QuickLinks -- Click here to rapidly navigate through this document

SCHEDULE 14A INFORMATION

Proxy Statement Pursuant to Section 14(a) of

the Securities Exchange Act of 1934 (Amendment No. )

| Filed by the Registrantý | ||

Filed by a Party other than the Registranto | ||

Check the appropriate box: | ||

o | Preliminary Proxy Statement | |

o | Confidential, for Use of the Commission Only (as permitted by Rule 14a-6(e)(2)) | |

ý | Definitive Proxy Statement | |

o | Definitive Additional Materials | |

o | Soliciting Material Pursuant to Rule14a-12 | |

MIDWAY GAMES INC. | ||||

(Name of Registrant as Specified In Its Charter) | ||||

(Name of Person(s) Filing Proxy Statement, if other than the Registrant) | ||||

| Payment of Filing Fee (Check the appropriate box): | ||||

ý | No fee required | |||

o | Fee computed on table below per Exchange Act Rules 14a-6(i)(1) and 0-11 | |||

| (1) | Title of each class of securities to which transaction applies: | |||

| (2) | Aggregate number of securities to which transaction applies: | |||

| (3) | Per unit price or other underlying value of transaction computed pursuant to Exchange Act Rule 0-11 (set forth the amount on which the filing fee is calculated and state how it was determined): | |||

| (4) | Proposed maximum aggregate value of transaction: | |||

| (5) | Total fee paid: | |||

o | Fee paid previously with preliminary materials. | |||

o | Check box if any part of the fee is offset as provided by Exchange Act Rule 0-11(a)(2) and identify the filing for which the offsetting fee was paid previously. Identify the previous filing by registration statement number, or the Form or Schedule and the date of its filing. | |||

(1) | Amount Previously Paid: | |||

| (2) | Form, Schedule or Registration Statement No.: | |||

| (3) | Filing Party: | |||

| (4) | Date Filed: | |||

MIDWAY GAMES INC.

NOTICE OF ANNUAL MEETING OF STOCKHOLDERS

To Be Held on June 10, 2004

To the Stockholders of

MIDWAY GAMES INC.

NOTICE IS HEREBY GIVEN that the Annual Meeting of Stockholders of Midway Games Inc. ("Midway") will be held on Thursday, June 10, 2004, at 10:00 a.m. Central Time at the Harris Bank Building Auditorium, 8th Floor, 115 South La Salle Street, Chicago, Illinois 60603, to consider and act upon the following matters:

- 1.

- To elect eight directors to serve until our next annual meeting and until their successors are duly elected and shall qualify;

- 2.

- To ratify the appointment of Ernst & Young LLP as independent auditors for the fiscal year ending December 31, 2004; and

- 3.

- To transact such other business as may properly come before the meeting or any adjournment or adjournments of the meeting.

The close of business on April 20, 2004 has been fixed as the record date for the determination of stockholders entitled to notice of and to vote at the meeting and any adjournments thereof. A list of the stockholders entitled to vote at the annual meeting will be open to the examination of any stockholder of Midway for any purpose germane to the annual meeting during regular business hours at the offices of Midway for the ten-day period prior to the annual meeting and will be available at the meeting.

Sumner M. Redstone and National Amusements Inc., as of the record date, beneficially owned approximately 45.2% of the voting power of our common stock. Mr. Redstone is Chairman, Chief Executive Officer and controlling stockholder of National Amusements. Therefore, they own enough of our common stock to virtually determine the outcome of the election of directors and ratification of Ernst & Young LLP.

YOU ARE REQUESTED, WHETHER OR NOT YOU PLAN TO BE PRESENT AT THE ANNUAL MEETING, TO MARK, DATE, SIGN AND RETURN PROMPTLY THE ACCOMPANYING PROXY IN THE ENCLOSED ENVELOPE. NO POSTAGE NEED BE AFFIXED IF MAILED IN THE UNITED STATES.

| By Order of the Board of Directors, | ||

DEBORAH K. FULTON Senior Vice President, Secretary and General Counsel | ||

Chicago, Illinois May 10, 2004 |

ANNUAL MEETING OF STOCKHOLDERS

OF

MIDWAY GAMES INC.

PROXY STATEMENT

Introduction

Midway Games Inc. ("we", "us" or "Midway") is furnishing this proxy statement to you in connection with the solicitation by the Board of Directors of proxies to be voted at our Annual Meeting of Stockholders. The meeting is scheduled to be held at the Harris Bank Building Auditorium, 8thFloor, 115 South La Salle Street, Chicago, Illinois 60603, on Thursday, June 10, 2004, at 10:00 a.m. Central Time, or at any proper adjournments.

If you properly execute and return your proxy card, it will be voted in accordance with your instructions. If you return your signed proxy but give us no instructions as to one or more matters, the proxy will be voted on those matters in accordance with the recommendations of the Board as indicated in this proxy statement. You may revoke your proxy, at any time prior to its exercise, by written notice to us, by submission of another proxy bearing a later date or by voting in person at the meeting. Your revocation will not affect a vote on any matters already taken. Your mere presence at the meeting will not revoke your proxy.

The mailing address of our principal executive offices is 2704 West Roscoe Street, Chicago, Illinois 60618. We are mailing this proxy statement and the accompanying form of proxy to our stockholders on or about May 12, 2004.

Only holders of our common stock, $.01 par value per share, of record at the close of business on April 20, 2004 (the "Record Date") will be entitled to vote at our annual meeting or any adjournments. There were 68,218,229 shares of our common stock outstanding on the Record Date (excluding 2,930,000 treasury shares). Each share of our common stock entitles the holder to one vote on each matter at the meeting.

Approval of Proposals

The Board of Directors recommends a voteFOR each of the following proposals:

- 1.

- The election of the 8 nominees for the Board of Directors; and

- 2.

- The ratification of the appointment of Ernst & Young LLP as independent auditors for the fiscal year ending December 31, 2004.

The affirmative vote of a plurality of the shares of our common stock present in person or by proxy is required to elect directors, and the affirmative vote of a majority of our common stock present in person or by proxy is required to ratify the appointment of Ernst & Young LLP.

As of the Record Date, Sumner M. Redstone and National Amusements Inc. beneficially owned approximately 45.2% of our outstanding common stock. See "Security Ownership of Certain Beneficial Owners and Management" below. Mr. Redstone and National Amusements requested that Shari E. Redstone and Kenneth D. Cron be nominated for election to our Board of Directors and indicated to us that they thought it would be appropriate for us to reduce the size of our Board to no more than eight directors and indicated that the other Board changes described in this proxy statement are appropriate. Mr. Redstone and National Amusements own enough of our outstanding common stock to virtually determine the outcome of any vote taken at the meeting.

Sumner Redstone and National Amusements have been our largest stockholders for many years. As of the record date for our 2003 Annual Meeting, their ownership represented just under 30% of our outstanding common stock. Since that time, Mr. Redstone and National Amusements have increased their ownership of our outstanding common stock as of May 7, 2004 to 49.9% through open market purchases. According to their SEC filings, purchases of our common stock by Mr. Redstone were made by using his personal funds as well as through margin and cash accounts at Bear Stearns and purchases of our common stock by National Amusements were made through its margin account at Bear Stearns. Prior to April 2004, Mr. Redstone had not sought representation on our board. During April 2004, Mr. Redstone and National

Amusements made several filings with the SEC stating, among other things, that they were reviewing strategic alternatives for their investment in our common stock including purchasing a significant amount of additional shares, seeking representation on our Board of Directors and/or acquiring control of us. In another filing with the SEC, Mr. Redstone stated that, subject to regulatory approvals, he intends to increase his ownership to at least 60%.

Mr. Redstone and National Amusements have requested that two persons designated by them, Shari E. Redstone and Kenneth D. Cron, be nominated for election as directors and advised us that they think it appropriate that the size of our Board of Directors be reduced from 11 to not more than 8 members and that the 6 incumbent directors who are standing for re-election at the meeting also be nominated for re-election. As reflected in this proxy statement, our Board reduced the size of our Board and nominated Ms. Redstone, Mr. Cron and the 6 incumbent directors indicated by Mr. Redstone and National Amusements.

SECURITY OWNERSHIP OF CERTAIN BENEFICIAL OWNERS AND MANAGEMENT

Principal Stockholders

The following table sets forth information as of the Record Date, except as otherwise noted in the footnotes, about persons which, to our knowledge, beneficially own more than 5% of the outstanding shares of our common stock:

| Name and Address of Beneficial Owner | Number of Shares of Common Stock Beneficially Owned | Percentage of Outstanding Common Stock (1) | |||

|---|---|---|---|---|---|

| Sumner M. Redstone and National Amusements, Inc. 200 Elm Street Dedham, MA 02026 | 30,824,453(2 | ) | 45.2 | % | |

Phyllis G. Redstone c/o Marta B. van Dam, Esq. Gadsby Hannah LLP 225 Franklin Street Boston, MA 02110 | 3,659,783(3 | ) | 5.4 | % |

- (1)

- Percentage calculations are based on 68,218,229 shares outstanding on the Record Date, excluding treasury shares.

- (2)

- Based upon a Form 4 filed with the SEC by Sumner M. Redstone on April 21, 2004, Mr. Redstone and National Amusements, Inc., a Maryland corporation, held direct and indirect beneficial ownership of 26,701,682 and 4,122,771 shares (shared voting power), respectively, of our common stock. Mr. Redstone's shares include 17,500 shares held by his wife, Paula Redstone, with respect to which shares Mr. Redstone disclaims beneficial ownership. As a result of his stock ownership in National Amusements, Mr. Redstone is deemed the beneficial owner of the shares of common stock owned by National Amusements. Mr. Redstone stated in amendment 35 to his Schedule 13D filed with the SEC on April 13, 2004 that he was reviewing strategic alternatives with respect to his investment in our common stock including purchasing a significant amount of additional shares, seeking representation on our Board of Directors and/or acquiring control of us. On April 28, 2004 he filed amendment 41 to his Schedule 13D stating that he intends to acquire at least 60% of our outstanding voting stock, depending on price and availability of our stock and surrounding market conditions. Since the Record Date, Mr. Redstone and National Amusements have increased their holdings to 34,102,253 shares of our common stock, or 49.9% of our outstanding common stock as of May 7, 2004.

- (3)

- Based upon Schedule 13D filed with the SEC on August 8, 2002. The filer reported beneficial ownership, with sole dispositive and voting power, of 3,659,783 shares. Ms. Phyllis Redstone acquired

2

the shares from Sumner M. Redstone on July 30, 2002 under a divorce settlement. Phyllis Redstone is the mother of Shari E. Redstone.

The table above does not include information about shares of common stock owned, or that may be considered to be beneficially owned, by Portside Growth and Opportunity Fund or by Smithfield Fiduciary LLC. This is because these holders do not currently own more than 4.99% of our outstanding common stock and, under the terms of the securities beneficially owned by them that are convertible or exercisable into shares of our common stock, these holders may not convert or exercise these securities to the extent that the conversion or exercise would cause either of them to hold outstanding common stock representing more than 4.99% of our common stock outstanding following such conversion or exercise.

Subject to the 4.99% limitation and to antidilution and other adjustment rights, Portside owns Series D preferred stock convertible into 4,794,521 shares of common stock, warrants associated with the Series D preferred stock exercisable for 570,500 shares of common stock, warrants associated with our Series B preferred stock exercisable for 375,000 shares of common stock and has exercised its right to purchase additional Series D preferred stock that will be convertible into 1,562,500 shares of common stock. As of April 21, 2004, Portside reported to us that it does not own any shares of our common stock. Ramius Capital Group, LLC is the investment adviser of Portside Growth and Opportunity Fund and consequently has voting control and investment discretion over securities held by Portside. Ramius Capital disclaims beneficial ownership of the securities held by Portside. Peter A. Cohen, Morgan B. Stark, Thomas W. Strauss and Jeffrey Solomon are the sole managing members of C4S& Co., LLC, the sole managing member of Ramius Capital.

Subject to the 4.99% limitation and to antidilution and other adjustment rights, Smithfield owns Series D preferred stock convertible into 4,539,658 shares of common stock, warrants associated with the Series D preferred stock exercisable for 407,500 shares of common stock and warrants associated with our Series B preferred stock exercisable for 1,180,161 shares of common stock. None of these shares of common stock have been issued. In addition, as of April 14, 2004, Smithfield reported to us ownership of 450,000 shares of our common stock outright. Highbridge Capital Management, LLC is the trading manager of Smithfield Fiduciary LLC and consequently has voting control and investment discretion over securities held by Smithfield. Glenn Dubin and Henry Swieca control Highbridge. Each of Highbridge, Glenn Dubin and Henry Swieca disclaims beneficial ownership of the securities held by Smithfield.

Until June 2005, Portside and Smithfield, together with the other holders of our Series D preferred stock, have the right to purchase a total of up to one third of any securities that we offer on the same terms as we offer them to any other purchasers. This right does not apply in the case of underwritten public offerings, issuances at or above the prevailing market price to investors for a primary purpose other than to raise capital, or offerings under our benefit plans and in other specified instances.

Stockholdings of Management

The following table sets forth, as of the Record Date, except as otherwise noted in the footnotes, information about the beneficial ownership of our common stock by each of our directors, nominees as

3

directors and the executive officers named in the Summary Compensation Table below and by all of our directors and executive officers as a group:

| Name of Beneficial Owner | Number of Shares of Common Stock Beneficially Owned (1) | Percentage of Outstanding Common Stock (1) | ||||

|---|---|---|---|---|---|---|

| Harold H. Bach, Jr. | 340,193 | (2) | * | |||

| William C. Bartholomay | 141,983 | (3) | * | |||

| Mark S. Beaumont | 41,250 | (4) | * | |||

| Kenneth D. Cron | -0 - | 0 | % | |||

| Kenneth J. Fedesna | 381,112 | (5) | * | |||

| William E. McKenna | 97,324 | (3) | * | |||

| Norman J. Menell | 112,569 | (6) | * | |||

| Louis J. Nicastro | 110,610 | (6) | * | |||

| Neil D. Nicastro | 3,471,585 | (7) | 4.9 | % | ||

| David W. Nichols | 95,901 | (8) | * | |||

| Thomas E. Powell | 198,403 | (9) | * | |||

| Shari Redstone | -0 - | (10) | 0 | %(10) | ||

| Harvey Reich | 112,054 | (11) | * | |||

| Ira S. Sheinfeld | 116,864 | (6) | * | |||

| Robert N. Waxman | 25,000 | (12) | * | |||

| Jay N. Whipple III | 75,000 | (12) | * | |||

| Richard D. White | 133,574 | (13) | * | |||

| David F. Zucker | 714,143 | (14) | 1.0 | % | ||

| Directors and Executive | ||||||

| Officers as a group (19 persons) | 6,365,002 | (15) | 8.6 | % | ||

- *

- Less than 1%

- (1)

- Under Rule 13d-3(d)(1) of the Securities Exchange Act of 1934, shares underlying options and warrants are deemed to be beneficially owned if the holder of the option or warrant has the right to acquire beneficial ownership of the underlying shares within 60 days. Percentage calculations are based on 68,218,229 shares outstanding on the Record Date, excluding treasury shares.

- (2)

- Includes 293,905 shares of common stock underlying stock options.

- (3)

- Includes 96,613 shares of common stock underlying stock options.

- (4)

- Includes 41,250 shares of common stock underlying stock options.

- (5)

- Includes 328,906 shares of common stock underlying stock options.

- (6)

- Includes 95,063 shares of common stock underlying stock options.

- (7)

- Represents 50,000 shares of common stock underlying warrants, 2,431,164 shares of common stock underlying stock options and 990,421 shares of common stock owned outright. Does not include an aggregate of 607,846 shares of our common stock issuable to Mr. Nicastro under the terms of his severance agreement. See "Employment Agreements" below.

- (8)

- Includes 92,682 shares of common stock underlying stock options.

- (9)

- Includes 197,903 shares of common stock underlying stock options.

- (10)

- As a director, president and shareholder of National Amusements, Ms. Redstone may be deemed a beneficial owner of the 4,576,471 shares (6.71%) of common stock owned by National Amusements as of May 6, 2004.

- (11)

- Includes 95,777 shares of common stock underlying stock options.

- (12)

- Includes 25,000 shares of common stock underlying stock options.

4

- (13)

- Includes 95,838 shares of common stock underlying stock options.

- (14)

- Includes 569,143 shares of common stock underlying stock options. Also includes 125,000 shares of common stock issued under a Restricted Stock Agreement between Mr. Zucker and Midway dated as of May 6, 2003. The period of restriction with respect to 83,333 of these shares shall lapse in eight equal quarterly installments on the first day of each August, November, February and May, beginning on August 1, 2004, if Mr. Zucker continues to be employed by us on these respective dates.

- (15)

- Includes an aggregate of 4,871,250 shares of common stock underlying stock options, and 50,000 shares of common stock underlying warrants.

PROPOSAL 1—ELECTION OF DIRECTORS

Our Board of Directors currently consists of 11 directors. Mr. Redstone and National Amusements have requested that Ms. Shari E. Redstone and Mr. Kenneth D. Cron be nominated for election as directors, and have indicated they think it appropriate that we reduce the size of our Board to no more than 8 directors and that the other 6 nominees named below who are incumbent directors be nominated for election as directors.

After consideration of Mr. Redstone's and National Amusement's views, the Board determined to reduce the size of the Board to 8 members effective at the Annual Meeting. The following 8 persons have been nominated by the Board of Directors for election to serve until the next annual meeting of stockholders and until their respective successors are elected and shall qualify or until their earlier resignation or removal. Six of the nominees are currently directors. Neil D. Nicastro is the son of Louis J. Nicastro. Shari E. Redstone is the daughter of Sumner M. Redstone and is President and a Director of National Amusements. If any of the nominees are unable to serve or refuse to serve as directors, an event which the Board does not anticipate, the proxies will be voted in favor of those nominees who do remain as candidates, except as you otherwise specify, and may be voted for substituted nominees.

| Name of Director Nominee (Age) | Position with Company and Principal Occupation | Director Since | ||

|---|---|---|---|---|

| Harold H. Bach, Jr.(71) | Director | 1996 | ||

William C. Bartholomay(75) | Director; Group Vice Chairman, Willis Group Holdings, Inc. | 1996 | ||

Kenneth D. Cron(47) | Nominee as Director; Director and Interim Chief Executive Officer of Computer Associates International Inc. | N/A | ||

Louis J. Nicastro(75) | Director; Chairman of the Board of WMS Industries Inc. | 1988 | ||

Neil D. Nicastro(47) | Director and Chairman of the Board | 1988 | ||

Shari E. Redstone(50) | Nominee as Director; Director and President, National Amusements. | N/A | ||

Ira S. Sheinfeld(66) | Director; Attorney, Hogan & Hartson L.L.P. | 1996 | ||

Robert N. Waxman(67) | Director; Principal, Corporate Finance Advisory | 2003 |

Harold H. Bach, Jr. joined our Board in 1996 and served as our Chief Financial Officer and an Executive Vice President from 1996 to September 2001, when he retired. Mr. Bach served as our Senior Vice President—Finance and Chief Financial Officer from 1990 to 1996, and he served as our Treasurer from 1994 to April 2001. Mr. Bach also served as Vice President—Finance, Chief Financial and Chief

5

Accounting Officer of WMS Industries Inc., our former parent company, for over five years until September 1999. Mr. Bach was a partner in the accounting firms of Ernst & Young (1989-1990) and Arthur Young & Company (1967-1989). Mr. Bach is a director and audit committee member of WMS.

William C. Bartholomay joined our Board in 1996. Mr. Bartholomay was appointed Group Vice Chairman of Willis Group Holdings, Inc. and Vice Chairman of its principal U.S. subsidiary, Willis North America, a global insurance brokerage, in August 2003. For more than five years previous to this appointment, Mr. Bartholomay served as President and a director of Near North National Group, insurance brokers in Chicago, Illinois. He has served as Vice Chairman of Turner Broadcasting System, Inc., a division of AOL-Time Warner, Inc. since 1994, having also held that office during the period 1976-1992. He is Chairman Emeritus of the Board and Chairman of the Executive Committee of the Atlanta Braves baseball team. Mr. Bartholomay is a director of WMS. He is also a director and audit committee member of International Steel Group Inc.

Kenneth D. Cron has been nominated for election as a director at the request of Mr. Redstone and National Amusements. Mr. Cron has been serving as interim Chief Executive Officer of Computer Associates International Inc. since April 2004, and has served as a Director of Computer Associates since 2002. From 2001 to 2004, Mr. Cron was Chairman and CEO of Vivendi Universal Games, Inc., a global leader in the publishing of online, PC and console-based interactive entertainment and a division of Vivendi Universal, S.A. In 2001, Mr. Cron served as Chief Executive Officer of the Flipside Network, now a part of Vivendi Universal Net USA. He was Chief Executive Officer of Uproar Inc. from September 1999 to March 2001, when Uproar was acquired by Flipside. Mr. Cron worked at CMP Media, Inc. from 1978 to June 1999. When at CMP Media, as the President of Publishing, Mr. Cron had responsibility for the company's United States businesses, including its print publications, trade shows/conferences and online services.

Louis J. Nicastro joined our Board in 1988. He was the Chief Executive Officer of WMS from 1998 until June 2001 and was also its President from 1998 to April 2000. He has served as Chairman of the Board of WMS since its incorporation in 1974. Mr. Nicastro also served WMS as Chief Executive Officer or Co-Chief Executive Officer from 1974 to 1996 and as President (1985-1988, 1990-1991), among other executive positions. Mr. Nicastro also served as Chairman of the Board and Chief Executive Officer of WHG Resorts & Casinos Inc. and its predecessors from 1983 until 1998. He also served as our Chairman of the Board and Chief Executive Officer or Co-Chief Executive Officer from 1988 to 1996 and our President from 1988 to 1991.

Neil D. Nicastro joined our Board in 1988 and was our President and Chief Operating Officer from 1991 until May 2003. In 1996, Mr. Nicastro became our Chairman of the Board and Chief Executive Officer, having served as Co-Chief Executive Officer since 1994. Mr. Nicastro also served in other executive positions for us in the past. Mr. Nicastro has served as a director of WMS since 1986 and as consultant to WMS since 1998. Mr. Nicastro became sole Chief Executive Officer of WMS in 1996, Co-Chief Executive Officer in 1994, President in 1991 and Chief Operating Officer in 1991. Mr. Nicastro resigned from his offices with WMS in 1998 to devote his full business time to Midway.

Shari E. Redstone has been nominated for election as a director at the request of Mr. Redstone and National Amusements. Ms. Redstone has been President of National Amusements since January 2000 and served as Executive Vice President of National Amusements from 1994 to January 2000. She is also a director of National Amusements. National Amusements, a closely held company, operates cinemas in the United States, the United Kingdom and Latin America and is also the largest shareholder of Viacom Inc. Ms. Redstone is Chairman and Chief Executive Officer of Rising Star Media, a company established in partnership wth National Amusements to build luxury-style cinemas in Russia. Ms. Redstone practiced law from 1978 to 1993, with her practice including corporate law, estate planning and criminal law. Ms. Redstone is a member of the Board of Directors and Executive Committee for the National Association of Theatre Owners, Co-Chairman and Co-Chief Executive Officer of MovieTickets.com, Inc., and Chairman and Chief Executive Officer of CineBridge Ventures, Inc. She is a member of the board of several charitable organizations, including the Board of Trustees at Dana Farber Cancer Institute, the

6

Board of Directors at Combined Jewish Philanthropies and the Board of Directors of the John F. Kennedy Library Foundation, and is a former member of the Board of Overseers at Brandeis University and the Board of Trustees at Tufts University. Ms. Redstone has served as a Director of Viacom Inc. since 1994.

Ira S. Sheinfeld joined our Board in 1996. He has been a partner of the law firm of Hogan & Hartson L.L.P., and its predecessor law firm, Squadron, Ellenoff, Plesent & Sheinfeld LLP, New York, New York for over five years. He is a director of WMS.

Robert N. Waxman, CPA, joined our Board on December 31, 2003. Mr. Waxman is a Principal of Corporate Finance Advisory, a New York-based accounting and consulting firm, which he founded in 1992. Mr. Waxman was a partner with Deloitte & Touche LLP, an international accounting and consulting firm, from 1962 to 1991 where he served as National Director of SEC Practice, and partner in charge of the Financial Services Group, among other positions. He is a member of the Board of Directors of the New York State Society of CPA's, and serves on the editorial board of the CPA Journal and on the audit committee of a large not-for-profit organization.

Required Vote

The affirmative vote of a plurality of the shares of our common stock present in person or by proxy at the annual meeting is required to elect the directors.

THE BOARD RECOMMENDS THAT YOU VOTE "FOR" THE NOMINEES FOR ELECTION AS DIRECTORS.

7

The Board of Directors

Our Board of Directors is our ultimate decision-making body, responsible for overseeing our affairs, except with respect to those matters reserved to the stockholders. The Board has adopted Corporate Governance Principles and a Code of Business Conduct and Ethics, each of which can be viewed atwww.investor.midway.com. These documents describe the responsibilities of our directors and other key corporate governance matters. We will provide a copy of these documents to stockholders, without charge, upon written request addressed to Midway Games Inc., 2704 West Roscoe Street, Chicago, IL 60618, Attention: Investor Relations.

The listing standards of the New York Stock Exchange impose additional new requirements on our Board and its committees which become effective at our annual meeting. These standards include a requirement that

- •

- A majority of the members of our Board of Directors qualify as "independent" directors who have no material relationship with us other than serving as a director and who meet the other specified requirements of independence set forth in Section 303A.02 of the listing standards of the New York Stock Exchange;

- •

- We have a nominating and corporate governance committee composed entirely of independent directors; and

- •

- We have a compensation committee composed entirely of independent directors.

The New York Stock Exchange exempts a "controlled" company from the above three requirements. For these purposes, a controlled company is a company of which more than 50% of the voting power is held by an individual, a group or another company. If a controlled company chooses to take advantage of any of the exemptions, it must disclose its election to do so, state that it is a controlled company and the basis for its determination in its annual proxy statement. If Mr. Redstone's ownership of our common stock exceeds 50%, we will be a controlled company. No determination has been made as to whether we will choose to take advantage of any exemptions under the New York Stock Exchange listing standards which may be available.

It has been our policy and, unless a controlled company exemption is subsequently claimed, it is a requirement of the listing standards of the New York Stock Exchange as of the annual meeting, that a majority of the members of our Board must qualify as "independent" directors who have no material relationship with us, other than serving as a director and who otherwise qualify as independent under the applicable provisions of the Securities Exchange Act of 1934 and the rules promulgated thereunder and the applicable rules of the New York Stock Exchange. Our Board has adopted the new director "independence" tests set forth in Section 303A.02 of the New York Stock Exchange listing standards as the basis for the Board to determine independence of a director or a nominee as director. Our Board has determined that all of the existing members of our Board of Directors and the two new nominees as directors are "independent" under those tests, except for Neil D. Nicastro and Louis J. Nicastro, and therefore such directors and nominees are independent in accordance with our policies. In addition, our directors must satisfy other qualification standards, as discussed below under the heading "Nominating and Corporate Governance Committee Policies." None of our 8 nominees is an officer or employee of Midway.

To assist it in carrying out its duties, the Board has delegated specific authority to several committees.

During fiscal 2003, the Board held 12 meetings. Each director attended at least 75% of the aggregate number of meetings of the Board and all committees on which he served during the fiscal year.

Director Compensation

We pay a fee of $32,500 per year to each of our directors. A director who serves as the chairman of the Compensation Committee or Stock Option Committee of the Board receives a further fee of $2,500 per

8

year for his services in that capacity. A director who serves as the chairman of the Nominating and Corporate Governance Committee of the Board receives a further fee of $7,500 per year for his services in that capacity and each other member of that Committee receives an additional fee of $5,000 per year. A director who serves as the chairman of the Audit Committee of the Board receives a further fee of $20,000 per year for his services in that capacity and each other member of that committee receives an additional fee of $15,000 per year.

During fiscal 2002, each of our directors elected to reduce his fiscal 2003 fees under the salary and director fee reduction/stock option program in exchange for options to purchase our common stock. These options vested during fiscal 2003. In addition, some of our directors are eligible to receive reimbursement for certain health insurance costs under our Exec-U-Care insurance program. In fiscal 2003, we paid the following amounts to directors under this program: $4,826 to Harold H. Bach Jr., $23,697 to Neil D. Nicastro, and $4,350 to Richard D. White.

Our directors may also receive options to purchase shares of common stock under our stock option plans. These options are generally granted at 100% of market value on the date of grant. On September 19, 2003, each of the following directors was granted an option to purchase 25,000 shares of our common stock, at an exercise price of $3.15: Messrs. N. Nicastro, L. Nicastro, Bach, Bartholomay, McKenna, Menell, Reich, Sheinfeld and White. In addition, on October 13, 2003, Mr. Neil D. Nicastro, Chairman of our Board, was granted an option to purchase 150,000 shares of our common stock at an exercise price of $2.93.

Committees of the Board of Directors

We have the following standing committees: Audit Committee; Nominating and Corporate Governance Committee; Stock Option Committee; and Compensation Committee. The Board of Directors has determined that all of the members of these committees are "independent" directors as that term is defined under the current NYSE listing standards. As discussed above, when we become a controlled company, we may choose to have directors who are not "independent" elected to the Nominating and Corporate Governance Committee and the Compensation Committee.

Our directors, none of whom are part of management, hold regular executive sessions without management being present. The Chairman of the Board, who is not an executive officer, presides at these meetings.

TheAudit Committee is composed of four independent directors (as independence is defined in Section 303.01(B) of the NYSE listing standards): Messrs. McKenna (Chairman), Bartholomay, Waxman and White. The Board has determined that each of Messrs. McKenna, Waxman and White is an audit committee "financial expert". In addition, each member of our Audit Committee is financially literate, in the Board's determination, and satisfies the definition of "independence" to be required of audit committee members under the new NYSE listing standards. The composition of this Committee will change after the Annual Meeting, but all members of the Committee will continue to be independent, all members will continue to be financially literate and it is expected that at least one member will be a "financial expert".

This Committee meets periodically with the independent auditors and internal personnel to: (1) consider the adequacy of internal accounting controls, our internal audit function and finance department staffing, (2) receive and review the recommendations of the independent auditors, (3) select, engage and review the performance of the independent auditors, (4) review and approve the scope of the audit and determine the compensation of the independent auditors, (5) pre-approve permitted non-audit fees and services, (6) review our consolidated financial statements, (7) receive and review confidential concerns regarding questionable accounting or auditing matters, (8) oversee our compliance with legal and regulatory requirements, (9) discuss our policies with respect to risk assessment and risk management, and generally (10) review our accounting policies and to resolve potential conflicts between management and our independent auditors. The Board has adopted a written charter for this committee, and a copy of the charter is included as Appendix A to this proxy statement and is available on our website at

9

www.investor.midway.com. Additional copies of the Audit Committee charter are available in print without charge to any of our stockholders requesting such information by contacting us at: Investor Relations, Midway Games Inc., 2704 West Roscoe Street, Chicago, IL 60618. The report of this committee is set forth later in this proxy statement. During fiscal 2003, this Committee held 15 meetings.

TheNominating and Corporate Governance Committee is composed of Messrs. Menell (Chairman) and Bartholomay. This Committee identifies individuals qualified to become Board members and makes recommendations about the nomination of candidates for election to the Board, as discussed in greater detail below. In addition, this Committee makes recommendations regarding corporate governance policies and procedures and oversees the annual evaluation of the Board and management. The Nominating and Corporate Governance Committee operates under a written charter which is available on our website at www.investor.midway.com. Additional copies of the Nominating and Corporate Governance Committee charter are available in print without charge to any of our stockholders requesting such information by contacting us at: Investor Relations, Midway Games Inc., 2704 West Roscoe Street, Chicago, IL 60618. During fiscal 2003, this Committee held 1 meeting.

TheStock Option Committee is composed of Messrs. Reich (Chairman) and McKenna. This Committee (1) adopts, administers, approves and ratifies awards under our incentive-compensation and stock plans, (2) coordinates with the Compensation Committee regarding our CEO's equity compensation, (3) makes recommendations and coordinates with the Compensation Committee regarding the equity compensation of our other senior officers, and (4) determines the timing, pricing and the amount of option grants to be made under the provisions of our stock option plans. The joint report of this Committee and the Compensation Committee is set forth later in this proxy statement. The Stock Option Committee operates under a written charter which is available on our website at www.investor.midway.com. Additional copies of the Stock Option Committee charter are available in print without charge to any of our stockholders requesting such information by contacting us at: Investor Relations, Midway Games Inc., 2704 West Roscoe Street, Chicago, IL 60618. During fiscal 2003, this Committee held 2 meetings.

TheCompensation Committee is composed of Messrs. Bartholomay (Chairman), McKenna and Reich. This Committee (1) reviews and approves corporate goals and objectives relevant to the compensation of our CEO and our other senior officers, (2) reviews periodically the succession plans relating to the CEO and the other senior officers, (3) evaluates the CEO's performance and determines the compensation of the CEO, (4) makes recommendations to the Board with respect to compensation of the other senior officers, and (5) administers, approves and ratifies awards under incentive-compensation and other benefit plans. The joint report of this Committee and the Stock Option Committee is set forth later in this proxy statement. The Compensation Committee operates under a written charter which is available on our website at www.investor.midway.com. Additional copies of the Compensation Committee charter are available in print without charge to any of our stockholders requesting such information by contacting us at: Investor Relations, Midway Games Inc., 2704 West Roscoe Street, Chicago, IL 60618. During fiscal 2003, this Committee held 7 meetings.

Compensation Committee Interlocks and Insider Participation

During fiscal 2003, Messrs. Bartholomay (Chairman), McKenna and Reich served on our Compensation Committee, and Messrs. McKenna and Reich (Chairman) served on our Stock Option Committee. No member of our Compensation Committee or our Stock Option Committee is or was an employee or officer of Midway or any of its subsidiaries, and no officer, director or other person had any relationship required to be disclosed under this heading, except that Mr. Bartholomay is Group Vice Chairman of Willis Group Holdings, Inc. and Vice Chairman of Willis North America, Inc., insurance brokers, which we retained to provide insurance brokerage services during fiscal 2003 and have retained to provide insurance brokerage services during the current fiscal year.

10

Nominating and Corporate Governance Committee Policies

Our Nominating and Corporate Governance Committee has a written charter. A current copy of this charter is available on our website at www.investor.midway.com. All of the members of our Nominating and Corporate Governance Committee are independent, as independence is defined in the listing standards of the New York Stock Exchange.

The Process of Identifying and Evaluating Candidates for Directors

In selecting candidates for nomination for election to the Board at our annual meetings of stockholders, the Nominating and Corporate Governance Committee begins by determining whether the incumbent directors whose terms expire at the meeting desire and are qualified to continue their service on the Board. We are of the view that the continuing service of qualified incumbents promotes stability and continuity in the boardroom, giving us the benefit of the familiarity and insight into our affairs that our directors have accumulated during their tenure, while contributing to the Board's ability to work as a collective body.

If there are Board positions for which the Nominating and Corporate Governance Committee will not be re-nominating a qualified incumbent, the Nominating and Corporate Governance Committee will solicit recommendations for nominees from persons whom the Nominating and Corporate Governance Committee believes are likely to be familiar with qualified candidates, including members of the Board and senior management. The Nominating and Corporate Governance Committee may also engage a search firm to assist in identifying qualified candidates. The Nominating and Corporate Governance Committee will review and evaluate each candidate whom it believes merits serious consideration, taking into account all available information concerning the candidate, the qualifications for Board membership established by the Nominating and Corporate Governance Committee, the existing composition and mix of talent and expertise on the Board and other factors that it deems relevant. In conducting its review and evaluation, the Nominating and Corporate Governance Committee may solicit the views of management and other members of the Board and may, if deemed helpful, conduct interviews of proposed candidates.

The Nominating and Corporate Governance Committee will evaluate candidates recommended by stockholders in the same manner as candidates recommended by other persons, except that the Nominating and Corporate Governance Committee may consider, as one of the factors in its evaluation of stockholder-recommended candidates, the size and duration of the interest of the recommending stockholder or stockholder group in our equity securities. Mr. Redstone and National Amusements requested that Ms. Redstone and Mr. Cron be presented for election at the annual meeting and indicated that they thought it appropriate that the other 6 nominees be presented for election to the Board. The Board, rather than the Nominating and Corporate Governance Committee, approved the final list of nominees included in this proxy statement.

Qualifications of Directors

Under a policy formulated by our Nominating and Corporate Governance Committee, we generally require that all candidates for director be persons of integrity and sound ethical character and judgment, have no interests that materially conflict with ours or those of our stockholders generally, have meaningful business, governmental or technical experience and acumen and have adequate time to devote to service on the Board. We have also required that a majority of directors be independent; at least three of the directors must have the financial literacy necessary for service on the audit committee, and at least one of these directors must qualify as an audit committee financial expert.

Stockholder Recommendation of Candidates for Election as Directors

The Nominating and Corporate Governance Committee will consider recommendations for director nominations submitted by stockholders that individually or as a group have beneficial ownership of at least 3% of our common stock and have had such ownership for at least one year. Submissions must be made in accordance with the Committee's procedures, as outlined below and set forth in Appendix B to this proxy

11

statement. For each annual meeting of our stockholders, the Nominating and Corporate Governance Committee will accept for consideration only one recommendation from any stockholder or affiliated group of stockholders. The Nominating and Corporate Governance Committee will only consider candidates who satisfy our minimum qualifications for director, as outlined above and set forth on our website at www.investor.midway.com. The Committee did not require Mr. Redstone and National Amusements to comply with all of these procedures in view of their substantial ownership of our common stock.

Procedures for Stockholder Submission of Nominating Recommendations

A stockholder wishing to recommend to the Nominating and Corporate Governance Committee a candidate for election as director must submit the recommendation in writing, addressed to the Committee care of our corporate secretary at 2704 West Roscoe Street, Chicago, Illinois 60618. Submissions recommending candidates for election at an annual meeting of stockholders must be received no later than 120 calendar days prior to the first anniversary of the date of the proxy statement for the prior annual meeting of stockholders. In the event that the date of the next annual meeting of stockholders is more than 30 days following or preceding the first anniversary date of the annual meeting of stockholders for the prior year, the submission must be made a reasonable time in advance of the mailing of our next annual proxy statement. Each nominating recommendation must be accompanied by the information called for by our "Procedures for Stockholders Submitting Nominating Recommendations," which is attached as Appendix B to this Proxy Statement. This includes specified information concerning the stockholder or group of stockholders making the recommendation, the proposed nominee, any relationships between the recommending stockholder and the proposed nominee and the qualifications of the proposed nominee to serve as director. The recommendation must also be accompanied by the consent of the proposed nominee to serve if nominated and the agreement of the nominee to be contacted by the Nominating and Corporate Governance Committee, if the Nominating and Corporate Governance Committee decides in its discretion to do so.

Selection of 2004 Nominees

Six of the nominees listed on the accompanying proxy card are currently serving on our Board and are standing for reelection. Two of the nominees were recommended by Mr. Redstone and National Amusements, and Mr. Redstone and National Amusements indicated they thought it appropriate that the other 6 nominees be nominated for re-election. We did not receive any other recommendations from stockholders for nominees that are required to be identified in this proxy statement.

Stockholder Communications with Directors

Stockholders may communicate with our Board of Directors, any committee of the Board or any individual director, and any interested party may communicate with the non-management directors of the Board, by following the procedures set forth below.

Our acceptance and forwarding of communications to the directors does not imply that the directors owe or assume duties to persons submitting the communications, the duties of the directors being only those prescribed by applicable law.

All communications should be delivered either in writing addressed c/o Legal Department at 2704 West Roscoe Street, Chicago, Illinois 60618; or by e-mail toir@midway.com.

All communications must be accompanied by the following information:

- •

- if the person submitting the communication is a stockholder, a statement of the type and amount of our securities that the person holds;

- •

- if the person submitting the communication is not a stockholder and is submitting the communication to the non-management directors as an interested party, the nature of the person's interest in us;

12

- •

- any special interest, meaning an interest not in the capacity as a stockholder of ours, of the person in the subject matter of the communication; and

- •

- the address, telephone number and e-mail address, if any, of the person submitting the communication.

It is not appropriate to send the following types of communications to directors:

- •

- communications regarding individual grievances or other interests that are personal to the party submitting the communication and could not reasonably be construed to be of concern to our stockholders or other constituencies generally;

- •

- communications that advocate our engaging in illegal activities;

- •

- communications that, under community standards, contain offensive, scurrilous or abusive content; and

- •

- communications that have no rational relevance to our business or operations.

All communications that comply with the procedural requirements that are described here will be relayed to the directors. Communications addressed to directors may, at the direction of the directors, be shared with Company management.

Director Attendance at Annual Meetings

Each of the nominees is expected to be present at our annual meetings of stockholders, absent exigent circumstances that prevent his or her attendance. Where a director is unable to attend an annual meeting in person but is able to do so by electronic conferencing, we will arrange for the director's participation by means where the director can hear, and be heard, by those present at the meeting. At last year's annual meeting, seven of our nine directors attended in person, one director attended by electronic conferencing, and one of our directors was unable to attend due to exigent circumstances that prevented his attendance.

13

The following individuals were elected to serve in the capacities set forth below until the 2004 Annual Meeting of the Board of Directors and until their respective successors are elected and shall qualify.

| Name | Age | Position | ||

|---|---|---|---|---|

| David F. Zucker | 41 | President and Chief Executive Officer | ||

| Kenneth J. Fedesna | 54 | Executive Vice President — Product Development | ||

| Thomas E. Powell | 42 | Executive Vice President — Finance, Treasurer and Chief Financial Officer | ||

| Mark S. Beaumont | 48 | Senior Vice President — Entertainment | ||

| David W. Nichols | 50 | Senior Vice President — Administration and Operations | ||

| Steven M. Allison | 36 | Senior Vice President and Chief Marketing Officer | ||

| Deborah K. Fulton | 40 | Senior Vice President, Secretary and General Counsel | ||

| Miguel Iribarren | 38 | Vice President — Corporate Communications and Strategic Planning |

DAVID F. ZUCKER has been our President and Chief Executive Officer since May 6, 2003. Prior to that he was President and Chief Operating Officer of Playboy Enterprises, Inc., a men's lifestyle and adult entertainment company, from July 2002 to May 2003. From October 2000 to June 2002 he was President and Chief Executive Officer of Skillgames, LLC, and Managing Director of Walker Digital, LLC, online "pay for play" games companies. From February 1999 to September 2000 he was President and Chief Executive Officer of Diva Systems Corporation, an interactive television and information technology company. From 1988 to January 1999, Mr. Zucker served in a number of executive positions for The Walt Disney Company, a global entertainment company, including Executive Publisher ofTravel Agent Magazine; Manager of Current Series for ABC Television; Vice President of Programming for ESPN; and Executive Vice President of ESPN, Inc. and the Managing Director of ESPN International, Inc.

KENNETH J. FEDESNA has been our Executive Vice President — Product Development since May 2000 and was our Executive Vice President — Coin-Op Video from 1996 until May 2000. Mr. Fedesna served as our Vice President and General Manager from 1988 to 1996. He also served as Vice President and General Manager of Williams Electronics Games, Inc., a subsidiary of WMS, for over five years until August 1999. Mr. Fedesna served on our Board of Directors from 1996 until June 12, 2003.

THOMAS E. POWELL joined us as Executive Vice President—Finance and Treasurer in April 2001. In September 2001, he became our Executive Vice President — Finance, Treasurer and Chief Financial Officer. From 1997 to February 2001, Mr. Powell was employed by Dade Behring, Inc., a manufacturer of medical equipment, serving most recently as Vice President of Corporate Business Development, Strategic Planning. From 1991 to 1997, he was employed by Frito-Lay, a division of PepsiCo, Inc., ultimately serving as Director of Finance.

MARK S. BEAUMONT has served as our Senior Vice President — Entertainment since October 17, 2003. Prior to that, since January 2002, he served as our Senior Vice President — Publishing. He has served as Senior Vice President — Business Development of our wholly-owned subsidiary, Midway Games West Inc., since January 2000. Mr. Beaumont provided marketing and business development consulting services to Midway from October 1999 to January 2000. Prior to joining Midway, from 1996 to 1999, Mr. Beaumont was Executive Vice President and General Manager of U.S. Operations for Psygnosis, a division of Sony Corporation of America.

DAVID W. NICHOLS has served as our Senior Vice President — Administration and Operations since January 2002. He has served as Executive Vice President — Operations of our wholly-owned subsidiary, Midway Home Entertainment Inc., since February 2001. From May 2000 to February 2001, Mr. Nichols served as Vice President — Operations, of Midway Home Entertainment, after serving as that company's Vice President — Administration, from 1997 to May 2000. Mr. Nichols joined us in 1995 as Controller for Midway Home Entertainment.

14

STEVEN M. ALLISON joined us as Senior Vice President — Marketing and Chief Marketing Officer on December 22, 2003. Prior to joining us, he was Vice President of Marketing and Business Development, Atari/Infogrames, from December 2001 to December 2003. Prior to that, he served as Infogrames' Vice President of New Business Development and Production Content, from May 2000 to December 2001, Vice President of Licensing and Product Planning from October 1999 to April 2000, and Director of Product Marketing from April 1999 to October 1999. Before joining Infogrames, Mr. Allison was Director of Product Marketing at Accolade, Inc. from 1998 to April 1999.

DEBORAH K. FULTON has served as our Senior Vice President, Secretary and General Counsel since January 2002. She served us as Vice President, Secretary and General Counsel from May 2000 to January 2002. She was employed by us as Senior Counsel from 1998 until May 2000 and by WMS as Senior Counsel from 1994 to 1998. Formerly, she was employed by the law firm of Gardner Carton & Douglas from 1988 until 1994.

MIGUEL IRIBARREN has served as our Vice President, Corporate Communications and Strategic Planning, since February 2002. Prior to joining Midway, Mr. Iribarren was a Vice President, Research for Wedbush Morgan Securities. At Wedbush, where he worked from May 2000 to February 2002, Mr. Iribarren was responsible for research on the interactive entertainment industry. From 1993 to May 2000, Mr. Iribarren was employed by the Atlantic Richfield Corporation, an oil and gas company, in various finance and planning positions, ultimately serving as Manager, Corporate Finance.

The summary compensation table below sets forth the compensation earned during fiscal 2003, fiscal 2002, the transition period and fiscal 2001 by our former Chief Executive Officer, our current Chief Executive Officer and our four next most highly compensated executive officers.

| | Annual Compensation | Long Term Compensation Awards | |||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Name and Principal Position | Fiscal Year | Salary($) | Bonus($) | Other($)(1) | Restricted Stock Awards($) | Securities Underlying Options(#) | All Other Compensation($) | ||||||||

| Neil D. Nicastro Chairman of the Board(2) | 2003 2002 2001 2001 | * | 165,765 602,000 302,000 — | (3) (3) (3) (4) | — — — — | 27,286 15,665 2,318 10,680 | — — — — | 175,000 485,806 — — | 9,582,210 170,149 84,763 169,959 | (5) (6) (6) (6) | |||||

David F. Zucker President and Chief Executive Officer(7) | 2003 | 390,000 | 300,000 | (8) | 3,646 | 446,250 | (9) | 1,825,968 | — | ||||||

Kenneth J. Fedesna Executive Vice President — Product Development | 2003 2002 2001 2001 | * | 278,906 325,000 162,500 325,000 | (10) | — — — — | 26,303 27,525 3,600 11,209 | — — — — | 50,000 119,677 — — | 1,796 2,346 1,250 2,500 | (11) (11) (11) (11) | |||||

Thomas E. Powell Executive Vice President — Finance, Treasurer and Chief Financial Officer(12) | 2003 2002 2001 2001 | * | 238,541 300,000 129,231 46,154 | (13) | — — 87,692 — | 6,599 4,971 1,082 1,305 | — — — — | 50,000 142,903 — 100,000 | — — — — | ||||||

Mark S. Beaumont Senior Vice President — Entertainment(14) | 2003 2002 | 256,538 245,000 | — — | 63 — | — — | 60,000 25,000 | — — | ||||||||

David W. Nichols Senior Vice President — Administration and Operations(15) | 2003 2002 | 221,245 225,000 | (16) | — — | 4,971 1,868 | — — | 20,000 30,676 | — — | |||||||

- *

- Six-month transition period ended December 31, 2001.

15

- (1)

- Represents payments made under our health insurance programs.

- (2)

- Mr. Nicastro was our Chief Executive Officer, President and Chief Operating Officer until May 6, 2003. He remains as Chairman of the Board.

- (3)

- Mr. Nicastro's former employment agreement with us permitted him to receive advances against estimated bonus payments. Advances were made in the first six months of fiscal 2000 for bonuses accrued that were reversed in the second six months of fiscal 2000 totaling $984,000. Mr. Nicastro applied salary of $102,000 during fiscal 2003, $580,000 during fiscal 2002 and $302,000 during the transition period to the repayment of these advances. See "Certain Relationships and Related Transactions—Other Related Party Transactions" below. Fiscal 2003 amounts also represent a reduction in salary of $123,871 due to Mr. Nicastro's participation in our salary and director fee reduction/stock option program under the 2002 Non-Qualified Stock Option Plan.

- (4)

- On May 4, 2000, our Board granted to Mr. Nicastro an option to purchase 300,000 shares of our common stock in lieu of his salary for fiscal 2001, which he waived. The option expires on June 30, 2005. The exercise price is $7.00 per share.

- (5)

- Includes life insurance premiums of $2,211, $4,000,000 of severance paid to Mr. Nicastro pursuant to the terms of his severance agreement, $1,963,460 of deferred severance payable to Mr. Nicastro pursuant to the terms of his severance agreement, $64,552 of interest due to Mr. Nicastro on the deferred severance, $110,311 paid to Mr. Nicastro, representing the cash surrender value of his life insurance policies and $175,895 equal to conversion value of Mr. Nicastro's deferred severance in the event that Mr. Nicastro elects to have his deferred severance paid to him in shares of common stock. The remaining $3,265,781 represents amounts accrued for Mr. Nicastro's retirement benefits, and not yet paid, under the terms of Mr. Nicastro's severance agreement. See "Employment Agreements" below.

- (6)

- Includes life insurance premiums of $2,677 for fiscal 2002, $1,027 for the transition period and $2,091 for fiscal 2001. The remaining amounts represent amounts accrued for Mr. Nicastro's retirement benefits, and not yet paid, under the terms of Mr. Nicastro's former employment agreement. Pursuant to a letter agreement amending Mr. Nicastro's former employment agreement on October 30, 2000, Mr. Nicastro received contractual retirement benefits in the form of 607,846 shares of our common stock to be delivered to him over time beginning upon the later to occur of (1) his 45th birthday (October 25, 2001), or (2) the date of his termination from our employ. On October 30, 2000, we valued these retirement shares at $3,950,999, determined by multiplying 607,846 shares by $6.50, the closing price of our common stock on the NYSE on that date. For accrual purposes, we also assumed that Mr. Nicastro's employment with us would terminate on his 65th birthday, October 25, 2021, which was 260 months after October 2000. Immediately prior to entering into the October 30, 2000 letter agreement, we had recorded on our books an accrual in the amount of $322,362 which related to contractual retirement benefits afforded to Mr. Nicastro in earlier agreements. The retirement benefits of those earlier agreements were superceded by the October 30, 2000 letter agreement. Therefore, we applied the existing accrual balance to the $3,950,999 fair value of the Retirement Shares, leaving a remaining balance of $3,628,637. Dividing the $3,628,637 balance by the estimated 260 months, we calculated an accrual of $13,956 per month for Mr. Nicastro. These amounts accrued for each year are reflected in this column of the Summary Compensation Table. See "Employment Agreements" below.

- (7)

- Mr. Zucker joined Midway on May 6, 2003.

- (8)

- Represents a $150,000 signing bonus under Mr. Zucker's employment agreement, and an additional bonus of $150,000 received in December 2003.

- (9)

- Represents the fair value of the restricted stock award granted to Mr. Zucker on May 6, 2003 pursuant to his restricted stock agreement, calculated by multiplying the 125,000 restricted shares of common stock by $3.57, the closing price of our common stock on the NYSE on that date. See "Employment Agreements" below.

- (10)

- Mr. Fedesna reduced his fiscal 2003 salary by $46,451 in connection with his participation in the salary and director fee reduction/stock option program under the 2002 Non-Qualified Stock Option Plan.

- (11)

- Represents life insurance premiums.

- (12)

- Mr. Powell joined Midway on April 9, 2001.

- (13)

- Mr. Powell reduced his fiscal 2003 salary by $61,935 in connection with his participation in the salary and director fee reduction/stock option program under the 2002 Non-Qualified Stock Option Plan.

- (14)

- Mr. Beaumont served as our Senior Vice President — Publishing, from January 30, 2002 to October 17, 2003, and since that date, he has served as our Senior Vice President — Entertainment.

- (15)

- Mr. Nichols has served as our Senior Vice President — Administration and Operations, since January 30, 2002.

- (16)

- Mr. Nichols reduced his fiscal 2003 salary by $3,784 in connection with his participation in the salary and director fee reduction/stock option program under the 2002 Non-Qualified Stock Option Plan.

16

Stock Options

During fiscal 2003, the following options to purchase common stock were granted under our stock option plans to the persons named in the Summary Compensation Table:

OPTION GRANTS IN LAST FISCAL YEAR

| | | Individual Grants | | | | |||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| | | | Potential Realizable Value at Assumed Annual Rates of Stock Price Appreciation For Option Term(1) | |||||||||

| | | % of Total Options Granted to Employees in Fiscal Year | | | ||||||||

| Name | Options Granted(#) | Exercise Price ($/Share) | Expiration Date | |||||||||

| 5%($) | 10%($) | |||||||||||

| Neil D. Nicastro | 25,000 150,000 | 0.7 4.4 | 3.15 2.93 | 9/18/2013 10/12/2013 | 128,275 715,899 | 204,257 1,139,950 | ||||||

David F. Zucker | 500,000 1,000,000 25,000 300,968 | 14.8 29.6 0.7 8.9 | 3.57 3.57 3.15 2.92 | 5/5/2013 5/5/2013 9/18/2013 10/13/2013 | 2,907,577 5,815,154 128,275 1,431,516 | 4,629,830 9,259,661 204,257 2,279,450 | ||||||

Kenneth J. Fedesna | 50,000 | 1.5 | 2.35 | 8/12/2013 | 191,395 | 304,765 | ||||||

Thomas E. Powell | 50,000 | 1.5 | 2.35 | 8/12/2013 | 191,395 | 304,765 | ||||||

Mark S. Beaumont | 60,000 | 1.8 | 2.35 | 8/12/2013 | 229,674 | 365,718 | ||||||

David W. Nichols | 20,000 | 0.6 | 2.35 | 8/12/2013 | 76,558 | 121,906 | ||||||

- (1)

- The assumed appreciation rates are examples set by rules promulgated under the Securities Exchange Act of 1934 and are not related to or derived from the historical or projected prices of our common stock.

The following table sets forth information with respect to the number and year-end values of options to purchase common stock owned by the executive officers named in the Summary Compensation Table.

AGGREGATED OPTION EXERCISES IN LAST FISCAL YEAR

AND FISCAL YEAR-END OPTION VALUES

| Name | Shares Acquired on Exercise(#) | Value Realized($) | Number of Securities Underlying Unexercised Options at 12/31/03(#) Exercisable/Unexercisable | Value of Unexercised In-the-Money Options at 12/31/03($)(1) Exercisable/Unexercisable | ||||

|---|---|---|---|---|---|---|---|---|

| Neil D. Nicastro | — | — | 2,341,164/210,000 | 160,750/0 | ||||

David F. Zucker | — | — | 25,000/1,800,968 | 18,250/753,929 | ||||

Kenneth J. Fedesna | — | — | 308,906/90,000 | 0/76,500 | ||||

Thomas E. Powell | — | — | 162,903/130,000 | 0/76,500 | ||||

Mark S. Beaumont | — | — | 36,250/98,750 | 0/91,800 | ||||

David W. Nichols | — | — | 84,682/59,250 | 0/30,600 |

- (1)

- Based on the closing price of our common stock on the NYSE on December 31, 2003, which was $3.88 per share.

We have adopted a 2002 Non-Qualified Stock Option Plan, a 2002 Stock Option Plan, a 2000 Non-Qualified Stock Option Plan, a 1999 Stock Option Plan, a 1998 Stock Incentive Plan, a 1998 Non-Qualified Stock Option Plan and a 1996 Stock Option Plan. The plans provide for the granting of stock options to our directors, officers, employees, consultants and advisors.

17

The plans are intended to encourage stock ownership by our directors, officers, employees, consultants and advisors and thereby enhance their proprietary interest in us. Subject to the provisions of the plans, the Stock Option Committee determines which of the eligible directors, officers, employees, consultants and advisors receive stock options, the terms, including applicable vesting periods, of the options, and the number of shares for which options are granted.

The option price per share with respect to each option is determined by the Stock Option Committee and generally is not less than 100% of the fair market value of our common stock on the date the option is granted. The Plans each have a term of ten years, unless terminated earlier.

During fiscal 2002, we adopted a salary and director fee reduction/stock option program under the 2002 Non-Qualified Stock Option Plan. Employees and Directors who elected to participate in the program voluntarily elected to reduce their base salary or director's fee for a one-year period beginning in January 2003. For each dollar of salary or fee reduction, employees and directors were granted options to purchase one and one-half shares of our common stock at an exercise price of $5.29. The options vested over fiscal 2003 and are exercisable until September 2, 2012. The following table shows the reduction in fees and corresponding number of options granted to the participating directors:

| Name | Reduction in Fees($) | Options Granted(#) | |||

|---|---|---|---|---|---|

| Harold H. Bach Jr. | $ | 6,709 | 10,063 | ||

| William C. Bartholomay | $ | 7,742 | 11,613 | ||

| William E. McKenna | $ | 7,742 | 11,613 | ||

| Norman J. Menell | $ | 6,709 | 10,063 | ||

| Louis J. Nicastro | $ | 6,709 | 10,063 | ||

| Harvey Reich | $ | 7,185 | 10,777 | ||

| Ira S. Sheinfeld | $ | 6,709 | 10,063 | ||

| Richard D. White | $ | 7,225 | 10,838 | ||

The 1998 Stock Incentive Plan required that participants purchase shares of our common stock at the market price in order to be eligible to receive options.

The following is a summary of additional information about securities authorized for issuance under our equity compensation plans as of December 31, 2003:

EQUITY COMPENSATION PLAN INFORMATION

| | (a) | (b) | (c) | ||||

|---|---|---|---|---|---|---|---|

| Plan category | Number of securities to be issued upon exercise of outstanding options, warrants and rights | Weighted-average exercise price of outstanding options, warrants and rights | Number of securities remaining available for future issuance under equity compensation plans (excluding securities reflected in column (a)) | ||||

| Equity compensation plans approved by stockholders | 5,416,466 | $ | 11.18 | 1,713,823 | |||

| Equity compensation plans not approved by stockholders | 5,813,366 | $ | 5.62 | 2,100,909 | |||

| Total | 11,229,832 | $ | 8.30 | 3,814,732 | |||

The average exercise price of outstanding options, as of the Record Date, was approximately $8.38 per share. See "Security Ownership of Management" above for information about options held by officers and directors of Midway.

18

Midway Incentive Plan

Our executive officers, as well as our other senior employees, are also eligible for participation under the Midway Incentive Plan. The plan offers participants the opportunity to receive bonuses based on a combination of the following factors: (1) base salary; (2) the achievement of targets set for Midway's financial performance; and (3) management's evaluation of the individual and the degree to which he or she meets individual performance goals.

JOINT REPORT OF THE COMPENSATION COMMITTEE AND STOCK OPTION

COMMITTEE ON EXECUTIVE COMPENSATION FOR FISCAL 2003

The Compensation Committee is responsible for determining the compensation of our Chief Executive Officer and for making recommendations to the Board of Directors regarding the compensation of our other executive officers. To the extent that stock options form a portion of a compensation package, the Compensation Committee works together with the Stock Option Committee, which is responsible for making stock option grants and awards.

It is the policy of the Compensation and Stock Option Committees to provide attractive compensation packages to executive officers so as to motivate them to devote their full energies to our business, to reward them for their services and to align the interests of senior management with the interests of stockholders. Our executive compensation packages are comprised primarily of base salaries, annual contractual and discretionary cash bonuses, stock options and awards, and retirement and other benefits. It is the philosophy of the Compensation Committee that Midway be staffed with a small number of well-compensated executive officers. In establishing compensation levels, we consider compensation paid by our principal competitors. For 2003, we believe the base salaries and cash bonuses paid to our executive officers were generally lower than those paid by our principal competitors to similarly situated executives primarily due to the fact that our financial performance in 2003 was worse than that of our principal competitors.

In general, the level of base salary is intended to provide appropriate basic pay to executive officers taking into account their historical contributions to our business, each person's unique education, skills and value, the recommendation of the Chief Executive Officer and the competitive marketplace for executive talent.

The amount of any discretionary bonus is subjective but is generally based on our actual financial performance in the preceding fiscal year, the special contribution of the executive to this performance and the overall level of the executive's compensation including other elements of the compensation package. Contractual bonuses are likewise designed to give effect to one or more of these factors. For fiscal years beginning in 2003 and thereafter, we adopted the Midway Incentive Plan. In view of our poor financial performance in 2003, no bonuses were awarded to our executive officers, except that $300,000 was awarded to our new Chief Executive Officer, David F. Zucker, in accordance with his May 6, 2003 employment agreement.

Generally, the Stock Option Committee determines the size of stock option grants to our executive officers on an individual, discretionary basis in consideration of financial corporate results and each recipient's performance, contributions and responsibilities without assigning specific weight to any of these factors. We also have used stock options, which increase in value only if our common stock increases in value, and which terminate a short time after an executive leaves our employ, as a means of long-term incentive compensation. During fiscal 2002, we adopted a salary and director fee reduction/stock option program under the 2002 Non-Qualified Stock Option Plan. Participants in the program voluntarily elected to reduce their base salary or director's fee for a one-year period beginning in January 2003. For each dollar of salary or fee reduction, options to purchase one and one-half shares of our common stock were granted to the participant. During 2003 we also granted options to executive officers notwithstanding our poor financial performance. Most of the options granted to Mr. Zucker were required under his employment agreement. The grants of options to other executive officers were intended to provide additional motivation during a difficult financial period when most of their outstanding stock options were

19

under water. The number of options granted to executive officers other than our Chief Executive Officer was determined by the Stock Option Committee in its discretion based upon recommendations of our Chief Executive Officer.

In May 2003 Neil D. Nicastro was succeeded by Mr. Zucker as our Chief Executive Officer. As a result, severance provisions of Mr. Nicastro's employment agreement were triggered, and Mr. Nicastro entered into a severance agreement with us.

Mr. Zucker's compensation arrangements under his employment agreement, including stock option grants and restricted stock awards, were negotiated at arm's length by the Compensation Committee and the Stock Option Committee, with the assistance of an outside consultant. Among other matters, in negotiating this agreement we considered compensation levels of chief executives at our principal competitors.

The Omnibus Budget Reconciliation Act of 1993 (the "Budget Act") generally provides that publicly-held corporations will only be able to deduct, for income tax purposes, compensation paid to the chief executive officer or any of the four most highly paid senior executive officers in excess of one million dollars per year if it is paid pursuant to qualifying performance-based compensation plans approved by stockholders. Compensation as defined by the Budget Act includes, among other things, base salary, incentive compensation and gains on stock option transactions. Total compensation of some of our officers may be paid under plans or agreements that have not been approved by stockholders and may exceed one million dollars in a particular fiscal year. We will not be able to deduct these excess payments for income tax purposes. The Compensation Committee intends to consider, on a case by case basis, how the Budget Act will affect our compensation plans and contractual and discretionary cash compensation, taking into account, among other matters, our substantial net operating loss carryforwards.

| The Compensation Committee: | The Stock Option Committee: | |

| William C. Bartholomay, Chairman | Harvey Reich, Chairman | |

| Harvey Reich | William E. McKenna | |

| William E. McKenna |

20

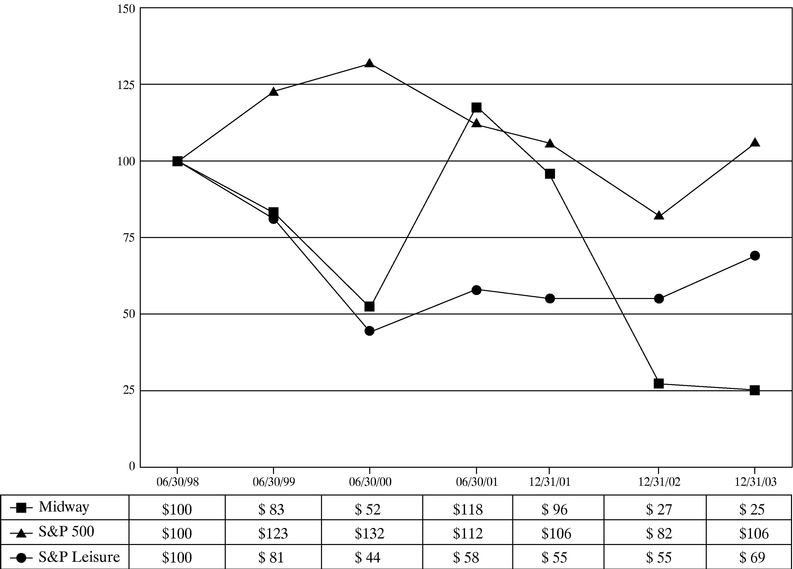

The following graph compares, for the period beginning June 30, 1998 and ending December 31, 2003, the percentage change during each period ending on the dates shown below in cumulative total stockholder return on our common stock with that of (1) the Standard and Poor's 500 Stock Index ("S&P 500") and (2) the Standard and Poor's Leisure Time Index ("S&P Leisure"). The graph assumes an investment of $100 on June 30, 1998 in our common stock and $100 invested at that time in each of the indices and the reinvestment of dividends where applicable. Note that our fiscal year changed in 2001 from a fiscal year ending on June 30 to a fiscal year ending on December 31. Therefore, the data shown at December 31, 2001 reflects the six-month transition period ended on December 31, 2001.

21

Neil D. Nicastro is the chairman of our Board of Directors. Until May 6, 2003, we employed Mr. Nicastro as our chief executive officer, chief operating officer and president under an employment agreement dated July 1, 1996, as amended. His annual base salary was $600,000. Under the employment agreement, upon the termination of his employment by Midway, Mr. Nicastro was entitled to receive cash severance payments and delivery of 607,846 shares of Midway common stock in lieu of cash retirement payments (the "Retirement Shares").

On May 6, 2003, David F. Zucker succeeded Mr. Nicastro as our chief executive officer and president. As a result of this event, the severance provisions of Mr. Nicastro's employment agreement were triggered. On the same date, we entered into a severance agreement with Mr. Nicastro that supersedes the termination provisions under his employment agreement.