ORIENTAL FINANCIAL GROUP

ANNUAL MEETING APRIL 24, 2013

FORWARD LOOKING STATEMENTS

The information included in this document contains certain forward-looking statements within the meaning of the Private Securities Litigation Reform Act of 1995. These statements are based on management’s current expectations and involve certain risks and uncertainties that may cause actual results to differ materially from those expressed in the forward-looking statements.

Factors that might cause such a difference include, but are not limited to (i) difficulties in integrating the acquired Puerto Rico operations of Banco Bilbao Vizcaya Argentaria, S.A (BBVA PR) into Oriental’s operations; (ii) the amounts by which our assumptions related to the acquisition fail to approximate actual results; (iii) the rate of growth in the economy and employment levels, as well as general business and economic conditions; (iv) changes in interest rates, as well as the magnitude of such changes; (v) the fiscal and monetary policies of the federal government and its agencies; (vi) changes in federal bank regulatory and supervisory policies, including required levels of capital; (vii) the relative strength or weakness of the consumer and commercial credit sectors and of the real estate market in Puerto Rico; (viii) the performance of the stock and bond markets; (ix) competition in the financial services industry; (x) possible legislative, tax or regulatory changes; and (xi) difficulties in combining the operations of any other acquired entity.

For a discussion of such factors and certain risks and uncertainties to which Oriental is subject, see Oriental’s annual report on Form 10-K for the year ended December 31, 2012, as well as its other filings with the U.S. Securities and Exchange Commission. Other than to the extent required by applicable law, including the requirements of applicable securities laws, Oriental assumes no obligation to update any forward-looking statements to reflect occurrences or unanticipated events or circumstances after the date of such statements.

2

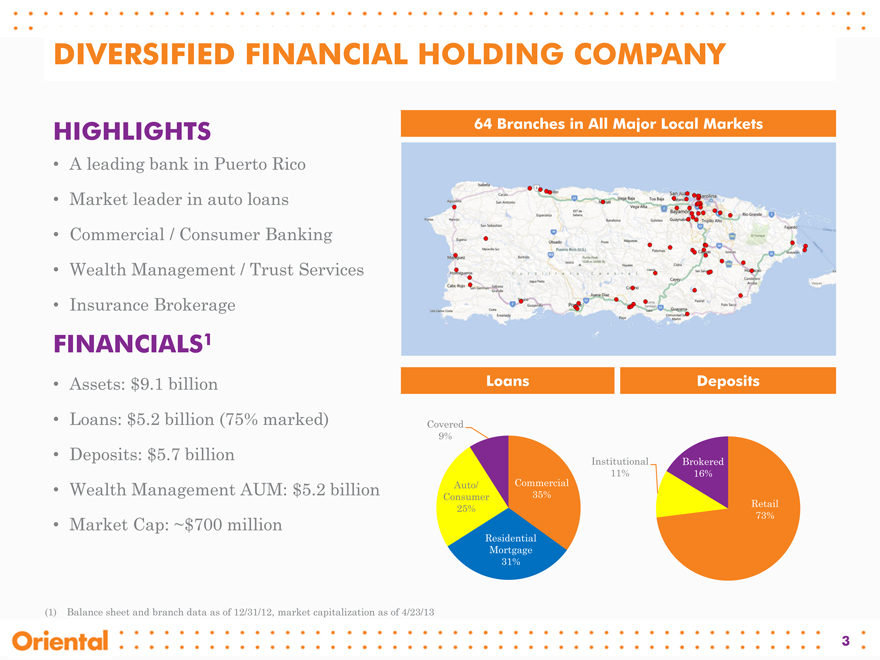

DIVERSIFIED FINANCIAL HOLDING COMPANY

HIGHLIGHTS

• A leading bank in Puerto Rico

• Market leader in auto loans

• Commercial / Consumer Banking

• Wealth Management / Trust Services

• Insurance Brokerage

FINANCIALS1

• Assets: $9.1 billion

• Loans: $5.2 billion (75% marked)

• Deposits: $5.7 billion

• Wealth Management AUM: $5.2 billion

• Market Cap: ~$700 million

64 Branches in All Major Local Markets

Loans

Deposits

Covered

9%

Auto/ Commercial

Consumer 35%

25%

Residential

Mortgage

31%

Institutional Brokered

11% 16%

Retail

73%

(1) Balance sheet and branch data as of 12/31/12, market capitalization as of 4/23/13

3

COMPLETE TRANSFORMATION

2007

Growth & Deleveraging

BBVA PR Acquisition

December 2012

Eurobank Acquisition

April 2010

TODAY

• Secondary bank

• Niche products and services

• Earnings driven by investment securities

• Reliance on repos

• Full service commercial-consumer bank

• #1 in auto loans among PR banks

• Earnings increasingly driven by loans and wealth management

• Reliance on core deposits

4

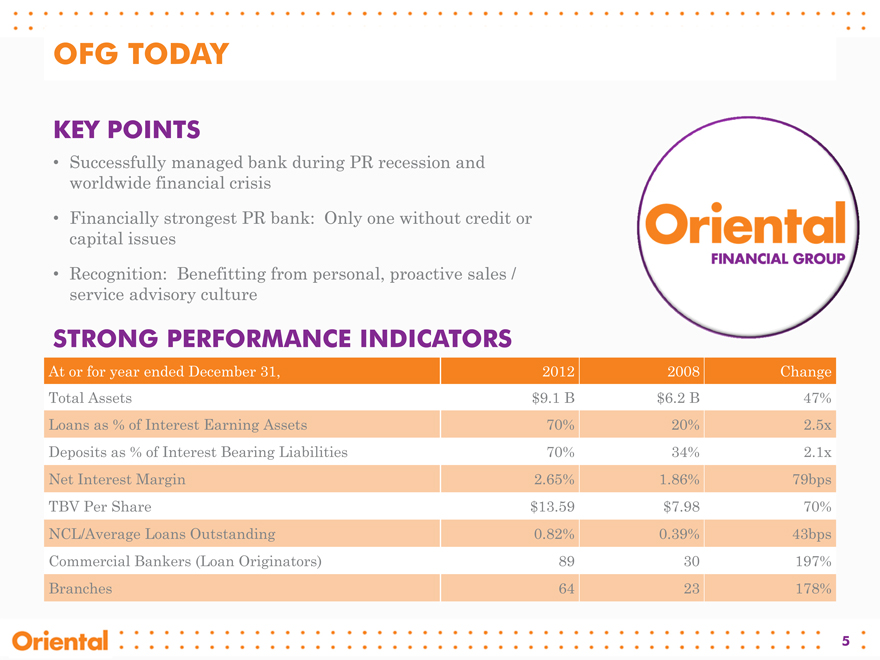

OFG TODAY

KEY POINTS

• Successfully managed bank during PR recession and worldwide financial crisis

• Financially strongest PR bank: Only one without credit or capital issues

• Recognition: Benefitting from personal, proactive sales / service advisory culture

STRONG PERFORMANCE INDICATORS

At or for year ended December 31, 2012 2008 Change

Total Assets $9.1 B $6.2 B 47%

Loans as % of Interest Earning Assets 70% 20% 2.5x

Deposits as % of Interest Bearing Liabilities 70% 34% 2.1x

Net Interest Margin 2.65% 1.86% 79bps

TBV Per Share $13.59 $7.98 70%

NCL/Average Loans Outstanding 0.82% 0.39% 43bps

Commercial Bankers (Loan Originators) 89 30 197%

Branches 64 23 178%

5

MAJOR GROWTH OPPORTUNITIES

Business

Tactical

Strategic

Financial

• Exploit larger scale and platform, proactive client-oriented culture, to sell into 3X customer base

• Expand market share in commercial, auto and consumer lending as well as continue to gain share of core deposit market, taking advantage of market disruption and relatively weaker competition

• Employ operating leverage to enhance earnings

• Cross sell wealth management services, reduce cost of funds, effect cost synergies from acquisition, wind down FDIC loss share amortization

• Restore TBV from dilution from BBVA PR acquisition within two years

• PR market lacks differentiation among most banks

• Continue developing our strong culture in advice, sales and service, to attract customers and become the leading bank in Puerto Rico

• Target +1% ROA, +12% ROE, efficiency ratio in low 50s, consistent performance

• Once integration efforts are completed, consider increasing dividends, buying back shares or possible acquisition of complementary businesses

6

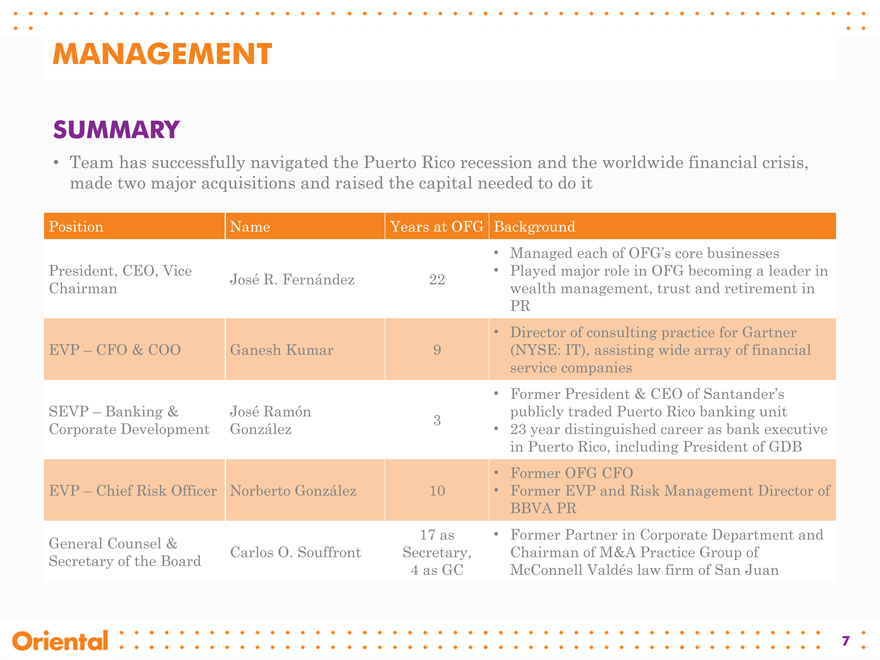

MANAGEMENT

SUMMARY

• Team has successfully navigated the Puerto Rico recession and the worldwide financial crisis, made two major acquisitions and raised the capital needed to do it

Position Name Years at OFG Background

• Managed each of OFG’s core businesses

President, CEO, Vice • Played major role in OFG becoming a leader in

José R. Fernández 22

Chairman wealth management, trust and retirement in

PR

• Director of consulting practice for Gartner

EVP – CFO & COO Ganesh Kumar 9(NYSE: IT), assisting wide array of financial

service companies

• Former President & CEO of Santander’s

SEVP – Banking & José Ramón publicly traded Puerto Rico banking unit

3

Corporate Development González • 23 year distinguished career as bank executive

in Puerto Rico, including President of GDB

• Former OFG CFO

EVP – Chief Risk Officer Norberto González 10 • Former EVP and Risk Management Director of

BBVA PR

General Counsel & 17 as • Former Partner in Corporate Department and

Carlos O. Souffront Secretary, Chairman of M&A Practice Group of

Secretary of the Board 4 as GC McConnell Valdés law firm of San Juan

7

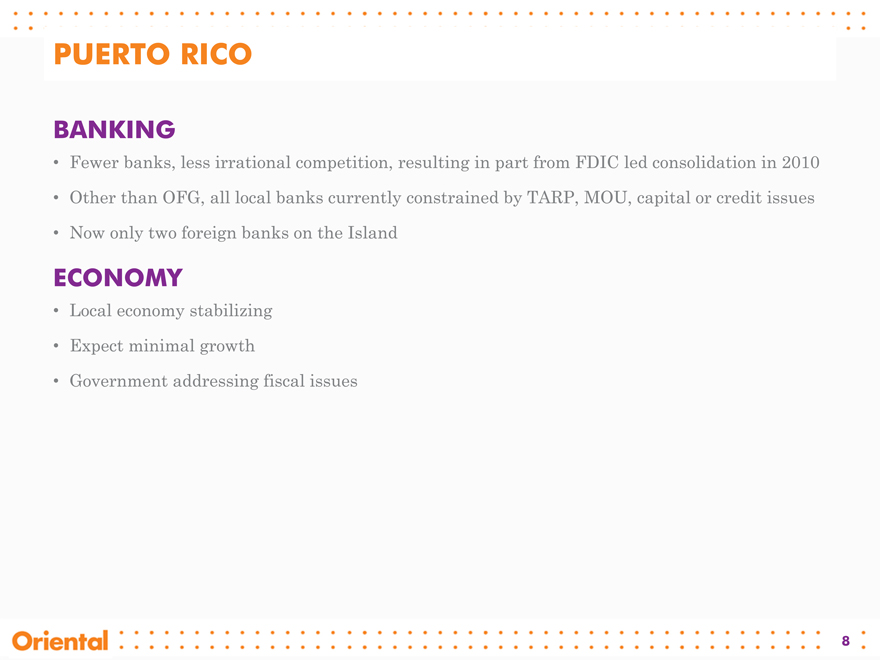

PUERTO RICO

BANKING

• Fewer banks, less irrational competition, resulting in part from FDIC led consolidation in 2010

• Other than OFG, all local banks currently constrained by TARP, MOU, capital or credit issues

• Now only two foreign banks on the Island

ECONOMY

• Local economy stabilizing

• Expect minimal growth

• Government addressing fiscal issues

8

ORIENTAL FINANCIAL GROUP

FINANCIAL UPDATE AS OF 12/31/12

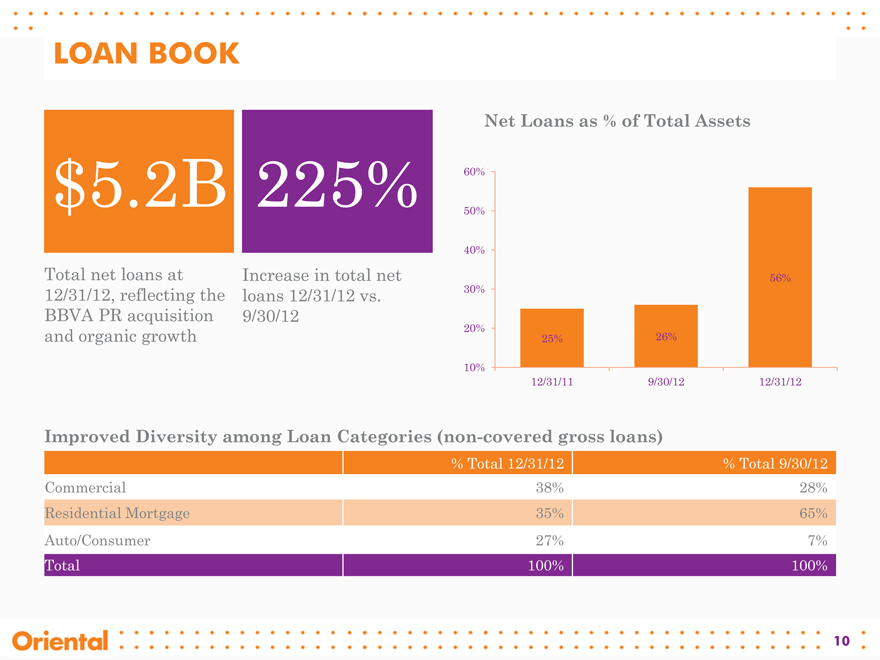

LOAN BOOK

$5.2B 225%

Net Loans as % of Total Assets

Total net loans at 12/31/12, reflecting the BBVA PR acquisition and organic growth

Increase in total net loans 12/31/12 vs. 9/30/12

60%

50%

40%

56%

30%

20%

25% 26%

10%

12/31/11 9/30/12 12/31/12

Improved Diversity among Loan Categories (non-covered gross loans)

% Total 12/31/12% Total 9/30/12

Commercial 38% 28%

Residential Mortgage 35% 65%

Auto/Consumer 27% 7%

Total 100% 100%

10

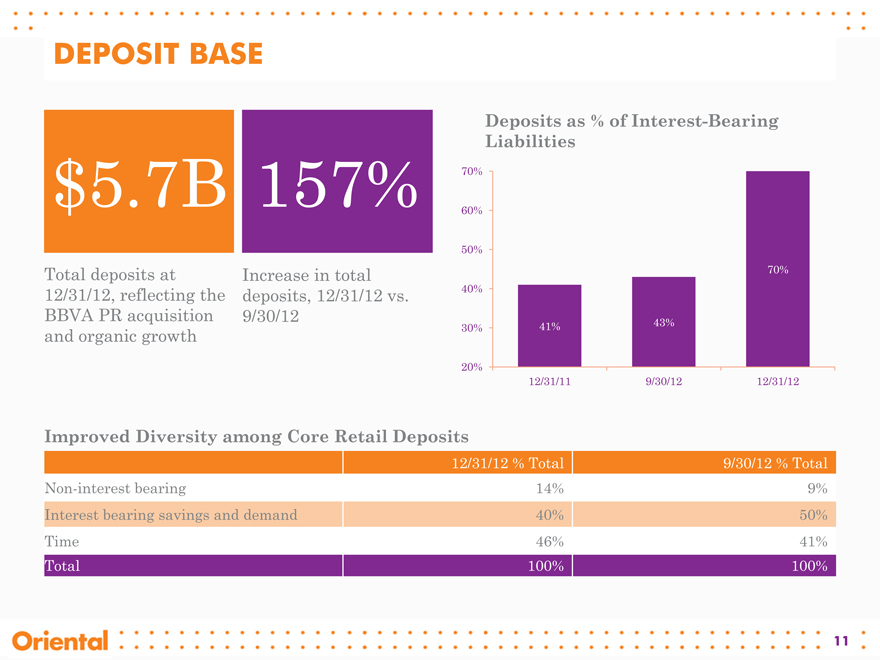

DEPOSIT BASE

$5.7B

157%

Total deposits at 12/31/12, reflecting the BBVA PR acquisition and organic growth

Increase in total deposits, 12/31/12 vs. 9/30/12

Deposits as % of Interest-Bearing

Liabilities

70%

60%

50%

70%

40%

30% 41% 43%

20%

12/31/11 9/30/12 12/31/12

Improved Diversity among Core Retail Deposits

12/31/12 % Total 9/30/12 % Total

Non-interest bearing 14% 9%

Interest bearing savings and demand 40% 50%

Time 46% 41%

Total 100% 100%

11

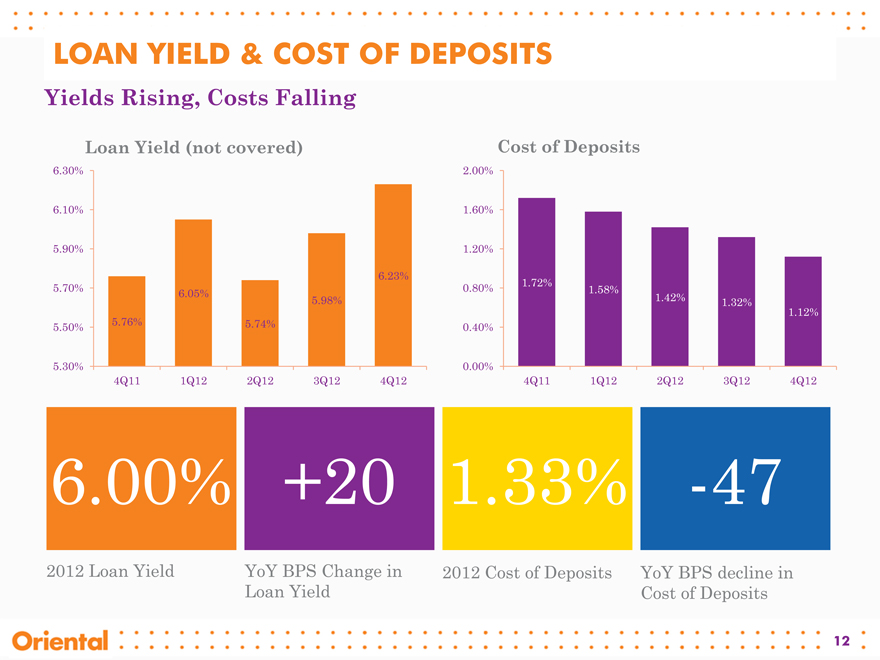

LOAN YIELD & COST OF DEPOSITS

Yields Rising, Costs Falling

Loan Yield (not covered)

Cost of Deposits

6.30%

6.10%

5.90%

6.23%

5.70% 6.05%

5.98%

5.50% 5.76% 5.74%

5.30%

4Q11 1Q12 2Q12 3Q12 4Q12

2.00%

1.60%

1.20%

0.80% 1.72% 1.58%

1.42% 1.32%

1.12%

0.40%

0.00%

4Q11 1Q12 2Q12 3Q12 4Q12

6.00% +20 1.33% -47

2012 Loan Yield YoY BPS Change in 2012 Cost of Deposits YoY BPS decline in Loan Yield Cost of Deposits

12

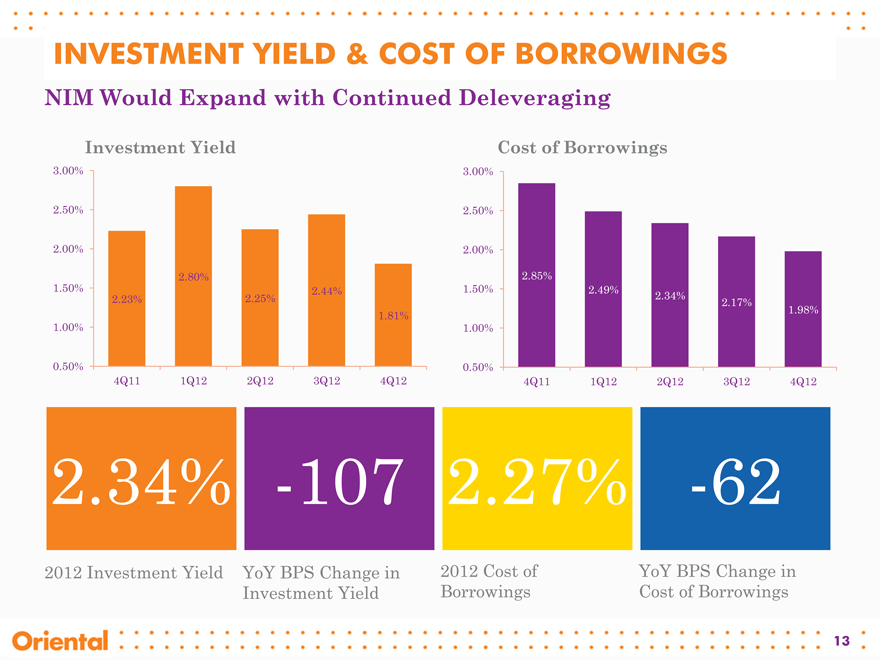

INVESTMENT YIELD & COST OF BORROWINGS

NIM Would Expand with Continued Deleveraging

Investment Yield

3.00%

2.50%

2.00%

2.80%

1.50% 2.44%

2.23% 2.25%

1.81%

1.00%

0.50%

4Q11 1Q12 2Q12 3Q12 4Q12

Cost of Borrowings

3.00%

2.50%

2.00%

2.85%

1.50% 2.49% 2.34%

2.17% 1.98%

1.00%

0.50%

4Q11 1Q12 2Q12 3Q12 4Q12

2.34% -107 2.27% -62

2012 Investment Yield YoY BPS Change in 2012 Cost of YoY BPS Change in Investment Yield Borrowings Cost of Borrowings

13

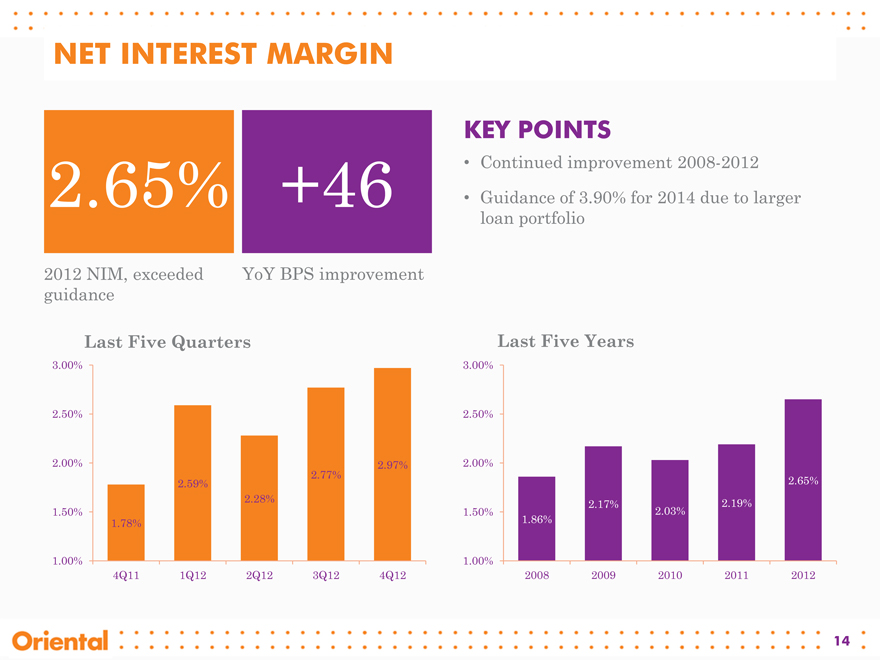

NET INTEREST MARGIN

2.65% +46

2012 NIM, exceeded YoY BPS improvement guidance

KEY POINTS

• Continued improvement 2008-2012

• Guidance of 3.90% for 2014 due to larger loan portfolio

Last Five Quarters

3.00%

2.50%

2.00% |

| 2.97% |

2.77%

2.59%

2.28%

1.50%

1.78%

1.00%

4Q11 1Q12 2Q12 3Q12 4Q12

Last Five Years

3.00%

2.50%

2.00%

2.65%

2.17% |

| 2.19% |

1.50% |

| 2.03% |

1.86%

1.00%

2008 2009 2010 2011 2012

14

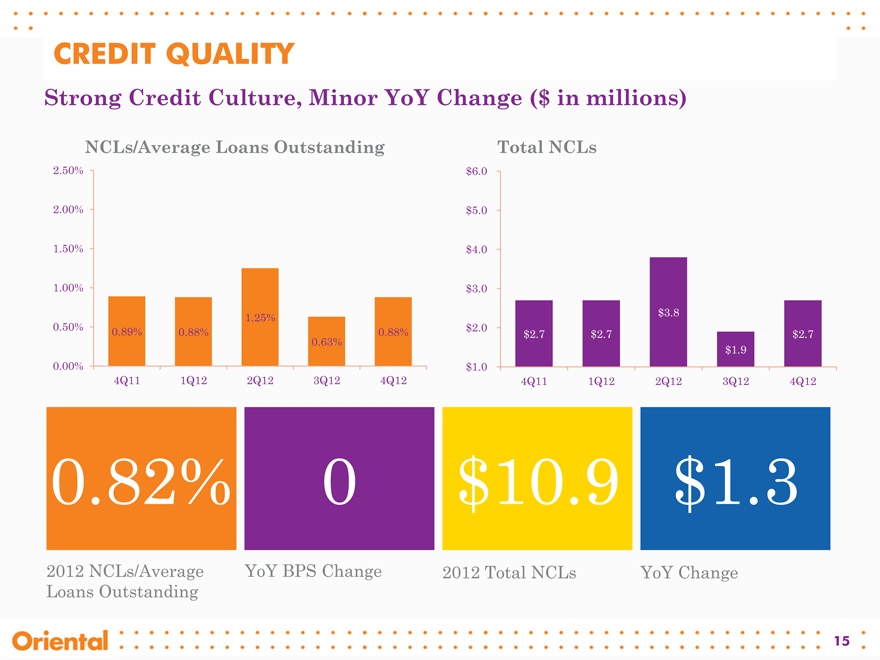

CREDIT QUALITY

Strong Credit Culture, Minor YoY Change ($ in millions)

NCLs/Average Loans Outstanding

2.50%

2.00%

1.50%

1.00%

1.25%

0.50% 0.89% 0.88% 0.88%

0.63%

0.00%

4Q11 1Q12 2Q12 3Q12 4Q12

Total NCLs

$ 6.0

$ 5.0

$ 4.0

$ 3.0

$ 3.8

$ 2.0 $ 2.7 $ 2.7 $ 2.7

$ 1.9

$ 1.0

4Q11 1Q12 2Q12 3Q12 4Q12

0.82% 0 $10.9 $1.3

2012 NCLs/Average YoY BPS Change 2012 Total NCLs YoY Change Loans Outstanding

15

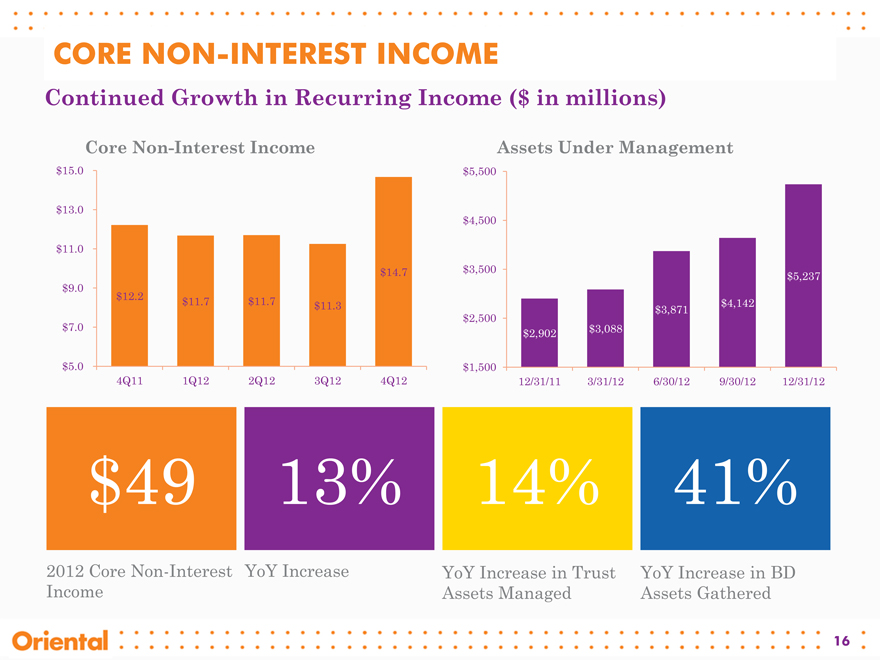

CORE NON-INTEREST INCOME

Continued Growth in Recurring Income ($ in millions)

Core Non-Interest Income

$15.0

$13.0

$11.0

$14.7

$9.0

$12.2

$11.7 |

| $11.7 $11.3 |

$7.0

$5.0

4Q11 1Q12 2Q12 3Q12 4Q12

Assets Under Management

$ 5,500

$ 4,500

$ 3,500 $ 5,237

$ 3,871 $ 4,142

$ 2,500

$ 2,902 $ 3,088

$ 1,500

12/31/11 3/31/12 6/30/12 9/30/12 12/31/12

$49 13% 14% 41%

2012 Core Non-Interest YoY Increase YoY Increase in Trust YoY Increase in BD Income Assets Managed Assets Gathered

16

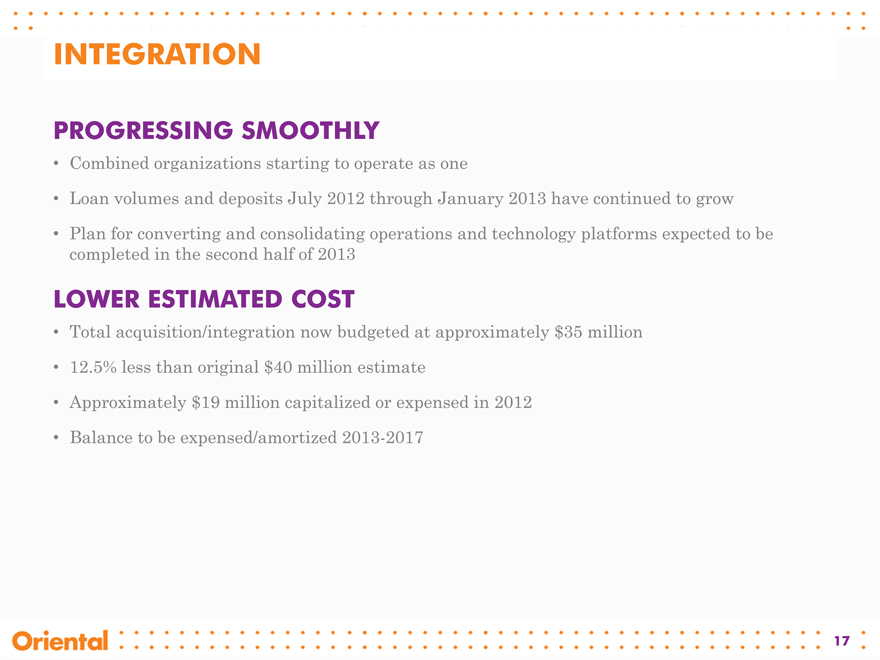

INTEGRATION

PROGRESSING SMOOTHLY

• Combined organizations starting to operate as one

• Loan volumes and deposits July 2012 through January 2013 have continued to grow

• Plan for converting and consolidating operations and technology platforms expected to be completed in the second half of 2013

LOWER ESTIMATED COST

• Total acquisition/integration now budgeted at approximately $35 million

• 12.5% less than original $40 million estimate

• Approximately $19 million capitalized or expensed in 2012

• Balance to be expensed/amortized 2013-2017

17

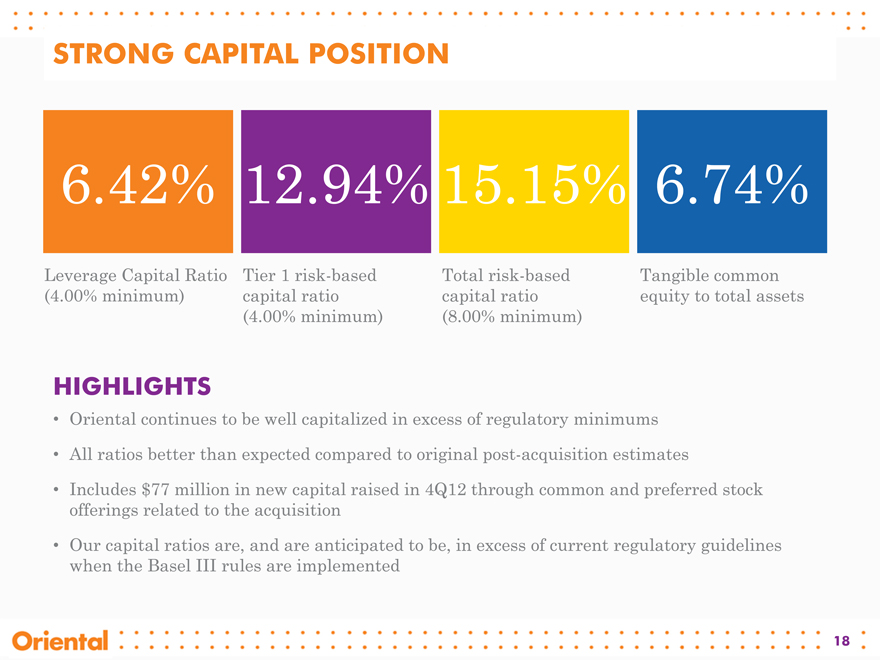

STRONG CAPITAL POSITION

6.42% 12.94% 15.15% 6.74%

Leverage Capital Ratio Tier 1 risk-based Total risk-based Tangible common (4.00% minimum) capital ratio capital ratio equity to total assets (4.00% minimum) (8.00% minimum)

HIGHLIGHTS

• Oriental continues to be well capitalized in excess of regulatory minimums

• All ratios better than expected compared to original post-acquisition estimates

• Includes $77 million in new capital raised in 4Q12 through common and preferred stock offerings related to the acquisition

• Our capital ratios are, and are anticipated to be, in excess of current regulatory guidelines when the Basel III rules are implemented

18

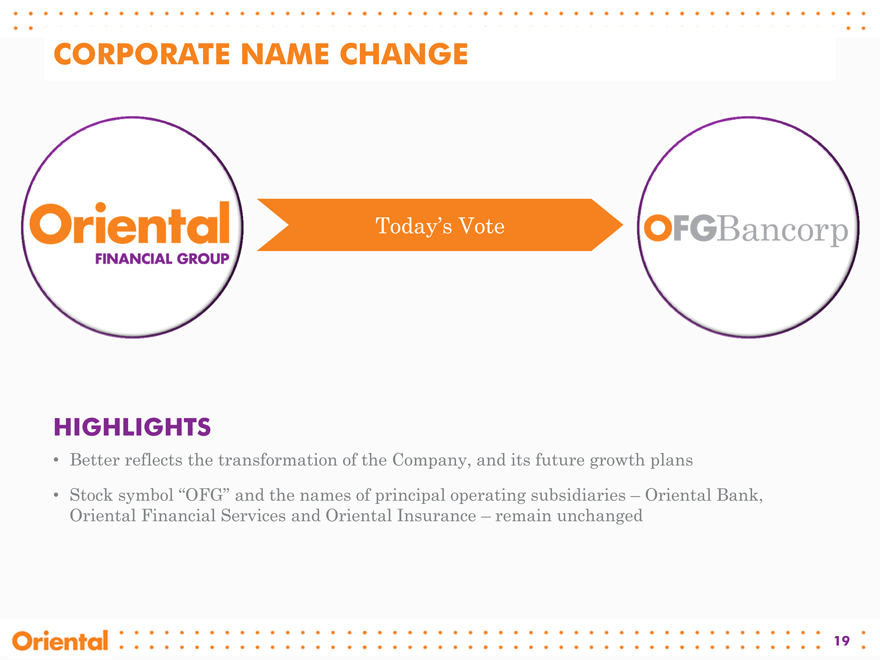

CORPORATE NAME CHANGE

Today’s Vote

HIGHLIGHTS

• Better reflects the transformation of the Company, and its future growth plans

• Stock symbol “OFG” and the names of principal operating subsidiaries – Oriental Bank, Oriental Financial Services and Oriental Insurance – remain unchanged

19