Minco GOLD Corporation

Management’s Discussion and Analysis

For the three and six months ended June 30, 2014

This Management’s Discussion and Analysis (“MD&A”) of Minco Gold Corporation (“we”, “our”, “us”, “Minco Gold” or the “Company”) has been prepared on the basis of available information up to August 13, 2014, should be read in conjunction with the unaudited condensed consolidated interim financial statements and notes thereto prepared by management for the three and six months ended June 30, 2014 and the audited consolidated financial statements and related notes for the year ended December 31, 2013. The Company’s condensed consolidated interim financial statements have been prepared in accordance with International Financial Reporting Standards (“IFRS”) as issued by the International Accounting Standards Board (“IASB”) applicable to the preparation of interim financial statements, including IAS 34, Interim Financial Reporting. All references to "$" and "dollars" are to Canadian dollars, all references to “US$” are United States dollars and all references to "RMB" are to Chinese Renminbi.

Additional information, including the audited consolidated financial statements for the year ended December 31, 2013, and the MD&A and annual report on Form 20-F for the same period, is available under the Company's profile on SEDAR at www.sedar.com. The Company’s audit committee reviews the condensed consolidated interim financial statements and MD&A, and recommends approval to the Company’s board of directors.

Minco Gold (TSX: MMM/NYSE MKT: MGH/FSE: MI5) was incorporated in 1982 under the laws of British Columbia, Canada as Caprock Energy Ltd. The Company changed its name to Minco Gold in 2007. The principal business activities of the Company include the acquisition, exploration and development of gold properties.

The Company’s subsidiaries are as follows:

Our wholly-owned subsidiaries include:Minco Mining (China) Co., Ltd. (“Minco China”), Yuanling Minco Mining Ltd (“Yuanling Minco”)., Huaihua Tiancheng Mining Ltd. (“Huaihua Tiancheng), Minco Resource Limited.

The Company, through Minco China, established Tibet Minco on January 29, 2013 for the purpose of potential future transactions.

The Company, indirectly through Minco China and Tibet Minco, owns a 51% interest in a company formed and known as Guangdong Mingzhong Mining Co., Ltd. (“Mingzhong”), which holds the Changkeng Gold property and the Changkeng Exploration Permit.

As at June 30, 2014, the Company owned a 18.45% equity interest in Minco Silver Corporation ("Minco Silver"), a publicly traded company listed on the Toronto Stock Exchange, which through its subsidiary holds title to the Fuwan Silver Project located in Guangdong Province, P.R China.

As at the date of this MD&A, the Company had 50,498,215 common shares and 6,581,167 stock options outstanding, for a total of 57,079,382 common shares outstanding, on a fully diluted basis.

Table of Contents

| 1. | Highlights for the Period |

| 2. | Projects and Equity Investment in Minco Silver |

| 4. | Summary of Quarterly Results |

| 5. | Liquidity and Capital Resource |

| 6. | Off – Balance Sheet Arrangements |

| 7. | Transactions with Related Parties |

| 8. | Critical Accounting Estimates |

| 9. | Adoption of New Accounting Standard |

| 11. | Risk Factors and Uncertainties |

| 12. | Disclosure Controls and Procedures and Internal Controls over Financing Reporting |

| 13. | Cautionary Statement on Forward Looking Information |

| 1. | | Highlights for the Period |

During the six months ended June 30, 2014, the Company has compiled and analyzed the exploration data from last year’s exploration program on the Baimashi area of the Yejiaba project, which is located in the Wudu district of Gansu Province, China. Six drilling targets have been identified, and the Company started the drilling program in early July 2014 on the Baimashi area.

During the six months ended June 30, 2014, Mingzhong started a metallurgical test on the Changkeng Gold project.

On April 22, 2014, the Company sold 2,000,000 shares of Minco Silver for the cash proceeds of $1,500,000. As a result of this transaction, the Company recognized a loss on partial disposition of its investment in Minco Silver of $399,536. Upon disposition of the 2,000,000 shares, the Company concluded that it no longer had significant influence over Minco Silver, as we did not own more than 20% of Minco Silver’s outstanding common shares, and therefore, equity accounting was no longer applicable resulting in a loss on derecognition of investment in Minco Silver of $1,647,446. The investment in Minco Silver was subsequently classified as available-for-sale financial asset.

In its continuing efforts to dispose of its non-core assets, Minco China entered into a sale agreement on June 28, 2014 to dispose of its interest in Yuanling Minco for RMB 7 million ($1.2 million). Yuanling Minco’s wholly owned subsidiary Huaihua Tiancheng owns the Gold Bull Mountain exploration permit. As at June 30, 2014, the process of transferring the titles of Yuanling Minco was pending approval by governing authorities and the assets and liabilities have been presented as held for sale on the condensed interim statements of financial position.

| 2. | | Projects and Equity Investment in Minco Silver |

The following is a brief discussion of the properties that Minco Gold holds through its subsidiaries and its equity investment in the Fuwan Silver Project of Minco Silver. Information of a technical or scientific nature respecting the Company's mineral properties ("Technical Information") is primarily derived from the documents referenced herein. Technical Information which appears in this MD&A has been reviewed and approved by Thomas Wayne Spilsbury, an independent director of Minco Silver, in which the Company owned a 18.45% equity interest as at June 30, 2014. Mr. Spilsbury is a Member of the Association of Professional Engineers and Geoscientists of British Columbia (P Geo), a Member of the Australian Institute of Geoscientists and a Fellow of the Australasian Institute of Mining and Metallurgy CP (Geo) and is a "qualified person", as defined in NI 43-101. The Company operates quality assurance and quality control of sampling and analytical procedures.

All sample length information that follows refers to reported sample length; the lengths reported may not necessarily represent true thickness of the mineralization.

The following is a brief description of the Company's Longnan Properties. Technical Information respecting the Company's Yejiaba Project appearing in this MD&A has been primarily derived from the NI 43-101 compliant technical report entitled "Independent Technical Report on the Yejiaba Gold-Polymetallic Project Gansu Province, P.R. China", dated effective April 29, 2012 and prepared by Calvin R. Herron, P. Geo Ontario, a consultant to the Company and a qualified person for NI 43-101, available on SEDAR at www.sedar.com. Readers should refer to the aforementioned technical report for more information.

Exploration Activities - Longnan Region Projects

The Company’s wholly-owned subsidiary, Minco China, held ten exploration permits in the Longnan region in the south of Gansu Province in China. The Longnan region is within the southwest Qinling gold field. The Longnan region consists of three projects according to their geographic distribution, type and potential of mineralization.

| Yejiaba: | Includes four exploration permits along a regional structural belt parallel to the Yangshan gold belt. The potential in this area is for polymetallic mineralization (gold-silver-iron-lead-zinc). The Company completed the NI 43-101 compliant technical report (refer to above) on Yejiaba Project, which is available on SEDAR. |

| Yangshan: | Includes five exploration permits located in the northeast extension of the Yangshan gold belt and its adjacent area. |

Xicheng East: Includes one exploration permit for the east extension of the Xicheng Pb-Zn mineralization belt. The potential in this area is for polymetallic mineralization (gold-silver-lead-zinc).

Yejiaba Project

The Yejiaba Project is located along the collisional boundary separating the Huabei and Yangtze Precambrian cratons. This major E-W trending collision zone has localized a number of large gold and polymetallic deposits within a geologic province that is often referred to as the Qinling Orogenic Belt. Gold and polymetallic mineralization on the Company’s lease package is generally hosted in Silurian-Devonian, thin-bedded limestone interbedded with phyllite. Mineralization is associated with shears and quartz veins, with higher grades typically found along sheared contacts separating massive limestone from the thin-bedded limestone and phyllite unit. Granite porphyry and quartz diorite dykes tend to be spatially associated with mineralization. Alteration accompanying mineralization consists of weak silicification and pyritization with carbonate veining and secondary carbon. Small quartz veinlets are noted in several places. Associated metals consist of silver, lead, antimony and arsenic.

Semi-regional geochemical anomalies were first delineated by the Company in 2005, extending 10 km along a hydrothermally altered zone that follows a NE trending thrust and regional unconformity.

Subsequent work between 2006 and 2012 has included traverse-line investigations, soil sampling, geologic mapping, geophysical surveys (ground magnetic and IP), trenching and drilling.

To date several targets have been identified and tested including: Shanjinba (Zone 1 and 2), Yaoshang, Fujiawan, Baimashi, Bailuyao, Baojia and Paziba.

The Company engaged an independent consultant to conduct a detailed review of the Yejiaba Project in April 2013, in particular to focus on the Baimashi North and East Targets. The sample work performed on the Yejiaba project during 2013 consisted of 912 rock chip samples, 818 soil samples, 41 stream sediment samples and 339 trench channels. The detailed results at the Baimashi North and East Targets are described in the sections below.

The Company started a drilling program on its Baimashi North Target in early July 2014. The drilling program, consisting of 1,200 meters core drilling in 6 holes, is designed to test a target area of roughly 1,200 meters long and 600 meters wide.

Sampling and assaying

The channel samples taken in the trenches are generally 10 cm wide; 5 cm deep, lengths are typically 1m but can be slightly longer or shorter to match geological boundaries. Only significant channel sample results are reported below, where composited gold grades are over 0.50 g/t. Reported composites may comprise individual samples with gold assays lower than 0.5g/t if it is deemed that the geology and mineralization is continuous over the interval. Channel sample intervals may not necessarily represent true thickness of the mineralization.

Sample preparation was performed by independent laboratory SGS-Tianjin, at their laboratory in Xian (PRC). Pulps are then analyzed at the SGS-Tianjin assay facility in Tianjin. Sample QAQC methods consisted of insertion of blank and duplicates in the field (one in twenty samples), while SGS-Tianjin inserted analytical duplicates and reference standards into the sample stream at their laboratory.

Baimashi Target

The Baimashi gold-antimony mineralization was discovered on the boundary between Weiziping-Baimashi and Shajinba-Yangjiagou permits and includes the Baimashi North Target that was identified in 2013, located approximately 1Km north of the Baimashi Target; and the Baimashi East Target.

During 2013, the samples in Table 1 were collected within the Baimashi North and East Target. Out of total samples, 118 trench, 75 soil and 37 rock samples were collected from Baimashi East, but the results of these samples demonstrated the gold values in the Baimashi East are tightly confined to narrow structure and thereby effectively diminished the target’s size and significance. The Company has no further exploration planned on this target.

All of the exploration to date conducted during 2013 indicates the Baimashi North Target is the only target with good potential to host a substantial bulk tonnage gold deposit.

| Table 1. Summary of sample types collected within the Baimashi Targets |

| | # of Samples | Gold Range (ppm) | Average Au (ppm) |

| Rock Chip | 912 | <0.005 – 47.115 | 0.729 |

| Soil | 818 | <0.005 – 3.968 | 0.055 |

| Trench Channels | 339 | <0.005 – 14.250 | 0.190 |

| Stream Sediment | 41 | <0.005 – 0.226 | 0.015 |

Baimashi North Target

Gold Mineralization Observed within the Baimashi North Target

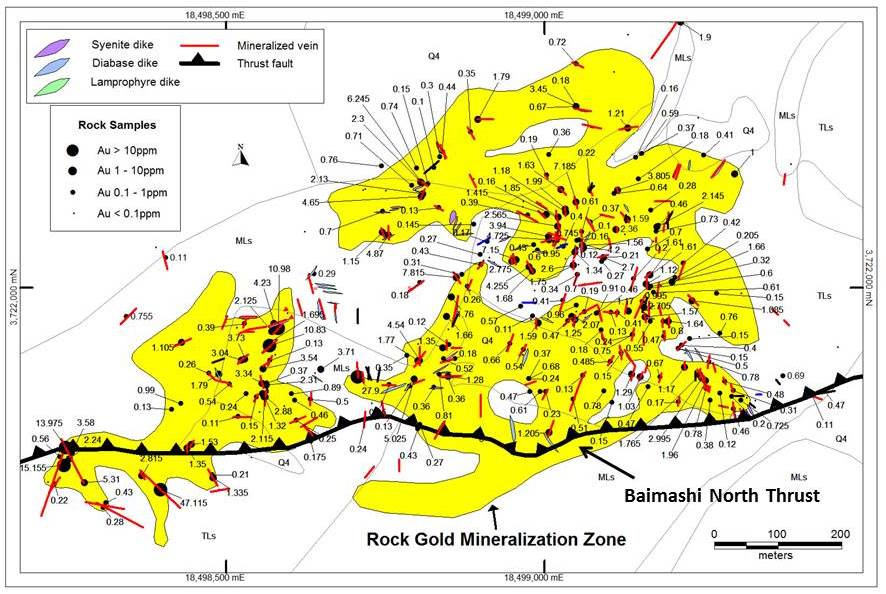

The Rock Gold Zone shown in Figure 1 represents the distribution of rock chip gold values exceeding 0.100ppm, and the zone boundaries were defined by combining the rock chip and soil sample results together with the structural data. The gold-in-soil distribution fairly represents the gold zone.

Figure1. Outline of Baimashi North Gold Mineralization Zone relative to soil samples results

In Figure 2, the same Rock Gold Zone is shown relative to the distribution of rock chip sample results together with the mapped mineralized structures (shears, veins, dikes). Here again, the sample data fits well within the zone boundaries, which suggests that the soil sample values generally do a fair job of reflecting the rock sample data. The dominantly northeast-trending Rock Gold Mineralization Zone is approximately 1,200m long by 600m wide. It measures 317,000m2 in plain view and is open to the north. The Baimashi North Target certainly possesses sufficient size for hosting a large gold deposit but will need sufficient gold grade as well

Figure 2. Outline of Baimashi North Gold Mineralization Zone relative to rock chip results and mineralized structures.

Samples collected within the Baimashi North Target

Following the encouraging results found in the third quarter of 2013 described below, a total of 589 soil samples and 39 rock samples were collected within this target during the fourth quarter of 2013. The soil sample results show a gold range from 0.005 to 3.968 ppm (refer to Table 1).

During the year ended December 31, 2013, 247 rock chip samples, 125 soil samples and 41 stream sediment samples within Baimashi North Target were collected.

The 247 rock samples collected within the Rock Gold Mineralization Zone run from 0.005 to 47.115ppm Au and average 1.49ppm, which is a potentially economic grade for an open-pit operation if this grade can be maintained. A rough analysis of the rock sample data is presented in Table 2, where we see a high percentage of samples (39%) carrying gold values exceeding 0.5 g/t, while 68% run in excess of 0.1 g/t. Six samples included in the >3.0 ppm Au category in Table 2 exceed 10ppm Au. If these six high-grade samples are taken out, the overall average grade drops to 1.00ppm, which illustrates the weight carried by high-grade numbers in this zone.

Table 2. Summary of rock chip sample results (excludes dumps). |

| Sample Ranges | Number of Samples | % of Total Samples | Average Au (ppm) | Average As (ppm) | Average Sb (ppm) |

| >3.0 ppm Au | 22 | 8 | 8.391 | 4292 | 99 |

| 1.0-3.0 ppm Au | 48 | 17 | 1.764 | 2358 | 66 |

| 0.5-1.0 ppm Au | 41 | 14 | 0.691 | 1797 | 54 |

| 0.1-0.5 ppm Au | 83 | 29 | 0.276 | 1340 | 25 |

| <0.1 ppm Au | 94 | 32 | 0.027 | 241 | 8 |

The overall gold grade distribution is summarized in Table 3. This is obviously a low grade system, and the amount of high grade found within the low-grade blanket will determine whether or not this target can be economical.

| Table 3. Distribution of gold grades in 247 rock samples collected at Baimashi North Target |

| Grade Range (ppm Au) | <0.1 | 0.1 -- 0.5 | 0.5 -- 2 | 2 -- 4 | 4 -- 6 | 6 -- 8 | >8 |

| % of Total | 18 | 32 | 33 | 9.3 | 3.2 | 1.6 | 2.4 |

The rock samples collected within this zone tested a variety of geologic features and they can be grouped into vein/fault, dike-related, and altered rock types. The carbonate veins and altered faults usually range from 0.1m to1.0m wide, and the sampling often includes some of the surrounding low-grade wallrock. Altered dikes and dike margins were also sampled as a separate rock type, as were several zones of altered phyllitic limestone (the “altered rock type”) hosting stockwork-type carbonate veinlets.

Averaged Au-As sample results for these three rock groups are compared in Table 4. Based on the As:Au ratios, arsenic values look to be following the intrusive dikes and sills, which suggests a congenetic relationship between the intrusive plumbing and Au-As mineralization. In contrast, the lower As:Au ratio seen in the vein/fault type is attributed to post-intrusion mineralization in younger, more dilatant zones.

| Table 4. Comparison of Au-As mineralization in major sample types at Baimashi North Target |

| Sample Type | Ave. Au (ppm) | Ave. As (ppm) | As/Au Ratio |

| V: Vein/Fault type | 2.190 | 2185 | 997 |

| D: Dike related | 0.951 | 1726 | 1815 |

| R: Altered rock type | 0.958 | 1325 | 1383 |

Yangshan and Xicheng East

During three and six months ended June 30, 2014, the Company did not conduct any exploration activities on these two projects except for maintaining the exploration permits in respect of the projects.

On December 13, 2013, Minco China entered into an agreement with YDIC pursuant to which the Company agreed to sell two exploration permits in the Xicheng East and Yejiaba area to YDIC for RMB 0.8 million ($140,000). The process of transferring the titles of the two permits to YDIC was not completed as at June 30, 2014 due to the pending approval by Gansu province.

| 2.2 | | Changkeng Gold Project |

The following is a discussion of the Company's Changkeng Gold Project. Technical Information respecting the Changkeng Gold Project is primarily derived from the NI 43-101 technical report entitled "Technical Report and Updated Resource Estimate on the Changkeng Gold Project Guangdong Province, China", dated effective February 21, 2009 and prepared by Tracy Armstrong, P. Geo Ontario, Eugene Puritch, P. Eng. Ontario and Antoine Yassa, P.Geo. Québec, all of P&E Mining Consultants Inc., and all qualified persons for the purposes of NI 43-101. This technical report includes relevant information regarding the data, data validation and the assumptions, parameters and methods of the mineral resource estimates on the Changkeng Gold Project.

Location

The Changkeng gold deposit is located approximately 45 km southwest of Guangzhou, the fourth largest city in China with 13 million people and the capital city of Guangdong Province. The project is adjacent to Minco Silver's Fuwan silver deposit and situated close to well-established water, power and transportation infrastructure.

Ownership

Mingzhong, a cooperative joint-venture established among Minco China, Guangdong Geological Bureau, Guangdong Gold Corporation, and two private Chinese companies to jointly explore and develop the Changkeng Property, signed a purchase agreement in January 2008 to buy a 100% interest in the Changkeng Exploration Permit on the Changkeng Project from 757 Exploration Team. The transfer of the Changkeng Exploration Permit from 757 Exploration Team to Mingzhong was approved by the MOLAR in 2009. The renewed Changkeng Exploration Permit for a two-year period expires on September 10, 2015.

The purchase price of the Changkeng Exploration Permit was set at RMB 48 million ($8.15 million). As of December 31, 2008, Mingzhong paid the first payment of RMB 19 million ($3.22 million) to the 757 Exploration Team for the Changkeng Exploration Permit. The remaining balance of RMB 29 million ($4.92 million) was settled in May 2013. According to the Supplementary Agreement signed between 757 Exploration Team and Mingzhong, 757 Exploration Team agreed to refund RMB 3.8 million ($622,293) to Mingzhong for the exploration costs incurred during the early stage of exploration of Changkeng project. The refunded amount was recorded as an exploration cost recovery during the year ended December 31, 2013. On July 31, 2013, Mingzhong paid the RMB 1.03 million ($169,669) to 757 Exploration Team for the completed hydro-geological program on the Changkeng Gold Project. The hydro-geological program was conducted to assist the preparation of the NI 43-101 technical report entitled "Technical Report and Updated Resource Estimate on the Changkeng Gold Project Guangdong Province, China”: dated effective February 21, 2009.

Geology, Drilling Program and Resources Estimate

There have been no significant changes in the geology, drilling program and resource estimate during the six months ended June 30, 2014 and as at the MD&A date compared to the year ended December 31, 2013.

A comprehensive discussion of the geology, drilling program and resource estimate are included in the Company’s Annual Report on Form 20-F for the year ended December 31, 2013, dated March 28, 2014 available on SEDAR at www.sedar.com. During the six months ended June 30, 2014, the Company started a metallurgical test on the Changkeng Gold project.

| 2.3 | | Equity Investment in Minco Silver Corporation |

As at June 30, 2014, the Company owned 11,000,000 common shares of Minco Silver (December 31, 2013 - 13,000,000 common shares) that were acquired in 2004 in exchange for the transfer of the Fuwan property and the silver interest in the Changkeng property. As at June 30, 2014, the Company owned a 18.45% (December 31, 2013 – 21.91%) equity interest in Minco Silver.

The following discussion respecting the Fuwan Silver Project held by Minco Silver is based on Minco Silver's public disclosure available on SEDAR at www.sedar.com.

Current Developments on the Fuwan Silver Project

Minco Silver continues its focus on the EIA report and the permitting process in order to apply for a mining license for the Fuwan Silver Project

Minco Silver made great efforts to regain the support of local communities and had productive communication with Zhaoqian District government and Gaoyao County government for development of the Fuwan Silver Project before the submission of the revised Environmental Impact Assessment (“EIA”) report to Guangdong EPA department. Due to the fact that the last public opinion survey was carried out in 2008, the Company conducted a new survey among local communities concerning the development of the Fuwan Silver Project and obtained very strong support from the locals. On May 26, 2013, Gaoyao County government issued an official approval of the development of the Fuwan Silver Project to the Company.

Several large mining groups in China expressed an interest in the Fuwan Silver Project in late 2012. Minco Silver hosted site visits, data reviews, and preliminary discussions with those groups; however no definitive agreements have been concluded as at the date of this MD&A. Minco Silver’s strategy is to secure a large Chinese mining group as a business partner.

Minco Silver engaged the Guangdong Nuclear Design Institute (“GNDI”) to complete the Chinese Regulatory EIA report in 2010. The EIA report was reviewed by a technical panel appointed by the Department of Environmental Protection Administration of Guangdong Province in principle on March 7, 2010 with certain comments. Minco Silver submitted the revised report to the Department in December 2010 after addressing the comments received from the panel.

Minco Silver engaged General Station for Geo-Environmental Monitoring of Guangdong Province (“GSGEM”) for a water monitoring study to comply with the new water regulations issued by the Ministry of Environmental Protection of China effective on June 1, 2011. GSGEM carried out the required monitoring study and prepared all reports required for compliance with the new National Water Guidelines. Minco Silver successfully completed the field work in January 2012 and received the comprehensive water monitoring report from GSGEM in April 2012. The report concluded that Minco Silver is in compliance with the requirements of the new National Water Guidelines.

Revision of the EIA report has been completed incorporating the results from the water monitoring survey report. The revised EIA will be submitted to the Guangdong Environment Protection Administration (“EPA”) as soon as they are accepting new EIA reports. The delay in approval of the EIA report for the Fuwan Silver Project is due to the negative impact caused by the collapse of the tailing dam of an operating mine in Guangdong Province four years ago. The preliminary mine design was completed in 2013 by China Nerin Engineering Co. Ltd (“NERIN”) and will be released after the requirements from the approved EIA report are met.

Minco Silver successfully renewed the exploration permit of Luoke- Jilinggang in 2013 for a two-year period ending on July 20, 2015. Another three silver exploration permits on the Fuwan belt, referred to as Guyegang (55.88 sq. km.), Hecun (12.7 sq. km.), and Guanhuatang (27.3 sq. km.), are held by Minco China in trust for Minco Silver. Minco Silver decided not to renew the Guanhuatang property permit, which expired on April 4, 2014, due to its proximity to new town developments and water reservoirs. Minco China is in the process of renewing the two remaining permits with the Ministry of Land and Resources. The following summarizes significant progress in permitting on the Fuwan Silver Deposit.

| · | The Chinese Preliminary Feasibility Study was completed by Changsha Non-Ferrous Mine Design Institute and approved by an expert panel |

| · | The Mining Area Permit, covers approximately 0.79 km2, defines the mining limits of the Fuwan Silver Deposit and restricts the use of this land to mining activities. The Permit was approved by MOLAR and renewed subsequent to the original approval in October 2009. The renewed permit expires on April 10, 2016. |

| · | The Soil and Water Conservation Plan was completed and approved. |

| · | The Land Usage Permit was approved by the Gaoming County, Foshan City and Guangdong provincial governments. It was renewed for a one year period until December 31, 2014. The Company is currently in the process of renewing this permit. |

| · | The Geological Hazard Assessment was completed and approved in September 2009. |

| · | The Mine Geological Environment Treatment Plan was reviewed and approved by the Environment Committee of China Geology Association. |

| · | The preliminary Safety Assessment draft report was completed in December 2011 and submitted to the Safety Bureau of Guangdong Province for approval. |

Investment in Minco Silver is as follows:

June 30, 2014 | December 31, 2013 |

| $ | $ |

| Investment in associate | - | 13,368,836 |

| Available-for-sale investment | 11,000,000 | - |

| | 11,000,000 | 13,368,836 |

| | | | |

| a) | Investment in associate |

On April 22, 2014, the Company sold 2,000,000 common shares of Minco Silver for cash proceeds of $1,500,000 which decreased the Company’s equity interest in Minco Silver from 21.81% to 18.45%. As a result of this transaction, the Company recognized a loss on partial disposition of its investment in Minco Silver of $558,333 and a resulting reduction in the carrying value of the investment in associate of $2,058,333. Upon the sale of the 2,000,000 common shares of Minco Silver, the Company reclassified a gain of $158,797 for items previously recognized in the other comprehensive income related to the investment in Minco Silver resulting in a net loss on partial disposition of its investment in Minco Silver of $399,536.

On April 22, 2014, the Company concluded that it no longer had significant influence over Minco Silver, as it did not own more than 20% of Minco Silver’s outstanding common shares, and therefore, equity accounting for our investment in Minco Silver was no longer applicable. This resulted in the derecognition of the carrying value of our investment in associate and the recognition of our shareholding at fair value as an available-for-sale financial asset. The fair value of the shares upon initial recognition was $8,800,000. The difference between the carrying value of the investment and the fair value of the shares was recorded in the condensed consolidated interim statements of loss, resulting in a loss of $2,520,831. Upon the loss of significant influence of Minco Silver, the Company reclassified a gain of $873,385 for items previously recognized in the other comprehensive income related to the investment in Minco Silver resulting in a net loss on derecognition of investment in Minco Silver of $1,647,446. Subsequent changes in fair value after April 22, 2014 are recognized in other comprehensive loss.

| | 2014 | 2013 |

| | $ | $ |

| Equity investment in Minco Silver as at January 1, | 13,368,836 | 13,375,407 |

| | | |

| Dilution loss | (78,177) | (77,414) |

| Equity loss | (94,626) | (656,132) |

| Cumulative translation adjustment | 183,131 | 726,975 |

| Partial disposition | (2,058,333) | - |

| Derecognition of investments in associates | (11,320,831) | - |

| Equity investment in Minco Silver as at June 30, 2014 and December 31, 2013 | - | 13,368,836 |

| | | | | |

| b) | Available-for-sale investment |

The available-for-sale investment represents the Company’s investment in Minco Silver. On April 22, 2014, the Company no longer had significant influence over Minco Silver and therefore ceased accounting for this investment on an equity basis and reclassified it to available-for-sale. The fair market value of the available-for-sale investment on initial recognition was $8,800,000, based on the quoted market price for the underlying security. During the three and six months ended June 30, 2014, the Company has recognized unrealized gains of $2,200,000 and a corresponding deferred income tax expense of $286,000 in the Condensed Consolidated Interim Statements of Comprehensive Loss. As at June 30, 2014, the fair market value of the available-for-sale investment was $11,000,000, based on the quoted market price of $1 per share of Minco Silver.

On December 16, 2010, Minco China entered into a JV agreement with the 208 Team, a subsidiary of China National Nuclear Corporation, to acquire a 51% equity interest in the Tugurige Gold Project located in Inner Mongolia, China. The 208 Team did not comply with certain of its obligations under the JV Agreement, including its obligation to set up a new entity (the “JV Co”) and the transfer of its 100% interest in the Tugurige Gold Project to the JV Co. As a result, Minco China commenced legal action in China seeking compensation.

On March 25, 2013, Minco China settled its claim against the 208 Team relating to the JV Agreement for an amount of RMB 14 million ($2.4 million). The Company recognized a gain of $1,343,638 on the legal settlement, net of accrued legal fees of RMB 900,000 ($157,425) during the year ended December 31, 2013.

As at June 30, 2014, the Company had received RMB 9 million in total ($1,521,490) and did not recognize the remaining RMB 5 million ($865,711) balances due under the legal settlement due to the uncertainty of collectability. In the event of non-payment of the final settlement amount, Minco China has reserved the right to take further legal action.

| 2.5 | | Gold Bull Mountain project |

Yuanling Minco’s wholly owned subsidiary Huaihua Tiancheng owns the Gold Bull Mountain exploration permit, which was renewed for a two-year period ending on June 28, 2015.

On June 28, 2014, Minco China entered into a sale agreement to dispose of its interest in Yuanling Minco for RMB 7 million ($1.2 million).

The buyer will make the following payments to Minco China:

| i) | 30% of the selling price within 7 days from the date of signing this agreement (received subsequent to June 30, 2014); |

| ii) | 55% of the selling price prior to the formal transfer request being submitted to the governing authorities; and |

| iii) | 15% upon completing the transfer and obtaining all governing authorities’ approval. |

As at June 30, 2014, the process of transferring the titles of Yuanling Minco and the completion of the transaction was pending approval by governing authorities and the assets and liabilities have been presented as held for sale on the condensed consolidated interim statements of financial position.

The following is a summary of exploration costs incurred by each project:

| | Three months ended June 30, | Six months ended June 30, | Accumulative to June 30, |

| Currently active properties: | 2014 | 2013 | 2014 | 2013 | 2014 |

| | $ | $ | $ | $ | $ |

| Gansu | | | | | |

| - Longnan | 197,560 | 237,049 | 371,213 | 482,342 | 11,217,459 |

| Guangdong | | | | | |

| - Changkeng (*) | 25,031 | (626,765) | 109,696 | (606,272) | 8,027,963 |

| Hunan | | | | | |

| - Gold Bull Mountain | 14,390 | 8,532 | 25,433 | 12,657 | 2,261,674 |

| Guangdong | | | | | |

| - Sihui | - | - | 526 | 1,644 | 4,999 |

| | | | | | |

| Total | 236,981 | (381,184) | 506,868 | (109,629) | 21,512,095 |

During the three and six months ended June 30, 2014, the Company did not conduct any exploration activities on the Changkeng and Gold Bull Mountain projects, except for maintaining the exploration permits.

(*) During the three and six months ended June 30, 2013, the Company recorded a refund from 757 Exploration Team of $622,293 for certain exploration costs incurred during the early stage of the Changkeng gold project. The refunded amount was recorded as an exploration cost recovery.

| 3.2 | | Administrative Expenses |

The Company’s administrative expenses include overhead associated with administering and financing the Company’s exploration activities.

For the three months ended June 30, 2014, the Company incurred a total of $501,224 of administrative expenses (2013 - $747,246).

For the six months ended June 30, 2014, the Company incurred a total of $1,049,004 of administrative expenses (2013 - $1,528,993).

The following table is a summary of the Company’s administrative expenses for the three months and six months ended June 30, 2014 and 2013.

| | Three months ended June 30, | Six months ended June 30, |

| | 2014 | 2013 | 2014 | 2013 |

| Administrative expenses | $ | $ | $ | $ |

| Accounting and audit | 28,288 | 48,746 | 50,406 | 80,189 |

| Amortization | 17,731 | 17,422 | 36,127 | 32,416 |

| Consulting | 2,263 | 2,349 | 7,144 | 25,680 |

| Directors’ fees | 13,000 | 12,749 | 31,000 | 25,749 |

| Foreign exchange loss (gain) | (7,776) | 9,084 | (2,928) | 13,732 |

| Investor relations | 9,678 | 20,999 | 19,207 | 75,131 |

| Legal and regulatory and filing | 27,075 | 44,835 | 60,884 | 83,307 |

| Office administration expenses | 83,897 | 72,830 | 207,859 | 196,332 |

| Property investigation | 18,557 | 29,264 | 38,482 | 60,961 |

| Salaries and benefit | 194,944 | 144,939 | 347,504 | 264,546 |

| Share-based compensation | 99,685 | 325,271 | 222,025 | 639,365 |

| Travel and transportation | 13,882 | 18,758 | 31,294 | 31,585 |

| | 501,224 | 747,246 | 1,049,004 | 1,528,993 |

Significant changes in expenses are as follows:

Accounting and auditing

Accounting and auditing expenses for the three months ended June 30, 2014 were $28,288 compared to $48,746 for the comparative period of 2013. The decrease was due to reduced audit fees.

Accounting and auditing expenses for the six months ended June 30, 2014 were $50,406 compared to $80,189 for the comparative period of 2013. The decrease was due to the same reason described above.

Consulting fees

Consulting fees for the three months ended June 30, 2014 were $2,263, which was consistent with the $2,349 for the comparative period of 2013.

Consulting fees for the six months ended June 30, 2014 were $7,144 compared to $25,680 for the comparative period of 2013. The decrease was due to the reduction in the use of external consultants in China.

Investor relations

Investor relations expenses for the three months ended June 30, 2014 were $9,678 compared to $20,999 for the comparative period of 2013. The decrease was primarily due to the reduction in the use of external consultants and also the resignation of the Company’s Vice President of Corporate Communication in the latter half of 2013.

Investor relations expenses for the six months ended June 30, 2014 were $19,207 compared to $75,131 for the comparative period of 2013. The decrease was due to the same reason described above.

Legal, regulatory and filing

Legal, regulatory, and filing expenses for the three months ended June 30, 2014 were $27,075 compared to $44,835 for the comparative period of 2013. The decrease was due to the Company reducing use of its external legal counsel to assist with regulatory compliance.

Legal, regulatory and filing expenses for the six months ended June 30, 2014 were $60,884 compared to $83,307 for the comparative period of 2013. The decrease was mainly due to the same reason described above.

Property investigation

Property investigation expenses for the three months ended June 30, 2014 were $18,557 compared to $29,264 for the comparative period of 2013. The decrease was due to the Company’s Vice President of Business Development reducing his time spent on the Company’s operations during the first half of 2014.

Property investigation expenses for the six months ended June 30, 2014 were $38,482 compared to $60,961 for the comparative period of 2013. The decrease was due to the same reason described above.

Salaries and benefit

Salaries and benefit expenses for the three months ended June 30, 2014 were $194,944 compared to $144,939. The increase was due to benefit paid/ accrued for the departure of the Company’s former CFO during the period of 2014.

Salaries and benefit expenses for the six months ended June 30, 2014 were $347,504 compared to $264,546. The increase was due to the same reason described above, and also due to severance paid for termination of employees in China during the first quarter of 2014. In addition, the Company recovered salary expenses of $29,000 from Minco Base Metals Corporation (“MBM”) during the first quarter of 2013.

Share-based compensation

Share-based compensation expense for the three months ended June 30, 2014 was $99,685 compared to $325,271 for the comparative period of 2013. The decrease was due to the reduced number of options and reduced value per stock option granted in 2014 compared to 2013.

Share-based compensation expense for the six months ended June 30, 2014 was $222,025 compared to $639,365 for the comparative period of 2013. The decrease was due to the same reason described above.

| 3.3 | | Finance and Other Income (Expense) |

For the three months ended June 30, 2014, the finance income was $5,321 compared to $29,902 for the comparative period of 2013. The decrease was due to the funds being used to settle the final payment of Changkeng Exploration Permit in May 2013.

For the six months ended June 30, 2014, the finance income was $6,340 compared to $95,452 for the comparative period of 2013. The decrease was due to the same reason described above.

| 3.4 | | Income Tax Expense (Recovery) |

Deferred income tax recovery for the three and six months ended June 30, 2014 was $286,000 compared to $nil in 2013. Deferred income tax recovery was related to the change in deferred income tax assets recognized, which was primarily affected by the change in unrealized gains in the equity investment in Minco Silver.

| 4. | | Summary of Quarterly Results |

| | | Loss per share |

| Period ended | Net loss attributable to shareholders | Basic | Diluted |

| 06-30-2014 (**) | (2,519,526) | (0.05) | (0.05) |

| 03-31-2014 | (904,665) | (0.02) | (0.02) |

| 12-31-2013 | (637,398) | (0.01) | (0.01) |

| 09-30-2013 | (1,370,204) | (0.02) | (0.02) |

| 06-30-2013 | (826,767) | (0.02) | (0.02) |

| 03-31-2013(*) | (310,156) | (0.01) | (0.01) |

| 12-31-2012 | (1,386,778) | (0.03) | (0.03) |

| 09-30-2012 | (1,024,173) | (0.02) | (0.02) |

Variations in quarterly performance over the eight quarters can be primarily attributed to changes in dilution gains and losses and equity gains and losses resulting from the Company’s investment in Minco Silver. Another contributing factor is changes in the amount of share-based compensation recognized in each period.

(*) Net loss decreased to $0.3 million for the period ended March 31, 2013 mainly due to the Company recognizing a gain on legal settlement of $0.8 million.

(**) Net loss increased to $2.5 million for the period ended June 30, 2014 mainly due to the loss on partial disposition of investment in Minco Silver of $0.4 million and loss on derecognition of investment in Minco Silver of $1.6 million.

| 5. | | Liquidity and Capital Resources |

| | Six months ended June 30, |

| | 2014 | 2013 |

| | $ | $ |

| Operating activities | (1,362,406) | (5,737,047) |

| Investing activities | 2,206,329 | 5,972,898 |

| Financing activities | 69,000 | 600,000 |

Operating activities

For the six months ended June 30, 2014, the Company used cash of $1,362,406 in operating activities compared to cash of $5,737,047 used in the comparative period of 2013. The decrease was primarily due to the final payment of RMB 25.2 million ($4.28 million) for the Changkeng Exploration Permit paid to 757 Exploration Team in 2013.

Investing activities

For the six months ended June 30, 2014, the Company received RMB 4 million ($720,095) proceeds from the legal settlement with the 208 Team and also proceeds of $1,500,000 from the disposition of Minco Silver’s shares.

Investing activities during the six months ended June 30, 2013 included the redemption of short-term investments of $5.2 million and proceeds of RMB 5 million ($801,395) received from the legal settlement with the 208 Team.

Financing activities

For the six months ended June 30, 2014, the Company received $Nil advanced by Minco Silver compared to $600,000 advanced by Minco Silver for the Comparative period of 2013. In addition, the proceeds of $69,000 was received during the period of 2014 from the stock option exercised compared to $Nil for the comparative period of 2013.

| 5.2 | | Capital Resources and Liquidity Risk |

As at June 30, 2014, the Company had cash of $1,822,529 held by the Company’s Chinese subsidiaries. The Company may face delays repatriating funds held in China if at any time the Company requires additional resources to enable it to undertake projects elsewhere in the world.

The Company is exposed to liquidity risk, which is the risk that the Company may encounter difficulty in settling its commitments when due including the continued forbearance to the amounts due to Minco Silver. In managing this risk, management determined that the Company’s cash balance as at June 30, 2014 of $2.7 million and the proceeds received from the Yuanling Minco disposition would be sufficient to meet its cash requirements for the Company’s administrative overhead and to maintain its mineral interest throughout the next 12 months.

The Company's ability to meet its obligations and finance exploration and development activities over the long-term depends on its ability to generate cash flow through various debt or equity financing initiatives. Capital markets may not be receptive to offerings of new equity from treasury or debt, whether by way of private placements or public offerings. The Company's growth and success is dependent on external sources of financing which may not be available on acceptable terms or at all.

| 5.3 | | Contractual Obligations |

The Company’s contractual obligations are related to a cost sharing agreement between the Company, Minco Silver and MBM, related parties domiciled in Canada, including $3.6 million to be used for the repayment of amounts due to Minco Silver, and $0.6 million for other obligations.

There have been no material changes in the Company’s contractual obligations for the six months ended June 30, 2014 compared to the year ended December 31, 2013. Please refer to the Company’s 2013 MD&A dated March 26, 2014, available on SEDAR.

| 6. | | Off -Balance Sheet Arrangements |

The Company does not have any off-balance sheet arrangements.

| 7. | | Transactions with Related Parties |

Shared expenses

Minco Silver and Minco Gold share offices and certain administrative expenses in Beijing and Minco Silver, MBM and Minco Gold share offices and certain administrative expenses in Vancouver.

At June 30, 2014, the Company had $3,628,605 due to Minco Silver (December 31, 2013 – $3,584,387) and consisted of the following:

Amount due from Foshan Minco as at June 30, 2014 of $26,760 (December 31, 2013 - $15,847), representing the expenditures incurred by Minco China on behalf of Foshan Minco and shared office expenses.

Amount due to Minco Silver as at June 30, 2014 was $3,655,365 (December 31, 2013 – $3,600,234) representing funds advanced from Minco Silver to Minco Gold to support its operating activities in Canada net of shared head office expenses.

The amounts due are unsecured, non-interest bearing and payable on demand.

At June 30, 2014, the Company has $54,792 due from MBM (December 31, 2013 - $67,418), in relation to shared office expenses. The Company is related to MBM through significant influence of one common director and common management.

The amounts due are unsecured, non-interest bearing and payable on demand.

Funding of Foshan Minco

Minco Silver cannot invest directly in Foshan Minco as Foshan Minco is legally owned by Minco China. All funding supplied by Minco Silver for exploration of the Fuwan Project must first go through Minco China via the Company to comply with Chinese Law. In the normal course of business, Minco Silver uses trust agreements when providing cash, denominated in US dollars, to Minco China via the Company for the purpose of increasing the registered capital of Foshan Minco. Minco China is a registered entity in China; however it is classified as being a wholly foreign owned entity and therefore can receive foreign investment. Foshan Minco is a Chinese company with registered capital denominated in RMB and can only receive domestic investment from Minco China. Increase to the registered capital of Foshan Minco must be denominated in RMB.

In 2013, Minco Silver advanced US$20 million to Minco China via the Company and Minco Resources in accordance with a trust agreement signed on April 30, 2013, in which Minco Silver agreed to advance US$20 million to Minco China to increase Foshan Minco’s registered share capital.

As at June 30, 2014, Minco China held US $11,221,907 ($11,974,731) (December 31, 2013 – US $12,526,138 ($13,399,210)) and RMB 39,435 ($6,828) (December 31, 2013 – RMB 14,613,570 ($2,556,161)) in trust for Minco Silver.

Key management compensation

Key management includes the Company’s directors and senior management. This compensation is included in exploration costs and administrative expenses.

For the three and six months ended June 30, 2014 and 2013, the following compensation was paid to key management:

| Three months ended June 30, | Six months ended June 30 |

| | 2014 | 2013 | 2014 | 2013 |

| | $ | $ | $ | $ |

| Cash remuneration | 94,202 | 80,249 | 156,452 | 159,495 |

| Share-based compensation | 68,533 | 236,379 | 156,153 | 483,252 |

| Total | 162,735 | 316,628 | 312,605 | 642,747 |

The above transactions were conducted in the normal course of business.

| 8. | | Critical Accounting Estimates |

The preparation of financial statements requires management to use judgment in applying its accounting policies and estimates and assumptions about the future. Estimates and other judgments are continuously evaluated and are based on management’s experience and other factors, including expectations about future events that are believed to be reasonable under the circumstances. The following discusses the most significant accounting judgments and estimates that the Company has made in the preparation of the financial statements:

Investment in Minco Silver

Significant Influence

On April 22, 2014, the Company determined that we no longer held significant influence over Minco Silver, as we did not own more than 20% of Minco Silver’s outstanding common shares, and therefore, equity accounting for our investment in Minco Silver was no longer applicable. The Company and Minco Silver continues to have a board member and the CEO in common. The investment in Minco Silver was subsequently classified as available-for-sale financial asset.

Impairment

At each reporting date, we conduct a review to determine whether there are any indications of impairment. This determination requires significant judgment. In making this judgment, we evaluate, among other factors, the duration and extent to which the fair value of the equity investment in Minco Silver is less than its cost.

If the decline in fair value below cost were significant or prolonged, we would recognize a loss, being the transfer of the accumulated fair value adjustments recognized in other comprehensive income on the impaired available-for-sale financial assets to the statement of income.

Management has assessed for impairment indicators on the Company’s equity investment in Minco Silver and has concluded that no impairment indicators existed as of June 30, 2014.

Liquidity risk

The Company is exposed to liquidity risk, which is the risk that the Company may encounter difficulty in settling its commitments when due. In managing this risk, management determined that the Company’s cash balance as at June 30, 2014 of $2.7 million along with the proceeds from the Yuanling Minco disposition ($1.2 million) would be sufficient to meet its cash requirements for the Company’s administrative overhead and to maintain its mineral interest for the next 12 months.

| 9. | | Adoption of new accounting standard |

Effective January 1, 2014, the Company adopted the following standard.

IFRIC 21 -Levies

This standard was issued on May 20, 2013 and provided guidance on when to recognize a liability for a levy imposed by a government, both for levies that are accounted for in accordance with IAS 37 Provisions, Contingent Liabilities and Contingent Assets and those where the timing and amount of the levy is certain. The adoption of this standard did not have an impact on the Company’s condensed consolidated interim financial statements.

Financial assets and liabilities have been classified into categories that determine their basis of measurement and, for items measured at fair value, whether changes in fair value are recognized in the statement of income or comprehensive income. Those categories are: fair value through profit or loss, loans and receivables, available-for-sale and other financial liabilities.

The following table summarizes the fair value for items categorized as available-for-sale and the carrying value of items categorized as loans and receivable and other liabilities as at June 30, 2014 and 2013.

| | June 30, | December 31, | |

| | | 2014 | 2013 | |

| Loans and receivables | | $ | $ |

| Cash and cash equivalents | | 2,674,726 | 1,797,809 | |

| Receivables | | 51,485 | 715,649 | |

| Due from related parties | | 54,792 | 67,418 | |

Available-for-sale | | | | |

| Equity investment in Minco Silver | | 11,000,000 | - | |

| Other liabilities | | | | |

| Account payable | 454,642 | 552,177 | |

| Advance from non-controlling interest | 166,217 | 167,920 | |

| Due to related party | 3,628,605 | 3,584,387 | |

| | | | |

| | | | | | | | | | | | | |

The equity investment in Minco Silver is measured at fair value based on quoted market price.

Financial instruments that are not measured at fair value on the balance sheet are represented by cash and cash equivalents, due from related parties, receivables, accounts payable, advance from non-controlling interest and due to related party. The fair values of these financial instruments approximate their carrying values due to their short term nature.

Financial risk factors

The Company’s operations consist of the acquisition, exploration and development of properties in China. The Company examines the various financial risks to which it is exposed and assesses the impact and likelihood of occurrence. These risks may include credit risk, price risk, liquidity risk, currency risk and interest rate risk. Management reviews these risks on a monthly basis and when material, they are reviewed and monitored by the Board of Directors.

Credit risk

Counterparty credit risk is the risk that the financial benefits of contracts with a specific counterparty will be lost if the counterparty defaults on its obligations under the contract. This includes any cash amounts owed to the Company by these counterparties, less any amounts owed to the counterparty by the Company where a legal right of set-off exists and also includes the fair value contracts with individual counterparties which are recorded in the condensed consolidated interim financial statements. The Company considers the following financial assets to be exposed to credit risk:

| · | Cash and cash equivalents – In order to manage credit and liquidity risk the Company places its cash with major financial institutions in the PRC (not subject to deposit insurance) and one major bank in Canada (subject to deposit insurance up to $100,000). At June 30, 2014, the balance of $2,674,726 (December 31, 2013 - $1,797,809) was placed with a few institutions. |

Price risk

Financial instrument that expose the Company to price risk is the equity investment in Minco Silver.

We hold common shares of Minco Silver which is measured at fair value, being the closing price at the reporting date. We are exposed to changes in share prices which would result in gains and losses being recognized in total comprehensive income or loss. A +/- 10% in share prices would have a +/- $1.1 million impact on total comprehensive income or loss.

Foreign exchange risk

The Company’s functional currency is the Canadian dollar in Canada and RMB in China. The foreign currency risk is related to US dollar funds. Therefore the Company’s net earnings are impacted by fluctuations in the valuation of the US dollar in relation to the Canadian dollar and RMB. The Company did not hold significant amounts of US dollar cash during the period and therefore the impact of the changes in the US dollar foreign exchange rate is insignificant to the Company’s net earnings.

Interest rate risk

The effective interest rate on financial liabilities (accounts payable) ranged up to 1%. The interest rate risk is the risk that the fair value of future cash flows of a financial instrument fluctuates because of changes in market interest rates. Cash and short-term investments entered into by the Company bear interest at a fixed rate thus exposing it to the risk of changes in fair value arising from interest rate fluctuations. Short term investments are invested in high grade, highly liquid instruments and expose the Company to variable interest rate fluctuations. A 1% increase in the interest rate in Canada will have a net (before tax) income effect of $26,747 (December 31, 2013- $17,978), assuming the foreign exchange rate remains constant.

| 11. | | Risks Factors and Uncertainties |

A comprehensive discussion of risk factors is included in the Company's annual report on Form 20-F for the year ended December 31, 2013, dated March 28, 2014, available on SEDAR at www.sedar.com.

| 12. | | Disclosure Controls and Procedures and Internal Controls over Financial Reporting |

Management has established disclosure controls and procedures to ensure that information disclosed in this MD&A and the related financial statements was properly recorded, processed, summarized and reported to the Company’s Board and Audit Committee.

Management is also responsible for establishing and maintaining adequate internal controls over financial reporting. Any system of internal control over financial reporting, no matter how well designed, has inherent limitations. Therefore, even those systems determined to be effective can provide only reasonable assurance with respect to financial statement preparation and presentation.

The control framework used to design the Company’s internal control over financial reporting is the Internal Control – Integrated Framework (1992) issued by the Committee of Sponsoring Organizations of the Treadway Commission (“COSO”).

During the six months ended June 30, 2014, there have been no material changes in the Company’s internal control over financial reporting.

| 13. | | Cautionary Statement on Forward-Looking Information |

Except for statements of historical fact, this MD&A contains certain “forward looking information” and “forward looking statements” within the meaning of applicable securities laws, which reflect management’s current expectations regarding, among other things and without limitation, the Company’s future growth, results of operations, performance and business prospects, opportunities, future price of minerals and effects thereof, the estimation of mineral reserves and resources, the timing and amount of estimated capital expenditures, the realization of mineral reserve estimates, costs and timing of proposed activities, plans and budgets for and expected results of exploration timing of proposed activities, plans and budgets for and expected results of exploration activities, exploration and permitting time-lines, requirements for additional capital, government regulation of mining operations, environmental risks, reclamation obligation and expenses, the availability of future acquisition opportunities and use of the proceeds from financing. Generally, forward looking statements and information can be identified by the use of forward looking terminology such as “plans”, “expects”, “is expected”, “budget”, “scheduled”, “estimates”, “forecasts”, “intends”, “anticipates”, “believes” or variations of such words and phrases or statements that certain actions, events or results “may”, “could”, “would”, “might” or “will be taken”, “occur” or “be achieved” or the negative connotation thereof.

Forward-looking statements are included throughout this document and include, but are not limited to, statements with respect to: our plans for future exploration programs for our mineral properties; the ability to generate working capital; markets; economic conditions; performance; business prospects; results of operations; capital expenditures; and foreign exchange rates. All such forward-looking statements are based on certain assumptions and analyses made by us in light of our experience and perception of historical trends, current conditions and expected future developments, as well as other factors we believe are appropriate in the circumstances. These statements are, however, subject to known and unknown risks and uncertainties and other factors. As a result, actual results, performance or achievements could differ materially from those expressed in, or implied by, these forward-looking statements and, accordingly, no assurance can be given that any of the events anticipated by the forward-looking statements will transpire or occur, or if any of them do so, what benefits will be derived therefrom. These risks, uncertainties and other factors include, among others: our interest in our mineral properties may be challenged or impugned by third parties or governmental authorities; economic, political and social changes in China; uncertainties relating to the Chinese legal system; failure or delays in obtaining necessary approvals; exploration and development is a speculative business; the Company's inability to obtain additional funding for the Company's projects on satisfactory terms, or at all; hazardous risks incidental to exploration and test mining; the Company has limited experience in placing resource properties into production; government regulation; high levels of volatility in market prices; environmental hazards; currency exchange rates; and the Company's ability to obtain mining licenses and permits in China.

Although the Company has attempted to identify important factors that could cause actual results to differ materially, there may be other factors that cause results not to be as anticipated, estimated or intended. There can be no assurance that statements containing forward looking information will prove to be accurate as actual results and future events could differ materially from those anticipated in such statements. Accordingly, readers should not place undue reliance on statements containing forward looking information. All of the forward-looking information and statements contained in this document are expressly qualified, in their entirety, by this cautionary statement. The various risks to which we are exposed are described in additional detail under the section entitled "Item 3: Key Information – D. Risk Factors" in the Company's annual report on Form 20-F available on SEDAR at www.sedar.com. The forward-looking information and statements are made as of the date of this document, and we assume no obligation to update or revise them except as required pursuant to applicable securities laws.