Use these links to rapidly review the document

TABLE OF CONTENTS

INDEX TO CONSOLIDATED FINANCIAL STATEMENTS

Filed pursuant to Rule 424(b)(4)

Registration File No. 333-110932

Prospectus

3,120,000 Shares

Common Stock

Coldwater Creek Inc. and the selling stockholders named in this prospectus are offering 2,000,000 shares and 1,120,000 shares, respectively, of our common stock. We will not receive any of the proceeds from the sale of shares by the selling stockholders.

Our common stock is quoted on the Nasdaq National Market under the symbol "CWTR." The last reported sale price of our common stock on the Nasdaq National Market on May 20, 2004 was $21.01 per share.

Investing in our common stock involves a high degree of risk. See "Risk Factors" beginning on page 5.

| | Per Share | Total | ||

|---|---|---|---|---|

| Offering price | $20.50 | $63,960,000 | ||

| Discounts and commissions to underwriters | $1.13 | $3,517,800 | ||

| Proceeds to Coldwater Creek, before expenses | $19.37 | $38,745,000 | ||

| Proceeds to the selling stockholders, before expenses | $19.37 | $21,697,200 | ||

Neither the Securities and Exchange Commission nor any state securities regulator has approved or disapproved of these securities or determined if this prospectus is accurate or complete. Any representation to the contrary is a criminal offense.

The underwriters will purchase the shares on a firm commitment basis.

We and certain of the selling stockholders have granted the underwriters a 30-day option to purchase up to an additional 468,000 shares of common stock to cover over-allotments. The underwriters expect to deliver the shares of common stock to investors on or about May 26, 2004.

| Banc of America Securities LLC | ||||

| Morgan Stanley | ||||

| RBC Capital Markets | ||||

The date of this prospectus is May 20, 2004.

You should rely only on the information contained or incorporated by reference in this prospectus. We, the selling stockholders and the underwriters have not authorized anyone to provide you with information different from that contained in this prospectus. We are not making an offer to sell, and are not seeking offers to buy, these securities in any jurisdiction where the offer or sale is not permitted. You should assume that the information contained in this prospectus is accurate as of the date on the cover of this prospectus only. Our business, financial condition, results of operations and prospects may have changed since that date.

Information contained in our website does not constitute part of this prospectus.

Coldwater Creek®, Coldwater Creek Spirit® and the stylized Coldwater Creek Inc. logo used in this prospectus are trademarks of Coldwater Creek Inc. All other product and service names used are trademarks or service marks, registered or otherwise, of their respective owners.

In this prospectus, the "company," "Coldwater Creek," "we," "us," and "our" refer to Coldwater Creek Inc., a Delaware corporation, and its subsidiaries.

References to a fiscal year refer to the calendar year in which the fiscal year commences. In December 2002, our Board of Directors approved a change in our fiscal year end from the Saturday nearest February 28 to the Saturday nearest January 31, effective in 2003, in order to align our financial reporting schedule with the majority of other national retail companies. The financial statements for the fiscal year ended February 1, 2003 included in this prospectus cover the 11-month transition period of March 3, 2002 through February 1, 2003 and do not reflect a full 12-month fiscal year as presented in the financial statements for the other fiscal year periods appearing elsewhere in this prospectus.

Our Board of Directors declared two 50% stock dividends, each having the effect of a 3-for-2 stock split, on December 19, 2002 and August 4, 2003, respectively. Unless otherwise indicated, the share, per share and stock price information contained in our financial statements and appearing elsewhere in this prospectus have been adjusted to reflect these stock dividends.

We operate in two segments, direct and retail. Beginning in the quarter ended May 3, 2003, we reclassified our outlet stores and phone and Internet orders that originate in our retail stores from our direct segment to our retail segment to reflect the manner in which these segments are currently managed. We have reclassified prior period financial statements on a consistent basis for fiscal years 2002, 2001 and 2000. Due to information systems limitations, we have not reclassified the financial statements for periods prior to fiscal 2000 because it was not practicable for us to do so. In addition, management believes that the reclassification of these prior periods would be immaterial.

When we use the term "active customers" in this prospectus, we are referring to customers who have made a purchase with us through any of our sales channels during the preceding 12 months. Active customers do not include retail customers who have not provided identifying information to us.

We have cited industry data from the U.S. Census Bureau and NPD Group. We have not independently verified this data.

ii

This summary highlights information contained elsewhere in this prospectus. You should read the following summary together with the more detailed information and consolidated financial statements and the related notes appearing elsewhere in this prospectus or incorporated herein by reference. This prospectus contains forward-looking statements that involve risks and uncertainties. We urge you to read the entire prospectus carefully, especially the risks of investing in our common stock discussed under the heading "Risk Factors" and elsewhere in this prospectus, including information incorporated by reference in this prospectus from our other filings with the SEC.

Our Business

Coldwater Creek Profile

Coldwater Creek is a specialty retailer of women's apparel, accessories, jewelry and gift items. Since we were founded in 1984, we have grown from a catalog company to a multi-channel retailer generating $518.8 million in net sales in fiscal 2003. We have established a differentiated brand by offering exceptional value through a unique, proprietary merchandise assortment that reflects a sophisticated yet relaxed and casual lifestyle, coupled with superior customer service. Our target customers are women between the ages of 30 and 60, a group that spent in excess of $29 billion on apparel in 2002.

We reach our customers through our direct segment, which comprises our catalog and e-commerce businesses, and our rapidly expanding base of retail stores. We believe this multi-channel approach allows us to cross-promote the Coldwater Creek brand and meet our customers' apparel and accessory needs by providing them convenient access to our merchandise lines regardless of the preferred shopping channel.

During fiscal 2003, we sent 117.8 million catalogs, which generated $175.9 million in net sales via phone and mail orders. Our catalogs also serve as a valuable marketing tool and help us promote our website and stores. Our website,www.coldwatercreek.com, provides a convenient shopping alternative for our customers and is a cost-effective means to expand our customer base. Our website generated $148.3 million in net sales in fiscal 2003. We currently have over 2.2 million e-mail addresses to which we regularly send customized e-mails.

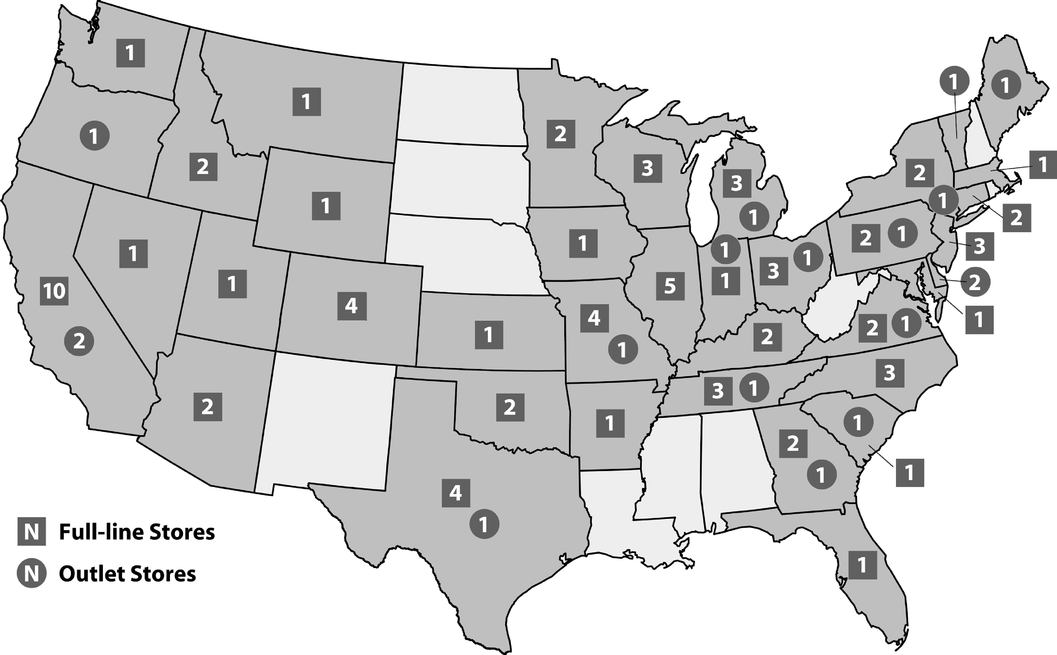

Our retail segment is the key driver in our growth strategy, and, in fiscal 2003, accounted for $194.6 million in net sales, or 37.5% of our total net sales. As of January 31, 2004, our retail segment was comprised of 66 full-line retail stores, 25 of which had been opened in fiscal 2003, as well as two resort stores and 16 merchandise clearance outlet stores in 51 markets. We currently plan to open 45 new full-line retail stores in fiscal 2004, including two stores opened in March 2004, and 40 to 50 new stores in fiscal 2005.

Business Strategies

We believe our success and future growth will be the result of consistent execution of the following business strategies:

- •

- We target a highly desirable, underserved demographic of women between the ages of 30 and 60, with median household incomes in excess of $75,000. We believe women in this demographic have limited shopping options that cater specifically to their tastes and needs;

- •

- We differentiate our brand through our selection of unique, proprietary merchandise and the design of our retail stores, catalogs and e-commerce website, all of which embody a casual and relaxed lifestyle and attitude that appeals to our customers;

- •

- We leverage the integration of our three channels to enhance the visibility of our brand, accessibility to our merchandise and customer loyalty;

1

- •

- We provide an extraordinary shopping experience through exceptional customer service to further build our loyal customer base and monitor key service metrics to continually improve our customer service;

- •

- We leverage our data collection discipline as a direct marketer to promote and optimize the productivity of all our channels; and

- •

- We have recruited a management team with extensive experience in retail, merchandising, brand-building, real estate, information technology and finance gained from a variety of retail, direct marketing and apparel companies.

Growth Strategy

We believe that refinements to our retail store model and infrastructure developments made over the past four years have positioned us to enter a phase of more rapid retail store growth. Our management team is committed to executing the following key growth strategies:

- •

- rapidly expanding our retail operations to address what we believe is an opportunity for us to grow to 400 to 500 stores in up to 275 to 300 identified markets nationwide over the next six to eight years;

- •

- further promoting our brand and providing multiple points of access to our merchandise; and

- •

- improving our operating margins as we grow our business and open more retail stores.

Recent Developments

On May 19, 2004, we announced unaudited results for the first quarter ended May 1, 2004. Net income for the three-month period ended May 1, 2004, increased $3.5 million, or 185.0 percent, to $5.5 million, or $0.22 per diluted share, compared with net income of $1.9 million, or $0.08 per diluted share for the three-month period ended May 3, 2003. Net sales in the fiscal 2004 first quarter increased 8.0 percent to $124.5 million from $115.2 million in the fiscal 2003 first quarter.

Net sales from our retail segment increased 69.5 percent to $56.5 million, on a 42 percent increase in store square footage in the fiscal 2004 first quarter, from $33.3 million in the fiscal 2003 first quarter. Retail segment net sales represented 45.4 percent of our total net sales in the fiscal 2004 first quarter, compared with 28.9 percent in the fiscal 2003 first quarter.

We operated 71 full-line retail stores at the end of the fiscal 2004 first quarter, compared with 44 full-line retail stores at the end of the fiscal 2003 first quarter.

Net sales from our direct segment decreased 17.0 percent to $68.0 million in the fiscal 2004 first quarter from $81.9 million in the fiscal 2003 first quarter. Direct segment net sales represented 54.6 percent of our total net sales in the fiscal 2004 first quarter, compared with 71.1 percent in the fiscal 2003 first quarter. The decrease in direct segment net sales is a result of planned reductions in catalog circulation and less promotional activity.

Gross profit for the fiscal 2004 first quarter was $54.4 million, or 43.7 percent of net sales, compared with $45.1 million, or 39.2 percent of net sales, for the fiscal 2003 first quarter. The improvement in gross profit dollars and rate was primarily attributable to improved merchandise margins on sales in all channels and, to a lesser extent, to improved leveraging of our full-line retail store occupancy costs.

Selling, general and administrative expenses for the fiscal 2004 first quarter were $45.4 million, or 36.5 percent of net sales, compared with $42.1 million, or 36.6 percent of net sales, for the fiscal 2003 first quarter. Selling, general and administrative expenses increased due to additional employee expenses, primarily associated with our retail expansion, partially offset by a decrease in catalog circulation.

Income from operations for the fiscal 2004 first quarter was $9.0 million, or 7.2 percent of net sales, compared with income from operations of $3.0 million, or 2.6 percent of net sales, for the fiscal 2003 first quarter.

2

Our principal executive offices are located at One Coldwater Creek Drive, Sandpoint, Idaho 83864, and our telephone number is (208) 263-2266. We maintain a website atwww.coldwatercreek.com. Information contained in our website is not part of this prospectus.

The Offering

| Common stock offered by Coldwater Creek | 2,000,000 shares | |

Common stock offered by the selling stockholders | 1,120,000 shares | |

Total common stock offered | 3,120,000 shares | |

Common stock to be outstanding after the offering | 26,166,201 shares | |

Use of proceeds | We currently intend to use the net proceeds to continue to expand our retail operations and for working capital and other general corporate purposes. We will not receive any proceeds from the sale of common stock by the selling stockholders. See "Use of Proceeds". | |

Nasdaq National Market Symbol | "CWTR" |

The number of shares of common stock to be outstanding after this offering is based on 24,166,201 shares of our common stock outstanding as of January 31, 2004, and excludes:

- •

- 1,720,105 shares of common stock issuable upon the exercise of options outstanding under our Stock Option/Stock Issuance Plan, as amended, at a weighted average exercise price of $8.99 per share, of which options to purchase 1,113,041 shares are exercisable, having a weighted average exercise price of $8.98 per share;

- •

- 630,116 shares reserved for issuance under our Stock Option/Stock Issuance Plan, as amended; and

- •

- 1,460,264 shares of common stock reserved for issuance under our Employee Stock Purchase Plan, as amended.

Unless otherwise noted, all information contained in this prospectus assumes that the underwriters' over-allotment option is not exercised and reflects the adjustments for our two 50% stock dividends, each having the effect of a 3-for-2 stock split.

3

Summary Consolidated Financial Data

(in thousands, except per share and store data)

| | Fiscal Year Ended | |||||||||

|---|---|---|---|---|---|---|---|---|---|---|

| | March 2, 2002 (52 weeks) | February 1, 2003(a) (48 weeks) | January 31, 2004 (52 weeks) | |||||||

| Statement of Operations Data: | ||||||||||

| Net sales | $ | 464,024 | $ | 473,172 | $ | 518,844 | ||||

| Cost of sales | 272,665 | 284,406 | 316,026 | |||||||

| Gross profit | 191,359 | 188,766 | 202,818 | |||||||

| Selling, general and administrative expenses | 188,902 | 173,330 | 182,210 | |||||||

| Income from operations | 2,457 | 15,436 | 20,608 | |||||||

| Interest, net, and other | 483 | 170 | (93 | ) | ||||||

| Income tax provision | 1,140 | 6,249 | 8,037 | |||||||

| Net income | $ | 1,800 | $ | 9,357 | $ | 12,478 | ||||

| Net income per share — basic(b) | $ | 0.08 | $ | 0.39 | $ | 0.52 | ||||

| Net income per share — diluted(b) | $ | 0.07 | $ | 0.39 | $ | 0.51 | ||||

Selected Operating Data: | ||||||||||

| Total catalogs mailed | 161,000 | 136,000 | 117,784 | |||||||

| Total active customers | 2,600 | 2,700 | 2,601 | |||||||

| Number of stores at period end(c) | 29 | 43 | 68 | |||||||

| Average square feet per store(c) | 8,200 | 7,600 | 6,700 | |||||||

| | As of January 31, 2004 | |||||

|---|---|---|---|---|---|---|

| | Actual | As Adjusted(d) | ||||

| Balance Sheet Data: | ||||||

| Cash and cash equivalents | $ | 45,754 | $ | 83,334 | ||

| Working capital | 50,738 | 88,318 | ||||

| Total assets | 210,657 | 248,237 | ||||

| Total debt(e) | — | — | ||||

| Total stockholders' equity | 119,797 | 157,377 | ||||

- (a)

- Fiscal 2002 is an 11-month transition period as a result of the change in our fiscal year end from the Saturday nearest February 28 to the Saturday nearest January 31, effective February 1, 2003.

- (b)

- The net income per share amounts reflect two 50% stock dividends, each having the effect of a 3-for-2 stock split, declared by our Board of Directors on December 19, 2002 and August 4, 2003, respectively.

- (c)

- Excludes outlet stores and includes our two resort stores.

- (d)

- The as adjusted balance sheet data as of January 31, 2004 reflects the receipt of the estimated net proceeds from the sale of 2,000,000 shares of our common stock in this offering at the public offering price of $20.50 per share, after deducting underwriting discounts and commissions and our estimated offering expenses.

- (e)

- We currently have a $60 million unsecured revolving line of credit, and, as of the date of this prospectus, we have not borrowed under this facility.

4

You should carefully consider the following risk factors and all other information contained or incorporated by reference in this prospectus before purchasing shares of our common stock. Investing in our common stock involves a high degree of risk. The risks and uncertainties described below are not the only ones that we face. Additional risks and uncertainties not presently known to us or that we currently believe are immaterial also may negatively impact our business. If any of the events described in the following risks occur, our business, results of operations and financial condition could be materially adversely affected. In addition, the trading price of our common stock could decline due to any of the events described in these risks, and you may lose all or part of your investment.

Risks Related to Our Business

We may be unable to successfully implement our retail store rollout strategy, which could result in significantly lower revenue growth.

The key driver of our growth strategy is our retail store expansion. We currently plan to open 45 new stores in fiscal 2004, including two stores opened in March 2004, and 40 to 50 new stores in fiscal 2005. We believe we will ultimately have 400 to 500 retail stores. However, there can be no assurance that these stores will be opened, will be opened in a timely manner, or, if opened, that these stores will be profitable. Our ability to open our planned retail stores depends on our ability to successfully:

- •

- Identify or secure premium retail space;

- •

- Negotiate site leases or obtain favorable lease terms for the retail store locations we identify; and

- •

- Avoid construction delays and cost overruns in connection with the build-out of new stores.

Any miscalculations or shortcomings in the planning and control of our retail growth strategy could materially impact our results of operations and our financial condition.

We may continue to refine our retail store model, which could delay our planned retail store rollout and result in slower revenue growth.

We have made numerous refinements in our retail store format since opening our first full-line store in 1999. Our retail model may undergo further refinements as we gain experience operating more stores. If we determine to make further refinements to our store model, it may delay the progress of our retail store rollout, which could slow our anticipated revenue growth. We are required to make long-term financial commitments when leasing retail store locations, which would make it more costly for us to close or relocate stores that do not prove to be successful. Furthermore, retail store operations entail substantial fixed costs, including costs associated with maintaining inventory levels, leasehold improvements, fixtures, store design and information and management systems, and we must continue to make these investments to maintain our current and future stores.

We may not select optimal locations for our retail stores, which could harm our net sales.

The success of individual retail stores will depend to a great extent on locating them in desirable shopping venues in markets that include our target demographic. The success of individual stores may depend on the success of the shopping malls or lifestyle centers in which they are located. In addition, the demographic and other marketing data we rely on in determining the location of our stores cannot predict future consumer preferences and buying trends with complete accuracy. As a result, retail stores we open may not be profitable or may be less successful than we anticipate.

5

We may be unable to manage the costs associated with our catalog business, which could harm our results of operations.

We incur substantial costs associated with our catalog mailings, including paper, postage, merchandise acquisition and human resource costs associated with catalog layout and design, production and circulation and increased inventories. Most of these costs are incurred prior to mailing. As a result, we are not able to adjust the costs of a particular catalog mailing to reflect the actual subsequent performance of the catalog. Increases in U.S. Postal Service rates and the cost of telecommunications services, paper and catalog production could significantly increase our catalog production costs and result in lower profits for our catalog business to the extent we are unable to pass these costs onto our customers or implement more cost effective printing, mailing or distribution systems. Because our catalog business accounts for a significant portion of total net sales, any performance shortcomings experienced by our catalog business would likely have a material adverse effect on our overall business, financial condition, results of operations and cash flows.

Response rates to our catalogs could decline, which would negatively impact our net sales and results of operations.

Response rates to our catalog mailings and, as a result, the net sales generated by each catalog mailing, can be affected by factors beyond our control such as changing consumer preferences, willingness to purchase goods through catalogs, weak economic conditions and uncertainty, and unseasonable weather in key geographic markets. A portion of our catalog mailings are to prospective customers. These mailings involve risks not present in mailings to our existing customers, including lower and less predictable response rates. Additionally, it has become more difficult for us and other direct retailers to obtain quality prospecting mailing lists, which may limit our ability to maintain the size of our active catalog customer list. Lower response rates could result in lower-than-expected full-price sales and higher-than-expected clearance sales at substantially reduced margins.

Our direct segment sales may decline if we are unable to timely mail our catalogs.

The timely mailing of our catalogs is critical to the success of our direct business, particularly during our peak holiday selling seasons, and requires the involvement of many different groups within our organization as well as outside vendors. Consequently, we are subject to potential delays at multiple points throughout the process of producing a catalog, many of which we may be unable to prevent. Any delay in mailing a catalog could cause customers to forego or defer purchases from us.

Consumers concerns about purchasing items via the Internet as well as external or internal infrastructure system failures could negatively impact our e-commerce sales or cause us to incur additional costs.

Our e-commerce business is vulnerable to consumer privacy concerns relating to purchasing items over the Internet, security breaches, and failures of internet infrastructure and communications systems. If consumer confidence in making purchases over the Internet declines as a result of privacy or other concerns, our e-commerce net sales could decline. We may be required to incur increased costs to address or remedy any system failures or security breaches.

We may be unable to manage expanding operations and the complexities of our multi-channel strategy, which could harm our results of operations.

During the past few years, with the implementation of our multi-channel business model, our overall business has become substantially more complex. This increasing complexity has resulted and will continue to result in increased demands on our managerial, operational and administrative resources and has forced us to

6

develop new expertise. In order to manage our complex multi-channel strategy, we will be required to continue, among other things, to:

- •

- improve and integrate our management information systems and controls, including installing and integrating a new inventory management system;

- •

- expand our distribution capabilities;

- •

- attract, train and retain qualified personnel, including middle and senior management, and manage an increasing number of employees; and

- •

- obtain sufficient manufacturing capacity from vendors to produce our merchandise.

We may be unable to anticipate changing customer preferences and to respond in a timely manner by adjusting our merchandise offerings, which could result in lower sales.

Our future success will depend on our ability to continually select the right merchandise assortment, maintain appropriate inventory levels and creatively present merchandise in a way that is appealing to our customers. Consumer preferences cannot be predicted with certainty, as they continually change and vary from region to region. On average, we begin the design process for our apparel nine to ten months before merchandise is available to our customers, and we typically begin to make purchase commitments four to six months in advance. These lead times make it difficult for us to respond quickly to changing consumer preferences and amplify the consequences of any misjudgments we might make in anticipating customer preferences. Consequently, if we misjudge our customers' merchandise preferences or purchasing habits, our sales may decline significantly, and we may be required to mark down certain products to significantly lower prices to sell excess inventory, which would result in lower margins.

We depend on key vendors for timely and effective sourcing and delivery of our merchandise. If these vendors are unable to timely fill orders or meet our quality standards, we may lose customer sales and our reputation may suffer.

Our direct business depends largely on our ability to fulfill orders on a timely basis, and our direct and retail businesses largely depend on our ability to keep appropriate levels of inventory in our distribution center and our stores. As we grow our retail business, we may experience difficulties in obtaining sufficient manufacturing capacity from vendors to produce our merchandise. We generally maintain non-exclusive relationships with multiple vendors that manufacture our merchandise. However, we have no contractual assurances of continued supply, pricing or access to new products, and any vendor could discontinue selling to us at any time. If we were required to change vendors or if a key vendor were unable to supply desired merchandise in sufficient quantities on acceptable terms, we may experience delays in filling customer orders or delivering inventory to our stores until alternative supply arrangements are secured, which could result in lost sales and a decline in customer satisfaction.

Our increasing reliance on foreign vendors will subject us to uncertainties that could impact our cost to source merchandise and delay or prevent merchandise shipments.

As we expand our retail stores and our merchandise volume requirements increase, we expect to source merchandise directly from foreign vendors, particularly those located in Asia. This will expose us to new and greater risks and uncertainties, the occurrence of which could substantially impact our ability to source merchandise through foreign vendors and to realize any perceived cost savings. We will be subject to, among other things:

- •

- burdens associated with doing business overseas, including the imposition of, or increases in, tariffs or import duties, or import/export controls or regulation, and the availability of quotas, as well as credit assurances we are required to provide to foreign vendors;

7

- •

- declines in the relative value of the U.S. dollar to other foreign currencies;

- •

- failure of foreign vendors to adhere to our quality assurance standards or our standards for conducting business;

- •

- changing or uncertain economic conditions, political uncertainties or unrest, or epidemics or other health or weather-related events in foreign countries resulting in the disruption of trade from exporting countries; and

- •

- restrictions on the transfer of funds or transportation delays or interruptions.

We may be unable to fill customer orders efficiently, which could harm customer satisfaction.

If we are unable to efficiently process and fill customer orders, customers may cancel or refuse to accept orders, and customer satisfaction could be harmed. We are subject to, among other things:

- •

- failures in the efficient and uninterrupted operation of our customer service call centers or our sole distribution center in Mineral Wells, West Virginia, including system failures caused by telecommunications systems providers and order volumes that exceed our present telephone or Internet system capabilities;

- •

- delays or failures in the performance of third parties, such as shipping companies and the U.S. postal and customs services, including delays associated with labor disputes, labor union activity, inclement weather, natural disasters, health epidemics and possible acts of terrorism; and

- •

- disruptions or slowdowns in our order processing or fulfillment systems resulting from the recently increased security measures implemented by U.S. customs, or from homeland security measures, telephone or Internet down times, system failures, computer viruses, electrical outages, mechanical problems, human error or accidents, fire, natural disasters or comparable events.

We have a liberal merchandise return policy, and we may experience a greater number of returns than we anticipate.

As part of our customer service commitment, we maintain a liberal merchandise return policy that allows customers to return any merchandise, virtually at any time and for any reason, and regardless of condition. We make allowances in our financial statements for anticipated merchandise returns based on historical return rates and our future expectations. These allowances may be exceeded, however, by actual merchandise returns as a result of many factors, including changes in the merchandise mix or consumer preferences or confidence. Any significant increase in merchandise returns or merchandise returns that exceed our allowances could materially adversely affect our financial condition, results of operations and cash flows.

Our quarterly results of operations fluctuate and may be negatively impacted by a failure to predict sales trends and by seasonal influences.

Our net sales, operating results, liquidity and cash flows have fluctuated, and will continue to fluctuate, on a quarterly basis, as well as on an annual basis, as a result of a number of factors, including, but not limited to, the following:

- •

- the number and timing of our full-line retail store openings;

- •

- the timing of our catalog mailings and the number of catalogs we mail;

- •

- our ability to accurately estimate and accrue for merchandise returns and the costs of obsolete inventory disposition;

- •

- the timing of merchandise receiving and shipping, including any delays resulting from labor strikes or slowdowns, adverse weather conditions, health epidemics or national security measures; and

8

- •

- shifts in the timing of important holiday selling seasons relative to our fiscal quarters, including Valentine's Day, Easter, Mother's Day, Thanksgiving and Christmas, and the day of the week on which certain important holidays fall.

Our results continue to depend materially on sales and profits from the November and December holiday shopping season. In anticipation of traditionally increased holiday sales activity, we incur certain significant incremental expenses, including the hiring of a substantial number of temporary employees to supplement our existing workforce. If, for any reason, we were to realize lower-than-expected sales or profits during the November and December holiday selling season, our financial condition, results of operations, including related gross margins, and cash flows for the entire fiscal year would be materially adversely affected.

We face substantial competition from discount retailers in the women's apparel industry.

We believe our customers are willing to pay slightly higher prices for our unique merchandise and superior customer service. However, we face substantial competition from discount retailers, such as Kohl's and Target, for basic elements in our merchandise lines, and our net sales may decline if we are unable to differentiate our merchandise and shopping experience from these discount retailers. In addition, the retail apparel industry has experienced significant price deflation over the past several years largely due to the downward pressure on retail prices caused by discount retailers. This price deflation may make it more difficult for us to maintain our gross margins and to compete with retailers that have greater purchasing power than we have. Furthermore, because we currently source a significant percentage of our merchandise through intermediaries and from suppliers and manufacturers located in the United States and Canada, where labor and production costs, on average, tend to be higher, our gross margins may be lower than those of competing retailers.

Our success is dependent upon our senior management team.

Our future success depends largely on the efforts of Dennis Pence, Chairman and Chief Executive Officer; Georgia Shonk-Simmons, President and Chief Merchandising Officer; Melvin Dick, Executive Vice President and Chief Financial Officer; and Dan Griesemer, Executive Vice President, Retail Stores. The loss of any of these individuals or other key personnel could have a material adverse effect on our business. Furthermore, the location of our corporate headquarters in Sandpoint, Idaho may make it more difficult to replace key employees who leave us, or to add qualified employees we will need to manage our further growth.

Prior to joining our company, Melvin Dick, our Executive Vice President and Chief Financial Officer, served as the lead engagement partner for Arthur Andersen's audit of WorldCom's consolidated financial statements for the fiscal year ended December 31, 2001, and its subsequent review of WorldCom's condensed consolidated financial statements for the fiscal quarter ended March 31, 2002. The ongoing investigation of the WorldCom matter may require Mr. Dick's attention, which may impair his ability to devote his full time and attention to our company. Further, Mr. Dick's association with the WorldCom matter may adversely affect customers' or investors' perception of our company.

Lower demand for our merchandise could reduce our gross margins and cause us to slow our retail expansion.

Our merchandise is comprised primarily of discretionary items, and demand for our merchandise is affected by a number of factors that influence consumer spending. Lower demand may cause us to move more full-price merchandise to clearance, which would reduce our gross margins, and could adversely affect our liquidity (including compliance with our debt covenants) and, therefore, slow the pace of our retail expansion. We have maintained conservative inventory levels, which we believe will make us less vulnerable to sales shortfalls. However, low inventory levels also carry the risk that, if demand is stronger than we

9

anticipate, we will be forced to backorder merchandise, which may result in lost sales and lower customer satisfaction.

Our tax collection policy may expose us to the risk that we may be assessed for unpaid taxes.

Many states have attempted to require that out-of-state direct marketers and e-commerce retailers whose only contact with the taxing state are solicitations and delivery of purchased products through the mail or the Internet collect sales taxes on sales of products shipped to their residents. The U.S. Supreme Court has held that these states, absent congressional legislation, may not impose tax collection obligations on an out-of-state mail order or Internet company. Although we believe that we have collected sales tax where we are required to do so under existing law, state tax authorities may disagree, and we could be subject to assessments for uncollected sales taxes, as well as penalties and interest and demands for prospective collection of such taxes. Furthermore, if Congress enacts legislation permitting states to impose sales tax collection obligations on out-of-state catalog or e-commerce businesses, or if we are otherwise required to collect additional sales taxes, such tax collection obligations may negatively affect customer response and could have a material adverse effect on our financial position, results of operations and cash flows. In addition, as we open more retail stores, our tax collection obligations will increase significantly and complying with the greater number of state and local tax regulations to which we will be subject may strain our resources.

In fiscal 2003, we accrued $1.0 million for expected tax liabilities resulting from an error in our Canadian tax returns related to refunds of the Canadian Goods and Services Tax, known as GST. We believe that we have accrued an appropriate amount for the expected Canadian tax liabilities. However, the Canadian taxing authorities have not completed their review of our GST returns and may determine that we owe additional tax, in which case we may incur additional expenses.

Risks Relating to This Offering

Our stock price has fluctuated and may continue to fluctuate widely.

The market price for our common stock has fluctuated and has been and will continue to be significantly affected by, among other factors, our quarterly operating results, changes in any earnings estimates publicly announced by us or by analysts, customer response to our merchandise offerings, the size of our catalog mailings, the timing of our retail store openings or of important holiday seasons relative to our fiscal periods, seasonal effects on sales and various factors affecting the economy in general. The reported high and low closing sale prices of our common stock were $11.36 per share and $5.37 per share, respectively, during the fiscal year ended February 1, 2003, and were $14.71 per share and $5.86 per share, respectively, during the fiscal year ended January 31, 2004. In addition, the Nasdaq National Market has experienced a high level of price and volume volatility and market prices for the stock of many companies have experienced wide price fluctuations not necessarily related to the operating performance of such companies.

Our largest stockholders may exert influence over our business regardless of the opposition of other stockholders or the desire of other stockholders to pursue an alternate course of action.

Dennis Pence, our Chairman and Chief Executive Officer, and Ann Pence, our Vice Chairman, have informed the company that they have an informal arrangement pursuant to which they have agreed to vote their shares together and, when selling shares, doing so in equal amounts. This arrangement is not in writing, and can be terminated at any time, and there is no assurance that Dennis Pence and Ann Pence will continue to act together with respect to their shares. Because of their informal arrangement, Dennis Pence and Ann Pence together may be deemed to beneficially own, directly and indirectly, approximately 49.4% of our outstanding common stock as of January 31, 2004, and 42.9% after giving effect to this offering. Dennis Pence and Ann Pence acting together, or either of them acting independently, could have significant influence over any matters submitted to our stockholders, including the election of our directors and approval of business combinations, and could delay, deter or prevent a change of control of our company, which may

10

adversely affect the market price of our common stock. The interests of Dennis Pence and Ann Pence may not always coincide with the interests of our other stockholders.

Provisions in our charter documents and Delaware law may inhibit a takeover and discourage, delay or prevent our stockholders from replacing or removing our current directors or management.

Provisions in our Certificate of Incorporation and Bylaws may have the effect of delaying or preventing a merger with or acquisition of us, even where the stockholders may consider it to be favorable. These provisions could also prevent or hinder an attempt by our stockholders to replace our current directors and include:

- •

- providing for a classified Board of Directors with staggered, three-year terms;

- •

- prohibiting cumulative voting in the election of directors;

- •

- authorizing the issuance of "blank check" preferred stock;

- •

- limiting persons who can call special meetings of the Board of Directors or stockholders;

- •

- prohibiting stockholder action by written consent; and

- •

- establishing advance notice requirements for nominations for election to the Board of Directors or for proposing matters that can be acted on by stockholders at a stockholders meeting.

Because our Board of Directors appoints management, any inability to effect a change in our Board of Directors may also result in the entrenchment of management.

We are also subject to Section 203 of the Delaware General Corporation Law, which, subject to exceptions, prohibits a Delaware corporation from engaging in any business combination with an interested stockholder for a period of three years following the date that the stockholder became an interested stockholder. The preceding provisions of our Certificate of Incorporation and Bylaws, as well as Section 203 of the Delaware General Corporation Law, could discourage potential acquisition proposals, delay or prevent a change of control and prevent changes in our management.

Future sales of our common stock may depress our stock price.

All of our executive officers and directors holding an aggregate of 12,548,087 shares of our common stock as of January 31, 2004 have agreed that they will not offer, sell, agree to sell, directly or indirectly, or otherwise dispose of any shares of common stock other than in connection with this offering without the prior written consent of Banc of America Securities LLC for a period of 90 days after the date of this prospectus. After the expiration of this period, shares held by these stockholders will become eligible for sale to the public free from any contractual restrictions. We have agreed to the same lock-up period. After expiration of this lock-up, we may sell equity securities to raise additional funds, which would result in dilution to our stockholders. In addition, there are 1,113,041 shares of common stock issuable upon the exercise of outstanding options as of January 31, 2004 that may be sold 30 days or 90 days after the date of this prospectus. The market price of our common stock could decline as a result of sales of a large number of shares after this offering or the perception that sales could occur. In addition, the large number of secondary shares eligible for resale might make it more difficult for us to sell common stock in the future at a time and or a price that we deem appropriate.

Because we do not plan to pay cash dividends in the foreseeable future, investors must look solely to stock appreciation for a return on their investment in us.

We do not anticipate paying cash dividends to the holders of our common stock in the foreseeable future. Additionally, we are currently restricted from paying cash dividends under our credit facility. Accordingly, investors must rely on sales of their common stock after price appreciation, which may never

11

occur, as the only way to realize a return on their investment. Investors seeking cash dividends should not purchase our common stock.

We may need to raise additional funds, which may impose limitations on our operations or prevent or delay our retail expansion.

If our cash flow from operations together with the proceeds of this offering are insufficient to meet our future capital requirements, we will have to raise additional funds to continue our retail expansion. If we raise funds through the issuance of debt securities, it could result in a substantial portion of our cash flow being devoted to the payment of principal and interest, and could render us more vulnerable to competitive pressures and economic downturns and impose restrictions on our operations. If adequate funds are not available, we may be required to reduce the number of new retail stores we open in the future, or to obtain funds through other arrangements that may only be available on unattractive terms, if at all.

Risks Related to Engagement of Arthur Andersen LLP as our Former Auditors

We have not obtained the consent of Arthur Andersen LLP to be named in the registration statement to which this prospectus is a part as having audited our financial statements for our 2001 and 2000 fiscal years. This will limit your ability to assert claims against Arthur Andersen.

Arthur Andersen LLP audited our financial statements included in this prospectus for the years ended March 2, 2002 and March 3, 2001. We are unable to obtain the consent of Arthur Andersen LLP to the inclusion in the registration statement, of which this prospectus is a part, of their report with respect to our consolidated financial statements for the fiscal years ended March 2, 2002 and March 3, 2001. Under these circumstances, Rule 437a under the Securities Act of 1933 permits us to file the registration statement without a written consent from Arthur Andersen LLP. The absence of this consent may limit your recovery on certain claims. In particular, and without limitation, you will not be able to assert claims against Arthur Andersen LLP under Section 11 of the Securities Act of 1933 for any untrue statement of a material fact contained in our consolidated financial statements for the fiscal years ended March 2, 2002 and March 3, 2001 which appear in this prospectus, or any omission to state a material fact required to be stated therein. In addition, the impact on Arthur Andersen LLP's financial condition of the conviction of Arthur Andersen LLP on federal obstruction of justice charges may adversely affect its ability to satisfy any claims arising from its provision of auditing services to us.

12

SPECIAL NOTE REGARDING FORWARD-LOOKING STATEMENTS

This prospectus contains various statements regarding our current strategies, financial position, results of operations, cash flows, operating and financial trends and uncertainties, as well as certain forward-looking statements regarding our future expectations. When used in this discussion, words such as "anticipate," "believe," "estimate," "expect," "could," "may," "will," "should," "plan," "predict," "potential" and similar expressions are intended to identify such forward-looking statements. Our forward-looking statements are based on our current expectations and are subject to numerous risks and uncertainties. As such, our actual future results, performance or achievements may differ materially from the results expressed in, or implied by, our forward-looking statements. These risks and uncertainties include, but are not limited to, the risks identified above under the caption "Risk Factors" and elsewhere in this prospectus. We assume no future obligation to update any of our forward-looking statements or to provide periodic updates or guidance.

The public offering price of the shares of common stock in this offering will be based on the market price of our common stock as reported on the Nasdaq National Market. We estimate the net proceeds to us from the sale of 2,000,000 shares of our common stock in this offering to be approximately $37.6 million based on the public offering price of $20.50 per share, after deducting underwriting discounts and commissions and our estimated offering expenses. The net proceeds to us will be approximately $42.3 million if the underwriters exercise their over-allotment option in full. We will not receive any proceeds from the sale of the 1,120,000 shares of common stock offered pursuant to this prospectus for the account of the selling stockholders.

We currently intend to use the net proceeds from this offering to continue to expand our retail operations and for working capital and for other general corporate purposes. Pending the application of the proceeds, we intend to invest the net offering proceeds in short-term, interest-bearing, investment-grade securities.

The foregoing represents our current intentions based upon our present plans and business condition. We will have broad discretion in the application of the net proceeds from this offering, and the occurrence of unforeseen events or changes in business conditions could result in the application of the net proceeds from this offering in a manner other than as described in this prospectus.

13

PRICE RANGE OF COMMON STOCK AND DIVIDEND POLICY

Our common stock has been quoted on the Nasdaq National Market under the symbol "CWTR" since our initial public offering on January 29, 1997. The following table sets forth for the indicated periods the high and low closing sale prices of our common stock as quoted on the Nasdaq National Market. On December 19, 2002 and on August 4, 2003, our Board of Directors declared 50% stock dividends, each having the effect of a 3-for-2 stock split, on our issued and outstanding common stock. The new shares were distributed on January 30, 2003 and on September 9, 2003, respectively. The stock prices below reflect the effect of these two stock dividends.

| | Price Range of Common Stock | |||||

|---|---|---|---|---|---|---|

| | High | Low | ||||

| Fiscal 2004: | ||||||

| First Quarter | $ | 22.90 | $ | 14.92 | ||

| Second Quarter (through May 20, 2004) | 21.49 | 19.02 | ||||

Fiscal 2003: | ||||||

| First Quarter | $ | 8.29 | $ | 5.86 | ||

| Second Quarter | 11.92 | 5.94 | ||||

| Third Quarter | 13.10 | 9.29 | ||||

| Fourth Quarter | 14.71 | 11.00 | ||||

Fiscal 2002: | ||||||

| First Quarter | $ | 10.31 | $ | 7.32 | ||

| Second Quarter | 11.36 | 6.52 | ||||

| Third Quarter | 7.09 | 5.37 | ||||

| Fourth Quarter | 8.94 | 6.30 | ||||

Fiscal 2001: | ||||||

| First Quarter | $ | 10.88 | $ | 8.09 | ||

| Second Quarter | 12.52 | 8.83 | ||||

| Third Quarter | 11.98 | 7.56 | ||||

| Fourth Quarter | 11.96 | 5.84 | ||||

On May 19, 2004, the last reported sale price of our common stock on the Nasdaq National Market was $21.49, and there were 24,250,452 shares of common stock outstanding, with approximately 141 holders of record.

We have never paid any cash dividends on our common stock and do not expect to declare cash dividends in the foreseeable future. Additionally, we are currently restricted from paying cash dividends under our credit facility.

14

The following table sets forth our cash and cash equivalents and our consolidated capitalization as of January 31, 2004:

- •

- On an actual basis; and

- •

- On an as adjusted basis to reflect the sale of 2,000,000 shares of common stock offered by us at the public offering price of $20.50 per share, after deducting underwriting discounts and commissions and our estimated offering expenses.

This table should be read in conjunction with our selected consolidated financial data and the consolidated financial statements included elsewhere in this prospectus.

| | As of January 31, 2004 | ||||||||

|---|---|---|---|---|---|---|---|---|---|

| | Actual | As Adjusted | |||||||

| | (in thousands) | ||||||||

| Cash and cash equivalents | $ | 45,754 | $ | 83,334 | |||||

| Long-term debt(a) | — | — | |||||||

| Stockholders' equity: | |||||||||

| Preferred stock, $0.01 par value; 1,000,000 shares authorized; no shares issued and outstanding | — | — | |||||||

| Common stock, $0.01 par value; 60,000,000 shares authorized; 24,166,201 shares issued and outstanding, actual; and 26,166,201 shares issued and outstanding, as adjusted | 242 | 262 | |||||||

| Additional paid-in-capital | 47,927 | 85,487 | |||||||

| Retained earnings | 71,628 | 71,628 | |||||||

| Total stockholders' equity | 119,797 | 157,377 | |||||||

| Total capitalization | $ | 119,797 | $ | 157,377 | |||||

- (a)

- We currently have a $60 million unsecured revolving line of credit, and, as of the date of this prospectus, we have not borrowed under this facility.

The number of shares of common stock outstanding is based on 24,166,201 shares of our common stock outstanding as of January 31, 2004, and excludes the following:

- •

- 1,720,105 shares of common stock issuable upon the exercise of options outstanding under our Stock Option/Stock Issuance Plan, as amended, at a weighted average exercise price of $8.99 per share, of which options to purchase 1,113,041 shares are exercisable, having a weighted average exercise price of $8.98 per share.

- •

- 630,116 shares reserved for issuance under our Stock Option/Stock Issuance Plan, as amended.

- •

- 1,460,264 shares reserved for issuance under our Employee Stock Purchase Plan, as amended.

15

SELECTED CONSOLIDATED FINANCIAL AND OPERATING DATA

The selected consolidated financial and operating data in the following table sets forth (i) balance sheet data as of January 31, 2004 and February 1, 2003, and statement of operations data for the respective 12-month period and 11-month transition period then ended, derived from our consolidated financial statements audited by KPMG LLP, independent accountants, which are included elsewhere in this prospectus, (ii) balance sheet data as of March 2, 2002 and statement of operations data for the fiscal year ended March 2, 2002, derived from our consolidated financial statements audited by Arthur Andersen LLP, independent auditors, which are included elsewhere in this prospectus, (iii) balance sheet data as of March 3, 2001 and February 26, 2000, and statement of operations data for the fiscal years ended February 26, 2000, derived from our consolidated financial statements audited by Arthur Andersen LLP, which are not presented in this prospectus, and (iv) selected operating data as of and for the periods indicated. The information below should be read in conjunction with "Management's Discussion and Analysis of Financial Condition and Results of Operations" and our financial statements and the related notes included elsewhere in this prospectus.

| | Fiscal Years Ended(a) | ||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| | February 26, 2000 (52 weeks) | March 3, 2001 (53 weeks) | March 2, 2002 (52 weeks) | February 1, 2003 (48 weeks) | January 31, 2004 (52 weeks) | ||||||||||||

| | (in thousands, except per share and store data) | ||||||||||||||||

| Statement of Operations Data: | |||||||||||||||||

| Net sales | $ | 361,566 | $ | 458,445 | $ | 464,024 | $ | 473,172 | $ | 518,844 | |||||||

| Cost of sales | 196,281 | 255,187 | 272,665 | 284,406 | 316,026 | ||||||||||||

| Gross profit | 165,285 | 203,258 | 191,359 | 188,766 | 202,818 | ||||||||||||

| Selling, general and administrative expenses | 143,553 | 182,770 | 188,902 | 173,330 | 182,210 | ||||||||||||

| Income from operations | 21,732 | 20,488 | 2,457 | 15,436 | 20,608 | ||||||||||||

| Interest, net, and other | 864 | 1,114 | 483 | 170 | (93 | ) | |||||||||||

| Gain on sale of Milepost Four assets | 826 | — | — | — | — | ||||||||||||

| Income before provision for income taxes | 23,422 | 21,602 | 2,940 | 15,606 | 20,515 | ||||||||||||

| Income tax provision | 9,251 | 8,364 | 1,140 | 6,249 | 8,037 | ||||||||||||

| Net income | $ | 14,171 | $ | 13,238 | $ | 1,800 | $ | 9,357 | $ | 12,478 | |||||||

| Net income per share — basic(b) | $ | 0.62 | $ | 0.56 | $ | 0.08 | $ | 0.39 | $ | 0.52 | |||||||

| Weighted average shares outstanding — basic(b) | 23,031 | 23,619 | 23,832 | 23,898 | 24,074 | ||||||||||||

| Net income per share — diluted(b) | $ | 0.59 | $ | 0.54 | $ | 0.07 | $ | 0.39 | $ | 0.51 | |||||||

| Weighted average shares outstanding — diluted(b) | 23,823 | 24,507 | 24,323 | 24,098 | 24,407 | ||||||||||||

| Selected Channel Data:(c) | |||||||||||||||||

| Net sales: | |||||||||||||||||

| Catalog | $ | 319,710 | $ | 300,723 | $ | 246,048 | $ | 200,157 | $ | 175,912 | |||||||

| Internet | 28,970 | 112,399 | 141,873 | 144,838 | 148,308 | ||||||||||||

| Retail | 12,886 | 45,323 | 76,103 | 128,177 | 194,624 | ||||||||||||

| Selected Operating Data: | |||||||||||||||||

| Total catalogs mailed | 139,800 | 183,600 | 161,000 | 136,000 | 117,784 | ||||||||||||

| Total active customers(d) | 2,200 | 2,600 | 2,600 | 2,700 | 2,601 | ||||||||||||

| Number of stores at period end(e) | 4 | 10 | 29 | 43 | 68 | ||||||||||||

| Average square feet per store(e) | 13,500 | 10,300 | 8,200 | 7,600 | 6,700 | ||||||||||||

16

| | As of | ||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| | February 26, 2000 (52 weeks) | March 3, 2001 (53 weeks) | March 2, 2002 (52 weeks) | February 1, 2003 (48 weeks) | January 31, 2004 (52 weeks) | ||||||||||

| | (in thousands, except per share and store data) | ||||||||||||||

| Balance Sheet Data: | |||||||||||||||

| Cash and cash equivalents | $ | 7,533 | $ | 4,600 | $ | 4,989 | $ | 26,630 | $ | 45,754 | |||||

| Working capital | 36,735 | 42,954 | 26,679 | 37,365 | 50,738 | ||||||||||

| Total assets | 122,870 | 150,890 | 169,247 | 187,647 | 210,657 | ||||||||||

| Total debt(f) | — | — | — | — | — | ||||||||||

| Stockholders' equity | 76,570 | 96,135 | 94,928 | 105,963 | 119,797 | ||||||||||

- (a)

- References to a fiscal year refer to the calendar year in which the fiscal year commences. On December 16, 2002, our Board of Directors approved a change in our fiscal year end from the Saturday nearest February 28 to the Saturday nearest January 31, effective February 1, 2003. We made this decision to align our reporting schedule with the majority of other national retail companies. Accordingly, our 2002 fiscal year consisted of an 11-month transition period. In addition, our floating fiscal year-end typically results in 13-week fiscal quarters and a 52-week fiscal year, but will occasionally give rise to an additional week resulting in a 14-week fiscal fourth quarter and a 53-week fiscal year. For the fiscal years presented above, only our fiscal year ended March 3, 2001 reflects an incremental fifty-third week.

- (b)

- The weighted average shares outstanding and net income per share amounts reflect two 50% stock dividends, each having the effect of a 3-for-2 stock split, declared by our Board of Directors on December 19, 2002 and August 4, 2003, respectively.

- (c)

- Beginning with our first quarter of fiscal 2003, we reclassified our outlet store business and phone and Internet orders that originate in our retail stores from our direct segment to our retail segment. We have reclassified prior period financial statements on a consistent basis for fiscal years 2002, 2001 and 2000 only. Due to information systems limitations, we did not reclassify periods prior to fiscal 2000 because it was not practicable for us to do so. In addition, management believes that the reclassification of these periods would be immaterial.

- (d)

- An "active customer" is defined as a customer who purchased merchandise from us through any of our sales channels during the 12-month period preceding the end of the period indicated. Active customers do not include retail customers who have not provided identifying information to us.

- (e)

- Excludes outlet stores and includes our two resort stores.

- (f)

- We currently have a $60 million unsecured revolving line of credit, and, as of the date of this prospectus, we have not borrowed under this facility.

17

MANAGEMENT'S DISCUSSION AND ANALYSIS OF

FINANCIAL CONDITION AND RESULTS OF OPERATIONS

We encourage you to read this Management's Discussion and Analysis of Financial Condition and Results of Operations in conjunction with our accompanying consolidated financial statements and their related notes. Our discussion of our results of operations and financial condition includes various forward-looking statements about our markets, the demand for our products and services and our future results. We based these statements on assumptions that we consider reasonable. Actual results may differ materially from those suggested by our forward-looking statements for various reasons including those discussed in the "Risk Factors" beginning on page 5 of this prospectus.

When we refer to a fiscal year, we mean the calendar year in which the fiscal year begins. On December 16, 2002, our Board of Directors approved a change in our fiscal year end from the Saturday nearest February 28 to the Saturday nearest January 31, effective February 1, 2003. Accordingly, our 2002 fiscal year consisted of an 11-month transition period. We made this decision to align our financial reporting schedule with the majority of other national retail companies.

We currently operate in two reportable segments, our direct segment and our retail segment. Beginning in the quarter ended May 3, 2003, we reclassified our outlet store business and phone and Internet orders that originate in our retail stores from our direct segment to our retail segment. We made these reclassifications to reflect the manner in which our segments are currently managed. We have reclassified prior period financial statements on a consistent basis for fiscal years 2002, 2001 and 2000. These reclassifications had no impact on our consolidated net sales, net income, retained earnings or cash flows for any period. Due to information systems limitations, we did not reclassify periods prior to fiscal 2000 because it was not practicable for us to do so. In addition, management believes that the reclassification of these prior periods would be immaterial.

Unless otherwise indicated, the common stock outstanding, retained earnings and net income per share amounts appearing in this prospectus and the financial statements included herein reflect two 50% stock dividends, each having the effect of a 3-for-2 stock split, declared by our Board of Directors on December 19, 2002 and August 4, 2003, respectively. These stock dividends have the combined effect of a 2.25-for-1 stock split.

Coldwater Creek Profile

Coldwater Creek is a multi-channel, specialty retailer of women's apparel, accessories, jewelry and gift items. Our unique, proprietary merchandise assortment and our retail stores, catalogs and e-commerce website are designed to appeal to women between the ages of 30 and 60, with median household incomes in excess of $75,000. We reach our customers through our direct segment, which consists of our catalog and e-commerce businesses, and our rapidly expanding base of retail stores.

Our catalog business is a significant sales channel and acts as an efficient marketing platform to cross-promote our website and retail stores. During fiscal 2003, we mailed 117.8 million catalogs. We launched our full-scale e-commerce website,www.coldwatercreek.com, in 1999 to cost-effectively expand our customer base and provide another convenient shopping alternative for our customers. We currently have a database of over 2.2 million e-mail addresses to which we regularly send customized e-mails.

We expect our retail business, which represented 37.5% of our total net sales in fiscal 2003, to be the key driver of our growth strategy. As of January 31, 2004, we operated 66 full-line retail stores, 25 of which were opened in fiscal 2003, as well as two resort stores and 16 merchandise clearance outlet stores in 51 markets. We currently plan to open 45 new stores in fiscal 2004, including two stores opened in March 2004, and 40 to 50 new stores in fiscal 2005. Over the past four years, we have been refining our retail store model and have taken the following steps to support the growth of our retail business and realize the benefits of our multi-channel model:

- •

- introducing a scaleable retail store model for national rollout;

18

- •

- enhancing the management team, particularly in our retail segment, by hiring key members of management with extensive retail experience;

- •

- focusing our merchandise offering by refining our product assortment and increasing our investment in key items; and

- •

- integrating our retail and direct merchandise planning and inventory management functions to maintain fashion continuity and brand integrity across all channels.

Direct Segment Operations

Our direct segment includes our catalog and e-commerce businesses. Our direct channel generated $324.2 million in net sales, or approximately 62.5% of our total net sales, in fiscal 2003. As we continue to roll out our retail stores, we expect our direct segment to decrease as a percentage of total net sales over time. However, we expect our direct segment to continue to be a core component of our operations and brand identity and an important vehicle to promote each of our channels and provide cash flow to support our retail store expansion.

Our Catalogs

During fiscal 2003, our catalog business generated $175.9 million in net sales, or 33.9% of total net sales. Historically, we used three catalogs,Northcountry, Spirit andElements, to feature our entire line of full-price merchandise with different assortments for each title to target separate sub-groups of our core demographic. In January 2004, we combined our two smaller catalogs,Spirit andElements, and re-introduced the combined catalog under theSpirit title. Additionally, each year we assemble selected merchandise from the most popular items in our primary merchandise lines and feature them in a festiveGifts-to-Go holiday catalog and on our website.

Since 2000, in an effort to increase the productivity of our direct business and reduce costs, we have reduced our catalog circulation and have been actively promoting the migration of our customers from our catalogs to our more cost-efficient e-commerce website. We have also focused on decreasing the number of mailings to prospective customers because they increasingly produce lower response rates and contribute fewer sales than mailings to active customers. In fiscal 2003, we mailed 117.8 million catalogs, down 35.8% from our peak mailings of 183.6 million catalogs in 2000. We expect to continue to reduce our catalog circulation, particularly to prospective customers, which we believe will continue to have a positive impact on our selling, general and administrative expenses. Although we anticipate losing some potential prospect sales, we believe that optimizing the level of our prospect mailings will have an overall positive impact on our net income.

E-commerce Website

We launched our full-scale e-commerce website,www.coldwatercreek.com, in July of 1999 to offer a convenient, user-friendly and secure online shopping option for our customers. The website features our entire full-price merchandise offering found in our catalogs and retail stores. It also serves as an efficient promotional vehicle for the disposition of excess inventory.

In fiscal 2003, online net sales were $148.3 million and represented 28.6% of total net sales. As of January 31, 2004, we had over 2.2 million opt-in e-mail addresses to which we regularly send customized e-mails to drive sales through our website and our other channels. We also participate in a net sales commission-based program whereby numerous popular Internet search engines and consumer and charitable websites provide hotlink access to our website. This affiliate program serves as an effective tool in prospecting for new customers.

19

Retail Segment Operations

Our retail segment includes our retail and outlet stores and catalog and Internet sales that originate in our retail stores. Our retail channel is our fastest growing sales channel and generated $194.6 million in net sales, or 37.5% of total net sales in fiscal 2003.

Full-Line Stores

We opened our first full-line retail store in November 1999 and have since tested and refined our store format and reduced capital expenditures required for build-out. We believe there is an opportunity to grow to 400 to 500 stores in up to 275 to 300 identified markets nationwide over the next six to eight years. At January 31, 2004, we operated 66 stores and plan to open 45 new stores in fiscal 2004, including two stores opened in March 2004. We have identified suitable locations for these planned stores and believe we will be able to complete our 2004 expansion plans with available working capital. In 2005, we currently plan to open 40 to 50 new stores, and are in the process of securing appropriate sites for these stores.

After 2005 it is our current intention to continue to open new stores at our current pace, although we do not maintain a specific rollout plan beyond a two-year horizon. We continually reassess our store rollout plans based on the overall retail environment, the performance of our retail business, our access to working capital and external financing and the availability of suitable store locations. For example, it is possible that in any year we will increase our planned store openings, particularly if we experience strong retail sales and have access to the necessary working capital or external financing. Likewise, we would be inclined to curtail our store rollout if we were to experience weaker retail sales or if we did not have adequate working capital or access to financing.

Our core new store model, which we introduced in the second half of 2002, consists of 5,000 to 6,000 square foot stores. These stores reflect improvements in our construction processes, materials and fixtures, merchandise layout and store design and have reduced our initial capital investment per store compared to previously opened stores. This model assumes an average initial net investment per store of approximately $560,000 and anticipates net sales per square foot of approximately $500 in the third year of operations. In fiscal 2003, our 41 full-line stores that had been open at least 13 months averaged 7,207 square feet and net sales per square foot of $460. Most of these stores have been open for one to two years.

We are also introducing a smaller store model of 3,000 to 4,000 square foot stores. We have designed these stores to access smaller markets and to increase our presence in larger metropolitan markets. This model assumes an average initial net investment per store of approximately $400,000 and anticipates net sales per square foot of approximately $600 in the third year of operations. We currently have six stores open in this model, none of which has been open for a full year.

Outlet Stores and Resort Stores

We currently operate 18 outlet stores where we sell excess inventory. We plan to open an additional outlet store in fiscal 2004. We generally locate the outlets within clusters of our retail stores to efficiently manage our inventory and clearance activities, but far enough away to avoid significantly diminishing our full-line store sales. Unlike many other apparel retailers, we use our outlet stores only to sell overstocked premium items from our full-line retail stores and do not have merchandise produced directly for them. We currently operate two resort stores in Sandpoint, Idaho and Jackson, Wyoming.

20

Results of Operations

The following table sets forth certain information regarding our costs and expenses expressed as a percentage of consolidated net sales:

| | Fiscal Year Ended | ||||||

|---|---|---|---|---|---|---|---|

| | March 2, 2002 (52 weeks) | Feb. 1, 2003 (48 weeks) | Jan. 31, 2004 (52 weeks) | ||||

| Net sales | 100.0 | % | 100.0 | % | 100.0 | % | |

| Cost of sales | 58.8 | 60.1 | 60.9 | ||||

| Gross profit | 41.2 | 39.9 | 39.1 | ||||

| Selling, general and administrative expenses | 40.7 | 36.6 | 35.1 | ||||

| Income from operations | 0.5 | 3.3 | 4.0 | ||||

| Interest, net, and other | 0.1 | 0.0 | 0.0 | ||||

| Income before provision for income taxes | 0.6 | 3.3 | 4.0 | ||||

| Income tax provision | 0.2 | 1.3 | 1.5 | ||||

| Net income | 0.4 | % | 2.0 | % | 2.4 | % | |

Comparison of the Twelve-Month Period Ended January 31, 2004 with the Eleven-Month Period Ended February 1, 2003

Consolidated Results of Operations

Fiscal year 2002 was an 11-month transition period attributable to the change in our fiscal year end as of February 1, 2003. To assist the reader, the following discussions first compare a 12-month fiscal year 2003 with an 11-month fiscal year 2002, including the amount attributed to the fact that there was one less month in fiscal 2002. The remaining discussions compare the 12-month fiscal 2003 with the comparable 12-month period ended February 1, 2003.

The table below is provided to assist the reader in assessing differences in our overall fiscal 2003 and 2002 performance and sets forth our results of operations for the periods indicated below:

| | 11 Months Ended February 1, 2003 (1) | One Month Ended March 2, 2002 (unaudited) | 12 Months Ended February 1, 2003 (unaudited) | 12 Months Ended January 31, 2004 (1) | |||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| | (in thousands) | ||||||||||||

| Net sales | $ | 473,172 | $ | 28,283 | $ | 501,455 | $ | 518,844 | |||||

| Cost of sales | 284,406 | 18,111 | 302,517 | 316,026 | |||||||||

| Gross profit | 188,766 | 10,172 | 198,938 | 202,818 | |||||||||

| Selling, general and administrative expenses | 173,330 | 12,617 | 185,947 | 182,210 | |||||||||

| Income (loss) from operations | 15,436 | (2,445 | ) | 12,991 | 20,608 | ||||||||

| Interest, net, and other | 170 | 18 | 188 | (93 | ) | ||||||||

| Income (loss) before provision for income taxes | 15,606 | (2,427 | ) | 13,179 | 20,515 | ||||||||

| Income tax provision (benefit) | 6,249 | (939 | ) | 5,310 | 8,037 | ||||||||

| Net income (loss) | $ | 9,357 | $ | (1,488 | ) | $ | 7,869 | $ | 12,478 | ||||

- (1)

- This information is derived from our consolidated financial statements audited by KPMG LLP, independent auditors, which are included elsewhere in this prospectus.

21

Net Sales. Our consolidated net sales for the 12-month fiscal 2003 were $518.8 million, an increase of $45.7 million, or 9.7%, compared with consolidated net sales of $473.2 million during the 11-month fiscal 2002. We attribute $28.3 million of the $45.7 million increase in our consolidated net sales to the fact that there was one less month in fiscal 2002 than in fiscal 2003.

Our consolidated net sales for the 12-month fiscal 2003 increased $17.4 million, or 3.5%, compared with consolidated net sales of $501.5 million during the comparable 12-month period ended February 1, 2003. This increase is primarily due to incremental net sales of $47.9 million contributed by our retail expansion and, to a lesser extent, to improved direct segment sales returns. In fiscal 2003, our direct segment sales returns expressed as a percentage of gross sales declined by 2.1 percentage points from the comparable 12-month period ended February 1, 2003. We have experienced improved direct segment sales returns primarily due to technical design improvements we have made to the fit of our merchandise and our quality control efforts. These positive impacts were partially offset primarily by a decrease of $30.1 million, or 17.2%, in full-price net sales by our direct segment's catalog business. Please refer to our discussions titled"Comparison of the Twelve-Month Period Ended January 31, 2004 with the Eleven-Month Period Ended February 1, 2003—Consolidated Results of Operations—Operating Segment Results" below for further details.

Gross Profit Dollars. Our consolidated gross profit dollars for the 12-month fiscal 2003 were $202.8 million, an increase of $14.1 million, or 7.4%, compared with consolidated gross profit dollars for the 11-month fiscal 2002 of $188.8 million. We attribute $10.2 million of the $14.1 million increase in consolidated gross profit to the fact that there was one more month in fiscal 2003 than in fiscal 2002.

Our consolidated gross profit dollars for the 12-month fiscal 2003 increased $3.9 million, or 2.0%, compared with consolidated gross profit dollars of $198.9 million during the comparable 12-month period ended February 1, 2003. The increase in our consolidated gross profit dollars was primarily attributable to the increase in consolidated net sales.