Table of Contents

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

SCHEDULE 14A

(Rule 14a-101)

INFORMATION REQUIRED IN

PROXY STATEMENT

SCHEDULE 14A INFORMATION

Proxy Statement Pursuant to Section 14(a) of the

Securities Exchange Act of 1934

(Amendment No.)

Filed by the Registrant x Filed by a Party other than the Registrant ¨

| Check | the appropriate box: |

| x | Preliminary Proxy Statement |

| ¨ | Confidential, For Use of the Commission Only (as permitted by Rule 14a-6(e)(2)) |

| ¨ | Definitive Proxy Statement |

| ¨ | Definitive Additional Materials |

| ¨ | Soliciting Material Pursuant to § 240.14a-12 |

W. P. Carey & Co. LLC and

Corporate Property Associates 15 Incorporated

(Name of Registrant as Specified in Its Charter)

(Name of Person(s) Filing Proxy Statement, if Other Than the Registrant)

Payment of Filing Fee (Check the appropriate box):

| ¨ | No fee required. |

| x | Fee computed on table below per Exchange Act Rules 14a-6(i)(1) and 0-11. |

| (1) | Title of each class of securities to which transaction applies: |

| (2) | Aggregate number of securities to which transaction applies: |

| (3) | Per unit price or other underlying value of transaction computed pursuant to Exchange Act Rule 0-11 (set forth the amount on which the filing fee is calculated and state how it was determined): |

| (4) | Proposed maximum aggregate value of transaction: $2,512,335,179 |

| (5) | Total fee paid: $287,915 |

| ¨ | Fee paid previously with preliminary materials: |

| x | Check box if any part of the fee is offset as provided by Exchange Act Rule 0-11(a)(2) and identify the filing for which the offsetting fee was paid previously. Identify the previous filing by registration statement number, or the Form or Schedule and the date of its filing. |

| (1) | Amount previously paid: $287,915 |

| (2) | Form, Schedule or Registration Statement No.: Form S-4, File No. 333-180328 |

| (3) | Filing Party: W. P. Carey Inc. |

| (4) | Date Filed: March 23, 2012 |

Table of Contents

The information in this joint proxy statement/prospectus is not complete and may be changed. A registration statement relating to these securities has been filed with the Securities and Exchange Commission. These securities may not be sold nor may offers to buy be accepted until the Registration Statement is effective. This joint proxy statement/prospectus is not an offer to sell or exchange these securities and it is not soliciting an offer to buy these securities in any state where the offer or sale is not permitted.

SUBJECT TO COMPLETION, DATED JULY 27, 2012

PRELIMINARY JOINT PROXY STATEMENT/PROSPECTUS

|  |

YOUR VOTE IS VERY IMPORTANT

Dear W. P. Carey Shareholders and CPA®:15 Stockholders:

W. P. Carey & Co. LLC (“W. P. Carey”) and Corporate Property Associates 15 Incorporated (“CPA®:15”) are proposing a combination of their companies by a merger and related transactions, which we refer to collectively as the “Merger,” pursuant to a definitive agreement and plan of merger dated as of February 17, 2012, which we refer to as the “Merger Agreement.” In the Merger, each holder of CPA®:15 common stock issued and outstanding immediately prior to the effective time of the Merger will receive for each share of CPA®:15 common stock consideration consisting of: (i) $1.25 in cash and (ii) 0.2326 shares of W. P. Carey Inc. (as defined below) common stock (the “Merger Consideration”). Based on the number of shares of CPA®:15 common stock outstanding on July 23, 2012, the record date for CPA®:15’s special meeting of stockholders, W. P. Carey Inc. expects to issue approximately 28,190,000 shares of W. P. Carey Inc. common stock in connection with the Merger. Based on the closing price of $46.08 per W. P. Carey listed share on the New York Stock Exchange (“NYSE”) on July 23, 2012, the last practicable date before the printing of this joint proxy statement/prospectus, the Merger Consideration has a total value of approximately $11.97 per share of CPA®:15 common stock. We anticipate that the common stock of W. P. Carey Inc. issued in the Merger will be listed on the NYSE at the time of issuance under the symbol “WPC.”Due to the fixed stock component of the Merger Consideration, the value of the Merger Consideration will fluctuate with changes in the market price of W. P. Carey’s listed shares. We urge you to obtain current market quotations of W. P. Carey’s listed shares.

In addition, the board of directors of W. P. Carey has unanimously approved a plan to reorganize the business operations of W. P. Carey to allow W. P. Carey to qualify as a real estate investment trust (“REIT”) for federal income tax purposes. The conversion of W. P. Carey to a REIT will be implemented through a series of reorganizations and transactions (the “REIT Conversion”), including, among other things (i) certain mergers of W. P. Carey subsidiaries with and into W. P. Carey Inc., a wholly-owned subsidiary of W. P. Carey (“W. P. Carey Inc.”), (ii) the merger of W. P. Carey with and into W. P. Carey Inc., with W. P. Carey Inc. surviving the merger (the “W. P. Carey Merger”) pursuant to a definitive agreement and plan of merger dated as of February 17, 2012 between W. P. Carey and W. P. Carey Inc., which we refer to as the “REIT Conversion Agreement,” and (iii) the qualification by W. P. Carey Inc. as a REIT for federal income tax purposes. In the W. P. Carey Merger, W. P. Carey shareholders will receive one share of W. P. Carey Inc. common stock for each W. P. Carey listed share that they own. Based on the number of W. P. Carey listed shares and the number of shares of common stock of W. P. Carey’s subsidiaries outstanding on July 16, 2012, the record date for W. P. Carey’s special meeting of shareholders, W. P. Carey Inc. expects to issue approximately 40,365,000 shares of W. P. Carey Inc. common stock expected to be issued in connection with the REIT Conversion, for a total of approximately 68,555,000 shares of W. P. Carey Inc. common stock in connection with the Merger and the REIT Conversion.

The affirmative vote of the holders of a majority of the outstanding W. P. Carey listed shares and shares of CPA®:15 common stock entitled to vote is required for the approval of the Merger. The affirmative vote of the holders of a majority of the outstanding W. P. Carey listed shares entitled to vote is required for the adoption of the REIT Conversion Agreement and approval of the W. P. Carey Merger.

After careful consideration, the board of directors of W. P. Carey has unanimously declared both the Merger and the W. P. Carey Merger are advisable and recommends that all W. P. Carey shareholders vote “FOR” approval of the Merger and “FOR” adoption of the REIT Conversion Agreement and approval of the W. P. Carey Merger. After careful consideration, following the recommendation of a special committee of independent directors, the board of directors of CPA®:15 has unanimously declared that the Merger is advisable and recommends that all CPA®:15 stockholders vote “FOR” approval of the Merger.

Your vote is very important regardless of the number of shares you own. Whether or not you plan to attend the special meeting of shareholders of W. P. Carey or of stockholders of CPA®:15, please take the time to vote by completing, signing and mailing the enclosed proxy cards. If you do not vote, in the case of W. P. Carey, the effect will be the same as voting against approval of the Merger and against adoption of the REIT Conversion Agreement and approval of the W. P. Carey Merger, and in the case of CPA®:15, the effect will be the same as voting against approval of the Merger. In addition, failure to vote may result in W. P. Carey or CPA®:15 not having a sufficient quorum of a majority of its outstanding shares represented in person or by proxy at the meetings. A meeting cannot be held unless a quorum is present.

Each of W. P. Carey and CPA®:15 has scheduled a special meeting for its respective shareholders and stockholders to vote on the proposals described in this joint proxy statement/prospectus. The date, place and time of the meetings are as follows:

FOR W. P. CAREY SHAREHOLDERS: September 13, 2012, 5 p.m., Eastern Time at the offices of Clifford Chance US LLP, 31 West 52nd Street, 4th Floor Conference Center New York, NY 10019 | FOR CPA®:15 STOCKHOLDERS: September 13, 2012, 3 p.m., Eastern Time at the offices of Clifford Chance US LLP, 31 West 52nd Street, 4th Floor Conference Center New York, NY 10019 |

This joint proxy statement/prospectus is a prospectus of W. P. Carey Inc. as well as a proxy statement for W. P. Carey and CPA®:15 and provides you with detailed information about the Merger, the REIT Conversion and the special meetings.We encourage you to read carefully this entire joint proxy statement/prospectus, including all its annexes, and we especially encourage you to read the section entitled “Risk Factors” beginning on page 36.

NEITHER THE SECURITIES AND EXCHANGE COMMISSION NOR ANY STATE SECURITIES COMMISSION HAS APPROVED OR DISAPPROVED THE SHARES OF W. P. CAREY INC. COMMON STOCK TO BE ISSUED UNDER THIS JOINT PROXY STATEMENT/PROSPECTUS. ANY REPRESENTATION TO THE CONTRARY IS A CRIMINAL OFFENSE.

Sincerely,

| Trevor P. Bond | Richard J. Pinola | |

Chief Executive Officer | Director and Co-Chair of the Special Committee | |

W. P. Carey & Co. LLC | Corporate Property Associates 15 Incorporated |

This joint proxy statement/prospectus is dated[—], 2012 and is expected to be first mailed to holders of W. P. Carey listed shares and CPA®:15 common stock on or about[—], 2012.

Table of Contents

W. P. CAREY & CO. LLC

NOTICE OF SPECIAL MEETING OF SHAREHOLDERS TO BE HELD ON SEPTEMBER 13, 2012

To the shareholders of W. P. Carey & Co. LLC:

A special meeting of shareholders of W. P. Carey & Co. LLC (“W. P. Carey”) will be held on September 13, 2012, at 5 p.m. Eastern Time, at the offices of Clifford Chance US LLP, 31 West 52nd Street, 4th Floor Conference Center, New York, NY 10019 for the following purposes:

1. To consider and vote upon a proposal to approve the transactions described in the Agreement and Plan of Merger dated as of February 17, 2012 (the “Merger Agreement”) by and among Corporate Property Associates 15 Incorporated (“CPA®:15”), CPA®:15 Holdco, Inc., a wholly-owned subsidiary of CPA®:15 (“CPA®:15 Holdco”), W. P. Carey, W. P. Carey REIT, Inc. (now named W. P. Carey Inc.), a wholly-owned subsidiary of W. P. Carey (“W. P. Carey Inc.”), CPA®:15 Merger Sub Inc., an indirect subsidiary of W. P. Carey Inc. (“CPA®:15 Merger Sub”), and the other parties thereto. As contemplated by the Merger Agreement:

| • | CPA®:15 will merge with an indirect wholly-owned subsidiary of CPA®:15, with CPA®:15 surviving the merger as a wholly-owned subsidiary of CPA®:15 Holdco, and immediately thereafter, CPA®:15 Holdco will merge with and into CPA®:15 Merger Sub, with CPA®:15 Merger Sub surviving the merger as an indirect subsidiary of W. P. Carey Inc. and CPA®:15 becoming a direct subsidiary of CPA®:15 Merger Sub and an indirect subsidiary of W. P. Carey Inc. |

| • | Each issued and outstanding share of CPA®:15 common stock will be converted into one share of common stock of CPA®:15 Holdco, and immediately thereafter into the right to receive (i) $1.25 in cash and (ii) 0.2326 shares of W. P. Carey Inc. common stock (the “Merger Consideration”). |

| • | Based on the closing price of $46.08 per W. P. Carey listed share on the New York Stock Exchange on July 23, 2012, the last practicable date before the printing of this joint proxy statement/prospectus, the total Merger Consideration was valued at approximately $11.97 per share of CPA®:15 common stock. |

We refer to the transactions described above collectively as the “Merger.”

2. To consider and vote upon a proposal to adopt the Agreement and Plan of Merger dated February 17, 2012 (the “REIT Conversion Agreement”) between W. P. Carey and W. P. Carey Inc., and approve the merger of W. P. Carey with and into W. P. Carey Inc., with W. P. Carey Inc. surviving the merger (the “W. P. Carey Merger”), pursuant to the REIT Conversion Agreement, as part of the conversion of W. P. Carey to a real estate investment trust for federal income tax purposes through a series of reorganizations and transactions, including the W. P. Carey Merger (the “REIT Conversion”). In the W. P. Carey Merger, W. P. Carey shareholders will receive one share of W. P. Carey Inc. common stock for each W. P. Carey listed share that they own.

3. To transact such other business as may properly come before W. P. Carey’s special meeting or any adjournments or postponements of the special meeting, including, without limitation, a motion to adjourn the special meeting to another time for the purpose of soliciting additional proxies to approve the proposals above.

AT A MEETING ON FEBRUARY 17, 2012, W. P. CAREY’S BOARD OF DIRECTORS UNANIMOUSLY ADOPTED A RESOLUTION DECLARING THAT BOTH THE MERGER AND THE W. P. CAREY MERGER ARE ADVISABLE AND UNANIMOUSLY RECOMMENDS THAT YOU VOTE FOR THE APPROVAL OF THE MERGER AND FOR THE ADOPTION OF THE REIT CONVERSION AGREEMENT AND APPROVAL OF THE W. P. CAREY MERGER.

The Merger and the Merger Agreement and the W. P. Carey Merger and the REIT Conversion Agreement are each described in more detail in the accompanying joint proxy statement/prospectus, which you should read

Table of Contents

in its entirety before authorizing a proxy to vote. Copies of the Merger Agreement and the REIT Conversion Agreement are attached as Annexes A and B, respectively, to the accompanying joint proxy statement/prospectus. If you do not vote, the effect will be the same as voting against approval of the Merger and against adoption of the REIT Conversion Agreement and approval of the W. P. Carey Merger.

Only those shareholders whose names appear in W. P. Carey’s records as owning W. P. Carey listed shares at the close of business on July 16, 2012, referred to as the W. P. Carey record date, are entitled to notice of, and to vote at, W. P. Carey’s special meeting.

The affirmative vote of shareholders entitled to cast a majority of all the votes entitled to be cast by W. P. Carey shareholders on the matter on the W. P. Carey record date is necessary to approve the proposals relating to the approval of the Merger and the adoption of the REIT Conversion Agreement and the approval of the W. P. Carey Merger. If that vote is not obtained, the Merger and the W. P. Carey Merger cannot be completed.

All shareholders of W. P. Carey are cordially invited to attend W. P. Carey’s special meeting in person. To ensure your representation at W. P. Carey’s special meeting, you are urged to complete, sign and return the enclosed proxy card as promptly as possible in the enclosed postage-prepaid envelope or to authorize a proxy via telephone or Internet as instructed in the enclosed proxy card. You may revoke your proxy in the manner described in the accompanying joint proxy statement/prospectus at any time before it is voted at W. P. Carey’s special meeting.

By Order of the Board of Directors,

Susan C. Hyde

Managing Director and Secretary

New York, New York

July 27, 2012

Table of Contents

CORPORATE PROPERTY ASSOCIATES 15 INCORPORATED

NOTICE OF SPECIAL MEETING OF STOCKHOLDERS TO BE HELD ON SEPTEMBER 13, 2012

To the stockholders of Corporate Property Associates 15 Incorporated:

A special meeting of stockholders of Corporate Property Associates 15 Incorporated (“CPA®:15”) will be held on September 13, 2012, at 3 p.m. Eastern Time, at the offices of Clifford Chance US LLP, 31 West 52nd Street, 4th floor Conference Center, New York, NY 10019 for the following purposes:

1. To consider and vote upon a proposal to approve the transactions described in the Agreement and Plan of Merger dated as of February 17, 2012 (the “Merger Agreement”) by and among CPA®:15, CPA®:15 Holdco, Inc., a wholly-owned subsidiary of CPA®:15 (“CPA®:15 Holdco”), W. P. Carey & Co. LLC (“W. P. Carey”), W. P. Carey REIT, Inc. (now named W. P. Carey Inc.), a wholly-owned subsidiary of W. P. Carey (“W. P. Carey Inc.”), CPA®:15 Merger Sub Inc., an indirect subsidiary of W. P. Carey Inc. (“CPA®:15 Merger Sub”), and the other parties thereto. As contemplated by the Merger Agreement:

| • | CPA®:15 will merge with an indirect wholly-owned subsidiary of CPA®:15, with CPA®:15 surviving the merger as a wholly-owned subsidiary of CPA®:15 Holdco, and immediately thereafter, CPA®:15 Holdco will merge with and into CPA®:15 Merger Sub, with CPA®:15 Merger Sub surviving the merger as an indirect subsidiary of W. P. Carey Inc. and CPA®:15 becoming a direct subsidiary of CPA®:15 Merger Sub and an indirect subsidiary of W. P. Carey Inc. |

| • | Each issued and outstanding share of CPA®:15 common stock will be converted into one share of common stock of CPA®:15 Holdco, and immediately thereafter, into the right to receive (i) $1.25 in cash and (ii) 0.2326 shares of W. P. Carey Inc. common stock (the “Merger Consideration”). |

| • | Based on the closing price of $46.08 per W. P. Carey listed share on the New York Stock Exchange on July 23, 2012, the last practicable date before the printing of this joint proxy statement/prospectus, the total Merger Consideration was valued at approximately $11.97 per share of CPA®:15 common stock. |

We refer to the transactions described above collectively as the “Merger.”

2. To transact such other business as may properly come before CPA®:15’s special meeting or any adjournments or postponements of the special meeting, including, without limitation, a motion to adjourn the special meeting to another time for the purpose of soliciting additional proxies to approve the proposal above.

AT A MEETING ON FEBRUARY 17, 2012, CPA®:15’S BOARD OF DIRECTORS, AFTER RECEIVING THE RECOMMENDATION OF A SPECIAL COMMITTEE OF INDEPENDENT DIRECTORS OF CPA®:15’S BOARD OF DIRECTORS, UNANIMOUSLY ADOPTED A RESOLUTION DECLARING THAT THE MERGER IS ADVISABLE AND UNANIMOUSLY RECOMMENDS THAT YOU VOTE FOR THE APPROVAL OF THE MERGER.

The Merger Agreement and the proposed Merger are each described in more detail in the accompanying joint proxy statement/prospectus, which you should read in its entirety before authorizing a proxy to vote. A copy of the Merger Agreement is attached as Annex A to the accompanying joint proxy statement/prospectus. If you do not vote, the effect will be the same as voting against approval of the Merger.

Only those stockholders whose names appear in CPA®:15’s records as owning shares of CPA®:15 common stock at the close of business on July 23, 2012, referred to as the CPA®:15 record date, are entitled to notice of, and to vote at, CPA®:15’s special meeting.

The affirmative vote of stockholders entitled to cast a majority of all the votes entitled to be cast by holders of CPA®:15 common stock on the matter on the CPA®:15 record date is necessary to approve the Merger. If that

Table of Contents

vote is not obtained, the Merger cannot be completed. CPA®:15’s bylaws prohibit any of its directors or affiliates, including W. P. Carey, from voting their shares on any matters submitted to stockholders regarding any transaction between CPA®:15 and its advisor, or any of its directors or affiliates, including W. P. Carey; however, these shares are considered to be outstanding and eligible to vote for the purposes of determining whether the requisite stockholder approval has been obtained and therefore will have the effect of counting as votes against the Merger.

All stockholders of CPA®:15 are cordially invited to attend CPA®:15’s special meeting in person. To ensure your representation at CPA®:15’s special meeting, you are urged to complete, sign and return the enclosed proxy card as promptly as possible in the enclosed postage-prepaid envelope or to authorize a proxy via telephone or Internet as instructed in the enclosed proxy card. You may revoke your proxy in the manner described in the accompanying joint proxy statement/prospectus at any time before it is voted at CPA®:15’s special meeting.

By Order of the Board of Directors,

Susan C. Hyde

Managing Director and Secretary

New York, New York

July 27, 2012

Table of Contents

Table of Contents

ANNEXES

Table of Contents

GLOSSARY

In this joint proxy statement/prospectus, unless the context otherwise requires, when used herein, the following terms shall have the meanings set forth below.

| • | “Advisory Agreement” means the Amended and Restated Advisory Agreement, dated as of October 1, 2009, between CPA®:15 and CAM. |

| • | “AFFO” means FFO as modified to also exclude certain non-cash charges such as amortization of intangibles, deferred income tax benefits and expenses, straight-line rents, stock compensation, gains or losses from extinguishment of debt and deconsolidation of subsidiaries and unrealized foreign currency exchange gains and losses. See the section entitled “Prospective Financial Information.” |

| • | “Asset Management Agreement” means the Asset Management Agreement, dated as of July 1, 2008, between CPA®:15 and BV. |

| • | “BV” means W. P. Carey & Co. B.V., a private limited liability company organized in the Netherlands. |

| • | “CAM” means Carey Asset Management Corp., a Delaware corporation and a wholly-owned subsidiary of W. P. Carey. |

| • | “Carey Storage” means Carey Storage Management LLC, a Delaware limited liability company. |

| • | “combined company” refers to W. P. Carey Inc. after completion of the Merger. |

| • | “CPA®:14” means Corporate Property Associates 14 Incorporated, a Maryland corporation. |

| • | “CPA®:14/16 Merger” means the merger of CPA®:14 with a subsidiary of CPA®:16—Global. |

| • | “CPA®:15” means Corporate Property Associates 15 Incorporated, a Maryland corporation, and its subsidiaries. |

| • | “CPA®:15 Advisory Agreements” means the Advisory Agreement and the Asset Management Agreement. |

| • | “CPA®:15 Bylaws” means the amended and restated bylaws of CPA®:15. |

| • | “CPA®:15 Charter” means the charter of CPA®:15. |

| • | “CPA®:15 common stock” means, as the context requires, the common stock of CPA®:15 outstanding immediately prior to the effective time of the Merger and/or the common stock of CPA®:15 Holdco outstanding immediately prior to the effective time of the merger with and into CPA®:15 Merger Sub. |

| • | “CPA®:15 Holdco” means CPA®:15 Holdco, Inc., a Maryland corporation and a wholly-owned subsidiary of CPA®:15. |

| • | “CPA®:15 Merger Sub” means CPA®:15 Merger Sub Inc., a Maryland corporation and an indirect subsidiary of W. P. Carey Inc. |

| • | “CPA®:16—Global” means Corporate Property Associates 16—Global Incorporated, a Maryland corporation. |

| • | “CPA®:17—Global” means Corporate Property Associates 17—Global Incorporated, a Maryland corporation. |

| • | “CPA® REITs” means CPA®:15, CPA®:16—Global and CPA®:17—Global. |

| • | “CWI” means Carey Watermark Investors Incorporated, a Maryland corporation. |

Table of Contents

| • | “FFO” means the non-GAAP financial measure defined by NAREIT as net income or loss (as computed in accordance with GAAP) excluding: depreciation and amortization expense from real estate assets, impairment charges on real estate, gains or losses from sales of depreciated real estate assets and extraordinary items; however, FFO related to assets held for sale, sold or otherwise transferred and included in the results of discontinued operations are included. These adjustments also incorporate the pro rata share of unconsolidated subsidiaries. See the section entitled “Prospective Financial Information.” |

| • | “GAAP” means United States generally accepted accounting principles. |

| • | “Livho” means Livho, Inc., a Delaware corporation. |

| • | “Merger” means the combination of W. P. Carey and CPA®:15 accomplished by, collectively, the merger of an indirect, wholly-owned subsidiary of CPA®:15 with and into CPA®:15, with CPA®:15 surviving the merger as a wholly-owned subsidiary of CPA®:15 Holdco, and the merger immediately thereafter of CPA®:15 Holdco with and into CPA®:15 Merger Sub, with CPA®:15 Merger Sub surviving the merger as an indirect subsidiary of W. P. Carey Inc. and CPA®:15 becoming a direct subsidiary of CPA®:15 Merger Sub and an indirect subsidiary of W. P. Carey Inc. |

| • | “Merger Agreement” means the definitive Agreement and Plan of Merger dated as of February 17, 2012 by and among CPA®:15, CPA®:15 Holdco, CPA®:15 Merger Sub, W. P. Carey, W. P. Carey Inc. and, for the limited purposes set forth therein, CAM and BV. |

| • | “Merger Consideration” means the right of each share of CPA®:15 common stock to receive (i) $1.25 in cash and (ii) 0.2326 shares of W. P. Carey Inc. common stock. |

| • | “Merger Sub 2” means WPC REIT Merger Sub, a Maryland corporation and a wholly-owned subsidiary of WPC Holdco LLC, a disregarded limited liability company organized under the laws of Maryland and a wholly-owned subsidiary of W. P. Carey Inc. |

| • | “MFFO” means the NAREIT computation of FFO as modified in accordance with the guidelines and definition of MFFO of the Investment Program Association (the “IPA”), an industry trade group, and excludes acquisition-related expenses, amortization of above- and below-market leases, fair value adjustments or derivative financial instruments, deferred rent receivables and the adjustments of such items related to noncontrolling interests. See the section entitled “Prospective Financial Information.” |

| • | “NAREIT” means the National Association of Real Estate Investment Trusts. |

| • | “NAV” means net asset value. |

| • | “QRS” means a qualified REIT subsidiary. |

| • | “REIT” means a real estate investment trust. |

| • | “REIT Conversion” means the conversion of W. P. Carey to a REIT, implemented through a series of reorganizations and transactions, including, among other things, (i) certain mergers of W. P. Carey subsidiaries with and into W. P. Carey Inc., (ii) the W. P. Carey Merger, and (iii) the qualification by W. P. Carey Inc. as a REIT for federal income tax purposes. |

| • | “REIT Conversion Agreement” means the definitive Agreement and Plan of Merger dated as of February 17, 2012, by and between W. P. Carey and W. P. Carey Inc., whereby W. P. Carey will merge with and into W. P. Carey Inc., with W. P. Carey Inc. surviving the merger. |

| • | “TRS” means a taxable REIT subsidiary. |

| • | “W. P. Carey” means W. P. Carey & Co. LLC, a Delaware limited liability company. |

| • | “W. P. Carey Bylaws” means the amended and restated bylaws of W. P. Carey. |

| • | “W. P. Carey Inc.” means W. P. Carey Inc., a Maryland corporation formerly named W. P. Carey |

Table of Contents

REIT, Inc. and a wholly-owned subsidiary of W. P. Carey. |

| • | “W. P. Carey Inc. Bylaws” means the amended and restated bylaws of W. P. Carey Inc. |

| • | “W. P. Carey Inc. Charter” means the charter of W. P. Carey Inc., including W. P. Carey Inc.’s articles of amendment and restatement. |

| • | “W. P. Carey Inc. common stock” means the common stock, $0.001 par value per share, of W. P. Carey Inc. |

| • | “W. P. Carey LLC Agreement” means W. P. Carey’s Amended and Restated Limited Liability Company Agreement. |

| • | “W. P. Carey listed share” means each outstanding listed share of W. P. Carey. |

| • | “W. P. Carey Merger” means the merger of W. P. Carey with and into W. P. Carey Inc., with W. P. Carey Inc. surviving the merger. |

Table of Contents

QUESTIONS AND ANSWERS FOR W. P. CAREY SHAREHOLDERS AND CPA®:15 STOCKHOLDERS REGARDING THE MERGER AND THE SPECIAL MEETINGS

The following questions and answers for W. P. Carey shareholders and CPA®:15 stockholders briefly address some frequently asked questions about the Merger and the special meetings of shareholders of W. P. Carey and of stockholders of CPA®:15. They may not include all the information that is important to you. We urge you to read carefully this entire joint proxy statement/prospectus, including the annexes.

| Q. | What are we planning to do? |

| A. | W. P. Carey and CPA®:15 are proposing a combination of their companies through the Merger. In addition, W. P. Carey is proposing a plan to reorganize the business operations of W. P. Carey prior to the consummation of the Merger to allow W. P. Carey Inc. to qualify as a REIT for federal income tax purposes beginning with its 2012 taxable year. W. P. Carey expects the REIT election to be effective from February 15, 2012, the date of incorporation of W. P. Carey Inc. |

| Q. | What will holders of CPA®:15 common stock receive in connection with the Merger? When will they receive it? |

| A. | In the Merger, each issued and outstanding share of CPA®:15 common stock will be converted into one share of common stock of CPA®:15 Holdco, and immediately thereafter, into the right to receive total consideration valued at approximately $11.97 per share of CPA®:15 common stock (based on the closing price of $46.08 per W. P. Carey listed share on the New York Stock Exchange (the “NYSE”) on July 23, 2012, the last practicable date before the printing of this joint proxy statement/prospectus), and consisting of (i) $1.25 in cash and (ii) 0.2326 shares of W. P. Carey Inc. common stock. We anticipate that the shares of W. P. Carey Inc. common stock will trade on the NYSE under the symbol “WPC,” upon the consummation of the Merger. |

| Q. | How was the Merger Consideration determined? |

| A. | The Merger Consideration, including the stock component of 0.2326 shares of W. P. Carey Inc. common stock for one share of CPA®:15 common stock, was determined by the board of directors of W. P. Carey and a special committee of the board of directors of CPA®:15 following negotiations based in part upon (i) the historical market price of the W. P. Carey listed shares as quoted on the NYSE, and (ii) the estimated NAV per share for CPA®:15 of $10.40 as of September 30, 2011. The estimated NAV was determined on behalf of CPA®:15 by W. P. Carey, in its capacity as CPA®:15’s advisor, based in part upon a valuation of CPA®:15’s real estate portfolio as of September 30, 2011, as prepared by Robert A. Stanger & Co., Inc. (“Stanger”), a third-party valuation firm, with adjustments for indebtedness, cash and other items. |

| Q. | What is the expected ongoing rate of return of a CPA®:15 stockholder on his or her original investment? |

| A. | Each CPA®:15 stockholder currently receives $0.729 of annual distributions per share, which represents an annual rate of return of 7.35% on invested capital of $9.92 per share (an original investment of $10.00 per share of CPA®:15 common stock, less a special distribution of $0.08 per share on January 15, 2008). Following the Merger, CPA®:15 stockholders will be entitled to receive ongoing distributions paid by W. P. Carey Inc. Based on W. P. Carey Inc.’s anticipated annualized distribution rate of $2.60 per share following completion of the Merger, divided by the stock component of the Merger Consideration of 0.2326, each holder of CPA®:15 common stock is expected to receive $0.605 in distributions on the 0.2326 shares of W. P. Carey Inc. common stock received in exchange for each CPA®:15 share they own. This represents an annual rate of return of 6.98% on invested capital of $8.67 per share (an original investment of $10.00 per share of CPA®:15 common stock less the $0.08 per share special distribution on January 15, 2008 and the $1.25 of cash received as part of the Merger Consideration). |

1

Table of Contents

| Current | After the Merger | |||||||

| Invested Capital of $9.92 | Invested Capital of $8.67 | |||||||

Rate of Return on Invested Capital | 7.35 | % | 6.98 | % | ||||

On a NAV basis, CPA®:15’s current annual distribution of $0.729 per share represents an annual rate of return of 7.01% on the estimated NAV per share of CPA®:15 common stock of $10.40 as of September 30, 2011. W. P. Carey Inc.’s anticipated annualized distribution of $0.605 per share of W. P. Carey Inc. common stock (calculated as described above) represents an annual rate of return of 6.61% on the estimated NAV per share of CPA®:15 common stock of $9.15 (after deducting the $1.25 of cash received as part of the Merger Consideration) as of September 30, 2011.

| Current | After the Merger | |||||||

| Net Asset Value of $10.40 | Net Asset Value of $9.15 | |||||||

Rate of Return on Net Asset Value | 7.01 | % | 6.61 | % | ||||

Future distributions by W. P. Carey Inc. are not guaranteed and there can be no assurance of the future returns that CPA®:15 stockholders might receive as stockholders of W. P. Carey Inc. W. P. Carey Inc.’s anticipated distribution rate is based upon its current estimates of its annual REIT taxable income and its intention to qualify as a REIT. While W. P. Carey Inc. believes that its estimates are reasonable, they are subject to uncertainty and to factors outside of its control. See the “Risk Factors” section of this joint proxy statement/prospectus for a discussion of factors which may affect W. P. Carey Inc.’s payment of distributions. Pursuant to the terms of W. P. Carey’s amended and restated credit facility, following the completion of the REIT Conversion, W. P. Carey may make Restricted Payments (as such term is defined in the amended and restated credit facility) in an aggregate amount in any fiscal year not to exceed the greater of 95% of (i) the adjusted funds from operations, and (ii) the amount of Restricted Payments required to be paid in order to maintain its status as a REIT. There is a prohibition on W. P. Carey making Restricted Payments if the obligations under its amended and restated credit facility are declared immediately due and payable upon an event of default, as defined in the amended and restated credit facility. In addition, the ability of W. P. Carey to make Restricted Payments will be either automatically reduced to an amount required in order to maintain W. P. Carey’s status as a REIT, or prohibited, as the case may be, upon the occurrence of certain specified events of default.

| Q. | Are there any conditions to completion of the Merger? |

| A. | Yes. The Merger is subject to a number of conditions, including, among others, the following: |

| • | approval of the Merger by the requisite vote of the W. P. Carey shareholders and the CPA®:15 stockholders; |

| • | the registration statement, of which this joint proxy statement/prospectus forms a part, will have become effective and no stop order will have been issued or threatened by the Securities and Exchange Commission (the “SEC”) with regard to the registration statement and all necessary state securities or blue sky authorizations shall have been received; |

| • | no order, injunction or other legal restraint or prohibition preventing the consummation of the Merger will be in effect; |

| • | all consents and waivers from third parties will have been obtained or waived; |

| • | the closing of the REIT Conversion will have occurred; |

| • | the merger of CPA®:15 with and into an indirect wholly-owned subsidiary of CPA®:15 will have occurred; and |

| • | the shares of W. P. Carey Inc. common stock shall have been approved for listing on the NYSE. |

If any of these conditions or any of the other conditions specified in the Merger Agreement are not satisfied, the Merger may be abandoned by either W. P. Carey or CPA®:15.

2

Table of Contents

| Q. | Who will be the board of directors and management of the surviving entity after the Merger? |

| A. | The board of directors and executive management of W. P. Carey immediately prior to the Merger and the REIT Conversion will be the board of directors and executive management, respectively, of W. P. Carey Inc. |

| Q. | What fees will CPA®:15’s advisor receive in connection with the Merger? |

| A. | CAM and its affiliates serve as the advisor for CPA®:15. CAM and its affiliates will not receive any subordinated disposition or termination fees in connection with the Merger but will continue to receive all other accrued fees in the ordinary course of business until the closing of the Merger. |

| Q. | Will W. P. Carey or any of its subsidiaries receive any consideration for the shares of CPA®:15 common stock that they own? |

| A. | No. Each share of CPA®:15 common stock that is owned by W. P. Carey or any W. P. Carey subsidiary immediately prior to the effective time of the Merger will automatically be canceled and retired and cease to exist and neither W. P. Carey nor any W. P. Carey subsidiary will receive any Merger Consideration for those shares. |

| Q. | Will CPA®:15 and W. P. Carey continue to pay distributions prior to the effective time of the Merger? |

| A. | Yes. The Merger Agreement permits CPA®:15 to continue to pay a regular quarterly distribution and any distribution that is necessary for CPA®:15 to maintain its REIT qualification and to avoid other adverse tax consequences. W. P. Carey intends to continue to pay a regular quarterly distribution to its shareholders with respect to quarters completed prior to the Merger. |

| Q. | Will CPA®:15 stockholders who participated in CPA®:15’s distribution reinvestment and stock purchase plan immediately prior to its suspension, and who desire to participate in the distribution reinvestment and stock purchase plan of W. P. Carey Inc. following completion of the Merger, be able to continue to participate in such plan? |

| A. | CPA®:15 has suspended its distribution reinvestment and stock purchase plan (the “CPA®:15 DRIP”) because of the Merger. Each CPA®:15 stockholder who was a participant in the CPA®:15 DRIP immediately prior to its suspension and who desires to take part in the distribution reinvestment and stock purchase plan of W. P. Carey Inc. (the “W. P. Carey Inc. DRIP”) following completion of the Merger will automatically be enrolled in such plan. Each CPA®:15 stockholder who was a participant in the CPA®:15 DRIP but who does not desire to take part in the W. P. Carey Inc. DRIP should contact W. P. Carey’s investor relations department by calling 1-800-WPCAREY. Each CPA®:15 stockholder who desires to take part in the W. P. Carey Inc. DRIP but is not a participant in the CPA®:15 DRIP will be allowed to follow the procedures applicable to participation in the W. P. Carey Inc. DRIP. Such stockholders should contact W. P. Carey’s investor relations department by calling 1-800-WPCAREY. |

| Q. | When and where are the special meetings? |

| A. | The special meeting of W. P. Carey shareholders will be held on September 13, 2012, at 5 p.m., Eastern Time, at the offices of Clifford Chance US LLP, 31 West 52nd Street, 4th Floor Conference Center, New York, NY 10019. |

The special meeting of CPA®:15 stockholders will be held on September 13, 2012, at 3 p.m., Eastern Time, at the offices of Clifford Chance US LLP, 31 West 52nd Street, 4th Floor Conference Center, New York, NY 10019.

| Q. | What will I be voting on at the special meetings? |

| A. | W. P. Carey shareholders are requested to vote on two proposals: (i) to approve the Merger and (ii) to adopt the REIT Conversion Agreement and approve the W. P. Carey Merger. CPA®:15 stockholders are requested to vote on the proposal to approve the Merger. In addition, W. P. Carey shareholders and CPA®:15 |

3

Table of Contents

| stockholders are each requested to vote on the proposal to adjourn the special meetings of the respective entities, if necessary, to solicit additional proxies in the event that there are not sufficient votes at the time of the special meetings to approve the respective proposals. |

| Q. | Are the proposals being voted on at the special meetings conditioned on each other? |

| A. | The proposal for the W. P. Carey shareholders to approve the Merger is not conditioned upon the proposal for the W. P. Carey shareholders to adopt the REIT Conversion Agreement and approve the W. P. Carey Merger; however, CPA®:15’s obligations to consummate the Merger are subject to the completion of the REIT Conversion and the approval of the Merger by W. P. Carey’s shareholders. |

| Q. | Who can vote at the special meetings? |

| A. | If you are a shareholder of record of W. P. Carey at the close of business on July 16, 2012, or if you are a stockholder of record of CPA®:15 at the close of business on July 23, 2012, the record dates for W. P. Carey’s and CPA®:15’s special meetings, which we refer to as the W. P. Carey record date or the CPA®:15 record date, respectively, or the record date, you may vote the W. P. Carey listed shares and the shares of CPA®:15 common stock, as applicable, that you hold on the record date at each of the respective special meetings. |

| Q. | Why is my vote important? |

| A. | If you do not submit a proxy or vote in person at the meetings, it will be more difficult for us to obtain the necessary quorum to hold the special meetings. In addition, if you are a holder of W. P. Carey listed shares, your abstention or failure to submit a proxy or to vote in person will have the same effect as a vote against approval of the Merger and against adoption of the REIT Conversion Agreement and approval of the W. P. Carey Merger and if you are a holder of CPA®:15 common stock, your abstention or failure to submit a proxy or to vote in person will have the same effect as a vote against approval of the Merger. |

If you hold your W. P. Carey listed shares through a broker, bank, or other nominee, your broker, bank, or other nominee will not be able to cast a vote on the proposal to approve the Merger or the proposal to adopt the REIT Conversion Agreement and approve the W. P. Carey Merger without instructions from you and will have the same effect as a vote against such proposals.

| Q. | What constitutes a quorum for the special meetings? |

| A. | A majority of the outstanding W. P. Carey listed shares being present in person or represented by proxy constitutes a quorum for the W. P. Carey special meeting. A majority of the outstanding shares of CPA®:15 common stock being present in person or represented by proxy constitutes a quorum for the CPA®:15 special meeting. |

| Q. | What vote is required? |

| A. | The affirmative vote of the holders of a majority of the outstanding W. P. Carey listed shares entitled to vote is required to approve the Merger and to approve the adoption of the REIT Conversion Agreement and approve the W. P. Carey Merger. The affirmative vote of the holders of a majority of the outstanding shares of CPA®:15 common stock entitled to vote is required to approve the Merger. |

As of the close of business on the W. P. Carey record date and the CPA®:15 record date, respectively, there were 40,358,186 W. P. Carey listed shares and 131,598,907.515 shares of CPA®:15 common stock outstanding. Each outstanding W. P. Carey listed share and share of CPA®:15 common stock on the record date is entitled to one vote on each proposal submitted to you for consideration. The CPA®:15 Bylaws

4

Table of Contents

prohibit any of its directors or affiliates, including W. P. Carey, from voting their shares on any matters submitted to stockholders regarding any transaction between CPA®:15 and its advisor, or any of its directors or affiliates, including W. P. Carey; however, these shares are considered to be outstanding and eligible to vote for the purposes of determining whether the requisite stockholder approval has been obtained and therefore will have the effect of counting as votes against the Merger. As of the close of business on the CPA®:15 record date, CPA®:15’s directors and affiliates, including W. P. Carey and its subsidiaries, owned 10,418,731.366 shares of CPA®:15 common stock, or approximately 7.92% of the outstanding shares of CPA®:15 common stock.

| Q. | Is there a voting agreement relating to the Merger and the W. P. Carey Merger? |

| A. | On July 23, 2012, W. P. Carey and W. P. Carey Inc. entered into a Voting Agreement with the Estate of Wm. Polk Carey and W. P. Carey & Co., Inc., a wholly-owned corporation of the Estate, pursuant to which the Estate and W. P. Carey & Co., Inc. have agreed to vote any and all of the W. P. Carey listed shares that they beneficially own in favor of the approval of the W. P. Carey Merger and the Merger. As of June 30, 2012, the W. P. Carey listed shares beneficially owned by the Estate and W. P. Carey & Co., Inc. represented in the aggregate approximately 28.91% of the outstanding W. P. Carey listed shares. Mr. Wm. Polk Carey, who was the founder and Chairman of W. P. Carey, passed away on January 2, 2012. The Voting Agreement and other related documents are more fully described below in the section entitled “Certain Relationships and Related Transactions—Estate of Wm. Polk Carey.” |

| Q. | How do the boards of directors recommend I vote on the proposals? |

| A. | The board of directors of W. P. Carey believes that both the Merger and the W. P. Carey Merger are advisable and in the best interests of W. P. Carey and its shareholders.The W. P. Carey board of directors unanimously recommends that you vote “FOR” approval of the Merger and “FOR” adoption of the REIT Conversion Agreement and approval of the W. P. Carey Merger. |

The board of directors of CPA®:15 believes that the Merger is advisable and in the best interests of CPA®:15 and its stockholders.The board of directors of CPA®:15 unanimously recommends that you vote “FOR” approval of the Merger.

| Q. | When is the Merger expected to be completed? |

| A. | W. P. Carey and CPA®:15 expect to complete the Merger by the third quarter of 2012 or as soon as possible thereafter; however, there can be no assurance as to when, or if, the Merger will be completed. W. P. Carey and CPA®:15 reserve the right to abandon the Merger even if W. P. Carey shareholders and CPA®:15 stockholders vote to approve the Merger and other conditions to the completion of the Merger are satisfied or waived, if the boards of directors determine that the Merger is no longer in the best interests of W. P. Carey shareholders or CPA®:15 stockholders, respectively. |

| Q. | Are there risks associated with the Merger that I should consider in deciding how to vote? |

| A. | Yes. There are a number of risks related to the Merger that are discussed in this joint proxy statement/prospectus. In evaluating the Merger, you should read carefully the detailed description of the risks associated with the Merger described in the section entitled “Risk Factors” and other information included in this joint proxy statement/prospectus. |

| Q. | Will holders of W. P. Carey listed shares have to pay federal income taxes as a result of the Merger? |

| A. | No. Holders of W. P. Carey listed shares (who will become holders of W. P. Carey Inc. common stock in the REIT Conversion) are generally not expected to recognize gain in the Merger for federal income tax purposes. |

The federal income tax treatment of holders of W. P. Carey listed shares and W. P. Carey Inc. common stock depends in some instances on determinations of fact and interpretations of complex provisions of

5

Table of Contents

federal income tax law for which no clear precedent or authority may be available. In addition, the tax consequences to any particular shareholder will depend on that shareholder’s particular tax circumstances. We urge you to consult your tax advisor, particularly if you are a non-U.S. holder, regarding the specific tax consequences, including the federal, state, local, and foreign tax consequences, to you in light of your particular investment in, or the tax circumstances of acquiring, holding, exchanging or otherwise disposing of W. P. Carey Inc. common stock.

| Q. | Will holders of CPA®:15 common stock have to pay federal income taxes as a result of the Merger? |

| A. | Although holders of CPA®:15 common stock generally will not recognize gain in the Merger for federal income tax purposes with respect to their receipt of W. P. Carey Inc. common stock, they will recognize gain on their CPA®:15 common stock for federal income tax purposes up to the amount of cash that they receive in the Merger, which is $1.25 per share for each share of CPA®:15 common stock. In addition, a holder of CPA®:15 common stock who receives cash in lieu of a fractional share of W. P. Carey Inc. common stock in the Merger will generally be treated as having received the cash in redemption of the fractional share interest. Any gain or loss recognized by a holder of CPA®:15 common stock in the Merger will generally be treated as capital gain or loss. Any capital gain or loss recognized in connection with the Merger will be long-term capital gain or loss if a holder of CPA®:15 common stock has held the surrendered shares for more than one year. |

The federal income tax treatment of holders of CPA®:15 common stock in the Merger depends in some instances on determinations of fact and interpretations of complex provisions of federal income tax law for which no clear precedent or authority may be available. In addition, the tax consequences of participating in the Merger and of holding W. P. Carey Inc. common stock to any particular shareholder will depend on that shareholder’s particular tax circumstances. We urge you to consult your tax advisor, particularly if you are a non-U.S. holder, as defined in the section entitled “Material Federal Income Tax Considerations—Taxation of Shareholders—Taxation of Non-U.S. Holders,” regarding the specific tax consequences, including the federal, state, local, and foreign tax consequences, to you in light of your particular investment in, or the tax circumstances of acquiring, holding, exchanging or otherwise disposing of, your shares of CPA®:15 common stock or W. P. Carey Inc. common stock.

| Q. | Am I entitled to objecting stockholders’ rights of appraisal in connection with the Merger? |

| A. | CPA®:15 stockholders who do not vote in favor of the merger of CPA®:15 with its indirect wholly-owned subsidiary are entitled to objecting stockholders’ rights of appraisal with respect to that merger under Maryland law. For holders of CPA®:15 common stock, you can vote against approval of that merger by (i) indicating a vote against approval of the Merger on your proxy card and signing and mailing your proxy card in accordance with the instructions provided, (ii) authorizing your proxy by telephone or the Internet and indicating a vote against approval of the Merger or (iii) voting against approval of the Merger in person at CPA®:15’s special meeting. If a properly executed proxy card is returned or properly submitted by telephone or over the Internet and the stockholder has abstained from voting on the Merger, the shares of CPA®:15 common stock represented by the proxy will not be considered to have been voted on the Merger. Abstentions will have the same effect as a vote against approval of the Merger. To qualify as an objecting CPA®:15 stockholder, you must deliver to CPA®:15’s corporate secretary, at or prior to CPA®:15’s special meeting, your written objection to the Merger. The written objection must be separate from and in addition to any proxy or vote against the Merger. In addition, if you wish to exercise your right to demand payment of the fair value of your common stock, within 20 days following the date the articles of merger for the merger of CPA®:15 with its indirect wholly-owned subsidiary are accepted for record by the State Department of Assessments and Taxation of Maryland, you must make a written demand on CPA®:15 for the payment of your shares of CPA®:15 common stock, stating the number and class of shares for which you demand payment. Strict compliance with statutory procedures is necessary in order to perfect your rights to an appraisal and to receive fair value for your shares of CPA®:15 common stock. A copy of the relevant provisions of Maryland law appears as Annex E to this joint proxy statement/prospectus. |

6

Table of Contents

| Q. | How do I vote without attending the special meetings? |

| A. | If you are a holder of W. P. Carey listed shares or shares of CPA®:15 common stock on the record date, you may vote by completing, signing and promptly returning the proxy card in the self-addressed stamped envelope provided. You may also authorize a proxy to vote your shares by telephone or over the Internet as described in your proxy card. Authorizing a proxy by telephone or over the Internet or by mailing a proxy card will not limit your right to attend the special meetings and vote your shares in person. Those shareholders and stockholders of record who choose to authorize a proxy by telephone or over the Internet must do so no later than 11:59 p.m., Eastern Time, on September 12, 2012. |

| Q. | Can I attend the special meetings and vote my shares in person? |

| A. | Yes. All holders of W. P. Carey listed shares and all holders of CPA®:15 common stock are invited to attend the special meetings for the entity in which they hold shares. Shareholders and stockholders of record at the close of business on the record date are invited to attend and vote at the special meetings. If your W. P. Carey listed shares are held by a broker, bank or other nominee, then you are not the shareholder of record. Therefore, to vote at the W. P. Carey special meeting, you must bring the appropriate documentation from your broker, bank or other nominee confirming your beneficial ownership of the W. P. Carey listed shares. |

| Q. | If my W. P. Carey listed shares are held in “street name” by my broker, bank or other nominee, will my broker, bank or other nominee vote my W. P. Carey listed shares for me? |

| A. | No. If your W. P. Carey listed shares are held in “street name” by your broker, bank or other nominee, you should follow the directions provided by your broker, bank or other nominee. Your broker, bank or other nominee will vote your W. P. Carey listed shares only if you provide instructions on how you would like your shares to be voted. |

| Q. | Once the Merger has been completed, do CPA®:15 stockholders have to do anything to receive their shares of W. P. Carey Inc. common stock? |

| A. | No. Following completion of the Merger, W. P. Carey Inc. will cause a third party transfer agent to record the issuance of the shares of W. P. Carey Inc. common stock to the holders of CPA®:15 common stock on its stock records. We will issue shares of W. P. Carey Inc. common stock to holders of CPA®:15 common stock in uncertificated book-entry form. No physical share certificates will be delivered. |

| Q. | What do I need to do now? |

| A. | You should carefully read and consider the information contained in this joint proxy statement/prospectus, including its annexes. It contains important information about the factors that the board of directors of each of W. P. Carey and CPA®:15 considered in evaluating whether to vote to approve the Merger. |

You should then complete and sign your proxy card and return it in the enclosed envelope as soon as possible so that your shares will be represented at the special meetings, or authorize your proxy by telephone or over the Internet in accordance with the instructions on your proxy card. If your W. P. Carey listed shares are held through a broker, bank or other nominee, you should receive a separate voting instruction form with this joint proxy statement/prospectus.

| Q. | Can I change my vote after I have mailed my signed proxy card? |

| A. | Yes. You can change your vote at any time before your proxy is voted at your special meeting. To revoke your proxy, you must either (i) notify the secretary of either W. P. Carey or CPA®:15, as applicable, in writing, (ii) mail a new proxy card dated after the date of the proxy you wish to revoke, (iii) submit a later dated proxy by telephone or over the Internet by following the instructions on your proxy card or (iv) attend the special meetings and vote your shares in person. Merely attending the special meetings will not |

7

Table of Contents

| constitute revocation of your proxy. If your W. P. Carey listed shares are held through a broker, bank, or other nominee, you should contact your broker, bank or other nominee to change your vote. |

| Q. | Where will my W. P. Carey Inc. common stock be publicly traded? |

| A. | W. P. Carey Inc. will apply to have the new shares of W. P. Carey Inc. common stock listed on the NYSE upon the closing of the Merger. We anticipate that the shares of W. P. Carey Inc. common stock issued in the Merger will trade on the NYSE under the symbol “WPC,” upon the consummation of the Merger. |

| Q. | Will a proxy solicitor be used? |

| A. | Yes. We may utilize some of the officers and employees of W. P. Carey’s wholly-owned subsidiaries, CAM and Carey Management Services, Inc. (who will receive no compensation in addition to their regular salaries), to solicit proxies personally and by telephone. In addition, we have engaged Computershare Fund Services (“Computershare”) to assist in the solicitation of proxies for the meeting and estimate we will pay Computershare a fee of approximately $115,000. We have also agreed to reimburse Computershare for reasonable out-of-pocket expenses and disbursements incurred in connection with the proxy solicitation and to indemnify Computershare against certain losses, costs and expenses. No portion of the amount that W. P. Carey is required to pay Computershare is contingent upon the closing of the Merger or the REIT Conversion. |

| Q. | Who can help answer my questions? |

| A. | If you have more questions about the Merger, or would like additional copies of this joint proxy statement/prospectus, please contact: |

For W. P. Carey shareholders:

W. P. CAREY & CO. LLC

Investor Relations Department

50 Rockefeller Plaza

New York, New York 10020

Telephone: (800) WP-CAREY

Facsimile: (212) 492-8922

For CPA®:15 stockholders:

CORPORATE PROPERTY ASSOCIATES 15 INCORPORATED

Investor Relations Department

50 Rockefeller Plaza

New York, New York 10020

Telephone: (800) WP-CAREY

Facsimile: (212) 492-8922

8

Table of Contents

QUESTIONS AND ANSWERS FOR W. P. CAREY SHAREHOLDERS

REGARDING THE REIT CONVERSION

The following questions and answers for W. P. Carey shareholders briefly address some frequently asked questions about the REIT Conversion. They may not include all the information that is important to you. We urge you to read carefully this entire joint proxy statement/prospectus, including the annexes.

| Q. | What are we planning to do? |

| A. | In addition to the Merger, W. P. Carey is proposing a plan to reorganize its business operations to allow W. P. Carey Inc. to qualify as a REIT for federal income tax purposes beginning with its 2012 taxable year. W. P. Carey expects the REIT election to be effective from February 15, 2012, the date of incorporation of W. P. Carey Inc. W. P. Carey shareholders will not become holders of W. P. Carey Inc. common stock unless and until the Merger and the REIT Conversion are consummated. |

| Q. | What is a REIT? |

| A. | A REIT is an entity that qualifies for special treatment for federal income tax purposes provided that it meets certain requirements including, among other things, that it derives most of its income from real estate-based sources and makes a special election under the Internal Revenue Code of 1986, as amended (the “Code”). A corporation that qualifies as a REIT generally is not subject to federal income tax on its corporate income and gains that it distributes to its shareholders, reducing its corporate level income taxes and substantially eliminating the “double taxation” of corporate income. |

Even if we qualify as a REIT, we may continue to be required to pay federal income tax on earnings from all or a portion of our non-REIT assets or operations, which consists primarily of the investment management business of W. P. Carey. In addition, our international assets and operations will continue to be subject to taxation in the foreign jurisdictions where those assets are held or those operations are conducted. We also may be subject to federal income and excise taxes in certain circumstances, as well as state, local, and foreign income, franchise, property and other taxes.

| Q. | What will happen in the REIT Conversion? |

| A. | The REIT Conversion involves the following key elements: |

REIT Conversion. Following certain reorganizations of most of W. P. Carey’s subsidiaries, W. P. Carey will then merge with and into W. P. Carey Inc. with W. P. Carey Inc. surviving the merger. Effective at the time of the W. P. Carey Merger, W. P. Carey Inc. will hold, directly or indirectly through its subsidiaries, the assets currently held by W. P. Carey and will conduct the existing businesses of W. P. Carey and its subsidiaries and assume the obligations of W. P. Carey. The REIT Conversion will facilitate W. P. Carey’s compliance with REIT tax rules by ensuring the effective adoption of the charter provisions that implement the transfer restrictions that are intended to assist us in meeting the share ownership requirements of the REIT tax rules.

As a consequence of the REIT Conversion, among other things:

| • | there will be no change in the assets W. P. Carey holds or in the businesses it conducts; |

| • | there will be no fundamental change to W. P. Carey’s discretionary capital allocation strategy or current operational strategy; |

| • | effective at the time of the REIT Conversion, W. P. Carey Inc. will, subject to approval by the NYSE, become a publicly traded NYSE-listed company that will continue to operate, directly or indirectly, all of W. P. Carey’s existing business; and |

9

Table of Contents

| • | the rights of the stockholders of W. P. Carey Inc. will be governed by the W. P. Carey Inc. Charter and the W. P. Carey Inc. Bylaws. |

See the section entitled “Structure of the Merger and the REIT Conversion.”

Other Reorganization Transactions. W. P. Carey’s existing subsidiaries that are taxable as REITs will become QRSs of W. P. Carey Inc., and W. P. Carey’s existing subsidiaries that are taxable as corporations will jointly elect with W. P. Carey Inc. to be treated as TRSs in order to comply with certain REIT qualification requirements. See the section entitled “Material Federal Income Tax Considerations—Subsidiary Entities” for a more detailed description of the requirements and limitations regarding our expected use of TRSs.

The business that we expect to contribute to, or retain in, one or more subsidiaries that will elect to be treated as TRSs effective upon the REIT Conversion principally consists of our investment management business. Net income from our TRSs either will be retained by our TRSs and used to fund their operations, or will be distributed to us, where it either will be reinvested by us into our business or will be contributed to the income available for distribution to our stockholders.

| Q. | What are the reasons for the REIT Conversion? |

| A. | The REIT Conversion, together with the Merger, is being proposed primarily for the following reasons: |

| • | the Merger and the REIT Conversion are part of a larger transformation that implements W. P. Carey’s overall business strategy of expanding real estate assets under ownership which in turn is expected to provide a platform for future growth; |

| • | the Merger and the REIT Conversion substantially increase W. P. Carey’s scale and liquidity, which in turn provide a basis for an expected continuation of stable dividend growth; |

| • | the Merger and the REIT Conversion are expected to provide income contribution from owned properties, while preserving the investment management business; and |

| • | the Merger and the REIT Conversion are expected to increase analyst coverage and the combined company’s access to capital markets by creating a company with increased scale and trading volume and enhanced liquidity. |

To review the background of, and reasons for, the REIT Conversion in greater detail, and the related risks associated with the reorganization, see the sections entitled “The Merger and the REIT Conversion—Background of the Merger and the REIT Conversion,” “The Merger and the REIT Conversion—W. P. Carey’s Reasons for the Merger and the REIT Conversion and the W. P. Carey Merger” and “Risk Factors.”

| Q. | What will W. P. Carey shareholders receive in connection with the REIT Conversion and when will they receive it? |

| A. | At the effective time of the W. P. Carey Merger, W. P. Carey shareholders will receive one share of W. P. Carey Inc. common stock in exchange for each W. P. Carey listed share that they then own. In addition, as a REIT, W. P. Carey Inc. will be required to distribute annually at least 90% of its REIT taxable income (determined without regard to the dividends paid deduction and excluding net capital gain). |

If the REIT Conversion is approved by W. P. Carey shareholders and the Merger is approved by both W. P. Carey shareholders and CPA®:15 stockholders, W. P. Carey Inc. expects to commence declaring regular quarterly distributions beginning in the quarter in which the Merger closes, the amount of which will be determined, and is subject to adjustment, by the board of directors. W. P. Carey Inc. anticipates that its annualized distribution rate will be $2.60 per share of W. P. Carey Inc. common stock. The actual timing and amount of the distributions will be as determined and authorized by the board of directors and will depend on, among other factors, our financial condition, earnings, debt covenants, applicable provisions under the Maryland General Corporation Law (the “MGCL”) and other possible uses of such funds. See the section entitled “Dividend and Distribution Policy.”

10

Table of Contents

If you dispose of your shares before the record date for the first quarterly distribution, you will not receive the first quarterly distribution or any other regular quarterly distribution.

Any W. P. Carey subsidiaries currently taxable as REITs will distribute their current and accumulated earnings and profits to W. P. Carey prior to the REIT Conversion.

| Q. | Should I send in my W. P. Carey listed share certificates (or share certificates of W. P. Carey’s predecessor, Carey Diversified, LLC) now or at all? |

| A. | No. As soon as practicable following the effective time of the W. P. Carey Merger, W. P. Carey Inc. will cause a third party transfer agent to record the transfer on the stock records of W. P. Carey Inc. of the amount of W. P. Carey Inc. common stock issued pursuant to the terms of the REIT Conversion Agreement. We will issue shares of W. P. Carey Inc. common stock to holders of W. P. Carey listed shares in uncertificated book-entry form. No physical share certificates will be delivered. See “Terms of the REIT Conversion—Recordation of Exchange.”Please do not send in your W. P. Carey share certificates (or share certificates of W. P. Carey’s predecessor, Carey Diversified, LLC) with your proxy or following completion of the W. P. Carey Merger. Any share certificate or book entry representing W. P. Carey listed shares or its predecessor, Carey Diversified, LLC, will instead automatically represent shares of W. P. Carey Inc. common stock following completion of the W. P. Carey Merger. |

| Q. | Will converting to a REIT change W. P. Carey’s business objectives and strategy? |

| A. | No. W. P. Carey’s business objectives and strategy will remain the same. |

| Q. | When is the REIT Conversion expected to be completed and the REIT election expected to be made? |

| A. | We expect to complete the REIT Conversion by the third quarter of 2012, or as soon as possible thereafter, prior to the Merger. However, there can be no assurance as to when, or if, the REIT Conversion will be completed. If the REIT Conversion and the Merger are completed in 2012, we expect W. P. Carey Inc. to elect to qualify as a REIT for federal income tax purposes beginning with its 2012 taxable year. W. P. Carey expects the REIT election to be effective from February 15, 2012, the date of incorporation of W. P. Carey Inc. W. P. Carey reserves the right to abandon the REIT Conversion even if the shareholders of W. P. Carey vote to adopt the REIT Conversion Agreement, which sets forth the terms and conditions of the W. P. Carey Merger, and approve the W. P. Carey Merger, and other conditions to the completion of the REIT Conversion are satisfied or waived, if the W. P. Carey board of directors determines that the REIT Conversion is no longer in the best interests of W. P. Carey and its shareholders. See the section entitled “Terms of the REIT Conversion” for a more detailed description of the REIT Conversion. |

| Q. | Are there risks associated with the REIT Conversion that I should consider in deciding how to vote? |

| A. | Yes. There are a number of risks related to the REIT Conversion that are discussed in this joint proxy statement/prospectus. In evaluating the REIT Conversion, you should read carefully the detailed description of the risks associated with the REIT Conversion described under the heading “Risk Factors—Risks Related to the REIT Conversion and REIT Structure” and other information included in this joint proxy statement/prospectus. |

| Q. | Will I have to pay federal income taxes as a result of the REIT Conversion? |

| A. | You should not recognize gain or loss for federal income tax purposes as a result of the exchange of W. P. Carey listed shares for shares of W. P. Carey Inc. common stock in the REIT Conversion except to the extent that your allocable share of W. P. Carey indebtedness exceeds your basis in your listed shares of W. P. Carey. |

11

Table of Contents

The federal income tax treatment of holders of W. P. Carey shares in the REIT Conversion depends in some instances on determinations of fact and interpretations of complex provisions of federal income tax law for which no clear precedent or authority may be available. In addition, the tax consequences of participating in the REIT Conversion and of holding W. P. Carey Inc. common stock to any particular shareholder will depend on that shareholder’s particular tax circumstances. We urge you to consult your tax advisor, particularly if you are a non-U.S. holder, as defined in the section entitled “Material Federal Income Tax Considerations—Taxation of Shareholders—Taxation of Non-U.S. Holders,” regarding the specific tax consequences, including the federal, state, local, and foreign tax consequences, to you in light of your particular investment in, or the tax circumstances of acquiring, holding, exchanging or otherwise disposing of, W. P. Carey listed shares or W. P. Carey Inc. common stock.

| Q. | Am I entitled to dissenters’ rights of appraisal in connection with the REIT Conversion? |

| A. | No. Under Delaware law, you are not entitled to any dissenters’ rights of appraisal in connection with the REIT Conversion. |

| Q. | If my W. P. Carey listed shares are held in “street name” by my broker, bank or other nominee, will my broker, bank or other nominee vote my shares for me? |

| A. | No. If your W. P. Carey listed shares are held in “street name” by your broker, bank or other nominee, you should follow the directions provided by your broker, bank or other nominee. Your broker, bank or other nominee will vote your shares only if you provide instructions on how you would like your W. P. Carey listed shares to be voted. |

| Q. | Where will my W. P. Carey Inc. common stock be publicly traded? |

| A. | W. P. Carey Inc. will apply to have the new shares of W. P. Carey Inc. common stock listed on the NYSE upon the closing of the REIT Conversion. We anticipate that the shares of W. P. Carey Inc. common stock issued in the W. P. Carey Merger will trade on the NYSE under the symbol “WPC,” upon the consummation of the Merger. |

12

Table of Contents

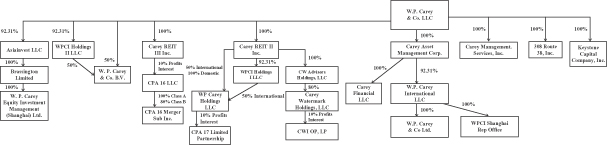

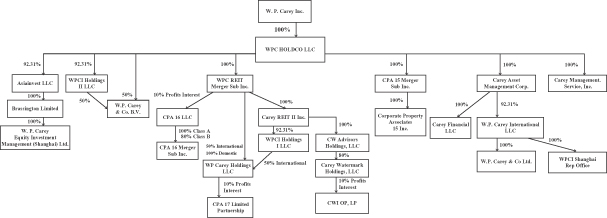

STRUCTURE OF THE MERGER AND THE REIT CONVERSION

The following diagrams summarize the corporate structure of W. P. Carey Inc. before and after the Merger and the REIT Conversion.

Before the Merger and REIT Conversion:

After the Merger and REIT Conversion:

13

Table of Contents

This summary highlights selected information from this joint proxy statement/prospectus and may not contain all of the information that is important to you. You should carefully read this entire joint proxy statement/prospectus and the other documents to which this joint proxy statement/prospectus refers to fully understand the Merger and the REIT Conversion. In particular, you should read the annexes attached to this joint proxy statement/prospectus, including the Merger Agreement and the REIT Conversion Agreement, which are attached as Annexes A and B, respectively, as they are the legal documents that govern the Merger and the W. P. Carey Merger. You also should read the W. P. Carey Inc. Charter and the W. P. Carey Inc. Bylaws, attached as Annexes F and G, respectively, as they are the legal documents that will govern your rights as a stockholder of W. P. Carey Inc. following the Merger and the REIT Conversion. See the section entitled “Where You Can Find More Information.” For a discussion of the risk factors that you should carefully consider, see the section entitled “Risk Factors.”

The Companies

W. P. Carey & Co. LLC

50 Rockefeller Plaza

New York, New York 10020

(212) 492-1100

W. P. Carey provides long-term financing via sale-leaseback and build-to-suit transactions for companies worldwide and manages a global investment portfolio. W. P. Carey invests primarily in commercial properties domestically and internationally that are generally triple-net leased to single corporate tenants, which requires each tenant to pay substantially all of the costs associated with operating and maintaining the property. W. P. Carey also earns revenue as the advisor to the CPA® REITs and invests in similar properties. W. P. Carey is currently the advisor to the following CPA® REITs: CPA®:15, CPA®:16—Global and CPA®:17—Global. W. P. Carey is also the advisor to CWI, which W. P. Carey formed in March 2008 for the purpose of acquiring interests in lodging and lodging-related properties.

Collectively, at March 31, 2012, W. P. Carey owned and managed over 970 properties domestically and internationally, including its owned portfolio. W. P. Carey’s portfolio was comprised of its full or partial ownership interest in 156 properties, substantially all of which were triple-net leased to 72 tenants, and totaled approximately 12.0 million square feet (on a pro rata basis) with an occupancy rate of approximately 93%. In addition, through its Carey Storage and Livho subsidiaries, W. P. Carey had interests in 21 self-storage properties and a hotel property, respectively, with an aggregate of approximately 0.8 million square feet (on a pro rata basis) at March 31, 2012.

Most of W. P. Carey’s properties were either acquired as a result of its consolidation with certain affiliated Corporate Property Associates limited partnerships or subsequently acquired from other CPA® REIT programs in connection with the provision of liquidity to stockholders of those CPA® REITs. Because its advisory agreements with each of the existing CPA® REITs and CWI require that W. P. Carey use its best efforts to present to them a continuing and suitable program of investment opportunities that meet their investment criteria, W. P. Carey generally provides investment opportunities to these funds first and earn revenues from transaction and asset management services performed on their behalf. W. P. Carey’s principal focus on its owned real estate portfolio in recent years has therefore been on enhancing the value of its existing properties. Under the advisory agreements with the CPA® REITs and CWI, W. P. Carey performs various services, including but not limited to the day-to-day management of the CPA® REITs and CWI and transaction-related services, for which W, P. Carey earns revenue. The advisory agreements allow W. P. Carey to elect to receive stock in lieu of cash for any revenue due from the CPA® REITs and CWI. W. P. Carey also receives a percentage of distributions of

14

Table of Contents

available cash from the operating partnerships of CPA®:16—Global, CPA®:17—Global and CWI. W. P. Carey may also earn incentive and disposition revenue and receive other compensation in connection with providing liquidity alternatives to the stockholders of the CPA® REITs and CWI. The CPA® REITs and CWI also reimburse W. P. Carey for certain costs, primarily broker-dealer commissions paid on their behalf and marketing and personnel costs. As a result of electing to receive certain payments for services in shares, W. P. Carey holds ownership interests in the CPA® REITs and CWI.

W. P. Carey was formed as a limited liability company under the laws of Delaware on July 15, 1996. On January 1, 1998 the limited partnership interests of nine CPA® partnerships were combined and became listed on the NYSE under the name “Carey Diversified” and the symbol “CDC.” In 2000, Carey Diversified merged with W. P. Carey after W. P. Carey became listed on the NYSE under the symbol “WPC.”

At March 31, 2012, W. P. Carey employed 214 individuals through its wholly-owned subsidiaries. W. P. Carey’s website is www.wpcarey.com. On the website, investors can find press releases, financial filings and other information about W. P. Carey. The SEC website, www.sec.gov, also offers access to reports and documents that W. P. Carey has electronically filed with or furnished to the SEC. These website addresses are not intended to function as hyperlinks, and the information contained on W. P. Carey’s website and in the SEC’s website is not intended to be a part of this joint proxy statement/prospectus.

Corporate Property Associates 15 Incorporated

50 Rockefeller Plaza

New York, New York 10020

(212) 492-1100