ABS East Conference

Boca Raton, Florida

September 13-16, 2005

Forward looking disclosure

Certain matters discussed in this presentation may constitute forward-looking statements within the meaning of the

federal securities laws that inherently include certain risks and uncertainties. Actual results and the timing of certain

events could differ materially from those projected in or contemplated by the forward-looking statements due to a

number of factors, including our ability to generate sufficient liquidity on favorable terms; the size and frequency of our

securitizations; interest rate fluctuations on our assets that differ from our liabilities; increases in prepayment or default

rates on our mortgage assets; changes in assumptions regarding estimated loan losses and fair value amounts;

changes in origination and resale pricing of mortgage loans; our compliance with applicable local, state and federal

laws and regulations and the impact of new local, state or federal legislation or regulations or court decisions on our

operations; the initiation of margin calls under our credit facilities; the ability of our servicing operations to maintain high

performance standards and maintain appropriate ratings from rating agencies; our ability to expand origination volume

while maintaining an acceptable level of overhead; our ability to adapt to and implement technological changes; the

stability of residential property values; the outcome of litigation or regulatory actions pending against us; the impact of

general economic conditions; and other risk factors that are from time to time included in our filings with the SEC,

including our 2005 Quarterly Report on Form 10-Q. Other factors not presently identified may also cause actual results

to differ. Management continuously updates and revises these estimates and assumptions based on actual conditions

experienced. It is not practicable to publish all revisions and, as a result, no one should assume that results projected

in or contemplated by the forward-looking statements will continue to be accurate in the future. This presentation

contains statistics and other data that in some cases have been obtained from, or compiled from, information made

available by service providers or included in publicly filed reports of other entities. Although we believe this information

to be reliable, we are not able to independently verify the accuracy thereof.

2

Overview

Founded: June, 1996

IPO: October, 1997 (NYSE: NFI)

$1.1 billion market cap; $580 million of GAAP equity

Top 15 residential mortgage ABS issuer

Current production run rate of $800-$1000 million per month

Cost to originate historically in the 2.25%-2.50% range

Servicer rating of “Strong” by S&P

Completed 30 ABS transactions, total issuance over $25 billion

Disciplined underwriting approval through automated system

manages to a 3.5-5.0% (pre-MI) loss under normal market

conditions.

3

6/30/05 YTD Subprime Market Rankings

(in millions)

4

Originations

1.

Ameriquest

$45,690

2.

New Century

$23,695

3.

Countrywide

$20,256

4.

Option One

$18,220

5.

WAMU

$17,125

6.

Fremont

$17,000

7.

Wells Fargo

$14,449

8.

WMC

$14,272

9.

First Franklin

$13,564

10.

HSBC

$10,434

11.

GMAC-RFC

$8,110

20.

NovaStar Mortgage

$4,400

Source: Inside B&C Lending

MBS Issuers

1.

Ameriquest

$28,262

2.

New Century

$20,536

3.

Countrywide

$18,411

4.

Lehman

$16,874

5.

CSFB

$10,910

6.

Option One

$10,595

7.

WMC

$10,169

8.

GMAC-RFC

$9,466

9.

First Franklin

$8,135

10.

Bear Stearns

$7,907

11.

Morgan Stanley

$6,864

17.

NovaStar Mortgage

$3,996

Source: Inside B&C Lending

NovaStar Organizational Structure

5

NovaStar Operating Strategy

Originate high margin, non-conforming residential mortgages

Service our own collateral (no third party servicing)

Use technology to be an efficient originator and servicer

Create mortgage securities with good risk-adjusted returns

from our loans through securitization

Use capital markets to price and manage risks

Interest rate risks hedged with swaps / caps

Credit risk managed through the purchase of deep MI and/or

execution in the NIM market

NovaStar is structured as a REIT

Parent company does not pay corporate taxes

Focus is on being a portfolio investor vs. pure mortgage banking

6

Origination Strategy

Primarily an A- wholesale lender

Vertical integration

Originator and end investor

Whole loan portfolio exceeding $13.3 billion

Centralized origination operation

Strive to be a low cost producer - cost to originate ~ 2.25%

Better risk controls - over 40% appraisal reviews

Manage underwriting - 100% prefunding audits

Diversify credit risk - deep MI / NIM execution

Focus on developing competitive advantages in every

channel in which we choose to operate

7

Distribution Channels

Wholesale

Production centers located in Cleveland, OH; Lake Forest, CA and Troy, MI

376 person inside & outside sales force located in 40 states call on a

customer base of over 21,000 independent retail brokers

Compete on service, primarily a price taker

Correspondent

Sales force dedicated solely to the sourcing of closed loans

Focus is on the development of correspondent flow relationships and

purchase of mini bulk pools ($1-$20 million)

Attempt to create competitive advantages by offering small warehouse

lines and private labeling our origination system

Current production run rate of approx. $180 million per quarter

8

Distribution Channels - Continued

Retail

Offices located in Columbia, MD and Kansas City, MO focusing

primarily on retention of existing portfolio

Total of 106 loan officers

Secondary focus on new business using primarily purchased leads

Also maintain a chain local branch in a few select markets

Current production run rate of approx. $375 million per quarter

9

Production Mix by Channel

10

2002

2003

2004

2005YTD*

Channel

Actual

Actual

Actual

Actual

Independent Brokers

79%

67%

65%

77%

Retail

19%

28%

25%

16%

Correspondent

2%

5%

10%

7%

Total Nonconforming

Production

$2.50B

$5.25B

$8.42B

$5.19B

* Thru July 31, 2005

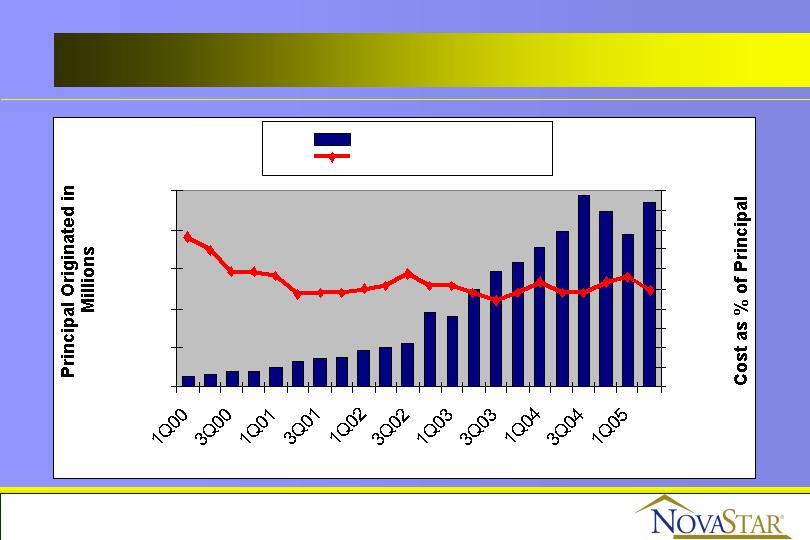

Securitization History

11

2002

2003

2004

2005YTD*

Actual

Actual

Actual

Actual

Production

$2.50B

$5.25B

$8.42B

$5.19B

Underlying Deals

3

4

4

3

Resecuritizations

1

1

3

1

* Includes 2005-3

Non-Conforming Production

$0

$500

$1,000

$1,500

$2,000

$2,500

Quarter

0.00%

0.50%

1.00%

1.50%

2.00%

2.50%

3.00%

3.50%

4.00%

4.50%

5.00%

Principal Originated

Cost to Originate

12

NovaStar Operations

Troy, MI

Wholesale - Central

Independence, OH

Wholesale - East

Columbia, MD

Retail - East

Lake Forest, CA

Wholesale - West

Kansas City, MO

Corporate Headquarters

Servicing

Correspondent

Retail - Central

13

NovaStar Origination Practices

100% Pre-funding Audit (100% DISSCO / 40% full QC audit)

Quality/Fraud procedures for new and existing brokers

Watch list / Do not take list for 3rd party vendors

Quality Control - Identifies negative trends / provides feedback

10% random review of all files within 30-45 days of funding

100% Appraisal Review

60% cleared by underwriter using AVMs or on-line data sources (SiteXdata)

40% referred to on staff licensed appraisers

15% of those reviewed by staff appraisers have their value reduced

Predatory Lending Issues

We do not originate high cost loans (HOEPA or State High Cost loans)

Net tangible benefit test automated and performed on all eligible loans

Adhere to the FNMA fee test (5% max) on all loans where NovaStar acts as

the lender

14

Risks and Risk Management

Interest rate/prepayment

Hedging - match duration using swaps and caps

Prepayment/convexity - prepayment penalties

Portfolio is hedged within maximum exposure of 10% of equity

up/down 100 bps

Credit

Geographic diversification

Lender paid deep MI to 50-55% LTV and/or NIM execution

Common sense U/W and strong quality control

Servicing

Liquidity

$3.65 billion of borrowing capacity from 5 separate lenders

($3.45 billion of which is committed)

15

Servicing Overview

$13.3 billion portfolio representing 95,000 accounts

19th largest sub-prime servicer (as of 6/30/04; Source: National Mortgage News)

Total staff of 264

16 years average experience among Management/Supervisors

Approved FHA, VA, Fannie Mae and Freddie Mac

seller/servicer

Rated by all three rating agencies

S&P: Strong

Moody’s: SQ2

Fitch: RSP3+

16

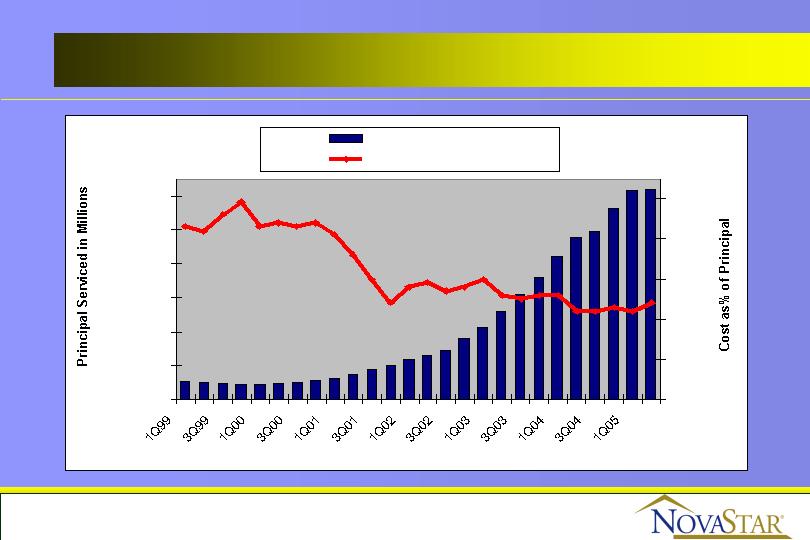

Servicing

$0

$2,000

$4,000

$6,000

$8,000

$10,000

$12,000

Quarter

0.00%

0.10%

0.20%

0.30%

0.40%

0.50%

Principal Serviced

Cost to Service

17

Summary of 6/30/2005 YTD Results

GAAP earnings of $71.3 million; $2.49 / share

$2.80 dividend / share

$4.30 billion in non-conforming production

Servicing portfolio grew to $13.3 billion

$343 million of cash and available liquidity

Completed two whole loan Sr./Sub securitizations backed

by $3.9 billion of collateral

18

Collateral Performance

Pre-Mortgage Insurance

(All data as of August 31, 2005 unless stated otherwise)

Production Summary

Year

Average

Balance

WAC

LTV

CLTV

FICO

PPP

(% with)

PPP

Years

ARM

NON-FULL

DOC

NOO

CASH OUT

1997-98

$104,540

10.04%

79.6%

81.3%

604

70%

2.2

68%

35.1%

5.9%

52.8%

1999

$100,837

9.90%

81.6%

82.9%

615

90%

3.2

64%

39.8%

7.7%

49.5%

2000

$116,009

10.55%

82.5%

84.9%

616

90%

2.9

77%

41.4%

6.1%

42.9%

2001

$128,925

9.76%

82.7%

85.5%

613

84%

2.5

74%

39.1%

4.5%

49.4%

2002

$146,642

8.21%

81.0%

83.3%

627

82%

2.4

70%

45.4%

3.7%

56.9%

2003

$153,639

7.22%

80.0%

82.6%

637

78%

2.3

69%

50.3%

3.6%

62.0%

2004

$155,529

7.56%

82.2%

84.0%

620

75%

2.0

83%

48.9%

3.9%

61.3%

6/30/05YTD

$150,972

7.62%

82.2%

85.7%

631

65%

1.5

83%

51.8%

5.0%

57.8%

20

Actual Loss Severity

21

Production

Principal

Average

Loss

Year

Loans

Liquidated

Balance

Severity

1997-1998

1,987

$198,801,415

$100,051

42.4%

2000

525

$59,955,413

$114,201

34.8%

2001

691

$81,875,274

$118,488

34.3%

2002

397

$57,644,268

$145,200

28.2%

2003

164

$23,235,654

$141,681

26.1%

2004

20

$3,171,001

$158,500

24.8%

2000-2004

1,797

$225,880,611

$125,699

31.9%

Production Performance

22

Production Performance

23

Early Performance Indicators

24

MBS method

OTS method

Early

First Payment

First Payment

Payment

Default

Default

Default *

1997-1998

4.67%

2.05%

9.20%

2000

1.65%

0.80%

5.61%

2001

1.33%

0.66%

5.02%

2002

1.05%

0.45%

2.77%

2003

0.67%

0.25%

1.79%

2004

1.57%

0.55%

3.35%

2000-2004

1.22%

0.47%

3.01%

*Early payment default is defined as missing one payment in the first six payments

Additional Data

Complete production and performance data can be found on

NovaStar’s website: http://www.novastarmortgage.com/corporate/

Monthly Production Reports

Bond Investor Reports

Bond Remittance Statements

Mortgage Insurance Claim Statistics

25