www.ppbi.com

Investor Presentation

Investor Presentation

December 10, 2009

December 10, 2009

Steven R. Gardner

Steven R. Gardner

President & CEO

President & CEO

www.ppbi.com

The statements contained herein that are not historical facts are forward-looking

statements based on management's current expectations and beliefs concerning future

developments and their potential effects on the Company. There can be no assurance

that future developments affecting the Company will be the same as those anticipated

by management. Actual results may differ from those projected in the forward-

looking statements. These forward-looking statements involve risks and uncertainties.

These include, but are not limited to, the following risks: changes in the performance

of the financial markets; changes in the demand for and market acceptance of the

Company's products and services; changes in general economic conditions including

interest rates, presence of competitors with greater financial resources, and the impact

of competitive projects and pricing; the effect of the Company's policies; the

continued availability of adequate funding sources; and various legal, regulatory and

litigation risks; as well as additional risks factors discussed in the reports filed by the

Company with the SEC, which are available on its website at www.sec.gov. Except as

required by law, the Company undertakes no obligation to update any information.

statements based on management's current expectations and beliefs concerning future

developments and their potential effects on the Company. There can be no assurance

that future developments affecting the Company will be the same as those anticipated

by management. Actual results may differ from those projected in the forward-

looking statements. These forward-looking statements involve risks and uncertainties.

These include, but are not limited to, the following risks: changes in the performance

of the financial markets; changes in the demand for and market acceptance of the

Company's products and services; changes in general economic conditions including

interest rates, presence of competitors with greater financial resources, and the impact

of competitive projects and pricing; the effect of the Company's policies; the

continued availability of adequate funding sources; and various legal, regulatory and

litigation risks; as well as additional risks factors discussed in the reports filed by the

Company with the SEC, which are available on its website at www.sec.gov. Except as

required by law, the Company undertakes no obligation to update any information.

www.ppbi.com

• In 1983, Pacific Premier Bank (the “Bank”)

was founded and later expanded into

subprime lending

was founded and later expanded into

subprime lending

• By 1999, growing losses prompted the Bank

to refocus its strategy

to refocus its strategy

• In 2000, the current management team

took over and developed a three phase

strategic plan to transform the Bank from

a nationwide subprime lender into a

traditional Community Bank

took over and developed a three phase

strategic plan to transform the Bank from

a nationwide subprime lender into a

traditional Community Bank

Phase 1 - Recapitalize Pacific Premier

• Issued $12 million note and warrants

• Lowered the risk profile of the Bank

Phase 2 - Return to Profitability

• Grew the balance sheet

• Raised $27 million via secondary offering

• Retired $12 million note

• Sustained profitability

Phase 3 - Transition into Commercial Bank

• Recruit experienced bankers

• Expand market footprint

• Offer new products and services

• Diversify loan and deposit portfolios

www.ppbi.com

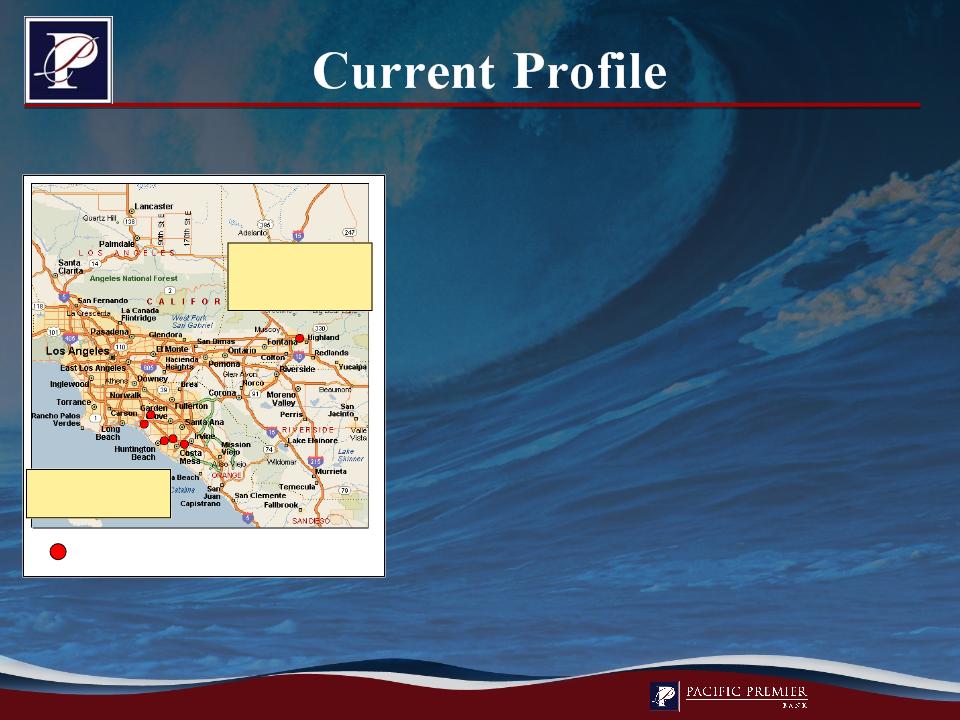

1 Branch in San

Bernardino

County

Bernardino

County

5 Branches in

Orange County

Orange County

Headquarters: | Costa Mesa, California |

Total Assets: | $847.9 million |

Net Loans: | $576.5 million |

Total Deposits: | $606.4 million |

Regional Focus: | Southern California |

Business Focus: | Small and middle market businesses |

Branches: | 6 locations |

As of September 30, 2009

PPBI Branch

www.ppbi.com

At or For the Nine Months Ended | At or For the Year Ended December 31, | |||

dollars in thousands, except per share data | September 30, 2009 | 2008 | 2007 | 2006 |

Balance Sheet | ||||

Total assets | $ 847,865 | $ 739,956 | $ 763,420 | $ 730,874 |

Total loans | 584,614 | 629,019 | 627,461 | 608,642 |

Total deposits | 606,382 | 457,128 | 386,735 | 339,449 |

Total borrowings | 176,810 | 220,210 | 308,275 | 326,801 |

Fully diluted book value per share* | $6.77 | $9.60 | $9.69 | $9.16 |

Statement of Operations | ||||

Net interest income | 17,019 | 21,118 | 18,266 | 17,125 |

Provision for loan losses | 5,535 | 2,241 | 1,651 | 531 |

Net income (loss) | (183) | 708 | 3,619 | 7,428 |

Bank Capital Ratios** | ||||

Tier 1 Leverage | 9.54% | 8.71% | 8.81% | 8.38% |

Tier 1 Risk Based | 12.98% | 10.71% | 10.68% | 10.94% |

Total Risk Based | 14.23% | 11.68% | 11.44% | 11.55% |

*Proforma, post capital raise at 9/30/09 ** Proforma, post capital raise at 9/30/09 assuming $13.5 million in additional capital to the Bank | ||||

www.ppbi.com

• Core deposit growth through small and middle market

business focus

business focus

• Relationship banking via high service levels

• Offensive capital raise - expansion opportunities

Develop the Bank into one of Southern California’s

top performing commercial banks.

top performing commercial banks.

www.ppbi.com

Texas ratio defined as NPAs / tangible equity plus loan loss reserves; Circle

radius represents 100 miles

radius represents 100 miles

SoCal Stressed Institutions

Possible failures as of September 30, 2009 within 100 miles of Costa Mesa, California | ||

Texas Ratio | # of Institutions | |

Near term | 100% + | 9 |

Longer term | 50% to 100% | 19 |

Possible near and longer term failures

Texas Ratio > 100%

Texas Ratio b/t 50-100%

www.ppbi.com

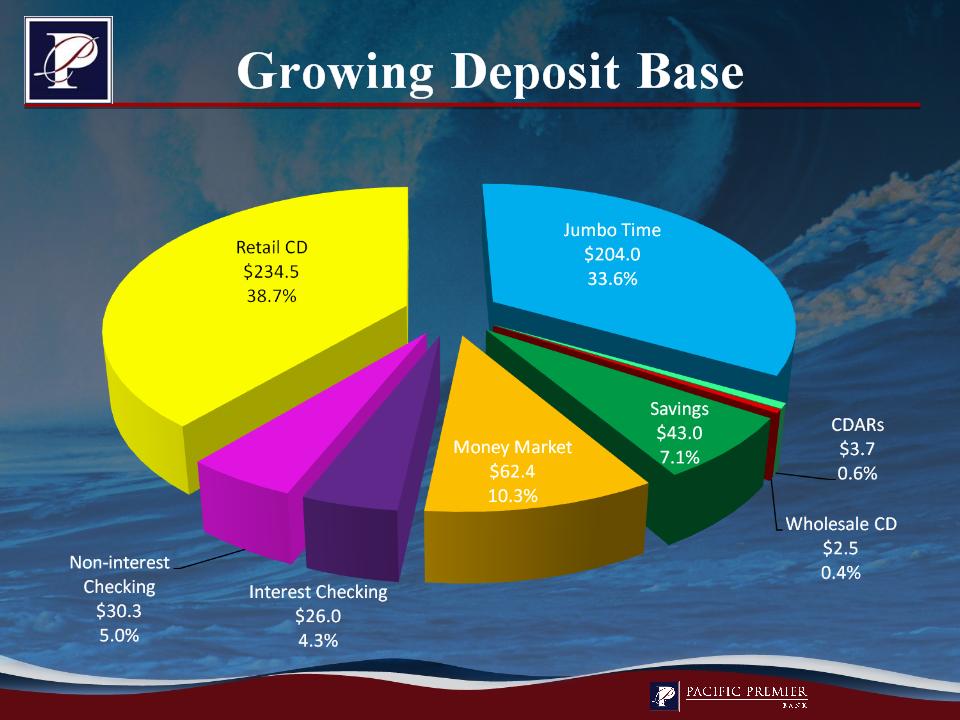

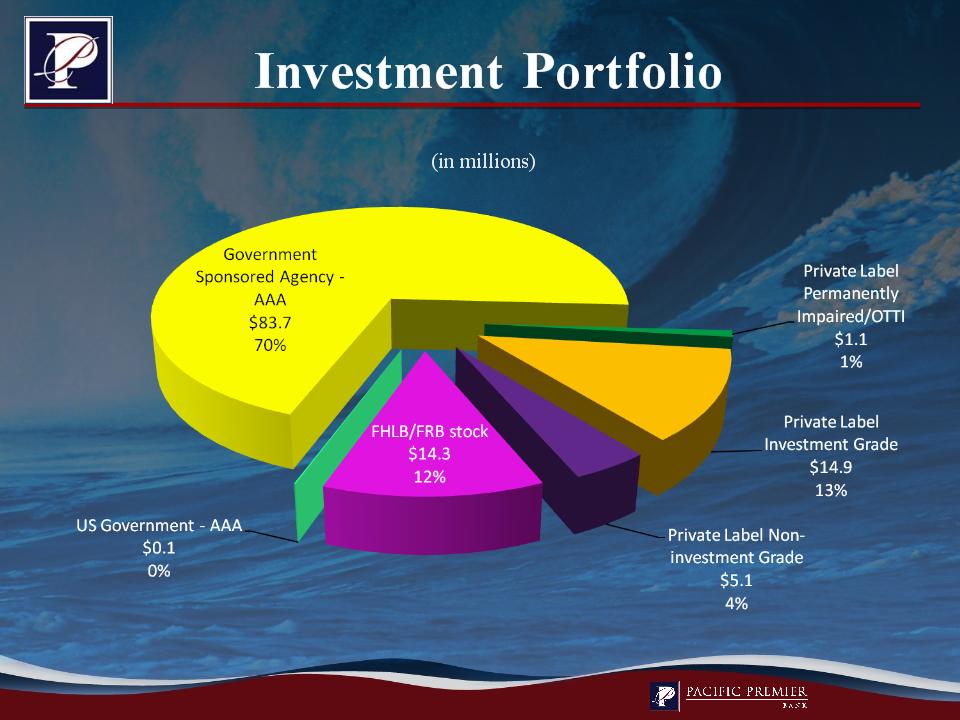

At September 30, 2009

(dollars in millions)

www.ppbi.com

As of September 30, 2009

www.ppbi.com

• Overall Underwriting Philosophy:

• CRE, C&I - business/property and global cash flow

• CRE Loans:

• Multifamily

• Commercial

• No construction, no L&D, no condo conversion, no int. reserves, no

repositioning, no covenant lite, no low doc

repositioning, no covenant lite, no low doc

• Personal guarantees, cross collateral, cross guarantees

• Portfolio Management

• Collections

www.ppbi.com

Average Loan Size | Seasoning (months) | LTV | DCR | |

Multifamily RE | $ 1,052,000 | 49 | 67% | 1.20 |

CRE Investor | $ 1,208,000 | 42 | 58% | 1.42 |

CRE Owner | $ 964,000 | 45 | 54% | ---- |

C & I | $ 356,000 | 25 | ---- | ---- |

SBA | $ 107,000 | 27 | ---- | ---- |

At September 30, 2009

www.ppbi.com

12/31/07 | 12/31/08 | 09/30/09 | |

Balance | $341.3 | $287.6 | $284.1 |

Avg. Bal | $1.087 | $1.053 | $1.052 |

DCR | 1.17 | 1.47 | 1.20 |

LTV | 65 | 65 | 67 |

Rate | 6.77% | 6.30% | 6.20% |

County | Bal | LTV | DCR | |

Los Angeles | $197.8 | 66% | 1.26 | |

Orange | $21.0 | 63% | 1.30 | |

Riv./San Bern. | $25.5 | 76% | 0.87 | |

San Diego | $23.6 | 68% | 1.26 | |

Other * | $16.2 | 64% | 1.17 | |

Total | $284.1 | 67% | 1.20 |

At September 30, 2009

www.ppbi.com

12/31/07 | 12/31/08 | 09/30/09 | |

Balance | $142.1 | $163.4 | $153.4 |

Avg. Bal | $1.184 | $1.202 | $1.208 |

DCR | 1.34 | 1.54 | 1.42 |

LTV | 62 | 57 | 58 |

Rate | 7.25% | 7.04% | 6.88% |

Type | Bal | LTV | DCR |

Office | $45.0 | 60% | 1.43 |

Retail | $46.6 | 55% | 1.41 |

Industrial | $25.8 | 63% | 1.33 |

Other | $35.7 | 57% | 1.52 |

Total | $153.4 | 58% | 1.42 |

At September 30, 2009

www.ppbi.com

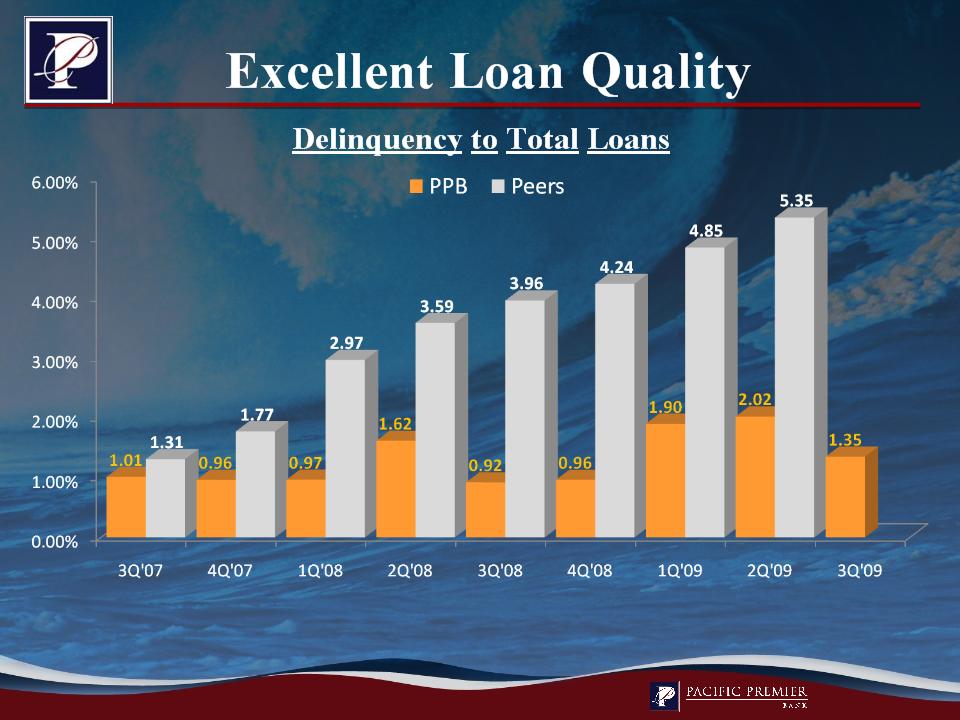

Peers consist of California commercial banks between $500 million and $1 billion, as of the end of the period covered.

Source: FDIC

www.ppbi.com

Peers consist of California commercial banks between $500 million and $1 billion, as of the end of the period covered.

Source: FDIC

www.ppbi.com

Book Value at September 30, 2009

In October, private label MBS totaled $9.0 million.

www.ppbi.com

• Bank transition gaining momentum

• Outperform peers due to: Credit Culture

• Target rich environment for acquisitions

• Undervalued stock relative to peers

www.ppbi.com

Questions?

Questions?