UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

___________________

FORM 10-K

___________________

| x | ANNUAL REPORT PURSUANT TO SECTION 13 or 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

| For the fiscal year ended December 30, 2011 |

| | |

| OR |

| |

| o | TRANSITION REPORT PURSUANT TO SECTION 13 or 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the Transition Period from ____________ to _____________

Commission file number 1-7567

___________________

URS CORPORATION

(Exact name of registrant as specified in its charter)

| Delaware | 94-1381538 |

| (State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) |

| | |

600 Montgomery Street, 26th Floor | |

| San Francisco, California | 94111-2728 |

| (Address of principal executive offices) | (Zip Code) |

| | |

(415) 774-2700

(Registrant’s telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class: | | Name of each exchange on which registered: |

| | | |

| Common Shares, par value $.01 per share | | New York Stock Exchange |

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes x No o

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Act. Yes o No x

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No o

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes x No o

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. x

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See definition of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one): Large accelerated filer x Accelerated filer o Non-accelerated filer o Smaller reporting company o

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes o No x

The aggregate market value of the common stock of the registrant held by non-affiliates on February 20, 2012 and July 1, 2011 (the last business day of the registrant’s most recently completed second fiscal quarter) was $3,211.5 million and $3,534.7 million, respectively, based upon the closing sales price of the registrant’s common stock on such dates as reported in the consolidated transaction reporting system. On February 20, 2012 and July 1, 2011, there were 76,321,172 shares and 79,606,275 shares of the registrant’s common stock outstanding, respectively.

Documents Incorporated by Reference

Part III incorporates information by reference from the registrant’s definitive proxy statement for its 2012 Annual Meeting of Stockholders to be filed with the Securities and Exchange Commission.

URS CORPORATION AND SUBSIDIARIES

This Annual Report on Form 10-K contains forward-looking statements within the meaning of the Private Securities Litigation Reform Act of 1995. These forward-looking statements may be identified by words such as “anticipate,” “believe,” “estimate,” “expect,” “potential,” “intend,” “may,” “plan,” “predict,” “project,” “will,” and similar terms used in reference to our future revenues, services, project awards and business trends; future accounting, goodwill and actuarial estimates; future contract gains or losses; future acquisition of Flint Energy Services Ltd.; future backlog and book of business conversion and debookings; future income tax payments and deductions; future stock-based compensation expenses; future bonus, pension and post-retirement expenses; future compliance with regulations; future legal proceedings and accruals; future bonding and insurance coverage; future debt payments; future capital expenditures and commitments; future effectiveness of our disclosure and internal controls over financial reporting and future economic and industry conditions. We believe that our expectations are reasonable and are based on reasonable assumptions, however, we caution against relying on any of our forward-looking statements as such forward-looking statements by their nature involve risks and uncertainties. A variety of factors, including but not limited to the following, could cause our business and financial results, as well as the timing of events, to differ materially from those expressed or implied in our forward-looking statements: declines in the economy or client spending; changes in our book of business; our compliance with government contract procurement regulations; impairment of our goodwill; integration of acquisitions; employee, agent or partner misconduct; our ability to procure government contracts; liabilities for pending and future litigation; environmental liabilities; availability of bonding and insurance; our reliance on government appropriations; unilateral termination provisions in government contracts; our ability to make accurate estimates and assumptions; our accounting policies; workforce utilization; our and our partners’ ability to bid on, win, perform and renew contracts and projects; liquidated damages; our dependence on partners, subcontractors and suppliers; customer payment defaults; our ability to recover on claims; impact of target and fixed-priced contracts on earnings; the inherent dangers at our project sites; the impact of changes in laws and regulations; nuclear indemnifications and insurance; misstatements in expert reports; a decline in defense spending; industry competition; our ability to attract and retain key individuals; retirement plan obligations; our leveraged position and the ability to service our debt; restrictive covenants in our credit agreement; risks associated with international operations; business activities in high security risk countries; information technology risks; natural and man-made disaster risks; our relationships with labor unions; our ability to protect our intellectual property rights; anti-takeover risks and other factors discussed more fully in Management’s Discussion and Analysis of Financial Condition and Results of Operations beginning on page 40, Risk Factors beginning on page 18, as well as in other reports subsequently filed from time to time with the United States Securities and Exchange Commission. We assume no obligation to revise or update any forward-looking statements.

Summary

We are a leading international provider of engineering, construction and technical services. We offer a broad range of program management, planning, design, engineering, construction and construction management, operations and maintenance, and decommissioning and closure services to public agencies and private sector clients around the world. We also are a United States (“U.S.”) federal government contractor in the areas of systems engineering and technical assistance, operations and maintenance, and information technology (“IT”) services. We have more than 46,000 employees in a global network of offices and contract-specific job sites in more than 40 countries.

We provide our services through three reporting segments, which we refer to as our Infrastructure & Environment, Federal Services and Energy & Construction Divisions. Our Infrastructure & Environment Division provides a wide range of program management, planning, design, engineering, construction and construction management, and operations and maintenance services to a variety of U.S. and international government agencies and departments, as well as to private sector clients. Our Federal Services Division provides program management, planning, systems engineering and technical assistance, construction and construction management, operations and maintenance, and decommissioning and closure services to U.S. federal government agencies, primarily the Department of Defense (“DOD”), the National Aeronautics and Space Administration (“NASA”), and the Department of Homeland Security (“DHS”). Our Energy & Construction Division provides program management, planning, design, engineering, construction and construction management, operations and maintenance, and decommissioning and closure services to U.S. and international government agencies and departments, as well as to private sector clients.

On June 1, 2011, we completed the acquisition of Apptis Holdings, Inc. (“Apptis”). Apptis provides IT services to the U.S. federal government. The addition of Apptis expands our capabilities in the federal IT market. At the close of the transaction, Apptis’ operations became part of our Federal Services Division.

For information on our business by segment and geographic region, please refer to Note 15, “Segment and Related Information” to our “Consolidated Financial Statements and Supplementary Data,” which is included under Item 8 of this report and incorporated into this Item by reference. For information on risks related to our business, segments and geographic regions, including risks related to foreign operations, please refer to Item 1A, “Risk Factors” of this report.

Clients, Market Sectors and Services

We serve public agencies and private sector companies worldwide through our global network of offices including locations in the Americas, the United Kingdom (“U.K.”), continental Europe, the Middle East, India, China, Australia and New Zealand. Our clients include U.S. federal government agencies, national governments of other countries, state and local government agencies both in the U.S. and in other countries, and private sector clients representing a broad range of industries. See Note 15, “Segment and Related Information,” to our “Consolidated Financial Statements and Supplementary Data” included under Item 8 of this report for financial information regarding geographic areas.

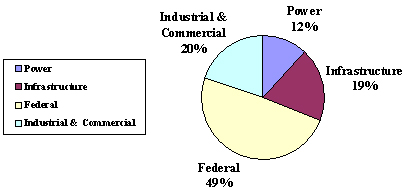

Our expertise is focused in four market sectors: power, infrastructure, federal, and industrial and commercial. Within these markets, we offer a broad range of services, including program management; planning, design and engineering; systems engineering and technical assistance; IT services; construction and construction management; operations and maintenance; and decommissioning and closure.

The following chart and table illustrate the percentage of our revenues by market sector for the year ended December 30, 2011, and representative services we provide in each of these markets.

2011 Revenues by Market Sector

| | | Market Sector | |

| Representative Services | | Power | | Infrastructure | | Federal | | Industrial & Commercial | |

| Program Management | | ü | | ü | | ü | | ü | |

| Planning, Design and Engineering | | ü | | ü | | ü | | ü | |

| Systems Engineering and Technical Assistance | | — | | — | | ü | | — | |

| Information Technology Services | | — | | — | | ü | | — | |

| Construction and Construction Management | | ü | | ü | | ü | | ü | |

| Operations and Maintenance | | ü | | ü | | ü | | ü | |

| Decommissioning and Closure | | ü | | — | | ü | | ü | |

ü the service is provided in the market sector.

— the service is not provided in the market sector.

Market Sectors

The following table summarizes the primary market sectors served by our three divisions for the year ended December 30, 2011.

| | | Division |

| Market Sector | | Infrastructure & Environment | | Federal Services | | Energy & Construction |

| Power | | ü | | — | | ü |

| Infrastructure | | ü | | — | | ü |

| Federal | | ü | | ü | | ü |

| Industrial & Commercial | | ü | | — | | ü |

ü a primary market sector for the division.

— not a primary market sector for the division.

Power

We plan, design, engineer, construct, retrofit and maintain a wide range of power-generating facilities, as well as the systems that transmit and distribute electricity. Our services include planning, siting and licensing, permitting, engineering, procurement, construction and construction management, facility start-up, operations and maintenance, upgrades and modifications, and decommissioning and closure. We provide these services to utilities, industrial co-generators, independent power producers, original equipment manufacturers and government utilities. We also specialize in the development and installation of clean air technologies that reduce emissions at both new and existing fossil fuel power plants. These technologies help power-generating facilities comply with air quality regulations.

Our project expertise in our power market sector encompasses services related to the following:

| · | Fossil fuel power generating facilities; |

| · | Nuclear power generating facilities; |

| · | Hydroelectric power generating facilities; |

| · | Alternative and renewable energy sources, including biomass, geothermal, solar energy and wind systems; |

| · | Transmission and distribution systems; and |

| · | Emissions control systems. |

Infrastructure

We provide a broad range of the services required to build, expand and modernize infrastructure, including surface, air and rail transportation networks; ports and harbors; water supply, treatment and conveyance systems; and many types of facilities. We serve as the program manager, planner, architect, engineer, general contractor, constructor and/or construction manager for a wide variety of infrastructure projects, and we also provide operations and maintenance services when a project has been completed.

Our clients in our infrastructure market sector include local municipalities, community planning boards, state and municipal departments of transportation and public works, transit authorities, water and wastewater authorities, environmental protection agencies, school boards and authorities, colleges and universities, judiciary agencies, hospitals, ports and harbors authorities and owners, airport authorities and owners, and airline carriers.

Our project expertise in our infrastructure market sector encompasses services related to the following:

| · | Highways, interchanges, bridges, tunnels and toll road facilities; |

| · | Intelligent transportation systems, such as traffic management centers; |

| · | Airport terminals, hangars, cargo facilities and people movers; |

| · | Air traffic control towers, runways, taxiways and aircraft fueling systems; |

| · | Baggage handling, baggage screening and other airport security systems; |

| · | Light rail, subways, bus rapid transit systems, commuter/intercity railroads, heavy rail and high-speed rail systems; |

| · | Rail transportation structures, including terminals, stations, multimodal facilities, parking facilities, bridges and tunnels; |

| · | Piers, wharves, seawalls, recreational marinas and small craft harbors; |

| · | Container terminals, liquid and dry bulk terminals and storage facilities; |

| · | Water supply, storage, distribution and treatment systems; |

| · | Municipal wastewater treatment and sewer systems; |

| · | Dams, levees, watershed and stormwater management, flood control systems and coastal restoration; |

| · | Education, judicial, correctional, healthcare, retail, sports and recreational facilities; and |

| · | Industrial, manufacturing, research and office facilities. |

Federal

As a major contractor to the U.S. federal government and national governments of other countries, we serve a wide variety of government departments and agencies, including the DOD, DHS, Department of Energy (“DOE”), as well as the General Services Administration, the Environmental Protection Agency (“EPA”), NASA and other federal agencies. We also serve departments and agencies of other national governments, such as the U.K. Nuclear Decommissioning Authority (“NDA”). Our services range from program management; planning, design and engineering; systems engineering and technical assistance; and IT services to construction and construction management; operations and maintenance; and decommissioning and closure.

We modernize weapons systems, refurbish military vehicles and aircraft, train pilots and manage military and other government installations. We provide logistics support for military operations and help decommission former military bases for redevelopment. In the area of global threat reduction, we support programs to eliminate nuclear, chemical and biological weapons, and we assist the DOE and other nuclear regulatory agencies outside the U.S. in the management of complex programs and facilities. We also provide a wide range of IT services to both defense and civilian agencies to improve the efficiency and productivity of their IT networks and systems, and to combat cyber security threats.

Our project expertise in our federal market sector encompasses the following:

| · | Operation and maintenance of complex government installations, including military bases and test ranges; |

| · | Logistics support for government supply and distribution networks, including warehousing, packaging, delivery and traffic management; |

| · | Weapons system design, maintenance and modernization, including acquisition support for new defense systems, and engineering and technical assistance for the modernization of existing systems; |

| · | Maintenance planning to extend the service life of weapons systems and other military equipment; |

| · | Maintenance, modification and overhaul of military aircraft and ground vehicles; |

| · | Training military pilots; |

| · | Management and operations and maintenance services for complex DOE and NDA programs and facilities; |

| · | Deactivation, decommissioning and disposal of nuclear weapons stockpiles and other nuclear waste; |

| · | Safety analyses for high-hazard facilities and licensing for DOE sites; |

| · | Threat assessments of public facilities and the development of force protection and security systems; |

| · | Planning and conducting emergency preparedness exercises; |

| · | First responder training for the military and other government agencies; |

| · | Management and operations and maintenance of chemical agent and chemical weapon disposal facilities; |

| · | Installation of monitoring technology to detect the movement of nuclear and radiological materials across national borders; |

| · | Planning, design and construction of aircraft hangars, barracks, military hospitals and other government buildings; |

| · | Environmental remediation and restoration for the redevelopment of military bases and other government installations; and |

| · | Network and communications engineering, software engineering, IT infrastructure design and implementation, cyber defense and cloud computing technologies. |

Industrial & Commercial

We provide a wide range of engineering, procurement and construction services for new industrial and commercial infrastructure and process facilities and the expansion, modification and upgrade of existing facilities. These services include front-end studies, engineering and process design, procurement, construction and construction management, facility management, and operations and maintenance. Our expertise also includes due diligence, permitting, compliance, environmental management, pollution control, health and safety, waste management and hazardous waste remediation. For facilities that are no longer in use, we provide site decommissioning and closure services.

Our industrial and commercial clients represent a broad range of industries, including automotive, chemical, consumer products, pharmaceutical, manufacturing, mining, power, oil and gas, and pipelines. Over the past several years, many of these companies have reduced the number of service providers they use, selecting larger, global multi-service contractors, like URS, in order to control overhead costs.

Our project expertise in our industrial and commercial market sector encompasses services related to the following:

| · | Oil and gas refineries, processing and storage facilities, and pipelines; |

| · | Biotechnology and pharmaceutical research laboratories, pilot plants and production facilities; |

| · | Petrochemical, specialty chemical and polymer facilities; |

| · | Consumer products and food and beverage production facilities; |

| · | Automotive and other manufacturing facilities; |

| · | Pulp and paper production facilities; and |

| · | Mines and mining facilities for base and precious metals, industrial minerals and energy fuels. |

Representative Services

We provide program management; planning, design and engineering; systems engineering and technical assistance; information technology services; construction and construction management; operations and maintenance; and decommissioning and closure services to U.S. federal government agencies, national governments of other countries, state and local government agencies both in the U.S. and overseas, and private sector clients representing a broad range of industries. Although we are typically the prime contractor, in some cases, we provide services as a subcontractor or through joint ventures or partnership agreements with other service providers.

The following table summarizes the services provided by our divisions for the year ended December 30, 2011.

| | | Division | |

| Services | | Infrastructure & Environment | | Federal Services | | Energy & Construction | |

| Program Management | | ü | | ü | | ü | |

| Planning, Design and Engineering | | ü | | ü | | ü | |

| Systems Engineering and Technical Assistance | | — | | ü | | — | |

| Information Technology Services | | — | | ü | | — | |

| Construction and Construction Management | | ü | | ü | | ü | |

| Operations and Maintenance | | ü | | ü | | ü | |

| Decommissioning and Closure | | ü | | ü | | ü | |

| ü | the division provides the listed service. |

| — | the division does not provide the listed service. |

Program Management. We provide the technical and administrative services required to manage, coordinate and integrate the multiple and concurrent assignments that comprise a large program – from conception through completion. For large military programs, which typically involve naval, ground, vessel and airborne platforms, our program management services include logistics planning, acquisition management, risk management of weapons systems, safety management and subcontractor management. We also provide program management services for large capital improvement programs, which typically involve the oversight of a wide variety of activities ranging from planning, coordination, scheduling and cost control to design, construction and commissioning.

Planning, Design and Engineering. The planning process is typically used to develop a blueprint or overall scheme for a project. Based on the project requirements identified during the planning process, detailed engineering drawings and calculations are developed, which may include material specifications, construction cost estimates and schedules. Our planning, design and engineering services include the following:

| · | Transportation planning; |

| · | Technical and economic feasibility studies; |

| · | Environmental impact assessments; |

| · | Project development/design; |

| · | Quality assurance and validation; |

| · | Integrated safety management and analysis; |

| · | Alternative design analysis; |

| · | Conceptual and final design documents; |

| · | Technical specifications; and |

| · | Process engineering and design. |

We provide planning, design and engineering services for the construction of new transportation projects and for the renovation and expansion of existing transportation infrastructure, including bridges, highways, roads, airports, mass transit systems and railroads, and ports and harbors. We also plan and design many types of facilities, such as schools, courthouses and hospitals; power generation, industrial and commercial facilities; waste treatment and disposal facilities; water supply and conveyance systems and wastewater treatment plants; and corporate offices and retail outlets. Our planning, design and engineering capabilities also support homeland security and global threat reduction programs; hazardous and radioactive waste clean-up activities at government sites and facilities; and environmental assessment, due diligence and permitting at government, commercial and industrial facilities. We also provide planning, design and engineering support to U.S. federal government clients for major research and development projects, as well as for technology development and deployment.

Systems Engineering and Technical Assistance. We provide a broad range of systems engineering and technical assistance to all branches of the U.S. military for the design and development of new weapons systems and the modernization of aging weapons systems. We have the expertise to support a wide range of platforms including aircraft and helicopters, tracked and wheeled vehicles, ships and submarines, shelters and ground support equipment. Representative systems engineering and technical assistance services include the following:

| · | Defining operational requirements and developing specifications for new weapons systems; |

| · | Reviewing hardware and software design data; and |

| · | Developing engineering documentation for these systems. |

We support a number of activities including technology insertion, system modification, installation of new systems/equipment, design of critical data packages, and configuration management.

Information Technology Services. We provide a broad range of IT services to U.S. federal government clients, including both civilian and defense agencies. Our expertise covers network and communications engineering, software engineering, IT infrastructure design and implementation, cyber defense and cloud computing technologies. Our services typically include:

| · | Assisting government agencies in developing, implementing and managing secure, federally compliant cloud computing technologies; |

| · | Cyber defense services, including vulnerability assessments, policy development and management, compliance, incident response, disaster recovery and continuity of operations; |

| · | Engineering, procuring, installing, certifying and operating IT networks; and |

| · | Developing software applications for complex, multi-user, multi-platform systems. |

Construction and Construction Management Services. We provide construction contracting and construction management services for projects involving transportation, environmental and waste management, power generation and transmission, industrial and manufacturing facilities, water resources and wastewater treatment, government buildings and facilities, and mining projects. As a contractor, we are responsible for the construction and completion of a project in accordance with its specifications and contracting terms. In this capacity, we often manage the procurement of materials, equipment and supplies; directly supervise craft labor; and manage and coordinate subcontractors. Our services typically include the following:

| · | Procuring specified materials and equipment; |

| · | Managing project logistics; |

| · | Supervising and completing physical construction; |

| · | Managing project milestone and completion schedules; |

| · | Managing project cost controls and accounting; |

| · | Negotiating and expediting change orders; |

| · | Administering job site safety, security and quality control programs; and |

| · | Preparing and delivering as-built drawings. |

As a construction manager, we serve as the client’s representative to ensure compliance with design specifications and contract terms. In performing these services, we may purchase equipment and materials on behalf of the client; monitor the progress, cost and quality of construction projects in process and oversee and coordinate the activities of construction contractors. Our services typically include the following:

| · | Contract administration; |

| · | Change order management; |

| · | Cost and schedule management; |

| · | Safety program and performance monitoring; |

| · | Quality control and quality assurance; |

| · | Claims and dispute resolution. |

Operations and Maintenance. We provide operations and maintenance services in support of large military installations and operations, and hazardous facilities, as well as for transportation systems, industrial and manufacturing facilities, and mining operations. Our services include the following:

| · | Management of military base logistics, including overseeing the operation of government warehousing and distribution centers, as well as government property and asset management; |

| · | Maintenance, modification, overhaul and life service extension services for military vehicles, vessels and aircraft; |

| · | Management, maintenance and operation of chemical agent and chemical weapons disposal systems; |

| · | Comprehensive military flight training services; |

| · | Development and maintenance of high-security systems; |

| · | Management of high-risk, technically complex chemical and nuclear processing facilities; |

| · | Integrated facilities and logistics management for industrial and manufacturing facilities; |

| · | Toll road, light rail and airport operations; |

| · | Operating mine and metal and mineral processing facilities; and |

| · | Other miscellaneous services such as staffing, repair, renovation, predictive and preventive maintenance, and health and safety services. |

Decommissioning and Closure. We provide decommissioning and closure services for nuclear power plants, nuclear research and test facilities, production sites and laboratories. Many of these facilities have been highly contaminated and contain significant inventories of chemical and nuclear materials. We also provide decommissioning and closure services for the DOD at chemical weapons depots and for military installations under the DOD’s Base Realignment and Closure program, as well as for industrial facilities and mining operations. Our services include the following:

| · | Planning, scoping surveys and cost estimating; |

| · | Due diligence and permitting; |

| · | Environmental remediation; |

| · | Hazardous chemical and nuclear waste stabilization treatment and disposition; |

| · | Construction/demolition management; and |

| · | Redevelopment and reuse. |

Major Customers

Our largest clients are from our federal market sector. Within this sector, we have multiple contracts with our two major customers: the U.S. Army and DOE. For the purpose of analyzing revenues from major customers, we do not consider the combination of all federal departments and agencies as one customer because the different federal agencies we serve manage separate budgets. As such, reductions in spending by one federal agency do not affect the revenues we could earn from another federal agency. In addition, the procurement processes for federal agencies are not centralized, and procurement decisions are made separately by each agency. The loss of the federal government, the U.S. Army, or the DOE as clients would have a material adverse effect on our business; however, we are not dependent on any single contract on an ongoing basis. We believe that the loss of any single contract would not have a material adverse effect on our business.

Our revenues from the U.S. Army and DOE by division for the years ended December 30, 2011, December 31, 2010, and January 1, 2010 are presented below:

| | | Year Ended | |

| | | December 30, | | | December 31, | | | January 1, | |

| (In millions, except percentages) | | 2011 | | | 2010 | | | 2010 | |

The U.S. Army (1) | | | | | | | | | |

Infrastructure & Environment | | $ | 141.7 | | | $ | 167.0 | | | $ | 145.0 | |

Federal Services | | | 1,351.1 | | | | 1,408.7 | | | | 1,403.1 | |

Energy & Construction | | | 199.5 | | | | 346.6 | | | | 117.3 | |

Total U.S. Army | | $ | 1,692.3 | | | $ | 1,922.3 | | | $ | 1,665.4 | |

Revenues from the U.S. Army as a percentage of our consolidated revenues | | | 18 | % | | | 21 | % | | | 18 | % |

| | | | | | | | | | | | | |

| DOE | | | | | | | | | | | | |

Infrastructure & Environment | | $ | 5.9 | | | $ | 7.2 | | | $ | 9.5 | |

Federal Services | | | 26.8 | | | | 13.7 | | | | 37.4 | |

Energy & Construction | | | 1,236.3 | | | | 1,182.6 | | | | 785.3 | |

Total DOE | | $ | 1,269.0 | | | $ | 1,203.5 | | | $ | 832.2 | |

Revenues from DOE as a percentage of our consolidated revenues | | | 13 | % | | | 13 | % | | | 9 | % |

| | | | | | | | | | | | | |

Revenues from the federal market sector as a percentage of our consolidated revenues | | | 49 | % | | | 49 | % | | | 45 | % |

| (1) | The U.S. Army includes U.S. Army Corps of Engineers. |

Competition

Our industry is highly fragmented and intensely competitive. We have numerous competitors, ranging from small private firms to multi-billion dollar companies. The technical and professional aspects of our services generally do not require large upfront capital expenditures and, therefore, provide limited barriers against new competitors. Some of our competitors have achieved greater market penetration in some of the markets in which we compete and have substantially more financial resources and/or financial flexibility than we do. To our knowledge, no individual company currently dominates any significant portion of our markets.

We believe that we are well positioned to compete in our markets because of our reputation, our cost effectiveness, long-term client relationships, extensive network of offices, employee expertise, and broad range of services. In addition, as a result of our national and international network of offices and contract-specific job sites in more than 40 countries, we are able to offer our clients localized knowledge and expertise, as well as the support of our worldwide professional staff.

Our Infrastructure & Environment, Federal Services, and Energy & Construction Divisions operate in similar competitive environments. All three divisions compete based on performance, reputation, expertise, price, technology, customer relationships and a range of service offerings. In addition, our Infrastructure & Environment and Energy & Construction Divisions compete through domestic and international office networks. The following is a list of primary competitors for each of our divisions:

| · | The primary competitors of our Infrastructure & Environment Division include AECOM Technology Corporation, CH2M HILL Companies, Ltd., Fluor Corporation, Jacobs Engineering Group Inc., Tetra Tech, Inc., and The Shaw Group Inc. |

| · | The primary competitors of our Federal Services Division include CACI International Inc., Computer Sciences Corporation, ManTech International Corporation, NCI, Inc. and Science Applications International Corporation. |

| · | The primary competitors of our Energy & Construction Division include AMEC, Bechtel Corporation, Black & Veatch Corporation, CH2M HILL Companies, Ltd., EnergySolutions, Inc., Fluor Corporation, Granite Construction Company, Jacobs Engineering Group Inc., KBR, Inc., Kiewit Corporation, Skanska, The Babcock & Wilcox Company, The Shaw Group Inc and Worley Parsons, Ltd. |

For the purpose of calculating our book of business, we determine the amounts of all contract awards that may potentially be recognized as revenues. We also include an estimate of the equity in income of unconsolidated joint ventures over the life of the contracts in our book of business. We categorize the amount of our book of business into backlog, option years and indefinite delivery contracts (“IDCs”), based on the nature of the award and its current status.

Backlog. Our contract backlog represents the monetary value of signed contracts, including task orders that have been issued and funded under IDCs and, where applicable, a notice to proceed has been received from the client that is expected to be recognized as revenues or equity in income of unconsolidated joint ventures as services are performed.

The performance periods of our contracts vary widely from a few months to many years. In addition, contract durations often differ significantly among our divisions. As a result, the amount of revenues that will be realized beyond one year also varies from segment to segment. As of December 30, 2011, we estimated that approximately 57% of our total backlog would not be realized within one year, based upon the timing of awards and the long-term nature of many of our contracts; however, no assurance can be given that backlog will be realized at this rate.

Option Years. Our option years represent the monetary value of option periods under existing contracts in backlog, which are exercisable at the option of our clients without requiring us to go through an additional competitive bidding process and would be canceled only if a client decided to end the project (a termination for convenience) or through a termination for default. Option years are in addition to the “base periods” of these contracts. Base periods for these contracts can vary from one to five years.

Indefinite Delivery Contracts. IDCs represent the expected monetary value to us of signed contracts under which we perform work only when the client awards specific task orders or projects to us. When agreements for such task orders or projects are signed and funded, we transfer their value into backlog. Generally, the terms of these contracts exceed one year and often include a maximum term and potential value. IDCs generally range from one to twenty years in length.

While the value of our book of business is a predictor of future revenues and equity in income of unconsolidated joint ventures, we have no assurance, nor can we provide assurance, that we will ultimately realize the maximum potential values for backlog, option years or IDCs. Based on our historical experience, our backlog has the highest likelihood of converting into revenues or equity in income of unconsolidated joint ventures because it is based upon signed and executable contracts with our clients. Option years are not as certain as backlog because our clients may decide not to exercise one or more option years. Because we do not perform work under IDCs until specific task orders are issued by our clients, the value of our IDCs is not as likely to convert into revenues or equity in income of unconsolidated joint ventures as other categories of our book of business.

As of December 30, 2011 and December 31, 2010, our total book of business was $27.0 billion and $29.1 billion, respectively. In addition to reductions for recognition of revenues and equity in earnings of unconsolidated joint ventures, we reduced backlog amounts as follows:

| · | $1,183.0 million caused by successfully achieving early completion of chemical weapons stockpile processing under three federal contracts; |

| · | $222.2 million due to the cancellation of a Jamaican mining project; |

| · | $106.2 million caused by successful cost underruns on two target-price power projects; |

| · | $85.0 million related to scope adjustments under a federal maintenance contract; |

| · | $44.8 million caused by project scope changes on other power projects; and |

| · | $35.0 million caused by a scope adjustment on a federal nuclear remediation project. |

Additional decreases were caused, in part, by delays in federal procurement activities. These decreases were partially offset by additions of $727 million to our book of business resulting from our acquisition of Apptis and $887 million from contracts to retrofit coal-fired power plants with clean air technology to meet increasingly stringent emissions reduction mandates. The following tables summarize our book of business:

| | | | | Infrastructure | | | | | Energy | | | |

| | | | | & | | Federal | | & | | | |

| (In millions) | | Environment | | Services | | Construction | | Total |

| As of December 30, 2011 | | | | | | | | | | | | |

Backlog | | $ | 2,993.1 | | $ | 4,141.8 | | $ | 7,124.7 | | $ | 14,259.6 |

Option years | | | 316.6 | | | 2,370.1 | | | 2,026.2 | | | 4,712.9 |

Indefinite delivery contracts | | | 2,806.5 | | | 3,304.0 | | | 1,948.0 | | | 8,058.5 |

| | | Total book of business | | $ | 6,116.2 | | $ | 9,815.9 | | $ | 11,098.9 | | $ | 27,031.0 |

| | | | | | | | | | | | | | | |

| As of December 31, 2010 | | | | | | | | | | | | |

Backlog | | $ | 3,259.1 | | $ | 6,002.2 | | $ | 7,346.4 | | $ | 16,607.7 |

Option years | | | 342.6 | | | 2,288.1 | | | 2,117.7 | | | 4,748.4 |

Indefinite delivery contracts | | | 3,436.3 | | | 3,208.9 | | | 1,071.2 | | | 7,716.4 |

| | | Total book of business | | $ | 7,038.0 | | $ | 11,499.2 | | $ | 10,535.3 | | $ | 29,072.5 |

| | | | | | | | | | | | | | | |

| | | | | | | | | | | December 30, | | December 31, | | |

| | (In millions) | | 2011 | | 2010 | | |

| | Backlog by market sector: | | | | | | | | |

| | | | Power | | $ | 1,623.8 | | $ | 1,407.7 | | |

| | | | Infrastructure | | | 3,011.0 | | | 2,564.5 | | |

| | | | Industrial and commercial | | | 1,082.4 | | | 1,347.3 | | |

| | | | Federal | | | 8,542.4 | | | 11,288.2 | | |

| | | | | | Total backlog | | $ | 14,259.6 | | $ | 16,607.7 | | |

We were originally incorporated in California on May 1, 1957, under the former name of Broadview Research Corporation. On May 18, 1976, we re-incorporated in Delaware under the name URS Corporation. After several additional name changes, we re-adopted the name “URS Corporation” on February 21, 1990.

Regulations

We provide services for projects that are subject to government oversight, including environmental laws and regulations, general government procurement laws and regulations, and other government regulations and requirements. Below is a summary of some of the regulations that impact our business. For more information on risks associated with our government regulations, please refer to Item 1A, “Risk Factors,” of this report.

Environmental Regulations. A portion of our business involves the planning, design, construction management, and operation and maintenance of pollution control facilities, as well as the assessment, design and management of remediation activities at hazardous waste or Superfund sites and military bases. In addition, we have contracts with U.S. federal governmental entities to destroy hazardous and radioactive materials, including chemical agents and weapons stockpiles. These activities may require us to manage, handle, remove, treat, transport and dispose of toxic or hazardous substances.

Some environmental laws including the Resource Conservation and Recovery Act of 1976, as amended, and the Comprehensive Environmental Response Compensation and Liability Act of 1980, as amended, (“CERCLA”), as well as other governmental laws can impose liability for the entire cost of the clean-up of contaminated facilities or sites upon present and former owners and operators as well as generators, transporters and persons arranging for the treatment or disposal of such substances. While we strive to handle hazardous and toxic substances with care and in accordance with safe methods, the possibility of accidents, leaks, spills and the events of force majeure always exist. Humans exposed to these materials, including employees or subcontractors engaged in the transportation and disposal of hazardous materials, and persons in affected areas may be injured or become ill, resulting in lawsuits that expose us to liability and may result in substantial damage awards against us. Liabilities for contamination or human exposure to hazardous or toxic materials or a failure to comply with applicable regulations could result in substantial costs to us, including clean-up costs, fines and civil or criminal sanctions, third-party claims for property damage or personal injury, or cessation of remediation activities.

Some of our business operations are covered by Public Law 85-804, which provides for indemnification by the U.S federal government against claims and damages arising out of unusually hazardous or nuclear activities performed at the request of the U.S. federal government. Should public policies and laws be changed, however, U.S. federal government indemnification may not be available in the case of any future claims or liabilities relating to hazardous activities that we undertake to perform.

Government Procurement. The services we provide to the U.S. federal government are subject to the Federal Acquisition Regulation (“FAR”), the Truth in Negotiations Act, the Cost Accounting Standards (“CAS”), the American Recovery and Reinvestment Act (“ARRA”), the Service Contract Act, DOD security regulations, and other rules and regulations applicable to government contracts, each as amended. These laws and regulations affect how we transact business with our government clients and in some instances, impose added costs to our business operations. A violation of specific laws and regulations could lead to fines, contract termination or suspension of future contracts. Our government clients can also terminate, renegotiate, or modify any of their contracts with us at their convenience, and many of our government contracts are subject to renewal or extension annually.

Other regulations and requirements. We provide services to the DOD and other defense-related entities that often require specialized professional qualifications and security clearances. Our international business is also subject to the Foreign Corrupt Practices Act, as well as various export control, anti-boycott, and embargo laws. In addition, as engineering design services professionals, we are subject to a variety of local, state, federal and foreign licensing and permit requirements and ethics rules.

Sales and Marketing

Our Infrastructure & Environment Division performs business development, sales and marketing activities primarily through our network of local offices around the world. For large, market-specific projects requiring diverse technical capabilities, we utilize the company-wide resources of specific disciplines. This often involves coordinating marketing efforts on a regional, national or global level. Our Federal Services Division performs business development, sales and marketing activities primarily through its management groups, which address specific markets, such as homeland security and defense systems. In addition, our Federal Services Division coordinates national marketing efforts on large projects, which often involve a multi-segment or multi-market scope. Our Energy & Construction Division conducts business development, sales and marketing activities at a market sector level. For large complex projects, markets or clients that require broad-based capabilities, business development efforts are coordinated across our divisions. Over the past year, our divisions have been successful in marketing their combined capabilities to win new work with clients in the various markets we serve.

Seasonality

We experience seasonal trends in our business in connection with federal holidays, such as Memorial Day, Independence Day, Thanksgiving, Christmas and New Year’s Day. Our revenues are typically lower during these times of the year because many of our clients’ employees, as well as our own employees, do not work during these holidays, resulting in fewer billable hours worked on projects and thus lesser revenues recognized. In addition to holidays, our business also is affected by seasonal bad weather conditions, such as hurricanes, floods, snowstorms or other inclement weather, which may cause some of our offices and projects to temporarily reduce activities.

Raw Materials

We purchase most of the raw materials and components necessary to operate our business from numerous sources. However, the price and availability of raw materials and components may vary from year to year due to customer demand, production capacity, market conditions and material shortages. While we do not currently foresee the lack of availability of any particular raw materials in the near term, prolonged unavailability of raw materials necessary to our projects and services or significant price increases for those raw materials could have a material adverse effect on our business in the near term.

Government Contracts

Generally, our government contracts are subject to renegotiation or termination of contracts or subcontracts at the discretion of the U.S. federal, state or local governments, and national governments of other countries.

Trade Secrets and Other Intellectual Property

We rely principally on trade secrets, confidentiality policies and other contractual arrangements to protect much of our intellectual property where we do not believe that patent or copyright protection is appropriate or obtainable.

Research and Development

We have not incurred material costs for company-sponsored research and development activities.

Insurance

Generally, our insurance program covers workers’ compensation and employer’s liability, general liability, automobile liability, professional errors and omissions liability, property, marine property and liability, and contractor’s pollution liability (in addition to other policies for specific projects). Our insurance program includes deductibles or self-insured retentions for each covered claim. In addition, our insurance policies contain exclusions and sublimits that insurance providers may use to deny or restrict coverage. Excess liability, contractor’s pollution liability, and professional liability insurance policies provide for coverages on a “claims-made” basis, covering only claims actually made and reported during the policy period currently in effect. Thus, if we do not continue to maintain these policies, we will have no coverage for claims made after the termination date even for claims based on events that occurred during the term of coverage. While we intend to maintain these policies, we may be unable to maintain existing coverage levels.

Employees

The number of our employees varies with the volume, type and scope of our operations at any given time. As of January 27, 2012, we had more than 46,000 employees, including part-time workers. The Infrastructure & Environment, Federal Services, and Energy & Construction Divisions employed approximately 21,000, 15,000, and 10,000 persons (including part-time workers), respectively. At various times, we have employed up to several thousand workers on a part-time basis to meet our contractual obligations. Approximately 12% of our employees are covered by collective bargaining agreements or by specific labor agreements, which expire upon completion of the relevant project.

Executive Officers of the Registrant

| | | | | |

| | | | | | |

| Martin M. Koffel | | Chief Executive Officer (“CEO”), President and Director since May 1989; Chairman of the Board since June 1989. | | | 72 | |

| Thomas W. Bishop | | Senior Vice President of the Infrastructure & Environment Division since January 2011; Vice President, Strategy since July 2003; Senior Vice President, Construction Services since March 2002. | | | 65 | |

| Hugh Blackwood | | Senior Vice President, International Operations and Vice President since September 2010; CEO of Scott Wilson Group plc. (“Scott Wilson”) from May 2006 to September 2010. | | | 63 | |

| Reed N. Brimhall | | Chief Accounting Officer since May 2005; Vice President since May 2003; Corporate Controller from May 2003 to January 2012. | | | 58 | |

| H. Thomas Hicks | | Vice President and Chief Financial Officer (“CFO”) since March 2006; Vice President, Finance from September 2005 to March 2006. | | | 61 | |

| Gary V. Jandegian | | President of the Infrastructure & Environment Division and Vice President since July 2003. | | | 59 | |

| Susan B. Kilgannon | | Vice President, Communications since October 1999. | | | 53 | |

| Joseph Masters | | Secretary since March 2006; General Counsel since July 1997; and Vice President since July 1994. | | | 55 | |

| Randall A. Wotring | | President of the Federal Services Division and Vice President since November 2004. | | | 55 | |

| Robert W. Zaist | | President of the Energy & Construction Division since July 2011; Senior Executive Vice President Business Development of Energy & Construction Division from January 2008 to July 2011; President of Mining Business Unit for Washington Group International, Inc. (“WGI”) from April 2005 to January 2008. | | | 63 | |

| Thomas H. Zarges | | Chairman of the Energy & Construction Division since July 2011; Vice President since March 2008; President of the Energy & Construction Division from January 2008 to July 2011; Senior Executive Vice President Operations of the Energy & Construction Division from November 2007 through January 2008; Senior Executive Vice President – Operations of WGI from October 2002 through November 2007. | | | 63 | |

Available Information

Our Annual Reports on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K and amendments to those reports filed or furnished pursuant to Section 13(a) or 15(d) of the Securities Exchange Act of 1934, as amended, are available free of charge on our web site at www.urs.com. These reports, and any amendments to these reports, are made available on our web site as soon as reasonably practicable after we electronically file or furnish the reports with the Securities and Exchange Commission (“SEC”). In addition, our Corporate Governance Guidelines, the charters for our Audit, Board Affairs and Compensation Committees, and our Code of Business Conduct and Ethics are available on our web site at www.urs.com under the “Corporate Governance” section. Any waivers or amendments to our Code of Business Conduct and Ethics will be posted on our web site. A printed copy of this information is also available without charge by sending a written request to: Corporate Secretary, URS Corporation, 600 Montgomery Street, 26th Floor, San Francisco, CA 94111-2728.

In addition to the other information included or incorporated by reference in this Annual Report on Form 10-K, the following risk factors could also affect our financial condition and results of operations:

Demand for our services is cyclical and vulnerable to economic downturns and reductions in government and private industry spending. If the economy remains weak or client spending declines further, then our revenues, profits and our financial condition may deteriorate.

Demand for our services is cyclical and vulnerable to economic downturns and reductions in government and private industry spending, which has resulted and may continue to result in delays, curtailment or cancellation of proposed and existing projects. In fiscal years 2010 and 2011, our clients were affected by the weak economic conditions caused by the declines in the global economy and constraints in the credit market. As a result, some clients delayed, curtailed or cancelled proposed and existing projects and may continue to do so. For example, as of December 30, 2011, our book of business declined compared to the end of our 2010 fiscal year, particularly in our federal market sector backlog. In addition, our clients may find it more difficult to raise capital in the future due to limitations on the availability of credit and other uncertainties in the federal, municipal and corporate credit markets, especially in light of the downgrade by Standard & Poor’s of U.S. sovereign debt. Also, our clients may demand more favorable pricing terms and find it increasingly difficult to timely pay invoices for our services, which would impact our future cash flows and liquidity. In addition, any rapid changes in the prices of commodities make it difficult for our clients and us to forecast future capital expenditures. Inflation or significant changes in interest rates could reduce the demand for our services. Any inability to timely collect our invoices may lead to an increase in our accounts receivable and potentially to increased write-offs of uncollectible invoices. If the economy remains weak or uncertain, or client spending declines further, then our revenues, book of business, net income and overall financial condition could deteriorate.

The federal debt ceiling legislation approved in 2011 could significantly reduce government spending for the services we provide.

Congressional negotiations during July and August of 2011 leading to the debt ceiling legislation and related concerns regarding the ability of government to address critical economic issues, together with the announcement by Standard & Poor’s of the downgrading of its rating on U.S. sovereign debt, resulted in significant and continuing financial market and economic disruptions. On August 2, 2011, federal legislation increasing the federal debt ceiling included significant reductions in spending, a substantial portion of which is related to defense spending. Moreover, further spending cutbacks, including severe reductions in defense spending, could result from the efforts, or the failure of efforts, by the Joint Select Committee on Deficit Reduction to reduce the federal debt mandated by the second phase of the debt ceiling legislation. Any significant reduction in federal government expenditures could reduce government demand for the services we provide, including defense spending and could have a material adverse effect on our results of operation and financial condition.

Our failure to conduct due diligence effectively or our inability to integrate acquisitions successfully could impede us from realizing all of the benefits of the acquisition, which could severely weaken our results of operations.

Historically, we have used acquisitions as one way to expand our business. For example, we have just announced our proposed acquisition of Flint Energy Services Ltd. (“Flint”) If we fail to conduct due diligence on our potential targets effectively, we may, for example, not identify problems at target companies or fail to recognize incompatibilities or other obstacles to successful integration. Our inability to successfully integrate future acquisitions could impede us from realizing all of the benefits of those acquisitions and could severely weaken our business operations. The integration process may disrupt our business and, if implemented ineffectively, may preclude realization of the full benefits expected by us and could seriously harm our results of operations. In addition, the overall integration of two combining companies may result in unanticipated problems, expenses, liabilities, competitive responses, loss of customer relationships, and diversion of management’s attention, and may cause our stock price to decline. The difficulties of integrating an acquisition include, among others:

| · | unanticipated issues in integrating information, communications and other systems; |

| · | unanticipated incompatibility of logistics, marketing and administration methods; |

| · | maintaining employee morale and retaining key employees; |

| · | integrating the business cultures of both companies; |

| · | preserving important strategic and customer relationships; |

| · | consolidating corporate and administrative infrastructures and eliminating duplicative operations; |

| · | the diversion of management’s attention from ongoing business concerns; and |

| · | integrating geographically separate organizations. |

In addition, even if the operations of an acquisition are integrated successfully, we may not realize the full benefits of the acquisition, including the synergies, cost savings, or sales or growth opportunities that we expect. These benefits may not be achieved within the anticipated time frame, or at all.

If our goodwill or intangible assets become impaired, then our profits will be reduced.

If our goodwill or intangible assets become impaired, then our profits will be reduced. For example, during the quarter ended September 30, 2011, a decline in our stock price and market capitalization triggered an interim impairment test, which resulted in a goodwill impairment charge of $825.8 million for the year ended December 30, 2011. Goodwill may be impaired if the estimated fair value of one or more of our reporting units is less than the carrying value of the respective reporting unit. Because we have grown in part through acquisitions, goodwill and other intangible assets represent a substantial portion of our assets. Goodwill and other net intangible assets were $3.3 billion as of December 30, 2011. We perform an analysis on our goodwill balances to test for impairment on an annual basis and whenever events occur that indicate impairment could exist. There are several instances that may cause us to further test our goodwill for impairment between the annual testing periods including the following:

| · | continued deterioration of market and economic conditions that may adversely impact our ability to meet our projected results; |

| · | declines in our stock price caused by continued volatility in the financial markets that may result in increases in our weighted-average cost of capital or other inputs to our goodwill assessment; and |

| · | the occurrence of events that may reduce the fair value of a reporting unit below its carrying amount, such as the sale of a significant portion of one or more of our reporting units. |

We also perform an analysis of our intangible assets to test for impairment whenever events occur that indicate impairment could exist. The following are examples of such events:

| · | significant adverse changes in the intangible asset’s market value, useful life, or in the business climate that could affect its value; |

| · | a current-period operating or cash flow loss or a projection or forecast that demonstrates continuing losses associated with the use of the intangible asset; and |

| · | a current expectation that, more likely than not, the intangible asset will be sold or otherwise disposed of before the end of its previously estimated useful life. |

We may not realize the full amount of revenues reflected in our book of business, particularly in light of the current economic conditions, which could harm our operations and could significantly reduce our expected profits and revenues.

We account for all contract awards that may eventually be recognized as revenues or equity in income of unconsolidated joint ventures as our “book of business,” which includes backlog, option years and IDCs. As of December 30, 2011, our book of business was estimated at approximately $27.0 billion, which included $14.3 billion of backlog. Our book of business estimates may not result in realized profits and revenues in any particular period because clients may delay, modify terms or terminate projects and contracts and may decide not to exercise contract options or issue task orders. For example, during the year ended December 30, 2011, our federal backlog decreased $1.2 billion because of successful early completion of chemical weapons stockpile processing under three federal contracts. This uncertainty is particularly acute in light of current economic conditions as the risk of contracts in backlog being delayed, adjusted in scope or cancelled is more likely to increase during periods of economic volatility. In addition, our government contracts or subcontracts are subject to renegotiation or termination at the convenience of the applicable U.S. federal, state or local governments, as well as national governments of other countries. Accordingly, if we do not realize a substantial amount of our book of business, our operations could be harmed and our expected profits and revenues could be significantly reduced.

As a government contractor, we must comply with various procurement laws and regulations and are subject to regular government audits; failure to comply with any of these laws and regulations could result in sanctions, contract termination, forfeiture of profit, harm to our reputation or loss of our status as an eligible government contractor. Any interruption or termination of our government contractor status could reduce our profits and revenues significantly.

As a government contractor, we enter into many contracts with federal, state and local government clients. For example, revenues from our federal market sector represented 49% of our total revenues for the year ended December 30, 2011. We are affected by and must comply with federal, state, local and foreign laws and regulations relating to the formation, administration and performance of government contracts. For example, we must comply with FAR, the Truth in Negotiations Act, CAS, ARRA, the Services Contract Act, export controls rules and DOD security regulations, as well as many other laws and regulations. In addition, we must also comply with other government regulations related to employment practices, environmental protection, health and safety, tax, accounting and anti-fraud, as well as many others in order to maintain our government contractor status. These laws and regulations affect how we transact business with our clients and in some instances, impose additional costs on our business operations. Even though we take precautions to prevent and deter fraud, misconduct and non-compliance, we face the risk that our employees or outside partners may engage in misconduct, fraud or other improper activities.

Government agencies, such as the U.S. Defense Contract Audit Agency (“DCAA”), routinely audit and investigate government contractors. These government agencies review and audit a government contractor’s performance under its contracts, a government contractor’s direct and indirect cost structure, and a government contractor’s compliance with applicable laws, regulations and standards. For example, during the course of its audits, the DCAA may question our incurred project costs and, if the DCAA believes we have accounted for these costs in a manner inconsistent with the requirements for the FAR or CAS, the DCAA auditor may recommend to our U.S. government corporate administrative contracting officer to disallow such costs. We can provide no assurance that the DCAA or other government audits will not result in material disallowances for incurred costs in the future. In addition, government contracts are subject to a variety of other socioeconomic requirements relating to the formation, administration, performance and accounting for these contracts. We may also be subject to qui tam litigation brought by private individuals on behalf of the government under the Federal Civil False Claims Act, which could include claims for treble damages. Government contract violations could result in the imposition of civil and criminal penalties or sanctions, contract termination, forfeiture of profit, and/or suspension of payment, any of which could make us lose our status as an eligible government contractor. We could also suffer serious harm to our reputation. Any interruption or termination of our government contractor status could reduce our profits and revenues significantly.

Employee, agent or partner misconduct or failure to comply with anti-bribery and other government laws and regulations could harm our reputation, reduce our revenues and profits, and subject us to criminal and civil enforcement actions.

Misconduct, fraud, non-compliance with applicable laws and regulations, or other improper activities by one of our employees, agents or partners could have a significant negative impact on our business and reputation. Such misconduct could include the failure to comply with government procurement regulations, regulations regarding the protection of classified information, regulations prohibiting bribery and other foreign corrupt practices, regulations regarding the pricing of labor and other costs in government contracts, regulations on lobbying or similar activities, regulations pertaining to the internal controls over financial reporting, environmental laws and any other applicable laws or regulations. For example, the United States Foreign Corrupt Practices Act and similar anti-bribery laws in other jurisdictions generally prohibit companies and their intermediaries from making improper payments to foreign officials for the purpose of obtaining or retaining business. In addition, we regularly provide services that may be highly sensitive or that relate to critical national security matters; if a security breach were to occur, our ability to procure future government contracts could be severely limited.

Our policies mandate compliance with these regulations and laws, and we take precautions intended to prevent and detect misconduct. However, since our internal controls are subject to inherent limitations, including human error, it is possible that these controls could be intentionally circumvented or become inadequate because of changed conditions. As a result, we cannot assure that our controls will protect us from reckless or criminal acts committed by our employees and agents. Failure to comply with applicable laws or regulations or acts of misconduct could subject us to fines and penalties, loss of security clearances, and suspension or debarment from contracting, any or all of which could harm our reputation, reduce our revenues and profits and subject us to criminal and civil enforcement actions.

Legal proceedings, investigations and disputes could result in substantial monetary penalties and damages, which could affect us adversely, especially if these penalties and damages exceed or are excluded from existing insurance coverage.

We engage in engineering, construction and technical services that can result in substantial injury or damages that may expose us to legal proceedings, investigations and disputes. For example, in the ordinary course of our business, we may be involved in legal disputes regarding personal injury and wrongful death claims, employee or labor disputes, professional liability claims, and general commercial disputes involving project cost overruns and liquidated damages as well as other claims. See Note 16, “Commitments and Contingencies,” to our “Consolidated Financial Statements and Supplementary Data” included under Item 8 of this report for a discussion of some of our legal proceedings. In addition, in the ordinary course of our business, we frequently make professional judgments and recommendations about environmental and engineering conditions of project sites for our clients. We may be deemed to be responsible for these judgments and recommendations if they are later determined to be inaccurate. Any unfavorable legal ruling against us could result in substantial monetary damages or even criminal violations. We maintain insurance coverage as part of our overall legal and risk management strategy to minimize our potential liabilities. Generally, our insurance program covers workers’ compensation and employer’s liability, general liability, automobile liability, professional errors and omissions liability, property, marine property and liability, and contractor’s pollution liability (in addition to other policies for specific projects). Our insurance program includes deductibles or self-insured retentions for each covered claim. In addition, our insurance policies contain exclusions and sublimits that insurance providers may use to deny us insurance coverage. Excess liability, contractor’s pollution liability, and professional liability insurance policies provide for coverages on a “claims-made” basis, covering only claims actually made and reported during the policy period currently in effect. If we sustain liabilities that exceed our insurance coverage or for which we are not insured, it could have a material adverse impact on our results of operations and financial condition, including our profits and revenues.

Unavailability or cancellation of third-party insurance coverage would increase our overall risk exposure as well as disrupt the management of our business operations.

We maintain insurance coverage from third-party insurers as part of our overall risk management strategy and because some of our contracts require us to maintain specific insurance coverage limits. If any of our third-party insurers fail, suddenly cancel our coverage or otherwise are unable to provide us with adequate insurance coverage then our overall risk exposure and our operational expenses would increase and the management of our business operations would be disrupted. In addition, there can be no assurance that any of our existing insurance coverage will be renewable upon the expiration of the coverage period or that future coverage will be affordable at the required limits.

We may be subject to substantial liabilities under environmental laws and regulations.

A portion of our environmental business involves the planning, design, program management, construction and construction management, and operations and maintenance of pollution control systems and nuclear facilities, hazardous waste or Superfund sites and military bases. In addition, we have contracts with U.S. federal government entities to destroy hazardous materials, including chemical agents and weapons stockpiles, as well as to decontaminate and decommission nuclear facilities. These activities may require us to manage, handle, remove, treat, transport and dispose of toxic or hazardous substances. We must comply with a number of governmental laws that strictly regulate the handling, removal, treatment, transportation and disposal of toxic and hazardous substances. Under CERCLA, as amended, and comparable state laws, we may be required to investigate and remediate regulated hazardous materials. CERCLA and comparable state laws typically impose strict, joint and several liabilities without regard to whether a company knew of or caused the release of hazardous substances. The liability for the entire cost of cleanup could be imposed upon any responsible party. Other principal federal environmental, health and safety laws affecting us include, but are not limited to, the Resource Conservation and Recovery Act, the National Environmental Policy Act, the Clean Air Act, the Clean Air Mercury Rule, the Occupational Safety and Health Act, the Toxic Substances Control Act and the Superfund Amendments and Reauthorization Act. Our business operations may also be subject to similar state and international laws relating to environmental protection. Our past waste management practices and contract mining activities as well as our current and prior ownership of various properties may also expose us to such liabilities. Liabilities related to environmental contamination or human exposure to hazardous substances, or a failure to comply with applicable regulations could result in substantial costs to us, including clean-up costs, fines and civil or criminal sanctions, third-party claims for property damage or personal injury or cessation of remediation activities. Our continuing work in the areas governed by these laws and regulations exposes us to the risk of substantial liability.

Our inability to win or renew government contracts during regulated procurement processes could harm our operations and reduce our profits and revenues.

Revenues from our federal market sector represented 49% of our total revenues for the year ended December 30, 2011. Government contracts are awarded through a regulated procurement process. The federal government has increasingly relied upon multi-year contracts with pre-established terms and conditions, such as IDCs, that generally require those contractors that have previously been awarded the IDC to engage in an additional competitive bidding process before a task order is issued. The increased competition, in turn, may require us to make sustained efforts to reduce costs in order to realize revenues and profits under government contracts. If we are not successful in reducing the amount of costs we incur, our profitability on government contracts will be negatively impacted. In addition, the U.S. government has announced its intention to scale back outsourcing of some types of services in favor of “insourcing” jobs to its employees, which could reduce our revenues. Moreover, even if we are qualified to work on a government contract, we may not be awarded the contract because of existing government policies designed to protect small businesses and under-represented minority contractors. Our inability to win or renew government contracts during regulated procurement processes could harm our operations and reduce our profits and revenues.

Each year, client funding for some of our government contracts may rely on government appropriations or public-supported financing. If adequate public funding is delayed or is not available, then our profits and revenues could decline.