MANAGEMENT’S DISCUSSION AND ANALYSIS

This management’s discussion and analysis (“MD&A”) of ARC Resources Ltd. (“ARC” or the “Company”) is Management’s analysis of the financial performance and significant trends or external factors that may affect future performance. It is dated April 28, 2016 and should be read in conjunction with the unaudited condensed interim consolidated financial statements (the "financial statements") as at and for the three months ended March 31, 2016, and the MD&A and audited consolidated financial statements as at and for the year ended December 31, 2015, as well as ARC’s Annual Information Form that is filed on SEDAR at www.sedar.com. All financial information is reported in Canadian dollars and all per share information is based on diluted weighted average shares, unless otherwise noted.

This MD&A contains non-GAAP measures and forward-looking statements. Readers are cautioned that the MD&A should be read in conjunction with ARC’s disclosure under the headings “Non-GAAP Measures,” “Forward-looking Information and Statements,” and "Glossary" included at the end of this MD&A.

ABOUT ARC RESOURCES LTD.

ARC is a dividend-paying Canadian crude oil and natural gas company headquartered in Calgary, Alberta. ARC’s activities relate to the exploration, development and production of conventional crude oil and natural gas in Canada with an emphasis on the development of properties with a large volume of hydrocarbons in place commonly referred to as “resource plays.”

ARC’s vision is to be a leading energy producer, focused on delivering results through its strategy of risk-managed value creation. ARC is committed to providing superior long-term financial returns for its shareholders, creating a culture where respect for the individual is paramount and action and passion are rewarded. ARC runs its business in a manner that protects the safety of employees, communities and the environment. ARC’s vision is realized through the four pillars of its strategy:

| |

| (1) | High quality, long-life assets – ARC’s unique suite of assets includes both Montney and other assets. ARC’s Montney assets consist of world-class resource play properties, concentrated in the Montney geological formation in northeast British Columbia and northern Alberta. The Montney assets provide substantial growth opportunities, which ARC will pursue to create value through long-term profitable development. Other assets are located in Alberta and Saskatchewan and include core assets in the Cardium formation in the Pembina area of Alberta. These assets deliver stable production and contribute cash flow to fund future development and support ARC's dividend. |

| |

| (2) | Operational excellence – ARC is focused on capital discipline and cost management to extract the maximum return on its investments while operating in a safe and environmentally responsible manner. Production from individual crude oil and natural gas wells naturally declines over time. In any one year, ARC approves a budget to drill new wells with the intent to first replace production declines and second to potentially increase production volumes and profitability. At times, ARC may also acquire strategic producing or undeveloped properties to enhance current production and reserves or to provide potential future drilling locations. Alternatively, it may strategically dispose of non-core assets that no longer meet its investment criteria. |

| |

| (3) | Financial flexibility – ARC provides returns to shareholders through a combination of a monthly dividend, currently $0.05 per share outstanding per month, and the potential for capital appreciation. ARC’s long-term goal is to fund dividend payments and capital expenditures necessary for the replacement of production declines using funds from operations (1). ARC will finance value-creating activities through a combination of sources including funds from operations, proceeds from ARC’s Dividend Reinvestment Program (“DRIP”), reduced funding required under the Stock Dividend Program ("SDP"), proceeds from property dispositions, debt capacity, and when appropriate, equity issuance. ARC chooses to maintain prudent debt levels, targeting a maximum net debt to annualized funds from operations of less than two times during specific periods with a long-term target for net debt to be one to 1.5 times annualized funds from operations and less than 20 per cent of total capitalization over the long-term (1). |

| |

| (4) | Top talent and strong leadership culture – ARC is committed to the attraction, retention and development of the best and brightest people in the industry. ARC’s employees conduct business every day in a culture of trust, respect, integrity and accountability. Building leadership talent at all levels of the organization is a key focus. ARC is also committed to corporate leadership through community investment, environmental reporting practices and open communication with all stakeholders. As of April 28, 2016, ARC had 492 employees with 263 professional, technical and support staff in the Calgary office, and 229 individuals located across ARC’s operating areas in western Canada. |

| |

| (1) | Refer to Note 8 "Capital Management" in the financial statements as at and for the three months ended March 31, 2016 and to the sections entitled "Funds from Operations" and "Capitalization, Financial Resources and Liquidity" contained within this MD&A. |

Total Return to Shareholders

ARC's business plan has resulted in significant operational success and helped mitigate the headwinds of a challenging commodity price environment, resulting in a trailing five year annualized total return that exceeds the Standard & Poor's ("S&P")/Toronto Stock Exchange ("TSX") Exploration & Producers Index (Table 1).

Table 1 |

| | | | | | |

Total Returns (1) | Trailing One Year |

| Trailing Three Year |

| Trailing Five Year |

|

| Dividends per share outstanding ($) | 1.10 |

| 3.50 |

| 5.90 |

|

| Capital appreciation (depreciation) per share outstanding ($) | (2.87 | ) | (7.95 | ) | (7.46 | ) |

| Total return per share outstanding (%) | (8.2 | ) | (18.8 | ) | (8.7 | ) |

| Annualized total return per share outstanding (%) | (8.2 | ) | (6.7 | ) | (1.8 | ) |

| S&P/TSX Exploration & Producers Index annualized total return (%) | (22.5 | ) | (13.4 | ) | (14.3 | ) |

| |

| (1) | Non-GAAP measure which may not be comparable to similar non-GAAP measures used by other entities. Refer to the section entitled "Non-GAAP Measures" contained within this MD&A. Calculated as at March 31, 2016. |

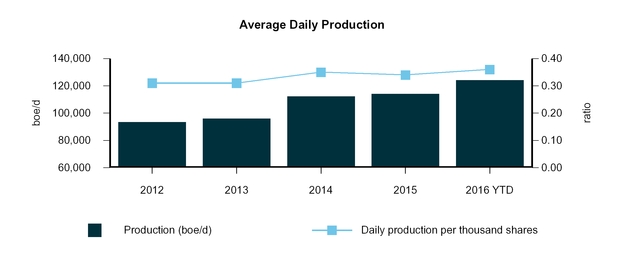

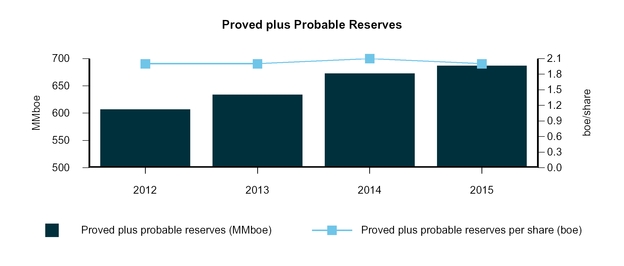

Since 2012, ARC’s production has grown by 30,678 boe per day, or 33 per cent, while its proved plus probable reserves have grown by 79.9 MMboe, or 13 per cent. Table 2 highlights ARC’s production and reserves for the first three months of 2016 and over the past four years:

Table 2 |

| | | | | | | | | | |

| | 2016 YTD |

| 2015 |

| 2014 |

| 2013 |

| 2012 |

|

Production (boe/d) (1) | 124,224 |

| 114,167 |

| 112,387 |

| 96,087 |

| 93,546 |

|

Daily production per thousand shares (2) | 0.36 |

| 0.34 |

| 0.35 |

| 0.31 |

| 0.31 |

|

Proved plus probable reserves (MMboe) (3)(4) | n/a |

| 686.9 |

| 672.7 |

| 633.9 |

| 607.0 |

|

| Proved plus probable reserves per share (boe) | n/a |

| 2.0 |

| 2.1 |

| 2.0 |

| 2.0 |

|

| |

| (1) | Reported production amount is based on company interest before royalty burdens. |

| |

| (2) | Daily production per thousand shares represents average daily production for the three months ended March 31, 2016 and annual average daily production for the full years ended December 31, 2015, 2014, 2013 and 2012 divided by the diluted weighted average common shares for the respective periods. |

| |

| (3) | As determined by ARC’s independent reserve evaluator with an effective date of December 31 for the years shown in accordance with the COGE Handbook. |

| |

| (4) | Company gross reserves are the gross interest reserves before deduction of royalties and without including any royalty interests. For more information, see ARC’s Annual Information Form as filed on SEDAR at www.sedar.com and the news release entitled “ARC Resources Ltd. Announces the 8th Consecutive Year of ~200% Reserves Replacement, 2015 Finding and Development Costs for 2P Reserves of $6.97 and a Significant Increase in Montney Resource Estimates in 2015” dated February 10, 2016. |

Exhibit 1

Exhibit 1a

ECONOMIC ENVIRONMENT

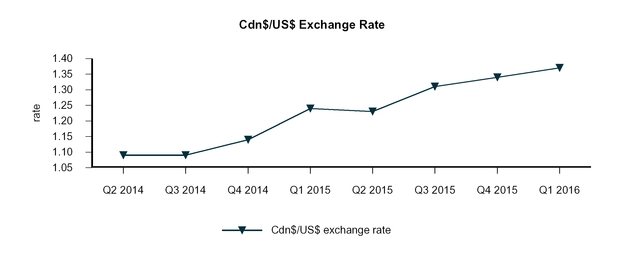

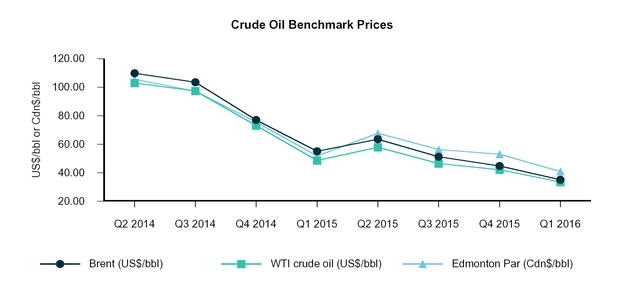

ARC’s first quarter 2016 financial and operating results were impacted by commodity prices and foreign exchange rates which are outlined in Table 3 below:

Table 3 |

| | | | | | |

Selected Benchmark Prices and Exchange Rates (1) | Three Months Ended |

| | March 31 |

| | 2016 |

| 2015 |

| % Change |

|

| Brent (US$/bbl) | 35.21 |

| 55.11 |

| (36 | ) |

| WTI crude oil (US$/bbl) | 33.63 |

| 48.57 |

| (31 | ) |

| Edmonton Par (Cdn$/bbl) | 40.90 |

| 51.85 |

| (21 | ) |

| NYMEX Henry Hub (US$/MMbtu) | 2.09 |

| 2.98 |

| (30 | ) |

| AECO natural gas (Cdn$/Mcf) | 2.11 |

| 2.95 |

| (28 | ) |

| Cdn$/US$ exchange rate | 1.37 |

| 1.24 |

| 10 |

|

| |

| (1) | The benchmark prices do not reflect ARC's realized sales prices. For average realized sales prices, refer to Table 13 in this MD&A. Prices and exchange rates presented above represent averages for the respective periods. |

Global crude oil prices continued to decline at the onset of the first quarter of 2016 as market oversupply remained a concern, with inventories showing no real signs of contraction and as new Iranian production entered the market. As the quarter progressed, crude oil prices experienced a modest rebound, as data signaled that US crude oil production volumes were declining. In the first quarter of 2016, the WTI benchmark price averaged 20 per cent lower than the fourth quarter of 2015 and 31 per cent lower than the first quarter of 2015. ARC's crude oil price is primarily referenced to the Edmonton Par benchmark price, which decreased 23 per cent compared to the fourth quarter of 2015, and 21 per cent compared to the first quarter of 2015. The differential between WTI and Edmonton Par widened in the first quarter of 2016 to average a discount of US$3.84, 52 per cent greater than the fourth quarter of 2015 and 43 per cent lower than the first quarter of 2015.

Exhibit 2

North American natural gas prices, referenced by the average NYMEX Henry Hub price, decreased eight per cent relative to the fourth quarter of 2015 and 30 per cent compared to the first quarter of 2015. ARC's realized natural gas price is primarily referenced to the AECO hub, which was 20 per cent lower in the first quarter of 2016 compared to the fourth quarter of 2015 and 28 per cent lower compared to the first quarter of 2015. The deterioration of natural gas prices was largely the result of significantly warmer continental weather through the winter months, which reduced normal seasonal residential and commercial demand. As a result, North American storage levels were at record highs entering the injection season. The muted winter heating demand was partially offset by strong natural gas power-generation demand in the US and a continued increase in exports to Mexico. Near-term uncertainty with demand and storage surpluses is expected to result in continued downward pressure on natural gas prices through the summer months.

Subsequent to March 31, 2016, AECO natural gas prices have continued to deteriorate. Oversupply continues to be a concern as Canadian inventories remain high.

Exhibit 2a

The Canadian dollar remained weak relative to the US dollar during the first quarter of 2016 averaging US$0.73 (Cdn$/US$1.37). As the US Federal Reserve tempered expectations of an interest rate increase in the United States, the Canadian dollar ended the quarter in a relatively stronger position.

Exhibit 2b

ANNUAL GUIDANCE AND FINANCIAL HIGHLIGHTS

ARC's Board of Directors has approved a $390 million capital program for 2016 that focuses on balance sheet strength and long-term value creation through continued development of ARC's low-cost, high-value northeast British Columbia Montney assets. ARC expects to spend approximately 75 per cent of the 2016 capital budget in northeast British Columbia. The budget will allow ARC to operate facilities at capacity at Dawson, Sunrise and Parkland/Tower, while advancing key strategic projects at Dawson and Attachie. Full-year 2016 annual average production is expected to be in the range of 116,000 to 120,000 boe per day, resulting in modest year-over-year growth.

Ongoing commodity price volatility may affect ARC's funds from operations and profitability on capital programs. As continued volatility is expected, ARC will continue to take steps to mitigate these risks, focus on capital discipline and cost control, and protect its strong financial position. ARC will continue to screen projects for profitability in a disciplined manner and will adjust spending and the pace of development, if required, to ensure balance sheet strength is protected.

Table 4 is a summary of ARC’s 2016 annual guidance and a review of 2016 year-to-date actual results.

Table 4

|

| | | | | | |

| | 2016

Guidance |

2016 YTD | % Variance from Guidance |

|

| Production | | | |

| Crude oil (bbl/d) | 32,000 - 34,000 |

| 34,852 |

| 3 |

|

| Condensate (bbl/d) | 3,000 - 3,400 |

| 3,442 |

| 1 |

|

| Natural gas (MMcf/d) | 460 - 470 |

| 489.7 |

| 4 |

|

| NGLs (bbl/d) | 3,800 - 4,200 |

| 4,319 |

| 3 |

|

| Total (boe/d) | 116,000 - 120,000 |

| 124,224 |

| 4 |

|

| Expenses ($/boe) | | | |

| Operating | 7.40 - 7.80 |

| 6.10 |

| (18 | ) |

| Transportation | 2.40 - 2.70 |

| 2.20 |

| (8 | ) |

| G&A expenses before share-based compensation plans | 1.55 - 1.65 |

| 1.93 |

| 17 |

|

G&A - share-based compensation plans (1) | 0.45 - 0.65 |

| 0.88 |

| 35 |

|

| Interest | 1.10 - 1.30 |

| 1.16 |

| — |

|

Current income tax (per cent of funds from operations) (2) | 0 - 5 |

| — |

| — |

|

| Capital expenditures before land purchases and net property acquisitions (dispositions) ($ millions) | 390 |

| 59.1 |

| N/A |

|

| Land purchases and net property acquisitions (dispositions) ($ millions) | — |

| 15.1 |

| N/A |

|

| Weighted average shares, diluted (millions) | 351 |

| 349 |

| N/A |

|

| |

| (1) | Comprises expenses recognized under the RSU and PSU, Share Option and LTRSA Plans. In periods where substantial share price fluctuation occurs, ARC’s G&A expenses are subject to greater volatility. |

| |

| (2) | The 2016 corporate tax estimate varies depending on the level of commodity prices. |

ARC's 2016 guidance is based on full-year 2016 estimates; certain variances between first quarter 2016 actual results and 2016 full-year guidance estimates were due to the cyclical and seasonal nature of operations. ARC expects full-year 2016 actual results to closely approximate guidance as the year progresses. First quarter 2016 production was above the 2016 guided production range as a result of strong performance at ARC's northeast British Columbia Montney properties and uplift from optimization activities conducted throughout the quarter; ARC expects that full-year 2016 production will closely approximate the guided range as production is expected to trend downwards over the course of the year with limited capital activity planned for certain areas of ARC's portfolio.

Exhibit 3

2016 Production Guidance

On a per boe basis, ARC's first quarter 2016 operating expenses were below the 2016 guidance range due the addition of new Montney production at lower relative costs to operate, lower power prices throughout the period, and diligent cost control efforts. On a per boe basis, ARC's first quarter 2016 transportation expenses were below the 2016 guidance range as a result of minimal pipeline disruptions in the quarter; ARC expects full-year 2016 actual transportation expenses to closely approximate guidance as the year progresses. ARC's first quarter 2016 G&A expenses were above the 2016 guidance range due primarily to lower capitalized G&A as a result of lower capital expenditures, increased costs associated with ARC's share-based compensation plans due to the increase in ARC's share price and improved total return relative to its peers at March 31, 2016, as well as severance costs associated with reducing the size of ARC's workforce; ARC expects full-year 2016 G&A expenses before share-based compensation to closely approximate guidance as the year progresses. ARC expects to record a current tax recovery due to an estimated tax loss for 2016 related to decreased commodity prices.

Exhibit 3a

2016 Expenses Guidance

The guidance information presented is intended to provide shareholders with information on Management’s expectations for results from operations. Readers are cautioned that the guidance may not be appropriate for other purposes.

2016 FIRST QUARTER FINANCIAL AND OPERATING RESULTS

Financial Highlights

Table 5 |

| | | | | | |

| | Three Months Ended |

| | March 31 |

| ($ millions, except per share and volume data) | 2016 |

| 2015 |

| % Change |

|

Funds from operations (1) | 150.1 |

| 191.5 |

| (22 | ) |

Funds from operations per share (1) | 0.43 |

| 0.57 |

| (25 | ) |

| Net income (loss) | 64.1 |

| (1.7 | ) | 100 |

|

| Net income (loss) per share | 0.18 |

| (0.01 | ) | 100 |

|

Dividends per share (2) | 0.20 |

| 0.30 |

| (33 | ) |

| Average daily production (boe/d) | 124,224 |

| 120,354 |

| 3 |

|

| |

| (1) | Refer to Note 8 "Capital Management" in the financial statements as at and for the three months ended March 31, 2016 and to the section entitled "Funds from Operations" contained within this MD&A. |

| |

| (2) | Dividends per share are based on the number of shares outstanding at each dividend record date. |

Funds from Operations

ARC considers funds from operations to be a key measure of operating performance as it demonstrates ARC’s ability to generate the necessary funds to fund future growth through capital investment and to repay debt. Management believes that such a measure provides an insightful assessment of ARC’s operations on a continuing basis by eliminating certain non-cash charges and charges that are nonrecurring.

ARC reports funds from operations in total and on a per share basis. Refer to Note 8 "Capital Management" in the financial statements as at and for the three months ended March 31, 2016. Table 6 is a reconciliation of ARC’s net income (loss) to funds from operations and cash flow from operating activities:

Table 6 |

| | | | |

| | Three Months Ended |

| | March 31 |

| ($ millions) | 2016 |

| 2015 |

|

| Net income (loss) | 64.1 |

| (1.7 | ) |

| Adjusted for the following non-cash items: | | |

| DD&A and impairment | 134.2 |

| 178.7 |

|

| Accretion of ARO | 3.1 |

| 3.6 |

|

| E&E expenses | 1.7 |

| — |

|

| Deferred tax expense | 6.5 |

| 13.0 |

|

| Unrealized loss (gain) on risk management contracts | 7.2 |

| (77.7 | ) |

| Unrealized loss (gain) on foreign exchange | (67.4 | ) | 88.3 |

|

| Loss (gain) on disposal of petroleum and natural gas properties | — |

| (12.7 | ) |

| Other | 0.7 |

| — |

|

| Funds from operations | 150.1 |

| 191.5 |

|

| Net change in other liabilities | (1.1 | ) | (11.6 | ) |

| Change in non-cash working capital | 3.7 |

| (34.2 | ) |

| Cash flow from operating activities | 152.7 |

| 145.7 |

|

Details of the change in funds from operations from the three months ended March 31, 2015 to the three months ended March 31, 2016 are included in Table 7 below:

Table 7 |

| | | | |

| | Three Months Ended |

| | March 31 |

| | $ millions |

| $/Share |

|

| Funds from operations – 2015 | 191.5 |

| 0.57 |

|

| Volume variance | | |

| Crude oil and liquids | (3.1 | ) | (0.01 | ) |

| Natural gas | 9.8 |

| 0.03 |

|

| Price variance | | |

| Crude oil and liquids | (37.2 | ) | (0.11 | ) |

| Natural gas | (44.4 | ) | (0.13 | ) |

| Other Revenue | (0.5 | ) | — |

|

| Realized gain on risk management contracts | 23.7 |

| 0.07 |

|

| Royalties | 12.1 |

| 0.03 |

|

| Expenses (recoveries) | | |

| Transportation | 0.8 |

| — |

|

| Operating | 9.4 |

| 0.03 |

|

| G&A | (20.9 | ) | (0.06 | ) |

| Interest | (0.2 | ) | — |

|

| Current tax | 9.3 |

| 0.03 |

|

| Realized loss on foreign exchange | (0.2 | ) | — |

|

| Diluted shares | — |

| (0.02 | ) |

| Funds from operations – 2016 | 150.1 |

| 0.43 |

|

Funds from operations decreased by 22 per cent in the first quarter of 2016 to $150.1 million from $191.5 million generated in the first quarter of 2015. The decrease reflects lower revenue due primarily to significantly lower realized commodity prices, reduced crude oil and liquids production, and an increase in G&A in the first quarter of 2016 as compared to the first quarter of 2015. Increased natural gas production and realized gains on risk management contracts relative to the first quarter of the prior year along with lower royalties, operating costs and current taxes partially offset the impact of the reduction in commodity prices.

Exhibit 4

2016 Funds from Operations Sensitivity

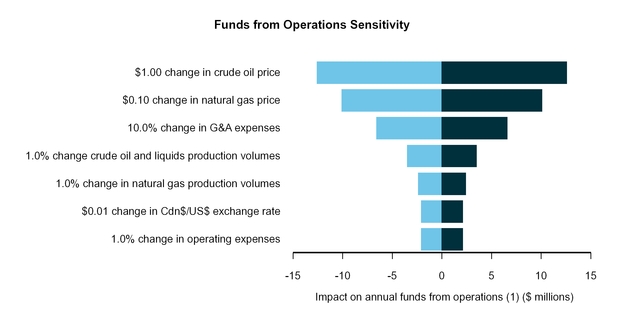

Table 8 illustrates sensitivities of pre-hedged operating items to operational and business environment changes and the resulting impact on funds from operations per share:

Table 8 |

| | | | | |

| | Impact on Annual Funds from Operations (6) |

|

| | Assumption | Change |

| $/Share |

|

Business Environment (1) | | | |

Crude oil price (US$ WTI/bbl) (2)(3) | 33.63 | 1.00 |

| 0.036 |

|

Natural gas price (Cdn$ AECO/Mcf) (2)(3) | 2.11 | 0.10 |

| 0.029 |

|

Cdn$/US$ exchange rate (2)(3)(4) | 1.37 | 0.01 |

| 0.006 |

|

Operational (5) | | | |

| Crude oil and liquids production volumes (bbl/d) | 42,613 | 1.0 | % | 0.010 |

|

| Natural gas production volumes (MMcf/d) | 489.7 | 1.0 | % | 0.007 |

|

| Operating expenses ($/boe) | 6.10 | 1.0 | % | 0.006 |

|

| G&A expenses ($/boe) | 2.81 | 10.0 | % | 0.019 |

|

| |

| (1) | Calculations are performed independently and may not be indicative of actual results that would occur when multiple variables change at the same time. |

| |

| (2) | Prices and rates are indicative of published prices for the first quarter of 2016. See Table 13 of this MD&A for additional details. The calculated impact on funds from operations would only be applicable within a limited range of these amounts. |

| |

| (3) | Analysis does not include the effect of risk management contracts. |

| |

| (4) | Includes impact of foreign exchange on crude oil, condensate, and NGLs prices that are presented in US dollars. |

| |

| (5) | Operational assumptions are based upon results for the three months ended March 31, 2016. |

| |

| (6) | Refer to Note 8 "Capital Management" in the financial statements as at and for the three months ended March 31, 2016 and to the section entitled "Funds from Operations" contained within this MD&A. |

Exhibit 5

| |

| (1) | Refer to Note 8 "Capital Management" in the financial statements as at and for the three months ended March 31, 2016 and to the section entitled "Funds from Operations" contained within this MD&A. |

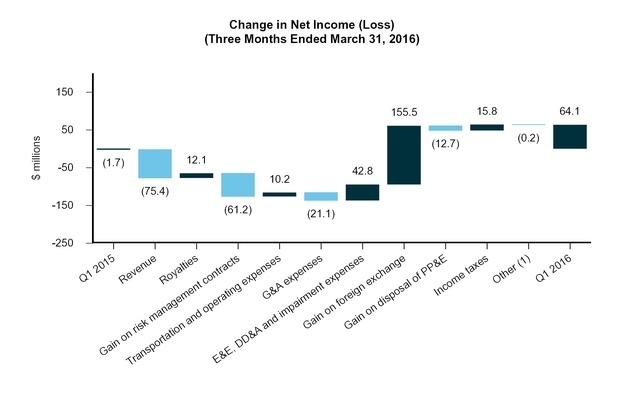

Net Income (Loss)

Net income of $64.1 million ($0.18 per share) was incurred in the first quarter of 2016, a $65.8 million ($0.19 per share) increase compared to a net loss of $1.7 million (loss of $0.01 per share) in the first quarter of 2015. Lower transportation and operating expenses, reduced DD&A and impairment charges, higher foreign exchange gains and a higher income tax recovery increased net income, while lower revenue net of royalties, decreased gains on risk management contracts, higher G&A expenses and lower gains on disposal of petroleum and natural gas properties served to partially offset the increase.

Exhibit 6

| |

| (1) | Includes gain or loss on short-term investments, accretion on ARO, and interest and financing charges. |

Production

Table 9 |

| | | | | | |

| | Three Months Ended |

| | March 31 |

| Production | 2016 |

| 2015 |

| % Change |

|

| Light and medium crude oil (bbl/d) | 34,367 |

| 34,740 |

| (1 | ) |

| Heavy crude oil (bbl/d) | 485 |

| 1,111 |

| (56 | ) |

| Condensate (bbl/d) | 3,442 |

| 3,591 |

| (4 | ) |

| Natural gas (MMcf/d) | 489.7 |

| 459.6 |

| 7 |

|

| NGLs (bbl/d) | 4,319 |

| 4,314 |

| — |

|

| Total production (boe/d) | 124,224 |

| 120,354 |

| 3 |

|

| % Natural gas production | 66 |

| 64 |

| 3 |

|

| % Crude oil and liquids production | 34 |

| 36 |

| (6 | ) |

During the three months ended March 31, 2016, crude oil and liquids production decreased three per cent from the first quarter of the prior year. The decrease in crude oil and liquids production primarily reflects natural declines associated with reduced drilling activity and the disposition of certain non-core assets in southwest Saskatchewan in the third quarter of 2015 and in Manitoba in the fourth quarter of 2015 which had been producing approximately 500 boe per day and 1,300 boe per day prior to disposal, respectively. The decrease was partially offset by additional production at Tower following the crude oil battery expansion that was completed during the fourth quarter of 2015.

Natural gas production was 489.7 MMcf per day in the first quarter of 2016, an increase of seven per cent from the 459.6 MMcf per day produced in the first quarter of 2015. The increase is mainly attributed to new production from drilling throughout 2015 in northeast British Columbia, particularly at Sunrise to fill ARC's 60 MMcf per day natural gas processing facility which was commissioned during the third quarter of 2015. The increase in natural gas production was partially offset by the disposition of certain non-core assets in South Central Alberta in the second quarter of 2015 which had been producing approximately 14.4 MMcf per day prior to disposal.

Exhibit 7

During the first quarter of 2016, ARC drilled eight gross wells (eight net wells) on operated properties consisting of five gross (five net) natural gas wells, two gross (two net) liquids-rich natural gas wells, and one gross (one net) service well. Table 10 summarizes ARC’s production by core area for the first quarter of 2016 and 2015:

Table 10

|

| | | | | | | | | | |

| | Three Months Ended March 31, 2016 |

| Production | Total |

| Crude Oil |

| Condensate |

| Natural Gas |

| NGLs |

|

Core Area (1) | (boe/d) |

| (bbl/d) |

| (bbl/d) |

| (MMcf/d) |

| (bbl/d) |

|

| Northeast BC | 80,906 |

| 9,207 |

| 2,547 |

| 401.5 |

| 2,231 |

|

| Northern AB | 20,416 |

| 7,135 |

| 628 |

| 67.7 |

| 1,375 |

|

| Pembina | 10,035 |

| 7,122 |

| 192 |

| 13.5 |

| 477 |

|

South Central AB (2) | 4,776 |

| 3,583 |

| 20 |

| 6.0 |

| 165 |

|

Southeast SK (3) | 8,091 |

| 7,805 |

| 55 |

| 1.0 |

| 71 |

|

| Total | 124,224 |

| 34,852 |

| 3,442 |

| 489.7 |

| 4,319 |

|

|

| | | | | | | | | | |

| | Three Months Ended March 31, 2015 |

| Production | Total |

| Crude Oil |

| Condensate |

| Natural Gas |

| NGLs |

|

Core Area (1) | (boe/d) |

| (bbl/d) |

| (bbl/d) |

| (MMcf/d) |

| (bbl/d) |

|

| Northeast BC | 66,581 |

| 3,155 |

| 2,609 |

| 353.2 |

| 1,947 |

|

| Northern AB | 22,323 |

| 8,405 |

| 692 |

| 70.0 |

| 1,561 |

|

| Pembina | 12,167 |

| 9,295 |

| 180 |

| 13.2 |

| 490 |

|

South Central AB (2) | 8,437 |

| 4,451 |

| 63 |

| 22.1 |

| 242 |

|

Southeast SK & MB (3) | 10,846 |

| 10,545 |

| 47 |

| 1.1 |

| 74 |

|

| Total | 120,354 |

| 35,851 |

| 3,591 |

| 459.6 |

| 4,314 |

|

| |

| (1) | Provincial references: "AB" is Alberta, "BC" is British Columbia, "SK" is Saskatchewan, "MB" is Manitoba. |

| |

| (2) | During the second quarter of 2015, ARC disposed of certain non-core assets in this district. These assets that had been producing approximately 2,400 boe per day prior to disposal. An additional 500 boe per day of non-core assets were disposed from this district toward the end of the third quarter of 2015. |

| |

| (3) | During the fourth quarter of 2015, ARC disposed of certain non-core assets in this district that had been producing approximately 1,300 boe per day prior to disposal. |

Exhibit 8

Sales of Crude Oil, Natural Gas, Condensate, NGLs and Other Income

Sales revenue from crude oil, natural gas, condensate, NGLs and other income decreased by 25 per cent in the first quarter of 2016 compared to the same period in 2015. The decrease reflects lower average realized commodity prices for all products in the first quarter of 2016 compared to the first quarter of 2015 and was partially offset by increased natural gas production volumes.

A breakdown of sales revenue by product is outlined in Table 11:

Table 11 |

| | | | | | |

| | Three Months Ended |

| | March 31 |

Sales revenue by product ($ millions) | 2016 |

| 2015 |

| % Change |

|

| Crude oil | 122.5 |

| 157.2 |

| (22 | ) |

| Condensate | 13.2 |

| 15.9 |

| (17 | ) |

| Natural gas | 91.5 |

| 126.1 |

| (27 | ) |

| NGLs | 3.3 |

| 6.2 |

| (47 | ) |

| Total sales revenue from crude oil, natural gas, condensate and NGLs | 230.5 |

| 305.4 |

| (25 | ) |

| Other income | 0.7 |

| 1.2 |

| (42 | ) |

| Total sales revenue | 231.2 |

| 306.6 |

| (25 | ) |

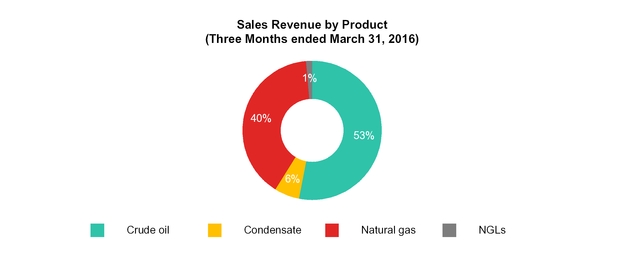

While ARC’s production mix on a per boe basis is weighted more heavily to natural gas than to crude oil and liquids, ARC's revenue contribution is more heavily weighted to crude oil and liquids production as shown by the table below:

Table 12

|

| | |

| | Three Months Ended |

| | March 31 |

| Revenue by Product Type | 2016 | 2015 |

| | % of Total Revenue | % of Total Revenue |

| Crude oil and liquids | 60 | 59 |

| Natural gas | 40 | 41 |

| Total sales revenue | 100 | 100 |

Exhibit 9

Commodity Prices Prior to Hedging

Table 13 |

| | | | | | |

| | Three Months Ended |

| | March 31 |

| | 2016 |

| 2015 |

| % Change |

|

| Average Benchmark Prices | | | |

| AECO natural gas (Cdn$/Mcf) | 2.11 |

| 2.95 |

| (28 | ) |

| WTI crude oil (US$/bbl) | 33.63 |

| 48.57 |

| (31 | ) |

| Cdn$/US$ exchange rate | 1.37 |

| 1.24 |

| 10 |

|

| WTI crude oil (Cdn$/bbl) | 46.07 |

| 60.23 |

| (24 | ) |

| Edmonton Par (Cdn$/bbl) | 40.90 |

| 51.85 |

| (21 | ) |

| ARC Average Realized Prices Prior to Hedging | | | |

| Crude oil ($/bbl) | 38.64 |

| 48.73 |

| (21 | ) |

| Condensate ($/bbl) | 42.07 |

| 49.12 |

| (14 | ) |

| Natural gas ($/Mcf) | 2.05 |

| 3.05 |

| (33 | ) |

| NGLs ($/bbl) | 8.42 |

| 16.07 |

| (48 | ) |

| Total average realized commodity price prior to other income and hedging ($/boe) | 20.39 |

| 28.20 |

| (28 | ) |

| Other income ($/boe) | 0.06 |

| 0.11 |

| (45 | ) |

| Total average realized price prior to hedging ($/boe) | 20.45 |

| 28.31 |

| (28 | ) |

In the first quarter of 2016, WTI decreased 31 per cent to US$33.63 per barrel as compared to US$48.57 per barrel in the same period in 2015. Similarly, ARC’s realized crude oil price decreased by 21 per cent over the same time period, averaging $38.64 per barrel. During the first quarter of 2016, the differential between WTI and Edmonton posted prices narrowed to an average discount of US$3.84 per barrel compared to US$6.76 per barrel in the same period in 2015. During the same period, the average exchange rate for the Canadian dollar as compared to the US dollar weakened from $1.24 to $1.37. The narrowing of the differential combined with a weaker Canadian dollar served to partially mitigate the overall impact of the decrease in WTI on ARC's average realized prices.

ARC's realized natural gas price decreased by 33 per cent during the first quarter of 2016 as compared to the same period in 2015, averaging $2.05 per Mcf. ARC's realized natural gas price is primarily benchmarked against the AECO monthly index, which was 28 per cent lower compared to the first quarter of 2015. ARC's realized natural gas price has declined more than the AECO monthly index in the first quarter of 2016 due to a portion of ARC's production being sold at the AECO daily index which settled significantly lower than the AECO monthly index during the first quarter of 2016.

Risk Management

ARC maintains a risk management program to reduce the volatility of revenues, increase the certainty of funds from operations, and to protect acquisition and development economics. ARC’s risk management program is governed by certain guidelines approved by the Board of Directors (the "Board"). These guidelines currently restrict risk management contracts to a maximum of 55 per cent of total forecast production where a specific commodity (crude oil or natural gas) cannot exceed a maximum of 70 per cent of forecast production for that commodity over the next two years, and with a maximum of 25 per cent of forecast natural gas production in risk management contracts beyond two years and up to five years. ARC’s risk management program guidelines allow for further risk management contracts on anticipated volumes associated with new production arising from specific capital projects and acquisitions or to further protect cash flows for a specific period with approval of the Board.

Gains and losses on risk management contracts are composed of both realized gains and losses, representing the portion of risk management contracts that have settled in cash during the period, and unrealized gains or losses that represent the change in the mark-to-market position of those contracts throughout the period. ARC does not employ hedge accounting for any of its risk management contracts currently in place. ARC considers all of its risk management contracts to be effective economic hedges of its underlying business transactions.

Table 14 summarizes the total gain or loss on risk management contracts for the first quarter of 2016 compared to the same period in 2015:

Table 14

|

| | | | | | | | | | |

Risk Management Contracts ($ millions) | Crude Oil & Liquids |

| Natural Gas |

| Power |

| Q1 2016 Total |

| Q1 2015 Total |

|

Realized gain (loss) on contracts (1) | 26.0 |

| 42.9 |

| (0.6 | ) | 68.3 |

| 44.6 |

|

Unrealized gain (loss) on contracts (2) | (9.1 | ) | 1.8 |

| 0.1 |

| (7.2 | ) | 77.7 |

|

| Gain (loss) on risk management contracts | 16.9 |

| 44.7 |

| (0.5 | ) | 61.1 |

| 122.3 |

|

| |

| (1) | Represents actual cash settlements under the respective contracts. |

| |

| (2) | Represents the change in fair value of the contracts during the period. |

During the three months ended March 31, 2016, ARC recorded gains of $61.1 million on its risk management contracts comprising realized gains of $68.3 million and unrealized losses of $7.2 million. The realized gains reflect positive cash settlements received on crude oil swaps with an average price of $77.20 and crude oil collars with a floor of $70.00, on Henry Hub natural gas contracts with an average floor price of US$4.00/MMbtu, on AECO basis swaps at an average ratio of 90.3 per cent and on AECO natural gas swaps with an average price of $2.99/GJ. These realized gains are partially offset by realized losses on power contracts of $0.6 million.

ARC's first quarter 2016 unrealized losses on crude oil contracts are as a result of settled positions, partially offset by a decrease in the forward curve. During the same period, net unrealized gains on natural gas contracts reflected a lower forward curve for NYMEX Henry Hub and AECO prices as well as a wider AECO basis, offset by closed positions.

ARC’s risk management contracts provide protection from natural gas prices for 2016 to 2020 and for crude oil for 2016 and 2017. Table 15 summarizes ARC’s average crude oil and natural gas hedged volumes as at the date of this MD&A. For a complete listing and terms of ARC’s risk management contracts at March 31, 2016, see Note 9 “Financial Instruments and Market Risk Management” in the financial statements as at and for the three months ended March 31, 2016.

Table 15

|

| | | | | | | | | | | | | | | | | | | | | | | | |

Hedge Positions Summary (1) | | | | | | | | | | | | |

| As at April 28, 2016 | Q2 2016 | H2 2016 | 2017 | 2018 | 2019 | 2020 |

Crude Oil - WTI (2) | US$/bbl |

| bbl/day |

| US$/bbl |

| bbl/day |

| US$/bbl |

| bbl/day |

| US$/bbl |

| bbl/day |

| US$/bbl |

| bbl/day |

| US$/bbl |

| bbl/day |

|

| Ceiling | — |

| — |

| 50.00 |

| 3,000 |

| 52.24 |

| 5,000 |

| — |

| — |

| — |

| — |

| — |

| — |

|

| Floor | — |

| — |

| 40.00 |

| 3,000 |

| 41.00 |

| 5,000 |

| — |

| — |

| — |

| — |

| — |

| — |

|

| Sold Floor | — |

| — |

| — |

| — |

| 30.00 |

| 2,000 |

| — |

| — |

| — |

| — |

| — |

| — |

|

| Swap | — |

| — |

| 42.10 |

| 2,000 |

| — |

| — |

| — |

| — |

| — |

| — |

| — |

| — |

|

Crude Oil - $CWTI (3) | Cdn$/bbl |

| bbl/day |

| Cdn$/bbl |

| bbl/day |

| Cdn$/bbl |

| bbl/day |

| Cdn$/bbl |

| bbl/day |

| Cdn$/bbl |

| bbl/day |

| Cdn$/bbl |

| bbl/day |

|

| Ceiling | 83.38 |

| 3,000 |

| 83.38 |

| 3,000 |

| 83.38 |

| 1,488 |

| — |

| — |

| — |

| — |

| — |

| — |

|

| Floor | 70.00 |

| 3,000 |

| 70.00 |

| 3,000 |

| 70.00 |

| 1,488 |

| — |

| — |

| — |

| — |

| — |

| — |

|

| Swap | 77.20 |

| 7,000 |

| 77.20 |

| 7,000 |

| — |

| — |

| — |

| — |

| — |

| — |

| — |

| — |

|

| Total Crude Oil Volumes Hedged (bbl/day) |

|

| 10,000 |

|

|

| 15,000 |

|

|

| 6,488 |

|

|

| — |

|

|

| — |

|

|

| — |

|

| | | | | | | | | | | | | |

Crude Oil - MSW (Differential to WTI) (4) | US$/bbl |

| bbl/day |

| US$/bbl |

| bbl/day |

| US$/bbl |

| bbl/day |

| US$/bbl |

| bbl/day |

| US$/bbl |

| bbl/day |

| US$/bbl |

| bbl/day |

|

| Swap | (3.72 | ) | 10,000 |

| (3.72 | ) | 10,000 |

| — |

| — |

| — |

| — |

| — |

| — |

| — |

| — |

|

| | | | | | | | | | | | | |

Natural Gas - NYMEX Henry Hub (5) | US$/MMbtu |

| MMbtu/day |

| US$/MMbtu |

| MMbtu/day |

| US$/MMbtu |

| MMbtu/day |

| US$/MMbtu |

| MMbtu/day |

| US$/MMbtu |

| MMbtu/day |

| US$/MMbtu |

| MMbtu/day |

|

| Ceiling | 4.79 |

| 105,000 |

| 4.79 |

| 105,000 |

| 4.81 |

| 145,000 |

| 4.92 |

| 90,000 |

| 5.00 |

| 40,000 |

| — |

| — |

|

| Floor | 4.00 |

| 105,000 |

| 4.00 |

| 105,000 |

| 4.00 |

| 145,000 |

| 4.00 |

| 90,000 |

| 4.00 |

| 40,000 |

| — |

| — |

|

| Swap | 4.00 |

| 40,000 |

| 4.00 |

| 40,000 |

| — |

| — |

| — |

| — |

| — |

| — |

| — |

| — |

|

Natural Gas - AECO (6) | Cdn$/GJ |

| GJ/day |

| Cdn$/GJ |

| GJ/day |

| Cdn$/GJ |

| GJ/day |

| Cdn$/GJ |

| GJ/day |

| Cdn$/GJ |

| GJ/day |

| Cdn$/GJ |

| GJ/day |

|

| Ceiling | — |

| — |

| — |

| — |

| — |

| — |

| — |

| — |

| 3.30 |

| 10,000 |

| 3.60 |

| 30,000 |

|

| Floor | — |

| — |

| — |

| — |

| — |

| — |

| — |

| — |

| 3.00 |

| 10,000 |

| 3.08 |

| 30,000 |

|

| Swap | 2.99 |

| 30,000 |

| 2.99 |

| 30,000 |

| 2.75 |

| 10,000 |

| 2.96 |

| 40,000 |

| 3.16 |

| 20,000 |

| 3.35 |

| 30,000 |

|

| Total Natural Gas Volumes Hedged (MMbtu/day) |

|

| 173,435 |

|

|

| 173,435 |

|

|

| 154,478 |

|

|

| 127,913 |

|

|

| 68,435 |

|

|

| 56,869 |

|

| | | | | | | | | | | | | |

| Natural Gas - AECO Basis | AECO/NYMEX |

| MMbtu/day |

| AECO/NYMEX |

| MMbtu/day |

| AECO/NYMEX |

| MMbtu/day |

| AECO/NYMEX |

| MMbtu/day |

| AECO/NYMEX |

| MMbtu/day |

| AECO/NYMEX |

| MMbtu/day |

|

| Swap (percentage of NYMEX) | 90.3 |

| 140,000 |

| 90.3 |

| 140,000 |

| 89.7 |

| 145,000 |

| 84.9 |

| 90,000 |

| 83.7 |

| 40,000 |

| — |

| — |

|

| Natural Gas - AECO Basis | US$/MMbtu |

| MMbtu/day |

| US$/MMbtu |

| MMbtu/day |

| US$/MMbtu |

| MMbtu/day |

| US$/MMbtu |

| MMbtu/day |

| US$/MMbtu |

| MMbtu/day |

| US$/MMbtu |

| MMbtu/day |

|

| Swap (differential to NYMEX) | — |

| — |

| — |

| — |

| (0.71 | ) | 25,000 |

| (0.69 | ) | 45,000 |

| (0.60 | ) | 35,000 |

| (0.57 | ) | 35,000 |

|

| Total AECO Basis Volumes Hedged (MMbtu/day) |

|

| 140,000 |

|

|

| 140,000 |

|

|

| 170,000 |

|

|

| 135,000 |

|

|

| 75,000 |

|

|

| 35,000 |

|

| |

| (1) | The prices and volumes in this table represent averages for several contracts representing different periods. The average price for the portfolio of options listed above does not have the same payoff profile as the individual option contracts. Viewing the average price of a group of options is purely for indicative purposes. All positions are financially settled against the benchmark prices disclosed in Note 9 “Financial Instruments and Market Risk Management” in the financial statements as at and for the three months ended March 31, 2016. |

| |

| (2) | Crude oil prices referenced to WTI. |

| |

| (3) | Crude oil prices referenced to WTI, multiplied by the Bank of Canada monthly average noon day rate. |

| |

| (4) | MSW differential refers to the discount between WTI and the mixed sweet crude grade at Edmonton, calculated on a monthly weighted average basis in US$. |

| |

| (5) | Natural gas prices referenced to NYMEX Henry Hub last day settlement. |

| |

| (6) | Natural gas prices referenced to AECO 7(a) index. |

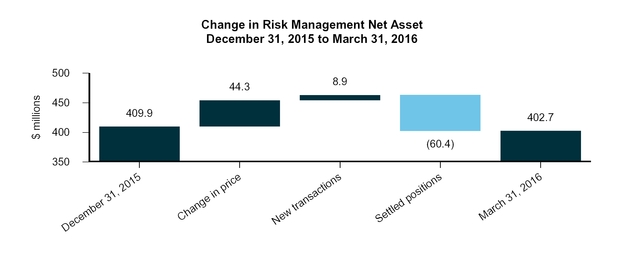

The fair value of ARC’s risk management contracts at March 31, 2016 was a net asset of $402.7 million, representing the expected market price to settle ARC’s contracts at the balance sheet date after any adjustments for credit risk. This may differ from what will eventually be settled in future periods.

Exhibit 10

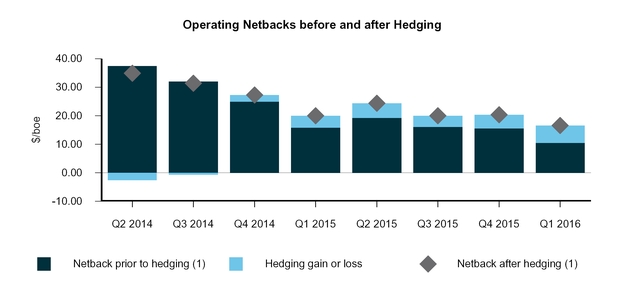

Operating Netbacks

ARC’s operating netbacks prior to hedging was $10.53 per boe in the first quarter of 2016 as compared to $15.91 per boe in the same period in 2015, representing a decrease of 34 per cent.

ARC’s first quarter 2016 netback, including realized hedging gains and losses, was $16.57 per boe, as compared to $20.03 per boe in the same period in 2015, representing a decrease of 17 per cent.

The components of operating netbacks for the first quarter of 2016 compared to the same period in 2015 are summarized in Table 16:

Table 16 |

| | | | | | | | | | | | | | |

Netbacks (1) | Light and Medium Crude Oil |

| Heavy Crude Oil |

| Condensate |

| Natural Gas |

| NGLs |

| Q1 2016 Total |

| Q1 2015 Total |

|

| | ($/bbl) |

| ($/bbl) |

| ($/bbl) |

| ($/Mcf) |

| ($/bbl) |

| ($/boe) |

| ($/boe) |

|

| Average sales price | 39.04 |

| 10.46 |

| 42.07 |

| 2.05 |

| 8.42 |

| 20.39 |

| 28.20 |

|

| Other income | — |

| — |

| — |

| — |

| — |

| 0.06 |

| 0.11 |

|

| Total sales | 39.04 |

| 10.46 |

| 42.07 |

| 2.05 |

| 8.42 |

| 20.45 |

| 28.31 |

|

| Royalties | (4.48 | ) | (0.83 | ) | (7.26 | ) | (0.03 | ) | (1.64 | ) | (1.62 | ) | (2.80 | ) |

| Transportation | (2.77 | ) | (0.79 | ) | (2.49 | ) | (0.29 | ) | (6.53 | ) | (2.20 | ) | (2.36 | ) |

Operating expenses (2) | (12.36 | ) | (14.03 | ) | (6.82 | ) | (0.57 | ) | (5.96 | ) | (6.10 | ) | (7.24 | ) |

| Netback prior to hedging | 19.43 |

| (5.19 | ) | 25.50 |

| 1.16 |

| (5.71 | ) | 10.53 |

| 15.91 |

|

| Realized hedging gain | 8.14 |

| — |

| — |

| 0.96 |

| — |

| 6.04 |

| 4.12 |

|

| Netback after hedging | 27.57 |

| (5.19 | ) | 25.50 |

| 2.12 |

| (5.71 | ) | 16.57 |

| 20.03 |

|

| % of total netback | 46 |

| — |

| 4 |

| 51 |

| (1 | ) | 100 |

| 100 |

|

| |

| (1) | Non-GAAP measure which may not be comparable to similar non-GAAP measures used by other entities. Refer to the section entitled "Non-GAAP Measures" contained within this MD&A. |

| |

| (2) | Composed of direct costs incurred to operate crude oil and natural gas wells. A number of assumptions have been made in allocating these costs between light and medium crude oil, heavy crude oil, condensate, natural gas and NGLs production. |

Exhibit 11

| |

| (1) | Non-GAAP measure which may not be comparable to similar non-GAAP measures used by other entities. Refer to the section entitled "Non-GAAP Measures" contained within this MD&A. |

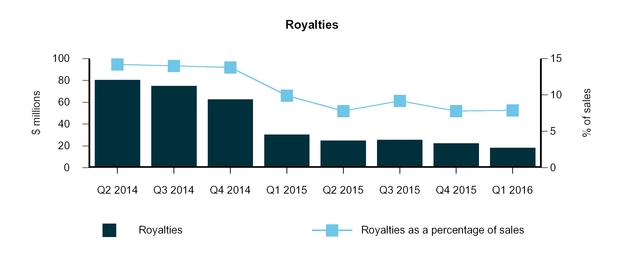

Royalties

ARC pays royalties to the respective provincial governments and landowners of the three western Canadian provinces in which it operates. Approximately 86 per cent of these royalties are Crown royalties. Each province that ARC operates in has established a separate and distinct royalty regime which impacts ARC’s average corporate royalty rate.

In British Columbia, two thirds of ARC’s royalty expense stems from production of crude oil. This has changed significantly from periods prior to 2016 when the majority of ARC’s royalty expense was attributed to the production of natural gas. This change in the composition of royalty expense is due to lower natural gas prices which have reduced ARC's natural

gas royalties, combined with increased crude oil production from ARC's Tower field. Royalty rates for crude oil are based on commodity prices, well royalty classification and well productivity.

In Alberta, the majority of ARC’s royalties are related to crude oil production where royalty rates are based on reference prices, production levels and well depths. Similarly, most royalties remitted in Saskatchewan relate to crude oil production and royalty calculations are based on commodity prices, the classification of the product and well productivity.

Each province has various incentive programs in place to promote drilling by reducing the overall royalty expense for producers and offsetting gathering and processing costs. In most cases, the incentive period lasts for a finite period of time (usually twelve months upon commencement of production), after which point the royalty rate usually increases depending on the production rate of the well and prevailing market commodity prices.

In 2016, the provincial government of Alberta announced the key highlights of a proposed Modernized Royalty Framework ("MRF") that will be effective on January 1, 2017. These highlights include providing royalty incentives for the efficient development of conventional crude oil, natural gas and NGL resources, no changes to the royalty structure of wells drilled prior to 2017 for a 10-year period from the royalty program's implementation date, the replacement of royalty credits and holidays on conventional wells by a revenue minus cost framework with a post-payout royalty rate based on commodity prices, the reduction of royalty rates for mature wells, and a neutral internal rate of return for any given play compared to the current royalty framework. Details of the MRF calibration formulas have been released and more specific information will be provided by the provincial government in the coming months to help crude oil and natural gas producers better understand the economics of investment in Alberta.

For ARC, the economics of drilling in its Ante Creek Montney and Pembina Cardium plays, within expected price ranges, are expected to be relatively consistent with the previous Alberta Royalty Framework. ARC will continue to evaluate the impact of the MRF on the Company’s expected results of operations and cash flows to evaluate investment in its assets located in Alberta. Given that only 28 per cent of ARC's production is in Alberta, the impact is expected to be minimal.

Total royalties as a percentage of pre-hedged commodity product sales revenue decreased from 9.9 per cent ($2.80 per boe) in the first quarter of 2015 to 7.9 per cent ($1.62 per boe) in the first quarter of 2016 reflecting the "sliding scale" effect of royalty rates on decreased average commodity prices during that time period. Similarly, total royalties decreased from $30.4 million in the first quarter of 2015 to $18.3 million in the first quarter of 2016.

Exhibit 12

Operating and Transportation Expenses

Operating expenses decreased $1.14 per boe to $6.10 per boe in the first quarter of 2016 compared to $7.24 per boe in the first quarter of 2015. On an absolute dollar basis, operating expenses have also decreased by $9.4 million or 12 per cent in the first quarter of 2016 as compared to the first quarter of 2015. The decrease in operating costs for the three months ended March 31, 2016 is mainly a result of the disposition of certain non-core assets in 2015, increased production volumes from new wells with relatively lower average operating costs, and diligent cost control efforts, including negotiating service cost decreases with many of ARC's suppliers throughout 2015 and into 2016. Additionally, electricity costs were lower in the first quarter of 2016 at an average Alberta Power Pool Rate of $18.09 per megawatt hour compared to an average of $29.14 per megawatt hour in the first quarter of 2015, further reducing operating costs year-over-year.

Exhibit 13

Transportation expenses were $2.20 per boe during the first quarter of 2016 as compared to $2.36 per boe in the first quarter of 2015. Transportation per boe was seven per cent lower for the first quarter of 2016 compared to 2015 due to reduced trucking costs at the Parkland/Tower area, which became pipeline-connected for its crude oil and liquids volumes over the course of 2015 and early 2016.

Exhibit 14

G&A Expenses and Share-Based Compensation

G&A, prior to share-based compensation expense and net of capitalized G&A and overhead recoveries on operated properties, increased by 33 per cent to $21.9 million in the first quarter of 2016 from $16.5 million in the first quarter of 2015. While G&A expenses before the impact of capitalized G&A and overhead recoveries did not change from the first quarter of 2015 to the first quarter of 2016, capitalized G&A and overhead recoveries decreased by 50 per cent during the same period. The reduction in capitalized G&A is related to reduced capital spending in the first quarter compared to the same period in 2015.

Table 17 is a breakdown of G&A and share-based compensation expenses:

Table 17 |

| | | | | | |

| | Three Months Ended |

| | March 31 |

| G&A and Share-Based Compensation | 2016 |

| 2015 |

| % Change |

|

| ($ millions, except per boe) |

G&A expenses (1) | 27.2 |

| 27.2 |

| — |

|

| Capitalized G&A and overhead recoveries | (5.3 | ) | (10.7 | ) | (50 | ) |

| G&A expenses before share-based compensation plans | 21.9 |

| 16.5 |

| 33 |

|

G&A – share-based compensation plans (2) | 9.9 |

| (5.8 | ) | 271 |

|

| Total G&A and share-based compensation expenses | 31.8 |

| 10.7 |

| 197 |

|

| Total G&A and share-based compensation expenses per boe | 2.81 |

| 0.99 |

| 184 |

|

| |

| (1) | Includes expenses recognized under the DSU Plan. |

| |

| (2) | Comprises expenses recognized under the RSU and PSU, Share Option and LTRSA Plans. |

Exhibit 15

Share-Based Compensation Plans – Restricted Share Unit and Performance Share Unit Plan, Share Option Plan, Deferred Share Unit Plan, and Long-term Restricted Share Award Plan

Restricted Share Unit and Performance Share Unit Plan

The RSU and PSU Plan is designed to offer each eligible employee and officer (the “plan participants”) cash compensation in relation to the underlying value of a specified number of share units. The RSU and PSU Plan consists of RSUs for which the number of units is fixed and will vest over a period of three years and PSUs for which the number of units is variable and will vest at the end of three years.

Upon vesting, the plan participant is entitled to receive a cash payment based on the underlying value of the share units plus accrued dividends. The cash compensation issued upon vesting of the PSUs is dependent upon the total return performance of ARC compared to its peers. Total return is calculated as a sum of the change in the market price of the common shares in the period plus the amount of dividends in the period. A performance multiplier is applied to the PSUs based on the percentile rank of ARC’s total shareholder return compared to its peers. The performance multiplier ranges from zero if ARC’s performance ranks in the bottom quartile, to two for top quartile performance.

ARC recorded G&A expenses of $8.9 million during the first quarter of 2016 in accordance with the RSU and PSU Plan, as compared to recoveries of $6.6 million during the first quarter of 2015. ARC recognized an increase in compensation charges for the first quarter of 2016 as compared to the first quarter of 2015 due to a higher estimated performance

multiplier for its PSU rewards relative to what ARC had been estimating at the end of the prior quarter, as well as a heightened valuation of awards at March 31, 2016 as ARC's share price increased from $16.70 per share outstanding at December 31, 2015 to $18.89 at March 31, 2016.

During the three months ended March 31, 2016, ARC made cash payments of $11.8 million in respect of the RSU and PSU Plan ($14.4 million for the three months ended March 31, 2015). Of these payments, $9.1 million were in respect of amounts recorded to G&A expenses ($11 million for the three months ended March 31, 2015) and $2.7 million were in respect of amounts recorded to operating expenses and capitalized as PP&E and E&E assets ($3.4 million for the three months ended March 31, 2015). These amounts were accrued in prior periods.

Table 18 shows the changes to the RSU and PSU Plan during 2016:

Table 18 |

| | | |

RSU and PSU Plan

(number of units, thousands) |

RSUs | PSUs (1) | Total RSUs and PSUs |

| Balance, December 31, 2015 | 730 | 1,577 | 2,307 |

| Granted | 206 | 375 | 581 |

| Distributed | (139) | (207) | (346) |

| Forfeited | (86) | (83) | (169) |

| Balance, March 31, 2016 | 711 | 1,662 | 2,373 |

| |

| (1) | Based on underlying units before any effect of the performance multiplier. |

The liability associated with the RSUs and PSUs granted is recognized in the consolidated statements of income (the "statements of income") over the vesting period while being adjusted each period for changes in the underlying share price, accrued dividends and the number of PSUs expected to be issued on vesting. In periods where substantial share price fluctuation occurs, ARC’s G&A expenses are subject to greater volatility.

Due to the variability in the future payments under the plan, ARC estimates that between $13.8 million and $79 million will be paid out in 2016 through 2019 based on the current share price, accrued dividends, and ARC’s market performance relative to its peers. Table 19 is a summary of the range of future expected payments under the RSU and PSU Plan based on variability of the performance multiplier and units outstanding under the RSU and PSU Plan as at March 31, 2016:

Table 19 |

| | | | | | |

| Value of RSU and PSU Plan as at | | | |

| March 31, 2016 | Performance multiplier |

| (units thousands and $ millions, except per share) | — |

| 1.0 |

| 2.0 |

|

| Estimated units to vest | | | |

| RSUs | 731 |

| 731 |

| 731 |

|

| PSUs | — |

| 1,726 |

| 3,452 |

|

Total units (1) | 731 |

| 2,457 |

| 4,183 |

|

Share price (2) | 18.89 |

| 18.89 |

| 18.89 |

|

| Value of RSU and PSU Plan upon vesting | 13.8 |

| 46.4 |

| 79.0 |

|

| 2016 | 3.2 |

| 8.4 |

| 13.7 |

|

| 2017 | 5.5 |

| 13.9 |

| 22.2 |

|

| 2018 | 3.8 |

| 15.7 |

| 27.6 |

|

| 2019 | 1.3 |

| 8.4 |

| 15.5 |

|

| |

| (1) | Includes additional estimated units to be issued under the RSU and PSU Plan for dividends accrued to date. |

| |

| (2) | Per share outstanding. Values will fluctuate over the vesting period based on the volatility of the underlying share price. Assumes a future share price of $18.89, which is based on the closing share price at March 31, 2016. |

Share Option Plan

Share options are granted to employees and consultants of ARC, vesting evenly on the fourth and fifth anniversaries of their respective grant dates, and have a maximum term of seven years. The option holder has the right to exercise the options at the original exercise price or at a reduced exercise price, equal to the exercise price at grant date less all dividends paid subsequent to the grant date and prior to the exercise date.

At March 31, 2016, ARC had 3.1 million share options outstanding under this plan, representing less than one per cent of outstanding shares, with a weighted average exercise price of $21.71 per share. At March 31, 2016, approximately 0.3 million share options were exercisable with a weighted average exercise price of $21.16 per share. Compensation expense related to share options of $0.9 million has been recorded during the first quarter of 2016 compared to $0.8 million for the first quarter of 2015 and is included within G&A expenses.

Deferred Share Unit Plan

ARC has a DSU Plan for its non-employee directors under which each director receives a minimum of 60 per cent of their total annual remuneration in the form of DSUs. Each DSU fully vests on the date of grant but is settled in cash only when the director has ceased to be a member of the Board. For the three months ended March 31, 2016, G&A expenses of $1.3 million were recorded in relation to the DSU Plan (G&A recoveries of $0.3 million in 2015).

Long-term Restricted Share Award Plan

ARC's LTRSA Plan awards shares of ARC to qualifying officers and employees and is intended to further align participant compensation with the interests of the Company and its shareholders over the long-term. LTRSA grants consist of restricted common shares that are awarded at the date of grant and a cash payment made equal to the estimated personal tax obligation associated with the total award. The restricted shares issued on the grant date of the award are held in trust until the vesting conditions have been met.

While in trust, the restricted shares earn dividends which are reinvested into ARC common shares via the stock dividend program and these stock dividends are also held in trust until vested. Each LTRSA has a 10 year term and vests evenly on the eighth, ninth, and tenth anniversaries of the grant date of the award. Restricted shares and any accrued dividends that are subject to forfeiture will be redeemed and cancelled by ARC.

Compensation expense associated with the cash payment is recognized at the fair value on the grant date, while expense associated with the restricted common shares is estimated as the fair value of the award equal to the previous five-day weighted average trading price of ARC shares on the grant date and is recognized over the vesting period.

At March 31, 2016, ARC had 90 thousand restricted shares outstanding under this plan. ARC did not record any cash payments under the LTRSA Plan during the three months ended March 31, 2016 or 2015.

Interest and Financing Charges

Interest and financing charges increased two per cent to $13.1 million in the first quarter of 2016 from $12.9 million in the first quarter of 2015. The increase in interest charges primarily reflects the increased value of the US dollar relative to the Canadian dollar in 2016 as compared to 2015 as ARC's debt and related interest obligations are primarily held in US dollars.

At March 31, 2016, ARC had $1 billion of long-term debt outstanding, including a current portion of $54.7 million that is due for repayment within the next 12 months. ARC's debt balance is fixed at a weighted average interest rate of 4.43 per cent. Approximately 96 per cent (US$762.1 million) of ARC’s debt outstanding is denominated in US dollars.

Foreign Exchange Gains and Losses

ARC recorded a foreign exchange gain of $67.4 million in the first quarter of 2016 compared to a loss of $88.1 million in the first quarter of 2015. The gain is attributed to the unrealized gain associated with the revaluation of ARC’s US dollar denominated debt outstanding from the period of December 31, 2015 to March 31, 2016 and reflects the change in value of the US dollar relative to the Canadian dollar from $1.38 to $1.30.

Table 20 shows the various components of foreign exchange gains and losses:

Table 20 |

| | | | | | |

| | Three Months Ended |

| | March 31 |

Foreign Exchange Gains and Losses ($ millions) | 2016 |

| 2015 |

| % Change |

|

| Unrealized gain (loss) on US denominated debt | 67.4 |

| (88.3 | ) | (176 | ) |

| Realized gain on US denominated transactions | — |

| 0.2 |

| (100 | ) |

| Total foreign exchange gain (loss) | 67.4 |

| (88.1 | ) | (177 | ) |

Taxes

ARC recorded a current income tax recovery of $7 million in the first quarter of 2016 compared to $2.3 million expense during the first quarter of 2015. This movement from a current tax expense to a current tax recovery reflects an estimated tax loss for 2016 relating primarily to decreased commodity prices. These tax losses can be carried back to the previous three taxation years to recover current taxes that were previously paid.

During the first quarter of 2016, a deferred income tax expense of $6.5 million was recorded compared to an expense of $13 million in the first quarter of 2015. For the three months ended March 31, 2016 as compared to the three months ended March 31, 2015, ARC’s decrease in deferred tax expense primarily relates to an unrealized loss on risk management contracts in the current period as compared to unrealized gains in the comparable period, slightly offset by a smaller net increase in ARO in the current period.

The income tax pools (detailed in Table 21) are deductible at various rates and annual deductions associated with the initial tax pools will decline over time.

Table 21

|

| | | | |

Income Tax Pool Type ($ millions) | March 31, 2016 |

|

Annual Deductibility |

|

| Canadian oil and gas property expense | 611.6 |

| 10% declining balance |

|

| Canadian development expense | 792.7 |

| 30% declining balance |

|

| Canadian exploration expense | — |

| 100 | % |

| Undepreciated capital cost | 766.4 |

| Primarily 25% declining balance |

|

| Other | 20.0 |

| Various rates, 7% declining balance to 20% |

|

| Total federal tax pools | 2,190.7 |

| |

| Additional Alberta tax pools | 8.6 |

| Various rates, 25% declining balance to 100% |

|

DD&A Expense and Impairment Charges

ARC records DD&A expense on its PP&E over the individual useful lives of the assets employing the unit of production method using proved plus probable reserves and associated estimated future development capital required for its crude oil and natural gas assets, and a straight-line method for its corporate administrative assets. Assets in the E&E phase are not amortized. For the three months ended March 31, 2016, ARC recorded DD&A expense of $134.2 million as compared to $165.3 million for the three months ended March 31, 2015. The decrease in DD&A expense for the three months ended March 31, 2016 to $11.87 per boe compared to $15.26 per boe for the first quarter of 2015 reflects the effect of a lower depletable base as result of reduced costs of finding and development of reserves and $469.6 million of impairment charges recorded during the year ended December 31, 2015.

Impairment is recognized when the carrying value of an asset or group of assets exceeds its recoverable amount, defined as the higher of its value in use or fair value less costs of disposal. Any asset impairment that is recorded is recoverable to its original value less any associated DD&A expense should there be indicators that the recoverable amount of the asset has increased in value since the time of recording the initial impairment. There were no impairment charges or recoveries recorded for the three months ended March 31, 2016. At March 31, 2015, an impairment charge of $13.4 million was recognized associated with the disposition of non-core assets located in southern Alberta. As future commodity prices remain volatile, impairment charges or recoveries could be recorded in future periods.

A breakdown of DD&A expense and impairment charges is summarized in Table 22:

Table 22 |

| | | | | | |

| | Three Months Ended |

| | March 31 |

DD&A Expense and Impairment Charges ($ millions, except per boe amounts) | 2016 |

| 2015 |

| % Change |

|

| Depletion of crude oil and natural gas assets | 132.8 |

| 163.7 |

| (19 | ) |

| Depreciation of administrative assets | 1.4 |

| 1.6 |

| (13 | ) |

| Impairment charges | — |

| 13.4 |

| (100 | ) |

| Total DD&A expense and impairment charges | 134.2 |

| 178.7 |

| (25 | ) |

| DD&A rate before impairment per boe | 11.87 |

| 15.26 |

| (22 | ) |

| DD&A and impairment rate per boe | 11.87 |

| 16.50 |

| (28 | ) |

Capital Expenditures, Acquisitions and Dispositions

Capital expenditures before acquisitions, dispositions or purchases of undeveloped land totaled $59.1 million in the first quarter of 2016 as compared to $129.5 million during the first quarter of 2015. This total includes development and production additions to PP&E of $43.6 million and additions to E&E assets of $15.5 million. PP&E expenditures include additions to crude oil and natural gas development and production assets and administrative assets. E&E expenditures include asset additions in areas that have been determined by Management to be in the E&E stage.

A breakdown of capital expenditures, acquisitions and dispositions is shown in Table 23:

Table 23 |

| | | | | | | | | | | | | | |

| | Three Months Ended March 31 |

| | 2016 | 2015 | |

Capital Expenditures ($ millions) | E&E |

| PP&E |

| Total |

| E&E |

| PP&E |

| Total |

| % Change |

|

| Geological and geophysical | 0.2 |

| 2.6 |

| 2.8 |

| (0.3 | ) | 2.6 |

| 2.3 |

| 22 |

|

| Drilling and completions | 11.0 |

| 12.2 |

| 23.2 |

| — |

| 83.0 |

| 83.0 |

| (72 | ) |

| Plant and facilities | 4.3 |

| 28.4 |

| 32.7 |

| — |

| 43.7 |

| 43.7 |

| (25 | ) |

| Administrative assets | — |

| 0.4 |

| 0.4 |

| — |

| 0.5 |

| 0.5 |

| (20 | ) |

| Total capital expenditures | 15.5 |

| 43.6 |

| 59.1 |

| (0.3 | ) | 129.8 |

| 129.5 |

| (54 | ) |

| Undeveloped land | — |

| — |

| — |

| — |

| 1.4 |

| 1.4 |

| (100 | ) |

| Total capital expenditures including undeveloped land purchases | 15.5 |

| 43.6 |

| 59.1 |

| (0.3 | ) | 131.2 |

| 130.9 |

| (55 | ) |

| Acquisitions | — |

| 15.1 |

| 15.1 |

| — |

| — |

| — |

| 100 |

|

Dispositions (1) | — |

| — |

| — |

| — |

| (11.0 | ) | (11.0 | ) | (100 | ) |

| Total capital expenditures, land purchases and net acquisitions and dispositions | 15.5 |

| 58.7 |

| 74.2 |

| (0.3 | ) | 120.2 |

| 119.9 |

| (38 | ) |

| |

| (1) | Represents proceeds and adjustments to proceeds from divestitures. |

Asset Retirement Obligations and Reclamation Fund

At March 31, 2016, ARC has recorded ARO of $603.5 million ($573.2 million at December 31, 2015) for the future abandonment and reclamation of ARC’s properties. The estimated ARO includes assumptions in respect of actual costs to abandon wells or reclaim the property, the time frame in which such costs will be incurred, as well as annual inflation factors in order to calculate the undiscounted total future liability. The future liability has been discounted at a liability-specific risk-free interest rate of 2.0 per cent (2.2 per cent at December 31, 2015).

Accretion charges of $3.1 million for the three months ended March 31, 2016 ($3.6 million for Q1 2015) have been recognized in the statements of income to reflect the increase in ARO associated with the passage of time. Actual spending under ARC’s abandonment and reclamation program for the three months ended March 31, 2016 was $2.1 million ($2 million for Q1 2015). For the three months ended March 31, 2016, acquisitions increased ARO by $1.2 million ($nil for Q1 2015).

In 2005, ARC established a restricted reclamation fund to finance obligations specifically associated with its Redwater property. Minimum contributions to this fund will be approximately $60 million in total over the next 39 years. The balance of this fund totaled $33.5 million at March 31, 2016 compared to $34.3 million at December 31, 2015, primarily reflecting reimbursement from the fund for reclamations that occurred in 2015 totaling $1.9 million. Under the terms of ARC’s investment policy, cash in the reclamation fund can only be invested in certain securities and require a minimum credit rating for investments of A or higher.

Environmental stewardship is a core value at ARC and abandonment and reclamation activities continue to be made in a prudent, responsible manner with the oversight of the Health, Safety and Environment Committee of the Board. Ongoing abandonment expenditures for all of ARC’s assets are funded entirely out of cash flow from operating activities. ARC’s Licensee Liability Rating is well within the Alberta Energy Regulator’s guidelines at this date.

Exhibit 16

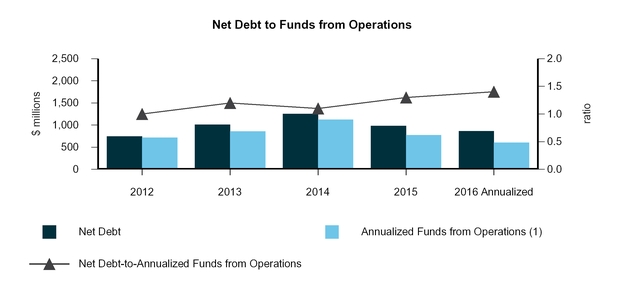

Capitalization, Financial Resources and Liquidity

ARC’s long-term goal is to fund current period reclamation expenditures, dividend payments and capital expenditures necessary for the replacement of production declines using funds from operations. Value-creating activities will be financed with a combination of funds from operations and other sources of capital.

ARC typically uses three markets to raise capital: equity, bank debt and long-term notes. Long-term notes are issued to large institutional investors normally with an average term of five to 12 years. The cost of this debt is based upon two factors: the current rate of long-term government bonds and ARC’s credit spread. ARC’s weighted average interest rate on its outstanding long-term notes is currently 4.43 per cent.

A breakdown of ARC’s capital structure as at March 31, 2016 and December 31, 2015 is outlined in Table 24:

Table 24 |

| | | | |

Capital Structure and Liquidity ($ millions, except per cent and ratio amounts) | March 31, 2016 |

| December 31, 2015 |

|

Long-term debt (1) | 1,034.4 |

| 1,114.3 |

|

Working capital surplus (2) | (166.0 | ) | (129.2 | ) |

| Net debt | 868.4 |

| 985.1 |

|

Market capitalization (3) | 6,607.7 |

| 5,796.6 |

|

| Total capitalization | 7,476.1 |

| 6,781.7 |

|

| Net debt as a percentage of total capitalization (%) | 11.6 |

| 14.5 |

|

| Net debt to annualized funds from operations (ratio) | 1.4 |

| 1.3 |

|

| |

| (1) | Includes a current portion of long-term debt of $54.7 million at March 31, 2016 and $57.9 million at December 31, 2015. |

| |

| (2) | Working capital surplus or deficit is calculated as current assets less current liabilities as they appear on the condensed interim consolidated balance sheets (the "balance sheets"), and excludes current unrealized amounts pertaining to risk management contracts, assets held for sale and ARO contained within liabilities associated with assets held for sale, as well as the current portion of long-term debt and current portion of ARO. |

| |

| (3) | Calculated using the total common shares outstanding at March 31, 2016 multiplied by the closing share price of $18.89 at March 31, 2016 (closing share price of $16.70 at December 31, 2015). |

Management intends to keep its net debt balance to a ratio of less than two times annualized funds from operations during specific periods with a long-term strategy to keep its net debt balance to a ratio of between one to 1.5 times annualized funds from operations and less than 20 per cent of total market capitalization. This strategy has resulted in manageable debt levels to date and has positioned ARC to remain well within its debt covenants. Refer to Note 8 "Capital Management" in the financial statements as at and for the three months ended March 31, 2016.

Exhibit 17

| |

| (1) | Refer to Note 8 "Capital Management" in the financial statements as at and for the three months ended March 31, 2016 and to the section entitled "Funds from Operations” contained within this MD&A. |

The following exhibits the balance of cash inflows and outflows over the past four years and for the year-to-date. In any period when cash outflows exceed inflows, ARC’s net debt balance will increase to cover the shortfall and will decrease in any period when inflows exceed outflows.

Exhibit 18

Table 25

|

| | | | | | | | | | |

| | 2016 YTD |

| 2015 |

| 2014 |

| 2013 |

| 2012 |

|

| Cash Inflows | | | | | |

Funds from operations (1) | 150.1 |

| 773.4 |

| 1,124.0 |

| 861.8 |

| 719.8 |

|

| DRIP & SDP | 43.7 |

| 195.5 |

| 151.0 |

| 130.1 |

| 116.3 |

|

| Equity issuance (net proceeds) | — |

| 386.1 |

| — |

| — |

| 330.7 |

|

Dispositions (2) | — |

| 88.8 |

| 39.3 |

| 89.8 |