REPORT OF FOREIGN PRIVATE ISSUER PURSUANT TO RULE 13a-16 OR 15d-16 OF THE SECURITIES EXCHANGE ACT OF 1934

| Atlatsa Resources Corporation |

| |

| Management Discussion and Analysis of Financial Condition and Results of Operations for the three and nine months ended September 30, 2014 |

Management Discussion and Analysis of Financial Condition and Results of Operations for the three and nine months ended September 30, 2014

| Atlatsa Resources Corporation |

| |

| Management Discussion and Analysis of Financial Condition and Results of Operations for the three and nine months ended September 30, 2014 |

TA B L E O F C O N T E N T S

| 1.0 Glossary of Terms | 3 |

| 1.1 Introduction | 8 |

| 1.2 Overview | 11 |

| 1.3 Restructure Plan | 15 |

| 1.3.1 Phase One | 15 |

| 1.3.2 Phase Two | 16 |

| 1.4 Debt Arrangements | 18 |

| 1.4.1. 2009 Senior Debt Facility | 18 |

| 1.4.2. New Senior Facilities Agreement | 19 |

| 1.4.3. Working Capital Facility | 19 |

| 1.4.4. Advance on the Purchase of Concentrate Revenue | 20 |

| 1.4.5. Vendor Finance Facility – Share Settled Financing – The “B” Preference Shares | 21 |

| 1.4.6. Security | 21 |

| 1.5 Black Economic Empowerment | 22 |

| 1.6 Environmental Matters | 22 |

| 1.7 Operations | 23 |

| 1.7.1 Bokoni Mine | 23 |

| 1.7.2 Platreef Exploration Properties, Northern Limb | 25 |

| 1.7.2.1 Rietfontein Project | 25 |

| 1.7.2.2 Central Block | 26 |

| 1.7.2.3 Kwanda Project | 26 |

| 1.8 Market Trends and Outlook | 27 |

| 1.9 Discussion of Operations | 29 |

| 1.10 Summary of Quarterly Results | 35 |

| 1.11 Liquidity | 36 |

| 1.12 Capital Resources | 39 |

| 1.13 Off-Balance Sheet Arrangements | 41 |

| 1.14 Transactions with Related Parties | 41 |

| 1.15 Critical Accounting Estimates | 43 |

| 1.16 Changes in accounting policies | 47 |

| 1.17 Financial Instruments and Risk Management | 47 |

| 1.18 Other MD&A Requirements | 51 |

| 1.20 Internal Controls over Financial Reporting Procedures | 51 |

| 1.20 Disclosure of Outstanding Share Data | 53 |

| Atlatsa Resources Corporation |

| |

| Management Discussion and Analysis of Financial Condition and Results of Operations for three and nine months ended September 30, 2014 |

1.0 Glossary of Terms

Certain terms used in this MD&A are defined as follows:

“2009 Senior Debt Facility” means the senior term loan facility provided by RPM to Plateau, which was paid out and settled on December 13, 2013;

“4E” means platinum, palladium, rhodium and gold;

““A” Preference Share Facility” means the A Preference Shares in the capital of Plateau subscribed for by RPM in the amount of ZAR1.722 billion, together with accrued dividends thereon and the attributable amount of the equivalent A Preference Share facilities outstanding in the capital of Bokoni Holdco and Bokoni;

“Advance” has the meaning ascribed to it in Section 1.4.4. Advance on the Purchase of Concentrate Revenue;

“Advance on Concentrate Revenue Agreement” has the meaning ascribed to it in Section 1.3.2 Phase Two;

“AG8” means an adjustment to the carrying amount of the financial instrument (i.e. the New Senior Facilities Agreement) should the estimated future cash flows or the interest rate change after the calculation of the effective interest rate on initial recognition. This means that any change in expectations of future cash flows or interest rates are reflected in the adjusted carrying amount, and that change in the carrying amount is recognized immediately as a gain or loss in the Consolidated Statement of Profit or Loss and Other Comprehensive Income;

“Amending Agreement” has the meaning ascribed to it in Section 1.3.2 Phase Two;

“Anglo Platinum” means Anglo American Platinum Limited, a subsidiary of Anglo American plc;

“Atlatsa” or the “Company” means Atlatsa Resources Corporation; a corporation incorporated under the laws of the Province of British Columbia and listed on the TSX, the JSE and the NYSE MKT, and includes its subsidiaries where the context requires;

“Atlatsa Holdings” means Atlatsa Holdings Proprietary Limited, a private company incorporated under the laws of South Africa (formerly known as Pelawan Investments Proprietary Limited);

“Atlatsa Holdings Vendor Finance Loan” has the meaning ascribed to it in Section 1.3.2 Phase Two;

““B” Preference Shares” means collectively, the 115,800 cumulative convertible preference shares in the authorized capital of Pelawan SPV, the 115,800 cumulative convertible redeemable preference shares in the capital of Plateau and the 111,600 cumulative convertible redeemable preference shares in the capital of Plateau, and is described in Section 1.4.5. Vendor Finance Facility – Share Settled Financing – The “B” Preference Shares;

“BEE” means Black Economic Empowerment, as envisaged pursuant to the Mineral Development Act and related legislation and guidelines, being a strategy aimed at substantially increasing participation by HDPs at all levels in the economy of South Africa. BEE is aimed at redressing the imbalances of the past caused by the Apartheid system in South Africa, by seeking to substantially and equitably increase

| Atlatsa Resources Corporation |

| |

| Management Discussion and Analysis of Financial Condition and Results of Operations for three and nine months ended September 30, 2014 |

the ownership and management of South Africa's resources by the majority of its citizens and so ensure broader and more meaningful participation in the economy by HDPs;

“BIC” means the Bushveld Igneous Complex, South Africa;

“Boikgantsho” means the Boikgantsho Platinum Mine Proprietary Limited, a wholly owned subsidiary of Bokoni Holdco, located on the Northern Limb of the Bushveld Complex in South Africa, on the Drenthe and Witrivier farms, and the northern portion of the Overysel farm. The mineral properties of both farms were sold to RPM on December 13, 2013. This company is dormant as of December 13, 2013;

“Bokoni” or “Bokoni Mine” means Bokoni Platinum Mines Proprietary Limited, a private company incorporated under the laws of South Africa, formerly named Richtrau No. 177 Proprietary Limited, and which is a wholly owned subsidiary of Bokoni Holdco;

“Bokoni Group” means, collectively, Bokoni Holdco and all subsidiaries thereof, including Bokoni, Kwanda, Boikgantsho and Ga-Phasha;

“Bokoni Holdco” means Bokoni Platinum Holdings Proprietary Limited, a private company incorporated under the laws of South Africa, which is the holding company of Bokoni, Kwanda, Boikgantsho and Ga-Phasha;

“Bokoni Holdco Shareholders Agreement” means the March 27, 2013 shareholders agreement between Plateau, RPM and Bokoni Holdco more fully described in Section 1.7.1 Bokoni Mine under the heading “Management of Bokoni Operations”;

“Bokoni Mine” means the PGM mine, located on the Eastern Limb of the Bushveld Complex in South Africa on the Diamond, Wintersveld, Jagdlust, Middelpunt, Umkoanesstad, Zeekoegat, Avoca and Klipfontein farms, formerly known as the Lebowa Platinum Mine;

“CAD” or “$” or “dollars” means Canadian Dollar, the currency of Canada;

“Common Shares” mean common shares without par value in the capital of the Company;

“Concentrate Agreement” has the meaning ascribed to it in Section 1.7.1 Bokoni Mine under the heading “Sale of Concentrate”;

“DMR” means the Government of South Africa, acting through the Minister of Mineral Resources and the Department of Mineral Resources and their respective successors and delegates;

“Eastern Ga-Phasha” means the Eastern section of Ga-Phasha, located on the Eastern Limb of the Bushveld Complex in South Africa, comprising the farms Paschaskraal and De Kamp, which was sold and transferred to RPM on December 13, 2013;

“EBITDA” means earnings before net finance expense, income tax, depreciation and amortisation;

“EDGAR” means the SEC’s Electronic Document Gathering and Retrieval System;

“Environmental Trust Fund” has the meaning ascribed to it in Section 1.6 Environmental Matters;

“ETFs” means Exchange Traded Funds;

| Atlatsa Resources Corporation |

| |

| Management Discussion and Analysis of Financial Condition and Results of Operations for three and nine months ended September 30, 2014 |

“Exchange Agreement” has the meaning ascribed to it in Section 1.4.5. Vendor Finance Facility – Share Settled Financing – The “B” Preference Shares;

“Existing JO” has the meaning ascribed to it in Section 1.7.2.1 Rietfontein Project;

“Extended JO” has the meaning ascribed to it in Section 1.7.2.1 Rietfontein Project;

“Fair value” of a loan represents the fair value difference between the Company’s cost of borrowing when compared to a market related cost of borrowing available to the Company;

“Fiscal 2011” means the year ended December 31, 2011;

“Fiscal 2012” means the year ended December 31, 2012;

“Fiscal 2013” means the year ended December 31, 2013;

“Fiscal 2014” means the year ended December 31, 2014;

“Form 20-F” as amended, means Atlatsa’s Annual Report on Form 20-F for the fiscal year ended December 31, 2013;

“Ga-Phasha” means the Ga-Phasha Platinum Mine Proprietary Limited, a wholly owned subsidiary of Bokoni Holdco. This company is dormant as of December 13, 2013;

“HDPs” means Historically Disadvantaged Persons;

“IASB” means the International Accounting Standards Board;

“ICFR” means internal control over financial reporting; as such term is defined in applicable securities regulations, including The United States Securities Exchange Act of 1934, as amended, and Section 404 of the Sarbanes-Oxley Act of 2002;

“IFRS” means International Financial Reporting Standards as issued by the IASB;

“Ivanplats” means Ivanhoe Nickel & Platinum Limited;

“JIBAR” means the three month Johannesburg Interbank Agreed Rate;

“JSE” means the JSE Limited, a company incorporated in accordance with the laws of South Africa, licensed as an exchange under the South African Securities Services Act, 2004;

“ktpm” means kilo tonnes per month;

“Kwanda” means Kwanda Platinum Mine Proprietary Limited, a wholly owned subsidiary of Bokoni Holdco, which owns the Kwanda Project;

“Kwanda Exploration Project” means the Kwanda PGM project, located on the Northern Limb of the Bushveld Complex in South Africa, on 12 farms, described further in Section 1.7.2.3 Kwanda Project;

“LTIFR” means Lost Time Injury Frequency Rate (including serious);

“MD&A” means Management’s Discussion and Analysis;

| Atlatsa Resources Corporation |

| |

| Management Discussion and Analysis of Financial Condition and Results of Operations for three and nine months ended September 30, 2014 |

“Minxcon” means Minxcon Proprietary Limited, a private company incorporated under the laws of South Africa;

“MPRDA” means the Mineral and Petroleum Resources Development Act of 2002 as described in Section 1.6 Environmental Matters;

“NEDs” means Non-Executive Directors, as described in Section 1.20 Disclosure of Outstanding Share Data;

“New Equity Incentive Plans” means the Share Option Plan, the Share Appreciation Rights Plan and the Conditional Share Unit Plan, each as adopted by the Board on May 19, 2014 and approved by shareholders of the Company on June 27, 2014, as described in Section 1.20 Disclosure of Outstanding Share Data;

“New Senior Facilities Agreement” means the new senior term loan and revolving facility agreement dated March 27, 2013 between Plateau and RPM, pursuant to which RPM made available to Plateau on December 13, 2013, a senior term loan and revolving facility in a total amount of up to $228.0 million (ZAR2.3 billion). Subsequent to the repayment of $74.3 million (ZAR750.0 million) from the subscription for 125 million Common Shares, in the Company by RPM on January 31, 2014, the facility’s limit was reduced to $153.6 million (ZAR1.55 billion). This facility is described in Section 1.4.1. 2009 Senior Debt Facility;

“NYSE MKT” means the NYSE MKT LLC;

“NI 43-101” means the National Instrument 43-101 – Standards of Disclosure for Mineral Projects of the Canadian Securities Administrators;

“OCSF” means the operating cash flow shortfall facility provided by RPM to Plateau, which, as of September 28, 2012, consolidated into the 2009 Senior Debt Facility, and is no longer in effect;

“Pelawan SPV” means Pelawan Finance SPV Proprietary Limited, a wholly owned subsidiary of Atlatsa Holdings;

“PGM” means platinum group metals, comprising platinum, palladium, rhodium, ruthenium, osmium and iridium;

“Phase One” means the first phase of the Restructure Plan, as more fully described in Section 1.3.1 Phase One;

“Phase Two” means the second phase of the Restructure Plan, as more fully described in Section 1.3.2 Phase Two;

“Plateau” means Plateau Resources Proprietary Limited, a private company incorporated under the laws of South Africa, being an indirect wholly owned subsidiary of Atlatsa;

“Plateau Ordinary Shares” has the meaning ascribed to it in Section 1.4.5. Vendor Finance Facility – Share Settled Financing – The “B” Preference Shares;

| Atlatsa Resources Corporation |

| |

| Management Discussion and Analysis of Financial Condition and Results of Operations for three and nine months ended September 30, 2014 |

“Platreef projects” means the mineral rights (known as “farms”) of the Central Block, the Rietfontein Block and the Kwanda Project, which are collectively, known as the Platreef Properties as more fully described in Section 1.7.2 Platreef Exploration Properties, Northern Limb;

“Project companies” or “Projects” means mining exploration in Kwanda. In the previous year this also included Boikgantsho, Kwanda and Ga-Phasha. Boikgantsho and two farms in Ga-Phasha (De Kamp and Paschaskraal) were sold to RPM and the remaining two farms in Ga-Phasha (Avoca and Klipfontein) were transferred to Bokoni Mine on December 13, 2013. See the segment information (note 13) in the unaudited condensed consolidated interim financial statements for Q3 2014 for more details;

“PSG” mean PSG Capital Proprietary Limited, a private company incorporated under the laws of South Africa;

“Q1 2013” means the three month period ended March 31, 2013;

“Q1 2014” means the three month period ended March 31, 2014;

“Q2 2013” means the three month period ended June 30, 2013;

“Q2 2014” means the three month period ended June 30, 2014;

“Q3 2013” means the three month period ended September 30, 2013;

“Q3 2014” means the three month period ended September 30, 2014;

“Q4 2012” means the three month period ended December 31, 2012;

“Q4 2013” means the three month period ended December 31, 2013;

“Restructure Plan” means the restructure plan for the refinancing, recapitalization and restructure of the Company and the Bokoni Group, more fully described in Section 1.3 Restructure Plan;

“Royalty Act” means The Mineral and Petroleum Resources Royalty Act, Act No 28 of 2008, in relation to royalties to be levied by the South African state in respect of the transfer of mineral or petroleum resources;

“RPM” means Rustenburg Platinum Mines Limited, a wholly owned subsidiary of Anglo Platinum;

“SEC” means the U.S. Securities and Exchange Commission;

“SEDAR” means the System for Electronic Document Analysis and Retrieval available at www.sedar.com;

“Settlement Agreement” has the meaning ascribed to it in Section 1.7.2.1 Rietfontein Project;

“Share-Settled Financing” has the meaning ascribed to it in Section 1.4.5. Vendor Finance Facility – Share Settled Financing – The “B” Preference Shares

“SPV Ordinary Shares” has the meaning ascribed to it in Section 1.4.5. Vendor Finance Facility – Share Settled Financing – The “B” Preference Shares;

| Atlatsa Resources Corporation |

| |

| Management Discussion and Analysis of Financial Condition and Results of Operations for three and nine months ended September 30, 2014 |

“SPV Preferred Shares” has the meaning ascribed to it in Section 1.4.5. Vendor Finance Facility – Share Settled Financing – The “B” Preference Shares;

“tpm” means tonnes milled per month;

“Transaction Cost Loan Agreement” has the meaning ascribed to it in Section 1.4.4. Advance on the Purchase of Concentrate Revenue;

“United States” or “U.S.” means the United States of America;

“USD” or “US$” means the U.S. Dollar, the currency of the United States of America;

“TSX” means the Toronto Stock Exchange;

“TSXV” means the TSX Venture Exchange;

“WACC” means weighted average cost of capital, as described in Section 1.15 Critical Accounting Estimates under the heading “Impairment of Mining Assets”;

“Western Ga-Phasha” means the Western section of Ga-Phasha, located on the Eastern Limb of the Bushveld Complex in South Africa, comprising the Klipfontein and Avoca mineral properties, which was consolidated with the Bokoni Mine’s activities on December 13, 2013;

“Working Capital Facility” has the meaning ascribed to it in Section 1.4.3. Working Capital Facility; and

“ZAR” means the South African Rand.

1.1 Introduction

This MD&A should be read in conjunction with the unaudited condensed consolidated interim financial statements for the three months and nine months ended September 30, 2014 and the audited annual consolidated financial statements of Atlatsa for the years ended December 31, 2013, and 2012, prepared in accordance with IFRS, which are publicly available on SEDAR at www.sedar.com and on EDGAR at www.sec.gov. This MD&A is prepared as of November 14, 2014.

Certain statements in this MD&A constitute forward-looking statements or forward-looking information within the meaning of applicable securities laws. Investors should carefully read the cautionary note in this MD&A regarding forward-looking statements and should not place undue reliance on any such forward-looking statements. Refer to “Cautionary Note Regarding Forward-Looking Statements”.

All dollar figures stated herein are expressed in Canadian dollars (“$”), unless otherwise specified.

The closing South African Rand (“ZAR”) to $ exchange rate as at September 30, 2014 was ZAR10.09=$1 compared to ZAR9.77=$1 at September 30, 2013 and ZAR9.87=$1 at December 31, 2013.

The Company’s Common Shares are listed for trading on the TSX (symbol: ATL), NYSE MKT (symbol: ATL) and the JSE (symbol: ATL). The Company migrated to the TSX from the TSXV on February 5, 2014. Following approval by the Company’s shareholders at the Annual General and Special Meeting of the Company held on Friday, June 27, 2014, the Company’s listing status on the

| Atlatsa Resources Corporation |

| |

| Management Discussion and Analysis of Financial Condition and Results of Operations for three and nine months ended September 30, 2014 |

JSE was amended from a primary to a secondary status with effect from July 3, 2014. This allows the Company to comply only with the listing requirements of the TSX on which the Company maintains its primary listing, except as otherwise specifically provided for in the Listings Requirements of the JSE.

Additional information about Atlatsa, including its Annual Report on Form 20-F for Fiscal 2013, as amended, can be found on SEDAR at www.sedar.com and on EDGAR at www.sec.gov.

Cautionary Note Regarding Forward-Looking Statements

This MD&A includes certain statements that may be deemed “forward-looking statements” or “forward-looking information” within the meaning of applicable securities laws. All statements in this MD&A, other than statements of historical facts, that address the potential acquisitions, future production, reserve potential, exploration drilling, exploitation activities and events or developments that Atlatsa expects, are forward-looking statements. These statements appear in a number of different places in this MD&A and can be identified by words such as “anticipates”, “estimates”, “projects”, “expects”, “intends”, “believes”, “plans”, “will”, “could”, “may”, or their negatives or other comparable words. Such forward-looking statements involve known and unknown risks, uncertainties and other factors that may cause Atlatsa’s actual results, performance or achievements to be materially different from any future results, performance or achievements that may be expressed or implied by such forward-looking statements. Atlatsa believes that such forward-looking statements are based on material factors and reasonable assumptions, including assumptions that: the anticipated benefits of the Restructure Plan will be achieved; the Bokoni Mine will maintain production levels in accordance with the mine operating plan; the Bokoni Mine operating plan will continue to be implemented as expected and will achieve improvements in production and operational efficiencies as anticipated; the Platreef Projects will continue to have positive exploration results; contracted parties will provide goods and/or services on the agreed timeframes; equipment necessary for construction and development will be available as scheduled and will not incur unforeseen breakdowns; no material labour slowdowns or strikes will occur; plant, equipment and processes will continue to function as specified; geological or financial parameters will not necessitate future mine plan changes; and no geological or technical problems occur.

Forward-looking statements, however, are not guarantees of future performance and actual results or developments may differ materially from those projected in forward-looking statements. Factors that could cause actual results to differ materially from those in forward looking statements include: uncertainties related to achievement of the financial and operational improvements expected as a result of the Restructure Plan; uncertainties related to the continued implementation of the Bokoni Mine operating plan and opencast mining operations; uncertainties related to the timing of the implementation of the Bokoni Mine deferred expansion plans; fluctuations in market prices, levels of exploitation and exploration successes; changes in and the effect of government policies with respect to mining and natural resource exploration and exploitation; continued availability of capital and financing, general economic, market or business conditions, failure of plant, equipment or processes to operate as anticipated; accidents, labour disputes, industrial unrest and strikes, political instability, suspension of operations and damage to mining property as result of community unrest and safety incidents, insurrection or war and the effect of HIV/AIDS on labour force availability and turnover, delays in obtaining government approvals; and the Company’s ability to satisfy the terms and conditions of its letter of support from Anglo Platinum, dated November 10, 2014, as described in Section 1.11 Liquidity in th MD&A and under “Going Concern” in note two of the Consolidated Financial Statements. These factors and other risk factors that could cause actual results to differ materially from those in forward-looking statements are described in further detail under Item 3D “Risk Factors” in Atlatsa’s Form 20-F.

| Atlatsa Resources Corporation |

| |

| Management Discussion and Analysis of Financial Condition and Results of Operations for three and nine months ended September 30, 2014 |

Atlatsa advises investors that these cautionary remarks expressly qualify in their entirety all forward-looking statements attributable to Atlatsa or persons acting on its behalf. Atlatsa assumes no obligation to update its forward-looking statements to reflect actual results, changes in assumptions or changes in other factors affecting such statements, except as required by law. Investors should carefully review the cautionary statements and risk factors contained in this and other documents that Atlatsa files from time to time with, or furnishes to, Canadian securities regulators or the SEC and which are publicly available on SEDAR at www.sedar.com and on EDGAR at www.sec.gov.

Cautionary Note Regarding Non-IFRS Measures

EBITDA is not a recognized measure under IFRS and should not be construed as an alternative to net earnings or loss determined in accordance with IFRS as an indicator of the financial performance of Atlatsa or as a measure of Atlatsa’s liquidity and cash flows. While EBITDA is a useful supplemental measure of cash flow prior to debt service, changes in working capital, capital expenditures and taxes the Atlatsa’s method of calculating EBITDA may differ from other issuers and, accordingly, EBITDA may not be comparable to similar measures presented by other issuers. See the section entitled “Segment Information” of our audited consolidated financial statements for Fiscal 2013 and the unaudited interim consolidated financial statements for Q3 2014, for a reconciliation of EBITDA to net income (loss) which is publicly available on SEDAR at www.sedar.com and on EDGAR at www.sec.gov.

Cautionary Note to U.S. Investors Concerning Estimates of Measured and Indicated Resources

This MD&A uses the terms “measured resources” and “indicated resources”. Atlatsa advises U.S. investors that while those terms are recognised and required by Canadian securities regulators, the SEC does not recognise them. U.S. investors are cautioned not to assume that any mineralized material in these categories, not already classified as reserves, will ever be converted into reserves. In addition, requirements of NI 43-101 for identification of “reserves” are not the same as those of the SEC, and reserves reported by Atlatsa in compliance with NI 43-101 may not qualify as “reserves” under SEC standards. Under U.S. standards, mineralization may not be classified as a “reserve” unless the determination has been made that the mineralization could be economically and legally produced or extracted at the time the reserve determination is made. Investors should refer to the disclosure under the heading “Resource Category (Classification) Definitions” in Atlatsa’s Form 20-F.

Cautionary Note to U.S. Investors Concerning Estimates of Inferred Resources

This MD&A uses the term “inferred resources”. Atlatsa advises U.S. investors that while this term is recognised and required by Canadian securities regulators, the SEC does not recognize it. “Inferred resources” have a great amount of uncertainty as to their existence, and as to their economic and legal feasibility. It cannot be assumed that all or any part of an inferred resource will ever be upgraded to a higher category. Under Canadian rules, estimates of inferred resources may not form the basis of economic studies, except in rare cases. U.S. investors are cautioned not to assume that any part or all of an inferred resource exists, or is economically or legally mineable. Investors should refer to the disclosure under the heading “Resource Category (Classification) Definitions” in Atlatsa’s Form 20-F.

Cautionary Note to Investors Concerning Technical Review of the Bokoni Mine and Western Ga-Phasha

The following are the principal risk factors and uncertainties which, in management's opinion, are likely to most directly affect the conclusions of the technical review of the Bokoni Mine and of (Western) Ga-Phasha. Some of the mineralized material classified as a measured and indicated resource has been

| Atlatsa Resources Corporation |

| |

| Management Discussion and Analysis of Financial Condition and Results of Operations for three and nine months ended September 30, 2014 |

used in the cash flow analysis. Under U.S. mining standards, a full feasibility study would be required in order for such mineralized material to be included in the cash flow analysis, which would require more detailed studies. Additionally, all necessary mining permits would be required in order to classify these parts of the Bokoni Mine’s and Western Ga-Phasha’s mineralized material as a mineral reserve. There can be no assurance that this mineralized material will become classifiable as a reserve and there is no assurance as to the amount, if any, which might ultimately qualify as a reserve or what the grade of such reserve amounts would be. Data is not complete and cost estimates have been developed, in part, based on the expertise of the individuals participating in the preparation of the technical review and on costs at projects believed to be comparable, and not based on firm price quotes. Costs, including design, procurement, construction and on-going operating costs and metal recoveries could be materially different from those contained in the technical review. There can be no assurance that mining can be conducted at the rates and grades assumed in the technical review. There can be no assurance that the infrastructure facilities can be developed on a timely and cost-effective basis. Energy risks include the potential for significant increases in the cost of fuel and electricity and for fluctuation in the availability of electricity. Projected metal prices have been used for the technical review. The prices of these metals are historically volatile, and the Company has no control or influence over the prices of these metals, which are determined in international markets. There can be no assurance that the prices of platinum, palladium, rhodium, gold, copper or nickel will continue at current levels or that they will not decline below the prices assumed in the technical review. Prices for these commodities have been below the price ranges assumed in the technical report at times during the past ten years and for extended periods of time. The expansion projects described herein will require major financing; probably a combination of debt and equity financing. There can be no assurance that debt and/or equity financing will be available to the Company on acceptable terms or at all. A significant increase in costs of capital could materially adversely affect the value and feasibility of constructing the expansions. Other general risks include those ordinary to large construction projects, including the general uncertainties inherent in engineering and construction cost, the need to comply with generally increasing environmental obligations and the accommodation of local and community concerns. The conclusions, assumptions and economics of the technical review are sensitive to the currency exchange rates, which have been subject to large fluctuations in the last several years.

1.2 Overview

Atlatsa is engaged in the mining, exploration and development of PGM mineral deposits located in the BIC. The BIC is the world’s largest platinum producing geological region, producing about 75% of the world’s annual primary platinum supply to international markets.

Atlatsa, through its wholly owned South African subsidiary, Plateau, holds a 51% interest in Bokoni Holdco, which in turn holds a 100% interest in several PGM projects, including the operating Bokoni Mine and the Kwanda Exploration Project. Plateau also holds a 100% direct interest in a number of other PGM exploration projects in the northern limb of the BIC. On December 13, 2013, the mineral properties in Boikgantsho and the Eastern portion of Ga-Phasha (Paschaskraal and De Kamp mineral properties) were sold to RPM. The Western portion of Ga-Phasha, containing the Klipfontein and Avoca mineral properties was subsequently incorporated into the Bokoni mining right; such that Boikgantsho and Ga-Phasha do not currently hold any mineral properties. Both companies are now dormant.

The Bokoni Mine is the Company’s operating mine and its only producing asset. Kwanda holds assets which are currently in the exploration stage. Refer to Section 1.7 Operations, for more details of each of the entities.

| Atlatsa Resources Corporation |

| |

| Management Discussion and Analysis of Financial Condition and Results of Operations for three and nine months ended September 30, 2014 |

Atlatsa’s objective is to become a significant PGM producer with a substantial and diversified PGM asset base, including production and exploration assets. Atlatsa controls a significant estimated mineral resource base of approximately 56 million ounces in the measured category, 27.7 million ounces in the indicated category and 70.5 million ounces in the inferred category. Of this estimated mineral resource base, approximately 28.5 million ounces in the measured category, 14.1 million ounces in the indicated category and 36 million ounces in the inferred category are attributable to Atlatsa. Refer to page 13 of Atlatsa’s technical report entitled “An Independent Qualified Persons’ Report on the Bokoni Platinum Mine, in the Mpumalanga Province, South Africa” dated April 24, 2013 and filed on SEDAR at www.sedar.com on May 14, 2013.

Anglo Platinum, through its wholly owned subsidiary RPM, holds a 49% interest in Bokoni Holdco. During Fiscal 2011, Fiscal 2012 and Fiscal 2013, Atlatsa and Anglo Platinum engaged in negotiations to refinance, restructure and recapitalize the Company. On January 31, 2014, the Company announced completion of the Restructure Plan. Refer to Section 1.3 Restructure Plan for more details.

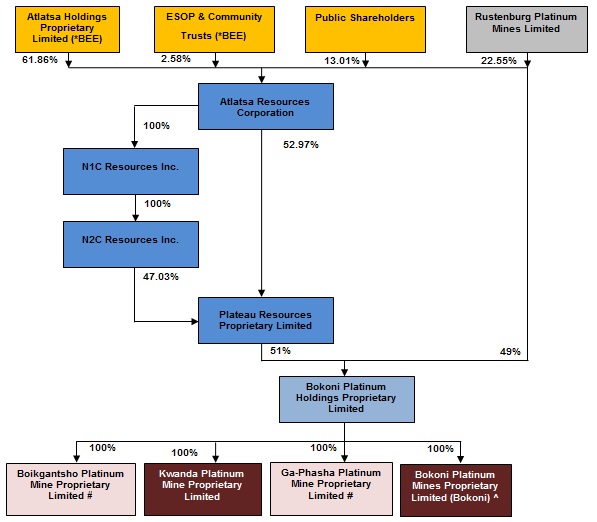

The corporate structure of Atlatsa and its subsidiaries as at September 30, 2014 is as follows:

* Black Economic Empowerment

| Atlatsa Resources Corporation |

| |

| Management Discussion and Analysis of Financial Condition and Results of Operations for three and nine months ended September 30, 2014 |

# Dormant from December 13, 2013. Refer to Section 1.3 – Restructure Plan

^ Bokoni Rehabilitation Trust is consolidated into Bokoni

The following are key financial consolidated performance highlights for Atlatsa for Q3 2014:

| | · | Atlatsa realised a gross profit for Q3 2014 of $3.7 million, which is an improvement of $8.5 million compared to the gross loss incurred in Q3 2013 of ($4.8 million). |

| | · | Atlatsa had an operating loss of ($0.8 million) and a loss before income tax of ($2.3 million) for Q3 2014, compared to an operating loss of ($2.2 million) and a loss before income tax of ($17.2 million) for Q3 2013. |

| | · | The net loss (after tax) was ($0.6 million) for Q3 2014, as compared to a net loss (after tax) of ($15.5 million) for Q3 2013. |

| | · | The Company has recognised a fair value loss and AG8 adjustments of ($0.04 million) in its Consolidated Statement of Profit or Loss and Other Comprehensive Income for Q3 2014, compared to a fair value gain and AG8 adjustments of $5.4 million for Q3 2013, due to the refinancing cash flow implications being moved out as a result of the delay in finalisation of the Restructure Plan and no drawdowns being made in Q3 2014 compared to drawdowns of $15.2 million in Q3 2013. In addition to this, post December 13, 2013, only the debt between Plateau and RPM was fair valued as the 49% contribution by RPM to Holdco was treated as a shareholders loan with the intention to capitalise these loans, which took place on March 31, 2014. Refer to Section 1.3 Restructure Plan for a discussion on the fair value adjustments. |

| | · | The basic and diluted loss per share for Q3 2014 was ($0.00) as compared to a basic and diluted loss per share of ($0.03) for Q3 2013. The basic and diluted loss per share is calculated by dividing the loss attributable to the shareholders of the Company of ($0.5 million) for Q3 2014 and a loss of ($12.9 million) for Q3 2013 by the weighted average number of shares of 593.1 million (593.1 million on a diluted basis) for Q3 2014 and the weighted average number of shares of 424.8 million (424.8 million on a diluted basis) for Q3 2013. The number of shares outstanding increased from Q3 2013 to Q3 2014 as a result of the additional shares issued during the course of the Restructure Plan, discussed below. All share options and unvested treasury shares were disregarded in the calculation of the basic and diluted loss per share, as these are anti-dilutive. |

| | · | Atlatsa generated cash from operations of $10.0 million in Q3 2014 compared to cash generated from operations of $7.4 million in Q3 2013. Cash generated before working capital changes increased from $2.1 million in Q3 2013 to $10.8 million in Q3 2014. |

| | · | Bokoni’s EBITDA increased year-on-year with Bokoni achieving a positive EBITDA of $11.3 million for Q3 2014, compared to a positive EBITDA of $10.4 million in Q3 2013. This increase is mainly due to Bokoni realising a gross profit for Q3 2014 of $3.9 million (ZAR38.5 million) and an operating profit of $1.8 million (ZAR17.3 million). |

| | · | During Q3 2014, the Bokoni Mine produced 56,025 4E ounces as compared to 47,611 4E ounces during Q3 2013. The increase is mainly attributable to the increase in tonnage. |

The following are key financial consolidated performance highlights for Atlatsa for the nine months ended September 30, 2014:

| | · | Atlatsa had an operating loss of ($18.6 million), and a loss before income tax of ($29.9 million) for the nine months ended September 30, 2014, compared to an to an operating profit of $3.0 million and a loss before income tax of ($40.8 million) for the nine months ended September 30, 2013. |

| Atlatsa Resources Corporation |

| |

| Management Discussion and Analysis of Financial Condition and Results of Operations for three and nine months ended September 30, 2014 |

| | · | The net loss (after tax) was ($25.3 million) for the nine months ended September 30, 2014, as compared to a net loss (after tax) of ($33.3 million) for the nine months ended September 30, 2013. |

| | · | The Company has recognised a fair value gain and AG8 adjustments of $0.5 million in its Consolidated Statement of Profit or Loss and Other Comprehensive Income for the nine months ended September 30, 2014, compared to a fair value gain and AG8 adjustments of $34.8 million for the nine months ended September 30, 2013. This is mainly due to the difference in the fair value gain and AG8 adjustments recognised on the debt, due to the refinancing cash flow implications being moved out as a result of the delay in finalisation of the restructure plan and the drawdowns for the nine months ended September 30, 2014, being lower than for the nine months ended September 30, 2013. Also, post December 13, 2013, only the debt between Plateau and RPM was fair valued as the 49% contribution by RPM to Holdco was treated as a shareholder loan with the intention to capitalise these loans which took place on March 31, 2014. Refer to Section 1.3 Restructure Plan - 1.3.1 Phase One for a discussion on the fair value adjustments. |

| | · | The basic and diluted loss per share for the nine months ended September 30, 2014 was ($0.02) as compared to ($0.07) for the nine months ended September 30, 2013. The basic and diluted loss per share is calculated by dividing the loss attributable to the shareholders of the Company of ($12.4 million) for the nine months ended September 30, 2014 and ($28.3 million) for the nine months ended September 30, 2013 by the weighted average number of shares of 593.1 million (593.1 million on a diluted basis) for September 30, 2014 and the weighted average number of shares of 424.8 million (424.8 million on a diluted basis) for the nine months ended September 30, 2013. The number of shares outstanding increased from September 30, 2013 to September 30, 2014 as a result of the additional shares issued during the course of the Restructure Plan, discussed below. All share options and unvested treasury shares were disregarded in the calculation of the basic and diluted loss per share, as these are anti-dilutive. |

| | · | During the nine months ended September 30, 2014, the Bokoni Mine produced 145,622 4E ounces as compared to 126,555 4E ounces during the nine months ended September 30, 2013. The increase is mainly attributable to the increase in tonnage. |

The following are the key changes in financial condition for Atlatsa for Q3 2014 compared to Fiscal 2013:

| | · | Atlatsa’s total assets decreased by $41.8 million (5.4%) from $773.6 million at December 31, 2013 to $731.8 million at September 30, 2014. This decrease in total assets is primarily due to: |

| | o | a decrease of $26.8 million in cash and cash equivalents mainly due to the payment after December 31, 2013 of the Value Added Tax (“VAT”) liability on the sale of the mineral properties of Boikgantsho and Eastern Ga-Phasha on December 13, 2013; |

| | o | a decrease of $8.4 million in trade and other receivables as a result of the impact of utilizing the Advance; |

| | o | amortisation on the mineral property interests of $2.1 million; |

| | o | depreciation on property plant and equipment of $27.4 million; and |

| | o | a deterioration of 2.2% of the ZAR against the $ since December 31, 2013. |

These decreases were partially off-set by additions to capital work-in-progress of $8.7 million and an increase in inventory of $6.5 million mainly as a result of the increase in stockpile.

| Atlatsa Resources Corporation |

| |

| Management Discussion and Analysis of Financial Condition and Results of Operations for three and nine months ended September 30, 2014 |

| | · | Atlatsa’s total liabilities decreased by $95.5 million (24%) from $394.5 million at December 31, 2013 to $299.0 million at September 30, 2014. This decrease in total liabilities is primarily due to: |

| | o | a decrease of $24.1 million in trade and other payables mainly as a result of the VAT incurred on the sale of the mineral properties of Boikgantsho and Eastern Ga-Phasha on December 13, 2013 and paid after December 31, 2013; |

| | o | a net decrease in the Company’s loans and borrowings of $64.9 million resulting mainly from $74.8 million (ZAR750.0 million – translated at transaction date; January 31, 2014) being repaid of the New Senior Facilities Agreement in Q1 2014 as part of the Restructure Plan (this was disclosed as short-term portion of loans and borrowings at December 31, 2013), additional drawdowns of $14.7 million, shareholder loans capitalised of $12.5 million and interest accrued of $12.4 million; and |

| | o | a deterioration of 2.2% of the ZAR against the $ since December 31, 2013. |

1.3 Restructure Plan

On February 2, 2012, the Company and Anglo Platinum announced the parties’ conclusion of a term sheet comprising the first iteration of the Restructure Plan.

Subsequent to announcing the material terms of the Restructure Plan in February 2012, the Company announced that it, together with Anglo Platinum and the management of Bokoni; had undertaken a strategic review of the Bokoni Mine operations in order to assess the optimal operating and financial plan for the Bokoni Mine going forward.

1.3.1 Phase One

In Phase One of the Restructure Plan (September 28, 2012), the 2009 Senior Debt Facility was amended to increase the total amount available under the facility, and this additional amount was utilized to repay the amounts owed to RPM under the OCSF, such that the principal amount outstanding under the OCSF as at September 28, 2013 was $0, and to redeem the existing “A” Preference Share Facility. As a result, the Company lowered its cost of borrowing. After the consolidation of the balance outstanding under the OCSF into the 2009 Senior Debt Facility, a portion of the available balance under the 2009 Senior Debt Facility continued to represent a facility available to the Company under the terms of the OCSF.

These transactions resulted in all outstanding debt owing to RPM as at that date being consolidated into one single facility on terms and conditions agreed between the parties, including an interest rate adjustment, which lowered the Company’s cost of borrowing from 12.31% (prior to implementation of Phase One) to a current interest rate of 4.58% (such rate being linked to JIBAR, which was 6.13% at September 30, 2014) compared to 5.92% at the end of Q3 2013.

The portion of the debt between RPM and Bokoni Holdco was considered a shareholder loan. As a result, when a transaction is with a shareholder at terms and conditions that would not be expected from a third party, it is clear that either the company or the shareholder obtained a benefit because of the shareholder relationship. In respect of loans with shareholders, the difference between the loan received and the amount recognised at fair value on initial recognition, is recognised as a fair value gain or loss directly in equity. A fair value adjustment was therefore recorded on the 2009 Senior Debt Facility.

| Atlatsa Resources Corporation |

| |

| Management Discussion and Analysis of Financial Condition and Results of Operations for three and nine months ended September 30, 2014 |

1.3.2 Phase Two

On March 27, 2013, the Company announced the execution of definitive agreements for Phase Two of the Restructure Plan which included the disposal of certain mineral properties representing undeveloped estimated PGM resources to RPM, and the recapitalization and refinancing of Atlatsa and the Bokoni Group, together with an undertaking to accelerate production growth at the Bokoni Mine. The first part of Phase Two was completed on December 13, 2013 and the remainder of the Phase Two transactions were completed by January 31, 2014.

Certain of the transactions completed as part of Phase Two of the Restructure Plan were “related party transactions” pursuant to Multilateral Instrument 61-101 – Protection of Minority Securityholders Interest in Special Transactions. Readers are referred to the management information circular of the Company dated May 28, 2013 (as filed on SEDAR on May 31, 2013), for more information regarding the related party aspects of Phase Two, including details of formal valuations obtained by Atlatsa. Included in the information circular are details of Minxcon (an independent valuator) as well as PSG (in relation to a fairness opinion over the Restructure Plan).

Management received disinterested Shareholder approval for Phase Two of the Restructure Plan on June 28, 2013.

As part of Phase Two of the Restructure Plan, under the New Senior Facilities Agreement signed on March 27, 2013, Anglo Platinum agreed to make additional facilities available to the Company, after the 2009 Senior Debt Facility had been fully utilised by the Company, to finance the Company’s pro rata share of the Bokoni Mine going forward. The Company was not entitled to drawdown amounts under the New Senior Facilities Agreement until, amongst other things, certain conditions precedent were met. These conditions precedent were completed on December 12, 2013.

Due to delays in closing the Restructure Plan, and the fact that the Company required additional funding prior to the date the New Senior Facilities Agreement became available to the Company (i.e. December 13, 2013), the parties agreed to increase the amount available for drawdown under the 2009 Senior Debt Facility by $21.4 million (ZAR215.7 million). An agreement effecting this increase was signed on May 28, 2013 (the “Amending Agreement”).

In addition to the facilities described above, RPM and Bokoni entered into an agreement on November 13, 2013 (the “Advance on Concentrate Revenue Agreement”) pursuant to which RPM agreed to fund Bokoni with an advance on the revenue from the sale of concentrate made to RPM under the Concentrate Agreement (the “Advance”) at an interest rate of JIBAR plus 1.41% per annum, from November 1, 2013 to November 30, 2014. The Advance on Concentrate Revenue Agreement was amended in July 2014 to extend the term to December 31, 2015. The Advance on Concentrate Revenue Agreement was necessary to cover the additional cash requirements of the Bokoni Mine which resulted from the delay in the completion of the Restructure Plan. Refer to Section 1.4.4. Advance on the Purchase of Concentrate Revenue for more details.

The conditions precedent for the completion of Phase Two of the Restructure Plan were completed on December 12, 2013. On December 13, 2013 the following transactions, forming part of Phase Two of the Restructure Plan, were completed:

| | · | the sale and transfer of the Company’s mineral properties in Boikgantsho and Eastern Ga-Phasha to RPM for a net consideration of $168.5 million (ZAR1.7 billion). For accounting purposes; this sale gave rise to a profit on sale of $171.1 million in the Consolidated Statement |

| Atlatsa Resources Corporation |

| |

| Management Discussion and Analysis of Financial Condition and Results of Operations for three and nine months ended September 30, 2014 |

of Profit or Loss and Other Comprehensive Income for the year ended December 31, 2013 (also refer to note 35 in the audited annual financial statements for Fiscal 2013);

| | · | the purchase consideration payable for the sale of the Boikgantsho mineral property was paid to the Company on December 13, 2013, excluding an amount of $2.9 million (ZAR29.0 million), which is payable on the date of execution of the notarial deed of extension of the RPM Mining Right to include the Boikgantsho Prospecting Rights. The proceeds paid to the Company of $165.6 million (ZAR1,671 million) were used to reduce the outstanding debt to RPM under the 2009 Senior Debt Facility; |

| | · | RPM subscribed for additional shares of Bokoni Holdco to the value of $192.2 million (ZAR1,939.4 million). Bokoni Holdco utilised these funds to repay certain shareholder loans outstanding between Bokoni Holdco and RPM in the amount of $192.2 million (ZAR1,939.4 million); |

| | · | Plateau subscribed for additional shares of Bokoni Holdco as part of the funding between Plateau and Bokoni Holdco, and as such Plateau’s interest in Bokoni Holdco has not been diluted. This transaction is eliminated for the Company’s consolidation purposes; |

| | · | the 2009 Senior Debt Facility was repaid in full (refer to Section 1.4.1. 2009 Senior Debt Facility) and the New Senior Facilities Agreement between Plateau and RPM as signed on March 27, 2013 was made effective. $228.0 million (ZAR2.3 billion) was made available under the New Senior Facilities Agreement of which $156.4 million (ZAR1,578.0 million) inclusive of interest, was utilized by September 30, 2014. Refer to Section 1.4.2. New Senior Facilities Agreement; |

| | · | Plateau also entered into the Working Capital Facility of $8.9 million (ZAR90 million) with RPM to fund Atlatsa’s corporate and administrative expenses through to the end of 2015 of which $5.6 million (ZAR56.4 million) was utilised as at September 30, 2014. Refer to Section 1.4.3. Working Capital Facility; and |

| | · | the Concentrate Agreement (as described in Section 1.7.1 Bokoni Mine, under the sub-heading “Sale of Concentrate”) was extended until 2020. |

The replacement of the 2009 Senior Debt Facility with the New Senior Facilities Agreement between RPM and Plateau gave rise to fair value adjustments as the terms of the New Senior Facilities Agreement differ significantly from those of the 2009 Senior Debt Facility. The fair value adjustment resulted from the Company’s new cost of borrowing under the consolidated 2009 Senior Debt Facility and the fact that the New Senior Facilities Agreement is more favourable to the Company compared to a market related cost of borrowing available to the Company.

The loan between Bokoni Holdco and RPM resulted in a fair value loss as the contractual debt that was settled was greater than the fair value of the debt.

During January 2014, Phase Two of the Restructure Plan was finalized by completing the following:

| | · | Pelawan SPV converted the SPV Preferred Shares held by RPM into SPV Ordinary Shares and converted the “B” Preference Shares held by Pelawan SPV in Plateau into Plateau Ordinary Shares. In addition, in accordance with the terms of the Plateau Ordinary Shares, Plateau issued Pelawan SPV a special dividend in cash of $24.0 million (ZAR241.7 million), which Pelawan SPV used to subscribe for additional Plateau Ordinary Shares. |

| | · | As per the Exchange Agreement, Atlatsa issued 227.4 million Atlatsa Common Shares to Pelawan SPV in exchange for the Plateau Ordinary Shares. Following this issuance, Pelawan |

| Atlatsa Resources Corporation |

| |

| Management Discussion and Analysis of Financial Condition and Results of Operations for three and nine months ended September 30, 2014 |

SPV immediately bought back all SPV Ordinary Shares held by RPM and settled the buyback consideration by delivering to RPM 115.8 million Common Shares in the Company. On January 29, 2014, RPM sold these 115.8 million Common Shares in the Company to Atlatsa Holdings, held in trust by the Pelawan Trust in exchange for the Atlatsa Holdings Vendor Finance Loan. Atlatsa Holdings increased its shareholding in the Company to 61.86%.

| | · | On January 29, 2014, Atlatsa Holdings, the Company’s majority shareholder; acquired the 115.8 million Common Shares in the Company from RPM on a vendor financed basis, which resulted in Atlatsa Holdings owing $45.9 million (ZAR463.2 million) to RPM, to be repaid in stages by December 31, 2020 (the “Atlatsa Holdings Vendor Finance Loan”); |

| | · | Pelawan SPV transferred the remaining 111.6 million Common Shares in the Company issued to Pelawan SPV pursuant to the Exchange Agreement to Atlatsa Holdings in trust for the Pelawan Trust. Such Common Shares are subject to a lock-in that prevents Pelawan SPV and Atlatsa Holdings from disposing of such Common Shares for so long as Atlatsa Holdings is required to maintain a minimum 51% shareholding in Atlatsa (at present the contractual lock up provision for Atlatsa Holdings on all of its Atlatsa Common Shares remains in place up to January 1, 2015). |

| | · | Atlatsa Holdings provided security to RPM in relation to the Atlatsa Holdings Vendor Finance Loan by way of a pledge and cession of its entire shareholding in Atlatsa, which shares remain subject to a lock-in arrangement through to 2020. Should Atlatsa Holdings be unable to meet its minimum repayment commitments under the Atlatsa Holdings Vendor Finance Loan between 2018 to 2020, Atlatsa will have a discretionary right, with no obligation, to step in and remedy such obligation in order to protect its BEE shareholding status, subject to commercial terms being agreed between Atlatsa Holdings and Atlatsa for that purpose and receipt of the necessary regulatory and shareholder approvals; and |

| | · | RPM subscribed for 125 million Common Shares of the Company on January 31, 2014, for $74.3 million (ZAR750.0 million), which proceeds were used to repay a portion of the Company’s outstanding debt to RPM under the New Senior Facilities Agreement. |

On February 1, 2014, after completion of Phase Two of the Restructure Plan; Atlatsa had an outstanding share capital of 554,288,473 Common Shares.

For additional information on the Restructure Plan refer to the press releases of Atlatsa between February 2, 2012, and February 3, 2014 as well as the material change reports filed on February 13, 2012, September 27, 2012 and April 8, 2013, all of which are available on SEDAR at www.sedar.com and on EDGAR at www.sec.gov.

1.4 Debt Arrangements

1.4.1. 2009 Senior Debt Facility

The balance under the 2009 Senior Debt Facility as at December 13, 2013 was $216.9 million (ZAR2,188.8 million) after repaying $165.6 million (ZAR1,671 million) of the 2009 Senior Debt Facility with the cash received from the sale of the mineral properties of Eastern Ga-Phasha and Boikgantsho. On December 13, 2013, the Company drew down $216.9 million (ZAR2,188.8 million) under the New Senior Facilities Agreement to pay and settle the 2009 Senior Debt Facility. As of December 13, 2013, the 2009 Senior Debt Facility is no longer in effect and is described herein for historical purposes only.

| Atlatsa Resources Corporation |

| |

| Management Discussion and Analysis of Financial Condition and Results of Operations for three and nine months ended September 30, 2014 |

1.4.2. New Senior Facilities Agreement

The total amount available to Plateau under the New Senior Facilities Agreement is $228 million (ZAR2.3 billion). Subsequently, Atlatsa used the proceeds of $74.8 million (ZAR750.0 million - translated at transaction date; January 31, 2014) from the subscription for 125 million Common Shares in the Company by RPM on January 31, 2014 to reduce the amount outstanding between Plateau and RPM under the New Senior Facilities Agreement to $153.6 million (ZAR1.55 billion); this becoming the amended maximum available under this facility.

In the event Plateau draws down on the facility available under the New Senior Facilities Agreement to fund its 51% contribution to Bokoni Holdco, RPM is obliged to meet its 49% contribution to Bokoni Holdco as a shareholder loan to Bokoni Holdco.

During Q1 2014, Plateau drew down $6.2 million (ZAR61.3 million) on the New Senior Facilities Agreement to contribute to Bokoni Holdco for utilisation by Bokoni Mine. RPM provided $6.0 million (ZAR58.9 million) to Bokoni Holdco as their 49% contribution. This resulted in the facility being fully utilised. Although the facility limit of the New Senior Facilities Agreement has been reached, Anglo Platinum’s Board of Directors agreed to allow an amount of $15.9 million (ZAR160.0 million) in unpaid interest to accrue above the facility limit of $153.6 million (ZAR1,550 million), up to December 31, 2015. The total amount outstanding under the New Senior Facilities Agreement as at September 30, 2014 was $156.4 million (ZAR1,578.0 million) inclusive of interest.

Pursuant to the Bokoni Holdco Shareholders Agreement, the board of directors of Bokoni Holdco, which is controlled by Atlatsa, has the right to call for shareholder contributions, either by way of a shareholder loan or equity cash call.

RPM’s 49% contributions to Bokoni Holdco between December 13, 2013 and March 31, 2014 were treated as shareholder loans. The treatment of these shareholder loans was decided by the Board of Directors of Bokoni Holdco as per the Bokoni Holdco Shareholders Agreement. On March 31, 2014, these shareholder loans to the value of $9.3 million were capitalised for additional shares in Bokoni Holdco.

As of September 30, 2014, no shareholder loans remain outstanding. The shareholder loans bear no interest and no repayment terms.

The repayment terms of the New Senior Facilities Agreement include quarterly cash sweeps, when cash is available. Atlatsa will be required to reduce the outstanding balance (including capitalised interest) under the New Senior Facilities Agreement to $99.1 million (ZAR1.0 billion) by December 31, 2018, to $49.6 million (ZAR500.0 million) by December 31, 2019 and to zero by December 31, 2020.

1.4.3. Working Capital Facility

Prior to implementation of Phase Two of the Restructure Plan and as an interim measure prior to the closing of the Restructure Plan, RPM and Plateau agreed to a transaction cost loan agreement, as signed and implemented on May 28, 2013 (the “Transaction Cost Loan Agreement”), to make a facility of $2.2 million (ZAR22.5 million) available to Plateau.

The increase of $21.4 million (ZAR215.7 million) under the 2009 Senior Debt Facility pursuant to the Amending Agreement is inclusive of the $2.2 million (ZAR22.5 million) provided for under the Transaction Cost Loan Agreement. The facility under the Transaction Cost Loan Agreement carried interest at the Prime Rate plus 5%.

| Atlatsa Resources Corporation |

| |

| Management Discussion and Analysis of Financial Condition and Results of Operations for three and nine months ended September 30, 2014 |

On December 13, 2013, Plateau and RPM entered into a working capital facility whereby RPM agreed to provide a maximum of $3.0 million (ZAR30.0 million) to Plateau each year from 2013 to 2015, inclusive, up to an aggregate amount of $8.9 million (ZAR90.0 million), (including capitalised interest), to fund Plateau’s corporate and administrative expenses through to 2015 (the “Working Capital Facility”). On December 13, 2013, Plateau drew down $3.0 million (ZAR29.9 million) on the Working Capital Facility and repaid the amount outstanding under the Transaction Cost Loan Agreement of $0.7 million (ZAR7.2 million) including interest. The Transaction Cost Loan Agreement is no longer in effect and is described herein for historical purposes only.

Pursuant to the terms of the Working Capital Facility, interest will be charged on the outstanding amounts of the Working Capital Facility at a rate of three-month JIBAR plus 4% per annum. The balance of the Working Capital Facility cannot exceed $8.9 million (ZAR90.0 million) at any time, including capitalised interest. Atlatsa is prohibited from paying any dividends until the Working Capital Facility is fully repaid. The Working Capital Facility is repayable in full by December 31, 2018.

During Q3 2014, $1.0 million (ZAR10.0 million) was drawn down under the Working Capital Facility, which brought the contractual balance to $5.6 million (ZAR56.4 million) as at September 30, 2014, inclusive of cumulative interest.

In March 2014, Plateau entered into an agreement with RPM whereby, in the event Bokoni Mine requires additional cash resources in the short term, Plateau could use the undrawn amounts under the Working Capital Facility for such purposes.

1.4.4. Advance on the Purchase of Concentrate Revenue

In addition to the other facilities provided, RPM agreed to fund the Bokoni Mine, pursuant to the Advance on Concentrate Revenue Agreement, with an advance on the sale of concentrate revenue made to RPM pursuant to the Concentrate Agreement, at an interest rate of JIBAR plus 1.41% per annum, from November 1, 2013 to November 30, 2014.

The Advance on Concentrate Revenue Agreement provided that RPM may advance funds to Bokoni up to an amount equal to the lower of 90% of an advance on revenue for the preceding two months and $35.7 million (ZAR360.0 million), provided that the amount advanced shall not exceed the actual cash requirements for that month. The terms of the Advance on Concentrate Revenue Agreement were re-negotiated in March 2014 to permit RPM to advance funds to Bokoni up to an amount equal to the lower of 95% of an advance on revenue for the preceding two months and $47.1 million (ZAR475.0 million), provided that the amount advanced shall not exceed the actual cash requirements of Bokoni Mine for that month, and to extend the term of the Advance on Concentrate Revenue Agreement to March 31, 2015. In July 2014, the Advance on Concentrate Revenue Agreement was amended to extend the term of the agreement to December 31, 2015.

Drawdowns pursuant to the Advance on Concentrate Revenue Agreement of $36.5 million (ZAR368.0 million) were made against the concentrate revenue in Q3 2014, of which $7.9 million (ZAR80.0 million) was already recovered and $28.5 million (ZAR288.0 million) will be recovered as part of revenue received from RPM in October and November 2014.

Also refer to Section 1.11 Liquidity, under the sub-heading “Going Concern” for details on how the Advance will be utilised.

| Atlatsa Resources Corporation |

| |

| Management Discussion and Analysis of Financial Condition and Results of Operations for three and nine months ended September 30, 2014 |

1.4.5. Vendor Finance Facility – Share Settled Financing – The “B” Preference Shares

On July 1, 2009, RPM provided a vendor finance facility to Plateau consisting of a cash component, the “A” Preference Share Facility of $118.9 million (ZAR1.2 billion) and a share settled component (the “Share-Settled Financing”) amounting to $109.0 million (ZAR1.1 billion). Refer to Section 1.3 Restructure Plan for details of the repayment of these facilities.

Pursuant to the Share Settled Financing, Atlatsa Holdings, the majority shareholder of Atlatsa, established a wholly owned subsidiary, Pelawan SPV, and transferred 56,691,303 Common Shares in the Company to the Pelawan SPV. RPM subscribed for convertible preferred shares in the capital of the Pelawan SPV (the “SPV Preferred Shares”) for an aggregate sum of $109.0 million (ZAR1.1 billion). Atlatsa Holdings encumbered its shareholding in the Pelawan SPV in favour of RPM as security for the obligations of the Pelawan SPV pursuant to the SPV Preferred Shares.

Pelawan SPV then subscribed for two different classes of convertible class B preferred shares (the ““B” Preference Shares”) in Plateau for $109.0 million (ZAR1.1 billion), each such class being convertible into ordinary shares in the capital of Plateau (“Plateau Ordinary Shares”) and entitling the holder of the Plateau Ordinary Shares to a special dividend in cash, which, upon receipt, would immediately be used to subscribe for additional Plateau Ordinary Shares. The “B” Preference Shares were zero coupon shares and carried no rights to preference dividends.

Pursuant to the agreement between Pelawan SPV and Atlatsa (the “Exchange Agreement”), upon Plateau issuing Plateau Ordinary Shares to Pelawan SPV, Atlatsa would take delivery of all Plateau Ordinary Shares held by the Pelawan SPV and, in consideration thereof, issue to Pelawan SPV such number of Atlatsa Common Shares that would have a value equal to the value of such Plateau Ordinary Shares. The total number of Atlatsa Common Shares to be issued on implementation of the Share-Settled Financing arrangement was 227.4 million Atlatsa Common Shares.

The SPV Preferred Shares were convertible in one or more tranches into ordinary shares in the capital of the Pelawan SPV (“SPV Ordinary Shares”) immediately upon demand by RPM, upon the earlier of (i) the date of receipt by the Pelawan SPV of a conversion notice from RPM and (ii) July 1, 2018. Pelawan SPV received a conversion notice from RPM on January 7, 2014.

Pursuant to the conversion notice received by Pelawan SPV on January 7, 2014, Pelawan SPV converted the SPV Preferred Shares held by RPM into SPV Ordinary Shares on January 14, 2014 and converted the “B” Preference Shares held by Pelawan SPV in Plateau into Plateau Ordinary Shares. In addition, in accordance with the terms of the Plateau Ordinary Shares, Plateau issued Pelawan SPV a special dividend in cash of $24.0 million (ZAR241.7 million), which Pelawan SPV used to subscribe for additional Plateau Ordinary Shares.

The Share Settled Financing is now complete and is described herein for historical purposes only.

Refer to Section 1.3 Restructure Plan for details of Phase Two of the Restructure Plan.

1.4.6. Security

The New Senior Facilities Agreement is secured through various security instruments, guarantees and undertakings provided by Atlatsa against its portion (51%) of the cash flows generated by Bokoni, together with its portion (51%) of Bokoni’s asset base.

| Atlatsa Resources Corporation |

| |

| Management Discussion and Analysis of Financial Condition and Results of Operations for three and nine months ended September 30, 2014 |

1.5 Black Economic Empowerment

Atlatsa Holdings, the majority shareholder of Atlatsa, is a broad based BEE entity. Through Atlatsa Holdings, Atlatsa remains compliant with the BEE equity requirements contemplated under South African legislation and the associated charters regarding BEE equity holding requirements.

1.6 Environmental Matters

The South African National Environmental Management Act 107 of 1998 as well as the MPRDA, which applies to all prospecting and mining operations, requires that operations be carried out in accordance with generally accepted principles of sustainable development. It is a MPRDA requirement that an applicant for a mining right must make prescribed financial provision for the rehabilitation or management of negative environmental impacts, which must be reviewed annually. The financial provisions deal with anticipated costs for:

| | · | planned decommissioning and closure; and |

| | · | post closure management of residual and latent environmental impacts. |

In respect of the Bokoni Mine, an internal assessment was completed in Q3 2014, with an external review scheduled to take place in November 2014 to determine the environmental closure liability as at December 31, 2014. As at September 30, 2014, the total environmental rehabilitation liability for the Bokoni Mine, in current monetary terms (discounted), was estimated at $11.5 million (ZAR116.3 million) compared to $10.3 million (ZAR100.7 million) in Q3 2013 and $11.1 million (ZAR109.6 million) as of December 31, 2013.

The undiscounted future rehabilitation liability was estimated at $18.4 million (ZAR185.6 million) as at December 31, 2013, compared to $13.5 million (ZAR115.3 million) as at December 31, 2012. This is valued on an annual basis.

The Company makes annual contributions to a dedicated trust fund (the “Environmental Trust Fund”) to cover the estimated cost of rehabilitation during and at the end of life of the Bokoni Mine.

As at September 30, 2014, the amount invested in the Environmental Trust Fund was $3.6 million (ZAR35.9 million) compared to $3.2 million (ZAR31.3 million) in Q3 2013 and $3.3 million (ZAR32.5 million) at December 31, 2013. The shortfall of $8.0 million between the funds invested in the Environmental Trust Fund and the estimated rehabilitation cost is covered by a guarantee from RPM.

Atlatsa’s mining and exploration activities are subject to extensive environmental laws and regulations. These laws and regulations are continually changing and are generally becoming more restrictive. Atlatsa has incurred, and expects to incur in the future, expenditures to comply with such laws and regulations, but cannot predict the full amount of such future expenditures. Estimated future reclamation costs are based principally on current legal and regulatory requirements.

As at December 31, 2013, the Company identified a potential future pollution risk posed by deep groundwater in certain underground shafts. As such a contingency was disclosed at December 31, 2013 (also refer to note 34 in the audited annual financial statements for Fiscal 2013). In light of the current information, no reliable estimate can be made for a potential obligation.

| Atlatsa Resources Corporation |

| |

| Management Discussion and Analysis of Financial Condition and Results of Operations for three and nine months ended September 30, 2014 |

1.7 Operations

1.7.1 Bokoni Mine

Overview

The Bokoni Mine is an operating mine situated in the Sekhukhune-land District of the Limpopo Province, approximately 80km southeast of Polokwane, the provincial capital, and 330km northeast of Johannesburg.

The Bokoni Mine is permitted by two “new order” mining licenses covering an area of 20,394.26 hectares. After the conclusion of Phase Two of the Restructure Plan in December 2013, the Bokoni mining right (LP30/5/1/2/2/59 MR) was amended to include two mineral properties - Avoca 472 KS and Klipfontein 465 KS, which were previously considered part of Ga-Phasha. Mining at the Bokoni Mine consists of both surface and underground operations. The surface operation is an opencast operation mining the Merensky reef and contributes approximately 20% of the total tonnage produced. A vertical shaft and three decline shaft systems provide access to underground mine development and production on the Merensky and UG2 reef horizons. The UG2 production currently accounts for approximately 25% of total production.

Road, water and power infrastructure, as well as two processing concentrators, have been installed at the Bokoni Mine, which are sufficient to meet the operational requirements of the Bokoni Mine up to the completion of its first phase growth plans (i.e. increased output to 160.0 ktpm).

The Bokoni Mine has an extensive ore body, capable of supporting a life-of-mine plan that is estimated at 23 years (as Bokoni’s mining licence is expiring in 2038). Current mining operations are being conducted at shallow depths, on average 300m below the surface. This benefits the Bokoni Mine’s operations as there are no major refrigeration (and consequent power) requirements at shallower mining depths.

The Bokoni Mine’s production for Q3 2014 averaged 159,793 tpm of ore from its UG2 and Merensky reef horizons (including the opencast), representing an increase of 10% from Q3 2013.

Klipfontein opencast project:

In Q2 2013, Bokoni successfully commissioned its opencast Merensky mine operations which at steady state, is expected to produce up to 40.0 ktpm of Merensky ore. The ore mined at the open cast surface operations is used to the fill any mill gap (25.0 ktpm to 40.0 ktpm) created as a result of the difference between underground production (120.0 ktpm to 135.0 ktpm) and the concentrator capacity (160.0 ktpm). As the underground operations ramp up to a steady state production of 160.0 ktpm, the tonnages from the opencast operations will decrease accordingly. The expected life of the opencast operation is approximately 4 years.

On October 8, 2014, Bokoni suspended operations at its Klipfontein opencast mine pending the outcome of an urgent and full investigation into the fatal injury of a Mosotsi community member. This could have an impact on the production for the three months up to December 31, 2014. The Bokoni Mine resumed operations on the western side of the Klipfontein opencast on November 3, 2014. The eastern side of the opencast remains suspended pending finalisation of the investigation by the DMR and the South African Police Services (“SAPS”).

| Atlatsa Resources Corporation |

| |

| Management Discussion and Analysis of Financial Condition and Results of Operations for three and nine months ended September 30, 2014 |

Operating Plan

The operating plan to 2020 targets an output of 160.0 ktpm from underground operations, to meet the current installed processing capacity at the Bokoni Mine. The Brakfontein Shaft and Middelpunt Hill shafts are expected to ramp up to steady state levels of production of 100.0 ktpm and 60.0 ktpm respectively by 2018. The older UM2 and Vertical underground shafts are expected to continue to produce at a steady state rate of 10.0 ktpm and 35.0 ktpm until 2017 and 2018 respectively. The mill gap between the processing capacity (160.0 ktpm) and the underground production (currently 130.0 ktpm) will be filled by the opencast operation that will be managed on a flexible volume basis to produce sufficient ore. Material capital expenditure associated with the proposed UG2 and Merensky expansion plans at the Bokoni Mine, as well as a new UG2 Concentrator plant (100.0 ktpm), estimated at $197.2 million (ZAR2.0 billion), have been deferred beyond 2020.

The operating plan will allow the Bokoni Mine to fill its processing capacity in the near term, whilst allowing underground mining operations to build up from the current level of 130,000 tpm to 160,000 tpm. The Company considers this plan to be both lower risk and less capital intensive. Annual production from the Bokoni Mine is expected to increase from the current base of 200,000 PGM Oz to 250,000 PGM Oz over the next five years.

The operating plan will result in Bokoni becoming a predominantly Merensky Reef producer, with Merensky Reef accounting for approximately 75% of its total estimated production in the medium term. The capital cost estimate to increase production from the Brakfontein and Middlepunt Hill projects to steady state levels of 100.0 ktpm and 60.0 ktpm, respectively, is estimated at $188.3 million (ZAR1.9 billion).

Atlatsa will finance its obligations in respect of the expansion plans at the Bokoni Mine until December 31, 2015, using the Advance on Concentrate Revenue Agreement and available cash resources and by deferring capital expansion costs that do not affect the Bokoni operating plan. If required, Atlatsa can also drawdown under the Working Capital Facility. RPM, as a 49% shareholder of Bokoni Holdco, will meet its 49% shareholder commitment to match any cash resources that Atlatsa contributes.

Management of the Bokoni Operations

On March 27, 2013, Plateau, RPM and Bokoni Holdco entered into a shareholders’ agreement (the “Bokoni Holdco Shareholders Agreement”) to govern the relationship between Plateau and RPM, as shareholders of Bokoni Holdco, and to provide management to Bokoni Holdco and its subsidiaries, including Bokoni.

Under the Bokoni Holdco Shareholders Agreement, Plateau is entitled to nominate the majority of the directors of Bokoni Holdco and Bokoni, and has undertaken that the majority of such nominees will be HDPs in South Africa. Atlatsa has given certain undertakings to RPM in relation to the maintenance of its status as an HDP controlled group pursuant to the Bokoni Holdco Shareholders Agreement.

Pursuant to the Bokoni Holdco Shareholders Agreement, the board of directors of Bokoni Holdco, which is controlled by Atlatsa, has the right to call for shareholder contributions, either by way of a shareholder loan or equity cash call. If a shareholder should default on an equity cash call, the other shareholder may increase its equity interest in Bokoni Holdco by funding the entire cash call, provided that Plateau's shareholding in Bokoni Holdco cannot be diluted for default in respect of equity contributions until the earlier of (a) the date on which the BEE credits attributable to RPM, and/or arising as a result of the acquisition by Atlatsa of its 51% interest in Bokoni Holdco, become legally

| Atlatsa Resources Corporation |

| |

| Management Discussion and Analysis of Financial Condition and Results of Operations for three and nine months ended September 30, 2014 |

secure, and (b) the date on which Plateau has repaid the debt owed to RPM pursuant to the New Senior Facilities Agreement in full.

Pursuant to the terms of shared services agreements between RPM and Bokoni, RPM provides certain services to Bokoni at a cost that is no greater than the costs charged to any other Anglo American plc group company for the same or similar services. It is anticipated that, as Atlatsa builds its internal capacity and transforms into a fully operational PGM producer, these services will be phased out and will be replaced either with internal or third party services. Atlatsa, through Plateau, provides certain management services to Bokoni pursuant to certain services agreements entered into with effect from July 1, 2009, which remain in effect.

Sale of Concentrate