Paul Hastings LLP

101 California Street, Forty-Eighth Floor

San Francisco, CA 94111

telephone (415) 856-7000

facsimile (415) 856-7100

www.paulhastings.com

July 21, 2021

VIA EDGAR CORRESPONDENCE

Securities and Exchange Commission

100 F Street, NE

Washington, DC 20549

| Re: | Metropolitan West Funds - File Nos. 333-18737 and 811-07989 |

Ladies and Gentlemen:

On behalf of the Metropolitan West Funds (the “Registrant”), we hereby respond to the oral comments provided on June 23, 2021 by Ms. Alison T. White of the staff (the “Staff”) of the Securities and Exchange Commission (the “Commission”) with respect to the Registrant’s Post-Effective Amendment No. 75 to its Registration Statement filed on May 13, 2021 (the “Registration Statement”), which contained disclosure with respect to two new series of the Registrant, the Metropolitan West ESG Securitized Fund (the “ESG Securitized Fund”) and the Metropolitan West Opportunistic High Income Credit Fund (the “Opportunistic High Income Credit Fund”).

The Registrant’s responses to those comments are provided below. We have restated the substance of those comments to the best of our understanding. Capitalized terms have the same respective meanings as in the Registration Statement, unless otherwise indicated. Revised disclosure intended to address these comments will be included in the Registrant’s annual update to its registration statement (the “Annual Update”), which is expected to be filed on or about July 26, 2021. Per the request of Ms. White, the Registrant will provide completed disclosure for review prior to the effective date of the Annual Update.

COVER PAGE

| 1. | Comment: Please update the Funds’ EDGAR series/Class IDs with their ticker symbols. |

Response: Comment accepted. The Registrant has included that information in the Annual Update.

TABLE OF CONTENTS

| 2. | Comment: Please include Environmental Social and Governance Investing Risk in the Table of Contents. |

Response: Comment accepted. The Registrant has included that risk in the table of contents of the Annual Update.

FEE TABLES

Securities and Exchange Commission

July 21, 2021

Page 2

| 3. | Comment: Please conform the second sentence of each Fund’s fee table preamble to the exact wording of Form N-1A, i.e., “You may pay other fees, such as brokerage commissions and other fees to financial intermediaries, which are not reflected in the tables and examples below.” |

Response: Comment accepted. The Registrant has revised that disclosure accordingly.

| 4. | Comment: In the preamble to each Fund’s fee table, please change “buy and hold” to “buy, hold and sell” as required by Item 3 of Form N-1A. |

Response: Comment accepted. The Registrant has revised that disclosure accordingly.

| 5. | Comment: Please advise supplementally how the Registrant estimated each Fund’s Other Expenses and determined such amounts were reasonable. |

Response: Other Expenses are estimated based on the experience of the Adviser and the Administrator with other start-up funds, primarily those relatively new funds that are series of the Registrant.

| 6. | Comment: Footnote 3 to each Fund’s fee table that states the Adviser may recoup fees within three years but does not say when that three-year period commences; please clarify. |

Response: Comment accepted. The Registrant has supplemented that disclosure to state as follows: “The Adviser may recoup reduced fees and expenses only within three years of the waiver or reimbursement, provided that the recoupment does not cause the Fund’s annual expense ratio to exceed the lesser of (i) the expense limitation applicable at the time of that fee waiver and/or expense reimbursement or (ii) the expense limitation in effect at the time of recoupment.

PRINCIPAL INVESTMENT STRATEGIES

| 7. | Comment: Please advise the Staff how the Funds will value derivatives for purposes of their 80% policies. |

Response: Derivatives will count toward each Fund’s 80% level, and will be valued for that purpose using their market value rather than their notional value.

| 8. | Comment: Please replace “include, without limitation” with “are” in the statement that “[i]nstruments considered to be economically tied to emerging market countries include, without limitation, those that are principally traded in an emerging market country…” and revise the disclosure as appropriate. |

Response: Comment accepted. The Registrant has revised that disclosure as follows:

“Instruments considered to be economically tied to emerging market countriesinclude, without limitation, are (i) those that are principally traded in an emerging

Securities and Exchange Commission

July 21, 2021

Page 3

market country, or (ii) those that are issued by: (ia) an issuer organized under the laws of or maintaining a principal place of business in an emerging market country, (iib) an issuer that derives or is expected to derive 50% or more of its total revenues, earnings or profits from business activity in an emerging market country, or that maintains or is expected to maintain 50% or more of its employees, assets, investments or operations in an emerging market country, or (iiic) a governmental or quasi-governmental entity of an emerging market country.”

| 9. | Comment: Please revise the derivatives disclosure throughout the filing to discuss only those derivatives that the Funds will actually use as part of their principal investment strategies, the specific purposes for which those derivatives will be used and the risk factors associated with the use of those derivatives. For additional guidance, see the letter from Barry Miller to the ICI dated July 30, 2010 and revise the disclosure as appropriate. See also IM Guidance Update (No. 2013-05). |

Response: Comment accepted. The Registrant has revised that disclosure for the ESG Securitized Fund as follows:

“Derivatives, such as options, futures and swaps, are used in an effort to hedge investments, for risk management, or to increase income or gains for the Fund. The types of derivatives in which the Fundmay will principally investmay include, but are not limited toare options, futures and swap agreements, as well as: (i) securitization structures securitized instruments that isolate specific cash flows, such as Principal only (PO) bonds or Interest only (IO) bonds; (ii) tiered index bonds that reference a series of cash securitizations (such as CMBX, a non-agency securitized index where the underlying assets are commercial mortgage-backed securities), and (iii) TBAs (to-be-announced securities), which are traded as agency mortgage-backed securities prior to the underlying mortgage loans being allocated to the pool (giving them a derivative nature).”

Please see the response to Comment 11(e) below for revisions that describe the nature of the derivative instruments referenced in (i), (ii) and (iii) above.

The Registrant has revised the related disclosure for the Opportunistic High Income Credit Fund as follows:

“Derivatives are used in an effort to hedge investments, for risk management, or to increase income or gains for the Fund. TheFund may invest in types of derivative instruments in which the Fund will principally invest are, primarily currency and other futures, forward contracts, options, and swap agreements (typically interest rate swaps, index-linked swaps, total return swaps and credit default swaps) and swap agreements.”

Securities and Exchange Commission

July 21, 2021

Page 4

| 10. | Comment: Please replace “may include, but are not limited to” with “are” in the statement that “[t]he derivatives in which the Fund may invest may include, but are not limited to….” Revise the disclosure to list all the derivatives the Fund may use as part of its principal investment strategies, as also noted in Comment 10. |

Response: Comment accepted. Please see the Registrant’s response to Comment 10 above.

| 11. | With respect to the ESG Securitized Fund: |

| a. | Comment: Please explain why the Registrant believes that satisfying “one or more” positive-screening criteria to support sustainable initiatives is sufficient to justify characterizing the Fund as an ESG fund. |

Response: Comment acknowledged. The Adviser evaluates the Fund’s potential investments based on both fundamental and sustainability factors. The Adviser implements a positive ESG screening approach to securitized investing, which includes using a positive screening matrix to review each purchase by the Fund for social, environmental and/or sustainability factors and ensuring a minimum of 80% of net assets are positively screened and meet positive-screen criteria as defined in the Adviser’s policies and procedures. Therefore, at least 80% of the Fund’s net assets will be invested in issuers meeting the Adviser’s ESG screening process as described in the prospectus.

| b. | Comment: Please disclose more information about the nature of the securitized vehicles in which the Fund will invest and the degree to which those vehicles will focus on sustainable initiatives, including the types of initiatives. If the deal terms, investment analysis/thesis, or investment liquidity of these vehicles differ materially from other forms of asset backed securities the Adviser would typically consider, that should be addressed in revised disclosure as well. |

Response: Comment accepted. The Registrant has supplemented the Fund’s Item 4 disclosure with the following:

“The types of ESG securitized vehicles in which the Fund invests typically include, but are not limited to: (i) agency mortgage-backed securities and private label residential mortgage-backed securities that are collateralized by mortgage loans originated to support energy-efficient home improvements or with a financial inclusion component, focusing on promoting affordability and/or lending to low-to-moderate income individuals and communities; (ii) commercial mortgage-backed securities collateralized by certified energy efficient commercial properties (usually LEED-certified but also including alternative green building certifications such as BREEAM, NABERS, and Energy Star), or by loans focused on promoting affordable rental housing, typically through a landlord commitment and/or requirement to sustain below-market rents in existing or new construction multifamily properties; and (iii) asset-backed securities with an energy efficiency component, such as lower-carbon transportation and green asset transportation. Other securities considered for positive ESG screening include ESG collateralized loan obligations that often also include investment restrictions in certain sectors such as production and/or sale of

Securities and Exchange Commission

July 21, 2021

Page 5

weapons or tobacco-related products. The investment analysis and liquidity of these securitized vehicles do not differ materially from other forms of asset-backed securities the Adviser would typically consider for its other registered funds, except for the addition of the positive ESG screening process.”

| c. | Comment: With respect to the statement that “[i]n implementing its positive-screening ESG strategy, the Adviser evaluates potential investments based on a number of factors”, what information and analysis does the Adviser use to evaluate these factors? Please disclose. |

Response: Comment accepted. The Registrant has supplemented that disclosure as follows:

“In conducting its positive ESG screening process, the Adviser reviews for environmental, social and/or sustainable features related to the underlying security collateral and issuer programs, evidenced by marketing materials, borrower underwriting criteria, loan tapes (electronic files that capture lending product data from a financial firm’s internal systems), additional issuer disclosures and clarification from engagement, as well as third-party reports such as rating agency presales and second-party opinions where applicable. Typically, there is significant disclosure around issuer lending programs that offers insight into the environmental, social and/or sustainable nature of a securitization, such as supporting energy-efficient property improvements (environmental positive) and/or supporting affordable rental housing access and availability (social positive). The Adviser will also engage with issuers to obtain additional materials, clarification, and/or data points to support the viability of their lending and securitization programs and/or confirm their compliance with industry standards such as the International Capital Market Association (ICMA) Green, Social and/or Sustainable bond principles. The Adviser will continue to monitor the market for additional information sources as well as issuer best-practices to enhance its diligence and positive screening approach.”

| d. | Comment: Please describe the Adviser’s due diligence practices in applying its ESG screening criteria to potential investments. This includes what underlying data the Adviser will review to determine whether an investment meets its ESG criteria, and the sources of that data. For example: directly engaging with portfolio companies to better understand their ESG risks and practices; reviewing third-party scoring/data; and/or conducting research using other types of information from either the Fund or an outside source. |

Response: Comment accepted. Please see the Registrant’s response to Comment 11(c) above.

| e. | Comment: Please disclose in the filing in plain English what PO bonds, IO bonds, tiered index bonds and TBAs are. Please also define the acronym TBA. Lastly, it is unclear why you mention these instruments here, but nowhere else in the prospectus or SAI. Please advise or revise. |

Securities and Exchange Commission

July 21, 2021

Page 6

Response: Comment accepted. The Registrant has added descriptions of these securities to the Item 9 disclosure under “Additional Fund Information – Principal Investment Strategies – ESG Securitized Fund,” as follows:

“The types of derivatives in which the Fund will principally invest are options, futures and swap agreements, as well as: (i) securitized instruments that isolate specific cash flows, such as Principal only (PO) bonds or Interest only (IO) bonds; (ii) tiered index bonds that reference a series of cash securitizations (such as CMBX, a non-agency securitized index where the underlying assets are commercial mortgage-backed securities), and (iii) TBAs (to-be-announced securities). PO and IO bonds are debt obligations that strip the principal cash flows from the interest cash flows of mortgage collateral, such that the principal cash flows form one bond, the PO, and the interest cash flows form a separate bond, the IO. Tiered index bonds are derivative instruments for which the interest rate is tied to a specified index or market rate. So long as this index or market rate is below a predetermined “strike” rate, the interest rate on the tiered index bond remains fixed; if, however, the specified index or market rate rises above the “strike” rate, the interest rate on the tiered index bond will decrease. TBAs are to-be-announced mortgage pass-through securities, which settle on a delayed delivery basis, thus giving them a derivative nature. Please see “Securities and Techniques Used by the Funds” in the Statement of Additional Information for additional information regarding those investment types.”

In addition, the Registrant has revised the disclosure in the SAI under the section called “Securities and Techniques Used by the Funds,” which describes the various investment types and related risks, as follows:

Under “Asset-Backed Securities” on page 10 of the Registration Statement’s SAI:

“The Funds may invest in securities issued by trusts and special purpose corporations with principal and interest payouts backed by, or supported by, any of various types of assets. These assets typically include receivables related to the purchase of automobiles, credit card loans, and home equity loans. These securities generally take the form of a structured type of security, including pass-through, pay-through, and stripped interest payout structures, such as Principal only (PO) and Interest only (IO) bonds, similar to the CMO structure. Investments in these and other types of asset-backed securities must be consistent with the investment objectives and policies of the Funds.”

Under “Mortgage-Related Securities” on page 30 of the Registration Statement’s SAI:

“The Funds may invest in residential or commercial mortgage-related securities, including mortgage pass-through securities, including TBAs (to-be-announced), collateralized mortgage obligations (“CMOs”), adjustable rate mortgage securities, CMO residuals, stripped mortgage-related securities, such as Principal

Securities and Exchange Commission

July 21, 2021

Page 7

only (PO) bonds and Interest only (IO) bonds, floating and inverse floating rate securities and tiered index bonds”

Under “Mortgage-Related Securities – Mortgage Pass-Through Securities” on page 30 of the Registration Statement’s SAI:

“Mortgage pass-through securities represent interests in pools of mortgages in which payments of both principal and interest on the securities are generally made monthly, in effect “passing through” monthly payments made by borrowers on the residential or commercial mortgage loans which underlie the securities (net of any fees paid to the issuer or guarantor of the securities). Mortgage pass-through securities differ from other forms of debt securities, which normally provide for periodic payment of interest in fixed amounts with principal payments at maturity or specified call dates. TBAs, or to-be-announced, are a type of mortgage pass-through security that settle on a delayed delivery basis, thus giving them a derivative nature.”

The Registrant notes that tiered index bonds and their associated risks are described on page 32 of the Registration Statement’s SAI.

| 12. | With respect to the Opportunistic High Income Credit Fund: |

| a. | Comment: It appears that the Fund may invest significantly in below investment grade asset-backed and mortgage-related securities and defaulted and distressed securities. Given the liquidity profile of these investments, please explain how the Fund determined that its investment strategy was appropriate for the open-end structure. Your response should include general market data on the types of investments and information concerning the relevant factors referenced in the release adopting rule 22e-4 under the 1940 Act. See Investment Company Liquidity Risk Management Programs, Investment Company Act Release No. 32315 (Oct. 13, 2016) at pp. 154-155. |

Response: Comment accepted. With respect to distressed and defaulted securities, the Registrant has revised the disclosure as follows:

“The Fund pursues its objective by utilizing a flexible investment approach that, under normal circumstances, invests at least 80% of its net assets in investments across a range of global investment opportunities related to income-generating credit securities, including distressed and defaulted securities that may not be current with their interest, distribution, or dividend payments, with an emphasis on higher volatility, lower-quality debt securities rated below investment grade (commonly known as “junk bonds”) by Moody’s Investors Services, Inc. (“Moody’s”), S&P Global rating (“S&P”) and Fitch Ratings, Inc. (“Fitch”), or unrated securities determined by the Adviser to be of comparable quality. The use of the term “opportunistic” in the Fund’s name means that it is not limited to any single type of investment strategy, sector or income-producing security. Income-generating credit securities may include defaulted securities that are not current with their interest,

Securities and Exchange Commission

July 21, 2021

Page 8

distribution, or dividend payments, but defaulted securities are not expected to constitute more than 15% of the Fund’s portfolio.”

Please see the Appendix for the Registrant’s detailed response with respect to below investment grade ABS and MBS.

| b. | Comment: Regarding the Fund’s disclosure about selling securities short, please confirm supplementally to the Staff that expenses associated with short sales (e.g., dividends paid on stocks sold short) will be reflected in the fee table if appropriate. Also, should Short Sales Risk be included as a principal risk of investing in the Fund? Please advise or revise. |

Response: Comment accepted. The Registrant confirms that expenses associated with short sales will be reflected in the fee table where appropriate. The Registrant has revised the Principal Risks section for the Fund to include Short Sales Risk.

PRINCIPAL RISKS

| 13. | Comment: For each Fund, please add principal investment strategy disclosure corresponding to Frequent Trading Risk. |

Response: Comment accepted. The Registrant has revised the Item 4 disclosure under “Principal Investment Strategies” for each Fund to include the following statement: “The Fund may engage in active and frequent trading of portfolio securities to achieve its primary investment strategies.”

| 14. | Comment: With respect to the ESG Securitized Fund, the disclosure on page 17 of the Registration Statement states that “[u]nder normal circumstances, the Fund invests at least 80% of its net assets in investment grade securities.” Is this statement accurate? If so, please also include this statement in the Item 4 principal investment strategies section and reconcile with the disclosure that the Fund may allocate up to 25% of assets in junk bonds |

Response: Comment accepted. The Registrant has revised the Item 4 and Item 9 disclosure for the ESG Securitized Fund to state that the Fund will invest at least 80% of its net assets in investment grade securities and may invest up to 20% of its assets in junk bonds.

| 15. | Comment: Similarly, at the top of page 18 should “20%” be replaced with “25%” in the statement that “[u]p to 20% of the Fund’s net assets may be invested in securities rated below investment grade or unrated securities determined by the Adviser to be of comparable quality”? Please advise or revise. |

Response: Comment accepted. The Registrant confirms that the Fund will invest up to 20% of its net assets in those securities.

Securities and Exchange Commission

July 21, 2021

Page 9

| 16. | Comment: It is unclear why you state on page 18 that the ESG Securitized Fund “may normally short sell up to 33 1/3% of the value of its total assets,” but not in the Item 4 strategy and risk disclosure. Please reconcile. |

Response: Comment accepted. The Registrant has revised the Item 4 strategy and risk disclosure to include the Fund’s ability to sell short up to 33 1/3% of the value of its total assets.

| 17. | Comment: It is unclear why the Opportunistic High Income Credit Fund would invest 100% of assets in investment grade securities under normal circumstances (page 18). Please advise. Also, please: (1) explain why the Fund has two 80% policies and how they are consistent and not mutually exclusive; and (2) address the factors the Adviser considers when deciding to emphasize investment grade securities versus non-investment grade securities from a portfolio construction perspective. |

Response: Comment accepted. The Registrant has revised the Item 9 disclosure to correspond to the Item 4 disclosure that the Fund may invest up to 100% of its net assets in securities rated below investment grade. According to the Fund’s 80% investment policy, the Fund will invest 80% of its net assets in investments across a range of investment opportunities related to income-generating credit securities, “with an emphasis on higher volatility, lower-quality debt securities rated below investment grade….” The Fund anticipates that all of the securities meeting its 80% test may be rated below investment grade, and that the remaining 20% of the Fund’s net assets may also be invested in securities rated below investment grade.

When evaluating potential investments, the Adviser considers the investment’s prospective total return profile on an absolute and risk-adjusted basis (i.e., in relation to the investment’s risk factors, principally fundamental risk factors). In certain instances, the Adviser may identify and choose to emphasize investments in investment grade securities with enhanced total return properties, through either higher income or greater price appreciation potential, compared to non-investment grade securities. In making this determination, the Adviser considers factors including, but not limited to:

| i. | the price or credit spread at which the security trades, and how that price compares to valuations in the market in which the security trades (as well as relative to the Adviser’s determination of intrinsic value); |

| ii. | security-level metrics such as duration and convexity; |

| iii. | the fundamental characteristics of the borrower, as well as prospective improvements to those fundamental characteristics over time; and |

| iv. | event catalysts, including ratings improvement and acquisition transactions. |

Securities and Exchange Commission

July 21, 2021

Page 10

PRINCIPAL RISK CHART

| 18. | Comment: Please include Environmental Social and Governance Investing Risk in the chart on page 20 of the Registration Statement. |

Response: Comment accepted. The Registrant has included that risk in the principal risk chart in the Annual Update.

| 19. | Comment: Please see the prior comment about Short Sales and the ESG Securitized Fund; if investing in short sales will be a principal strategy of the fund, please include a statement to that effect in the Item 4 disclosure. |

Response: Comment accepted. The Registrant has updated the Item 4 disclosure accordingly.

| 20. | Comment: With respect to Bank Loan Risk on page 22 of the Registration Statement, please disclose, if accurate, that by “extended trade settlement periods” the Registrant means longer than 7 days. |

Response: Comment accepted. The Registrant has revised that disclosure accordingly.

| 21. | Comment: It is unclear why you mention the Flexible Income Fund in two places on page 22. Please advise or revise. |

Response: Comment accepted. The disclosure under “Below Investment Grade Mortgage-Backed Securities Risk” has been revised in the Annual Update to refer to both the Flexible Income Fund and the Opportunistic High Income Credit Fund.

| 22. | Comment: Please consider whether LIBOR Risk should be included in the Item 4 and/or Item 9 disclosure for the Opportunistic High Income Credit Fund. |

Response: Comment accepted. The Registrant has added LIBOR Risk to the Item 4 and Item 9 disclosure in the Annual Update for each series of the Trust.

* * * * *

Please contact the undersigned at (415) 856-7007 with comments and questions.

Very truly yours,

/s/ David A. Hearth

David A. Hearth

for PAUL HASTINGS LLP

Securities and Exchange Commission

July 21, 2021

Page 11

cc: Metropolitan West Asset Management, LLC

Securities and Exchange Commission

July 21, 2021

Page 12

APPENDIX

Opportunistic High Income Credit Fund’s Investments in Below Investment Grade Asset-Backed and Mortgage-Related Securities

| I. | Liquidity determination process and procedure |

In general, the Fund’s policies classify certain specified types of securities (such as U.S. Treasuries) as presumptively liquid and certain other specified types of securities (such as non-agency MBS derivatives) as presumptively illiquid. For all securities other than those specifically designated as liquid or illiquid, a separate liquidity determination at the individual CUSIP level is required. Certain types of RMBS, CMBS and ABS that are below investment grade are classified as presumptively illiquid, but no below investment grade RMBS, CMBS or ABS bonds (hereinafter Below IG Securitized) would be classified as presumptively liquid. Accordingly, a CUSIP-level liquidity determination is required to be made for most below investment grade RMBS, CMBS and ABS.

The liquidity determination process works as follows: at the time of initial purchase of a security not already held by any of the funds advised by the Adviser, the new CUSIP is entered into the system by a trader. The Adviser’s data management group then determines whether the security is of a type that is presumptively liquid or illiquid, with input from the investment team, compliance, and/or legal if needed. If the security requires a liquidity determination, the data management group populates a liquidity determination form with data sourced from industry leading vendors, and then sends the form to the trader. The trader makes a liquidity determination based on the applicable factors listed below. A portfolio manager or specialist from the appropriate trading desk – in this case, the non-agency RMBS, CMBS or ABS desk – reviews and approves the determination. The completed, approved form is returned to the data management group for entry.

| a. | Factors for consideration |

A security may be classified as liquid only if the trading desk reasonably determines that it can generally be disposed of within seven (7) days for approximately the same value as it is held in the Fund. To make that determination, the desk may consider the following list of factors. This list is not all-inclusive, and not all factors are applicable to all types of securities.

| • | Size of position |

| • | Spread between bid and ask |

| • | Frequency of trades or quotes; ease or difficulty of obtaining a second quote |

| • | Number of dealers willing to purchase or sell the security (less than two/two or more) or willing to make a market |

Securities and Exchange Commission

July 21, 2021

Page 13

| • | Nature of the security and the marketplace in which it trades |

| • | Rating of the security or rating changes |

| • | De-listing of the security |

| • | Occurrence of corporate events such as bankruptcy or reorganization |

| • | Whether the security trades electronically and/or is centrally cleared |

| • | Whether the security is trading at or close to par |

| • | Whether the security is in default or trading flat |

| • | Whether there are any contractual penalties for unwinding a transaction |

| • | Whether there are contractual restrictions on trading the security |

| • | Any other information, research or other factors that are reasonably deemed relevant by the desk |

| b. | Periodic and event-driven review |

The liquidity classifications are reviewed by the portfolio risk team monthly. On a quarterly basis, the portfolio managers provide focused liquidity reporting for review and oversight by the Fund’s Board of Trustees. These quarterly reports include, for each fund, liquidity classification methodology and assumptions, based on a 5-tier classification system, from 1 (most liquid) to 5 (least liquid), historical liquidity percentages, and stress test results assuming widely varying interest rate scenarios. The portfolio managers present these reports to the Board with their analysis and observations, and respond to questions.

The portfolio risk team generates daily reports that assist the portfolio managers in monitoring liquidity. In addition, classifications are reviewed by the Adviser’s internal pricing group (consisting of personnel from legal, compliance, mutual fund administration, and fixed income) if there is either a rating decline of six tiers (for example, BB+ to B- if rated by S&P), or a rating decline of three tiers (for example, BB+ to BB- if rated by S&P) in combination with a 10% price drop. The investment team or the risk team may review the liquidity classification of any security more frequently upon receipt of material information, such as a bankruptcy proceeding involving the issuer.

| c. | Compliance with Rule 22e-4 |

TCW expects the Fund will follow the same testing and reporting procedures of the other public funds it manages subject to Rule 22e-4 under the 1940 Act and does not anticipate any special considerations or factors will come into play with regards to liquidity bucketing of the Fund’s holdings. The asset types in question are currently part of TCW’s testing efforts with external vendors and internal modeling teams for liquidity assessment. Looking at a representative subset of all Below IG Securitized securities that TCW manages, a great percentage of these securities meet the definition of highly liquid securities when tested at

Securities and Exchange Commission

July 21, 2021

Page 14

reasonable price concessions according to third-party models. Investment in this segment of the market will not put the Fund in danger of approaching the maximum illiquid concentration.

At the commencement of operations of the Fund, the Adviser would not have historical data for the Fund available to assist with establishing various liquidity and other parameters because the Fund would be new and the liquidity committee will need to establish those parameters based on an analysis of other factors. The Adviser expects the Fund to be in compliance with Rule 22e-4 when operations commence.

| II. | Liquidity/illiquidity of investment types |

The Fund classifies non-agency RMBS and CMBS interest-only (“IO”), non-agency RMBS and CMBS principal-only (“PO”) securities, and any other non-agency RMBS and CMBS derivatives as illiquid for the purposes of compliance with the 1940 Act. With the exception of these types of securities, which the Fund classifies as illiquid based on their historical performance and current analysis, the Fund determines liquidity at the CUSIP level, rather than the security type level, as described above.

If the trading desk determines that any Below IG Securitized bonds cannot be sold within seven (7) days for approximately the same value as it is held in the Fund or that security falls under the definition of illiquid noted above for non-agency RMBS and CMBS derivatives, that security will be deemed illiquid in the Fund. All other securities within these sectors can be determined to be liquid using the process described above if the available information supports such a determination. A determination that such a security is liquid can be well supported and reasonable based upon TCW’s experience managing and trading these types of securities in different market environments, TCW’s past and on-going research into broader market trading conditions, as well as its firsthand knowledge of the broad availability of independent and recognized third party daily pricing information. The Registrant expands on these points below.

| III. | Data on types and liquidity of investments. |

| a. | Limits imposed on position sizes for each investment type |

The Fund will impose a 25% limit on Below IG Securitized exposure. Given the portfolio management team’s experience managing and trading Below IG Securitized products, the Adviser is confident of the Fund’s ability to meet its redemption obligations, considering the observed liquidity of these investments, the Adviser’s risk management regarding CUSIP concentration, and the liquidity the Adviser would maintain with the remaining 75% of assets.

| b. | Measures for addressing potential large redemption requests |

Securities and Exchange Commission

July 21, 2021

Page 15

As previously mentioned, the portfolio management team has extensive experience and expertise in both analyzing and trading Below IG Securitized securities. In order to explain how the Adviser might handle a large redemption request in a fund with exposure of up to 25% in these assets, the Adviser believes it is useful to explain how it handled such a situation in the past as well as listing additional measures it can employ.

In December of 2009, the portfolio management team assumed management responsibilities for the TCW Total Return Bond Fund. At that time, the fund’s AUM was $12.02 billion and approximately 28% of the assets were below investment grade RMBS and CMBS. Within one week of assuming management, the fund received $3.9 billion of redemptions and over the first two weeks, the fund incurred $5.23 billion of redemptions or 44% of the AUM two weeks prior to that date. While the data available to the Adviser and its in-depth market knowledge support an assessment that today’s market liquidity in below investment grade securitized products is better than late 2009, the Adviser was still able to meet all the redemption requests for that fund in an orderly and timely fashion without resorting to additional measures such as borrowing or in-kind redemptions. The Adviser’s goal was simple, to treat both exiting and remaining shareholders in an equitable fashion by maintaining a similar portfolio asset allocation when comparing that fund’s pre and post redemption profile. This simply meant selling, to the best of the Adviser’s ability, a pro-rata allocation of the asset mix, compared with an alternative approach that would attempt to sell the most liquid assets first which could very well work to the detriment of all remaining shareholders. By the end of December 2009, the redemption activity in that fund had subsided. Notwithstanding that nearly one-half of the AUM of the fund had been liquidated in a mere three weeks, during the traditionally slow December holiday season, and in a market environment that had just recently undergone deep distress in the securitized sector, the Adviser had achieved its objective in that situation. The portfolio composition on December 31, 2009 looked much like it had on December 9, 2009 with a NAV movement that had closely tracked that of its peer group. This demonstrated a de minimis amount of transaction costs resulting from the sales of all assets including over $1.0 billion of below investment grade CMBS and RMBS. The fund’s sales of portfolio holdings were a simple combination of traditional multi-participant BWIC’s (bid wanted in competition) as well as some select block trades negotiated with a single counterparty. In the Adviser’s view, that approach struck the right balance of competitive bids along with the minimal market disruption that identifying a single buyer can achieve.

Should the Fund experience a similar situation the Adviser would approach it in the same way, starting with the fair and equitable treatment of both exiting and remaining shareholders. In addition to the strategy described above for the large redemption experienced in 2009, the Adviser could use other methods to meet the Fund’s redemption obligations. These methods include the use of Rule 17a-7 transfers (should the assets to be sold also be appropriate for other registered funds the Adviser manages as well as the purchasing funds having the need for them) and pre-existing bank liquidity lines for the Metropolitan West Funds complex. While the Adviser is aware of, and would use if necessary, these two liquidity solutions, the Fund would

Securities and Exchange Commission

July 21, 2021

Page 16

have set the 25% limit on Below IG Securitized securities based upon the Adviser’s comfort level of selling securities to raise the necessary cash proceeds.

| c. | Existence of active market for investment types |

TCW participates in a healthy and active Below IG Securitized market. It believes the trading information as it relates to broker-dealer participants is a good indication of both the breadth and depth of these markets. While TCW is one of the larger investors in these sectors, the firm still represents just a small fraction of the overall market, which TCW estimates to be over $670 billion. Since the beginning of 2016, TCW has conducted over 1,350 Below IG Securitized sale transactions with 43 different counterparties. No single broker made up more than 15% of sales by count or current face volume, and TCW has conducted more than 100 sales with 8 different counterparties each over this time period and more than 20 sales with 12 different counterparties.

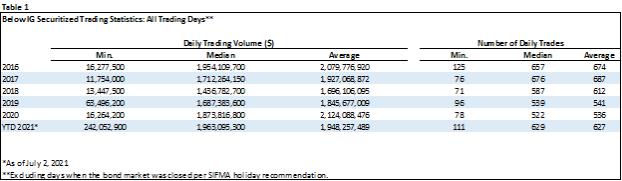

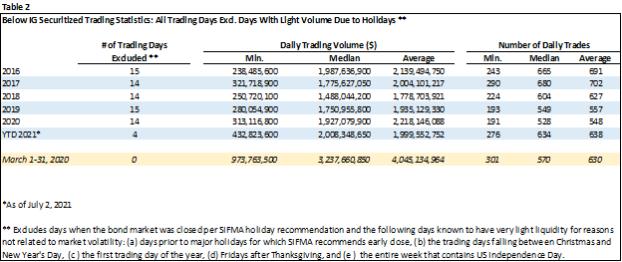

The broader market trading information TCW has researched also demonstrates an active market for these investment types. The first table below shows trading statistics for Below IG Securitized bonds for the most recent five calendar years as well as year to date through July 2, 2021. Table 2 refines the raw data in Table 1 by excluding days known to have very thin liquidity due to holidays/seasonality, as defined in the table footnote. Table 2 illustrates that since 2016 the median number of Below IG Securitized daily trades occurring within a calendar year has ranged between 528 and 680 trades per day, with 191 trades on the slowest trading day in the last five and a half years. That information can also be expressed in volume, with the median daily trade volume per calendar year ranging from $1.5 billion to $2.0 billion per day and the lowest volume of daily trading occurring in 2016 with still healthy $238 million of trading volume. The fact that Below IG Securitized trading volumes held up fairly well in a volatile month like March 2020, which saw secondary market liquidity dry up in many sectors of the fixed income market, further demonstrates the existence of active markets for Below IG Securitized.

Securities and Exchange Commission

July 21, 2021

Page 17

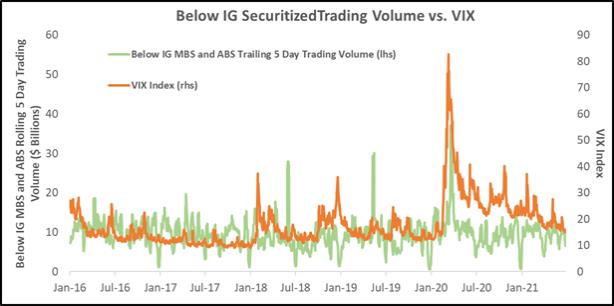

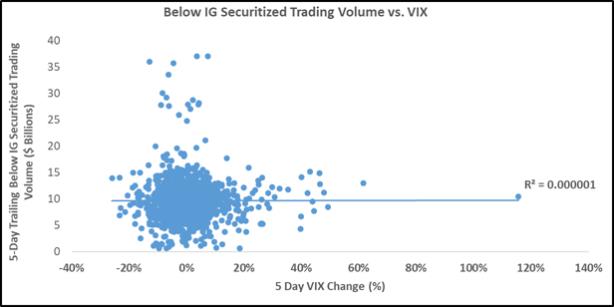

Below IG Securitized trading volume has also demonstrated a generally relatively low correlation to broader market volatility (see Charts 1 and 2 below). Consistent with findings in Table 2 above, Below IG Securitized trading volumes do exhibit positive correlation in March 2020, confirming the presence of active trading markets during market dislocation episodes. TCW’s direct trading experience is consistent with the broader market trading and volatility information detailed above and should provide adequate support for the proposed 25% limit.

Chart 1

Securities and Exchange Commission

July 21, 2021

Page 18

Source: FINRA, Nomura, Deutsche Bank, Bloomberg, TCW

Chart 2

Source: FINRA, Nomura, Deutsche Bank, Bloomberg, TCW

Securities and Exchange Commission

July 21, 2021

Page 19

| d. | Volatility of trade prices |

Below IG Securitized securities exhibit more trade price volatility than some other spread assets such as investment grade corporate bonds. However, on an absolute basis, the volatility is reasonable given the proposed percent limitation for the Fund and has continued to decline over time as the number of market participants grows and cash flow certainty (particularly with respect to below investment grade RMBS) improves. TCW examined all Below IG Securitized sales (regardless of “round lot” or “odd lot” size) TCW has made in the five-year period ending June 30, 2021 where the sold security was priced the prior day by a third-party pricing service. Of the 1,175 sales that met these criteria, only 9.2% were sold more than 3.0% below the prior day’s price and only 2.6% were sold more than 5.0% below the prior day’s price.

| e. | Bid/ask spreads |

The bid/ask spreads for these asset classes vary by CUSIP because of many different factors such as interest rate duration, spread duration, and credit enhancement just to name a few. Currently TCW estimates bid/ask spreads to range from 25 to 50 basis points for below IG RMBS and CMBS, and 50 to 100 basis points for below IG ABS bonds. Of course, some securities might fall outside of this range, but TCW’s view is that the large majority of the market would fall within it.

| f. | Restrictions on trading and transfer |

Any security that is subject to legal or contractual restrictions on trading or transfer will generally be subject to legal review at the CUSIP level. The Adviser will generally classify any security that is subject to such restrictions as illiquid, unless the Adviser’s legal and investment teams reasonably determine that, despite the restrictions, the security could be disposed of within seven days under then-current market conditions at approximately the same value at which it is held in the Fund.

| g. | Availability of information on underlying loans or other assets held by CLOs, CDOs, and non-agency RMBS and CMBS |

The availability of information on assets underlying securitized products is generally quite robust. Information about the collateral is provided at issuance via the prospectus/offering circular and detailed collateral data via a “loan tape” or “Annex A.” TCW has internal systems for loading this data directly from a loan tape or Annex A. Once a transaction closes, TCW loads collateral data via third party systems such as Intex, CoreLogic, and Bloomberg which aggregate

Securities and Exchange Commission

July 21, 2021

Page 20

and normalize loan data as well as provide monthly updates to the loan balance and collateral performance. TCW loads updated ratings from Moody’s, S&P, and Fitch daily. In addition TCW augments the information it receives for residential loans with borrower credit information from Equifax, and updated property values using data from CoreLogic. Additional commercial loan and property data is collected from rating agency presale and surveillance reports, aggregated market fundamentals and updated financials from CBRE, property publications and research from brokers such as JLL, Marcus & Millichap, and Cushman & Wakefield, and industry publications from Commercial Mortgage Alert (CMA), National Real Estate Investor, Preqin (Real Estate Spotlight), and websites such as TheRealDeal.com. Corporate loan data is updated with pricing, rating, and loan characteristics from Markit, borrower updates via LCD News, and pricing, published financials, and company data from Syndtraks, Intralinks, and Debtdomain. Finally, TCW’s credit research group also has access to Covenant Review, which enables TCW to look more closely at the loan terms of a deal.

| h. | Daily Valuation |

TCW prices fixed-income securities for which market quotations are readily available using independent pricing vendors. The funds managed by TCW and the Adviser receive pricing information from independent pricing vendors approved by the applicable Board of Trustees or Directors. The funds also use a benchmark pricing system to the extent vendors’ prices for their securities are either inaccurate (such as when the reported prices are different from recent known market transactions) or are not available from another pricing source. As of market close on June 30, 2021, TCW managed 1,045 Below IG Securitized CUSIPS with a total market value of over $5.4 billion across all TCW and MetWest mutual fund families and UCITS funds. 100% of these assets are priced by a leading independent pricing vendor (including ICE, JPM-Pricing Direct, and BVAL) as part of the daily NAV calculation.