NovaStar Financial

(NYSE-NFI)

www.novastarmortgage.com

2006 FBR Investor Conference

November 28, 2006

Scott Hartman, CEO

Safe Harbor Statement

Certain matters discussed in this release constitute forward-looking statements within the meaning of the

federal securities laws. Forward-looking statements are those that predict or describe future events and that do

not relate solely to historical matters. Forward-looking statements are subject to risks and uncertainties and

certain factors can cause actual results to differ materially from those anticipated. Some important factors that

could cause actual results to differ materially from those anticipated include: our ability to generate sufficient

liquidity on favorable terms; the size, frequency and structure of our securitizations; interest rate fluctuations

on our assets that differ from our liabilities; increases in prepayment or default rates on our mortgage assets;

changes in assumptions regarding estimated loan losses and fair value amounts; changes in origination and

resale pricing of mortgage loans; our compliance with applicable local, state and federal laws and regulations

or opinions of counsel relating thereto and the impact of new local, state or federal legislation or regulations or

opinions of counsel relating thereto or court decisions on our operations; the initiation of margin calls under

our credit facilities; the ability of our servicing operations to maintain high performance standards and

maintain appropriate ratings from rating agencies; our ability to expand origination volume while maintaining

an acceptable level of overhead; our ability to adapt to and implement technological changes; the stability of

residual property values; the outcome of litigation or regulatory actions pending against us or other legal

contingencies; compliance with new accounting pronouncements; the impact of general economic conditions;

and the risks that are from time to time included in our filings with the SEC, including our Annual Report on

Form 10-K, for the period ending December 31, 2005 and our quarterly report on form 10-Q, for the period

ending September 30, 2006. Other factors not presently identified may also cause actual results to differ. This

document speaks only as of its date and we expressly disclaim any duty to update the information herein.

2

Business Overview

High margin, nonconforming residential

mortgages

Market size of $400B to $600B

NovaStar has less than 2% market share

Create mortgage securities with good risk-adjusted

returns from our loans through securitization

Use capital markets to price and lay off risks

Interest rate risks – swaps / caps

Credit risk – Deep mortgage insurance to

approximately 55% LTV

NovaStar is structured as a REIT, no corporate

taxes at the REIT level.

3

Mortgage Banking

Origination Channels*

Primarily Wholesale (79%)

Independent brokers

Includes correspondent flow

Retail (19%)

Primarily portfolio retention

Oak Street acquisition scheduled to close by

year-end ‘06

Correspondent Bulk (2%)

Opportunistic and price sensitive

*Figures are current run-rate including $100 mil. per month from Oak Street acquisition

5

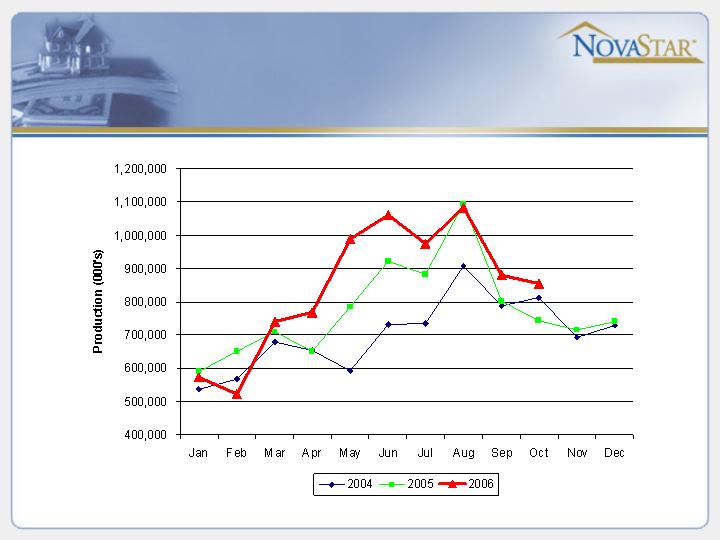

Production

6

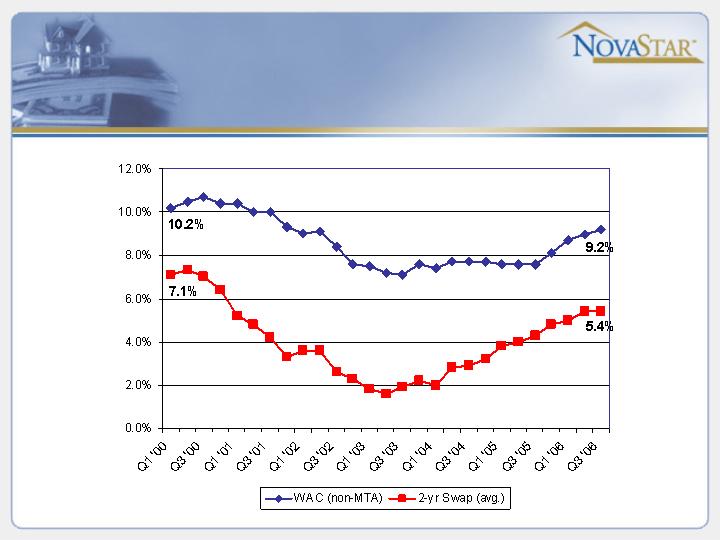

Historical WAC/Swap

Spreads

7

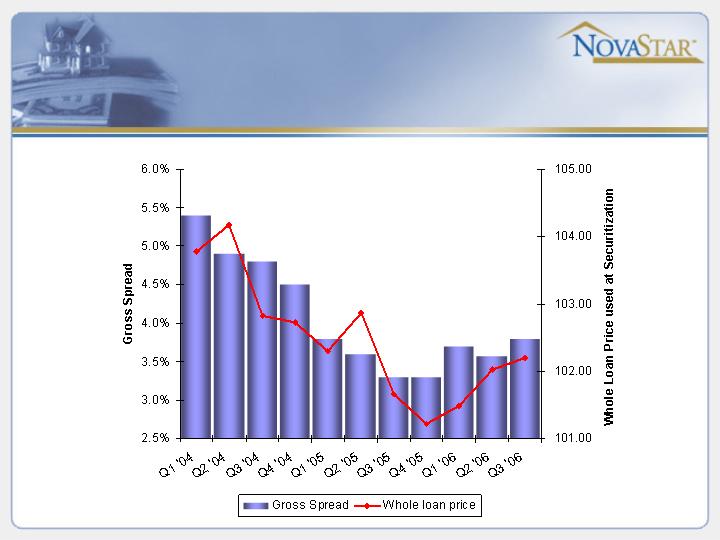

Spreads/Whole loan Prices

8

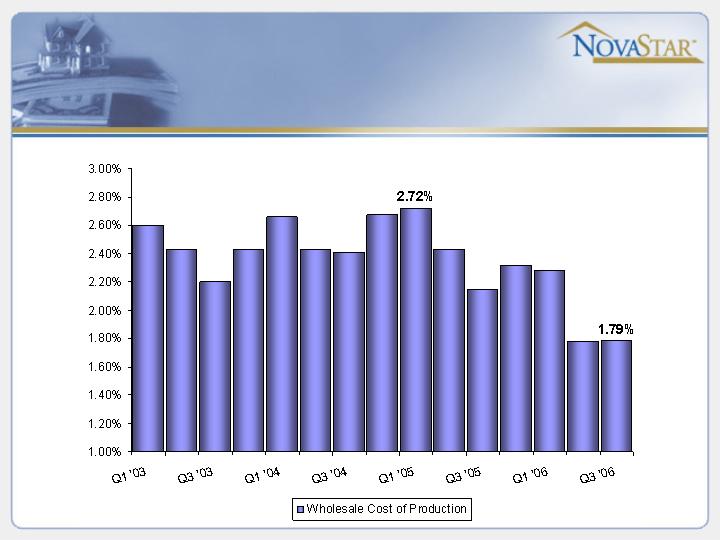

Wholesale COP

9

Mortgage Banking

Trends

Reasonable demand for whole-loans but pricing is

a little tighter

Adapting with changes to guidelines

Some originators continue to price low for volume

Gain-on-sale margins continue to be too tight when

adjusted for risks

Premium recapture

Loan buyback

Driving down cost to originate still a focus

10

Portfolio Management

World Class Portfolio

Management Team

Mike Bamburg, CIO

Former Partner with Smith Breeden

More than 19 years specializing in analysis and

hedging of mortgage backed securities

Proprietary modeling

Staff includes three PhD's or PhD candidates

12

Risks and Risk management

Interest rate/prepayment

Hedging – match duration using swaps and caps

Prepayment/convexity – prepayment penalties

Portfolio is hedged within maximum exposure of 10%

of equity up/down 100 bps

Credit

Geographic diversification

Lender paid deep MI to 50-60% LTV

Common sense U/W and strong quality control

Servicing

13

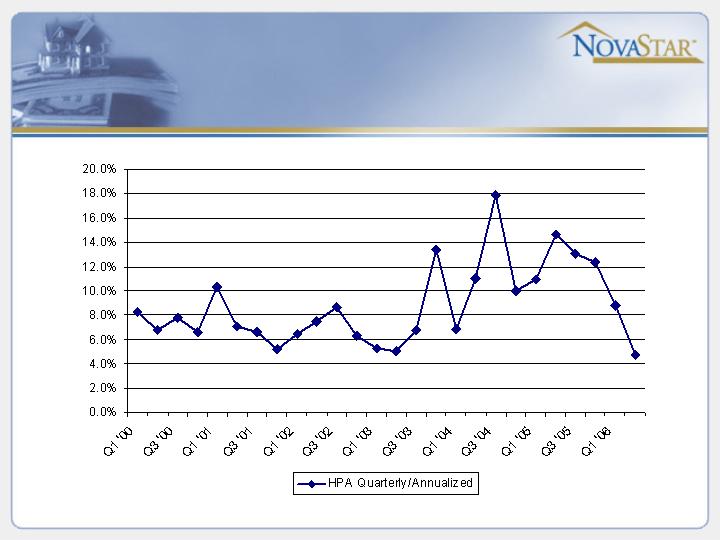

U.S. Housing Price

Appreciation

Source: OFHEO

14

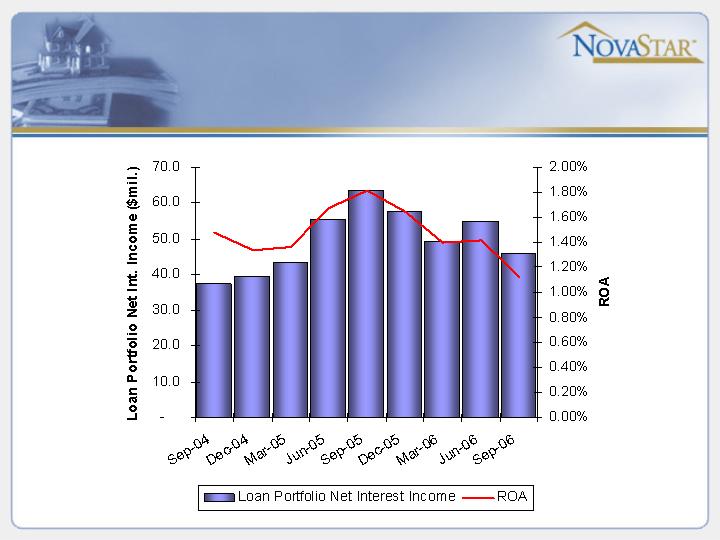

Portfolio ROA

15

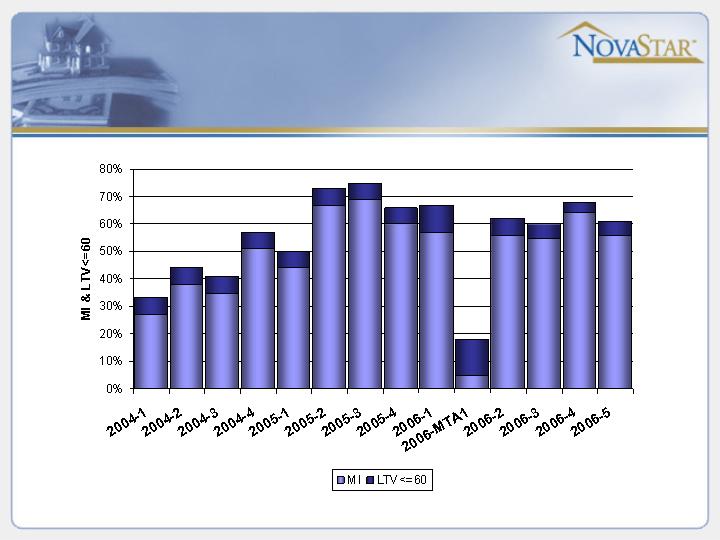

Credit Risk Management

16

Portfolio Management

Trends

Generally positive about our portfolio and

the value it has created

Reasonably good demand for our bonds

Credit weaker than in the past

Portfolio is diversified and hedged from a

credit and interest rate perspective

Delinquencies, severities and housing price

data will drive forward assumptions

17