When compared to the first quarter, the composition of our second quarter 2005 steel operations’ shipments trended toward more value-added and cold-finished product offerings, which are more costly to manufacture and typically command higher selling prices. Our Bar Products Division consumes a greater amount and variety of alloys than our other operations. The increased production of bar products has increased our overall manufacturing costs as the costs of alloys per ton produced increased over 60% during the second quarter of 2005 when compared to the same period of 2004. We anticipate a further diversification of our product mix during the second half of 2005 as we continue to develop new bar products and increase rail production. The following table depicts our product mix by major product category based on tons shipped by our steel operations segment for the indicated three month periods

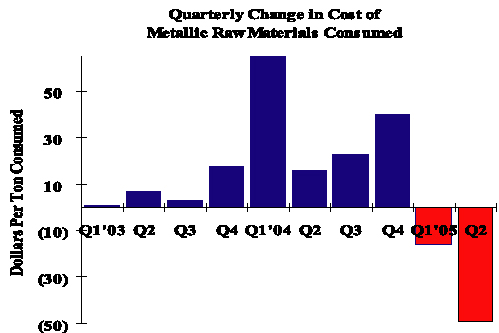

Metallic raw materials used in our electric arc furnaces represent our single-most significant manufacturing cost. Our metallic raw material cost per net ton consumed in our furnaces decreased $49 during the second quarter of 2005 and remained steady with a $2 decrease when compared to the same period of 2004. Historically our metallic raw material costs represented between 45% and 50% of our total manufacturing costs; however, for the year 2004 this percentage increased to 67% during the third quarter due to the elevated cost of our metallic raw materials, specifically steel scrap. This increase in the cost of our primary raw material as a percentage of our total manufacturing costs necessitated the initiation of a surcharge mechanism which was adopted by many steel producers during the first quarter of 2004. The surcharge is derived from an indexed scrap number and designed to pass some of the increased costs associated with rising metallic prices through to our customers. As these costs decrease, the surcharge also declines. During a portion of the second quarter of 2005 actual steel scrap costs were below the indexed surcharge numbers and in some instances no surcharge was utilized in determining prices for our products. Metallic raw materials represented 53% and 59% of our total manufacturing costs during the second quarter and first half of 2005, respectively.

We are currently experiencing continued softness in base prices for our products, most significantly within the flat-rolled and bar steel markets. Our customers’ inventories remained higher than expected during the first half of 2005 and are being depleted more slowly than anticipated. We believe this will result in a somewhat lower average selling price for our third quarter.

Back to Contents

Other (Income) Expense. Other income was $175,000 during the second quarter of 2005, as compared to $3.1 million during 2004. During the first quarter of 2004 we entered into a one-time short-term U.S. Treasury Bond transaction to generate net interest income in an increasing interest rate environment and to generate capital gains. This transaction was completed during the fourth quarter of 2004 and we recorded associated gains of $2.0 million during the second quarter of 2004.

Income Taxes. During the second quarter of 2005, our income tax provision was $31.7 million, as compared to $40.4 million during the same period in 2004. Our effective income tax rate was 37.5% for the first half of 2004. We increased our effective income tax rate to 38.5% beginning January 1, 2005 in anticipation of the year’s expected profitability levels and the resulting impact to our state income taxes.

First Half Operating Results 2005 vs. 2004

Net income was $111.4 million or $2.12 per diluted share during the first half of 2005, compared with $99.3 million or $1.78 per diluted share during the first half of 2004.

Gross Profit. During the first half of 2005, our net sales increased $206.7 million, or 23%, to $1.1 billion and our consolidated shipments increased 63,000 tons, or 4%, to 1.8 million tons, compared with the first half of 2004. The increase in shipments was primarily due to a 96,000 ton increase in shipments from our Bar Products Division, which started commercial operations during the first quarter of 2004 combined with a decrease of 39,000 tons from our Flat Roll Division. Our first half 2005 average consolidated selling price increased $99 per ton, or 18%, compared with the first half of 2004.

Selling, General and Administrative Expenses. Selling, general and administrative expenses were $42.5 million during the first half of 2005, as compared to $39.5 million during the same period in 2004, an increase of $3.0 million, or 8%. This increase was attributed in part to increased profit sharing expense of $3.1 million. During the first half of 2005 and 2004, selling, general and administrative expenses represented approximately 4% of net sales.

Interest Expense. During the first half of 2005, gross interest expense decreased $6.4 million, or 27%, to $17.5 million and capitalized interest decreased $3.3 million to $545,000, as compared to the same period in 2004. This decrease in gross interest expense was the result of the repayment of certain debt instruments during the second half of 2004 and due to interest expense of $3.5 million that was recorded during the first half of 2004 in conjunction with the aforementioned short-term U.S. Treasury bond transaction.

Other (Income) Expense. Other income was $753,000 during the first half of 2005, as compared to $5.2 million during 2004. During the first half of 2004 we recorded gains of $4.0 million related to the aforementioned U.S. Treasury Bond transaction which was completed during the fourth quarter of 2004. We also recorded a $1.0 million gain from the early extinguishment of certain debt associated with our Structural and Rail Division during the first half of 2004.

Income Taxes. During the first half of 2005, our income tax provision was $69.8 million, as compared to $59.6 million during the same period in 2004. Our effective income tax rate was 37.5% for the first half of 2004. We increased our effective income tax rate to 38.5% beginning January 1, 2005 in anticipation of the year’s expected profitability levels and the resulting impact to our state income taxes.

Liquidity and Capital Resources

Our business is capital intensive and requires substantial expenditures for, among other things, the purchase and maintenance of equipment used in our steelmaking and finishing operations and to remain in compliance with environmental laws. Our short-term and long-term liquidity needs arise primarily from capital expenditures, working capital requirements and principal and interest payments related to our outstanding indebtedness. We have met these liquidity requirements with cash provided by operations, equity, long-term borrowings, state and local grants and capital cost reimbursements.

Working Capital. During the first half of 2005, our operating working capital position, representing our cash invested in trade receivables and inventories less trade payables and accruals increased $97.5 million to $506.4 million compared to December 31, 2004. Due to decreased sales volume and price, trade receivables decreased $14.5 million during the first half to $239.4 million, of which 95%, were current or less than 60 days past due. Our largest customer is an affiliated company, Heidtman Steel, which represented 20% and 15% of our outstanding trade receivables at June 30, 2005 and December 31, 2004, respectively. During the first half of 2005 our inventories increased $40.4 million to $421.9 million. Raw materials and supplies increased $57.6 million while finished goods and work-in-process inventories decreased by $17.2 million. The increase in raw materials and supplies was driven by a 58% increase in our steel scrap supply which was the result of our decision to gain favorable pricing as the cost of steel scrap declined during the first half of the year and due to increased alloy volumes required as product diversification increases at our Bar Products Division. Our trade payables and accruals decreased $71.6 million, or 32%, during the first half of 2005 due to the timing of funding certain payables, including our 2004 401(k) retirement savings and profit sharing plan contribution in March 2005.

12

Back to Contents

Capital Expenditures. During the first half of 2005 we invested $36.3 million in property, plant and equipment related to a new joist and deck production facility and to improvement projects in our existing facilities. Approximately 47% of these capital investments were related to the expansion of our New Millennium joist and deck operations with the addition of a plant in Lake City, Florida. We believe these capital investments will increase our net sales and related cash flows as each project develops.

Capital Resources. During the first half of 2005 our total outstanding debt, including unamortized bond premium, increased $125.0 million to $573.4 million. Our long-term debt to capitalization ratio, representing our long-term debt divided by the sum of our long-term debt and our total stockholders’ equity, was 42% and 34% at June 30, 2005 and December 31, 2004, respectively.

At June 30, 2005, we had $125.0 million in outstanding borrowings related to our $230.0 million senior secured revolving credit facility. Our senior secured credit agreement is secured by liens and mortgages on substantially all of our personal and real property assets, by liens and mortgages on substantially all of the personal and real property assets of our wholly-owned subsidiaries, and by pledges of all shares of capital stock and inter-company debt held by us and each wholly-owned subsidiary. The senior secured credit agreement contains financial covenants and other covenants that limit or restrict our ability to make capital expenditures; incur indebtedness; permit liens on our property; enter into transactions with affiliates; make restricted payments or investments; enter into mergers, acquisitions or consolidations; conduct asset sales; pay dividends or distributions and enter into other specified transactions and activities. Our ability to draw down the revolver is dependent upon our continued compliance with the financial covenants and other covenants contained in our senior secured credit agreement. We were in compliance with these covenants at June 30, 2005.

During the second quarter of 2005, our board of directors declared a cash dividend of $.10 (ten cents) per common share for shareholders of record at close of business on June 30, 2005. The cash dividend of $4.4 million was paid on July 12, 2005. On April 20, 2005, we announced the approval of our board of directors to increase the shares available for the company to repurchase from 5 million shares to 7.5 million shares pursuant to the 2004 share repurchase program. At June 30, 2005, we had repurchased 7.3 million shares pursuant to the program in the open market at an average price of $32 per share. We repurchased the remaining 200,000 authorized shares during July at an average price of $32 per share.

Our ability to meet our debt service obligations and reduce our total debt will depend upon our future performance, which in turn, will depend upon general economic, financial and business conditions, along with competition, legislation and regulation factors that are largely beyond our control. In addition, we cannot assure you that our operating results, cash flow and capital resources will be sufficient for repayment of our indebtedness in the future. We believe that based upon current levels of operations and anticipated growth, cash flow from operations, together with other available sources of funds, including additional borrowings under our senior secured credit agreement, will be adequate for the next two years for making required payments of principal and interest on our indebtedness and for funding anticipated capital expenditures and working capital requirements.

Other Matters

Inflation. We believe that inflation has not had a material effect on our results of operations.

Environmental and Other Contingencies. We have incurred, and in the future will continue to incur, capital expenditures and operating expenses for matters relating to environmental control, remediation, monitoring and compliance. We believe, apart from our dependence on environmental construction and operating permits for our existing and proposed manufacturing facilities, that compliance with current environmental laws and regulations is not likely to have a material adverse effect on our financial condition, results of operations or liquidity; however, environmental laws and regulations are subject to change and we may become subject to more stringent environmental laws and regulations in the future.

ITEM 3. QUANTITATIVE AND QUALITATIVE DISCLOSURES ABOUT MARKET RISK

Market Risk. In the normal course of business we are exposed to interest rate changes. Our objectives in managing exposure to interest rate changes are to limit the impact of these rate changes on earnings and cash flows and to lower overall borrowing costs. To achieve these objectives, we primarily use interest rate swaps to manage net exposure to interest rate changes related to our borrowings. We generally maintain fixed rate debt as a percentage of our net debt between a minimum and maximum percentage. A portion of our debt has an interest component that resets on a periodic basis to reflect current market conditions. At June 30, 2005, no material changes had occurred related to our interest rate risk from the information disclosed in our Annual Report on Form 10-K for the year ended December 31, 2004.

Commodity Risk. In the normal course of business we are exposed to the market risk and price fluctuations related to the sale of steel products and to the purchase of commodities used in our production process, such as metallic raw materials, electricity, natural gas and alloys. Our risk strategy associated with product sales has generally been to obtain competitive prices for our products and to allow operating results to reflect market price movements dictated by supply and demand. Generally, our risk strategy associated with the purchase of commodities utilized within our production process is to make certain commitments with suppliers relating to future expected requirements for such commodities. Certain of these commitments contain provisions which require us to “take or pay” for specified quantities without regard to actual usage for periods of up to two years. We believe that our production requirements will be such that consumption of the products or services purchased under these commitments will occur in the normal production process. At June 30, 2005, no material changes had occurred related to these commodity risks from the information disclosed in our Annual Report on Form 10-K for the year ended December 31, 2004.

13

Back to Contents

ITEM 4. CONTROLS AND PROCEDURES

(a) Evaluation of Disclosure Controls and Procedures. An evaluation was performed under the supervision and with the participation of registrant’s management, including the chief executive officer and chief financial officer, of the effectiveness of the design and operation of registrant’s disclosure controls and procedures, as of the end of the period covered by this report. Based upon their evaluation, registrant’s principal executive officer and principal financial officer have concluded that registrant’s disclosure controls and procedures (as defined in Rules 13a-15(e) and 15d-15(e) under the Securities Exchange Act of 1934) were effective to ensure that information required to be disclosed by registrant in reports that it files or submits under the Exchange Act is recorded, processed, summarized and reported within the time periods specified in Securities and Exchange Commission rules and forms.

(b) Changes in Internal Controls. There have been no significant changes in registrant’s internal controls or in other factors that could significantly affect internal controls subsequent to their evaluation. There were no significant deficiencies or material weaknesses, and, therefore, there were no corrective actions taken.

PART II

OTHER INFORMATION

ITEM 2. CHANGES IN SECURITIES, USE OF PROCEEDS AND ISSUER PURCHASES OF EQUITY SECURITIES

On April 20, 2005, our board of directors approved an increase in the shares authorized for repurchase pursuant to the 2004 share repurchase program from 5 million shares to 7.5 million shares. The following table indicates shares repurchased during the six months ended June 30, 2005.

| | | | | | | | | | | | Total Shares Still | |

| | | Total Shares | | Average Price | | Total Program | | Available For Purchase | |

| Period | | Purchased | | Paid Per Share | | Shares Purchased | | Under the Program | |

| |

|

| |

|

| |

|

| |

|

| |

| 2005 | | | | | | | | | | | | | |

| January 1 to 26 | | | 1,037,100 | | $ | 35.46 | | | 1,037,100 | | | 4,875,167 | |

| February 1 | | | 10,076 | | | 37.80 | | | — | | | 4,875,167 | |

| March 16 to 30 | | | 1,099,400 | | | 35.97 | | | 1,099,400 | | | 3,775,767 | |

| April 1 to 29 | | | 1,875,767 | | | 31.40 | | | 1,875,767 | | | 1,900,000 | |

| May 2 to 25 | | | 1,302,000 | | | 26.41 | | | 1,302,000 | | | 598,000 | |

| June 20 to 27 | | | 398,000 | | | 26.21 | | | 398,000 | | | 200,000 | |

| | | | | | | | | | | | | | |

14

Back to Contents

ITEM 4. SUBMISSION OF MATTERS TO A VOTE OF SECURITY HOLDERS

Our Annual Meeting of Shareholders was held May 19, 2005. Proxies were solicited for the Annual Meeting in accordance with the requirements of The Securities Exchange Act 1935. At the Annual Meeting, the following occurred:

| • | With respect to Item 1 in our Proxy Statement (Election of Directors): |

| | Director | | | Shares Voted For | | | Shares Voted

Against or Withheld | |

| |

|

|

|

|

|

|

| |

| | Keith E. Busse | | | 44,362,385 | | | 1,031,591 | |

| | Mark D. Millett | | | 44,640,996 | | | 752,980 | |

| | Richard P. Teets, Jr. | | | 44,637,550 | | | 756,426 | |

| | John C. Bates | | | 43,514,423 | | | 1,879,553 | |

| | Dr. Frank D. Byrne | | | 45,262,727 | | | 131,249 | |

| | Paul B. Edgerley | | | 45,262,608 | | | 131,368 | |

| | Richard J. Freeland | | | 45,262,696 | | | 131,280 | |

| | Naoki Hidaka | | | 45,168,012 | | | 225,964 | |

| | Dr. Jürgen Kolb | | | 45,261,319 | | | 132,657 | |

| | James C. Marcuccilli | | | 45,266,308 | | | 127,668 | |

| | Joseph D. Ruffolo | | | 45,265,326 | | | 128,650 | |

| | |

| • | With respect to Item 2 in our Proxy Statement (Approval of Ernst & Young LLP as Auditors for the Year 2005), Ernst & Young LLP was approved as our independent auditors for the year 2005: |

| | | | | | |

| | Shares Voted For | | | 45,204,126 | |

| | Shares Voted Against | | | 181,486 | |

| | Abstentions | | | 8,364 | |

ITEM 6.EXHIBITS

| 31.1 | Chief Executive Officer Certification pursuant to Section 302 of the Sarbanes-Oxley Act of 2002 |

| | |

| 31.2 | Principal Financial Officer Certification pursuant to Section 302 of the Sarbanes-Oxley Act of 2002 |

| | |

| 32.1 | Chief Executive Officer Certification pursuant to 18 U.S.C. Section 1350 |

| | |

| 32.2 | Principal Financial Officer Certification pursuant to 18 U.S.C. Section 1350 |

_____________________________________________________________________________________________________________

Items 1, 3 and 5 of Part II are not applicable for this reporting period and have been omitted.

* Filed concurrently herewith.

SIGNATURE

Pursuant to the requirements of Section 13 or 15(d) of Securities Exchange Act of 1934, Steel Dynamics, Inc. has duly caused this report to be signed on its behalf by the undersigned, thereunto duly authorized.

August 5, 2005

| | | STEEL DYNAMICS, INC. |

| | | |

| | By: | /s/ Gary E. Heasley |

| | |

|

| | | Gary E. Heasley |

| | | Vice President of Finance and CFO |

| | | |

15