, Term Loan and Security Agreement (the “Loan Agreement”) with PNC Bank, National Association as agent and lender (“PNC”) and the other lenders party thereto.

The Loan Agreement provides for a total of $11,727 in senior secured financing (the “Senior Credit Facility”) as follows: (i) discretionary advances (“Revolving Advances”) based on eligible accounts receivable and eligible inventory in the maximum amount of $8,000 (the “Revolving Credit Facility”) and (ii) a term loan in the amount of $3,727 (the “Term Loan”). The Senior Credit Facility is secured by all assets of the Borrowers, including, without limitation, machinery and equipment, real estate owned by IHT Properties, and common stock of iBio owned by the Company. Revolving Advances bear interest at PNC’s Base Rate or the Eurodollar Rate, at Borrowers’ option, plus 2.75% (3.25% as of March 31, 2015 and June 30, 2014). The Term Loan bears interest at PNC’s Base Rate or the Eurodollar Rate, at Borrowers’ option, plus 3.25% (3.75% as of March 31, 2015 and June 30, 2014). Upon and after the occurrence of any event of default under the Loan Agreement, and during the continuation thereof, interest shall be payable at the interest rate then applicable plus 2%. The Senior Credit Facility matures on June 27, 2017 (the “Senior Maturity Date”).

9

INTEGRATED BIOPHARMA, INC. AND SUBSIDIARIES

NOTES TO THE CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

(in thousands, except share and per share amounts)

The principal balance of the Revolving Advances is payable on the Senior Maturity Date, subject to acceleration, based upon a material adverse event clause, as defined, subjective accelerations for borrowing base reserves, as defined or upon the occurrence of any event of default under the Loan Agreement or earlier termination of the Loan Agreement pursuant to the terms thereof. The Term Loan shall be repaid in sixty (60) consecutive monthly installments of principal, the first fifty nine (59) of which shall be in the amount of $44, commencing on the first business day of August, 2012, and continuing on the first business day of each month thereafter, with a final payment of any unpaid balance of principal and interest payable on the first business day of July, 2017. The foregoing is subject to customary mandatory prepayment provisions and acceleration upon the occurrence of any event of default under the Loan Agreement or earlier termination of the Loan Agreement pursuant to the terms thereof.

The Revolving Advances are subject to the terms and conditions set forth in the Loan Agreement and are made in aggregate amounts at any time equal to the lesser of (x) $8.0 million or (y) an amount equal to the sum of: (i) up to 85%, subject to the provisions in the Loan Agreement, of eligible accounts receivables (“Receivables Advance Rate”), plus (ii) up to the lesser of (A) 65%, subject to the provisions in the Loan Agreement, of the value of the eligible inventory (“Inventory Advance Rate” and together with the Receivables Advance Rate, collectively, the “Advance Rates”), (B) 85% of the appraised net orderly liquidation value of eligible inventory (as evidenced by the most recent inventory appraisal reasonably satisfactory to PNC in its sole discretion exercised in good faith) and (C) the inventory sublimit in the aggregate at any one time (“Inventory Advance Rate” and together with the Receivables Advance Rate, collectively, the “Advance Rates”), minus (iii) the aggregate Maximum Undrawn Amount of all outstanding Letters of Credit, minus (iv) such reserves as Agent may reasonably deem proper and necessary from time to time.

The Loan Agreement contains customary mandatory prepayment provisions, including, without limitation, (i) the requirement that if the trading price per share of the iBio Stock falls below a certain amount, the Company must sell the iBio Stock and use the proceeds to repay the Term Loan and (ii) the requirement to prepay the outstanding amount of all loans in an amount equal to fifty percent (50%) of Excess Cash Flow for each fiscal year commencing with the fiscal year ending June 30, 2013, payable upon delivery of the financial statements to PNC referred to in and required by the Loan Agreement for such fiscal year but in any event not later than one hundred twenty (120) days after the end of each such fiscal year, which prepayment amount shall be applied ratably to the outstanding principal installments of the Term Loan in the inverse order of the maturities thereof until the aggregate amount of payments made with regard to the Term Loan pursuant to Loan Agreement equals $1.0 million. The Loan Agreement also contains customary representations and warranties, covenants and events of default, including, without limitation, (i) a fixed charge coverage ratio maintenance requirement and (ii) an event of default tied to any change of control as defined in the Loan Agreement. As of March 31, 2015, the Company was in compliance with the fixed charge coverage ratio maintenance requirement.

During certain periods in the fiscal years ended June 30, 2014 and 2013, the trading price of the iBio Stock was less than $0.88 for a period of fifteen (15) consecutive trading days and continued to have a trading price less than $0.88 during certain periods through April 8, 2015. However, PNC temporarily waived the requirement to sell the iBio Stock due to certain trading rules and restrictions under Rule 144 under the Securities Act of 1933, as amended. As of May 14, 2015, PNC has not required the Company to sell any of the iBio Stock but reserves the right to do so at any time in the future. Although not required to do so, on or about April 30, 2015, the Company sold 60,000 shares of iBio Stock, providing net trading proceeds of approximately $64 which proceeds were used to prepay principal outstanding under the Term Loan.

In October, 2013, when the Company delivered its annual financial statements for the fiscal year ended June 30, 2013 to PNC, as required under the Loan Agreement, the Company was required to make a prepayment in respect of loans outstanding under the Loan Agreement of approximately $293, representing 50% of Excess Cash Flows for the fiscal year ended June 30, 2013. This payment, along with the scheduled monthly principal payments of $44 made by the Company in respect of the Term Loan through November 1, 2013 provided for principal payments of $1.0 million in the aggregate.

10

INTEGRATED BIOPHARMA, INC. AND SUBSIDIARIES

NOTES TO THE CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

(in thousands, except share and per share amounts)

In connection with the Senior Credit Facility, each of E. Gerald Kay, an officer, director and major stockholder of the Company, and Carl DeSantis, a director and major stockholder of the Company and a member of CD Financial, LLC(“CD Financial”) (collectively, the “Guarantors”), entered into Continuing Limited Guarantees (collectively, the “Individual Guarantees”) with PNC whereby each Guarantor irrevocably and unconditionally guarantees the full, prompt and unconditional payment, when due, whether by acceleration or otherwise, of any and all obligations of the Borrowers under the Loan Agreement and the other loan documents. The liability of each Guarantor under his respective Individual Guarantee is limited to a maximum of $1.0 million. The Individual Guarantees automatically terminate upon the satisfaction of certain conditions set forth in the Loan Agreement. These conditions included the Company repaying an aggregate amount of $1.0 million of principal on the Term Loan and the Company meeting a minimum EBITDA, as defined in the Loan Agreement, of $1.5 million for the fiscal year ended June 30, 2013. The Company met these requirements on November 1, 2013 and Mr. DeSantis and Mr. Kay were released as guarantors under the Individual Guarantees.

Also, in connection with the Senior Credit Facility, PNC and CD Financial entered into the Intercreditor and Subordination Agreement (the “Intercreditor Agreement”), which was acknowledged by the Borrowers, pursuant to which, among other things, (a) the lien of CD Financial on assets of the Borrowers is subordinated to the lien of PNC on such assets during the effectiveness of the Senior Credit Facility, and (b) priorities for payment of the debt for the Company and its subsidiaries (as described in this Note 5) are established.

In addition, in connection with the Senior Credit Facility, the following loan documents were executed: (i) a Stock Pledge Agreement with PNC, pursuant to which the Company pledged to PNC the iBio Stock; (ii) a Mortgage and Security Agreement with PNC with IHT Properties; and (iii) an Environmental Indemnity Agreement with PNC.

CD FINANCIAL, LLC TROUBLED DEBT RESTRUCTURING

On June 27, 2012, the Company also entered into an Amended and Restated Securities Purchase Agreement (the “CD SPA”) with CD Financial, which amended and restated the Securities Purchase Agreement, dated as of February 21, 2008, between the Company and CD Financial, pursuant to which the Company issued to CD Financial a 9.5% Convertible Senior Secured Note in the original principal amount of $4,500 (the “Original CD Note”). Pursuant to the CD SPA, the Company issued to CD Financial (i) the Amended and Restated Convertible Promissory Note in the principal amount of $5,350 (the “CD Convertible Note”) and (ii) the Promissory Note in the principal amount of $1,714 (the “Liquidity Note”, and collectively with the CD Convertible Note, the “CD Notes”). The CD Notes mature on July 7, 2017.

The proceeds of the CD Notes were used to refinance (a) the Original CD Note, (b) a $300,000 note issued by MDC to CD Financial which was assigned by MDC to the Company, (c) past due interest in the aggregate amount of $333 and (d) other expenses owed to CD Financial by the Company in the aggregate amount of approximately $217.

The CD Notes are secured by all assets of the Borrowers, including, without limitation, machinery and equipment, real estate owned by IHT Properties, and iBio Stock owned by the Company. The CD Notes bear interest at an annual rate of 6% and have a default rate of 10%.

The CD Convertible Note is convertible at the option of CD Financial into common stock of the Company at a conversion price of $0.65 per share, subject to customary adjustments including conversion price protection provisions.

11

INTEGRATED BIOPHARMA, INC. AND SUBSIDIARIES

NOTES TO THE CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

(in thousands, except share and per share amounts)

Pursuant to the terms of the Loan Agreement and the Intercreditor Agreement, during the effectiveness of the Senior Credit Facility, (i) the principal of the CD Convertible Note may not be repaid, (ii) the principal of the Liquidity Note may only be repaid if certain conditions under the Loan Agreement are satisfied, and (iii) interest in respect of the CD Notes may only be paid if certain conditions under the Intercreditor Agreement are satisfied.

The CD SPA contains customary representations and warranties, covenants and events of default, including, without limitation, an event of default tied to any change of control as defined in the CD SPA.

In connection with the CD SPA, the Borrowers entered into an Amended and Restated Security Agreement and Amended and Restated Subsidiary Guaranty.

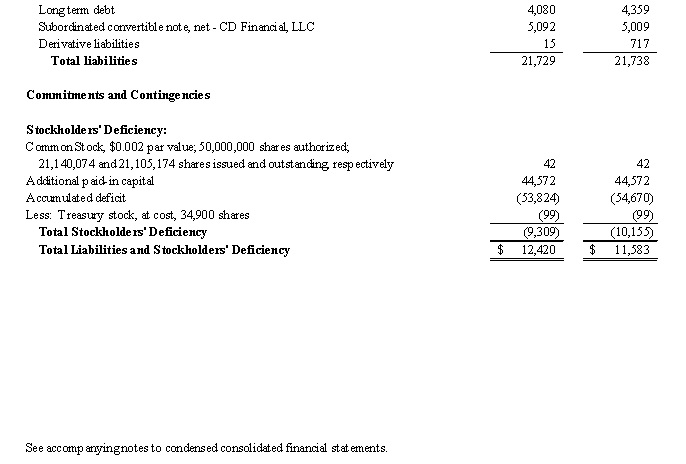

As of March 31, 2015 and June 30, 2014, the related embedded derivative liability with respect to conversion price protection provisions on the CD Convertible Note has an estimated fair value of $15 and $717, respectively.

The Company used the following assumptions to calculate the fair value of the derivative liability using the Black-Scholes option pricing model:

OTHER LONG TERM DEBT

Related Party Debt. On June 27, 2012, MDC and the Company entered into separate promissory notes with (i) Vitamin Realty Associates, LLC (“Vitamin Realty”), which is 100% owned by E. Gerald Kay, the Company’s Chairman of the Board, President and major shareholder and certain of his family members, who are also executive officers and directors of the Company, and (ii) E. Gerald Kay, in the principal amounts of approximately $686 (the “Vitamin Note”) and $27 (the “Kay Note”), respectively (collectively the “Related Party Notes”). The principal amount of the Vitamin Note represents the aggregate amount of unpaid, past due rent owing by MDC under the Lease Agreement, dated as of January 10, 1997, between MDC, as lessor, and Vitamin Realty, as landlord, pertaining to the real property located at 225 Long Avenue, Hillside, New Jersey. (See Note 7. Commitments and Contingencies (a) Leases – Related Party Leases). The Kay Note represents amounts owed to Mr. Kay for unreimbursed business expenses incurred by Mr. Kay in the fiscal year ended June 30, 2008. The Related Party Notes mature on July 7, 2017 and accrue interest at an annual rate of 4% per annum. Interest in respect of the Related Party Notes is payable on the first business day of each calendar month. Pursuant to the terms of the Loan Agreement, during the effectiveness of the Senior Credit Facility, the Related Party Notes may only be repaid or prepaid if certain conditions set forth in the Loan Agreement are satisfied.

Other Note Payable. On February 23, 2015, the Company satisfied the outstanding balance of approximately $19 with Acura Financial Services, Inc, (“Acura”), originally entered into on March 31, 2012 in the original amount of $41, under a trade in with Acura for a new auto vehicle with an operating lease with Acura. The loan was secured by an automobile and was set to mature on April 15, 2017. Interest and principal in the amount of less than $1 was payable monthly and had an interest rate of 1.9%.

12

INTEGRATED BIOPHARMA, INC. AND SUBSIDIARIES

NOTES TO THE CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

(in thousands, except share and per share amounts)

Capitalized Lease Obligations. On August 22, 2014, the Company entered into a capitalized lease obligation with Marlin Leasing in the amount of $47, which lease is secured by certain machinery and equipment and matures on August 28, 2016. The lease payment amount of approximately $2 is payable monthly and has an imputed interest rate of 5.6%.

On August 28, 2014, the Company entered into a capitalized lease obligation with Quantum Analytics in the amount of $138, which lease is secured by certain machinery and equipment and matures on February 27, 2016. The lease payment amount of approximately $8 is payable monthly and has an imputed interest rate of 0%.

On February 28, 2015, the capitalized lease obligation the Company entered into on March 5, 2013 with Marlin Leasing in the amount of $68, which lease was secured by certain machinery and equipment, was satisfied with all payments being made under the capitalized lease obligation. The monthly lease payment amount was approximately $2 and had an imputed interest rate of 7.1%.

Equipment Financing Note. On September 22, 2014, MDC entered into a Convertible Line of Credit Note (the “LC Note”) in the amount of $350 with PNC Equipment Finance, LLC (“PNCEF”). The LC Note is convertible into a term note upon completion of the advances under the LC Note. During the period from September 22, 2014 to and including the Conversion Date (defined below), the Company may borrow up to the full value of the LC Note ($350). The “Conversion Date” is the earliest to occur of (i) July 31, 2015 or (ii) the date when the Company notifies PNCEF that no more advances will be requested or (iii) the date when PNCEF has made advances in an aggregate amount of $350. As of March 31, 2015, the Company has requested and received advances under the LC Note in the amount of $307. Prior to the Conversion Date, amounts outstanding under the LC Note bear interest at a rate per annum (“Floating Rate”) which is at all times equal to the sum of LIBOR Rate plus 325 basis points (3.25%). As of March 31, 2015, the Floating Rate was approximately 3.43%. The Company is expecting to complete the advances no later than the fiscal quarter ending June 30, 2015 and convert the LC Note to a three year term note, at which time the Company will have the option to elect a fixed rate of interest as offered by PNCEF on the Conversion Date.

In addition, in connection with the LC Note, the following loan documents were executed: (i) a Security Agreement with PNCEF and MDC; (ii) a Guaranty and Security Agreement with PNCEF and the Company; and (iii) a Cross Collateralization Agreement with PNC, PNCEF and MDC.

Note 6. Significant Risks and Uncertainties

(a) Major Customers. For the three months ended March 31, 2015 and 2014, approximately 83% and 78%, respectively of consolidated net sales, were derived from two customers. These two customers are in the Company’s Contract Manufacturing Segment and represent approximately 37% and 56% and 58% and 30% of this Segment’s net sales in the three months ended March 31, 2015 and 2014, respectively. A third customer in the Branded Nutraceutical Segment, while not a significant customer of the Company’s consolidated net sales, represented approximately 82% and 15% of net sales in the three months ended March 31, 2015 and 2014, respectively, of the Branded Nutraceutical Segment.

For the nine months ended March 31, 2015 and 2014, approximately 83% and 80%, respectively of consolidated net sales, were derived from the same two customers. These two customers are in the Company’s Contract Manufacturing Segment and represent approximately 48% and 42% and 68% and 21% of this Segment’s net sales in the nine months ended March 31, 2015 and 2014, respectively. A third customer in the Branded Nutraceutical Segment, while not a significant customer of the Company’s consolidated net sales, represented approximately 79% and 52% of net sales in the nine months ended March 31, 2015 and 2014, respectively, of the Branded Nutraceutical Segment.

13

INTEGRATED BIOPHARMA, INC. AND SUBSIDIARIES

NOTES TO THE CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

(in thousands, except share and per share amounts)

Accounts receivable from major customers represented approximately 80% and 74% of total net accounts receivable as of March 31, 2015 and June 30, 2014, respectively. The loss of any of these customers could have an adverse affect on the Company’s operations. Major customers are those customers who account for more than 10% of net sales.

(b) Other Business Risks. Approximately 62% of the Company’s employees are covered by a union contract and are employed in its New Jersey facilities. The contract was renewed in May 2012 and expires in August 2015.

Note 7. Commitments and Contingencies

(a) Leases

Related Party Leases. Warehouse and office facilities are leased from Vitamin Realty, which is 100% owned by the Company’s chairman, president and major stockholder and certain of his family members, who are also executive officers and directors of the Company. On January 5, 2012, MDC, a wholly-owned subsidiary of the Company, entered into a second amendment of lease (the “Second Lease Amendment”) with Vitamin Realty for its office and warehouse space in New Jersey increasing its rentable square footage from an aggregate of 74,898 square feet to 76,161 square feet and extending the expiration date to January 31, 2026. This Second Lease Amendment provides for minimum annual rental payments of $533, plus increases in real estate taxes and building operating expenses. On May 19, 2014, AgroLabs entered into an Amendment to the lease agreement entered into on January 5, 2012, with Vitamin Realty for an additional 2,700 square feet of warehouse space in New Jersey, the term of which was to expire on January 31, 2019 to extend the expiration date to January 1, 2024. This additional lease provides for minimum lease payments of $27 with annual increases plus the proportionate share of operating expenses.

Rent expense for the three and nine months ended March 31, 2015 and 2014 on these leases were $223 and $215 and $637 and $622, respectively, and are included in both cost of sales and selling and administrative expenses in the accompanying Condensed Consolidated Statements of Operations. As of March 31, 2015 and June 30, 2014, the Company had an outstanding obligation to Vitamin Realty of $947 and $902, respectively, included in accounts payable, accrued expenses and other liabilities and long term debt in the accompanying Condensed Consolidated Balance Sheet.

Other Lease Commitments. The Company has entered into certain non-cancelable operating lease agreements expiring up through January 31, 2026, related to office and warehouse space, equipment and vehicles (inclusive of the related party lease with Vitamin Realty).

The minimum rental and lease commitments for long-term non-cancelable leases are as follows:

14

INTEGRATED BIOPHARMA, INC. AND SUBSIDIARIES

NOTES TO THE CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

(in thousands, except share and per share amounts)

Total rent expense, including real estate taxes and maintenance charges, was approximately $262 and $258 and $759 and $749 for the three and nine months ended March 31, 2015 and 2014, respectively. Rent expense is included in cost of sales and selling and administrative expenses in the accompanying Condensed Consolidated Statements of Operations.

(b) Legal Proceedings.

The Company is subject, from time to time, to claims by third parties under various legal theories. The defense of such claims, or any adverse outcome relating to any such claims, could have a material adverse effect on the Company’s liquidity, financial condition and cash flows.

(c) Other Claims.

On May 15, 2012, Cedarburg Pharmaceuticals, Inc. ("Cedarburg") sent the Company a letter (the "Demand Letter") setting forth a demand for indemnification under the Stock Purchase Agreement, dated March 17, 2009 (the "Cedarburg SPA"), by and among Cedarburg, InB: Hauser Pharmaceutical Services, Inc., InB: Paxis Pharmaceuticals, Inc. and the Company. In the Demand Letter, Cedarburg demanded payment by the Company of $0.6 million in respect of the Company's indemnification obligations under the Cedarburg SPA. In addition, in the Demand Letter, Cedarburg informed the Company that there are also environmental issues pending which may lead to additional costs to Cedarburg which will likely be in excess of $0.3 million.

On May 30, 2012, the Company sent a letter responding to the Demand Letter and setting forth the Company’s position that it has no obligation to indemnify Cedarburg as demanded. On June 18, 2012, Cedarburg responded to the Company’s letter and, on July 27, 2012, the Company sent another letter to Cedarburg reiterating its position that the Company has no obligation to indemnify Cedarburg as demanded. On December 18, 2012, Cedarburg responded to the Company’s letter and, on January 15, 2013, the Company sent another letter to Cedarburg reiterating its position that the Company has no obligation to indemnify Cedarburg as demanded. As of May 14, 2015, the Company has not received any further communication from Cedarburg with respect to its demand for indemnification as set forth in the Demand Letter. The Company intends to vigorously contest Cedarburg's demand as set forth in the Demand Letter.

Note 8. Related Party Transactions

On June 27, 2012, Carl DeSantis, a director and major shareholder of the Company and a member of CD Financial and E. Gerald Kay, the Company’s Chief Executive Officer, Chairman of the Board, President and a major shareholder each entered into Limited Guaranty Agreements with PNC in the amount of $1.0 million each. (See Note 5. Senior Credit Facility, Subordinated Convertible Note, net - CD Financial, LLC and other Long Term Debt).

Neither Mr. DeSantis nor Mr. Kay received any compensation from the Company in connection with these guarantees. The Individual Guarantees automatically terminated upon the satisfaction of certain conditions set forth in the Loan Agreement which included the Company repaying an aggregate amount of $1.0 million of principal on the Term Loan and the Company meeting a minimum EBITDA, as defined in the Loan Agreement, of $1.5 million for the fiscal year ended June 30, 2013. These two conditions were met by the Company on November 1, 2013 and Mr. DeSantis and Mr. Kay were released as guarantors under the Individual Guarantees.

See Note 5. Senior Credit Facility, Subordinated Convertible Note, net - CD Financial, LLC and other Long Term Debt for related party securities transactions.

See Note 7. Commitments and Contingencies (a) Leases – Related Party Leases.

15

INTEGRATED BIOPHARMA, INC. AND SUBSIDIARIES

NOTES TO THE CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

(in thousands, except share and per share amounts)

Note 9. Segment Information

The basis for presenting segment results generally is consistent with overall Company reporting. The Company reports information about its operating segments in accordance with GAAP which establishes standards for reporting information about a company’s operating segments.

The Company has divided its operations into three reportable segments as follows: Contract Manufacturing, Branded Proprietary Products and Other Nutraceutical Businesses. The international sales, concentrated primarily in Europe and Canada, for the three months ended March 31, 2015 and 2014 were $2,174 and $2,113, respectively and for the nine months ended March 31, 2015 and 2014 were $6,570 and $8,369, respectively.

Financial information relating to the three months ended March 31, 2015 and 2014 operations by business segment are as follows:

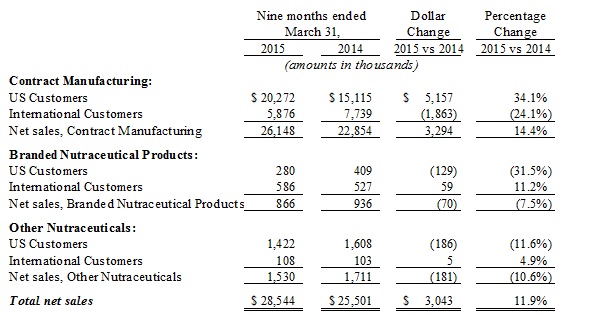

Financial information relating to the nine months ended March 31, 2015 and 2014 operations by business segment are as follows:

16

INTEGRATED BIOPHARMA, INC. AND SUBSIDIARIES

NOTES TO THE CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

(in thousands, except share and per share amounts)

17

Item 2. MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANICAL CONDITION AND RESULTS OF OPERATION

Certain statements set forth under this caption constitute “forward-looking statements.” See “Disclosure Regarding Forward-Looking Statements” on page 1 of this Quarterly Report on Form 10-Q for additional factors relating to such statements. The following discussion should also be read in conjunction with the condensed consolidated financial statements of the Company and Notes thereto included herein and the Company’s Annual Report on Form 10-K for the fiscal year ended June 30, 2014.

The Company is engaged primarily in the manufacturing, distributing, marketing and sales of vitamins, nutritional supplements and herbal products. The Company’s customers are located primarily in the United States, Luxembourg and Canada.

Business Outlook

Our future results of operations and the other forward-looking statements contained in this Quarterly Report on Form 10-Q, including this MD&A, involve a number of risks and uncertainties---in particular, the statements regarding our goals and strategies, new product introductions, plans to cultivate new businesses, pending divestitures, future economic conditions, revenue, pricing, gross margin and costs, the tax rate, and potential legal proceedings. We are focusing our efforts to improve operational efficiency and reduce spending that may have an impact on expense levels and gross margin. In addition to the various important factors discussed above, a number of other important factors could cause actual results to differ significantly from our expectations. See the risks described in “Risk Factors” in Part II, Item 1A of this Quarterly Report on Form 10-Q.

We continue to focus on our core businesses and maintaining our cost structure in line with our sales. Our selling and administrative expenses were lower in the nine months ended March 31, 2015, by $115,000, compared to the same period a year ago. This represents a decline of 4%, whereas our sales in the nine months ended March 31, 2015 increased approximately 12% compared to the nine months ended March 31, 2014. The increase of approximately $3.0 million was primarily in our Contract Manufacturing Segment of approximately $3.3 million, offset, by declines in sales in our other Segments aggregating approximately $0.3 million.

In our Contract Manufacturing Segment the increase is primarily the result of increased sales to a major customer, Life Extensions, in the amount of $6.2 million which was offset, in part, by decreased sales to our other major customer in this segment, Herbalife, of $2.9 million. Our sales to one of our largest customers has been adversely affected by currency controls in their Venezuelan business and product import controls in their Argentina business. At this time our customer does not expect the situation in either market to improve in the foreseeable future.

In our Branded Product Segment, we continue to maintain and strengthen the relationships developed in the fiscal year ended June 30, 2013, which were focused primarily in the international markets of Canada, Mexico and Asia. We are also developing new products, including branded products for solid dosage, which will be manufactured by MDC and sold using our AgroLabs brand. We believe that this will increase sales and further leverage our fixed manufacturing and selling costs in each of these segments as we diversify our branded product offerings to our existing and prospective customers. We forecasted that we would sell new items in our Canada market by the three month period ended September 30, 2014, however, due to delays in the approval process of the labels and other artwork as well as production schedules of our third party contractor, the sales of some of these new items shipped primarily in December 2014 and January 2015, others are expected to ship in our first quarter of 2016, as we were unable to have our product produced in time to meet our customer’s time slot. Although we are not expecting the dollar amount to be significant to our consolidated net sales, this segment was successful in introducing new products to its existing customer base which should result in additional exposure of the AgroLabs brand. For the nine months ended March 31, 2015, our net sales in the Branded Product Segment decreased by 8% and the margins on these sales decreased from approximately 11% to negative margins due to the nature of these sales, as they were primarily to liquidators at reduced margins in order to sell through expiring products in our inventory and the destruction of labels for product that the Company determined it would no longer offer for sale.

18

In the nine months ended March 31, 2015, our income from operations was approximately $0.9 million, which covered our debt service requirements and assisted us in continuing to improve our days past due to suppliers and to pay our vendors on a more timely basis than we had been able to in the past.

Critical Accounting Policies and Estimates

There have been no changes to our critical accounting policies in the nine months ended March 31, 2015. Critical accounting policies and the significant estimates made in accordance with them are regularly discussed by management with our Audit Committee. Those policies are discussed under “Critical Accounting Policies” in our “Management’s Discussion and Analysis of Financial Condition and Results of Operations” included in Item 7 of our Annual Report on Form 10-K for the year ended June 30, 2014.

Results of Operations

Our results from operations in the following table, sets forth the income statement data of our results as a percentage of net sales for the periods indicated:

19

For the Nine Months Ended March 31, 2015 compared to the Nine Months Ended March 31, 2014

Sales, net. Sales, net, for the nine months ended March 31, 2015 and 2014 were $28.5 million and $25.5million, respectively, an increase of 12%, and are comprised of the following:

For the nine months ended March 31, 2015 and 2014, a significant portion of our consolidated net sales, approximately 83% and 80%, respectively, were concentrated among two customers, Herbalife and Life Extensions, customers in our Contract Manufacturing Segment. Herbalife and Life Extensions represented approximately 48% and 42% and 68% and 21%, respectively, of our Contract Manufacturing Segment’s net sales in the nine months ended March 31, 2015 and 2014, respectively. The loss of any of these customers could have a significant adverse impact on our financial condition and results of operations. Costco Wholesale Corporation (“Costco”) (a customer of our Branded Proprietary Products Segment), while not a significant customer of our consolidated net sales, represented approximately 79% and 52% of net sales in the nine months ended March 31, 2015 and 2014, respectively of the Branded Nutraceutical Products Segment.

The increase in net sales of approximately $3.0 million was primarily the result of:

| · | Net sales increase in our Contract Manufacturing Segment by $3.3 million primarily due to increased sales volumes to one of our major customers, Life Extensions, in the nine months ended March 31, 2015, of approximately $6.2 million, offset in part by, a decrease in net sales volume to Herbalife of approximately $2.9 million (primarily in the international markets for Herbalife) compared to the comparable prior period. |

| · | Net sales in our Branded Nutraceutical Segment decreased by approximately $0.1 million in the nine months ended March 31, 2015, primarily as the result of the decreased sales volume of $0.3 million to customers other than Costco, which sales increased by $0.2 million. Other customer sales in this segment decreased by approximately $0.3 million as we were selling through short dated products at reduced pricing as well as being out of stock of our 3 ounce product until late December 2014. |

| · | Net sales in our Other Nutraceutical segments decreased by $0.2 million primarily as a result of decreased sales volumes to customers of IHT Health Products. |

Cost of sales. Cost of sales increased by $3.4 million to $25.1 million for the nine months ended March 31, 2015, as compared to $21.7 million for the nine months ended March 31, 2014. Cost of sales increased as a percentage of sales to 88% for the nine months ended March 31, 2015 as compared to 85% for the nine months ended March 31, 2014. The increase in the cost of sales amount, as well as the increase in the cost of sales as a percentage of net sales, was primarily the result of the increased sales to Life Extension. The cost of the raw materials for the Life Extension finished goods, on average, cost more per bottle than goods produced for our other customers in the Contract Manufacturing Segment as they tend to use raw materials with trademarked characteristics which limits the ability to negotiate pricing. A secondary cause is the production of more capsules than tablets. There is a higher loss factor in the production of capsules than in tablets. Our Contract Manufacturing Segment had a $3.5 million increase in the cost of sales with the Other Nutraceutical Businesses Segment decreasing by approximately $0.3 million (primarily as the result of decreased sales) offset by an increase in cost of sales of $0.1 million in the Branded Nutraceutical Products Segment (primarily the result of increased reserves for slow moving inventory).

20

Selling and Administrative Expenses. There was a decrease in selling and administrative expenses of $0.1 million or approximately 4% for the nine months ended March 31, 2015 to $2.6 million from $2.7 million for the nine months ended March 31, 2014. As a percentage of sales, net, selling and administrative expenses were 9.1% and 10.6% for the nine months ended March 31, 2015 and 2014, respectively. Our professional fees and salaries and employee benefits decreased in the nine months ended March 31, 2015 by approximately $56,000 and $41,000, respectively from the comparable nine month period ended March 31, 2014. Our professional fees decreased as a result of lower legal costs in the nine months ended March 31, 2015 compared to the nine months ended March 31, 2014. The decrease in salaries and employee benefits was primarily the result of changing the medical plans offered to employees that provided a lower monthly premium cost to us, as the employer, and to our employees.

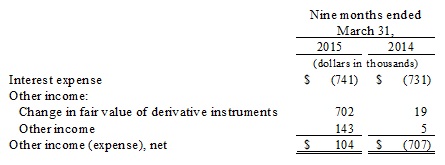

Other income (expense), net. Other income, net was approximately $0.1 million for the nine months ended March 31, 2015 compared to a net expense of $0.7 million for the nine months ended March 31, 2014, and is composed of:

The change in fair value of derivative instruments was mainly the result of the decrease in the trading price of our common stock from $0.25 as of June 30, 2014 to $0.08 as of March 31, 2015. The closing trading price of our stock is one of the variables used to calculate the estimated fair value of our derivative liabilities associated with the underlying derivative instruments. The change in other income is primarily the result of us recovering $0.1 million from a legal settlement involving certain vendors in our supply chain for the Branded Nutraceutical Segment.

Federal and state income tax, net. For each of the nine months ended March 31, 2015 and 2014, we had state tax expenses of approximately $0.1 million. We continue to maintain a full reserve on our deferred tax assets as it has been determined that based upon past losses, the Company’s past liquidity concerns and the current economic environment, that it is “more likely than not” the Company’s deferred tax assets may not be realized. The state tax expense is the result of MDC having state taxable income, all of our other subsidiaries still have adequate net operating losses for state income tax purposes to absorb any taxable income for state tax purposes.

Net income. Our net income for the nine months ended March 31, 2015 and 2014 was approximately $0.8 million and $0.2 million, respectively. The increase of approximately $0.6 million was primarily the result of the change in fair value of derivative instruments of approximately $0.7 million.

21

For the Three Months Ended March 31, 2015 compared to the Three Months Ended March 31, 2014

Sales, net. Sales, net, for the three months ended March 31, 2015 and 2014 were approximately $9.7 million and $7.5 million, respectively, an increase of 29%, and are comprised of the following:

For the three months ended March 31, 2015 and 2014 a significant portion of our consolidated net sales, approximately 83% and 78%, respectively, were concentrated among two customers, Herbalife and Life Extensions, customers in our Contract Manufacturing Segment. Herbalife and Life Extensions represented approximately 37% and 56% and 58% and 30%, respectively of our Contract Manufacturing Segment’s net sales in the three months ended March 31, 2015 and 2014, respectively. The loss of any of these customers could have a significant adverse impact on our financial condition and results of operations. Costco Wholesale Corporation (“Costco”) (a customer of our Branded Proprietary Products Segment), while not a significant customer of our consolidated net sales, represented approximately 82% and 15% of net sales in the three months ended March 31, 2015 and 2014, respectively of the Branded Propriety Products Segment.

The increase in net sales of approximately $2.1 million was primarily the result of:

| · | Net sales increased in our Contract Manufacturing Segment by approximately $1.9 million primarily due to increased sales volumes to one of our major customers, Life Extensions of approximately $2.8 million, offset by, in part, by a decrease in net sales volume to Herbalife of approximately $0.7 million (primarily in the international markets for Herbalife) in the three months ended March 31, 2015, compared to the comparable prior period. |

| · | Net sales in our Branded Nutraceutical Segment increased by approximately $0.2 million in the three months ended March 31, 2015, primarily as the result of the increased sales volume of $0.3 million to Costco. Other customer sales in this segment decreased by approximately $0.1 million as we were selling through short dated products at reduced pricing in the three month period ended March 31, 2014, with no comparable sales in the three months ended March 31, 2015. |

Cost of sales. Cost of sales increased by $2.0 million to $8.8 million for the three months ended March 31, 2015, from $6.8 million for the three months ended March 31, 2014. Cost of sales increased as a percentage of sales to 90.7% for the three months ended March 31, 2015 as compared to 90.3% for the three months ended March 31, 2014. The increase in the cost of goods sold amount, as well as the slight increase in the cost of sales as a percentage of sales, was primarily the result of the increased sales to Life Extension. The cost of the raw materials for the Life Extension finished goods, on average, cost more per bottle than goods produced for our other customers in the Contract Manufacturing Segment as they tend to use raw materials with trademarked characteristics which limits the ability to negotiate pricing. A secondary cause is the production of more capsules than tablets. There is a higher loss factor in the production of capsules than in tablets. Our Contract Manufacturing Segment had a $1.9 million increase in the cost of sales with the Branded Nutraceutical Segment increasing by $0.1 million (primarily as the result of increased sales and secondarily as the result of increased markdowns relating to expiring inventory and the disposal of packaging material that was deemed no longer usable).

22

Selling and Administrative Expenses. There was a slight decrease in selling and administrative expenses of $36,000 or 4% for the three months ended March 31, 2015 as compared to the three months ended March 31, 2014. As a percentage of sales, net, selling and administrative expenses were 9.2% and 12.3% for the three months ended March 31, 2015 and 2014, respectively. The significant changes in selling and administrative expenses from the three months ended March 31, 2014 to the three months ended March 31, 2015 were primarily from two expense categories, a decrease in professional and consulting fees of $70,000, offset in part, by an increase in advertising of $42,000. Our decrease in professional and consulting fees was the result of the lack of any significant legal matters to engage law firms to represent us in the three months ended March 31, 2015 compared to the three months ended March 31, 2014. The increase in advertising was in our Branded Nutraceutical Segment as we allocated funds to promote our products with Costco by placing an advertisement in their quarterly circular to their members, as well as placing a one page advertisement in one of the trade magazines in an effort to increase our brand exposure and to promote sales.

Other expense, net. Other expense, net was approximately $0.1 million and $0.2 million for the three months ended March 31, 2015 and 2014, respectively, and is composed of:

The change in other income is primarily the result of us recovering $0.1 million from a legal settlement involving certain vendors in our supply chain for the Branded Nutraceutical Segment.

Federal and state income tax, net. For the three months ended March 31, 2015 and 2014, we had a minimal amount of state income tax expenses, $24,000 and $27,000, respectively. We continue to maintain a full reserve on our deferred tax assets as it has been determined that based upon past losses, the Company’s past liquidity concerns and the current economic environment, that it is “more likely than not” the Company’s deferred tax assets may not be realized.

Net loss. Our net loss for the three months ended March 31, 2015 and 2014 was approximately $0.1 million and $0.5 million, respectively. The decrease of approximately $0.4 million was primarily from increased operating income of $0.2 million and the increase in other income of $0.1 million from the legal settlement described in other expense, net.

Seasonality

The nutraceutical business tends to be seasonal. We have found that in our first fiscal quarter ending on September 30th of each year, orders for our branded proprietary nutraceutical products usually slow (absent the addition of new customers or a new product launch with a significant first time order), as buyers in various markets may have purchased sufficient inventory to carry them through the summer months. Conversely, in our second fiscal quarter, ending on December 31st of each year, orders for our products increase as the demand for our branded nutraceutical products, as well as sales orders from our customers in our contract manufacturing segment, seems to increase in late December to early January as consumers become health conscious as they enter the new year.

23

The Company believes that there are other non-seasonal factors that may also influence the variability of quarterly results including, but not limited to, general economic and industry conditions that affect consumer spending, changing consumer demands and current news on nutritional supplements. Accordingly, a comparison of the Company’s results of operations from consecutive periods is not necessarily meaningful, and the Company’s results of operations for any period are not necessarily indicative of future periods.

Liquidity and Capital Resources

The following table sets forth, for the periods indicated, the Company’s net cash flows used in operating, investing and financing activities, its period end cash and cash equivalents and other operating measures:

At March 31, 2015 and June 30, 2014, our working capital deficit was approximately $2.5 million, with our current assets and liabilities each increasing by approximately $0.8 million.

Net cash provided by operating activities of $44,000 in the nine months ended March 31, 2015, includes net income of approximately $0.8 million. After excluding the effects of non-cash expenses, including depreciation and amortization, and changes in the fair value of derivative liabilities, the adjusted cash provided from operations before the effect of the changes in working capital components was $0.6 million. Cash was used in operations from our working capital assets and liabilities in the amount of approximately $0.6 million and was primarily the result of increases in accounts receivable of $0.6 million, inventories of $0.2 million and prepaid expenses and other assets of $0.1 million offset, in part, by a net decrease in accounts payable and accrued expenses and other liabilities of approximately $0.4 million.

Net cash provided by operating activities of 2.1 million in the nine months ended March 31, 2014, includes net loss of approximately $0.2 million. After excluding the effects of non-cash expenses, including depreciation and amortization, and changes in the fair value of derivative liabilities, the adjusted cash provided from operations before the effect of the changes in working capital components was $0.7 million. Cash was provided by operations from our working capital assets and liabilities in the amount of approximately $1.4 million and was primarily the result of decreases in accounts receivable of $0.5 million and inventories of $1.8 million offset, in part, by a decrease in accounts payable and accrued expenses and other liabilities of approximately $0.8 million.

Cash used in investing activities of $0.2 million and $0.1 million in the nine months ended March 31, 2015 and 2014, respectively, was for the purchase of property and equipment primarily in our contract manufacturing segment.

Net cash provided by financing activities was approximately $0.1million for the nine months ended March 31, 2015, $27.6 million from advances under our revolving credit facility and $0.3 million from proceeds under our convertible line of credit for equipment financing offset by repayments of advances under our revolving credit facility of $27.3 million, principal under our term notes in the amount of $0.4 million and payments under our capitalized lease obligations of $0.1 million.

24

Net cash used in financing activities was approximately $1.9 million for the nine months ended March 31, 2014, $25.3 million for payments under our revolving credit facility and repayments of principal under our term note in the amount of $0.7 million (including $0.3 million of principal prepaid, which represented 50% of Excess Cash Flows for the fiscal year ended June 30, 2013 as required under the term note with PNC), offset by advances under our revolving credit facility of $24.1 million.

As of March 31, 2015, we had cash of $0.4 million, funds available under our revolving credit facility of approximately $1.0 million and a working capital deficit of $2.5 million. Our working capital deficit includes $4.4 million outstanding under our revolving line of credit which is not due until July 2017 but classified as current due to a subjective acceleration clause that could cause the advances to become currently due. (See Note 5 to the condensed consolidated financial statements included in this Quarterly Report on Form 10-Q). Furthermore, we had income from operations of approximately $0.9 million in the nine months ended March 31, 2015. After taking into consideration our interim results and current projections, management believes that operations, together with the revolving credit facility will support our working capital requirements through the period ending March 31, 2016.

Our total annual commitments at March 31, 2015 for long term non-cancelable leases of approximately $0.6 million consists of obligations under operating leases for facilities and operating lease agreements for the rental of warehouse equipment, office equipment and automobiles.

On May 15, 2012, Cedarburg Pharmaceuticals, Inc. ("Cedarburg") sent us a letter (the "Demand Letter") setting forth a demand for indemnification under the Stock Purchase Agreement, dated March 17, 2009 (the "Cedarburg SPA"), by and among Cedarburg, InB: Hauser Pharmaceutical Services, Inc., InB: Paxis Pharmaceuticals, Inc. and the Company. In the Demand Letter, Cedarburg demanded payment by us of $0.6 million in respect of the Company's indemnification obligations under the Cedarburg SPA. In addition, in the Demand Letter, Cedarburg informed us that there are also environmental issues pending which may lead to additional costs to Cedarburg which will likely be in excess of $0.3 million.

On May 30, 2012, we sent a letter responding to the Demand Letter and setting forth our position that we have no obligation to indemnify Cedarburg as demanded. On June 18, 2012, Cedarburg responded to our letter and, on July 27, 2012, we sent another letter to Cedarburg reiterating our position that we have no obligation to indemnify Cedarburg as demanded. On December 18, 2012, Cedarburg responded to our letter and, on January 15, 2013, we sent another letter to Cedarburg reiterating our position that we have no obligation to indemnify Cedarburg as demanded. As of May 14, 2015, we have not received any further communication from Cedarburg with respect to its demand for indemnification as set forth in the Demand Letter. We intend to vigorously contest Cedarburg's demand as set forth in the Demand Letter.

Capital Expenditures

The Company's capital expenditures for the nine months ended March 31, 2015 and 2014 were approximately $413,000 ($169,000 funded with proceeds under our convertible line of credit for equipment financing and $185,000 funded with capitalized lease financing) and $191,000 ($76,000 funded with capitalized lease financing), respectively. The Company has budgeted approximately $0.5 million for capital expenditures for fiscal 2015. The total amount is expected to be funded from lease financing, financing under the Company’s equipment financing note (See Note 5 to the condensed consolidated financial statements included in this Quarterly Report on Form 10-Q) and from cash provided from the Company’s operations.

Off-Balance Sheet Arrangements

The Company has no off-balance sheet arrangements.

25

Recent Accounting Pronouncements

None.

Impact of Inflation

The Company does not believe that inflation has significantly affected its results of operations.

Item 3. QUANTITATIVE AND QUALITATIVE DISCLOSURES ABOUT MARKET RISK

Not applicable.

Item 4. CONTROLS AND PROCEDURES

Disclosure Controls and Procedures

Disclosure controls and procedures are controls and other procedures that are designed to ensure that information required to be disclosed by the Company in the reports it files or submits under the Securities Exchange Act of 1934, as amended (the “Exchange Act”) is recorded, processed, summarized, and reported within the time periods specified by the Commission’s rules and forms. Disclosure controls and procedures include, without limitation, controls and procedures designed to provide reasonable assurance that information required to be disclosed by the Company in the reports it files or submits under the Exchange Act is accumulated and communicated to management, including the Chief Executive Officer and Chief Financial Officer, as appropriate, to allow timely decisions regarding required disclosure.

Under the supervision and with the participation of management, including the Chief Executive Officer and Chief Financial Officer, the Company has evaluated the effectiveness of its disclosure controls and procedures (as such term is defined in Rule 13a-15(e) and 15d-15(e) under the Exchange Act) as of March 31, 2015, and, based upon this evaluation, the Chief Executive Officer and Chief Financial Officer have concluded that these controls and procedures are effective in providing reasonable assurance of compliance.

Changes in Internal Control over Financial Reporting

No change in our internal control over financial reporting occurred during the nine months ended March 31, 2015 that has materially affected, or is reasonably likely to materially affect, our internal control over financial reporting.

PART II – OTHER INFORMATION

Item 1. LEGAL PROCEEDINGS

None.

Item 1A. Risk Factors

The risks described in Item 1A, Risk Factors, in our Annual Report on Form 10-K for the year ended June 30, 2014, could materially and adversely affect our business, financial condition and results of operations. The risk factors discussed in that Form 10-K do not identify all risks that we face because our business operations could also be affected by additional factors that are not presently known to us or that we currently consider to be immaterial to our operations. There have been no material changes to our risk factors from those disclosed in our Form 10-K for the year ended June 30, 2014.

Item 2. UNREGISTERED SALES OF EQUITY SECURITIES AND USE OF PROCEEDS

None.

26

Item 3. DEFAULTS UPON SENIOR SECURITIES

None.

Item 4. MINE SAFETY DISCLOSURE

Not Applicable.

Item 5. OTHER INFORMATION

None.

Item 6. EXHIBITS

(a) Exhibits

Exhibit

Number

| 31.1 | Certification of pursuant to Section 302 of Section 302 of the Sarbanes-Oxley Act of 2002 by Chief Executive Officer. |

| 31.2 | Certification of pursuant to Section 302 of Section 302 of the Sarbanes-Oxley Act of 2002 by Chief Financial Officer. |

| 32.1 | Certification of periodic financial report pursuant to Section 906 of the Sarbanes-Oxley Act of 2002 by Chief Executive Officer. |

| 32.2 | Certification of periodic financial report pursuant to Section 906 of the Sarbanes-Oxley Act of 2002 by Chief Financial Officer. |

| 101 | The following financial information from Integrated BioPharma, Inc.’s Quarterly Report on Form 10-Q for the quarter ended March 31, 2015, formatted in XBRL (eXtensible Business Reporting Language): (i) Condensed Consolidated Statements of Operations for the three and nine months ended March 31, 2015 and 2014, (ii) Condensed Consolidated Balance Sheets as of March 31, 2015 and June 30, 2014, (iii) Condensed Consolidated Statements of Cash Flows for the nine months ended March 31, 2015 and 2014, and (iv) the Notes to Condensed Consolidated Statements. |

27

SIGNATURES

Pursuant to the requirements of Section 13 or 15(d) of the Securities Exchange Act of 1934, the Company has duly caused this report to be signed on its behalf by the undersigned thereunto duly authorized.

INTEGRATED BIOPHARMA, INC.

| Date: May 14, 2015 | By: /s/ E. Gerald Kay |

| | E. Gerald Kay, |

| | President and Chief Executive Officer |

| Date: May 14, 2015 | By: /s/ Dina L. Masi |

| | Dina L. Masi, |

| | Chief Financial Officer & Senior Vice President |

28