UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

SCHEDULE 14A

Proxy Statement Pursuant to Section 14(a) of the

Securities Exchange Act of 1934

Filed by the Registrant ☒

Filed by a Party other than the Registrant ☐

Check the appropriate box:

☐ | Preliminary Proxy Statement |

| ☐ | Confidential, for Use of the Commission Only (as permitted by Rule 14a-6(e)(2)) |

| ☐ | Definitive Proxy Statement |

| ☒ | Definitive Additional Materials |

| ☐ | Soliciting Material under §240.14a-12 |

HIBBETT, INC.

(Name of Registrant as Specified In Its Charter)

N/A

(Name of Person(s) Filing Proxy Statement, if other than the Registrant)

Payment of Filing Fee (Check all boxes that apply):

| ☒ | No fee required. |

| ☐ | Fee paid previously with preliminary materials. |

☐ | Fee computed on table in exhibit required by Item 25(b) per Exchange Act Rules 14a-6(i)(1) and 0-11. |

Hibbett, Inc. (“Hibbett”) used the following presentation in a meeting with Institutional Shareholder Services on June 25, 2024. This investor presentation was also posted by Hibbett to investors.hibbett.com.

JUNE 2024 JD SPORTS ACQUISITION MAXIMIZES VALUE FOR HIBBETT SHAREHOLDERS

This presentation contains forward-looking statements, which include all statements that do not relate solely to historical or current facts, such as statements regarding our expectations, intentions or strategies regarding the future. In some cases, you can identify forward-looking statements by the following words: “aim,” “anticipate,” “believe,” “can,” “continue,” “could,” “estimate,” “expect,” “forecast,” “goal,” “guidance,” “intend,” “may,” “plan,” “possible,” “potential,” “predict,” “project,” “ongoing,” “outlook,” “should,” “seek,” “target,” “will,” “would,” or the negative of these terms or other similar expressions, although not all forward-looking statements contain these words. These forward-looking statements are based on management’s beliefs, as well as assumptions made by, and information currently available to, Hibbett, Inc. ("Hibbett" or the "Company"). Because such statements are based on expectations as to future financial and operating results and are not statements of fact, actual results may differ materially from those projected and are subject to a number of known and unknown risks and uncertainties, including: (i) the risk that the proposed transaction may not be completed in a timely manner or at all, which may adversely affect Hibbett’s business and the price of Hibbett’s common stock; (ii) the failure to satisfy any of the conditions to the consummation of the proposed transaction, including the adoption of the Merger Agreement by Hibbett’s stockholders; (iii) the occurrence of any event, change or other circumstance or condition that could give rise to the termination of the Merger Agreement, including in circumstances requiring Hibbett to pay a termination fee; (iv) the effect of the announcement or pendency of the proposed transaction on Hibbett’s business relationships, operating results and business generally; (v) risks that the proposed transaction disrupts Hibbett’s current plans and operations; (vi) Hibbett’s ability to retain and hire key personnel in light of the proposed transaction; (vii) risks related to diverting management’s attention from Hibbett’s ongoing business operations; (viii) unexpected costs, charges or expenses resulting from the proposed transaction; (ix) potential litigation relating to the transaction that could be instituted against JD Sports Fashion plc ("JD Sports"), Hibbett or their affiliates’ respective directors, managers or officers, including the effects of any outcomes related thereto; (x) continued availability of capital and financing and rating agency actions; (xi) certain restrictions during the pendency of the transaction that may impact Hibbett’s ability to pursue certain business opportunities or strategic transactions; (xii) unpredictability and severity of catastrophic events, including but not limited to acts of terrorism, war, hostilities, epidemics or pandemics, as well as management’s response to any of the aforementioned factors; (xiii) other risks described in Hibbett’s filings with the Securities and Exchange Commission (“SEC”), such risks and uncertainties described under the headings “Forward-Looking Statements,” “Risk Factors” and other sections of Hibbett’s Annual Report on Form 10-K filed with the SEC on March 25, 2024, as amended by Amendment No. 1 thereto on Form 10-K/A filed with the SEC on May 29, 2024, and subsequent filings; and (xiv) those risks and uncertainties that are described in the definitive proxy statement on Schedule 14A filed with the SEC on June 13, 2024. While the list of risks and uncertainties presented here is, and the discussion of risks and uncertainties to be presented in the definitive proxy statement that will be filed with the SEC will be, considered representative, no such list or discussion should be considered a complete statement of all potential risks and uncertainties. Unlisted factors may present significant additional obstacles to the realization of forward-looking statements. Consequences of material differences in results as compared with those anticipated in the forward-looking statements could include, among other things, business disruption, operational problems, financial loss, and legal liability to third parties and similar risks, any of which could have a material adverse effect on the completion of the transaction and/or Hibbett’s consolidated financial condition, results of operations, credit rating or liquidity. The forward-looking statements speak only as of the date they are made. Hibbett undertakes no obligation to update any forward-looking statements, whether as a result of new information, future events or otherwise. Forward-Looking Statements

Important Additional Information and Where to Find It In connection with the transaction, Hibbett filed a definitive proxy statement on Schedule 14A with the SEC on June 13, 2024. BEFORE MAKING ANY VOTING OR INVESTMENT DECISION, COMPANY STOCKHOLDERS ARE URGED TO READ THE DEFINITIVE PROXY STATEMENT AND ANY OTHER RELEVANT DOCUMENTS THAT ARE FILED OR WILL BE FILED WITH THE SEC (INCLUDING ANY AMENDMENTS OR SUPPLEMENTS THERETO) CAREFULLY AND IN THEIR ENTIRETY IF AND WHEN THEY BECOME AVAILABLE BECAUSE THEY WILL CONTAIN IMPORTANT INFORMATION ABOUT THE TRANSACTION. The definitive proxy statement was mailed to stockholders of Hibbett on or about June 14, 2024. Stockholders may obtain the documents (when they are available) free of charge at the SEC’s website, http://www.sec.gov. In addition, stockholders may obtain free copies of the documents (when they are available) on Hibbett’s website, https://investors.hibbett.com. Participants in the Solicitation Hibbett and certain of its directors, executive officers and other employees, under the SEC’s rules, may be deemed to be participants in the solicitation of proxies of Hibbett’s stockholders in connection with the transaction. Information about Hibbett’s directors and executive officers is available in Hibbett’s Annual Report on Form 10-K filed with the SEC on March 25, 2024, as amended by Amendment No. 1 thereto on Form 10-K/A filed with the SEC on May 29, 2024. Additional information regarding the interests of those participants and other persons who may be deemed participants in the transaction and their respective direct and indirect interests in the transaction, by security holdings or otherwise, are included in the definitive proxy statement filed with the SEC on June 13, 2024 and other materials to be filed with the SEC in connection with the transaction (if and when they become available). Free copies of these documents may be obtained as described in the preceding paragraph. Non-GAAP Financial Measures This presentation contains certain non-GAAP financial measures, including EBITDA and adjusted EBITDA. These non-GAAP financial measures are not calculated in accordance with GAAP and may exclude items that are significant in understanding and assessing Hibbett’s financial condition or operating results. Therefore, these non-GAAP financial measures should not be considered in isolation or as alternatives to financial measures calculated under GAAP. In addition, these non-GAAP financial measures may not be comparable to similarly-titled measures used by other companies. Hibbett’s management believes that these non-GAAP financial measures, taken in conjunction with GAAP financial measures, provide useful information for both Hibbett’s management and investors by excluding certain items that are not indicative of Hibbett’s core operating results. Hibbett’s management uses non-GAAP financial measures to compare Hibbett’s performance relative to forecasts and strategic plans and to benchmark Hibbett’s performance externally against competitors. Non-GAAP information is not prepared under a comprehensive set of accounting rules and should only be used to supplement an understanding of Hibbett’s operating results as reported under GAAP. Hibbett encourages investors to carefully consider its results under GAAP, as well as its supplemental non-GAAP information and the reconciliations between these presentations, to more fully understand its business. A reconciliation between GAAP and non-GAAP operating results is presented in the Appendix of this presentation. Further discussion of the non-GAAP financial measures is included in Hibbett’s filings with the SEC. Additional information

JD Sports agreement is culmination of multi-month competitive process to maximize shareholder value EXECUTIVE SUMMARY (1) Board Believes Approval of JD Sports Agreement is Warranted and the Best Path to Maximize Value Process catalyzed by contemporaneous inbound interest from JD Sports and three other potential strategic acquirors Process overseen by independent Strategic Review Committee reporting to highly-qualified Board supported by experienced financial and legal advisors Full engagement with the most logical and motivated potential buyers of Hibbett Multiple indications that M&A discussions and potential sale of Hibbett were a widespread rumor in the industry Rigorous negotiations resulted in two price increases from JD Sports – despite missed and lowered projections No alternative acquisition proposals have been made

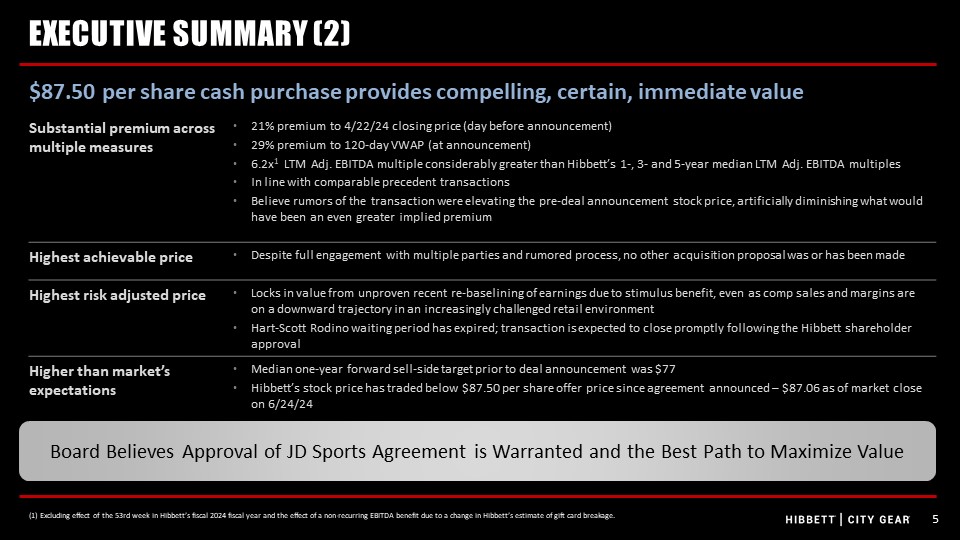

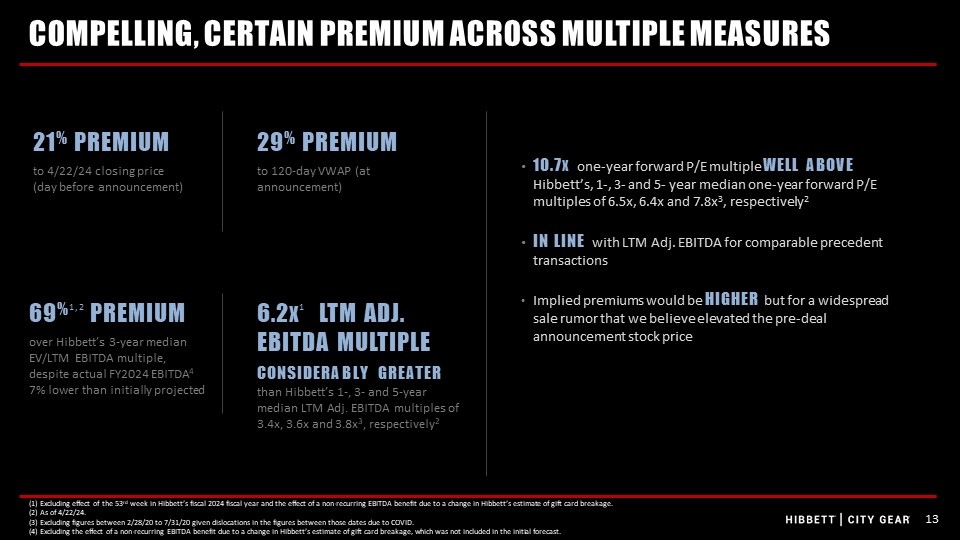

$87.50 per share cash purchase provides compelling, certain, immediate value EXECUTIVE SUMMARY (2) Substantial premium across multiple measures 21% premium to 4/22/24 closing price (day before announcement) 29% premium to 120-day VWAP (at announcement) 6.2x1 LTM Adj. EBITDA multiple considerably greater than Hibbett’s 1-, 3- and 5-year median LTM Adj. EBITDA multiples In line with comparable precedent transactions Believe rumors of the transaction were elevating the pre-deal announcement stock price, artificially diminishing what would have been an even greater implied premium Highest achievable price Despite full engagement with multiple parties and rumored process, no other acquisition proposal was or has been made Highest risk adjusted price Locks in value from unproven recent re-baselining of earnings due to stimulus benefit, even as comp sales and margins are on a downward trajectory in an increasingly challenged retail environment Hart-Scott Rodino waiting period has expired; transaction is expected to close promptly following the Hibbett shareholder approval Higher than market’s expectations Median one-year forward sell-side target prior to deal announcement was $77 Hibbett’s stock price has traded below $87.50 per share offer price since agreement announced – $87.06 as of market close on 6/24/24 (1) Excluding effect of the 53rd week in Hibbett’s fiscal 2024 fiscal year and the effect of a non-recurring EBITDA benefit due to a change in Hibbett’s estimate of gift card breakage. Board Believes Approval of JD Sports Agreement is Warranted and the Best Path to Maximize Value

While we have continued to win share, growth is slowing and comp sales and margins are on a downward trajectory Recent peak performance was driven by temporary COVID stimulus benefit – which has been expended Retail industry is under significant, sustained pressure Hibbett’s core customer is particularly exposed to macroeconomic challenges Hibbett’s highly concentrated vendor base creates further business risk Management has found it difficult to accurately measure its business risks as evidenced by missed guidance and missed consensus over multiple periods Ability to exceed $87.50 per share on a standalone basis in foreseeable future relies on achieving sustained aggressive growth despite challenging and unpredictable retail environment, with Hibbett’s current fiscal year performance already below plan EXECUTIVE SUMMARY (3) Hibbett’s standalone prospects carry meaningful risk. Board believes standalone value is significantly less than certain, premium $87.50 per share value on risk adjusted basis Board Believes Approval of JD Sports Agreement is Warranted and the Best Path to Maximize Value

JD Sports agreement is culmination of multi-month competitive process designed to maximize shareholder value

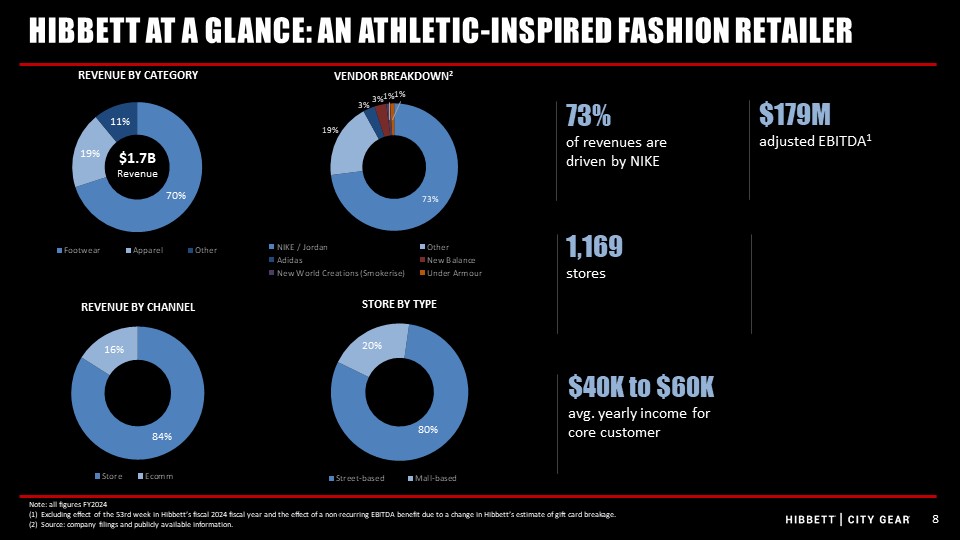

$1.7BRevenue $40K to $60K avg. yearly income for core customer HIBBETT AT A GLANCE: AN ATHLETIC-INSPIRED FASHION RETAILER Note: all figures FY2024 Excluding effect of the 53rd week in Hibbett’s fiscal 2024 fiscal year and the effect of a non-recurring EBITDA benefit due to a change in Hibbett’s estimate of gift card breakage. Source: company filings and publicly available information. $179M adjusted EBITDA1 73% of revenues are driven by NIKE 1,169 stores

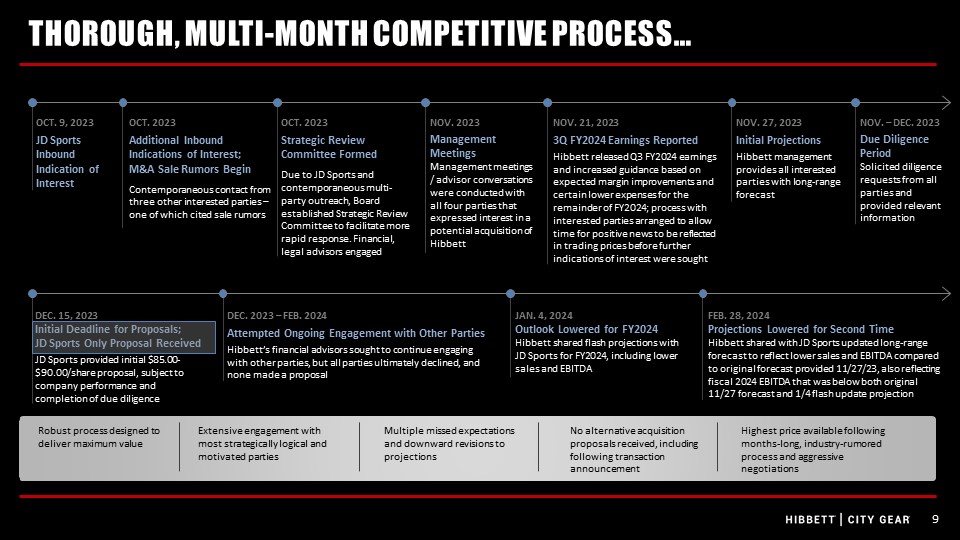

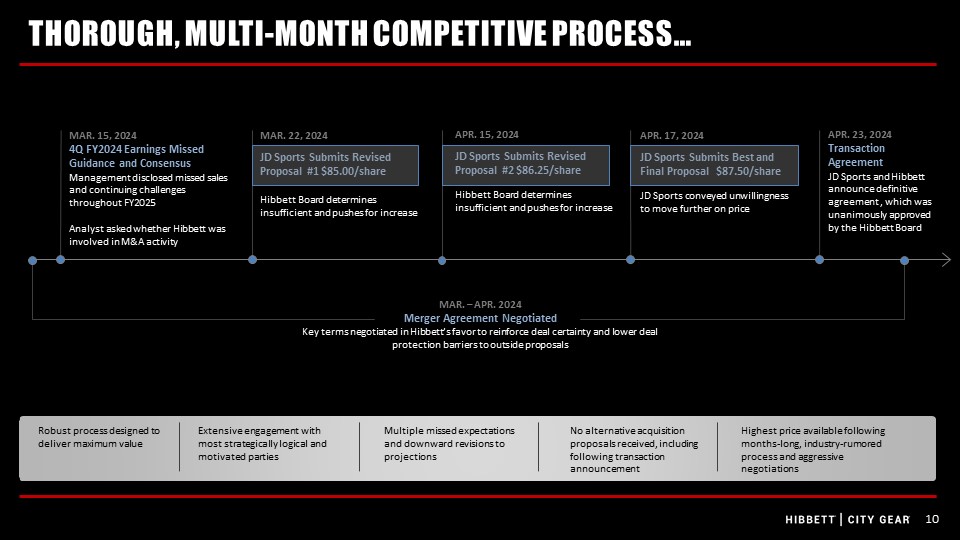

THOROUGH, MULTI-MONTH COMPETITIVE PROCESS… OCT. 2023 Additional Inbound Indications of Interest; M&A Sale Rumors Begin Contemporaneous contact from three other interested parties – one of which cited sale rumors OCT. 2023 Strategic Review Committee Formed Due to JD Sports and contemporaneous multi-party outreach, Board established Strategic Review Committee to facilitate more rapid response. Financial, legal advisors engaged NOV. 2023 Management Meetings Management meetings / advisor conversations were conducted with all four parties that expressed interest in a potential acquisition of Hibbett NOV. 27, 2023 Initial Projections Hibbett management provides all interested parties with long-range forecast NOV. – DEC. 2023 Due Diligence Period Solicited diligence requests from all parties and provided relevant information DEC. 15, 2023 Initial Deadline for Proposals;JD Sports Only Proposal Received JD Sports provided initial $85.00-$90.00/share proposal, subject to company performance and completion of due diligence JAN. 4, 2024 Outlook Lowered for FY2024 Hibbett shared flash projections with JD Sports for FY2024, including lower sales and EBITDA FEB. 28, 2024 Projections Lowered for Second Time Hibbett shared with JD Sports updated long-range forecast to reflect lower sales and EBITDA compared to original forecast provided 11/27/23, also reflecting fiscal 2024 EBITDA that was below both original 11/27 forecast and 1/4 flash update projection OCT. 9, 2023 JD Sports Inbound Indication of Interest NOV. 21, 2023 3Q FY2024 Earnings Reported Hibbett released Q3 FY2024 earnings and increased guidance based on expected margin improvements and certain lower expenses for the remainder of FY2024; process with interested parties arranged to allow time for positive news to be reflected in trading prices before further indications of interest were sought DEC. 2023 – FEB. 2024 Attempted Ongoing Engagement with Other Parties Hibbett’s financial advisors sought to continue engaging with other parties, but all parties ultimately declined, and none made a proposal Robust process designed to deliver maximum value Extensive engagement with most strategically logical and motivated parties Multiple missed expectations and downward revisions to projections No alternative acquisition proposals received Highest price available following months-long, industry-rumored process and aggressive negotiations Robust process designed to deliver maximum value Extensive engagement with most strategically logical and motivated parties Multiple missed expectations and downward revisions to projections No alternative acquisition proposals received, including following transaction announcement Highest price available following months-long, industry-rumored process and aggressive negotiations

THOROUGH, MULTI-MONTH COMPETITIVE PROCESS… Robust process designed to deliver maximum value Extensive engagement with most strategically logical and motivated parties Multiple missed expectations and downward revisions to projections No alternative acquisition proposals received, including following transaction announcement Highest price available following months-long, industry-rumored process and aggressive negotiations MAR. – APR. 2024 Merger Agreement NegotiatedKey terms negotiated in Hibbett’s favor to reinforce deal certainty and lower deal protection barriers to outside proposals APR. 17, 2024 JD Sports Submits Best and Final Proposal $87.50/share JD Sports conveyed unwillingness to move further on price APR. 23, 2024 Transaction AgreementJD Sports and Hibbett announce definitive agreement , which was unanimously approved by the Hibbett Board MAR. 15, 2024 4Q FY2024 Earnings Missed Guidance and Consensus Management disclosed missed sales and continuing challenges throughout FY2025 Analyst asked whether Hibbett was involved in M&A activity MAR. 22, 2024 JD Sports Submits Revised Proposal #1 $85.00/share Hibbett Board determines insufficient and pushes for increase APR. 15, 2024 JD Sports Submits Revised Proposal #2 $86.25/share Hibbett Board determines insufficient and pushes for increase

…OVERSEEN BY HIGHLY QUALIFIED, INDEPENDENTLY LED BOARD AND STRATEGIC REVIEW COMMITTEE STRATEGIC REVIEW COMMITTEE Anthony Crudele Independent Chairman (director since 2012) 30+ years of retail strategy, financial, operations and accounting experience EVP CFO, Treasurer of Tractor Supply, EVP CFO of Gibson Guitar, EVP CFO of Xcelerate, SVP and CFO at The Sports Authority Member of Advisory Board for Northern Tool & Equipment, former member of Tuesday Morning Board Dorlisa K. Flur Chair, Nominating and Corporate Governance Committee, Independent (director since 2019) 25 years of retail strategy, ecommerce, real estate, marketing and merchandise experience Chief Strategy and Transformation Officer of Southeastern Grocers, EVP Omnichannel for Belk, Vice Chair, Strategy and Chief Administrative Officer at Family Dollar Stores, McKinsey partner advising pubic and private retail companies Member of U.S. Cold Storage, Inc. Board, Chair, Strategic Committee; member of Sally Beauty Board Extensive corporate strategy experience in determining whether to remain independent or pursue other strategic alternatives Linda Hubbard Chair, Audit Committee, Independent (director since 2021) 20+ years of retail strategy, operations, sourcing, logistics and financial experience President and CEO of Carhartt, Inc. Secretary/Treasurer/Director of Carhartt Board 20+ years of accounting experience Plante Moran audit partner Differentiated business and geographic experience Member of the Board of the Federal Reserve Bank of Chicago; former Chair of the Board of the Federal Reserve Bank of Chicago/Detroit Branch Ramesh Chikkala Independent (director since 2022) 20+ years of retail IT and operations/supply chain experience EVP, COO of Grocery Outlet Holding Corporation Former SVP, Global Supply Chain (Omnichannel) and Food Manufacturing and SVP, IT of Walmart, Inc., as well as senior positions at Family Dollar Stores, Gap and Food Lion Advisory board member for Vorto, an AI powered supply chain technology company Pamela Edwards Independent (director since 2022) 30+ years of retail strategy and finance experience EVP and CFO of Citi Trends and CFO of L Brand's Mast Global, Victoria's Secret and Express divisions and various business and financial planning roles at Gap/Old Navy, Sears Roebuck and Kraft Foods Member of Neiman Marcus Board, Chair, Audit Committee; member of Azek, Inc. Board NACD, Director Certified Karen Etzkorn Independent (director since 2016) 35+ years of retail technology and cybersecurity experience CIO of Qurate Retail Group (QVC Group - HSN's parent company), Formerly CIO for HSNi and Ascena Retail Additional senior positions at The Home Depot, Williams-Sonoma, Inc., Gap Inc. and The Limited Inc. Terrance Finley Independent (director since 2008) 40+ years of retail operations, merchandising and marketing experience CEO of Books-A-Million, where he previously served as President and COO, EVP-Chief Merchandising Officer James Hilt Independent (director since 2017) 20+ years of retail ecommerce and consumer digital experience CEO of Asset Marketing Services, President of Shutterfly, EVP and Chief Customer Experience Officer at Express, SVP of e-Commerce and EVP, CMO of Express, additional executive positions at Barnes and Noble, Inc., Sears, Kmart Corporation, SAP and IBM Lorna Nagler Chair, Compensation Committee, Independent (director since 2019) 40+ years of retail strategy, management, operations experience President of Bealls Department Stores, President and CEO of Christopher & Banks, several leadership roles at Charming Shoppes, including President of Lane Bryant and President of Catherine Stores, merchandising leadership roles at Kmart and Kids “R” Us Chair of Ulta Beauty Board, member of Leslie's, Inc. Board and former member of Christopher & Banks Board Note: bio summaries include former and current positions. See Hibbett IR website for further detail. Mike Longo CEO and President (director since 2019) 30+ years of retail strategy management, operations, supply chain and IT experience CEO and President of Hibbett, CEO of City Gear, and AutoZone EVP of Supply Chain, IT, Development, Mexico Member of the Board of the Federal Reserve Bank of Atlanta

$87.50 per share cash purchase provides compelling, certain, immediate value

21% PREMIUM to 4/22/24 closing price (day before announcement) COMPELLING, CERTAIN PREMIUM ACROSS MULTIPLE MEASURES (1) Excluding effect of the 53rd week in Hibbett’s fiscal 2024 fiscal year and the effect of a non-recurring EBITDA benefit due to a change in Hibbett’s estimate of gift card breakage. (2) As of 4/22/24. (3) Excluding figures between 2/28/20 to 7/31/20 given dislocations in the figures between those dates due to COVID. (4) Excluding the effect of a non-recurring EBITDA benefit due to a change in Hibbett’s estimate of gift card breakage, which was not included in the initial forecast. 10.7x one-year forward P/E multiple WELL ABOVE Hibbett’s, 1-, 3- and 5- year median one-year forward P/E multiples of 6.5x, 6.4x and 7.8x3, respectively2 IN LINE with LTM Adj. EBITDA for comparable precedent transactions Implied premiums would be HIGHER but for a widespread sale rumor that we believe elevated the pre-deal announcement stock price 29% PREMIUM to 120-day VWAP (at announcement) 69%1,2 PREMIUM over Hibbett’s 3-year median EV/LTM EBITDA multiple, despite actual FY2024 EBITDA4 7% lower than initially projected 6.2x1 LTM ADJ.EBITDA MULTIPLE CONSIDERABLY GREATER than Hibbett’s 1-, 3- and 5-year median LTM Adj. EBITDA multiples of 3.4x, 3.6x and 3.8x3, respectively2

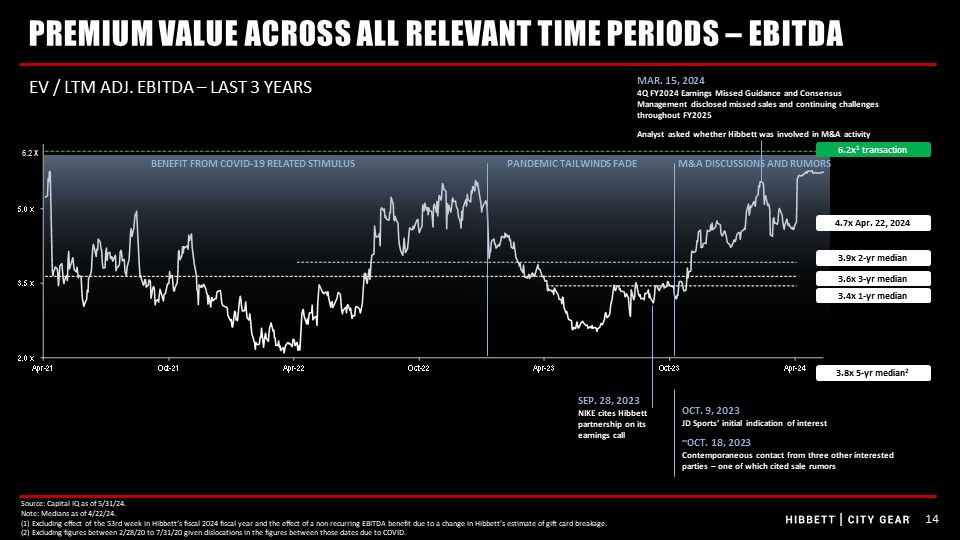

M&A DISCUSSIONS AND RUMORS PREMIUM VALUE ACROSS ALL RELEVANT TIME PERIODS – EBITDA EV / LTM ADJ. EBITDA – Last 3 Years Source: Capital IQ as of 5/31/24. Note: Medians as of 4/22/24. (1) Excluding effect of the 53rd week in Hibbett’s fiscal 2024 fiscal year and the effect of a non-recurring EBITDA benefit due to a change in Hibbett’s estimate of gift card breakage. (2) Excluding figures between 2/28/20 to 7/31/20 given dislocations in the figures between those dates due to COVID. 6.2 X BENEFIT FROM COVID-19 RELATED STIMULUS OCT. 9, 2023 JD Sports’ initial indication of interest ~OCT. 18, 2023 Contemporaneous contact from three other interested parties – one of which cited sale rumors MAR. 15, 20244Q FY2024 Earnings Missed Guidance and ConsensusManagement disclosed missed sales and continuing challenges throughout FY2025 Analyst asked whether Hibbett was involved in M&A activity 3.8x 5-yr median2 PANDEMIC TAILWINDS FADE 3.9x 2-yr median 3.6x 3-yr median 3.4x 1-yr median 4.7x Apr. 22, 2024 SEP. 28, 2023 NIKE cites Hibbett partnership on its earnings call 6.2x1 transaction

PREMIUM VALUE ACROSS ALL RELEVANT TIME PERIODS – P/E 6.5x 1-yr median 6.4x 3-yr median 6.3x 2-yr median 10.7x transaction Forward P/E (FY+1)1 – Last 3 Years BENEFIT FROM COVID-19 RELATED STIMULUS OCT. 9, 2023 JD Sports’ initial indication of interest ~OCT. 18, 2023 Contemporaneous contact from three other interested parties – one of which cited sale rumors 7.8x 5-yr median2 Source: Capital IQ as of 5/31/24. Note: Medians as of 4/22/24. (1) Reflects median Wall Street estimates. (2) Excluding figures between 2/28/20 to 7/31/20 given dislocations in the figures between those dates due to COVID. PANDEMIC TAILWINDS FADE M&A DISCUSSIONS AND RUMORS MAR. 15, 20244Q FY2024 Earnings Missed Guidance and ConsensusManagement disclosed missed sales and continuing challenges throughout FY2025 Analyst asked whether Hibbett was involved in M&A activity 8.9x Apr. 22, 2024

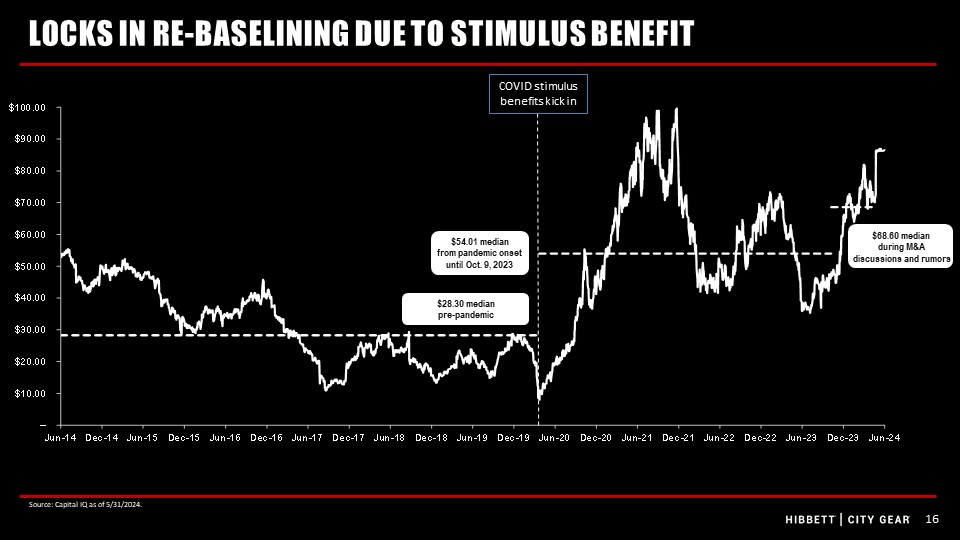

LOCKS IN RE-BASELINING DUE TO STIMULUS BENEFIT Source: Capital IQ as of 5/31/2024. COVID stimulus benefits kick in $28.30 median pre-pandemic $68.60 median during M&A discussions and rumors $54.01 median from pandemic onsetuntil Oct. 9, 2023

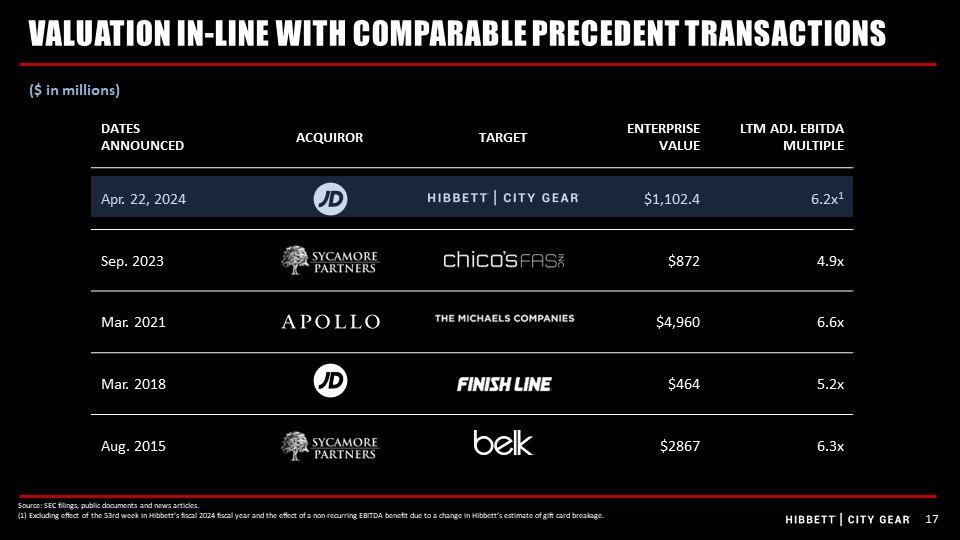

VALUATION IN-LINE WITH COMPARABLE PRECEDENT TRANSACTIONS Source: SEC filings, public documents and news articles. (1) Excluding effect of the 53rd week in Hibbett’s fiscal 2024 fiscal year and the effect of a non-recurring EBITDA benefit due to a change in Hibbett’s estimate of gift card breakage. DATESANNOUNCED ACQUIROR TARGET ENTERPRISEVALUE LTM ADJ. EBITDA MULTIPLE Apr. 22, 2024 $1,102.4 6.2x1 Sep. 2023 $872 4.9x Mar. 2021 $4,960 6.6x Mar. 2018 $464 5.2x Aug. 2015 $2867 6.3x ($ in millions)

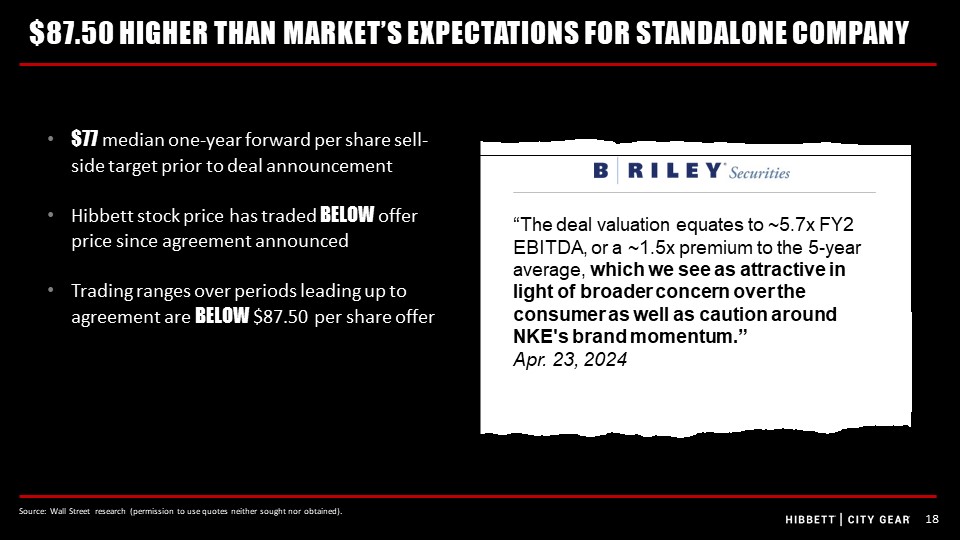

$87.50 HIGHER THAN MARKET’S EXPECTATIONS FOR STANDALONE COMPANY $77 median one-year forward per share sell-side target prior to deal announcement Hibbett stock price has traded BELOW offer price since agreement announced Trading ranges over periods leading up to agreement are BELOW $87.50 per share offer “The deal valuation equates to ~5.7x FY2 EBITDA, or a ~1.5x premium to the 5-year average, which we see as attractive in light of broader concern over the consumer as well as caution around NKE's brand momentum.”Apr. 23, 2024 Source: Wall Street research (permission to use quotes neither sought nor obtained).

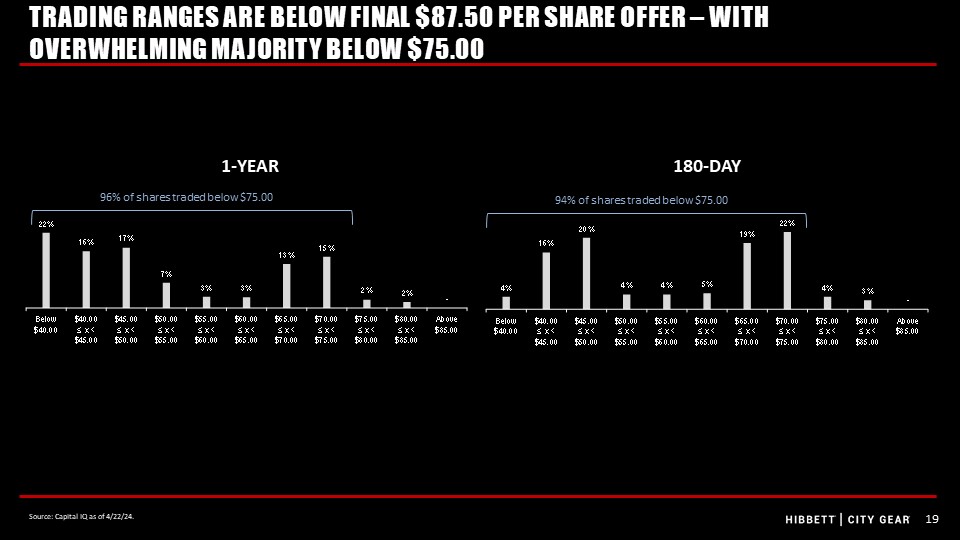

TRADING RANGES ARE BELOW FINAL $87.50 PER SHARE OFFER – WITH OVERWHELMING MAJORITY BELOW $75.00 Source: Capital IQ as of 4/22/24. 180-DAY 96% of shares traded below $75.00 1-YEAR 94% of shares traded below $75.00

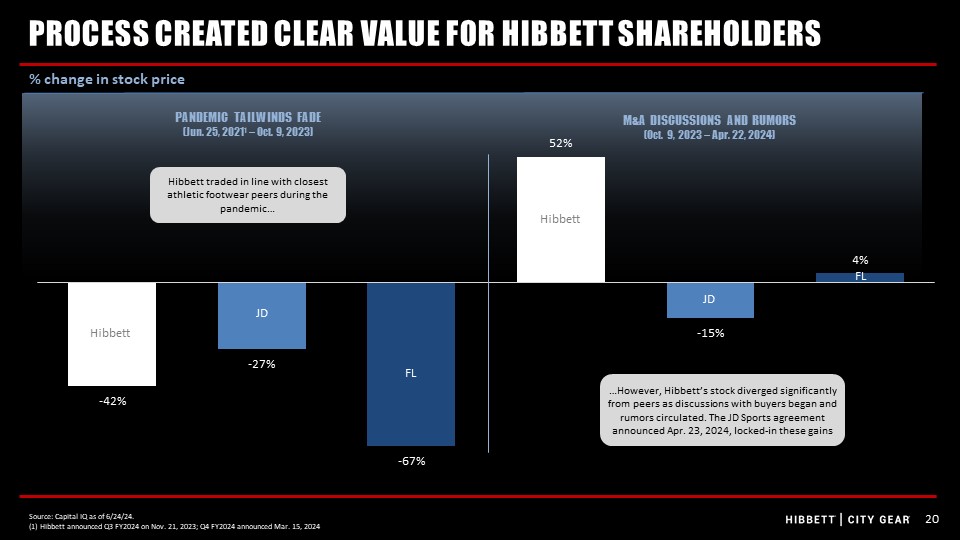

PROCESS CREATED CLEAR VALUE FOR HIBBETT SHAREHOLDERS PANDEMIC TAILWINDS FADE (Jun. 25, 20211 – Oct. 9, 2023) Hibbett traded in line with closest athletic footwear peers during the pandemic… M&A Discussions and Rumors (Oct. 9, 2023 – Apr. 22, 2024) …However, Hibbett’s stock diverged significantly from peers as discussions with buyers began and rumors circulated. The JD Sports agreement announced Apr. 23, 2024, locked-in these gains Hibbett Hibbett JD JD FL FL FL Source: Capital IQ as of 6/24/24. (1) Hibbett announced Q3 FY2024 on Nov. 21, 2023; Q4 FY2024 announced Mar. 15, 2024 % change in stock price

Hibbett’s standalone prospects carrymeaningful riskBoard believes standalone value is significantly less than certain, premium $87.50 per share value on risk adjusted basis

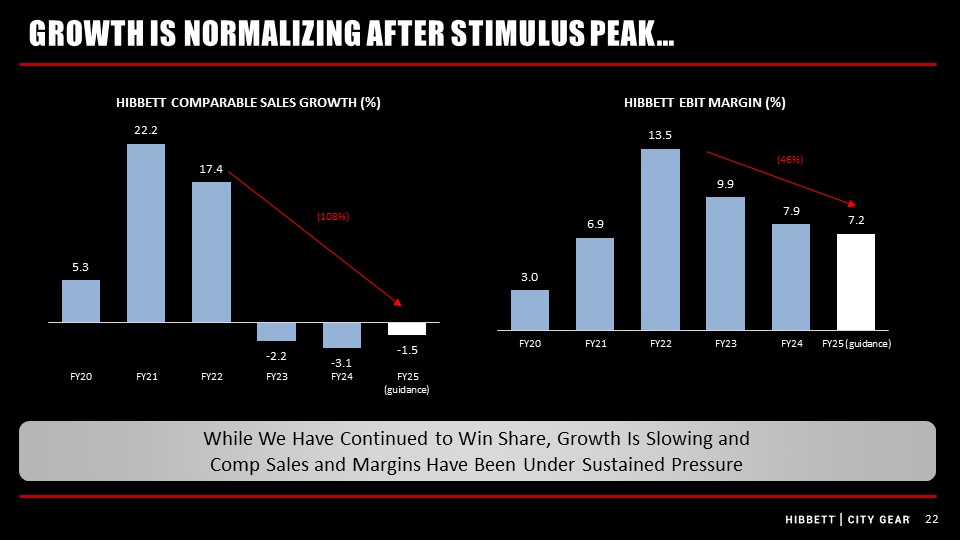

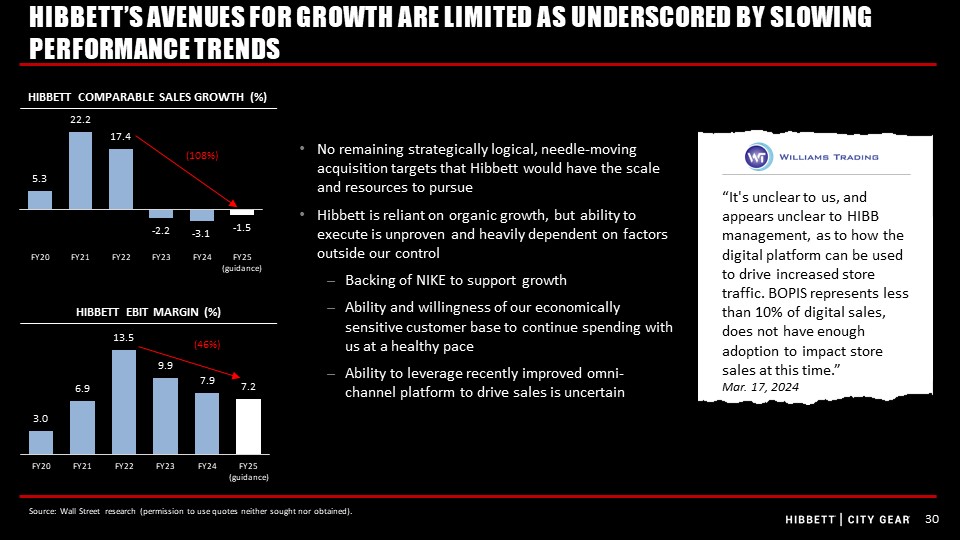

GROWTH IS NORMALIZING AFTER STIMULUS PEAK… HIBBETT COMPARABLE SALES GROWTH (%) HIBBETT EBIT MARGIN (%) While We Have Continued to Win Share, Growth Is Slowing and Comp Sales and Margins Have Been Under Sustained Pressure (108%) (46%)

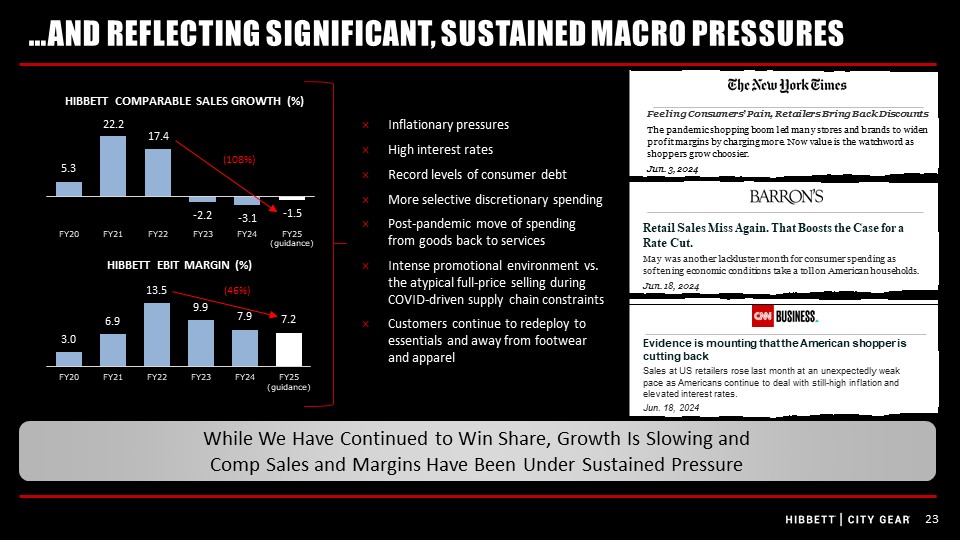

…AND REFLECTING SIGNIFICANT, SUSTAINED MACRO PRESSURES Inflationary pressures High interest rates Record levels of consumer debt More selective discretionary spending Post-pandemic move of spending from goods back to services Intense promotional environment vs. the atypical full-price selling during COVID-driven supply chain constraints Customers continue to redeploy to essentials and away from footwear and apparel HIBBETT COMPARABLE SALES GROWTH (%) HIBBETT EBIT MARGIN (%) Feeling Consumers’ Pain, Retailers Bring Back Discounts The pandemic shopping boom led many stores and brands to widen profit margins by charging more. Now value is the watchword as shoppers grow choosier. Jun. 3, 2024 Retail Sales Miss Again. That Boosts the Case for a Rate Cut. May was another lackluster month for consumer spending as softening economic conditions take a toll on American households. Jun. 18, 2024 Evidence is mounting that the American shopper is cutting back Sales at US retailers rose last month at an unexpectedly weak pace as Americans continue to deal with still-high inflation and elevated interest rates. Jun. 18, 2024 (108%) (46%) While We Have Continued to Win Share, Growth Is Slowing and Comp Sales and Margins Have Been Under Sustained Pressure

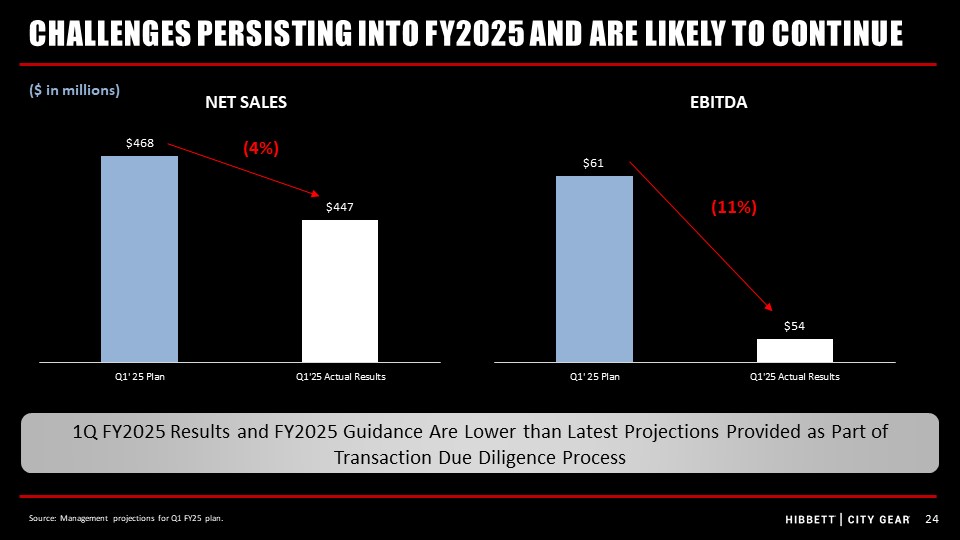

CHALLENGES PERSISTING INTO FY2025 AND ARE LIKELY TO CONTINUE Source: Management projections for Q1 FY25 plan. Net Sales 1Q FY2025 Results and FY2025 Guidance Are Lower than Latest Projections Provided as Part of Transaction Due Diligence Process EBITDA (4%) (11%) ($ in millions)

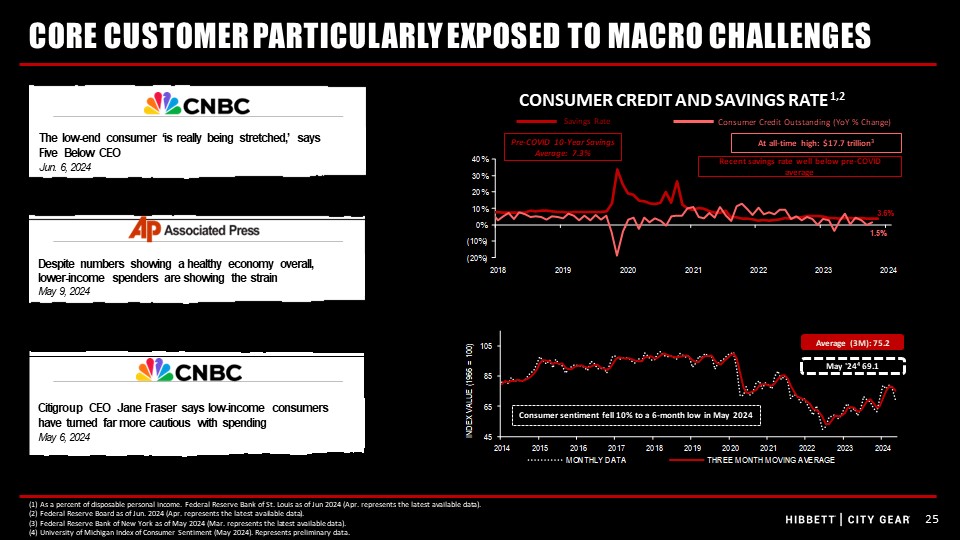

CONSUMER CREDIT AND SAVINGS RATE 1,2 CORE CUSTOMER PARTICULARLY EXPOSED TO MACRO CHALLENGES Savings Rate At all-time high: $17.7 trillion3 Recent savings rate well below pre-COVID average Pre-COVID 10-Year Savings Average: 7.3% Consumer Credit Outstanding (YoY % Change) May '244 69.1 Average (3M): 75.2 Consumer sentiment fell 10% to a 6-month low in May 2024 (1) As a percent of disposable personal income. Federal Reserve Bank of St. Louis as of Jun 2024 (Apr. represents the latest available data). (2) Federal Reserve Board as of Jun. 2024 (Apr. represents the latest available data). (3) Federal Reserve Bank of New York as of May 2024 (Mar. represents the latest available data). (4) University of Michigan Index of Consumer Sentiment (May 2024). Represents preliminary data. Despite numbers showing a healthy economy overall, lower-income spenders are showing the strain May 9, 2024 Citigroup CEO Jane Fraser says low-income consumers have turned far more cautious with spending May 6, 2024 The low-end consumer ‘is really being stretched,’ says Five Below CEO Jun. 6, 2024

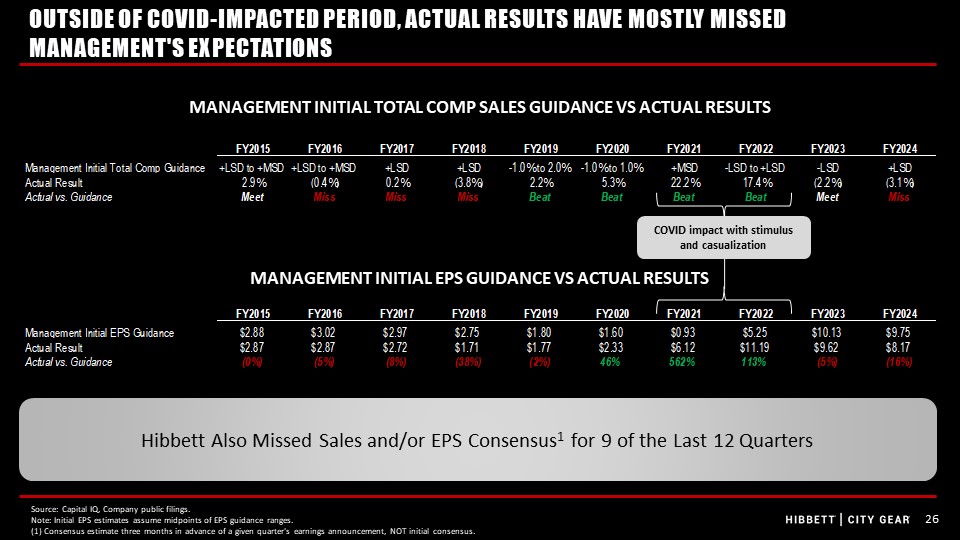

OUTSIDE OF COVID-IMPACTED PERIOD, ACTUAL RESULTS HAVE MOSTLY MISSED MANAGEMENT'S EXPECTATIONS Management Initial Total COMp Sales guidance vs actual results Source: Capital IQ, Company public filings. Note: Initial EPS estimates assume midpoints of EPS guidance ranges. (1) Consensus estimate three months in advance of a given quarter's earnings announcement, NOT initial consensus. Management Initial EPS guidance vs actual results COVID impact with stimulus and casualization Hibbett Also Missed Sales and/or EPS Consensus1 for 9 of the Last 12 Quarters

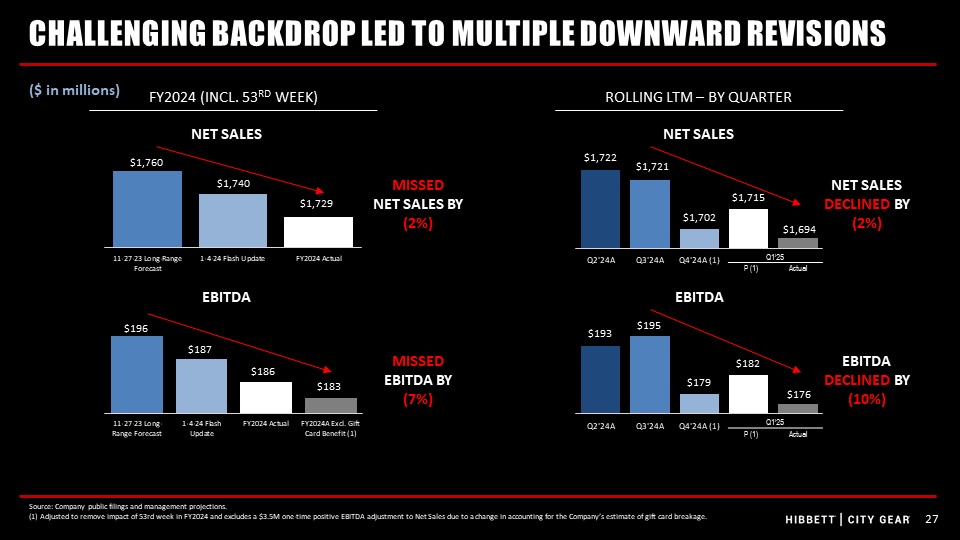

CHALLENGING BACKDROP LED TO MULTIPLE DOWNWARD REVISIONS Net Sales EBITDA FY2024 (incl. 53rd week) Rolling LTM – By Quarter Q1’25 P (1) Actual $1,760 $1,740 $1,729 $196 $187 $186 $183 $1,722 $1,721 $1,702 $1,715 $1,694 Q1’25 P (1) Actual $193 $195 $179 $182 $176 Source: Company public filings and management projections. (1) Adjusted to remove impact of 53rd week in FY2024 and excludes a $3.5M one-time positive EBITDA adjustment to Net Sales due to a change in accounting for the Company’s estimate of gift card breakage. Net Sales EBITDA Net Sales DECLINED BY (2%) EBITDADECLINED BY (10%) MISSED Net Sales BY (2%) MISSED EBITDA BY (7%) ($ in millions)

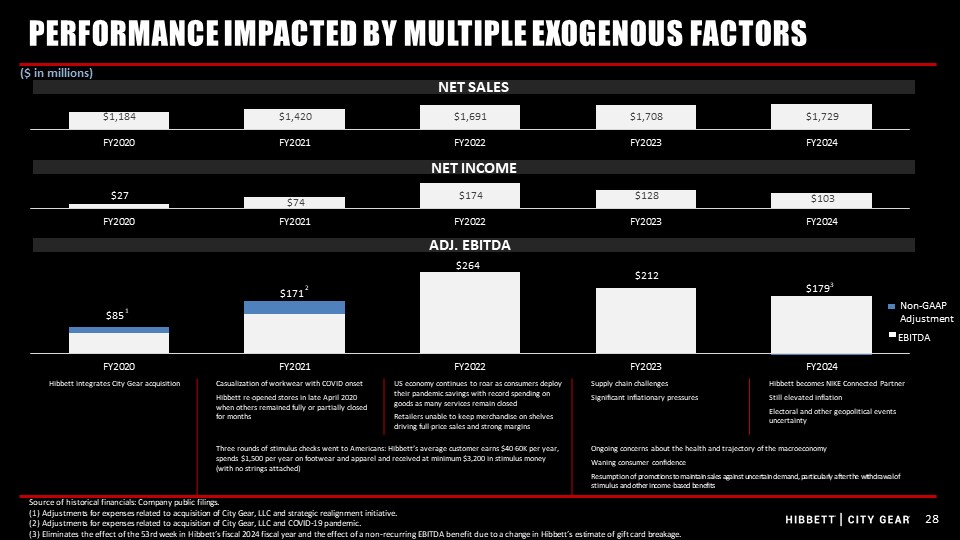

EBITDA Non-GAAPAdjustment Adj. EBITDA Source of historical financials: Company public filings. (1) Adjustments for expenses related to acquisition of City Gear, LLC and strategic realignment initiative. (2) Adjustments for expenses related to acquisition of City Gear, LLC and COVID-19 pandemic. (3) Eliminates the effect of the 53rd week in Hibbett’s fiscal 2024 fiscal year and the effect of a non-recurring EBITDA benefit due to a change in Hibbett’s estimate of gift card breakage. Hibbett integrates City Gear acquisition Casualization of workwear with COVID onset Hibbett re-opened stores in late April 2020 when others remained fully or partially closed for months US economy continues to roar as consumers deploy their pandemic savings with record spending on goods as many services remain closed Retailers unable to keep merchandise on shelves driving full-price sales and strong margins Supply chain challenges Significant inflationary pressures Hibbett becomes NIKE Connected Partner Still elevated inflation Electoral and other geopolitical events uncertainty Three rounds of stimulus checks went to Americans: Hibbett’s average customer earns $40-60K per year, spends $1,500 per year on footwear and apparel and received at minimum $3,200 in stimulus money (with no strings attached) Ongoing concerns about the health and trajectory of the macroeconomy Waning consumer confidence Resumption of promotions to maintain sales against uncertain demand, particularly after the withdrawal of stimulus and other income-based benefits PERFORMANCE IMPACTED BY MULTIPLE EXOGENOUS FACTORS NET INCOME Net SALES $264 $212 $179 $171 $85 ($ in millions) 1 2 3

“Nike (NKE, covered by Baird analyst Jonathan Komp) accounted for ~70% of HIBB's inventory purchases in FY22. The loss of key vendor support or decline/discontinuation of vendor incentives could have a material adverse effect on business.” Mar.15, 2024 “We attribute the [HIBB] softness to a difficult YoY comparison, a cautious consumer, and less innovation from Nike (73% of Hibbett's 2023 sales).” Jun. 5, 2024 HIBBETT’S HIGHLY CONCENTRATED VENDOR BASE CREATES BUSINESS RISK “NIKE represents >60% of HIBB’s sales; any disruption to this relationship would likely have material implications for HIBB’s fundamentals.” Mar. 15, 2024 Hibbett’s Growth and Revenues Rely on Consistent, Favorable Product Allocation and Strong Product Innovation from a Highly Concentrated Vendor Base “HIBB partly attributed the weak 4Q24 comp to a less-than-compelling launch calendar, and HIBB also mentioned that it would like to see the innovation pipeline speed up a bit.” Mar. 15, 2024 Sources: Wall Street research (permission to use quotes neither sought nor obtained). Slower vendor innovation has negatively impacted Hibbett’s results, contributing to guidance misses Hibbett loyalty program is tied to its largest vendor – NIKE We have seen key vendors change course and reduce allocations with other core partners over time No guarantee this would not be the same for Hibbett Could impact how much and where Hibbett can expand and grow Vendors continue to focus on DTC efforts Example: NIKE has grown its own DTC sales from 31% as of May 2019 to 44% in the most recent fiscal year Strategic vendors continue to have a meaningful relationshipwith Foot Locker, among others, given its scale and turnaround underway Vendors increasingly prefer to work with fewer, more global partners Unclear whether/how strategic vendors will use pricing/MAP and shifts to vendor-owned channels to manage challenges to their sales/margins/earnings

No remaining strategically logical, needle-moving acquisition targets that Hibbett would have the scale and resources to pursue Hibbett is reliant on organic growth, but ability to execute is unproven and heavily dependent on factors outside our control Backing of NIKE to support growth Ability and willingness of our economically sensitive customer base to continue spending with us at a healthy pace Ability to leverage recently improved omni-channel platform to drive sales is uncertain Hibbett’s AVENUES for growth are limited As Underscored by slowing Performance trends “It's unclear to us, and appears unclear to HIBB management, as to how the digital platform can be used to drive increased store traffic. BOPIS represents less than 10% of digital sales, does not have enough adoption to impact store sales at this time.” Mar. 17, 2024 Source: Wall Street research (permission to use quotes neither sought nor obtained). HIBBETT COMPARABLE SALES GROWTH (%) HIBBETT EBIT MARGIN (%) (108%) (46%)

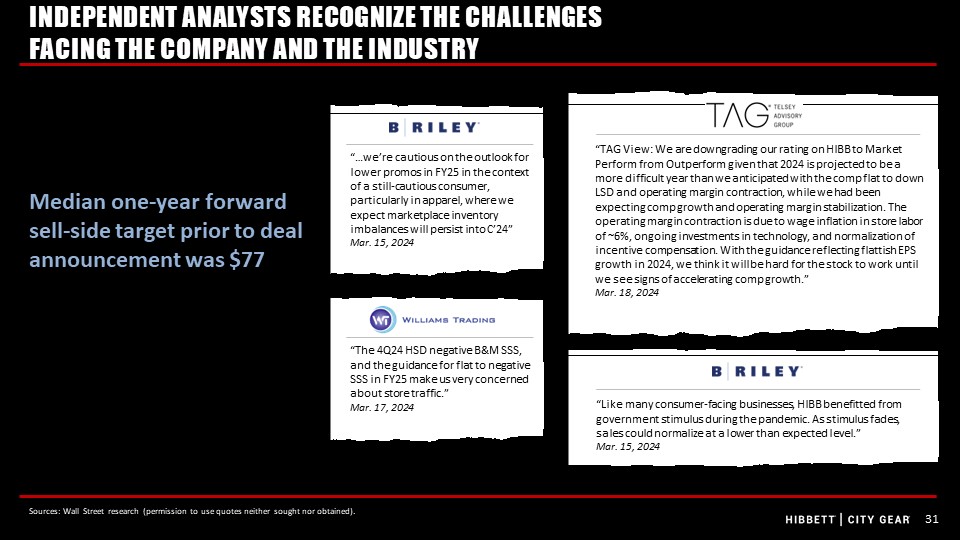

INDEPENDENT ANALYSTS RECOGNIZE THE CHALLENGES FACING THE COMPANY AND THE INDUSTRY Median one-year forward sell-side target prior to deal announcement was $77 “TAG View: We are downgrading our rating on HIBB to Market Perform from Outperform given that 2024 is projected to be a more difficult year than we anticipated with the comp flat to down LSD and operating margin contraction, while we had been expecting comp growth and operating margin stabilization. The operating margin contraction is due to wage inflation in store labor of ~6%, ongoing investments in technology, and normalization of incentive compensation. With the guidance reflecting flattish EPS growth in 2024, we think it will be hard for the stock to work until we see signs of accelerating comp growth.”Mar. 18, 2024 “…we’re cautious on the outlook for lower promos in FY25 in the context of a still-cautious consumer, particularly in apparel, where we expect marketplace inventory imbalances will persist into C’24” Mar. 15, 2024 “The 4Q24 HSD negative B&M SSS, and the guidance for flat to negative SSS in FY25 make us very concerned about store traffic.”Mar. 17, 2024 “Like many consumer-facing businesses, HIBB benefitted from government stimulus during the pandemic. As stimulus fades, sales could normalize at a lower than expected level.” Mar. 15, 2024 Sources: Wall Street research (permission to use quotes neither sought nor obtained).

Board believes approval of JD Sports agreement is warranted and the best path to maximize value

CONCLUSION JD Sports agreement is culmination of multi-month competitive process to maximize shareholder value $87.50 per share cash purchase provides compelling, certain, immediate value Despite full engagement with multiple parties and rumored process, no other acquisition proposal was or has been made Recent peak performance driven by COVID-related stimulus that has been expended – transaction locks in the value from this re-baselining of earnings, even as growth has turned negative Hibbett’s standalone prospects carry meaningful risk. Comp sales and margins are on a downward trajectory in an increasingly challenged retail environment compounded by reduced buying power in core customer base. Organic growth, which is clouded by these factors, is only realistic path for growth Hart-Scott-Rodino waiting period has expired; transaction is expected to close promptly following the Hibbett shareholder vote Board believes standalone value is significantly less than certain, premium $87.50 per share value on risk adjusted basis BOARD BELIEVES APPROVAL OF JD SPORTS AGREEMENT IS WARRANTED AND THE BEST PATH TO MAXIMIZE VALUE

Appendix

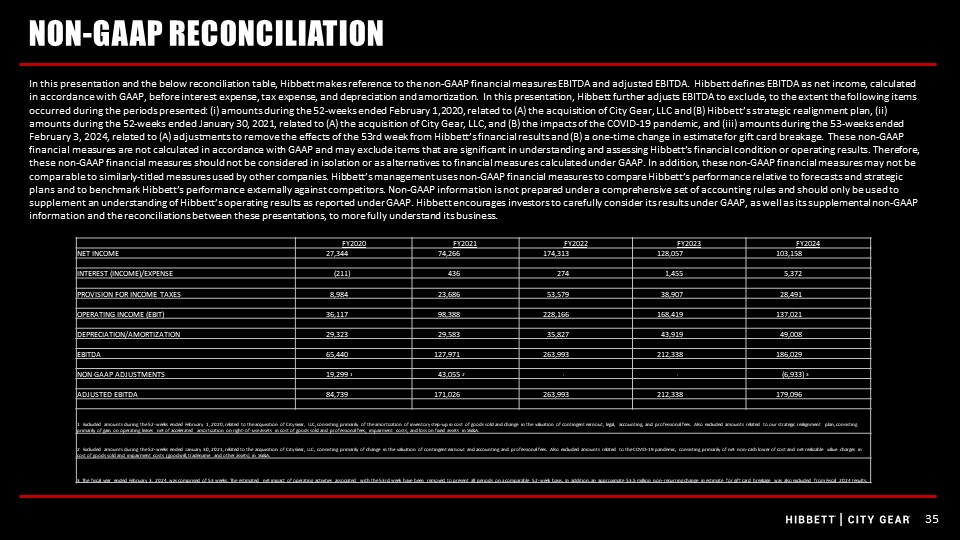

In this presentation and the below reconciliation table, Hibbett makes reference to the non-GAAP financial measures EBITDA and adjusted EBITDA. Hibbett defines EBITDA as net income, calculated in accordance with GAAP, before interest expense, tax expense, and depreciation and amortization. In this presentation, Hibbett further adjusts EBITDA to exclude, to the extent the following items occurred during the periods presented: (i) amounts during the 52-weeks ended February 1,2020, related to (A) the acquisition of City Gear, LLC and (B) Hibbett’s strategic realignment plan, (ii) amounts during the 52-weeks ended January 30, 2021, related to (A) the acquisition of City Gear, LLC, and (B) the impacts of the COVID-19 pandemic, and (iii) amounts during the 53-weeks ended February 3, 2024, related to (A) adjustments to remove the effects of the 53rd week from Hibbett’s financial results and (B) a one-time change in estimate for gift card breakage. These non-GAAP financial measures are not calculated in accordance with GAAP and may exclude items that are significant in understanding and assessing Hibbett’s financial condition or operating results. Therefore, these non-GAAP financial measures should not be considered in isolation or as alternatives to financial measures calculated under GAAP. In addition, these non-GAAP financial measures may not be comparable to similarly-titled measures used by other companies. Hibbett’s management uses non-GAAP financial measures to compare Hibbett’s performance relative to forecasts and strategic plans and to benchmark Hibbett’s performance externally against competitors. Non-GAAP information is not prepared under a comprehensive set of accounting rules and should only be used to supplement an understanding of Hibbett’s operating results as reported under GAAP. Hibbett encourages investors to carefully consider its results under GAAP, as well as its supplemental non-GAAP information and the reconciliations between these presentations, to more fully understand its business. NON-GAAP RECONCILIATION FY2020 FY2021 FY2022 FY2023 FY2024 NET INCOME 27,344 74,266 174,313 128,057 103,158 INTEREST (INCOME)/EXPENSE (211) 436 274 1,455 5,372 PROVISION FOR INCOME TAXES 8,984 23,686 53,579 38,907 28,491 OPERATING INCOME (EBIT) 36,117 98,388 228,166 168,419 137,021 DEPRECIATION/AMORTIZATION 29,323 29,583 35,827 43,919 49,008 EBITDA 65,440 127,971 263,993 212,338 186,029 NON-GAAP ADJUSTMENTS 19,299 1 43,055 2 - - (6,933) 3 ADJUSTED EBITDA 84,739 171,026 263,993 212,338 179,096 1 Excluded amounts during the 52-weeks ended February 1, 2020, related to the acquisition of City Gear, LLC, consisting primarily of the amortization of inventory step-up in cost of goods sold and change in the valuation of contingent earnout, legal, accounting, and professional fees. Also excluded amounts related to our strategic realignment plan, consisting primarily of gain on operating leases net of accelerated amortization on right-of-use assets in cost of goods sold and professional fees, impairment costs, and loss on fixed assets in SG&A. 2 Excluded amounts during the 52-weeks ended January 30, 2021, related to the acquisition of City Gear, LLC, consisting primarily of change in the valuation of contingent earnout and accounting and professional fees. Also excluded amounts related to the COVID-19 pandemic, consisting primarily of net non-cash lower of cost and net realizable value charges in cost of goods sold and impairment costs (goodwill, tradename and other assets) in SG&A. 3 The fiscal year ended February 3, 2024, was comprised of 53 weeks. The estimated net impact of operating activities associated with the 53rd week have been removed to present all periods on a comparable 52-week basis. In addition, an approximate $3.5 million non-recurring change in estimate for gift card breakage was also excluded from Fiscal 2024 results.