Aging

Infrastructure*

Population

Growth/Migration

Regulations/

Compliance

Technical

Innovations

Public

Awareness

• Regional population growth driving need for new schools, hospitals, water,

transportation infrastructure (Texas, Nevada, Arizona)

• Aging boomer generation requiring additional health care facilities

• Clean Water and Safe Drinking Water Acts

• Smaller class sizes mandated by the No Child Left Behind Act

• Technology in classrooms driving renovation of facilities

• Medical advances require retrofitting of medial centers and hospitals

• Mass transit ridership increased 23% from 1997 to 2007**, faster than highway

travel or U.S. population

• Water quality issues and shortages focusing attention on infrastructure needs

• Political Initiatives (Coalition for Building America’s Future, National Infrastructure

Bank Act)

*Source: American Society of Civil Engineers; Urban Land Institute, May 2007

**Source: American Public Transportation Association, 2008 Public Transportation Fact Book, June 2008

11

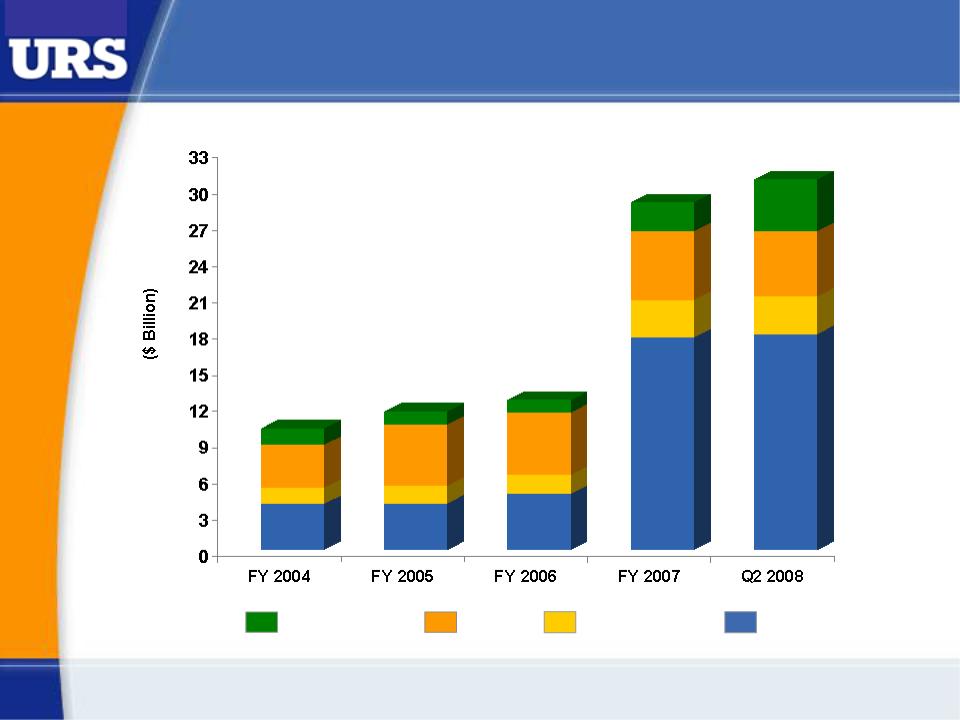

Long-Term Need for Infrastructure

Investment is Clear

• $30-40B of additional annual highway investment required

• More than 25% of nation's bridges rated structurally or functionally deficient

• More than $200B in investments needed in water over next 20 years