Table of Contents

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number: 811-07763

LITMAN GREGORY FUNDS TRUST

(Exact name of registrant as specified in charter)

2301 Rosecrans Avenue, Suite 2150

El Segundo, California

(Address of principal executive offices)(Zip code)

(Name and Address of Agent for Service)

Jeffrey K. Seeley

2301 Rosecrans Avenue, Suite 2150

El Segundo, California

Registrant’s telephone number, including area code: (925) 254-8999

Date of fiscal year end: December 31

Date of reporting period: December 31, 2023

Table of Contents

Item 1. Report to Shareholders.

(a) The following is a copy of the report transmitted to shareholders pursuant to Rule 30e-1 under the Investment Company Act of 1940, as amended (the “Act”):

Table of Contents

Annual Report

iMGP Global Select Fund

iMGP International Fund

iMGP Oldfield International Value Fund

iMGP SBH Focused Small Value Fund

iMGP Alternative Strategies Fund

iMGP High Income Fund

iMGP Dolan McEniry Corporate Bond Fund

iMGP DBi Managed Futures Strategy ETF

iMGP DBi Hedge Strategy ETF

iMGP RBA Responsible Global Allocation ETF

iMGP Berkshire Dividend Growth ETF

December 31, 2023

Table of Contents

| ii | Litman Gregory Funds Trust | |||||

Table of Contents

| 2 | ||

iMGP Global Select Fund | ||

| 4 | ||

| 7 | ||

iMGP International Fund | ||

| 9 | ||

| 13 | ||

iMGP Oldfield International Value Fund | ||

| 14 | ||

| 18 | ||

iMGP SBH Focused Small Value Fund | ||

| 19 | ||

| 22 | ||

iMGP Alternative Strategies Fund | ||

| 23 | ||

Alternative Strategies Fund Consolidated Schedule of Investments | 32 | |

iMGP High Income Fund | ||

| 71 | ||

| 75 | ||

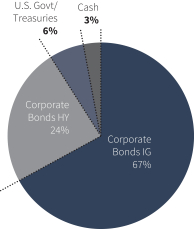

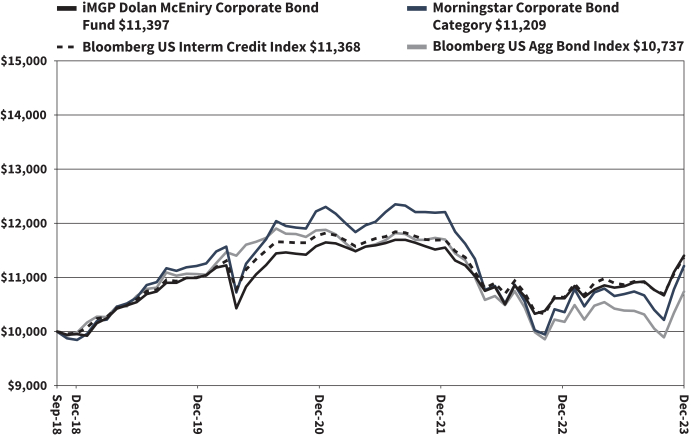

iMGP Dolan McEniry Corporate Bond Fund | ||

| 90 | ||

| 92 | ||

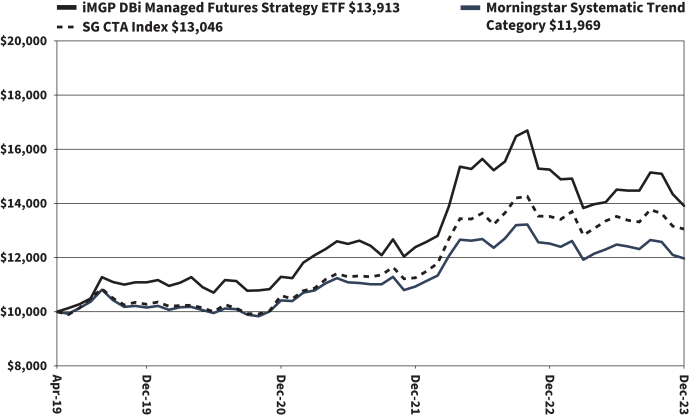

iMGP DBi Managed Futures Strategy ETF | ||

| 94 | ||

DBi Managed Futures Strategy ETF Consolidated Schedule of Investments | 96 | |

iMGP DBi Hedge Strategy ETF | ||

| 98 | ||

| 100 | ||

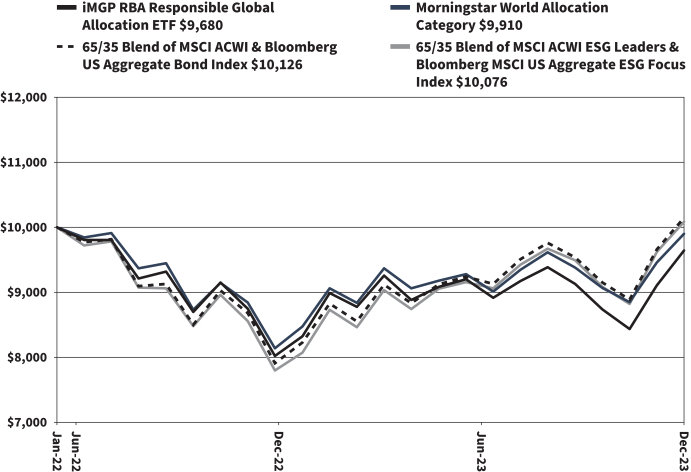

iMGP RBA Responsible Global Allocation ETF | ||

| 102 | ||

RBA Responsible Global Allocation ETF Schedule of Investments | 104 | |

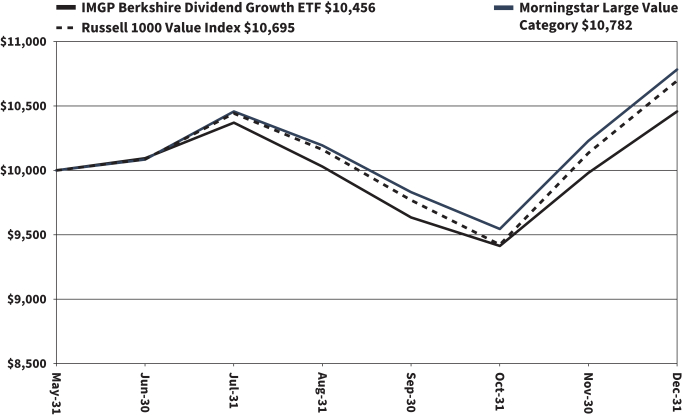

iMGP Berkshire Dividend Growth ETF | ||

| 105 | ||

| 108 | ||

| 109 | ||

| 111 | ||

| 115 | ||

| 118 | ||

| 118 | ||

| 119 | ||

| 119 | ||

| 120 | ||

| 120 | ||

| 121 | ||

| 122 | ||

| 122 | ||

| 123 | ||

| 123 | ||

Financial Highlights | ||

| 124 | ||

| 125 | ||

| 126 | ||

| 127 | ||

| 128 | ||

| 129 | ||

| 130 | ||

| 131 | ||

| 132 | ||

| 133 | ||

| 134 | ||

| 135 | ||

| 136 | ||

| 169 | ||

| 170 | ||

| 171 | ||

| 173 | ||

| 178 | ||

| 180 | ||

| 182 |

This report is intended for shareholders of the funds and may not be used as sales literature unless preceded or accompanied by a current prospectus for the iMGP Funds. Statements and other information in this report are dated and are subject to change.

iM Global Partner Fund Management, LLC has ultimate responsibility for the funds’ performance due to its responsibility to oversee its investment managers and recommend their hiring, termination and replacement.

| Table of Contents | 1 | |||||

Table of Contents

iM Global Partner Fund Management

Commitment to Shareholders

We are deeply committed to making each iMGP Fund a highly satisfying long-term investment for shareholders. In following through on this commitment we are guided by our core values, which influence four specific areas of service:

First, we are committed to the IMGP concept.

| • | We will only hire managers who we strongly believe will deliver exceptional long-term returns relative to their benchmarks. We base this belief on extremely thorough due diligence research. This not only requires us to assess their stock-picking skills, but also to evaluate their ability to add incremental performance by investing in a concentrated portfolio of their highest conviction ideas. |

| • | We will monitor each of the managers so that we can maintain our confidence in their ability to deliver the long-term performance we expect. In addition, our monitoring will seek to assess whether they are staying true to their IMGP Funds mandate. Consistent with this mandate, we focus on long-term performance evaluation so that the IMGP managers will not be distracted by short-term performance pressure. |

Second, we will do all we can to ensure that the framework within which our stock pickers do their work further increases the odds of success.

| • | Investments from new shareholders in each fund are expected to be limited so that each fund’s asset base remains small enough to retain flexibility to add value. |

| • | The framework also includes either a single-manager or a multi-manager structure; the former allowing each fund an individual, highly disciplined investment process, and the latter making it possible for each manager to invest, when appropriate, in an opportunistic manner knowing that the potential volatility within his or her portfolio will be diluted at the fund level by the performance of the other managers. In this way, the multi-manager structure seeks to provide fund-level diversification. |

| • | We will work hard to discourage short-term speculators so that cash flows into the funds are not volatile. Lower volatility helps prevent our managers from being forced to sell stocks at inopportune times or to hold excessive cash for non-investment purposes. |

Third, is our commitment to do all we can from an operational standpoint to maximize shareholder returns.

| • | We will remain attentive to fund overhead, and whenever we achieve savings we will pass them through to shareholders. For example, we have had several manager changes that resulted in lower sub-advisory fees to our funds. In every case we have passed through the full savings to shareholders in the form of fee waivers. |

| • | We will provide investors with a low minimum, no-load, no 12b-1 Institutional share class for all iMGP Funds, and a low minimum, no-load Investor share class for the Alternative Strategies Fund. |

| • | We also will work closely with our managers to make sure they are aware of tax-loss selling opportunities (only to be taken if there are equally attractive stocks to swap into). We account for partial sales on a specific tax lot basis so that shareholders will benefit from the most favorable tax treatment. The goal is not to favor taxable shareholders over tax-exempt shareholders but to make sure that the managers are taking advantage of tax savings opportunities when doing so is not expected to reduce pre-tax returns. |

Fourth, is our commitment to communicate honestly about all relevant developments and expectations.

| • | We will continue to do this by providing thorough and educational shareholder reports. |

| • | We will continue to provide what we believe are realistic assessments of the investment environment. |

Our commitment to iMGP Funds is also evidenced by our own investment. Our retired founders and current employees have, collectively, substantial investments in the funds, as does our company retirement plan. In addition, we use the funds extensively in the client accounts of our investment advisor practice (through our affiliate Litman Gregory Wealth Management, LLC). We have no financial incentive to do so because the fees we receive from iMGP Funds held in client accounts are fully offset against the advisory fees paid by our clients. In fact, we have a disincentive to use the funds in our client accounts because each iMGP Fund is capacity constrained (they may be closed as mentioned above), and by using them in client accounts we are using up capacity for which we may not be paid. But we believe these funds offer value that we can’t get elsewhere and this is why we enthusiastically invest in them ourselves and on behalf of clients.

While we believe highly in the ability of the Funds’ sub-advisors, our commitments are not intended as guarantees of future results.

While the funds are no-load, there are management fees and operating expenses that do apply, as well as a 12b-1 fee that applies to Investor class shares. Please refer to the prospectus for further details.

Diversification does not assure a profit or protect against loss in a declining market.

Must be preceded or accompanied by a prospectus.

| 2 | Litman Gregory Funds Trust | |||||

Table of Contents

General Disclosures

Past performance does not guarantee future results. Index performance is not illustrative of fund performance. An investment cannot be made directly in an index. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance of the fund may be lower or higher than the performance quoted. To obtain the performance of the funds as of the most recently completed calendar month, please visit www.imgpfunds.com. Investment performance reflects fee waivers in effect. In the absence of such waivers, total return would be reduced.

Diversification does not assure a profit or protect against loss in a declining market.

Must be preceded or accompanied by a prospectus

Multi-investment management styles may lead to higher transaction expenses compared to single investment management styles. Outcomes depend on the skill of the sub-advisors and advisor and the allocation of assets amongst them.

Some of the comments are based on current management expectation and are considered “forward-looking statements”. Actual future results, however, may prove to be different from our expectations. You can identify forward-looking statement by words such as “estimate”, “may”, “expect”, “should”, “could”, “believe”, “plan”, and similar terms. We cannot promise future returns and our opinions are a reflection of our best judgment at the time this report is compiled.

Opinions expressed are subject to change, are not guaranteed and should not be considered recommendations to buy or sell any security.

iM Global Partner Fund Management has ultimate responsibility for the performance of the funds due to its responsibility to oversee the sub-advisors and recommend their hiring, termination and replacement.

Each of the funds may invest in foreign securities. Investing in foreign securities exposes investors to economic, political, and market risks and fluctuations in foreign currencies. Each of the funds may invest in the securities of small companies. Small-company investing subjects investors to additional risks, including security price volatility and less liquidity than investing in larger companies. Debt obligations of distressed companies typically are unrated, lower rated, in default or close to default and may become worthless. The International Fund will invest in emerging markets. Investments in emerging market countries involve additional risks such as government dependence on a few industries or resources, government-imposed taxes on foreign investment or limits on the removal of capital from a country, unstable government, and volatile markets. Investments in debt securities typically decrease when interest rates rise. This risk is usually greater for longer-term debt securities. Investments in mortgage-backed securities include additional risks that investor should be aware of including credit risk, prepayment risk, possible illiquidity, and default, as well as increased susceptibility to adverse economic developments. Investments in lower-rated and non-rated securities present a greater risk of loss to principal and interest than higher-rated securities. The funds may invest in master limited partnership units. Investing in MLP units may expose investors to additional liability and tax risks. Derivatives may involve certain costs and risks such as liquidity, interest rate, market, credit, management, and the risk that a position could not be closed when most advantageous. Investing in derivatives could lose more than the amount invested. The funds may make short sales of securities, which involves the risk that losses may exceed the original amount invested.

A commission may apply when buying or selling an ETF.

© 2021 Morningstar, Inc. All Rights Reserved. The information contained herein: (1) is proprietary to Morningstar; (2) may not be copied or distributed; and (3) is not warranted to be accurate, complete or timely. Neither Morningstar nor its content providers are responsible for any damages or losses arising from any use of this information. Past performance is no guarantee of future results.

| Fund Summary | 3 | |||||

Table of Contents

iMGP Global Select Fund 2023 Annual Report (Unaudited)

The iMGP Global Select Fund rose 17.26% in 2023, trailing the 23.79% return for the MSCI World Index. The fund narrowly trailed the 17.77% return of the Morningstar Global Large-Stock Blend category over the trailing 12 months.

Performance as of 12/31/2023 |

| |||||||||||||||||||

One- Year | Three- Year | Five- Year | Ten- Year | Since Inception 12/31/1996 | ||||||||||||||||

iMGP Global Select Fund | 17.26% | 0.94% | 9.41% | 7.64% | 7.87% | |||||||||||||||

MSCI World NR USD | 23.79% | 7.27% | 12.80% | 8.60% | 6.99% | |||||||||||||||

MSCI ACWI NR USD | 22.20% | 5.75% | 11.72% | 7.93% | 6.82% | |||||||||||||||

Morningstar US Fund Global Large-Stock Blend | 17.77% | 4.47% | 10.19% | 6.98% | 7.40% | |||||||||||||||

| Gross Expense Ratio 1.50% Net Expense Ratio 1.01% Adjusted Expense Ratio exclusive of Interest and Dividend Expense 0.98%* |

| |||||||||||||||||||

Performance quoted represents past performance and does not guarantee future results. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance of the funds may be lower or higher than the performance quoted. To obtain standardized performance of the funds, and performance as of the most recently completed calendar month, please visit www.imgpfunds.com. The Advisor has contractually agreed to limit the expenses of the fund through April 30, 2025. Without this limit the fund’s net expenses would be higher and the return would be lower.

* The expense ratios disclosed in the performance table are based on the most recent prospectus and may not tie to what are disclosed in the financial highlights. |

| |||||||||||||||||||

Key Performance Drivers

The fund’s performance in 2023 was hurt by security selection, particularly within the technology sector. The fund’s dedicated exposure to small and mid-cap stocks also hurt relative returns. Broadly speaking, global small and mid-cap stocks (proxied by MSCI World SMID) underperformed their larger-cap counterparts in 2023. MSCI World SMID returned 15.62% compared to 23.79% year. While most of the discussion about the “Magnificent 7’s” (Alphabet, Amazon, Apple, Meta, Microsoft, Nvidia, Tesla), impact on returns relates to the S&P 500 Index, their impact is also felt within MSCI World. The Magnificent 7 make up nearly 19% of MSCI World and the fund is underweight to this basket of stocks. The impact of this large weight can be seen in the return of the MSCI World Equal Weighted Index, which returned 16.70% in 2023 or more than seven percentage points behind the market cap weighted MSCI World Index.

The fund’s selection within the technology sector was hurt mainly by a position in Keywords Studios. The stock was eventually sold during the third quarter for risk management reasons related to the threat of Artificial Intelligence. The company is a leader in the gaming development industry and facilitates outsourcing various functions to 24 of the top 25 gaming companies in the world. Artificial Intelligence is not new to gaming, but the adoption and experimentation are accelerating. The Polen Global SMID team modeled various scenarios, and the range of outcomes is unacceptably wide.

Security selection in the health care sector was a bright spot for the fund in 2023. ICON was the main contributor thanks to a greater than 45% return during the year. ICON is one of a handful of large, globally scaled players in the Clinical Research Organization (CRO) market and provides research and testing facilities to global pharmaceutical companies of all sizes. The stock saw a robust rebound in 2023 following a period of weakness driven by disruption from COVID, softer Biotech funding, and the escalation of the war in Ukraine. Fundamentals remain solid for ICON, the integration with PRA Health (previously a competitor) is progressing well, customer retention remains high and top-line growth is in line with long-term expectations of mid- to high single-digits. ICON continues to expect to reach $10 billion in sales by 2025, up from the $8bn it achieved over the last 12 months and $2.5bn it achieved in 2020. The combined company benefits from tremendous scale advantages and continues to win new business. After its rebound Polen Large Cap team trimmed their holding back to a mid-sized position. They continue to think the company maintains a strong competitive position, offers an attractive value proposition for pharmaceutical and biotech partners, and remain confident in the company’s ability to drive solid earnings growth in the coming years.

Goosehead Insurance helped drive strong security selection within the financials sector. Goosehead Insurance, a personal line property and casualty insurance brokerage primarily focused on home and auto markets, rose roughly 120% over the year. The company delivered consecutive quarters of robust results, continuing to execute its plan to clean up the corporate organization and return the company to its pre-COVID-19 productivity metrics. In its latest quarterly results total revenue increased 23% year on year, core revenue grew 22%, and premiums, the leading indicator of future revenue growth, increased 30%. Margins also showed healthy expansion. Broker upgrades and inclusion in the S&P Small Cap Index through the year further boosted the stock.

Industrials security selection hurt relative returns in 2023. 3M Company is a diversified industrial conglomerate with leading market share positions across a variety of businesses including industrial materials and adhesives, healthcare consumables, safety equipment, and consumer products. The company has historically enjoyed stable market share positions across its portfolio and its businesses benefit from structural demand drivers including the shift from traditional fasteners to adhesives, aging populations, and rising safety standards globally. These characteristics have contributed to the company exhibiting high and stable returns on capital over time.

| 4 | Litman Gregory Funds Trust | |||||

Table of Contents

Nuance’s view of 3M’s normalized earnings power is near $10.00 per share, and believes the company is currently under-earning relative to Wall Street consensus estimates for 2024. The first source of under-earning, in Nuance’s opinion, is related to cyclical weakness in 3M’s consumer-facing businesses. Discretionary consumer spending has weakened as inflation has impacted consumer budgets and consumers have worked down pandemic-related savings. According to their research, this has led to a cyclical decline in discretionary consumer electronics purchases including smartphones, TVs, tablets, and their related semiconductor content. These are all categories that utilize MMM’s products. On top of this headwind to sales driven by the end consumer, general inventory destocking by retailers has compounded this decrease in sales, in Nuance’s opinion.

The second source of under-earning is related to cost inflation for 3M’s key inputs including resins, petrochemicals, wood pulp, labor, and transportation. Nuance’s estimate that 3M’s EBITDAR margins are currently more than 200 basis points below levels they would consider normal. They believe additional pricing actions and/or moderating input cost inflation should result in margin normalization over the next few years.

Additionally, 3M is currently facing two legal battles which Nuance believes have led to negative sentiment and helped create a compelling valuation opportunity in the stock. The Investment Team has thoroughly studied both situations, has examined past analogous corporate litigation, and has stress tested 3M’s earnings power and balance sheet for a variety of scenarios. Importantly, they do not expect these legal issues to impact the competitive position of 3M’s broad line of businesses and have incorporated their own expected litigation and settlement costs into our balance sheet and normalized earnings estimates. It is Nuance’s belief that the company’s strong balance sheet and its normalized annual free cash flow in excess of $5.5 billion should provide an ample cushion from which to service any costs related to these matters. To emphasize, these issues and their own internal estimate of their long-term impact to the company are included in Nuance’s view of normalized earnings, cash flows, and balance sheet strength. In legal matters, there is always uncertainty, but based on their study of these issues, it appears to be a situation where the uncertainty is providing a solid risk reward opportunity. Nuance added to our position throughout 2023.

Revolve Group was a cause for negative security selection with the consumer discretionary sector. Revolve Group, a next-generation online retailer, sold off after posting a set of disappointing results against tough comparisons. The company had gone through a period of strength in 2022, boosted by “reopening” demand, with 2022 sales almost double that of 2020. 2023 has seen growth slow and turn negative, with operating margins also down. The share price is trading at lower levels than pre-pandemic despite being a much stronger business, having almost doubled revenues and grown annualized earnings at approximately 20%. This reflects a stark shift in sentiment. Revolve remains a high-quality company run by one of the better management teams, in the view of the Polen Small Cap team, but given their huge opportunity set and an appreciation for the wider range of outcomes, they sold out of the position in the fourth quarter.

Akzo Nobel posted a strong 26.9% return in 2023 and contributed to solid security selection in the materials sector. The company is a global manufacturer of paints and coatings with leading market share positions for paint in Europe, Asia, and Latin America. The company is also a global leader in several functional coating categories such as industrial, coil, wood, aerospace, and marine coatings. Nuance’s research suggested that the company was currently underearning its long-term potential for two transitory reasons. First, Akzo Nobel has faced raw material cost inflation, particularly in resins (40% of raw materials costs), which had depressed margins below normal levels, in their opinion. Inflationary pressures abated over the past few quarters and as raw material prices declined further from still elevated levels, Nuance believed the company would continue to see margin improvement. Second, the company faced cyclically lower demand for its products due to rising interest rates and slower growth across its geographies. Depressed demand led to inventory destocking across the channel in Europe and slower growth in China caused overall volumes to decline mid-single digits over the past year, according to their research. Nuance believed that the company’s stable market share position and structurally stable demand for paints and coatings, would position it to benefit from a cyclical demand improvement across both these markets. In their opinion, both these factors caused Akzo Nobel to post below normal earnings per share (EPS) relative to their internal estimates of normal EPS, creating what Nuance believed was an attractive risk reward relative to other opportunities. As the stock appreciated during the year, they exited the position and moved into what they viewed were more attractive risk rewards elsewhere.

Portfolio Mix

The Global Select Fund is built stock by stock from the bottom-up and can at times look very different from its benchmark. We believe this is key to generating excess long-term returns.

Over the course of 2023 the portfolio mix changed in the following way:

| • | Exposure to the information technology sector decreased from 24.3% to 15.9%. Exposure to smaller cap names within the sector were decreased over the year. |

| • | The financial sector weighting increased with the addition of names such as Brookfield, Markel, Fiserv, Morningstar, Hartford Financial Services, and Globe Life. |

| • | The health care sector remains the fund’s largest overweight. |

| • | At the start of 2023, the fund’s largest overweight was industrial stocks. This is no longer the case as the fund now has roughly the same amount as the index. The fund added six new names within the sector. |

| Fund Summary | 5 | |||||

Table of Contents

| • | The fund has zero exposure to energy and materials stocks as of the end of 2023. |

| • | Exposure to US equities increased throughout 2023. The fund remains underweight relative to MSCI World, however, the fund’s 59.9% weight is closer to the 69.6% in the index. |

By Sector

| Fund | ||||

Finance | 18.6% | |||

Consumer Discretionary | 8.4% | |||

Information Technology | 15.9% | |||

Communication Services | 5.5% | |||

Health Care & Pharmaceuticals | 22.2% | |||

Industrials | 11.9% | |||

Consumer Staples | 8.1% | |||

Real Estate | 2.1% | |||

Utilities | 3.6% | |||

Energy | 0% | |||

Materials | 0% | |||

Cash | 3.7% | |||

|

| |||

| 100% | ||||

By Region

| Fund | ||||

Europe | 28.4% | |||

North America | 67.4% | |||

Asia ex-Japan | 2.5% | |||

Japan | 1.7% | |||

Latin America | 0.0% | |||

Africa | 0.0% | |||

Australia/New Zealand | 0.0% | |||

Middle East | 0.0% | |||

Other Countries | 0.0% | |||

|

| |||

* Cash is excluded from calculation. | 100% | |||

By Region

US Equities | 59.9% | |||

Developed International Equities | 37.6% | |||

Emerging Market Equities | 2.5% | |||

|

| |||

| 100% |

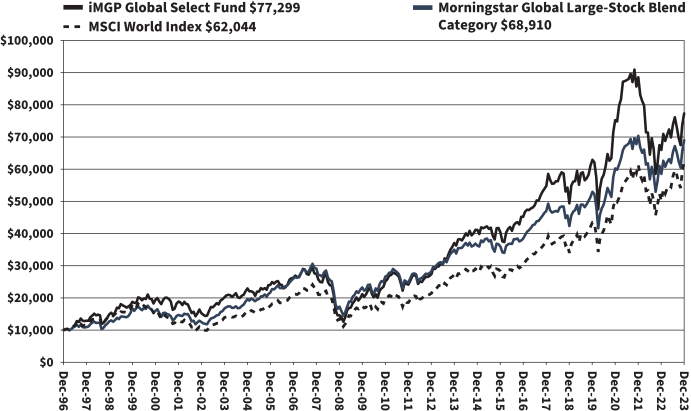

iMGP Global Select Fund Value of Hypothetical $10,000

The value of a hypothetical $10,000 investment in the iMGP Global Select Fund from December 31, 1996 to December 31, 2023 compared with the Morningstar Global Large-Stock Blend Category and MSCI World Index.

The hypothetical $10,000 investment at fund inception includes changes due to share price and reinvestment of dividends and capital gains. The chart does not imply future performance. Indexes are unmanaged, do not incur fees, expenses or taxes, and cannot be invested in directly.

Performance quoted does not include a deduction for taxes that a shareholder would pay on the redemption of fund shares.

| 6 | Litman Gregory Funds Trust | |||||

Table of Contents

iMGP Global Select Fund

SCHEDULE OF INVESTMENTS IN SECURITIES at December 31, 2023

| Shares | Value | |||||||

COMMON STOCKS: 93.9% | ||||||||

| Communication Services: 5.5% | ||||||||

| 15,889 | Alphabet, Inc. - Class A* | $ | 2,219,534 | |||||

| 58,200 | Comcast Corp. - Class A | 2,552,070 | ||||||

| 24,720 | CTS Eventim AG & Co. KGaA | 1,711,582 | ||||||

|

| |||||||

| 6,483,186 | ||||||||

|

| |||||||

| Consumer Discretionary: 8.4% | ||||||||

| 17,529 | Amazon.com, Inc.* | 2,663,356 | ||||||

| 75,300 | Compass Group PLC | 2,058,706 | ||||||

| 10,518 | Five Below, Inc.* | 2,242,017 | ||||||

| 8,625 | Floor & Decor Holdings, Inc. - Class A* | 962,205 | ||||||

| 1,155 | LVMH Moet Hennessy Louis Vuitton SE | 937,166 | ||||||

| 19,090 | YETI Holdings, Inc.* | 988,480 | ||||||

|

| |||||||

| 9,851,930 | ||||||||

|

| |||||||

| Consumer Staples: 8.1% | ||||||||

| 19,670 | Beiersdorf AG - ADR | 588,084 | ||||||

| 3,382 | Clorox Co. | 482,239 | ||||||

| 8,631 | Diageo PLC - ADR | 1,257,191 | ||||||

| 20,400 | Heineken NV | 2,040,000 | ||||||

| 116,875 | Henkel AG & Co. KGaA - ADR | 2,109,594 | ||||||

| 11,217 | Kimberly-Clark Corp. | 1,362,978 | ||||||

| 1,970 | L’Oreal SA | 981,930 | ||||||

| 11,013 | Pernod Ricard SA - ADR | 388,759 | ||||||

| 2,037 | Target Corp. | 290,109 | ||||||

|

| |||||||

| 9,500,884 | ||||||||

|

| |||||||

| Financials: 18.6% | ||||||||

| 3,982 | Aon PLC - Class A | 1,158,842 | ||||||

| 2 | Berkshire Hathaway, Inc. - Class A* | 1,085,250 | ||||||

| 3,209 | Berkshire Hathaway, Inc. - Class B* | 1,144,522 | ||||||

| 58,650 | Brookfield Corp. - Class A | 2,353,038 | ||||||

| 1,994 | Charles Schwab Corp. | 137,187 | ||||||

| 892 | Chubb Ltd. | 201,592 | ||||||

| 14,875 | Fiserv, Inc.* | 1,975,995 | ||||||

| 1,678 | Globe Life, Inc. | 204,246 | ||||||

| 15,350 | Goosehead Insurance, Inc. - Class A* | 1,163,530 | ||||||

| 2,645 | Hartford Financial Services Group, Inc. | 212,605 | ||||||

| 1,415 | Markel Group, Inc.* | 2,009,158 | ||||||

| 3,980 | Morningstar, Inc. | 1,139,235 | ||||||

| 16,171 | Northern Trust Corp. | 1,364,509 | ||||||

| 5,112 | Reinsurance Group of America, Inc. | 827,019 | ||||||

| 55,450 | TMX Group Ltd. | 1,345,884 | ||||||

| 6,624 | Travelers Cos., Inc. | 1,261,806 | ||||||

| 16,413 | Visa, Inc. - Class A | 4,273,125 | ||||||

|

| |||||||

| 21,857,543 | ||||||||

|

| |||||||

| Health Care: 22.2% | ||||||||

| 13,158 | Abbott Laboratories | 1,448,301 | ||||||

| 5,522 | Align Technology, Inc.* | 1,513,028 | ||||||

| 29,565 | Centene Corp.* | 2,194,019 | ||||||

| 26,400 | CVS Health Corp. | 2,084,544 | ||||||

| 38,394 | DENTSPLY SIRONA, Inc. | 1,366,442 | ||||||

| 25,210 | Eurofins Scientific SE | 1,644,571 | ||||||

| 10,465 | Henry Schein, Inc.* | 792,305 | ||||||

| 2,968 | Hologic, Inc.* | 212,064 | ||||||

| 4,504 | ICON PLC* | 1,274,947 | ||||||

| 4,748 | Illumina, Inc.* | 661,112 | ||||||

| 4,435 | McKesson Corp. | 2,053,316 | ||||||

| 20,235 | Novartis AG - ADR | 2,043,128 | ||||||

| Shares | Value | |||||||

| Health Care (continued) | ||||||||

| 38,030 | Progyny, Inc.* | $ | 1,413,955 | |||||

| 19,665 | Qiagen NV* | 854,051 | ||||||

| 3,631 | Quest Diagnostics, Inc. | 500,642 | ||||||

| 25,140 | Siemens Healthineers AG(a) | 1,462,601 | ||||||

| 76,168 | Smith & Nephew PLC - ADR | 2,077,863 | ||||||

| 3,070 | Tecan Group AG | 1,254,299 | ||||||

| 575 | Thermo Fisher Scientific, Inc. | 305,204 | ||||||

| 1,484 | Universal Health Services, Inc. - Class B | 226,221 | ||||||

| 2,166 | Waters Corp.* | 713,112 | ||||||

|

| |||||||

| 26,095,725 | ||||||||

|

| |||||||

| Industrials: 11.9% | ||||||||

| 19,207 | 3M Co. | 2,099,709 | ||||||

| 195,630 | Alight, Inc. - Class A* | 1,668,724 | ||||||

| 70,935 | Assa Abloy AB - Class B | 2,040,445 | ||||||

| 26,397 | Canadian Pacific Kansas City Ltd. | 2,086,947 | ||||||

| 21,794 | Core & Main, Inc. - Class A* | 880,696 | ||||||

| 13,230 | Daikin Industries Ltd. - ADR | 213,929 | ||||||

| 1,676 | Graco, Inc. | 145,410 | ||||||

| 81,363 | Knorr-Bremse AG - ADR | 1,323,125 | ||||||

| 36,272 | Legrand SA - ADR | 754,095 | ||||||

| 72,275 | MillerKnoll, Inc. | 1,928,297 | ||||||

| 3,960 | Paycom Software, Inc. | 818,611 | ||||||

|

| |||||||

| 13,959,988 | ||||||||

|

| |||||||

| Information Technology: 13.5% | ||||||||

| 2,637 | Accenture PLC - Class A | 925,350 | ||||||

| 3,888 | Adobe, Inc.* | 2,319,581 | ||||||

| 14,950 | Dynatrace, Inc.* | 817,616 | ||||||

| 13,345 | Kinaxis, Inc.* | 1,502,923 | ||||||

| 5,625 | Microsoft Corp. | 2,115,225 | ||||||

| 20,683 | Murata Manufacturing Co. Ltd. - ADR | 218,309 | ||||||

| 18,935 | Oracle Corp. | 1,996,317 | ||||||

| 11,620 | SAP SE | 1,792,639 | ||||||

| 6,100 | SHIFT, Inc.* | 1,550,704 | ||||||

| 2,600 | Tyler Technologies, Inc.* | 1,087,112 | ||||||

| 5,853 | Workday, Inc. - Class A* | 1,615,779 | ||||||

|

| |||||||

| 15,941,555 | ||||||||

|

| |||||||

| Real Estate: 2.1% | ||||||||

| 36,016 | Altus Group Ltd. | 1,149,392 | ||||||

| 56,881 | Healthcare Realty Trust, Inc. - REIT | 980,060 | ||||||

| 19,228 | Healthpeak Properties, Inc. - REIT | 380,714 | ||||||

|

| |||||||

| 2,510,166 | ||||||||

|

| |||||||

| Utilities: 3.6% | ||||||||

| 4,355 | American Water Works Co., Inc. | 574,816 | ||||||

| 7,066 | Essential Utilities, Inc. | 263,915 | ||||||

| 41,459 | Severn Trent PLC - ADR | 1,367,318 | ||||||

| 72,781 | United Utilities Group PLC - ADR | 1,997,839 | ||||||

|

| |||||||

| 4,203,888 | ||||||||

|

| |||||||

| | TOTAL COMMON STOCKS | 110,404,865 | ||||||

|

| |||||||

PREFERRED STOCK: 2.4% | ||||||||

| Information Technology: 2.4% | ||||||||

| 57,915 | Samsung Electronics Co. Ltd. -(Preference Shares) | 2,801,541 | ||||||

|

| |||||||

| | TOTAL PREFERRED STOCK | 2,801,541 | ||||||

|

| |||||||

The accompanying notes are an integral part of these financial statements.

| Schedule of Investments | 7 | |||||

Table of Contents

iMGP Global Select Fund

SCHEDULE OF INVESTMENTS IN SECURITIES at December 31, 2023 (Continued)

| Principal Amount | Value | |||||||

SHORT-TERM INVESTMENTS: 3.4% | ||||||||

REPURCHASE AGREEMENTS: 3.4% | ||||||||

| $4,034,971 | Fixed Income Clearing Corp. 1.600%, 12/29/2023, due 01/02/2024 [collateral: par value $4,484,000, U.S. Treasury Note, 0.625%, due 07/31/2026, value $4,116,243] (proceeds $4,035,688) | $ | 4,034,971 | |||||

|

| |||||||

| | TOTAL SHORT-TERM INVESTMENTS | 4,034,971 | ||||||

|

| |||||||

| | TOTAL INVESTMENTS | 117,241,377 | ||||||

|

| |||||||

| Other Assets in Excess of Liabilities: 0.3% | 361,991 | |||||||

|

| |||||||

NET ASSETS: 100.0% | $ | 117,603,368 | ||||||

|

| |||||||

Percentages are stated as a percent of net assets.

| ADR | American Depositary Receipt |

| REIT | Real Estate Investment Trust |

| * | Non-Income Producing Security. |

| (a) | Security was purchased pursuant to Rule 144A under the Securities Act of 1933 and may be sold in transactions exempt from registration only to qualified institutional buyers or in a public offering registered under Securities Act of 1933. |

The accompanying notes are an integral part of these financial statements.

| 8 | Litman Gregory Funds Trust | |||||

Table of Contents

iMGP International Fund 2023 Annual Report (Unaudited)

The iMGP International Fund rose 17.40% in 2023, trailing the 18.24% return for the MSCI EAFE Index. It outgained both the 15.62% of MSCI ACWI ex. US Index and 16.29% return of the Morningstar Foreign Large Blend category. Since the fund’s 1997 inception, the fund has an annualized return of 6.27%—comparing favorably to the 5.01% return for MSCI EAFE and 4.19% gain for the category.

Performance as of 12/31/2023 | ||||||||||||||||||||

| One- Year | Three- Year | Five- Year | Ten- Year | Since 12/1/1997 | ||||||||||||||||

iMGP International Fund | 17.40% | 0.95% | 7.11% | 1.92% | 6.27% | |||||||||||||||

MSCI ACWI ex US Index NET | 15.62% | 1.55% | 7.08% | 3.83% | 5.13% | |||||||||||||||

MSCI EAFE Index NET | 18.24% | 4.02% | 8.16% | 4.28% | 5.01% | |||||||||||||||

Morningstar Foreign Large Blend Category | 16.29% | 2.45% | 7.33% | 3.67% | 4.19% | |||||||||||||||

Gross Expense Ratio 1.47%, Net Expense Ratio 1.24%* | ||||||||||||||||||||

Performance quoted represents past performance and does not guarantee future results. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance of the funds may be lower or higher than the performance quoted. To obtain standardized performance of the funds, and performance as of the most recently completed calendar month, please visit www.imgptfunds.com. The Advisor has contractually agreed to waive a portion of the management fee through April 30, 2025. Without this waiver the fund’s net expenses would be higher and the return would be lower.

* The expense ratios disclosed in the performance table are based on the most recent prospectus and may not tie to what are disclosed in the financial highlights.

MSCI index returns source: MSCI. Neither MSCI nor any other party involved in or related to compiling, computing, or creating the MSCI data makes any express or implied warranties or representations with respect to such data (or the results to be obtained by the use thereof), and all such parties hereby expressly disclaim all warranties of originality, accuracy, completeness, merchantability, or fitness for a particular purpose with respect to any of such data. Without limiting any of the foregoing, in no event shall MSCI, any of its affiliates, or any third party involved in or related to compiling, computing, or creating the data have any liability for any direct, indirect, special, punitive, consequential, or any other damages (including lost profits) even if notified of the possibility of such damages. No further distribution or dissemination of the MSCI data is permitted without MSCI’s express written consent. Source note: Returns prior to 1999 are the MSCI ACWI ex-US GR index. Returns from 1999 onwards are MSCI ACWI ex-US NR index. |

| |||||||||||||||||||

Key Performance Drivers

Sector allocation was a benefit to returns in 2023, while security selection detracted from relative returns. The fund’s overweight to technology and consumer discretionary stocks benefited the fund, while its underweight to consumer staples stocks also aided returns. A modest overweight to health care stocks detracted from returns, however, stock security selection within the sector more than made up for the overweight allocation. Security selection within the technology sector was the largest benefit to fund returns. While security within the financials sector was a leading detractor during the year.

The largest contributor to performance in 2023 was Ryanair. The position is held by both David Herro of Harris Associates and the team at Lazard Asset Management. Ryanair stock gained over 78% during the year. Herro says that Ryanair released strong results for the first half of fiscal-year 2024 and was accompanied by an even stronger outlook, in our view. The company’s revenue grew 30% year-over-year, and average fares increased by 24% to €58, driven by record demand and constrained capacity at European peers. Total passengers flown expanded 11% year over year to 105.4 million, and management is on track to maintain its target of 183.5 million passengers for 2024, depending on Boeing’s ability to meet its delivery commitments. Management is expecting full-year 2024 net income to be between €1.85-2.05 billion ahead of the €1.82 billion consensus estimate. The company’s strong free cash flow levels and balance sheet allowed Ryanair to reinstate a €400 million dividend (35 cents per share). The team at Harris Associates spoke with CEO Michael O’Leary about additional uses for its excess capital and were happy to hear about an incremental €1.5 billion return to shareholders starting in 2025. They continue to be optimistic about Ryanair’s future.

Mark Little and Robin Jones (Lazard Asset Management) say that Ryanair continues to enjoy a favorable cost position in the short-haul aviation market compared to its competition. This advantage has expanded during COVID as the company has been able to invest through a downturn. The financial strength of the business enables them to operate a modern and more efficient fleet, which further enhances their competitive advantage. The company reported strong results over the course of the year. Demand for air travel continues to be robust with a positive outlook for pricing. Cash flow generation has been strong which helps fund attractive cash returns to shareholders and helps to underpin an undemanding valuation.

Ryanair’s strong return within the industrials sector was offset by another industrial stock: Teleperformance. The stock, owned by the team at Polen Capital, fell meaningfully in 2023. France-based Teleperformance is the world’s leading outsourced customer services manager. Teleperformance shares suffered in 2023 as sentiment surrounding AI adoption reached a crescendo and related market narratives assumed customer experience services will be fully automated. Polen Capital believes Teleperformance’s customers, and many other businesses will continue to require effective human customer experience management. Teleperformance continues to leverage technologies, including AI, to

| Fund Summary | 9 | |||||

Table of Contents

deliver successful business outcomes to customers. Management effectively navigated the impacts of transformational technologies at times over its 40 years in business and is proactively thinking through opportunities in the present environment. Teleperformance can weather today’s weak IT services market environment and rebound to the recent years’ steady growth trajectory. The Polen team estimates low double-digit total returns ahead. At 8x 2024 earnings, shares discount a darker future than we think is in store.

Strong security selection in the information technology sector was helped by a greater than 70% return for Sage Group. The position is held by the team at Polen Capital. Sage Group, a UK-based software company, continues to demonstrate strong business momentum with organic revenue growth in the low double-digit range. Management’s thoughtful product development and sales force alignment investments in recent years transitioned Sage Group’s software to a cloud-centric model. In its most recent quarterly update, management guided for continued low double-digit revenue growth for their fiscal 2024, a function of Sage’s strong value proposition providing mission critical accounting and business management software to small and medium-sized businesses. This level of growth, coupled with steady margin expansion, should in Polen’s estimation allow Sage to grow earnings at a mid-teens annualized rate going forward. Polen believes Sage Group’s margins have significant runway to expand from here, adding a nice profit lever to the coming years’ growth algorithm. In their view, a high-20s multiple on calendar 2024 earnings is a reasonable multiple as Sage Group is well positioned for steady growth.

The financials sector was a difficult area for the fund in 2023. By the far the biggest detractor within the sector was Worldline (owned by Harris Associates). Worldline, a European merchant acquirer and payment processor, was the top detractor for the year. The company’s third-quarter earnings missed consensus and Harris’ expectations, and management cut its full-year 2023 and 2024 guidance. The implied 2024 adjusted earnings guidance is around 16% below consensus expectations. This resulted in a 60% sell-off in the stock, an amount that Harris does not think is proportional to the impact to the company’s fair value. In their view, the negative guidance revision derives from two causes. First, due to evolving regulatory requirements around cybercrime in Europe, Worldline cut ties with certain online merchants that would have required excessive investment to be fully compliant with regulatory standards. Second, Worldline highlighted weak macroeconomic trends in Germany, where it is the market leader, and these are driving spending shifts toward non-discretionary categories that produce less revenue and profit from merchants for Worldline. Collectively, Worldline’s actions impact €210 million in annualized revenue (sub-6% consolidated revenues), reset margins down by 250 basis points, and will burden near-term cash generation due to restructuring charges. The negative impact should start to ease by the second half of 2024. The team at Harris Associates has spoken to management, former Worldline employees, and payment industry competitors. In their view, Worldline’s negative share price reaction is disproportional to the likely impact on its long-term prospects. The fundamentals of the business are still intact. The European payment market is cash heavy and still largely operated by legacy banks that are ceding share to pure acquirers like Worldline. The company’s scaled pan-European footprint, capital light and cash-generative operating profile, strong medium-term growth potential, and washed-out valuation make it an attractive holding.

Harris Associates appreciates Worldline’s position as a leader in European payments, and believe it has a long growth runway ahead due to Europe’s lower cashless penetration and higher levels of bank payment in-sourcing when compared to the U.S. They believe the payments industry is structurally attractive with high recurring revenues, low customer churn and strong free cash flow generation. In their view, Worldline’s revenue acceleration, which is driven by e-commerce business, travel recovery and synergy opportunities, is underappreciated by the market.

Another financial stock that struggled in 2023 was Sampo. The company, owned by the team at Lazard Asset Management, is a high-quality P&C insurance company operating across Scandinavia. The insurance markets in Scandinavia are highly consolidated, and policies are largely sold direct, which makes it a very price-disciplined market. Sampo generates very attractive and stable combined ratios as a result. The combination of a healthy economic backdrop and disciplined pricing generates good premium growth over time. Sampo has over time made investments outside their core business; however, new management have refocused capital allocation into the core P&C franchise and undergone a process to divest non-core assets.

The strong inflationary backdrop has put upward pressure on claims inflation in Sampo’s key markets at a time when frequency has also picked post COVID. This has put some pressure on combined ratios. However, the team at Lazard is encouraged to see strong price increases come through to compensate for higher claims at a time when inflationary pressures are moderating. This is a very common cycle in P&C insurance, and they are confident Sampo will rebuild their combined ratios to historical levels as pricing comes through at a lag. In addition to these cyclical headwinds, earnings have been hit by the deconsolidation of Sampo’s life insurance business as part of the simplification of the portfolio. Life insurance is a less attractive business given the long-duration book with higher sensitivity to financial asset values.

The fund’s main position within the materials sector is Glencore (owned by Harris Associates). The stock was a detractor last year. The company is one of the world’s largest mining firms. The Harris team likes that Glencore is run by smart, hyper-competitive and value-focused managers with a focus on improving asset returns. In their estimation, Glencore differentiates itself from other miners with its trading business that provides high returns and cash flow with low cyclicality and significant barriers to entry. They appreciate the company’s leading market positions in attractive commodities and believe existing mining operations will benefit from normalized prices, higher volumes, lower costs and the move towards a low carbon economy. Harris believes Glencore is an attractive investment and trades at approximately two-thirds of their estimate of its intrinsic value.

| 10 | Litman Gregory Funds Trust | |||||

Table of Contents

Glencore was a detractor for the year. The UK-based materials company’s stock price fell in January following its release of full-year 2022 results that missed expectations. In Harris’ view, the shortfall was driven by the industrial business given a mix of production issues within coal and two copper assets and cost inflation related to labor, diesel and explosives. During the second quarter, the market reacted unfavorably towards discussions of a merger between Glencore’s agricultural trader Viterra and Bunge, one of the world’s largest crop merchants, before seeing an increase in Glencore’s stock price once the companies entered into a definitive agreement. In August, Glencore released first-half of 2023 results that missed expectations which led Harris to modestly lower their estimate of intrinsic value. They believe the miss can be attributed to three main reasons: timing, costs and first-quarter results for nickel that were loss-making. Harris Associates believes Glencore’s management team makes smart capital allocation decisions and continue to think the company remains undervalued.

A solid contributor within the consumer staples sector was Coca-Cola Europacific Partners (owned by Lazard Asset Management). The strategic shift in the Coca-Cola system to focus on value over volume has been a transformational moment for their bottling partners. A more pricing-driven topline model has produced strong operational leverage for the bottlers resulting in improving margins and returns. As a strong operator, the company has also been in a position to consolidate new territories with opportunities to improve operational efficiency in established markets (e.g., Australia) and drive category growth in less developed markets (e.g., Indonesia).

The company delivered good results over the course of the year. The management team started the year with a confident outlook for full year 2023 despite concerns of weaker backdrop for the consumer. Fast-moving consumer goods companies have generally struggled with weaker volumes after a period of strong inflationary pressures. The resilient performance at Coca-Cola Europacific Partners reflects the strong pricing power in the category and good commercial execution by the management team.

Portfolio Mix

The International Fund is built stock by stock from the bottom-up and can at times look very different from its benchmark. We believe this is key to generating excess long-term returns.

Over the last 12 months, the overall portfolio mix changed modestly.

| • | The fund’s regional allocation did not meaningfully change over the course of the year. The fund remains significantly underweight to Japan with just two holdings at year-end. |

| • | The fund’s maintains an overweight to the technology sector. At the end of 2022, the fund had 13.6% in the sector. At year-end 2023, the exposure had increased modestly to 14.7%. The technology sector within the index is 8.6%. |

| • | Exposure to health care stocks jumped the most during the year (going from 12.8% to 19.1% at the end of 2023). New positions added during the year include Novo Nordisk and Gerresheimer. |

| • | The fund’s weight to communication services stocks decreased from 8.8% to 2.9% over the year. Liquidated positions in Universal Music Group and Informa drove most of the decrease within the sector. |

| Fund Summary | 11 | |||||

Table of Contents

By Sector

| 12/31/2023 | ||||

Finance | 19.0% | |||

Consumer Discretionary | 17.4% | |||

Information Technology | 14.7% | |||

Communication Services | 2.9% | |||

Health Care & Pharmaceuticals | 19.1% | |||

Industrials | 13.0% | |||

Consumer Staples | 5.4% | |||

Real Estate | 0.0% | |||

Utilities | 0.0% | |||

Energy | 0.0% | |||

Materials | 2.2% | |||

Cash | 6.3% | |||

|

| |||

| 100.0% | ||||

|

| |||

By Region

| 12/31/2023 | ||||

US Equities | 5.5% | |||

Developed International Equities | 91.2% | |||

Emerging Market Equities | 3.3% | |||

|

| |||

| 100.0% | ||||

|

| |||

| Cash not included. | ||||

By Region

| 12/31/2023 | ||||

Europe | 77.7% | |||

North America | 8.4% | |||

Asia ex-Japan | 5.3% | |||

Japan | 3.1% | |||

Latin America | 1.6% | |||

Africa | 0.0% | |||

Australia/New Zealand | 1.3% | |||

Middle East | 2.6% | |||

Other Countries | 0.0% | |||

|

| |||

Total | 100.0% | |||

|

| |||

| Cash not included. |

| |||

By Market Cap

| 12/31/2023 | ||||

Small Cap | 1.1% | |||

Mid Cap | 12.6% | |||

Large Cap | 86.3% | |||

|

| |||

| 100.0% | ||||

|

| |||

| Cash not included. | ||||

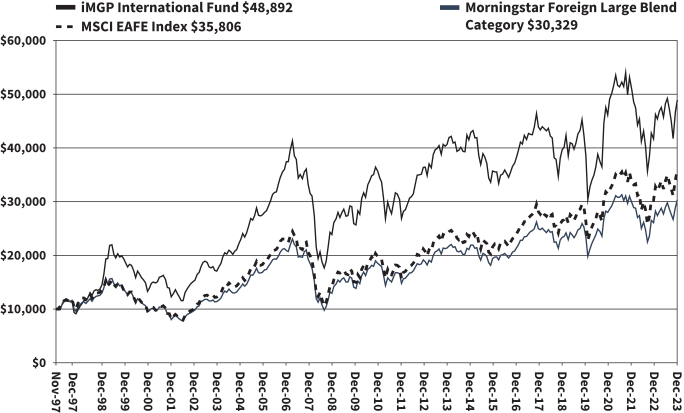

iMGP International Fund Value of Hypothetical $10,000

The value of a hypothetical $10,000 investment in the iMGP International Fund from November 30, 1997 to December 31, 2023 compared with the MSCI EAFE Index, and Morningstar Foreign Large Blend Category.

The hypothetical $10,000 investment at fund inception includes changes due to share price and reinvestment of dividends and capital gains. The chart does not imply future performance. Indexes are unmanaged, do not incur fees, expenses or taxes, and cannot be invested in directly.

Performance quoted does not include a deduction for taxes that a shareholder would pay on the redemption of fund shares.

| 12 | Litman Gregory Funds Trust | |||||

Table of Contents

iMGP International Fund

SCHEDULE OF INVESTMENTS IN SECURITIES at December 31, 2023

| Shares | Value | |||||||

COMMON STOCKS: 93.7% | ||||||||

| Argentina: 1.5% | ||||||||

| 2,143 | MercadoLibre, Inc.* | $ | 3,367,810 | |||||

|

| |||||||

| Australia: 1.2% | ||||||||

| 445,300 | Glencore PLC | 2,678,282 | ||||||

|

| |||||||

| Canada: 2.7% | ||||||||

| 39,678 | Canadian Pacific Kansas City Ltd. | 3,150,321 | ||||||

| 37,425 | Shopify, Inc. - Class A* | 2,915,408 | ||||||

|

| |||||||

| 6,065,729 | ||||||||

|

| |||||||

| China: 1.6% | ||||||||

| 117,601 | Prosus NV | 3,510,010 | ||||||

|

| |||||||

| Denmark: 3.6% | ||||||||

| 28,235 | Carlsberg AS - Class B | 3,547,652 | ||||||

| 43,876 | Novo Nordisk AS - Class B | 4,544,823 | ||||||

|

| |||||||

| 8,092,475 | ||||||||

|

| |||||||

| Finland: 2.6% | ||||||||

| 132,455 | Sampo OYJ - Class A | 5,802,940 | ||||||

|

| |||||||

| France: 8.7% | ||||||||

| 74,900 | BNP Paribas SA | 5,185,154 | ||||||

| 10,255 | Kering SA | 4,525,676 | ||||||

| 2,050 | LVMH Moet Hennessy Louis Vuitton SE | 1,663,367 | ||||||

| 21,710 | Teleperformance SE | 3,170,831 | ||||||

| 279,500 | Worldline SA*(a) | 4,844,240 | ||||||

|

| |||||||

| 19,389,268 | ||||||||

|

| |||||||

| Germany: 24.4% | ||||||||

| 13,255 | Adidas AG | 2,699,914 | ||||||

| 11,425 | Allianz SE | 3,057,432 | ||||||

| 143,900 | Bayer AG | 5,352,572 | ||||||

| 69,749 | Continental AG | 5,934,063 | ||||||

| 54,292 | CTS Eventim AG & Co. KGaA | 3,759,110 | ||||||

| 80,618 | Daimler Truck Holding AG | 3,033,481 | ||||||

| 121,665 | Fresenius SE & Co. KGaA | 3,777,313 | ||||||

| 31,527 | Gerresheimer AG | 3,290,027 | ||||||

| 132,689 | Hensoldt AG | 3,580,961 | ||||||

| 80,400 | Mercedes-Benz Group AG | 5,562,349 | ||||||

| 57,360 | SAP SE | 8,849,036 | ||||||

| 94,420 | Siemens Healthineers AG(a) | 5,493,190 | ||||||

|

| |||||||

| 54,389,448 | ||||||||

|

| |||||||

| Ireland: 10.7% | ||||||||

| 51,152 | ICON PLC - ADR* | 14,479,597 | ||||||

| 69,945 | Ryanair Holdings PLC - ADR* | 9,327,865 | ||||||

|

| |||||||

| 23,807,462 | ||||||||

|

| |||||||

| Israel: 2.4% | ||||||||

| 617,091 | Israel Discount Bank Ltd. - Class A | 3,104,580 | ||||||

| 440,085 | Tel Aviv Stock Exchange Ltd. | 2,355,960 | ||||||

|

| |||||||

| 5,460,540 | ||||||||

|

| |||||||

| Japan: 2.9% | ||||||||

| 83,600 | Nippon Sanso Holdings Corp. | 2,240,329 | ||||||

| 234,200 | Renesas Electronics Corp.* | 4,236,726 | ||||||

|

| |||||||

| 6,477,055 | ||||||||

|

| |||||||

| Netherlands: 2.4% | ||||||||

| 3,990 | ASML Holding NV | 3,008,438 | ||||||

| 23,488 | EXOR NV | 2,351,091 | ||||||

|

| |||||||

| 5,359,529 | ||||||||

|

| |||||||

| Shares | Value | |||||||

| South Korea: 1.3% | ||||||||

| 16,035 | NAVER Corp. | $ | 2,788,912 | |||||

|

| |||||||

| Spain: 2.4% | ||||||||

| 75,265 | Amadeus IT Group SA | 5,401,057 | ||||||

|

| |||||||

| Sweden: 2.7% | ||||||||

| 51,196 | Evolution AB(a) | 6,122,944 | ||||||

|

| |||||||

| Switzerland: 2.1% | ||||||||

| 82,400 | Julius Baer Group Ltd. | 4,622,439 | ||||||

|

| |||||||

| Taiwan: 2.2% | ||||||||

| 249,000 | Taiwan Semiconductor Manufacturing Co. Ltd. | 4,811,163 | ||||||

|

| |||||||

| United Kingdom: 13.1% | ||||||||

| 542,043 | CNH Industrial NV | 6,642,757 | ||||||

| 104,661 | Coca-Cola Europacific Partners PLC | 6,968,772 | ||||||

| 8,470,550 | Lloyds Banking Group PLC | 5,148,618 | ||||||

| 602,980 | Sage Group PLC | 9,007,108 | ||||||

| 31,153 | Unilever PLC | 1,508,180 | ||||||

|

| |||||||

| 29,275,435 | ||||||||

|

| |||||||

| United States: 5.2% | ||||||||

| 19,932 | Aon PLC - Class A | 5,800,611 | ||||||

| 69,219 | Medtronic PLC | 5,702,261 | ||||||

|

| |||||||

| 11,502,872 | ||||||||

|

| |||||||

| | TOTAL COMMON STOCKS | 208,925,370 | ||||||

|

| |||||||

| Principal Amount | ||||||||

SHORT-TERM INVESTMENTS: 5.9% | ||||||||

| REPURCHASE AGREEMENTS: 5.9% | ||||||||

| $13,139,674 | Fixed Income Clearing Corp. 1.600%, 12/29/2023, due 01/02/2024 [collateral: par value $14,601,200, U.S. Treasury Note, 0.625%, due 07/31/2026, value $13,403,677] (proceeds $13,142,010) | 13,139,674 | ||||||

|

| |||||||

| | TOTAL SHORT-TERM INVESTMENTS | 13,139,674 | ||||||

|

| |||||||

| | TOTAL INVESTMENTS | 222,065,044 | ||||||

|

| |||||||

| Other Assets in Excess of Liabilities: 0.4% | 843,935 | |||||||

|

| |||||||

NET ASSETS: 100.0% | $ | 222,908,979 | ||||||

|

| |||||||

Percentages are stated as a percent of net assets.

| ADR | American Depositary Receipt |

| * | Non-Income Producing Security. |

| (a) | Security was purchased pursuant to Rule 144A under the Securities Act of 1933 and may be sold in transactions exempt from registration only to qualified institutional buyers or in a public offering registered under Securities Act of 1933. |

The accompanying notes are an integral part of these financial statements.

| Schedule of Investments | 13 | |||||

Table of Contents

iMGP Oldfield International Value Fund 2023 Annual Report (Unaudited)

The iMGP Oldfield International Value Fund rose 17.74% in 2023, underperforming the 18.95% gain for the MSCI EAFE Value Index. The MSCI EAFE Index returned 18.24%. The fund outperformed the Morningstar Foreign Large Blend category’s gain of 17.48%. Since the fund’s inception, the fund’s annualized return of 6.15% trails the 8.90% return of the MSCI EAFE Value Index but is ahead of the 5.45% gain of the MSCI EAFE Index.

Performance as of 12/31/2023 | ||||||||||||

One- Year | Three- Year | Since Inception 11/30/2020 | ||||||||||

iMGP Oldfield Internatl Value Fund | 17.74% | 4.29% | 6.15% | |||||||||

MSCI EAFE Value NR USD | 18.95% | 7.59% | 8.90% | |||||||||

MSCI EAFE NR USD | 18.24% | 4.02% | 5.45% | |||||||||

Morningstar US Fund Foreign Large Value | 17.48% | 6.08% | 7.66% | |||||||||

Gross Expense Ratio:2.11% Net Expense Ratio 0.94%* | ||||||||||||

Performance quoted represents past performance and does not guarantee future results. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance of the funds may be lower or higher than the performance quoted. Short term performance is not a good indication of the fund’s future performance and should not be the sole basis for investing in the fund. To obtain standardized performance of the funds, and performance as of the most recently completed calendar month, please visit www.imgptfunds.com. The Advisor has contractually agreed to limit the expenses of the fund through April 30, 2025. Without this limit the fund’s net expenses would be higher and the return would be lower.

* The expense ratios disclosed in the performance table are based on the most recent prospectus and may not tie to what are disclosed in the financial highlights.

MSCI index returns source: MSCI. Neither MSCI nor any other party involved in or related to compiling, computing, or creating the MSCI data makes any express or implied warranties or representations with respect to such data (or the results to be obtained by the use thereof), and all such parties hereby expressly disclaim all warranties of originality, accuracy, completeness, merchantability, or fitness for a particular purpose with respect to any of such data. Without limiting any of the foregoing, in no event shall MSCI, any of its affiliates, or any third party involved in or related to compiling, computing, or creating the data have any liability for any direct, indirect, special, punitive, consequential, or any other damages (including lost profits) even if notified of the possibility of such damages. No further distribution or dissemination of the MSCI data is permitted without MSCI’s express written consent. Source note: Returns prior to 1999 are the MSCI ACWI ex-US GR index. Returns from 1999 onwards are MSCI ACWI ex-US NR index. |

| |||||||||||

Manager Commentary

The portfolio’s performance lagged the MSCI EAFE Value benchmark slightly in 2023. The largest detractor for the year was LG H&H, the South Korean consumer goods company, which halved during (-51% total return in local currency terms). The other leading detractors for the year were, in order of their impact on the portfolio: Bayer (-28%), Alibaba (-11%), C.K. Hutchison (-5%) and Korea Tobacco & Ginseng (-4%).

In the last week of October, LG H&H reported third quarter results that fell short of the markets, and our, expectations. While they reported continued resilience of sales and profits in their Refreshment division (soft drinks) and the Home and Daily Beauty (HDB) division (combined 60% of profits for the last twelve months), their Beauty division (luxury skin care and cosmetics) reported weak sales and profit.

The Beauty division has been challenged since 2021 and is dominated by its luxury skincare range sold largely in China and Korea (to Chinese tourists). Sales to China, largely luxury skincare, fell 29% on the same period last year. Given some restructuring, rebranding expense and negative operating leverage, profit in beauty for the quarter was down almost 90%.

The problem in China is not unique to LG H&H. Other global skin care companies such as Estee Lauder and Beiersdorf have seen similar declines in their Asian travel business. In response they, like LG H&H, are working hard to return the industry to its pre-COVID structure by reducing exposure to resellers and reducing inventory in the channel—both tough decisions to take.

The results raise concerns that the problem is more than skin deep and that brand equity for these international players has been impaired, ceding market share to domestic Chinese players. The fact that global industry leaders like Estee Lauder are also suffering similar issues offers us some comfort. That said, after adjusting for the net cash on the balance sheet, the shares are now valued at 12.6x the lowered consensus expectations for profit in 2024 (earnings which are based on Beauty operating profit which is just 20% of 2021 levels).

The extreme weakness in the share price and the slow recovery in Beauty are disappointing but we think the current valuation fails to recognize Beauty’s recovery potential, the strength and stability of HDB and Refreshment (60% of operating profit) and LG H&H’s strong cash generation and net cash balance sheet.

| 14 | Litman Gregory Funds Trust | |||||

Table of Contents

The largest positive contributors to the strategy’s performance in 2023 were, in order of their impact on the strategy, Embraer (+69%), easyJet (+57%), Siemens (+35%), Exor (+33%), Samsung Electronics (+44%) and Tesco (+35%).

Embraer is an aircraft development and manufacturing firm, based in Brazil but largely selling into global markets—namely the United States. The firm had hit a severe valuation discount due to the scuppering of an expected deal with Boeing and downturn in demand due to COVID-19. In 2023, Embraer has demonstrated that these were transitionary setbacks. The valuation remains compelling, especially when compared to global peers. Beyond the core business on which our valuation is based, the firm also has a majority holding in Eve Air Mobility. EVE is a U.S.-listed entity developing electric powered aircraft for short passenger flights—the aircraft looks much like a large drone. While EVE is not profitable, and will likely not be for some time, it is a leading player in a market that is forecasted to be large in size. This is evidenced by the firm’s already substantive and growing international orderbook. As the technology and regulatory hurdles are met, the value of EVE will be added to the Embraer base valuation.

While easyJet’s shares started and finished the year strongly, the share price suffered significant turbulence during the year. In the second half of the fiscal year ending September 2023 the company flew 3% more miles than the year before the pandemic started. Strong pricing, a growing package holiday business and welcome cost control helped the company deliver record second half profits. Despite concerns about a slowing economy and pressure on consumers the company continues to expect a robust demand environment and firm pricing. The company ended the year with a net cash balance sheet and the shares valued at just 7.5x net income expected in 2024.

During the fourth quarter we bought two new holdings for the strategy—Michelin, the French automotive tire company, and Heineken Holdings, the Heineken family-controlled holding company that owns 50.4% of Heineken, the Dutch-based global brewing company. These purchases were funded from the sale of Mitsubishi Heavy Industries and a reduction in the holding of Sanofi (we later increased Sanofi after its profit warning funded by a reduction of Tesco).

Michelin is the largest global tire manufacturer. The company generates around half of its sales from the passenger car market, with the remainder split equally between trucks and specialty vehicles, including mining and aircraft tires. The low end of the tire market is commoditized, but Michelin is largely insulated as they focus on the premium end where customers care about performance and are willing to pay for it. Michelin tires have industry leading performance metrics and tend to be priced at a 10% premium. The initial purchase of a set of Michelin tires is often indirect, with customers choosing to buy a premium car which happens to come with a set of Michelin tires. When those tires are up for replacement after around four years, purchasers of premium cars tend to stick with the brand of tire the car was delivered with. The company spends a great deal of time and money to meet the strict performance requirements set by premium auto manufacturers. For this reason, the premium end of the market has significant barriers to entry.

Michelin is likely to benefit from industry tailwinds over the next few years. First, the move to electric vehicles means that tires gain in relative importance. This is because factors such as rolling resistance become more relevant. With cheap tires, an electric vehicle may not achieve the advertised energy efficiency and thus mileage. A second tailwind is more stringent regulation, including CO2 and microplastic emissions—Michelin performs well on both metrics and cheaper brands struggle to compete. These trends make it likely that Michelin can defend their market share and pricing premium.

Given its brand and pricing power, Michelin has a history of passing raw material costs on to customers, resulting in stable operating margins of 10-12% and return on invested capital of around 10%. With 75% of tire sales coming from the replacement market, this is also not a particularly cyclical business. We were able to buy Michelin at a historically high free cash flow yield of almost 10% which in our view does not reflect the quality and earnings profile of the business.

Heineken is a global beer company that was founded in 1864 by Gerard Heineken. Heineken owns 300 brands with the largest being Heineken (c.20% of volume). The Heineken brand competes with AB InBev’s Budweiser for the status of largest global brand outside of China. Other global brands the company owns include Amstel and Tiger.

Heineken owns 167 breweries with 14% share of the global beer market, second only to AB InBev (27%). A decade ago, Western Europe accounted for 44% of volumes, 50% of revenue, and 36% of profit. Following a series of acquisitions across several of the largest emerging-market countries, revenue from emerging-markets now accounts for 53% of revenue and Europe accounts for 30% of volume, 35% of revenue and 25% of profit. With the brewing costs for all beers being very similar, the key to profitability is the focus on cultivating premium branded beers. For Heineken, premium brands now account for 40% of sales. Among these is the world’s leading zero alcohol beer, Heineken 0.0%, a new growth area for the business.

The last three years have created the opportunity in Heineken today. Cost pressures and COVID-19 have seen gross margins fall from 50% to 44%. The competition has seen similar cost pressures that has meant that all operators have had to push through price increases not seen in a generation. Looking forward, we would expect pricing to hold but some of the costs to fall and this will help restore gross margins.

Today the Heineken family remains the controlling shareholders of Heineken through their 53.7% holding of Heineken Holding which in turn owns 50.4% of the main Heineken listing. Heineken Holding shares fell to a valuation of 14x price to 2024 earnings, a 17% discount to the valuation of the main listing, and we see a multiple in the high teens as fair.

| Fund Summary | 15 | |||||

Table of Contents

The strategy overall is valued at a price to expected earnings ratio of less than 10x and a price to book ratio of 1.1x. This compares with a price to expected earnings ratio of 13.2x and a price to book ratio of 1.8x for the MSCI EAFE benchmark and a price to expected earnings of 9.8x and a price to book ratio of 1.2x for the MSCI EAFE Value index. The weighted average upside for the portfolio ended the year at 54%, offering a prospective total return over the next couple of years of 60%, substantially ahead of its long-term average.

Portfolio Mix

The fund is built stock by stock from the bottom-up and can at times look very different from its benchmark. We believe this is key to generating excess long-term returns.

Over the last 12 months, the overall portfolio mix changed in the following way:

| • | The fund’s underweight to the financials sector increased as the strategy liquidated positions in Mitsubishi UFJ Financial and Nomura Holdings. Relative to its benchmark, this is now the largest sector underweight. |

| • | The fund overweight to consumer staples increased over the course of the year and it is the largest overweight in the strategy. A new position in Heineken was the main driver of this increase. |

| • | Consumer discretionary exposure increased over the year due to a new position in Michelin. |

| • | The largest change from a regional allocation standpoint is a reduction in Japanese equities. Following the sale of Mitsubishi UFJ Financial and Nomura Holdings, the fund’s sole position in the country is East Japan Railway. |

| • | As a result of the Japanese allocation decreasing, the European equity allocation increased by a similar amount. |

By Sector

Finance | 16.3% | |||

Consumer Discretionary | 8.1% | |||

Information Technology | 4.1% | |||

Communication Services | 5.1% | |||

Health Care & Pharmaceuticals | 13.6% | |||

Industrials | 22.9% | |||

Consumer Staples | 20.1% | |||

Real Estate | 0.0% | |||

Utilities | 4.9% | |||

Energy | 5.0% | |||

Materials | 0.0% | |||

Cash | -0.1% | |||

|

| |||

| 100.0% | ||||

|

|

By Region

US Equities | 0.0% | |||

Developed International Equities | 84.4% | |||

Emerging Market Equities | 15.6% | |||

|

| |||

| 100.0% | ||||

|

|

By Region

Europe | 73.4% | |||

North America | 0.0% | |||

Asia ex-Japan | 19.0% | |||

Japan | 3.0% | |||

Latin America | 4.6% | |||

Africa | 0.0% | |||

Australia/ New Zealand | 0.0% | |||

Middle East | 0.0% | |||

Other Countries | 0.0% | |||

|

| |||

| 100.0% | ||||

|

| |||

* Cash is excluded from calculation |

By Market Cap

Small Cap | 0.0% | |||

Mid Cap | 10.6% | |||

Large Cap | 89.4% | |||

|

| |||

| 100.0% | ||||

|

|

| 16 | Litman Gregory Funds Trust | |||||

Table of Contents

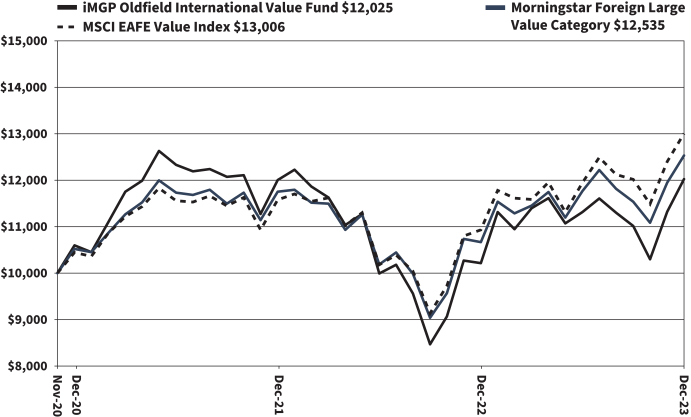

iMGP Oldfield International Value Fund Value of Hypothetical $10,000

The value of a hypothetical $10,000 investment in the iMGP Oldfield International Value Fund from November 30, 2020 to December 31, 2023 compared with the MSCI EAFE Value Index, and Morningstar Foreign Large Value Category.

The hypothetical $10,000 investment at fund inception includes changes due to share price and reinvestment of dividends and capital gains. The chart does not imply future performance. Indexes are unmanaged, do not incur fees, expenses or taxes, and cannot be invested in directly.

Performance quoted does not include a deduction for taxes that a shareholder would pay on the redemption of fund shares.

| Fund Summary | 17 | |||||

Table of Contents

iMGP Oldfield International Value Fund

SCHEDULE OF INVESTMENTS IN SECURITIES at December 31, 2023

| Shares | Value | |||||||

COMMON STOCKS: 95.3% | ||||||||

| Brazil: 4.7% | ||||||||

| 89,000 | Embraer SA - ADR* | $ | 1,642,050 | |||||

|

| |||||||

| China: 8.0% | ||||||||

| 140,200 | Alibaba Group Holding Ltd. | 1,356,913 | ||||||

| 274,500 | CK Hutchison Holdings Ltd. | 1,470,687 | ||||||

|

| |||||||

| 2,827,600 | ||||||||

|

| |||||||

| France: 9.1% | ||||||||

| 41,541 | Cie Generale des Etablissements Michelin SCA | 1,491,421 | ||||||

| 17,263 | Sanofi SA | 1,713,855 | ||||||

|

| |||||||

| 3,205,276 | ||||||||

|

| |||||||

| Germany: 18.7% | ||||||||

| 36,642 | Bayer AG | 1,362,953 | ||||||

| 128,080 | E.ON SE | 1,721,205 | ||||||

| 55,726 | Fresenius SE & Co. KGaA | 1,730,116 | ||||||

| 9,371 | Siemens AG | 1,761,186 | ||||||

|

| |||||||

| 6,575,460 | ||||||||

|

| |||||||

| Italy: 5.0% | ||||||||

| 104,386 | Eni SpA | 1,772,021 | ||||||

|

| |||||||

| Japan: 3.0% | ||||||||

| 18,500 | East Japan Railway Co. | 1,067,290 | ||||||

|

| |||||||

| Netherlands: 9.8% | ||||||||

| 17,197 | EXOR NV | 1,721,378 | ||||||

| 20,301 | Heineken Holding NV | 1,719,971 | ||||||

|

| |||||||

| 3,441,349 | ||||||||

|

| |||||||

| South Korea: 11.0% | ||||||||

| 23,147 | KT&G Corp. | 1,561,825 | ||||||

| 3,091 | LG H&H Co. Ltd. | 852,011 | ||||||

| 23,860 | Samsung Electronics Co. Ltd. | 1,454,313 | ||||||

|

| |||||||

| 3,868,149 | ||||||||

|

| |||||||

| Sweden: 6.5% | ||||||||

| 210,464 | Svenska Handelsbanken AB - Class A | 2,291,612 | ||||||

|

| |||||||

| United Kingdom: 19.5% | ||||||||

| 1,139,106 | BT Group PLC | 1,793,710 | ||||||

| 326,056 | easyJet PLC* | 2,118,517 | ||||||

| 2,883,396 | Lloyds Banking Group PLC | 1,752,602 | ||||||

| 324,706 | Tesco PLC | 1,201,728 | ||||||

|

| |||||||

| 6,866,557 | ||||||||

|

| |||||||

| | TOTAL COMMON STOCKS | 33,557,364 | ||||||

|

| |||||||

PREFERRED STOCK: 5.0% | ||||||||

| Germany: 5.0% | ||||||||

| 21,867 | Henkel AG & Co. KGaA - (Preference Shares) | 1,762,192 | ||||||

|

| |||||||

| | TOTAL PREFERRED STOCK | 1,762,192 | ||||||

|

| |||||||

| | TOTAL INVESTMENTS | 35,319,556 | ||||||

|

| |||||||

| Liabilities in Excess of Other Assets: (0.3)% | (96,742 | ) | ||||||

|

| |||||||

NET ASSETS: 100.0% | $ | 35,222,814 | ||||||

|

| |||||||

Percentages are stated as a percent of net assets.

| ADR | American Depositary Receipt |