STEWARDSHIP FINANCIAL CORPORATION AND SUBSIDIARY

STOCK PERFORMANCE GRAPH

The following graph compares the cumulative total return on a hypothetical $100 investment made on December 31, 2001 in: (a) Stewardship Financial Corporation’s common stock; (b) Nasdaq Composite Index; and (c) Peer index. The Peer index consists of ten banks located in New Jersey and Pennsylvania with total asset size and operating performance comparable with the Corporation. The peer group consists of 1st Constitution Bancorp, Boardwalk Bancorp, Inc., Central Jersey Bancorp, Codorus Valley Bancorp, Inc., Community Bank of Bergen County, Mid Pen Bancorp, Somerset Hills Bancorp, Sterling Bank, Sussex Bancorp, and Unity Bancorp, Inc. The information provided is not necessarily indicative of the Corporation’s future performance.

| | | | | | Period Ending | | | | | |

Index | | 12/31/01 | | 12/31/02 | | 12/31/03 | | 12/31/04 | | 12/31/05 | | 12/31/06 | |

| Stewardship Financial Corporation | | $ | 100.00 | | $ | 104.14 | | $ | 199.11 | | $ | 197.86 | | $ | 194.82 | | $ | 191.22 | |

| Nasdaq Composite Index | | | 100.00 | | | 68.80 | | | 103.64 | | | 113.07 | | | 115.43 | | | 127.36 | |

| Peer Index | | | 100.00 | | | 113.54 | | | 170.37 | | | 207.19 | | | 212.37 | | | 214.56 | |

STEWARDSHIP FINANCIAL CORPORATION AND SUBSIDIARY

CONSOLIDATED FINANCIAL SUMMARY OF SELECTED FINANCIAL DATA

| | | December 31, | |

| | | 2006 | | 2005 | | 2004 | | 2003 | | 2002 | |

| | | (Dollars in thousands, except per share amounts) | |

Earnings Summary: | | | | | | | | | | | |

| | | | | | | | | | | | |

| Net interest income | | $ | 19,084 | | $ | 18,211 | | $ | 16,367 | | $ | 14,324 | | $ | 12,507 | |

| Provision for loan losses | | | (264 | ) | | (600 | ) | | (540 | ) | | (425 | ) | | (160 | ) |

| Net interest income after provision for loan losses | | | 18,820 | | | 17,611 | | | 15,827 | | | 13,899 | | | 12,347 | |

| Noninterest income | | | 4,189 | | | 3,240 | | | 2,726 | | | 2,894 | | | 2,250 | |

| Noninterest expense | | | 15,629 | | | 13,867 | | | 12,501 | | | 11,394 | | | 9,847 | |

| Income before income tax expense | | | 7,380 | | | 6,984 | | | 6,052 | | | 5,399 | | | 4,750 | |

| Income tax expense | | | 2,627 | | | 2,504 | | | 2,204 | | | 1,908 | | | 1,634 | |

| Net income | | $ | 4,753 | | $ | 4,480 | | $ | 3,848 | | $ | 3,491 | | $ | 3,116 | |

| | | | | | | | | | | | | | | | | |

Common Share Data: (1) | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | |

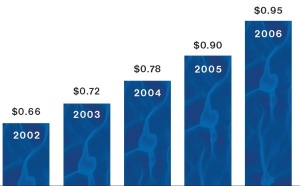

| Basic net income | | $ | 0.95 | | $ | 0.90 | | $ | 0.78 | | $ | 0.72 | | $ | 0.66 | |

| Diluted net income | | | 0.94 | | | 0.89 | | | 0.77 | | | 0.71 | | | 0.65 | |

| Cash dividends declared | | | 0.30 | | | 0.25 | | | 0.21 | | | 0.17 | | | 0.14 | |

| Book value at year end | | | 7.43 | | | 6.70 | | | 6.16 | | | 5.56 | | | 4.96 | |

| Average shares outstanding, net of treasury stock | | | 5,021 | | | 4,991 | | | 4,911 | | | 4,847 | | | 4,749 | |

| Shares outstanding at year end | | | 5,018 | | | 4,986 | | | 4,948 | | | 4,886 | | | 4,802 | |

| Dividend payout ratio | | | 32.19 | % | | 27.79 | % | | 26.46 | % | | 23.37 | % | | 21.41 | % |

| | | | | | | | | | | | | | | | | |

Selected Consolidated Ratios: | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | |

| Return on average assets | | | 0.96 | % | | 1.00 | % | | 0.95 | % | | 0.97 | % | | 1.03 | % |

| Return on average stockholders' equity | | | 13.41 | % | | 13.86 | % | | 13.48 | % | | 13.68 | % | | 14.01 | % |

| Average stockholders' equity as a percentage of average total assets | | | 7.19 | % | | 7.20 | % | | 7.06 | % | | 7.12 | % | | 7.36 | % |

| Tier-l capital leverage (2) | | | 8.85 | % | | 8.71 | % | | 9.08 | % | | 8.89 | % | | 7.02 | % |

| Tier-l risk based capital (3) | | | 11.25 | % | | 11.16 | % | | 12.48 | % | | 12.93 | % | | 10.53 | % |

| Total risk based capital (3) | | | 12.28 | % | | 12.21 | % | | 13.57 | % | | 14.03 | % | | 11.74 | % |

| Allowance for loan loss to total loans | | | 1.11 | % | | 1.11 | % | | 1.11 | % | | 1.10 | % | | 1.24 | % |

| Nonperforming loans to total loans | | | 0.41 | % | | 0.15 | % | | 0.48 | % | | 0.42 | % | | 0.62 | % |

| | | | | | | | | | | | | | | | | |

Selected Year-end Balances: | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | |

| Total assets | | $ | 519,749 | | $ | 482,727 | | $ | 424,306 | | $ | 401,768 | | $ | 331,087 | |

| Total loans, net of allowance for loan loss | | | 365,443 | | | 341,976 | | | 292,909 | | | 258,776 | | | 213,579 | |

| Total deposits | | | 434,223 | | | 403,466 | | | 356,730 | | | 341,335 | | | 302,304 | |

| Stockholders' equity | | | 37,306 | | | 33,384 | | | 30,460 | | | 27,149 | | | 23,817 | |

| (1) | All share and per share amounts have been restated to reflect a 5% stock dividend paid November 2002, 2003, 2004, 2005 and 2006, respectively, a 3 for 2 stock split that occurred July 2003 and a 4 for 3 stock split that occurred July 2005. |

| (2) | As a percentage of average quarterly assets. |

| (3) | As a percentage of total risk-weighted assets. |

Management’s Discussion and Analysis of Financial Condition and Results of Operations

This section provides an analysis of the Stewardship Financial Corporation’s (the “Corporation”) consolidated financial condition and results of operations for the years ended December 31, 2006, 2005 and 2004. The analysis should be read in conjunction with the related audited consolidated financial statements and the accompanying notes presented elsewhere herein.

This annual report contains certain “forward looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995, and may be identified by the use of such words as “believe,” “expect,” “anticipate,” “should,” “plan,” “estimate,” and “potential.” Examples of forward looking statements include, but are not limited to, estimates with respect to the financial condition, results of operations and business of the Corporation that are subject to various factors which could cause actual results to differ materially from these estimates. These factors include: changes in general, economic and market conditions, legislative and regulatory conditions, or the development of an interest rate environment that adversely affects the Corporation’s interest rate spread or other income anticipated from operations and investments. As used in this annual report, “we” and “us” and “our” refer to Stewardship Financial Corporation and its consolidated subsidiary, Atlantic Stewardship Bank, depending on the context.

Introduction

The Corporation, organized in January 1995, as a business corporation under the laws of the State of New Jersey, was established by the Board of Directors of Atlantic Stewardship Bank (the “Bank”) to become a holding company for the Bank. The shareholders of the Bank approved the holding company formation at the annual meeting in 1996. After obtaining approval and submitting appropriate applications, the Corporation, on November 22, 1996, acquired all of the shares of the Bank in exchange for its own shares, on a share per share basis. The Bank, and its subsidiaries, Stewardship Investment Corporation and Stewardship Realty Corporation LLC, are wholly-owned subsidiaries of the Corporation. The Corporation also formed a second subsidiary in 2003, Stewardship Statutory Trust I (the "Trust”). The Trust was formed to issue Trust Preferred Securities to enhance the capital position of the Corporation. The Trust is not consolidated with the Corporation’s financial statements due to the adoption of Financial Accounting Standards Board (FASB) Interpretation No. 46 (revised December 2003) “Consolidation of Variable Interest Entities” (“FIN 46R”).

The Corporation conducts a general commercial and retail banking business encompassing a wide range of traditional deposit and lending functions along with the other customary banking services. Stewardship Investment Corporation is a wholly-owned nonbank subsidiary of the Bank, whose primary business is to own and manage the Bank’s investment portfolio. Stewardship Realty Corporation, a subsidiary of the Bank was formed in September 2005 to purchase a property located at 612 Godwin Avenue, Midland Park, Bergen County, New Jersey. The property, located next to the main office of the Corporation, will be used for future office space for the administrative area of the Bank. The Corporation earns income and generates cash primarily through the deposit gathering activities of the branch network. These deposits are then utilized to fund the Corporation’s lending and investing activities.

The Corporation is affected by the overall economic conditions in northern New Jersey, the interest rate and yield curve environment, and the overall national economy. These factors are relevant because they will affect our ability to attract specific deposit products, our ability to invest in loan and investment products, and our ability to earn acceptable profits without incurring increased risks.

When evaluating the financial condition and operating performance of the organization, management reviews historical trends, peer comparisons, asset and deposit concentrations, interest margin analysis, adequacy of loan loss reserve and loan quality performance, adequacy of capital under current positions as well as to support future expansion, adequacy of liquidity, and overall quality of earnings performance.

The Corporation has developed a strong deposit base with good franchise value. Several challenges are to continue to grow the existing branch levels, explore new branch opportunities, provide adequate technology enhancements to achieve efficiencies, provide strong products, and provide the highest level of customer service.

During 2006, the Corporation opened its tenth branch location at 2 Changebridge Road, Montville, Morris County, New Jersey. This is a full service facility offering safe deposits, a two lane drive-up and an ATM drive-up facility. This represents a new market area for the Corporation where our products and services have been well accepted.

The Corporation also worked during the second half of 2006 to build its eleventh branch location at 378 Franklin Avenue, Wyckoff, Bergen County, New Jersey. This branch opened in March 2007, with its grand opening scheduled in April and is expected to be a convenient location to service existing as well as new customers. It will also be a full service facility offering safe deposits, a two lane drive-up and an ATM drive-up facility.

Early in January 2007, the Corporation signed a lease for its twelfth branch to be located in Westwood, Bergen County, New Jersey and, pending all appropriate approvals, plans to provide services to a new market area beginning in the third quarter of 2007. The branch network built by the Corporation covers a strong market area designed to attract a diversified customer base that has and will continue to utilize our strong base of loan and deposit products.

During the fourth quarter of 2006, Management completed two transactions that positioned the Corporation to improve future profitability and asset yields. The Corporation successfully completed a sale of its $3.4 million credit card portfolio to Elan Financial Services (“Elan”). Elan, a national provider of credit card services, purchased the portfolio and will continue to service and offer credit card products in the name of Atlantic Stewardship Bank. The proceeds from the sale were reinvested in other lending opportunities. The Corporation will realize, in addition to the premium paid on the portfolio, future income from Elan based on new card production and customer activity.

Management also completed the sale of $17.3 million available for sale securities that were yielding less than 5%. The proceeds realized from the sale were used to purchase higher yielding securities and to fund loan growth. Management anticipates that this transaction will improve portfolio yields and reduce exposure to future interest rate risk.

Recent Accounting Pronouncements

A discussion of recent pronouncements and their effect on the Corporation’s financial statements can be found in Note 20 of the financial statements.

Critical Accounting Policies And Estimates

“Management’s Discussion and Analysis of Financial Condition and Results of Operation,” is based upon the Corporation’s consolidated financial statements, which have been prepared in accordance with accounting principles generally accepted in the United States of America. The preparation of these financial statements requires the Corporation to make estimates and judgments that affect the reported amounts of assets, liabilities, revenues and expenses. Note 1 to the Corporation’s Audited Consolidated Financial Statements for the year ended December 31, 2006 contains a summary of the Corporation’s significant accounting policies. Management believes the Corporation’s policy with respect to the methodology for the determination of the allowance for loan losses involves a higher degree of complexity and requires management to make difficult and subjective judgments, which often require assumptions or estimates about highly uncertain matters. Changes in these judgments, assumptions or estimates could materially impact results of operations. This critical policy and its application are periodically reviewed with the Audit Committee and the Board of Directors.

The allowance for loan losses is based upon management’s evaluation of the adequacy of the allowance, including an assessment of known and inherent risks in the portfolio, giving consideration to the size and composition of the loan portfolio, actual loan loss experience, level of delinquencies, detailed analysis of individual loans for which full collectibility may not be assured, the existence and estimated net realizable value of any underlying collateral and guarantees securing the loans, and current economic and market conditions. Although management uses the best information available, the level of the allowance for loan losses remains an estimate, which is subject to significant judgment and short-term change. Various regulatory agencies, as an integral part of their examination process, periodically review the Corporation’s allowance for loan losses. Such agencies may require the Corporation to make additional provisions for loan losses based upon information available to them at the time of their examination. Furthermore, the majority of the Corporation’s loans are secured by real estate in the State of New Jersey. Accordingly, the collectibility of a substantial portion of the carrying value of the Corporation’s loan portfolio is susceptible to changes in local market conditions and may be adversely affected should real estate values decline or the northern New Jersey area experience an adverse economic shock. Future adjustments to the allowance for loan losses may be necessary due to economic, operating, regulatory and other conditions beyond the Corporation’s control.

Earnings Summary

The Corporation reported net income of $4.75 million, or $0.95 basic earnings per share, for the year ended December 31, 2006, an increase of $273,000, or 6.1%, above the $4.48 million recorded for 2005. Earnings for 2005 had increased $632,000, or 16.4%, over the 2004 earnings of $3.85 million. Earnings have increased in both years as a result of increases in net interest income and noninterest income, offset by increases in noninterest expense.

The Federal Reserve began a period of measured increases in interest rates in June 2004 that continued through June 2006. For 2004, the targeted federal funds rate began at 1.00% and increased 0.25% at each Federal Open Market Committee meeting in 2004 and 2005 and paused at the June 2006 meeting at 5.25%. Short-term interest rates increased as a result of the increases by the Federal Reserve, while market driven longer term interest rates remained mostly unchanged at historically low levels creating an inverted yield curve. The level of interest rates, inverted yield curve and competitive loan and deposit environment created pressure on net interest margins. The Corporation’s net interest income increased $873,000. An increase in the average loan volume partially offset by the rising costs of deposits and borrowings contributed to this increase.

The return on average assets decreased in 2006 to 0.96% from 1.00% in 2005. The return on average equity decreased to 13.41% in 2006 from 13.86% in 2005.

Results of Operations

Net Interest Income

The Corporation’s principal source of revenue is the net interest income derived from the Bank, which represents the difference between the interest earned on assets and interest paid on funds acquired to support those assets. Net interest income is affected by the balances and mix of interest-earning assets and interest-bearing liabilities, changes in their corresponding yields and costs, and by the volume of interest-earning assets funded by noninterest-bearing deposits. The Corporation’s principal interest-earning assets are loans made to businesses and individuals, investment securities, and federal funds sold.

In 2006, net interest income, on a tax equivalent basis, increased to $19.35 million from $18.48 million in 2005, an increase of $872,000, or 4.7%. This was caused by an increase of $3.6 million, or 3.6%, in net average interest-earning assets (average interest-earning assets less average interest-bearing liabilities).

Interest income, on a tax equivalent basis, increased $5.1 million, or 20.3%, during 2006 to $30.27 million from $25.17 million earned during 2005. The increase was due to an increase in the average volume of interest-earning assets and an increase in yields on interest-earning assets. Average interest-earning assets increased $40.4 million in 2006, or 9.5%, over the 2005 amount with average loans attributing to $44.2 million of the increase due primarily to the Corporation’s competitiveness within the marketplace. Yields on interest earning assets increased 59 basis points from 5.93% in 2005 to 6.52% in 2006.

Interest expense increased $4.2 million, or 63.2%, during 2006 to $10.92 million. The increase was due to an increase in average interest-bearing liabilities of $36.8 million, or 11.3%, to $361.50 million during 2006. Yields on interest-bearing liabilities increased to 3.02% during 2006 from 2.06% during 2005. The competitive interest rate environment created a challenging deposit market. With the rise in short-term interest rates, customers have become very interest rate sensitive, demanding higher interest rates on short-term investments. The Corporation experienced a shift from interest-bearing demand and savings deposits into certificate of deposits. In order to supplement funding needs, the Corporation utilized the brokered certificate of deposit market. As of December 31, 2006, the Corporation had $19.67 million brokered certificates with average yields of 5.37% and average maturities of 0.64 years. The Corporation also encouraged depositors by enhancing our Kids Savings product and introducing our Business Freedom Checking Account. The Corporation anticipates that new branches and products will provide future core deposit growth for the Corporation.

In 2005, net interest income, on a tax equivalent basis, increased to $18.48 million from $16.66 million in 2004, an increase of $1.8 million, or 10.9%. Interest income, on a tax equivalent basis, increased $3.7 million, or 17.4%, during 2005 to $25.17 million from $21.45 million earned in 2004 and yields increased 34 basis points to 5.93% for 2006. The increase was due to an increase in the average volume of interest-earning assets and an increase in yields on interest-earning assets. Average interest-earning assets increased $40.8 million in 2005, or 10.6%, over the 2004 amount. Interest expense increased $1.9 million, or 39.8%, during 2005. The increase was due to an increase in average interest-bearing liabilities and an increase in yields on interest-bearing liabilities. Average noninterest-bearing demand deposits increased $7.5 million, or 9.3% to $88.86 million during 2005 and yields increased 42 basis points to 2.06% for 2006.

The following table reflects the components of the Corporation’s net interest income for the years ended December 31, 2006, 2005 and 2004 including, (1) average assets, liabilities, and stockholders’ equity, (2) interest income earned on interest-earning assets and interest expense paid on interest-bearing liabilities, (3) average yields earned on interest-earning assets and average rates paid on interest-bearing liabilities, and (4) net yield on interest-earning assets. Nontaxable income from investment securities is presented on a tax-equivalent basis assuming a statutory tax rate of 34% for the years presented. This was accomplished by adjusting this income upward to make it equivalent to the level of taxable income required to earn the same amount after taxes.

| | | 2006 | | 2005 | | 2004 | |

| | | Average Balance | | Interest Income/ Expense | | Average Rates Earned Paid | | Average Balance | | Interest Income/ Expense | | Average Rates Earned / Paid | | Average Balance | | Interest Income/ Expense | | Average Rates Earned/ Paid | |

| | | (Dollars in thousands) | |

Assets | | | | | | | | | | | | | | | | | | | |

| Interest-earning assets: | | | | | | | | | | | | | | | | | | | |

| Loans (1) | | $ | 359,806 | | $ | 25,619 | | | 7.12 | % | $ | 315,605 | | $ | 20,927 | | | 6.63 | % | $ | 275,334 | | $ | 17,346 | | | 6.30 | % |

| Taxable investment securities (1) | | | 85,322 | | | 3,732 | | | 4.37 | | | 81,332 | | | 3,130 | | | 3.85 | | | 84,641 | | | 3,103 | | | 3.67 | |

| Tax-exempt investment securities (1) (2) | | | 18,702 | | | 868 | | | 4.64 | | | 18,998 | | | 852 | | | 4.48 | | | 20,134 | | | 952 | | | 4.73 | |

| Other interest-earning assets | | | 741 | | | 51 | | | 6.88 | | | 8,200 | | | 262 | | | 3.20 | | | 3,270 | | | 46 | | | 1.41 | |

| Total interest-earning assets | | | 464,571 | | | 30,270 | | | 6.52 | | | 424,135 | | | 25,171 | | | 5.93 | | | 383,379 | | | 21,447 | | | 5.59 | |

| Non-interest-earning assets: | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Allowance for loan losses | | | (4,020 | ) | | | | | | | | (3,600 | ) | | | | | | | | (3,086 | ) | | | | | | |

| Other assets | | | 32,862 | | | | | | | | | 28,442 | | | | | | | | | 24,139 | | | | | | | |

| Total assets | | $ | 493,413 | | | | | | | | $ | 448,977 | | | | | | | | $ | 404,432 | | | | | | | |

Liabilities and Stockholders' Equity | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Interest-bearing liabilities: | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Interest-bearing demand deposits | | $ | 116,405 | | $ | 2,064 | | | 1.77 | % | $ | 133,968 | | $ | 1,531 | | | 1.14 | % | $ | 122,426 | | $ | 810 | | | 0.66 | % |

| Savings deposits | | | 41,682 | | | 256 | | | 0.61 | | | 48,300 | | | 286 | | | 0.59 | | | 49,390 | | | 344 | | | 0.70 | |

| Time deposits | | | 160,816 | | | 6,560 | | | 4.08 | | | 114,763 | | | 3,673 | | | 3.20 | | | 91,163 | | | 2,450 | | | 2.69 | |

| Repurchase agreements | | | 7,461 | | | 331 | | | 4.44 | | | 3,371 | | | 98 | | | 2.91 | | | 2,832 | | | 37 | | | 1.31 | |

| FHLB borrowings | | | 27,923 | | | 1,218 | | | 4.36 | | | 17,054 | | | 614 | | | 3.60 | | | 19,138 | | | 657 | | | 3.43 | |

| Subordinated debenture | | | 7,217 | | | 487 | | | 6.75 | | | 7,217 | | | 487 | | | 6.75 | | | 7,217 | | | 487 | | | 6.75 | |

| Total interest-bearing liabilities | | | 361,504 | | | 10,916 | | | 3.02 | | | 324,673 | | | 6,689 | | | 2.06 | | | 292,166 | | | 4,785 | | | 1.64 | |

| Noninterest-bearing liabilities: | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Demand deposits | | | 92,217 | | | | | | | | | 88,863 | | | | | | | | | 81,321 | | | | | | | |

| Other liabilities | | | 4,234 | | | | | | | | | 3,120 | | | | | | | | | 2,398 | | | | | | | |

| Stockholders' equity | | | 35,458 | | | | | | | | | 32,321 | | | | | | | | | 28,547 | | | | | | | |

| Total liabilities and stockholders' equity | | $ | 493,413 | | | | | | | | $ | 448,977 | | | | | | | | $ | 404,432 | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Net interest income (taxable equivalent basis) | | | | | | 19,354 | | | | | | | | | 18,482 | | | | | | | | | 16,662 | | | | |

| Tax equivalent adjustment | | | | | | (270 | ) | | | | | | | | (271 | ) | | | | | | | | (295 | ) | | | |

| Net interest income | | | | | $ | 19,084 | | | | | | | | $ | 18,211 | | | | | | | | $ | 16,367 | | | | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Net interest spread (taxable equivalent basis) | | | | | | | | | 3.50 | % | | | | | | | | 3.87 | % | | | | | | | | 3.95 | % |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Net yield on interest-earning assets (taxable equivalent basis) (3) | | | | | | | | | 4.17 | % | | | | | | | | 4.36 | % | | | | | | | | 4.35 | % |

| (1) | For purpose of these calculations, nonaccruing loans are included in the average balance. Fees are included in loan interest. Loans and total interest-earning assets are net of unearned income. Securities are included at amortized cost. |

| (2) | The tax equivalent adjustments are based on a marginal tax rate of 34%. |

| (3) | Net interest income (taxable equivalent basis) divided by average interest-earning assets. |

The following table analyzes net interest income in terms of changes in the volume of interest-earning assets and interest-bearing liabilities and changes in yields earned and rates paid on such assets and liabilities on a tax equivalent basis. The table reflects the extent to which changes in the Corporation’s interest income and interest expense are attributable to changes in volume (changes in volume multiplied by prior year rate) and changes in rate (changes in rate multiplied by prior year volume). Changes attributable to the combined impact of volume and rate have been allocated proportionately to changes due to volume and changes due to rate.

| | | 2006 Versus 2005 | | 2005 Versus 2004 | |

| | | (In thousands) | |

| | | Increase (Decrease) Due to Change in | | | | Increase (Decrease) Due to Change in | | | |

| | | Volume | | Rate | | Net | | Volume | | Rate | | Net | |

| | | | | | | | | | | | | | |

| Interest income: | | | | | | | | | | | | | |

| | | | | | | | | | | | | | |

| Loans. | | $ | 3,073 | | $ | 1,619 | | $ | 4,692 | | $ | 2,635 | | $ | 946 | | $ | 3,581 | |

| Taxable investment securities | | | 159 | | | 443 | | | 602 | | | (230 | ) | | 257 | | | 27 | |

| Tax-exempt investment securities | | | (13 | ) | | 29 | | | 16 | | | (52 | ) | | (48 | ) | | (100 | ) |

| Other interest-earning assets | | | (360 | ) | | 149 | | | (211 | ) | | 117 | | | 99 | | | 216 | |

| | | | | | | | | | | | | | | | | | | | |

| Total interest-earning assets. | | | 2,859 | | | 2,240 | | | 5,099 | | | 2,470 | | | 1,254 | | | 3,724 | |

| | | | | | | | | | | | | | | | | | | | |

| Interest expense: | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | |

| Interest-bearing demand deposits | | $ | (222 | ) | $ | 755 | | $ | 533 | | $ | 83 | | $ | 638 | | $ | 721 | |

| Savings deposits | | | (40 | ) | | 10 | | | (30 | ) | | (7 | ) | | (51 | ) | | (58 | ) |

| Time deposits | | | 1,714 | | | 1,173 | | | 2,887 | | | 704 | | | 519 | | | 1,223 | |

| Repurchase agreements | | | 163 | | | 70 | | | 233 | | | 8 | | | 53 | | | 61 | |

| FHLB borrowings | | | 453 | | | 151 | | | 604 | | | (74 | ) | | 31 | | | (43 | ) |

| | | | | | | | | | | | | | | | | | | | |

| Total interest-bearing liabilities | | | 2,068 | | | 2,159 | | | 4,227 | | | 714 | | | 1,190 | | | 1,904 | |

| | | | | | | | | | | | | | | | | | | | |

| Net change in net interest income. | | $ | 791 | | $ | 81 | | $ | 872 | | $ | 1,756 | | $ | 64 | | $ | 1,820 | |

Provision for Loan Losses

The Corporation maintains an allowance for loan losses considered by management to be adequate to cover the inherent risk of loss associated with its loan portfolio. On an ongoing basis, management analyzes the adequacy of this allowance by considering the nature and volume of the Corporation’s loan activity, financial condition of the borrower, fair market value of underlying collateral, and changes in general market conditions. Additions to the allowance for loan losses are charged to operations in the appropriate period. Actual loan losses, net of recoveries, serve to reduce the allowance. The appropriate level of the allowance for loan losses is based on estimates, and ultimate losses may vary from current estimates.

The loan loss provision totaled $264,000 in 2006 representing a 56.0% decrease from the 2005 provision of $600,000. The 2005 provision increased 11.1% from the 2004 provision of $540,000. The loan loss provision for 2006 contained an $86,000 reversal of loan loss due to the sale of the credit card portfolio. The provision expense for each year is a reflection of loan growth, loan mix, net chargeoffs, and the overall level of nonperforming loans.

Noninterest Income

Noninterest income consists of all income other than interest income and is principally derived from service charges on deposits, gain on sales of mortgage loans, income derived from bank owned life insurance, fees on safe deposit boxes, credit card merchant income and income derived from debit cards and ATM usage.

Noninterest income increased $949,000, or 29.3%, to $4.19 million during the year ended December 31, 2006, when compared with $3.24 million during the comparable 2005 period. The increase in noninterest income resulted primarily from the gain on the sale of the credit card portfolio of $746,000, an increase of $214,000 in fees and service charges primarily caused by the implementation of an overdraft protection program for personal customers, an increase of $102,000 representing the full year effect of purchasing bank owned life insurance in 2005 and an increase of $323,000 in merchant processing, partially offset by the loss on the sale of available for sale securities of $435,000. The sale of the credit card portfolio was completed during the fourth quarter of 2006, pursuant to which management sold $3.4 million credit card loans to Elan. Under the agreement, Elan

purchased the portfolio for a 19% premium and agreed to honor the existing award program offered to customers. Under the terms of the agreement, cards will still be offered in the name of Atlantic Stewardship Bank. The Corporation will share in future income as new cards are issued and as cardholders complete transactions. Management’s analysis revealed that proceeds could be reinvested and resources reallocated to other more profitable lending products and customers could retain strong credit card products and services.

The investment restructuring completed during the fourth quarter of 2006 resulted in the sale of $17.3 million available for sale securities yielding less than 5% with a loss of $435,000. Proceeds were reinvested in higher yielding investments and loans that should improve earning asset yields and decrease future interest rate risk.

Noninterest income increased by $514,000, or 18.9%, to $3.24 million during the year ended December 31, 2005, when compared with $2.73 million during the 2004 period. The increase resulted from an increase of $104,000 in gains on sales of mortgage loans due to an increase in the volume of loans originated for sale. In April 2005, the Corporation purchased $8.0 million in bank owned life insurance on key management personnel. The increase in the cash surrender value of the insurance policies was recognized in income for 2005 in the amount of $210,000. Income from merchant card processing increased by $135,000 in 2005 compared with the year ended 2004 due to an increase in the number of customers using this service.

Noninterest Expense

Although management is committed to containing noninterest expense, the continued growth of the Corporation has caused noninterest expense to increase by $1.8 million or 12.7%, to $15.63 million for the year ended December 31, 2006, compared to $13.87 million for the same period in 2005. Salaries and employee benefits, the major component of noninterest expense, increased $712,000, or 11.7%. The increase was due primarily to staffing increases in lending, new business development, and the new Montville branch and for general merit and performance increases. Occupancy and equipment expenses increased $467,000 primarily due to the expenses relating to the new Montville and Wyckoff branches. Data processing expenses increased $122,000 due to continued growth of deposit and loan processing and merchant processing expenses increased $309,000 due to the growth in the merchant business.

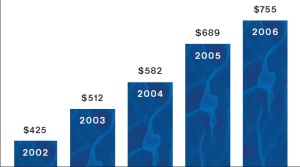

In accordance with its By-laws to tithe ten percent (10%) of its pre-tax profits to various charities, the Corporation had charitable contributions totaling $755,000 for the year ended December 31, 2006, an increase of $66,000, or 9.6%, over the same period in 2005.

Noninterest expense increased $1.4 million, or 10.9%, to $13.87 million for the year ended December 31, 2005, compared to $12.50 million for the same period in 2004. Increases in salaries and employee benefits totaling $441,000, or 7.8%, were primarily a result of general merit and performance increases and increases in benefit related expenses. Data processing expenses increased $134,000, or 13.2%, due to increases in our deposit and lending base and advertising increased $137,000 to support product offerings and the 20th anniversary celebration. Merchant expense increased $101,000 due to increased merchant business and donation expense increased $107,000 due to the increase in pretax earnings. Miscellaneous expenses increased $346,000, or 19.0%, as a result of increases in consulting expense and the general growth of the Corporation. During 2005, the Corporation hired an outside consulting firm to work with management in the documentation of internal controls. This has helped in moving the Corporation towards compliance with Sarbanes Oxley Act Section 404 which requires management to assess and document the adequacy of internal controls. Management anticipates that the consulting firm will continue their work in 2007.

Income Taxes

Income tax expense totaled $2.63 million for the year ended December 31, 2006, for an effective tax rate of 35.6%, compared to $2.50 million, for an effective tax rate of 35.9% for the year ended December 31, 2005, and $2.20 million, for an effective tax rate of 36.4% for the year ended December 31, 2004. The decrease in the effective tax rate can be attributed primarily to the tax deferred income derived from bank owned life insurance.

Financial Condition

Total assets at December 31, 2006 were $519.75 million, an increase of $37.0 million, or 7.7%, over the $482.73 million at December 31, 2005. This increase in assets reflects, among other things, a $23.5 million increase in net loans held for portfolio, and an $8.6 million increase in securities available for sale.

Loan Portfolio

The Corporation’s loan portfolio at December 31, 2006, net of allowance for loan losses, totaled $365.44 million, an increase of $23.5 million, or 6.9%, over the $341.98 million at December 31, 2005. Commercial real estate mortgage loans consisting of $177.41 million, or 47.9% of the total portfolio, comprised the largest portion of the loan portfolio. This represented an increase of $14.1 million from $163.31 million, or 47.2% of the total loan portfolio at December 31, 2005. Commercial loans increased $7.6 million to $72.61 million, representing 19.6% of the total loan portfolio. Consumer installment loans increased $849,000, despite the sale of $3.4 million of credit cards. Residential real estate mortgages increased $1.4 million. The Corporation continued its policy of selling the majority of its residential real estate loans in the secondary market. All of these loans have been sold with servicing released.

The Corporation’s lending activities are concentrated in loans secured by real estate located in northern New Jersey and therefore collectibility of the loan portfolio is susceptible to changes in real estate market conditions in the northern New Jersey market. The Corporation has not made loans to borrowers outside the United States.

At December 31, 2006, there were no concentrations of loans exceeding 10% of total loans outstanding. Loan concentrations are considered to exist when there are amounts loaned to a multiple number of borrowers engaged in similar activities which would cause them to be similarly impacted by economic or other related conditions.

The following table sets forth the classification of the Corporation’s loans by major category at the end of the last five years:

| | | December 31, | |

| | | 2006 | | 2005 | | 2004 | | 2003 | | 2002 | |

| | | (In thousands) | |

| | | | | | | | | | | | |

| Real estate mortgage: | | | | | | | | | | | |

| Residential | | $ | 47,020 | | $ | 45,604 | | $ | 41,569 | | $ | 44,835 | | $ | 39,705 | |

| Commercial | | | 177,411 | | | 163,309 | | | 130,762 | | | 109,708 | | | 88,593 | |

| | | | | | | | | | | | | | | | | |

| Commercial loans | | | 72,606 | | | 65,011 | | | 55,252 | | | 48,950 | | | 38,228 | |

| | | | | | | | | | | | | | | | | |

| Consumer loans: | | | | | | | | | | | | | | | | |

| Installment (1). | | | 52,389 | | | 51,540 | | | 47,218 | | | 41,067 | | | 37,293 | |

| Home equity. | | | 20,010 | | | 20,271 | | | 21,484 | | | 17,181 | | | 12,471 | |

| Other | | | 560 | | | 506 | | | 260 | | | 238 | | | 241 | |

| | | | | | | | | | | | | | | | | |

| Total gross loans | | | 369,996 | | | 346,241 | | | 296,545 | | | 261,979 | | | 216,531 | |

| Less: Allowance for loan losses | | | 4,101 | | | 3,847 | | | 3,299 | | | 2,888 | | | 2,689 | |

| Deferred loan fees | | | 452 | | | 418 | | | 337 | | | 315 | | | 263 | |

| Net loans | | $ | 365,443 | | $ | 341,976 | | $ | 292,909 | | $ | 258,776 | | $ | 216,579 | |

| (1) | Includes automobile, home improvement, second mortgages and unsecured loans. Credit card loans are also included for all years prior to December 31, 2006. |

The following table sets forth certain categories of gross loans as of December 31, 2006 by contractual maturity. Borrowers may have the right to prepay obligations with or without prepayment penalties. This might cause actual maturities to differ from the contractual maturities summarized below.

| | | Within 1 Year | | After 1 Year But Within 5 Years | | After 5 Years | | Total | |

| | | (In thousands) | |

| | | | | | | | | | |

| Real estate mortgage | | $ | 38,616 | | $ | 15,240 | | $ | 170,575 | | $ | 224,431 | |

| Commercial | | | 33,429 | | | 32,251 | | | 6,926 | | | 72,606 | |

| Consumer | | | 1,143 | | | 8,697 | | | 63,119 | | | 72,959 | |

| Total gross loans | | $ | 73,188 | | $ | 56,188 | | $ | 240,620 | | $ | 369,996 | |

The following table sets forth the dollar amount of all gross loans due one year or more after December 31, 2006, which have predetermined interest rates or floating or adjustable interest rates:

| | | Predetermined Rates | | Floating or Adjustable Rates | | Total | |

| | | (In thousands) | |

| | | | | | | | |

| Real estate mortgage | | $ | 63,679 | | $ | 122,136 | | $ | 185,815 | |

| Commercial | | | 22,184 | | | 16,993 | | | 39,177 | |

| Consumer | | | 51,680 | | | 20,136 | | | 71,816 | |

| | | $ | 137,543 | | $ | 159,265 | | $ | 296,808 | |

Asset Quality

The Corporation’s principal earning asset is its loan portfolio. Inherent in the lending function is the risk of deterioration in a borrower’s ability to repay loans under existing loan agreements. Management realizes that because of this risk, reserves are maintained to absorb loan losses. In determining the adequacy of the allowance for loan losses, management of the Corporation considers the risks inherent in its loan portfolio and changes in the nature and volume of its loan activities, along with general economic and real estate market conditions. Although management attempts to establish a reserve sufficient to offset probable incurred losses in the portfolio, changes in economic conditions, regulatory policies and borrower’s performance could require future changes to the allowance.

The Corporation utilizes a two tier approach by (1) identifying problem loans and allocating specific loss allowances on such loans and (2) establishing a general valuation allowance on the remainder of its loan portfolio. The Corporation maintains a loan review system that allows for a periodic review of its loan portfolio and the early identification of potential problem loans. Such a system takes into consideration, among other things, delinquency status, size of loans, type of collateral and financial condition of the borrowers. Allocations of specific loan loss allowances are established for identified loans based on a review of such information and/or appraisals of underlying collateral. General loan loss allowances are based upon a combination of factors including, but not limited to, actual loss experience, composition of loan portfolio, current economic conditions and management’s judgment.

The Corporation’s accounting policies are set forth in Note 1 to the audited financial statements. The application of some of these policies require significant management judgment and the utilization of estimates. Actual results could differ from these judgments and estimates resulting in a significant impact on the financial statements. A critical accounting policy for the Corporation is the policy utilized in determining the adequacy of the allowance for loan losses. Although management uses the best information available, the level of the allowance for loan losses remains an estimate which is subject to significant judgment and short-term change. Various regulatory agencies, as an integral part of their examination process, periodically review the Corporation’s allowance for loan losses. Such agencies may require the Corporation to make additional provisions for loan losses based upon information available to them at the time of their examination. Furthermore, the majority of the Corporation’s loans are secured by real estate in the state of New Jersey. Accordingly, the collectibility of a substantial portion of the carrying value of the Corporation’s loan portfolio is susceptible to changes in the local market conditions and may be adversely affected should real estate values decline or the northern New Jersey area experience an adverse economic shock. Future adjustments to the allowance may be necessary due to economic, operating, regulatory, and other conditions beyond the Corporation’s control. The allowance for loan losses represents 1.11% of total loans, or 2.7 times non-performing loans at December 31, 2006, compared with 1.11% of total loans or 7.3 times non-performing loans at December 31, 2005. In management’s opinion, the allowance for loan losses totaling $4.1 million is adequate to cover losses inherent in the portfolio at December 31, 2006.

Nonperforming Assets

Nonperforming assets include nonaccrual loans, restructured loans, loans past due 90 days or more and accruing, and other real estate owned. There were no other real estate owned assets for the periods presented. The Corporation’s loans are generally placed in a nonaccrual status when they become past due in excess of 90 days as to payment of principal and interest. Interest previously accrued on these loans and not yet paid is charged against income during the current period. Interest earned thereafter is only included in income to the extent that it is received in cash. Loans past due 90 days or more and accruing represent those loans which are sufficiently collateralized and management believes all interest and principal owed will be collected. Restructured loans are loans that have been renegotiated to permit a borrower, who has incurred adverse financial circumstances, to continue to perform. Management can reduce the contractual interest rates to below market rates or make significant concessions to the terms of the loan in order for the borrower to continue to make payments.

The following table sets forth certain information regarding the Corporation’s nonperforming assets as of December 31 of each of the preceding five years:

| | | December 31, | |

| | | 2006 | | 2005 | | 2004 | | 2003 | | 2002 | |

| | | (Dollars in thousands) | |

| | | | | | | | | | | | |

| Nonaccrual loans: (1) | | | | | | | | | | | |

| Commercial real estate | | $ | 123 | | $ | 122 | | $ | 56 | | $ | 83 | | $ | 80 | |

| Commercial | | | 167 | | | 258 | | | 159 | | | 163 | | | 326 | |

| Consumer | | | 154 | | | 92 | | | 47 | | | 11 | | | 89 | |

| Total nonaccrual loans | | | 444 | | | 472 | | | 262 | | | 257 | | | 495 | |

| | | | | | | | | | | | | | | | | |

| Loans past due ninety days or more and accruing: (2) | | | | | | | | | | | | | | | | |

| Construction | | | 840 | | | - | | | 940 | | | - | | | - | |

| Commercial | | | 241 | | | - | | | - | | | 314 | | | - | |

| Consumer | | | 9 | | | 55 | | | 7 | | | 6 | | | 4 | |

| Total loans past due ninety days or more and accruing. | | | 1,090 | | | 55 | | | 947 | | | 320 | | | 4 | |

| | | | | | | | | | | | | | | | | |

| Restructured loans: | | | | | | | | | | | | | | | | |

| Commercial | | | - | | | - | | | - | | | 269 | | | 451 | |

| Consumer | | | - | | | - | | | 215 | | | 244 | | | 397 | |

| Total restructured loans | | | - | | | - | | | 215 | | | 513 | | | 848 | |

| Total nonperforming loans | | $ | 1,534 | | $ | 527 | | $ | 1,424 | | $ | 1,090 | | $ | 1,347 | |

| | | | | | | | | | | | | | | | | |

| Nonaccrual loans to total gross loans | | | 0.12 | % | | 0.14 | % | | 0.09 | % | | 0.10 | % | | 0.23 | % |

| Nonperforming loans to total gross loans | | | 0.41 | % | | 0.15 | % | | 0.48 | % | | 0.42 | % | | 0.62 | % |

| Nonperforming loans to total assets | | | 0.30 | % | | 0.11 | % | | 0.34 | % | | 0.27 | % | | 0.41 | % |

| Allowance for loan losses to nonperforming loans | | | 267.34 | % | | 729.98 | % | | 231.67 | % | | 264.95 | % | | 199.63 | % |

___________________________________________

| (1) | There were no restructured loans classified as nonaccrual for the year ended December 31, 2006. Restructured loans classified in the nonaccrual category totaled $152,000, $162,000, $174,000 and $329,000 for 2005, 2004, 2003 and 2002, respectively. |

| (2) | There were no restructured loans classified in the past due ninety days or more and accruing for the years ended 2006, 2005, 2004 and 2002. In 2003, restructured loans totaling $150,000 were classified in the past due ninety days or more and accruing category. |

The construction loan balance of $840,000 shown as past due ninety days or more and accruing at December 31, 2006 represented one loan which was fully satisfied in February 2007.

There were no loans, other than those included in the above table, where the Corporation was aware of any credit conditions of any borrowers that would indicate a strong possibility of the borrowers not complying with the present terms and conditions of repayment and which may result in such loans being included as nonaccrual, past due or restructured at a future date.

The following table sets forth, for each of the preceding five years, the historical relationships among the amount of loans outstanding, the allowance for loan losses, the provision for loan losses, the amount of loans charged off and the amount of loan recoveries:

| | | 2006 | | 2005 | | 2004 | | 2003 | | 2002 | |

| | | (Dollars in thousands) | |

| | | | | | | | | | | | |

| Balance at beginning of period | | $ | 3,847 | | $ | 3,299 | | $ | 2,888 | | $ | 2,689 | | $ | 2,602 | |

| Loans charged off: | | | | | | | | | | | | | | | | |

| Commercial | | | 7 | | | - | | | 49 | | | 173 | | | 65 | |

| Consumer | | | 33 | | | 57 | | | 92 | | | 56 | | | 25 | |

| Total loans charged off | | | 40 | | | 57 | | | 141 | | | 229 | | | 90 | |

| | | | | | | | | | | | | | | | | |

| Recoveries of loans previously charged off: | | | | | | | | | | | | | | | | |

| Commercial | | | 23 | | | - | | | 3 | | | 1 | | | 9 | |

| Consumer | | | 7 | | | 5 | | | 9 | | | 2 | | | 8 | |

| Total recoveries of loans previously charged off | | | 30 | | | 5 | | | 12 | | | 3 | | | 17 | |

| | | | | | | | | | | | | | | | | |

| Net loans charged off | | | 10 | | | 52 | | | 129 | | | 226 | | | 73 | |

| | | | | | | | | | | | | | | | | |

| Provisions charged to operations | | | 264 | | | 600 | | | 540 | | | 425 | | | 160 | |

| | | | | | | | | | | | | | | | | |

| Balance at end of period | | $ | 4,101 | | $ | 3,847 | | $ | 3,299 | | $ | 2,888 | | $ | 2,689 | |

| | | | | | | | | | | | | | | | | |

| Net charge offs during the period to average loans outstanding during the period | | | 0.00 | % | | 0.02 | % | | 0.05 | % | | 0.10 | % | | 0.04 | % |

| | | | | | | | | | | | | | | | | |

| Balance of allowance for loan losses at the end of year to gross year end loans | | | 1.11 | % | | 1.11 | % | | 1.11 | % | | 1.10 | % | | 1.24 | % |

The following table sets forth the allocation of the allowance for loan losses, for each of the preceding five years, as indicated by loan categories:

| | | 2006 | | 2005 | | 2004 | | 2003 | | 2002 | |

| | | Amount | | Percent to Total (1) | | Amount | | Percent to Total (1) | | Amount | | Percent to Total (1) | | Amount | | Percent to Total (1) | | Amount | | Percent to Total (1) | |

| | | (Dollars in thousands) | |

| | | | | | | | | | | | | | | | | | | | | | |

| Real estate - residential | | $ | 298 | | | 12.7 | % | $ | 320 | | | 13.2 | % | $ | 297 | | | 14.0 | % | $ | 306 | | | 17.1 | % | $ | 289 | | | 18.3 | % |

| Real estate - commercial | | | 1,705 | | | 48.0 | % | | 1,562 | | | 47.1 | % | | 1,272 | | | 44.1 | % | | 1,038 | | | 41.9 | % | | 911 | | | 40.9 | % |

| Commercial | | | 1,407 | | | 19.6 | % | | 1,192 | | | 18.8 | % | | 979 | | | 18.6 | % | | 910 | | | 18.7 | % | | 906 | | | 17.7 | % |

| Consumer | | | 691 | | | 19.7 | % | | 773 | | | 20.9 | % | | 751 | | | 23.3 | % | | 634 | | | 22.3 | % | | 583 | | | 23.1 | % |

| Total allowance for loan losses | | $ | 4,101 | | | 100.0 | % | $ | 3,847 | | | 100.0 | % | $ | 3,299 | | | 100.0 | % | $ | 2,888 | | | 100.0 | % | $ | 2,689 | | | 100.0 | % |

| (1) | Represents percentage of loan balance in category to total gross loans. |

Investment Portfolio

The Corporation maintains an investment portfolio to enhance its yields and to provide a secondary source of liquidity. The portfolio is comprised of U.S. Treasury securities, U.S. government and agency obligations, mortgage-backed securities, and state and political subdivision obligations and has been classified as held to maturity or available for sale. Investments in debt securities that the Corporation has the positive intent and the ability to hold to maturity are classified as held to maturity securities and reported at amortized cost. All other securities are classified as available for sale securities and reported at fair value, with unrecognized holding gains or losses reported in a separate component of stockholders’ equity. Securities in the available for sale category may be held for indefinite periods of time and include securities that management intends to use as part of its Asset/Liability strategy or that may be sold in response to changes in interest rates, changes in prepayment risks, the need to provide liquidity, the need to increase regulatory capital or similar factors. Securities available for sale increased to $72.75 million at December 31, 2006, from $64.17 million at December 31, 2005, an increase of $8.6 million, or 13.4%. Securities held to maturity increased $1.4 million, or 3.6%, to $39.16 million at December 31, 2006 from $37.80 million at December 31, 2005.

During the fourth quarter of 2006, the Corporation completed an investment restructuring consisting of the sale of $17.3 million available for sale securities with yields of less than 5.0%. Proceeds from the sale were used to purchase higher yielding investments and to fund loan growth.

The following table sets forth the classification of the Corporation’s investment securities by major category at the end of the last three years:

| | | December 31, | |

| | | 2006 | | 2005 | | 2004 | |

| | | Carrying Value | | Percent | | Carrying Value | | Percent | | Carrying Value | | Percent | |

| | | (Dollars in thousands) | |

| | | | | | | | | | | | | | |

| Securities available for sale: | | | | | | | | | | | | | |

| | | | | | | | | | | | | | |

| U.S. Treasury | | $ | — | | | 0.0 | % | $ | 496 | | | 0.8 | % | $ | 495 | | | 0.9 | % |

| U.S. government-sponsored agencies | | | 32,117 | | | 44.2 | % | | 32,478 | | | 50.6 | % | | 23,344 | | | 41.3 | % |

| Obligations of state and political subdivisions | | | 1,823 | | | 2.5 | % | | 2,031 | | | 3.2 | % | | 1,915 | | | 3.4 | % |

| Mortgage-backed securities | | | 37,707 | | | 51.8 | % | | 28,110 | | | 43.8 | % | | 29,730 | | | 52.6 | % |

| Community Reinvestment Act Fund | | | 1,099 | | | 1.5 | % | | 1,051 | | | 1.6 | % | | 1,030 | | | 1.8 | % |

| | | | | | | | | | | | | | | | | | | | |

| Total | | $ | 72,746 | | | 100.0 | % | $ | 64,166 | | | 100.0 | % | $ | 56,514 | | | 100.0 | % |

| | | | | | | | | | | | | | | | | | | | |

| Securities held to maturity: | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | |

| U.S. Treasury | | $ | 502 | | | 1.3 | % | $ | 1,004 | | | 2.7 | % | $ | 1,007 | | | 2.5 | % |

| U.S. government- sponsored agencies | | | 10,776 | | | 27.5 | % | | 12,113 | | | 32.0 | % | | 8,655 | | | 21.6 | % |

| Obligations of state and political subdivisions | | | 20,516 | | | 52.4 | % | | 15,747 | | | 41.7 | % | | 17,688 | | | 44.1 | % |

| Mortgage-backed securities | | | 7,369 | | | 18.8 | % | | 8,937 | | | 23.6 | % | | 12,761 | | | 31.8 | % |

| Total | | $ | 39,163 | | | 100.0 | % | $ | 37,801 | | | 100.0 | % | $ | 40,111 | | | 100.0 | % |

The following table sets forth the maturity distribution and weighted average yields (calculated on the basis of stated yields to maturity, considering applicable premium or discount) of the Corporation’s securities available for sale as of December 31, 2006. Issuers may have the right to call or prepay obligations with or without call or prepayment penalties. This might cause actual maturities to differ from contractual maturities.

| | | | | After 1 Year | | After 5 Years | | | | | |

| | | Within | | Through | | Through | | After | | | |

| | | 1 Year | | 5 Years | | 10 Years | | 10 Years | | Total | |

| | | (Dollars in thousands) | |

| | | | | | | | | | | | |

| U.S. government sponsored agencies : | | | | | | | | | | | |

| Carrying value | | $ | 4,180 | | $ | 11,375 | | $ | 8,384 | | $ | 8,178 | | $ | 32,117 | |

| Yield | | | 2.70 | % | | 4.83 | % | | 5.78 | % | | 5.89 | % | | 5.07 | % |

| Obligations of state and political subdivisions : | | | | | | | | | | | | | | | | |

| Carrying value | | | — | | | 1,331 | | | 143 | | | 349 | | | 1,823 | |

| Yield | | | — | | | 3.07 | % | | 3.75 | % | | 3.88 | % | | 3.28 | % |

| | | | | | | | | | | | | | | | | |

| Mortgage-backed securities : | | | | | | | | | | | | | | | | |

| Carrying value | | | 4 | | | 2,190 | | | 6,376 | | | 29,137 | | | 37,707 | |

| Yield | | | 8.00 | % | | 3.79 | % | | 4.41 | % | | 5.26 | % | | 5.03 | % |

| | | | | | | | | | | | | | | | | |

| Community Reinvestment Act Fund: | | | | | | | | | | | | | | | | |

| Carrying value | | | 1,099 | | | — | | | — | | | — | | | 1,099 | |

| Yield | | | 3.75 | % | | — | | | — | | | — | | | 3.75 | % |

| Total carrying value | | $ | 5,283 | | $ | 14,896 | | $ | 14,903 | | $ | 37,664 | | $ | 72,746 | |

| Weighted average yield | | | 2.92 | % | | 4.52 | % | | 5.17 | % | | 5.38 | % | | 4.99 | % |

The following table sets forth the maturity distribution and weighted average yields (calculated on the basis of stated yields to maturity, considering applicable premium or discount) of the Corporation’s securities held to maturity as of December 31, 2006. Issuers may have the right to call or prepay obligations with or without call or prepayment penalties. This might cause actual maturities to differ from contractual maturities.

| | | | | After 1 Year | | After 5 Years | | | | | |

| | | Within | | Through | | Through | | After | | | |

| | | 1 Year | | 5 Years | | 10 Years | | 10 Years | | Total | |

| | | (Dollars in thousands) | |

| | | | | | | | | | | | |

| U.S. Treasury : | | | | | | | | | | | |

| Carrying value | | $ | — | | $ | 502 | | $ | — | | $ | — | | $ | 502 | |

| Yield | | | — | | | 4.57 | % | | — | | | — | | | 4.57 | % |

| | | | | | | | | | | | | | | | | |

| U.S. government-sponsored agencies : | | | | | | | | | | | | | | | | |

| Carrying value. | | | 1,455 | | | 5,091 | | | 2,748 | | | 1,482 | | | 10,776 | |

| Yield | | | 2.90 | % | | 4.67 | % | | 5.91 | % | | 5.83 | % | | 4.91 | % |

| | | | | | | | | | | | | | | | | |

| Obligations of state and political subdivisions : | | | | | | | | | | | | | | | | |

| Carrying value | | | 4,596 | | | 4,475 | | | 6,499 | | | 4,946 | | | 20,516 | |

| Yield | | | 3.18 | % | | 2.99 | % | | 3.76 | % | | 3.82 | % | | 3.48 | % |

| | | | | | | | | | | | | | | | | |

| Mortgage-backed securities : | | | | | | | | | | | | | | | | |

| Carrying value | | | 20 | | | 698 | | | 1,725 | | | 4,926 | | | 7,369 | |

| Yield | | | 5.34 | % | | 4.38 | % | | 5.19 | % | | 5.20 | % | | 5.12 | % |

| | | | | | | | | | | | | | | | | |

| Total carrying value | | $ | 6,071 | | $ | 10,766 | | $ | 10,972 | | $ | 11,354 | | $ | 39,163 | |

| | | | | | | | | | | | | | | | | |

| Weighted average yield | | | 3.12 | % | | 3.95 | % | | 4.52 | % | | 4.68 | % | | 4.19 | % |

Deposits

Corporation deposits at December 31, 2006 totaled $434.22 million, an increase of $30.8 million, or 7.6%, over the comparable period of 2005, when deposits totaled $403.47 million. The Corporation relied on its existing market area and current competitive products and services to provide growth during 2006. The economic and interest rate environment made it difficult to attract core deposits. In addition, the Corporation utilized the brokered certificate of deposit market with $19.67 million included in the time deposit balances as of December 31, 2006.

The following table sets forth the classification of the Corporation’s deposits by major category as of December 31 of each of the three preceding years:

| | | December 31, | |

| | | 2006 | | 2005 | | 2004 | |

| | | Amount | | Percent | | Amount | | Percent | | Amount | | Percent | |

| | | (Dollars in thousands) | |

| Noninterest-bearing demand | | $ | 92,105 | | | 21.2 | % | $ | 94,331 | | | 23.4 | % | $ | 90,635 | | | 25.4 | % |

| Interest-bearing demand | | | 120,899 | | | 27.8 | % | | 122,867 | | | 30.5 | % | | 124,161 | | | 34.8 | % |

| Saving deposits | | | 37,324 | | | 8.6 | % | | 45,779 | | | 11.3 | % | | 49,967 | | | 14.0 | % |

| Certificates of deposit | | | 183,895 | | | 42.4 | % | | 140,489 | | | 34.8 | % | | 91,967 | | | 25.8 | % |

| Total | | $ | 434,223 | | | 100.0 | % | $ | 403,466 | | | 100.0 | % | $ | 356,730 | | | 100.0 | % |

As of December 31, 2006, the aggregate amount of outstanding time deposits issued in amounts of $100,000 or more, broken down by time remaining to maturity, was as follows (In thousands):

| Three months or less | | $ | 14,402 | |

| Four months through six months | | | 11,536 | |

| Seven months through twelve months | | | 29,021 | |

| Over twelve months | | | 14,943 | |

| Total | | $ | 69,902 | |

Market Risk

Market risk is the risk of loss from adverse changes in market prices and rates. The Corporation’s market risk arises primarily from interest rate risk inherent in its lending and deposit taking activities. Management actively monitors and manages its interest rate risk exposure.

The Corporation’s profitability is affected by fluctuations in interest rates. A sudden and substantial increase or decrease in interest rates may adversely impact the Corporation’s earnings to the extent that the interest rates borne by assets and liabilities do not change at the same speed, to the same extent, or on the same basis. The Corporation monitors the impact of changes in interest rates on its net interest income using several tools. One measure of the Corporation’s exposure to differential changes in interest rates between assets and liabilities is shown in the Corporation’s Maturity and Repricing Analysis under the Interest Rate Sensitivity caption below.

The Corporation’s primary objective in managing interest rate risk is to minimize the adverse impact of changes in interest rates on the Corporation’s net interest income and capital, while maintaining the asset-liability structure to obtain the maximum yield- cost spread on that structure. The Corporation relies primarily on its asset-liability structure to control interest rate risk.

The Corporation continually evaluates interest rate risk management opportunities, including the use of derivative financial instruments. Management believes that hedging instruments currently available are not cost effective, and therefore, has focused its efforts on increasing the Corporation’s yield-cost spread through retail growth opportunities.

The following table shows the Corporation’s financial instruments that are sensitive to changes in interest rates, categorized by expected maturity, and the instruments’ fair values at December 31, 2006. Market rate sensitive instruments are generally defined as on and off balance sheet derivatives and other financial instruments. Expected maturities are contractual maturities adjusted for projected payments of principal. The actual maturities of these instruments could vary substantially if future prepayments differ from the projections. For non-maturity deposit liabilities, in accordance with standard industry practice, “decay factors” were used to estimate deposit runoff.

| | | Average Interest Rate | | 2007 | | 2008 | | 2009 | | 2010 | | 2011 | | Thereafter | | Balance | | Fair Value | |

| | | (Dollars in thousands) | |

Interest-Sensitive Assets: | | | | | | | | | | | | | | | | | | | |

| Interest-bearing due from banks. | | | 4.92 | % | $ | 836 | | $ | — | | $ | — | | $ | — | | $ | — | | $ | — | | $ | 836 | | $ | 836 | |

| Loans: | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Real estate mortgage | | | 6.82 | % | | 49,339 | | | 11,982 | | | 10,115 | | | 8,656 | | | 8,982 | | | 135,357 | | | 224,431 | | | 223,165 | |

| Commercial | | | 8.42 | % | | 39,263 | | | 12,091 | | | 8,297 | | | 4,951 | | | 4,194 | | | 3,810 | | | 72,606 | | | 72,507 | |

| Consumer | | | 6.68 | % | | 7,462 | | | 6,443 | | | 6,311 | | | 6,525 | | | 6,055 | | | 40,163 | | | 72,959 | | | 70,924 | |

| Mortgage loans held for sale | | | 6.12 | % | | 2,155 | | | — | | | — | | | — | | | — | | | — | | | 2,155 | | | 2,155 | |

| Investment securities (1) | | | 4.63 | % | | 41,458 | | | 15,606 | | | 12,368 | | | 7,570 | | | 8,647 | | | 28,159 | | | 113,808 | | | 113,526 | |

| | | | 6.52 | % | | 140,513 | | | 46,122 | | | 37,091 | | | 27,702 | | | 27,878 | | | 207,489 | | | 486,795 | | | 483,113 | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Interest-Sensitive Liabilities: | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Savings | | | 0.74 | % | | 3,969 | | | 2,739 | | | 2,315 | | | 1,998 | | | 1,747 | | | 24,556 | | | 37,324 | | | 37,324 | |

| Interest-bearing | | | 2.09 | % | | 12,945 | | | 8,639 | | | 7,040 | | | 5,817 | | | 4,887 | | | 81,571 | | | 120,899 | | | 120,899 | |

| Time deposits | | | 4.47 | % | | 142,138 | | | 25,129 | | | 6,490 | | | 9,202 | | | 780 | | | 156 | | | 183,895 | | | 183,987 | |

| Securites sold under agreement to repurchase | | | 5.28 | % | | 9,023 | | | — | | | — | | | — | | | — | | | — | | | 9,023 | | | 9,023 | |

| FHLB borrowings | | | 4.53 | % | | 15,054 | | | 675 | | | 698 | | | 721 | | | 744 | | | 10,000 | | | 27,892 | | | 26,655 | |

| Subordinated debentures | | | 6.75 | % | | — | | | — | | | — | | | — | | | — | | | 7,217 | | | 7,217 | | | 7,436 | |

| | | | 3.43 | % | | 183,129 | | | 37,182 | | | 16,543 | | | 17,738 | | | 8,158 | | | 123,500 | | | 386,250 | | | 385,324 | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Net Interest-Sensitive Assets (Liabilities) | | | | | $ | (42,616 | ) | $ | 8,940 | | $ | 20,548 | | $ | 9,964 | | $ | 19,720 | | $ | 83,989 | | $ | 100,545 | | $ | 97,789 | |

| (1) | Includes securities held to maturity, securities available for sale and FHLB-NY stock. |

Interest Rate Sensitivity

Interest rate movements and deregulation of interest rates have made managing the Corporation’s interest rate sensitivity increasingly important. The Corporation attempts to maintain stable net interest margins by generally matching the volume of assets and liabilities maturing, or subject to repricing, by adjusting interest rates to market conditions, and by developing new products. One method of measuring the Corporation’s exposure to changes in interest rates is the maturity and repricing gap analysis. The difference between the volume of assets and liabilities that reprice in a given period is the interest sensitivity gap. A “positive” gap results when more assets than liabilities mature or are repricing in a given time frame. Conversely, a “negative” gap results when there are more liabilities than assets maturing or repricing in a given period of time. The smaller the gap, the less the effect of the market volatility on net interest income. During a period of rising interest rates, an institution with a negative gap position would not be in as favorable a position, as compared to an institution with a positive gap, to invest in higher yielding assets. This may result in yields on its assets increasing at a slower rate than the increase in its costs of interest-bearing liabilities than if it had a positive gap. During a period of falling interest rates, an institution with a negative gap would experience a repricing of its assets at a slower rate than its interest-bearing liabilities, which consequently may result in its net interest income growing at a faster rate than an institution with a positive gap position.

The following tables sets forth estimated maturity/repricing structure of the Corporation’s interest-earning assets and interest- bearing liabilities as of December 31, 2006. The amounts of assets or liabilities shown which reprice or mature during a particular period were determined in accordance with the contractual terms of each asset or liability and adjusted for prepayment assumptions where applicable. The table does not necessarily indicate the impact of general interest rate movements on the Corporation’s net interest income because the repricing of certain categories of assets and liabilities, for example, prepayments of loans and withdrawal of deposits, is beyond the Corporation’s control. As a result, certain assets and liabilities indicated as repricing within a period may in fact reprice at different times and at different rate levels.

| | | Three Months or Less | | More than Three Months Through One Year | | After One Year | | Noninterest Sensitive | | Total | |

| | | (Dollars in thousands) | |

| | | | | | | | | | | | |

Assets: | | | | | | | | | | | |

| Loans: | | | | | | | | | | | |

| Real estate mortgage | | $ | 17,064 | | $ | 39,850 | | $ | 167,517 | | $ | — | | $ | 224,431 | |

| Commercial | | | 11,931 | | | 28,279 | | | 32,396 | | | — | | | 72,606 | |

| Consumer | | | 21,334 | | | 5,097 | | | 46,528 | | | — | | | 72,959 | |

| Mortgage loans held for sale | | | 2,155 | | | — | | | — | | | — | | | 2,155 | |

| Investment securities (1) | | | 21,703 | | | 22,442 | | | 69,663 | | | — | | | 113,808 | |

| Other assets | | | 836 | | | — | | | — | | | 32,954 | | | 33,790 | |

| Total assets | | $ | 75,023 | | $ | 95,668 | | $ | 316,104 | | $ | 32,954 | | $ | 519,749 | |

| | | | | | | | | | | | | | | | | |

Source of funds: | | | | | | | | | | | | | | | | |

| Savings | | $ | — | | $ | 37,324 | | $ | — | | $ | — | | $ | 37,324 | |

| Interest-bearing | | | 120,899 | | | — | | | — | | | | | | 120,899 | |

| Certificates of deposit | | | 32,747 | | | 109,604 | | | 41,544 | | | — | | | 183,895 | |

| Repurchase agreements | | | 8,277 | | | 746 | | | — | | | — | | | 9,023 | |

| Borrowings | | | 14,561 | | | 492 | | | 12,839 | | | — | | | 27,892 | |

| Subordinated debenture | | | — | | | — | | | 7,217 | | | — | | | 7,217 | |

| Other liabilities | | | — | | | — | | | — | | | 96,193 | | | 96,193 | |

| Stockholders’ equity | | | — | | | — | | | — | | | 37,306 | | | 37,306 | |

| Total source of funds | | $ | 176,484 | | $ | 148,166 | | $ | 61,600 | | $ | 133,499 | | $ | 519,749 | |

| Interest rate sensitivity gap | | $ | (101,461 | ) | $ | (52,498 | ) | $ | 254,504 | | $ | (100,545 | ) | | | |

| Cumulative interest rate sensitivity gap | | $ | (101,461 | ) | $ | (153,959 | ) | $ | 100,545 | | $ | — | | | | |

| Ratio of GAP to total assets | | | -19.5 | % | | -10.1 | % | | 49.0 | % | | -19.4 | % | | | |

| Ratio of cumulative GAP assets to total assets | | | - 19.5 | % | | -29.6 | % | | 19.4 | % | | — | | | | |

______________________________________

| (1) | Includes securities held to maturity, securities available for sale and FHLB-NY stock. |

The Corporation also uses a simulation model to analyze the sensitivity of net interest income to movements in interest rates. The simulation model projects net interest income, net income, net interest margin, and capital to asset ratios based on various interest rate scenarios over a twelve month period. The model is based on the actual maturity and repricing characteristics of all rate sensitive assets and liabilities. Management incorporates into the model certain assumptions regarding prepayments of certain assets and liabilities. The model assumes an immediate rate shock to interest rates without management’s ability to proactively change the mix of assets or liabilities. According to the reports generated for year end 2006, an immediate interest rate increase of 200 basis points resulted in a decrease in net interest income of 12.1%, or $2.5 million, while an immediate interest rate decrease of 200 basis points resulted in an increase in net interest income of 2.9% or $614,000. Management has a goal to maintain a percentage change of no more than 15% given a 200 basis point change in interest rates. Management cannot provide any assurance about the actual effect of changes in interest rates on the Corporation’s net interest income. Assumptions have been built into the model for prepayments for assets and decay rates for nonmaturity deposits such as savings and interest bearing demand.

Liquidity

The Corporation’s primary sources of funds are deposits, amortization and prepayments of loans and mortgage-backed securities, maturities of investment securities and funds provided by operations. While scheduled loan and mortgage-backed securities amortization and maturities of investment securities are a relatively predictable source of funds, deposit flow and prepayments on loan and mortgage-backed securities are greatly influenced by market interest rates, economic conditions, and competition.

The Corporation’s liquidity, represented by cash and cash equivalents, is a product of its operating, investing and financing activities. These activities are summarized below:

| | | Years Ended December 31, | |

| | | 2006 | | 2005 | | 2004 | |

| | | (In thousands) | |

| | | | | | | | |

| Cash and cash equivalents - beginning | | $ | 14,028 | | $ | 24,792 | | $ | 19,138 | |

| Operating activities: | | | | | | | | | | |

| Net income | | | 4,753 | | | 4,480 | | | 3,848 | |

| Adjustments to reconcile net income to net cash provided by operating activities | | | (70 | ) | | (921 | ) | | 2,010 | |

| Net cash provided by operating activities | | | 4,683 | | | 3,559 | | | 5,858 | |

| Net cash used in investing activities | | | (34,261 | ) | | (68,436 | ) | | (19,182 | ) |

| Net cash provided by financing activities | | | 31,247 | | | 54,113 | | | 18,978 | |

| Net increase (decrease) in cash and cash equivalents | | | 1,669 | | | (10,764 | ) | | 5,654 | |

| Cash and cash equivalents - ending | | $ | 15,697 | | $ | 14,028 | | $ | 24,792 | |

Cash was generated by operating activities in each of the above periods. The primary source of cash from operating activities during each period was net income.

Liquidity management is both a daily and long-term function of business management. Excess liquidity is generally invested in short-term investments, such as federal funds sold.

The Corporation enters into commitments to extend credit, such as letters of credit, which are not reflected in the consolidated financial statements.

The Corporation has various contractual obligations that may require future cash payments. The following table summarizes the Corporation’s contractual obligations at December 31, 2006 and the effect of such obligations is expected to have on our liquidity and cash flows in future periods

| | | Total | | Less than 1 Year | | 1-3 Years | | 4-5 Years | | After 5 Years | |

| | | (In thousands) | |

| | | | | | | | | | | | |

| Contractual obligations | | | | | | | | | | | |

| Operating lease obligations | | $ | 5,058 | | $ | 545 | | $ | 1,099 | | $ | 997 | | $ | 2,417 | |

| Total contracted cost obligations | | $ | 5,058 | | $ | 545 | | $ | 1,099 | | $ | 997 | | $ | 2,417 | |

| | | | | | | | | | | | | | | | | |

| Other long-term liabilities/long-term debt | | | | | | | | | | | | | | | | |

| Time deposits | | $ | 183,895 | | $ | 142,351 | | $ | 31,587 | | $ | 9,957 | | $ | - | |

| Federal Home Loan Bank advances | | | 27,892 | | | 14,400 | | | 3,492 | | | - | | | 10,000 | |

| Subordinated debentures | | | 7,217 | | | - | | | - | | | - | | | 7,217 | |

| Total other long-term liabilities/long-term debt | | $ | 219,004 | | $ | 156,751 | | $ | 35,079 | | $ | 9,957 | | $ | 17,217 | |

| | | | | | | | | | | | | | | | | |

| Other commitments - off balance sheet | | | | | | | | | | | | | | | | |

| Letter of credit | | $ | 3,126 | | $ | 2,248 | | $ | 861 | | $ | 17 | | $ | - | |

| | | | | | | | | | | | | | | | | |

| Other commitments - off balance sheet | | | 11,459 | | | 11,459 | | | - | | | - | | | - | |

| Unused lines of credit | | | 83,387 | | | 83,387 | | | - | | | - | | | - | |

| Total off balance sheet arrangements and contractual obligations | | $ | 97,972 | | $ | 97,094 | | $ | 861 | | $ | 17 | | $ | - | |

For further information, see Note 16 of Notes to Consolidated Financial Statements.

Management believes that a significant portion of the time deposits will remain with the Corporation. In addition, management does not believe that all of the unused lines of credit will be exercised. The Corporation anticipates that it will have sufficient funds available to meet its current contractual commitments. Should the Corporation need temporary funding, the Corporation has an overnight line of credit with the FHLB-NY for a maximum of $47.1 million.

Capital

Banks and bank holding companies are subject to regulatory capital requirements administered by federal banking agencies. Capital adequacy guidelines and, additionally for banks, prompt corrective action regulations, involve quantitative measures of assets, liabilities, and certain off-balance-sheet items calculated under regulatory accounting practices. Capital amounts and classifications are also subject to qualitative judgments by regulators. Failure to meet capital requirements can initiate regulatory action. Regulations of the Board of Governors of the Federal Reserve System (“FRB”) require bank holding companies to maintain minimum levels of regulatory capital. Under the regulations in effect at December 31, 2006, the Corporation was required to maintain (i) a minimum leverage ratio of Tier 1 capital to total adjusted assets of 4.0% and (ii) minimum ratios of Tier 1 and total capital to risk-weighted assets of 4.0% and 8.0%, respectively. The Bank must comply with substantially similar capital regulations promulgated by the FDIC. The following table summarizes the capital ratios for the Corporation and the Bank at December 31, 2006.

| | | Required | | Actual | | Excess | |

| Risk-based capital: | | | | | | | |

| Tier 1 | | | | | | | |

| Corporation | | | 4.00 | % | | 11.25 | % | | 7.25 | % |

| Bank | | | 4.00 | % | | 10.01 | % | | 6.01 | % |

| Total | | | | | | | | | | |

| Corporation | | | 8.00 | % | | 12.28 | % | | 4.28 | % |

| Bank | | | 8.00 | % | | 11.04 | % | | 3.04 | % |

| Leverage ratio* | | | | | | | | | | |

| Corporation | | | 4.00 | % | | 8.85 | % | | 4.85 | % |

| Bank | | | 4.00 | % | | 7.91 | % | | 3.91 | % |

| * | The minimum leverage ratio set by the FRB and the FDIC is 3.00%. Institutions which are not “top-rated” will be expected to maintain a ratio of approximately 100 to 200 basis points above this ratio. |

REPORT OF INDEPENDENT REGISTERED PUBLIC ACCOUNTING FIRM

Board of Directors and Shareholders

Stewardship Financial Corporation

Midland Park, New Jersey: