Exhibit 99.1

2 FORWARD - LOOKING STATEMENT This confidential presentation, and the oral presentation that supplements it, have been developed by Sussex Bancorp (“Sussex” or the “Company”), were prepared exclusively for the benefit and internal use of the recipient and are not an offer or the solicitation of an offer to buy securities. Neither this presentation, nor the oral presentation that supplements it, nor any of their contents, may be used, reproduced, disseminated, quoted or referred to for any other purpose, in whole or in part, without the prior written consent of the Company. Some of the statements contained in this presentation are “forward - looking statements” within the meaning of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended. When used in this presentation, words such as “may,” “plan,” “contemplate,” “anticipate,” “believe,” “intend,” “continue,” “expect,” “project,” “predict,” “estimate,” “target,” “could,” “is likely,” “should,” “would,” “will,” or similar expressions are intended to identify “forward - looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995. You are cautioned not to place undue reliance on any forward - looking statements, which speak only as of the date made. These statements may relate to the Company’s future financial performance, strategic plans or objectives, revenue, expense or earnings projections, or other financial items. By their nature, these statements are subject to numerous uncertainties that could cause actual results to differ materially from those anticipated in the statements. Factors that could cause actual results to differ materially from the results anticipated or projected include, but are not limited to, the following: ( i ) competition in the industry and markets in which the Company operates; (ii) levels of non - performing assets; (iii) changes in general interest rates; (iv) loan demand; (v) rapid changes in technology affecting the financial services industry; (vi) real estate values; (vii) changes in government regulation; and (viii) general economic and business conditions.

3 Ticker Symbol SBBX Closing Price (Jan. 21, 2015) $10.25 Price to tangible book 98.7% Price to LTM EPS 18.0x Annualized Dividend/ Yield $0.16 / 1.56% 52 week high (12/8/14) $10.75 52 week low (2/4/14) $8.10 • Founded in 1975 • Commercial Bank » Operates an insurance agency • Total Assets of $596 million and 10 branches • Market Cap: $47.8 million • Regional Corporate Offices (Sussex and Morris Counties NJ) • Regional Lending Offices in Sussex, Bergen and Morris Counties NJ (new lending and branch office in Queens NYC - 1 st Qtr ‘ 15) Company Overview

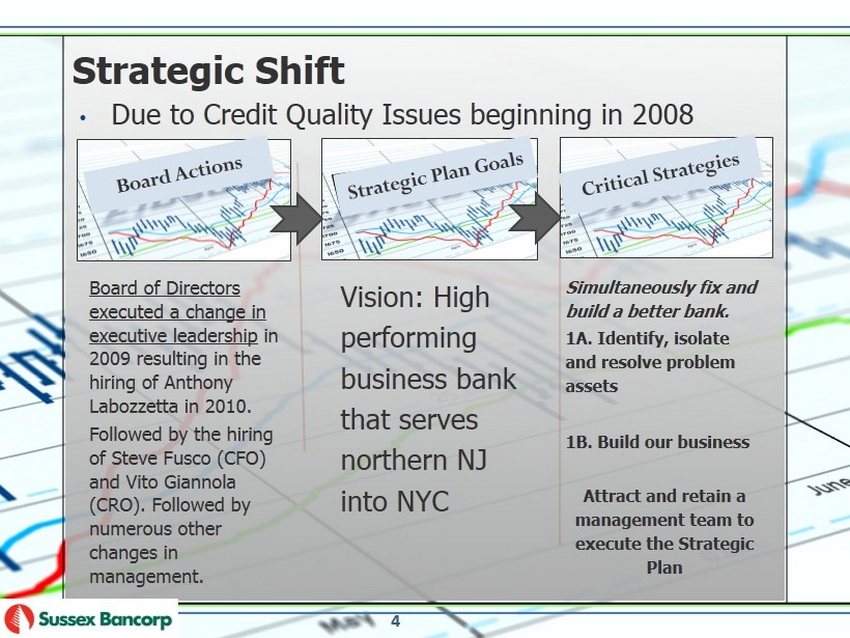

Strategic Shift • Due to Credit Quality Issues beginning in 2008 Board of Directors executed a change in executive leadership in 2009 resulting in the hiring of Anthony Labozzetta in 2010. Followed by the hiring of Steve Fusco (CFO) and Vito Giannola (CRO). Followed by numerous other changes in management. Simultaneously fix and build a better bank. 1A. Identify, isolate and resolve problem assets 1B. Build our business Attract and retain a management team to execute the Strategic Plan Vision : High performing business bank that serves northern NJ into NYC 4

SUSSEX BANCORP REPORTS A 54% INCREASE IN EPS DRIVEN BY COMMERCIAL LOAN GROWTH AND IMPROVED CREDIT QUALITY FOR FISCAL 2014 ROCKAWAY , NEW JERSEY – February 2, 2015 – Sussex Bancorp ( Nasdaq: SBBX), the holding company for Sussex Bank, today announced a 54.1% increase in net income per diluted common share for the year ended December 31, 2014, as compared to the same period last year. The improvement for 2014 was driven by strong growth in the commercial loan portfolio, which increased $76.1 million, or 26.9%, and a 49.3% decline in credit quality costs (provision for loan losses, loan collection costs and expenses and write - downs related to foreclosed real estate) as a result of improved credit quality as non - performing assets (excluding performing troubled debt restructured loans ) fell to 1.75% of total assets at December 31, 2014 from 2.80% at December 31, 2013. In addition, increased the quarterly dividend by 33%. 5

Vision: High performing business bank that serves northern NJ into NYC Target 2014 NJ Banks and Thrifts Avg (a) High Performing Peer Median (b) Total Assets > $1 billion in assets $596 million $2.4 billion (average) Med. $553 million $1.4 billion (average) Med. $1.0 million ROA 1.00% or better 0.46% 0.40% 1.10% ROE 8.00% to 12.00% 5.25% 3.2% 10.00% NPAs / Assets <1.25% 2.02% 2.49% 1.01% Annual EPS growth Double digit 54.1% N/A N/A (a) Source: SNL - NJ Banks and Thrifts (51) 9/30/14 (b) Source: SNL - High Performing Peers (Banks and Thrifts Assets < or = $5.5 bill and ROAA >0.75% at 9/30/14 6

1A. Identify , isolate and resolve problem assets 7 Source: SNL Financial • Reduced problem assets by $41 million, or 65% since March 31, 2010

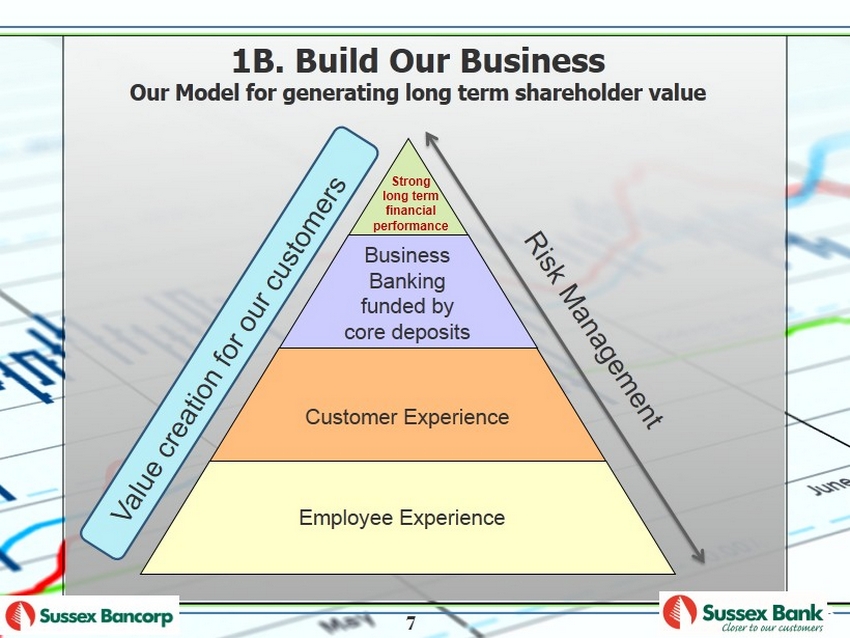

1B. Build Our Business Our Model for generating long term shareholder value Employee Experience Customer Experience Business Banking funded by core deposits Strong long term financial performance 8 7

Critical Strategy to build our business: Market extension outside Sussex County will be critical to accomplish our growth and profitability objectives 9 Sussex County, NJ • HHI (med): $86k • Population: 146k • Total Deposit Market Share: $2.5 b illion ( avg br. size $44 million) • # 2 market share (8 branches - avg $50 million) Bergen County, NJ • HHI (med): $80k • Population: 928k • Total Deposit Market Share: $41.6 billion (#1 in NJ) ( avg br. size $87 million) NYC • Density and strong markets • Branches of the top 10 banks based on NJ deposit market share (6/30/13) Sussex Bank branches

Commercial Lending • Originated over $236 million in new commercial loans in the last 2 years • Commercial loans grew 27% LTM and CAGR 20.2% for last 2 years • Approx. 69% of the loan portfolio were originated outside of Sussex County • Loan pipeline: principally Bergen , Morris and NYC Build our Business 10 $ in thousands

Our Commercial Loan Portfolio 11 • Commercial loans, ∆ Regional Commercial Lending Offices

Retail Banking • Total deposits are up 23% ( avg 4.6% per year) since Dec 31, 2009 • Significant improvement in quality of deposits (NIB checking accts are up 106% or 21% annually) • New branches for 2014 - 2015 • Heath Village, Morris County - September 2014 • Astoria, NYC - First Quarter 2015 Tri - state Insurance Agency • In 2010, operating at a loss and today reporting record profits • Represents 14% of our revenue Build our Business 12

• Total capital is 48% higher at December 31, 2014 than December 31, 2009, which reflects a successful rights offering in August 2013. All regulatory ratios are deemed “well - capitalized”. • Managing and controlling operating expenses (a) , which increased 4.2% (CAGR) for FY 2013 vs. FY 2009 • Closed an underperforming branch (Warwick NY) in 2013 • No fiscal year losses, while recording approximately $24 million in credit quality costs (b) during those 5 fiscal years (2009 through 2014) 13 (a) Excluding loan collection costs and net expenses and write - downs related to foreclosed real estate (b) Provision for loan losses, loan collection costs and net expenses and write - downs related to foreclosed real estate Capital and managing costs

• Net income (total FY 2006 thru 2009) $7.3 million • Costs to resolve problem loans (total FY 2010 thru 2014) $24 million, or $16 million after tax (tax rate of 34%) • Net income (total 2010 thru 2014) $9.4 million 14 Performance over the last 9 fiscal years

Banks with similar credit quality profiles as SBBX in 2010 15 Source: SNL Financial (Peer Group: PNBK, CARV, SVBI, IFSB, NMNB, PKBK, CMTB, RBPAA, PEBC, BRBW) - Total assets between $175 million and $825 million [Average $468 million]

Stock Performance 1/1/05 through 1/21/15 16 Total Return 1/1/05 – 12/31/09 1/1/10 – 1/21/15 1/1/05 – 1/21/15 SBBX - 74% +208% - 20% SNL US Bank Index - 48% +64% - 15% Need to update Source: SNL Financial

Regional Lending Platform Branch Expansion Attract and retain talent Manage operational growth and costs Opportunities for strategic alliances and growth Continue to grow shareholder value “we are building a better bank by growing our businesses, enhancing the quality of our balance sheet, improving profitability and building shareholder value .” Anthony Labozzetta (First Quarter 2014 Earnings Release) Where do we go from here? Continue “Building a better bank” 17

Growing shareholder value □ Expand into markets that support long - term growth objectives ▪ Continue growing commercial loans o Regional lending office(s) in NY o Attracting and retaining talent o Relationships , not just transactions ▪ Branch expansion o De - novo branch expansion into NYC o Identifying branch sites in Bergen, Morris, Hudson counties in NJ and NYC □ Target existing markets within Sussex County for deposit growth □ Digital banking o Enhancing the Customer Experience o Technology upgrades / new products o Develop a new branch operating model 18

□ Continue to strengthen profitability and build a high performing bank through: • Managing risks, • Operational efficiencies, • Growing fee income, largely through our insurance subsidiary, and expanding wealth management services • Significantly reducing credit quality costs □ Legacy Problem assets • Resolving top 5 non - performing loan relationships represents 59% of non - performing loans □ Outperform the total return of the broader market and bank indexes 19 Growing shareholder value