Cumberland Resources Ltd. is a well financed mineral development and exploration company which is positioning itself to become a mid-tier gold producer by developing the 100% owned Meadowbank gold project.

The Company has completed a bankable feasibility study on the project, establishing Canada’s largest pure gold open pit reserves. Meadowbank will be one of the largest and lowest cash cost gold mines in Canada and is designed to deliver an average of 330,000 ounces of gold annually for over 8 years. The project is in the final stages of environmental assessment and a production decision is anticipated in the third quarter of 2006.

The shares of Cumberland are traded on the Toronto Stock Exchange and American Stock Exchange under the symbol CLG.

This document contains "forward-looking statements", including, but not limited to, statements regarding our expectations as to the market price of gold, strategic plans, future commercial production, production targets and timetables, mine operating costs, capital expenditures, work programs, exploration budgets and mineral reserve and resource estimates. Forward-looking statements express, as at the date of this report, our plans, estimates, forecasts, projections, expectations or beliefs as to future events or results. We caution that forward-looking statements involve a number of risks and uncertainties, and there can be no assurance that such statements will prove to be accurate. Therefore, actual results and future events could differ materially from those anticipated in such statements. Factors that could cause results or events to differ materially from current expectations expressed or implied by the forward-looking statements include, but are not limite d to, factors associated with fluctuations in the market price of precious metals, mining industry risks and hazards, environmental risks and hazards, uncertainty as to calculation of mineral reserves and resources, requirement of additional financing, risks of delays in construction and other risks more fully described in our AIF filed with the Securities Commissions of the Provinces of British Columbia, Alberta, Ontario, Quebec and Nova Scotia and the Toronto Stock Exchange and in our 40-F filed with the United States Securities and Exchange Commission (the "SEC"). All dollars stated in Canadian currency unless otherwise noted.

M E A D O W B A N K G O L D P R O J E C T

2005 AND RECENT HIGHLIGHTS

Meadowbank Gold Project Achievements

- Completed feasibility study and positive bank due diligence for a project that is forecast to produce an average of 330,000 ounces of gold per year at an average cash cost of US$201 per ounce over an 8.1 year mine life. (Assumptions include a long term gold price of US$400/oz. and an exchange rate of US$0.75 per Cdn$1.00.)

- Advanced Meadowbank to the final stages of environmental review by submitting Final Environmental Impact Statement and completing public hearings.

- Signed a comprehensive Inuit Impact and Benefit Agreement with the Kivalliq Inuit Association as a requirement for development.

- Arranged a 420,000 ounce gold loan commitment which, subject to the satisfaction of certain conditions, will finance a major part of the initial construction costs at Meadowbank.

- Increased Canada's largest pure gold open pit reserves to 2.9 million ounces.

- Discovered a new zone of mineralization, the Cannu zone, and announced initial Cannu inferred resource of 85,000 ounces gold in April 2006.

- Completed a $7.4 million 2005 exploration, engineering and environmental program.

- Closed $5 million flow-through private placement in April 2006.

2006 Goals

- Secure project certificate from the Nunavut Impact Review Board.

- Make a production decision and start construction.

- Complete project financing.

- Continue to increase resources and reserves at Meadowbank by completing a $3.9 million 2006 exploration program.

Message to Shareholders

I am very pleased to report on Cumberland's activities across 2005 and early 2006. This has been a period of significant achievements by our experienced and disciplined team of explorers, financiers, builders and operators at Cumberland. Many of the necessary steps to develop Meadowbank into Canada's next large gold producer are now completed or within sight.

The Meadowbank bankable feasibility study was successfully concluded in early 2005. Scheduled for construction over the next several years it will emerge as one of Canada's largest gold producers, achieving up to 450,000 ounces of gold per year at peak production. Meadowbank's large, high grade open pit production profile will yield some of the lowest operating costs in the spectrum of Canadian gold mines. The feasibility also confirmed an open pit gold reserve which is the largest in Canada and is sufficient for a full eight years of production. Perhaps most importantly, the capital costs of development were estimated at $50 million below the guidance we provided a year prior. We owe this success to the skill and dedication of our mine engineering and design team.

Upon completion of the feasibility, our geology, engineering and financial teams guided Meadowbank through a successful due diligence audit conducted by bank appointed independent engineers. This audit was completed in late 2005 and in a rare turn of events the outcome actually improved the economics of the project and increased our gold reserves. Several months later we were pleased to announce the commitment of a 420,000 ounce gold loan from three major European banks. The gold loan is a simple and cost effective credit facility equating to a low percentage (15%) of our reserves and requires no incremental gold hedging during production. This credit facility is designed to provide a major part of the required funding to construct Meadowbank.

In the fall of 2005 we announced yet another discovery of gold mineralization at Meadowbank. In response, our exploration group extended the drilling season late into November in order to fast-track a resource estimate on the zone. In early 2006 we were pleased to report an inferred resource at Cannu, estimating an additional 85,000 ounces at a gold grade of 6.0 g/t - some 50% higher than the average reserve grade of 4.2 g/t gold at Meadowbank. The Cannu discovery is another example of the continuous exploration success we have had at Meadowbank. Since 1995 we have increased resources from just 200,000 ounces to our current estimate of 4.0 million ounces. The potential for more discoveries remains as strong as ever and our 2006 exploration efforts are now well underway.

We commenced negotiations of the Inuit Impact Benefit Agreement in mid 2005. After seven months of working with the Kivalliq Inuit Organization, we emerged with a comprehensive agreement which fully outlines the jobs, training, business opportunities and ancillary benefits the Inuit can expect from Meadowbank over the 12 years of construction, operations and closure. This is a landmark agreement and we believe it will provide substantial benefits to both parties in the years to come.

Also across 2005 our permitting team worked extremely hard to complete the necessary documentation and rigorous reviews for the environmental permitting process. In April of 2006, after a week of public and regulatory hearings, the impact review board asked us to clarify several issues. We have now provided this information to the impact review board - a final step in what we believe will be the completion of the permitting process.

In the spring of 2006 the Government of Nunavut announced a new fuel tax rebate program for mining companies. Meadowbank will rely on fossil fuels to generate power and with energy costs continually rising we warmly welcome this incentive. We worked hard in 2005 to support the fuel tax rebate and believe that the program demonstrates the Government of Nunavut's strong desire to stimulate investment in the development of its promising mining sector.

Cumberland ended the year in a strong financial position with a cash position of $27.9 million dollars. With a major part of mine development financing in place and the permitting process nearing completion, we are striving towards a production decision in the third quarter of 2006. Construction of Canada's newest open pit gold mine is scheduled for completion in late 2008 or early 2009 at which point both the value of the Company as a low cost mid-tier gold producer and its positive impact on the economy of Nunavut will be fully realized.

Cumberland strengthened its Meadowbank engineering and development team in 2005 with the addition of Raj Anand as Manager, Engineering, and Jim Koski as Manager, Construction.

Mr. Anand is a professional engineer with over twenty five years of experience in multidisciplinary project management of mining projects. He was with Homestake Mining Company for over seventeen years and was responsible for several projects including the Eskay Creek mine in British Columbia.

Mr. Koski has over 39 years of heavy construction experience primarily in the mine development field. He has management experience in numerous projects across Canada including the Golden Giant mine at Hemlo, Ontario, the Kemess South mine in British Columbia and the Winston Lake mine in Ontario.

I would like to thank the Board, management and especially our staff for their commitment and dedication to advancing Meadowbank towards production. I would also like to welcome our new shareholders and thank all shareholders for your continued support.

Kerry M. Curtis

President and Chief Executive Officer

June 2006

Significant Achievements at Meadowbank Position

Cumberland to Deliver Mid-Tier Gold Production

High Grade, Low Cost Production Profile

Cumberland is focused on advancing its 100% owned Meadowbank gold project, host to Canada's largest pure gold open pit reserves, towards mid-tier gold production. Open pit production is forecast at 330,000 ounces per year with total cash costs estimated at US$201 per ounce over an 8.1 year mine life based on a bankable feasibility study completed in December 2005. Meadowbank is located 70 kilometres north of the Hamlet of Baker Lake in the Kivalliq region of Nunavut, Canada.

Bank Due Diligence Improves Economics

The Meadowbank feasibility study was completed by AMEC Americas Ltd. in early 2005 and, as a requirement for bank financing, SRK Consulting (UK) Limited completed a due diligence audit of the feasibility study in December 2005. The resulting improved production profile comparison is highlighted below:

Meadowbank Gold Project Production Profile Comparison*

| AMEC Feasibility March 2005 | SRK Update December 2005 | |

Open Pit Mineral Reserve (Proven & Probable) | 2,768,000 ounces | 2,890,000 ounces | |

Metallurgical Recovery | 93.5% | 93.2% | |

Mine Throughput | 2.73 Mtpa | 2.73 Mtpa | |

Mine Life | 8.3 years | 8.1 years | |

| Average Annual Production Rate | |||

Years 1 to 4 | 376,000 ounces 316,000 ounces | 400,000 ounces 330,000 ounces | |

| Total Cash Cost per Oz. | |||

Years 1 to 4 | US$199 | US$175 | |

| Cash Flow(Undiscounted) | |||

Pre-tax | Cdn$232 million Cdn$154 million | Cdn$324 million Cdn$207 million | |

| Internal Rate of Return | |||

Pre-tax | 14.3% | 17.6% | |

Pre-production Capital Costs | US$227 million Cdn$302 million | US$235 million Cdn$313 million | |

*SRK assumptions remain unchanged from the AMEC feasibility and include 100% equity financing, a long term gold price of US$400/oz. and an exchange rate of US$0.75 per Cdn$1.00. The feasibility study was prepared in accordance with the Standards of Disclosure for Mineral Projects as defined by National Instrument 43-101.

Robust Economics* Improve with Canadian Gold Price, Cash Flow Analysis with Varying Gold Price (Pre-tax, Cdn$) |  |

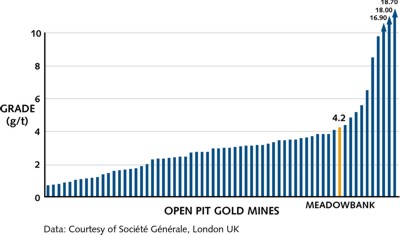

Canada's Largest Pure Gold Open Pit Reserves Increase Further

The most significant improvement from the SRK due diligence is a gold reserve increase at Meadowbank of approximately 120,000 ounces. This is largely due to grade capping adjustments that resulted in an increase in the proven and probable mineral reserve to 2.9 million ounces. The corresponding grade increase also reduced the base case total cash cost (as defined by the Gold Institute standard) by US$23 per ounce to an average US$201 per ounce for the life of operations.

The revised proven and probable open pit mineral reserve estimate for the three open pits is highlighted below:

Open Pit | Ore (t) | Au Grade (g/t) | Contained Ounces |

Portage | 11,010,000 | 4.5 | 1,590,000 |

Vault | 8,010,000 | 3.4 | 870,000 |

Goose | 2,310,000 | 5.7 | 420,000 |

Total | 21,320,000 | 4.2 | 2,890,000 |

The reserves (fourth quarter 2005) have been prepared in accordance with NI 43-101. Dr. Mike Armitage, Managing Director of SRK Consulting (UK) Limited, is the independent Qualified Person responsible for preparation of stated reserves. | |||

|

World Open Pit Gold Mines, |

Gold Loan Commitment Estimated at $250 Million Provides a Major Part of Required Financing

After the extensive independent due diligence process completed in 2005, a gold loan facility for up to 420,000 ounces of gold from a group of three European banks (Barclays Capital, Bayerische Hypo-und Vereinsbank and Societe Generale) was arranged in March 2006. The gold loan commitment represents only 15% of Meadowbank's reserves and will not require incremental production hedging. If monetized at a Cdn$600 per ounce spot gold price, the value of the gold loan will be $250 million, representing approximately 80% of the estimated initial capital ($313 million) required to develop the project. The gold loan commitment is subject to the satisfaction of certain conditions including, among other things, Cumberland securing all requisite regulatory permits and licences and completion of final loan documentation.

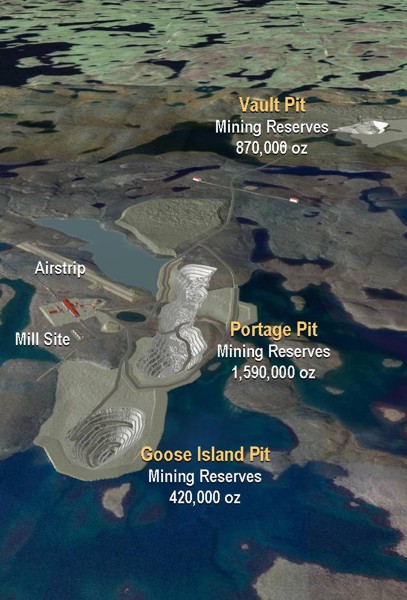

2005 Meadowbank Feasibility Mine Plan The Meadowbank project is located 70 kilometres north of the community of Baker Lake. The project site is at 134 metre elevation in low lying topography with numerous lakes. With a typical Arctic climate, the site experiences a wide range of average annual temperatures and low annual precipitation. Conventional Open Pit Mining Three open pits are proposed at Meadowbank: Portage, Goose Island and Vault. The high grade ores from the Portage and Goose Island pits will be mined in the first four years allowing production to average at 400,000 ounces over the first four years of operations. Peak production is achieved in Year 1 with 451,000 ounces forecast to be produced from the Portage pit. Ore will be extracted conventionally using drilling and blasting with truck haulage to a primary crusher located adjacent to the mill. Waste rock will be hauled to one of two waste storage areas on the property, used for dike construction or stored in selective areas of the open pits that have previously been mined out. Waste material from the pre-stripping will be used as bulk construction materials for dike construction, as well as for construction fill material around the site. Conventional Gold Ore Processing The Meadowbank process plant is designed to operate 365 days per year with a design capacity of 7,500 tonnes of ore per day (2.73 million tonnes per year) resulting in gold production averaging 330,000 ounces per year over the 8.1 year mine life. The conventional design of mill processing will consist of primary gyratory crushing, grinding, gravity concentration, leaching and gold recovery in a carbon-in-pulp circuit. Gold recovery is forecast at 93.2% with approximately 40% recovered in the gravity circuit. Conventional Access Road The proposed 115 kilometre long conventional access road will connect the Meadowbank project to the community of Baker Lake. Conventional road access, compared to winter road access, extends the access season, reduces on-site infrastructure requirements, improves efficiencies in construction scheduling and reduces overall operating costs. |  |

|  |

| Generations of Cold Climate Experience, Traditional Knowledge is a Component of Mine Design | Airstrip Construction in 2005, Commenced Construction of Primary Infrastructure |

Cumberland's Commitment to the Environment and Nunavut Advances Meadowbank Permitting to Final Stages

Environmental Permitting Moves to Final Stages

The development of the Meadowbank project is being reviewed by the Nunavut Impact Review Board ("NIRB"), the lead authorizing agency, as provided under the Nunavut Land Claims Agreement. In November 2005 the Company submitted the Final Environmental Impact Statement and final public hearings were held at the end of March 2006.

In April 2006 the NIRB requested further information related to the all weather road, socio-economic impacts and suggested further consultation with the residents of nearby Chesterfield Inlet. In early June the Company provided the NIRB with the requested information. To complete the environmental impact review the NIRB will submit its recommendation and report to the Federal Minister of Indian and Northern Affairs Canada (INAC) for approval of the project certificate.

Commitment to the Inuit is Formalized

Cumberland and the Kivalliq Inuit Association signed a comprehensive Inuit Impact and Benefit Agreement ("IIBA") during early 2006. As a requirement for development, the IIBA ensures that local employment, training and business opportunities arising from all phases of development, operation and closure of the Meadowbank project are accessible to the Kivalliq Inuit.

Support from the Government of Nunavut

In early 2006 the Government of Nunavut announced a fuel tax rebate for the mining sector. This initiative will provide a substantial economic benefit to the Meadowbank project and demonstrates the commitment of the Government of Nunavut to attract mineral development.

Cumberland Dedicated to Advancing Meadowbank Towards Production

Nearing a Production Decision and Construction

Cumberland will make a Meadowbank production decision following the NIRB's recommendation to the INAC. Initial equipment and supplies are in place to build fuel storage tanks and construction of an airstrip at site commenced in 2005. Cumberland will obtain water licences before road construction and plant construction begin. Depending on receipt of permits and licences, operations from three, shallow open pits could commence in late 2008 or early 2009.

Ongoing Exploration for Continued Resource and Reserve Growth at Meadowbank

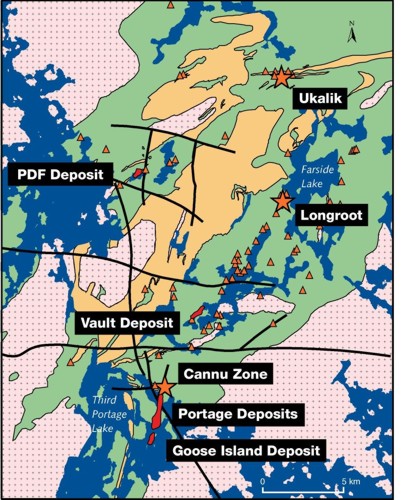

2005 Drilling Program Discovers New High Grade, Near Surface Cannu Zone

Cumberland completed 11,700 metres of drilling in three phases at Meadowbank in 2005. The Phase I and Phase II programs expanded the size of the Goose Island deposit, intersected encouraging mineralization in the Goose Island South area and discovered the Cannu zone. The Cannu zone, a zone of high grade, near surface gold mineralization, represents the potential northward extension of the mineralization delineated in the proposed Portage open pit. Follow up drilling during the Phase II and expanded Phase III drill programs outlined the Cannu zone mineralization along a 350 metre strike length.

|

2005 Cannu Discovery and Initial Inferred Resource, |

New Mineral Resource at Cannu Zone

A total of 30 holes were completed at the new Cannu zone in 2005 and an initial resource estimate for the zone was prepared by SRK in April 2006. The estimate is based on 64 intersections in 34 drill holes (including four pre-2005 holes) and, as with previously released Meadowbank resource estimates, utilizes three dimensional block models interpolated using inverse distance methods:

Cannu Zone Mineral Resource (April 2006)

Resource Category | Tonnes | AU Grade (g/t) | Contained Ouunces |

Inferred | 440,000 | 6.0 | 85,000 |

The inferred mineral resource estimate was prepared in conformance with the requirements set out in NI 43-101 under the direction of Dr. Mike Armitage, Managing Director of SRK Consulting (UK) Limited, who is an independent Qualified Person as defined by NI 43-101. The Cannu zone resource is not included in the feasibility study of the Meadowbank project.

2006 Exploration Focuses on Cannu Zone and Targets

A $3.9 million 2006 exploration program commenced at Meadowbank in April 2006. The two phased program, including approximately 9,000 metres of diamond drilling, is focused on increasing gold resources and reserves at the Cannu zone and other targets along the 25 kilometre Meadowbank gold trend.

Exploration at Cannu includes both infill and step-out drilling to define the extent of the mineralization and enable a reserve estimate. Additional drilling at Meadowbank in 2006 will focus on previously-defined mineralization south of the Goose Island deposit and drill testing of the Ukalik prospect north of the Vault deposit.

| Prolific Archean Greenstone Belt with |

| |

Continous Resource Growth, |  |

Meliadine Gold Projects

The Meliadine projects are located 20 kilometres north of Rankin Inlet, Nunavut. The area is divided into two projects - Meliadine West and Meliadine East.

Meliadine West Project

Cumberland holds a 22% (carried to production) interest in the Meliadine West project. Comaplex Minerals Corp. is the Operator of the project. Cumberland received an annual option payment of $1.5 million from the Operator in January 2006 in accordance with the joint venture agreement signed in 1995. Beginning in January 2007, the annual option payment of $1.5 million will be adjusted upward pursuant to an annual Consumer Price Index formula.

Drilling by Comaplex in 2005 indicated that the Tiriganiaq Main and Western Deeps zones are likely part of the same ore body and mineralized lodes are continuous between the two areas. A resource estimate, which includes these two zones as one deposit, was undertaken to examine the potential of the deposit to support a combined underground and open pit operation.

Comaplex estimated in January 2006 that the Tiriganiaq deposit contained gold resources of approximately 1,192,000 ounces of indicated resources and 1,552,000 ounces of inferred resources. The resource estimate does not include satellite deposits on the property.

Meliadine East Project

Cumberland has a 50% joint venture interest with partner Comaplex Minerals Corp. on the Meliadine East project. Cumberland is Operator of the project. A small program of mapping and prospecting was completed in 2005.

G O L D R E S E R V E S & R E S O U R C E S

GOLD RESERVES

Meadowbank Gold Project (100% interest)

Proven and probable mineral reserves are a subset of measured and indicated mineral resources.

Meadowbank mineral Reserves (Proven & Probable) (Fourth Quarter 2005)1

Open Pit | Reserve | Ore | Au | Cumberland |

Portage | Proven | 3,020,000 | 4.8 | 470,000 |

| Probable | 7,990,000 | 4.4 | 1,120,000 |

| Proven & Probable | 11,010,000 | 4.5 | 1,590,000 |

Vault | Proven | - | - | - |

| Probable | 8,010,000 | 3.4 | 870,000 |

| Proven & Probable | 8,010,000 | 3.4 | 870,000 |

Goose Island | Proven | - | - | - |

| Probable | 2,310,000 | 5.7 | 420,000 |

| Proven & Probable | 2,310,000 | 5.7 | 420,000 |

Total | Proven | 3,020,000 | 4.8 | 470,000 |

| Probable | 18,300,000 | 4.1 | 2,420,000 |

Proven & Probable | 21,320,000 | 4.2 | 2,890,000 | |

Note: 95% mining recovery and contact dilution applied.

GOLD RESOURCES

Meadowbank Gold Project (100% interest)

Meadowbank Mineral resources (Fourth Quarter 2005) 2

Open Pit | Resource Category | Tonnes | Au | Cumberland Contained Ounces |

Portage | Measured | 2,790,000 | 5.4 | 480,000 |

(1.5 g/t cutoff) | Indicated | 8,550,000 | 5.0 | 1,370,000 |

| Sub-Total | 11,340,000 | 5.1 | 1,850,000 |

| Inferred | 600,000 | 4.8 | 90,000 |

Vault | Measured | - | - | - |

(2.0 g/t cutoff) | Indicated | 8,610,000 | 3.9 | 1,080,000 |

| Sub-Total | 8,610,000 | 3.9 | 1,080,000 |

| Inferred | 870,000 | 5.4 | 150,000 |

Goose Island | Measured | - | - | - |

(1.5 g/t cutoff) | Indicated | 2,240,000 | 6.5 | 470,000 |

| Sub-Total | 2,240,000 | 6.5 | 470,000 |

| Inferred | 1,370,000 | 4.2 | 190,000 |

Total | Measured | 2,790,000 | 5.4 | 480,000 |

| Indicated | 19,400,000 | 4.7 | 2,920,000 |

| Sub-Total | 22,190,000 | 4.8 | 3,400,000 |

Inferred | 2,840,000 | 4.7 | 430,000 | |

Meadowbank mineral Resources not Invluded in Feasibility Study

| Resource | Tonnes | Au | Cumberland |

PDF Deposit 3 | Inferred | 507,000 | 4.5 | 73,000 |

Cannu Zone 4 | Inferred | 440,000 | 6.0 | 85,000 |

Meliadine West Gold Project (22% carried to production interest)

Meliadine West Mineral Resource from Comaplex Minerals Corp., January 2006 3

Tiriganiaq | Resource | Tonnes | Au | 100% | Cumberland |

| Indicated

| 4,200,000 507,000 | 7.5 11.3 | 1,009,000 184,000 | 222,000 40,000 |

Inferred | 3,244,000 3,188,000 | 4.1 10.9 | 432,000 1,120,000 | 95,000 246,000 | |

Meliadine East Gold Project (50% operating interest)

Meliadine East Mineral Resources 4

Deposit | Resource | Tonnes | Au | 100% | Cumberland |

Discovery | Indicated | 1,841,000 | 6.7 | 397,000 | 198,000 |

Cautionary Note to U.S. Investors - The SEC permits U.S. mining companies, in their filings with the SEC, to disclose only those mineral deposits that a company can economically and legally extract or produce. We use certain terms in this document such as “measured”, “indicated” and “inferred” “resources” that the SEC guidelines strictly prohibit U.S. registered companies from including in their filings with the SEC. U.S. investors are urged to consider closely the disclosure in our Form 40-F, which is available from us at Suite 950 – 505 Burrard Street, Vancouver, B.C. V7X 1M4. You can also obtain this form from the SEC’s website at: http://sec.gov/edgar.shtml.

Cautionary Note to U.S. Investors concerning estimates of Measured and Indicated Resources – This document uses the terms “measured” and “indicated resources”. We advise U.S. investors that while those terms are recognized and required by Canadian regulations, the SEC does not recognize them. U.S. investors are cautioned not to assume that any part or all of mineral deposits in these categories will ever be converted into mineral reserves.

Cautionary Note to U.S. Investors concerning estimates of Inferred Resources – This document uses the term “inferred resources”. We advise U.S. investors that while this term is recognized and required by Canadian regulations, the SEC does not recognize it. “Inferred resources” have a great amount of uncertainty as to their existence, and great uncertainty as to their economic and legal feasibility. It cannot be assumed that all or any part of an Inferred Resource will ever be upgraded to a higher category. Under Canadian rules, estimates of Inferred Resources may not form the basis of feasibility or pre-feasibility studies, except in rare cases. U.S. investors are cautioned not to assume that part or all of an inferred resource exists, or is economically or legally mineable.

Cautionary Note to U.S. Investors concerning estimates of Proven and Probable Reserves - The estimates of mineral reserves described in this document have been prepared in accordance with Canadian National Instrument 43-101. The definitions of proven and probable reserves used in NI 43-101 differ from the definitions in SEC Industry Guide 7. Accordingly, the Company’s disclosure of mineral reserves in this document may not be comparable to information from U.S. companies subject to the SEC’s reporting and disclosure requirements.

1 Meadowbank Gold Reserves (Fourth Quarter 2005) – The open pit mineral reserves have been prepared in accordance with NI 43-101. Dr. Mike Armitage, Managing Director of SRK Consulting (UK) Limited, is the independent Qualified Person responsible for preparation of stated reserves.

2 Meadowbank Gold Resources (Fourth Quarter 2005) - The resource estimates were prepared in conformance with the requirements set out in NI 43-101 under the direction of Dr. Mike Armitage, Managing Director of SRK Consulting (UK) Limited, who is an independent Qualified Person as defined by NI 43-101.

3 PDF deposit gold resources (August 2000) – The estimateswere prepared by Cumberland in accordance with standards outlined in National Instrument 43-101 and CIM Standards on Mineral Resources and Reserves (August 2000). James McCrea, P.Geo., Manager, Mineral Resources for Cumberland, is the Qualified Person under NI 43-101. PDF deposit resources are not included in the feasibility study of the Meadowbank project.

4 Cannu zone gold resource (April 2006) - The inferred mineral resource estimate was prepared in conformance with the requirements set out in NI 43-101 under the direction of Dr. Mike Armitage, Managing Director of SRK Consulting (UK) Limited, who is an independent Qualified Person as defined by NI 43-101. The Cannu zone resource is not included in the feasibility study of the Meadowbank project.

5 Meliadine West Gold Resources (January 2006) – The resource estimate was completed by Snowden Mining Industry Consultants of Vancouver on Comaplex Minerals’ Tiriganiaq gold deposit. The resource estimate does not include satellite deposits on the property.

6 Meliadine East Gold Resources - Resources estimated (1997) by MRDI Canada, a division of AMEC E&C Services Limited. Resource classification conforms to CIM Standards on Mineral Resources and Reserves (August 2000).

Cumberland Resources Ltd.

Management’s Discussion and Analysis of Financial Condition and Results of Operations

For the year ended December 31, 2005

INTRODUCTION

This Management Discussion and Analysis (“MD&A”) provides a detailed analysis of the business of Cumberland Resources Ltd. (“Cumberland” or the “Company”) and compares its 2005 financial results to the previous two years. This MD&A should be read in conjunction with the Company’s audited consolidated financial statements for the year-ended December 31, 2005 (the “Financial Statements”). The Company’s reporting currency is the Canadian dollar and all amounts in this MD&A are expressed in Canadian dollars, unless otherwise noted. The Company reports its financial position, results of operations and cash-flows in accordance with Canadian generally accepted accounting principles (“Canadian GAAP”). Differences between Canadian and United States generally accepted accounting principles that would affect the Company’s reported financial results are disclosed in Note 15 of the Financial Statements. This MD&A is made as of March 30, 2006.

This MD&A contains certain statements which may constitute “forward-looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995 of the United States. Forward-looking statements include, but are not limited to, statements regarding mine development programs, mineral resource estimates and statements that describe the Company’s future plans, objectives or goals. Forward-looking statements involve various known and unknown risks and uncertainties, which may cause actual results, performance and achievements of the Company to be materially different from any future results, performance or achievements expressed or implied by such statements. As a result, readers are cautioned not to place undue reliance on these forward-looking statements that speak only as of their respective dates. Important factors that could cause actual results to differ materially from the Company’ ;s expectations include results of mine permitting activities, future gold prices, future prices of fuel, steel and other construction items, as well as other risk factors described under the heading “Risk Factors” in the Company’s most recent Annual Information Form.

Additional information relating to Cumberland, including the Company’s Annual Information Form, is available on SEDAR atwww.sedar.com.

TABLE OF CONTENTS

1.

Summary of Recent Activities and Business Outlook

2.

Business Overview

3.

Review of Financial Results

4.

Liquidity and Capital Resources

5.

Financial Outlook

6.

Foreign Currency, Interest Rate and Commodity Price Risk

7.

Disclosure Controls and Procedures

8.

Outstanding Share Data

9.

Risk Factors

1. SUMMARY OF RECENT ACTIVITIES AND BUSINESS OUTLOOK

The Meadowbank Feasibility Study

In the first quarter of 2005 the Company announced the results from the Feasibility Study (“Study”) on the Company’s 100% owned Meadowbank Gold Project located in Nunavut, Canada. The results of the Study are summarized in the Technical Report prepared by AMEC Americas Ltd. in accordance with National Instrument 43-101 and filed on SEDAR on March 31, 2005. The Study incorporates improvements to the Meadowbank mine model as a result of a re-design completed in 2004 by the Company and the study manager, AMEC, including increased annual production and mill throughput, changes to open pit scheduling, and a proposed conventional access road to connect the project to the community of Baker Lake.

As a requirement of bank financing, bank-appointed independent engineers SRK Consulting (UK) Limited (“SRK”) completed a due diligence audit of the Study in December 2005. SRK reviewed all technical aspects of the Study. The Company updated the Feasibility Study financial model for the findings of the SRK audit and announced improvements to the project’s economics in December 2005. The financial projections assume a long term gold price of US$400/oz., an exchange rate of US$0.75 per Cdn$1.00, and full equity financing.

Meadowbank Gold Project (December 2005 update)*

(assuming US$400/oz. gold, and US$0.75 per Cdn$1.00)

Open Pit Mineral Reserve (Proven & Probable)** | 2,890,000 ounces |

Average Life of Mine Recovery Rate | 93.2% |

Mine Life | 8.1 years |

Average Annual Production Rate Years 1 to 4 Life of Mine |

330,000 ounces |

Total Cash Cost per Oz. Years 1 to 4 Life of Mine |

US$201 |

Pre-tax Net Present Value @ 0% After-tax Net Present Value @ 0% | US$243 million US$155 million |

Pre-tax Internal Rate of Return After-tax Internal Rate of Return | 17.6% 12.8% |

Pre-production Capital Costs | $313 million |

Payback Period | 3.8 years |

Cautionary Note to U.S. Investors concerning estimates of Proven and Probable Reserves - The estimates of mineral reserves described in this MD&A have been prepared in accordance with Canadian National Instrument 43-101. The definitions of proven and probable reserves used in NI 43-101 differ from the definitions in SEC Guide 7. Accordingly, the Company’s disclosure of mineral reserves in this MD&A may not be comparable to information from U.S. companies subject to the SEC’s reporting and disclosure requirements.

* Meadowbank Feasibility Study Due Diligence (December 2005) – As a requirement of bank financing, bank-appointed independent engineers SRK completed a due diligence audit of the Meadowbank feasibility study completed in early 2005 by AMEC Americas Ltd. (“AMEC”). The results from the feasibility study by AMEC are summarized in a Technical Report, dated March 31, 2005, prepared by AMEC in accordance with the Standards of Disclosure for Mineral Projects as defined by National Instrument 43-101. Construction scheduling and capital cost estimation has been prepared by Merit International Consultants Inc. (“Merit”). Metallurgical and process test work was completed by SGS Lakefield Research Ltd. Process design was completed by International Metallurgical and Environmental Inc. and AMEC. Supporting geotechnical engineering, hydrogeological and geochemical studies were completed by Golder Associates Ltd. (“Golder”). Both the SRK and AMEC assumptions include a long term gold price of US$400/oz. and an exchange rate of US$0.75 per Cdn$1.00.

** Meadowbank Gold Reserves (First Quarter 2005) - The open pit mineral reserves have been prepared in accordance with NI 43-101. Dr. Mike Armitage, Managing Director of SRK (the bank appointed independent engineer) is the independent Qualified Person responsible for preparation of stated reserves.

Meadowbank exploration

The Company completed 11,700 metres of drilling at Meadowbank in 2005 in three phases. The Phase I and Phase II exploration programs were successful in expanding the size of the Goose Island deposit, intersected encouraging mineralization in the Goose Island South area, and resulted in the discovery of the new Cannu zone. The Cannu zone represents the potential northward extension of the mineralization delineated in the proposed Portage open pit. A Phase III drill program, which was undertaken to assess the expansion potential of the Cannu zone, returned additional high grade, near surface gold mineralization which appears to indicate the continuous nature of the Cannu mineralization.

The Company has planned a $3.9 million (9,000 metres) drilling program for 2006, which will commence in late March. The two phase exploration program will focus on defining gold resources and reserves at the Cannu zone and exploring other targets along the 25 kilometre Meadowbank gold trend.

Environmental Permitting & Inuit Impact Benefit Agreement

The development of the Meadowbank Project is being reviewed by the Nunavut Impact Review Board (“NIRB”) as provided under the Nunavut Land Claims Agreement. The NIRB has reviewed the Company’s Draft Environmental Impact Study and, in May 2005, advanced the project from a conformity review to a technical review. The Company participated in pre-hearing conferences with the NIRB in June 2005. In July 2005, the Company received the NIRB’s Pre-Hearing Decision Report. The Company submitted the Final Environmental Impact Statement (“Final EIS”) to the NIRB in early November. The Final EIS included responses to matters raised through the NIRB’s review of the Draft EIS. The NIRB, the leading authorizing agency, is completing a technical review of the Final EIS, the final hearings for which commenced on March 27, 2006. The NIRB will then submit its recommendation a nd report to the Federal Minister of Indian and Northern Affairs, for final approval of the project certificate. The Company believes that the permitting process is substantially on track for completion in early 2006. However, government regulatory agencies are key participants in the review and licensing process and, as a result, the schedule is not entirely under the Company’s control.

During 2005 the Company also commenced formal discussions and negotiations with the Kivalliq Inuit Association (“KIA”) relating to the Inuit Impact Benefit Agreement (“IIBA”) for the Meadowbank project. In February 2006, the Company and the KIA announced that they had reached an Agreement in Principle with respect to the IIBA. The IIBA will ensure that local employment, training and business opportunities arising from all phases of the project are accessible to the Kivalliq Inuit. The IIBA also outlines the special considerations and compensation that Cumberland will provide for Inuit regarding traditional, social and cultural matters.

Development schedule

The engineering and construction schedule for the project assumes that a positive NIRB recommendation and report is obtained in early 2006 allowing for procurement and mobilization of construction equipment and supplies during the limited 2006 summer shipping season (mid-July to late September). Construction of the access road from Baker Lake to the Meadowbank site would commence in the fall of 2006, subject to the receipt of requisite licences. Upon completion of the access road, a mine construction period of approximately 18 months is required with production commencing during the second half of 2008. Construction activities in 2007 and 2008 assume that all requisite financing and licences are received, and that the Company is able to procure all necessary equipment on a timely basis.

Project financing

In March, 2006, a wholly-owned subsidiary of the Company secured a commitment from a group of banks to arrange and underwrite a seven-year limited recourse gold loan facility for up to 420,000 ounces. At a Cdn$600 per ounce gold price, the monetized value of the gold loan would be approximately Cdn$250 million. The bank commitment and the Company’s ability to draw down under the facility are subject to the satisfaction of certain conditions, including, among other things, the Company securing all requisite regulatory permits and licences and the completion of final loan documentation. The first draw down under the debt facility is expected by the first quarter of 2007. The proceeds from this gold loan facility would be applied to partially finance the development and construction activities at the Meadowbank Gold Project.

Meliadine Property Interests

On January 1, 2006, the Company received a $1.5 million option payment from Comaplex Minerals Corp. (Comaplex) with respect to its 22% interest (carried to production) in the Meliadine West Gold Project. The Company is entitled to receive an annual option payment of $1.5 million (plus an inflation adjustment) from Comaplex every year until commercial production is achieved at the Meliadine West Gold Project.

2. BUSINESS OVERVIEW

The Company is in the business of exploring and developing mineral properties, and is currently focused on the development of its 100% owned Meadowbank Gold Project located in the Nunavut Territory of Canada, on which we propose to develop an open pit gold mine.

The Company completed a bankable feasibility study on the Meadowbank project in 2005. The Study outlines a conventional open pit gold mine with a mine life of 8.1 years and proven and probable reserves of 2.9 million ounces. The Company is currently in the process of securing the requisite mine permitting and financing to allow a production decision. The project schedule assumes that a positive NIRB recommendation and report is received on a timely basis to allow procurement and mobilization of construction equipment and supplies in the limited 2006 summer shipping season. Construction activities would then commence in the fall of 2006, subject to the receipt of requisite licences, with mine production commencing during the second half of 2008. Construction activities in 2007 and 2008 assume that all requisite financing and licences are received, and that the Company is able to procure all necessary equipment on a timely ba sis.

The Company continues to conduct exploration at the Meadowbank project in order to increase gold reserves and resources. The Company completed a $3.9 million exploration program in 2005 which resulted in the discovery of the new Cannu zone. The Company has planned a $3.9 million exploration program for 2006 to focus on defining gold resources and reserves at the Cannu zone and exploring other targets on the Meadowbank property.

At December 31, 2005, the Company also had a 22% carried to production interest in the Meliadine West joint venture, and was receiving annual option payments from the operator of the joint venture (Comaplex) in accordance with the option agreement signed in 1995. On January 1, 2006 the Company received an option payment of $1.5 million. Under the option agreement, the Company is entitled to receive an annual option payment of $1.5 million (plus an inflation adjustment) from Comaplex every year until commercial production is achieved at the Meliadine West Gold Project. The Company’s share of exploration costs on the Meliadine West property is funded through a contingent non-recourse loan and is only repayable by the Company if commercial production is achieved and would be repaid only out of production cash flow.

The Company currently has no other sources of operating revenue. The Company has working capital of $27.5 million at December 31, 2005 and will require substantial additional financing to complete development of a mine at Meadowbank.

3. REVIEW OF FINANCIAL RESULTS

a) Selected Annual Information

The Company’s results of operations for the years ended December 31 are summarized below:

2005 | 2004 | 2003 | |

Option receipts | 500,000 | 500,000 | 500,000 |

Interest and other income | 1,904,718 | 2,499,210 | 1,056,077 |

Exploration and development costs | (7,667,949) | (9,040,483) | (11,518,663) |

General administrative and other expenses | (3,311,135) | (2,590,257) | (1,990,241) |

Stock based compensation expense | (1,117,671) | (1,900,013) | (1,481,612) |

Loss for the period | (9,692,037) | (10,531,543) | (13,434,439) |

Net loss per share, basic and fully diluted | ($0.18) | ($.19) | ($0.30) |

Total assets | 43,472,291 | 51,519,283 | 59,302,768 |

Total long-term liabilities | 475,603 | 640,847 | 889,696 |

Shareholders’ equity | 41,676,900 | 49,986,909 | 57,082,453 |

Dividends | n/a | n/a | n/a |

This financial information has been reported in accordance with Canadian GAAP, and is denominated in Canadian Dollars, the Company’s reporting currency. A reconciliation of the Company’s results of operations and financial position to US GAAP is provided in Note 15 of the Financial Statements.

b) Critical Accounting Policies and Estimates

The Company’s significant accounting policies are disclosed in Note 2 of the Financial Statements. The following is a discussion of the critical accounting policies and estimates which management believes are important for an understanding of the Company’s financial results:

Use of estimates

The preparation of financial statements in conformity with generally accepted accounting principles requires management to make estimates and assumptions which affect the reported amounts of assets and liabilities at the date of the financial statements and revenues and expenses for the period reported. By their nature, these estimates are subject to measurement uncertainty and the effect on the financial statements of changes in such estimates in future periods could be significant. Actual results could be materially different from those estimates.

Exploration and development of mineral property interests

Exploration costs are expensed as incurred. Development costs are expensed until it has been established that a mineral deposit is commercially mineable and a production decision has been made by the Company to implement a mining plan and develop a mine, at which point the costs subsequently incurred to develop the mine on the property prior to the start of mining operations are capitalized.

The Company has not yet made a production decision to develop a mine on any of its mineral properties and therefore all development costs were expensed in 2005.

The Company capitalizes the cost of acquiring mineral property interests, including undeveloped mineral property interests, until the viability of the mineral interest is determined. Capitalized acquisition costs are expensed if it is determined that the mineral property has no future economic value. Exploration stage mineral interests represent interests in properties that are believed to potentially contain (i) other mineralized material such as measured, indicated or inferred resources with insufficient drill hole spacing to qualify as proven and probable mineral reserves and (ii) other mine-related or greenfield exploration potential that are not an immediate part of measured or indicated resources. The Company’s mineral rights are generally enforceable regardless of whether proven and probable reserves have been established. The Company has the ability and intent to renew mineral rights where the existing term is not sufficie nt to recover undeveloped mineral interests.

Capitalized amounts (including capitalized development costs) are also written down if future cash flows, including potential sales proceeds, related to the mineral property are estimated to be less than the property’s total carrying value. Management of the Company reviews the carrying value of each mineral property periodically, and whenever events or changes in circumstances indicate that the carrying value may not be recoverable. Reductions in the carrying value of a property would be recorded to the extent that the total carrying value of the mineral property exceeds its estimated fair value. No write downs of mineral property interests were recorded in 2005.

Site closure costs

Accrued site closure costs relate to the Company’s legal obligation to remove exploration equipment and other assets from it’s mineral property sites in Nunavut and to perform other site reclamation work. Although the timing and amount of future site restoration costs to be incurred for existing exploration interests is uncertain, the Company has estimated the fair value of this liability to be $475,603 at December 31, 2005 based on the expected payments of $1,168,526 to be made primarily in 2017, discounted at interest rates of 8.5% or 10.0% per annum. Future changes in the assumed timing and amount of site restoration costs, or in the discount rate, could have a material impact on the Company’s recorded obligation for site closure costs.

Accounting for stock-based compensation

The Company accounts for stock-based compensation, including stock options and warrants granted to employees, directors and consultants, under the fair value based method. The fair value of the stock options and warrants is calculated at the date of grant and then amortized over the vesting period. The Company uses a Black-Scholes option pricing model to estimate the fair value of stock options and warrants. This model is subject to various assumptions including the expected life of the option and the volatility of the Company’s share price. The Company relies primarily on historical information as the basis for these assumptions.

c) Results of Operations

2005 compared to 2004

The Company incurred a net loss of $9.7 million for the year-ended December 31, 2005, compared to a net loss of $10.5 million for the year-ended December 31, 2004. The reduction in net loss during 2005 is primarily attributable to a $1.4 million reduction in exploration and development costs and a $0.8 million reduction in stock-based compensation expense, which were partially offset by increased project financing costs and lower gains on investments in public companies.

The Company had no operating revenues in either 2005 or 2004, as it has not commenced mining operations. In both 2005 and 2004, the Company received the annual $500,000 option payment from the operator of the Meliadine West joint venture in accordance with an option agreement signed in 1995.

The most significant component of the Company’s net loss for both 2005 and 2004 was exploration and development costs related to Meadowbank. During 2005 and 2004, the Company incurred costs of $7.4 million and $9.0 million respectively on exploration and development of the Meadowbank project. The $1.6 million reduction in 2005 is due to the completion of the infill drilling and engineering studies which were necessary to complete the feasibility study in early 2005. These cost reductions were partially offset by increased environmental and permitting related costs in 2005.

The $7.4 million of costs incurred at Meadowbank in 2005 included (i) a $3.9 million exploration program, comprised of approximately 11,700 meters of drilling designed to increase gold resources and reserves, and to further explore the newly identified Cannu zone, (ii) $2.6 million in environmental and permitting related costs, including costs related to the IIBA negotiations and (iii) $0.9 million of costs related to completion of the feasibility study and other engineering studies in 2005.

The costs associated with the Company’s 22% carried interest in Meliadine West are being financed by way of a contingent non-recourse loan from the property operator which will only be repayable by the Company if commercial production is achieved and will be repaid only out of production cash flow.

General and administrative and other expenses increased to $3.3 million in 2005 from $2.6 million in 2004. This increase is primarily due to the $0.6 million of project financing costs related to the pre-arranging advisory mandate awarded in June 2005 to SG Corporate & Investment Banking (a division of Societe Generale Group). Project financing costs also include the costs of the technical audit of the Meadowbank feasibility study that was performed by the bank-appointed independent engineer in 2005.

Stock-based compensation expense decreased to $1.1 million in 2005 from $1.9 million in 2004. The expense decreased primarily because the stock options vesting in 2005 had a lower average fair value than the stock options that vested in 2004. The amount of stock options granted in 2005 was comparable to 2004.

Interest and other income decreased to $1.9 million in 2005 from $2.5 million in 2004 due to lower gains realized from sales of the Company’s investment in Eurozinc Mining. During 2005 the Company sold its remaining 1,480,000 Eurozinc shares for a gain of $1.1 million compared to 2,920,000 Eurozinc shares sold in 2004 for a gain of $1.6 million.

2004 compared to 2003

The Company incurred a net loss of $10.5 million for the year-ended December 31, 2004, compared to a net loss of $13.4 million for the year-ended December 31, 2003. The reduction in net loss during 2004 is primarily attributable to a $2.5 million reduction in exploration and development costs and a $1.5 million increase in the gain on investments in public companies, which were partially offset by increases in stock-based compensation expense and general and administrative and other expenses.

The Company had no operating revenues in either 2004 or 2003, as it had not commenced mining operations. In both 2004 and 2003, the Company received the annual $500,000 option payment from the operator of the Meliadine West joint venture in accordance with an option agreement signed in 1995.

The most significant component of the Company’s net loss for both 2004 and 2003 was exploration and development costs related to Meadowbank. During the years ending December 31, 2004 and December 31, 2003, the Company incurred exploration and development costs of $9.0 million and $11.2 million respectively on the Meadowbank project. The $2.2 million reduction in 2004 is primarily attributable to the additional costs associated with the timely completion of the 2003 programs, including helicopter related costs, which resulted in higher exploration costs in 2003. Consulting engineering costs related to completion of the Meadowbank feasibility study were also lower in 2004 than in the prior year.

The $9.0 million of costs incurred at Meadowbank during 2004, included (i) a $5.8 million field program, comprising two phases of drilling totaling approximately 18,200 meters designed to increase the open pit potential of the project in support of the ongoing feasibility study, and to further explore the PDF deposit and other targets, (ii) $1.4 million of costs related to the feasibility studies which commenced in early 2003 and (iii) $1.7 million in environmental permitting related costs.

General and administrative and other expenses increased from $2.0 million in 2003 to $2.6 million in 2004. This increase primarily relates to the higher level of activity and required management staff in 2004 as well as higher corporate insurance costs.

Stock-based compensation expense increased from $1.5 million in 2003 to $1.9 million in 2004. The stock-based compensation expense is a non-cash item based on the estimated fair value of stock options vesting during the year. The total number of stock options granted in 2004 was comparable to 2003 and the average fair value of stock options granted in 2004 was lower than in the prior year, however, a significant portion of the 2003 option grants did not vest until 2004 resulting in a higher recorded expense in the current year.

Interest and other income increased from $1.0 million in 2003 to $2.5 million in 2004 due to the increased gains realized from sales of the Company’s investment in Eurozinc Mining. During the year ended December 31, 2004 the Company sold 2,920,000 Eurozinc shares for a gain of $1.6 million compared to 266,666 shares sold in 2003 for a gain of $0.04 million.

d) Summary of Quarterly Results

The table below sets out the quarterly results, expressed in thousands of Canadian dollars, for the past eight quarters:

2005 | 2004 | |||||||||

Fourth | Third | Second | First | Fourth | Third | Second | First | |||

Option receipts | - | - | - | 500,000 | - | - | - | 500,000 | ||

Other income | 207,563 | 478,239 | 358,457 | 860,459 | 354,885 | 303,512 | 732,859 | 1,107,954 | ||

Exploration and development costs | (1,799,989) | (2,191,953) | (2,572,390) | (1,103,617) | (939,069) | (2,125,327) | (3,937,040) | (2,039,047) | ||

Stock-based compensation | (33,062) | (52,804) | (939,518) | (92,287) | (194,272) | (1,276,206) | (204,845) | (224,690) | ||

Other expenses | (1,050,676) | (944,328) | (699,087) | (617,044) | (557,591) | (554,831) | (760,328) | (717,507) | ||

Net loss | (2,676,164) | (2,710,846) | (3,852,538) | (452,489) | (1,336,047) | (3,652,852) | (4,169,354) | (1,373,290) | ||

Net loss per share | (0.05) | (0.05) | (0.07) | (0.01) | (0.02) | (0.07) | (0.08) | (0.03) | ||

The majority of exploration costs are incurred in the second and third quarters of the fiscal year due to the seasonal weather conditions in Nunavut Territory. The increase in Other expenses in the third and fourth quarter of 2005 is due to increased project financing costs for the pre-arranging advisory mandate and the related technical audit of the feasibility study. Option receipts are received from the operator of the Meliadine West joint venture in the first quarter.

4. LIQUIDITY AND CAPITAL RESOURCES

The Company’s principal sources of cash during the 2005 were proceeds from the sale of shares in Eurozinc Mining ($1.1 million), interest income and option receipts from the operator of the Meliadine West joint venture ($0.5 million). The Company has not yet commenced mining operations and consequently has no other internal sources of cash.

At December 31, 2005 the Company had cash and cash equivalents and short-term investments of $27.9 million (2004 - $37.1 million). The majority of this amount is invested in highly liquid Canadian dollar denominated investments in investment grade debt and banker’s acceptances, with maturities through October 20, 2006. The counter-parties consist of financial institutions and the Canadian government.

The Company used $8.8 million in operating activities, primarily for exploration and development costs on the Company’s 100% owned Meadowbank property. The Company also had capital expenditures of $1.3 million during the year, primarily related to the construction of an airstrip at the Meadowbank site.

At December 31, 2005 the Company had working capital of $27.5 million as compared to $37.0 million at December 31, 2004. The following is a summary of the Company’s outstanding contractual obligations and commitments as at December 31, 2005:

Payments due by period | |||||

Less than | 1 to 3 | 4 to 5 | After | ||

Total | 1 year | years | years | 5 years | |

Capital lease obligations | 204,995 | 204,995 | - | - | - |

Operating lease obligations | 363,267 | 204,267 | 159,000 | - | - |

Contingent payments(1) | 1,300,000 | - | 1,300,000 | - | - |

Site closure costs(2) | 1,168,526 | - | - | - | 1,168,526 |

Total contractual obligations | 3,036,788 | 409,262 | 1,459,000 | - | 1,168,526 |

(1) The Company has three employment contracts in place that provide for the payment of specific bonus amounts should certain financial and operating milestones with respect to the Meadowbank Project be attained in the future.

(2) The Company has estimated future costs of $1,168,526 to be incurred primarily in 2017 related to the Company’s legal obligation to remove exploration equipment and other assets from its mineral property sites in Nunavut and to perform other site reclamation work.

The Company has committed to use certain third party mobile equipment between 2006 and 2007. Whereas the ultimate commitment amount will depend on usage, the maximum commitment amount is approximately $3.7 million.

The Company also has a contingent loan balance which totals $17,216,767 at December 31, 2005 [2004 - $15,121,045]. This loan is to be repaid only if commercial production at Meliadine West is achieved and is to be paid only out of production cash flow (as defined in the joint venture agreement).

5. FINANCIAL OUTLOOK

The outlook for the Company is dependent on the successful permitting, development and exploitation of the Meadowbank Gold Project. Assuming that all required approvals are received and a final production decision is made by the Company with respect to Meadowbank, substantial long-term financing would be required to develop and construct the property. The estimated initial capital costs for the Meadowbank project are $313 million, excluding working capital, capitalized financing costs and the costs associated with any cost overrun security that may be required as a condition of bank financing. The Company anticipates that financing would be derived from a combination of debt and equity financing. In March, 2006, a wholly-owned subsidiary of the Company secured a commitment from a group of banks to arrange and underwrite a seven-year limited recourse gold loan facility for up to 420,000 ounces. The bank commitmen t and the Company’s ability to draw down under the facility are subject to the satisfaction of certain conditions, including, among other things, the Company securing all requisite regulatory permits and licences and the completion of final loan documentation. The first draw down under the debt facility is expected by the first quarter of 2007. The proceeds realized from this project debt facility will finance a significant portion of the development and construction activities at the Meadowbank Gold Project. The amount of additional equity that the Company may be required to raise has yet to be determined and will depend on a number of factors, including i)the amount of cash the Company has on hand, ii)the amount of any project capital assistance that the Company may be able to secure from government sources and iii) proceeds realized from any incremental subordinated indebtedness that the Company may raise in the future.

The ultimate success of Meadowbank will be dependent on, among other factors, the actual capital and operating costs of the project, the U.S. dollar price of gold as well as the U.S. dollar currency exchange rate relative to the Canadian dollar. In addition, if the Company partially finances the development of Meadowbank with long-term debt financing, the Company’s future profitability may be sensitive to market interest rates.

On January 1, 2006 the Company received the $1.5 million option payment from the operator of the Meliadine West joint venture. The Company has planned a $3.9 million exploration program at Meadowbank in 2006. In addition, the Company expects to incur approximately $5.4 million on other Meadowbank project development activities and a further $3.4 million on general and administrative, project financing and other corporate expenditures. The Company will be able to fund these expenditures from its existing balances of cash and short-term investments.

If the required approvals are received on a timely basis to allow procurement and shipping of equipment during the limited 2006 summer shipping season, and if a final production decision is made to construct a mine at Meadowbank, then the Company could spend an additional $30-35 million on mine construction activities in 2006, in which case additional financing would be required.

6. FOREIGN CURRENCY, INTEREST RATE AND COMMODITY PRICE RISK

The Company has not commenced mining operations and accordingly, has no gold operating revenues. However, fluctuations in the prices of commodities such as gold, fuel, steel and other items required for the construction and operation of a gold mine could have a significant impact on the profitability of the Meadowbank project and therefore could impact the Company’s production decision and its ability to secure future financing on reasonable terms.

At December 31, 2005 the Company does not have significant foreign currency assets or liabilities and does not incur significant expenses in foreign currencies. However, it is anticipated that the sales price of gold derived from the Company’s Meadowbank project will be denominated in U.S. dollars, while the capital and operating costs of the Meadowbank project will be denominated primarily in Canadian dollars. As a result, the fair value of the Meadowbank mineral property, as well as the future profitability of the Meadowbank project, could be impacted by changes in the U.S. dollar currency exchange rate relative to the Canadian dollar.

The Company currently has no interest bearing long-term liabilities. However, if the Company partially finances the development of Meadowbank with long-term debt financing, the Company’s future profitability could be sensitive to market interest rates. In addition, the rate of return on the Company’s portfolio of short-term investments and cash equivalents is subject to change based on movements in market interest rates.

The Company does not currently engage in any hedging or derivative transactions to manage these risks

7. DISCLOSURE CONTROLS AND PROCEDURES

The Company’s management has completed an evaluation of the effectiveness of the Company’s disclosure controls and procedures (as defined under Multilateral Instrument 52-109), as of December 31, 2005. Based on that evaluation, the Chief Executive Officer and Chief Financial Officer have concluded that the design and operation of these disclosure controls and procedures was effective.

8. OUTSTANDING SHARE DATA

The following is a summary of changes in outstanding shares and stock options since December 31, 2005:

9. RISK FACTORS

The Company’s business is subject to factors that could cause actual results to differ materially from the Company’s expectations. Such factors include results of mine permitting activities, future gold prices, future prices of fuel, steel and other construction items, the availability of mining equipment and seasonal shipping as well as other risk factors described under the heading “Risk Factors” in the Company’s most recent Annual Information Form, which is available on SEDAR atwww.sedar.com.

Consolidated Annual Financial Statements

Cumberland Resources Ltd.

December 31, 2005

Management's Responsibility for Financial Reporting

The consolidated financial statements and the information contained in the annual report are the responsibility of the Board of Directors and management. The consolidated financial statements have been prepared by management in accordance with Canadian generally accepted accounting principles and reconciled to United States generally accepted accounting principles as set out in note 15.

The Audit Committee of the Board of Directors is composed of three Directors and meets periodically with management and the independent auditors to review the scope and results of the annual audit and to review the consolidated financial statements and related financial reporting matters prior to submitting the consolidated financial statements to the Board for approval.

The Company has developed and maintains a system of control to provide reasonable assurance that financial information is accurate and reliable.

The consolidated financial statements have been audited by Ernst & Young LLP, Chartered Accountants, who were appointed by the shareholders. The auditors’ report outlines the scope of their examination and their opinion on the consolidated financial statements.

![[exhibit2001.jpg]](https://capedge.com/proxy/6-K/0001016724-06-000018/exhibit2001.jpg) | |

Michael L. Carroll

Kerry M. Curtis

Senior Vice President and

President and Chief Executive Officer

Chief Financial Officer

Vancouver, Canada

March 30, 2006

AUDITORS’ REPORT

To the Shareholders of Cumberland Resources Ltd.

We have audited the consolidated balance sheets ofCumberland Resources Ltd. as at December 31, 2005 and 2004 and the consolidated statements of loss and deficit and cash flows for each of the years in the three year period ended December 31, 2005. These financial statements are the responsibility of the Company’s management. Our responsibility is to express an opinion on these financial statements based on our audits.

We conducted our audits in accordance with Canadian generally accepted auditing standards. Those standards require that we plan and perform an audit to obtain reasonable assurance whether the financial statements are free of material misstatement. An audit includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements. An audit also includes assessing the accounting principles used and significant estimates made by management, as well as evaluating the overall financial statement presentation.

In our opinion, these consolidated financial statements present fairly, in all material respects, the financial position of the Company as at December 31, 2005 and 2004 and the results of its operations and its cash flows for each of the years in the three year period ended December 31, 2005 in accordance with Canadian generally accepted accounting principles.

|

Vancouver, Canada

March 22, 2006 (except as to note 16

Chartered Accountants

which is as of March 30, 2006)

CONSOLIDATED BALANCE SHEETS

(Canadian dollars)

As at December 31

2005 | 2004 | |

$ | $ | |

ASSETS | ||

Current | ||

Cash and cash equivalents[note 3] | 16,493,481 | 10,063,509 |

Short term investments[note 3] | 11,419,988 | 27,062,928 |

Accounts receivable | 450,897 | 391,715 |

Prepaid expenses | 411,005 | 384,541 |

Total current assets | 28,775,371 | 37,902,693 |

Mineral property interests[note 4] | 8,289,214 | 8,246,083 |

Capital assets, net[note 6] | 5,777,706 | 4,676,302 |

Reclamation deposit[note 11(b)] | 630,000 | 605,000 |

Investments in public companies[note 13] | — | 89,205 |

43,472,291 | 51,519,283 | |

LIABILITIES AND SHAREHOLDERS’ EQUITY | ||

Current | ||

Accounts payable and accrued liabilities | 1,122,700 | 532,949 |

Current portion of capital leases[note 7] | 197,088 | 358,578 |

Total current liabilities | 1,319,788 | 891,527 |

Accrued site closure costs[note 8] | 475,603 | 443,759 |

Capital leases[note 7] | — | 197,088 |

Commitments and contingencies [note 11] | ||

Shareholders’ equity | ||

Share capital[note 9] | 112,565,733 | 112,404,856 |

Contributed surplus[note 9[e]] | 4,535,091 | 3,313,940 |

Deficit | (75,423,924) | (65,731,887) |

Total shareholders’ equity | 41,676,900 | 49,986,909 |

43,472,291 | 51,519,283 |

See accompanying notes to consolidated financial statements

On behalf of the Board:

![[exhibit2004.jpg]](https://capedge.com/proxy/6-K/0001016724-06-000018/exhibit2004.jpg)

Director

Director

CONSOLIDATED STATEMENTS OF LOSS AND DEFICIT

(Canadian dollars)

Years ended December 31

2005 | 2004 | 2003 | |

$ | $ | $ | |

REVENUE | |||

Option receipts[note 4[c][v]] | 500,000 | 500,000 | 500,000 |

Interest and other revenue | 854,779 | 943,801 | 1,014,964 |

Gain on investments in public companies[note 13[a]] | 1,049,939 | 1,555,409 | 41,113 |

2,404,718 | 2,999,210 | 1,556,077 | |

EXPENSES | |||

Exploration and development costs [note 5] | 7,667,949 | 9,040,483 | 11,518,663 |

Employee compensation | 828,566 | 613,997 | 473,704 |

Stock-based compensation[note 9[d]] | 1,117,671 | 1,900,013 | 1,481,612 |

Public and investor relations | 530,216 | 324,330 | 447,003 |

Office and miscellaneous | 456,526 | 476,240 | 449,454 |

Legal, audit and accounting | 218,739 | 303,602 | 257,766 |

Project financing | 553,151 | — | — |

Other fees and taxes | 107,851 | 191,421 | 211,013 |

Insurance | 476,224 | 484,831 | 66,100 |

Depreciation and amortization | 53,840 | 82,150 | 25,762 |

Accrued site closure costs - accretion expense[note 8] | 39,544 | 31,759 | 10,119 |

Interest expense on capital leases | 46,478 | 81,927 | 49,320 |

12,096,755 | 13,530,753 | 14,990,516 | |

Net loss for the year | 9,692,037 | 10,531,543 | 13,434,439 |

Deficit, beginning of year | 65,731,887 | 55,205,622 | 39,836,296 |

Share issue costs | — | (5,278) | 1,934,887 |

Deficit, end of year | 75,423,924 | 65,731,887 | 55,205,622 |

Loss per share – basic and diluted | $0.18 | $0.19 | $0.30 |

Weighted average number of shares outstanding | 55,000,199 | 54,539,310 | 45,497,756 |

See accompanying notes to consolidated financial statements

CONSOLIDATED STATEMENTS OF CASH FLOWS

(Canadian dollars)

Years ended December 31

2005 | 2004 | 2003 | |

$ | $ | $ | |

OPERATING ACTIVITIES | |||

Net loss for the year | (9,692,037) | (10,531,543) | (13,434,439) |

Add (deduct) items not affecting cash: | |||

Depreciation and amortization | 53,840 | 82,150 | 25,762 |

Exploration related amortization | 118,419 | 185,500 | 293,878 |

Accrued site closure costs - accretion expense | 39,544 | 31,759 | 10,119 |

Gain on investments in public companies | (1,049,939) | (1,555,409) | (41,113) |

Stock-based compensation | 1,117,671 | 1,900,013 | 1,481,612 |

Project financing costs[note 9(c)] | 117,157 | — | — |

Net changes in non-cash working capital items: | |||

Accounts receivable | (59,182) | 239,979 | (126,090) |

Prepaid expenses | (26,464) | (316,668) | (1,223) |

Accounts payable and accrued liabilities | 589,751 | (468,561) | 331,961 |

Cash used in operating activities | (8,791,240) | (10,432,780) | (11,459,533) |

FINANCING ACTIVITIES | |||

Issuance of common shares | 147,200 | 1,530,708 | 43,720,516 |

Share issue costs | — | 5,278 | (1,934,887) |

Repayment of capital lease obligation | (358,578) | (323,139) | (315,415) |

Cash (used in) provided by financing activities | (211,378) | 1,212,847 | 41,470,214 |

INVESTING ACTIVITIES | |||

Purchase of capital assets | (1,281,363) | (1,192,249) | (1,988,715) |

Acquisition of mineral property interests | (43,131) | — | — |

Short term investments, net | 15,642,940 | (4,919,935) | (4,955,301) |

Reclamation deposit | (25,000) | (605,000) | — |

Proceeds on sale of investments in public companies | 1,139,144 | 1,730,609 | 56,708 |

Cash provided by (used in) investing activities | 15,432,590 | (4,986,575) | (6,887,308) |

Increase (decrease) in cash and cash equivalents | 6,429,972 | (14,206,508) | 23,123,373 |

Cash and cash equivalents, beginning of year | 10,063,509 | 24,270,017 | 1,146,644 |

Cash and cash equivalents, end of year | 16,493,481 | 10,063,509 | 24,270,017 |

Supplemental information: | |||

Taxes paid | — | 36,204 | 52,153 |

Interest paid | 46,478 | 81,927 | 49,320 |

See accompanying notes to consolidated financial statements

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

(Canadian dollars)

December 31, 2005

1. NATURE OF BUSINESS

Cumberland Resources Ltd. (the “Company”) is engaged in the business of developing, exploring and acquiring mineral properties in Canada, with an emphasis on gold, and is in the process of exploring properties located in the Nunavut Territory in Northern Canada. The recoverability of amounts shown for mineral property interests in the Company’s balance sheet are dependent upon the existence of economically recoverable reserves, the ability of the Company to arrange appropriate financing to complete the development of its properties, the receipt of necessary permitting and upon achieving future profitable production or receiving proceeds from the disposition of the properties. The timing of such events occurring, if at all, is not yet determinable. The Company is considered to be a development stage enterprise as it has yet to generate significant revenue from operations.

2. SIGNIFICANT ACCOUNTING POLICIES

a)

Basis of presentation

These consolidated financial statements include the accounts of the Company and its wholly-owned subsidiary. These consolidated financial statements have been prepared in accordance with Canadian generally accepted accounting principles. As described in note 15, these principles differ in certain material respects from those that the Company would have followed had the consolidated financial statements been prepared in accordance with United States generally accepted accounting principles.

Certain prior year amounts have been reclassified to conform with the current year’s presentation.

b)

Use of estimates

The preparation of financial statements in conformity with generally accepted accounting principles requires management to make estimates and assumptions which affect the reported amounts of assets and liabilities at the date of the financial statements and revenues and expenses for the period reported. By their nature, these estimates are subject to measurement uncertainty and the effect on the financial statements of changes in such estimates in future periods could be significant. Actual results will likely differ from those estimates.

c) Exploration and development of mineral property interests

Exploration costs are expensed as incurred. Development costs are expensed until it has been established that a mineral deposit is commercially mineable and a production decision has been made by the Company to implement a mining plan and develop a mine, at which point the costs subsequently incurred to develop the mine on the property prior to the start of mining operations are capitalized.