Exhibit 99.1

November 11, 201 6 Enabling Next Generation Energy Storage Room Temperature Production of High Purity Lithium Meta l & Associated Products High Purity Lithium Metal - Clean Technology

Thi s presentatio n i s fo r informationa l purpose s onl y and doe s no t constitut e a n o f fe r t o sell , o r th e solicitatio n o f a n o f fe r t o b u y , an y securitie s o f th e alpha - En Corporatio n o r it s subsidia r y , Clea n Lithiu m Corporation ; o r a promis e o r representatio n tha t an y suc h o f fer wil l b e mad e t o th e recipien t o r an y othe r par t y . This presentation contains “forward - looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995 . Forward - looking statements can be identified by words such as : “expect,” “anticipate,” “intend,” “plan,” “believe,” “seek,” “estimate,” “project,” “goal,” “may,” “should,” “will” and similar expressions that concern our prospects, objectives, strategies, plans or intentions . Forward - looking statements are neither historical facts nor assurances of future performance . They are based on current beliefs, expectations and assumptions that are subject to inherent risks and uncertainties and our actual results and financial condition may differ materially from those indicated in the forward - looking statements . Therefore, you should not place undue reliance on any forward - looking statements . Important factors that could cause our actual results and financial condition to differ materially from those indicated in forward - looking statements include unfavorable changes in general economic and financial conditions ; our lack of relevant operating history and revenues ; competition and technical alternatives in the overall battery market ; government regulation ; our ability to attract and retain key personnel ; our ability to successfully collaborate with partners ; the availability of financing ; marketplace acceptance of our technology ; and such other factors discussed in our filings with the Securities and Exchange Commission . Any forward - looking statement speaks only as of the date on which it is made . We undertake no obligation to publicly update any forward - looking statement, whether written or oral, whether as a result of new information, future developments or otherwise . SAFE HARBOR STATEMENT 2

3 MARKET OPPORTUNITY • Lithium Ion (Li - Ion) battery market was >$10B in 2015, and expected to be >$20B in 2020* • Li - Ion technology was introduced in the ‘90s. It is mature and has plateaued. • The next leap in performance is anticipated from Lithium Metal (Li - M) battery technology. • Disruptive technology. Can displace Li - Ion and accelerate market growth. ALPHA - EN TECHNOLOGY • apha - En’s cleaner process is less costly and produces high purity Li - M , a component of Li - M batteries. • a lpha - En’s f lexible deposition m ethod can also streamline battery manufacturing leading to battery production cost benefits . • Furthermore, we believe alpha - En’s core technology can potentially recycle discarded Lithium batteries as feedstock for Li - M production. STATUS • a lpha - En has held discussions with global battery manufacturers and end users. • P otential partnering and/or licensing opportunities. • a lpha - En has strategic research partnerships with Argonne National Laboratory, Princeton University, and the City University of New York to advance commercialization and scale - up of production. ENABLING NEXT GENERATION ENERGY STORAGE *Source: Avicenne Energy

ALPE Process Benefits

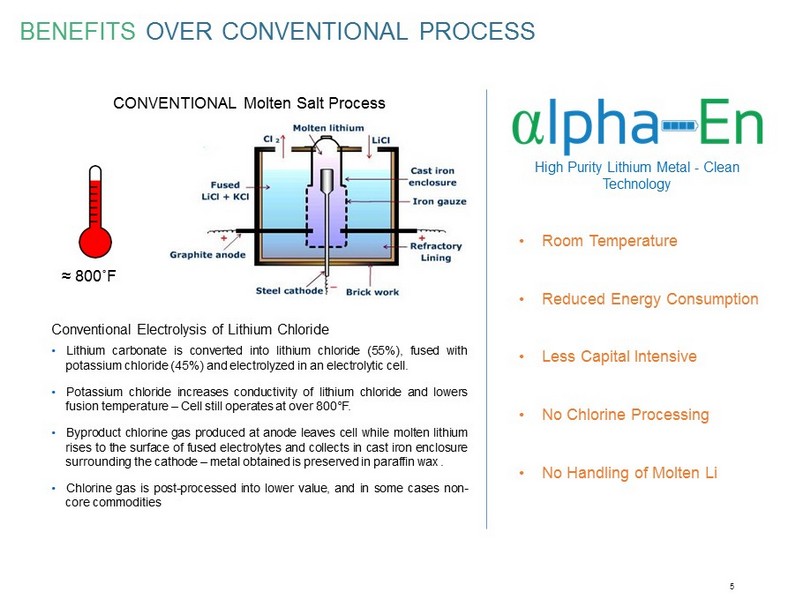

5 CONVENTIONAL Molten Salt Process Conventional Electrolysis of Lithium Chloride • Lithium carbonate is converted into lithium chloride ( 55 % ), fused with potassium chloride ( 45 % ) and electrolyzed in an electrolytic cell . • Potassium chloride increases conductivity of lithium chloride and lowers fusion temperature – Cell still operates at over 800 ° F . • Byproduct chlorine gas produced at anode leaves cell while molten lithium rises to the surface of fused electrolytes and collects in cast iron enclosure surrounding the cathode – metal obtained is preserved in paraffin wax . • Chlorine gas is post - processed into lower value, and in some cases non - core commodities BENEFITS OVER CONVENTIONAL PROCESS • Room Temperature • Reduced Energy Consumption • Less Capital Intensive • No Chlorine Processing • No Handling of Molten Li ≈ 800˚F High Purity Lithium Metal - Clean Technology

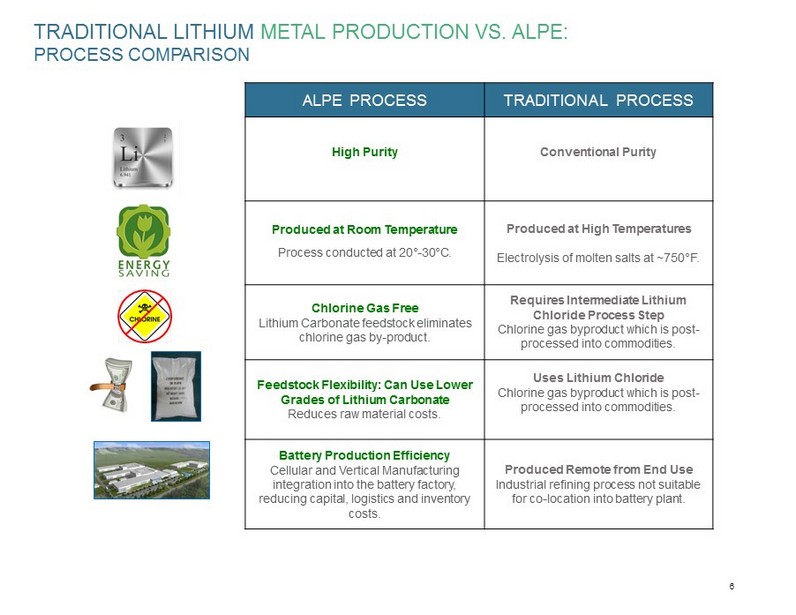

6 TRADITIONAL LITHIUM METAL PRODUCTION VS. ALPE: PROCESS COMPARISON ALPE PROCESS TRADITIONAL PROCESS High Purity Conventional Purity Produced at Room Temperature Process conducted at 20 ° - 30 ° C. Produced at High Temperatures Electrolysis of molten salts at ~750 ° F. Chlorine Gas Free Lithium Carbonate feedstock eliminates chlorine gas by - product. Requires Intermediate Lithium Chloride Process Step Chlorine gas byproduct which is post - processed into commodities. Feedstock Flexibility: Can Use Lower Grades of Lithium Carbonate Reduces raw material costs. Uses Lithium Chloride Chlorine gas byproduct which is post - processed into commodities. Battery Production Efficiency Cellular and Vertical Manufacturing integration into the battery factory, reducing capital, logistics and inventory costs. Produced Remote from End Use Industrial refining process not suitable for co - location into battery plant.

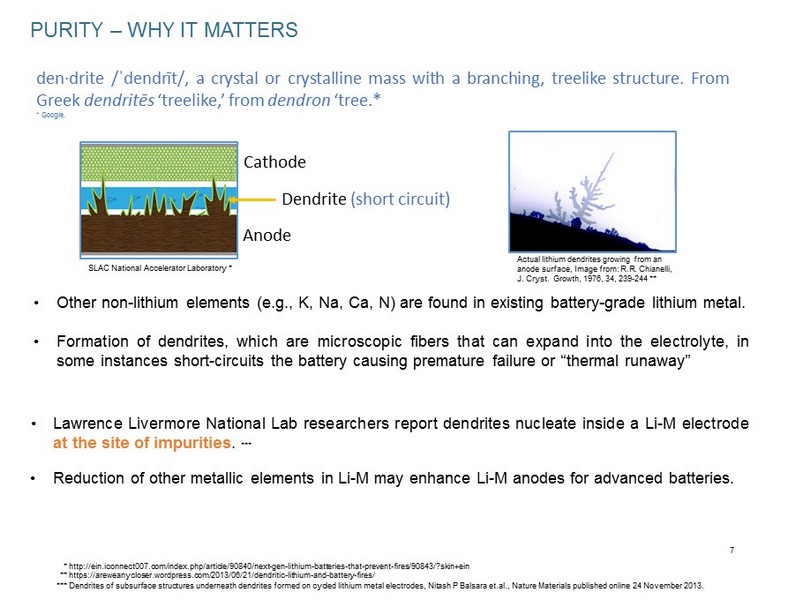

7 PURITY – WHY IT MATTERS • Other non - lithium elements (e . g . , K , Na, Ca , N) are found in existing battery - grade lithium metal . • F ormation of dendrites, which are microscopic fibers that can expand into the electrolyte, in some instances short - circuits the battery causing premature failure or “thermal runaway ” • Lawrence Livermore National Lab researchers report dendrites nucleate inside a Li - M electrode at the site of impurities . *** den·drite /ˈ dendrīt /, a crystal or crystalline mass with a branching, treelike structure . From Greek dendritēs ‘treelike,’ from dendron ‘tree . * * Google . Cathode Anode Dendrite (short circuit) • Reduction of other metallic elements in Li - M may enhance Li - M anodes for advanced batteries . Actual lithium dendrites growing from an anode surface, Image from: R.R. Chianelli , J. Cryst . Growth, 1976, 34, 239 - 244 ** ** https:// areweanycloser.wordpress.com /2013/06/21/dendritic - lithium - and - battery - fires/ SLAC National Accelerator Laboratory * * http://ein.iconnect007.com/ index.php /article/90840/next - gen - lithium - batteries - that - prevent - fires/90843/? skin+ein *** Dendrites of subsurface structures underneath dendrites formed on cycled lithium metal electrodes, Nitash P Balsara et.al ., Nature Materials published online 24 November 2013.

INTELLECTUAL PROPERTY • ALPE engaged K&L Gates in 2015 to implement IP strategy . • Initial 201 3 ALPE patent portfolio was broadened and strengthened and now includes filings for international markets . • The Company is securing additional IP related to other aspects of its core technology. • ALPE has filed process and use patents totaling over 100 claims, and continues to innovate. • K&L Gates distinctions: • Global Dispute of the Year, The American Lawyer’s Global Legal Awards (2016). • Included on IP Hot List, National Law Journal (2013). • Included among IP Practices of the Year, Law360 (2013). • Top 10 Client Service: In - house corporate counsel in an unprompted BTI survey ranked K&L Gates in the top 10 among all law firms in the past two consecutive years (2015 and 2016). 8

The Lithium Battery Market

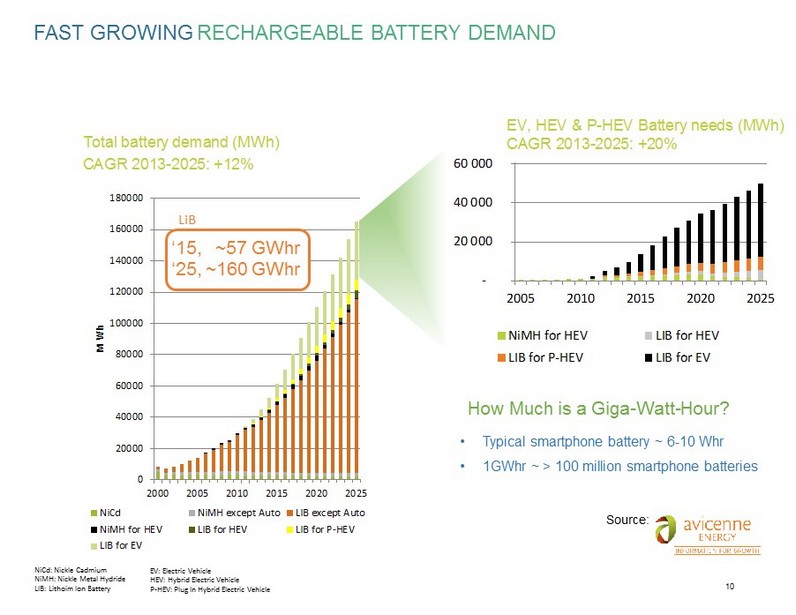

10 Christophe PILLOT + 33 1 47 78 46 00 c.pillot@avicenne.com Battery Market Development for Consumer Electronics, Automotive, and Industrial BATTERIES 2014 September24 –26, 2014 NICE, FRANCE TOTAL BATTERYDEMAND 2025 FORECASTS EV, HEV & P-HEV Battery needs (MWh) CAGR 2013-2025: +20% Total battery demand (MWh) CAGR 2013-2025: +12% 28 0 20000 40000 60000 80000 100000 120000 140000 160000 180000 2000 2005 2010 2015 2020 2025 M W h NiCd NiMH except Auto LIB except Auto NiMH for HEV LIB for HEV LIB for P-HEV LIB for EV - 20 000 40 000 60 000 80 000 100 000 120 000 140 000 160 000 180 000 2005 2010 2015 2020 2025 M W h NiMH for HEV LIB for HEV LIB for P-HEV LIB for EV Christophe PILLOT + 33 1 47 78 46 00 c.pillot@avicenne.com Battery Market Development for Consumer Electronics, Automotive, and Industrial BATTERIES 2014 September24 –26, 2014 NICE, FRANCE TOTAL BATTERYDEMAND 2025 FORECASTS EV, HEV & P-HEV Battery needs (MWh) CAGR 2013-2025: +20% Total battery demand (MWh) CAGR 2013-2025: +12% 28 0 20000 40000 60000 80000 100000 120000 140000 160000 180000 2000 2005 2010 2015 2020 2025 M W h NiCd NiMH except Auto LIB except Auto NiMH for HEV LIB for HEV LIB for P-HEV LIB for EV - 20 000 40 000 60 000 80 000 100 000 120 000 140 000 160 000 180 000 2005 2010 2015 2020 2025 M W h NiMH for HEV LIB for HEV LIB for P-HEV LIB for EV Christophe PILLOT + 33 1 47 78 46 00 c.pillot@avicenne.com Battery Market Development for Consumer Electronics, Automotive, and Industrial BATTERIES 2014 September24 –26, 2014 NICE, FRANCE TOTAL BATTERYDEMAND 2025 FORECASTS EV, HEV & P-HEV Battery needs (MWh) CAGR 2013-2025: +20% Total battery demand (MWh) CAGR 2013-2025: +12% 28 0 20000 40000 60000 80000 100000 120000 140000 160000 180000 2000 2005 2010 2015 2020 2025 M W h NiCd NiMH except Auto LIB except Auto NiMH for HEV LIB for HEV LIB for P-HEV LIB for EV - 20 000 40 000 60 000 80 000 100 000 120 000 140 000 160 000 180 000 2005 2010 2015 2020 2025 M W h NiMH for HEV LIB for HEV LIB for P-HEV LIB for EV LiB ‘15, ~57 GWhr ‘25, ~160 GWhr GLOBAL MARKET ISSUES & TRENDS Christophe Pillot Director avicenneENERGY BatteryMarketDevelopmentfor Consumer Electronics, Automotive, and Industrial: MaterialsRequirements& Trends Source: FAST GROWING RECHARGEABLE BATTERY DEMAND • Typical smartphone battery ~ 6 - 10 Whr • 1GWhr ~ > 100 million smartphone batteries How Much is a Giga - Watt - Hour? NiCd : Nickle Cadmium NiMH: Nickle Metal Hydride LIB: Lithoim Ion Battery EV: Electric Vehicle HEV: Hybrid Electric Vehicle P - HEV: Plug In Hybrid Electric Vehicle

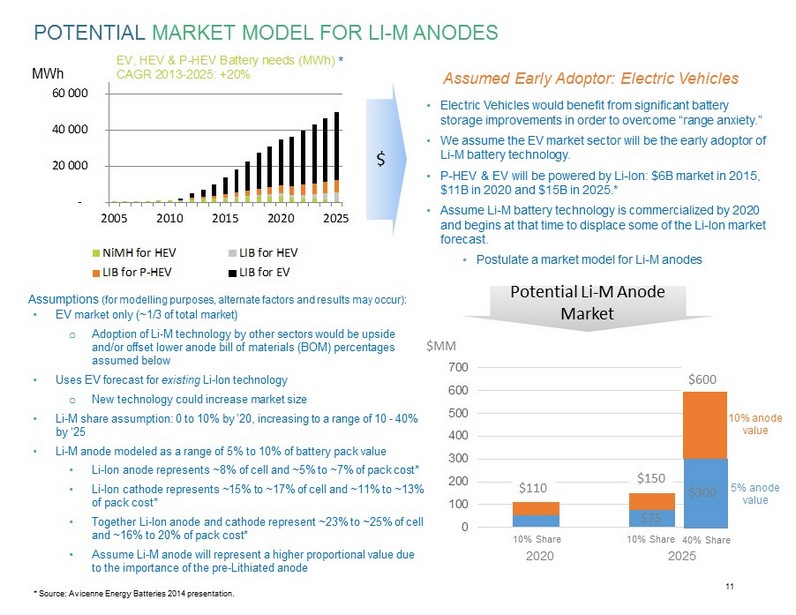

11 Christophe PILLOT + 33 1 47 78 46 00 c.pillot@avicenne.com Battery Market Development for Consumer Electronics, Automotive, and Industrial BATTERIES 2014 September24 –26, 2014 NICE, FRANCE TOTAL BATTERYDEMAND 2025 FORECASTS EV, HEV & P-HEV Battery needs (MWh) CAGR 2013-2025: +20% Total battery demand (MWh) CAGR 2013-2025: +12% 28 0 20000 40000 60000 80000 100000 120000 140000 160000 180000 2000 2005 2010 2015 2020 2025 M W h NiCd NiMH except Auto LIB except Auto NiMH for HEV LIB for HEV LIB for P-HEV LIB for EV - 20 000 40 000 60 000 80 000 100 000 120 000 140 000 160 000 180 000 2005 2010 2015 2020 2025 M W h NiMH for HEV LIB for HEV LIB for P-HEV LIB for EV Christophe PILLOT + 33 1 47 78 46 00 c.pillot@avicenne.com Battery Market Development for Consumer Electronics, Automotive, and Industrial BATTERIES 2014 September24 –26, 2014 NICE, FRANCE TOTAL BATTERYDEMAND 2025 FORECASTS EV, HEV & P-HEV Battery needs (MWh) CAGR 2013-2025: +20% Total battery demand (MWh) CAGR 2013-2025: +12% 28 0 20000 40000 60000 80000 100000 120000 140000 160000 180000 2000 2005 2010 2015 2020 2025 M W h NiCd NiMH except Auto LIB except Auto NiMH for HEV LIB for HEV LIB for P-HEV LIB for EV - 20 000 40 000 60 000 80 000 100 000 120 000 140 000 160 000 180 000 2005 2010 2015 2020 2025 M W h NiMH for HEV LIB for HEV LIB for P-HEV LIB for EV Potential Li - M Anode Market $MM $ • EV market only (~1/3 of total market) o Adoption of Li - M technology by other sectors would be upside and/or offset lower anode bill of materials (BOM) percentages assumed below • Uses EV forecast for existing Li - Ion technology o New technology could increase market size • Li - M share assumption: 0 to 10% by ’ 20 , increasing to a range of 10 - 40% by ‘25 • Li - M anode modeled as a range of 5% to 10% of battery pack value • Li - Ion anode represents ~8% of cell and ~5% to ~7% of pack cost* • Li - Ion cathode represents ~15% to ~17% of cell and ~11% to ~13% of pack cost* • Together Li - Ion anode and cathode represent ~23% to ~25% of cell and ~16% to 20% of pack cost* • Assume Li - M anode will represent a higher proportional value due to the importance of the pre - Lithiated anode POTENTIAL MARKET MODEL FOR LI - M ANODES $165 Assumed Early Adoptor : Electric Vehicles Assumptions (for modelling purposes, alternate factors and results may occur): * Source: Avicenne Energy Batteries 2014 presentation. 5 % anode value 10% anode value 0 100 200 300 400 500 600 700 2020 2025 2020 2025 10% Share 10% Share 4 0% Share $150 $600 • Electric Vehicles would benefit from significant battery storage improvements in order to overcome “range anxiety.” • We assume the EV market sector will be the early adoptor of Li - M battery technology. • P - HEV & EV will be powered by Li - Ion: $6B market in 2015, $11B in 2020 and $15B in 2025.* • Assume Li - M battery technology is commercialized by 2020 and begins at that time to displace some of the Li - Ion market forecast. • Postulate a market model for Li - M anodes MWh * $300 $75 $110

Company Information

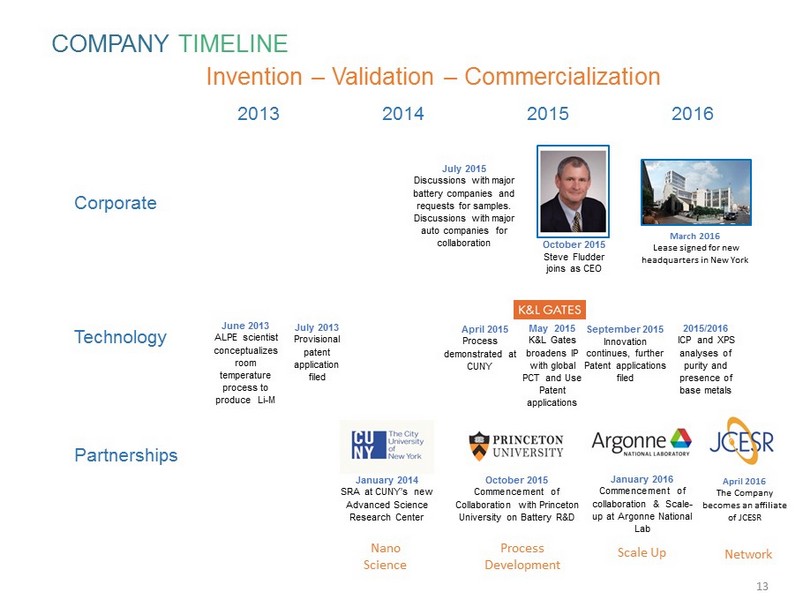

13 Corporate Technology Partnerships 2013 2014 2015 2016 October 2015 Steve Fludder joins as CEO January 201 4 SR A at CUNY ’ s new Advanced Science Resea r ch Center J anuary 2016 Commencement of collaboration & Scale - up at Argonne National Lab October 2015 Commencement of Collaboration with Princeton University on Battery R&D April 2016 The Company becomes an affiliate of JCESR March 2016 Lease signed for new headquarters in New York May 2015 K&L Gates b r oadens IP with global PCT and Use Patent applications April 2015 P r ocess demonstrated at CUNY June 2013 ALPE scientist conceptualizes r oom temperatu r e p r ocess to p r oduce Li - M September 2015 Innovation continues, further Patent applications filed 2015 /2016 ICP and XPS a nalys e s of purity and presence of base metals July 2013 P r ovisional patent application filed July 2015 Discussions with major battery companies and request s for samples. Discussions with major auto companies for collaborat ion Invention – Validation – Commercialization COMPANY TIMELINE Process Development Nano S cience Scale Up Network

14 R&D / / PRODUCT DEVELOPMENT CENTER • 8 , 000 Sq . Ft . facility with high tech lab and product development operations • Global HQ, New York, USA • Innovative iPark Hudson development with Tech . , Bio/Pharma and innovation incubators in historic Otis elevator manufacturing plant . • Lease effective March ‘ 16 • Alpha - En to move in by ‘ 16 year end Producing prototype lithium products and samples for global battery manufacturers

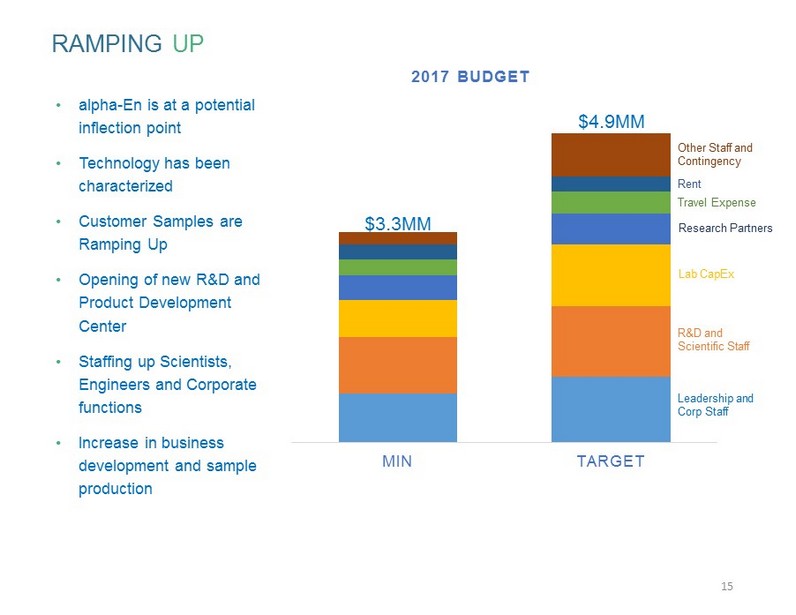

15 • a lpha - En is at a potential inflection point • Technology has been characterized • Customer Samples are Ramping Up • Opening of new R&D and Product Development Center • Staffing up Scientists, Engineers and Corporate functions • I ncrease in business development and sample production RAMPING UP MIN TARGET 2017 BUDGET Leadership and Corp Staff R&D and Scientific Staff Lab CapEx Research Partners Travel Expense Rent Other Staff and Contingency $3.3MM $4.9MM

The Team

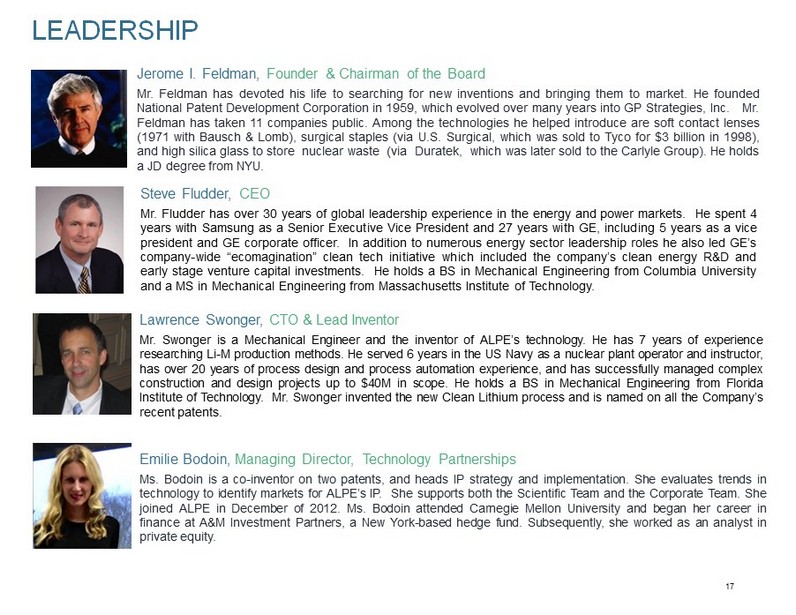

17 LEADERSHIP Jerome I . Feldman, Founder & Chairman of the Board Mr . Feldman has devoted his life to searching for new inventions and bringing them to market . He founded National Patent Development Corporation in 1959 , which evolved over many years into G P Strategies , Inc . Mr . Feldman has taken 11 companies public . Among the technologies he helped introduce are soft contact lenses ( 1971 with Bausch & Lomb), surgical staples (via U . S . Surgical, which was sold to Tyco for $ 3 billion in 1998 ), and high silica glass to store nuclear waste (via Duratek, which was later sold to the Carlyle Group) . He holds a JD degree from NYU . Steve Fludder, CEO Mr . Fludder has over 30 years of global leadership experience in the energy and power markets . He spent 4 years with Samsung as a Senior Executive Vice President and 27 years with GE, including 5 years as a vice president and GE corporate officer . In addition to numerous energy sector leadership roles he also led GE’s company - wide “ ecomagination ” clean tech initiative which included the company’s clean energy R&D and early stage venture capital investments . He holds a BS in Mechanical Engineering from Columbia University and a MS in Mechanical Engineering from Massachusetts Institute of Technology . Lawrence Swonger, C TO & Lead Inventor Mr . Swonger is a Mechanical Engineer and the i nventor of ALPE’s technology . He has 7 years of experience researching Li - M production methods . He served 6 years in the US Navy as a nuclear plant operator and instructor, has over 20 years of process design and process automation experience, and has successfully managed complex construction and design projects up to $ 40 M in scope . He holds a BS in Mechanical Engineering from Florida Institute of Technology . Mr . Swonger invented the new Clean Lithium process and is named on all the Company’s recent patents . Emilie Bodoin, Managing Director , Technology Partnerships Ms . Bodoin is a co - inventor on two patents, and heads IP strategy and implementation . She evaluates trends in technology to identify markets for ALPE’s IP . She supports both the Scientific Team and the Corporate Team . She joined ALPE in December of 2012 . Ms . Bodoin attended Carnegie Mellon University and began her career in finance at A&M Investment Partners, a New York - based hedge fund . Subsequently, she worked as an analyst in private equity .

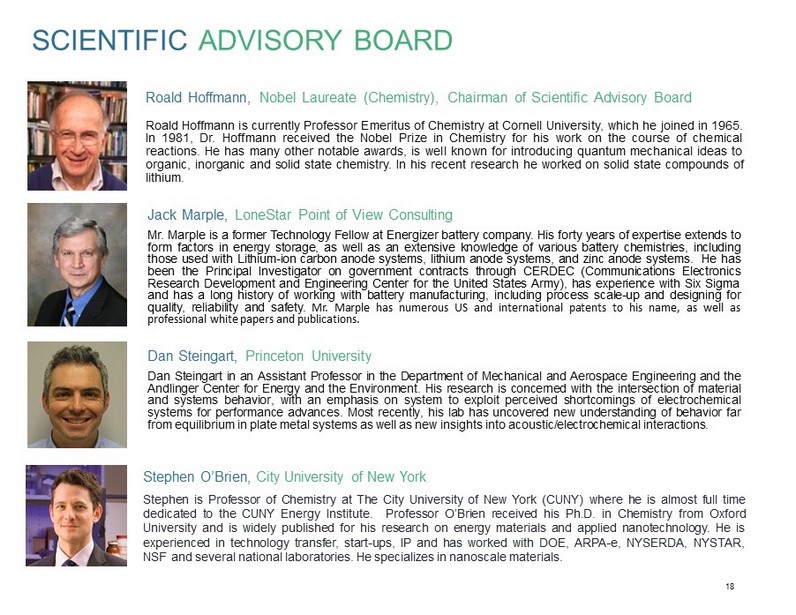

18 SCIENTIFIC ADVISORY BOARD Roald Hoffman n , Nobel Laureate (Chemistry) , Chairman of Scientific Advisory Board Roald Hoffmann is currently Professor Emeritus of Chemistry at Cornell University, which he joined in 1965 . In 1981 , Dr . Hoffmann received the Nobel Prize in Chemistry for his work on the course of chemical reactions . He has many other notable awards , is well known for introducing quantum mechanical ideas to organic, inorganic and solid state chemistry . In his recent research he worked on solid state compounds of lithium . Dan Steingart, Princeton University Dan Steingart in an Assistant Professor in the Department of Mechanical and Aerospace Engineering and the Andlinger Center for Energy and the Environment . His research is concerned with the intersection of material and systems behavior, with an emphasis on system to exploit perceived shortcomings of electrochemical systems for performance advances . Most recently, his lab has uncovered new understanding of behavior far from equilibrium in plate metal systems as well as new insights into acoustic/electrochemical interactions . Stephen O’Brien, C ity University of New York Stephen is Professor of Chemistry at The City University of New York (CUNY) where he is almost full time dedicated to the CUNY Energy Institute . Professor O’Brien received his Ph . D . in Chemistry from Oxford University and is widely published for his research on energy materials and applied nanotechnology . He is experienced in technology transfer, start - ups, IP and has worked with DOE, ARPA - e, NYSERDA, NYSTAR, NSF and several n ational laboratories . He specializes in nanoscale materials . Jack Marple , LoneStar Point of View Consulting Mr . Marple is a former Technology Fellow at Energizer battery company . His forty years of expertise extends to form factors in energy storage, as well as an extensive knowledge of various battery chemistries, including those used with Lithium - ion carbon anode systems, lithium anode systems, and zinc anode systems . He has been the Principal Investigator on government contracts through CERDEC (Communications Electronics Research Development and Engineering Center for the United States Army), has experience with Six Sigma and has a long history of working with battery manufacturing, including process scale - up and designing for quality, reliability and safety . Mr . Marple has numerous US and international patents to his name, as well as professional white papers and publications .

19 CONTACT alpha - En Corporation 120 White Plains Road Suite 425 Tarrytown, NY 10591 914 418 2000 www.alpha - encorp.com Steve Fludder , CEO steve.fludder@alpha - encorp.com Thomas Suppanz , Director of Finance tsuppanz@alpha - encorp.com “The world we were born into is not the same one we live in …” - Anyoymous