PART I

ITEM 1. BUSINESS.

BUSINESS OVERVIEW

We help organizations around the world protect their information, reduce storage costs, comply with regulations, facilitate corporate disaster recovery, and better use their information and IT infrastructure for business advantages, regardless of its format, location or life cycle stage. We do this by storing physical records and data backup media, offering information management solutions, and providing data center space for enterprise-class colocation and hyperscale deployments. We offer comprehensive records and information management services and data management services, along with the expertise and experience to address complex storage and information management challenges such as rising storage rental costs, legal and regulatory compliance, and disaster recovery requirements. We provide secure and reliable data center facilities to protect digital information and ensure the continued operation of our customers’ IT infrastructure, with reliable and flexible deployment options.

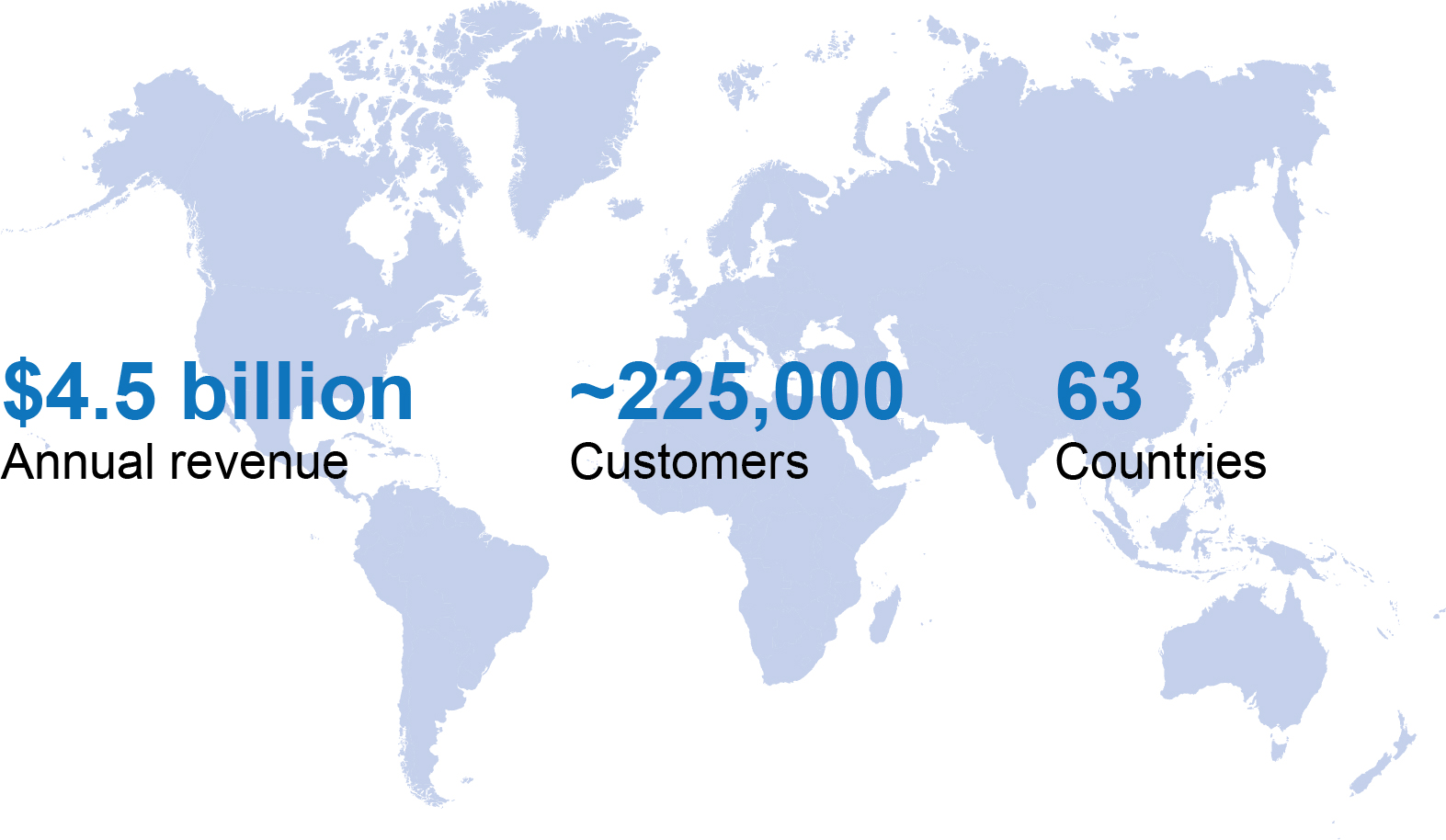

Founded in an underground facility near Hudson, New York in 1951, Iron Mountain Incorporated, a Delaware corporation, has approximately 225,000 customers in a variety of industries in 63 countries around the world, as of December 31, 2021. We currently serve customers across an array of market verticals - commercial, legal, financial, healthcare, insurance, life sciences, energy, business services, entertainment and government organizations, including approximately 95% of the Fortune 1000. As of December 31, 2021, we employed approximately 25,000 people. We are listed on the New York Stock Exchange (the “NYSE”) and are a constituent of the Standard & Poor’s 500 Index and the MSCI REIT index. As of December 31, 2021, we were number 605 on the Fortune 1000.

We have been organized and have operated as a REIT beginning with our taxable year ended December 31, 2014.

BUSINESS STRATEGY

OVERVIEW

Our company has been a market leader in the physical ecosystem supporting information storage and retrieval, as most businesses have relied on paper documents or computer tapes to store their valuable information. Over time, customers are increasing their digital information, with the new information storage ecosystem being a hybrid of physical and digital mediums. We are a different company than the one we have been historically. The strategic journey we are on is driving this change and our focus remains on four pillars outlined below to grow our business.

| | | | | |

| |

| Continued growth in physical storage through revenue management as well as volume growth achieved in faster growing emerging markets and consumer and adjacent business growth in developed markets | •We are establishing and enhancing leadership positions in higher-growth markets such as central and eastern Europe, Latin America, Asia and Africa, through both organic expansion and acquisitions in countries where GDP growth is faster and outsourcing information management is at an earlier stage. •We continue to identify, acquire, incubate and scale complementary businesses and products to support our long-term growth objectives and drive solid returns on invested capital. These opportunities include our digital services and our ALM, Entertainment Services, Fine Arts and Consumer Storage (each as defined below) businesses. |

| |

| |

| Utilizing our global scale as well as 70 years of customer trust to deliver differentiated data center offerings | •We have made significant progress in scaling our Global Data Center Business through acquisitions and organic growth, with 19 operating data centers across 16 global markets. •As of December 31, 2021, approximately 89% of our data center capacity was leased. With total potential capacity of 604 megawatts ("MW") in land and buildings currently owned or operated by us, we are among the largest global data center operators. |

| |

| Developing and offering new products and services that allow our customers to achieve reliable and secure information management solutions in an increasingly hybrid physical and digital world | •Our customers are faced with navigating a more complex regulatory environment, and one in which hybrid physical and digital solutions have become the norm. Our strategy is underpinned by our persistent focus on best-in-class customer experience, as we continue to seek innovative solutions to help our customers progress on their journey from physical storage to a digital ecosystem. |

| |

| | | | | |

| Increased investment in our business and customer-centric solutions | •We have established an investment strategy to fuel our growth. The investments are enabled by the success of Project Summit and informed by our established leadership position in the physical storage business, expanding services, and our significant progress in the Global Data Center business. |

| |

| |

PROJECT SUMMIT

In October 2019, we announced our global program ("Project Summit") designed to better position us for future growth and achievement of our strategic objectives. We expanded Project Summit during the first quarter of 2020 to include additional opportunities to streamline our business and operations, as well as accelerated the timing of certain opportunities previously identified. As a result of this initiative, we simplified our global structure, rebalanced resources to focus on higher growth areas, realigned our management structure to create a more dynamic, agile organization, and made investments to enhance the customer experience. All Project Summit activities were completed in 2021, resulting in $375.0 million in annual Adjusted EBITDA benefits of which $165.0 million were delivered in 2020 and $160.0 million were delivered in 2021, with the remainder to come in 2022. Project Summit charges totaled approximately $450.0 million since the program's inception. For further details on Project Summit, see the "Overview" section of “Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations” in this Exhibit 99.1 to this Current Report.

BUSINESS SEGMENTS

The amount of revenues derived from our business segments and other relevant data, including financial information about geographic areas and product and service lines, for the years ended December 31, 2021, 2020 and 2019, are set forth in Note 11 to Notes to Consolidated Financial Statements included in this Exhibit 99.1 to this Current Report.

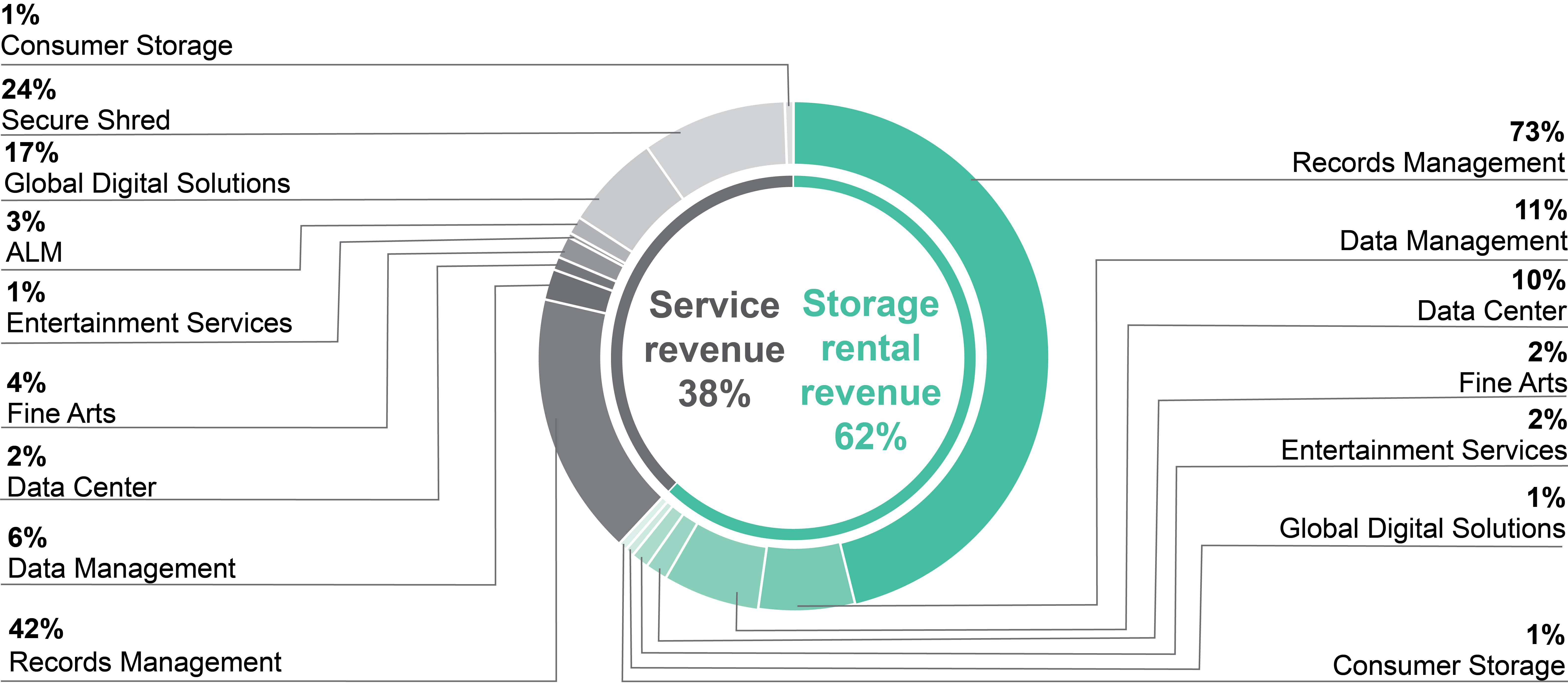

The Global RIM Business segment includes several distinct offerings.

Records Management, stores physical records and provides healthcare information services, vital records services, courier operations, and the collection, handling and disposal of sensitive documents (collectively, “Records Management”) for customers in 63 countries around the globe. As of December 31, 2021, we stored approximately 740 million cubic feet of hardcopy records.

Data Management, provides storage and rotation of backup computer media as part of corporate disaster recovery plans, including service and courier operations (“Data Protection & Recovery”); server and computer backup services; and related services offerings, (collectively, “Data Management”).

Global Digital Solutions (“GDS”), develops, implements and supports comprehensive storage and information management solutions for the complete lifecycle of our customers’ information, including the management of physical records, conversion of documents to digital formats and digital storage of information, primarily in the United States and Canada.

Secure Shredding, includes the scheduled pick-up of office records that customers accumulate in specially designed secure containers we provide and is a natural extension of our hardcopy records management operations, completing the lifecycle of a record. Through a combination of shredding facilities and mobile shredding units consisting of custom built trucks, we are able to offer secure shredding services to our customers throughout the United States, Canada and South Africa.

Entertainment Services, entertainment and media services which help industry clients store, safeguard and deliver physical media of all types, and provides digital content repository systems that house, distribute, and archive key media assets, throughout the United States, Canada, France, China - Hong Kong S.A.R, the Netherlands and the United Kingdom.

Consumer Storage, provides on-demand, valet storage for consumers (“Consumer Storage”) across 31 markets in North America through a strategic partnership that utilizes data analytics and machine learning to provide effective customer acquisition and a convenient and seamless consumer storage experience.

| | |

|

| GLOBAL DATA CENTER BUSINESS |

|

The Global Data Center Business segment provides enterprise-class data center facilities and hyperscale-ready capacity to protect mission-critical assets and ensure the continued operation of our customers’ IT infrastructure, with secure, reliable and flexible data center options. The world’s most heavily regulated organizations have trusted us with their data centers for over 15 years, and as of December 31, 2021, five of the top 10 global cloud providers were Iron Mountain Data Center customers.

As of December 31, 2021, our Global Data Center Business footprint spans nine markets in the United States and seven international markets.

| | | | | |

| |

| UNITED STATES | INTERNATIONAL MARKETS |

| Denver, Colorado | Amsterdam |

| Kansas City, Missouri | London |

| Boston, Massachusetts | Singapore |

| Boyers, Pennsylvania | Frankfurt (directly and through an unconsolidated joint venture) |

| Manassas, Virginia | Mumbai (through an unconsolidated joint venture) |

| Edison, New Jersey | Pune (through an unconsolidated joint venture) |

| Columbus, Ohio | Noida (through an unconsolidated joint venture) |

| Phoenix and Scottsdale, Arizona | |

| | |

|

| CORPORATE AND OTHER BUSINESS |

|

Corporate and Other Business consists primarily of our Fine Arts and Asset Lifecycle Management businesses and other corporate items.

Fine Arts, provides technical expertise in the handling, installation and storing of art in the United States, Canada and Europe.

Asset Lifecycle Management ("ALM"), provides hyperscale and corporate IT infrastructure managers with services and solutions that enable the decommissioning and disposition or sale of IT hardware and component assets. ALM services are enabled by: secure logistics and chain of custody practices, environmentally-responsible asset processing and recycling, and data sanitization and asset refurbishment services that enable value recovery through asset remarketing. Our ALM services focus on protecting and eradicating customer data while maintaining strong, auditable and transparent chain of custody practices.

Corporate and Other Business also includes costs related to executive and staff functions, including finance, human resources and IT, which benefit the enterprise as a whole.

BUSINESS ATTRIBUTES

Our business has the following attributes:

| | | | | |

| |

Large, Diversified, Global Business | The world’s most heavily regulated organizations trust us with the storage of their records. Our mission-critical storage offerings and related services generated approximately $4.5 billion in annual revenue in 2021. Our business has a highly diverse customer base of approximately 225,000 customers - with no single customer accounting for more than approximately 1% of revenue during the year ended December 31, 2021 - and operates in 63 countries globally. This presents a significant cross-sell opportunity for our Global Data Center, Global Digital Solutions and ALM businesses. |

| |

| |

Recurring, Durable Revenue Stream | We generate a majority of our revenues from contracted storage rental fees, via agreements that generally range from one to five years in length. Historically, in our Records Management business, we have seen strong customer retention (of approximately 98%) and solid physical records retention; more than 50% of physical records that entered our facilities 15 years ago are still with us today. We have also seen strong customer retention in our Global Data Center Business. |

| |

| |

Comprehensive Information Management Solution | As an S&P 500 REIT with approximately 1,450 locations globally and with offerings spanning physical storage, digitization solutions and digital storage, we are positioned to provide a holistic offering to our customers. We are able to cater to our customers’ physical and digital needs and to help guide their digital transformation journey. |

| |

| |

Significant Owner and Operator of Real Estate | We operate approximately 95 million square feet of real estate worldwide. Our owned real estate footprint spans nearly 25 million square feet and is concentrated in major metropolitan statistical areas in North America, Western Europe and Latin America. |

| |

| |

Limited Revenue Cyclicality | Historically, economic downturns have not significantly affected our storage rental business. Due to the durability of our total global physical volumes, the success of our revenue management initiatives, and the growth of our Global Data Center Business, we believe we can continue to grow organic storage rental revenue over time. |

| |

| |

Shifting Revenue Mix | We have identified a number of areas where we see opportunity for growth as we position ourselves to unlock greater value for our customers. These business lines, including Data Center, Fine Arts and Entertainment Services, Consumer Storage and ALM, represent markets with strong secular growth. |

| |

In addition, our Global Data Center business has the following attributes:

| | | | | |

| |

Large Data Center Platform with Significant Expansion Opportunity | As of December 31, 2021, we had 177 MW of leasable capacity with an additional 427 MW under construction or held for development. |

| |

| |

Differentiated Compliance and Security | We offer comprehensive compliance support and physical and cyber security. Our Security-in-Depth approach to security includes a combination of technical and human security measures, and experienced senior military and public sector security leaders oversee our security. As of December 31, 2021, our data centers comply with one of the most comprehensive compliance programs in the industry, including enterprise-wide certified ISO 14001 and 50001 environmental and energy management systems. We also report globally on service organizational controls, as well as global ISO 27001 certification, and PCI-DSS compliance, and met FISMA HIGH and FedRAMP controls in the United States. |

| |

| |

Efficient Access and Flexibility | We have the ability to provide customers with a range of deployment options from one cabinet to an entire building, leveraging our global portfolio of hyperscale-ready and underground data centers. We also provide access to numerous carriers, cloud providers and peering exchanges with migration support and IT. |

| |

| |

100% Green Powered Data Centers | As of December 31, 2021, our Global Data Center platform was powered by 100% renewable energy, with carbon credit assistance and low power usage effectiveness (“PUE"). We are one of the top 30 buyers of renewable energy among the Fortune 1000 and now offer the Green Power Pass, which allows customers to include the power they consume at any Iron Mountain data centers as green power in their CDP, RE100, GRI, or other sustainability reporting. |

| |

COMPETITION

We compete with thousands of storage and information management services providers around the world as well as storage and information management services managed and operated internally by organizations. We believe that competition for records and information customers is based on price, reputation and reliability, quality and security of storage, quality of service and scope and scale of technology. While the majority of our competitors operate in only one market or region, we believe we provide a differentiated global offering that competes effectively in these areas.

We also compete with numerous data center developers, owners and operators, many of whom own properties similar to ours in some of the same metropolitan areas where our facilities are located. We believe that competition for data center customers is based on availability of power, security considerations, location, connectivity and rental rates, and we generally believe we compete effectively in each of these areas. Additionally, we believe our strong brand, global footprint and excellent commercial relationships enable us to compete successfully and provide significant cross-sell opportunities with our existing customer base.

HUMAN CAPITAL MANAGEMENT

EMPLOYEES

As of December 31, 2021, we employed approximately 9,000 employees in the United States and approximately 16,000 employees outside of the United States. As of December 31, 2021, approximately 500 employees were represented by unions in North America and approximately 1,250 employees were represented by unions in Latin America. All union employees are currently under renewed labor agreements or operating under an extension agreement.

BENEFIT PROGRAMS

We provide our employees with benefits that are designed to support their overall physical, financial, emotional and social well-being. These benefits vary by location but may include health and welfare benefits, paid time off, and programs to support financial security. Additionally, employees are able to access emotional well-being resources through global employee assistance programs. Certain unionized employees receive benefits through unions and are not eligible to participate in our benefit programs. In addition to base compensation and other usual benefits, a significant portion of full-time employees participate in some form of incentive-based compensation program that provides payments based on revenues, profits or attainment of specific objectives for the unit in which they work.

DIVERSITY, EQUITY AND INCLUSION

At Iron Mountain, we believe that an inclusive environment with diverse teams produces more creative solutions, results in better, more innovative products and services and is crucial to our efforts to attract and retain key talent. As one of our five core company values, Promoting Including and Teamwork is a behavior all of our employees are expected to demonstrate every day. We have prioritized diversity, equity and inclusion ("DEI") as part of our corporate-wide strategic goals. Steps we have taken to create and sustain a more diverse, equitable and inclusive environment include: hiring a Global Chief Diversity, Equity & Inclusion Officer with significant DEI experience to lead our cultural transformation, the path to creating an environment of inclusiveness and belonging. We review and revise our systems, policies and processes to assure that our structures facilitate inclusiveness and accountability. We ensure that our recruiting efforts reflect our diversity goals and we launch, expand and support our Employee Resource Groups, who meet and connect on shared characteristics and life experiences that can prove impactful to our business, our customers and our employees.

COMPANY CULTURE

We recognize that an inspired culture is foundational to how we deliver on our purpose and create sustained growth and value for our shareholders. Iron Mountain's culture is deeply rooted in its enduring values: Act with Integrity, Own Safety and Security, Build Customer Value, Take Ownership and Promote Inclusion and Teamwork. While Iron Mountain is a culture of learning, collaboration, diversity and well-being, we know that culture overall comes down to what it feels like to work at Iron Mountain. This is why we celebrate our employees who consistently demonstrate Iron Mountain's values in measurable ways while inspiring others to do the same. We commit significant resources to sustaining a culture that enables innovation and facilitates trust, engagement, belonging and performance. We regularly survey our employees on a range of topics to measure our effectiveness and to obtain their views. In addition, headcount data and cost analyses offer insights into how and where our employees work. We use all of this information to refine our approach when necessary to drive increased employee engagement and success.

COMMUNITY INVOLVEMENT

We are committed to integrating responsible and sustainable practices throughout our organization to help our operations to have a positive impact on the environment and the communities in which we operate. We aim to give back to the communities where we live and work, and believe that this commitment helps in our efforts to attract and retain employees. We offer philanthropic support to our global community through our Living Legacy Initiative, which is our commitment to help preserve and make accessible cultural and historical information and artifacts. We encourage volunteerism in the communities in which we live and work through our Moving Mountains volunteer program, offering paid time off for employees to help community-based and civic-minded organizations.

INSURANCE

For strategic risk transfer purposes, we maintain a comprehensive insurance program with insurers that we believe to be reputable and that have adequate capitalization in amounts that we believe to be appropriate. Property insurance is purchased on a comprehensive basis, including flood and earthquake (including excess coverage), subject to certain policy conditions, sublimits and deductibles. Property is insured based upon the replacement cost of real and personal property, including leasehold improvements, business income loss and extra expense. Other types of insurance that we carry, which are also subject to certain policy conditions, sublimits and deductibles, include medical, workers’ compensation, general liability, umbrella, automobile, professional, warehouse legal liability and directors’ and officers’ liability policies.

GOVERNMENT REGULATION

We are required to comply with numerous U.S. federal, state, and foreign laws and regulations covering a wide variety of subject matters which may have a material effect on our capital expenditures, earnings and competitive position.

For example, some of our current and formerly owned or leased properties were previously used by entities other than us for industrial or other purposes, or were affected by waste generated from nearby properties, that involved the use, storage, generation and/or disposal of hazardous substances and wastes, including petroleum products. In some instances, this prior use involved the operation of underground storage tanks or the presence of asbestos-containing materials. Where we are aware of environmental conditions that require remediation, we undertake appropriate activity, in accordance with all legal requirements. Although we have from time to time conducted limited environmental investigations and remedial activities at some of our former and current facilities, we have not undertaken an environmental review of all of our properties, including those we have acquired. We therefore may be potentially liable for environmental cost and may be unable to sell, rent, mortgage or use contaminated real estate owned or leased by us. Under various federal, state and local environmental laws, we may be liable for environmental compliance and remediation costs to address contamination, if any, located at owned and leased properties as well as damages arising from such contamination, whether or not we know of, or were responsible for, the contamination, or the contamination occurred while we owned or leased the property. Environmental conditions for which we might be liable may also exist at properties that we may acquire in the future. In addition, future regulatory action and environmental laws may impose costs for environmental compliance that do not exist today.

We transfer a portion of our risk of financial loss due to currently undetected environmental matters by purchasing an environmental impairment liability insurance policy, which covers all owned and leased locations. Coverage is provided for both liability and remediation costs.

In addition, we are subject to numerous U.S. federal, state, local and foreign laws and regulations relating to data privacy and cybersecurity, which are complex, change frequently and have tended to become more stringent over time. We devote substantial resources, and may in the future have to devote significant additional resources, to facilitate compliance with these laws and regulations, and to investigate, defend or remedy actual or alleged violations or breaches. Any failure by us to comply with, or remedy any violations or breaches of, these laws and regulations could result in the curtailment of certain of our operations, the imposition of fines and penalties, liability resulting from litigation, restrictions on our ability to carry on or expand our operations, significant costs and expenses and reputational harm.

For more information about laws and regulations that could affect our business, see “Item 1A. Risk Factors” included in our Original Annual Report (as defined below).

CORPORATE SOCIAL RESPONSIBILITY

Through our approach to Corporate Social Responsibility, we not only see ourselves as having our own responsibility to society, but also in helping our customers with their own environmental, social and governance (ESG) goals, and helping them gain value, make improvements and save costs. We are committed to responsible, sustainable growth. To that end, we have publicly adopted 20 goals to address our environmental footprint, corporate philanthropy and volunteerism and DEI practices. As signatories of The Climate Pledge, we are on a path to reach net zero carbon emissions by 2040. We are committed to the safety and well-being of our employees and strive to cultivate a culture of inclusion that values diverse perspectives across our global workforce. Iron Mountain and its employees also make a social impact in the communities in which we operate through charitable giving and volunteerism.

We have been recognized for our commitment to Corporate Social Responsibility. We ranked 93rd on Newsweek’s 2022 list of America’s Most Responsible Companies. We were a top scorer on the Disability Equality Index in 2020 and 2021. We received a 100% on the Human Rights Campaign Corporate Equality Index for each of the years 2018 through 2022.

We are committed to transparent reporting on sustainability and corporate responsibility efforts in accordance with the guidelines of the Global Reporting Initiative. Our corporate responsibility report highlights our progress against key measures of success for our efforts in the community, our environment, and for our people. We are a member of the FTSE4 Good Index, MSCI World ESG Index, MSCI World Climate Change Index and MSCI USA ESG Select Index, each of which include companies that meet globally recognized corporate responsibility standards. A copy of our corporate responsibility report is available on the “About Us” section of our website, www.ironmountain.com, under the heading “Corporate Social Responsibility." We are not including the information contained on or available through our website as part of, or incorporating such information by reference into, this Exhibit 99.1 to this Current Report. In addition, we continue to work to further align our reporting with the recommendations of the Financial Stability Board’s Task Force on Climate-related Financial Disclosures to disclose climate-related financial risks and opportunities.

| | | | | |

| |

STRONG SUSTAINABILITY FOCUS •Green Power Pass solution in Data Center market to help customers manage their carbon footprint. •Part of RE100 Initiative — commitment to using renewable energy sources for 100% of our worldwide electricity. •Founding signatory of the 24/7 Carbon-Free Energy (CFE) Compact committed to consuming carbon-free electricity every hour on every grid where we operate. •81% of our global electricity use - including 100% of the electricity used to power our Data Center business was from renewable sources in 2020. •Reduced GHG emissions by 62% (since 2016) as part of our Science Based Target and net zero by 2040 commitment. •Received a 100% on the Human Rights Campaign Corporate Equality Index for each of the years 2018 through 2022. |

|

|

INTERNET WEBSITE

Our Internet address is www.ironmountain.com. Under the “Investors” section on our website, we make available, free of charge, our Annual Reports on Form 10-K, our Quarterly Reports on Form 10-Q, our Current Reports on Form 8-K and amendments to those reports filed or furnished pursuant to Section 13(a) or 15(d) of the Securities Exchange Act of 1934 (the “Exchange Act”) as soon as reasonably practicable after such forms are filed with or furnished to the SEC. We are not including the information contained on or available through our website as a part of, or incorporating such information by reference into, this Exhibit 99.1 to this Current Report. Copies of our corporate governance guidelines, code of ethics and the charters of our audit, compensation, finance, nominating and governance, risk and safety, and technology committees are available on the “Investors” section of our website, www.ironmountain.com, under the heading “Corporate Governance."

ITEM 2. PROPERTIES.

As of December 31, 2021, we conducted operations through 1,184 leased facilities and 263 owned facilities. Our facilities are divided among our reportable operating segments as follows: Global RIM Business (1,386), Global Data Center Business (17) and Corporate and Other Business (44). These facilities contain a total of approximately 94.6 million square feet of space. A breakdown of owned and leased facilities by country (and by state within the United States) is listed below:

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | LEASED | | OWNED | | TOTAL |

| COUNTRY/STATE | NUMBER | | SQUARE FEET | | NUMBER | | SQUARE FEET | | NUMBER | | SQUARE FEET |

| North America | | | | | | | | | | | | | | | | | | | | | | | |

| United States (Including Puerto Rico) | | | | | | | | | | | | | | | | | | | | | | | |

| Alabama | | 3 | | | | | 312,473 | | | | | 1 | | | | | 12,621 | | | | | 4 | | | | | 325,094 | | |

| Arizona | | 8 | | | | | 496,448 | | | | | 6 | | | | | 1,207,281 | | | | | 14 | | | | | 1,703,729 | | |

| Arkansas | | 2 | | | | | 63,604 | | | | | — | | | | | — | | | | | 2 | | | | | 63,604 | | |

| California | | 67 | | | | | 5,908,150 | | | | | 10 | | | | | 958,856 | | | | | 77 | | | | | 6,867,006 | | |

| Colorado | | 8 | | | | | 466,336 | | | | | 4 | | | | | 484,490 | | | | | 12 | | | | | 950,826 | | |

| Connecticut | | 6 | | | | | 309,836 | | | | | 3 | | | | | 527,666 | | | | | 9 | | | | | 837,502 | | |

| Delaware | | 3 | | | | | 239,640 | | | | | 1 | | | | | 120,921 | | | | | 4 | | | | | 360,561 | | |

| District of Columbia | | 1 | | | | | 1,670 | | | | | — | | | | | — | | | | | 1 | | | | | 1,670 | | |

| Florida | | 31 | | | | | 2,240,035 | | | | | 5 | | | | | 263,930 | | | | | 36 | | | | | 2,503,965 | | |

| Georgia | | 9 | | | | | 798,880 | | | | | 5 | | | | | 265,049 | | | | | 14 | | | | | 1,063,929 | | |

| Idaho | | 2 | | | | | 105,021 | | | | | — | | | | | — | | | | | 2 | | | | | 105,021 | | |

| Illinois | | 15 | | | | | 1,213,808 | | | | | 7 | | | | | 1,309,975 | | | | | 22 | | | | | 2,523,783 | | |

| Indiana | | 6 | | | | | 344,516 | | | | | — | | | | | — | | | | | 6 | | | | | 344,516 | | |

| Iowa | | 2 | | | | | 145,138 | | | | | 1 | | | | | 14,200 | | | | | 3 | | | | | 159,338 | | |

| Kansas | | 3 | | | | | 253,919 | | | | | — | | | | | — | | | | | 3 | | | | | 253,919 | | |

| Kentucky | | 2 | | | | | 64,000 | | | | | 4 | | | | | 418,760 | | | | | 6 | | | | | 482,760 | | |

| Louisiana | | 4 | | | | | 388,475 | | | | | — | | | | | — | | | | | 4 | | | | | 388,475 | | |

| Maine | | — | | | | | — | | | | | 1 | | | | | 95,000 | | | | | 1 | | | | | 95,000 | | |

| Maryland | | 20 | | | | | 2,139,060 | | | | | 2 | | | | | 83,442 | | | | | 22 | | | | | 2,222,502 | | |

| Massachusetts (including Corporate Headquarters) | | 8 | | | | | 545,039 | | | | | 7 | | | | | 1,025,167 | | | | | 15 | | | | | 1,570,206 | | |

| Michigan | | 17 | | | | | 1,068,499 | | | | | 2 | | | | | 62,300 | | | | | 19 | | | | | 1,130,799 | | |

| Minnesota | | 12 | | | | | 908,474 | | | | | — | | | | | — | | | | | 12 | | | | | 908,474 | | |

| Mississippi | | 3 | | | | | 201,300 | | | | | — | | | | | — | | | | | 3 | | | | | 201,300 | | |

| Missouri | | 13 | | | | | 1,548,828 | | | | | 1 | | | | | 25,120 | | | | | 14 | | | | | 1,573,948 | | |

| Montana | | 3 | | | | | 38,548 | | | | | — | | | | | — | | | | | 3 | | | | | 38,548 | | |

| Nebraska | | 1 | | | | | 34,560 | | | | | 2 | | | | | 266,733 | | | | | 3 | | | | | 301,293 | | |

| Nevada | | 7 | | | | | 276,520 | | | | | 1 | | | | | 107,041 | | | | | 8 | | | | | 383,561 | | |

| New Hampshire | | — | | | | | — | | | | | 1 | | | | | 146,467 | | | | | 1 | | | | | 146,467 | | |

| New Jersey | | 33 | | | | | 3,074,071 | | | | | 8 | | | | | 2,476,635 | | | | | 41 | | | | | 5,550,706 | | |

| New Mexico | | 3 | | | | | 151,473 | | | | | — | | | | | — | | | | | 3 | | | | | 151,473 | | |

| New York | | 18 | | | | | 877,103 | | | | | 12 | | | | | 1,166,558 | | | | | 30 | | | | | 2,043,661 | | |

| North Carolina | | 19 | | | | | 976,504 | | | | | 3 | | | | | 150,624 | | | | | 22 | | | | | 1,127,128 | | |

| Ohio | | 14 | | | | | 1,074,262 | | | | | 4 | | | | | 250,291 | | | | | 18 | | | | | 1,324,553 | | |

| Oklahoma | | 5 | | | | | 228,425 | | | | | — | | | | | — | | | | | 5 | | | | | 228,425 | | |

| Oregon | | 11 | | | | | 384,296 | | | | | 1 | | | | | 55,621 | | | | | 12 | | | | | 439,917 | | |

| Pennsylvania | | 23 | | | | | 2,181,786 | | | | | 3 | | | | | 2,062,761 | | | | | 26 | | | | | 4,244,547 | | |

| Puerto Rico | | 4 | | | | | 237,969 | | | | | 1 | | | | | 54,352 | | | | | 5 | | | | | 292,321 | | |

| Rhode Island | | 1 | | | | | 70,159 | | | | | 1 | | | | | 12,748 | | | | | 2 | | | | | 82,907 | | |

| South Carolina | | 5 | | | | | 261,011 | | | | | 2 | | | | | 214,238 | | | | | 7 | | | | | 475,249 | | |

| Tennessee | | 5 | | | | | 256,743 | | | | | 4 | | | | | 63,909 | | | | | 9 | | | | | 320,652 | | |

| Texas | | 43 | | | | | 2,349,451 | | | | | 21 | | | | | 1,894,453 | | | | | 64 | | | | | 4,243,904 | | |

| Utah | | 2 | | | | | 78,148 | | | | | 1 | | | | | 90,553 | | | | | 3 | | | | | 168,701 | | |

| Vermont | | 2 | | | | | 55,200 | | | | | — | | | | | — | | | | | 2 | | | | | 55,200 | | |

| Virginia | | 12 | | | | | 685,369 | | | | | 7 | | | | | 795,036 | | | | | 19 | | | | | 1,480,405 | | |

| Washington | | 6 | | | | | 701,991 | | | | | 5 | | | | | 196,028 | | | | | 11 | | | | | 898,019 | | |

| West Virginia | | 2 | | | | | 105,502 | | | | | — | | | | | — | | | | | 2 | | | | | 105,502 | | |

| Wisconsin | | 5 | | | | | 379,857 | | | | | 1 | | | | | 10,655 | | | | | 6 | | | | | 390,512 | | |

| Total United States | | 469 | | | | | 34,242,097 | | | | | 138 | | | | | 16,889,481 | | | | | 607 | | | | | 51,131,578 | | |

| Canada | | 46 | | | | | 3,081,804 | | | | | 16 | | | | | 1,783,258 | | | | | 62 | | | | | 4,865,062 | | |

| Total North America | | 515 | | | | | 37,323,901 | | | | | 154 | | | | | 18,672,739 | | | | | 669 | | | | | 55,996,640 | | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | |

| | | | | | | | | | | |

| LEASED | | OWNED | | TOTAL |

| COUNTRY/STATE | NUMBER | | SQUARE FEET | | NUMBER | | SQUARE FEET | | NUMBER | | SQUARE FEET |

| International | | | | | | | | | | | | | | | | | | | | | | | |

| Argentina | | 2 | | | | | 134,753 | | | | | 4 | | | | | 298,864 | | | | | 6 | | | | | 433,617 | | |

| Armenia | | 3 | | | | | 13,712 | | | | | — | | | | | — | | | | | 3 | | | | | 13,712 | | |

| Australia | | 41 | | | | | 2,888,639 | | | | | 2 | | | | | 33,845 | | | | | 43 | | | | | 2,922,484 | | |

| Austria | | 3 | | | | | 92,296 | | | | | 1 | | | | | 58,771 | | | | | 4 | | | | | 151,067 | | |

| Bahrain | | 2 | | | | | 33,659 | | | | | — | | | | | — | | | | | 2 | | | | | 33,659 | | |

| Belarus | | 4 | | | | | 18,472 | | | | | — | | | | | — | | | | | 4 | | | | | 18,472 | | |

| Belgium | | 4 | | | | | 202,106 | | | | | 1 | | | | | 104,391 | | | | | 5 | | | | | 306,497 | | |

| Brazil | | 41 | | | | | 2,813,259 | | | | | 6 | | | | | 291,280 | | | | | 47 | | | | | 3,104,539 | | |

| Bulgaria | | 1 | | | | | 68,889 | | | | | — | | | | | — | | | | | 1 | | | | | 68,889 | | |

| Chile | | 2 | | | | | 6,846 | | | | | 17 | | | | | 667,790 | | | | | 19 | | | | | 674,636 | | |

| China Mainland (including China - Hong Kong S.A.R., China-Taiwan and China-Macau S.A.R.) | | 46 | | | | | 1,960,751 | | | | | 1 | | | | | 20,518 | | | | | 47 | | | | | 1,981,269 | | |

| Colombia | | 21 | | | | | 799,378 | | | | | — | | | | | — | | | | | 21 | | | | | 799,378 | | |

| Croatia | | 2 | | | | | 62,786 | | | | | 1 | | | | | 36,447 | | | | | 3 | | | | | 99,233 | | |

| Cyprus | | 2 | | | | | 51,118 | | | | | 2 | | | | | 46,246 | | | | | 4 | | | | | 97,364 | | |

| Czech Republic | | 7 | | | | | 152,889 | | | | | — | | | | | — | | | | | 7 | | | | | 152,889 | | |

| Denmark | | 3 | | | | | 161,361 | | | | | — | | | | | — | | | | | 3 | | | | | 161,361 | | |

| Egypt | | — | | | | | — | | | | | 1 | | | | | 163,611 | | | | | 1 | | | | | 163,611 | | |

| England | | 66 | | | | | 3,551,854 | | | | | 18 | | | | | 598,009 | | | | | 84 | | | | | 4,149,863 | | |

| Estonia | | 1 | | | | | 38,861 | | | | | — | | | | | — | | | | | 1 | | | | | 38,861 | | |

| Eswatini | | 3 | | | | | 6,997 | | | | | — | | | | | — | | | | | 3 | | | | | 6,997 | | |

| Finland | | 3 | | | | | 95,896 | | | | | — | | | | | — | | | | | 3 | | | | | 95,896 | | |

| France | | 31 | | | | | 2,078,227 | | | | | 12 | | | | | 936,486 | | | | | 43 | | | | | 3,014,713 | | |

| Germany | | 15 | | | | | 698,593 | | | | | 3 | | | | | 308,504 | | | | | 18 | | | | | 1,007,097 | | |

| Greece | | 5 | | | | | 314,894 | | | | | — | | | | | — | | | | | 5 | | | | | 314,894 | | |

| Hungary | | 8 | | | | | 388,033 | | | | | — | | | | | — | | | | | 8 | | | | | 388,033 | | |

| India | | 70 | | | | | 3,147,462 | | | | | — | | | | | — | | | | | 70 | | | | | 3,147,462 | | |

| Indonesia | | 15 | | | | | 485,809 | | | | | 2 | | | | | 58,965 | | | | | 17 | | | | | 544,774 | | |

| Ireland | | 2 | | | | | 118,831 | | | | | 3 | | | | | 158,558 | | | | | 5 | | | | | 277,389 | | |

| Jordan | | — | | | | | — | | | | | 1 | | | | | 24,757 | | | | | 1 | | | | | 24,757 | | |

| Kazakhstan | | 4 | | | | | 46,482 | | | | | — | | | | | — | | | | | 4 | | | | | 46,482 | | |

| Latvia | | 2 | | | | | 50,681 | | | | | — | | | | | — | | | | | 2 | | | | | 50,681 | | |

| Lesotho | | 2 | | | | | 4,736 | | | | | — | | | | | — | | | | | 2 | | | | | 4,736 | | |

| Lithuania | | 2 | | | | | 60,543 | | | | | — | | | | | — | | | | | 2 | | | | | 60,543 | | |

| Malaysia | | 8 | | | | | 443,149 | | | | | — | | | | | — | | | | | 8 | | | | | 443,149 | | |

| Mexico | | 10 | | | | | 478,471 | | | | | 8 | | | | | 585,885 | | | | | 18 | | | | | 1,064,356 | | |

| Morocco | | 6 | | | | | 554,439 | | | | | — | | | | | — | | | | | 6 | | | | | 554,439 | | |

| The Netherlands | | 7 | | | | | 522,687 | | | | | 1 | | | | | 37,355 | | | | | 8 | | | | | 560,042 | | |

| New Zealand | | 6 | | | | | 413,959 | | | | | — | | | | | — | | | | | 6 | | | | | 413,959 | | |

| Northern Ireland | | 3 | | | | | 129,083 | | | | | — | | | | | — | | | | | 3 | | | | | 129,083 | | |

| Norway | | 5 | | | | | 194,321 | | | | | — | | | | | — | | | | | 5 | | | | | 194,321 | | |

| Oman | | 2 | | | | | 60,202 | | | | | — | | | | | — | | | | | 2 | | | | | 60,202 | | |

| Peru | | 3 | | | | | 60,720 | | | | | 10 | | | | | 433,770 | | | | | 13 | | | | | 494,490 | | |

| Philippines | | 9 | | | | | 338,040 | | | | | — | | | | | — | | | | | 9 | | | | | 338,040 | | |

| Poland | | 19 | | | | | 796,561 | | | | | — | | | | | — | | | | | 19 | | | | | 796,561 | | |

| Romania | | 8 | | | | | 451,954 | | | | | — | | | | | — | | | | | 8 | | | | | 451,954 | | |

| Russia | | 42 | | | | | 1,811,370 | | | | | — | | | | | — | | | | | 42 | | | | | 1,811,370 | | |

| Saudi Arabia | | 7 | | | | | 400,687 | | | | | — | | | | | — | | | | | 7 | | | | | 400,687 | | |

| Scotland | | 1 | | | | | 67,191 | | | | | 4 | | | | | 375,294 | | | | | 5 | | | | | 442,485 | | |

| Serbia | | 3 | | | | | 98,876 | | | | | — | | | | | — | | | | | 3 | | | | | 98,876 | | |

| Singapore | | 6 | | | | | 297,581 | | | | | 3 | | | | | 345,056 | | | | | 9 | | | | | 642,637 | | |

| Slovakia | | 5 | | | | | 173,792 | | | | | — | | | | | — | | | | | 5 | | | | | 173,792 | | |

| South Africa | | 16 | | | | | 477,046 | | | | | — | | | | | — | | | | | 16 | | | | | 477,046 | | |

| South Korea | | 8 | | | | | 257,233 | | | | | — | | | | | — | | | | | 8 | | | | | 257,233 | | |

| Spain | | 30 | | | | | 754,667 | | | | | 5 | | | | | 170,707 | | | | | 35 | | | | | 925,374 | | |

| Sweden | | 6 | | | | | 759,793 | | | | | — | | | | | — | | | | | 6 | | | | | 759,793 | | |

| Switzerland | | 12 | | | | | 283,857 | | | | | — | | | | | — | | | | | 12 | | | | | 283,857 | | |

| | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | |

| LEASED | | OWNED | | TOTAL |

| COUNTRY/STATE | NUMBER | | SQUARE FEET | | NUMBER | | SQUARE FEET | | NUMBER | | SQUARE FEET |

| International (Continued) | | | | | | | | | | | | | | | | | | | | | | | |

| Thailand | | 4 | | | | | 267,989 | | | | | 2 | | | | | 105,487 | | | | | 6 | | | | | 373,476 | | |

| Turkey | | 9 | | | | | 683,641 | | | | | — | | | | | — | | | | | 9 | | | | | 683,641 | | |

| Ukraine | | 10 | | | | | 208,050 | | | | | — | | | | | — | | | | | 10 | | | | | 208,050 | | |

| United Arab Emirates | | 10 | | | | | 833,421 | | | | | 1 | | | | | 349,526 | | | | | 11 | | | | | 1,182,947 | | |

| Vietnam | | 1 | | | | | 54,767 | | | | | — | | | | | — | | | | | 1 | | | | | 54,767 | | |

| Total International | | 669 | | | | | 32,422,360 | | | | | 109 | | | | | 6,210,122 | | | | | 778 | | | | | 38,632,482 | | |

| Total | | 1,184 | | | | | 69,746,261 | | | | | 263 | | | | | 24,882,861 | | | | | 1,447 | | | | | 94,629,122 | | |

The leased facilities typically have initial lease terms of five to 10 years with one or more renewal options. In addition, some of the leases contain either a purchase option or a right of first refusal upon the sale of the property. We believe that the space available in our facilities is adequate to meet our current needs, although future growth may require that we lease or purchase additional real property.

Our total building utilization and total racking utilization by region as of December 31, 2021 in Records Management and Data Management are as follows:

| | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | RECORDS MANAGEMENT(1) | | DATA MANAGEMENT |

| REGION | | BUILDING

UTILIZATION | | RACKING

UTILIZATION | | BUILDING

UTILIZATION | | RACKING

UTILIZATION |

| North America | | 80% | | 87% | | 58% | | 66% |

| Europe | | 85% | | 91% | | 40% | | 59% |

| Latin America | | 87% | | 90% | | 73% | | 75% |

| Asia | | 84% | | 92% | | 58% | | 70% |

| Total | | 82% | | 89% | | 55% | | 66% |

(1)Total building utilization and total racking utilization for Records Management includes the utilization for GDS and Consumer Storage.

See Note 2.i. to Notes to Consolidated Financial Statements included in this Exhibit 99.1 to this Current Report for information regarding our minimum annual lease commitments as a lessee.

See Schedule III—Schedule of Real Estate and Accumulated Depreciation in this Exhibit 99.1 to this Current Report for information regarding the cost, accumulated depreciation and encumbrances associated with our owned real estate.

The following table sets forth a summary of the lease expirations for leases in place related to our Global Data Center Business, for which we are the lessor, as of December 31, 2021. The information set forth in the table assumes that tenants exercise no renewal options and all early termination rights.

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| YEAR | | NUMBER OF LEASES EXPIRING | | TOTAL MEGAWATTS

EXPIRING | | PERCENTAGE

OF TOTAL MEGAWATTS

EXPIRING | | ANNUALIZED

TOTAL CONTRACT

RENT EXPIRING

(IN THOUSANDS) | | PERCENTAGE OF

TOTAL CONTRACT

VALUE ANNUALIZED

RENT |

| 2022 | | 556 | | | 15.1 | | | 8.4 | % | | $ | 47,646 | | | 14.7 | % |

| 2023 | | 350 | | | 22.7 | | | 12.6 | % | | 63,540 | | | 19.6 | % |

| 2024 | | 237 | | | 12.9 | | | 7.2 | % | | 32,704 | | | 10.1 | % |

| 2025 | | 77 | | | 20.0 | | | 11.1 | % | | 43,748 | | | 13.5 | % |

| 2026 | | 63 | | | 20.0 | | | 11.1 | % | | 33,746 | | | 10.4 | % |

| 2027 | | 10 | | | 3.2 | | | 1.8 | % | | 6,429 | | | 2.0 | % |

| 2028 | | 13 | | | 37.7 | | | 20.9 | % | | 47,216 | | | 14.6 | % |

| Thereafter | | 14 | | | 48.5 | | | 26.9 | % | | 48,715 | | | 15.1 | % |

| Total | | 1,320 | | | 180.1 | | | 100.0 | % | | $ | 323,744 | | | 100.0 | % |

PART II

ITEM 7. MANAGEMENT'S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS.

The following discussion should be read in conjunction with the Consolidated Financial Statements and Notes thereto and the other financial and operating information included elsewhere in this Exhibit 99.1 to this Current Report.

This discussion contains “forward-looking statements” as that term is defined in the Private Securities Litigation Reform Act of 1995 and in other securities laws. See “Cautionary Note Regarding Forward-Looking Statements” on page iii of our Annual Report on Form 10-K, filed with the SEC on February 24, 2022 (our “Original Annual Report”) and “Item 1A. Risk Factors” beginning on page 9 of our Original Annual Report.

OVERVIEW

COVID-19

In March 2020, the World Health Organization declared a novel strain of coronavirus (“COVID-19”) a pandemic. While we have broad geographic and customer diversification with operations in 63 countries and no single customer accounting for more than approximately 1% of revenue during the year ended December 31, 2021, COVID-19 is a global pandemic impacting numerous industries and geographies. While our service operations have increased from the reductions we experienced during the first and second quarter of 2020, future service revenues remain uncertain and will be dependent on the severity of the COVID-19 pandemic, including new variants of COVID-19 that may emerge.

PROJECT SUMMIT

In October 2019, we announced Project Summit, our global program designed to better position us for future growth and achievement of our strategic objectives. As of December 31, 2021, we have completed Project Summit. As a result of the program we have simplified our global structure, rebalanced resources to focus on higher growth areas, realigned our management structure to create a more dynamic, agile organization, made investments to enhance the customer experience and leveraged new technology solutions that enabled us to modernize our service delivery model and more efficiently utilize our fleet, labor and real estate. Project Summit has improved annual Adjusted EBITDA (as defined below) by approximately $375.0 million exiting 2021, of which approximately $160.0 million and $165.0 million were realized in 2021 and 2020, respectively, with the remainder to come in 2022.

| | | | | | | | |

| 2021 | | $160 million |

| Exiting 2021 | | $375 million |

The implementation of Project Summit resulted in total operating expenditures ("Restructuring Charges") of approximately $450.0 million that primarily consisted of: (1) employee severance costs; (2) internal costs associated with the development and implementation of Project Summit initiatives; (3) professional fees, primarily related to third party consultants who assisted with the design and execution of various initiatives as well as project management activities and (4) system implementation and data conversion costs. The following table presents (in millions) total Restructuring Charges related to Project Summit from the inception of Project Summit through December 31, 2021 and for the years ended December 31, 2021, 2020 and 2019:

| | | | | | |

From the Inception of

Project Summit through

December 31, 2021 | | |

For the Year Ended

December 31, 2021 | | |

For the Year Ended

December 31, 2020 | | |

For the Year Ended

December 31, 2019 | | |

We have also incurred approximately $33.8 million in capital expenditures related to Project Summit from the inception of Project Summit through December 31, 2021.

DIVESTMENTS

INTELLECTUAL PROPERTY MANAGEMENT BUSINESS

On June 7, 2021, we sold our Intellectual Property Management ("IPM") business, also known as our technology escrow services business, which we predominantly operated in the United States, for total gross consideration of approximately $215.4 million (the “IPM Divestment”). As a result of the IPM Divestment, we recorded a gain on sale of approximately $179.0 million to Other (income) expense, net, during the year ended December 31, 2021, the substantial majority of which was recorded during the second quarter of 2021, representing the excess of the fair value of the consideration received over the sum of the carrying value of the IPM business. Our IPM business represented approximately $14.2 million, $32.8 million and $33.2 million of total revenues for the years ended December 31, 2021, 2020 and 2019, respectively, and approximately $6.8 million, $16.0 million and $17.2 million of total net income for the years ended December 31, 2021, 2020 and 2019, respectively.

IRON MOUNTAIN CONSUMER STORAGE

In March 2019, we contributed our customer contracts and certain intellectual property and other assets used by us to operate our consumer storage business in the United States and Canada (the “IM Consumer Storage Assets”) and approximately $20.0 million in cash (gross of certain transaction expenses) (the “Cash Contribution”) to a strategic partnership (the “MakeSpace JV”) established by us and MakeSpace Labs, Inc. (“MakeSpace”) pursuant to a transaction which closed on March 19, 2019 (the "Consumer Storage Transaction"). Upon the closing of the Consumer Storage Transaction, the MakeSpace JV owned (i) the IM Consumer Storage Assets, (ii) the Cash Contribution and (iii) the customer contracts, intellectual property and certain other assets used by MakeSpace to operate its consumer storage business in the United States. As part of the Consumer Storage Transaction, we received an initial equity interest of approximately 34% in the MakeSpace JV (the “MakeSpace Investment”). In the second quarter of 2020, we committed to participate in a round of equity funding for the MakeSpace JV whereby we contributed $36.0 million of the $45.0 million being raised in installments between May 2020 through October 2021. At December 31, 2021, we owned 49.99% of the outstanding equity in the MakeSpace JV.

In connection with the Consumer Storage Transaction and the MakeSpace Investment, we also entered into a storage and service agreement with the MakeSpace JV to provide certain storage and related services to the MakeSpace JV (the “MakeSpace Agreement”). Revenues and expenses associated with the MakeSpace Agreement are presented as a component of our Global RIM Business segment. During the years ended December 31, 2021, 2020 and 2019, we recognized revenue of approximately $34.7 million, $33.6 million and $22.5 million, respectively, associated with the MakeSpace Agreement.

As a result of the Consumer Storage Transaction, we recorded a gain on sale of approximately $4.2 million to Other (income) expense, net, during the first quarter of 2019, representing the excess of the fair value of the consideration received over the sum of the carrying value of our consumer storage operations and (ii) the Cash Contribution.

________________________________________________________

As described in Note 4 to Notes to Consolidated Financial Statements included in this Exhibit 99.1 to this Current Report, we have concluded that the divestments of IPM and the IM Consumer Storage Assets in the Consumer Storage Transaction do not meet the criteria to be reported as discontinued operations in our consolidated financial statements.

GENERAL

RESULTS OF OPERATIONS - KEY TRENDS

•In spite of the COVID-19 pandemic, we have experienced relatively steady volume in our Global RIM Business segment, with organic storage rental revenue growth driven primarily by revenue management. We expect organic storage rental revenue growth to benefit from revenue management and volume to be relatively stable in the near term.

•Our organic service revenue growth is primarily due to increases in our service activity, particularly in regions where governments have lifted or eased COVID-19-related restrictions on our customers’ non-essential business operations. We expect organic service revenue growth in 2022 to benefit from our new and existing digital offerings.

•We expect revenue and Adjusted EBITDA growth to accelerate in 2022 with continued focus on new product and service offerings, innovation, customer solutions and market expansion.

Our revenues consist of storage rental revenues as well as service revenues and are reflected net of sales and value-added taxes. Storage rental revenues, which are considered a key driver of financial performance for the storage and information management services industry, consist primarily of recurring periodic rental charges related to the storage of materials or data (generally on a per unit basis) that are typically retained by customers for many years and revenues associated with our data center operations. Service revenues include charges for related service activities, the most significant of which include: (1) the handling of records, including the addition of new records, temporary removal of records from storage, refiling of removed records, customer termination and permanent withdrawal fees, project revenues, and courier operations, consisting primarily of the pickup and delivery of records upon customer request; (2) destruction services, consisting primarily of secure shredding of sensitive documents and the subsequent sale of shredded paper for recycling, the price of which can fluctuate from period to period; (3) digital solutions, including the scanning, imaging and document conversion services of active and inactive records, and consulting services; and (4) data center services, including set up, monitoring and support of our customers' assets which are protected in our data center facilities, and special project services, including data center fitout. Our service revenue growth has been negatively impacted by declining activity rates as stored records are becoming less active. While customers continue to store their records and tapes with us, they are less likely than they have been in the past to retrieve records for research and other purposes, thereby reducing service activity levels.

BREAKDOWN OF REVENUES

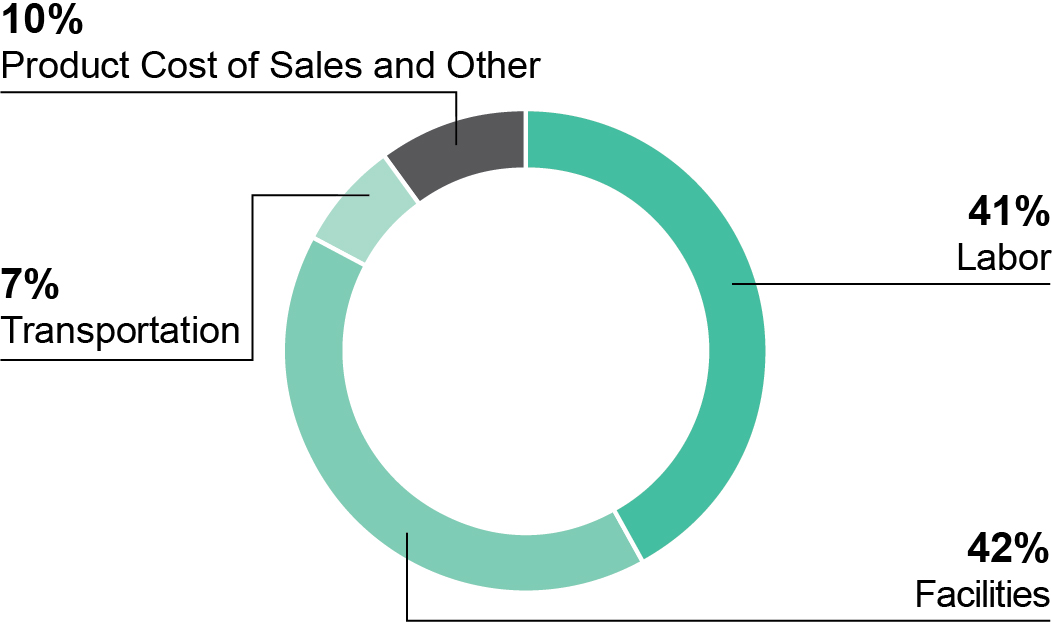

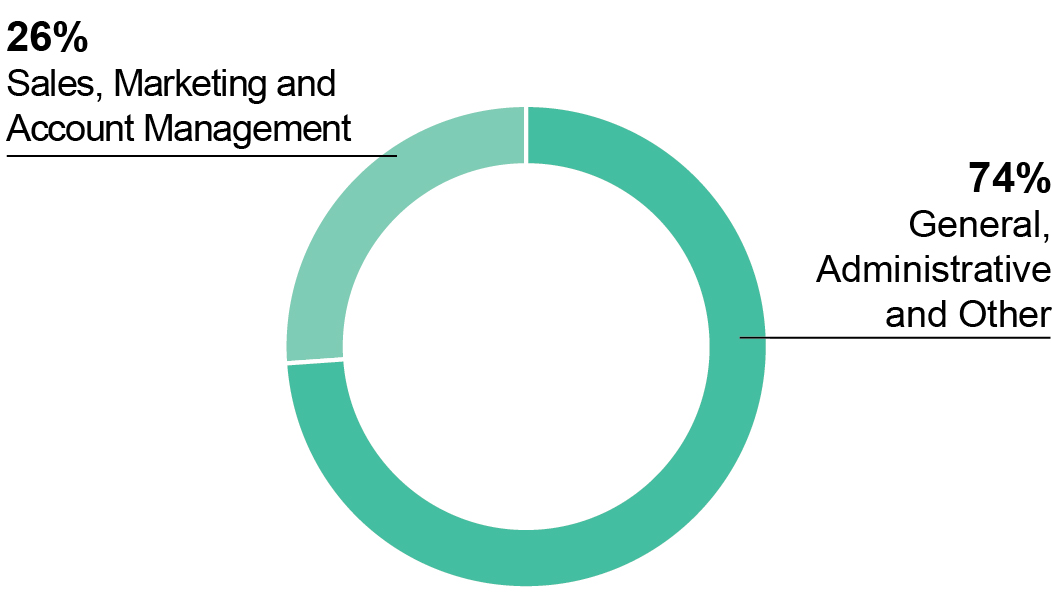

Cost of sales (excluding depreciation and amortization) consists primarily of labor, including wages and benefits for field personnel, facility occupancy costs (including rent and utilities), transportation expenses (including vehicle leases and fuel), other product cost of sales and other equipment costs and supplies. Of these, labor and facility occupancy costs are the most significant. Selling, general and administrative expenses consist primarily of wages and benefits for management, administrative, IT, sales, account management and marketing personnel, as well as expenses related to communications and data processing, travel, professional fees, bad debts, training, office equipment and supplies.

Cost of sales (excluding depreciation and amortization) and Selling, general and administrative expenses for the year ended December 31, 2021 consists of the following:

| | | | | | | | |

| COST OF SALES | | SELLING, GENERAL AND ADMINISTRATIVE EXPENSES |

| | |

| | | | | |

| |

Trends in facility occupancy costs are impacted by: •the total number of facilities we occupy; •the mix of properties we own versus properties we lease; •fluctuations in per square foot occupancy costs; and •the levels of utilization of these properties. Trends in total wages and benefits in dollars and as a percentage of total consolidated revenue are influenced by: •changes in headcount and compensation levels; •achievement of incentive compensation targets; •workforce productivity; and •variability in costs associated with medical insurance and workers’ compensation. The expansion of our international businesses has impacted the major cost of sales components and selling, general and administrative expenses. •Our international operations are more labor intensive relative to revenue than our operations in North America and, therefore, labor costs are a higher percentage of international operational revenue. •The overhead structure of our expanding international operations has generally not achieved the same level of overhead leverage as our North American operations, which may result in an increase in selling, general and administrative expenses as a percentage of consolidated revenue as our international operations become a larger percentage of our consolidated results. | |

| |

Our depreciation and amortization charges result primarily from depreciation related to storage systems, which include racking structures, buildings, building and leasehold improvements and computer systems hardware and software. Amortization relates primarily to customer relationship intangible assets, contract fulfillment costs and data center lease-based intangible assets. Both depreciation and amortization are impacted by the timing of acquisitions.

Our consolidated revenues and expenses are subject to the net effect of foreign currency translation related to our operations outside the United States. It is difficult to predict the future fluctuations of foreign currency exchange rates and how those fluctuations will impact our Consolidated Statements of Operations. As a result of the relative size of our international operations, these fluctuations may be material on individual balances. Our revenues and expenses from our international operations are generally denominated in the local currency of the country in which they are derived or incurred. Therefore, the impact of currency fluctuations on our operating income and operating margin is partially mitigated. In order to provide a framework for assessing how our underlying businesses performed excluding the effect of foreign currency fluctuations, we compare the percentage change in the results from one period to another period in this report using constant currency presentation. The constant currency growth rates are calculated by translating the 2020 results at the 2021 average exchange rates and the 2019 results at the 2020 average exchange rates. Constant currency growth rates are a non-GAAP measure.

The following table is a comparison of underlying average exchange rates of the foreign currencies that had the most significant impact on our United States dollar-reported revenues and expenses:

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | PERCENTAGE OF

UNITED STATES DOLLAR-

REPORTED REVENUE FOR THE

YEAR ENDED DECEMBER 31, | | AVERAGE EXCHANGE RATES

FOR THE YEAR ENDED

DECEMBER 31, | | PERCENTAGE

STRENGTHENING /

(WEAKENING) OF

FOREIGN CURRENCY |

| | 2021 | | 2020 | | 2021 | | 2020 |

| Australian dollar | 3.3 | % | | 3.2 | % | | $ | 0.751 | | | $ | 0.690 | | | 8.8 | % |

| Brazilian real | 1.8 | % | | 1.9 | % | | $ | 0.186 | | | $ | 0.196 | | | (5.1) | % |

| British pound sterling | 6.6 | % | | 6.0 | % | | $ | 1.376 | | | $ | 1.283 | | | 7.2 | % |

| Canadian dollar | 5.6 | % | | 5.4 | % | | $ | 0.798 | | | $ | 0.746 | | | 7.0 | % |

| Euro | 7.7 | % | | 7.5 | % | | $ | 1.183 | | | $ | 1.141 | | | 3.7 | % |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | PERCENTAGE OF

UNITED STATES DOLLAR-

REPORTED REVENUE FOR THE

YEAR ENDED DECEMBER 31, | | AVERAGE EXCHANGE RATES

FOR THE YEAR ENDED

DECEMBER 31, | | PERCENTAGE

STRENGTHENING /

(WEAKENING) OF

FOREIGN CURRENCY |

| | 2020 | | 2019 | | 2020 | | 2019 |

| Australian dollar | 3.2 | % | | 3.4 | % | | $ | 0.690 | | | $ | 0.695 | | | (0.7) | % |

| Brazilian real | 1.9 | % | | 2.6 | % | | $ | 0.196 | | | $ | 0.254 | | | (22.8) | % |

| British pound sterling | 6.0 | % | | 6.4 | % | | $ | 1.283 | | | $ | 1.277 | | | 0.5 | % |

| Canadian dollar | 5.4 | % | | 5.7 | % | | $ | 0.746 | | | $ | 0.754 | | | (1.1) | % |

| Euro | 7.5 | % | | 7.4 | % | | $ | 1.141 | | | $ | 1.120 | | | 1.9 | % |

The percentage of United States dollar-reported revenues for all other foreign currencies was 14.6%, 13.8% and 12.7% for the years ended December 31, 2021, 2020 and 2019, respectively.

NON-GAAP MEASURES

ADJUSTED EBITDA

Adjusted EBITDA is defined as income (loss) from continuing operations before interest expense, net, provision (benefit) for income taxes, depreciation and amortization (inclusive of our share of Adjusted EBITDA from our unconsolidated joint ventures), and excluding certain items we do not believe to be indicative of our core operating results, specifically:

| | | | | |

| |

| EXCLUDED | |

•Acquisition and Integration Costs •Restructuring Charges •Intangible impairments •(Gain) loss on disposal/write-down of property, plant and equipment, net (including real estate)

| •Other (income) expense, net •Stock-based compensation expense •COVID-19 Costs (as defined below)

|

| |

Adjusted EBITDA Margin is calculated by dividing Adjusted EBITDA by total revenues. We also show Adjusted EBITDA and Adjusted EBITDA Margin for each of our reportable operating segments under “Results of Operations – Segment Analysis” below.

Adjusted EBITDA excludes both interest expense, net and the provision (benefit) for income taxes. These expenses are associated with our capitalization and tax structures, which we do not consider when evaluating the operating profitability of our core operations. Adjusted EBITDA also does not include depreciation and amortization expenses, in order to eliminate the impact of capital investments, which we evaluate by comparing capital expenditures to incremental revenue generated and as a percentage of total revenues. Adjusted EBITDA and Adjusted EBITDA Margin should be considered in addition to, but not as a substitute for, other measures of financial performance reported in accordance with accounting principles generally accepted in the United States of America (“GAAP”), such as operating income, income (loss) from continuing operations, net income (loss) or cash flows from operating activities from continuing operations (as determined in accordance with GAAP).

RECONCILIATION OF INCOME (LOSS) FROM CONTINUING OPERATIONS TO ADJUSTED EBITDA (IN THOUSANDS):

| | | | | | | | | | | | | | | | | |

| | | | | |

| | YEAR ENDED DECEMBER 31, |

| | 2021 | | 2020 | | 2019 |

| Income (Loss) from Continuing Operations | $ | 452,725 | | | $ | 343,096 | | | $ | 268,211 | |

| Add/(Deduct): | | | | | |

| Interest expense, net | 417,961 | | | 418,535 | | | 419,298 | |

| Provision (benefit) for income taxes | 176,290 | | | 29,609 | | | 59,931 | |

| Depreciation and amortization | 680,422 | | | 652,069 | | | 658,201 | |

| Acquisition and Integration Costs | 12,764 | | | — | | | 13,293 | |

| Restructuring Charges | 206,426 | | | 194,396 | | | 48,597 | |

| Intangible impairments | — | | | 23,000 | | | — | |

| (Gain) loss on disposal/write-down of property, plant and equipment, net (including real estate) | (172,041) | | | (363,537) | | | (63,824) | |

Other (income) expense, net, excluding our share of losses (gains) from our unconsolidated joint ventures(1) | (205,746) | | | 133,611 | | | 25,720 | |

| Stock-based compensation expense | 61,001 | | | 34,272 | | | 36,194 | |

COVID-19 Costs(2) | — | | | 9,285 | | | — | |

| Our share of Adjusted EBITDA reconciling items from our unconsolidated joint ventures | 4,897 | | | 1,385 | | | 3,388 | |

| Adjusted EBITDA | $ | 1,634,699 | | | $ | 1,475,721 | | | $ | 1,469,009 | |

(1)Includes foreign currency transaction losses (gains), net, debt extinguishment expense and other, net. See Note 2.u. to Notes to Consolidated Financial Statements included in this Exhibit 99.1 to this Current Report for additional information regarding the components of Other (income) expense, net.

(2)Costs that are incremental and directly attributable to the COVID-19 pandemic which are not expected to recur once the pandemic ends (“COVID-19 Costs”). These costs include the purchase of personal protective equipment for our employees and incremental cleaning costs of our facilities, among other direct costs.

ADJUSTED EPS

Adjusted EPS is defined as reported earnings per share fully diluted from continuing operations (inclusive of our share of adjusted losses (gains) from our unconsolidated joint ventures) and excluding certain items, specifically:

| | | | | |

| |

| EXCLUDED | |

•Acquisition and Integration Costs •Restructuring Charges •Intangible impairments •(Gain) loss on disposal/write-down of property, plant and equipment, net (including real estate)

| •Other (income) expense, net •Stock-based compensation expense •COVID-19 Costs •Tax impact of reconciling items and discrete tax items |

| |

We do not believe these excluded items to be indicative of our ongoing operating results, and they are not considered when we are forecasting our future results. We believe Adjusted EPS is of value to our current and potential investors when comparing our results from past, present and future periods.

RECONCILIATION OF REPORTED EPS—FULLY DILUTED FROM CONTINUING OPERATIONS TO ADJUSTED EPS—FULLY DILUTED FROM CONTINUING OPERATIONS:

| | | | | | | | | | | | | | | | | |

| | | | | |

| | YEAR ENDED DECEMBER 31, |

| | 2021 | | 2020 | | 2019 |

| Reported EPS—Fully Diluted from Continuing Operations | $ | 1.55 | | | $ | 1.19 | | | $ | 0.93 | |

| Add/(Deduct): | | | | | |

| Acquisition and Integration Costs | 0.04 | | | — | | | 0.05 | |

| Restructuring Charges | 0.71 | | | 0.67 | | | 0.17 | |

| Intangible impairments | — | | | 0.08 | | | — | |

| (Gain) loss on disposal/write-down of property, plant and equipment, net (including real estate) | (0.59) | | | (1.26) | | | (0.22) | |

| Other (income) expense, net, excluding our share of losses (gains) from our unconsolidated joint ventures | (0.71) | | | 0.46 | | | 0.09 | |

| Stock-based compensation expense | 0.21 | | | 0.12 | | | 0.13 | |

COVID-19 Costs(1) | — | | | 0.03 | | | — | |

| | | | | |

Tax impact of reconciling items and discrete tax items(2) | 0.28 | | | (0.11) | | | (0.03) | |

| Income (loss) Attributable to Noncontrolling Interests | 0.01 | | | — | | | — | |

Adjusted EPS—Fully Diluted from Continuing Operations(3) | $ | 1.51 | | | $ | 1.19 | | | $ | 1.11 | |

(1)These costs include the purchase of personal protective equipment for our employees and incremental cleaning costs of our facilities, among other direct costs.

(2)The difference between our effective tax rate and our structural tax rate (or adjusted effective tax rate) for the years ended December 31, 2021, 2020, and 2019 is primarily due to (i) the reconciling items above, which impact our reported income (loss) from continuing operations before provision (benefit) for income taxes but have an insignificant impact on our reported provision (benefit) for income taxes and (ii) other discrete tax items. Our structural tax rate for purposes of the calculation of Adjusted EPS for the years ended December 31, 2021, 2020 and 2019 was 17.7%, 15.1%, and 17.6%, respectively.

(3)Columns may not foot due to rounding.

FFO (NAREIT) AND FFO (NORMALIZED)

Funds from operations ("FFO") is defined by the National Association of Real Estate Investment Trusts (“Nareit”) as net income (loss) excluding depreciation on real estate assets, gains on sale of real estate, net of tax, and amortization of data center leased-based intangibles. FFO (Nareit) does not give effect to real estate depreciation because these amounts are computed, under GAAP, to allocate the cost of a property over its useful life. Because values for well-maintained real estate assets have historically increased or decreased based upon prevailing market conditions, we believe that FFO (Nareit) provides investors with a clearer view of our operating performance. Our most directly comparable GAAP measure to FFO (Nareit) is net income (loss).

Although Nareit has published a definition of FFO, we modify FFO (Nareit), as is common among REITs seeking to provide financial measures that most meaningfully reflect their particular business ("FFO (Normalized)"). Our definition of FFO (Normalized) excludes certain items included in FFO (Nareit) that we believe are not indicative of our core operating results, specifically:

| | | | | |

| |

| EXCLUDED | |

•Acquisition and Integration Costs •Restructuring Charges •Intangible impairments •(Gain) loss on disposal/write-down of property, plant and equipment, net (excluding real estate) •Other (income) expense, net | •Stock-based compensation expense •COVID-19 Costs •Real estate financing lease depreciation •Tax impact of reconciling items and discrete tax items •(Income) loss from discontinued operations, net of tax

|

| |

RECONCILIATION OF NET INCOME (LOSS) TO FFO (NAREIT) AND FFO (NORMALIZED) (IN THOUSANDS):

| | | | | | | | | | | | | | | | | | | | | |

| YEAR ENDED DECEMBER 31, | | | | |

| 2021 | | 2020 | | 2019 | | | | |

| Net Income (Loss) | $ | 452,725 | | | $ | 343,096 | | | $ | 268,315 | | | | | |

| Add/(Deduct): | | | | | | | | | |

Real estate depreciation(1) | 307,717 | | | 298,943 | | | 303,415 | | | | | |

Gain on sale of real estate, net of tax(2) | (142,892) | | | (365,709) | | | (99,194) | | | | | |

Data center lease-based intangible assets amortization(3) | 42,333 | | | 42,637 | | | 46,696 | | | | | |

| Our share of FFO (Nareit) reconciling items from our unconsolidated joint ventures | — | | | — | | | 1,284 | | | | | |

| FFO (Nareit) | 659,883 | | | 318,967 | | | 520,516 | | | | | |

| Add/(Deduct): | | | | | | | | | |

| Acquisition and Integration Costs | 12,764 | | | — | | | 13,293 | | | | | |

| Restructuring Charges | 206,426 | | | 194,396 | | | 48,597 | | | | | |

| Intangible impairments | — | | | 23,000 | | | — | | | | | |

| (Gain) loss on disposal/write-down of property, plant and equipment, net (excluding real estate) | (3,751) | | | 2,523 | | | 40,763 | | | | | |

Other (income) expense, net, excluding our share of losses (gains) from our unconsolidated joint ventures(4) | (205,746) | | | 133,611 | | | 25,720 | | | | | |

| Stock-based compensation expense | 61,001 | | | 34,272 | | | 36,194 | | | | | |

COVID-19 Costs(5) | — | | | 9,285 | | | — | | | | | |

| Real estate financing lease depreciation | 14,635 | | | 13,801 | | | 13,364 | | | | | |

Tax impact of reconciling items and discrete tax items(6) | 56,822 | | | (31,825) | | | (13,095) | | | | | |

| (Income) loss from discontinued operations, net of tax | — | | | — | | | (104) | | | | | |

| Our share of FFO (Normalized) reconciling items from our unconsolidated joint ventures | (38) | | | (38) | | | 148 | | | | | |

| FFO (Normalized) | $ | 801,996 | | | $ | 697,992 | | | $ | 685,396 | | | | | |

(1)Includes depreciation expense related to owned real estate assets (land improvements, buildings, building improvements, leasehold improvements and racking), excluding depreciation related to real estate financing leases.

(2)Tax expense associated with the gain on sale of real estate for the years ended December 31, 2021, 2020, and 2019, was $25.4 million, $0.4 million, and $5.4 million, respectively.

(3)Includes amortization expense for Data Center In-Place Lease Intangible Assets and Data Center Tenant Relationship Intangible Assets as defined in Note 2.l. to Notes to Consolidated Financial Statements included in this Exhibit 99.1 to this Current Report.

(4)Includes foreign currency transaction (gains) losses, net, debt extinguishment expense and other, net. See Note 2.u. to Notes to Consolidated Financial Statements included in this Exhibit 99.1 to this Current Report for additional information regarding the components of Other (income) expense, net.

(5)These costs include the purchase of personal protective equipment for our employees and incremental cleaning costs of our facilities, among other direct costs.

(6)Represents the tax impact of (i) the reconciling items above, which impacts our reported income (loss) from continuing operations before provision (benefit) for income taxes but has an insignificant impact on our reported provision (benefit) for income taxes and (ii) other discrete tax items. Discrete tax items resulted in a provision (benefit) for income taxes of $19.2 million, $(16.8) million and $(1.5) million for the years ended December 31, 2021, 2020 and 2019, respectively.

CRITICAL ACCOUNTING ESTIMATES

Our discussion and analysis of our financial condition and results of operations are based upon our Consolidated Financial Statements, which have been prepared in accordance with GAAP. The preparation of these financial statements requires us to make estimates, judgments and assumptions that affect the reported amounts of assets, liabilities, revenues and expenses, and related disclosure of contingent assets and liabilities at the date of the financial statements and for the period then ended. On an ongoing basis, we evaluate the estimates used. We base our estimates on historical experience, actuarial estimates, current conditions and various other assumptions that we believe to be reasonable under the circumstances. These estimates form the basis for making judgments about the carrying values of assets and liabilities and are not readily apparent from other sources. Actual results may differ from these estimates. The following should be read in conjunction with Note 2 to Notes to Consolidated Financial Statements included in this Exhibit 99.1 to this Current Report, which provides a summary of our significant accounting policies. Our critical accounting estimates include the following, which are listed in no particular order:

REVENUE RECOGNITION

Revenue is recognized when or as control of promised goods or services is transferred to the customer, in an amount that reflects the consideration we expect to be entitled to in exchange for those goods or services. See Note 2.r. to Notes to Consolidated Financial Statements included in this Exhibit 99.1 to this Current Report for additional details on our revenue recognition policies. Revenue for all our lines of business, with the exception of storage revenues in our Global Data Center Business (which is subject to leasing guidance), is recognized in accordance with Accounting Standards Codification ("ASC") 606, Revenue from Contracts with Customers (“ASC 606”), the application of which requires that we make estimates and judgements that may affect the amount and timing of revenue we recognize.

We have determined that the majority of our contracts contain series performance obligations which qualify to be recognized under a practical expedient available in ASC 606 known as the “right to invoice.” This determination allows variable consideration in such contracts to be allocated to and recognized in the period to which the consideration relates, which is typically the period in which it is billed, rather than requiring estimation of variable consideration at the inception of the contract.

From time to time, we make payments to entities that are also customers under a revenue contract. These payments are comprised of Customer Inducements (as defined in Note 2.l. to Notes to Consolidated Financial Statements included in this Exhibit 99.1 to this Current Report). Consideration payable to a customer is treated as a reduction of the transaction price over periods ranging from one to 10 years. If the payment to the customer does not represent payment for a distinct service, revenue is recognized only up to the amount of consideration remaining after customer payment obligations are considered.

Contract Fulfillment Costs are amortized over a three year term, which we have determined is consistent with the transfer of the underlying performance obligations to which the assets relate. Different determinations on term length would result in differences in the amount and timing of amortization expense recognized.

ACCOUNTING FOR ACQUISITIONS