Exhibit 99.1

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

[LOGO OF PACIFIC PREMIER BANCORP, INC.]

Carpenter & Company/CBA

“2006 Strategic Issues Summit”

April 4, 2006

Steven R. Gardner

President & CEO

WWW.PPBI.NET

[GRAPHIC APPEARS HERE]

Forward-Looking Comments

The statements contained herein that are not historical facts are forward looking statements based on management’s current expectations and beliefs concerning future developments and their potential effects on the Company. There can be no assurance that future developments affecting the Company will be the same as those anticipated by management. Actual results may differ from those projected in the forward-looking statements. These forward-looking statements involve risks and uncertainties. These include, but are not limited to, the following risks: (1) changes in the performance of the financial markets, (2) changes in the demand for and market acceptance of the Company’s products and services, (3) changes in general economic conditions including interest rates, presence of competitors with greater financial resources, and the impact of competitive projects and pricing, (4) the effect of the Company’s policies, (5) the continued availability of adequate funding sources, and (6) various legal, regulatory and litigation risks.

[GRAPHICS APPEAR HERE]

Southern California Community Bank

Data as of 12/31/05

• | NASDAQ National Market | PPBI |

|

|

|

• | Assets | $ 703 million |

|

|

|

• | Fully diluted shares | 6,658,240 |

|

|

|

• | Fully diluted BV | $ 8.09 |

|

|

|

• | Annualized ROAA | 1.18% |

|

|

|

• | Annualized ROAE | 15.17% |

[GRAPHICS APPEAR HERE] | |

|

|

• | Transitioning business model |

|

|

• | Balance Sheet strength |

|

|

• | Favorable relative valuation |

Three Phase | |

| |

Strategic Plan | |

| |

• | Phase 1 – Risk Reduction |

|

|

• | Phase 2 – Accelerated Growth |

|

|

• | Phase 3 – Transition business model |

[GRAPHICS APPEAR HERE]

What We Inherited

Nationwide Subprime Lender

• | Assets | $552 million |

|

|

|

• | Loans | $434 million |

|

|

|

• | Subprime loans | 75% |

|

|

|

• | NPA’s | 7.8% |

|

|

|

• | Employees/Offices | 334/10 |

|

|

|

• | Under capitalized |

|

|

|

|

• | Subject to Regulatory Enforcement |

|

[GRAPHICS APPEAR HERE]

Completed June 2002

• | Assets | $246 million |

|

|

|

• | Loans | $135 million |

|

|

|

• | Employees/Offices | 63/4 |

|

|

|

• | Substantial reduction in risk |

|

|

|

|

• | Recapitalized - Private Placement |

|

|

|

|

• | Note and warrant issued |

|

|

|

|

• | Regulatory concerns resolved |

|

[GRAPHICS APPEAR HERE]

Accelerated growth

[GRAPHICS APPEAR HERE]

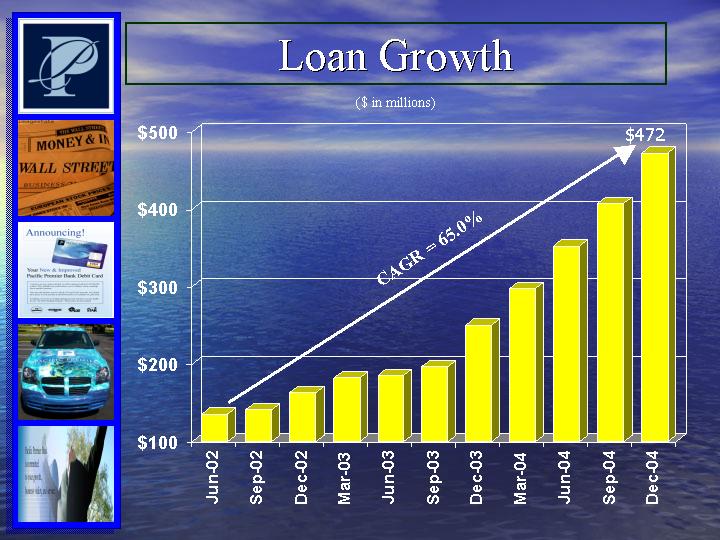

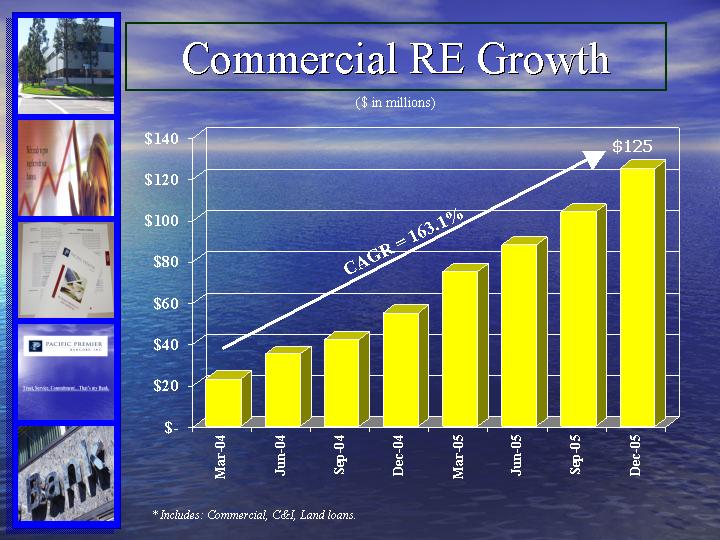

($ in millions)

[CHART APPEARS HERE]

[GRAPHICS APPEAR HERE]

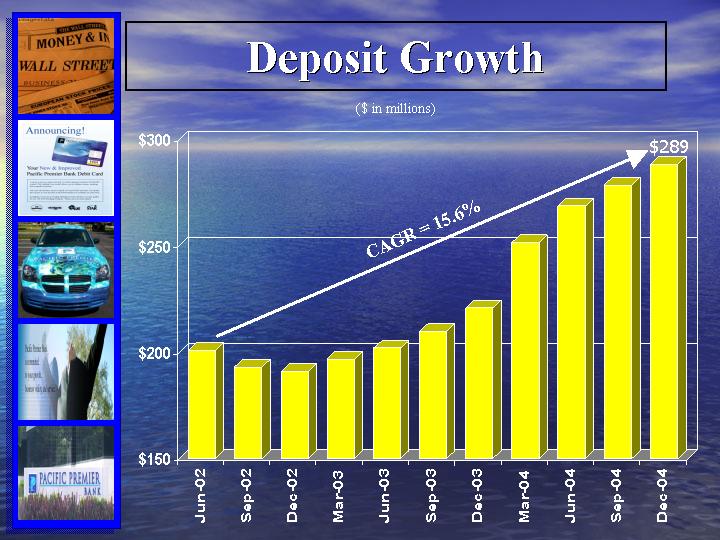

($ in millions)

[CHART APPEARS HERE]

[GRAPHICS APPEAR HERE]

Completed 2004

• | Assets | $543 million |

|

|

|

• | Loans | $472 million |

|

|

|

• | Secondary Offering | $26 million |

|

|

|

• | Note retired |

|

|

|

|

• | Stage set for further growth |

|

It’s the Economy

|

|

| OC |

|

| So. Cal. |

|

|

|

|

|

|

| ||

Total Deposits |

|

| $64 Billion |

|

| $385 Billion |

|

Deposit Growth Rate |

|

| 13.7% |

|

| 11.7% |

|

Population |

|

| 3,000,000 |

|

| 21,900,000 |

|

Population Growth |

|

| 4.96% |

|

| 6.56% |

|

Median Household Income |

|

| $ 64,611 |

|

| $ 51,212 |

|

No. of Households |

|

| 936,000 |

|

| 6,825,000 |

|

Sources: Dataplace, Rueters, State of California

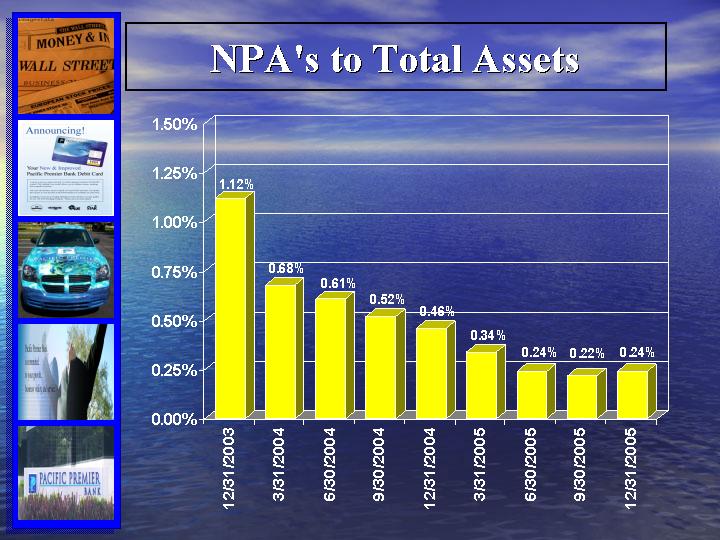

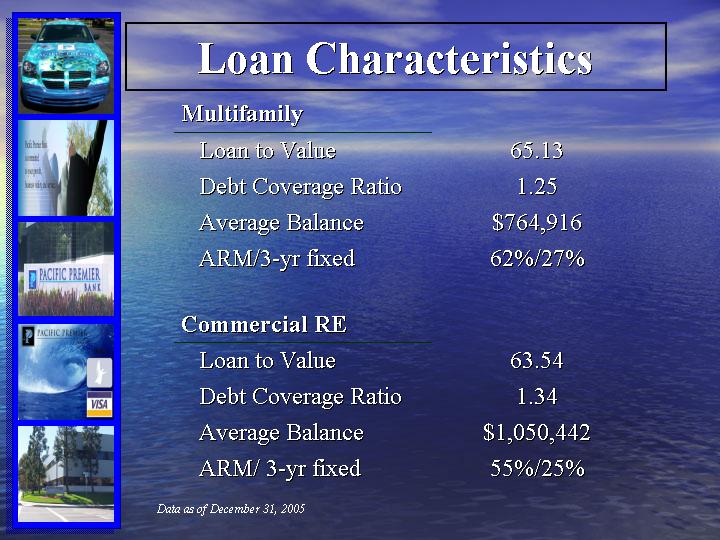

Balance Sheet Strength

[GRAPHICS APPEAR HERE]

[CHART APPEARS HERE]

[GRAPHICS APPEAR HERE]

Multifamily |

|

|

|

| |

Loan to Value |

| 65.13 |

Debt Coverage Ratio |

| 1.25 |

Average Balance |

| $764,916 |

ARM/3-yr fixed |

| 62%/27% |

| | |

|

| |

Loan to Value |

| 63.54 |

Debt Coverage Ratio |

| 1.34 |

Average Balance |

| $1,050,442 |

ARM/ 3-yr fixed |

| 55%/25% |

Data as of December 31, 2005

[GRAPHICS APPEAR HERE]

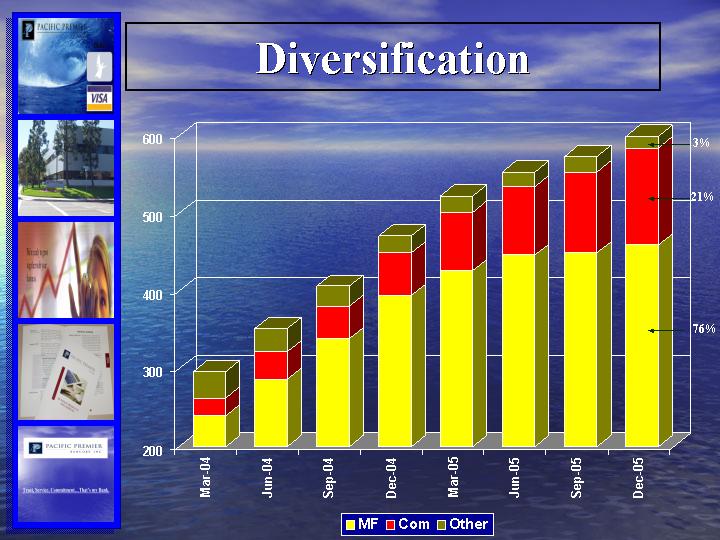

Transition Business Model

• | Diversification of Balance Sheet |

[GRAPHICS APPEAR HERE]

[CHART APPEARS HERE]

[GRAPHICS APPEAR HERE]

($ in millions)

[CHART APPEARS HERE]

* Includes: Commercial, C&I, Land loans. |

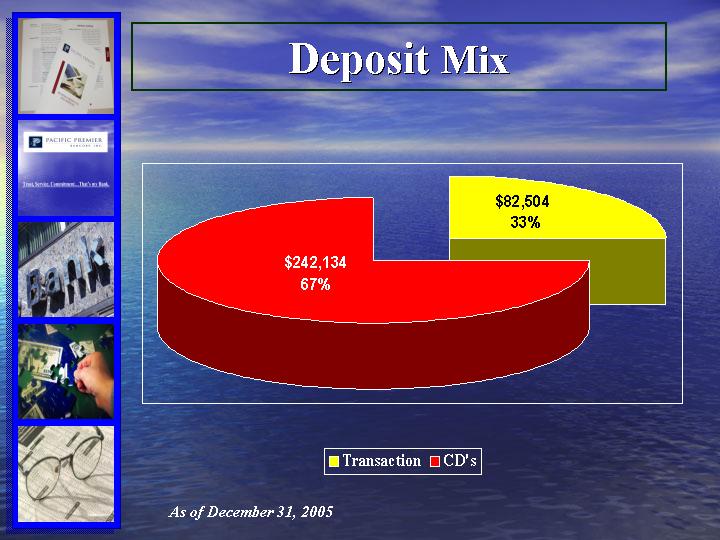

[GRAPHICS APPEAR HERE]

[CHART APPEARS HERE]

As of December 31, 2005

[GRAPHICS APPEAR HERE]

Transition Business Model

• | Diversification of Balance Sheet |

|

|

• | Relationship Banking |

[GRAPHIC APPEARS HERE]

[GRAPHICS APPEAR HERE]

|

| 9/30/ 2004 |

| 12/31/2005 |

| ||

|

|

|

| ||||

No. Relationships |

|

| 28 |

|

| 188 |

|

Loans |

| $ | 29,874,000 |

| $ | 226,793,000 |

|

Deposits |

| $ | 969,000 |

| $ | 16,025,000 |

|

[GRAPHIC APPEARS HERE]

Transition Business Model

• | Diversification of Balance Sheet |

|

|

• | Relationship Banking |

|

|

• | Expansion of Branch Network |

[GRAPHICS APPEAR HERE]

[CHART APPEARS HERE]

[GRAPHICS APPEAR HERE]

[CHART APPEARS HERE]

[GRAPHICS APPEAR HERE]

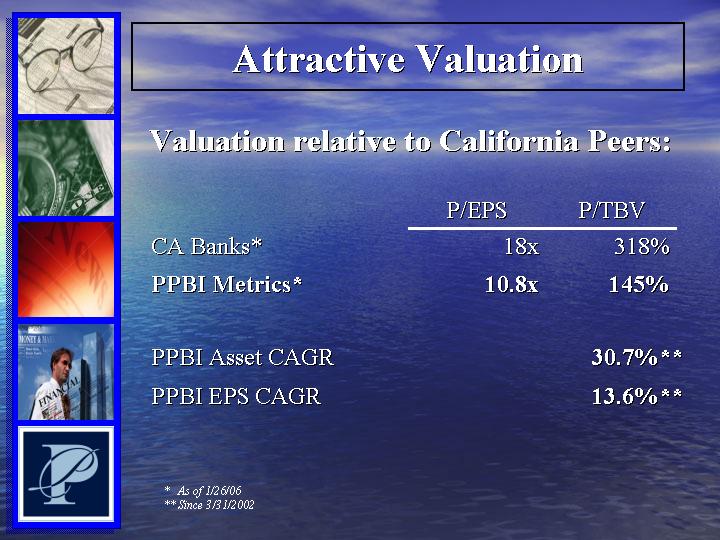

Valuation relative to California Peers:

|

| P/EPS |

| P/TBV |

| |||

|

|

|

| |||||

CA Banks* |

|

| 18 | x |

| 318 | % | |

PPBI Metrics* |

|

| 10.8 | x |

| 145 | % | |

PPBI Asset CAGR |

|

|

|

|

| 30.7 | %** | |

PPBI EPS CAGR |

|

|

|

|

| 13.6 | %** | |

|

|

* | As of 1/26/06 |

** | Since 3/31/2002 |

[GRAPHICS APPEAR HERE]

• | Transition to Commercial Bank model |

|

|

• | Low Risk Balance Sheet |

|

|

• | Sustainable earnings growth |

|

|

• | Excellent time to invest |

[LOGO OF PACIFIC PREMIER BANCORP, INC.]

Trust, Service, Commitment…That’s my Bank.

WWW.PPBI.NET