Table of Contents

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORMN-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number:811-07763

LITMAN GREGORY FUNDS TRUST

(Exact name of registrant as specified in charter)

1676 N. California Blvd., Suite 500

Walnut Creek, CA 94596

(Address of principal executive offices)(Zip code)

(Name and Address of Agent for Service)

Jeremy L. DeGroot

1676 N. California Blvd., Suite 500

Walnut Creek, CA 94596

Registrant’s telephone number, including area code: (925)254-8999

Date of fiscal year end: December 31

Date of reporting period: December 31, 2019

Table of Contents

Item 1. Report to Shareholders.

The following is a copy of the report transmitted to shareholders pursuant to Rule30e-1 under the Investment Company Act of 1940, as amended (the “Act”):

Table of Contents

LITMAN GREGORY FUNDS TRUST

Annual Report

Litman Gregory Masters Equity Fund

Litman Gregory Masters International Fund

Litman Gregory Masters Smaller Companies Fund

Litman Gregory Masters Alternative Strategies Fund

Litman Gregory Masters High Income Alternatives Fund

December 31, 2019

Beginning on January 1, 2021, as permitted by regulations adopted by the Securities and Exchange Commission, paper copies of the Litman Gregory Masters Funds’ shareholder reports will no longer be sent by mail, unless you specifically request paper copies of the reports from the Litman Gregory Masters Funds or from your financial intermediary, such as a broker-dealer or bank. Instead, the reports will be made available on www.mastersfunds.com, and you will be notified by mail each time a report is posted and provided with a website link to access the report.

If you already elected to receive shareholder reports electronically, you will not be affected by this change; and you need not take any action. You may elect to receive shareholder reports and other communications from the Litman Gregory Masters Funds or your financial intermediary electronically by notifying your financial intermediary directly or, if you are a direct investor, by calling 800-960-0188.

You may elect to receive all future reports in paper free of charge. If you invest through a financial intermediary, you can contact your financial intermediary to request that you continue to receive paper copies of your reports. If you invest directly with the Litman Gregory Masters Funds, you can call 800-960-0188. Your election to receive reports in paper will apply to all funds held with the Litman Gregory Masters Funds or your financial intermediary.

Table of Contents

Litman Gregory Masters Funds Concept

Investment Philosophy: Alternative Strategies and High Income Alternatives Fund

The Alternative Strategies Fund and the High Income Alternatives Fund were created based on the following fundamental beliefs:

First, Litman Gregory believes it is possible to identify investment managers who will deliver superior long-term performance relative to their passive benchmarks and peer groups. This belief is based on Litman Gregory’s extensive experience evaluating managers and mutual funds on behalf of their clients. The managers in these funds were chosen for their specialized and demonstrated expertise, as well as for their complementary,non-correlated investment approaches.

Second, not only do we want high-quality managers, but we want to offer access to them at an acceptable cost. We spent years engaged in research to find the right mix of managers we believe can deliver on both fronts.

Third, these funds don’t seek to simply replicate what each manager is already doing elsewhere, but to bring investors additionalvalue-add through flexibility, and the ability to be more opportunistic.

The Litman Gregory Masters Alternative Strategies Fund Concept

The Alternative Strategies Fund is a multi-manager fund that combines alternative and absolute-return-oriented strategies chosen based on Litman Gregory’s conviction that each individual strategy is compelling and that collectively the overall fund portfolio is well-diversified. This fund is intended to complement traditional stock and bond portfolios by offering diversification, seeking to reduce volatility, and to potentially enhance returns relative to various measures of risk.

This fund will contain many risk-control factors including the selection of strategies that seek lower risk exposure than conventional stock or stock-bond strategies, the risk-sensitive nature of the managers, the skill of the managers, and the overall strategy diversification.

Typically, each manager will run between 18% to 25% of the portfolio, but Litman Gregory may tactically alter the managers’ allocations to attempt to take advantage of particularly compelling opportunities for a specific strategy or to further manage risk. We will have a high hurdle for making a tactical allocation shift and don’t expect suchtop-down shifts to happen frequently.

The Litman Gregory Masters High Income Alternatives Fund Concept

The High Income Alternatives Fund is a multi-managed fund created to include multiple types of income-producing investments that could improve returns and diversify risks while playing an important strategic role in navigating interest rate and credit cycles.

We partnered with skilled, experienced managers running differentiated strategies. Each offers access to alternative sources of income that clients may otherwise not own, or to which they may be under-allocated. We seek to generate a high level of income with an eye toward capital preservation—meaning that we don’t want to chase high income without consideration for valuations and risk.

Investment Philosophy: The Equity Funds

Our equity funds are based on two fundamental beliefs:

First,it is possible to identify investment managers who will deliver superior long-term performance relative to their passive benchmarks and peer groups. This belief is based on our extensive experience evaluating stock pickers and mutual funds on behalf of our investment management clients.

Second, thatmost stock pickers have an unusually high level of conviction in only a small number of stocks and that a portfolio limited to these stocks will, on average, outperform a more diversified portfolio over a market cycle. However, most stock pickers typically manage portfolios that are diversified beyond these highest-conviction holdings in order to reduce risk and to facilitate the management of the larger amounts of money they oversee.

The Concept Behind Our Equity Funds

Based on the above beliefs, these funds seek to isolate the stock-picking skills of a group of highly regarded investment managers. To meet this objective, the funds are designed with both risk and return in mind, placing particular emphasis on the following factors:

| • | We only choose stock pickers we believe to be exceptionally skilled. |

| • | Each stock picker runs a very concentratedsub-portfolio of not more than 15 of his or her “highest-conviction” stocks. |

| • | Although each manager’s portfolio is concentrated, our equity funds seek to manage risk partly by building diversification into each fund. |

| ¡ | The Equity and International funds offer diversification by including managers with differing investment styles andmarket-cap orientations. |

| ¡ | The Smaller Companies Fund brings together managers who use different investment approaches, though each focuses on the securities of smaller companies. |

| • | We believe that excessive asset growth often results in diminished performance. Therefore, each fund may close to new investors at a level that Litman Gregory believes will preserve each manager’s ability to effectively implement the Litman Gregory Masters Funds concept. If moresub-advisors are added to a particular fund, the fund’s closing asset level may be increased. |

Diversification does not assure a profit or protect against a loss in a declining market.

| ii | Litman Gregory Funds Trust | |||||

Table of Contents

| 2 | ||

| 5 | ||

| 6 | ||

Litman Gregory Masters Equity Fund | ||

| 8 | ||

| 12 | ||

| 13 | ||

Litman Gregory Masters International Fund | ||

| 15 | ||

| 21 | ||

| 22 | ||

Litman Gregory Masters Smaller Companies Fund | ||

| 25 | ||

| 29 | ||

| 30 | ||

Litman Gregory Masters Alternative Strategies Fund | ||

| 31 | ||

| 42 | ||

| 43 | ||

Litman Gregory Masters High Income Alternatives Fund | ||

| 88 | ||

| 96 | ||

| 97 | ||

| 111 | ||

| 112 | ||

| 114 | ||

Statements of Changes in Net Assets | ||

| 115 | ||

| 115 | ||

| 116 | ||

| 116 | ||

| 117 | ||

Financial Highlights | ||

| 118 | ||

| 119 | ||

| 120 | ||

| 121 | ||

| 122 | ||

| 123 | ||

| 124 | ||

| 125 | ||

| 147 | ||

| 153 | ||

| 154 | ||

| 156 | ||

| 161 | ||

| 162 | ||

| 164 |

This report is intended for shareholders of the funds and may not be used as sales literature unless preceded or accompanied by a current prospectus for the Litman Gregory Masters Funds. Statements and other information in this report are dated and are subject to change.

Litman Gregory Fund Advisors, LLC has ultimate responsibility for the funds’ performance due to its responsibility to oversee its investment managers and recommend their hiring, termination and replacement.

| Table of Contents | 1 | |||||

Table of Contents

Litman Gregory Fund Advisors’

We are deeply committed to making each Litman Gregory Masters Fund a highly satisfying long-term investment for shareholders. In following through on this commitment we are guided by our core values, which influence four specific areas of service:

First, we are committed to the Litman Gregory Masters concept.

| • | We will only hire managers who we strongly believe will deliver exceptional long-term returns relative to their benchmarks. We base this belief on extremely thorough due diligence research. This not only requires us to assess their stock-picking skills, but also to evaluate their ability to add incremental performance by investing in a concentrated portfolio of their highest conviction ideas. |

| • | We will monitor each of the managers so that we can maintain our confidence in their ability to deliver the long-term performance we expect. In addition, our monitoring will seek to assess whether they are staying true to their Litman Gregory Masters Funds mandate. Consistent with this mandate, we focus on long-term performance evaluation so that the Masters managers will not be distracted by short-term performance pressure. |

Second, we will do all we can to ensure that the framework within which our stock pickers do their work further increases the odds of success.

| • | Investments from new shareholders in each fund are expected to be limited so that each fund’s asset base remains small enough to retain flexibility to add value. |

| • | The framework also includes the diversified multi-manager structure that makes it possible for each manager to invest, when appropriate, in an opportunistic manner knowing that the potential volatility within his or her portfolio will be diluted at the fund level by the performance of the other managers. In this way, the multi-manager structure seeks to provide fund-level diversification. |

| • | We will work hard to discourage short-term speculators so that cash flows into the funds are not volatile. Lower volatility helps prevent our managers from being forced to sell stocks at inopportune times or to hold excessive cash for non-investment purposes. |

Third, is our commitment to do all we can from an operational standpoint to maximize shareholder returns.

| • | We will remain attentive to fund overhead, and whenever we achieve savings we will pass them through to shareholders. For example, we have had several manager changes that resulted in lower sub-advisory fees to our funds. In every case we have passed through the full savings to shareholders in the form of fee waivers. |

| • | We will provide investors with a low minimum, no-load, no 12b-1 Institutional share class for all Litman Gregory Masters Funds, and a low minimum, no-load Investor share class for the Alternative Strategies and High Income Alternatives funds |

| • | We also will work closely with our managers to make sure they are aware of tax-loss selling opportunities (only to be taken if there are equally attractive stocks to swap into). We account for partial sales on a specific tax lot basis so that shareholders will benefit from the most favorable tax treatment. The goal is not to favor taxable shareholders over tax-exempt shareholders but to make sure that the managers are taking advantage of tax savings opportunities when doing so is not expected to reduce pre-tax returns. |

Fourth, is our commitment to communicate honestly about all relevant developments and expectations.

| • | We will continue to do this by providing thorough and educational shareholder reports. |

| • | We will continue to provide what we believe are realistic assessments of the investment environment. |

Our commitment to Litman Gregory Masters Funds is also evidenced by our own investment. Our employees have, collectively, substantial investments in the funds, as does our company retirement plan. In addition, we use the funds extensively in the client accounts of our investment advisor practice (through our affiliate Litman Gregory Asset Management, LLC). We have no financial incentive to do so because the fees we receive from Litman Gregory Masters Funds held in client accounts are fully offset against the advisory fees paid by our clients. In fact, we have a disincentive to use the funds in our client accounts because each Litman Gregory Masters Fund is capacity constrained (they may be closed as mentioned above), and by using them in client accounts we are using up capacity for which we may not be paid. But we believe these funds offer value that we can’t get elsewhere and this is why we enthusiastically invest in them ourselves and on behalf of clients.

While we believe highly in the ability of the Funds’ sub-advisors, our commitments are not intended as guarantees of future results.

While the funds are no-load, there are management fees and operating expenses that do apply, as well as a 12b-1 fee that applies to Investor class shares. Please refer to the prospectus for further details.

Diversification does not assure a profit or protect against loss in a declining market.

| 2 | Litman Gregory Funds Trust | |||||

Table of Contents

Must be preceded or accompanied by a prospectus.

Each of the funds may invest in foreign securities. Investing in foreign securities exposes investors to economic, political, and market risks and fluctuations in foreign currencies. Each of the funds may invest in the securities of small companies. Small-company investing subjects investors to additional risks, including security price volatility and less liquidity than investing in larger companies. Debt obligations of distressed companies typically are unrated, lower rated, in default or close to default and may become worthless. The International Fund will invest in emerging markets. Investments in emerging market countries involve additional risks such as government dependence on a few industries or resources, government-imposed taxes on foreign investment or limits on the removal of capital from a country, unstable government, and volatile markets. Investments in debt securities typically decrease when interest rates rise. This risk is usually greater for longer-term debt securities. Investments in mortgage-backed securities include additional risks that investor should be aware of including credit risk, prepayment risk, possible illiquidity, and default, as well as increased susceptibility to adverse economic developments. Investments in lower-rated and non-rated securities present a greater risk of loss to principal and interest than higher-rated securities. The funds may invest in master limited partnership units. Investing in MLP units may expose investors to additional liability and tax risks. Derivatives may involve certain costs and risks such as liquidity, interest rate, market, credit, management, and the risk that a position could not be closed when most advantageous. Investing in derivatives could lose more than the amount invested. The funds may make short sales of securities, which involves the risk that losses may exceed the original amount invested.

The Morningstar Rating for funds, or “star rating”, is calculated for managed products (including mutual funds, variable annuity and variable life subaccounts, exchange-traded funds, closed end funds, and separate accounts) with at least a three-year history. Exchange-traded funds and open ended mutual funds are considered a single population for comparative purposes. It is calculated based on a Morningstar Risk-Adjusted Return measure that accounts for variation in a managed products monthly excess performance, placing more emphasis on downward variations and rewarding consistent performance. The top 10% of products in each product category receive 5 stars, the next 22.5% receive 4 stars, the next 35% receive 3 stars the next 22.5% receive 2 stars, and the bottom 10% receive 1 star. The Overall Morningstar Rating for a managed product is derived from a weighted average of the performance figures associated with its three-, five, and 10-year (if applicable) Morningstar Rating metrics. The weights are 100% three-year rating for 36-59 months of total returns, 60% five-year rating/40% three-year rating for 60-119 months of total returns, and 50% 10-year rating/30% five-year rating/20% three-year rating for 120 or more months of total returns. While the 10 year overall rating formula seems to give the most weight to the 10-year period, the most recent three-year period actually has the greatest impact because it is included in all three rating periods. Litman Gregory Masters Alternative Strategies Fund was rated against the following numbers of Multialternative funds over the following time periods as of 12/31/2019: 237 funds in the last three years, and 187 funds in the last five years. With respect to these Multialternative funds, Litman Gregory Masters Alternative Strategies (MASFX) received a Morningstar Rating of 3 stars and 4 stars for the three- and five-year periods, respectively. Ratings for other share classes may be different. Morningstar rating is for the Institutional share class only; other classes may have different performance characteristics. The Investor share class received a rating of 3 stars and 4 stars for the three- and five-year periods, respectively.

Merger arbitrage investments risk loss if a proposed reorganization in which the fund invests is renegotiated or terminated.

Investments in absolute return strategies are not untended to outperform stocks and bonds during strong market rallies.

Multi-investment management styles may lead to higher transaction expenses compared to single investment management styles. Outcomes depend on the skill of the sub-advisors and advisor and the allocation of assets amongst them.

Past performance does not guarantee future results.

Mutual fund investing involves risk; loss of principal is possible.

Performance discussions for the Alternative Strategies Fund and the High Income Alternatives Fund are specifically related to the Institutional share class.

Some of the comments are based on current management expectation and are considered “forward-looking statements”. Actual future results, however, may prove to be different from our expectations. You can identify forward-looking statement by words such as “estimate”, “may”, “expect”, “should”, “could”, “believe”, “plan”, and similar terms. We cannot promise future returns and our opinions are a reflection of our best judgment at the time this report is compiled.

Opinions expressed are subject to change, are not guaranteed and should not be considered recommendations to buy or sell any security.

Sharpe ratio is the measure of a fund’s return relative to its risk. The Sharpe ratio uses standard deviation to measure a fund’s risk-adjusted returns. The higher a fund’s Sharpe ratio, the better a fund’s returns have been relative to the risk it has taken on. Because it uses standard deviation, the Sharpe ratio can be used to compare risk-adjusted returns across all fund categories. The Litman Gregory Masters Alternative Strategies Fund’s Sharpe ratio ranked 1 out of 105 in its Peer Group, US OE Multialternative Morningstar Category from 10/1/2011 to 12/31/2019. Past performance is no guarantee of future results.

| Fund Summary | 3 | |||||

Table of Contents

See pages 9, 16, and 26 for each fund’s top contributors. See pages 10, 19 and 28 for each fund’s portfolio composition. See pages 41 for the Alternative Strategies Fund’s individual strategy portfolio allocations. See pages 94 for the High Income Alternative Fund’s individual strategy portfolio allocations. Fund holdings and/or sector allocations are subject to change at any time and are not recommendations to buy or sell any security.

Diversification does not assure a profit or protect against a loss in a declining market.

Leverage may cause the effect of an increase or decrease in the value of the portfolio securities to be magnified and the fund to be more volatile than if leverage was not used.

References to other mutual funds should not be interpreted as an offer of these securities.

Litman Gregory Fund Advisors LLC has ultimate responsibility for the performance of the Masters Funds due to its responsibility to oversee the investment managers and recommend their hiring, termination and replacement.

Any tax or legal information provided is merely a summary of our understanding and interpretation of some of the current income tax regulations and it is not exhaustive. Investors must consult their tax advisor or legal counsel for advice and information concerning their particular situation. Neither the Funds nor any of their representatives may give legal or tax advice.

Please see page 154 for index definitions. You cannot invest directly in an index.

Please see page 156 for industry definitions.

| 4 | Litman Gregory Funds Trust | |||||

Table of Contents

Litman Gregory Masters Funds’ Performance

| Average Annual Total Returns | ||||||||||||||||||||||||||||

| Institutional Class Performance as of 12/31/2019 | Three- Month | 1-Year | 3-Year | 5-Year | 10-Year | 15-Year | Since Inception | |||||||||||||||||||||

Litman Gregory Masters Equity Fund (12/31/96) | 10.10% | 27.55% | 11.66% | 8.87% | 11.56% | 6.98% | 8.32% | |||||||||||||||||||||

Russell 3000 Index | 9.10% | 31.02% | 14.57% | 11.24% | 13.42% | 9.03% | 8.71% | |||||||||||||||||||||

Morningstar Large Blend Category Average | 8.10% | 28.59% | 13.25% | 9.53% | 11.47% | 7.66% | 7.24% | |||||||||||||||||||||

Gross Expense Ratio: 1.29% Net Expense Ratio as of 4/30/19*: 1.17% | ||||||||||||||||||||||||||||

Litman Gregory Masters International Fund (12/1/97) | 10.68% | 30.45% | 8.50% | 2.85% | 4.70% | 5.42% | 7.08% | |||||||||||||||||||||

MSCI ACWI ex-U.S. Index | 8.92% | 21.51% | 9.87% | 5.51% | 4.97% | 5.25% | 5.38% | |||||||||||||||||||||

MSCI EAFE Index | 8.17% | 22.01% | 9.56% | 5.67% | 5.50% | 4.84% | 5.02% | |||||||||||||||||||||

Morningstar Foreign Large Blend Category Average | 8.36% | 21.40% | 9.15% | 5.18% | 5.07% | 4.56% | 4.21% | |||||||||||||||||||||

Gross Expense Ratio: 1.33% Net Expense Ratio as of 4/30/19*: 1.09% | ||||||||||||||||||||||||||||

Litman Gregory Masters Smaller Companies Fund (6/30/2003) | 6.28% | 23.72% | 8.21% | 5.49% | 9.58% | 6.11% | 7.91% | |||||||||||||||||||||

Russell 2000 Index | 9.94% | 25.52% | 8.59% | 8.23% | 11.83% | 7.92% | 9.74% | |||||||||||||||||||||

Morningstar Small Blend Category Average | 7.98% | 23.33% | 6.59% | 6.67% | 10.59% | 7.11% | 8.99% | |||||||||||||||||||||

Gross Expense Ratio: 1.80% Net Expense Ratio as of 4/30/19*: 1.38% | ||||||||||||||||||||||||||||

Litman Gregory Masters Alternative Strategies Fund (9/30/2011) | 1.91% | 8.52% | 3.56% | 3.33% | n/a | n/a | 4.76% | |||||||||||||||||||||

3-Month LIBOR | 0.54% | 2.61% | 1.93% | 1.33% | n/a | n/a | 0.94% | |||||||||||||||||||||

Bloomberg Barclays Aggregate Bond Index | 0.18% | 8.72% | 4.03% | 3.05% | n/a | n/a | 2.95% | |||||||||||||||||||||

Morningstar Multialternative Category Average | 1.64% | 7.48% | 2.71% | 1.22% | n/a | n/a | 1.92% | |||||||||||||||||||||

HFRX Global Hedge Fund Index | 2.62% | 8.68% | 2.42% | 1.20% | n/a | n/a | 1.82% | |||||||||||||||||||||

Russell 1000 Index | 9.04% | 31.43% | 15.05% | 11.48% | n/a | n/a | 15.90% | |||||||||||||||||||||

Gross Expense Ratio as of 10/31/19: 1.64% | ||||||||||||||||||||||||||||

Net Expense Ratio as of 10/31/19: 1.36% | | The Net Expense Ratio reflects a contractual fee waiver and/or expense reimbursement, which is in place through 4/30/2021. See the Fund’s prospectus for more information. | | |||||||||||||||||||||||||

Adjusted Expense Ratio as of 10/31/19: 1.28% | | The Adjusted Expense Ratio is the same as the Net Expense Ratio exclusive of certain investment expenses, such as interest expense from borrowings and repurchase agreements, dividend expense from investments on short sales, and acquired fund fees and expenses. | | |||||||||||||||||||||||||

Litman Gregory Masters High Income Alternatives Fund (9/28/2018) | 1.44% | 8.37% | n/a | n/a | n/a | n/a | 3.99% | |||||||||||||||||||||

Bloomberg Barclays Aggregate Bond Index | 0.18% | 8.72% | n/a | n/a | n/a | n/a | 8.27% | |||||||||||||||||||||

ICE BofAML U.S. High Yield TR USD Index | 2.61% | 14.41% | n/a | n/a | n/a | n/a | 7.18% | |||||||||||||||||||||

HFRX Fixed Income—Credit Index | 2.52% | 6.20% | n/a | n/a | n/a | n/a | 2.36% | |||||||||||||||||||||

Gross Expense Ratio as of 4/30/19: 2.06% | ||||||||||||||||||||||||||||

Net Expense Ratio as of 4/30/19: 1.70% | | The Net Expense Ratio reflects a contractual fee waiver and/or expense reimbursement, which is in place through 4/30/2021. See the Fund’s prospectus for more information. | | |||||||||||||||||||||||||

Adjusted Expense Ratio as of 4/30/19: 0.98% | | The Adjusted Expense Ratio is the same as the Net Expense Ratio exclusive of certain investment expenses, such as interest expense from borrowings and repurchase agreements, dividend expense from investments on short sales, and acquired fund fees and expenses. | | |||||||||||||||||||||||||

Performance quoted represents past performance and does not guarantee future results. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance of the funds may be lower or higher than the performance quoted. To obtain the performance of the funds as of the most recently completed calendar month, please visitwww.mastersfunds.com.

The performance quoted does not include a deduction for taxes that a shareholder would pay on distributions or the redemption of fund shares.

*Gross and net expense ratios per the Prospectus dated 4/30/2019. There are contractual fee waivers in effect through 4/30/2021. Indexes are unmanaged, do not incur expenses, taxes or fees and cannot be invested in directly.

MSCI index returns source: MSCI. Neither MSCI nor any other party involved in or related to compiling, computing, or creating the MSCI data makes any express or implied warranties or representations with respect to such data (or the results to be obtained by the use thereof), and all such parties hereby expressly disclaim all warranties of originality, accuracy, completeness, merchantability, or fitness for a particular purpose with respect to any of such data. Without limiting any of the foregoing, in no event shall MSCI, any of its affiliates, or any third party involved in or related to compiling, computing, or creating the data have any liability for any direct, indirect, special, punitive, consequential, or any other damages (including lost profits) even if notified of the possibility of such damages.No further distribution or dissemination of the MSCI data is permitted without MSCI’s express written consent.Source note: Returns prior to 1999 are the MSCI ACWI ex-US GR index. Returns from 1999 onwards are MSCI ACWI ex-US NR index.

| Fund Summary | 5 | |||||

Table of Contents

What a difference a year makes. 2019 began with investors reeling from the nearly 20% decline in global equity markets in the fourth quarter of 2018. However, following the Federal Reserve’s (the Fed’s) pivot to looser monetary policy and a break in the U.S./China trade war, markets rebounded strongly and finished the year on a high note.

Across global equity markets, U.S. large-cap stocks were once again at the top of the leader board. The S&P 500 Index posted gains in every quarter and ended the year at an all-time high. The index’s 31.5% total return was its second-best year since 1997, trailing only its 33% gain in 2013. Growth stocks again trounced value stocks, with the Russell 1000 Growth Stock Index beating its Value Index counterpart by ten percentage points, extending a record 12-year trend. Smaller-cap U.S. stocks (Russell 2000 Index) rose 25.5% for the year, with small-cap growth beating small-cap value by six percentage points.

Foreign equity markets were also strong but trailed the U.S. market. Developed International stocks (MSCI EAFE Index) gained 22.0% for the year. After struggling in the third quarter, emerging-market (EM) stocks (MSCI Emerging Markets Index) shot up almost 12% in the fourth quarter and returned 18.4% for the year.

Domestic credit markets also did very well, with high-yield bonds (BofA Merrill Lynch U.S. High-Yield Cash Pay Index) gaining 14.4%. Somewhat surprisingly, core bonds also posted strong returns in what could be considered a “risk-on” market environment. On the back of three Fed rate cuts, the 10-year Treasury yield declined nearly 80 basis points and the core bond index (Bloomberg Barclays Aggregate Bond Index) returned 8.7%, its best annual return since 2002 (a year when the S&P 500lost 22%).

Note that it wasn’t corporate profit growth that drove stocks higher in 2019. Reported earnings for the S&P 500 were flat over the first three quarters of the year, with a low single-digit percentage increase projected for the fourth quarter. Instead, roughly two-thirds or more of the S&P’s return came from a sharp expansion in valuation multiples. The index’s price-to-earnings (P/E) ratio shot up from 19x trailing GAAP1 earnings to 23x at year-end. Meanwhile, the forward P/E, based on analyst earnings expectations, ended the year above 18x, close to its highest level outside of the tech stock bubble of 1999-2000. Many other valuations metrics also suggest the U.S. market is overvalued.

For the year, the Litman Gregory Masters International Fund gained 30.45%, strongly outperforming the 21.51% return for the MSCI ACWI ex USA Index. The Litman Gregory Masters Equity Fund gained 27.55%, trailing the 31.02% for its Russell 3000 Index benchmark. The Litman Gregory Masters Smaller Companies Fund was up 23.72%, compared to 25.52% for the Russell 2000 Index. The Litman Gregory Masters Alternative Strategies Fund returned 8.52%, compared to 2.61% for 3-month LIBOR and 7.50% for the Morningstar Multialternative category. Since inception, the Masters Alternative Strategies Fund has the highest risk-adjusted return (as measured by both the Sharpe and Sortino ratios) in its Morningstar category. Finally, the Litman Gregory Masters High Income Alternatives Fund gained 8.37%, compared to an 8.72% return for the Bloomberg Barclays Aggregate Bond Index, 14.41% for the BofA Merrill Lynch U.S. High-Yield Cash Pay Index and 6.22% for the HFRX Fixed Income – Credit Index.

Please see the individual fund annual reports for additional performance details and portfolio manager commentary.

We believe the Litman Gregory Masters Funds can fill a valuable role within a diversified investment portfolio. Each of the Masters Funds is sub-advised by a group of highly disciplined, experienced, and skilled investors who we believe can outperform their benchmark over a market cycle. On our three equity funds, each manager runs a distinctive, concentrated, high-conviction stock portfolio, with the goal of materially outperforming their respective market index over the long term. Our Alternative Strategies Fund can serve as a core, lower-risk yet opportunistic holding that provides access to proven managers and strategies, differentiated sources of return, and beneficial diversification relative to traditional bond and stock investments. The High Income Alternatives Fund is intended to be a complement to traditional fixed-income allocations, seeking long-term returns that are significantly higher than core fixed-income and comparable to high-yield bonds, but with lower volatility and downside risk than high-yield due to the fund’s diversified sources of return and manager strategy flexibility.

As always, we thank you for your continued trust and confidence. Our commitment and confidence are reflected in the collective personal investments in the funds by Litman Gregory principals, employees, and the Funds’ trustees of over $20 million, as of December 31, 2019.

| 6 | Litman Gregory Funds Trust | |||||

| 1 | GAAP= generally accepted accounting principles. A combination of authoritative standards (set by policy boards) and the commonly accepted ways of recording and reporting accounting information. |

Table of Contents

Sincerely,

Jeremy DeGroot, President and Portfolio Manager

Jack Chee, Portfolio Manager

Rajat Jain, Portfolio Manager

Jason Steuerwalt, Portfolio Manager

| Fund Summary | 7 | |||||

Table of Contents

Litman Gregory Masters Equity Fund Review

The Litman Gregory Masters Equity Fund returned 27.55% in 2019, underperforming both the 31.02% return for the Russell 3000 Index benchmark and the 28.59% return for the Morningstar Large Blend category. Since its inception on December 31, 1996, the Fund’s 8.32% average annual return slightly trails the benchmark but is ahead of its peer group’s 7.24% return.

Performance as of 12/31/2019 |

| |||||||||||||||||||||||||||

| Average Annual Total Returns | ||||||||||||||||||||||||||||

| Three Month | One- Year | Three- Year | Five- Year | Ten- Year | Fifteen- Year | Since Inception | ||||||||||||||||||||||

Litman Gregory Masters Equity Fund Institutional (12/31/96) | 10.10% | 27.55% | 11.66% | 8.87% | 11.56% | 6.98% | 8.32% | |||||||||||||||||||||

Russell 3000 Index | 9.10% | 31.02% | 14.57% | 11.24% | 13.42% | 9.03% | 8.71% | |||||||||||||||||||||

Morningstar Large Blend Category* | 8.10% | 28.59% | 13.25% | 9.53% | 11.47% | 7.66% | 7.24% | |||||||||||||||||||||

| Performance quoted represents past performance and does not guarantee future results. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance of the funds may be lower or higher than the performance quoted. To obtain standardized performance of the funds, and performance as of the most recently completed calendar month, please visitwww.mastersfunds.com.As of the prospectus dated 4/30/2019, the gross and net expense ratios for the Institutional Class were1.29% and1.17%, respectively. There are contractual fee waivers in effect through April 30, 2021. |

| |||||||||||||||||||||||||||

Performance of Managers

2019 was a stark reversal from the prior year. 2018 was the equity market’s first negative calendar year return since 2008, but a pivot from the Federal Reserve helped markets soar in 2019. Three out of the seven managers outperformed their respective benchmarks. Dick Weiss of Wells Capital was the top performing manager in 2019 – tacking 31.80% onto his track record that goes back to the Fund’s 1996 inception. Weiss has outperformed his Russell 3000 benchmark by almost six percentage points (an average) since inception. Scott Moore from Nuance Investments and Bill Nygren from Harris Associates also outpaced their respective value benchmarks last year. (Returns are net of sub-advisor management fees.)

Longer term, five of the seven managers are outperforming their respective benchmarks since their inception on the fund. We expect the two managers currently underperforming will make up relative ground during downdrafts in the stock market. Neither manager during their tenure on the fund has yet experienced an extended market environment where the benefits of their investment process would add the most value.

Key Performance Drivers

For the 2019 calendar-year period, both stock selection and sector allocations detracted from fund performance. It is important to understand that the portfolio is built stock by stock and that sector weightings are a residual of the bottom-up fundamental stock-picking process employed by each sub-advisor. That said, we do report on the short-term relative performance of both sector weights and stock selection to help shareholders understand the drivers of recent performance. It is also important to remember that the performance of a stock over a relatively short period tells us nothing about whether it will be a successful position; that is only known at the point when the stock is sold.

The Fund’s top performing position in 2019 was Visa. The stock price increased 43.32% last year. At year-end, Visa is the fund’s largest position and is owned by two sub-advisors (Clyde McGregor of Harris Associates and Sands Capital). Both managers have owned the stock for several years and point to Visa’s deep payments network that serves as a critical link connecting merchants, merchant acquirers, and card issuers as part of the appeal of the business. Additionally, Visa’s growth driver—the trend of paper payments to electronic payments—remains intact. Frank Sands, Jr. and Mike Sramek of Sands Capital note that electronic consumer payments are still only 40 to 50 percent penetrated globally. Many developed markets are over 60 percent penetrated, but some—like Germany, Italy, and Japan—are only around 30 percent penetrated. In addition, most emerging markets outside of China are under 30 percent penetrated.

Another top contributor in 2019 was Alphabet, which is owned by Nygren and Sands Capital. As traditional modes of advertising continue to shift online, both sub-advisors point to Alphabet’s dominance and ability to capitalize on targeted advertising. Alphabet’s infrastructure takes advantage of search intent, which is among the most powerful types of data that can be used to target advertisements, supporting high return on investment (ROI) for the company’s advertiser customers. Sands Capital expects Google Search and YouTube, in their opinion, both highly differentiated businesses to continue driving growth going forward, as more commerce moves online and YouTube continues to improve its capabilities for direct response advertisers.

Alibaba, the global e-commerce giant based in China, is a top-10 position at year-end. It was among the top contributor in 2019. Both Sands Capital and Chris Davis and Danton Goei of Davis Advisors own the stock. The duo at Davis Advisors initiated a position in Alibaba in the first quarter of 2019. They say Alibaba connects businesses and consumers in close to 200 countries via its online

| 8 | Litman Gregory Funds Trust | |||||

Table of Contents

platforms. The company is the largest e-commerce marketplace in the world. Given the company’s enviable competitive position, increasing use as an advertising platform, and promising investments abroad, Davis and Goei expect Alibaba to grow e-commerce revenues at a faster rate than the e-commerce market overall. When also considering the company’s leadership position in emerging businesses with large potential such as internet payments (Alipay), internet finance (ANT Financial), cloud computing (Alibaba Cloud), digital media (Youku Tudou), and offline retail (multiple investments), they believe Alibaba is uniquely positioned in the world’s largest online market.

Hilton Worldwide, owned by McGregor, was also among the top returners in 2019. The stock price increased 55.47% during the year. McGregor contends that Hilton recently transformed into an asset-light, fee-driven company with a more resilient earnings profile that he believes is currently under appreciated by the market. He says Hilton generates over 90% of its profits from franchise, management and incentive fees with long-term contracts; this model requires minimal capital investment and allows Hilton to convert its net income into free cash flow, which it can use to capitalize on attractive acquisition opportunities and fund share repurchases. The company continues to gain market share across all brands and regions and full-year 2019 is on pace to be the fifth consecutive year of net unit growth in excess of 6%. Importantly, Hilton’s development pipeline remained robust through the third quarter (with more than 2,530 hotels consisting of nearly 379,000 rooms throughout 111 countries and territories) and was tracking modestly above management’s expectations. Hilton has a wide spectrum of competitive advantages including the ability to leverage technology to offer guests superior quality and convenience, broad geographic coverage, diversity across brands from mid-range to luxury lodgings and loyalty programs that provide benefits to guests that choose accommodations within its collection.

The fund’s largest detractor in 2019 was Qurate Retail. The stock was owned by Nygren and sold during the third quarter. Quarte owns television shopping channels QVC and HSN (Home Shopping Network). Nygren says earnings results last year were weaker than market expectations. Revenues within QVC, HSN and Zulily declined mid-single digits, while investors were expecting revenue growth from these divisions. Margins were decent, in Nygren’s assessment, considering the surprising revenue decline, which led to earnings per share of $0.35, which exceeded market projections of $0.32. Synergy from the HSN acquisition was on target, and management committed to providing a quarterly update to report actual progress compared with goals. However, Nygren opted to eliminate the position in the company in July to pursue other investment opportunities where they thought there is more upside potential.

Mylan, a healthcare company owned by Weiss, was a detractor during 2019. The company announced quarterly results earlier in the year which were below expectations highlighted by weakness in Europe and this led to some skepticism about the back ended nature of the year. He felt this was sufficiently explained, however, management also announced that after eight months, a corporate strategic review was still ongoing and it was likely they would detail the outcome of this review in late-July at their analyst day. Given how long it’s been (almost a year by that point), the street was highly disappointed and shares underperformed in the first half of the year. Further, concerns over the company’s potential growth trajectory and strategic vision have been a headwind for the company. However, Weiss believes there are several events, including some business line rationalizations and corporate governance changes that could occur and that would be positive. In addition, recent launches of gAdvair and biosimilar Neulasts are gaining traction and should aid revenue growth in the quarters ahead. The company looks attractive on private market value estimates, creating a compelling risk-reward scenario.

| Top 10 Individual Contributors as of the Year Ended December 31, 2019 | ||||||||||||||||||

| Company Name | Fund Weight (%) | Benchmark Weight (%) | 12-Month Return (%) | Contribution to Return (%) | Economic Sector | |||||||||||||

Visa Inc. Class A | 3.29 | 1.00 | 43.32 | 1.32 | Information Technology | |||||||||||||

Alphabet Inc. A | 3.80 | 1.23 | 28.18 | 1.18 | Communication Services | |||||||||||||

Capital One Financial Corp. | 3.05 | 0.14 | 38.63 | 1.16 | Financials | |||||||||||||

Alibaba Group Holding | 2.17 | 0.00 | 54.74 | 0.97 | Consumer Discretionary | |||||||||||||

Hilton Worldwide Hldgs. | 1.76 | 0.00 | 55.47 | 0.88 | Consumer Discretionary | |||||||||||||

ServiceNow Inc. | 1.75 | 0.16 | 58.56 | 0.87 | Information Technology | |||||||||||||

TE Connectivity | 2.80 | 0.00 | 29.38 | 0.81 | Information Technology | |||||||||||||

Amazon.com Inc. | 3.30 | 2.53 | 23.03 | 0.76 | Consumer Discretionary | |||||||||||||

Alphabet Inc. C | 2.00 | 1.24 | 29.10 | 0.62 | Communication Services | |||||||||||||

United Technologies Corp. | 1.46 | 0.37 | 43.80 | 0.62 | Industrials | |||||||||||||

Portfolio contribution for a holding represents the product of the average portfolio weight and the total return earned by the holding during the period. Past performance is no guarantee of future results. Fund holdings and/or sector allocations are subject to change at any time and are not recommendations to buy or sell any security.

| Fund Summary | 9 | |||||

Table of Contents

| Top 10 Individual Detractors as of the Year Ended December 31, 2019 | ||||||||||||||||||

| Company Name | Fund Weight (%) | Benchmark Weight (%) | 12-Month Return (%) | Contribution to Return (%) | Economic Sector | |||||||||||||

Qurate Retail Inc. | 0.36 | 0.02 | -38.27 | -0.37 | Consumer Discretionary | |||||||||||||

US Silica Holdings Inc. | 0.46 | 0.00 | -42.04 | -0.35 | Energy | |||||||||||||

Mylan NV | 0.54 | 0.04 | -23.83 | -0.19 | Health Care | |||||||||||||

DXC Technology Co. | 0.35 | 0.05 | -30.41 | -0.18 | Information Technology | |||||||||||||

American Airlines Group Inc. | 0.68 | 0.04 | -12.00 | -0.12 | Industrials | |||||||||||||

Global Eagle Entertainment Inc. | 0.06 | 0.00 | -77.58 | -0.11 | Communication Services | |||||||||||||

C.H. Robinson Worldwide Inc | 1.32 | 0.04 | -4.71 | -0.09 | Industrials | |||||||||||||

ViacomCBS Inc. Class B | 0.73 | 0.05 | -2.34 | -0.03 | Communication Services | |||||||||||||

Henkel AG & Co. KGaA | 0.99 | 0.00 | -1.65 | -0.03 | Consumer Staples | |||||||||||||

Markel Corp. | 0.15 | 0.05 | -2.67 | -0.03 | Financials | |||||||||||||

Portfolio contribution for a holding represents the product of the average portfolio weight and the total return earned by the holding during the period. Past performance is no guarantee of future results. Fund holdings and/or sector allocations are subject to change at any time and are not recommendations to buy or sell any security.

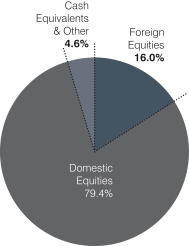

Portfolio Mix

The Equity Fund is the result of seven bottom-up stock pickers with diverse investment approaches building concentrated portfolios. Therefore, the portfolio often looks quite different from its benchmark. It is common for the fund to have meaningful sector over- and/or underweights. At year-end, the fund was more than seven percentage points overweight to the financials sector (20.7% vs. 13.5%), and underweight to the information technology sector by a similar amount (15.2% vs. 22.4%).

Over the year, the fund’s allocation to the financials sector decreased by about five percentage points. There were no other notable changes to sector weightings during the year. The fund’s cash position did increase over the year—going from 0.8% to 4.6% at year-end.

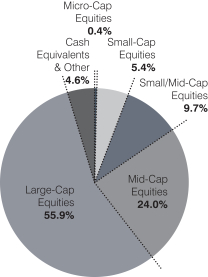

Over the course of the year, the fund’s market-cap exposure did not change materially, with mid- and smaller-cap companies accounting for about 40% of the portfolio (down from about three percentage points). Large-cap stocks make up roughly 56% of the portfolio, the same level it was at year-end 2018. (The balance of the decrease to mid- and smaller-cap names went to an increased cash position.) The fund’s weighted-average market cap stood at $185.6 billion at the year of 2019, while its median market was $38.8 billion. Foreign holdings account for approximately 16% of the portfolio, which is virtually unchanged from the prior year.

By Sector

| Sector Allocation | ||||||||||||

| Fund as of 12/31/19 | Fund as of 12/31/18 | Russell 3000 as of 12/31/19 | ||||||||||

Communication Services | 11.6% | 12.1% | 9.4% | |||||||||

Consumer Discretionary | 17.2% | 17.2% | 10.0% | |||||||||

Consumer Staples | 3.5% | 3.8% | 6.4% | |||||||||

Energy | 2.6% | 3.1% | 4.1% | |||||||||

Finance | 20.7% | 25.6% | 13.5% | |||||||||

Health Care & Pharmaceuticals | 9.9% | 7.3% | 14.2% | |||||||||

Industrials | 12.1% | 11.2% | 9.9% | |||||||||

Information Technology | 15.2% | 16.5% | 22.4% | |||||||||

Materials | 0.8% | 1.5% | 2.9% | |||||||||

Real Estate | 1.8% | 0.9% | 4.0% | |||||||||

Utilities | 0.0% | 0.0% | 3.2% | |||||||||

Cash Equivalents & Other | 4.6% | 0.8% | 0.0% | |||||||||

|

|

|

|

|

| |||||||

| 100.0% | 100.0% | 100.0% | ||||||||||

|

|

|

|

|

| |||||||

Fund holdings and/or sector allocations are subject to change at any time and are not recommendations to buy or sell any security.

| 10 | Litman Gregory Funds Trust | |||||

Table of Contents

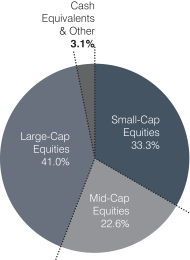

| By Market Capitalization | By Domicile | |

Market Capitalization: Micro-Cap < $981 million Small-Cap $981 million - $4.4 billion Small/Mid-Cap $4.4 billion - $10.6 billion Mid-Cap $10.6 billion - $29.4 billion Large-Cap > $29.4 billion Totals may not add up to 100% due to rounding |  | |

| Fund Summary | 11 | |||||

Table of Contents

Litman Gregory Masters Equity Fund Managers

| INVESTMENT MANAGER | FIRM | TARGET MANAGER ALLOCATION | MARKET CAPITALIZATION OF COMPANIES IN PORTFOLIO | STOCK-PICKING STYLE | BENCHMARK | |||||

| Christopher Davis Danton Goei | Davis Selected Advisers, L.P. | 15% | Mostly large companies | Blend | S&P 500 Index | |||||

| Pat English Jonathan Bloom | Fiduciary Management, Inc. | 15% | All sizes | Blend | S&P 500 Index | |||||

| Bill Nygren | Harris Associates L.P. | 15% | Mostly large- and mid-sized companies | Value | Russell 3000 Value Index | |||||

| Clyde McGregor | Harris Associates L.P. | 15% | All sizes, but mostly large- and mid-sized companies | Value | Russell 3000 Value Index | |||||

| Scott Moore | Nuance Investments, LLC | 10% | All sizes | Value | Russell 3000 Value Index | |||||

Frank Sands, Jr. A. Michael Sramek | Sands Capital Management, LLC | 17% | All sizes, but mostly large- and mid-sized companies | Growth | Russell 1000 Growth Index | |||||

| Richard Weiss | Wells Capital Management, Inc. | 13% | All sizes, but mostly small- and mid-sized companies | Blend | Russell 2000 Index |

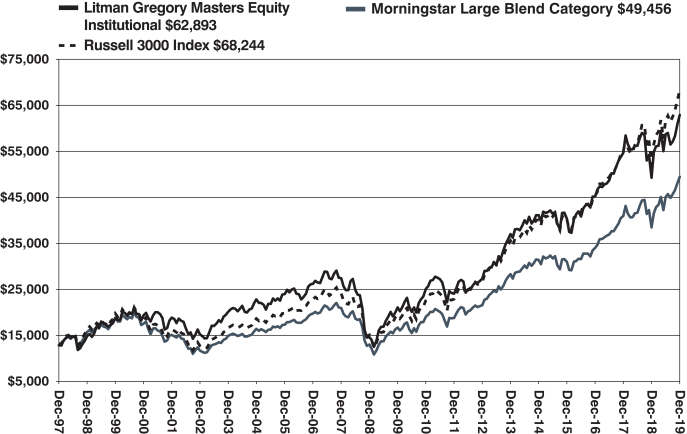

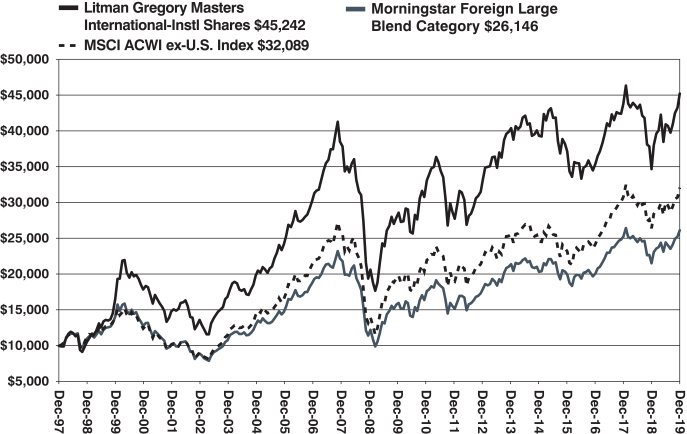

Equity Fund Value of Hypothetical $10,000

The value of a hypothetical $10,000 investment in the Litman Gregory Masters Equity Fund from December 31, 1996 to December 31, 2019 compared with the Russell 3000 Index and Morningstar Large Blend Category.

The hypothetical $10,000 investment at fund inception includes changes due to share price and reinvestment of dividends and capital gains. The chart does not imply future performance. Indexes are unmanaged, do not incur fees, expenses or taxes, and cannot be invested in directly.

| 12 | Litman Gregory Funds Trust | |||||

Table of Contents

Litman Gregory Masters Equity Fund

SCHEDULE OF INVESTMENTS IN SECURITIES at December 31, 2019

| Shares | Value | |||||||

| COMMON STOCKS: 94.7% | ||||||||

| Communication Services: 11.6% | ||||||||

| 7,560 | Alphabet, Inc. - Class A* | $ | 10,125,788 | |||||

| 3,736 | Alphabet, Inc. - Class C* | 4,995,107 | ||||||

| 5,500 | Charter Communications, Inc. - Class A* | 2,667,940 | ||||||

| 12,125 | Facebook, Inc. - Class A* | 2,488,656 | ||||||

| 139,849 | Global Eagle Entertainment, Inc.* | 69,925 | ||||||

| 10,200 | MultiChoice Group - ADR* | 83,130 | ||||||

| 19,275 | Netflix, Inc.* | 6,236,812 | ||||||

| 14,350 | Spotify Technology S.A.* | 2,146,043 | ||||||

| 45,725 | Tencent Holdings Ltd. | 2,205,015 | ||||||

| 53,250 | ViacomCBS, Inc. - Class B | 2,234,902 | ||||||

|

| |||||||

| 33,253,318 | ||||||||

|

| |||||||

| Consumer Discretionary: 17.2% | ||||||||

| 33,755 | Alibaba Group Holding Ltd. - ADR* | 7,159,435 | ||||||

| 4,660 | Amazon.com, Inc.* | 8,610,934 | ||||||

| 22,700 | Dollar General Corp. | 3,540,746 | ||||||

| 143,308 | Fiat Chrysler Automobiles N.V. | 2,105,195 | ||||||

| 119,700 | General Motors Co. | 4,381,020 | ||||||

| 48,005 | Hilton Worldwide Holdings, Inc. | 5,324,235 | ||||||

| 37,300 | Lear Corp. | 5,117,560 | ||||||

| 51,200 | Naspers Ltd. - Class N, ADR | 1,667,072 | ||||||

| 50,100 | Nordstrom, Inc. | 2,050,593 | ||||||

| 51,200 | Prosus N.V. - ADR* | 762,885 | ||||||

| 18,825 | Royal Caribbean Cruises Ltd. | 2,513,326 | ||||||

| 34,450 | Thor Industries, Inc. | 2,559,290 | ||||||

| 58,000 | TJX Cos., Inc. (The) | 3,541,480 | ||||||

|

| |||||||

| 49,333,771 | ||||||||

|

| |||||||

| Consumer Staples: 3.5% | ||||||||

| 25,945 | Cal-Maine Foods, Inc. | 1,109,149 | ||||||

| 60,000 | Conagra Brands, Inc. | 2,054,400 | ||||||

| 8,754 | Diageo Plc - ADR | 1,474,348 | ||||||

| 29,400 | Henkel AG & Co. KGaA | 2,772,495 | ||||||

| 30,300 | Monster Beverage Corp.* | 1,925,565 | ||||||

| 4,758 | Sanderson Farms, Inc. | 838,455 | ||||||

|

| |||||||

| 10,174,412 | ||||||||

|

| |||||||

| Energy: 2.6% | ||||||||

| 26,820 | Apache Corp. | 686,324 | ||||||

| 49,700 | Concho Resources, Inc. | 4,352,229 | ||||||

| 131,600 | Parsley Energy, Inc. - Class A | 2,488,556 | ||||||

|

| |||||||

| 7,527,109 | ||||||||

|

| |||||||

| Financials: 20.7% | ||||||||

| 89,200 | Ally Financial, Inc. | 2,725,952 | ||||||

| 45,500 | American International Group, Inc. | 2,335,515 | ||||||

| 77,000 | Bank of America Corp. | 2,711,940 | ||||||

| 49,475 | Bank of New York Mellon Corp. (The) | 2,490,077 | ||||||

| 19 | Berkshire Hathaway, Inc. - Class A* | 6,452,210 | ||||||

| 20,750 | Berkshire Hathaway, Inc. - Class B* | 4,699,875 | ||||||

| 25,000 | Blackstone Group, Inc. (The) - Class A | 1,398,500 | ||||||

| 83,460 | Capital One Financial Corp. | 8,588,868 | ||||||

| 7,338 | Chubb Ltd. | 1,142,233 | ||||||

| 36,300 | Citigroup, Inc. | 2,900,007 | ||||||

| 8,100 | Fairfax Financial Holdings Ltd. | 3,799,791 | ||||||

| 46,800 | HDFC Bank Ltd. - ADR | 2,965,716 | ||||||

| 15,030 | JPMorgan Chase & Co. | 2,095,182 | ||||||

| 19,450 | MetLife, Inc. | 991,366 | ||||||

| 36,250 | Pinnacle Financial Partners, Inc. | 2,320,000 | ||||||

| Shares | Value | |||||||

| Financials (continued) | ||||||||

| 8,513 | Reinsurance Group of America, Inc. | $ | 1,388,130 | |||||

| 16,688 | Travelers Cos., Inc. (The) | 2,285,422 | ||||||

| 48,640 | US Bancorp | 2,883,866 | ||||||

| 93,280 | Wells Fargo & Co. | 5,018,464 | ||||||

|

| |||||||

| 59,193,114 | ||||||||

|

| |||||||

| Health Care: 9.9% | ||||||||

| 20,500 | Alexion Pharmaceuticals, Inc.* | 2,217,075 | ||||||

| 30,000 | Cerner Corp. | 2,201,700 | ||||||

| 10,750 | Edwards Lifesciences Corp.* | 2,507,867 | ||||||

| 40,791 | Envista Holdings Corp.* | 1,209,045 | ||||||

| 6,782 | ICU Medical, Inc.* | 1,269,048 | ||||||

| 7,425 | Illumina, Inc.* | 2,463,170 | ||||||

| 10,970 | Johnson & Johnson | 1,600,194 | ||||||

| 31,823 | Merit Medical Systems, Inc.* | 993,514 | ||||||

| 101,200 | Mylan N.V.* | 2,034,120 | ||||||

| 29,000 | Quest Diagnostics, Inc. | 3,096,910 | ||||||

| 7,850 | Regeneron Pharmaceuticals, Inc.* | 2,947,518 | ||||||

| 37,636 | Smith & Nephew Plc - ADR | 1,809,163 | ||||||

| 13,200 | UnitedHealth Group, Inc. | 3,880,536 | ||||||

|

| |||||||

| 28,229,860 | ||||||||

|

| |||||||

| Industrials: 12.1% | ||||||||

| 11,214 | 3M Co. | 1,978,374 | ||||||

| 65,000 | American Airlines Group, Inc. | 1,864,200 | ||||||

| 68,400 | Arconic, Inc. | 2,104,668 | ||||||

| 21,100 | Carlisle Cos., Inc. | 3,414,824 | ||||||

| 42,955 | CH Robinson Worldwide, Inc. | 3,359,081 | ||||||

| 48,000 | Ferguson Plc | 4,362,849 | ||||||

| 208,000 | General Electric Co. | 2,321,280 | ||||||

| 17,400 | Honeywell International, Inc. | 3,079,800 | ||||||

| 31,500 | Knight-Swift Transportation Holdings, Inc. | 1,128,960 | ||||||

| 10,223 | Lindsay Corp. | 981,305 | ||||||

| 23,400 | ManpowerGroup, Inc. | 2,272,140 | ||||||

| 72,000 | Southwest Airlines Co. | 3,886,560 | ||||||

| 26,480 | United Technologies Corp. | 3,965,645 | ||||||

|

| |||||||

| 34,719,686 | ||||||||

|

| |||||||

| Information Technology: 14.5% | ||||||||

| 12,300 | Accenture Plc - Class A | 2,590,011 | ||||||

| 15,300 | Atlassian Corp. Plc - Class A* | 1,841,202 | ||||||

| 33,500 | Marvell Technology Group Ltd. | 889,760 | ||||||

| 67,100 | NCR Corp.* | 2,359,236 | ||||||

| 8,100 | Palo Alto Networks, Inc.* | 1,873,125 | ||||||

| 18,900 | salesforce.com, Inc.* | 3,073,896 | ||||||

| 18,475 | ServiceNow, Inc.* | 5,215,862 | ||||||

| 87,100 | TE Connectivity Ltd. | 8,347,664 | ||||||

| 55,000 | Visa, Inc. - Class A | 10,334,500 | ||||||

| 16,025 | Workday, Inc. - Class A* | 2,635,311 | ||||||

| 29,400 | Zendesk, Inc.* | 2,252,922 | ||||||

|

| |||||||

| 41,413,489 | ||||||||

|

| |||||||

| Materials: 0.8% | ||||||||

| 35,400 | Agnico Eagle Mines Ltd. | 2,180,994 | ||||||

|

| |||||||

| Real Estate: 1.8% | ||||||||

| 51,900 | CBRE Group, Inc. - Class A* | 3,180,951 | ||||||

| 57,496 | Equity Commonwealth | 1,887,594 | ||||||

|

| |||||||

| 5,068,545 | ||||||||

|

| |||||||

| | TOTAL COMMON STOCKS | 271,094,298 | ||||||

|

| |||||||

The accompanying notes are an integral part of these financial statements.

| Schedule of Investments | 13 | |||||

Table of Contents

Litman Gregory Masters Equity Fund

SCHEDULE OF INVESTMENTS IN SECURITIES at December 31, 2019 (Continued)

| Shares | Value | |||||||

| PREFERRED STOCK: 0.7% | ||||||||

| Information Technology: 0.7% | ||||||||

| 55,000 | Samsung Electronics Co. Ltd. - (Preference Shares) | $ | 2,159,194 | |||||

|

| |||||||

| | TOTAL PREFERRED STOCK | 2,159,194 | ||||||

|

| |||||||

| Principal Amount | ||||||||

| SHORT-TERM INVESTMENTS: 4.4% | ||||||||

| REPURCHASE AGREEMENTS : 4.4% | ||||||||

| $12,612,000 | Fixed Income Clearing Corp. 0.120%, 12/31/2019, due 01/02/2020 [collateral: par value $12,865,000, U.S. Treasury Note, 1.625%, due 12/31/2021, value $12,882,227] (proceeds $12,612,084) | 12,612,000 | ||||||

|

| |||||||

| | TOTAL SHORT-TERM INVESTMENTS | 12,612,000 | ||||||

|

| |||||||

| | TOTAL INVESTMENTS | 285,865,492 | ||||||

|

| |||||||

| Other Assets in Excess of Liabilities: 0.2% | 433,280 | |||||||

|

| |||||||

| NET ASSETS: 100.0% | $ | 286,298,772 | ||||||

|

| |||||||

Percentages are stated as a percent of net assets.

| ADR | American Depositary Receipt |

| * | Non-Income Producing Security. |

The accompanying notes are an integral part of these financial statements.

| 14 | Litman Gregory Funds Trust | |||||

Table of Contents

Litman Gregory Masters International Fund Review

The Litman Gregory Masters International Fund generated a strong 30.45% return in 2019, well ahead of its benchmarks, the MSCI ACWI ex. USA Index and the MSCI EAFE Index, which rose 21.51% and 22.01%, respectively. The fund also beat its average peer (up 21.40%) in the Morningstar Foreign Large Blend Category. The fund’s strong performance was driven in part by the easing of trade tensions. As a result, many cyclical and China-related holdings in the fund that had sold off materially in the second half of 2018 performed well in 2019.

Performance as of 12/31/2019 |

| |||||||||||||||||||||||||||

| Average Annual Total Returns | ||||||||||||||||||||||||||||

| Three Month Return | One- Year | Three- Year | Five- Year | Ten- Year | Fifteen- Year | Since Inception | ||||||||||||||||||||||

Litman Gregory Masters International Fund Institutional Class (12/1/1997) | 10.68% | 30.45% | 8.50% | 2.85% | 4.70% | 5.42% | 7.08% | |||||||||||||||||||||

MSCI ACWI (ex- U.S.) Index | 8.92% | 21.51% | 9.87% | 5.51% | 4.97% | 5.25% | 5.38% | |||||||||||||||||||||

MSCI EAFE Index | 8.17% | 22.01% | 9.56% | 5.67% | 5.50% | 4.84% | 5.02% | |||||||||||||||||||||

Morningstar Foreign Large Blend Category Average | 8.36% | 21.40% | 9.15% | 5.18% | 5.07% | 4.56% | 4.21% | |||||||||||||||||||||

| Performance quoted represents past performance and does not guarantee future results. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance of the funds may be lower or higher than the performance quoted. To obtain standardized performance of the funds, and performance as of the most recently completed calendar month, please visitwww.mastersfunds.com.As of the prospectus dated 4/30/2019, the gross and net expense ratios were1.33% and1.09%, respectively. There are contractual fee waivers in effect through April 30, 2021. |

| |||||||||||||||||||||||||||

MSCI index returns source: MSCI. Neither MSCI nor any other party involved in or related to compiling, computing, or creating the MSCI data makes any express or implied warranties or representations with respect to such data (or the results to be obtained by the use thereof), and all such parties hereby expressly disclaim all warranties of originality, accuracy, completeness, merchantability, or fitness for a particular purpose with respect to any of such data. Without limiting any of the foregoing, in no event shall MSCI, any of its affiliates, or any third party involved in or related to compiling, computing, or creating the data have any liability for any direct, indirect, special, punitive, consequential, or any other damages (including lost profits) even if notified of the possibility of such damages.Nofurther distribution or dissemination of the MSCI data is permitted without MSCI’s express written consent.Source note: Returns prior to 1999 are the MSCI ACWIex-US GR index. Returns from 1999 onwards are MSCI ACWIex-US NR index.

The fund’s long-term performance remains strong. Since inception, the fund has gained 7.08% and is ahead of the MSCI ACWI ex. USA Index return of 5.38%, the MSCI EAFE Index return of 5.02%, and the Morningstar Foreign Large Blend Category return of 4.21%. This long-term record, in our opinion, is a validation of the Masters Funds concept and our belief that concentration in the right hands can add significant value.

Performance of Managers

In 2019, all fivesub-advisors on the fund outperformed their respective benchmarks. The calendar-year performance of these fivesub-advisors ranged from 24.23% to 42.68% (returns are net of the management fee eachsub-advisor charges the fund). Four of the five managers are ahead of their benchmarks since they became a subadvisor on Litman Gregory Masters International. The fifth subadvisor has been with the fund for less than four years and is behind its primary benchmark by about 75 basis points (bps).

Key Performance Drivers

Below we discuss some of the key drivers of both absolute and relative performance. It is important to understand that the portfolio’s sector and country weightings are a residual of thebottom-up, fundamental stock-picking process employed by eachsub-advisor. That said, we do report on the relative performance contributions from stock selection, as well as sector and region weightings, to help shareholders better understand drivers of performance.

Stock selection was the primary driver of outperformance in 2019, while sector allocation, a residual of subadvsiors’bottom-up stock picking, was a slight headwind to relative performance. Stock picking within communication services, energy, and financial sectors were key areas of outperformance for the year. Regionally, stock selection was particularly strong in the UK and the eurozone.

| Fund Summary | 15 | |||||

Table of Contents

| Top 10 Individual Contributors as of the Year Ended December 31, 2019 | ||||||||||||||||||||

| Company Name | Fund Weight (%) | Benchmark Weight (%) | 12-Month Return (%) | Contribution to Return (%) | Country | Economic Sector | ||||||||||||||

Frontline Ltd. | 2.40 | 0.00 | 134.57 | 2.63 | Bermuda | Energy | ||||||||||||||

Informa PLC | 4.48 | 0.07 | 45.43 | 1.96 | United Kingdom | Communication Services | ||||||||||||||

ASML Holding NV ADR | 1.76 | 0.43 | 76.89 | 1.56 | Netherlands | Information Technology | ||||||||||||||

Teekay Lng Partners LP MLP | 3.46 | 0.00 | 48.46 | 1.39 | Bermuda | Energy | ||||||||||||||

Lloyds Banking Group PLC | 2.98 | 0.25 | 32.59 | 1.22 | United Kingdom | Financials | ||||||||||||||

Israel Discount Bank Ltd. Class A | 2.49 | 0.00 | 52.08 | 1.15 | Israel | Financials | ||||||||||||||

Vivendi SA | 5.27 | 0.14 | 21.45 | 1.12 | France | Communication Services | ||||||||||||||

JD.com Inc. ADR | 1.62 | 0.10 | 41.95 | 1.08 | China | Consumer Discretionary | ||||||||||||||

CNH Industrial NV | 3.43 | 0.06 | 24.75 | 1.05 | Netherlands | Industrials | ||||||||||||||

IWG PLC | 1.16 | 0.00 | 120.65 | 0.99 | Switzerland | Real Estate | ||||||||||||||

Portfolio contribution for a holding represents the product of the average portfolio weight and the total return earned by the holding during the period. Past performance is no guarantee of future results. Fund holdings and/or sector allocations are subject to change at any time and are not recommendations to buy or sell any security.

| Top 10 Individual Detractors as of the Year Ended December 31, 2019 | ||||||||||||||||||||

| Company Name | Fund (%) | Benchmark Weight (%) | 12-Month Return (%) | Contribution to Return (%) | Country | Economic Sector | ||||||||||||||

Trip.com Group Ltd. | 0.33 | 0.07 | -6.18 | -0.16 | China | Consumer Discretionary | ||||||||||||||

B2 Holding ASA | 0.19 | 0.00 | -43.50 | -0.14 | Norway | Financials | ||||||||||||||

Japan Tobacco Inc. | 1.02 | 0.13 | -5.27 | -0.14 | Japan | Consumer Staples | ||||||||||||||

Rolls-Royce Holdings PLC | 0.17 | 0.10 | -8.93 | -0.10 | United Kingdom | Industrials | ||||||||||||||

Borr Drilling Ltd. | 0.20 | 0.00 | -26.08 | -0.09 | Norway | Energy | ||||||||||||||

Incitec Pivot Ltd. | 1.12 | 0.00 | -3.41 | -0.08 | Australia | Materials | ||||||||||||||

Bombardier Inc. B | 0.22 | 0.02 | -17.84 | -0.05 | Canada | Industrials | ||||||||||||||

Nexon Co. ltd. | 1.25 | 0.03 | 3.60 | -0.04 | Japan | Communication Services | ||||||||||||||

Prosus NV Ordinary Shares Class N | 0.11 | 0.05 | -4.27 | -0.03 | Netherlands | Consumer Discretionary | ||||||||||||||

Codere SA | 1.04 | 0.00 | -21.44 | -0.01 | Spain | Consumer Discretionary | ||||||||||||||

Portfolio contribution for a holding represents the product of the average portfolio weight and the total return earned by the holding during the period. Past performance is no guarantee of future results. Fund holdings and/or sector allocations are subject to change at any time and are not recommendations to buy or sell any security.

Informa, owned by Lazard and Pictet, is a global information services group and academic publisher with a sizeable exhibitions business. Its niches in specific industry data, in market-leading journals, and in essential trade exhibitions, are highly defendable, according to Lazard’s Mark Little. He believes the stock has suffered from a historic perception of cyclicality in its exhibitions business as well as its over-levered status around the financial crisis.

Informa is slowly repairing this reputation through its consistent organic delivery, and by the successful execution of its merger with rival UBM. The company is gradually increasing the quality and defensiveness of its businesses and, as a result, Little says it has accelerated its organic growth from a lumpy1-2% to a steadier 3.5%.

Informa is the largest player in the exhibitions market, which benefits from structural growth and has attractive working capital characteristics and business visibility (on average 50% of customers book a year ahead). They have improved the quality of their conferences business and are increasingly focusing on more specialist areas as well as trying to layer in higher value-added analytics products.

In the more challenged publishing space, they operate in a more protected part of the market, and Little thinks the high-quality nature of their brands means this business will continue to grow low single-digits. He says its current valuation of around 14x earnings, with decent cash-flow conversion looks too low relative to its profitability, competitive moat, and steady growth profile. Little says Informa trades well below its industry peers with similar financial profiles, and well below the multiples seen in private transactions in exhibitions, an area where private equity interest is high. ln 2019, the stock was a strong performer on the back of solid results, but it was also among the stocks that rebounded from a very weak end to 2018, when Informa fell on overblown fears over its Chinese exhibition exposure.

| 16 | Litman Gregory Funds Trust | |||||

Table of Contents

Frontline, a stock owned by David Marcus of Evermore, is one of the largest owners and operators of modern crude tanker vessels with a market cap of $2.5 billion. Frontline has one of the youngest, modern fleets among its peers with an average age of 3.8 years. It is controlled by John Fredriksen (44% stake), a proven value creator in the shipping industry. Frontline’s stock was up 134.6% in 2019 due to several factors.

Throughout 2019, the incremental oil demand continued to be strong with the U.S. becoming atop-four global exporter with current exports amounting to over 3 million barrels per day. (In February 2019 the US became a net exporter after over 70 years.) With the U.S. becoming a net long crude exporter, crude tanker operators (especially Frontline) are the beneficiaries of longer ton miles as underscored by the increasing long-haul Atlantic basin exports. In addition, the new International Maritime Organisation (IMO) 2020 sulphur cap regulation (that went into effect in January 2020) will lead to longer trade routes, require additional crude runs and increase floating storage demand as refineries demand specific grades of fuel to refine into low-sulphur compliant fuel. This should also benefit Frontline.

Finally, scrapping of older vessels accelerated during the year, with the current run rate on track to reaching one of the highest levels in the last 20 years. The new IMO 2020 regulation has put increased pressure on older vessel operators, especially those with fleets older than 15 years old. (The regulations are aimed at curbing pollution caused by ships.) Marcus believes there will be additional scrapping of these older vessels, which will continue to reduce capacity further. In 2019, day/spot rates or pricing for shipping improved considerably from about $30,000 per day to $100,000. Marcus says the rise in spot rates reflects a fundamentally tighter tanker market driven by 1) widening spread between low and high sulphur fuels; 2) shortage of compliant fuels; 3) longer delays to retrofit scrubbers; and 4) order book at the lowest since 1996 with a growing scrapping pool of older tonnage. In summary, the recent movement in tankers rates provide affirmation on the tight supply and growing underlying freight demand.

While Frontline’s share price has performed well in 2019, Marcus sees significant additional upside from current levels. While the spot rates have improved, current asset values do not commensurately capture the improvement in underlying rates. Marcus believes the market has yet to fully appreciate the cash-flow generation potential that tanker companies offer. This is especially true in the case of Frontline, which has one of the lowestall-in cash breakeven levels among its peers (around $20,000), implying strong cash-flow generation at current spot rates.

Moscow Exchange, a Pictet stock, is the leading securities exchange in Russia. The company possesses all the attractive characteristics Pictet likes to see in its purchases: high recurrent revenues, a limited capital requirement, and high margins that lead to a high rate of cash conversion, attractive returns on capital, and substantial cash distributions to shareholders.

Moscow Exchange differs from its European peers in several compelling ways: (1) its market is relatively immature, which creates the opportunity for significant growth through the expansion of its product range; (2) it has a vertically integrated business model—trading and post-trade services—that both generates higher and steadier revenues raising the barrier to new entrants; (3) its customer base is highly diversified; and (4) it holds a near monopoly on trading in virtually all asset classes in Russia. Another characteristic of Moscow Exchange profitability has been a relatively high component of interest income on the customer cash (margin) balances. The stock was purchased in the third quarter of 2018 when sentiment towards Russian stocks was poor, resulting in part due to US sanctions on Russia.

Through 2019, growth in fee and commission income progressed at a healthy level. Pictet continues to believe that the low level of maturity of Russian capital markets should ensure the continuation of this upward trajectory. At the same time, and despite the reduction in local currency rates, net interest income (NII) revenue for the company has stabilized. This is largely due to a growth in client base (i.e. higher balances earning interest in all currencies) and is a development that shifts the balance of NII risk to the upside should hard currency rates begin to rise back to more ‘normal’ levels. One benefit of lower rates is that they are also reflected in Russia being accorded a lower risk premium. This latter effect helped drive Moscow Exchange’s (and the broad Russian market’s) strong performance in the second half of 2019. Moscow Exchange continues to trade at a significant discount to Pictet’s assessment of its intrinsic value.

Among the detractors, Trip.com, Chinese online travel agent and a Pictet holding, saw its stock price decline over 6% for the year in part due to US/China trade tensions and then Hong Kong political protests and civil unrest, which has meant that visitation to the region has almost dried up from mainland China, an effect Pictet estimates lowered Trip.com’s consolidated sales by close to 10%. However, despite revenues and RevPAR (revenues per available room) running on the light side versus Pictet’s expectations, the business has shown much higher than expected operating leverage, which is seen in a more positive progression in the bottom line.Pictet believes this is just the beginning of a profitability improvement for Trip.com that stems from an improved competitive environment and the company’s 60% market share—both generate significant network advantages in terms of number of listings and improving customer acquisition/stickiness.

From a valuation perspective the stock trades on amid-20s earnings multiple (and a lower free cash flow multiple given that the business operates with substantial negative working capital) and is achieving mid to high teens margins. Pictet estimates normalized operating margins (given a largely fixed cost structure) will be in themid-20s percentage and don’t believe this improvement in margins is factored in current valuations. As a result, Pictet has been adding to Trip.com in recent months during periods of weakness and remain holders.

| Fund Summary | 17 | |||||

Table of Contents

Another top detractor wasRolls Royce, held in David Herro’s sleeve. Its strong market position provides him visibility into earnings and free cash flow growth.Herro saysCEO Warren East’s overhaul of a weak management team, efforts to improve accountability and incentives to emphasize cash flow are all part of the restructuring that’s designed to increase efficiency and cost competitiveness.

Rolls Royce stock was down less than 10% in 2019, underperforming a strong market. Investors were disappointed with the company’s first-half earnings report that showed free cash flow was off to a sluggish start in 2019. In the third quarter, Rolls-Royce stated that full-year free cash flow and earnings would be at the low end of the previously issued guidance range, which weighed on its share price. Shortly after, the U.S. Navy awarded Rolls-Royce a $1.21 billion contract to provide maintenance, repair and other services for theV-22 AE1107C aircraft engine.