NovaStar Financial

(NYSE-NFI)

www.novastarmortgage.com

2006 Fourth Quarter Earnings

Conference Call

February 20, 2007

Safe Harbor Statement

This Presentation contains forward-looking statements within the meaning of Section 21E of the Securities Exchange Act of

1934, as amended, regarding management’s beliefs, estimates, projections, and assumptions with respect to, among other things,

the Company’s future operations, business plans and strategies, as well as industry and market conditions, all of which are

subject to change at any time without notice. Actual results and operations for any future period may vary materially from those

projected herein and from past results discussed herein. Some important factors that could cause actual results to differ

materially from those anticipated include: our ability to successfully integrate acquired businesses or assets with our existing

business; our ability to generate sufficient liquidity on favorable terms; the size, frequency and structure of our securitizations;

impairments on our mortgage assets; interest rate fluctuations on our assets that differ from our liabilities; increases in

prepayment or default rates on our mortgage assets; changes in assumptions regarding estimated loan losses and fair value

amounts; changes in origination and resale pricing of mortgage loans; our compliance with applicable local, state and federal

laws and regulations or opinions of counsel relating thereto and the impact of new local, state or federal legislation or regulations

or opinions of counsel relating thereto or court decisions on our operations; the initiation of margin calls under our credit

facilities; the ability of our servicing operations to maintain high performance standards and maintain appropriate ratings from

rating agencies; our ability to expand origination volume while maintaining an acceptable level of overhead; our ability to adapt

to and implement technological changes; the stability of residual property values; the outcome of litigation or regulatory actions

pending against us or other legal contingencies; compliance with new accounting pronouncements; the impact of general

economic conditions; and the risks that are from time to time included in our filings with the SEC, including our Annual Report

on Form 10-K, for the year ended December 31, 2005 and our quarterly report on form 10-Q, for the period ending September 30,

2006. Other factors not presently identified may also cause actual results to differ. Words such as “believe,” “expect,”

“anticipate,” “promise,” “plan,” and other expressions or words of similar meanings, as well as future or conditional verbs such

as “will,” “would,” “should,” “could,” or “may” are generally intended to identify forward-looking statements. This document

speaks only as of its date and we expressly disclaim any duty to update the information herein.

2

Presentation Overview

Q4 Earnings Overview

Credit Review

2007 Outlook

Mortgage Banking

Portfolio Strategies

Taxable income analysis

Detailed Q4 Earnings review

3

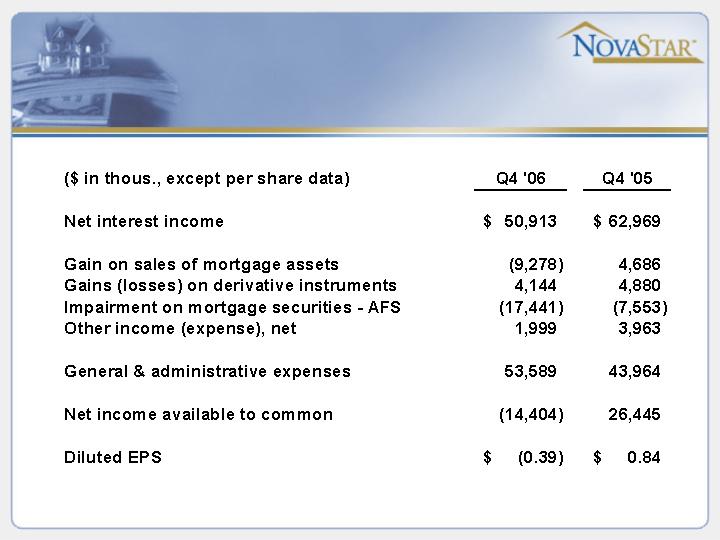

Q4 2006 Earnings Review

GAAP loss of $0.39 / share

Credit-related charges

REIT charges (pre-tax = after-tax)

Mortgage securities impairments – ($17M)

Loan loss reserve increase for on-balance sheet deal 06-1 Q4 - ($10M)

TRS charges

Increase to loan buy-back reserve – ($13M)

Other non-credit items

Settled six NHMI Branch-related class action suits ($3M)

MTM loss on trading securities for CDO – ($4M) from spread

widening

This will create quarterly noise

Spreads have continued to widen in Q1 2007 – could have a negative

impact on Q1 earnings

4

Credit Review

Keys to good loan performance

Stable housing market (systemic risk)

Appropriate underwriting guidelines

Appropriate exceptions to guidelines

Solid appraisal management process

Ability to identify and eliminate unacceptable

layered risk

Strong servicing operation

5

Credit Review

How do we improve performance?

Housing market is beyond our control

Tightened underwriting guidelines both in:

Loan characteristics that impact performance, and

LTV, FICO, Documentation Type, DTI, etc

Policies on verification of critical information

Seasoning of funds, property seasoning, income verification, etc

Enhanced appraisal management process:

Tighter tolerance levels on value estimates

Enhanced appraisal review process

Tightened exceptions to guidelines

Increased staffing levels in our delinquency

management and loss mitigation areas

6

Credit Review

Why do we expect these changes will

improve performance?

Q4 2005 through end of 2006 production was

run against new, tighter guidelines

Impact was positive; but not sufficient

Conclusion: Need to identify and eliminate

unacceptable levels of layered risk within our

guidelines

7

Credit Review

Identifying and reducing layered risk using

NovaStar’s Risk Assessment Score (NRAS)

Computed NRAS on all loans originated from the Q4

2005 through the end of 2006

Eliminated the highest risk scores from production and

appended performance data from fourth quarter 2005

through year end 2006

Risk performance fell within acceptable historical

standards with a negligible drop in coupon

8

Mortgage Banking Trends

Q4 2006 costs / production were good

Gain-on-sale margins continue to be tight when

adjusted for risks

Premium recapture

Loan buyback

Rates still need to come up (or credit risk go down)

More lenders continue to go out of business – good

for remaining competitors

We expect 2007 originations to perform better

9

2007 Mortgage

Banking Outlook

Expect to grow NovaStar retail platform via

integration of acquired assets (Q4)

First half 2007 production could be lower as

brokers adjust to tighter guideline implementation

Expect better quality and economics during the

year

Still need to continue focus on cost control

Growth may come in second half of the year

10

Portfolio

Strategies for 2007

Generally constructive on 2007 subprime

investment given guideline changes, tighter

appraisal processes and pricing

improvement

Housing price direction still unknown

Move up the capital structure

Allocate more capital to CDO equity (BBB mortgage

securities / CDS)

Sell a greater portion of loans or residuals that we

create

11

Portfolio Strategy - 2007

Consequences

Higher rated mortgage securities investments are held

in the taxable REIT subsidiary (TRS)

Doesn’t generate REIT taxable income, earnings in

TRS creates capital for reinvestment

Mortgage securities financed with CDOs have a much

longer duration than normal subprime residual

investments

Longer stream of earnings

Capital turns over less quickly

Selling more whole loans or residuals may shrink the

portfolio and reduce REIT taxable income

12

Taxable income dynamics

“REIT-only” taxable income drives dividend

distribution requirements

At year-end 2006 the tax/GAAP income difference

was approximately $370 million

We expect that this difference will reverse from 2007

– 2011 as the securitizations are called that caused the

high taxable income

Little or no taxable income from 2007 – 2011

Results in little / no dividend requirement to shareholders

13

Dividend strategy

(2008+)

Little / no required dividend distributions starting

in 2008

Dividend strategy set by NFI Board

Any dividends will be driven by our cost of equity and

investment opportunities

Can retain approximately $370M of capital in

REIT without paying taxes

Retained earnings in the REIT should build book value

starting in 2008

Given restrictions, is it in shareholder’s interests to

remain a REIT???

14

Q4 ’06

Earnings Review

15

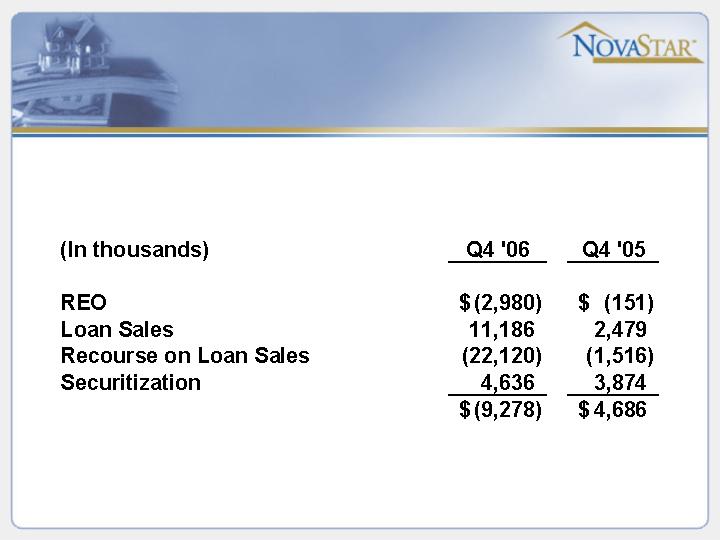

Gain on Sale

16

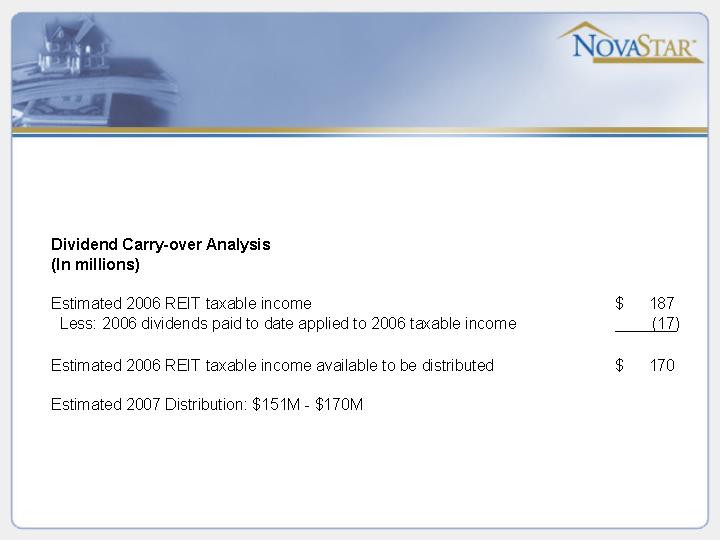

2007 Dividend Distributions

17

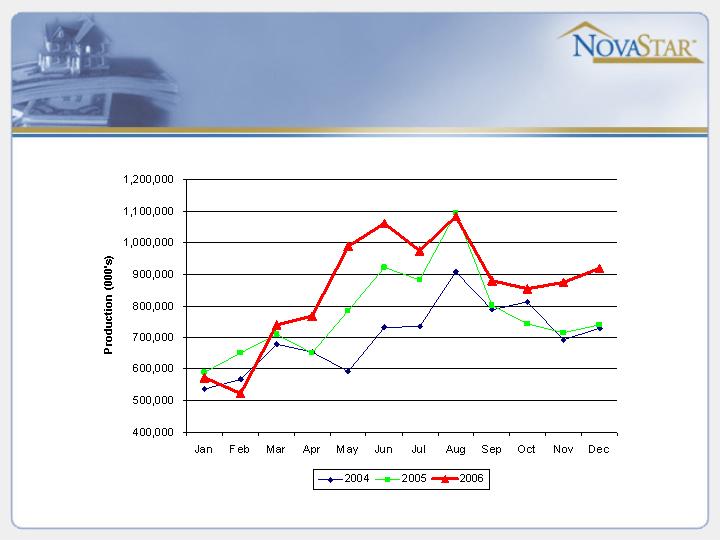

Production

10.2b

9.3b

8.4b

2006 production excludes Q1 MTA bulk

purchase of $991M

18

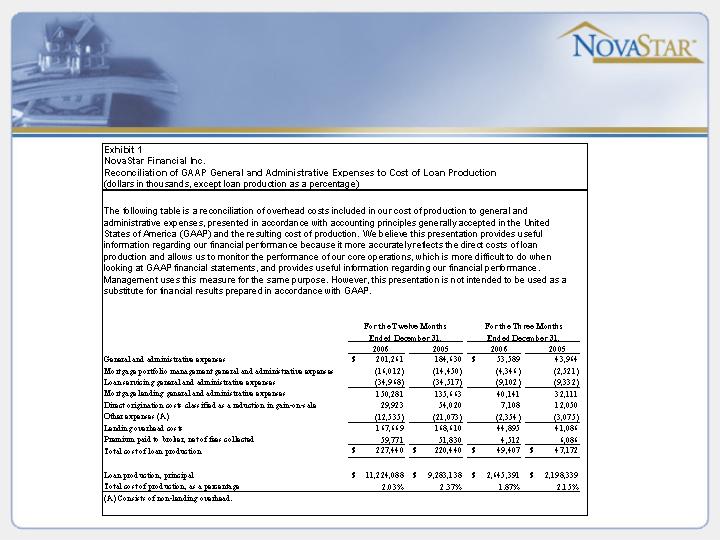

Cost of Production

See exhibit 1 for Reg. G disclosure on non-GAAP item

19

2007 Capital Planning

Liquidity

$154M of cash and available liquidity as of

Dec. ‘06

Cash on hand plus expected cash generated by

portfolio is sufficient for dividend payments during

the year and business operations

Additional equity required to grow the investment

portfolio and take advantage of good investment

opportunities in 2007

20

Questions

22