Exhibit 99.2

NovaStar Financial (NYSE-NFI) www.novastarmortgage.com

2005 Second Quarter Earnings Conference Call July 29, 2005

Safe Harbor Statement

Certain matters discussed in this presentation may constitute forward-looking statements within the meaning of the federal securities laws. Forward looking statements are those that predict or describe future events and that do not relate solely to historical matters. Forward looking statements are subject to risks and uncertainties and certain factors can cause actual results to differ materially from those anticipated. Some important factors that could cause actual results to differ materially from those anticipated include: our ability to generate sufficient liquidity on favorable terms; the size and frequency of our securitizations; interest rate fluctuations on our assets that differ from our liabilities; increases in prepayment or default rates on our mortgage assets; changes in assumptions regarding estimated loan losses and fair value amounts, changes in origination and resale pricing of mortgage loans; our compliance with applicable local, state and federal laws and regulations and the impact of new local, state or federal legislation or regulations or court decisions on our operations; the initiation of margin calls under our credit facilities; the ability of our servicing operations to maintain high performance standards and maintain appropriate ratings from rating agencies; our ability to expand origination volume while maintaining an acceptable level of overhead; our ability to adapt to and implement technological changes; the stability of residual property values; the outcome of litigation or regulatory actions pending against us; the impact of general economic conditions; and the risks that are from time to time included in our filings with the SEC, including our 2004 Annual Report on Form 10-K. Other factors not presently identified may also cause actual results to differ. This document speaks only as of its date and we expressly disclaim any duty to update the information herein.

2

Opening Comments

Scott Hartman, CEO

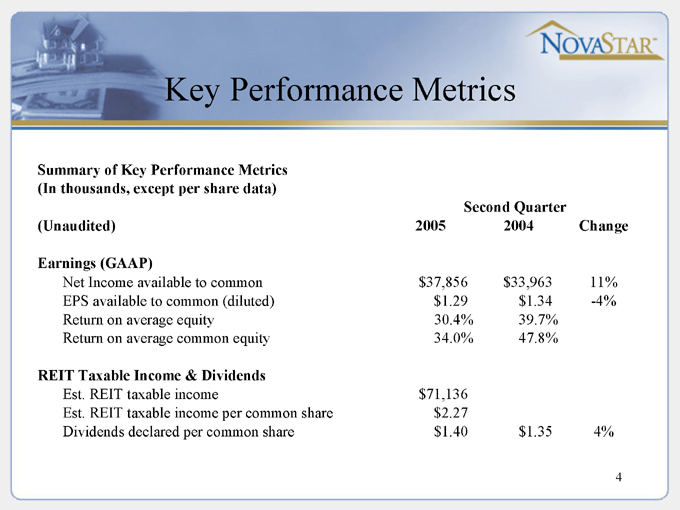

Key Performance Metrics

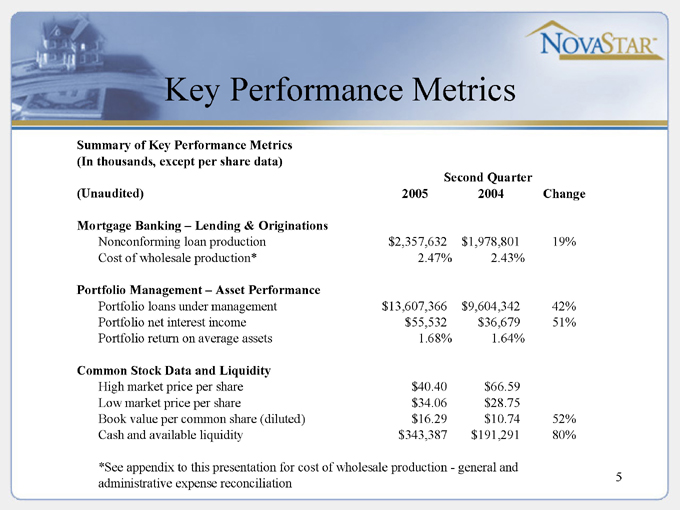

Summary of Key Performance Metrics (In thousands, except per share data) Second Quarter

(Unaudited) 2005 2004 Change

Earnings (GAAP)

Net Income available to common $37,856 $33,963 11%

EPS available to common (diluted) $1.29 $1.34 -4%

Return on average equity 30.4% 39.7%

Return on average common equity 34.0% 47.8%

REIT Taxable Income & Dividends

Est. REIT taxable income $71,136

Est. REIT taxable income per common share $2.27

Dividends declared per common share $1.40 $1.35 4%

4

Key Performance Metrics

Summary of Key Performance Metrics

(In thousands, except per share data)

Second Quarter

(Unaudited) 2005 2004 Change

Mortgage Banking – Lending & Originations

Nonconforming loan production $2,357,632 $1,978,801 19%

Cost of wholesale production* 2.47% 2.43%

Portfolio Management – Asset Performance

Portfolio loans under management $13,607,366 $9,604,342 42%

Portfolio net interest income $55,532 $36,679 51%

Portfolio return on average assets 1.68% 1.64%

Common Stock Data and Liquidity

High market price per share $40.40 $66.59

Low market price per share $34.06 $28.75

Book value per common share (diluted) $16.29 $10.74 52%

Cash and available liquidity $343,387 $191,291 80%

*See appendix to this presentation for cost of wholesale production—general and administrative expense reconciliation

5

Mortgage Banking

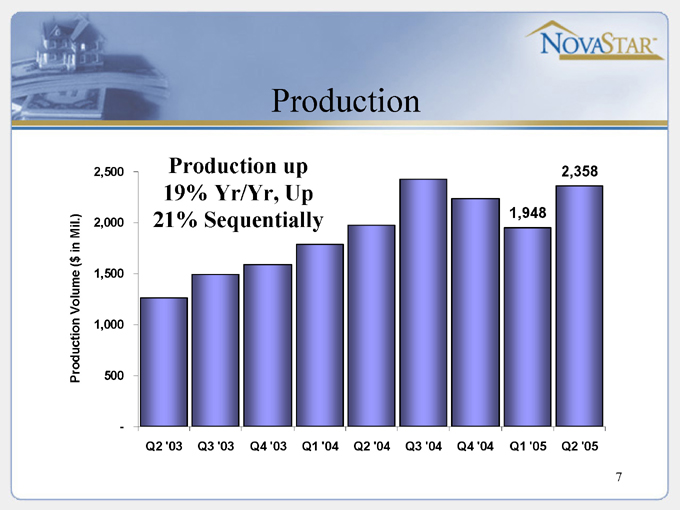

Production

Production Volume ($ in Mil.)

2,500 2,000 1,500 1,000 500 -

Q2 ‘03 Q3 ‘03 Q4 ‘03 Q1 ‘04 Q2 ‘04 Q3 ‘04 Q4 ‘04 Q1 ‘05 Q2 ‘05

Production up 19% Yr/Yr, Up 21% Sequentially

1,948

2,358 7

Production Credit Characteristics

Weighted Avg. FICO

655 650 645 640 635 630 625 620 615 610 605

Q2 ‘03

Q3’03

Q4 ‘03

Q1’04

Q2 ‘04

Q3 ‘04

Q4 ‘04

Q1 ‘05

Q2 ‘05

629

632

Weighted Avg. LTV

85.0 84.0 83.0 82.0 81.0 80.0 79.0 78.0 77.0 76.0 75.0

Q2’ 03 Q3 ‘03

Q4 ‘03

Q1 ‘04

Q2 ‘04

Q3 ‘04

Q4 ‘04

Q1 ‘05

Q2 ‘05

82.1

82.3

8

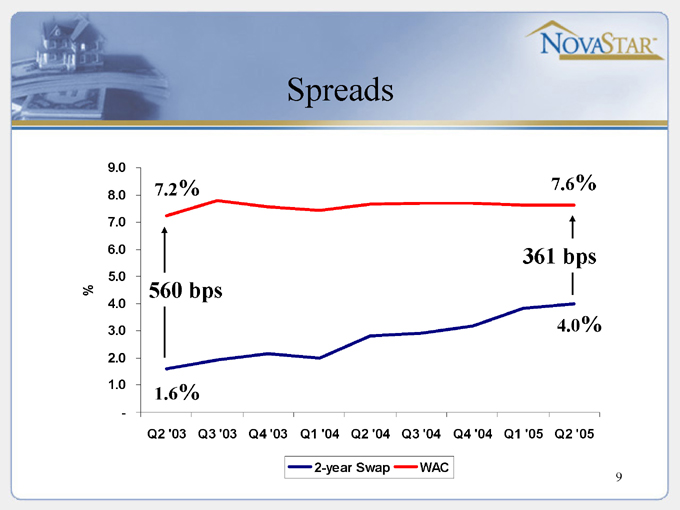

Spreads

%

9.0

8.0 7.0

6.0 5.0

4.0 3.0

2.0 1.0

-

Q2 ‘03 Q3 ‘03 Q4 ‘03 Q1 ‘04 Q2 ‘04 Q3 ‘04 Q4 ‘04 Q1 ‘05 Q2 ‘05

7.2%

560 bps

1.6%

7.6%

361 bps

4.0% 2-year Swap WAC 9

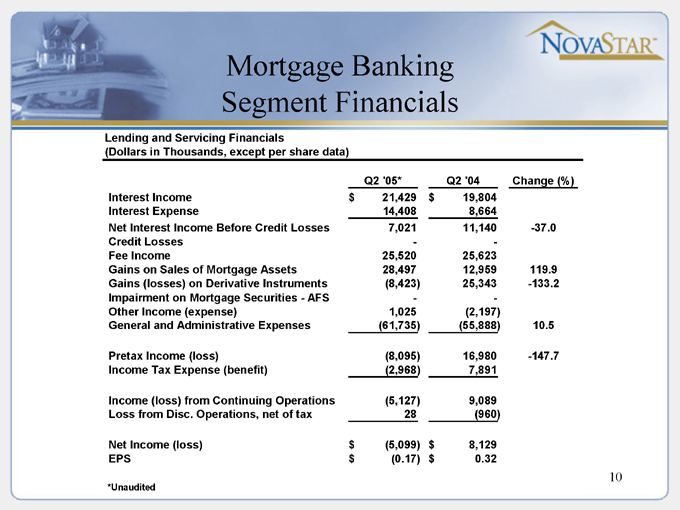

Mortgage Banking Segment Financials

Lending and Servicing Financials

(Dollars in Thousands, except per share data)

Q2 ‘05* Q2 ‘04 Change (%)

Interest Income $21,429 $19,804

Interest Expense 14,408 8,664

Net Interest Income Before Credit Losses 7,021 11,140 -37.0

Credit Losses - - -

Fee Income 25,520 25,623

Gains on Sales of Mortgage Assets 28,497 12,959 119.9

Gains (losses) on Derivative Instruments (8,423) 25,343 -133.2

Impairment on Mortgage Securities—AFS - -

Other Income (expense) 1,025 (2,197)

General and Administrative Expenses (61,735) (55,888) 10.5

Pretax Income (loss) (8,095) 16,980 - -147.7

Income Tax Expense (benefit) (2,968) 7,891

Income (loss) from Continuing Operations (5,127) 9,089

Loss from Disc. Operations, net of tax 28 (960)

Net Income (loss) $(5,099) $8,129

EPS $(0.17) $0.32

*Unaudited

10

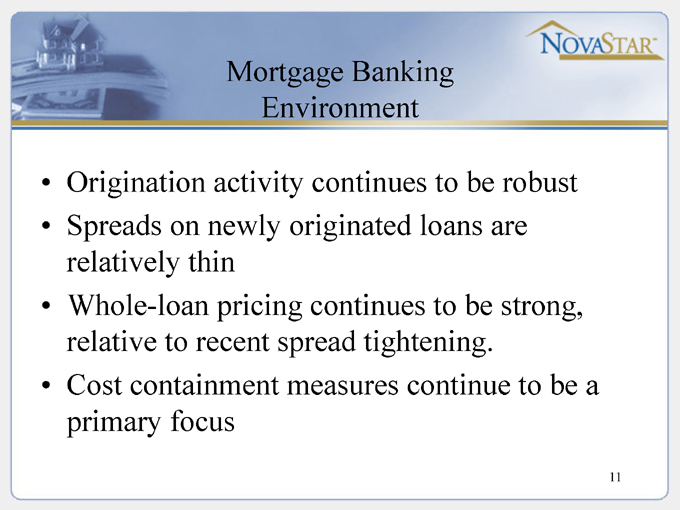

Mortgage Banking Environment

Origination activity continues to be robust

Spreads on newly originated loans are relatively thin

Whole-loan pricing continues to be strong, relative to recent spread tightening.

Cost containment measures continue to be a primary focus

11

Portfolio Management

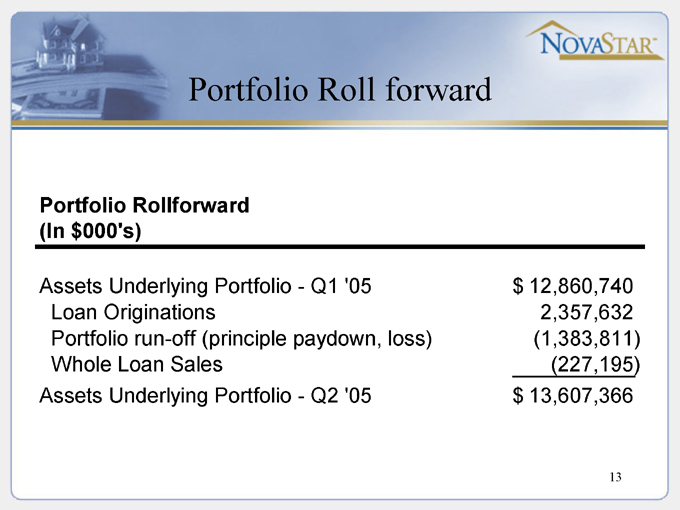

Portfolio Roll forward

Portfolio Rollforward (In $000’s)

Assets Underlying Portfolio—Q1 ‘05 $12,860,740

Loan Originations 2,357,632

Portfolio run-off (principle paydown, loss) (1,383,811)

Whole Loan Sales (227,195)

Assets Underlying Portfolio—Q2 ‘05 $13,607,366

13

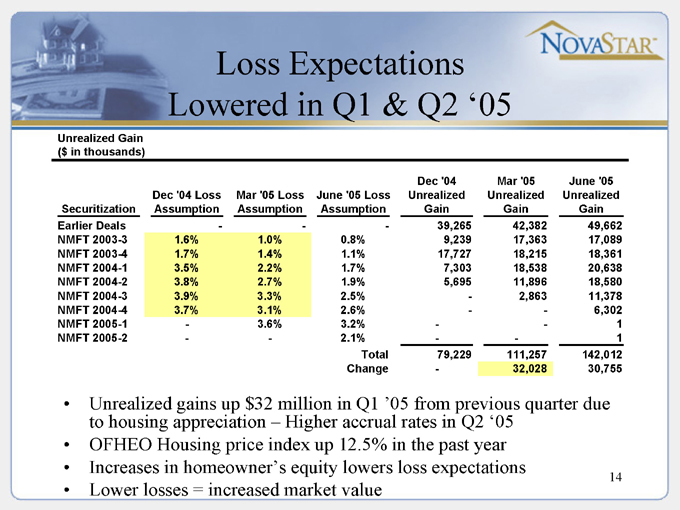

Loss Expectations Lowered in Q1 & Q2 ‘05

Unrealized Gain ($ in thousands)

Securitization Dec ‘04 Loss Assumption Mar ‘05 Loss Assumption June ‘05 Loss Assumption Dec ‘04 Unrealized Gain Mar ‘05 Unrealized Gain June ‘05 Unrealized Gain

Earlier Deals - - - 39,265 42,382 49,662

NMFT 2003-3 1.6% 1.0% 0.8% 9,239 17,363 17,089

NMFT 2003-4 1.7% 1.4% 1.1% 17,727 18,215 18,361

NMFT 2004-1 3.5% 2.2% 1.7% 7,303 18,538 20,638

NMFT 2004-2 3.8% 2.7% 1.9% 5,695 11,896 18,580

NMFT 2004-3 3.9% 3.3% 2.5% - 2,863 11,378

NMFT 2004-4 3.7% 3.1% 2.6% - - 6,302

NMFT 2005-1 - 3.6% 3.2% - - 1

NMFT 2005-2 - - 2.1% - - 1

Total 79,229 111,257 142,012

Change - 32,028 30,755

Unrealized gains up $32 million in Q1 ‘05 from previous quarter due to housing appreciation – Higher accrual rates in Q2 ‘05 OFHEO Housing price index up 12.5% in the past year Increases in homeowner’s equity lowers loss expectations Lower losses = increased market value

14

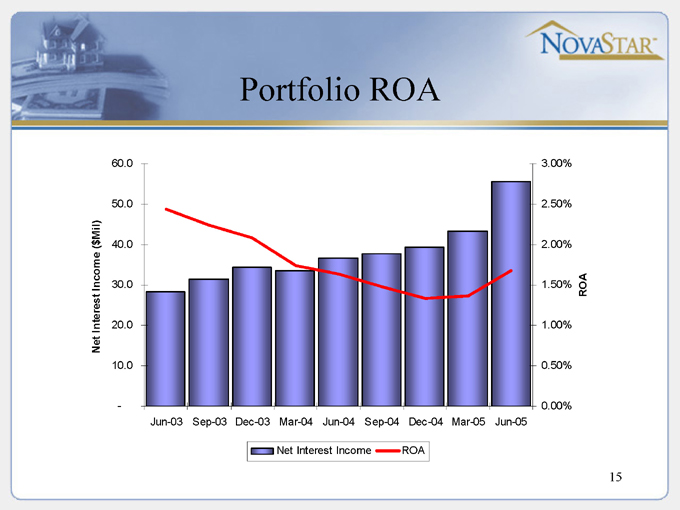

Portfolio ROA

Net Interest Income ($Mil)

60.0 50.0 40.0 30.0 20.0 10.0 -

Jun-03 Sep-03 Dec-03 Mar-04 Jun-04 Sep-04 Dec-04 Mar-05 Jun-05

3.00% 2.50% 2.00% 1.50% 1.00% 0.50% 0.00%

ROA

Net Interest Income

ROA

15

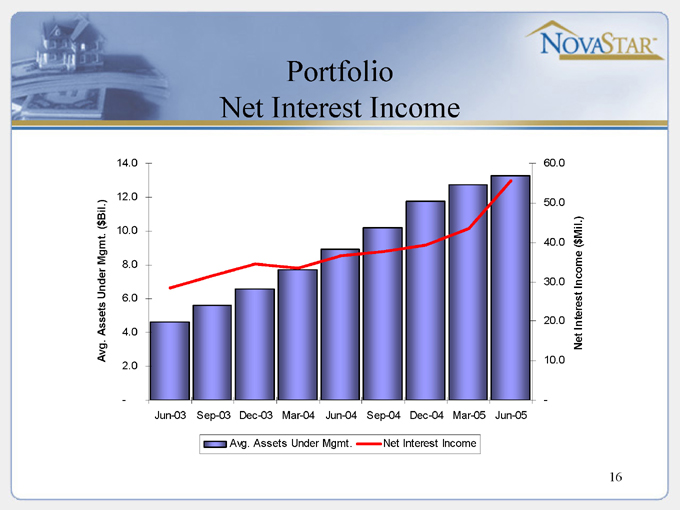

Portfolio Net Interest Income

Avg. Assets Under Mgmt. ($Bil.)

14.0 12.0 10.0 8.0 6.0 4.0 2.0 -

Jun-03 Sep-03 Dec-03 Mar-04 Jun-04 Sep-04 Dec-04 Mar-05 Jun-05

60.0 50.0 40.0 30.0 20.0 10.0 -

Net Interest Income ($Mil.)

Avg. Assets Under Mgmt.

Net Interest Income

16

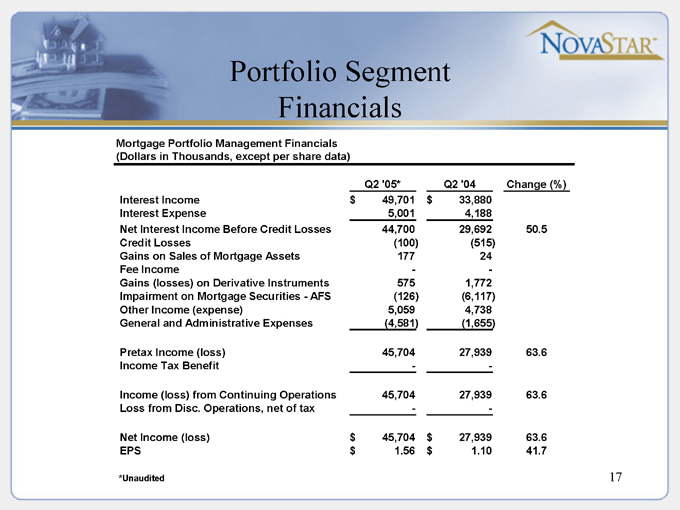

Portfolio Segment Financials

Mortgage Portfolio Management Financials (Dollars in Thousands, except per share data)

Q2 ‘05* Q2 ‘04 Change (%)

Interest Income $49,701 $33,880

Interest Expense 5,001 4,188

Net Interest Income Before Credit Losses 44,700 29,692 50.5

Credit Losses (100) (515)

Gains on Sales of Mortgage Assets 177 24

Fee Income - -

Gains (losses) on Derivative Instruments 575 1,772

Impairment on Mortgage Securities—AFS (126) (6,117)

Other Income (expense) 5,059 4,738

General and Administrative Expenses (4,581) (1,655)

Pretax Income (loss) 45,704 27,939 63.6

Income Tax Benefit - -

Income (loss) from Continuing Operations 45,704 27,939 63.6

Loss from Disc. Operations, net of tax - -

Net Income (loss) $45,704 $27,939 63.6

EPS $1.56 $1.10 41.7

*Unaudited

17

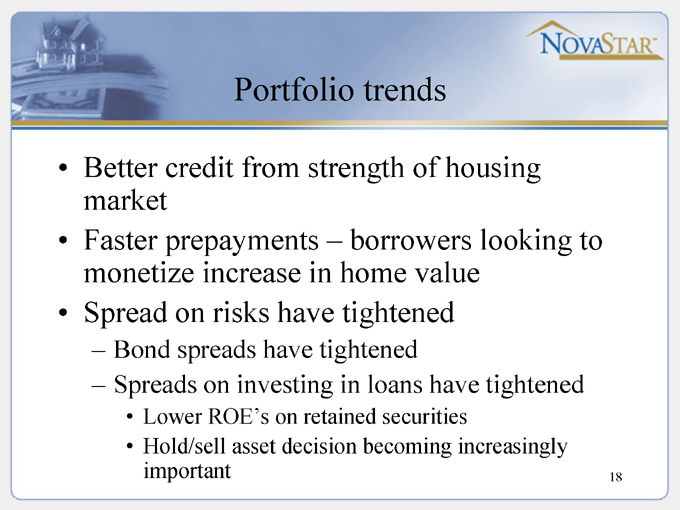

Portfolio trends

Better credit from strength of housing market Faster prepayments – borrowers looking to monetize increase in home value Spread on risks have tightened

Bond spreads have tightened

Spreads on investing in loans have tightened

Lower ROE’s on retained securities

Hold/sell asset decision becoming increasingly important

18

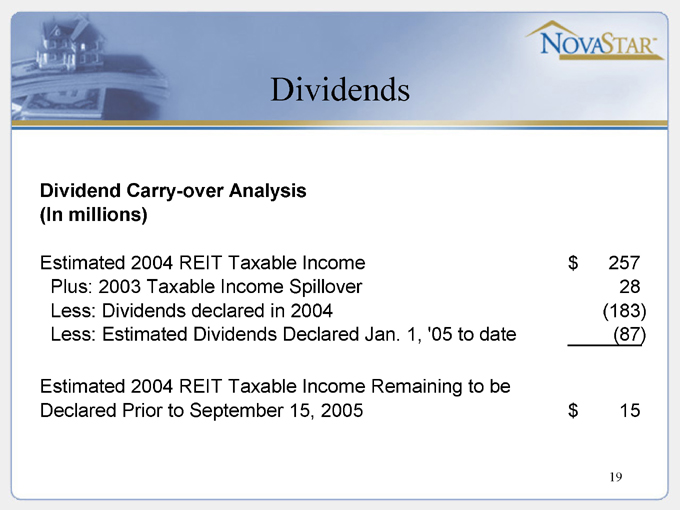

Dividends

Dividend Carry-over Analysis (In millions)

Estimated 2004 REIT Taxable Income $257

Plus: 2003 Taxable Income Spillover 28

Less: Dividends declared in 2004 (183)

Less: Estimated Dividends Declared Jan. 1, ‘05 to date (87)

Estimated 2004 REIT Taxable Income Remaining to be

Declared Prior to September 15, 2005 $15

19

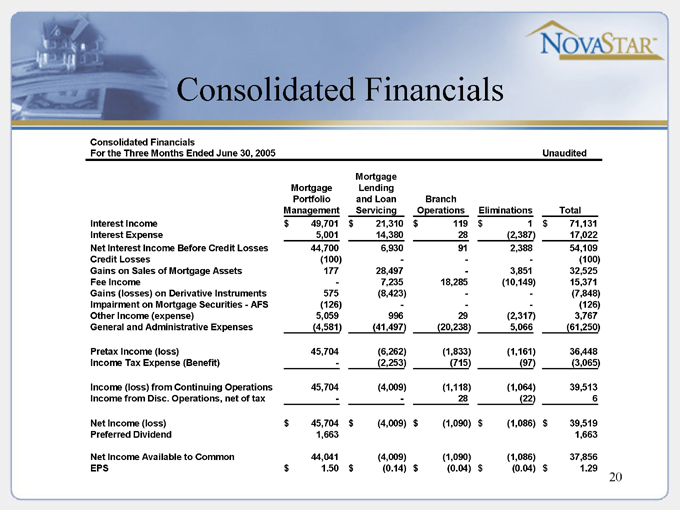

Consolidated Financials

Consolidated Financials

For the Three Months Ended June 30, 2005 Unaudited

Mortgage Portfolio Management Mortgage Lending and Loan Servicing Branch Operations Eliminations Total

Interest Income $49,701 $21,310 $119 $1 $71,131

Interest Expense 5,001 14,380 28 (2,387) 17,022

Net Interest Income Before Credit Losses 44,700 6,930 91 2,388 54,109

Credit Losses (100) - - - (100)

Gains on Sales of Mortgage Assets 177 28,497 - 3,851 32,525

Fee Income - 7,235 18,285 (10,149) 15,371

Gains (losses) on Derivative Instruments 575 (8,423) - - (7,848)

Impairment on Mortgage Securities—AFS (126) - - - (126)

Other Income (expense) 5,059 996 29 (2,317) 3,767

General and Administrative Expenses (4,581) (41,497) (20,238) 5,066 (61,250)

Pretax Income (loss) 45,704 (6,262) (1,833) (1,161) 36,448

Income Tax Expense (Benefit) - (2,253) (715) (97) (3,065)

Income (loss) from Continuing Operations 45,704 (4,009) (1,118) (1,064) 39,513

Income from Disc. Operations, net of tax - - 28 (22) 6

Net Income (loss) $45,704 $(4,009) $(1,090) $(1,086) $39,519

Preferred Dividend 1,663 1,663

Net Income Available to Common 44,041 (4,009) (1,090) (1,086) 37,856

EPS $1.50 $(0.14) $(0.04) $(0.04) $1.29

20

Questions

Appendix

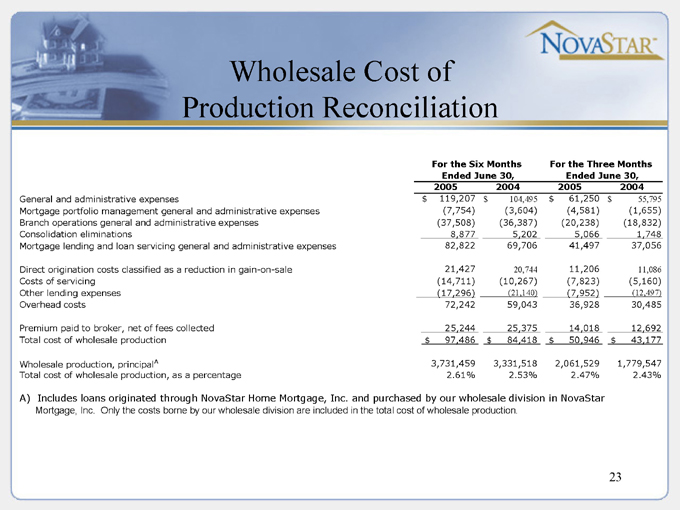

Wholesale Cost of Production Reconciliation

For the Six Months Ended June 30, For the Three Months Ended June 30,

2005 2004 2005 2004

General and administrative expenses $119,207 $104,495 $61,250 $55,795

Mortgage portfolio management general and administrative expenses (7,754) (3,604) (4,581) (1,655)

Branch operations general and administrative expenses (37,508) (36,387) (20,238) (18,832)

Consolidation eliminations 8,877 5,202 5,066 1,748

Mortgage lending and loan servicing general and administrative expenses 82,822 69,706 41,497 37,056

Direct origination costs classified as a reduction in gain-on-sale 21,427 20,744 11,206 11,086

Costs of servicing (14,711) (10,267) (7,823) (5,160)

Other lending expenses (17,296) (21,140) (7,952) (12,497)

Overhead costs 72,242 59,043 36,928 30,485

Premium paid to broker, net of fees collected 25,244 25,375 14,018 12,692

Total cost of wholesale production $97,486 $84,418 $50,946 $43,177

Wholesale production, principalA 3,731,459 3,331,518 2,061,529 1,779,547

Total cost of wholesale production, as a percentage 2.61% 2.53% 2.47% 2.43%

A) Includes loans originated through NovaStar Home Mortgage, Inc. and purchased by our wholesale division in NovaStar

Mortgage, Inc. Only the costs borne by our wholesale division are included in the total cost of wholesale production.

23