UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number 811-07959

Advisors Series Trust

(Exact name of registrant as specified in charter)

(Exact name of registrant as specified in charter)

615 East Michigan Street

Milwaukee, WI 53202

(Address of principal executive offices) (Zip code)

(Address of principal executive offices) (Zip code)

Jeffrey T. Rauman, President/Chief Executive Officer

Advisors Series Trust

c/o U.S. Bancorp Fund Services, LLC

777 East Wisconsin Avenue, 5th Floor

Milwaukee, WI 53202

(Name and address of agent for service)

(Name and address of agent for service)

(626) 914-7363

Registrant's telephone number, including area code

Date of fiscal year end: February 28, 2022

Date of reporting period: August 31, 2021

Item 1. Reports to Stockholders.

| (a) | [Insert full text of semi-annual or annual report here] |

| Pzena Funds | |

| Semi-Annual Report | |

| AUGUST 31, 2021 | |

PZENA MID CAP VALUE FUND

Investor Class PZVMX

Institutional Class PZIMX

PZENA EMERGING MARKETS VALUE FUND

Investor Class PZVEX

Institutional Class PZIEX

PZENA SMALL CAP VALUE FUND

Investor Class PZVSX

Institutional Class PZISX

PZENA INTERNATIONAL SMALL CAP VALUE FUND

Investor Class PZVIX

Institutional Class PZIIX

PZENA INTERNATIONAL VALUE FUND

Investor Class PZVNX

Institutional Class PZINX

1-844-PZN-1996 (1-844-796-1996) • www.pzenafunds.com

Table of Contents

Letter to Shareholders | 1 | ||

Pzena Funds Commentary | |||

| Pzena Mid Cap Value Fund | 2 | ||

| Pzena Emerging Markets Value Fund | 4 | ||

| Pzena Small Cap Value Fund | 7 | ||

| Pzena International Small Cap Value Fund | 9 | ||

| Pzena International Value Fund | 11 | ||

Pzena Mid Cap Value Fund | |||

| Portfolio Allocation | 13 | ||

| Schedule of Investments | 14 | ||

Pzena Emerging Markets Value Fund | |||

| Portfolio Allocation | 15 | ||

| Schedule of Investments | 16 | ||

| Portfolio Diversification | 18 | ||

Pzena Small Cap Value Fund | |||

| Portfolio Allocation | 19 | ||

| Schedule of Investments | 20 | ||

Pzena International Small Cap Value Fund | |||

| Portfolio Allocation | 22 | ||

| Schedule of Investments | 23 | ||

| Portfolio Diversification | 25 | ||

Pzena International Value Fund | |||

| Portfolio Allocation | 26 | ||

| Schedule of Investments | 27 | ||

| Portfolio Diversification | 29 | ||

Statements of Assets and Liabilities | 30 | ||

Statements of Operations | 32 | ||

Statements of Changes in Net Assets | |||

| Pzena Mid Cap Value Fund | 34 | ||

| Pzena Emerging Markets Value Fund | 35 | ||

| Pzena Small Cap Value Fund | 36 | ||

| Pzena International Small Cap Value Fund | 37 | ||

| Pzena International Value Fund | 38 | ||

Financial Highlights | |||

| Pzena Mid Cap Value Fund | 39 | ||

| Pzena Emerging Markets Value Fund | 41 | ||

| Pzena Small Cap Value Fund | 43 | ||

| Pzena International Small Cap Value Fund | 45 | ||

| Pzena International Value Fund | 47 | ||

Notes to Financial Statements | 49 | ||

Expense Example | 59 | ||

Approval of Investment Advisory Agreement | 61 | ||

Notice to Shareholders | 63 | ||

Privacy Notice | 64 |

Dear Shareholder:

Before the start of the reporting period, optimism, driven by COVID-19 vaccine success and stimulus packages, led global markets higher. Since the end of February, as COVID-19 concerns gradually eased, global equity markets mostly continued their positive trajectories, albeit less intensely than in the second half of 2020.

Value, which started to outperform in the fourth quarter of 2020, continued to lead markets higher in early 2021 on expectations of a sustained economic recovery (and, indeed, consumer spending increased as COVID-19 restrictions were relaxed) due in large part to both fiscal and monetary support from governments and central banks around the world, and on rising inflation expectations, which saw bond yields move higher.

Our Funds each started out strongly, as market sentiment favored companies that stood to benefit from economic reopening over many of the lockdown winners. Additionally, the “reflation trade,” driven by massive amounts of central bank stimulus, led to inflationary pressure and rising interest rates, boosting many companies in the financials and energy sectors.

But as we got deeper into the summer, sentiment shifted back to large cap growth names in many areas of the world, as uncertainties over reopenings grew as the Delta variant spread worldwide. From June through August, each of our Funds, except for the Emerging Markets Value Fund, gave back a good percentage of the outperformance they had built up in the first three months of the period.

Putting the six months together, our Funds ended with mixed results as large caps were favored over small caps, and growth outperformed value across much of the developed world. Value, however, was stronger among U.S. small cap and emerging markets stocks.

The spread of the Delta variant, particularly in India and subsequently East Asia, also pressured emerging market equities. Yet, while the MSCI EM Index was down slightly less than 1%, the MSCI Emerging Markets Value series outpaced the growth index by 953 basis points (USD). Importantly, the MSCI EM Index excluding China posted a strong 10.08% gain. The Chinese Communist Party’s abrupt regulatory crackdown that ensued in July took many investors by surprise, not only due to its swiftness, but because for the better part of the past 40 years, China’s ruling party had seemingly been willing to set aside a strict socialist agenda to prioritize growing the economy.

As economies continue to reopen, we expect the cost cutting and restructuring actions taken by management teams during the pandemic to continue to drive operating margin expansion as revenues recover. The current valuation gap between growth and value stocks globally is still extremely wide by historical standards, and the Funds remain heavily weighted toward cyclical stocks – most notably in financials, industrials, and consumer discretionary. We remain confident in current positioning given the robustness of the companies’ underlying franchises and balance sheets.

As always, we are committed to our philosophy of value investing with a long-term outlook, and we encourage our Fund investors to take a similar view.

The following pages review investment decisions and current positioning. Please take a few minutes to read these letters.

If you have questions about your Pzena Fund’s portfolio, please get in touch with your advisor or a member of our team of registered representatives. We thank you for investing with us.

Best regards,

Pzena Investment Management, LLC

Past performance does not guarantee future results. Index performance is not indicative of fund performance. One cannot invest directly in an index.

Mutual fund investing involves risk. Principal loss is possible.

Basis point – One-hundredth of a percentage point (0.01%).

1

Pzena Mid Cap Value Fund

Commentary

August 2021

Average Annual Total Returns for the Semi-Annual Period Ended August 31, 2021.

| Since | ||||||

| Three | Six | One | Three | Five | Inception | |

Months(1) | Months(1) | Year(1) | Years | Years | (3/31/2014) | |

| Pzena Mid Cap Value Fund – Investor Class (PZVMX) | -3.63% | 11.23% | 66.14% | 10.58% | 12.02% | 9.36% |

| Pzena Mid Cap Value Fund – Institutional Class (PZIMX) | -3.55% | 11.50% | 66.80% | 10.97% | 12.39% | 9.70% |

Russell Midcap® Value Index | 1.58% | 14.20% | 44.50% | 11.37% | 11.52% | 10.00% |

| (1) | Not annualized. |

Performance data quoted represents past performance and does not guarantee future results. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance of the Fund may be lower or higher than the performance quoted. Performance data current to the most recent month-end may be obtained by calling 844.PZN.1996 (844.796.1996).

PZVMX Expense Ratio – Gross: 1.41%

PZVMX Expense Ratio – Net: 1.25%*

PZIMX Expense Ratio – Gross: 1.06%

PZIMX Expense Ratio – Net: 0.90%*

Expense ratios shown are as of the Fund’s registration statement dated June 28, 2021.

| * | Pzena Investment Management, LLC, the Fund’s investment adviser, has contractually agreed to waive a portion or all of its management fees and pay Fund expenses through at least June 28, 2022. |

Building on late-2020 momentum, value stocks continued to surge in the first half of 2021 as the vaccine rollout accelerated. Massive fiscal and monetary stimulus drove consumer spending, setting the stage for a powerful rebound in the economy. Investor preference abruptly shifted from value to growth in June, as the Fed spoke about potential tapering, resulting in a significant flattening of the yield curve, and the Russell Midcap Value Index posted a negative return for the first time in five months. Domestic equities came under pressure again in July as the spread of the COVID-19 Delta variant in both Asia and the U.S. raised concerns about the potential economic implications, impacting shares of cyclical companies the most. Value’s summer hiatus led the Fund to underperform the index, with energy the largest detractor, while industrials, financials, and consumer discretionary drove gains.

Oil service companies Halliburton, NOV, and Baker Hughes were the worst performers in the period – falling victim to the summer crude price selloff that was prompted by concerns over global demand growth, as the Delta variant continued to spread. Halliburton nonetheless reported solid 2Q21 results, with margins and cash flow coming in ahead of consensus expectations, while sales were up year-over-year and on a sequential basis; importantly, management was bullish on its 2H21 outlook for the industry as a whole. NOV similarly reported strong 2Q21 results on the back of better revenue, EBITDA and cash flow, whereas Baker Hughes’ reported earnings per share came in below expectations due to higher taxes; but sales, operating income, and cash flow were all strong.

Olin Corp., a chemical producer of chlorine derivatives and caustic soda, was the portfolio’s top individual performer, as the company continues to realize pricing improvements amid tight market conditions. The new CEO’s strategy around rationalizing supply and maximizing the size of molecules is yielding positive results at a faster pace than anticipated, and future earnings growth looks encouraging assuming the industrial recovery remains intact. Management expects conditions to continue to improve in the third quarter, and as a result, they raised FY21 EBITDA guidance to at least $2.1bn, up from prior guidance of $1.8bn to $2.1bn. Global insurer American International Group was higher after reporting 2Q21 results that revealed tangible progress in the turnaround of its core General Insurance (P&C) unit, while Life & Retirement also exhibited strong performance. Lastly, defense contractor and private jet manufacturer Textron’s shares rose after the company reported two consecutive quarters of strong results due to robust commercial demand for both its Bell helicopters and business jets, resulting in the company’s highest level of backlog since before the global financial crisis.

During the period, we added IT services company Cognizant Technology Solutions to the portfolio. The key reason why Cognizant’s valuation looks discounted relative to its historical return profile is that the company has been underperforming peers in recent history in terms of both growth and margin trajectory – namely because prior management focused on margins at the expense of growth while competitors were moving up the learning curve and investing in digital capabilities. As a result, Cognizant has been undergoing a

2

Pzena Mid Cap Value Fund

Commentary (Continued)

August 2021

digital investment/restructuring period in an effort to catch up to its competitors, but management believes that its spending phase has peaked, restructuring charges are winding down, and importantly, backlog trends support the notion that its investments should start to pay off in the near future. We believe the relatively new management team will be able to stabilize the business and slow employee attrition, and margins will ultimately revert to normal levels while revenue grows in line with the industry. We also exited our position in Avis Budget Group on valuation, and generic drug manufacturer Viatris as the range of outcomes widened.

Management teams have cut costs and restructured operations to an extent that should continue to drive operating margin expansion as revenues recover. The current valuation gap between growth and value stocks is still extremely wide by historical standards, and the portfolio remains heavily weighted towards cyclical stocks – most notably in financials, industrials, and consumer discretionary. We remain confident in the positioning of the portfolio given the robustness of the companies’ underlying franchises and balance sheets.

Mutual fund investing involves risk. Principal loss is possible. Investments in small- and mid-cap companies involve additional risks such as limited liquidity and greater volatility than larger companies. Investments in foreign securities involve political, economic and currency risks, greater volatility and differences in accounting methods. These risks are greater for investments in emerging markets. The Fund may have emphasis on a specific sector which could adversely affect a fund to a greater extent than if its emphasis was less. The Fund may invest in securities which are less liquid and more difficult to sell than more liquid securities. The Fund may invest in participatory notes which are a type of equity linked derivative and involve counterparty risk and risk that the performance of the security may not exactly match the performance of the issuer. Investments in REITs are subject to the risks associated with the direct ownership of real estate.

The Pzena Funds are distributed by Quasar Distributors, LLC.

Fund holdings, exposures and characteristics are as of the date shown and are subject to change at any time. Please refer to the Schedule of Investments for more information.

The opinions expressed in this letter are those of the Fund manager, are subject to change, are not guaranteed, and should not be considered recommendations to buy or sell any security.

The Russell Midcap® Value Index is an unmanaged index that measures the performance of those Russell Mid Cap® companies with lower price-to-book ratios and lower forecasted growth rates.

An index cannot be invested in directly.

Fund holdings, exposures and characteristics are as of the date shown and are subject to change at any time. Please refer to the Schedule of Investments for more information.

Cash flow – net amount of cash being transferred into and out of a business.

EBITDA, or earnings before interest, taxes, depreciation, and amortization, is a measure of profitability.

Operating income – Gross profit minus operating expenses.

Operating margin – operating earnings (revenue minus cost of goods sold, and selling, general and administrative costs, excluding interest and taxes) divided by revenue.

3

Pzena Emerging Markets Value Fund

Commentary

August 2021

Average Annual Total Returns for the Semi-Annual Period Ended August 31, 2021.

| Since | ||||||

| Three | Six | One | Three | Five | Inception | |

Months(1) | Months(1) | Year(1) | Years | Years | (3/31/2014) | |

| Pzena Emerging Markets Value Fund – | ||||||

| Investor Class (PZVEX) | -1.79% | 6.33% | 42.10% | 8.52% | 9.87% | 4.57% |

| Pzena Emerging Markets Value Fund – | ||||||

| Institutional Class (PZIEX) | -1.63% | 6.57% | 42.61% | 8.91% | 10.21% | 4.89% |

| MSCI Emerging Markets Index | -4.12% | -0.98% | 21.12% | 9.87% | 10.40% | 6.27% |

| MSCI Emerging Markets Value Index | -2.68% | 3.98% | 29.34% | 6.40% | 7.69% | 3.77% |

| (1) | Not annualized. |

Performance data quoted represents past performance and does not guarantee future results. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance of the Fund may be lower or higher than the performance quoted. Performance data current to the most recent month-end may be obtained by calling 844.PZN.1996 (844.796.1996).

PZVEX Expense Ratio – Gross: 1.56%

PZVEX Expense Ratio – Net: 1.43%*

PZIEX Expense Ratio – Gross: 1.21%

PZIEX Expense Ratio – Net: 1.08%*

Expense ratios shown are as of the Fund’s registration statement dated June 28, 2021.

| * | Pzena Investment Management, LLC, the Fund’s investment adviser, has contractually agreed to waive a portion or all of its management fees and pay Fund expenses through at least June 28, 2022. |

As COVID-19 concerns gradually eased, most emerging-market bourses continued their positive trajectories, though the index was down nearly one percent, driven by China weakness – China composes nearly 35% of the index and was down over 17%. The Chinese central government announced some key regulatory changes for internet companies and some industry-specific regulations for the education and housing sectors among others. The European, South American, and Africa/Mideast regions were each up.

The underperformance of richly valued Chinese growth-oriented names helped the MSCI Emerging Markets Value Index outperform the style-neutral MSCI Emerging Markets Index for the period, continuing the trend that began last November. By sector, the MSCI Emerging Markets Index reported weakness in the consumer discretionary, real estate, and communication services sectors; energy, materials, and utilities were the strongest sectors.

With a favorable backdrop for value, the Pzena Emerging Markets Value Fund outpaced the benchmark (MSCI Emerging Markets Index) by over 730 basis points, with relative performance driven by holdings in the industrials, utilities, and financials sectors. All sectors contributed positively except health care, which was the only detractor. By country, positioning in China/Hong Kong and holdings in Korea and Brazil contributed the most. Holdings in India, Taiwan, and Singapore were the leading detractors.

By company, the largest individual contributors for the period were Pacific Basin Shipping Limited, DB Insurance Co., Ltd., and Companhia Energetica de Minas Gerais SA (CEMIG). The top performer was Hong Kong-based dry bulk shipper Pacific Basin, which continued to benefit from normalization of industry over-supply, and higher shipping rates on many of its key routes, largely stemming from supply chain bottlenecks and lack of new ship supply. Korean insurer DB Insurance Co. was strong on the back of reported results ahead of consensus, largely on improved loss ratio in general insurance. While the expense ratio was a bit higher, it stemmed from stronger sales, as premiums grew, notably faster than its peers. CEMIG, the Brazilian electric utility, did well as it reported EBITDA up significantly year over year on strong performance in both the power generation and gas distribution segments. Also, the Brazilian power regulator ANEEL laid out some measures to mitigate distribution companies’ tariff hikes, removing some of the regulatory uncertainty.

The largest detractors in the portfolio were Baidu Inc., Galaxy Entertainment Group Limited, and Brilliance China Automotive. Baidu (Chinese internet search company) shares suffered early in the period in reaction to the U.S. Securities and Exchange Commission’s (SEC) adoption of measures to remove foreign stocks from U.S. exchanges if they fail to comply with U.S. accounting standards and from the Archegos Capital Management unwind. We don’t see the share decline as having anything to do with fundamentals. However, shares

4

Pzena Emerging Markets Value Fund

Commentary (Continued)

August 2021

declined further – later in the period – with other Internet stocks as China told major tech firms to improve compliance management. Uncertainty around the extent of China’s regulatory crackdown as well as criticism over unfair competition in the form of fake reviews has weighed on shares. We believe the fundamentals of the company are strong and see strength in its core search business and its investments in other ventures including autonomous driving. Galaxy Entertainment shares have been weak with other reopening trades as the timeline remains uncertain on when Macau will be fully reopening to visitors. Galaxy did show a net profit in first-half 2021, compared with net losses at Macau peers. New outbreaks continue to slow the pace of Macau’s recovery, but we remain constructive based on pent-up demand, its asset quality, its net-cash balance sheet, and its large land bank. Brilliance China Automotive detracted, due to our decision to write down the value of our holding. On March 31st, trading in shares of Brilliance China was halted after the company delayed publishing its 2020 financials due to unauthorized guarantees and legal proceedings involving a subsidiary. On April 14th, the following details were released: Brilliance China’s wholly-owned subsidiary, Shenyang JinBei Automotive Industry Holdings (SJAI), had guaranteed the debt of Huachen at four banks; and, on April 13th, auditors discovered a cash discrepancy of RMB 2.38bn between SJAI’s bank accounts and what it recorded on its books. While the asset side and its operations remain strong, given the lack of clarity on Brilliance China’s residual market value (due to apparent fraud) once it does resume trading, we marked the position to a price of 0.01 HKD until further notice.

During the period we established positions in United Integrated Services (UIS), China Overseas Land & Investment (COLI), Alibaba Group Holding, Indian used commercial vehicle financier Shriram Transport Finance Co., and electronics player Vtech. Taiwan’s UIS is a cleanroom producer for the foundry industry and counts chip giant Taiwan Semiconductor Manufacturing Company (TSMC) among its most loyal and important customers. UIS should continue to benefit from TSMC’s strength and capital expenditure spending, and trades at a fraction of its intrinsic valuation. COLI is a large, partially state-owned homebuilder, which boasts a large landbank in Chinese tier 1 and 2 cities. Recently, the company suffered from stagnating volumes in its core markets, as well as from margin compression due to government-imposed property price caps. We believe COLI’s state-owned status allows it a lower cost of funding and better access to liquidity in a downturn where tight liquidity conditions are expected. Moreover, its strong balance sheet helps it to gain market share as more stringent leverage requirements push weaker competitors out of the market. We bought Alibaba as it is a top internet player with strong franchises in ecommerce, cloud, and adjacent markets. There is uncertainty because the Chinese government is cracking down on the internet sector (regulations are literally coming out every week) but we feel the company’s recent share price decline provides compelling valuation as it navigates through these challenges. Shriram is the industry leader in used commercial vehicle financing in India and is poised to benefit significantly as the country recovers from COVID-19. We continued to build our position in electronic company Vtech. Vtech, as the world’s largest manufacturer of electronic learning toys, and a niche Electronics Manufacturing Services company, is a solid franchise with strong cash-generating abilities trading at an exceptional valuation.

During this period, we added to Galaxy and Turkish lender Akbank on weakness. We trimmed relative outperformers Rosneft Oil from Russia, and Indian private bank ICICI Bank Limited. We sold positions in independent power producer China Resources Power Holdings, Korean bank Hana Financial Group, and China Dongxiang, also mostly on strength.

The Fund’s largest sector weightings remain in financials (relative overweight) and information technology. We have a small allocation to health care, communication services, and real estate. Communications services is the Fund’s largest underweight relative to the index. Geographically, the largest relative exposure remains to emerging Europe. The large commitments by country are to Korea (overweight versus the index), China (underweight) and Taiwan (roughly index weight).

While we continue to applaud the recovery in emerging markets value equities, valuation spreads remain extremely wide by historical standards, which is to say: we believe the current value cycle has legs. The portfolio remains positioned in businesses across geographies and industries that can capture significant upside as they recover from both company-specific and externally-driven pain.

5

Pzena Emerging Markets Value Fund

Commentary (Continued)

August 2021

Mutual fund investing involves risk. Principal loss is possible. Investments in foreign securities involve political, economic and currency risks, greater volatility and differences in accounting methods. These risks are greater for investments in emerging markets. The Fund may have emphasis on a specific sector which could adversely affect a fund to a greater extent than if its emphasis was less. The Fund may invest in securities which are less liquid and more difficult to sell than more liquid securities. The Fund may invest in participatory notes which are a type of equity linked derivative and involve counterparty risk and risk that the performance of the security may not exactly match the performance of the issuer. Investments in real estate investment trusts are subject to the risks associated with the direct ownership of real estate.

The Pzena Funds are distributed by Quasar Distributors, LLC.

Fund holdings, exposures and characteristics are as of the date shown and are subject to change at any time. Please refer to the Schedule of Investments for more information.

The opinions expressed in this letter are those of the Fund manager, are subject to change, are not guaranteed, and should not be considered recommendations to buy or sell any security.

The MSCI Emerging Markets Index is a free float-adjusted market capitalization index that is designed to measure equity market performance of emerging markets, and provides equity returns including dividends net of withholding tax rates as calculated by MSCI. The index cannot be invested in directly.

The MSCI Emerging Markets Value Index is based on a traditional market cap weighted parent index, the MSCI Emerging Markets Index. The value investment style characteristics for index construction are defined using three variables: book value to price, 12-month forward earnings to price and dividend yield.

Loss ratio – the losses an insurer incurs due to paid claims as a percentage of premiums earned.

EBITDA, or earnings before interest, taxes, depreciation, and amortization, is a measure of profitability.

6

Pzena Small Cap Value Fund

Commentary

August 2021

Average Annual Total Returns for the Semi-Annual Period Ended August 31, 2021.

| Since | ||||||

| Three | Six | One | Three | Five | Inception | |

Months(1) | Months(1) | Year(1) | Years | Years | (4/27/2016) | |

| Pzena Small Cap Value Fund – Investor Class (PZVSX) | -4.06% | 8.42% | 61.96% | 6.62% | 9.94% | 9.37% |

| Pzena Small Cap Value Fund – Institutional Class (PZISX) | -3.97% | 8.52% | 62.38% | 6.90% | 10.26% | 9.69% |

Russell 2000® Value Index | -1.60% | 8.93% | 59.49% | 8.41% | 11.66% | 12.61% |

| (1) | Not annualized. |

Performance data quoted represents past performance and does not guarantee future results. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance of the Fund may be lower or higher than the performance quoted. Performance data current to the most recent month-end may be obtained by calling 844.PZN.1996 (844.796.1996).

PZVSX Expense Ratio – Gross: 1.77%

PZVSX Expense Ratio – Net: 1.46%*

PZISX Expense Ratio – Gross: 1.42%

PZISX Expense Ratio – Net: 1.11%*

Expense ratios shown are as of the Fund’s registration statement dated June 28, 2021.

| * | Pzena Investment Management, LLC, the Fund’s investment adviser, has contractually agreed to waive a portion or all of its management fees and pay Fund expenses through at least June 28, 2022. |

Since the end of February, the Fund was up over eight percent, slightly lagging the index. Domestic stocks appreciated this period as the U.S. economy continued to reopen and markets benefited from ample liquidity. Small-cap stocks underperformed their large-cap peers, on a shift in investor preference to large growth. Within the small cap cohort, however, value outpaced growth. The strongest sectors in the index were basic materials, real estate, and consumer discretionary, while health care and technology delivered negative returns.

Relative Fund performance was driven by holdings in the health care, industrials, and technology sectors. Names in the financials, consumer discretionary, and real estate sectors lagged the most.

By name, the Fund’s largest contributors were Olin Corporation, Triple-S Management Corporation, and Belden Inc. Olin Corp. (chlor-alkali chemical producer) continues to realize pricing improvements and was a major contributor. The new CEO’s strategy around improving chlor-alkali profitability while demand rebounds, and rationalizing supply is bearing fruit, and future earnings growth is encouraging, assuming an industrial recovery and better industry supply/demand balance. Another contributor was Puerto Rico-based insurer Triple-S Management Corp. The stock traded in a somewhat choppy manner but ultimately ended up solidly. The company posted a strong set of results while issuing a positive outlook for the full year, which didn’t have much impact on the share price. But late in August management announced its agreement to be acquired by GuideWell Mutual Holding Corp. for $36 per share, a significant premium to its recent trading range. Signal transmission company Belden’s stock performed well having reported very strong back to back quarters. The company posted strong organic growth in concert with margin expansion due to cost take-outs and encouraging revenue growth.

The largest detractors for the period were NexTier Oilfield Solutions, Inc., TechnipFMC Plc, and WSFS Financial Corporation. Oil services company NexTier Oilfield Solutions shares were quite volatile. The stock rose in the second calendar quarter as crude prices rose, but came under pressure as crude prices fell toward the middle of July. In August the company reported in-line revenues but weaker-than-expected EBITDA, and also announced and closed on an acquisition of Alamo Pressure Pumping. We believe the acquisition adds top-tier fleets capable of burning dual fuels in diesel and natural gas, at an attractive price. Oilfield services company TechnipFMC’s shares were lower despite posting solid quarterly results in July. Investors became concerned about the company’s prospects for revenue growth, with book-to-bill remaining under 1x, as orders were still 40% below pre-COVID levels. WSFS’s underperformance can largely be attributed to technical and fundamental market selling pressure from the all-stock merger of Bryn Mawr Bank Corporation (BMBC), announced in March 2021. WSFS paid a 16% premium for BMBC and is not repurchasing its own shares while the transaction remains pending through expected close in early 4Q21. Further, the company’s primarily Commercial & Industrial customer base has not recovered as quickly as those in other sectors, and the significant excess liquidity on customer balance sheets led management to cut its full year net interest margin guidance by

7

Pzena Small Cap Value Fund

Commentary (Continued)

August 2021

35 basis points at the midpoint to 3.20-3.30%. Still, we believe the combination with BMBC creates a valuable franchise in the Greater Philadelphia and Delaware regions while the banking group, more broadly, is expected to move past economic uncertainty caused by the COVID-19 pandemic.

During the quarter, Huntington Bancshares came into the portfolio as a result of the TCF Financial Corporation acquisition, which the Fund owned. We will continue to evaluate Huntington over time but feel that the combined company remains attractive as they work through achieving synergies from the combination. We initiated a new position in MRC Global, a leading distributor of pipes, valves, and fittings for the transportation of oil & gas. The company has been negatively impacted by depressed energy demand, but its cash flows are countercyclical given the company’s working capital position. At the same time, MRC has a strong gas utility business that makes up almost one-third of sales, which has a growing revenue and profit stream. The company is actively right-sizing its cost structure, which will position it for profit growth as volumes normalize. We also continued to build our position in animal nutrition company Phibro Animal Health, and, in other activity, we opportunistically added to high-performance server manufacturer Super Micro Computer, NexTier Oilfield Solutions, chemical company Orion Engineered Carbons, index annuity writer American Equity Investment Life, and door & window manufacturer JELD-WEN Holdings, among others.

To help fund these purchases we exited our positions in investment bank Cowen, which performed well on strong earnings and particularly from SPAC activity, rental car company Avis Budget Group, and audio-video equipment manufacturer Poly (formally Plantronics) – both of which appreciated significantly due to increasing travel and video conferencing demand, respectively, and as a result, approached our estimate of fair value. We also sold out of a small position in Technip Energies, which had spun out from TechnipFMC, and trimmed Olin Corp., Murphy Oil Corporation, MasTec (infrastructure construction), and Ryder System (truck rental), on strength.

We believe the portfolio is positioned for a recovery from the COVID-19 recession. The portfolio remains heavily focused in holdings of strong cyclical businesses with solid balance sheets that are deeply discounted to the earnings growth and cash flows they can, and in many cases, are already delivering. We remain committed to discovering new opportunities where we see potential for significant valuation upside over the long term, as we view the current valuation gap between growth and value stocks (which is still extremely wide by historical standards) as irrational and exploitable. We believe the value rotation is in its early stages.

Mutual fund investing involves risk. Principal loss is possible. Investments in small-cap companies involve additional risks such as limited liquidity and greater volatility than larger companies. Investments in foreign securities involve political, economic and currency risks, greater volatility and differences in accounting methods. These risks are greater for investments in emerging markets. The Fund may have emphasis on a specific sector which could adversely affect a fund to a greater extent than if its emphasis was less. The Fund may invest in securities which are less liquid and more difficult to sell than more liquid securities. The value investing style may over time go in and out of favor. At times when the value investing style is out of favor, the Small Cap Value Fund may underperform other funds that use different investing styles. Investments in REITs are subject to the risks associated with the direct ownership of real estate.

The Pzena Funds are distributed by Quasar Distributors, LLC.

Fund holdings, exposures and characteristics are as of the date shown and are subject to change at any time. Please refer to the Schedule of Investments for more information. The opinions expressed in this letter are those of the Fund manager, are subject to change, are not guaranteed, and should not be considered recommendations to buy or sell any security.

The Russell 2000® Value Index measures the performance of those Russell 2000® companies with lower price-to-book ratios and lower forecasted growth values. The index cannot be invested in directly.

EBITDA, or earnings before interest, taxes, depreciation, and amortization, is a measure of profitability.

Net interest margin is a measure of the difference between the interest income generated by banks or other financial institutions and the amount of interest paid out to their lenders, relative to the amount of their assets.

Basis point – One-hundredth of a percentage point (0.01%).

Cash flow – net amount of cash being transferred into and out of a business.

Working capital – the difference between current assets and current liabilities.

8

Pzena International Small Cap Value Fund

Commentary

August 2021

Average Annual Total Returns for the Semi-Annual Period Ended August 31, 2021.

| Since | |||||

| Three | Six | One | Three | Inception | |

Months(1) | Months(1) | Year(1) | Years | (7/2/2018) | |

| Pzena International Small Cap Value Fund – Investor Class (PZVIX) | -0.46% | 14.13% | 52.64% | 4.10% | 4.21% |

| Pzena International Small Cap Value Fund – Institutional Class (PZIIX) | -0.37% | 14.33% | 53.14% | 4.36% | 4.49% |

| MSCI World ex-USA Small Cap Index | 2.60% | 11.63% | 33.13% | 10.49% | 10.41% |

| MSCI World ex-USA Small Cap Value Index | 0.65% | 11.38% | 36.28% | 7.54% | 7.56% |

| (1) | Not annualized. |

Performance data quoted represents past performance and does not guarantee future results. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance of the Fund may be lower or higher than the performance quoted. Performance data current to the most recent month-end may be obtained by calling 844.PZN.1996 (844.796.1996).

PZVIX Expense Ratio – Gross: 8.29%

PZVIX Expense Ratio – Net: 1.53%*

PZIIX Expense Ratio – Gross: 7.94%

PZIIX Expense Ratio – Net: 1.18%*

Expense ratios shown are as of the Fund’s registration statement dated June 28, 2021.

| * | Pzena Investment Management, LLC, the Fund’s investment adviser, has contractually agreed to waive a portion or all of its management fees and pay Fund expenses through at least June 28, 2022. |

International equity markets continued to ascend in the spring, with European stocks performing well, while Japanese equities declined modestly, partially due to a deteriorating COVID-19 situation in the country. Investor sentiment abruptly shifted toward growth, mostly in the month of June, on concerns about the spread of the COVID-19 Delta variant, as well as flattening yield curves. Nonetheless, developed small cap value stocks ended the period on a high note, spurred on by improving macro conditions and rising interest rates, as well as positive economic data out of Europe. Despite the brief summer setback for value, the Fund outperformed its benchmark over the full period, with industrials the clear standout performer, driving the bulk of the portfolio’s gains.

The top individual performer in the period was Hong Kong-based dry bulk shipper Pacific Basin, which continued to benefit from higher shipping rates on many of its key routes, largely stemming from supply chain bottlenecks and port congestion. The company’s 1H results in July reinforced investors’ positive sentiment on the sector, while the industry’s container ship order book remained muted, despite the massive influx of cash from surging spot freight rates, implying sustainably strong free cash flow going forward. Italian engineering & construction company Maire Tecnimont’s shares benefitted from general European macro strength in early June, particularly after Italy revised its 1Q GDP number higher. The company also reported 1H21 results that highlighted a return to growth, margin improvement stemming from structural cost cuts taken during the downturn, as well as a particularly strong backlog with a book-to-bill ratio of 1.7x. Italian specialty steel equipment company Danieli also benefited from rallying metals prices on increasing global demand and tighter supply.

Energy was the largest detracting sector due to the crude price volatility, followed by consumer discretionary and consumer staples. The company, Foster Electric Co., a Japanese manufacturer of audio and electronic equipment, was the worst performer after reporting full-year group revenue and net income below expectations. The deteriorating macro environment in Japan also pressured the stock during the period. European oil & gas equipment services company Subsea 7 sold off after reporting results that disappointed investors on the margin front. Management attributed the weakness to persistent COVID-19-related issues causing delays and elevated costs, but they expect margins to recover in the back half of the year as low-margin projects that were booked during the downturn start to roll off. The stock also came under pressure in August due to lower crude prices, which fell on demand concerns and dollar strength. UK oil services company John Wood Group underperformed after management provided investors with a disappointing first half trading statement, which hurt the stock. The company’s earnings for the second half, however, are expected to improve materially, benefiting from a combination of better mix and cost savings, despite the ongoing revenue headwind.

During the quarter we purchased United Integrated Services, a Taiwanese engineering & construction (E&C) company specializing in integrated cleanroom construction, and major supplier to TSMC. We also added BIC, which maintains an 80% market share in U.S. pocket lighters, UK-based aerospace component supplier Senior plc, and Sabre Insurance Group, a private motor-only insurer that focuses on the specialty segment. Sabre is attractive due to the competitive edge it

9

Pzena International Small Cap Value Fund

Commentary (Continued)

August 2021

possesses by serving higher premium, non-standard customers, which manifests in a consistently better combined ratio versus peers. Sabre’s management is also keenly focused on profitability over top-line growth; the company has essentially no leverage and a dividend yield north of 4%. We sold out of PostNL and Redde Northgate on valuation, as well as Vienna Insurance Group, after we became concerned about the company’s M&A strategy.

The eurozone and UK’s economic recoveries continue to gain pace, as the region’s vaccination rate recently surpassed that of the United States, while the situation in Japan is also progressing, providing governments with the confidence to further relax restrictions. That said, the portfolio remains deeply undervalued, with price-to-book spreads between the cheapest and most expensive stocks still at extreme levels, implying that the value rally still has plenty of steam.

Mutual fund investing involves risk. Principal loss is possible. Investments in small- and mid-cap companies involve additional risks such as limited liquidity and greater volatility than larger companies. Investments in foreign securities involve political, economic and currency risks, greater volatility and differences in accounting methods. These risks are greater for investments in emerging markets. The Fund may have emphasis on a specific sector which could adversely affect a fund to a greater extent than if its emphasis was less. The Fund may invest in securities which are less liquid and more difficult to sell than more liquid securities. The Fund may invest in participatory notes which are a type of equity linked derivative and involve counterparty risk and risk that the performance of the security may not exactly match the performance of the issuer. Investments in REITs are subject to the risks associated with the direct ownership of real estate.

The Pzena Funds are distributed by Quasar Distributors, LLC.

Fund holdings, exposures and characteristics are as of the date shown and are subject to change at any time. Please refer to the Schedule of Investments for more information.

The opinions expressed in this letter are those of the Fund manager, are subject to change, are not guaranteed, and should not be considered recommendations to buy or sell any security.

The MSCI World ex USA Small Cap Index captures small cap representation across 22 of 23 Developed Markets (DM) countries* (excluding the United States). The index covers approximately 14% of the free float-adjusted market capitalization in each country. *DM countries in this index include: Australia, Austria, Belgium, Canada, Denmark, Finland, France, Germany, Hong Kong, Ireland, Israel, Italy, Japan, Netherlands, New Zealand, Norway, Portugal, Singapore, Spain, Sweden, Switzerland and the UK.

The MSCI World ex USA Small Cap Value Index captures small cap securities exhibiting overall value style characteristics across 22 Developed Markets countries. The value investment style characteristics for index construction are defined using three variables: book value to price, 12-month forward earnings to price and dividend yield.

Free cash flow – cash available after spending on capital goods and changes in working capital.

Dividend yield – A ratio that indicates how much a company pays out in dividends each year relative to its share price.

Price to book (P/B ratio) – A ratio for valuing a company that measures its current share price relative to its book value per share.

10

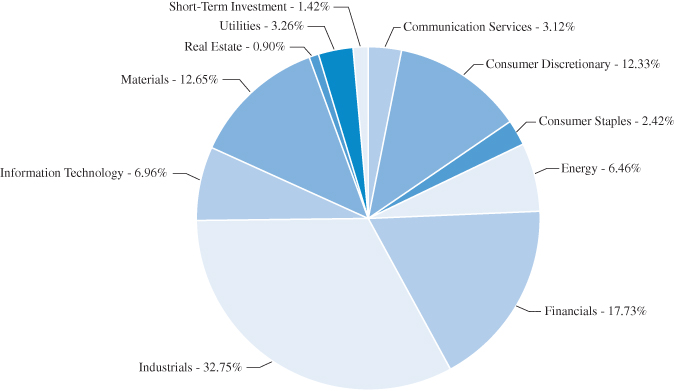

Pzena International Value Fund

Commentary

August 2021

Average Annual Total Returns for the Semi-Annual Period Ended August 31, 2021.

| Since | |

| Inception | |

(6/28/2021)(1) | |

| Pzena International Value Fund – Investor Class (PZVNX) | -0.80% |

| Pzena International Value Fund – Institutional Class (PZINX) | -0.70% |

| MSCI EAFE Index | 1.47% |

| MSCI EAFE Value Index | -0.35% |

| (1) | Not annualized. |

Performance data quoted represents past performance and does not guarantee future results. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance of the Fund may be lower or higher than the performance quoted. Performance data current to the most recent month-end may be obtained by calling 844.PZN.1996 (844.796.1996).

PZVNX Expense Ratio – Gross: 5.33%

PZVNX Expense Ratio – Net: 1.10%*

PZIIX Expense Ratio – Gross: 4.98%

PZIIX Expense Ratio – Net: 0.75*

Expense ratios shown are as of the Fund’s registration statement dated June 28, 2021.

| * | Pzena Investment Management, LLC, the Fund’s investment adviser, has contractually agreed to waive a portion or all of its management fees and pay Fund expenses through at least June 28, 2023. |

The Pzena International Value Fund launched on June 28, 2021. The discussion below covers the period from inception through August. Over this time the MSCI EAFE Index was up 1.47% while the MSCI EAFE Value Index was down 0.35%.

Three of the Fund’s largest detractors were oilfield services company TechnipFMC, Honda Motor Co., and Galaxy Entertainment Group Limited. TechnipFMC’s shares came under pressure despite posting solid quarterly results, after investors became concerned about the company’s prospects for revenue growth, with book-to-bill remaining under 1x, as orders were still 40% below pre-COVID levels. Automobile manufacturer Honda Motor was weak, despite reporting solid quarterly results, as supply chain challenges and chip shortages continue to weigh on the stock. Macau casino operator Galaxy Entertainment Group shares continued to decline amid delayed re-openings. Galaxy did show a net profit in first-half 2021, compared with net losses at Macau peers. New outbreaks continue to slow the pace of Macau’s recovery, but we remain constructive based on pent up demand, its asset quality, its net-cash balance sheet, and its large land bank.

Three of the largest contributors were John Wood Group PLC, J Sainsbury plc, and European telecom equipment company Nokia. UK oil services company John Wood Group rebounded strongly, helped by management’s upbeat guidance for the second half of 2021, with expected margins coming in ahead of the street’s estimates. UK grocer Sainsbury’s stock spiked on private equity buyout speculation. Nokia’s stock was higher after the company reported earnings ahead of consensus across the board, with sales rising 9% year-over-year on solid margins, reflecting good cost control and scale benefits. Management subsequently raised its full-year sales and free cash flow guidance.

The value recovery has taken a pause following remarkably strong moves from November through May. We view our portfolio holdings as very well positioned to achieve strong earnings improvement over the medium term, as they benefit from both self-help initiatives and a pronounced external demand recovery post-COVID-19. We believe the valuation gap between our portfolio and the market remains at extreme levels, which bodes well for future returns.

The Fund’s portfolio will generally consist of 60 to 80 stocks identified through a research-driven, bottom-up security selection process based on thorough fundamental research. The Fund seeks to invest in stocks that sell at a substantial discount to their intrinsic value but have solid long-term prospects.

The Fund may invest up to 15% of its net assets in emerging market and frontier market securities.

In evaluating an investment for purchase for the International Value Fund, we conduct a thorough fundamental assessment of the business, with a focus on those challenges that have created the value opportunity. We examine material issues that can influence the company’s long-term performance and risk profile. As a part of this process, we speak with competitors, customers, and suppliers; conduct field research such as site visits to plants, stores, or other facilities; analyze the financials and public filings of the company and its competitors; focus on the company’s underlying financial condition and business prospects considering estimated earnings, economic conditions, degree of competitive or pricing pressures, the experience and

11

Pzena International Value Fund

Commentary (Continued)

August 2021

competence of management; and integrate environmental, social, and governance (“ESG”) considerations, which can vary across companies and industries (ESG considerations may include, but are not limited to, environmental impact, corporate governance and ethical business practices).

Each step of this process contributes to our determination of whether to invest and at what position size. Once an investment has been made, we continue to engage with the company on an ongoing basis to exert a constructive, long-term oriented influence on the trajectory of the company. Our sell discipline is guided by the same process with which we originally screen the investment universe. We typically sell a security when it reaches what we judge to be fair value, there are more attractive opportunities, or there is a change in company fundamentals.

Mutual fund investing involves risk. Principal loss is possible. Investments in small-cap companies involve additional risks such as limited liquidity and greater volatility than larger companies. Investments in foreign securities involve political, economic and currency risks, greater volatility and differences in accounting methods. These risks are greater for investments in emerging markets. The Fund may have emphasis on a specific sector which could adversely affect a fund to a greater extent than if its emphasis was less. The Fund may invest in securities which are less liquid and more difficult to sell than more liquid securities. The value investing style may over time go in and out of favor. At times when the value investing style is out of favor, the International Value Fund may underperform other funds that use different investing styles. Investments in REITs are subject to the risks associated with the direct ownership of real estate.

The Pzena Funds are distributed by Quasar Distributors, LLC.

Fund holdings, exposures and characteristics are as of the date shown and are subject to change at any time. Please refer to the Schedule of Investments for more information. The opinions expressed in this letter are those of the Fund manager, are subject to change, are not guaranteed, and should not be considered recommendations to buy or sell any security.

MSCI EAFE Index (Europe, Australasia, Far East) is a free float-adjusted market capitalization index that is designed to measure the equity market performance of developed markets, excluding the U.S. & Canada, and provides equity returns including dividends net of withholding tax rates as calculated by MSCI.

MSCI EAFE Value Index captures large and mid-cap securities exhibiting overall value style characteristics across Developed Markets countries around the world, excluding the U.S. and Canada, and provides equity returns including dividends net of withholding tax rates as calculated by MSCI. The index targets 50% coverage of the free float-adjusted market capitalization of the MSCI EAFE Index.

12

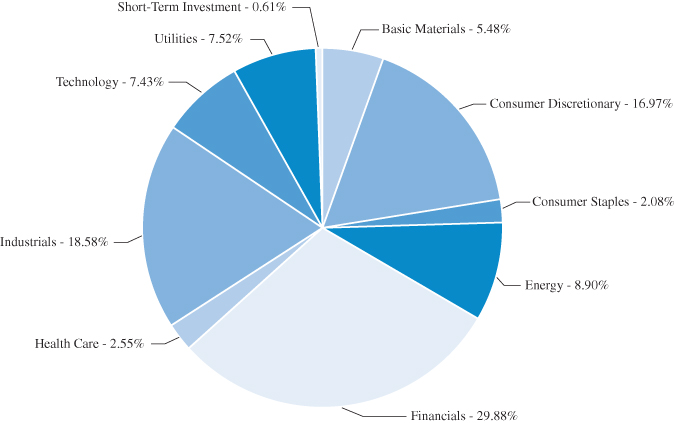

Pzena Mid Cap Value Fund

Portfolio Allocation

August 31, 2021 (Unaudited)

The portfolio’s holdings and allocations are subject to change. The percentages are of total investments as of August 31, 2021.

Note: For presentation purposes, the Fund has grouped some of the industry categories. For purposes of categorizing securities for compliance with Section 8(b)(1) of the Investment Company Act of 1940, as amended, the Fund uses more specific industry classifications.

13

Pzena Mid Cap Value Fund

Schedule of Investments

August 31, 2021 (Unaudited)

| Shares | Fair Value | |||||||

| COMMON STOCKS – 99.39% | ||||||||

| Basic Materials – 5.48% | ||||||||

| Dow, Inc. | 38,374 | $ | 2,413,724 | |||||

| Olin Corp. | 98,426 | 4,905,552 | ||||||

7,319,276 | ||||||||

| Consumer Discretionary – 16.97% | ||||||||

| Ford Motor Co. (a) | 216,287 | 2,818,220 | ||||||

| Gap, Inc. | 68,905 | 1,841,831 | ||||||

| Gildan Activewear, Inc. (b) | 107,191 | 4,121,494 | ||||||

| Lear Corp. | 25,918 | 4,145,325 | ||||||

| Newell Brands, Inc. | 147,029 | 3,736,007 | ||||||

| PVH Corp. (a) | 31,602 | 3,311,573 | ||||||

| Skechers U.S.A., Inc. – Class A (a) | 53,101 | 2,677,883 | ||||||

22,652,333 | ||||||||

| Consumer Staples – 2.08% | ||||||||

| McKesson Corp. | 13,592 | 2,774,671 | ||||||

| Energy – 8.90% | ||||||||

| Baker Hughes, a GE Co. | 165,391 | 3,767,607 | ||||||

| Cenovus Energy, Inc. (b) | 127,614 | 1,056,644 | ||||||

| Halliburton Co. | 201,466 | 4,025,291 | ||||||

| NOV, Inc. (a) | 165,627 | 2,181,307 | ||||||

| TechnipFMC PLC – ADR (a) | 129,300 | 857,259 | ||||||

11,888,108 | ||||||||

| Financials – 29.88% | ||||||||

| American International Group, Inc. | 114,268 | 6,234,462 | ||||||

| Axis Capital Holdings, Ltd. (b) | 87,872 | 4,496,410 | ||||||

| CNO Financial Group, Inc. | 155,643 | 3,807,028 | ||||||

| Equitable Holdings, Inc. | 140,915 | 4,369,774 | ||||||

| Fifth Third Bancorp | 106,123 | 4,123,940 | ||||||

| Invesco, Ltd. (b) | 101,065 | 2,558,966 | ||||||

| KeyCorp | 194,784 | 3,958,011 | ||||||

| Regions Financial Corp. | 195,608 | 3,996,271 | ||||||

| Reinsurance Group of America, Inc. | 26,750 | 3,098,185 | ||||||

| Voya Financial, Inc. | 49,988 | 3,248,220 | ||||||

39,891,267 | ||||||||

| Health Care – 2.55% | ||||||||

| Cardinal Health, Inc. | 28,137 | 1,476,911 | ||||||

| Fresenius Medical | ||||||||

| Care AG & Co. KGaA – ADR | 49,838 | 1,922,750 | ||||||

3,399,661 | ||||||||

| Industrials – 18.58% | ||||||||

| JELD-WEN Holding, Inc. (a) | 161,972 | $ | 4,460,709 | |||||

| MasTec, Inc. (a) | 23,374 | 2,137,319 | ||||||

| Mohawk Industries, Inc. (a) | 13,079 | 2,586,503 | ||||||

| Ryder System, Inc. | 34,961 | 2,779,050 | ||||||

| Terex Corp. | 81,220 | 4,146,281 | ||||||

| Textron, Inc. | 45,051 | 3,273,856 | ||||||

| Wabtec Corp. | 60,314 | 5,415,594 | ||||||

24,799,312 | ||||||||

| Technology – 7.43% | ||||||||

| Avnet, Inc. | 112,980 | 4,571,171 | ||||||

| Cognizant Technology | ||||||||

| Solutions Corp. – Class A | 34,337 | 2,620,257 | ||||||

| Hewlett Packard Enterprise Co. | 176,868 | 2,734,379 | ||||||

9,925,807 | ||||||||

| Utilities – 7.52% | ||||||||

| Edison International | 78,000 | 4,511,520 | ||||||

| NRG Energy, Inc. | 121,174 | 5,534,017 | ||||||

10,045,537 | ||||||||

| Total Common Stocks | ||||||||

| (Cost $88,109,328) | 132,695,972 | |||||||

| SHORT-TERM INVESTMENT – 0.61% | ||||||||

| Money Market Fund – 0.61% | ||||||||

| Fidelity Institutional Government | ||||||||

| Portfolio – Class I, 0.01% (c) | 814,609 | 814,609 | ||||||

| Total Short-Term Investment | ||||||||

| (Cost $814,609) | 814,609 | |||||||

| Total Investments | ||||||||

| (Cost $88,923,937) – 100.00% | 133,510,581 | |||||||

| Liabilities in Excess | ||||||||

| of Other Assets – (0.00)% | (5,345 | ) | ||||||

| TOTAL NET ASSETS – 100.00% | $ | 133,505,236 | ||||||

Percentages are stated as a percent of net assets.

| ADR | American Depositary Receipt |

| PLC | Public Limited Company |

| (a) | Non-income producing security. |

| (b) | Foreign issued security. |

| (c) | The rate listed is the 7-day annualized yield as of August 31, 2021. |

Note: For presentation purposes, the Fund has grouped some of the industry categories. For purposes of categorizing securities for compliance with Section 8(b)(1) of the Investment Company Act of 1940, as amended, the Fund uses more specific industry classifications.

The accompanying notes are an integral part of these financial statements.

14

Pzena Emerging Markets Value Fund

Portfolio Allocation

August 31, 2021 (Unaudited)

The portfolio’s holdings and allocations are subject to change. The percentages are of total investments as of August 31, 2021.

15

Pzena Emerging Markets Value Fund

Schedule of Investments

August 31, 2021 (Unaudited)

| Shares | Fair Value | |||||||

| COMMON STOCKS – 91.47% | ||||||||

| Brazil – 3.79% | ||||||||

| Ambev S.A. | 4,881,300 | $ | 16,001,012 | |||||

| Light S.A. | 1,275,300 | 3,408,495 | ||||||

19,409,507 | ||||||||

| China – 12.73% | ||||||||

| Alibaba Group Holding, Ltd. (a) | 464,400 | 9,882,185 | ||||||

| Baidu, Inc. – ADR (a) | 43,028 | 6,756,257 | ||||||

| Baidu, Inc. – Class A (a) | 171,850 | 3,376,258 | ||||||

| Brilliance China Automotive | ||||||||

| Holdings, Ltd. (a)(b) | 4,202,000 | 5,403 | ||||||

| China Construction Bank Corp. | 8,220,000 | 5,939,787 | ||||||

| China Overseas | ||||||||

| Land & Investment, Ltd. | 3,418,500 | 7,867,765 | ||||||

| Dongfeng Motor Group Co., Ltd. | 4,960,000 | 5,433,555 | ||||||

| Grand Baoxin Auto Group, Ltd. (a) | 10,102,000 | 1,454,749 | ||||||

| Lenovo Group, Ltd. | 6,446,000 | 7,144,311 | ||||||

| Trip.com Group, Ltd. – ADR (a) | 566,621 | 17,276,274 | ||||||

65,136,544 | ||||||||

| Czech Republic – 2.13% | ||||||||

| CEZ | 345,639 | 10,893,613 | ||||||

| Hong Kong – 10.72% | ||||||||

| Galaxy Entertainment Group, Ltd. (a) | 2,337,000 | 14,979,132 | ||||||

| Pacific Basin Shipping, Ltd. | 46,798,000 | 25,572,842 | ||||||

| VTech Holdings, Ltd. | 502,300 | 4,879,332 | ||||||

| Yue Yuen Industrial (Holdings), Ltd. (a) | 4,640,500 | 9,415,309 | ||||||

54,816,615 | ||||||||

| Hungary – 2.35% | ||||||||

| OTP Bank PLC (a) | 199,463 | 12,044,175 | ||||||

| India – 5.49% | ||||||||

| Aurobindo Pharma, Ltd. | 654,186 | 6,516,995 | ||||||

| ICICI Bank, Ltd. | 270,321 | 2,662,388 | ||||||

| Shriram Transport Finance Co., Ltd. | 547,364 | 10,141,688 | ||||||

| State Bank of India | 831,695 | 4,853,524 | ||||||

| State Bank of India – GDR | 67,053 | 3,922,600 | ||||||

28,097,195 | ||||||||

| Indonesia – 0.83% | ||||||||

| PT Bank Mandiri (Persero) Tbk | 9,985,100 | 4,270,577 | ||||||

| Malaysia – 0.72% | ||||||||

| Genting Malaysia Berhad | 5,181,300 | 3,701,819 | ||||||

| Republic of Korea – 16.18% | ||||||||

| DB Insurance Co., Ltd. | 324,990 | 16,453,416 | ||||||

| Hankook Tire & Technology Co., Ltd. | 333,689 | 13,411,451 | ||||||

| Hyundai Motor Co. | 11,880 | 2,177,326 | ||||||

| KB Financial Group, Inc. | 90,180 | 4,114,470 | ||||||

| Korea Shipbuilding & Offshore | ||||||||

| Engineering Co., Ltd. (a) | 57,613 | 5,888,258 | ||||||

| POSCO | 62,685 | 18,219,712 | ||||||

| Samsung Electronics Co., Ltd. | 231,857 | 15,337,817 | ||||||

| Shinhan Financial Group Co., Ltd. | 213,350 | 7,148,775 | ||||||

82,751,225 | ||||||||

| Romania – 1.01% | ||||||||

| Banca Transilvania S.A. | 7,261,053 | 5,151,408 | ||||||

| Russian Federation – 4.06% | ||||||||

| LUKOIL PJSC – ADR | 216,956 | 18,389,190 | ||||||

| Rosneft Oil Co. – GDR | 328,363 | 2,370,781 | ||||||

20,759,971 | ||||||||

| Singapore – 1.87% | ||||||||

| Wilmar International, Ltd. | 3,105,400 | 9,562,539 | ||||||

| South Africa – 2.69% | ||||||||

| Reunert, Ltd. | 826,836 | 2,970,661 | ||||||

| Sasol, Ltd. (a) | 698,541 | 10,771,754 | ||||||

13,742,415 | ||||||||

| Taiwan – 11.89% | ||||||||

| Catcher Technology Co., Ltd. | 864,000 | 5,206,415 | ||||||

| Compal Electronics, Inc. | 9,096,000 | 7,516,135 | ||||||

| Hon Hai Precision Industry Co., Ltd. | 3,980,132 | 15,941,496 | ||||||

| Lite-On Technology Corp. | 4,702,000 | 10,383,474 | ||||||

| Taiwan Semiconductor | ||||||||

| Manufacturing Co., Ltd. | 796,000 | 17,635,593 | ||||||

| United Integrated Services Co., Ltd. | 576,000 | 4,136,035 | ||||||

60,819,148 | ||||||||

| Thailand – 3.44% | ||||||||

| Bangkok Bank Public Co., Ltd. | 786,900 | 2,783,110 | ||||||

| Bangkok Bank Public Co., Ltd. – NVDR | 656,900 | 2,323,326 | ||||||

| Siam Commercial Bank PLC – NVDR | 3,781,900 | 12,495,846 | ||||||

17,602,282 | ||||||||

| Turkey – 2.42% | ||||||||

| Akbank T.A.S. | 7,919,313 | 5,608,700 | ||||||

| Ford Otomotiv Sanayi A.S. | 246,733 | 5,096,943 | ||||||

| Tofas Turk Otomobil Fabrikasi A.S. | 327,353 | 1,653,986 | ||||||

12,359,629 | ||||||||

The accompanying notes are an integral part of these financial statements.

16

Pzena Emerging Markets Value Fund

Schedule of Investments (Continued)

August 31, 2021 (Unaudited)

| Shares | Fair Value | |||||||

| COMMON STOCKS – 91.47% (Continued) | ||||||||

| United Arab Emirates – 2.02% | ||||||||

| Abu Dhabi Commercial Bank PJSC | 5,047,582 | $ | 10,320,118 | |||||

| United Kingdom – 2.91% | ||||||||

| Antofagasta PLC | 163,366 | 3,270,240 | ||||||

| Standard Chartered PLC | 1,859,820 | 11,629,149 | ||||||

14,899,389 | ||||||||

| United States – 4.22% | ||||||||

| Cognizant Technology | ||||||||

| Solutions Corp. – Class A | 186,351 | 14,220,445 | ||||||

| Flex, Ltd. (a) | 396,162 | 7,360,690 | ||||||

21,581,135 | ||||||||

| Total Common Stocks | ||||||||

| (Cost $404,501,388) | 467,949,304 | |||||||

| PREFERRED STOCKS – 4.94% | ||||||||

| Brazil – 4.52% | ||||||||

| Cia Energetica de Minas Gerais, 6.64% | 6,165,617 | 15,978,042 | ||||||

| Itau Unibanco Holding S.A., 2.29% | 1,201,443 | 7,144,808 | ||||||

23,122,850 | ||||||||

| Republic of Korea – 0.42% | ||||||||

| Hyundai Motor Co., 3.95% | 24,063 | 2,127,265 | ||||||

| Total Preferred Stocks | ||||||||

| (Cost $22,009,888) | 25,250,115 | |||||||

| SHORT-TERM INVESTMENT – 3.12% | ||||||||

| Money Market Fund – 3.12% | ||||||||

| Fidelity Institutional Government | ||||||||

| Portfolio – Class I, 0.01% (c) | 15,979,641 | 15,979,641 | ||||||

| Total Short-Term Investment | ||||||||

| (Cost $15,979,641) | 15,979,641 | |||||||

| Total Investments | ||||||||

| (Cost $442,490,917) – 99.53% | 509,179,060 | |||||||

| Other Assets in Excess | ||||||||

| of Liabilities – 0.47% | 2,408,772 | |||||||

| TOTAL NET ASSETS – 100.00% | $ | 511,587,832 | ||||||

Percentages are stated as a percent of net assets.

| ADR | American Depository Receipt |

| GDR | Global Depository Receipt |

| NVDR | Non-voting Depository Receipt |

| PJSC | Private Joint Stock Company |

| PLC | Public Limited Company |

| S.A. | Société Anonyme |

| (a) | Non-income producing security. |

| (b) | Value determined using significant unobservable inputs. |

| (c) | The rate listed is the 7-day annualized yield as of August 31, 2021. |

The accompanying notes are an integral part of these financial statements.

17

Pzena Emerging Markets Value Fund

Portfolio Diversification

August 31, 2021 (Unaudited)

| Fair | % of | |||||||

| Value | Net Assets | |||||||

| COMMON STOCKS | ||||||||

Communication Services | $ | 10,132,515 | 1.98 | % | ||||

Consumer Discretionary | 84,488,131 | 16.51 | % | |||||

Consumer Staples | 25,563,552 | 5.00 | % | |||||

Energy | 20,759,971 | 4.06 | % | |||||

Financials | 121,863,058 | 23.82 | % | |||||

Health Care | 6,516,995 | 1.27 | % | |||||

Industrials | 38,567,796 | 7.54 | % | |||||

Information Technology | 105,625,708 | 20.65 | % | |||||

Materials | 32,261,705 | 6.31 | % | |||||

Real Estate | 7,867,765 | 1.54 | % | |||||

Utilities | 14,302,108 | 2.79 | % | |||||

| Total Common Stocks | 467,949,304 | 91.47 | % | |||||

| PREFERRED STOCKS | ||||||||

Consumer Discretionary | 2,127,265 | 0.42 | % | |||||

Financials | 7,144,808 | 1.40 | % | |||||

Utilities | 15,978,042 | 3.12 | % | |||||

| Total Preferred Stocks | 25,250,115 | 4.94 | % | |||||

| Short-Term Investment | 15,979,641 | 3.12 | % | |||||

| Total Investments | 509,179,060 | 99.53 | % | |||||

| Other Assets in | ||||||||

| Excess of Liabilities | 2,408,772 | 0.47 | % | |||||

| Total Net Assets | $ | 511,587,832 | 100.00 | % | ||||

The Global Industry Classification Standard (GICS®) was developed by and/or is the exclusive property of MSCI, Inc. and Standard & Poor’s Financial Services LLC (“S&P”). GICS is a service mark of MSCI and S&P and has been licensed for use by Pzena Investment Management, LLC.

The accompanying notes are an integral part of these financial statements.

18

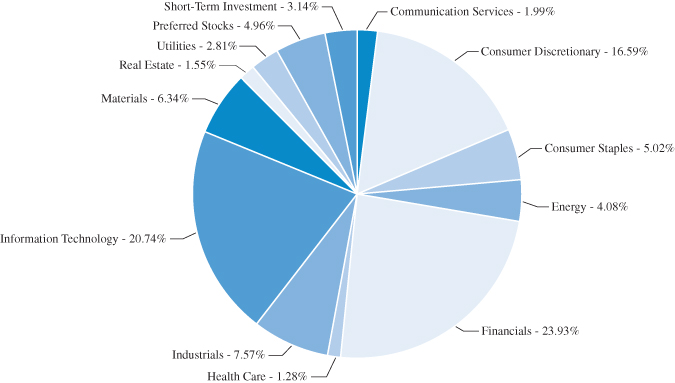

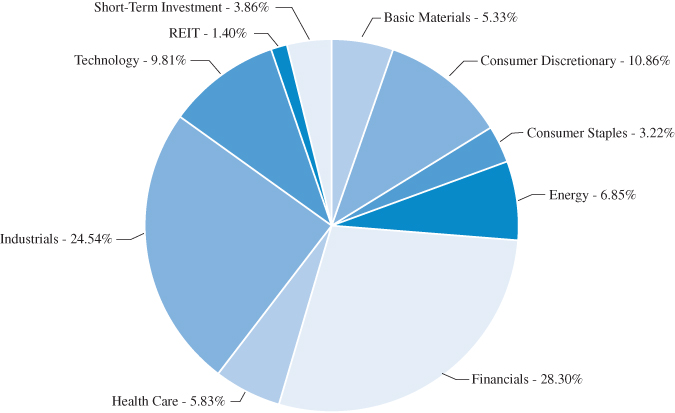

Pzena Small Cap Value Fund

Portfolio Allocation

August 31, 2021 (Unaudited)

The portfolio’s holdings and allocations are subject to change. The percentages are of total investments as of August 31, 2021.

Note: For presentation purposes, the Fund has grouped some of the industry categories. For purposes of categorizing securities for compliance with Section 8(b)(1) of the Investment Company Act of 1940, as amended, the Fund uses more specific industry classifications.

19

Pzena Small Cap Value Fund

Schedule of Investments

August 31, 2021 (Unaudited)

| Shares | Fair Value | |||||||

| COMMON STOCKS – 94.71% | ||||||||

| Basic Materials – 5.33% | ||||||||

| Olin Corp. | 73,416 | $ | 3,659,054 | |||||

| Orion Engineered Carbons S.A. (a) | 108,205 | 1,911,982 | ||||||

5,571,036 | ||||||||

| Consumer Discretionary – 10.86% | ||||||||

| Dana, Inc. | 128,122 | 2,980,118 | ||||||

| Hooker Furniture Corp. | 44,676 | 1,392,104 | ||||||

| Motorcar Parts of America, Inc. (a) | 72,226 | 1,431,519 | ||||||

| PVH Corp. (a) | 23,140 | 2,424,841 | ||||||

| Steelcase, Inc. | 221,478 | 3,120,625 | ||||||

11,349,207 | ||||||||

| Consumer Staples – 3.21% | ||||||||

| Spectrum Brands Holdings, Inc. | 19,278 | 1,504,841 | ||||||

| Universal Corp. | 36,666 | 1,855,299 | ||||||

3,360,140 | ||||||||

| Energy – 6.85% | ||||||||

| MRC Global, Inc. (a) | 119,344 | 978,621 | ||||||

| Murphy Oil Corp. | 77,006 | 1,637,147 | ||||||

| NexTier Oilfield Solutions, Inc. (a) | 585,532 | 2,107,915 | ||||||

| NOV, Inc. (a) | 111,146 | 1,463,793 | ||||||

| TechnipFMC PLC (a)(b) | 147,403 | 977,282 | ||||||

7,164,758 | ||||||||

| Financials – 28.30% | ||||||||

| American Equity Investment | ||||||||

| Life Holding Co. | 77,690 | 2,461,996 | ||||||

| Argo Group International | ||||||||

| Holdings, Ltd. (b) | 38,474 | 2,035,275 | ||||||

| Associated Banc-Corp. | 147,400 | 3,039,388 | ||||||

| Axis Capital Holdings, Ltd. (b) | 63,304 | 3,239,266 | ||||||

| CNO Financial Group, Inc. | 144,492 | 3,534,274 | ||||||

| First Midwest Bancorp, Inc. | 146,780 | 2,749,189 | ||||||

| Hope Bancorp, Inc. | 147,697 | 2,036,742 | ||||||

| Huntington Bancshares, Inc. | 137,926 | 2,141,991 | ||||||

| Umpqua Holdings Corp. | 101,807 | 1,982,182 | ||||||

| Univest Financial Corp. | 70,662 | 1,913,527 | ||||||

| Webster Financial Corp. | 61,395 | 3,101,675 | ||||||

| WSFS Financial Corp. | 29,654 | 1,346,588 | ||||||

29,582,093 | ||||||||

| Health Care – 5.83% | ||||||||

| Phibro Animal Health Corp. | 54,667 | 1,327,862 | ||||||

| Triple-S Management | ||||||||

| Corp. – Class B (a)(b) | 86,736 | 3,079,128 | ||||||

| Varex Imaging Corp. (a) | 57,673 | 1,682,321 | ||||||

6,089,311 | ||||||||

| Industrials – 24.53% | ||||||||

| Belden, Inc. | 69,824 | 3,997,424 | ||||||

| Enerpac Tool Group Corp. | 98,938 | 2,489,280 | ||||||

| JELD-WEN Holding, Inc. (a) | 129,417 | 3,564,144 | ||||||

| MasTec, Inc. (a) | 14,833 | 1,356,329 | ||||||

| Moog, Inc. – Class A | 22,384 | 1,778,185 | ||||||

| REV Group, Inc. | 131,516 | 2,138,450 | ||||||

| Ryder System, Inc. | 37,769 | 3,002,258 | ||||||

| Terex Corp. | 62,473 | 3,189,247 | ||||||

| TriMas Corp. (a) | 61,879 | 1,986,935 | ||||||

| TrueBlue, Inc. (a) | 78,385 | 2,142,262 | ||||||

25,644,514 | ||||||||

| Technology – 9.80% | ||||||||

| Avnet, Inc. | 58,114 | 2,351,293 | ||||||

| Celestica, Inc. (a)(b) | 355,436 | 3,376,642 | ||||||

| ScanSource, Inc. (a) | 72,966 | 2,596,130 | ||||||

| Super Micro Computer, Inc. (a) | 52,661 | 1,924,233 | ||||||

10,248,298 | ||||||||

| Total Common Stocks | ||||||||

| (Cost $80,990,345) | 99,009,357 | |||||||

| REIT – 1.40% | ||||||||

| Real Estate – 1.40% | ||||||||

| DiamondRock Hospitality Co. (a) | 161,454 | 1,459,544 | ||||||

| Total REIT | ||||||||

| (Cost $1,238,009) | 1,459,544 | |||||||

The accompanying notes are an integral part of these financial statements.

20

Pzena Small Cap Value Fund

Schedule of Investments (Continued)

August 31, 2021 (Unaudited)

| Shares | Fair Value | |||||||

| SHORT-TERM INVESTMENT – 3.86% | ||||||||

| Money Market Fund – 3.86% | ||||||||

| Fidelity Institutional Government | ||||||||

| Portfolio – Class I, 0.01% (c) | 4,032,739 | $ | 4,032,739 | |||||

| Total Short-Term Investment | ||||||||

| (Cost $4,032,739) | 4,032,739 | |||||||

| Total Investments | ||||||||

| (Cost $86,261,093) – 99.97% | 104,501,640 | |||||||

| Other Assets in Excess | ||||||||

| of Liabilities – 0.03% | 34,614 | |||||||

| TOTAL NET ASSETS – 100.00% | $ | 104,536,254 | ||||||

Percentages are stated as a percent of net assets.

| PLC | Public Limited Company |

| REIT | Real Estate Investment Trust |

| S.A. | Société Anonyme |

| (a) | Non-income producing security. |

| (b) | Foreign issued security. |

| (c) | The rate listed is the 7-day annualized yield as of August 31, 2021. |

Note: For presentation purposes, the Fund has grouped some of the industry categories. For purposes of categorizing securities for compliance with Section 8(b)(1) of the Investment Company Act of 1940, as amended, the Fund uses more specific industry classifications.

The accompanying notes are an integral part of these financial statements.

21

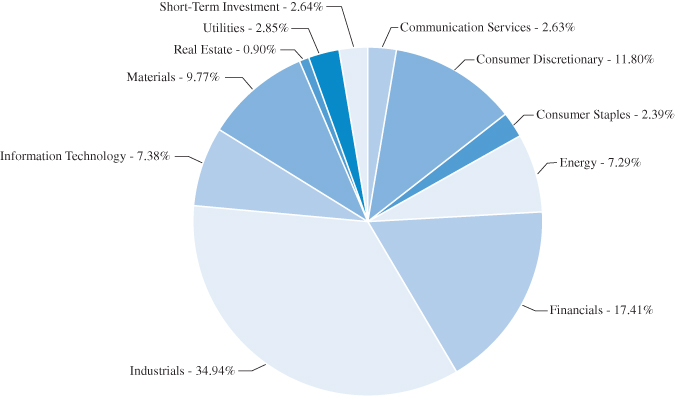

Pzena International Small Cap Value Fund

Portfolio Allocation

August 31, 2021 (Unaudited)

The portfolio’s holdings and allocations are subject to change. The percentages are of total investments as of August 31, 2021.

Note: For presentation purposes, the Fund has grouped some of the industry categories. For purposes of categorizing securities for compliance with Section 8(b)(1) of the Investment Company Act of 1940, as amended, the Fund uses more specific industry classifications.

22

Pzena International Small Cap Value Fund

Schedule of Investments

August 31, 2021 (Unaudited)

| Shares | Fair Value | |||||||

| COMMON STOCKS – 97.10% | ||||||||

| Austria – 1.95% | ||||||||

| ANDRITZ AG | 5,554 | $ | 319,106 | |||||

| Canada – 7.64% | ||||||||

| Celestica, Inc. (a) | 61,348 | 582,044 | ||||||

| Linamar Corp. | 6,241 | 353,590 | ||||||

| Transcontinental, Inc. – Class A | 16,153 | 312,651 | ||||||

1,248,285 | ||||||||

| France – 10.32% | ||||||||

| Ipsos | 8,844 | 428,144 | ||||||

| Rexel S.A. | 29,700 | 621,234 | ||||||

| SCOR SE | 10,521 | 322,865 | ||||||

| Societe BIC S.A. | 4,719 | 313,980 | ||||||

1,686,223 | ||||||||

| Germany – 6.76% | ||||||||

| Bertrandt AG | 2,636 | 150,176 | ||||||

| SAF-Holland S.A. (a) | 23,298 | 332,035 | ||||||

| Salzgitter AG (a) | 16,561 | 622,611 | ||||||

1,104,822 | ||||||||

| Hong Kong – 5.90% | ||||||||

| Pacific Basin Shipping, Ltd. | 614,000 | 335,521 | ||||||

| VTech Holdings, Ltd. | 31,100 | 302,105 | ||||||

| Yue Yuen Industrial (Holdings), Ltd. (a) | 161,000 | 326,660 | ||||||

964,286 | ||||||||

| Ireland – 4.39% | ||||||||

| Bank of Ireland Group PLC (a) | 52,209 | 328,325 | ||||||

| Origin Enterprises PLC | 98,406 | 389,246 | ||||||

717,571 | ||||||||

| Israel – 1.96% | ||||||||

| Ituran Location and Control, Ltd. – ADR | 12,258 | 319,811 | ||||||

| Italy – 9.46% | ||||||||

| Anima Holding S.p.A. | 81,243 | 418,820 | ||||||

| BPER Banca | 81,581 | 177,482 | ||||||

| Danieli & C Officine Meccaniche S.p.A. | 27,473 | 522,263 | ||||||

| Maire Tecnimont S.p.A. | 109,879 | 428,141 | ||||||

1,546,706 | ||||||||

| Japan – 14.64% | ||||||||

| DIC Corp. | 12,000 | 345,226 | ||||||

| Foster Electric Co., Ltd. | 36,734 | 290,159 | ||||||

| Fukuoka Financial Group, Inc. | 18,400 | 340,019 | ||||||

| Open House Co., Ltd. | 3,000 | 146,162 | ||||||

| Sankyu, Inc. | 7,200 | 335,736 | ||||||

| Tsubakimoto Chain Co. | 10,100 | 311,680 | ||||||

| Ube Industries, Ltd. | 15,500 | 312,635 | ||||||

| Zeon Corp. | 23,500 | 311,866 | ||||||

2,393,483 | ||||||||

| Netherlands – 4.09% | ||||||||

| Flow Traders | 3,331 | 135,691 | ||||||

| Koninklijke BAM Groep N.V. (a) | 117,872 | 389,140 | ||||||

| Technip Energies N.V. (a) | 6,243 | 81,565 | ||||||

| Technip Energies N.V. – ADR (a) | 4,760 | 61,499 | ||||||

667,895 | ||||||||

| Norway – 1.56% | ||||||||

| Subsea 7 S.A. | 33,601 | 255,923 | ||||||

| Republic of Korea – 4.74% | ||||||||

| DB Insurance Co., Ltd. | 9,592 | 485,618 | ||||||

| Hankook Tire & Technology Co., Ltd. | 7,179 | 288,535 | ||||||

774,153 | ||||||||

| Spain – 1.79% | ||||||||

| Unicaja Banco S.A. | 316,539 | 292,835 | ||||||

| Taiwan – 1.84% | ||||||||

| United Integrated Services Co., Ltd. | 42,000 | 301,586 | ||||||

| United Kingdom – 20.06% | ||||||||

| Balfour Beatty PLC | 112,522 | 442,446 | ||||||

| Capita PLC (a) | 491,788 | 331,036 | ||||||

| Drax Group PLC | 81,366 | 464,022 | ||||||

| Inchcape PLC | 26,335 | 332,921 | ||||||

| John Wood Group PLC (a) | 154,966 | 532,213 | ||||||

| Sabre Insurance Group PLC | 110,671 | 336,266 | ||||||

| Senior PLC (a) | 144,114 | 351,889 | ||||||

| TechnipFMC PLC (a) | 38,836 | 257,483 | ||||||

| Travis Perkins PLC | 9,301 | 230,364 | ||||||

3,278,640 | ||||||||

| Total Common Stocks | ||||||||

| (Cost $15,064,524) | 15,871,325 | |||||||

The accompanying notes are an integral part of these financial statements.

23

Pzena International Small Cap Value Fund

Schedule of Investments (Continued)

August 31, 2021 (Unaudited)

| Shares | Fair Value | |||||||

| SHORT-TERM INVESTMENT – 2.65% | ||||||||

| Money Market Fund – 2.65% | ||||||||

| Fidelity Institutional Government | ||||||||