UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

| | | | | | | | |

| ☑ | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 2024

or

| | | | | | | | |

| ☐ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to

Commission file number: 001-13461

Group 1 Automotive, Inc.

(Exact name of registrant as specified in its charter)

| | | | | | | | | | | |

| Delaware | | 76-0506313 |

| (State or other jurisdiction of incorporation or organization) | | (I.R.S. Employer Identification No.) |

| 730 Town and Country Blvd | Suite 500 | | 77024 |

| Houston, | TX | | (Zip code) |

| (Address of principal executive offices) | | |

(713) 647-5700

(Registrant’s telephone number, including area code)

Not Applicable

(Former name, former address and former fiscal year, if changed since last report)

| | | | | | | | | | | | | | |

| Securities registered pursuant to Section 12(b) of the Act: |

| Title of each class | | Ticker symbol(s) | | Name of exchange on which registered |

| Common stock, par value $0.01 per share | | GPI | | New York Stock Exchange |

Securities registered pursuant to Section 12(g) of the Act: None.

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes þ No ¨

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ¨ No þ

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes þ No ¨

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes þ No ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company” and “emerging growth company” in Rule 12b-2 of the Exchange Act. (Check one):

| | | | | | | | | | | | | | |

| Large accelerated filer | þ | | ¨ | Accelerated filer |

| | | | |

| Non-accelerated filer | ¨ | | ☐ | Smaller reporting company |

| | | | |

| | | ☐ | Emerging growth company |

If an emerging growth company, indicate by check mark if that registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ¨

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report. ☑

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction of an error to previously issued financial statements. ¨

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrant’s executive officers during the relevant recovery period pursuant to §240.10D-1(b). ¨

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes ☐ No þ

The aggregate market value of common stock held by non-affiliates of the registrant was approximately $3.9 billion based on the reported last sale price of common stock on June 30, 2024, which was the last business day of the registrant’s most recently completed second quarter.

As of February 7, 2025, there were 13,244,315 shares of our common stock, par value $0.01 per share, outstanding.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the registrant’s definitive proxy statement for its 2025 Annual Meeting of Stockholders, which will be filed with the Securities and Exchange Commission within 120 days of December 31, 2024, are incorporated by reference into Part III of this Form 10-K.

TABLE OF CONTENTS

| | | | | | | | |

| | |

| |

| |

| |

| Item 1. | | |

| Item 1A. | | |

| Item 1B. | | |

| Item 1C. | | |

| Item 2. | | |

| Item 3. | | |

| Item 4. | | |

| |

| |

| Item 5. | | |

| | |

| Item 7. | | |

| Item 7A. | | |

| Item 8. | | |

| Item 9. | | |

| Item 9A. | | |

| Item 9B. | | |

| Item 9C. | | |

| |

| |

| Item 10. | | |

| Item 11. | | |

| Item 12. | | |

| Item 13. | | |

| Item 14. | | |

| |

| |

| Item 15. | | |

| Item 16. | | |

| |

GLOSSARY OF DEFINITIONS

The following are abbreviations and definitions of terms used within this report: | | | | | | | | |

| Terms | | Definitions |

| AOCI | | Accumulated other comprehensive income (loss) |

| ASU | | Accounting Standards Update |

| | |

| DMS | | Dealer management system |

| EBITDA | | Earnings before interest, taxes, depreciation and amortization |

| EPS | | Earnings per share |

| EV | | Electric vehicle |

| F&I | | Finance, insurance and other |

| FASB | | Financial Accounting Standards Board |

| FMCC | | Ford Motor Credit Company |

| GBP | | British Pound Sterling (£) |

| | |

| OEM | | Original equipment manufacturer |

| PII | | Personally Identifiable Information |

| PRU | | Per retail unit |

| PSU | | Performance stock unit |

| ROU | | Right-of-use |

| RSA | | Restricted stock award |

| RSU | | Restricted stock unit |

| SEC | | Securities and Exchange Commission |

| SG&A | | Selling, general and administrative |

| SOFR | | Secured Overnight Financing Rate |

| | |

| USD | | United States Dollar |

| U.K. | | United Kingdom |

| U.S. | | United States of America |

| U.S. GAAP | | Accounting principles generally accepted in the U.S. |

| | |

| | |

| | |

| | |

CAUTIONARY STATEMENT ABOUT FORWARD-LOOKING STATEMENTS

Unless the context requires otherwise, references to “we,” “us,” “our”, “Group 1” or the “Company” are intended to mean the business and operations of Group 1 Automotive, Inc. and its subsidiaries.

This Annual Report on Form 10-K (this “Form 10-K”) includes certain “forward-looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995, Section 27A of the Securities Act of 1933, as amended (“Securities Act”) and Section 21E of the Securities Exchange Act of 1934, as amended (“Exchange Act”). These forward-looking statements include, but are not limited to, statements concerning the Company’s strategy, future operating performance, future liquidity and availability of financing, capital allocation, the completion of future acquisitions and divestitures, as well as the impact of cyberattacks or other privacy/data security incidents, business trends in the retail automotive industry, changes in regulations and potential changes in U.S. trade policy, including the imposition of tariffs and the resulting consequences. When used in this Form 10-K, the words “anticipate,” “believe,” “estimate,” “expect,” “intend,” “may” and similar expressions are intended to identify forward-looking statements.

These forward-looking statements are based on the Company’s expectations and beliefs as of the date of this Form 10-K concerning future developments and their potential effect on the Company. While management believes that these forward-looking statements are reasonable when and as made, there can be no assurance that future developments affecting the Company will be those that are anticipated. The Company’s forward-looking statements involve significant risks and uncertainties that could cause actual results to differ materially from those in the forward-looking statements, including, but not limited to, the risks set forth in Item 1A. Risk Factors of this Form 10-K.

Readers are cautioned not to place undue reliance on forward-looking statements, which speak only as of the date hereof. The Company undertakes no responsibility and expressly disclaims any duty, to update any such statements, whether as a result of new information, new developments or otherwise, or to publicly release the result of any revision the forward-looking statements after the date they are made, except to the extent required by law.

PART I

Item 1. Business

General

Group 1 Automotive, Inc. is a leading operator in the automotive retail industry. We sell and/or lease new and used cars and light trucks; arrange related vehicle financing; sell service and insurance contracts; provide automotive maintenance and repair services; and sell vehicle parts retail and wholesale. We have operations in geographically diverse markets that extend across 17 states in the U.S. and 72 towns and cities in the U.K. As of December 31, 2024, our retail network consists of 145 dealerships and 27 collision centers in the U.S. and 114 dealerships and 12 collision centers in the U.K.

Discontinued Operations

Discontinued operations within the Consolidated Statements of Operations consists of activity associated with our Brazil operations, which were disposed of during the year ended December 31, 2022. Refer to Note 4. Discontinued Operations and Other Divestitures within the Notes to Consolidated Financial Statements for additional information regarding business dispositions. Unless otherwise specified, disclosures in this Form 10-K reflect continuing operations only.

Dealership Operations

Our new vehicle revenues include new vehicle sales and lease transactions, completed at our dealerships or via our digital platform, AcceleRide®. We sell retail used vehicles directly to our customers at our dealerships and via AcceleRide® and wholesale our used vehicles at third-party auctions. We sell replacement parts and provide both warranty and non-warranty maintenance and repair services at each of our franchised dealerships, as well as provide collision repair services at the 39 collision centers that we operate. We also sell parts to wholesale customers. Revenues from our F&I operations consist primarily of fees for arranging financing and selling vehicle service and insurance contracts in connection with the retail sale of a new or used vehicle. We offer a wide variety of third-party finance, vehicle service and insurance products in a convenient manner at competitive prices.

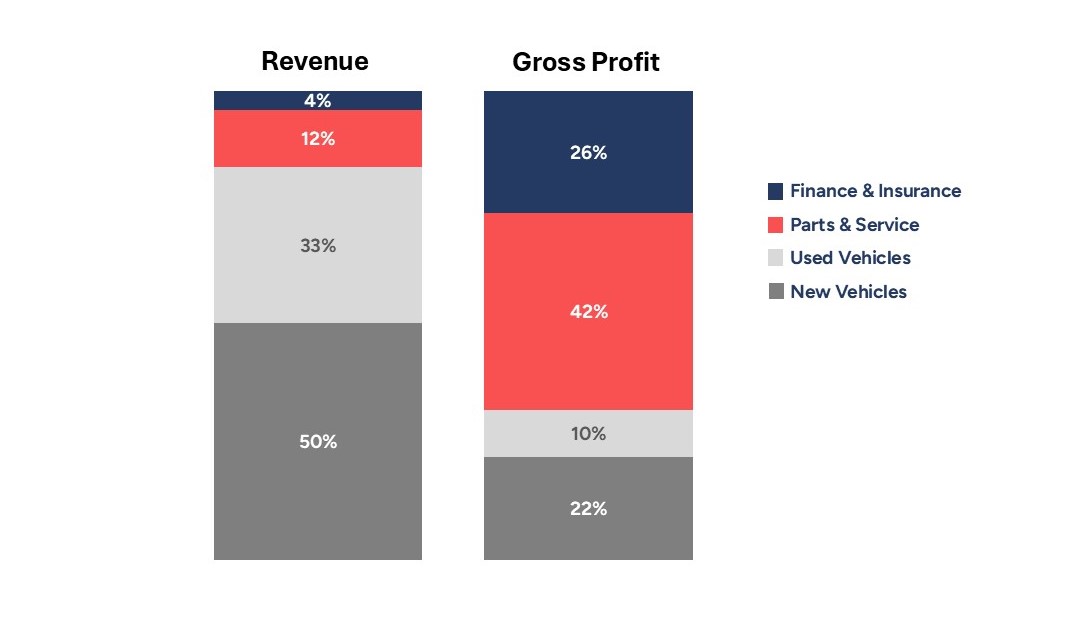

The following charts present total revenues and gross profit contribution from our operations by new vehicles, used vehicles, parts and service and F&I for the year ended December 31, 2024 (“Current Year”):

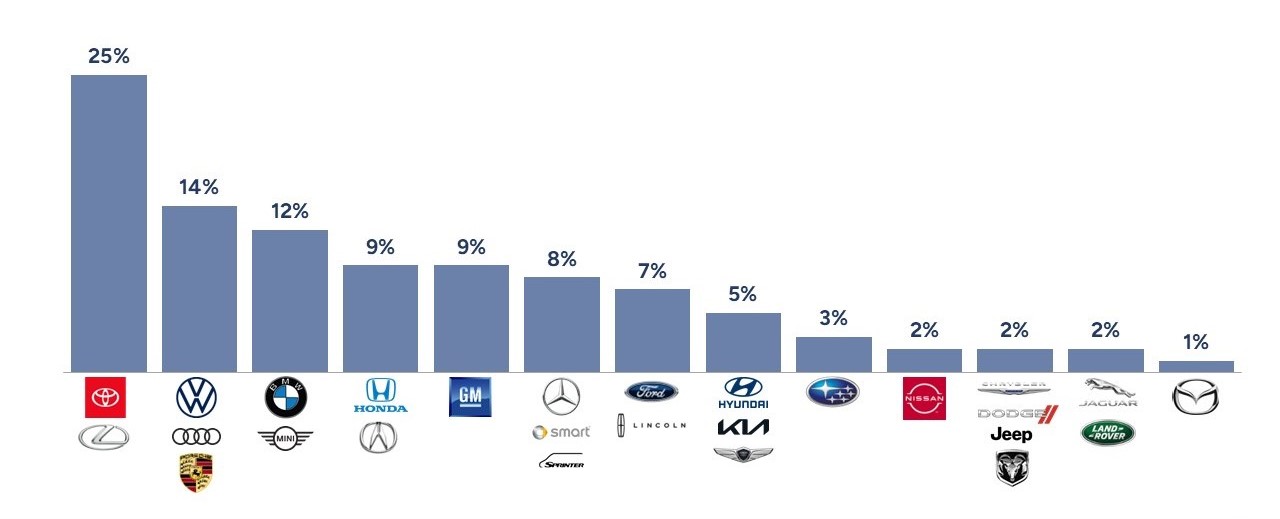

The following chart presents our diversity of new vehicle unit sales by manufacturer for the Current Year:

The following table shows our new vehicle unit sales geographic mix for the Current Year and our franchise count as of December 31, 2024:

| | | | | | | | | | | | | | | | | |

| | | New vehicle unit sales geographic mix (%) | | Franchises |

| Region | Geographic Market | | | | |

| U.S. | Texas | | 33.5 | % | | 70 |

| Massachusetts | | 7.8 | % | | 20 |

| California | | 7.2 | % | | 7 |

| Oklahoma | | 5.0 | % | | 19 |

| Georgia | | 3.5 | % | | 9 |

| Maryland | | 3.5 | % | | 7 |

| Florida | | 2.7 | % | | 5 |

| New Mexico | | 2.4 | % | | 7 |

| New Hampshire | | 2.3 | % | | 5 |

| South Carolina | | 2.1 | % | | 6 |

| New Jersey | | 2.0 | % | | 8 |

| Maine | | 1.5 | % | | 6 |

| Louisiana | | 1.3 | % | | 6 |

| Kansas | | 1.0 | % | | 3 |

| New York | | 0.8 | % | | 2 |

| Mississippi | | 0.4 | % | | 1 |

| Alabama | | 0.2 | % | | 1 |

| | | 77.4 | % | | 182 |

| | | | | |

| U.K. | United Kingdom | | 22.6 | % | | 153 |

| | | | | |

| | | 100.0 | % | | 335 | |

Business Strategy

Our business strategy is built on our commitment to maximize the return on investment for our stockholders. We intend to execute our business strategy through three interrelated pillars:

•Growth;

•Local Scale; and

•Full Rooftop Potential.

Growth

Allocating our shareholders’ capital in support of maximizing our return on investment is our highest priority. When evaluating an acquisition, we run disciplined valuation models, with expectations based on our experience, incorporating growth and investment. We then compare the projected acquisition return to the expected return of repurchasing shares of our common stock, repaying debt, or using the capital for other uses.

In 2024, we completed the acquisition of Inchcape Retail automotive operations (“Inchcape Retail”) in the U.K., consisting of 54 dealership locations, certain real estate and three collision centers (the “Inchcape Acquisition”). The Inchcape Acquisition approximately doubled our portfolio across the U.K.

Consistent with our acquisition activity completed in 2022 through 2024, we intend to pursue opportunities in growth-positioned markets that are economically accretive to our existing markets. Our focus is on brand, geographic fit, and large dealership operations and/or dealership clusters that will provide attractive returns to our portfolio. Acquisitions completed within our existing markets or large dealership groups allow us to capitalize on economies of scale and provide for cost saving opportunities in key expense areas such as used vehicle sourcing, advertising, purchasing, data processing and personnel utilization. In addition to cost savings opportunities, scale enables us to make the EV, facility, compliance, real estate, personnel development and training, and technology investments necessary to thrive in today’s retail automotive industry.

Acquisition success depends upon our relationship with our OEM partners. We work closely with our OEMs and regularly communicate with them regarding material sourcing, marketing, recalls, safety and other factors that influence our business relationship and the customer experience. We seek to perform well in the markets in which we operate, generally meeting or exceeding OEM metrics on market share and customer retention. Each OEM has acquisition eligibility criteria and our ability to meet these criteria across multiple brands provides an advantage to executing a growth strategy. We believe we can buy nearly any brand, so we can be selective with our acquisition target criteria. We believe we have access to a broader selection of assets and asset groups, some of which require the significant capital investment our scale allows, given our ability to operate successfully across multiple brand partners.

In addition to expanding our portfolio through acquisitions, from time to time, we make decisions to optimize our portfolio by disposing of certain assets or operations. In some instances, we dispose of underperforming dealerships which do not meet our return objectives. We may also dispose of certain dealerships in order to complete strategic acquisition opportunities. Specifically, we may dispose of a less significant dealership to allow us to acquire a more substantial dealership within the same or another geographic area based on the ownership limitations imposed in our franchise agreements.

Refer to Note 3. Acquisitions and Note 4. Discontinued Operations and Other Divestitures within the Notes to Consolidated Financial Statements, for additional information regarding our acquisitions and dispositions.

Local Scale

We believe capturing opportunities from building local scale will provide us a competitive advantage and leverage through greater market representation and facilitate an improved customer experience.

With our expansive portfolio of brands and service capabilities across significant geographical areas, we believe we can service the needs of our customers’ full families and friends. Using local scale, we will leverage our marketing prowess to drive business within our dealership clusters, while providing our customers a unique value proposition. We are growing and developing our retail talent internally by creating retail training academies within cluster markets. Our training is focused on creating consistent customer experiences across our rooftops. In addition to the enhancement of customer experience, local scale also allows us to reimagine how we handle our used vehicle inventory, including reconditioning and vehicle positioning. We are focused on reducing the cost and increasing throughput efficiency of our vehicle reconditioning operations, by establishing a more consistent approach to reconditioning. Lower costs drive higher shareholder returns and faster reconditioning gives our staff back a valuable resource, time, which can be spent improving customer retention through more customer interaction. Our business relies upon maximizing positive customer interactions to drive repeat and referral sales and service business. Disciplined inventory positioning, using our dealership clusters to best position used vehicles, allows us to drive the highest value.

Full Rooftop Potential

We seek to optimize our operations at each of our rooftops including leveraging our dealership’s full potential and local scale advantage to improve operational efficiency. This includes focusing on operational excellence at each dealership and other facilities, including, but not limited to, standardization of key common processes and taking advantage of shareable business resources. We believe our operations optimization efforts will provide a strategic advantage by structurally lowering our operating costs.

As innovative tools become available, we seek to quickly adopt those that provide a mutual benefit to our customers and Group 1. We want to replicate and grow our best practices across rooftops. Our scale amplifies the impact of replicating best practices and best practices lead to additional value extraction from existing stores and acquisition opportunities, which we believe to be a competitive advantage. We are prioritizing five areas for development in 2025.

F&I

We are piloting programs that enhance the in-store and online F&I experience, allowing our customers to shop how they want, when they want, while improving the speed of service within our dealerships. In addition, we believe we can extract further value from our top F&I performers by better managing their customer workflow, coupled with the assistance of virtual-based technology enhancements.

Procurement

We believe our scale provides us an advantage in the form of leverage to further improve our dealership costs. We continue to negotiate discounts, service level improvements and preferential pricing from suppliers to our dealerships through providers who can service multiple locations across more than one geographic market. We also routinely evaluate dealership processes with the purpose of identifying best practices which can be shared amongst our dealership operations.

Used Vehicle Purchasing and Transfers

Used vehicle profits are dependent on sourcing and our ability to fairly value the purchases we make. We have invested heavily in the technologies and processes we use to value used vehicle inventory. We have partnered with service providers to enable us to generate the most competitive market pricing available, across our dealership network.

We sell multiple brands in most markets in which we operate through our franchised dealer network. We have thousands of customers enter our stores daily. We have invested in the people and processes at many of our stores to enable used vehicle sourcing directly from the service drive. As a result, we are able to offer many of our customers a value for their car at every service visit, leading to significant organic sourcing. We are perfecting these best practices for replication across our dealerships.

In addition to sourcing, we have the ability to leverage our clusters of dealerships to sell our vehicles in the most advantageous location. We have developed disciplined processes to control the movement of our used vehicle inventory in order to maximize the selling price and throughput within our market clusters.

Customer Experience Center

We utilize central customer service centers to support our dealerships. We are investing in and developing new ways to support our customers and their dealership experience. We know that customers have challenges connecting with dealership personnel which is why we have developed processes to enable our centralized customer service centers to better assist our customers with their in-store needs. Whether that be vehicle service status or the availability of advertised vehicles, we believe our centralized customer service centers can further assist customers, improving the customer experience, if they are provided with the necessary tools and data.

Talent Management, Succession Planning and Workforce Evolution

To help our workforce feel heard and supported, we solicit employee feedback through multiple channels. We leverage our intracompany communication platform to bring our teams together digitally and provide our leadership team with the ability to interact in more frequent, engaging and direct communication with our employees. Our management team routinely visits our stores, meeting with and soliciting feedback from employees at all levels. The results of the annual engagement survey and employee discussions inform our overall human capital management methods and other growth strategies.

In addition to providing career growth pathways for employees, our Board of Directors annually reviews management’s succession planning for key positions throughout the organization. We routinely provide leadership training to key management personnel at varying levels within the organization in support of our employees. This training is designed to benefit the individual receiving the training as well as the workforce managed by those managers.

We are focused on attracting, developing, mentoring and retaining top talent. We routinely create and offer department or job-specific training and professional development opportunities to meet employees’ needs. Investments in our facilities and planned investments provide our employees working environments to meet their needs and the needs of the future.

In addition to our broader workforce, we are focused on retaining and hiring technicians. We believe we have sufficient facility capacity to support these technicians and do not view stall count as a limiter in growing our technician staffing. We have several stores where our technician headcount exceeds the stall count. Our scheduling methods and offering of a four day work week in many of our U.S. shops allow us to maximize our stall and technician utilization. Our technicians benefit from ongoing initiatives to provide air conditioning in shops with more difficult weather conditions, Group 1 training academies to support career growth and development and competitive wages and benefits.

Competition

The automotive retail industry is highly competitive across all our service lines. Consumers have a number of choices when deciding where and how to (i) purchase and/or lease a new or used vehicle as well as select related vehicle financing and insurance products; (ii) purchase related parts and accessories; and (iii) procure vehicle maintenance and repair services. We believe the principal competitive factors in the automotive retailing industry are location, service, price, selection, online capabilities, established customer relationships and reputation.

New Vehicles Sales

In the new vehicle market, our dealerships compete with other franchised dealerships in their market areas, as well as auto brokers, leasing companies and internet companies that provide referrals to, or broker vehicle sales with other dealerships or customers. Our principal new vehicle dealer competitors also have franchise agreements with the various vehicle manufacturers and, as such, generally have access to new vehicles on the same terms as we do. We do not have any cost advantage in purchasing new vehicles from vehicle manufacturers, and our current franchise agreements do not grant us the exclusive right to sell a manufacturer’s product within a given geographic area. Several companies are currently manufacturing EVs for sale primarily through the internet, under a direct-to-consumer model, without using the traditional dealer-network or are considering such a strategy, including some of our OEM partners. Certain of our vehicle manufacturers in the U.K. recently transitioned to an agency model for selling new vehicles. Under an agency model, our franchised dealerships receive a fee for facilitating the sale of a new vehicle to a customer but no longer record the vehicle sales price as revenue, record vehicles in inventory, incur loaner expense, or incur floorplan interest expense, as has been historical practice.

Used Vehicle Sales

In the used vehicle market, our dealerships compete both in their local markets and nationally with other franchised dealers, large multi-location used vehicle retailers, local independent used vehicle dealers, automobile rental agencies and private parties for the supply and resale of used vehicles.

Parts and Service

We believe the principal competitive factors in the parts and service business are the quality of customer service, timeliness of service, the use of factory-approved replacement parts, familiarity with a manufacturer’s brands and models, location, price, the availability and competence of technicians, and the availability of training programs to enhance such expertise. In the parts and service market, our dealerships compete with other franchised dealers to perform warranty maintenance and repairs, conduct manufacturer recall services and sell factory replacement parts. Our dealerships also compete with other automobile dealers, franchised and independent service center chains and independent repair shops for non-warranty repair and maintenance business. In addition, our dealerships sell replacement and aftermarket parts both locally and nationally in competition with franchised and independent retail and wholesale parts outlets. A number of regional or national chains offer selected parts and services at prices that may be lower than ours. Our collision centers compete with other large, multi-location companies, as well as local, independent, collision service operations.

F&I

We believe the principal competitive factors in the F&I business are convenience, interest rates, product availability and affordability, product knowledge, flexibility in contract length and ease of consumer understanding. We face competition in arranging financing for our customers’ vehicle purchases from a broad range of unaffiliated third-party financial institutions. Many financial institutions now offer their own menu of F&I products, providing an alternative to our product offering, which may reduce our profits from the sale of these products through reduced penetration. In certain cases, our customers in the normal course of business can cancel previously purchased F&I products resulting in the charge back to us by the product provider of a portion of the profit earned on the sale of those products.

Manufacturers’ Relationships and Agreements

Each of our U.S. dealerships operates under one or more franchise agreements with vehicle manufacturers or authorized distributors. The franchise agreements grant the franchised automobile dealership a non-exclusive right to sell the manufacturers or distributor’s brand of vehicles and offer related parts and service within a specified market area. These franchise agreements also grant franchised dealerships the right to use the manufacturer’s or distributor’s trademarks in connection with their operations, and impose numerous operational requirements and restrictions relating to, among other things, inventory levels, working capital levels, the sales process, sales performance requirements, customer satisfaction standards, marketing and branding, facility standards and signage, personnel, changes in management, change in control and monthly financial reporting.

Most of our U.S. dealerships’ franchise agreements continue indefinitely and those with finite terms are renewed or superseded by a new agreement. In the U.K., many of our agreements have two-year rolling terms. Each of our franchise agreements may be terminated or not renewed by the manufacturer for a variety of reasons, including network consolidation efforts, unapproved changes of ownership or management and performance deficiencies in such areas as sales volume, sales effectiveness and customer satisfaction. In most cases, manufacturers have renewed the franchises upon expiration so long as the dealership is in compliance with the terms of the agreement. We diligently work with our manufacturers to address any performance issues.

Our dealership service departments perform vehicle repairs and service for customers under manufacturer warranties. We are reimbursed for those repairs and service by the manufacturer. Some manufacturers offer rebates to new vehicle customers, which we are required, under specific program rules, to adequately document, support and collect. In addition, some manufacturers provide us with incentives to order and/or sell certain models and/or volumes of inventory over designated periods of time. Under the terms of our dealership franchise agreements, the respective manufacturers are able to perform warranty, incentive and rebate audits and charge us back for unsupported or non-qualifying warranty repairs, rebates or incentives.

In addition to the individual dealership franchise agreements discussed above, we have entered into framework agreements in the U.S. with most major vehicle manufacturers and distributors. These agreements impose a number of restrictions on our operations, including our ability to make acquisitions and obtain financing, and on our management. These agreements also contain change of control provisions related to the ownership of our common stock. For a discussion of these restrictions and the risks related to our relationships with vehicle manufacturers, please refer to Item 1A. Risk Factors.

Governmental Regulations

Automotive and Other Laws and Regulations

We operate in a highly regulated industry. A number of laws and regulations applicable to automotive companies affect our business and conduct, including, but not limited to our sales, operations, financing, insurance, advertising and employment practices. These laws and regulations include state franchise laws and regulations, consumer protection laws and other extensive laws and regulations applicable to new and used motor vehicle dealers. Additionally, in every jurisdiction in which we operate, we must obtain various permits and licenses in order to conduct our business.

In general, the U.S. jurisdictions in which we operate have automotive dealership franchise laws, which generally provide that it is unlawful for a manufacturer or distributor to terminate or not renew a franchise unless “good cause” exists. As a result, it generally is difficult, outside of bankruptcy, for a manufacturer or distributor to terminate, or not renew, a franchise under these laws, which were designed to protect dealers.

The U.K. generally does not have automotive dealership franchise laws and, as a result, our U.K. dealerships operate without these types of specific protections. However, similar protections may be available as a matter of general U.K. contractual law. In addition, our U.K. dealerships are subject to U.K. antitrust rules prohibiting certain restrictions on the sale of new vehicles and spare parts and on the provision of repairs and maintenance. For instance, authorized dealers are generally able to, subject to manufacturer facility requirements, relocate or add additional facilities, offer multiple brands in the same facility, allow the operation of service facilities independent of new car sales facilities and ease restrictions on cross supplies (including on transfers of dealerships) between existing authorized dealers within the network. However, under the U.K. Motor Vehicle Block Exemption Order 2023 (applicable until May 31, 2029) certain restrictions on dealerships are permissible in franchise agreements provided certain conditions are met.

In the U.K., the Financial Conduct Authority (the “FCA”) regulates financial services firms and financial markets, including our activities in acting as broker for the financing of vehicle sales. In January 2024, the FCA announced that it planned to undertake a formal review into the historic use of discretionary commission arrangements (“DCA”s) amid concerns that the practice of linking brokers’ commissions to the interest rate charged to customers may have been unfair to customers, resulting in customers paying too much for their car loans.

Additionally in the U.K., on October 25, 2024, the U.K. Court of Appeal issued a judgment in the three joint appeals for Johnson v Firstrand Bank Ltd, Wrench v Firstrand Bank Ltd and Hopcraft v Close Brothers Ltd (collectively, the “COA litigation”), finding that the claimants in those cases are entitled to be paid a sum equivalent to the undisclosed commission paid by their lenders to the dealerships from which they acquired their cars, plus interest. Underlying the Court’s judgment were the findings that, among other things, brokers owe fiduciary and/or disinterested duties to customers, which, among other things, require disclosure to the customer of the rate and amount of the commission paid and the basis for its calculation. As a result, the failure to provide such full commission disclosure effectively results in the failure to obtain a customer’s fully informed consent to the payment of commission. The judgment also appears to extend beyond DCAs to address all commission disclosures generally. Finally, the U.K. Court of Appeal held where there is a failure to disclose, lenders and dealerships who acted as brokers are jointly and severally liable for the repayment of the commission.

After the U.K. Court of Appeal denied an initial application for permission to appeal, the motor finance dealers involved requested, and were granted permission, to appeal the decision directly to the Supreme Court of the United Kingdom. The Supreme Court of the United Kingdom is scheduled to hear the appeal on April 1 – 3, 2025. The final outcomes of the FCA’s DCA review and the COA litigation, including the appeal thereof to the Supreme Court of the United Kingdom, are uncertain. Any judicial outcome or regulatory redress scheme, which ultimately results in a wider legal or regulatory requirement to refund historical commissions paid to us, could materially and adversely affect our U.K. operations.

Data Privacy

We are subject to numerous laws and regulations designed to protect the information of clients, customers, employees and other third parties that we collect and maintain. Some of the more significant regulations that we are required to comply with include the U.K.’s General Data Protection Regulation (“U.K. GDPR”) and, the California Consumer Privacy Act, as amended and enhanced effective January 1, 2023 by the California Privacy Rights Act (as so amended, the “CCPA”), and the Federal Trade Commission (“FTC”) Safeguards Rule. These regulations provide for various data protection requirements related to protection of customer’s PII, notice requirements related to data breaches and obligations to inform a consumer, at or before collection, of the purpose and intended use of the collection, and to delete a consumer’s personal information upon request. If an organization violates the U.K. GDPR, the organization can be fined up to 4% of annual global turnover or 20 million euros, whichever is greater. The CCPA allows the California Attorney General to bring actions against non-compliant businesses with fines of $2,500 per violation or, if intentional, up to $7,500 per violation and permits a private right of action for certain violations of laws. The FTC Safeguards Rule contains procedural, technical and personnel requirements that financial institutions, including dealers, must satisfy to meet their information security obligations.

Environmental and Occupational Health and Safety Laws and Regulations

Our business activities in the U.S. and the U.K. are subject to stringent federal, state and local laws, regulations and other controls governing specific health and safety criteria to address worker protection, the release of materials into the environment or otherwise relating to environmental protection. Our operations involve the use, handling and storage of materials such as motor oil and filters, transmission fluids, antifreeze, refrigerants, paints, thinners, batteries, cleaning products, lubricants, degreasing agents, tires and fuel. We contract for recycling and/or disposal of used fluids, filters and other waste materials generated by our operations.

These laws, regulations and controls may impose numerous obligations on our operations including the acquisition of permits to conduct regulated activities, the imposition of restrictions on where or how to manage or dispose of used products and wastes, the incurring of capital expenditures to limit or prevent releases of such material, and the imposition of substantial liabilities for pollution resulting from our operations or attributable to former operations. For example, in the U.S., most of our dealerships utilize storage tanks that are subject to testing, containment, upgrading and removal regulations under the federal Resource Conservation and Recovery Act, analogous state statutes and their implementing regulations. Failure to comply with these laws, regulations and permits may result in the assessment of sanctions, including administrative, civil and criminal penalties, the imposition of investigatory remedial and corrective action obligations or increase of capital expenditures, restrictions, delays and cancellations in permitting or in the performance or expansion of projects and the issuance of injunctions limiting or preventing some or all of our operations in affected areas. Additionally, certain environmental laws may result in imposition of joint and several strict liability, which could cause us to become liable as a result of our conduct that was lawful at the time it occurred or the conduct of, or conditions caused by, prior operators or other third parties. For instance, an accidental release from one of our storage tanks could subject us to substantial liabilities arising from environmental cleanup and restoration costs, claims made by neighboring landowners and other third parties for personal injury and property damage and fines or penalties for related violations of environmental laws or regulations.

Properties that we now or have in the past owned or leased in the U.S. are subject to the federal Comprehensive Environmental Response, Compensation and Liability Act and similar state statutes. These statutes can impose strict and joint and several liability for cleanup costs on those that are considered to have contributed to the release of a hazardous substance, including for historic spills that occurred prior to our ownership of our properties even if we did not know of, or did not cause the release of such hazardous substances. We also are subject to the Clean Water Act, analogous state statutes, and their implementing regulations which, among other things, prohibit discharges of pollutants into regulated waters, require containment of potential discharges of oil or hazardous substances, and require preparation of spill contingency plans. Air emissions from some of our operations, such as vehicle painting, may be subject to the federal Clean Air Act and analogous laws. Laws and regulations protecting the environment are complex and generally become more stringent over time, which may result in increased costs for future environmental compliance and remediation. Comparable laws and regulations have been enacted in the U.K. Certain health and safety standards promulgated by the Occupational Safety and Health Administration of the U.S. Department of Labor and related state agencies also apply to our operations.

In recent years, the threat of climate change has attracted considerable attention in the U.S., U.K. and elsewhere globally. As a result, numerous proposals have been made at the international, national and state levels of government, in locations affecting our business, to monitor and limit existing emissions of greenhouse gas (“GHG”), as well as to restrict or eliminate such future emissions. In December 2023, the United Arab Emirates hosted the 28th session of the Conference of the Parties where parties signed onto an agreement to transition “away from fossil fuels in energy systems in a just, orderly and equitable manner” and increase renewable energy capacity so as to achieve net zero by 2050, although no detailed timeline for doing so was set. Subsequent conferences have sought to build on the Paris Agreement, a United Nations-sponsored, non-binding agreement for nations to limit their GHG emissions through individually determined reduction goals every five years after 2020, by calling for various countries to phase out fossil fuels and subsidies related to the same, though none have been legally binding. President Donald Trump issued a series of executive orders since taking office in January 2025, including an executive order withdrawing from the Paris Agreement. Refer to Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations — Recent Events, for additional information regarding these executive orders.

The U.K. is committed to the Paris Agreement, and announced that it plans to ban sales of new gasoline and diesel-powered vehicles after 2035. Similar planned bans have been announced in California, New Mexico, Massachusetts and New York. Additional regulation of GHG emissions could increase the cost of the vehicles sold to us. Government bans or restrictions on certain vehicle types could impact the mix of vehicles that we offer for sale. Consumer concerns regarding climate change could also alter consumer preferences and adversely affect our ability to market and sell vehicles. These developments could increase our costs of operation as well as reduce our volume of business. The full impact of these actions is uncertain at this time, though these international agreements have the potential to result in increased pressure from financial institutions and other stakeholders to eliminate or reduce fossil fuel use and GHG emissions related to the same.

Gas and diesel-powered automobiles are a source of GHG emissions and in the recent past, the U.S. Environmental Protection Agency (“EPA”), together with the National Highway Traffic Safety Administration (“NHTSA”), implemented GHG emissions limits on vehicles manufactured for operation in the U.S. Vehicle manufacturers in the U.S. are subject to regulations by the EPA and the NHTSA that establish corporate average fuel economy (“CAFE”) standards applicable to light-duty vehicles. These agencies have finalized more stringent standards for both heavy-duty and light-duty vehicles and for increased fuel economy for vehicles in upcoming model years. California and other states have indicated they would pursue more stringent CAFE and GHG standards than required by current EPA and NHTSA standards. Comparable laws and regulations have been enacted in the U.K, including updated standards for cars, vans and heavy-duty trucks for upcoming model years. Our OEMs require lead time to prepare new vehicle models and more stringent regulations could result in increased costs and time constraints or result in our OEMs deciding to increase production targets of EVs in anticipation of such regulations. These developments could also significantly increase our costs of operation as well as reduce our volume of business. For additional information, see Item 1A. Risk Factors.

On March 20, 2024, the EPA finalized new emissions standards for light and medium-duty vehicles, including passenger cars, vans, pickups, sedans and sport utility vehicles for model years 2027 through 2032 and beyond. The final rule sets new, strict standards intended to reduce air pollutant emissions, including GHG emissions; however, the new standards are now subject to legal challenge. The EPA projects the final rule will accelerate the transition to, and availability of, clean vehicle technologies, including hybrid EVs and plug-in hybrid EVs.

President Donald Trump issued a series of executive orders since taking office in January 2025, including executive orders impacting environmental regulations. Refer to Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations — Recent Events, for additional information regarding these executive orders.

Insurance and Bonding

Our operations expose us to the risk of various liabilities, including:

•claims by employees, customers or other third parties for personal injury or property damage;

•natural disasters, such as hail, flood, tornadoes, hurricanes and wildfires; and

•potential fines and civil and criminal penalties resulting from alleged violations of federal and state laws, regulatory requirements and other local laws in the jurisdictions in which we operate.

The automotive retailing business is also subject to substantial risk of real and personal property loss as a result of significant concentration of real and personal property values at dealership locations. Under self-insurance programs, we retain various levels of risk associated with aggregate loss limits and per claim deductibles. In certain cases, we insure costs in excess of our retained risk under various contracts with third-party insurance carriers. Although we believe our insurance coverage is adequate, we cannot be assured that we will not be exposed to uninsured losses that could have a material adverse effect on our business, results of operations and financial condition. We are also subject to potential premium cost fluctuations and changes in loss retention limits with the annual renewal of these programs.

For further discussion, refer to Item 1A. Risk Factors.

Human Capital Management

Our human capital strategy is focused on attracting, developing, motivating and retaining top talent that will drive our success, enabling us to deliver market-leading business results. We strive to solidify Group 1 as the preferred employer of choice in automotive retail. We also believe that our workforce should be representative of the communities we serve. We foster a workplace culture around our core values of integrity, transparency, professionalism, teamwork and respect.

As of December 31, 2024, we had 20,413 employees (full-time, part-time and temporary), of which 13,398 were employed in the U.S. and 7,015 in the U.K.

Employee Engagement

Employee engagement is key to driving long-term business success and supporting our way towards becoming a truly customer-centric organization, which drives value for our investors. The annual Group 1 “Your Voice Matters” Engagement Survey has become our primary employee listening platform for gathering feedback and promoting a performance-based culture. That feedback provides us with valuable insight into employees’ perception of workplace culture and progress on our corporate mission. The results inform our overall human capital management methods and other growth strategies.

We maintain programs that offer safety and health and wellness initiatives. We provide competitive pay and employee benefits, routinely benchmarking ourselves against peers and the broader industry.

Training and Development

We routinely create and offer department or job-specific training, professional development opportunities, and leadership development training to meet employees’ needs. Employees have opportunities for various certification levels based on training completed and tenure. We have also developed a management training program and a technician training program to attract talent to the automotive industry. In addition to providing career growth pathways for employees, annually our Board of Directors reviews management’s succession planning for key positions throughout the organization.

Seasonality

Our operating results are generally subject to seasonal variations, as well as changes in the economic environment. In the U.S., we generally experience higher volumes of vehicle sales and service in the second and third calendar quarters of each year. In addition, in some regions of the U.S., vehicle purchases decline during the winter months due to inclement weather. In the U.K., the first and third quarters tend to be stronger, driven by the vehicle license plate change months of March and September. Other factors unrelated to seasonality, such as changes in economic conditions, manufacturer incentive programs, supply issues, seasonal weather events and/or changes in foreign currency exchange rates may exaggerate seasonal or cause counter-seasonal fluctuations in our revenues and operating income.

Internet Website and Availability of Public Filings

Our internet address is www.group1auto.com. We make the following information available free of charge on our website:

•Annual Report on Form 10-K;

•Quarterly Reports on Form 10-Q;

•Current Reports on Form 8-K;

•Amendments to the reports filed or furnished electronically with the SEC pursuant to Section 13(a) or 15(d) of the Exchange Act;

•Our Corporate Governance Guidelines;

•The charters for our Audit, Compensation & Human Resources, Finance/Risk Management and Governance & Corporate Responsibility Committees;

•Our Code of Conduct for Directors, Officers and Employees (“Code of Conduct”);

•Our Code of Ethics for our Chief Executive Officer, Chief Financial Officer and Controller (“Code of Ethics”); and

•Our Sustainability Report.

Within the time period required by the SEC and the New York Stock Exchange, as applicable, we will post on our website any modifications to the Code of Conduct and Code of Ethics and any waivers applicable to senior officers as defined in the Code of Conduct or Code of Ethics, as applicable, as required by the Sarbanes-Oxley Act of 2002. We make our filings with the SEC available on our website as soon as reasonably practicable after we electronically file such material with, or furnish such material to, the SEC. The SEC also maintains a website at http://sec.gov that contains reports, proxy and information statements, and other information regarding our company that we file and furnish electronically with the SEC.

References to the Company’s website in this Form 10-K are provided as a convenience and do not constitute, and should not be deemed, an incorporation by reference of the information contained on, or available through, the website, and such information should not be considered part of this Form 10-K.

Item 1A. Risk Factors

The following risks have had or in the future could have a material adverse effect on our business and results of operations.

Market and Industry Risks

Availability and demand for and pricing of our products and services may be adversely impacted by economic conditions, financial developments including rising inflation, high energy prices, increasing interest rates, a potential recessionary environment and other factors.

The automotive retail industry, and especially vehicle unit sales, is influenced by general economic conditions, particularly consumer confidence, the level of personal discretionary spending, interest rates, exchange rates, fuel prices, technology and business model changes, supply conditions, consumer transportation preferences, unemployment rates and credit availability. Consumer spending can be materially and adversely impacted by periods of economic uncertainty or by consumer concern about manufacturer viability. Increased tariffs may increase inflation, which would likely result in interest rates not decreasing as fast as expected and consumer demand declining as a result of increased costs of vehicle ownership.

The global economy experienced elevated levels of inflation beginning in 2022. In response to higher than historical average inflationary pressures and challenging macroeconomic conditions, the U.S. Federal Reserve (“the Federal Reserve”), along with other central banks, including in the U.K., maintained interest rates at elevated levels throughout 2023. In 2024, inflation began to return to historical norms. As a result, during the Current Year, the Federal Reserve and the Bank of England lowered their interest rates by 100 and 50 basis points, respectively, in an effort to stimulate economic activity and reduce unemployment. The impact of the lowering of interest rates on the levels of inflation and unemployment in the U.S., U.K. and Europe is uncertain. In Europe, rising energy costs as a result of supply disruptions and increased winter demand for heating could place strain on our suppliers’ ability to maintain current production levels of vehicles and vehicle parts. Across the European Union, these energy constraints could result in nations or regions enacting emergency energy related policies, limiting energy availability for manufacturers. The impact of these macroeconomic developments on our operations cannot be predicted with certainty. On January 29, 2025, the Federal Reserve held rates unchanged. On February 6, 2025, the Bank of England lowered interest rates by 25 basis points.

Additionally, President Donald Trump issued a series of executive orders since taking office in January 2025, including executive orders regarding tariffs. Refer to Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations — Recent Events, for additional information regarding these executive orders.

Inflation, increased energy costs and a prolonged recession could adversely impact our operations, the operations of our suppliers and customer demand for our vehicles and services. The risk of slower future interest rate cuts or the maintenance of interest rates at current elevated levels could have a material adverse impact on our interest expense and ability to obtain financing through the debt markets, as well as consumers’ ability to obtain financing for the purchase of new and used vehicles. Refer to Item 7A. Quantitative and Qualitative Disclosures About Market Risk for additional analysis regarding our interest rate sensitivity.

A significant portion of our vehicles purchased by customers are financed. Tightening of the credit markets, increases in interest rates and credit conditions have and may continue to decrease the availability or increase the costs of automotive loans and leases and adversely impact our new and used vehicle sales and margins. In particular, if sub-prime finance companies apply further higher credit standards or if there is a further decline in the overall availability of credit in the sub-prime lending market, the ability of some consumers to purchase vehicles and F&I products could be even more limited, which could have a material adverse effect on our business and results of operations.

In addition, local economic, competitive and other conditions affect the performance of our dealerships. Our results of operations depend substantially on general economic conditions and spending habits in those regions of the U.S. and U.K. where we maintain our operations.

While EV sales continued to increase in the U.S. in 2024, challenges with EV technologies, including the development of the necessary charging infrastructure, continue to make headlines within the U.S. media market, raising concerns around consumer demand and interest in the products. Should EV demand decline at the same time as more OEMs transition to EV models, this could have a material adverse effect on our business and results of operations. In addition, President Donald Trump issued a series of executive orders since taking office in January 2025, including an executive order eliminating the EV mandate. Refer to Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations — Recent Events, for additional information regarding these executive orders.

The U.K. government has established mandated targets for the sale of new zero emissions vehicles with increasing targets in future years. The overall U.K. market fell short of those mandated targets in 2024, with consumer preferences skewed towards traditional internal combustion engine vehicles. The government targets established for 2025 are higher than those previously required in 2024, and are expected to further challenge new vehicle sales in 2025 and beyond. These EV mandates could impact our vehicle manufacturers’ production mix and volumes, which in turn may impact our new vehicle sales and results of operations.

Deterioration in market conditions or changes in our credit profile could adversely affect our operations and financial condition.

We rely on the positive cash flow we generate from our operations and our access to the credit and capital markets to fund our operations, growth strategy, and return of cash to our shareholders through share repurchases and dividends. Changes in the credit and capital markets, including market disruptions, limited liquidity and interest rate fluctuations, may increase the cost of financing or restrict our access to these potential sources of future liquidity. Our continued access to liquidity sources on favorable terms depends on multiple factors, including our operating performance and credit ratings. Our debt securities currently are rated just below investment-grade and a downgrade of this rating likely would negatively impact our access to the debt markets and increase our cost of borrowing. Disruptions in the debt markets or any downgrade of our credit ratings could adversely affect our operations and financial condition and our ability to finance acquisitions or return cash to our shareholders. We can make no assurances that our ability to obtain additional financing through the debt markets will not be adversely affected by economic conditions or that we will be able to maintain or improve our current credit ratings.

Our floorplan notes payable, mortgages and other debt are benchmarked to SOFR, which can be highly volatile as a result of changing economic conditions. Although we utilize derivative instruments to partially mitigate our exposure to interest rate fluctuations, significant increases in SOFR or other variable interest rates could have a material adverse impact on our interest expense due to the significance of our debt and floorplan balances. Refer to Item 7A. Quantitative and Qualitative Disclosures About Market Risk for additional analysis regarding our interest rate sensitivity.

We are subject to risks associated with our dependence on manufacturer business relationships and agreements.

The success of our business is dependent on vehicle manufacturers on whom we rely exclusively on for our new vehicle inventory. Our ability to sell new vehicles is dependent on a vehicle manufacturer’s ability to produce and allocate to our dealerships an attractive, high quality and desirable product mix at the right time in order to satisfy customer demand.

Manufacturers generally support their franchisees by providing direct financial assistance in various areas, including, among others, incentives, floorplan assistance and advertising assistance. A discontinuation or change in our manufacturers’ warranty and incentive programs could adversely affect our business. Manufacturers also provide product warranties and, in some cases, service contracts to customers. Our dealerships perform warranty and service contract work for vehicles under manufacturer product warranties and service contracts and we bill the manufacturer directly, as opposed to invoicing the customer. In addition, we rely on manufacturers for various financing programs, OEM replacement parts, training, up-to-date product design, development of advertising materials and programs and other items necessary for the success of our dealerships.

Vehicle manufacturers may be adversely impacted by economic downturns or recessions, significant declines in the sales of their new vehicles, increases in interest rates, adverse fluctuations in currency exchange rates, declines in their credit ratings, reductions in access to capital or credit, labor strikes or similar disruptions (including within their major suppliers), supply shortages, rising raw material costs, rising employee benefit costs, adverse publicity that may reduce consumer demand for their products, including due to bankruptcy, product defects, litigation, ability to keep up with technology and business model changes, poor product mix or unappealing vehicle design, governmental laws and regulations, natural disasters or other adverse events. In particular, all of our OEMs are investing material amounts to develop electric and autonomous vehicles. These investments could cause financial strain on our OEMs or fail to deliver attractive vehicles for customers which could lead to adverse impacts on our business. The OEMs have been and could continue to be impacted by disruptions to the economy, lower than anticipated EV adoption, higher supply chain costs than emerging EV manufacturer competitors, delays in increasing factory production, labor negotiations, parts shortages, including semiconductor chips, and other disruptions. In the Current Year, a number of OEMs have announced write-offs of certain of their EV investments or scaled down electrification plans as EV demand slows, further contributing to the uncertainty of the EV market outlook and the long-term viability and profitability of OEM’s. These and other risks could materially adversely affect the financial condition of any manufacturer and impact its ability to profitably design, market, produce or distribute new vehicles, which in turn could have a material adverse effect on our business, results of operations and financial condition.

During the Current Year, the majority of our manufacturers’ production increased, driving an improvement in vehicles days’ supply. Our new vehicle days’ supply of inventory was approximately 44 days as of December 31, 2024, as compared to 37 days and 24 days for the years ended December 31, 2023 and 2022, respectively. It is impossible to predict with certainty when normalized production will resume at these manufacturers. If our manufacturers’ production remains at current reduced levels or in some cases continues to decline, diminishing our ability to meet the immediate needs of our customers, the production shortage could have a material adverse impact on our financial and operating results.

Additionally, President Donald Trump issued a series of executive orders since taking office in January 2025, including executive orders regarding tariffs. Refer to Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations — Recent Events, for additional information regarding these executive orders. Many manufacturers of vehicles, parts and supplies are dependent on imported products and raw materials in their production. Any significant increase in existing tariffs on such goods and raw materials, or implementation of new tariffs, could increase production costs for OEM’s that would then be passed on to consumers, potentially leading to higher vehicle prices and reduced demand, which in turn could adversely affect our profits on the vehicles we sell. Additionally, the tariffs and other market developments could potentially cause our current OEM’s to lose market share to emerging EV-only OEM’s. Market share losses could not only impair our sales and profits but lead to potential impairments.

If we are unable to enter into new franchise agreements with manufacturers in connection with dealership acquisitions or maintain or renew our existing franchise agreements on favorable terms, our operations may be significantly impaired.

We are dependent on our relationships with manufacturers, which exercise a great degree of influence over our operations through the franchise and similar agreements. These agreements may be terminated or not renewed by the manufacturer for a variety of reasons, including network consolidation plans, any unapproved changes of ownership or management, sales and customer satisfaction performance deficiencies and other material breaches of the franchise agreements. For example, in the U.K., the Volkswagen Group has disclosed a five-year plan to reduce the number of partners in its dealer network. That plan may require us to dispose of, or close, up to thirteen of our Volkswagen and up to three Audi dealerships. Correspondingly, the plan may require us to purchase dealerships adjacent to our territories. In the U.S., manufacturers may also have a right of first refusal if we seek to sell dealerships. We also cannot guarantee that the terms of any renewals will be as favorable to us as our current agreements. Although we are generally protected in the U.S. by automotive dealership franchise laws requiring “good cause” be shown for such termination, if such an instance occurs, we cannot guarantee that the termination of the franchise will not be successful.

A manufacturer may also limit the number of its dealerships that we may own overall or in a particular geographic area. From time to time, we have not met all of the manufacturers’ requirements to make acquisitions and have received requests from manufacturers to dispose of certain of our dealerships. In the event one or more of our manufacturers sought to prohibit future acquisitions or imposed requirements to dispose of one or more of our dealerships, our acquisition and growth strategy could be adversely affected. Furthermore, if current manufacturers or future manufacturers are not required to conduct their business in accordance with state franchise laws and thereby circumvent the current dealer-network to sell directly to the customer, our results of operations may be materially and adversely affected.

Substantial competition in automotive sales, F&I and services could adversely impact our sales and our margins.

The automotive retail industry is highly competitive. Within our markets we are subject to competition from franchised automotive dealerships and other businesses as it relates to new and used vehicles, F&I, and parts and service. The internet has become a significant part of the advertising and sales process in our industry. Customers are using the internet to compare prices for new and used vehicles, automotive repair and maintenance services, finance and insurance products and other automotive products. If we are unable to effectively use the internet to attract customers to our own online channels, such as our AcceleRide® platform, and mobile applications, and, in turn, to our stores, our business, financial condition, results of operations and cash flows could be materially adversely affected. The use of social media by consumers increases the speed and extent that information and opinions can be shared, and negative posts or comments on social media about the Company or any of our dealerships could damage our reputation and brand names, which could have a material adverse effect on our business, financial condition, results of operations and cash flows.

We also face competition in arranging financing for our customers’ vehicle purchases from a broad range of financial institutions. Additionally, we do not have any cost advantage in purchasing new vehicles from vehicle manufacturers, and our franchise agreements do not grant us the exclusive right to sell a manufacturer’s product within a given geographic area. Subject to state laws in the U.S. that are generally designed to protect dealers, a manufacturer may grant another dealer a franchise to start a new dealership near one of our locations, or an existing dealership may move its dealership to a location that would more directly compete against us. The location of new dealerships near our existing dealerships could have a material and adverse effect on our operations and reduce the profitability of our existing dealerships. Increased competition can adversely impact our sales volumes and margins as well as our ability to acquire dealerships.

Please see Item 1. Business — Competition for further discussion of competition in our industry.

If we are unable to acquire and successfully integrate new dealerships into our business, the growth of our revenues and earnings could be adversely affected.

Growth in our revenues and earnings partially depends on our ability to acquire new dealerships and successfully integrate those dealerships into our existing operations. We cannot guarantee that we will be able to identify and acquire dealerships in the future. In addition, we cannot guarantee that any acquisitions will be successful or on terms and conditions consistent with past acquisitions. Restrictions imposed by our manufacturers, as well as covenants contained in our debt instruments, may directly or indirectly limit our ability to acquire additional dealerships. As competition for acquisitions increases that may result in fewer acquisition opportunities available to us and/or higher acquisition prices, and some of our competitors may have greater financial resources than us.

In addition, acquisitions involve a number of particular risks, including, among other things:

•incurring significantly higher capital expenditures and operating expenses;

•failing to obtain manufacturers’ consents to acquisitions of additional franchises;

•failing to integrate the operations and personnel of the acquired dealerships;

•entering new markets with which we are not familiar;

•incurring undiscovered liabilities at acquired dealerships, generally, in the case of stock acquisitions;

•disrupting our ongoing business;

•failing to retain key personnel of the acquired dealerships;

•failing to implement or improve controls and policies and information systems;

•impairing relationships with employees, manufacturers and customers; and

•incorrectly valuing acquired entities.

The integration process for acquisitions requires us to expand the scope of our operations and financial and other systems. Our management devotes a substantial amount of time and attention to the process of integrating the operations of acquired dealerships into our business. Additionally, the Company doubled its footprint in the U.K. during the Current Year through its acquisition of Inchcape Retail. Failure to effectively integrate the Inchcape Acquisition into the legacy U.K. operations could negatively impact our operating results in the U.K.

If any of these factors limit our ability to successfully integrate acquired dealerships into our operations or on a timely basis, our expectations regarding future results of operations, including certain run-rate revenue and expense synergies expected to result from acquisitions, might not be met. As a result, we may not be able to realize the expected benefits that we seek to achieve from the acquisitions. In addition, we may be required to spend additional time or money on integration that otherwise would be spent on the development and expansion of our business, including efforts to further expand our product portfolio.

Vehicle manufacturers may alter their distribution models.

In 2023, Mercedes Benz transitioned to an agency model for distribution of vehicles in the U.K. after collaborating with various automotive retailers and conducting pilot programs. In addition to the transition by Mercedes Benz in the U.K., certain of our other vehicle manufacturers serving the U.K. and U.S. markets have announced plans to explore an agency model for selling new vehicles. Under an agency model, our franchised dealerships receive a fee for facilitating the sale of a new vehicle to a customer but no longer record the vehicle sales price as revenue, record vehicles in inventory or incur floorplan interest expense, as has been historical practice. The agency model, as adopted by Mercedes Benz, resulted in reduced revenues, as we act as an agent of Mercedes Benz, receiving a commission for each sale and other expense fee support. We did not experience a material negative or positive impact to the U.K. region gross margin and consolidated results of operations as a result of the change to the Mercedes Benz agency model. Notwithstanding this fact, we cannot predict the actions of other manufacturers and whether the agency models proposed by them will have the same terms and conditions as those contracted by Mercedes Benz. The agency model, if adopted by other manufacturers, would reduce revenues with only the facilitation fee recorded as revenue. The other impacts to our U.K. and the U.S. regions and consolidated results of operations remain uncertain until such time as the other vehicle manufacturers provide additional details regarding their specific agency model plans. We are uncertain if agency models will be widely adopted in the U.K. or U.S.

Vehicle technology advancements and changes in consumer vehicle ownership preferences could adversely affect our new and used vehicle sales volumes, parts and service revenues and results of operations.

Vehicle technology advancements are occurring at an accelerating pace. These include driver assist functionality, autonomous vehicle development and rideshare and vehicle co-ownership business models. Many in the automotive industry believe that in the near future vehicles will be available to the automotive consumer at low usage costs, which may entice many vehicle owners, particularly in larger, highly populated areas, to abandon individual car ownership in favor of multiple co-ownership ride-sharing opportunities. Increased popularity in the ride-sharing subscription business model could adversely affect our new and used vehicle sales volumes, parts and service revenues and results of operations.

Operational Risks

We rely on third-party vendors and suppliers for key components of our business.

Many components of our business, including data management, key operational processes and critical customer systems, are provided by or licensed from various third-party vendors and suppliers. In addition, we also rely on third-party vendors to supply key products and services to us and our customers. One or more of these third-party vendors or suppliers may experience financial distress, technology challenges, cybersecurity incidents, staffing shortages or liquidity challenges, file for bankruptcy protection, go out of business, or suffer other disruptions in their business, each of which could affect their ability to serve us and our customers. For example, in June 2024, CDK Global LLC (“CDK”) experienced a cybersecurity event, which resulted in service outages on CDK’s dealers’ systems including our CDK DMS. If any of our vendors or suppliers fail to deliver their products or services for any reason, our business and results of operations and financial condition could be adversely impacted.

A failure of any of our information systems or those of our third-party service providers or a cybersecurity incident, including loss or unauthorized access of confidential information or PII about our customers or employees, could negatively affect our business, operations and financial condition.

We depend on the efficient operation of our information systems and those of our third-party service providers and rely on information systems at our dealerships in all aspects of our sales and service efforts, as well as in the preparation of our consolidated financial and operating data. All of our dealerships currently operate on two DMSs, one DMS for the U.S. and one DMS for the U.K. Additionally, in the ordinary course of business, we receive significant PII about our customers and our employees. PII is primarily collected at our dealerships and through our AcceleRide® platform via an online DMS. A cybersecurity attack to obtain such information could be caused by malicious insiders and third parties using sophisticated, targeted methods to circumvent firewalls, encryption and other security defenses, including hacking, malware, fraud, trickery, or other forms of deception. Although companies across all industries are affected by malicious efforts to obtain access to PII, the automotive dealership industry has been a particular target of identity thieves. The techniques used by cyber attackers change frequently and may be difficult to detect. We have implemented security measures that are designed to detect and protect against cyberattacks, as well as policies governing the deletion of PII, to limit the information exposed to a potential cyberattack.