Investor Presentation

Third Quarter 2012 Update

Third Quarter 2012 Update

Steve Gardner

President & CEO

1

Forward-Looking Statements and

Where to Find Additional Information

Where to Find Additional Information

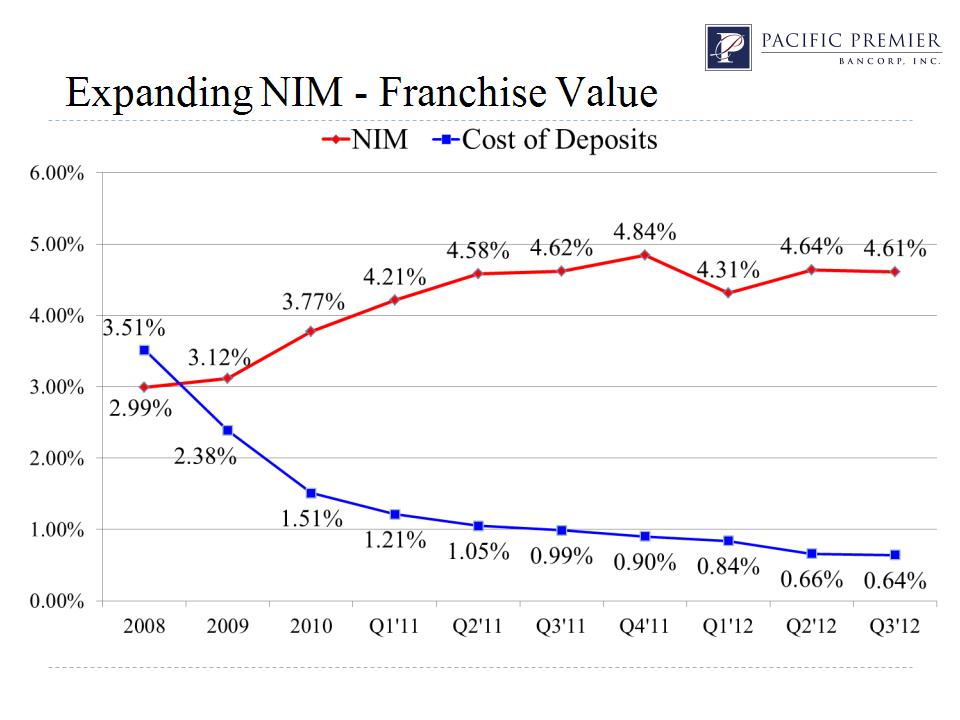

The statements contained in this presentation that are not historical facts are forward-looking statements based on management’s current expectations and beliefs concerning future developments and their

potential effects on Pacific Premier Bancorp, Inc. (the “Company”). Such statements involve inherent risks and uncertainties, many of which are difficult to predict and are generally beyond the control of the

Company. There can be no assurance that future developments affecting the Company will be the same as those anticipated by management. The Company cautions readers that a number of important factors

could cause actual results to differ materially from those expressed in, or implied or projected by, such forward-looking statements. These risks and uncertainties include, but are not limited to, the following:

the strength of the United States economy in general and the strength of the local economies in which the Company conducts operations; the effects of, and changes in, trade, monetary and fiscal policies and

laws, including interest rate policies of the Board of Governors of the Federal Reserve System; inflation, interest rate, market and monetary fluctuations; the timely development of competitive new products

and services and the acceptance of these products and services by new and existing customers; the willingness of users to substitute competitors’ products and services for the Company’s products and services;

the impact of changes in financial services policies, laws and regulations; technological changes; the effect of acquisitions that the Company may make, if any, including, without limitation, the failure to

achieve the expected revenue growth and expense savings from its pending acquisition of First Associations Bank (“FAB”); changes in the level of the Company’s nonperforming assets and charge-offs;

oversupply of inventory and continued deterioration in values of California real estate, both residential and commercial; the effect of changes in accounting policies and practices, as may be adopted from time-

to-time by bank regulatory agencies, the Securities and Exchange Commission (“SEC”), the Public Company Accounting Oversight Board, the Financial Accounting Standards Board or other accounting

standards setters; possible other-than-temporary impairments of securities held by the Company; the impact of current governmental efforts to restructure the U.S. financial regulatory system; changes in

consumer spending, borrowing and savings habits; the effects of the Company’s lack of a diversified loan portfolio, including the risks of geographic and industry concentrations; ability to attract deposits and

other sources of liquidity; changes in the financial performance and/or condition of the Company’s borrowers; changes in the competitive environment among financial and bank holding companies and other

financial service providers; unanticipated regulatory or judicial proceedings; and the Company’s ability to manage the risks involved in the foregoing.

potential effects on Pacific Premier Bancorp, Inc. (the “Company”). Such statements involve inherent risks and uncertainties, many of which are difficult to predict and are generally beyond the control of the

Company. There can be no assurance that future developments affecting the Company will be the same as those anticipated by management. The Company cautions readers that a number of important factors

could cause actual results to differ materially from those expressed in, or implied or projected by, such forward-looking statements. These risks and uncertainties include, but are not limited to, the following:

the strength of the United States economy in general and the strength of the local economies in which the Company conducts operations; the effects of, and changes in, trade, monetary and fiscal policies and

laws, including interest rate policies of the Board of Governors of the Federal Reserve System; inflation, interest rate, market and monetary fluctuations; the timely development of competitive new products

and services and the acceptance of these products and services by new and existing customers; the willingness of users to substitute competitors’ products and services for the Company’s products and services;

the impact of changes in financial services policies, laws and regulations; technological changes; the effect of acquisitions that the Company may make, if any, including, without limitation, the failure to

achieve the expected revenue growth and expense savings from its pending acquisition of First Associations Bank (“FAB”); changes in the level of the Company’s nonperforming assets and charge-offs;

oversupply of inventory and continued deterioration in values of California real estate, both residential and commercial; the effect of changes in accounting policies and practices, as may be adopted from time-

to-time by bank regulatory agencies, the Securities and Exchange Commission (“SEC”), the Public Company Accounting Oversight Board, the Financial Accounting Standards Board or other accounting

standards setters; possible other-than-temporary impairments of securities held by the Company; the impact of current governmental efforts to restructure the U.S. financial regulatory system; changes in

consumer spending, borrowing and savings habits; the effects of the Company’s lack of a diversified loan portfolio, including the risks of geographic and industry concentrations; ability to attract deposits and

other sources of liquidity; changes in the financial performance and/or condition of the Company’s borrowers; changes in the competitive environment among financial and bank holding companies and other

financial service providers; unanticipated regulatory or judicial proceedings; and the Company’s ability to manage the risks involved in the foregoing.

Additional factors that could cause actual results to differ materially from those expressed in the forward-looking statements are discussed in the Company’s 2011 Annual Report on Form 10-K filed with the

SEC and other filings made by the Company with the SEC. The Company specifically disclaims any obligation to update any factors or to publicly announce the result of revisions to any of the forward-

looking statements included herein to reflect future events or developments.

SEC and other filings made by the Company with the SEC. The Company specifically disclaims any obligation to update any factors or to publicly announce the result of revisions to any of the forward-

looking statements included herein to reflect future events or developments.

Notice to FAB Shareholders

This presentation does not constitute an offer to sell or the solicitation of an offer to buy any securities or a solicitation of any vote or approval. In connection with the proposed acquisition of FAB, the

Company filed a registration statement on Form S-4 (the “Registration Statement”) with the SEC, which contains a proxy statement of FAB and a prospectus of the Company (collectively, the “proxy

statement/prospectus”). A definitive proxy statement/prospectus will be distributed to the shareholders of FAB in connection with their vote on the proposed acquisition of FAB after the Registration Statement

is declared by the SEC to be effective. As of the date of this presentation, the Registration Statement has not been declared effective by the SEC. SHAREHOLDERS OF FAB ARE ENCOURAGED TO

READ THE REGISTRATION STATEMENT AND THE DEFINITIVE PROXY STATEMENT/PROSPECTUS AND ALL OTHER RELEVANT DOCUMENTS FILED WITH THE SEC, AS WELL AS

SUPPLEMENTS TO THOSE DOCUMENTS, BECAUSE THEY WILL CONTAIN IMPORTANT INFORMATION ABOUT THE PROPOSED ACQUISITION OF FAB. The definitive proxy

statement/prospectus will be mailed to shareholders of FAB. Investors and security holders will be able to obtain the definitive proxy statement/prospectus and the other documents free of charge at the SEC's

website, www.sec.gov. In addition, documents filed with the SEC by the Company will be available free of charge by (1) accessing the Company’s website at www.ppbi.com under the “Investor Relations”

link and then under the heading “SEC Filings,” (2) writing the Company at 17901 Von Karman Ave., Suite 1200, Irvine, California 92614, Attention: Investor Relations or (3) writing FAB at 12001 N. Central

Expressway, Suite 1165, Dallas, Texas 75243, Attention: Corporate Secretary.

Company filed a registration statement on Form S-4 (the “Registration Statement”) with the SEC, which contains a proxy statement of FAB and a prospectus of the Company (collectively, the “proxy

statement/prospectus”). A definitive proxy statement/prospectus will be distributed to the shareholders of FAB in connection with their vote on the proposed acquisition of FAB after the Registration Statement

is declared by the SEC to be effective. As of the date of this presentation, the Registration Statement has not been declared effective by the SEC. SHAREHOLDERS OF FAB ARE ENCOURAGED TO

READ THE REGISTRATION STATEMENT AND THE DEFINITIVE PROXY STATEMENT/PROSPECTUS AND ALL OTHER RELEVANT DOCUMENTS FILED WITH THE SEC, AS WELL AS

SUPPLEMENTS TO THOSE DOCUMENTS, BECAUSE THEY WILL CONTAIN IMPORTANT INFORMATION ABOUT THE PROPOSED ACQUISITION OF FAB. The definitive proxy

statement/prospectus will be mailed to shareholders of FAB. Investors and security holders will be able to obtain the definitive proxy statement/prospectus and the other documents free of charge at the SEC's

website, www.sec.gov. In addition, documents filed with the SEC by the Company will be available free of charge by (1) accessing the Company’s website at www.ppbi.com under the “Investor Relations”

link and then under the heading “SEC Filings,” (2) writing the Company at 17901 Von Karman Ave., Suite 1200, Irvine, California 92614, Attention: Investor Relations or (3) writing FAB at 12001 N. Central

Expressway, Suite 1165, Dallas, Texas 75243, Attention: Corporate Secretary.

The directors, executive officers and certain other members of management and employees of the Company may be deemed to be participants in the solicitation of proxies in favor of the proposed acquisition

from the shareholders of FAB. Information about the directors and executive officers of the Company is included in the proxy statement for its 2012 annual meeting of shareholders, which was filed with the

SEC on April 16, 2012. The directors, executive officers and certain other members of management and employees of FAB may also be deemed to be participants in the solicitation of proxies in favor of the

proposed acquisition from the shareholders of FAB. Information about the directors and executive officers of FAB is included in the definitive proxy statement/prospectus for the proposed acquisition of FAB.

Additional information regarding the interests of those participants and other persons who may be deemed participants in the transaction may be obtained by reading the definitive proxy statement/prospectus

regarding the proposed acquisition. You may obtain free copies of this document as described in the preceding paragraph.

from the shareholders of FAB. Information about the directors and executive officers of the Company is included in the proxy statement for its 2012 annual meeting of shareholders, which was filed with the

SEC on April 16, 2012. The directors, executive officers and certain other members of management and employees of FAB may also be deemed to be participants in the solicitation of proxies in favor of the

proposed acquisition from the shareholders of FAB. Information about the directors and executive officers of FAB is included in the definitive proxy statement/prospectus for the proposed acquisition of FAB.

Additional information regarding the interests of those participants and other persons who may be deemed participants in the transaction may be obtained by reading the definitive proxy statement/prospectus

regarding the proposed acquisition. You may obtain free copies of this document as described in the preceding paragraph.

2

Corporate Profile

NASDAQ | PPBI |

Focus | Small & Middle Market Businesses |

Total Assets | $1.089 Billion |

Branches | 10 Locations |

TCE Ratio | 8.94% (1) |

FD Book Value | $9.53 |

Net Income YTD ($000) | $11,965 |

ROAA YTD | 1.56% |

ROAE YTD | 17.23% |

NPAs / Assets | 1.08% |

As of September 30, 2012

(1) Non-GAAP financial measure. Please see the Appendix to this investor presentation for the GAAP reconciliation

3

Overview of PPBI

Strategic Plan - Pre 2008 Stage | o Convert from a Thrift to a Commercial Bank o Diversify the balance sheet, assets and liabilities |

Strategic Plan - Current Stage | o Growth by taking market share from competitors o Growth through disciplined acquisitions o Canyon National Bank - $209 million in assets as of 2/11/11 o Palm Desert National Bank - $121 million in assets as of 4/27/12 o First Associations Bank (Pending) - $356 million in assets as of 9/30/12 o Maintain positive trends in profitability, net interest margin, & credit quality |

Strategic Plan - Next Stage | o $31 million capital raise to support organic growth and acquisitions o Increase fee income - SBA lending o Increase non-interest bearing accounts to 35%+ of deposit base o Build out commercial banking franchise |

4

Deposit Base: Today vs. 2008

12/31/08 | 9/30/12 | Variance | |

(dollars in thousands) | |||

Transaction Accounts | |||

Noninterest bearing | $29,443 | $211,410 | 618.0% |

Interest bearing checking | 20,989 | 11,684 | (44.3%) |

Money market | 23,463 | 174,375 | 643.2% |

Savings | 14,401 | 80,419 | 458.4% |

Total transaction accounts | 88,296 | 477,888 | 441.2% |

CD Accounts | |||

Time deposits | 341,741 | 471,982 | 38.1% |

Broker/wholesale CDs | 27,091 | 0 | (100.0%) |

Total CDs | 368,832 | 417,982 | 13.3% |

Total deposits | $457,128 | $895,870 | 96.0% |

5

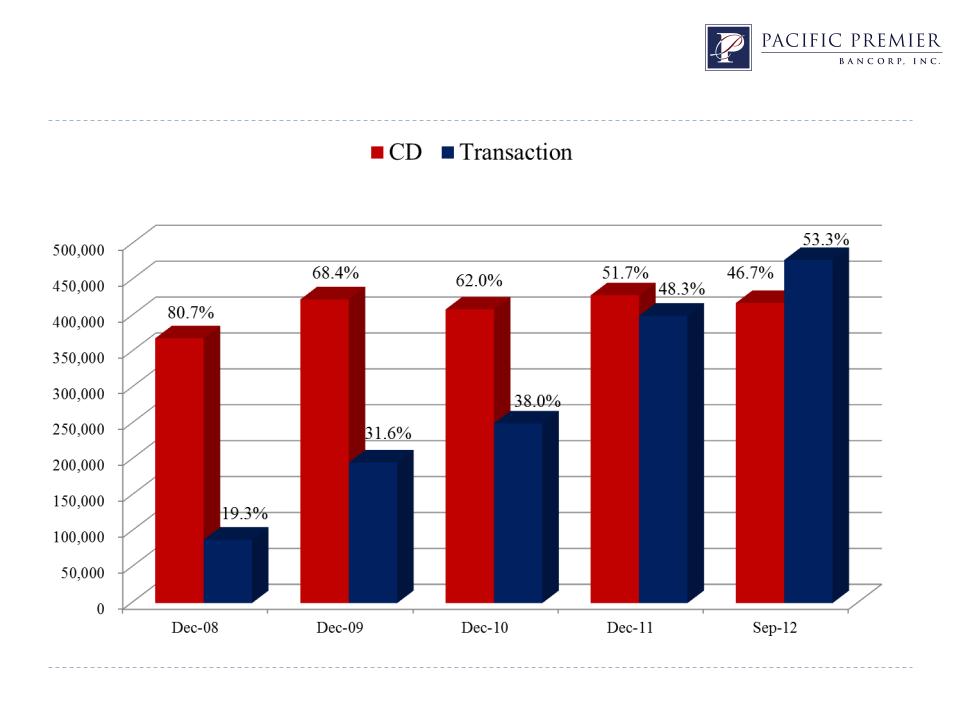

Deposit Mix - Increasing Shareholder Value

$457,128

$618,734

$659,240

$828,877

$895,870

6

Loan Portfolio: Today vs. 2008

12/31/08 | 09/30/12 | Variance | |

(dollars in thousands) | |||

Business Loans | |||

Commercial RE owner occupied | $112,406 | $148,139 | 31.8% |

Commercial and industrial | 43,235 | 88,105 | 103.8% |

Warehouse | 0 | 112,053 | n/a |

SBA | 4,942 | 4,736 | (4.2%) |

Total business loans | 160,583 | 353,033 | 119.8% |

CRE Loans | |||

Multi-family | 287,592 | 173,484 | (39.7%) |

Commercial non-owner occupied | 163,428 | 262,046 | 60.3% |

Total CRE loans | 451,020 | 435,530 | (3.4%) |

One-to-four family | 9,925 | 62,771 | 532.5% |

Other loans | 7,239 | 13,504 | 86.5% |

Gross loans | $628,767 | $864,838 | 37.5% |

7

Strategic Plan Execution

o Relationship banking model

o Growing core deposit base - shareholder value

o Robust earnings stream, building book value

o Excellent asset quality

o Increasing market share

o Strong execution on acquisitions

o Disciplined analysis and pricing of targets

8

Financial Summary

QTD 9/30/11 | QTD 12/31/11 | QTD 3/31/12 | QTD 6/30/12 | QTD 9/30/12 | |

Balance Sheet | (dollars in thousands, except per share data) | ||||

Total assets | $928,502 | $961,128 | $985,171 | $1,065,035 | $1,089,336 |

Net loans | 725,952 | 730,067 | 687,141 | 790,062 | 856,443 |

Total deposits | 797,378 | 828,877 | 846,717 | 913,191 | 895,870 |

Total borrowings | 38,810 | 38,810 | 38,810 | 38,810 | 85,810 |

Total equity | 84,620 | 86,777 | 89,479 | 96,069 | 99,886 |

Statements of Operations | |||||

Net interest income | $10,231 | $10,960 | $10,041 | $11,282 | $11,854 |

Noninterest income | 2,110 | 257 | 939 | 6,529 | 1,910 |

Noninterest expense | 7,074 | 6,616 | 6,641 | 8,205 | 8,031 |

Net income | 2,460 | 2,555 | 2,692 | 5,811 | 3,462 |

Diluted EPS | $0.23 | $0.24 | $0.25 | $0.55 | $0.32 |

Bank Capital Ratios | |||||

Tier 1 leverage | 9.29% | 9.44% | 9.49% | 9.48% | 9.48% |

Tier 1 risk-based | 11.57% | 11.68% | 12.54% | 11.28% | 11.04% |

Total risk-based | 12.71% | 12.81% | 13.66% | 12.18% | 11.88% |

9

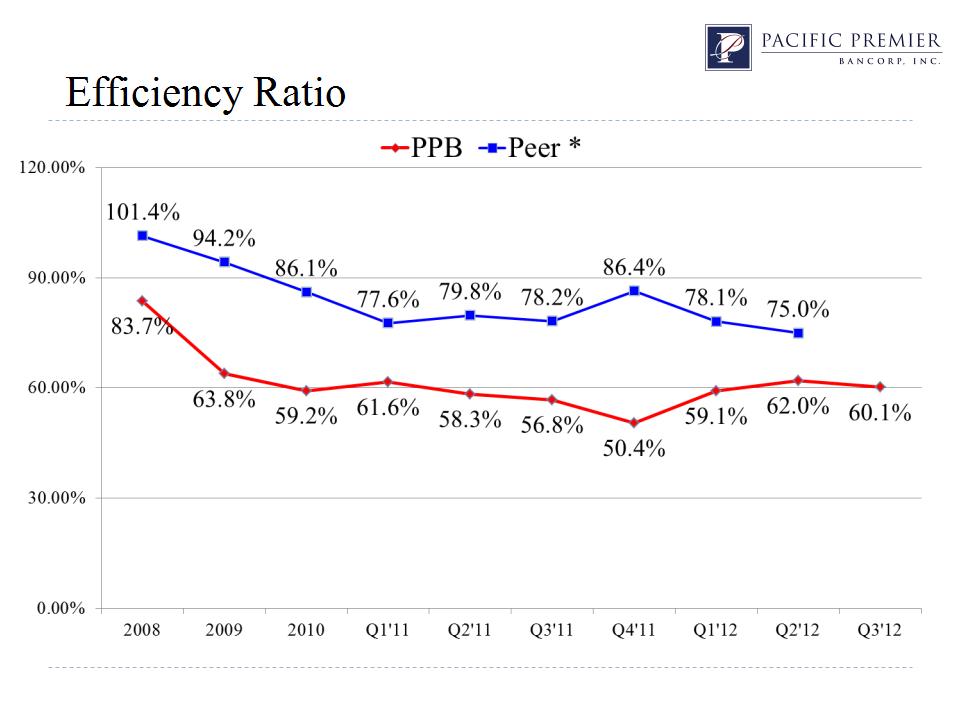

10

* California peer group consists of all insured California institutions in the FFIEC database

11

Conservative Credit Culture

o Overall Underwriting Approach:

o Global cash flow lender

o Loans:

o Business - full banking relationship

o CRE - no high risk product types or loan structures

o Personal guarantees, cross collateralized, cross guarantees

o Proactive Portfolio Management

12

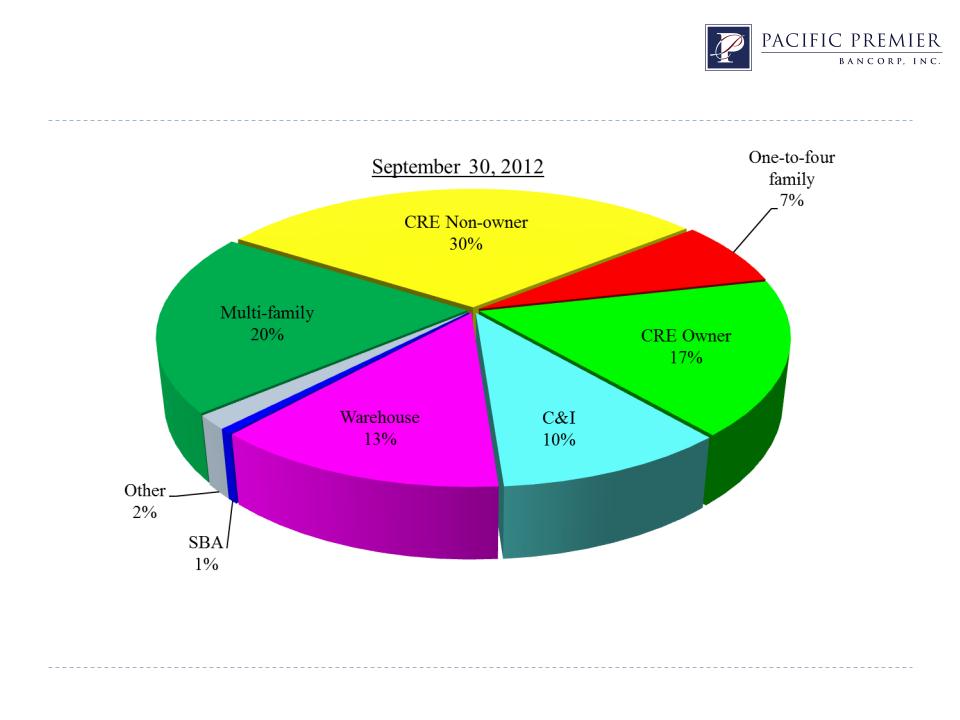

Loan Portfolio

Total loans: $864.8 million

WAVG Rate: 5.72%

13

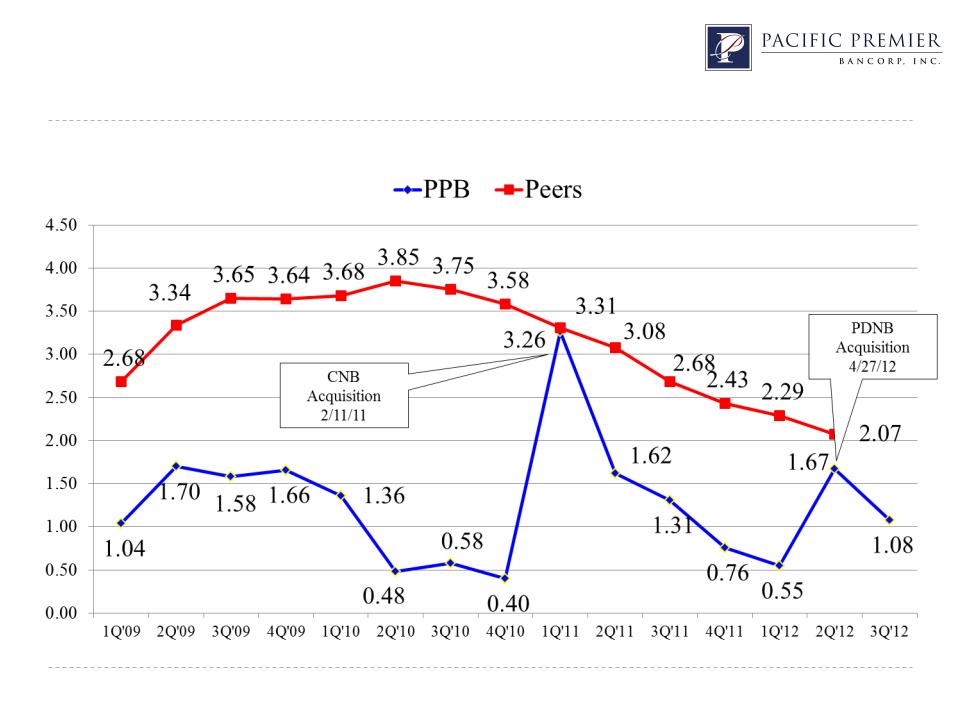

Solid Loan Performance

California peer group consists of all insured California institutions in the FFIEC database

Delinquency to Total Loans

PDNB

Acquisition

4/27/12

14

Proactive Asset Management

California peer group consists of all insured California institutions in the FFIEC database

Nonperforming Assets to Total Assets

15

Future Growth - Potential M&A Targets

Southern California Institutions

Source: SNL Financial

Total assets ………………………………….. | $ 15.3 |

Total deposits …………………..................... | 12.6 |

Total core deposits …………….................... | 11.0 |

Total loans ……………………..................... | 10.6 |

Total branches ………………........................ | 204 |

(dollars in billions)

Potential Targets - $100 to $500 million 100 miles from Irvine, California As of September 30, 2012 | |

# of Institutions | |

$100 to $250 million | 43 |

$250 to $500 million | 22 |

16

First Associations Bank Acquisition Overview

Strategic Rationale | o Valuable source of long-term low-cost core deposits o Improves PPBI’s deposit mix and enhances franchise value o HOA Management deposit platform provides additional funding for loan growth |

Attractive Valuation | o Price / tangible book value of 118.2%(1)(2) o Core deposit premium of 2.73%(1) o Price / earnings (last twelve months, tax adjusted)(1)(3) of 17.4x |

Pro Forma Impact to PPBI | o Accretive to EPS beginning in 2013 o Tangible book value payback period approximately 2 years(2)(4) |

Other Transaction Assumptions | o Core deposit intangible asset of $1.5 million, or 0.50% of FAB’s core deposits o Total transaction expenses of approximately $5.1 million |

Preliminary Fair Value Adjustments | o Positive mark on FAB’s HTM securities portfolio from unrealized gain ($5.6 million(1)) o 2.00% fair value mark on FAB’s gross loans |

Cost Savings | o Cost savings of approximately 10.0% (no personnel reduction) o Cost savings are 75.0% phased in during 2013 and 100.0% phased in by 2014 |

Revenue Enhancements | o Readily available liquidity that can be redeployed into PPBI’s commercial banking business model. Additional revenue enhancements from PPBI’s higher cost CD run-off |

(1) FAB balance sheet data as of 9/30/2012; PPBI market price data as of 12/4/2012

(2) Non-GAAP financial measure. Please see the Appendix to this investor presentation for GAAP reconciliation

(3) Adjusted for FAB’s S-Corporation status based on tax rate of 34.00%

(4) Incremental Tangible Book Value Payback represents the number of years to eliminate tangible book value dilution at closing utilizing incremental earnings created

in the merger including pro forma earnings from FAB

in the merger including pro forma earnings from FAB

17

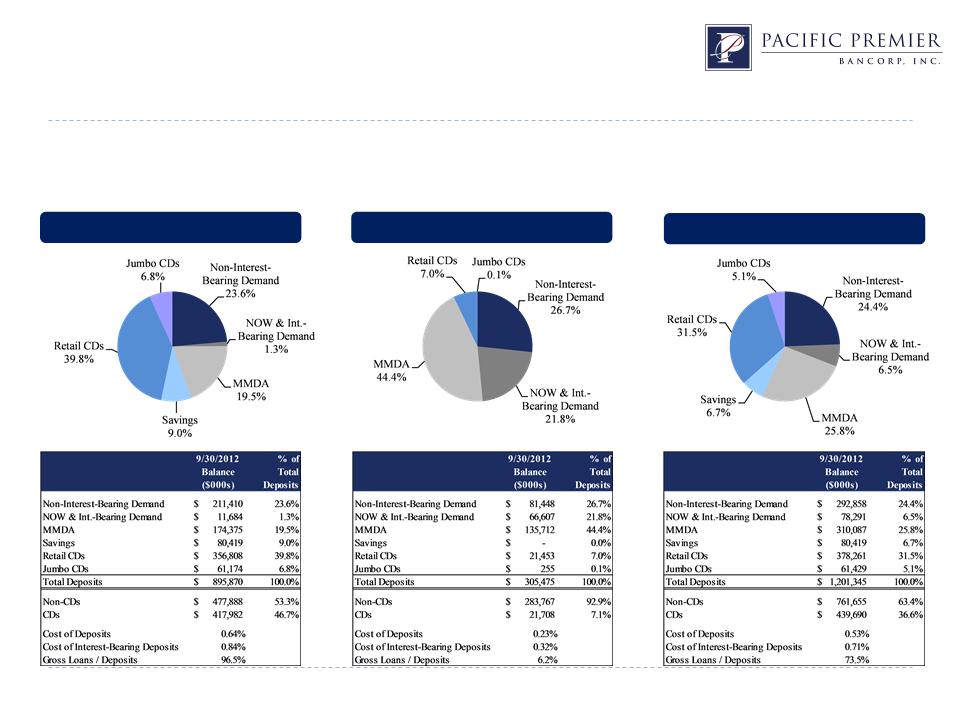

Attractive Pro Forma Deposit Franchise

Source: PPBI Form 10-Q and SNL Financial FAB regulatory call report data, each as of 9/30/2012

Note: Pro Forma does not include purchase accounting or merger related adjustments

o Strengthens PPBI’s deposit franchise with low-cost long-term funding platform (FAB cost of deposits was 0.23% during 2012 Q3)

o PPBI has $113.5 million CDs that will mature in 2012 Q4, with weighted average cost of 1.05%

o The acquisition would reduce PPBI’s loan / deposit ratio from 96.5% to pro forma 73.5%, as of 9/30/2012

PPBI (9/30/2012)

FAB (9/30/2012)

Pro Forma (9/30/2012)

18

Outlook

o Gaining market share from competitors

o Building franchise value

o Southern California is one of the best banking markets

o Target rich environment for acquisitions

o Proven management team and track record

o Experienced acquirer

o Liquidity from FAB acquisition will fund future loan growth

o Well positioned to expand reach throughout Southern California

19

Steve Gardner

sgardner@ppbi.com

(714) 431 - 4000

www.ppbi.com

20

Appendix

21

Non-GAAP Financial Measures

Tangible common equity and tangible book value per share are non-GAAP financial measures derived from GAAP-based amounts. We calculate tangible common

equity by excluding the balance of intangible assets from common stockholders’ equity. We calculate tangible book value per share by dividing tangible common

equity by common shares outstanding, as compared to book value per common share, which we calculate by dividing common stockholders’ equity by common

shares outstanding. We believe that this is consistent with the treatment by bank regulatory agencies, which exclude intangible assets from the calculation of risk-

based capital ratios. Accordingly, we believe that these non-GAAP financial measures provide information that is important to investors and that is useful in

understanding our capital position and ratios. However, these non-GAAP financial measures are supplemental and are not a substitute for an analysis based on GAAP

measures. As other companies may use different calculations for these measures, this presentation may not be comparable to other similarly titled measures reported

by other companies. A reconciliation of the non-GAAP measures of tangible common equity and tangible book value per share to the GAAP measures of common

stockholder’s equity and book value per share is set forth.

equity by excluding the balance of intangible assets from common stockholders’ equity. We calculate tangible book value per share by dividing tangible common

equity by common shares outstanding, as compared to book value per common share, which we calculate by dividing common stockholders’ equity by common

shares outstanding. We believe that this is consistent with the treatment by bank regulatory agencies, which exclude intangible assets from the calculation of risk-

based capital ratios. Accordingly, we believe that these non-GAAP financial measures provide information that is important to investors and that is useful in

understanding our capital position and ratios. However, these non-GAAP financial measures are supplemental and are not a substitute for an analysis based on GAAP

measures. As other companies may use different calculations for these measures, this presentation may not be comparable to other similarly titled measures reported

by other companies. A reconciliation of the non-GAAP measures of tangible common equity and tangible book value per share to the GAAP measures of common

stockholder’s equity and book value per share is set forth.

PPBI (1) | Pro Forma With FAB (2) | ||

Common Stockholders’ Equity | $99,886 | $109,367 | |

Less: Intangible Assets | $2,703 | $7,840 | |

Tangible Common Equity | $97,183 | $101,527 | |

Book Value per Share | $9.66 | $9.41 | |

Less: Intangible Assets per Share | $0.26 | $0.67 | |

Tangible Book Value per Share | $9.40 | $8.74 | |

Total Assets | $1,089,336 | $1,409,139 | |

Less: Intangible Assets | $2,703 | $7,840 | |

Tangible Assets | $1,086,633 | $1,401,299 | |

Tangible Common Equity Ratio | 8.94% | 7.25% |

(1) As of 9/30/2012

(2) Includes base merger assumptions for FAB as of 9/30/2012

Note: Dollars in thousands except per share

22