Deutsche Bank Securitization Conference

New York, NY

April 19, 2007

Forward looking disclosure

Certain matters set forth in this presentation contain forward-looking statements within the meaning of Section 21E of the Securities

Exchange Act of 1934, as amended, regarding management's beliefs, estimates, projections, and assumptions with respect to, among other

things, our future operations, business plans and strategies, as well as industry and market conditions, all of which are subject to change at

any time without notice. Actual results and operations for any future period may vary materially from those discussed herein. Some

important factors that could cause actual results to differ materially from those anticipated include: our ability to generate and maintain

sufficient liquidity on favorable terms; the size, frequency and structure of our securitizations; our ability to sell loans we originate in the

marketplace; impairments on our mortgage assets; increases in prepayment or default rates on our mortgage assets; increases in loan

repurchase requests; inability of potential borrowers to meet our underwriting guidelines; changes in assumptions regarding estimated

loan losses and fair value amounts; finalization of the amount and terms of any severance provided to terminated employees; finalization

of the accounting impact of our previously-announced reduction in workforce; events impacting the subprime mortgage industry in

general, including events impacting our competitors and liquidity available to the industry; the initiation of margin calls under our credit

facilities; the ability of our servicing operations to maintain high performance standards and maintain appropriate ratings from rating

agencies; our ability to generate acceptable origination volume while maintaining an acceptable level of overhead; residential property

values; our continued status as a REIT; interest rate fluctuations on our assets that differ from our liabilities; the outcome of litigation or

regulatory actions pending against us or other legal contingencies; our compliance with applicable local, state and federal laws and

regulations or opinions of counsel relating thereto and the impact of new local, state or federal legislation or regulations or opinions of

counsel relating thereto or court decisions on our operations; our ability to adapt to and implement technological changes; compliance

with new accounting pronouncements; our ability to successfully integrate acquired businesses or assets with our existing business; the

impact of general economic conditions; and the risks that are from time to time included in our filings with the SEC, including our Annual

Report on Form 10-K for the year ended December 31, 2006. Other factors not presently identified may also cause actual results to differ.

Words such as "believe," "expect," "anticipate," "promise," "plan," and other expressions or words of similar meanings, as well as future

or conditional verbs such as "will," "would," "should," "could," or "may" are generally intended to identify forward-looking statements.

This presentation speaks only as of its date and we expressly disclaim any duty to update the information herein.

2

Overview

Founded: June, 1996

IPO: October, 1997 (NYSE: NFI)

NovaStar is currently structured as a REIT

Parent company does not pay corporate taxes

Focus is on being a portfolio investor vs. pure mortgage banking

Top 25 subprime residential mortgage originator, servicer and issuer

Wholesale & Retail originator with a combined current run rate of

approximately $300 million per month

Servicer rating of “Strong” by S&P

Completed 39 ABS transactions, total issuance $37 billion

Disciplined underwriting approval through automated system manages

to a 4.0-6.0% (pre-MI) loss under normal market conditions

3

Corporate update

Liquidity

Received a commitment for an additional $100 million of liquidity collateralized by

mortgage servicing rights and residuals

EPD repurchases from whole loan sales

All EPD buybacks have either already taken place or have been fully reserved for

Anticipate most of 2007 production will be securitized

Retained Deutsche Bank as a financial advisor to help explore and

evaluate strategic alternatives

4

2006 vintage

Tone of the market was being driven by irrational competitors

Too great of a focus on volume rather than profitability

Guidelines became outdated for changing housing market

Delinquencies

December appears to have been the peak

We have seen month over month improvement in early stage delinquencies throughout

the first quarter. Rat in snake?

Mortgage Insurance

Performing as expected even in a down market

No material change in rescissions

While its early, performance for NovaStar’s 2006 vintage appears to

be in line or better than most issuers on a pre-mi basis

5

Delinquency trends

6

Month to Month Change for All 2006 Securitizations

(excluding 2006-MTA1)

Status

Nov-Dec

Dec-Jan

Jan-Feb

Feb-Mar

1-29

1.39%

-1.15%

-0.22%

-0.45%

30-59

0.13%

0.16%

-0.34%

-0.21%

60-89

0.17%

0.01%

0.17%

-0.16%

90+

0.13%

0.15%

0.17%

0.23%

FC

0.61%

0.86%

0.45%

0.54%

REO

0.11%

0.31%

0.40%

0.54%

MI claims summary

7

Loan Resolutions/Liquidations insured by Radian, PMI or MGIC

Data thru 2/28/2007

Resolution Type

Loans

Original

Balance

% by #

% by $

Severity

before MI

Severity

after MI

MI Benefit

MI Paid

2,864

$314,098,398

76.4%

68.2%

39.1%

8.2%

30.9%

MI Acquired

328

$55,874,343

8.7%

12.1%

19.2%

3.2%

16.0%

Not Filed - no loss

265

$39,565,034

7.1%

8.6%

-1.3%

-1.3%

0.0%

Not Filed - other

42

$4,532,621

1.1%

1.0%

41.3%

41.3%

0.0%

Settlement

83

$14,062,467

2.2%

3.1%

43.5%

26.7%

16.8%

Rescinded

169

$32,299,089

4.5%

7.0%

45.8%

45.8%

0.0%

3,751

$460,431,952

100.0%

100.0%

33.9%

10.3%

23.5%

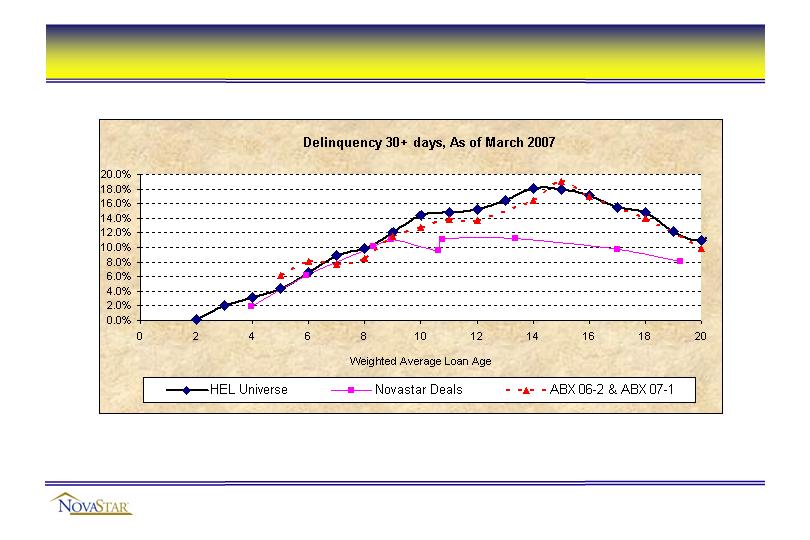

NovaStar securitizations vs. the industry

Notes:

1. Data source: NovaStar and Intex.

2. HEL Universe consists of 300+ deals for which NovaStar has loan level data and has deemed to be typical HEL transactions.

3. NovaStar Deals represent 2005-3 through 2007-1.

8

Changes to 2007 vintage

Screening for layered risk by moving the loss model to front end

Tighter guidelines

Eliminated 80/20’s

Increased minimum ficos in higher LTV buckets

Higher coupons

Less competition

Retail channel expected to represent a larger percent of production

Whole loan prices and ABS bond spreads need to readjust

CDO investors appear to be sitting on the sidelines

9

Recent production trends

10

1

2

1 Excludes MTA production. 2 OTS method. Month refers to first payment date, not origination date.

Oct '06

Nov '06

Dec '06

Jan '07

Feb '07

Mar '07

Production (000's)

$852,105

$872,895

$917,378

$739,226

$386,249

$314,741

WAC

8.91%

8.85%

8.74%

8.85%

8.81%

9.07%

FICO

624

626

626

624

617

618

LTV

82.7%

82.9%

82.7%

82.9%

81.6%

80.6%

CLTV

86.5%

86.6%

86.3%

86.6%

84.2%

83.2%

2nd Lien

4.4%

4.6%

4.8%

4.5%

3.1%

3.3%

ARMs

77.0%

75.7%

73.1%

75.0%

69.6%

67.3%

Interest Only

11.8%

11.2%

11.5%

12.4%

9.8%

8.4%

40/30

22.1%

23.8%

21.9%

23.7%

27.4%

29.1%

Non-Full Doc

52.3%

53.3%

50.9%

51.5%

45.2%

43.9%

NOO

6.7%

5.9%

5.5%

5.8%

4.9%

3.7%

Retail

9%

7%

10%

17%

28%

37%

Wholesale

91%

93%

90%

83%

72%

63%

FPD

2.85%

3.36%

2.76%

1.97%

1.70%

NA

Servicing

$16 billion portfolio

Total staff of approximately 250

Reduced average loans per collector metric from 225 to 150 (90 day bucket)

ARM conversion training

Modifications

Primarily rate adjustments which make it affordable for borrower to stay in the home

Running at about twice the rate of 2006

Geographically focused

LaunchPoint

Since inception have assisted in placing over 1,200 borrowers in new jobs

11

Additional data

Complete production and performance data can be found on

NovaStar’s websites:

http://www.novastarbondinvestors.com/

Static pool performance data

Offering documents

Bond remittance statements

http://www.novastarmortgage.com/corporate/

Monthly production reports

Mortgage insurance claim statistics

12