Sussex Bancorp

July 2005

KBW Community Bank Conference

AMEX / SBB

FORWARD-LOOKING DISCLAIMER

Statements contained in this presentation which are not historical facts are

forward-looking statements. In addition, Sussex Bancorp, through its senior

management, may from time to time make forward-looking public

statements concerning the matters described herein. Such forward-looking

statements are estimates reflecting the best judgment of Sussex Bancorp’s

senior management based upon current information and involve a number

of risks and uncertainties. Certain factors which could affect the accuracy of

such forward-looking statements are identified in the public filings made by

Sussex Bancorp with the Securities and Exchange Commission, including

the company’s annual report on form 10-K for the year ended December 31,

2004 and forward-looking statements contained in this or other public

statements of Sussex Bancorp or its senior management should be

considered in light of those factors. There can be no assurance that such

factors or other factors will not affect the accuracy of such forward-looking

statements. Sussex Bancorp undertakes no obligation to revise these

statements after the date of this presentation.

2

SUSSEX BANCORP

Headquartered in Sussex County, NJ

Chartered in 1975 with $1.5 million in

capital:

2000: Obtained capital contribution from

competitor Lakeland Bancorp

2004: Raised $15.2 million through

follow-on equity offering doubling our

capital

Lines of business:

Personal & business banking

Insurance agency

Mortgage banking

Title insurance & settlement services

Trust & investment services

OUR COMMUNITY BANK PHILOSOPHY EMPHASIZES A HIGH SERVICE LEVEL,

PERSONALIZED APPROACH WHICH IS GENERALLY NOT OFFERED BY OUR LARGER

COMPETITORS.

3

INVESTMENT THESIS

Demonstrated record of success managing and growing a community bank:

15% compounded annual growth of assets(1)

12% compounded annual growth of loans(1)

13% compounded annual growth of deposits(1)

20% compounded annual growth of net income(1)

14% compounded annual growth of EPS(1)

Contiguous markets are much larger than Sussex and have been disrupted by

consolidation. These markets include some of the wealthiest in the United States.

We intend to grow in these markets by capturing market share from our larger

competitors.

We have built an infrastructure and have obtained the capital to support a much

larger institution.

Experienced management team with deep knowledge of market area and large

ownership stake of 17%.

(1) For the ‘00 – ‘04 period

4

BUSINESS PLAN

ELEMENTS OF OUR 3-5 YEAR BUSINESS PLAN:

Continue to grow the balance sheet organically at rates consistent with our recent

track record (10 -13%) by expanding in Sussex and into contiguous markets:

Capitalize on dislocation caused by merger & acquisition activity

Take advantage of greater deposit base in surrounding counties by stealing market

share

De novo branching

M&A opportunities (whole bank, branch and insurance agency acquisitions)

Loan production offices

Improve the profitability of franchise over 3-5 year time horizon:

Focus on commercial loan growth to improve our yield on loans

Focus on growing core deposits to lower our cost of funds

Obtain economies of scale as our balance sheet grows into our infrastructure

Our goal is to create a $500 million + community banking company with an ROA

of at least 1%

5

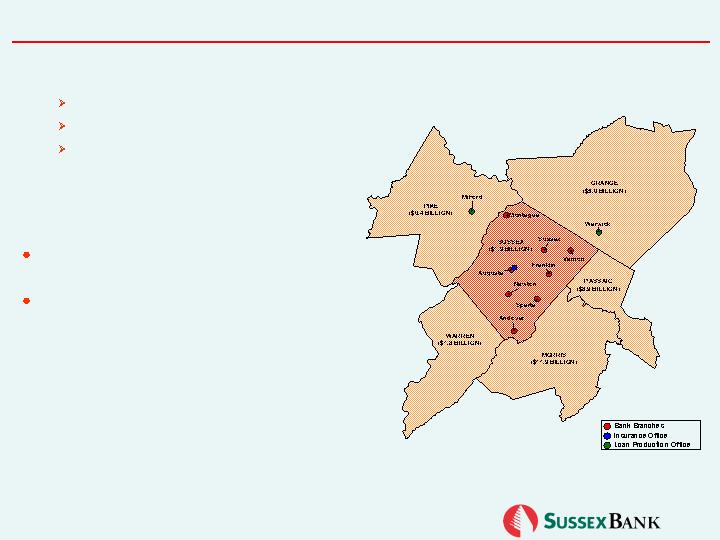

DISTRIBUTION NETWORK

Our distribution network currently consists of 8 full-service branch locations, 2

loan production offices and 1 insurance agency office.

(Parentheses indicate county deposits as of June 30, 2004)

6

BUSINESS STRATEGY

EXPAND THE FRANCHISE IN CONTIGUOUS COUNTIES: THE OPPORTUNITY

Leveraging our high touch / service business model

Significantly larger markets

Markets disrupted by consolidation

Market contains $29.9 billion in deposits

Market has experienced 10 mergers(1)

over the last 2 years where 22.1% of

deposits ($6.6 billion) have or will be

“turned over”

(1) Source: SNL Financial

Mergers include: Bank of America / Fleet, Citizens / Charter One, PNC / United National, North Fork / Trust Co. of NJ,

Lakeland / Newton Financial, Valley / NorCrown, Kearny / West Essex, Provident / Warwick Community,

Center Bancorp / Red Oak Bank, TD Banknorth / Hudson United

(Parentheses indicate county deposits as of June 30, 2004)

7

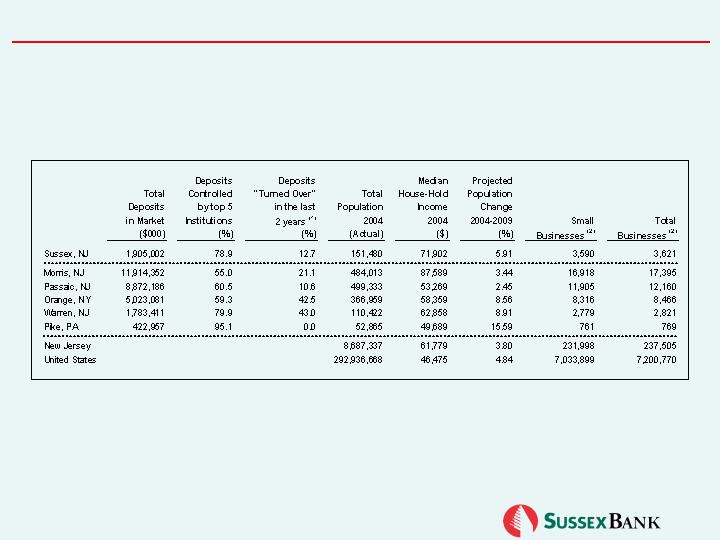

ATTRACTIVE DEMOGRAPHICS OF OUR TARGET MARKETS

Data obtained from: SNL Financial's Datasource database

SNL's source of deposit data: Federal Deposit Insurance Corporation; Data as of June 30, 2004

SNL's source of demographic data: Claritas

(1) Mergers include: Bank of America / Fleet, Citizens / Charter One, PNC / United National, North Fork / Trust Co. of NJ,

Lakeland / Newton Financial, Valley / NorCrown, Kearny / West Essex, Provident / Warwick Community,

Center Bancorp / Red Oak Bank, TD Banknorth / Hudson United

(2) Data as of 2002; Source: US Census; Small businesses defined as those with less than 100 employees

OUR TARGETED MARKETS ARE DENSELY POPULATED MARKETS WITH

ROBUST BUSINESS CLIMATES:

8

OUR EXISTING AND TARGET MARKETS

HIGHLY CONSOLIDATED MARKETS, POPULATED BY LARGE, OUT OF STATE

COMPETITORS:

Source: SNL Financial (FDIC data); Deposit data as of 6/30/2004 and pro forma for pending and completed acquisitions

9

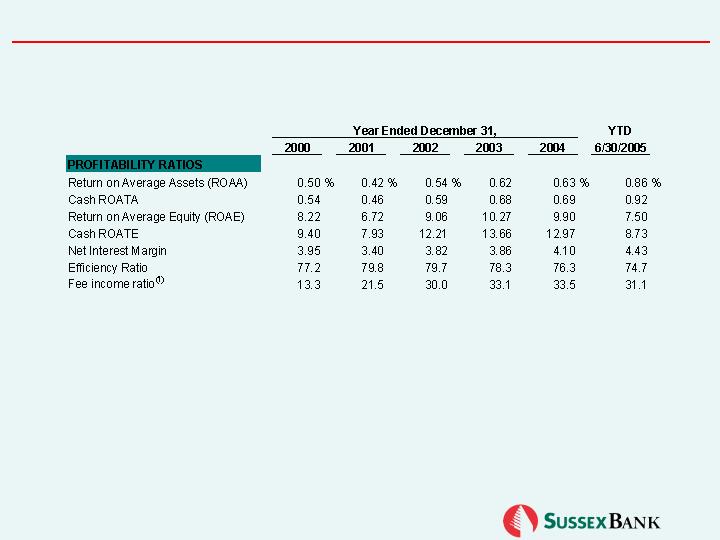

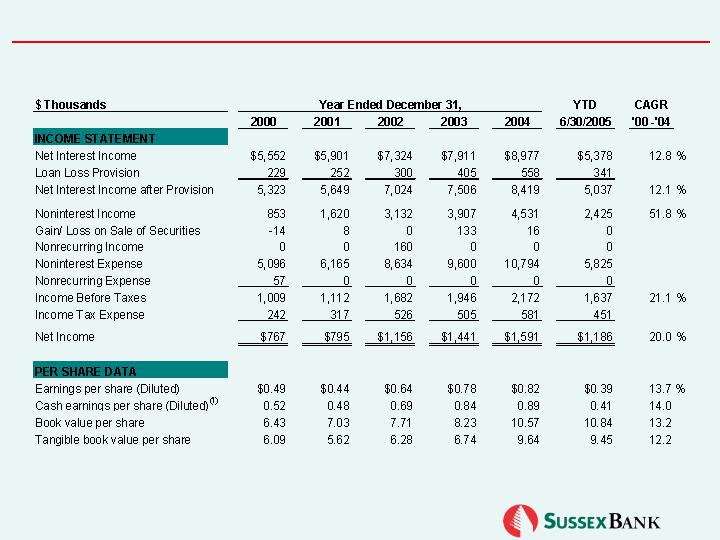

FINANCIAL PERFORMANCE

(1) Non-interest income as a percentage of net interest income + non-interest income; Excludes securities gains/losses

10

IMPROVE CORE PROFITABILITY

BALANCE SHEET INITIATIVES

Continue to transform the bank’s balance sheet:

Continue our growth in core deposits to reduce our cost of funds

Continue our commercial real estate and commercial loan growth to raise our yield on

earning assets

Will result in net interest margin expansion

NIM goal of 4.50% over 3-5 years

11

Efficiency ratio goal of 65% over 3-5 years

IMPROVE CORE PROFITABILITY

Improve Efficiency

Through growth &

scalability:

Investments in our

future have been

made:

Investments recently made in our infrastructure and

product platform, coupled with recent hires has created

the foundation to support a $500 million institution

Our expenses should not grow proportionally to our

earning asset growth

We have invested significantly in our future:

Relocated our corporate office to a sufficiently large space

Jack Henry bank-wide processing program

IBM computer mainframe

Retained Tammy Case, a veteran of our market, as our

new Executive Vice President – Loan Administration

Formed Sussex Settlement Services to provide title

insurance & settlement services

12

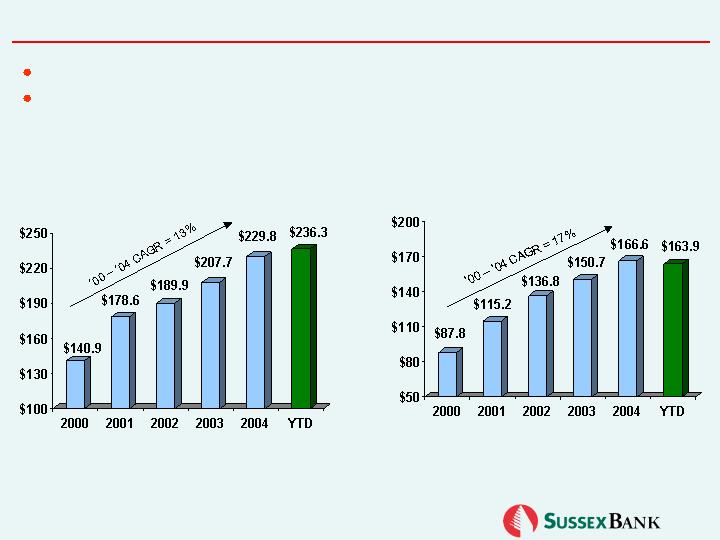

DEPOSIT GROWTH

Strong organic growth in total deposits

Shift towards lower costing core deposits

Total Deposits ($M)

Core Deposits ($M)*

* Excludes all CDs

13

SHIFTING DEPOSIT MIX

Our solid growth in core deposits has lowered our overall cost of funds

“High Performance Checking” (free checking)

Aggressive marketing

Targeted mailings

12/31/2000

6/30/2005

Total Deposits: $140.9 million

Cost of Deposits: 3.29%

Total Deposits: $236.3 million

Cost of Deposits: 1.33%

14

LOAN GROWTH

Demonstrating strong organic growth

Loan production offices in Port Jervis, NY and Milford, PA

Approximately 90% of loans in Sussex, Orange & Pike Counties

Gross Loans ($M)

Commercial Portfolio* ($M)

* Commercial portfolio includes commercial and commercial real estate loans.

15

LOAN PORTFOLIO DYNAMICS SINCE 1999

TRANSFORMATION FROM THRIFT-LIKE BALANCE SHEET TO A MORE

COMMERCIAL FOCUS:

12/31/2000

06/30/2005

Gross Loans: $101.1 million

Gross Loans: $186.3 million

16

ASSET QUALITY

83% of our portfolio is secured by real estate

Asset quality is closely monitored by Officers Loan Committee, Directors Loan

Committee and Board of Directors

We use an independent consultant to review a sample of our portfolio quarterly

and verify our gradings

Charge-offs have remained low throughout our history

(1)

YTD for Sussex is the six months ended June 30, 2005;

YTD for the nationwide peers is the three months ended March 31, 2005

(2)

Includes all publicly traded banks nationwide with $200 million - $400 million in assets

17

FEE BASED BUSINESSES

31.1% of our revenues come from fee income businesses as compared to 14.8%

for our nationwide peer group**.

YTD Nationwide Bank Median** = 14.8%

**Includes all publicly traded banks nationwide with $200 million - $400 million in assets

YTD is the three months ended March 31, 2005

*2005 data is annualized

Fee Income ($000)

Fee Income / Revenue (%)

18

FEE BASED BUSINESSES

We have a diversified source of revenues uncommon of an institution of our size.

Fee income

31.1%

Net interest income

68.9%

Investment

Brokerage

Fees

5.4%

Deposit

Services & ATM

fees

29.7%

Insurance

Brokerage

50.2%

Mortgage

Broker Fees

6.6%

Revenue Composition (YTD)

Fee Revenue Composition (YTD)

Other

8.1%

Analysis excludes securities gains / losses

19

FINANCIAL PERFORMANCE

In December of 2004, we raised $15.2 million in net proceeds in a follow-on

common stock offering which doubled our capital.

We now have the necessary capital to grow and execute our strategic plan:

Organic growth

Expand our footprint in contiguous markets

Opportunistic acquisitions

Strategic hires

*Includes all publicly traded banks nationwide with $200 million - $400 million in assets

20

FINANCIAL PERFORMANCE

(1) Excluding amortization of intangibles, net of tax

21

EXPANDING THE FRANCHISE AND BUILDING SHAREHOLDER VALUE

Business plan with realistic and achievable goals:

$500 million assets

1% ROA

Demonstrated track record of success as a community bank:

Historic growth of 12% – 13% of loans and deposits

Investments in our infrastructure have been made and we have obtained the

necessary capital to support our strategic plan.

Existing and contiguous markets are ideal for expansion:

Densely populated and affluent with strong business climates

Customer dislocation as a result of bank consolidation

Management and Board interest aligned with shareholders:

Management and Board ownership – 17%

CEO ownership – 4%

22