VIA EDGAR AND FEDERAL EXPRESS

May 29, 2012

Terence O’Brien

Branch Chief

Securities and Exchange Commission

Division of Corporation Finance

100 F Street, N.E.

Washington, DC 20549-7010

Re: URS Corporation

Form 10-K for the period ended December 30, 2011

Filed February 27, 2012

File No. 1-7567

Dear Mr. O’Brien:

We are providing to the staff of the SEC’s Division of Corporation Finance (the “Staff”) the responses of URS Corporation (the “Company” or “we”) to the comments in your letter dated May 2, 2012 regarding the Company’s Form 10-K for the year ended December 30, 2011, filed with the SEC on February 27, 2012. For your convenience, we have reproduced your comments in italics below.

Form 10-K for the year ended December 30, 2011

Risk Factors, page 18

| 1. | We note the risk factor on page 32 that legal restrictions and other contractual obligations could restrict or impair your subsidiaries’ ability to pay dividends or make loans or other distributions to the parent. Please tell us how you considered the requirements under Rule 5-04 of Regulation S-X to provide condensed parent only financial statements of the registrant in Schedule I. Explain any restrictions of foreign governments on distributions of dividends and assets and how you considered them in your analysis of your requirements under this rule. |

| Response |

Rule 5-04 of Regulation S-X states that Schedule I shall be filed when the restricted net assets (Rule 4-08(e)(3)) of the consolidated subsidiaries exceed 25 percent of consolidated net assets as of the end of the most recently completed fiscal year. We have determined that our consolidated subsidiaries’ “restricted net assets” are less than 25 percent of our consolidated net assets as prescribed by Rule 5-04 of Regulation S-X. In arriving at that conclusion, we took into account the fact that foreign governments may limit dividend and asset distributions by restricting the repatriation of funds or the conversion of currencies; however, we concluded that no current foreign government restrictions would be reasonably likely to limit distribution to us of a significant amount of net assets.

URS Corporation

600 Montgomery St

San Francisco, CA 94111-2728

Tel: 415.774.2700

Fax: 415.398.1905

Page 1

Management’s Discussion and Analysis, page 40 Subsequent Events, page 67

| 2. | We note the impending acquisition of Flint and the Form 8-K filed February 21, 2012. In the Form 8-K, you mention Flint’s historical financial statements, as well as pro forma combined financial information. However, it does not appear that you intend to file this information pursuant to Rule 3-05 of Regulation S-X. Please clarify this for us in your response and provide to us your significance calculations for Flint under the asset, investment and income tests as prescribed thereunder. |

| Response |

We are still in the process of finalizing our determination as to whether we are required to file historical financial statements, as well as pro forma combined financial information under Rule 3-05 of Regulation S-X. We performed the significant subsidiary tests shown below by using Flint’s balances measured under IFRS as of their fiscal year ended December 31, 2011, and incorporating a worst case scenario of consolidating three joint ventures, as if they were required to be consolidated under US GAAP. We also included an estimated adjustment to remove certain capital leases from the balance sheet in order to convert them to operating lease treatment, as would be required under US GAAP. All three tests produce results that are below the 20% significance level; thus, we currently do not believe that historical financial statements or pro forma combined financial information will be required.

If we determine that we are required to file the historical financial statements and pro forma combined financial statements, then we will do so on a timely basis. However, we are not aware of any additional IFRS-to-US GAAP differences that are sufficiently significant to cause us to believe that, after conversion, the asset test or the income test would exceed the 20% level.

| Investment Test | URS As of December 30, 2011 (Per 10-K) | Flint As of May 14, 2012 (Purchase Date) | ||||||||||||||

| (In thousands, except percentage) | (USD) | (CAD) | (USD (1)) | Level of Significance | ||||||||||||

Total assets | $ | 6,862,600 | ||||||||||||||

Purchase consideration | $ | 1,240,357 | $ | 1,239,863 | 18.1 | % | ||||||||||

| Asset Test | URS As of December 30, 2011 (Per 10-K) | Flint As of December 31, 2011 (Year Ended) | ||||||||||||||

| (In thousands, except percentage) | (USD) | (CAD) | (USD (2)) | Level of Significance | ||||||||||||

| Total assets per Flint's 2011 annual report | $ | 1,133,051 | ||||||||||||||

| Adjustments: | ||||||||||||||||

Net assets from joint ventures that may require to be consolidated under US GAAP | 132,356 | |||||||||||||||

| Property, plant and equipment - de-capitalization of capital lease assets | (30,200 | ) | ||||||||||||||

Total Assets | $ | 6,862,600 | $ | 1,235,207 | $ | 1,209,091 | 17.6 | % | ||||||||

| (1) | Translated using the spot rate of 0.99960 as of May 14, 2012, the purchase date. |

| (2) | Translated using the spot rate of 0.97886 as of December 31, 2011. |

Page 2

| Income Test | URS Year Ended December 30, 2011 | Flint Year Ended December 31, 2011 | ||||||||||||||

| (In thousands, except percentage) | (USD) | (CAD) | (USD (1)) | Level of Significance | ||||||||||||

Income for use in significant subsidiary test(2) | $ | 374,032 | $ | 31,700 | $ | 32,073 | 8.6 | % | ||||||||

| (1) | Translated using the average exchange rate of 1.01176 for the year ended December 31, 2011. |

| (2) | We used income before income taxes in the calculations of the significant subsidiary test. However, URS experienced a net loss for the year ended December 30, 2011. In determining the amount of income to use in the calculations for the significant subsidiary income test, we used the greater of the five-year average income before income taxes ($290.2 million), as shown in the table below, and the absolute value of our net loss before income tax ($374.0 million) for the year ended December 30, 2011. |

Calculation of the Denominator for the Income Test

| Years Ended | ||||||||||||||||||||||||

| (In thousands) | 2007 | 2008 | 2009 | 2010 | 2011(a) | 5-Yr Average | ||||||||||||||||||

| Income attributable to URS before income taxes | $ | 225,575 | $ | 377,950 | $ | 431,977 | $ | 415,497 | $ | - | $ | 290,200 | ||||||||||||

(a) URS experienced a net loss of $374.0 million for the year ended December 30, 2011.

Page 3

Liquidity, page 66

| 3. | Please tell us and revise future filings to disclose why costs and accrued earnings in excess of billings on contracts increased 14% at December 31, 2011, compared to a decrease in revenues of 3% during the fourth quarter of 2011. The $160 million increase in unbilled receivables had a material adverse impact on 2011 operating cash flows. Specifically address any disagreements with customers that may impact your ability to bill these amounts or any other known contracts/factors that materially impact the recoverability of this asset. Refer to Item 303(a)(1) of Regulation S-K. |

| Response |

Because of the nature of our business, our project accounts, which include accounts receivable, costs and accrued earnings in excess of billings on contracts (unbilled receivables) and billings in excess of costs and accrued earnings on contracts, vary with the nature and terms of the contracts being executed at any one time. At December 30, 2011, our unbilled receivables were $160.0 million higher than they were at December 31, 2010. The increase resulted primarily from the following:

| (In millions) | ||||

| Accruals of performance-based incentive awards to be billed upon client acknowledgement | $ | 109.6 | ||

| Unbilled amounts related to a company acquired during 2011 with no comparable balance in 2010 | 32.9 | |||

| Increase in year-over-year activity on major projects | 37.8 | |||

| Project settlement accrual; agreed-upon billing date not reached | 7.4 | |||

| Project cost savings incentive earned that cannot be billed until project completion | 5.5 | |||

| Reductions on other unbilled receivables and other normal flows within our billing cycles | (33.2 | ) | ||

| $ | 160.0 | |||

It should be noted that the accruals of performance-based incentive awards and the project cost savings incentive awards had no negative effect on cash flows because they represent profits rather than recovery of previously incurred costs. So, although they imply a use of cash in the calculation of operating cash flows, in fact, they did not have a material adverse impact on our cash flows because they did not actually consume cash.

Although we do occasionally find ourselves in billing disagreements with clients or receive requests to re-submit billings to clarify or re-format to better meet client requirements, such requests are infrequent and the amounts are generally not material.

In future filings, in periods when significant fluctuations occur in any of our project accounts, as described above, we will disclose the cause of the significant fluctuations.

Page 4

Operating Activities, page 68

| 4. | You state that during the first quarter of 2012, you expect to make estimated payments of $140 million to pension, post-retirement, defined contribution and multiemployer pension plans and incentive payments. On page 131, you disclose you expect to make cash contributions, including estimated employer-directed benefit payments, during 2012, of approximately $32.1million to the domestic and foreign defined benefit plans. Lastly, we note from the table of contractual obligations on page 70 that $75.8 million is due within one year for pension and other retirement plans funding requirements. Please describe the material components of these three amounts, and reconcile the totals accordingly. For the amounts within the table of contractual obligations, please clarify for us whether these represent the minimum required payments. If not, disclose the minimum required payments for the next five years. To the extent that you have made contributions in excess of the minimum requirement, please explain to investors why and how such payments are expected to impact future cash flows. |

| Response |

The table below shows the components of the estimated $139.5 million that we expected to pay in Q1 2012 with respect to pension, post-retirement, defined contribution plans and incentive payments and the $75.8 million included in the table of contractual obligations that is due within one year, including the reconciliation as applicable.

| (In millions) | Details of Expected Cash Outflow for Q1, 2012 | Contractual Obligations and Commitment Table Due in Less Than 1 Year | ||||||||

| As of December 30, 2011 | ||||||||||

| Defined benefits plans, including domestic and foreign plans* | $ | 4.4 | $ | 32.1 | ||||||

| Post-retirement benefit plans* | 0.8 | 3.5 | ||||||||

| CEO SERP* | — | 14.7 | (1 | ) | ||||||

| 401(K) plan | 63.1 | — | (2 | ) | ||||||

| Other contributory plans | 8.6 | 25.5 | ||||||||

| Multi-employer plans | 10.2 | — | (3 | ) | ||||||

| Incentive payments | 52.4 | — | (4 | ) | ||||||

| Total | $ | 139.5 | $ | 75.8 | ||||||

| * | The future minimum contributions for our defined benefit plans and post-retirement benefit plans, included in the contractual obligations table, are based on actuarially-determined estimates and projected future benefit payments. |

_______________

| (1) | Represents the fully vested amount of accumulated benefits under our CEO SERP as of December 30, 2011. We are obligated to deposit into a “rabbi trust” the lump sum value of our CEO's retirement benefit within 15 days of the earlier to occur of (1) our CEO’s request for a lump sum payment and (2) the termination of our CEO’s employment for any reason, including death. As a result, we included $14.7 million in the contractual obligations table under the "Less Than 1 year" column. However, this amount was not included in the $139.5 million we expected to pay in Q1 2012 because we did not expect the CEO to request a payment or terminate his employment during Q1 2012. |

| (2) | Our defined contribution plans (401(k) plans) include discretionary and non-discretionary provisions. For future filings, we will include our estimated 401(k) contributions in the contractual obligations table with a footnote explaining any conditions and limitations. |

| (3) | We contribute to many multiemployer pension plans under various collective bargaining arrangements that we do not control. For future filings, we will include our estimated contributions to our multiemployer pension plans in the contractual obligations table to the extent that we can develop reasonable estimates. |

Page 5

| (4) | While a portion of our incentive payments are discretionary, most of our incentive payments are formulaic and payable upon achievement of pre-defined measurement goals established by the Compensation Committee of our Board of Directors. Since we expected to pay $52.4 million in Q1 2012, we included this amount in the total cash flow to be paid in Q1 2012. For future filings, we will include an estimate of discretionary and non-discretionary incentive payments in our contractual obligations table to provide a better picture of our projected cash outflow arising from this obligation. |

Based on our annual actuarial analysis, we believe that the estimated contribution related to the retirement plans included in our contractual obligations table are the minimum required payments for the next five years and beyond.

Critical Accounting Policies and Estimates, page 76

| 5. | You state on page 116 that during 2011, you aggregated two reporting units within the Federal Services operating segment. Please explain to us your compliance with ASC 350-20-35-35 related to such aggregation. In this regard, please provide us with an analysis that includes historical revenues, gross profits, gross profit margins, operating profits, and operating profit margins, along with any other information you believe would be useful for each of the previously-separated reporting units to help us understand how these operations are economically similar. |

| Response |

In response to the Staff’s comment, we have attached as Appendix A to this letter, a whitepaper, “Federal Services Reporting Unit Determination,” which was prepared during the third quarter of 2011. It outlines our analysis of the various aggregation criteria referenced in ASC 350-20-35-35 and ASC 280-10.

Page 6

| 6. | We note the data provided for your unconsolidated joint ventures shown on page 111. Please provide to us your significance tests pursuant to Rule 3-09 of Regulation S-X for the unconsolidated joint venture(s) that comprise the largest portion of your equity income of $132.2 million for 2011. |

| Response |

With respect to our investment in the largest unconsolidated joint venture, the result of the investment significance test was less than 1% of our total assets as of December 30, 2011.

With respect to the joint venture that comprises the largest portion of our equity income of $132.2 million for our fiscal year ended December 30, 2011, the equity income significance test result was below the 20% level as shown below:

| Equity Income Significance Test | ||||

| (In thousands, except percentage) | Year Ended December 30, 2011 | |||

| Equity in income of our largest unconsolidated joint venture before income tax | $ | 40,600 | ||

Income for use in significant subsidiary test(1) | $ | 414,632 | ||

Level of significance | 9.8 | % | ||

| (1) | URS experienced a net loss for the year ended December 30, 2011. As a result, we calculated the denominator for the equity income significance test as follows: |

| Calculation of the Denominator for the Equity Income Significance Test | ||||

| (In thousands) | Year Ended December 30, 2011 | |||

| Net loss attributable to URS before income taxes | $ | (374,032 | ) | |

Less: equity in income of our largest unconsolidated joint venture before income tax(a) | 40,600 | |||

| Adjusted net loss attributable to URS before income taxes | $ | (414,632 | ) | |

| Absolute value of URS’ FY 2011 net loss before income taxes for use in the significant subsidiary test | $ | 414,632 | ||

| The five-year average income attributable to URS before income taxes (as previously shown on page 3 of this letter) | $ | 290,200 | ||

| Denominator: | ||||

| Denominator used in the significant subsidiary test is the absolute value of URS’ FY 2011 net loss before income taxes as it is greater than the five-year average income before income taxes | $ | 414,632 | ||

| (a) | Regulation S-X 1-02(w) requires that, in situations where there is a loss incurred by the parent and its consolidated subsidiaries, the equity income of the tested subsidiary be excluded from the consolidated income of the parent and its subsidiaries for purposes of the computation. |

Page 7

Note 16. Commitments and Contingencies, page 145

| 7. | We note your discussion of the USAID Egyptian Projects and New Orleans Levee Failure Class Action Litigation. For both of these matters, you also state that the potential range of loss cannot be determined at this time. Please supplementally: (1) explain to us the procedures you undertake on a quarterly basis to attempt to develop a range of reasonably possible loss for disclosure and (2) for each material matter, what specific factors are causing the inability to estimate and when you expect those factors to be alleviated. We recognize that there are a number of uncertainties and potential outcomes associated with loss contingencies. Nonetheless, an effort should be made to develop estimates for purposes of disclosure, including determining which of the potential outcomes are reasonably possible and what the reasonably possible range of losses would be for those reasonably possible outcomes. You may provide your disclosures on an aggregated basis. Please include your proposed disclosures in your response. |

| Response |

On a quarterly basis, we assess and monitor our legal contingencies, including determining whether we can estimate a range of potential loss in accordance with FASB Accounting Standards Codification Topic 450, Contingencies (“ASC 450”) (formerly FASB Statement No. 5, Accounting for Contingencies). This includes quarterly:

| · | Disclosure Committee meetings with senior management to review and monitor material legal contingency matters and litigation developments; |

| · | accounting and operational meetings to review and monitor material legal contingency matters and litigation developments; |

| · | legal department meetings to review and monitor material legal contingency matters and litigation developments; |

| · | meetings with our general counsel and Chief Accounting Officer before the filing of our quarterly report to review and monitor material legal contingency matters and litigation developments; and |

| · | discussions with the Audit Committee, as appropriate. |

At each stage in the process, we consider the accounting and disclosure implications of any legal developments and whether a loss is probable, reasonably possible or remote and whether we can reasonably estimate a range of potential loss in accordance with ASC 450. We consider, among others, the following factors in making our ASC 450 assessments:

| · | nature of the litigation, claim or assessment; |

| · | jurisdiction of the litigation; |

| · | opposing and other counsel involved in the litigation; |

| · | number of parties involved; |

| · | counter- and/or cross-claims included in the litigation; |

| · | status of the case, including its procedural posture and how quickly it is progressing; |

| · | the opinions of legal counsel and other advisers, including, but not limited to, consultants and experts; |

| · | the experience of the company and others similar companies in similar cases; |

| · | precedent in the jurisdiction in similar cases; |

| · | probative pending decisions that may impact the assessment of the case; |

| · | consideration of any alternative dispute resolution efforts made to date; and |

| · | any decision by management as to how we will respond to the lawsuit. |

Page 8

The ASC 450 assessment is then re-evaluated whenever a significant development occurs and also at the end of each quarter as we revise and update the disclosure in our periodic reports. This process is designed to ensure that we receive and review the information necessary to make appropriate judgments each quarter regarding the accounting and disclosure of our litigation contingencies in accordance with ASC 450. Following this process, a number of specific factors have prevented us from reasonably estimating ranges of potential loss for the USAID Egyptian Project and New Orleans Levee Failure Class Action Litigation matters. These include, but are not limited to the following:

USAID Project

| · | This matter has been stayed virtually since it was filed in 2004 and no substantive discovery or substantive motions have been filed to permit us to reasonably estimate a potential loss. This matter is further complicated by its duration as well as the length of time since Washington Group International (“WGI”) filed for bankruptcy May 14, 2001, well before URS acquired WGI in 2007. Since 2004, there has been substantial litigation over whether the WGI bankruptcy proceedings extinguished certain claims. WGI asserted in the lawsuit that WGI's bankruptcy court filing barred the federal government's claims because the federal government failed to preserve those claims in bankruptcy proceedings. Because of the stay, there has been no substantive discovery conducted or substantive motions filed in that matter that would have allowed for an estimate of even a potential range of liability. It was not until 2012 that the Bankruptcy Court decided that, even though certain claims in this matter were barred (i.e., pre-effective date source and origin of equipment contractual claims), other federal government claims were not automatically discharged with WGI's bankruptcy. |

| · | This matter is complex and involves multiple projects that span over one decade of time (1993-2004). Project documentation is substantial. Because of the previous stay of the case, WGI has not completed its review and analysis of the voluminous project documents and applicable substantive and procedural law. Consequently, URS remains unable to reasonably estimate loss or even a range of potential loss in accordance with ASC 450. |

New Orleans Levee Failure Class Action Litigation

| · | In this matter, the plaintiffs asserted claims of $200B relating primarily to damages caused by the failure of a levee in New Orleans, Louisiana that our affiliate, a defendant in the case, did not design, construct, repair or maintain. At the current stage of the litigation, there is still uncertainty concerning legal theories that might attribute negligence to our affiliate and their resolution by courts or regulators, and uncertainty about the plaintiffs’ claims that might survive certain key motions of our affiliate. In addition, there is an unusual degree of unpredictability regarding how the high profile nature of the case will affect the assessment of the case by the jury or other decision-makers. |

| · | This matter is being managed by the federal court as mass tort/putative class litigation and, as a result, there is, at this stage of the litigation, no reasonable basis for knowing or reasonably estimating how many individual plaintiffs are actually asserting claims against our affiliate, the specific bases for their claims against our affiliate or the nature and amount of damages each individual plaintiff claims or to which each plaintiff may reasonably be entitled. The damages for each plaintiff are unique. |

We believe the unique factual circumstances of the USAID Egyptian Project and New Orleans Levee Failure Class Action Litigation matters as disclosed in our Form 10-K and as updated in our most recent Form 10-Q, present a number of specific factors that prevent us from reasonably estimating a range of potential loss in accordance with ASC 450. Should any additional information become available that enables us to reasonably estimate a range of potential loss, we confirm that we will update our disclosures relating to loss contingencies in future filings.

Page 9

We would propose to revise the disclosure in our periodic reports to further reflect this point as highlighted below:

“USAID Egyptian Projects: In March 2003, Washington Group International (“WGI”), a wholly owned subsidiary, was notified by the Department of Justice that the federal government was considering civil litigation against WGI for potential violations of the U.S. Agency for International Development (“USAID”) source, origin, and nationality regulations in connection with five of WGI’s USAID-financed host-country projects located in Egypt beginning in the early 1990s. In November 2004, the federal government filed an action in the United States District Court for the District of Idaho against WGI, Contrack International, Inc., and MISR Sons Development S.A.E., an Egyptian construction company, asserting violations under the Federal False Claims Act, the Federal Foreign Assistance Act of 1961, as well as common law theories of payment by mistake and unjust enrichment. The federal government seeks damages and civil penalties for violations of the statutes as well as a refund of all amounts paid under the specified contracts of approximately $373.0 million. WGI has denied any liability in the action and contested the federal government’s damage allegations and its entitlement to any recovery. All USAID projects under the contracts have been completed and are fully operational.

In March 2005, WGI filed motions in the Bankruptcy Court in Nevada and in the Idaho District Court to dismiss the federal government’s claim for failure to give appropriate notice or otherwise preserve those claims. In August 2005, the Bankruptcy Court ruled that all federal government claims were barred. The federal government appealed the Bankruptcy Court's order to the United States District Court for the District of Nevada. In March 2006, the Idaho District Court stayed that action during the pendency of the federal government's appeal of the Bankruptcy Court's ruling. In December 2006, the Nevada District Court reversed the Bankruptcy Court’s order and remanded the matter back to the Bankruptcy Court for further proceedings. WGI renewed its motion in Bankruptcy Court that all of the federal government’s claims are barred for failure to give appropriate notice or otherwise preserve those claims. In November 2008, the Bankruptcy Court ruled that the federal government’s common law claims of unjust enrichment and payment by mistake are barred, and may not be further pursued. On April 24, 2012, the Bankruptcy Court ruled that the federal government’s claims under the False Claims and Foreign Assistance Acts are not barred by the WGI bankruptcy.

WGI intends to continue to defend this matter vigorously; however, we cannot provide assurance that we will be successful in these efforts. The potential range of loss and the resolution of these matters cannot be determined at this time primarily due to the very limited factual record that exists in light of our limited ability to evaluate discovery that has been conducted so far at this early stage of the litigation; the fact that the matter involves unique and complex bankruptcy, international, and federal regulatory legal issues; the uncertainty concerning legal theories and their potential resolution by the courts; and the duration of this matter, as well as a number of additional factors.”

“New Orleans Levee Failure Class Action Litigation: From July 1999 through May 2005, Washington Group International, Inc., an Ohio company (“WGI Ohio”), a wholly owned subsidiary acquired by us on November 15, 2007, performed demolition, site preparation, and environmental remediation services for the U.S. Army Corps of Engineers on the east bank of the Inner Harbor Navigation Canal (the “Industrial Canal”) in New Orleans, Louisiana. On August 29, 2005, Hurricane Katrina devastated New Orleans. The storm surge created by the hurricane overtopped the Industrial Canal levee and floodwall, flooding the Lower Ninth Ward and other parts of the city.

Page 10

Since September 2005, 59 personal injury, property damage and class action lawsuits have been filed in Louisiana State and federal court naming WGI Ohio as a defendant. Other defendants include the U.S. Army Corps of Engineers, the Board for the Orleans Levee District, and its insurer, St. Paul Fire and Marine Insurance Company. Over 1,450 hurricane-related cases, including the WGI Ohio cases, have been consolidated in the United States District Court for the Eastern District of Louisiana (“District Court”). The plaintiffs claim that defendants were negligent in their design, construction and/or maintenance of the New Orleans levees. The plaintiffs are all residents and property owners who claim to have incurred damages arising out of the breach and failure of the hurricane protection levees and floodwalls in the wake of Hurricane Katrina. The allegation against us is that the work we performed adjacent to the Industrial Canal damaged the levee and floodwall and caused and/or contributed to breaches and flooding. The plaintiffs allege damages of $200.0 billion and demand attorneys’ fees and costs. WGI Ohio did not design, construct, repair or maintain any of the levees or the floodwalls that failed during or after Hurricane Katrina. WGI Ohio performed the work adjacent to the Industrial Canal as a contractor for the federal government and has pursued dismissal from the lawsuits on a motion for summary judgment on the basis that government contractors are immune from liability.

On December 15, 2008, the District Court granted WGI Ohio’s motion for summary judgment to dismiss the lawsuit on the basis that we performed the work adjacent to the Industrial Canal as a contractor for the federal government and are therefore immune from liability, which was appealed by a number of the plaintiffs on April 27, 2009 to the United States Fifth Circuit Court of Appeals (“Court of Appeals”). On September 14, 2010, the Court of Appeals reversed the District Court’s summary judgment decision and WGI Ohio’s dismissal, and remanded the case back to the District Court for further litigation. On August 1, 2011, the District Court held that the defense of government contractor immunity is not available to WGI Ohio at trial, but would be an issue for appeal.

WGI Ohio intends to continue to defend these matters vigorously; however, we cannot provide assurance that we will be successful in these efforts. The potential range of loss and the resolution of these matters cannot be determined at this time primarily due to the unknown number of individual plaintiffs who are actually asserting claims against WGI Ohio; the uncertainty regarding the nature and amount of each individual plaintiff’s damage claims; uncertainty concerning legal theories and factual bases that plaintiffs may present and their resolution by courts or regulators; and uncertainty about the plaintiffs’ claims, if any, that might survive certain key motions of our affiliate, as well as a number of additional factors.

Our evaluation of the impact of pending actions could change in the future and unfavorable outcomes and/or defense costs, depending upon the amount and timing, could have a material adverse effect on our results of operations or cash flows for future periods.”

| 8. | We note your disclosure on page 148 and elsewhere that your insurance program covers general liability, among other items. Please confirm to us you have no accrual recorded for general liability in accordance with ASC 450-20-25-8. |

| Response |

We hereby confirm that we have no general or unspecified general liabilities accrued that do not meet the conditions for accrual under ASC 450-20-8. Our general liability insurance reserve is based on actuarial modeling of the estimate of ultimate loss using current open and historical claims data. The analysis complies with applicable Actuarial Standards of Practice and Statements of Principles.

Page 11

Closing

| In accordance with your letter, the Company acknowledges that: |

| · | The Company is responsible for the adequacy and accuracy of the disclosure in its filings; |

| · | Staff comments or changes to disclosure in response to Staff comments do not foreclose the Commission from taking any action with respect to the Company's filings; and |

| · | The Company may not assert staff comments as a defense in any proceeding initiated by the Commission or any person under the Federal securities laws of the United States. |

If you have any additional questions, please feel free to call me at (415) 774-2752.

Very truly yours,

Reed N. Brimhall

Vice President and

Chief Accounting Officer

URS Corporation

cc:

Martin M. Koffel

Chairman and Chief Executive Officer

URS Corporation

600 Montgomery Street, 26th Floor

San Francisco, CA 94111-2728

Page 12

| APPENDIX A |

Memorandum

Date: | September 30, 2011 |

To: | Reed Brimhall, VP, Controller & Chief Accounting Officer – URS Corporate |

From: | Bill Neeb, Jake Kennedy & Dave Tingley – URS Federal Services |

Subject: | Federal Services Reporting Unit Determination |

Purpose

This white paper assesses recent changes within the Federal Services business and proposes aggregation of the Federal Services components into a single reporting unit.

Background

Apptis Acquisition and Integration

On June 02, 2011, we completed our acquisition of Apptis Holdings, Inc., a leading provider of high-end information technology services to the federal government. This acquisition enables URS to compete in one of the fastest growing sectors of the federal market and enhances our ability to provide the full life cycle of project services to our customers. URS and Apptis share common customers that include the U.S. Departments of Defense (“DOD”) and Homeland Security. Apptis also holds key relationships with the Departments of State, Transportation, and Justice.

Subsequent to our acquisition of Apptis, we merged Apptis with components of the Defense Maintenance & Logistics Group (“DML”) and Systems & Technology Group (“SET”), to form the “Information Solution Group” (“ISG”). The combination of the Rapid Acquisition Support Services organization (previously part of the DML group), and the Electromagnetic Spectrum, C4I and Cyber resources operations (previously part of the SET Group), complements ISG’s services and customer base. This realignment exemplifies the increasingly interdependent and interchangeable relationships among FS groups and underscores the economic similarities amongst the various business lines. To stay competitive, we need to provide a broad portfolio of services to meet the evolving demands of the Federal marketplace. As such, the integration of Apptis with our existing FS business leverages Apptis’ additional operational capabilities and customer relationships. It also affords economic benefits and generates value for all FS groups.

A-1

Global Security Group Integration

In January 2011, FS transitioned the majority of the Global Security Group (“GSG”) support functions from the Energy & Construction business support systems (“EC”) to FS support systems. GSG is a component of the FS operating segment, and primarily provides Operations and Maintenance (“O&M”) services associated with the decommissioning and closure of chemical agent stockpiles, as well as various services to the U.S. intelligence community. The majority of current GSG contracts were originally awarded to the EC Defense business, formerly a component of Washington Group International, Inc. (“WGI”), an entity we acquired in 2007. These awards were contracted under a legacy WGI US legal entity. Subsequent to the acquisition of WGI, the EC Defense business and related goodwill was transferred to FS. The EC Defense business complemented the existing FS O&M business and federal customer base. Although FS has maintained operational responsibility for GSG since its transfer from EC, the sharing of GSG administrative resources with other FS groups was limited prior to 2011. EC continued to administer the majority of the finance, tax, and human resource functions for GSG, while the remainder of FS operations relied upon the centralized shared support functions provided by the FS Germantown Service Center (“GSC”). As a result of integrating many GSG support functions with the GSC, the majority of GSG is now sharing resources with other FS groups.

Resource Sharing and Realignment

2011 marked a “watershed” year for Federal Services; the changing federal service marketplace necessitated significant managerial and operational changes in response to the evolving environment. Shifting federal procurement methods, contract funding and award delays, acquisition integration efforts, and a new combined indirect cost strategy have all contributed to the redeployment of FS human and financial resources. In addition to the sharing and realignment of resources discussed above, other instances include: promotion of a business unit head within SET to the General Manager (“GM”) role for ISG; the SET group GM now manages both the SET group and the overall FS business development function.

FS is also transitioning its indirect rate strategy to a lower indirect cost model by combining the nine existing “group specific” general and administrative (“G&A”) rate segments into fewer segments (between two and five). As a result, components of each FS group will now share blended G&A cost rates, based on the combined indirect cost and base pools associated with the member business components. Management of the combined G&A rate segments will no longer be solely attributable to one group and its contract performance, as the performance of all member components will influence the shared rate. This initiative illustrates the interdependency of operational and indirect support resources between the groups, and the combination of economically similar components, in order to reduce indirect costs across the FS segment.

The FS business strategy driving resource sharing and realignment can be summed up in a recent communication to the business, by Randy Wotring, FS President, “We will continue to evolve our organization as we respond to new opportunities and changing market conditions and as we leverage the breadth and depth of the capabilities we bring as URS”.

As mentioned above, the events in 2011 drove significant changes to the FS business and its reporting units. The sections that follow detail the accounting guidance for identifying and evaluating reporting units for goodwill impairment analysis purposes, and address the impact of the recent changes on the FS reporting unit determination.

A-2

Identifying a Reporting Unit

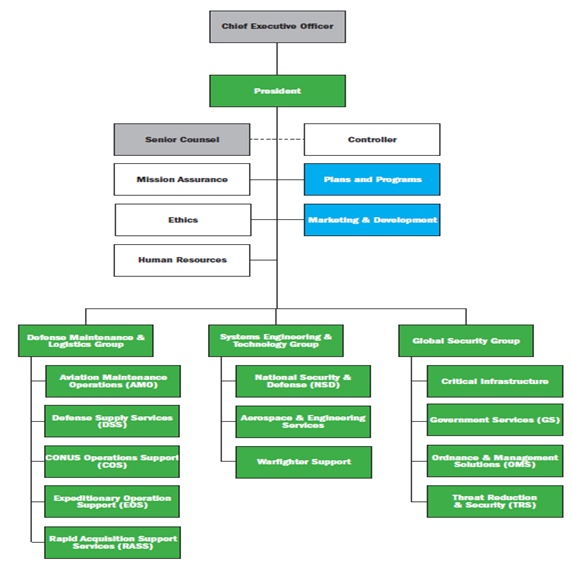

The FS business, an operating segment of URS, currently contains four components:

| o | Defense Maintenance & Logistics Group (DML) |

| o | Systems Engineering & Technology Group (SET) |

| o | Global Security Group (GSG) |

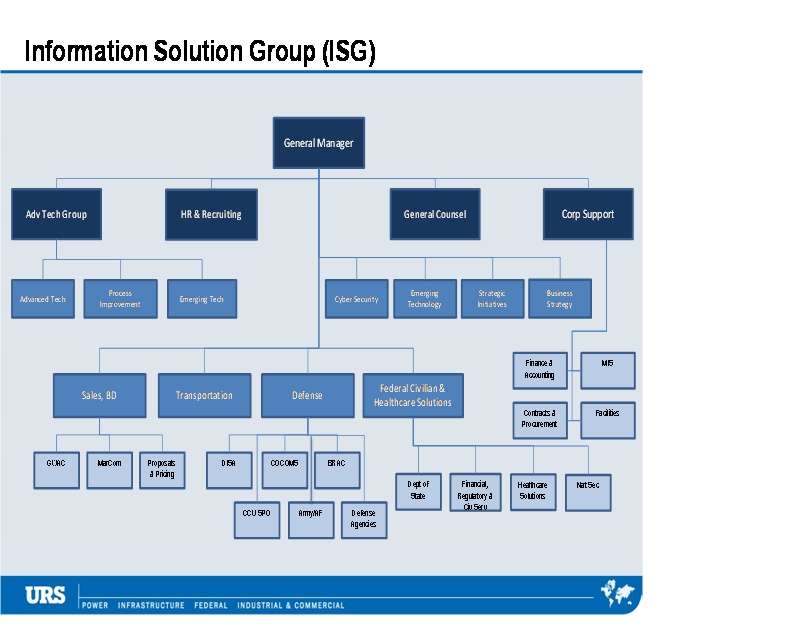

| o | Information Solutions Group (ISG) |

As previously noted, Apptis was combined with other portions of the FS business to form the ISG Group. The organizational charts for the FS components are provided in Appendix I.

Accounting Standards Codification (“ASC”) 350-20-55 identifies factors or characteristics which should be considered in determining whether a component of an operating segment is a reporting unit:

| v | Component constitutes a business and contains all of the inputs and processes necessary for it to continue to conduct normal operations after the transferred set is separated from the transferor. |

| v | How an entity manages its operations and how an acquired entity is integrated with the acquiring entity are key to determining the reporting units of the entity |

| v | Availability of discrete financial information at the component level |

| v | Reviewed by Segment Management. According to ASC 280, a segment manager is directly accountable to and maintains regular contact with the chief operating decision maker (“CODM”) to discuss operating activities, financial results, forecasts, or plans for the segment. |

The components of the FS business meet the definition of a reporting unit based on the factors noted above:

| o | Each component conducts business functions, earns revenues and incurs expenses from services provided. |

| o | Discrete operating performance information is available for each component and is reviewed by segment management. |

| Ø | Randy Wotring, FS President, monitors and presents segment operating information including financial results, forecasts, and plans. Randy reports to the CODM, URS Chairman and CEO Martin Koffel. |

As such, unless suitable for aggregation, each component may be a reporting unit for goodwill impairment analysis purposes. To determine whether aggregation of two or more reporting units is justified, an analysis of each component’s characteristics is required.

Aggregation Criteria

Two or more components of an operating segment shall be aggregated into a single reporting unit if they possess economically similar characteristics (ASC 350-20-35-35). Based on primarily qualitative factors from ASC 280-10, the implementation guidance found in ASC 350-20-55-7 outlines key aspects to consider whether two components are economically similar and should be aggregated:

| v | Similar financial performance |

| v | The nature of the products and services |

| v | The nature of the production processes |

| v | The type or class of customer for their products and services |

A-3

| v | The methods used to distribute their products and services |

| v | If applicable, the nature of the regulatory environment |

Additional factors to be considered include:

| v | The manner in which an entity operates its business and the nature of those operations |

| v | Whether goodwill is recoverable from two or more component businesses working in concert |

| v | The extent to which the component businesses share assets and other resources, as might be evidenced by extensive transfer pricing mechanisms |

| v | Whether the components support and benefit from common research and development projects [ASC 350-20-55] |

Aggregation Determination

To determine whether FS components have similar economic characteristics, we first assessed the following aggregation criteria:

| v | The nature of the products and services |

| v | The nature of the production processes |

| v | The type or class of customer for their products and services |

| v | The methods used to distribute their products and services |

| v | If applicable, the nature of the regulatory environment |

As part of our analysis, we examined each components primary market(s) served and service offerings. As disclosed in the 2010 URS 10-K, the FS business operates predominantly within the Federal market sector. FS components provide a range of project life-cycle services which include the following:

| Services Provided by Federal Services Components | ||||

Services | DML | SET | GSG | ISG |

| Program Management | √ | √ | √ | √ |

| Planning, Design, and Engineering | √ | √ | √ | √ |

| Systems Engineering and Technical Assistance | √ | √ | √ | √ |

| Construction and Construction Management | √ | √ | ||

| Operations and Maintenance | √ | √ | √ | √ |

As portrayed in the matrices above, FS components provide a portfolio of similar services. These services are provided through similar methods and are focused on the federal market. Component financial results largely rely on successful long-standing customer relationships with the US Department of Defense and many of its agencies. The same customer or government agency may also, at times, be served by different components yet receive similar services.

A-4

All of the components distribute their services in a similar fashion, ie. if expertise for services is available within a component, then the work would be performed by that component; otherwise, a team would be assembled from other components to perform the agreed upon work. As an example, one of the larger contracts awarded to FS in recent history, CR2, required the assembly of a team comprised of both the DML and SET components, which capitalized on the similar expertise of each component, working in concert to complete the scope of work and contribute to the financial performance of the FS business, as a whole.

FS components are subject to uniform regulatory environments. As a US government contractor, the FS business is subject to regulation by the Defense Contract Management Agency, an agency within the US Department of Defense. As such, we must comply with Federal Acquisition Regulation, Cost Accounting Standards, as well as US GAAP.

| v | Similar financial performance |

Our analysis of the FS component’s actual and estimated profit margins over a period of four years indicates they are economic similar. The table below provides an overview of the profitability of each component using earnings before income tax (“EBIT”) as a financial measure:

| EBIT ANALYSIS BY FS COMPONENT | ||||||

| DML | SET | GSG | ISG | Mean | Standard Deviation | |

| 2009 | 4.4% | 6.2% | 6.4% | 8.6% | 6.4% | 1.5% |

| 2010 | 6.6% | 6.2% | 7.8% | 8.5% | 7.3% | 0.9% |

| 2011 est. | 3.4% | 6.5% | 9.9% | 3.7% | 5.9% | 2.6% |

| 2012 est. | 4.6% | 5.9% | 11.3% | 6.4% | 7.1% | 2.5% |

| Group Average | 4.8% | 6.2% | 8.9% | 6.8% | 6.7% | 1.5% |

To summarize the margin analysis provided above, the average margin for all components is 6.7% and the standard deviation of these margins for the four year period is 1.5%. Based on this analysis, the margins all fall within a reasonably comparable range and the fairly low standard deviation indicates the dispersion of the component margins is minimal. This data indicates the financial performance of the FS components to be economically similar.

Although the profitability of the components may vary from year to year, the factors that contribute to this variability may be similarly experienced by all components, as they all share the same customer base. The factors contributing to the variability of financial performance include the timing of when an award is issued, the size of projects performed, and the preferred federal procurement vehicle and related fee structure chosen by the government at the time the work was contracted. The economic conditions facing the government at the time of award, administrative agenda, and type of work being performed all contribute to the variability of financial performance, but are not isolated to any one component. While there can be differences from year to year in the performance of a particular component, over time if the components perform similar projects with similar resources, and the federal procurement vehicles are similar, the profitability of the components is expected to be reasonably comparable over the long term (as evidenced in the table above).

Our determination also considered the following aggregation criteria described in ASC 350-20-55:

| v | The manner in which an entity operates its business and the nature of those operations |

| v | Whether goodwill is recoverable from two or more component businesses working in concert |

| v | The extent to which the component businesses share assets and other resources, as might be evidenced by extensive transfer pricing mechanisms |

A-5

FS intends to leverage Apptis’ customer relationships with the legacy components of the FS business in order to access previously unavailable contract vehicles and customers. The additional capabilities provided by Apptis provide a competitive advantage over our industry competition, and allow multiple components to combine efforts in order to execute large bundled service contracts. As noted previously, the majority of services provided by FS components are similar in nature and are not typically limited to a specific component to perform certain services (although in some cases, particular expertise for a project may be in one component, but managed by another). In addition, while services to some customers or agencies are limited to one component, (e.g., GSG serves the Chemical Threat Reduction Agency) they are ultimately for the same shared customer with other components, the US Department of Defense, and provided through similar methods.

In addition to the sharing of customers between components, the sharing of assets and other resources amongst components substantively changed in 2011. Previously, the three pre-existing FS components were characterized as two reporting units: Federal Maintenance, Logistics and Engineering and the Global Security Group. As noted in last year’s annual URS goodwill impairment memo “Analysis of Reporting Units for Goodwill Impairment Analysis”, the primary reason supporting a two reporting unit model was that the GSG reporting unit did not share resources, including operational and administrative functions, as extensively as the SET and DML components. As discussed in the “New Events in FY 2011” section above, due to the transition of the majority of the operational and administrative functions of GSG, the increasing allocation of direct and indirect resources across the business, as well as the transition to contracting all new awards (GSG and non-GSG work) to a common URS Federal Services, Inc. federal legal entity, the argument for disaggregation of reporting units for goodwill impairment purposes, is no longer compelling or practicable. Additionally, the discrete identification of future cash flows, by component of our business, is becoming significantly more difficult to isolate, due to the extensive sharing of assets and resources across the division.

The components also now share the majority of support services provided by FS, with some operational management overlaps. Most notably, as of January 2011, the majority of the components’ accounting, tax, treasury and human resource functions are provided centrally, by the GSC. As each group is not organized or ultimately intended to provide these functions independently, they are dependent on the shared services support functions provided centrally. Furthermore, the transition in 2011 to a combined G&A rate structure from the previous component specific structure will foster further financial and managerial interdependencies amongst the components. The blended G&A rate applied to the combined rate segments will be derived from the costs and base pools of all the member component’s operations, which crosses components and support functions. For example, the G&A costs and base associated with a portion of GSG’s AFCAP work and SET’s NASA work may be combined into one G&A tier, and the resulting blended rate would be borne by both components’ operations, equally.

Conclusion

Propelled by events in 2011 that increased the sharing of resources and financial performance interdependencies among FS components, we believe aggregation of components is appropriate, in accordance with ASC 280-10 and 350-20-55. Therefore, we propose combining the FS components into a single reporting unit for goodwill impairment analysis purposes.

In accordance with ASC 350-20-35-45, when an entity changes its reporting units, the entity should reassign assets and liabilities to the affected reporting unit and then goodwill should be reassigned by using a relative fair value approach. As we are aggregating all of the components within one operating segment, the goodwill of the Federal Services reporting unit is the summation of goodwill allocated to the previous reporting units. There is no reason to conclude that the assignment of assets and liabilities and of goodwill would be different after the transition from two reporting units in the Federal Services operating segment to one reporting unit.

Prior to our determination, we also reviewed the ASC guidance on components of reporting units which may be considered suitable for disaggregation. In our assessment, although there are components within a reporting unit that may be considered for disaggregation, it would not be appropriate in our case to disaggregate. The FS approach to managing its business and sharing resources across the reporting units, and the similar nature of FS’ operations more closely aligns with the criteria for aggregation of reporting units, rather than disaggregation.

A-6

The change in reporting units would not have changed the prior year results, as neither reporting unit failed step one. As described above, the proposal is resulting from the events that took place in 2011 with the sharing of management and resources across the components, which occurred prior to the interim impairment test as of September 30, 2011.

In consideration of our assessment that FS components meet the criteria for aggregation into a single reporting unit for goodwill impairment analysis purposes, we recommend management approves our proposal.

APPENDIX I – FEDERAL SERVICES ORGANIZATIONAL CHARTS

The three legacy FS components are below. The ISG component is reflected on the next page.

A-7

APPENDIX I – ORGANIZATIONAL CHARTS (continued)

A-8