Table of Contents

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Form 10-Q

| x | Quarterly report pursuant to Section 13 or 15 (d) of the Securities Exchange Act of 1934 |

For the quarterly period endedJune 30, 2003

| ¨ | Transition report pursuant to Section 13 or 15 (d) of the Securities Exchange Act of 1934 for the transition period from to |

Commission file number: 0-20971

EDGEWATER TECHNOLOGY, INC.

(Exact Name of Registrant as Specified in its Charter)

Delaware | 71-0788538 | |

| (State or Other Jurisdiction of Incorporation or Organization) | (I.R.S. Employer Identification No.) | |

20 Harvard Mill Square | 01880-3209 | |

| (Address of Principal Executive Offices) | (Zip Code) | |

Registrant’s telephone number including area code: (781) 246-3343

Indicate by check mark whether the Registrant (1) has filed all reports required to be filed by Section 13 or 15 (d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yesx No¨

Indicate by check mark whether the registrant is an accelerated filer (as defined in Rule 12b-2 of the Securities Exchange Act of 1934). Yes¨ Nox

The number of shares of Common Stock of the Registrant, par value $.01 per share, outstanding at August 14, 2003 was 11,372,948.

Table of Contents

FORM 10-Q FOR THE QUARTER ENDED JUNE 30, 2003

INDEX

| Page | ||

PART I—FINANCIAL INFORMATION | ||

Item 1—Unaudited Financial Statements | ||

Unaudited Condensed Consolidated Financial Statements | ||

Unaudited Condensed Consolidated Balance Sheets as of June 30, 2003 and December 31, 2002 | 3 | |

| 4 | ||

| 5 | ||

Notes to Unaudited Condensed Consolidated Financial Statements | 6 | |

Item 2—Management’s Discussion and Analysis of Financial Condition and Results of Operations | ||

| 13 | ||

| 15 | ||

| 16 | ||

| 16 | ||

| 18 | ||

| 19 | ||

| 20 | ||

Off Balance Sheet Arrangements, Contractual Obligations and Contingent Liabilities and Commitments | 20 | |

| 21 | ||

Item 3—Quantitative and Qualitative Disclosures About Market Risk | 21 | |

| 22 | ||

PART II—OTHER INFORMATION | ||

| 24 | ||

| 24 | ||

| 24 | ||

| 24 | ||

| 25 | ||

| 25 | ||

| 26 | ||

2

Table of Contents

UNAUDITED CONDENSED CONSOLIDATED BALANCE SHEETS

(In Thousands, Except Per Share Data)

June 30, 2003 | December 31, 2002 | |||||||

| (Unaudited) | ||||||||

| ASSETS | ||||||||

Current assets: | ||||||||

Cash and cash equivalents | $ | 28,768 | $ | 29,159 | ||||

Short-term investments | 13,520 | 17,623 | ||||||

Accounts receivable, net1 | 4,157 | 2,647 | ||||||

Deferred income taxes, net | 1,127 | 1,127 | ||||||

Prepaid expenses and other current assets | 675 | 925 | ||||||

Total current assets | 48,247 | 51,481 | ||||||

Property and equipment, net | 1,567 | 1,606 | ||||||

Intangible assets, net | 13,373 | 11,614 | ||||||

Deferred income taxes, net | 21,270 | 21,757 | ||||||

Other assets | 57 | 35 | ||||||

Total assets | $ | 84,514 | $ | 86,493 | ||||

| LIABILITIES AND STOCKHOLDERS’ EQUITY | ||||||||

Current liabilities: | ||||||||

Accounts payable and accrued liabilities | $ | 1,567 | $ | 1,662 | ||||

Other liabilities including discontinued operations | 1,295 | 1,662 | ||||||

Current portion of capital lease obligations | 4 | 60 | ||||||

Accrued payroll and related liabilities | 1,145 | 882 | ||||||

Other liabilities | 182 | 240 | ||||||

Litigation settlement | — | 950 | ||||||

Total current liabilities | 4,193 | 5,456 | ||||||

Commitments and contingencies (Note 12) | ||||||||

Stockholders’ equity: | ||||||||

Preferred stock, $.01 par value; 2,000 shares authorized, no shares issued or outstanding | — | — | ||||||

Common stock, $.01 par value; 48,000 shares authorized, 29,721 and 29,596 shares issued as of June 30, 2003 and December 31, 2002, respectively, 11,382 and 11,485 shares outstanding as of June 30, 2003 and December 31, 2002, respectively | 297 | 296 | ||||||

Paid-in capital | 217,867 | 217,302 | ||||||

Treasury stock, at cost, 18,339 and 18,111 shares at June 30, 2003 and December 31, 2002, respectively | (141,197 | ) | (140,276 | ) | ||||

Deferred stock-based compensation | (594 | ) | — | |||||

Retained earnings | 3,948 | 3,715 | ||||||

Total stockholders’ equity | 80,321 | 81,037 | ||||||

Total liabilities and stockholders’ equity | $ | 84,514 | $ | 86,493 | ||||

See notes to the unaudited condensed consolidated financial statements.

| 1 | Includes related party amounts of $1,939 and $1,900 at June 30, 2003 and December 31, 2002, respectively. |

3

Table of Contents

UNAUDITED CONDENSED CONSOLIDATED STATEMENTS OF OPERATIONS

(In Thousands, Except Per Share Data)

| Three Months Ended June 30, | Six Months Ended June 30, | |||||||||||||

| 2003 | 2002 | 2003 | 2002 | |||||||||||

| (Unaudited) | ||||||||||||||

Service revenues1 | $ | 6,158 | $ | 4,811 | $ | 11,347 | $ | 9,393 | ||||||

Cost of services | 3,219 | 2,873 | 6,087 | 6,278 | ||||||||||

Gross profit | 2,939 | 1,938 | 5,260 | 3,115 | ||||||||||

Operating expenses: | ||||||||||||||

Selling, general and administrative | 2,539 | 2,481 | 4,674 | 4,699 | ||||||||||

Depreciation and amortization | 223 | 242 | 427 | 532 | ||||||||||

Restructuring charges | — | — | — | 349 | ||||||||||

Total operating expenses | 2,762 | 2,723 | 5,101 | 5,580 | ||||||||||

Operating income (loss) | 177 | (785 | ) | 159 | (2,465 | ) | ||||||||

Interest income and other, net | 96 | 208 | 229 | 428 | ||||||||||

Income (loss) before income taxes | 273 | (577 | ) | 388 | (2,037 | ) | ||||||||

Provision for income taxes | 109 | — | 155 | — | ||||||||||

Net income (loss) before change in accounting principle | 164 | (577 | ) | 233 | (2,037 | ) | ||||||||

Change in accounting principle (Note 8) | — | — | — | (12,451 | ) | |||||||||

Net income (loss) | $ | 164 | ($ | 577 | ) | $ | 233 | ($ | 14,488 | ) | ||||

Basic and diluted earnings (loss) per share | ||||||||||||||

Net income (loss) before change in accounting principle | $ | 0.01 | ($ | 0.05 | ) | $ | 0.02 | ($ | 0.18 | ) | ||||

Change in accounting principle | — | — | — | ($ | 1.07 | ) | ||||||||

Net income (loss) | $ | 0.01 | ($ | 0.05 | ) | $ | 0.02 | ($ | 1.25 | ) | ||||

Weighted average shares, basic | 11,365 | 11,616 | 11,416 | 11,611 | ||||||||||

Weighted average shares, diluted | 11,554 | 11,616 | 11,553 | 11,611 | ||||||||||

See notes to the unaudited condensed consolidated financial statements.

1 Includes related party amounts of $2,967 and $3,174 for the three months ended June 30, 2003 and 2002, respectively, and $6,012 and $6,263 for the six months ended June 30, 2003 and 2002, respectively.

4

Table of Contents

UNAUDITED CONDENSED CONSOLIDATED STATEMENTS OF CASH FLOWS

(In Thousands)

| Three Months Ended June 30, | Six Months Ended June 30, | |||||||||||||||

| 2003 | 2002 | 2003 | 2002 | |||||||||||||

| (Unaudited) | ||||||||||||||||

CASH FLOWS FROM OPERATING ACTIVITIES: | ||||||||||||||||

Net income (loss) | $ | 164 | ($ | 577 | ) | $ | 233 | ($ | 14,488 | ) | ||||||

Adjustments to reconcile net income (loss) to net cash provided by (used in) operating activities, net of acquisition: | ||||||||||||||||

Change in accounting principle | — | — | — | 12,451 | ||||||||||||

Depreciation and amortization | 223 | 242 | 427 | 531 | ||||||||||||

Provision for bad debts | (20 | ) | 40 | 25 | 86 | |||||||||||

Deferred income taxes | 109 | — | 155 | — | ||||||||||||

Changes in operating accounts: | ||||||||||||||||

Accounts receivable | (653 | ) | (276 | ) | (828 | ) | 1,071 | |||||||||

Prepaid expenses and other current assets | 175 | 131 | 284 | 147 | ||||||||||||

Other assets | 3 | 22 | 3 | 22 | ||||||||||||

Accounts payable and accrued liabilities | 544 | 624 | (370 | ) | (245 | ) | ||||||||||

Accrued payroll and related liabilities | (270 | ) | (215 | ) | 46 | (63 | ) | |||||||||

Other liabilities | (12 | ) | 12 | (59 | ) | (6 | ) | |||||||||

Net cash provided by (used in) operating activities | 263 | 3 | (84 | ) | (494 | ) | ||||||||||

Net cash used in extraordinary item | — | (56 | ) | — | (85 | ) | ||||||||||

Net cash used in discontinued operating activities | (99 | ) | (708 | ) | (1,317 | ) | (2,922 | ) | ||||||||

CASH FLOWS FROM INVESTING ACTIVITIES: | ||||||||||||||||

Redemptions or purchases of short-term investments | (47 | ) | 9,845 | 4,103 | (2,370 | ) | ||||||||||

Acquisition of Intelix, Inc., net of cash acquired | (1,950 | ) | — | (1,950 | ) | — | ||||||||||

Capital expenditures | (58 | ) | (49 | ) | (138 | ) | (97 | ) | ||||||||

Net cash (used in) provided by investing activities | (2,055 | ) | 9,796 | 2,015 | (2,467 | ) | ||||||||||

CASH FLOW FROM FINANCING ACTIVITIES: | ||||||||||||||||

Payments on borrowings | (14 | ) | (83 | ) | (56 | ) | (167 | ) | ||||||||

Proceeds from employee stock plans and stock option exercises | 17 | — | 38 | — | ||||||||||||

Repurchases of common stock | (711 | ) | — | (987 | ) | — | ||||||||||

Net cash used in financing activities | (708 | ) | (83 | ) | (1,005 | ) | (167 | ) | ||||||||

Net (decrease) increase in cash and cash equivalents | (2,599 | ) | 8,952 | (391 | ) | (6,135 | ) | |||||||||

CASH AND CASH EQUIVALENTS, beginning of period | 31,367 | 25,041 | 29,159 | 40,128 | ||||||||||||

CASH AND CASH EQUIVALENTS, end of period | $ | 28,768 | $ | 33,993 | $ | 28,768 | $ | 33,993 | ||||||||

SUPPLEMENTAL DISCLOSURES OF CASH FLOW INFORMATION: | ||||||||||||||||

Interest paid | $ | — | $ | 6 | $ | 2 | $ | 16 | ||||||||

Cash receipts from related parties | $ | 3,002 | $ | 3,170 | $ | 5,993 | $ | 6,124 | ||||||||

Cash payments to related parties | $ | 56 | $ | 56 | $ | 112 | $ | 112 | ||||||||

See notes to the unaudited condensed consolidated financial statements.

5

Table of Contents

NOTES TO UNAUDITED CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

1. ORGANIZATION:

Edgewater Technology, Inc. (“Edgewater,” “Edgewater Technology,” “the Company,” “our Company,” “we,” “us” or “our”) is an award-winning strategic consulting firm that specializes in providing technical consulting, custom software development and systems integration services primarily to middle-market companies and divisions of Global 2000 companies. We develop scalable technology solutions, which expedite business processes and provide our customers with competitive advantages. Our consultants collaborate with customers to translate business goals into technology-driven strategies. Headquartered in Wakefield, Massachusetts, Edgewater Technology has developed a partnership approach with our customers, targeting strategic, mission-critical applications. With approximately 161 technical consulting professionals, Edgewater Technology services our customer base by leveraging a combination of our vertical industry knowledge with a broad base of strategic technologies, along with proven reengineering techniques provided by our network of strategically positioned solutions centers.

Our Company was incorporated in the State of Delaware in 1996. Our Company’s business operations are conducted primarily through two subsidiaries, Edgewater Technology (Delaware) Inc., a Delaware corporation that was incorporated in 1992 and acquired by our Company in May 1999, and Intelix, Inc., a Virginia corporation that was incorporated in 1993 and that was acquired by our Company on June 2, 2003.

2. BASIS OF PRESENTATION:

The accompanying unaudited condensed consolidated financial statements have been prepared pursuant to the rules and regulations of the Securities and Exchange Commission (the “SEC”). Certain information and note disclosures normally included in annual financial statements prepared in accordance with accounting principles generally accepted in the United States of America have been omitted pursuant to those rules and regulations, although we believe that the disclosures made are adequate to ensure the information presented is not misleading.

The accompanying unaudited condensed consolidated financial statements reflect all adjustments (which were of a normal, recurring nature) that, in the opinion of management, are necessary to present fairly our financial position, results of operations and cash flows as of and for the interim periods presented. All intercompany transactions have been eliminated in the accompanying unaudited condensed consolidated financial statements. These financial statements should be read in conjunction with the audited financial statements and notes thereto included in our 2002 Annual Report on Form 10-K as filed with the SEC on March 28, 2003.

The results of operations for the three and six months ended June 30, 2003 are not necessarily indicative of the results to be expected for any future period or the full fiscal year. Our revenue and earnings may fluctuate from quarter to quarter based on factors within and outside our control, including variability in demand for Internet-related professional services, the length of the sales cycle associated with our service offerings, the number, size and scope of our projects and the efficiency with which we utilize our employees.

3. BUSINESS COMBINATION:

On June 2, 2003, the Company acquired all of the outstanding common stock of Intelix, Inc. (“Intelix”), a provider of systems integration and custom software development services located in Fairfax, Virginia. The results of Intelix’s operations have been included in the Company’s accompanying unaudited condensed consolidated statements of operations since the acquisition date. Revenue, related to the acquisition, during the second quarter was $0.3 million. The acquisition was made to enhance Edgewater’s geographical presence and will provide additional vertical expertise in the telecommunications and real estate industries. The aggregate preliminary purchase price was $2.7 million, including cash paid to the Intelix stockholders of $0.9 million, assumed liabilities at fair value in the amount of $1.5 million, and direct costs incurred of $0.3 million.

6

Table of Contents

EDGEWATER TECHNOLOGY, INC.

NOTES TO UNAUDITED CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

3. BUSINESS COMBINATION (continued):

Included in the purchase price is $165,000 of cash being held in escrow subject to the satisfaction of certain conditions of the sale and will be released within one year if such conditions are satisfied. In addition, the stockholders of Intelix are eligible for an additional cash payment in the first quarter of 2004 based upon a formula applied to earnings of the Intelix business for the twelve month period ended December 31, 2003. Any return of the escrowed amount or any additional payments to the Intelix stockholders, as well as other changes in estimates, will be accounted for as adjustments to the purchase price and would impact the final determination of the recorded goodwill.

Related to the purchase of Intelix, the Company preliminarily recorded $1.4 million in goodwill and $0.5 million in identifiable intangible assets, all in accordance with SFAS No. 141. The identifiable intangible assets are being amortized on the straight-line basis over their estimated useful lives (4-8 years). The goodwill is an indefinite lived asset in accordance with SFAS No. 142 and is subject to periodic review for impairment. This goodwill is not deductible for tax purposes. The Intelix business is included in the Company’s only reportable segment (see Note 10).

4. REVENUE RECOGNITION:

A majority of the Company’s contracts are billed on a time and materials basis. Time and materials contracts represented 81% of revenues for the three and six months ended June 30, 2003 and 93% and 95% for the three and six months ended June 30, 2002, respectively. Revenue under time and materials contracts is generally recognized as services are rendered, as hours are billed as services are performed at contractually agreed upon rates.

Revenue pursuant to fixed price contracts is generally recognized under the proportional performance method of accounting. Over the course of a fixed price contract, we routinely evaluate whether revenue and profitability from such contracts should be recognized in the current period. To measure the performance and our ability to recognize revenue and profitability on fixed price contracts, we compare actual direct costs incurred to the total estimated direct costs and determine the percentage of the contract that is complete. This percentage is multiplied by the estimated total contract value to determine the amount of net revenue recognized, subject to any warranty provisions and other holdbacks on revenue. Any warranty provisions included in fixed-price contracts are accounted for as a holdback of revenue until such provisions are satisfied. A formal project review process takes place quarterly although most projects are evaluated on an ongoing basis. Management reviews the estimated total direct costs on each contract to determine if the estimated amounts are reasonable, and estimates are adjusted as needed.

Revenues and earnings may fluctuate from quarter to quarter based on the number, size and scope of projects in which we are engaged, the contractual terms and degree of completion of such projects, any delays incurred in connection with a project, employee utilization rates, the adequacy of provisions for losses, the use of estimates of resources required to complete ongoing projects, general economic conditions and other factors. Certain significant estimates include estimates used for fixed-price contracts and the allowance for doubtful accounts. These items are frequently monitored and analyzed by management for changes in facts and circumstances, which could affect our estimates. Reimbursement of “out-of-pocket” expenses charged to customers is reflected as revenue.

For the three months ended June 30, 2003 and 2002, two customers and one customer, respectively, including Synapse (a related party—See Note 11), each accounted for more than 10% of revenues. For the six months ended June 30, 2003 and 2002, two customers, including Synapse, each accounted for more than 10% of revenues. For the three months ended June 30, 2003 and 2002, our three largest customers represented 78.6% and 81.8% of our revenues in the aggregate, respectively. For the six months ended June 30, 2003 and 2002, our three largest customers represented 78.6% and 83.6% of our revenues in the aggregate, respectively.

7

Table of Contents

EDGEWATER TECHNOLOGY, INC.

NOTES TO UNAUDITED CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

5. PROVISION FOR INCOME TAXES:

The Company currently has deferred tax assets related to net operating loss carryforwards and tax credits, which expire at different times through and until 2021. The Company has provided a valuation allowance against certain deferred tax assets aggregating approximately $15.7 million which allowance is based on management estimates, representing tax credits and certain state net operating loss carryforwards and other assets that the Company concluded would not likely be realized. The Company concluded the remaining assets, which consist primarily of the U.S. Federal net operating loss carryforward, is more likely than not to be realized through future taxable income. The Company is recording a deferred tax provision against income earned in 2003 using an estimated effective tax rate of 40%, with a corresponding reduction in the recorded net deferred tax assets. The Company recorded a tax provision of $0.1 million and $0.2 million for the three and six months ended June 30, 2003, respectively, by reducing the net deferred tax asset, resulting in the remaining net deferred tax asset of $22.4 million as of June 30, 2003. The Company does not anticipate having to pay cash taxes for federal income tax purposes earned in 2003 because of the availability of the net operating loss carryforwards. Management evaluates the realizability of the deferred tax assets quarterly and may adjust the valuation allowance based on such analysis in the future. The effective tax rate for 2002 was zero, primarily due to net operating losses.

6. STOCKHOLDERS’ EQUITY:

Stockholder Rights Plan:

The Company has a stockholder rights plan, commonly referred to as a “poison pill”, that may discourage an attempt to obtain control by means of a tender offer, merger, proxy contest or otherwise. Under this plan our Board of Directors can issue preferred stock in one or more series without stockholder action. If a person acquires 20% or more of our outstanding shares of common stock, except for certain institutional stockholders, who may acquire up to 25% of our outstanding shares of common stock, then rights under this plan would be triggered, which would significantly dilute the voting rights of any such acquiring person. Certain provisions of the General Corporation Law of Delaware may also discourage someone from acquiring or merging with us. No preferred stock has been issued as of June 30, 2003.

2003 Equity Incentive Plan:

In May 2003, the Company’s Board of Directors approved the “Edgewater Technology, Inc. 2003 Equity Incentive Plan” (the “2003 Plan”) for the purpose of attracting and retaining employees and providing a vehicle to increase management’s equity ownership in the Company. The 2003 Plan provides for restricted share awards and grants of nonqualified stock options in the aggregate of up to 500,000 shares of the Company’s common stock. In June 2003, the Company’s Compensation Committee authorized restricted share awards to certain executive officers of the Company under the 2003 Plan aggregating 125,000 shares of the Company’s common stock (the “Restricted Share Awards”). The aggregate compensation expense associated with the Restricted Share Awards is approximately $0.6 million, which compensation expense amount will be amortized over the vesting term (five years) beginning on July 1, 2003.

In December 2002, the Financial Accounting Standards Board (“FASB”) issued Statement of Financial Accounting Standards (“SFAS”) No. 148, “Accounting for Stock-Based Compensation—Transition and Disclosure—an amendment of FASB Statement No. 123.” SFAS No. 148 provides alternative methods of transition for a voluntary change to the fair value based method of accounting for stock-based employee compensation. In addition, SFAS No. 148 amends the disclosure requirements of SFAS No. 123 to require prominent disclosure in both annual and interim financial statements about the method of accounting for stock-based compensation and the effect of the method used on reported results.

8

Table of Contents

EDGEWATER TECHNOLOGY, INC.

NOTES TO UNAUDITED CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

6. STOCKHOLDERS’ EQUITY (continued):

In accordance with and as allowed by SFAS No. 123 and SFAS No. 148, the Company records stock-based compensation awards issued to employees and directors using the intrinsic value method and stock-based compensation awards issued to non-employees using the fair-value method of accounting. Stock-based compensation expense, if any, is recognized on awards of restricted shares or grants of stock options issued to employees and directors if the purchase price or exercise price, as applicable, is less than the market price of the underlying stock on the measurement date, generally the date of grant. The differences between accounting for stock-based compensation under the intrinsic value method and the fair value method are shown below, with the fair value estimated on the grant date or award issue date, as applicable, using the Black-Scholes option-pricing model:

Three Months Ended June 30, | Six Months Ended June 30, | |||||||||||||||

| 2003 | 2002 | 2003 | 2002 | |||||||||||||

| (In Thousands, Except Per Share Data) | ||||||||||||||||

Net income (loss)* | ||||||||||||||||

As reported | $ | 164 | ($ | 577 | ) | $ | 233 | ($ | 14,488 | ) | ||||||

Stock based compensation, net of tax | (240 | ) | (552 | ) | (602 | ) | (1,113 | ) | ||||||||

Pro forma | ($ | 76 | ) | ($ | 1,129 | ) | ($ | 369 | ) | ($ | 15,601 | ) | ||||

Basic and diluted earnings (loss) per share | ||||||||||||||||

As reported: | $ | 0.01 | ($ | 0.05 | ) | $ | 0.02 | ($ | 1.25 | ) | ||||||

Pro forma | ($ | 0.01 | ) | ($ | 0.10 | ) | ($ | 0.03 | ) | ($ | 1.34 | ) | ||||

| * | No employee stock based compensation has been recorded in net income (loss) for any period presented. |

Assumptions included in Black-Scholes model:

Three Months Ended June 30, | Six Months Ended June 30, | |||||||||||

| 2003 | 2002 | 2003 | 2002 | |||||||||

Weighted average risk-free interest rate | 2.46 | % | 2.82 | % | 2.46 | % | 2.82 | % | ||||

Dividend yield | 0 | % | 0 | % | 0 | % | 0 | % | ||||

Weighted average expected life | 5 years | 4 years | 5 years | 4 years | ||||||||

Expected volatility | 67 | % | 74 | % | 67 | % | 74 | % | ||||

7. SHORT TERM INVESTMENTS:

Our short-term investments have maturity dates of one year or less when acquired and are classified as held-to-maturity securities, which are recorded at amortized cost and consist of marketable instruments, which include, but are not limited to, government obligations, including agencies, and commercial paper. All investments that are not cash equivalents are considered short-term investments. All short-term investments with remaining maturities at the date of purchase of three months or less are considered cash equivalents. As of June 30, 2003 and December 31, 2002, our short-term investments consisted of $11.3 million and $12.3 million in commercial paper, respectively, and $2.2 million and $5.3 million, in government obligations, including agencies, respectively, and amortized cost approximated fair value.

9

Table of Contents

EDGEWATER TECHNOLOGY, INC.

NOTES TO UNAUDITED CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

8. INTANGIBLE ASSETS:

During the first quarter of 2002, the Company adopted Statement of Financial Accounting Standards No. 142 (“SFAS 142”), “Goodwill and Other Intangible Assets”. Under SFAS 142, goodwill and certain intangible assets are deemed to have indefinite lives and are no longer amortized, but are reviewed at least annually for impairment. Other identifiable intangible assets will continue to be amortized over their estimated useful lives. SFAS 142 requires that goodwill be tested for impairment at the reporting unit level at adoption and at least annually thereafter, utilizing the “fair value” methodology. The Company evaluates the fair value of its reporting unit utilizing various valuation techniques. During the first quarter of 2002, as a result of declining industry stock prices, the Company recognized a transitional impairment loss of $12.5 million as the cumulative effect of a change in accounting principle.

The new statement also requires that goodwill be tested for impairment on an annual basis and between annual tests in certain circumstances. The Company performed an additional impairment test on December 2, 2002, our selected annual measurement date, and recorded a non-cash impairment charge of $7.4 million in the fourth quarter of 2002, primarily as a result of the decline in industry stock prices for our peer group and lower revenues and operating margins for our Company. Our net unamortized goodwill, as of June 30, 2003 and December 31, 2002, was $12.2 million and $10.8 million, respectively.

Intangible assets consisted of the following as of:

| June 30, 2003 | December 31, 2002 | |||||

| (In Thousands) | ||||||

Goodwill | $ | 21,389 | $ | 19,987 | ||

Other intangibles | 2,160 | 1,630 | ||||

| 23,549 | 21,617 | |||||

Less: Accumulated amortization | 10,176 | 10,003 | ||||

| $ | 13,373 | $ | 11,614 | |||

Total amortization expense was $0.1 million for the three months ended June 30, 2003 and 2002 and $0.2 million for the six months ended June 30, 2003. This amortization expense relates to certain non-competition covenants and customer lists, which will expire from 2004 through 2010. As further described in Note 3, the Company acquired Intelix on June 2, 2003 and preliminarily recorded $1.4 million in goodwill and $0.5 million in identifiable intangibles, which are being amortized over 4-8 years.

10

Table of Contents

EDGEWATER TECHNOLOGY, INC.

NOTES TO UNAUDITED CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

9. EARNINGS (LOSS) PER SHARE:

A reconciliation of net income (loss) and weighted average shares used in computing basic and diluted earnings per share is as follows:

Three Months Ended June 30, | Six Months Ended June 30, | |||||||||||||

| 2003 | 2002 | 2003 | 2002 | |||||||||||

| (In Thousands, Except Per Share Data) | ||||||||||||||

Basic earnings per share: | ||||||||||||||

Net income (loss) applicable to common shares | $ | 164 | ($ | 577 | ) | $ | 233 | ($ | 14,488 | ) | ||||

Weighted average common shares outstanding | 11,365 | 11,616 | 11,416 | 11,611 | ||||||||||

Basic income (loss) per share of common stock | $ | 0.01 | ($ | 0.05 | ) | $ | 0.02 | ($ | 1.25 | ) | ||||

Diluted earnings per share: | ||||||||||||||

Net income (loss) applicable to common shares | $ | 164 | ($ | 577 | ) | $ | 233 | ($ | 14,488 | ) | ||||

Weighted average common shares outstanding | 11,365 | 11,616 | 11,416 | 11,611 | ||||||||||

Dilutive effect of stock options | 189 | — | 137 | — | ||||||||||

Weighted average common shares, assuming dilutive effect of stock options | 11,554 | 11,616 | 11,553 | 11,611 | ||||||||||

Diluted earnings (loss) per share of common stock | $ | 0.01 | ($ | 0.05 | ) | $ | 0.02 | ($ | 1.25 | ) | ||||

Stock options for which the exercise price exceeds the average market price over the period have an anti-dilutive effect on earnings per share, and accordingly, are excluded from the diluted computations for all periods presented. Had such shares been included, shares for the diluted computation would have increased by approximately 2.9 million shares (at prices ranging from $4.55 to $39.63 per share) for the three and six months ended June 30, 2003. For the three and six months ended June 30, 2002 the diluted computations would have increased by approximately 3.1 and 3.2 million shares, respectively (at prices ranging from $3.72 to $39.63 per share), had there been net income in 2002. Total options outstanding as of June 30, 2003 and 2002 were 4.5 million shares and 3.8 million shares, respectively.

10. SEGMENT INFORMATION:

The Company engages in business activities under one reporting segment, which provides technical consulting, custom software development and systems integration services.

11

Table of Contents

EDGEWATER TECHNOLOGY, INC.

NOTES TO UNAUDITED CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

11. RELATED PARTIES:

The Synapse Group, Inc. (“Synapse”), one of our significant customers, is considered a related party as its President and Chief Executive Officer is also a member of the Company’s Board of Directors. Revenues, receivables and payments received from Synapse are disclosed in the accompanying unaudited condensed consolidated financial statements, which balances were within the Company’s normal business terms.

In 1999, the Company entered into a lease agreement with a stockholder, who was a former officer and director of the Company, to lease certain parcels of land and buildings in Fayetteville, Arkansas for its former corporate headquarters. Rent payments related to these facilities totaled approximately $0.06 million for the three months ended June 30, 2003 and 2002 and $0.1 million for the six months ended June 30, 2003 and 2002. As the Company’s corporate headquarters moved to Wakefield, Massachusetts during 2001, the Company subleased the Fayetteville facility to a third party in 2002.

12. COMMITMENTS AND CONTINGENCIES:

We are sometimes a party to litigation incidental to our business. We believe that these routine legal proceedings will not have a material adverse effect on the results of operations or financial condition of our Company. We maintain insurance in amounts with coverages and deductibles that we believe are reasonable.

On February 11, 2003, our Company entered into a mutual Settlement and Release Agreement with the Stephens Group, Inc., Staffmark Investment, LLC, a majority owned subsidiary of Stephens Group, Inc. and its subsidiaries (collectively, the “Stephens Group”), to terminate, dismiss and retain intact our Company’s favorable summary judgment ruling with respect to the litigation matter in Delaware Superior Court. In addition to the mutual releases, the mutual Settlement and Release Agreement required our Company to pay $950,000 to the Stephens Group. The parties agreed that the existence of the settlement agreement and all of its terms, including any payment, were not evidence of any wrongdoing or liability related to the sale of our Company’s commercial staffing business in June 2000. The settlement amount of $950,000 was charged to discontinued operations in the 2002 statement of operations and such amount was subsequently paid in February 2003.

During the second quarter of 2002, our Company was notified by the Internal Revenue Service (the “IRS”) that it would be auditing our consolidated income tax returns for the 1998, 1999 and 2000 fiscal years. Our Company has responded to various IRS information requests by delivering documents and answering questions. For the period of the fiscal years covered by the audit, we owned non-Solutions staffing related businesses, which were sold during the 2000 and 2001 fiscal years. The results of the IRS audit could have an impact on our deferred tax asset, however as of the date of the filing of this Form 10-Q, we do not believe any such impact would be material to our financial position.

The Company entered into employment agreements with certain executive officers and management personnel during the second quarter of 2003, which agreements provide for annual salaries, cost-of-living adjustments and additional compensation in the form of “performance-based” bonuses. Certain agreements include covenants against competition with our Company, which extend for a period of time after termination. These agreements extend for a four-year period through 2007.

13. RESTRUCTURING:

In February 2002, Edgewater implemented cost-cutting measures by realigning its workforce. Edgewater reduced its overall headcount by 38 employees, or 19% of its total workforce. The Company recorded a restructuring charge in the first quarter of 2002 of $349,000, which consisted primarily of severance and similar employee termination expenses. All restructuring amounts were paid by the end of the second quarter of 2002.

12

Table of Contents

ITEM 2.

MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION

AND RESULTS OF OPERATIONS

Edgewater Technology, Inc. (“Edgewater,” “Edgewater Technology,” “the Company,” “our Company,” “we,” “us” or “our”) is an award-winning strategic consulting firm that specializes in providing technical consulting, custom software development and systems integration services primarily to middle-market companies and divisions of Global 2000 companies. We develop scalable technology solutions, which expedite business processes and provide our customers with competitive advantages. Our consultants collaborate with customers to translate business goals into technology-driven strategies. Headquartered in Wakefield, Massachusetts, Edgewater Technology has developed a partnership approach with our customers, targeting strategic, mission-critical applications. With approximately 161 technical consulting professionals, we service our customer base by leveraging a combination of our vertical industry knowledge with a broad base of strategic technologies, along with proven reengineering techniques provided by our network of strategically positioned solutions centers.

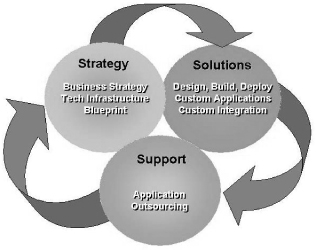

Edgewater Technology offers an end-to-end platform of technology-driven business solutions to help organizations tackle the barriers of technology transition, including:

| • | Strategy—We work with our customers to determine which IT investments provide the most value and how to apply technology to support their business goals—whether their goals are cost reductions, process improvements, customer service improvements or expanding into new markets and product lines. Our strategy services include analyzing our customers’ business goals, business processes and existing technology infrastructure. We emphasize quantifying the projected business impact of our recommended solutions in financial terms as a means to ensure that our strategy recommendations drive business value. We provide our customers with a tactical road map that they can implement immediately, as opposed to high-level consulting advice that often results in additional planning engagements prior to development and implementation. |

| • | Solutions—We specialize in developing and implementing technology applications that are tailored for each client’s unique business needs. Using a collaborative approach, our technical and vertical industry specialists take the time to understand a customer’s core business objectives and determine how technology can assist them in achieving their goals, not only in the immediate future but also in the long term. The customized applications that we develop are both flexible and scalable. Flexibility is critical so that our customers can easily integrate our solutions with their existing systems, upgrade solutions for technological changes and respond to developments in how business is conducted across Internet technologies. |

| • | Support—We provide a spectrum of post-deployment support services, including application outsourcing and site maintenance, that enables our customers to focus on their core competencies. We understand that being able to cater to all of the applications that support our customers’ businesses, especially applications that are in the early stages of evolution, requires the necessary technology skills and business understanding. We work with our customers to assist in the long-term care and feeding of their custom applications. We provide flexible and custom solutions that can range from remotely managing customer assets at onsite customer locations, to facilities management of our customers’ assets at Edgewater Technology’s network operating facility, or a complete solution with Edgewater Technology providing all services, including strategy, solutions and support. |

13

Table of Contents

The following diagram illustrates our service offerings:

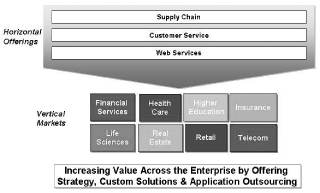

With a ten year operating history, Edgewater Technology has focused on five core values that differentiates our Company from the competition:

| (1) | Delivery Excellence—Our enviable delivery history is built upon ten years of proven methodology and processes, and by continually delivering solutions that work. Our delivery excellence is a derivative of a well-defined business plan, highly trained professionals, strong technical expertise, and established implementation and support methodologies. Most importantly, we provide effective and continued communication with our customers throughout the entire process. Our delivery history has contributed to our ability to build long-term relationships with our customers. |

| (2) | Vertical Expertise/Horizontal Service Offerings—We combine vertical industry knowledge with a broad base of key strategic technologies to serve our customers’ technology needs and deliver award-winning tailored strategies and solutions. We bring vertical industry knowledge together with a broad base of key strategic technologies. Edgewater Technology uses an iterative development methodology, with a focus on quality assurance and project management, to achieve rapid deployment capability and success in assisting organizations move through the barriers of technology transition. The primary vertical markets where we have developed core competencies to deliver our services include: Financial Services (Retail Banking, Portfolio/Asset Management); Health Care (Managed Care); Higher Education; Insurance; Life Sciences; Real Estate; Retail; Telecommunications; and various Emerging Markets that consist of untapped vertical markets which are just beginning to leverage the use of technology. We also focus on service offerings that cross each vertical such as Supply Chain, Customer Service and Web Services. |

14

Table of Contents

| (3) | Technology Excellence—We extend our services through proven key strategic technologies and through the focus of vertical business practices to build scalable custom solutions providing a solid return on the investment (ROI) and thereby competitive advantage to our customers. Our team of professionals has the technology expertise, coupled with vertical knowledge, to offer comprehensive strategies and solutions. Our established partnerships with industry leaders enable us to deliver market-leading insights and innovative solutions that meet our customers’ diverse business needs quickly. Our areas of technical expertise include: Web-based solutions; architectural strategy; Web services; data management; transaction processing and legacy systems integration. |

| (4) | Middle-Market Focus—We are well positioned to serve the technology needs of the middle market through our solutions centers based in second-tier cities in which middle-market enterprises typically reside. The middle market is defined as companies and/or subsidiaries of Global 2000 corporations with $50 million to $1 billion in revenue. By leveraging our solutions centers, we are able to create a virtual development environment that allows for efficiencies in staff management, while servicing clearly defined markets to leverage technology and gain competitive advantage. |

| (5) | Strong Operational Metrics—Since our inception in 1992, Edgewater Technology’s original management team has built an organization that is defined by a record of operational excellence, using electronic processes and systems to manage our consulting resources, company utilization and gross margin. |

Our unaudited condensed consolidated financial statements are prepared in accordance with accounting principles generally accepted in the United States of America (“GAAP”). These accounting principles require us to make certain estimates, judgments and assumptions. We believe that the estimates, judgments and assumptions, upon which we rely, are reasonable based upon information available to us at the time that they are made. These estimates, judgments and assumptions can affect the reported amounts of assets and liabilities as of the date of the financial statements, as well as the reported amounts of revenues and expenses during the periods presented. To the extent there are differences between these estimates, judgments or assumptions and actual results, our financial statements may be affected. The accounting policies that we believe are the most critical to aid in fully understanding and evaluating our reported financial results include the following:

| • | Revenue Recognition; |

| • | Accounting for Income Taxes; and |

| • | Valuation of Long-Lived and Intangible Assets. |

In many cases, the accounting treatment of a particular transaction is specifically dictated by GAAP and does not require management’s judgment in its application. There are also areas in which management’s judgment in selecting among available alternatives would not produce a materially different result. See notes to unaudited condensed consolidated financial statements included elsewhere herein, which contain additional information regarding our accounting policies and other disclosures required by GAAP. We have identified the policies listed below as critical to our business operations and the understanding of our results of operations.

Revenue Recognition. A majority of the Company’s contracts are billed on a time and materials basis. Time and materials contracts represented 81% of revenues for the three and six months ended June 30, 2003 and 93% and 95% for the three and six months ended June 30, 2002, respectively. Revenue under time and materials contracts is generally recognized as services are rendered, as hours are billed as services are performed at contractually agreed upon rates.

Revenue pursuant to fixed price contracts is generally recognized under the proportional performance method of accounting. Over the course of a fixed price contract, we routinely evaluate whether revenue and profitability from such contracts should be recognized in the current period. To measure the performance and our ability to recognize revenue and profitability on fixed price contracts, we compare actual direct costs incurred to the total estimated direct costs and determine the percentage of the contract that is complete. This percentage is multiplied by the estimated total contract value to determine the amount of net revenue recognized, subject to any warranty provisions and other holdbacks on revenue. Any warranty provisions included in fixed-price contracts are accounted for as a holdback of revenue until such provisions are satisfied. A formal project review process takes place quarterly although most projects are evaluated on an ongoing basis. Management reviews the estimated total direct costs on each contract to determine if the estimated amounts are reasonable, and estimates are adjusted as needed.

15

Table of Contents

Revenues and earnings may fluctuate from quarter to quarter based on the number, size and scope of projects in which we are engaged, the contractual terms and degree of completion of such projects, any delays incurred in connection with a project, employee utilization rates, the adequacy of provisions for losses, the use of estimates of resources required to complete ongoing projects, general economic conditions and other factors. Certain significant estimates include estimates used for fixed-price contracts and the allowance for doubtful accounts. These items are frequently monitored and analyzed by management for changes in facts and circumstances, which could affect our estimates. Reimbursement of “out-of-pocket” expenses charged to customers is reflected as revenue.

Accounting for Income Taxes. As part of the process of preparing our unaudited condensed consolidated financial statements, significant judgment is required in determining our provision for income taxes, the carrying value of deferred tax assets and liabilities and the valuation allowance recorded against our net deferred tax assets. We have recorded a $15.7 million valuation allowance against our net deferred tax assets as of June 30, 2003 and December 31, 2002, respectively, due to potential uncertainty related to our ability to utilize some of our deferred tax assets, primarily consisting of certain net operating losses carried forward and foreign tax credits, before they expire. We consider scheduled reversals of deferred tax liabilities, projected future taxable income, ongoing tax planning strategies and other matters, including the period over which our deferred tax assets will be recoverable in assessing the need for and the amount of the valuation allowance. In the event that actual results differ from these estimates or we adjust these estimates in future periods, adjustments to the deferred tax assets may be recorded, which could materially impact our financial position and net income (loss) in the period. The net deferred tax asset was $22.4 million as of June 30, 2003, which amount management believes is more likely than not to be realized.

Valuation of Long-Lived and Intangible Assets. We assess the impairment of identifiable intangibles, long-lived assets and related goodwill annually and whenever events or changes in circumstances indicate that the carrying value may not be recoverable. Factors we consider important, which could trigger an impairment review include: 1) significant negative industry or economic trends, 2) significant operating underperformance relative to expected historical or projected future results, 3) significant decline in our stock price or the stock price of our industry peers and/or 4) a decline in our market capitalization relative to our net book value. Our judgments regarding the existence of impairment indicators are based upon legal factors, market conditions and operational performance. Our Company adopted SFAS No. 142 in 2002 and in accordance therewith recorded as a change in accounting principle a non-cash impairment charge of $12.5 million upon adoption on January 1, 2002. On December 2, 2002, our selected annual measurement date, our Company recorded an additional non-cash charge of $7.4 million due to a further impairment of goodwill. As further described in Note 3 to the unaudited condensed consolidated financial statements included elsewhere herein, the Company acquired Intelix on June 2, 2003 and preliminarily recorded $1.4 million in goodwill and $0.5 million in identifiable intangibles, which are being amortized over 4-8 years.

The financial information that follows has been rounded in order to simplify its presentation. The amounts and percentages below have been calculated using the detailed financial information contained in the unaudited condensed consolidated financial statements, the notes thereto and the other financial data included in this Quarterly Report on Form 10-Q.

Results for the three and six months ended June 30, 2003 compared to results for the three and six months ended June 30, 2002

Service Revenues. Revenues for the three months ended June 30, 2003 increased $1.4 million, or 28%, to $6.2 million compared to $4.8 million for the three months ended June 30, 2002. Revenues for the six months ended June 30, 2003 increased $1.9 million, or 21% to $11.3 million compared to $9.4 million for the six months ended June 30, 2002. The revenue increase reflects the additional contracts related to the acquisition of Intelix since June 2, 2003, combined with organic growth from the positive effects of sales efforts designed to reduce customer concentration and engage new customers. For the three months ended June 30, 2003 and 2002, two customers and one customer each contributed more than 10% of revenues. For the six months ended June 30, 2003 and 2002, two customers each contributed more than 10% of revenues. For the three months ended June 30, 2003 and 2002, our three largest customers represented 78.6% and 81.8% of our revenues in the aggregate, respectively. For the six months ended June 30, 2003 and 2002, our three largest customers represented 78.6% and 83.6% of our revenues in the aggregate, respectively. Expenses reimbursed by our clients are also included in revenue in accordance with EITF topic D-103. Also see Note 11, Related Parties, to the unaudited condensed consolidated financial statements included elsewhere herein, for additional information.

16

Table of Contents

Cost of Services.Project personnel costs consist principally of salaries, payroll taxes, employee benefits and travel expenses for personnel dedicated to customer projects. These costs represent the most significant expense we incur in providing our services. Project personnel costs increased $0.3 million, or 12%, to $3.2 million for the three months ended June 30, 2003 compared to $2.9 million for the three months ended June 30, 2002. This increase is due to the increase in billable consultants from 124 at June 30, 2002 to 161 at June 30, 2003, which is in large part a result of the acquisition of Intelix during June 2003. For the six months ended June 30, 2003, project personnel costs decreased $0.2 million, or 3%, to $6.1 million, compared to $6.3 million for the six months ended June 30, 2002. The decrease is primarily the result of the net effect of the increase in billable headcount described above, combined with a workforce reduction in February 2002.

Gross Profit. Gross profit for the three months ended June 30, 2003 increased $1.0 million, or 52%, to $2.9 million, compared to $1.9 million for the three months ended June 30, 2002. For the six months ended June 30, 2003, gross profit increased $2.2 million or 69%, to $5.3 million compared to $3.1 million for the six months ended June 30, 2002. The increase in gross profit directly relates to the increase in billable hours and revenues combined with higher utilization during the period, in addition to $0.1 million in gross profit from the Intelix acquisition. Utilization rates were 83.3% for the three months ended June 30, 2003, compared to 69.8% for the three months ended June 30, 2002 and 80.2% for the six months ended June 30, 2003, compared to 64.3% for the six months ended June 30, 2002. Gross profit margin for the three months ended June 30, 2003 was 47.7%, compared to 44.7% during the three months ended June 30, 2002 and 46.4% during the six months ended June 30, 2003, compared to 33.2% during the six months ended June 30, 2002.

Selling, General and Administrative Expense (“SG&A”). SG&A increased $0.06 million, or 2%, to $2.5 million for the three months ended June 30, 2003 compared to $2.5 million for the three months ended June 30, 2002. For the six months ended June 30, 2003, SG&A decreased $0.02 million, or 1%, to $4.7 million compared to $4.7 million for the six months ended June 30, 2002. This decrease is directly related to reduced facilities and operating expenses, offset by accruals for performance-based bonuses, with a net effect that reflects a conscious effort to reduce costs and streamline operations. SG&A, as a percentage of revenue, was 41.2% and 51.6% for the three months ended June 30, 2003 and 2002, respectively and was 41.2% and 50.0% for the six months ended June 30, 2003 and 2002, respectively.

Depreciation and Amortization Expense. Depreciation and amortization expense decreased $0.02 million to $0.2 million for the three months ended June 30, 2003 compared to $0.2 million for the three months ended June 30, 2002. Depreciation and amortization expense also decreased $0.1 million to $0.4 million for the six months ended June 30, 2003 compared to $0.5 million for the six months ended June 30, 2002. This decrease reflects tighter spending controls on purchases of new fixed assets and a relative reduction in depreciation as older assets fully depreciate, offset by slightly higher depreciation due to the Intelix acquisition.

Restructuring. We implemented a workforce reduction in February 2002 to better align our consultant base to our expected revenues. The Company reduced headcount by nineteen percent (19%), or approximately 38 positions, which resulted in a restructuring charge of $349,000, which consisted primarily of severance and similar employee payroll related termination expenses. All restructuring amounts were paid by the end of the second quarter of 2002.

Operating Income (Loss). Operating income increased $1.0 million to $0.2 million for the three months ended June 30, 2003 compared to a net loss of ($0.8) million for the three months ended June 30, 2002. Operating income also increased $2.7 million to $0.2 million for the six months ended June 30, 2003 compared to a net loss of ($2.5) million for the six months ended June 30, 2002. Operating income increased from the prior year primarily due to higher utilization and a corresponding increase in revenue.

Interest Income (Expense), Net. We earned net interest income of $0.1 million for the three months ended June 30, 2003, compared to net interest income of $0.2 million for the three months ended June 30, 2002. We also earned net interest income of $0.2 million for the six months ended June 30, 2003 compared to net interest income of $0.4 million for the six months ended June 30, 2002. The decrease in net interest income is due to the reinvestment of matured securities into similar type securities at lower market interest yields and also due to the slightly lower average cash balances as a result of the acquisition of Intelix, common stock repurchases and discontinued operations payments.

17

Table of Contents

Provision for Income Taxes. The Company provides for income taxes at the end of each interim period based on the estimated effective tax rates for the full fiscal year. Cumulative adjustments to the tax provision are recorded in the interim period in which a change in the estimated annual effective rate is determined. We recorded a tax provision of $0.1 million and $0.2 million for the three and six months ended June 30, 2003, respectively, which represents an estimated effective rate of 40%, which includes state and federal income tax rates. We expect the effective tax rate to remain at approximately 40% for the remainder of 2003. The effective tax rate for 2002 was zero, primarily due to net operating losses.

Change in Accounting Principle.We adopted SFAS No. 142 on January 1, 2002 and, in accordance therewith, recorded as a change in accounting principle a non-cash charge of $12.5 million relating to an impairment of recorded goodwill. See Note 8 of the unaudited condensed consolidated financial statements included elsewhere herein.

Net Income (Loss).We generated net income of $0.2 million for the three months ended June 30, 2003 compared to a net loss of ($0.6) million for the three months ended June 30, 2002. We also generated net income of $0.2 million for the six months ended June 30, 2003 compared to a net loss of ($14.5) million for the six months ended June 30, 2002. Net income for the three and six months ended June 30, 2003, compared to the net loss for the three and six months ended June 30, 2002, was primarily affected by the increase in service revenues during 2003 over 2002 and the 2002 restructuring charge and the change in accounting principle charge of $12.5 million, as discussed above. Basic and diluted earnings (loss) per share was $0.01 and ($0.05) for the three months ended June 30, 2003 and 2002, respectively. Basic and diluted earnings (loss) per share was $0.02 and ($1.25) for the six months ended June 30, 2003 and 2002, respectively.

Liquidity and Capital Resources

The following table summarizes our cash flow activities for the periods indicated:

Three Months June 30, | Six Months Ended June 30, | |||||||||||||||

| 2003 | 2002 | 2003 | 2002 | |||||||||||||

| (In Thousands) | ||||||||||||||||

Cash flows provided by (used in): | ||||||||||||||||

Operating activities | $ | 263 | $ | 3 | ($ | 84 | ) | $ | (494 | ) | ||||||

Investing activities | (2,055 | ) | 9,796 | 2,015 | (2,467 | ) | ||||||||||

Financing activities | (708 | ) | (83 | ) | (1,005 | ) | (167 | ) | ||||||||

Extraordinary item | — | (56 | ) | — | (85 | ) | ||||||||||

Discontinued operating activities | (99 | ) | (708 | ) | (1,317 | ) | (2,922 | ) | ||||||||

Total cash (used) provided during the period | ($ | 2,599 | ) | $ | 8,952 | ($ | 391 | ) | ($ | 6,135 | ) | |||||

As of June 30, 2003, we had cash, cash equivalents and short-term investments of $42.3 million, a 10% decrease from the December 31, 2002 balance of $46.8 million. Working capital, which is defined as current assets less current liabilities, decreased to $44.1 million as of June 30, 2003 compared to $46.0 million as of December 31, 2002, which primarily reflects Edgewater’s net cash used for the acquisition of Intelix.

Our primary historical sources of funds are from operations and the proceeds from equity offerings and sales of businesses. Our principal historical uses of cash have been to fund working capital requirements and capital expenditures. We generally pay our consultants and associates bi-weekly for their services, while receiving payments from customers 30 to 60 days from the date of the invoice.

18

Table of Contents

Our Board of Directors, in September 2002, authorized management, subject to legal requirements, to use up to $20.0 million to repurchase our common stock over a period, as amended, to expire December 31, 2003. Repurchases have been and will be made from time to time on the open market at prevailing market prices or in negotiated transactions off the market. Under this repurchase program, during the three and six months ended June 30, 2003, we repurchased 167,277 and 238,209 shares, respectively, of our common stock for $0.7 million and $1.0 million, respectively. There were no repurchases made during the three and six months ended June 30, 2002. As part of this repurchase program, effective February 14, 2003, our Board authorized an SEC Rule 10b5-1 repurchase program with a broker that allows the Company to make more consistent repurchases of our common stock even during traditional blackout periods. As of June 30, 2003, the Company is authorized to repurchase up to $19 million of our common stock prior to December 31, 2003.

Net cash provided by operating activities was $0.3 million and $0.003 million for the three months ended June 30, 2003 and 2002, respectively. Net cash used in operating activities was ($0.08) million and ($0.5) million for the six months ended June 30, 2003 and 2002.

Net cash (used in) provided by investing activities was ($2.1) million and $9.8 million for the three months ended June 30, 2003 and 2002, respectively. Cash used in investing activities during the three months ended June 30, 2003 was primarily attributable to the purchase of Intelix, Inc., whereas the cash provided by investing activities during the three months ended June 30, 2002 was primarily attributable to the maturities of short-term investments. Cash provided by (used in) investing activities was $2.0 million and ($2.5) million for the six months ended June 30, 2003 and 2002. Cash provided by investing activities for the six months ended June 30, 2003 was attributed maturities of short-term investments combined with the purchase of Intelix and cash (used in) investing activities for the six months ended June 30, 2002 was primarily attributable to purchases of short-term investments. As of June 30, 2003, we have no commitments for capital expenditures and all capital expenditures are discretionary.

Net cash used in financing activities was $0.7 million and $0.1 million for the three months ended June 30, 2003 and 2002, respectively. Net cash used in financing activities was $1.0 million and $0.2 million for the six months ended June 30, 2003 and 2002, respectively. For the three and six months ended June 30, 2003, cash used in financing activities was primarily related to the repurchase of common stock and repayments on our capital lease obligations, net of proceeds from our employee stock purchase program. For the three and six months ended June 30, 2002, cash used in financing activities was primarily related to repayments on our capital lease obligations.

Net cash used by previously discontinued operations was $0.1 million and $0.7 million for the three months ended June 30, 2003 and 2002, respectively. Net cash used by previously discontinued operations was $1.3 million and $2.9 million for the six months ended June 30, 2003 and 2002, respectively. These amounts relate to expenses accrued in 2002 for discontinued operating activities, consisting principally of a $950,000 payment made in February 2003 for the litigation settlement related to discontinued operations and accrued for at December 31, 2002.

As a result of the above, our combined cash and cash equivalents decreased $2.6 million for the three months ended June 30, 2003, while increasing $9.0 million for the three months ended June 30, 2002. Cash and cash equivalents also decreased $0.4 million and $6.1 million for the six months ended June 30, 2003 and 2002, respectively. The aggregate cash and cash equivalents and short-term investments were $42.3 million and $46.8 million, as of June 30, 2003 and December 31, 2002, respectively.

We believe that our cash flows from operations and available cash will provide sufficient liquidity for our existing operations for the foreseeable future. We periodically reassess the adequacy of our liquidity position, taking into consideration current and anticipated operating cash flow, anticipated capital expenditures, business combinations, and public or private offerings of debt or equity securities.

On June 2, 2003, the Company acquired all of the outstanding common stock of Intelix, Inc. (“Intelix”), a provider of systems integration and custom software development services located in Fairfax, Virginia. The results of Intelix’s operations have been included in the Company’s accompanying unaudited condensed consolidated statements of operations since the acquisition date. Revenue, related to the acquisition, during the second quarter was $0.3 million. The acquisition was made to enhance Edgewater’s geographical presence and will provide additional vertical expertise in the telecommunications and real estate industries. The aggregate preliminary purchase price was $2.7 million, including cash paid to the Intelix stockholders of $0.9 million, assumed liabilities at fair value in the amount of $1.5 million, and direct costs incurred of $0.3 million.

Included in the purchase price is $165,000 of cash being held in escrow subject to the satisfaction of certain conditions of the sale and will be released within one year if such conditions are satisfied. In addition, the stockholders of Intelix are eligible for an additional cash payment in the first quarter of 2004 based upon a formula applied to earnings of the Intelix business for the twelve month period ended December 31, 2003. Any return of the escrowed amount or any additional payments to the Intelix stockholders, as well as other changes in estimates, will be accounted for as adjustments to the purchase price and would impact the final determination of the recorded goodwill.

Related to the purchase of Intelix, the Company preliminarily recorded $1.4 million in goodwill and $0.5 million in identifiable intangible assets, all in accordance with SFAS No. 141. The identifiable intangible assets are being amortized on the straight-line basis over their estimated useful lives (4-8 years). The goodwill is an indefinite lived asset in accordance with SFAS No. 142 and is subject to periodic review for impairment. This goodwill is not deductible for tax purposes. The Intelix business is included in the Company’s only reportable segment (see Note 10).

19

Table of Contents

During the second quarter of 2002, our Company was notified by the Internal Revenue Service (the “IRS”) that it would be auditing our consolidated income tax returns for the 1998, 1999 and 2000 fiscal years. Our Company has responded to various IRS information requests by delivering documents and answering questions. For the period of the fiscal years covered by the audit, we owned non-Solutions staffing related businesses, which were sold during the 2000 and 2001 fiscal years. The results of the IRS audit could have an impact on our deferred tax asset, however as of the date of the filing of this Form 10-Q, we do not believe any such impact would be material to our financial position.

Off Balance Sheet Arrangements, Contractual Obligations and Contingent Liabilities and Commitments

We lease office space and certain equipment under noncancelable operating and capital lease arrangements through 2009. Rent expense, including amounts paid to related parties for discontinued operations, was approximately $0.2 million, and $0.2 million for the three months ended June 30, 2003 and 2002, respectively and $0.4 million and $0.4 million for the six months ended June 30, 2003 and 2002.

The Company entered into employment agreements with certain executive officers and management personnel during the second quarter of 2003, which agreements provide for annual salaries, cost-of-living adjustments and additional compensation in the form of “performance-based” bonuses. Certain agreements include covenants against competition with our Company, which extend for a period of time after termination. These agreements extend for a four-year period through 2007.

20

Table of Contents

Special Note Regarding Forward Looking Statements

Some of the statements in this Quarterly Report on Form 10-Q (this “10-Q”) constitute forward-looking statements under Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended, including statements made with respect to significant customers, revenues, backlog, competitive and strategic initiatives, growth plans, potential stock repurchases, future results, tax consequences and liquidity needs. These statements involve known and unknown risks, uncertainties and other factors that may cause results, levels of activity, growth, performance, tax consequences or achievements to be materially different from any future results, levels of activity, growth, performance, tax consequences or achievements expressed or implied by such forward-looking statements. Such factors include, among other things, those listed below, as well as those further set forth under the heading “Business—Factors Affecting Finances, Business Prospects and Stock Volatility” in our 2002 Annual Report on Form 10-K as filed with the SEC on March 28, 2003.

The forward-looking statements included in this Form 10-Q relate to future events or our future financial performance. In some cases, you can identify forward-looking statements by terminology such as “may,” “believe,” “enable” “will,” “provide,” “anticipate,” “future,” “could,” “growth,” “increase,” “modifying,” “reacting,” or the negative of such terms or comparable terminology. These forward-looking statements inherently involve certain risks and uncertainties, although they are based on our current plans or assessments which are believed to be reasonable as of the date of this 10-Q. Factors that may cause actual results, financial statement effects, disposition plans or proceeds, goals, targets, objectives or repurchases to differ materially from those contemplated, projected, forecast, estimated, anticipated, planned or budgeted in such forward-looking statements include, among others, the following possibilities: (1) inability to execute upon growth objectives; (2) changes in industry trends, such as a decline in the demand for Solutions services or delays in industry-wide IT spending, whether on a temporary or permanent basis and/or delays by customers in initiating new projects or continuing new project milestones; (3) unanticipated events or the occurrence of fluctuations or variability in the matters identified under “Critical Accounting Policies”; (4) failure of our backlog to be converted to billable work and recorded as revenue; (5) inability of increased sales to result in increased revenues and/or increased consultant utilization rates; (6) inability to integrate the Intelix acquisition quickly and effectively within the Company’s consolidated group; (7) adverse developments and volatility involving debt, equity, currency, geopolitical or technology market conditions; (8) the occurrence of lawsuits or adverse results in tax matters; (9) failure to obtain new customers or retain significant existing customers; (10) loss of key executives; (11) general economic and business conditions (whether foreign, national, state or local) which include, but are not limited to, changes in interest or currency exchange rates; (12) failure of the middle market and the needs of middle-market enterprises for business services to develop as anticipated; (13) inability to recruit and retain professionals with the high level of information technology skills and experience needed to provide our services; (14) inability to repurchase shares in the future on terms acceptable to us; and/or (15) any changes in ownership, or adverse developments concerning the IRS audit of our corporate tax returns for the 1998-2000 fiscal years, that would result in a limitation on the use of the net operating loss carry-forward under applicable tax laws, which is referred to as a net deferred tax asset of approximately $22.4 million as of June 30, 2003. In evaluating these statements, you should specifically consider various factors described above as well as the risks outlined under Item I “Business—Factors Affecting Finances, Business Prospects and Stock Volatility” in our 2002 Form 10-K filed with the SEC on March 28, 2003. These factors may cause our actual results to differ materially from those contemplated, projected, anticipated, planned or budgeted in any such forward-looking statements.

Although we believe that the expectations in the forward-looking statements are reasonable, we cannot guarantee future results, levels of activity, performance, growth or achievements. However, neither we nor any other person assumes responsibility for the accuracy and completeness of such statements. We are under no duty to update any of the forward-looking statements after the date of this Form 10-Q to conform such statements to actual results.

ITEM 3. QUANTITATIVE AND QUALITATIVE DISCLOSURES ABOUT MARKET RISK

Our primary financial instruments include investments in money market funds, short-term municipal bonds, commercial paper and U.S. government securities that are sensitive to market risks and interest rates. The investment portfolio is used to preserve our capital until it is required to fund operations, to fund strategic acquisitions, or other transactions which may be authorized by our Company’s Board of Directors. None of our market-risk sensitive instruments are held for trading purposes. We do not purchase derivative financial instruments.

21

Table of Contents

ITEM 4. CONTROLS AND PROCEDURES

Evaluation of Disclosure Controls and Procedures

General. As of June 30, 2003 (the “Evaluation Date”), the Company evaluated the effectiveness of our “disclosure controls and procedures” (“Disclosure Controls”) and the Company’s “internal controls and procedures for financial reporting” (“Internal Controls”). This evaluation (the “Controls Evaluation”) was carried out by the Company’s disclosure controls and procedures committee under the supervision and with the participation of management, including our President and Chief Executive Officer (“the CEO”) and Chief Financial Officer (“the CFO”). Rules adopted by the SEC require that in this section of this report the Company present the conclusions of the CEO and the CFO about the effectiveness of our Disclosure Controls and Internal Controls as of the Evaluation Date.

CEO and CFO Certifications. Appearing as exhibits 31.1 and 31.2 to this quarterly report, there are two separate forms of “Certifications” of the CEO and the CFO. The Certifications are required under Rule 13a-14(a) of the Exchange Act (the “13a-14 Certifications”). This section of this report, which you are currently reading, is the information concerning the Controls Evaluation referred to in the 13a-14 Certifications and this information should be read in conjunction with the 13a-14 Certifications for a more complete understanding of the topics presented. In addition to the 13a-14 Certifications, a certification of the CEO and the CFO under 18 U.S.C. §1350 is included as Exhibit 32 of this Quarterly Report. The 1350 Certification requires the CEO and the CFO to certify to the best of their knowledge that this Quarterly Report complies with Section 13(a) or 15(d) of the Exchange Act (as defined below) and that such Quarterly Report fairly presents, in all material respects, the financial condition of the Company at the end of the period covered by this Quarterly Report. You are referenced to this certification for more information regarding the 1350 Certification.

Disclosure Controls and Internal Controls. Disclosure Controls are procedures that are designed with the objective of ensuring that information required to be disclosed in our reports filed under the Securities Exchange Act of 1934 (“Exchange Act”), such as this report, is recorded, processed, summarized and reported within the time periods specified in the SEC rules. Disclosure Controls are also designed with the objective of ensuring that such information is accumulated and communicated to our management, including the CEO and the CFO, as appropriate to allow timely decisions regarding required disclosure. Internal Controls are procedures which are designed with the objective of providing reasonable assurance that: (1) our transactions are properly authorized; (2) our assets are safeguarded against unauthorized or improper use; and (3) our transactions are properly recorded and reported, all to permit the preparation of our financial statements in conformity with generally accepted accounting principles. However, any control system, no matter how well conceived and operated, can provide only reasonable, not absolute, assurance that the objectives of the control system are met.

Scope of the Controls Evaluation. The CEO’s and the CFO’s evaluation of our Disclosure Controls and our Internal Controls included a review of the controls’ objectives and design, the controls’ implementation by the Company and the effect of the controls on the information generated for use in this report. This type of evaluation will be done on a quarterly basis so that the conclusions concerning controls effectiveness can be reported in our Quarterly and Annual Reports. Our Internal Controls are also evaluated on an ongoing basis by other personnel in our finance and accounting department.