As filed with the Securities and Exchange Commission on December 9, 2011

File No. 333-

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-14

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

¨ Pre-Effective Amendment No.

¨ Post-Effective Amendment No.

NUVEEN MULTISTATE TRUST IV

(Exact Name of Registrant as Specified in Charter)

333 West Wacker Drive

Chicago, Illinois 60606

(Address of Principal Executive Offices, Zip Code)

Registrant’s Telephone Number, including Area Code (312) 917-7700

Kevin J. McCarthy

Vice President and Secretary

333 West Wacker Drive

Chicago, Illinois 60606

(Name and Address of Agent for Service)

Copy to:

Deborah Bielicke Eades Vedder Price P.C. 222 North LaSalle Street Chicago, Illinois 60601 | Eric F. Fess Chapman and Cutler LLP 111 West Monroe Street Chicago, Illinois 60603 |

Approximate date of proposed public offering: As soon as practicable after the effective date of this Registration Statement.

TITLE OF SECURITIES BEING REGISTERED: Shares of Beneficial Interest (par value $0.01 per share) of the Registrant.

No filing fee is required because of reliance on Section 24(f) and an indefinite number of shares have previously been registered pursuant to Rule 24f-2 under the Investment Company Act of 1940.

It is proposed that this filing will become effective on January 8, 2012 pursuant to Rule 488 under the Securities Act of 1933.

Important Information for

Nuveen Missouri Tax Free Fund Shareholders

At a special meeting of shareholders of Nuveen Missouri Tax Free Fund (the “Acquired Fund”), a series of Nuveen Investment Funds, Inc. (the “Corporation”), you will be asked to vote upon an important change affecting your fund. The purpose of the special meeting is to allow you to vote on a reorganization of your fund into Nuveen Missouri Municipal Bond Fund (the “Acquiring Fund”). If the reorganization is approved and completed, you will become a shareholder of the Acquiring Fund. The Acquired Fund and the Acquiring Fund are collectively referred to herein as the “Funds.”

Although we recommend that you read the complete Proxy Statement/Prospectus, for your convenience, we have provided the following brief overview of the issue to be voted on.

| Q. | Why am I receiving this Proxy Statement/Prospectus? |

| A. | In December of 2010, Nuveen Investments, Inc. and certain of its affiliates (“Nuveen”) completed a strategic combination with U.S. Bank National Association and its wholly-owned subsidiary, FAF Advisors, Inc., the investment adviser to the First American Funds. Pursuant to this transaction, Nuveen acquired a portion of the investment advisory business of FAF Advisors, Inc., including assets related to the non-money market open-end funds in the First American family of funds. Effective January 1, 2011, these former First American Funds became part of the Nuveen family of funds and were re-branded as Nuveen Funds. As part of its efforts to integrate the portfolio management teams and investment products it offers following the closing of the transaction, Nuveen has recommended a number of reorganizations between funds with similar investment objectives and policies. The reorganization of the Acquired Fund into the Acquiring Fund has been proposed as part of this initiative. |

| Q. | What advantages will the reorganization produce for Acquired Fund shareholders? |

| A. | Nuveen Fund Advisors, Inc. (“Nuveen Fund Advisors”), the Funds’ investment adviser, and the Board of Directors of the Corporation (the “Board”) believe that shareholders of the Acquired Fund will benefit from operational efficiencies and economies of scale that are expected to arise as a result of the larger net asset size of the Acquiring Fund following the reorganization. These operational efficiencies and economies of scale, together with the Acquiring Fund’s lower management fee (described in further detail below), are expected to result in lower gross and net expenses for all shareholders. |

| Q. | What are the similarities between the investment policies of the Funds? |

| A. | The investment objective of the Acquired Fund is to provide maximum current income that is exempt from both federal income tax and Missouri state income tax to the extent consistent with prudent investment risk. The investment objective of the Acquiring Fund is to provide investors with as high a level of current interest income exempt from regular federal, Missouri state and, in some cases, Missouri local income taxes as is consistent with preservation of capital. Each Fund has similar principal investment strategies and risks. While there are differences in the current portfolio compositions of the Funds because they were formerly managed by different investment advisers, the Funds currently have the same portfolio manager and are expected to be managed in |

| a similar manner going forward. A more detailed comparison of the investment objectives, policies and risks of the Funds is contained in the Proxy Statement/Prospectus. |

| Q. | What will happen if shareholders do not approve the reorganization? |

| A. | If the reorganization is not approved by shareholders, the Board will take such actions as it deems to be in the best interests of the Acquired Fund, which may include additional solicitation or continuing to operate the Fund as a stand-alone fund. |

| Q. | Will Acquired Fund shareholders receive new shares in exchange for their current shares? |

| A. | Yes. If shareholders approve the reorganization and it is completed, each Acquired Fund shareholder will receive shares of the Acquiring Fund in an amount equal in total value to the total value of the Acquired Fund shares surrendered by such shareholder. |

| Q. | Will this reorganization create a taxable event for me? |

| A. | No. The reorganization is intended to qualify as a tax-free reorganization for federal income tax purposes. It is expected that you will recognize no gain or loss for federal income tax purposes as a direct result of the reorganization. Prior to the closing of the reorganization, the Acquired Fund expects to distribute all of its net investment income and net capital gains, if any. Except to the extent that this distribution is designated as an exempt-interest dividend, it will be taxable to the Acquired Fund’s shareholders for federal income tax purposes. All or a portion of this distribution may be subject to the federal alternative minimum tax. |

| Q. | How do total operating expenses compare between the two Funds? |

| A. | In light of the Acquiring Fund’s lower management fee, the gross and net expenses of the Acquiring Fund immediately following the reorganization are expected to be lower than the gross and net expenses of the Acquired Fund for all share classes. |

| Q. | Who will bear the costs of the reorganization? |

| A. | The reorganization is expected to result in cost savings for each Fund. In light of these anticipated cost savings, the costs of the reorganization will be allocated between the Funds ratably up to each Fund’s projected cost savings during the first year following the reorganization. Nuveen Fund Advisors estimates that reorganization costs will be approximately $126,000 and that the cost savings during the first year following the reorganization will be approximately $150,000 for the Acquired Fund and approximately $36,000 for the Acquiring Fund. As a result, the Acquired Fund is expected to be charged approximately $102,000, and the Acquiring Fund is expected to be charged approximately $24,000. Because the payment by the Acquired Fund of any portion of these costs would cause the Acquired Fund to exceed its expense cap currently in effect, Nuveen will reimburse all expenses charged to the Acquired Fund and none of the expenses charged to the Acquiring Fund. The Acquiring Fund is expected to recover its costs of the reorganization within the first year following the reorganization assuming that annual cost savings occur at the level shown above. If the reorganization is not approved or completed, Nuveen will pay all such reorganization expenses. |

| Q. | What is the timetable for the reorganization? |

| A. | If approved by shareholders on February 16, 2012, the reorganization is expected to occur at the close of business on February 24, 2012. |

| Q. | Whom do I call if I have questions? |

| A. | If you need any assistance, or have any questions regarding the proposal or how to vote your shares, please call Computershare Fund Services, your proxy solicitor, at (866) 612-5814 from 8 a.m. to 10 p.m. Central time on Monday through Friday or 11 a.m. to 5 p.m. Central time on Saturday. Please have your proxy material available when you call. |

| Q. | How do I vote my shares? |

| A. | You may vote by mail, telephone or over the Internet: |

| • | To vote by mail, please mark, sign, date and mail the enclosed proxy card. No postage is required if mailed in the United States. |

| • | To vote by telephone, please call the toll-free number located on your proxy card and follow the recorded instructions, using your proxy card as a guide. |

| • | To vote over the Internet, go to the Internet address provided on your proxy card and follow the instructions, using your proxy card as a guide. |

| Q. | Will Nuveen contact me? |

| A. | You may receive a call from representatives of Computershare Fund Services, the proxy solicitation firm retained by Nuveen, to verify that you received your proxy materials and to answer any questions you may have about the reorganization. |

| Q. | How does the Board suggest that I vote? |

| A. | After careful consideration, the Board has agreed unanimously that the reorganization is in the best interests of your Fund and recommends that you vote “FOR” the reorganization. |

, 2012

Dear Shareholders:

We are pleased to invite you to the special meeting of shareholders of Nuveen Missouri Tax Free Fund (the “Special Meeting”). The Special Meeting is scheduled for February 16, 2012, at [2:00] p.m., Central time, at the offices of Nuveen Investments, Inc., 333 West Wacker Drive, Chicago, Illinois 60606.

At the Special Meeting, you will be asked to consider and approve a very important proposal. Subject to shareholder approval, Nuveen Missouri Municipal Bond Fund (the “Acquiring Fund”) will acquire all the assets and liabilities of Nuveen Missouri Tax Free Fund (the “Acquired Fund”) in exchange solely for shares of the Acquiring Fund, which will be distributed in complete liquidation of the Acquired Fund to the shareholders of the Acquired Fund (the “Reorganization”).

Nuveen Fund Advisors, Inc. (“Nuveen Fund Advisors”), each Fund’s investment adviser, has proposed the Reorganization involving the Acquired Fund, as well as a number of other reorganizations involving other funds advised by Nuveen Fund Advisors, to eliminate certain redundancies among the products it offers and in an effort to achieve certain operating efficiencies.

The Reorganization is being proposed because Nuveen Fund Advisors and the Board of Directors of Nuveen Investment Funds, Inc. (the “Board”) believe that the shareholders of the Acquired Fund will benefit from potential operating efficiencies and economies of scale that may be achieved by combining the Funds pursuant to the Reorganization. Following the Reorganization, the Acquiring Fund is expected to have lower gross and net expenses than the Acquired Fund had prior to the Reorganization. The Board believes the Reorganization is in the best interests of the Acquired Fund, and recommends that you vote “For” the proposed Reorganization.

The attached Proxy Statement/Prospectus has been prepared to give you information about this proposal.

All shareholders are cordially invited to attend the Special Meeting. In order to avoid delay and additional expense, and to assure that your shares are represented, please vote as promptly as possible, whether or not you plan to attend the Special Meeting. You may vote by mail, telephone or over the Internet.

| • | To vote by mail, please mark, sign, date and mail the enclosed proxy card. No postage is required if mailed in the United States. |

| • | To vote by telephone, please call the toll-free number located on your proxy card and follow the recorded instructions, using your proxy card as a guide. |

| • | To vote over the Internet, go to the Internet address provided on your proxy card and follow the instructions, using your proxy card as a guide. |

We appreciate your continued support and confidence in Nuveen and our family of funds.

Very truly yours,

Kevin J. McCarthy

Vice President and Secretary

, 2012

NUVEEN MISSOURI TAX FREE FUND

NOTICE OF SPECIAL MEETING OF SHAREHOLDERS

TO BE HELD ON FEBRUARY 16, 2012

To the Shareholders:

Notice is hereby given that a special meeting of shareholders of Nuveen Missouri Tax Free Fund (the “Acquired Fund”), a series of Nuveen Investment Funds, Inc. (the “Corporation”), a Maryland corporation, will be held at the offices of Nuveen Investments, Inc., 333 West Wacker Drive, Chicago, Illinois 60606, on February 16, 2012 at [2:00] p.m., Central time (the “Special Meeting”), for the following purposes:

1. To approve an Agreement and Plan of Reorganization (and the related transactions) which provides for (i) the transfer of all the assets of the Acquired Fund to Nuveen Missouri Municipal Bond Fund (the “Acquiring Fund”) in exchange solely for voting shares of beneficial interest of the Acquiring Fund and the assumption by the Acquiring Fund of all the liabilities of the Acquired Fund; and (ii) the distribution by the Acquired Fund of Class A, Class A and Class I shares of the Acquiring Fund to the holders of Class A, Class C1 and Class I shares, respectively, of the Acquired Fund in complete liquidation and termination of the Acquired Fund (the “Reorganization”). A vote in favor of the Reorganization will be considered a vote in favor of an amendment to the Corporation’s Articles of Incorporation effecting the Reorganization.

2. To transact such other business as may properly come before the Special Meeting.

Only shareholders of record as of the close of business on December 20, 2011 are entitled to vote at the Special Meeting or any adjournments or postponements thereof.

All shareholders are cordially invited to attend the Special Meeting. In order to avoid delay and additional expense, and to assure that your shares are represented, please vote as promptly as possible, whether or not you plan to attend the Special Meeting. You may vote by mail, telephone or over the Internet.

| • | To vote by mail, please mark, sign, date and mail the enclosed proxy card. No postage is required if mailed in the United States. |

| • | To vote by telephone, please call the toll-free number located on your proxy card and follow the recorded instructions, using your proxy card as a guide. |

| • | To vote over the Internet, go to the Internet address provided on your proxy card and follow the instructions, using your proxy card as a guide. |

Kevin J. McCarthy

Vice President and Secretary

Proxy Statement/Prospectus

Dated , 2012

Relating to the Acquisition of the Assets and Liabilities of NUVEEN MISSOURI TAX FREE FUND by NUVEEN MISSOURI MUNICIPAL BOND FUND

This Proxy Statement/Prospectus is being furnished to shareholders of Nuveen Missouri Tax Free Fund (the “Acquired Fund”), a series of Nuveen Investment Funds, Inc. (the “Corporation”), a Maryland corporation and an open-end investment company registered under the Investment Company Act of 1940, as amended (the “1940 Act”), and relates to the special meeting of shareholders of the Acquired Fund to be held at the offices of Nuveen Investments, Inc., 333 West Wacker Drive, Chicago, Illinois 60606, on February 16, 2012 at [2:00] p.m., Central time and at any and all adjournments and postponements thereof (the “Special Meeting”). This Proxy Statement/Prospectus is provided in connection with the solicitation by the Board of Directors of the Corporation of proxies to be voted at the Special Meeting, and any and all adjournments or postponements thereof. The purpose of the Special Meeting is to consider the proposed reorganization (the “Reorganization”) of the Acquired Fund into Nuveen Missouri Municipal Bond Fund (the “Acquiring Fund”), a series of Nuveen Multistate Trust IV (the “Trust”), a Massachusetts business trust and an open-end investment company registered under the 1940 Act. The Acquired Fund and the Acquiring Fund are referred to herein collectively as the “Funds” and individually as a “Fund.” The Board of Directors of the Corporation and the Board of Trustees of the Trust, which are made up of the same individuals, are referred to herein as the “Board.” If shareholders approve the Reorganization and it is completed, shareholders of Class A, Class C1 and Class I shares of the Acquired Fund will receive Class A, Class A and Class I shares, respectively, of the Acquiring Fund with the same total value as the total value of the Acquired Fund shares surrendered by such shareholders. The Board has determined that the Reorganization is in the best interests of the Acquired Fund. The address, principal executive office and telephone number of the Funds, the Trust and the Corporation is 333 West Wacker Drive, Chicago, Illinois 60606, (800) 257-8787.

A vote in favor of the Reorganization will be considered a vote in favor of an amendment to the Corporation’s Articles of Incorporation effecting the Reorganization.

The enclosed proxy and this Proxy Statement/Prospectus are first being sent to shareholders of the Acquired Fund on or about , 2012. Shareholders of record as of the close of business on December 20, 2011 are entitled to vote at the Special Meeting and any adjournments or postponements thereof.

The Securities and Exchange Commission has not approved or disapproved these securities or determined whether the information in this Proxy Statement/Prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

This Proxy Statement/Prospectus concisely sets forth the information shareholders of the Acquired Fund should know before voting on the Reorganization (in effect, investing in Class A and Class I shares of the Acquiring Fund) and constitutes an offering of Class A and Class I shares of beneficial interest, par value $0.01 per share, of the Acquiring Fund. Please read it carefully and retain it for future reference.

The following documents have been filed with the Securities and Exchange Commission (“SEC”) and are incorporated into this Proxy Statement/Prospectus by reference and also accompany this Proxy Statement/Prospectus:

| (i) | the Trust’s prospectus dated September 30, 2011, as supplemented through the date of this Proxy Statement/Prospectus, relating to the Acquiring Fund; and |

| (ii) | the audited financial statements contained in the Trust’s Annual Report relating to the Acquiring Fund for the fiscal year ended May 31, 2011. |

The following documents contain additional information about the Acquired Fund and Acquiring Fund, have been filed with the SEC and are incorporated into this Proxy Statement/Prospectus by reference:

| (i) | the Statement of Additional Information relating to the proposed Reorganization, dated , 2012 (the “Reorganization SAI”); |

| (ii) | the Corporation’s prospectus dated September 30, 2011, as supplemented through the date of this Proxy Statement/Prospectus, relating to the Acquired Fund; |

| (iii) | the Corporation’s statement of additional information dated September 30, 2011, as supplemented through the date of this Proxy Statement/Prospectus, relating to the Acquired Fund; |

| (iv) | the audited financial statements contained in the Corporation’s Annual Report relating to the Acquired Fund for the fiscal year ended May 31, 2011; and |

| (v) | the Trust’s statement of additional information dated September 30, 2011, as supplemented through the date of this Proxy Statement/Prospectus, relating to the Acquiring Fund. |

No other parts of the documents referenced above are incorporated by reference herein.

Copies of the foregoing may be obtained without charge by calling or writing the Funds at the telephone number or address shown above. If you wish to request the Reorganization SAI, please ask for the “Reorganization SAI.” In addition, the Acquiring Fund will furnish, without charge, a copy of its most recent annual report and subsequent semi-annual report to a shareholder upon request. Any such request should be directed to the Acquiring Fund by calling (800) 257-8787 or by writing the Acquiring Fund at 333 West Wacker Drive, Chicago, Illinois 60606.

The Corporation and the Trust are subject to the informational requirements of the Securities Exchange Act of 1934, as amended, and the 1940 Act, and in accordance therewith file reports and other information with the SEC. Reports, proxy statements, registration statements and other information filed by the Corporation or the Trust (including the Registration Statement relating to the Acquiring Fund on Form N-14 of which this Proxy Statement/Prospectus is a part) may be inspected without charge and copied (for a duplication fee at prescribed rates) at the SEC’s Public Reference Room at 100 F Street, N.E., Washington, D.C. 20549 or at the SEC’s Northeast Regional Office (3 World Financial Center, New York, New York 10281) or Midwest Regional Office (175 W. Jackson Boulevard, Suite 900, Chicago, Illinois 60604). You may call the SEC at (202) 551-8090 for information about the operation of the Public Reference Room. You may obtain copies of this

information, with payment of a duplication fee, by electronic request at the following e-mail address: publicinfo@sec.gov, or by writing the SEC’s Public Reference Branch, Office of Consumer Affairs and Information Services, Securities and Exchange Commission, Washington, D.C. 20549. You may also access reports and other information about the Funds on the EDGAR database on the SEC’s Internet site at http://www.sec.gov.

i

(continued)

| Page | ||||

| 30 | ||||

| 30 | ||||

| 31 | ||||

| 31 | ||||

| 31 | ||||

| 31 | ||||

| 32 | ||||

| 32 | ||||

| 32 | ||||

| 33 | ||||

| I-1 | ||||

ii

The following is a summary of, and is qualified by reference to, the more complete information contained in this Proxy Statement/Prospectus and the information attached hereto or incorporated herein by reference, including the Agreement and Plan of Reorganization. As discussed more fully below and elsewhere in this Proxy Statement/Prospectus, the Board believes the proposed Reorganization is in the best interests of each Fund and that the interests of each Fund’s existing shareholders would not be diluted as a result of the Reorganization. If the Reorganization is approved and completed, shareholders of the Acquired Fund will become shareholders of the Acquiring Fund and will cease to be shareholders of the Acquired Fund.

Shareholders should read the entire Proxy Statement/Prospectus carefully together with the Acquiring Fund’s Prospectus that accompanies this Proxy Statement/Prospectus, which is incorporated herein by reference. This Proxy Statement/Prospectus constitutes an offering of Class A and Class I shares of the Acquiring Fund only.

On December 31, 2010, Nuveen Investments, Inc. and certain of its affiliates (“Nuveen”) completed a strategic combination with U.S. Bank National Association (“U.S. Bank”) and its wholly owned subsidiary, FAF Advisors, Inc. (“FAF Advisors”), the investment adviser to the First American Funds. As part of that transaction, U.S. Bank received a 9.5% ownership interest in Nuveen and cash consideration in exchange for Nuveen’s acquisition of a portion of FAF Advisors’ investment advisory business, including assets relating to the non-money market open-end funds in the First American family of funds (the “FAF Transaction”). Shareholders of these funds received a proxy statement in connection with the FAF Transaction pursuant to which Nuveen Fund Advisors, Inc. (“Nuveen Fund Advisors” or the “Adviser”) was appointed as the investment adviser to the funds and Nuveen Asset Management, LLC (“Nuveen Asset Management”) was appointed as the subadviser to the funds. Effective January 1, 2011, these former First American Funds became part of the Nuveen family of funds, and were re-branded as Nuveen Funds. Key investment and other personnel of FAF Advisors have become employees of Nuveen Fund Advisors and Nuveen Asset Management. The Reorganization is one of several reorganizations being proposed as part of Nuveen’s ongoing efforts to integrate the portfolio management teams and investment products it offers following the FAF Transaction. The proposed reorganizations seek to combine portfolios with similar objectives and investment strategies within the combined organization.

This Proxy Statement/Prospectus is being furnished to shareholders of the Acquired Fund in connection with the proposed combination of the Acquired Fund with and into the Acquiring Fund pursuant to the terms and conditions of the Agreement and Plan of Reorganization dated [ ] by the Corporation, on behalf of the Acquired Fund, the Trust, on behalf of the Acquiring Fund, and Nuveen Fund Advisors (the “Agreement”). The Agreement provides for (i) the transfer of all the assets of the Acquired Fund to the Acquiring Fund in exchange solely for Class A and Class I voting shares of beneficial interest, par value $0.01 per share, of the Acquiring Fund and the assumption by the Acquiring Fund of all the liabilities of the Acquired Fund; and (ii) the distribution by the Acquired Fund of Class A, Class A and Class I shares of the Acquiring Fund to the shareholders of Class A, Class C1 and Class I shares, respectively, of the Acquired Fund in complete liquidation and termination of the Acquired Fund as soon as practicable following the Closing Date (as defined herein).

1

If shareholders approve the Reorganization and it is completed, Acquired Fund shareholders will become shareholders of the Acquiring Fund. The Board has determined that the Reorganization is in the best interests of the Acquired Fund and that the interests of existing shareholders will not be diluted as a result of the Reorganization. The Board unanimously approved the Reorganization and the Agreement at a meeting held on September 20, 2011. The Board recommends a vote “FOR” the Reorganization.

If shareholders approve the Reorganization, each of the Acquired Fund and Acquiring Fund will be charged for expenses incurred in connection with the Reorganization based on its portion of the projected cost savings to the Funds during the first year following the Reorganization. Nuveen Fund Advisors estimates that Reorganization costs will be approximately $126,000 and that the cost savings during the first year following the Reorganization will be approximately $150,000 for the Acquired Fund and approximately $36,000 for the Acquiring Fund. As a result, the Acquired Fund is expected to be charged approximately $102,000, and the Acquiring Fund is expected to be charged approximately $24,000. To the extent that the payment of these expenses would cause the Acquired Fund’s expenses to exceed the expense cap then in effect, Nuveen would reimburse such expenses to the extent necessary to operate within the cap. Based on current expense levels, it is anticipated that Nuveen will reimburse all expenses charged to the Acquired Fund and none of the expenses charged to the Acquiring Fund. Nuveen will absorb any costs in excess of the estimated Reorganization costs. If the Reorganization is not approved or completed, Nuveen will pay all such Reorganization expenses.

The Board is asking shareholders of the Acquired Fund to approve the Reorganization at the Special Meeting to be held on February 16, 2012. Approval of the Reorganization requires the affirmative vote of the holders of a majority of the total number of shares outstanding and entitled to vote. See “Voting Information and Requirements” below.

If shareholders of the Acquired Fund approve the Reorganization, it is expected that the Reorganization will occur at the close of business on February 24, 2012 (the “Closing Date”), but it may be at a different time as described herein. If the Reorganization is not approved, the Board will take such action as it deems to be in the best interests of the Acquired Fund. The Closing Date may be delayed and the Reorganization may be abandoned at any time by the mutual agreement of the parties. In addition, either Fund may at its option terminate the Agreement at or before the Closing Date due to (i) a breach by any other party of any representation, warranty, or agreement contained in the Agreement to be performed at or before the Closing Date, if not cured within 30 days, (ii) a condition precedent to the obligations of the terminating party that has not been met and it reasonably appears that it will not or cannot be met, or (iii) a determination by the Board that the consummation of the transactions contemplated by the Agreement is not in the best interests of a Fund.

Reasons for the Proposed Reorganization

The Board believes that the proposed Reorganization would be in the best interests of each Fund. In approving the Reorganization, the Board considered a number of principal factors in reaching its determination, including the following:

| • | the similarities and differences in the Funds’ investment objectives and principal investment strategies; |

| • | the Funds’ relative risks; |

2

| • | the Funds’ relative sizes; |

| • | the relative investment performance of the Funds and portfolio managers; |

| • | the relative fees and expense ratios of the Funds, including caps on the Funds’ expenses agreed to by the Adviser; |

| • | the anticipated tax-free nature of the Reorganization; |

| • | the expected costs of the Reorganization and the extent to which the Funds would bear any such costs; |

| • | the terms of the Reorganization and whether the Reorganization would dilute the interests of shareholders of the Funds; |

| • | the effect of the Reorganization on shareholder services and shareholder rights; |

| • | alternatives to the Reorganization; and |

| • | any potential benefits of the Reorganization to the Adviser and its affiliates as a result of the Reorganization. |

For a more detailed discussion of the Board’s considerations regarding the approval of the Reorganization, see “The Board’s Approval of the Reorganization.”

Distribution, Purchase, Redemption, Exchange of Shares and Dividends

The Funds have substantially similar procedures for purchasing, exchanging and redeeming shares and for making distributions. The Funds’ procedures were harmonized in connection with the FAF Transaction. The Acquired Fund offers three classes of shares: Class A, Class C1 and Class I Shares. The Acquiring Fund offers four classes of shares: Class A, Class B, Class C and Class I Shares. Class A and Class I shares of the Acquired Fund have the same investment eligibility criteria as Class A and Class I shares, respectively, of the Acquiring Fund. Class C1 shareholders of the Acquired Fund will receive Class A shares of the Acquiring Fund in the Reorganization. Class C1 shares of the Acquired Fund are not available for new accounts or additional investment into existing accounts, but Class C1 shares may be issued for purposes of dividend reinvestment. See “Comparison of the Funds—Distribution, Purchase, Redemption, Exchange of Shares and Dividends” below for a more detailed discussion.

Material Federal Income Tax Consequences of the Reorganization

As a condition to closing, the Funds will receive an opinion from Vedder Price P.C. (which will be based on certain factual representations and certain customary assumptions and exclusions) substantially to the effect that the Reorganization will qualify as a tax-free reorganization under Section 368(a)(1) of the Internal Revenue Code of 1986, as amended (the “Code”). Accordingly, it is expected that no Fund will recognize gain or loss for federal income tax purposes as a direct result of the Reorganization. In connection with the Reorganization, a portion of the Acquired Fund’s portfolio assets may be sold prior to the Reorganization, which could result in the Acquired Fund declaring taxable distributions to its shareholders on or prior to the Closing Date. However, it is not expected that any material portfolio sales (i.e., more than 5% of the Acquired Fund assets) will occur in connection with the Reorganization. For a more detailed discussion of the federal income tax consequences of the Reorganization, please see “The Proposed Reorganization—Material Federal Income Tax Consequences” below.

3

The Funds have similar investment objectives. The investment objective of the Acquired Fund is to provide maximum current income that is exempt from both federal income tax and Missouri state income tax to the extent consistent with prudent investment risk. The investment objective of the Acquiring Fund is to provide investors with as high a level of current interest income exempt from regular federal, Missouri state and, in some cases, Missouri local income taxes as is consistent with preservation of capital. The investment objective of the Acquired Fund may be changed without shareholder approval upon providing notice at least 60 days in advance. The Acquiring Fund’s investment objective may not be changed without shareholder approval.

The Acquired Fund and the Acquiring Fund also have similar principal investment strategies and risks. The similarities and differences of the principal investment strategies of the Funds are:

Acquired Fund | Acquiring Fund | |

• Under normal market conditions, the Fund invests at least 80% of its net assets (plus the amount of any borrowings for investment purposes) in municipal securities that pay interest that is exempt from federal and Missouri income tax, including the federal alternative minimum tax (“AMT”). | • Under normal market conditions, the Fund invests at least 80% of its net assets in municipal bonds that pay interest that is exempt from regular federal and Missouri personal income tax. | |

• The Fund invests mainly in securities that, at the time of purchase, are either rated investment grade or are unrated and determined to be of comparable quality by the Fund’s sub-adviser.

• The Fund normally may invest up to 20% of its net assets in taxable obligations, including obligations the interest on which is subject to the federal AMT. | • The Fund invests at least 80% of its net assets in investment grade municipal bonds, which are those rated BBB/Baa or higher at the time of purchase by at least one independent rating agency, or, if unrated, judged by the Fund’s sub-adviser to be of comparable quality. | |

• The Fund may invest up to 20% of its total assets in securities that, at the time of purchase, are rated lower than investment grade or are unrated and of comparable quality (securities commonly referred to as “high-yield” securities or “junk bonds”). | • The Fund may invest up to 20% of its net assets in below investment grade municipal bonds, commonly referred to as “high yield” or “junk” bonds. | |

• The Fund may utilize futures contracts and options on futures contracts in an attempt to manage market risk, credit risk and yield curve risk, and to manage the effective maturity or duration of securities in the Fund’s portfolio. | • The Fund may invest up to 15% of its net assets in municipal securities whose interest payments vary inversely with changes in short-term tax-exempt interest rates (“inverse floaters”). | |

• The Fund will attempt to maintain the weighted average maturity of its portfolio securities at ten to twenty-five years under normal market conditions. | ||

4

Comparison of Principal Investment Strategies

The Acquired Fund and the Acquiring Fund have similar principal investment strategies and risks. However, there are some differences. The Acquired Fund has a limit of investing 20% of its net assets in taxable obligations, including those subject to the federal AMT, while the Acquiring Fund does not have a limitation on investing in obligations subject to the federal AMT. Also, the Acquiring Fund may invest up to 15% of its net assets in inverse floaters as a principal investment strategy; whereas, the Acquired Fund may invest in inverse floaters, but it is not a principal investment strategy of the Fund. In addition, the Acquired Fund may utilize futures contracts and options on futures contracts as a principal investment strategy and has a principal investment strategy of maintaining a weighted average maturity of its portfolio securities of ten to twenty-five years, while the Acquiring Fund does not have similar principal investment strategies. The Acquiring Fund, however, may utilize futures contracts, swap contracts, options on futures and swaps and other derivatives as a non-principal strategy. In addition, the Acquiring Fund generally maintains, under normal market conditions, a weighted average maturity of its portfolio securities of 15 to 30 years as a non-principal strategy. Also, the Acquiring Fund is a diversified fund, while the Acquired Fund is non-diversified, which means that the Acquiring Fund may not invest more than 5% of its net assets in securities of any one issuer (except U.S. government securities or with respect to 25% of its assets).

In evaluating the Reorganization, each Acquired Fund shareholder should consider the risks of investing in the Acquiring Fund. The principal risks of investing in the Acquiring Fund are described in the section below entitled “Risk Factors.”

The Reorganization may result in one-time brokerage costs for the Acquired Fund to the extent it is necessary for the Acquired Fund to sell holdings prior to the Reorganization so that the Acquiring Fund’s portfolio immediately following the Reorganization remains in compliance with its investment policies and restrictions. If the Reorganization had occurred as of November 30, 2011, the Acquiring Fund would not have been required to dispose of securities of the Acquired Fund in order to comply with its investment policies and restrictions, and would not have sold any material portion (i.e., more than 5% of its assets) of the securities in the Acquired Fund’s portfolio solely as a result of the Reorganization.

The tables below provide information about the fees and expenses attributable to each class of shares of the Funds, and the pro forma fees and expenses of the combined fund. You may qualify for sales charge discounts on purchases of Class A shares if you and your family invest, or agree to invest in the future, at least $50,000 in a Fund or other Nuveen mutual funds. Shareholder fees reflect the fees currently in effect for each Fund. Annual Fund Operating Expenses for the Acquired Fund have been restated to take into account the new fee and expense structure adopted by the Fund as of January 1, 2011 following the closing of the FAF Transaction. The fees and expenses for the Acquired Fund are estimated based on the actual fees and expenses incurred by the Fund from January 1, 2011 through May 31, 2011, which have been annualized. Annual Fund Operating Expenses for the Acquiring Fund reflect the Fund’s fees and expenses as of its fiscal year ended May 31, 2011. The pro forma fees and expenses are based on the amounts shown in the table for each Fund, assuming the Reorganization occurred as of May 31, 2011. Note that Class C1 shareholders of the Acquired Fund will receive Class A shares of the Acquiring Fund in the Reorganization.

5

Shareholder Fees

(paid directly from your investment)

| Acquired Fund | Acquiring Fund | Combined Fund Pro Forma | ||||||||||

Maximum Sales Charge (Load) Imposed on Purchases (as a percentage of offering price) | ||||||||||||

Class A | 4.20% | 4.20% | 4.20% | |||||||||

Class C1 | None | N/A | N/A | |||||||||

Class I | None | None | None | |||||||||

Maximum Deferred Sales Charge (Load) (as a percentage of the lesser of purchase price or redemption proceeds) | ||||||||||||

Class A | None | None | None | |||||||||

Class C11 | 1.00% | N/A | N/A | |||||||||

Class I | None | None | None | |||||||||

Maximum Sales Charge (Load) Imposed on Reinvested Dividends | ||||||||||||

Class A | None | None | None | |||||||||

Class C1 | None | N/A | N/A | |||||||||

Class I | None | None | None | |||||||||

Exchange Fees | ||||||||||||

Class A | None | None | None | |||||||||

Class C1 | None | N/A | N/A | |||||||||

Class I | None | None | None | |||||||||

Annual Low Balance Account fee (for accounts under $1,000)2 | ||||||||||||

Class A | $15 | $15 | $15 | |||||||||

Class C1 | $15 | N/A | N/A | |||||||||

Class I | $15 | $15 | $15 | |||||||||

| 1 | The CDSC on Class C1 shares applies only to redemptions within 12 months of purchase. |

| 2 | Fee applies to the following types of accounts held directly with the Fund: accounts established pursuant to the Uniform Transfers to Minors Act (UTMA) or Uniform Gifts to Minors Act (UGMA). |

Annual Fund Operating Expenses

(expenses that you pay each year as a percentage of the value of your investment)

| Acquired Fund | Acquiring Fund | Combined Fund Pro Forma1 | ||||||||||

Management Fees | ||||||||||||

Class A | 0.65 | % | 0.53% | 0.53% | ||||||||

Class C1 | 0.65 | % | N/A | N/A | ||||||||

Class I | 0.65 | % | 0.53% | 0.53% | ||||||||

Distribution and Service (12b-1) Fees | ||||||||||||

Class A | 0.20 | % | 0.20% | 0.20% | ||||||||

Class C1 | 0.65 | % | N/A | N/A | ||||||||

Class I | 0.00 | % | 0.00% | 0.00% | ||||||||

Other Expenses | ||||||||||||

Class A | 0.09 | % | 0.09% | 0.08% | ||||||||

Class C1 | 0.09 | % | N/A | N/A | ||||||||

Class I | 0.09 | % | 0.09% | 0.08% | ||||||||

6

| Acquired Fund | Acquiring Fund | Combined Fund Pro Forma1 | ||||||||||

Total Annual Fund Operating Expenses | ||||||||||||

Class A | 0.94% | 0.82% | 0.81% | |||||||||

Class C1 | 1.39% | N/A | N/A | |||||||||

Class I | 0.74% | 0.62% | 0.61% | |||||||||

Fee Waivers and/or Expense Reimbursements | ||||||||||||

Class A | (0.04% | )2 | (0.00)% | (0.00)% | ||||||||

Class C1 | (0.04% | )2 | N/A | N/A | ||||||||

Class I | (0.04% | )2 | (0.00)% | (0.00)% | ||||||||

Total Annual Fund Operating Expenses–After Fee Waivers and/or Expense Reimbursements | ||||||||||||

Class A | 0.90% | 0.82% | 0.81% | |||||||||

Class C1 | 1.35% | N/A | N/A | |||||||||

Class I | 0.70% | 0.62% | 0.61% | |||||||||

| 1 | Pro forma expenses do not include the expenses to be charged to the Funds in connection with the Reorganization. See “The Proposed Reorganization—Reorganization Expenses” for additional information about these expenses. |

| 2 | Nuveen Fund Advisors has agreed to waive fees and reimburse expenses for the Acquired Fund through March 31, 2013 so that Total Annual Fund Operating Expenses, after fee waivers and/or expense reimbursements and excluding Acquired Fund Fees and Expenses, do not exceed 0.90%, 1.35% and 0.70% for Class A, Class C1 and Class I, respectively. Fee waivers and expense reimbursements will not be terminated prior to that time without approval of the Board. |

Example

The example below is intended to help you compare the cost of investing in each Fund and the pro forma cost of investing in the combined fund. The example assumes you invest $10,000 in a Fund for the time periods indicated (based on information in the tables above) and then either redeem or do not redeem your shares at the end of a period. The example assumes that your investment has a 5% return each year and that a Fund’s expenses remain at the level shown in the table above. Expense caps are taken into account for the periods stated in the table above. Although your actual costs may be higher or lower, based on these assumptions your costs would be:

| Acquired Fund | Acquiring Fund | Combined Fund Pro Forma | ||||||||||

1 Year | ||||||||||||

Assuming you sold your shares at the end of each period | ||||||||||||

Class A | $ | 508 | $ | 500 | $ | 499 | ||||||

Class C1 | $ | 137 | N/A | N/A | ||||||||

Class I | $ | 72 | $ | 63 | $ | 62 | ||||||

Assuming you kept your shares | ||||||||||||

Class A | $ | 508 | $ | 500 | $ | 499 | ||||||

Class C1 | $ | 137 | N/A | N/A | ||||||||

Class I | $ | 72 | $ | 63 | $ | 62 | ||||||

7

| Acquired Fund | Acquiring Fund | Combined Fund Pro Forma | ||||||||||

3 Years | ||||||||||||

Assuming you sold your shares at the end of each period | ||||||||||||

Class A | $ | 703 | $ | 671 | $ | 668 | ||||||

Class C1 | $ | 436 | N/A | N/A | ||||||||

Class I | $ | 233 | $ | 199 | $ | 195 | ||||||

Assuming you kept your shares | ||||||||||||

Class A | $ | 703 | $ | 671 | $ | 668 | ||||||

Class C1 | $ | 436 | N/A | N/A | ||||||||

Class I | $ | 233 | $ | 199 | $ | 195 | ||||||

5 Years | ||||||||||||

Assuming you sold your shares at the end of each period | ||||||||||||

Class A | $ | 915 | $ | 856 | $ | 851 | ||||||

Class C1 | $ | 757 | N/A | N/A | ||||||||

Class I | $ | 408 | $ | 346 | $ | 340 | ||||||

Assuming you kept your shares | ||||||||||||

Class A | $ | 915 | $ | 856 | $ | 851 | ||||||

Class C1 | $ | 757 | N/A | N/A | ||||||||

Class I | $ | 408 | $ | 346 | $ | 340 | ||||||

10 Years | ||||||||||||

Assuming you sold your shares at the end of each period | ||||||||||||

Class A | $ | 1,523 | $ | 1,391 | $ | 1,380 | ||||||

Class C1 | $ | 1,665 | N/A | N/A | ||||||||

Class I | $ | 915 | $ | 774 | $ | 762 | ||||||

Assuming you kept your shares | ||||||||||||

Class A | $ | 1,523 | $ | 1,391 | $ | 1,380 | ||||||

Class C1 | $ | 1,665 | N/A | N/A | ||||||||

Class I | $ | 915 | $ | 774 | $ | 762 | ||||||

Each Fund pays transaction costs, such as commissions, when it buys and sells securities (or “turns over” its portfolio). A higher portfolio turnover rate may indicate higher transaction costs and may result in higher taxes when Fund shares are held in a taxable account. These costs, which are not reflected in annual fund operating expenses or in the example, affect each Fund’s performance. During their most recent fiscal periods for which audited financial statements are available, the Funds had the following portfolio turnover rates:

Fund | Fiscal Period | Rate | ||

Acquired Fund | Eleven months ended 5/31/11 | 10% | ||

Acquiring Fund | Twelve months ended 5/31/11 | 6% |

After the Reorganization is completed, the portfolio manager of the Acquiring Fund may, in his discretion, sell securities acquired from the Acquired Fund. To the extent that the portfolio manager chooses to sell a significant percentage of such securities, the Acquiring Fund’s portfolio turnover rate and brokerage costs may be higher than they otherwise would have been.

8

In evaluating the Reorganization, you should consider carefully the risks of the Acquiring Fund to which you will be subject if the Reorganization is approved and completed. Investing in a mutual fund involves risk, including the risk that you may receive little or no return on your investment or even that you may lose part or all of your investment. Because of these and other risks, you should consider an investment in the Acquiring Fund to be a long-term investment. An investment in the Acquiring Fund may not be appropriate for all shareholders. For a complete description of the risks of an investment in the Acquiring Fund, see the section in the Acquiring Fund’s Prospectus entitled “Principal Risks.”

Because the Funds have similar investment strategies, the principal risks of each Fund are similar. The principal risks of investing in the Acquiring Fund are described below. An investment in the Acquired Fund is also subject to each of these risks; however, as noted above, the Acquiring Fund may invest more of its assets in securities subject to the federal AMT and in inverse floating rate securities. In addition, the principal risks of the Acquired Fund include futures contract risk and non-diversification risk.

Alternative Minimum Tax Risk. The Fund has no limit as to the amount that can be invested in bonds subject to the federal AMT; therefore, all or a portion of the Fund’s otherwise exempt-interest dividends may be taxable to those shareholders subject to the federal AMT.

Call Risk. If an issuer calls higher-yielding bonds held by the Fund, performance could be adversely impacted.

Credit Risk. Credit risk is the risk that an issuer of a municipal bond may be unable or unwilling to make interest and principal payments when due and the related risk that the value of a bond may decline because of concerns about the issuer’s ability or willingness to make such payments. In addition, parties to other financial contracts with the Fund could default on their obligations.

High Yield Securities Risk. High yield securities generally are less liquid, have more volatile prices, and have greater credit risk than investment grade securities.

Income Risk. The Fund’s income could decline during periods of falling interest rates. Also, if the Fund invests in inverse floaters, the Fund’s income may decrease if short-term interest rates rise.

Interest Rate Risk. Interest rate risk is the risk that the value of the Fund’s portfolio will decline because of rising interest rates. Interest rate risk may be increased by the Fund’s investment in inverse floaters because of the leveraged nature of these investments.

Inverse Floaters Risk. The use of inverse floaters by the Fund creates effective leverage. Due to the leveraged nature of these investments, they will typically be more volatile and involve greater risk than the fixed rate municipal bonds underlying the inverse floaters. In other words, the value of an inverse floater will fluctuate to a significantly greater extent than the values of the fixed rate municipal bonds underlying the inverse floaters in response to changes in market interest rates or credit quality. Distributions on inverse floaters bear an inverse relationship to short-term municipal bond interest rates. Thus, distributions paid to the Fund on its inverse floaters will be reduced or even eliminated as short-term municipal interest rates rise and will increase when short-term municipal interest rates fall. Inverse floaters generally will underperform the market for fixed rate municipal bonds in a rising

9

interest rate environment. An investment in inverse floaters typically will involve greater risk than an investment in a fixed rate municipal bond, including, in the case of certain inverse floaters, the risk that the Fund may lose more than its original principal investment.

Market Risk. The market values of municipal bonds owned by the Fund may decline, at times sharply and unpredictably.

State Concentration Risk. Because the Fund primarily purchases municipal bonds from Missouri, the Fund is more susceptible to adverse economic, political or regulatory changes affecting municipal bond issuers in that state.

Tax Risk. Income from municipal bonds held by the Fund could be declared taxable because of unfavorable changes in tax laws, adverse interpretations by the Internal Revenue Service or state tax authorities, or noncompliant conduct of a bond issuer. On September 12, 2011, President Obama submitted to Congress the American Jobs Act of 2011 (the “Jobs Act”). If enacted in its proposed form, the Jobs Act generally would limit the exclusion from gross income of tax-exempt interest (which includes exempt-interest dividends received from the Fund) for individuals whose adjusted gross income for federal income tax purposes exceeds certain thresholds for taxable years beginning on or after January 1, 2013 in order to provide a tax benefit not greater than 28% of such interest. Such proposal could affect the value of the municipal bonds owned by the Fund. The likelihood of the Jobs Act being enacted in the form introduced or in some other form cannot be predicted. Shareholders should consult their own tax advisors regarding the potential consequences of the Jobs Act on their investment in the Fund.

Fundamental Investment Restrictions

The Funds have similar fundamental investment restrictions that cannot be changed without shareholder approval, with the exception that the Acquired Fund’s investment objective may be changed by the Board without shareholder approval. In accordance with federal securities laws, each Fund’s policy to invest at least 80% of its net assets in municipal bonds that pay interest that is exempt from regular federal and Missouri state income tax and, in the case of the Acquired Fund, the federal AMT is fundamental. Also, both Funds have adopted a policy of not concentrating their investments in any industry, except that state or municipal governments and their political subdivisions are not considered members of any industry. The Acquiring Fund is a diversified fund, and the Acquired Fund is a non-diversified fund.

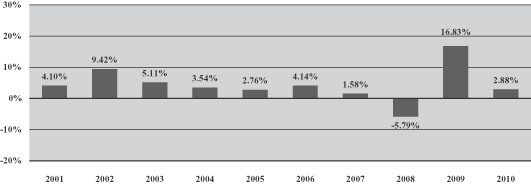

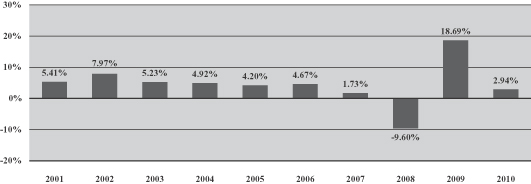

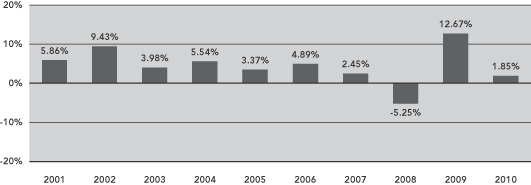

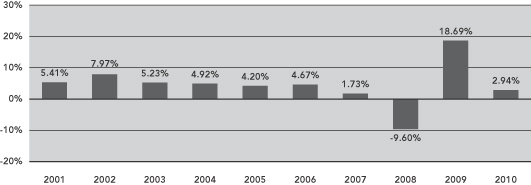

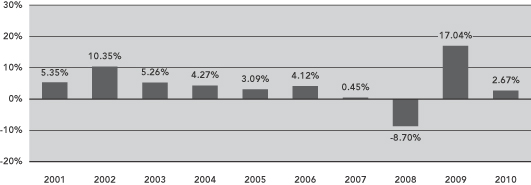

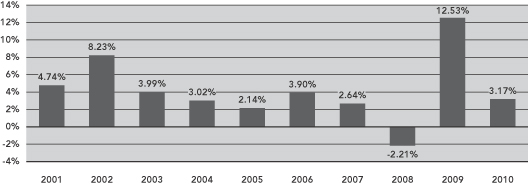

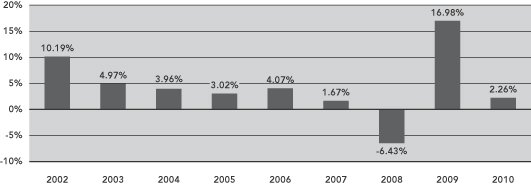

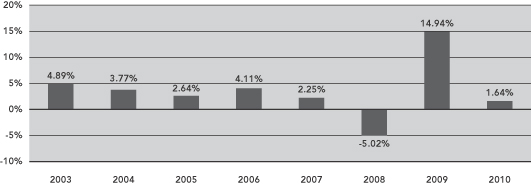

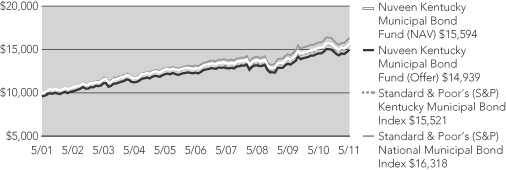

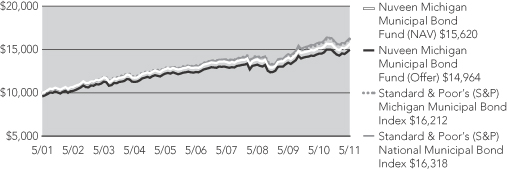

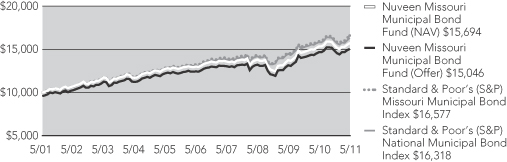

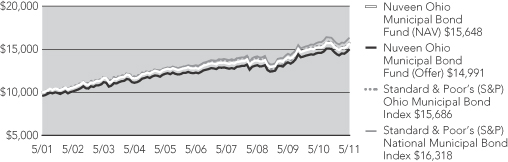

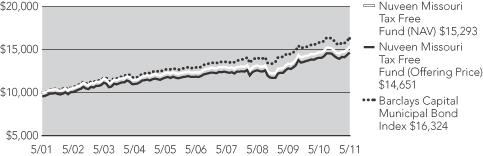

The total returns of the Funds for the periods ended December 31, 2010, based on historical fees and expenses for each period, are set forth in the chart and tables below.

The bar chart below illustrates annual calendar year returns for the Acquired Fund’s Class I shares and the Acquiring Fund’s Class A shares. The bar chart and highest/lowest quarterly returns that follow do not reflect Class A’s sales charge, and if this charge were reflected, the returns would be less than those shown. The tables below illustrate average annual returns for the periods ended December 31, 2010 for each Fund. The tables also show how each Fund’s performance compares with the returns of a broad measure of market performance and an index of funds with similar investment objectives. This information is intended to help you assess the variability of Fund returns (and consequently, the potential risks of a Fund investment).

10

All after-tax returns are calculated using the historical highest individual federal marginal income tax rates and do not reflect the impact of state and local taxes. For the Acquired Fund, after-tax returns are shown for Class I shares only; after-tax returns for Class A and Class C1 shares will vary. For the Acquiring Fund, after-tax returns are shown for Class A shares only; after-tax returns for Class I shares will vary. Returns for market indices do not include expenses, which are deducted from Fund returns, or taxes.

Your own actual after-tax returns will depend on your specific tax situation and may differ from what is shown here.

Performance reflects fee waivers, if any, in effect during the periods presented. If any such waivers were not in place, performance would be reduced. Past performance (before and after taxes) does not necessarily indicate future performance. Updated performance information is available at www.nuveen.com or by calling (800) 257-8787.

Acquired Fund – Class I Annual Total Return

During the periods shown in the bar chart, the Acquired Fund’s Class I highest and lowest calendar quarter returns were 8.16% and -3.98%, respectively, for the quarters ended September 30, 2009 and September 30, 2008. The Acquired Fund’s Class I year-to-date return through September 30, 2011 was 9.08%.

Acquiring Fund – Class A Total Return

During the periods shown in the bar chart, the Acquiring Fund’s Class A highest and lowest calendar quarter returns were 8.87% and -4.83%, respectively, for the quarters ended September 30,

11

2009 and December 31, 2008. The Acquiring Fund’s Class A year-to-date return through September 30, 2011 was 9.16%.

| Average Annual Total Returns for the Periods Ended December 31, 2010 | ||||||||||||||||

Acquired Fund | 1 Year | 5 Years | 10 Years | Since Inception (Class C1) | ||||||||||||

Class A (return before taxes) | (1.61 | )% | 2.57 | % | 3.62 | % | N/A | |||||||||

Class C1 (return before taxes) (Inception Date 9/24/01) | 2.22 | % | 3.01 | % | N/A | 3.44 | % | |||||||||

Class I (return before taxes) | 2.88 | % | 3.68 | % | 4.32 | % | N/A | |||||||||

Class I (return after taxes on distributions) | 2.84 | % | 3.61 | % | 4.24 | % | N/A | |||||||||

Class I (return after taxes on distributions and sale of fund shares) | 3.39 | % | 3.75 | % | 4.30 | % | N/A | |||||||||

Barclays Capital Municipal Bond Index (reflects no deduction for fees, expenses or taxes) | 2.38 | % | 4.09 | % | 4.83 | % | 3.44 | % | ||||||||

Lipper Other States Municipal Debt Funds Category | 1.11 | % | 2.90 | % | 3.81 | % | 3.60 | % | ||||||||

| Average Annual Total Returns for the Periods Ended December 31, 2010 | ||||||||||||

Acquiring Fund | 1 Year | 5 Years | 10 Years | |||||||||

Class A (return before taxes) | (1.42 | )% | 2.41 | % | 3.97 | % | ||||||

Class A (return after taxes on distributions) | (1.42 | )% | 2.39 | % | 3.95 | % | ||||||

Class A (return after taxes on distributions and sale of fund shares) | 0.58 | % | 2.67 | % | 4.04 | % | ||||||

Class I (return before taxes) | 3.27 | % | 3.49 | % | 4.62 | % | ||||||

Standard & Poor’s National Municipal Bond Index (reflects no deduction for fees, expenses or taxes) | 2.45 | % | 3.83 | % | 4.82 | % | ||||||

Standard & Poor’s Missouri Municipal Bond Index (reflects no deduction for fees, expenses or taxes) | 2.40 | % | 3.92 | % | 4.96 | % | ||||||

Lipper Peer Group (reflects no deduction for taxes or certain expenses) | 1.11 | % | 2.90 | % | 3.81 | % | ||||||

Investment Adviser and Sub-Adviser

Both Funds are managed by Nuveen Fund Advisors, which offers advisory and investment management services to a broad range of mutual fund clients. Nuveen Fund Advisors has overall responsibility for management of the Funds, oversees the management of the Funds’ portfolios, manages the Funds’ business affairs and provides certain clerical, bookkeeping and other administrative services. Nuveen Fund Advisors is located at 333 West Wacker Drive, Chicago, Illinois 60606. Nuveen Fund Advisors is a subsidiary of Nuveen Investments, Inc. (“Nuveen Investments”). On November 13, 2007, Nuveen Investments was acquired by investors led by Madison Dearborn Partners, LLC, which is a private equity investment firm based in Chicago, Illinois. The Nuveen family of advisers has been providing advice to investment companies since 1976.

Nuveen Fund Advisors has selected its affiliate, Nuveen Asset Management, located at 333 West Wacker Drive, Chicago, Illinois 60606, to serve as a sub-adviser to each of the Funds. Nuveen Asset Management manages the investment of the Funds’ assets on a discretionary basis, subject to the supervision of Nuveen Fund Advisors.

Prior to the FAF Transaction, the Acquired Fund was advised by FAF Advisors, a wholly-owned subsidiary of U.S. Bank National Association.

12

The Funds have been managed by the same portfolio manager since the FAF Transaction. Christopher L. Drahn, CFA, is the portfolio manager for the Funds. He has served as the portfolio manager for the Acquired Fund since December 2002 and the Acquiring Fund since January 2011. He entered the financial services industry when he joined FAF in 1980. He joined Nuveen Asset Management on January 1, 2011 in connection with the FAF Transaction and currently serves as a senior vice president. As of October 31, 2011, he manages 6 state-specific Nuveen-sponsored municipal bond funds, with a total of approximately $796 million under management.

For a complete description of the advisory services provided to the Acquiring Fund, see the section of the Fund’s Prospectus entitled “Who Manages the Funds” and the section of the Fund’s Statement of Additional Information entitled “Adviser and Sub-Adviser.”

Pursuant to investment management agreements between Nuveen Fund Advisors and the Corporation, on behalf of the Acquired Fund, and Nuveen Fund Advisors and the Trust, on behalf of the Acquiring Fund, each Fund pays Nuveen Fund Advisors fund-level fees, payable monthly, at the annual rates set forth below:

Acquired Fund - Management Fee | Acquiring Fund - Management Fee | |||||||||

Average Daily Net Assets | Fee Rate | Average Daily Net Assets | Fee Rate | |||||||

For the first $125 million | 0.4500% | For the first $125 million | 0.3500% | |||||||

For the next $125 million | 0.4375% | For the next $125 million | 0.3375% | |||||||

For the next $250 million | 0.4250% | For the next $250 million | 0.3250% | |||||||

For the next $500 million | 0.4125% | For the next $500 million | 0.3125% | |||||||

For the next $1 billion | 0.4000% | For the next $1 billion | 0.3000% | |||||||

For net assets over $2 billion | 0.3750% | For the next $3 billion | 0.2750% | |||||||

| For net assets over $5 billion | 0.2500% | |||||||||

In addition to the fund-level fee, each Fund pays a complex-level fee. The maximum complex-level fee is 0.20% of the Fund’s average daily net assets, based upon complex-level “eligible assets” of $55 billion. Therefore, the maximum management fee rate for each Fund is the fund-level fee rate plus 0.20%. As complex-level eligible assets increase, the complex-level fee rate decreases pursuant to a breakpoint schedule. Each Fund’s individual complex-level fee rate is determined by taking the current overall complex-level fee rate, which is based on the aggregate amount of the “eligible assets” of all Nuveen funds, and making an upward adjustment to that rate (subject to the maximum 0.20% rate noted above) based upon the percentage of the Fund’s assets, if any, that are not “eligible assets.”

Nuveen Fund Advisors has agreed to waive fees and reimburse expenses for the Acquired Fund through March 31, 2013 so that total annual fund operating expenses, after fee waivers and/or expense reimbursements and excluding the fees and expenses of other investment companies in which the Acquired Fund invests, do not exceed 0.90%, 1.35% and 0.70% for Class A, Class C1 and Class I, respectively. The Acquired Fund fee waivers and expense reimbursement will not be terminated prior to that time without approval of the Board.

13

For the Acquired Fund’s annualized five-month period ended May 31, 2011 and for the Acquiring Fund’s fiscal year ended May 31, 2011, each Fund paid Nuveen Fund Advisors the following management fees (net of fee waivers and expense reimbursements, where applicable) as a percentage of average net assets:

| Management Fee Rate | ||||

Acquired Fund | 0.59 | % | ||

Acquiring Fund | 0.53 | % | ||

Each Fund has adopted a distribution and service plan (the “Plans”) pursuant to Rule 12b-1 under the 1940 Act. Under the Plans, Class C1 shares are subject to a distribution fee, and Class A shares and Class C1 shares are subject to a service fee. Class I shares are not subject to either distribution or service fees.

Under the Plans, (a) for each Fund, Class A shares are subject to an annual service fee of 0.20% of the average daily net assets of Class A shares and (b) for the Acquired Fund, Class C1 shares are subject to (i) an annual distribution fee of 0.40% of the average daily net assets of Class C1 shares and (ii) an annual service fee of 0.25% of the average daily net assets of Class C1 shares. For a complete description of these arrangements for the Acquiring Fund, see the section of the Fund’s Prospectus entitled “What Share Classes We Offer” and the section of the Fund’s Statement of Additional Information entitled “Distributor.”

As of the closing of the FAF Transaction, the same individuals constitute the Board of each Fund, and the Corporation and the Trust have the same officers. The management of each Fund, including general oversight of the duties performed by Nuveen Fund Advisors under the Investment Management Agreement for each Fund, is the responsibility of the Board. There are currently ten members of the Board, one of whom is an “interested person” (as defined in the 1940 Act) and nine of whom are not interested persons (the “independent board members”). The names and business addresses of the board members and officers of the Acquiring Fund and their principal occupations and other affiliations during the past five years are set forth under “Directors and Executive Officers” in the Statement of Additional Information for the Acquiring Fund incorporated herein by reference.

Distribution, Purchase, Redemption, Exchange of Shares and Dividends

The Acquired Fund offers three classes of shares: Class A, Class C1 and Class I shares. The Acquiring Fund offers four classes of shares: Class A, Class B, Class C and Class I shares. You may purchase, redeem or exchange shares of the Funds on any business day, which is any day the New York Stock Exchange is open for business. You may purchase, redeem or exchange shares of each Fund through a financial advisor or other financial intermediary or directly from such Fund. Class C1 shares of the Acquired Fund are not available for new accounts or additional investment into existing accounts, but Class C1 shares may be issued for purposes of dividend reinvestment. The Acquiring Fund’s initial and subsequent investment minimums generally are as follows, although the Fund may reduce or waive the minimums in some cases. The Acquired Fund’s investment minimums for Class A and Class I shares are identical to the Acquiring Fund’s investment minimums for Class A and Class I shares, respectively.

14

| Class A | Class I | |||||

Eligibility and Minimum Initial Investment | $3,000 | Available only through fee-based programs and to other limited categories of investors as described in the prospectus.

$100,000 for all accounts except:

• $250 for clients of financial intermediaries and family offices that have accounts holding Class I shares with an aggregate value of at least $100,000 (or that are expected to reach this level).

• No minimum for certain other categories of eligible investors as described in the prospectus. | ||||

Minimum Additional Investment | $100 | No minimum. | ||||

No initial sales charge or contingent deferred sales charges will be imposed on shares of the Acquiring Fund received or shares of the Acquired Fund exchanged in connection with the Reorganization.

For a complete description of purchase, redemption and exchange options, see the section of the Acquiring Fund’s Prospectus entitled “How You Can Buy and Sell Shares” and “General Information” and the section of the Acquiring Fund’s Statement of Additional Information entitled “Purchase and Redemption of Fund Shares.”

Each Fund declares dividends daily and pays such dividends monthly. Each Fund declares and pays any taxable capital gains or other taxable distributions once a year at year end. If the Reorganization is approved by the shareholders of the Acquired Fund, the Acquired Fund intends to distribute to its shareholders, prior to the closing of the Reorganization, all its net investment income and net capital gains, if any, for the period ending on the Closing Date.

The Funds intend to make distributions that are exempt from regular federal and Missouri state income tax. All or a portion of all distributions, however, may be subject to the federal AMT. The Funds’ distributions that are not designated as exempt-interest dividends are generally taxed as ordinary income or capital gains for regular federal income tax purposes.

Payments to Broker-Dealers and Other Financial Intermediaries

If you purchase shares of a Fund through a broker-dealer or other financial intermediary (such as a bank or financial advisor), the Fund, its distributor or its investment adviser may pay the intermediary for the sale of Fund shares and related services. These payments may create a conflict of interest by influencing the broker-dealer or other financial intermediary and your salesperson to recommend the Fund over another investment. Ask your financial advisor or visit your financial intermediary’s website for more information.

15

Additional information concerning the Acquiring Fund and Acquired Fund is contained in this Proxy Statement/Prospectus and additional information regarding the Acquiring Fund is contained in the accompanying Acquiring Fund prospectus. The cover page of this Proxy Statement/Prospectus describes how you may obtain further information.

The proposed Reorganization will be governed by the Agreement, which is attached as Appendix I. The Agreement provides that the Acquired Fund will transfer all its assets to the Acquiring Fund solely in exchange for the issuance of full and fractional voting shares of the Acquiring Fund and the assumption by the Acquiring Fund of all the liabilities of the Acquired Fund. The closing of the Reorganization will take place at the close of business on the Closing Date. The following discussion of the Agreement is qualified in its entirety by the full text of the Agreement.

The Acquired Fund will transfer all its assets to the Acquiring Fund, and in exchange, the Acquiring Fund will assume all the liabilities of the Acquired Fund and deliver to the Acquired Fund a number of full and fractional shares of the Acquiring Fund having a net asset value equal to the value of the assets of the Acquired Fund less the liabilities of the Acquired Fund assumed by the Acquiring Fund. At the designated time on the Closing Date as set forth in the Agreement, the Acquired Fund will distribute in complete liquidation of the Acquired Fund, pro rata to its shareholders of record, all Acquiring Fund shares received by the Acquired Fund. This distribution will be accomplished by the transfer of the Acquiring Fund shares credited to the account of the Acquired Fund on the books of the Acquiring Fund to open accounts on the share records of the Acquiring Fund in the name of the Acquired Fund shareholders, and representing the respective pro rata number of Acquiring Fund shares due such shareholders. All issued and outstanding shares of the Acquired Fund will simultaneously be canceled on the books of the Acquired Fund. As a result of the proposed Reorganization, each Acquired Fund Class A, Class C1 and Class I shareholder will receive a number of Acquiring Fund Class A, Class A and Class I shares, respectively, equal in value, as of the close of regular trading on the New York Stock Exchange on the Closing Date, to the value of the Acquired Fund Class A, Class C1 or Class I shares surrendered by such shareholder.

The Board has determined that the proposed Reorganization is in the best interests of each Fund and that the interests of shareholders will not be diluted as a result of the transactions contemplated by the Agreement.

The consummation of the Reorganization is subject to the terms and conditions of, and the representations and warranties being true as set forth in, the Agreement. The Agreement may be terminated by mutual agreement of the Funds. In addition, either Fund may at its option terminate the Agreement at or before the Closing Date due to (i) a breach by any other party of any representation, warranty, or agreement to be performed at or before the Closing Date, if not cured within 30 days, (ii) a condition precedent to the obligations of the terminating party that has not been met and it reasonably appears that it will not or cannot be met, or (iii) a determination by the Board that the consummation of the transactions contemplated by the Agreement is not in the best interests of a Fund.

The Acquired Fund will, within a reasonable period of time before the Closing Date, furnish the Acquiring Fund with a list of the Acquired Fund’s portfolio securities and other investments. The

16

Acquiring Fund will, within a reasonable period of time before the Closing Date, furnish the Acquired Fund with a list of the securities, if any, on the Acquired Fund’s list referred to above that do not conform to the Acquiring Fund’s investment objective, policies, and restrictions. The Acquired Fund, if requested by the Acquiring Fund, will dispose of securities on the Acquiring Fund’s list before the Closing Date. In addition, if it is determined that the portfolios of the Funds, when aggregated, would contain investments exceeding certain percentage limitations imposed upon the Acquiring Fund with respect to such investments, the Acquired Fund, if requested by the Acquiring Fund, will dispose of a sufficient amount of such investments as may be necessary to avoid violating such limitations as of the Closing Date. The sale of such investments could result in taxable distributions to shareholders of the Acquired Fund prior to the Reorganization. Notwithstanding the foregoing, nothing in the Agreement will require the Acquired Fund to dispose of any investments or securities if, in the reasonable judgment of the Board or the Adviser, such disposition would adversely affect the tax-free nature of the Reorganization for federal income tax purposes or would otherwise not be in the best interests of the Acquired Fund. See “Material Federal Income Tax Consequences” below. However, it is not expected that any material portfolio sales (i.e., more than 5% of the Acquired Fund’s net assets) will occur in connection with the Reorganization.

As noted above, if the Reorganization had occurred as of November 30, 2011, the Acquiring Fund would not have been required to dispose of securities of the Acquired Fund in order to comply with its investment policies and restrictions, and would not have sold any material portion (i.e., more than 5% of its net assets) of the securities in the Acquired Fund’s portfolio solely as a result of the Reorganization.

Description of Securities to be Issued

Shares of Beneficial Interest. The Acquiring Fund has established and designated four classes of shares, par value $0.01 per share, including Class A and Class I shares. The Trust’s declaration of trust (the “Declaration of Trust”) permits the Board, in its sole discretion, and subject to compliance with the 1940 Act, to further subdivide the shares of the Acquiring Fund into one or more other classes of shares.

Voting Rights of Shareholders. Holders of shares of the Acquiring Fund are entitled to one vote per share on matters as to which they are entitled to vote, with fractional shares voting proportionally. The Acquiring Fund operates as a series of the Trust, an open-end management investment company registered with the SEC under the 1940 Act. The Trust currently has six series, including the Acquiring Fund, and the Board may, in its sole discretion, create additional series from time to time. Separate votes generally are taken by each series on matters affecting an individual series. In addition to the specific voting rights described above, shareholders of the Acquiring Fund are entitled, under current law, to vote with respect to certain other matters, including changes in fundamental investment policies and restrictions. Moreover, shareholders owning at least 10% of the outstanding shares entitled to vote may request that the Board call a shareholders’ meeting.

Continuation of Shareholder Accounts and Plans; Change in Exchange Privileges; Share Certificates

If the Reorganization is approved, the Acquiring Fund will establish an account for each Acquired Fund shareholder containing the appropriate number of shares of the appropriate class of the Acquiring Fund. Shareholders of the Acquired Fund who are accumulating shares through systematic investing,

17

or who are receiving payments under the systematic withdrawal plan, will retain the same rights and privileges after the Reorganization through plans maintained by the Acquiring Fund. The shareholder services and shareholder programs of the Funds are substantially similar, and services provided to shareholders generally are not expected to change, except to the extent services differ because the Funds have different transfer agents. Both Funds currently have exchange procedures that provide that shareholders may exchange their shares into the same class of another Nuveen mutual fund provided that such funds utilize the same transfer agent. Accordingly, because the Acquiring Fund and Acquired Fund utilize different transfer agents, if the Reorganization is approved and completed, the eligible exchange options for Acquired Fund shareholders will change. No certificates for Acquiring Fund shares will be issued as part of the Reorganization.

U.S. Bank National Association serves as the custodian for the assets of the Acquired Fund and State Street Bank & Trust Company serves as the custodian for the assets of the Acquiring Fund. U.S. Bancorp Fund Services, LLC serves as transfer agent for the Acquired Fund and Boston Financial Data Services, LLC serves as transfer agent for the Acquiring Fund. Ernst & Young LLP serves as the independent auditors for the Acquired Fund and PricewaterhouseCoopers LLP serves as independent auditors for the Acquiring Fund.

Material Federal Income Tax Consequences

As a condition to each Fund’s obligation to consummate the Reorganization, each Fund will receive a tax opinion from Vedder Price P.C. (which opinion will be based on certain factual representations and certain customary assumptions and exclusions) substantially to the effect that, on the basis of the existing provisions of the Internal Revenue Code of 1986, as amended (the “Code”), current administrative rules and court decisions, for federal income tax purposes:

| 1. | The transfer of all the assets of the Acquired Fund to the Acquiring Fund in exchange solely for Acquiring Fund shares and the assumption by the Acquiring Fund of all the liabilities of the Acquired Fund, followed by the pro rata distribution to the Acquired Fund shareholders of all the Acquiring Fund shares received by the Acquired Fund in complete liquidation of the Acquired Fund, will constitute a “reorganization” within the meaning of Section 368(a) of the Code, and the Acquiring Fund and the Acquired Fund will each be a “party to a reorganization” within the meaning of Section 368(b) of the Code with respect to the Reorganization. |