‘VALUE DRIVEN’ UAB Motors Pending Acquisition Brazil January 25, 2013 Exhibit 99.2 Copyright © 2012 Group 1 Automotive, Inc. All rights reserved. |

2 This presentation contains "forward-looking statements" within the meaning of the Private Securities Litigation Reform Act of 1995, which are statements related to future, not past, events and are based on our current expectations and assumptions regarding our business, the economy and other future conditions. While management believes that these forward-looking statements are reasonable as and when made, there can be no assurance that future developments affecting us will be those that we anticipate. In this context, the forward-looking statements often include statements regarding our goals, plans, projections and guidance regarding our financial position, results of operations, market position, pending and potential future acquisitions and business strategy, and often contain words such as “expects,” “anticipates,” “intends,” “plans,” “believes,” “seeks,” “should,” “foresee,” “may” or “will” and similar expressions. Any such forward-looking statements are not assurances of future performance and involve risks and uncertainties that may cause actual results to differ materially from those set forth in the statements. These risks and uncertainties include, among other things, (a) general economic and business conditions, (b) the level of manufacturer incentives, (c) the future regulatory environment, (d) our ability to obtain an inventory of desirable new and used vehicles, (e) our relationship with our automobile manufacturers and the willingness of manufacturers to approve future acquisitions, (f) our cost of financing and the availability of credit for consumers, (g) our ability to complete acquisitions and dispositions and the risks associated therewith, (h) foreign exchange controls and currency fluctuations, and (i) our ability to retain key personnel. For additional information regarding known material factors that could cause our actual results to differ from our projected results, please see our filings with SEC, including our Annual Report on Form 10-K, Quarterly Reports on Form 10-Q and Current Reports on Form 8-K. Readers are cautioned not to place undue reliance on forward-looking statements, which speak only as of the date hereof. We undertake no obligation to publicly update or revise any forward-looking statements after the date they are made, whether as a result of new information, future events or otherwise. Safe Harbor BMW Londrina Peugeot Sao Bernardo do Campo Group 1 Automotive, Inc. |

Table of Contents I. Transaction Overview II. Brazil Overview III. UAB Overview IV. Summary V. Appendix |

Transaction Overview |

UAB – Pending Acquisition Detail UAB Motors Participações S.A. Acquiring 18 dealerships / 21 franchises and 5 collision centers in Brazil with estimated annual revenues of US$650 million – No property purchases • Sale / Leaseback environment Consideration includes US$47.4 million cash / 1.45 million shares of GPI common stock and the assumption of ~US$62 million of net non- floorplan debt – Common stock priced at US$60.77 per share • Lockup period: 1/3 available annually first 3 years – Group 1 intends to use cash on hand to fund the cash consideration and to payoff the assumed debt Anticipate acquisition being accretive from day 1 – FY2013 ~US$0.03 to US$0.05 EPCS 5 Group 1 Automotive, Inc. |

Why Brazil? 4th Largest new vehicle sales market – 9.1% 5-year CAGR (2007-2012) Vehicles-per-population is one of the lowest in developed markets Highly fragmented, little consolidation – Top 15 auto dealers represent ~19% of the total market Numerous acquisition opportunities Positive economic outlook / significant growth potential Source: ANFAVEA Group 1 Automotive, Inc. Nissan Parque 6 |

Brazil Overview |

8 Brazil – Overview Number of States: 27 Country Dimension: 5.3 million sq mi 7th Largest economy – 2011 GDP: US$2.3 trillion – Real GDP Growth • 2011: 2.7% • 2012E: 0.9% – 5-year projected CAGR: 4.1% 5th Largest population – July 2012 Estimate:199 million – 2012 Estimated Growth: 0.86% – 2030 Estimated: 220 million 4th Largest auto market – 2012 Units sold: 3.8 million • 5-year CAGR: 9.1% – 2013E Unit growth: 3.5% – 4.5% Source: CIA World Factbook, ANFAVEA, and the U.N. Population Fund Group 1 Automotive, Inc. Brasilia Sao Paulo Rio de Janeiro |

9 Why Brazil? Future GROWTH! Brazil new vehicle market growing quickly – Industry sales have grown at a 9.1% CAGR since 2007 and are estimated to increase ~30% over the next five years – Expect new vehicle unit sales of 3.95 million in 2013 • Up ~9% from 2011 – Market growth is over-weighted toward non-Big Four brands in Brazil GDP growth likely to outperform U.S. over next five years – 5-year CAGR: • United States: 2.4% • Brazil: 4.1% Source: ANFAVEA, Roland Berger Strategy Consultants, and the IMF 1. Big Four brands include Chevrolet, Fiat, Ford, and VW (1) Group 1 Automotive, Inc. |

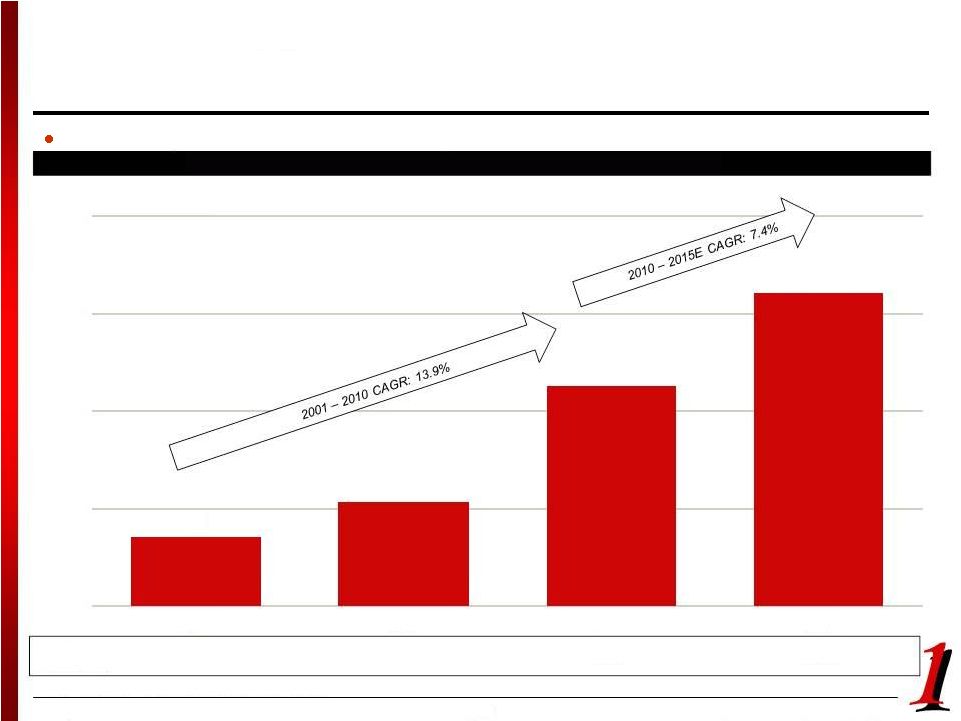

10 Brazil – New Vehicle Unit Sales Source: ANFAVEA (1957 – 2012) and IHS (2014-2020) Group 1 Automotive, Inc. 0.0 1.0 2.0 3.0 4.0 5.0 6.0 New Vehicle Unit Sales 1990: Opening of the Brazilian market to free trade Unit Sales (millions) Main Players 1950 – 1980 |

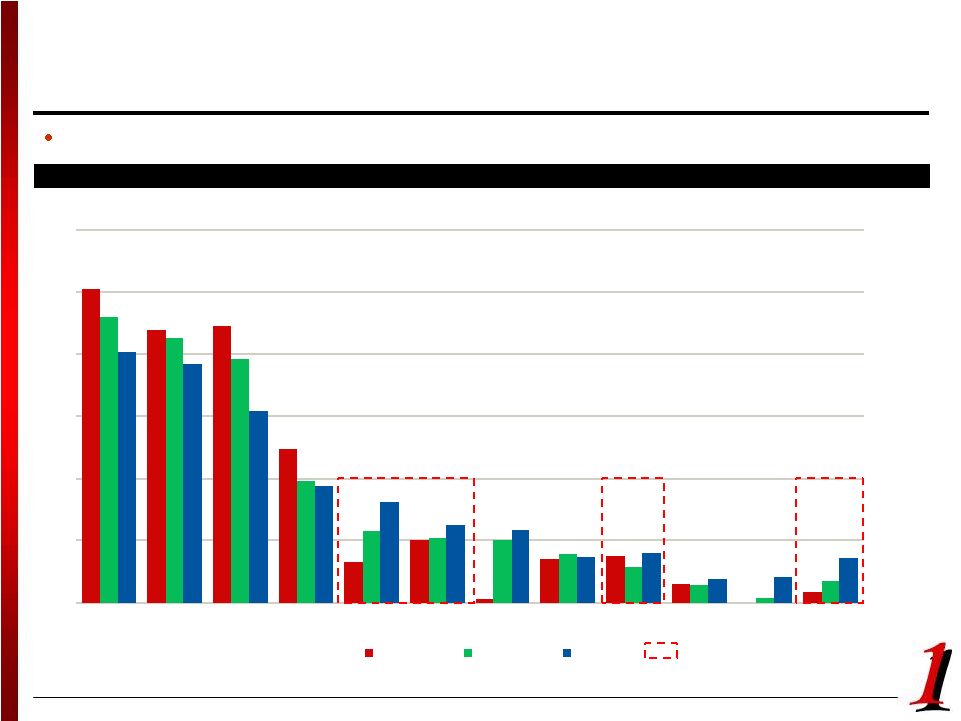

11 Brazil – Auto Industry Dynamics Source: J.D. Power 1. Others includes BMW and Land Rover brands UAB brands expected to gain 6.7% from 2005-2017 at the expense of the Big Four brands 25.2% 21.9% 22.2% 12.4% 3.3% 5.0% 0.3% 3.5% 3.8% 1.5% 0.9% 23.0% 21.3% 19.6% 9.8% 5.8% 5.2% 5.0% 3.9% 2.9% 1.4% 0.4% 1.7% 20.2% 19.2% 15.4% 9.4% 8.1% 6.3% 5.9% 3.7% 4.0% 2.0% 2.1% 3.6% 0% 5% 10% 15% 20% 25% 30% Fiat VW GM Ford Renault Peugeot Hyundai Honda Toyota Mitsubishi Chery Others Market Share 2005 2010 2017E Market Share Evolution UAB brands (1) N/A Group 1 Automotive, Inc. |

12 Overview of Recent IPI Modifications Source: ANFAVEA and news articles Going forward, IPI provides incentives to produce cars in Brazil, which represents a competitive advantage for auto retailers who have the relationships to sell locally-produced brands UAB’s major brands either operate or plan to operate local production facilities – Nissan – Renault early 2013 – Peugeot – Toyota – BMW / MINI IPI: National single-stage VAT-type tax levied on the manufacture of goods in Brazil and the import of goods • The reduction in the IPI tax was announced and originally expected to end by August 2012 • In August, sales reached record high volumes as consumers were afraid that the incentive would not be extended • Reductions were extended to October 31, 2012 Recent IPI News • The IPI tax on imported cars was raised by 30 percentage points across all categories of vehicles produced outside of Brazil, Mercosul, and Mexico to protect the local industry • President Dilma announced that the reduction in the IPI tax will be extended to December 31, 2012 • After the second extension, ANFAVEA expects total sales of 3.67m light vehicles in 2012, 6% higher YoY 2012 May August January October December • 12/31/2012: Govt announced a plan to gradually increase the IPI tax (terminate the reductions) back to pre-reduction levels, by July 2013 December Group 1 Automotive, Inc. IPI Legacy and Consequences : Opening light vehicle manufacturing plant in Resende, RJ in 2014 : Operates automobile manufacturing plant in Porto Real, RJ : Opened automobile manufacturing plant in Sorocaba, SP in 2H 2012 : Operates automobile plant in Curitiba; expanding plant capacity by 100,000 vehicles / year by : Opening automobile manufacturing plant in Joinville, SC in 2014 |

13 Group 1 Automotive, Inc. Brazil – Household Evolution Source: Roland Berger / Automotive Market Outlook Potentially 10 million new customers by 2015 7.0 10.7 22.5 32.1 0.0 10.0 20.0 30.0 40.0 2001 2005 2010 2015E (Households in millions) Households with Spending Power > EUR 11,000 per year Total Households 45.5 52.9 57.3 64.6 |

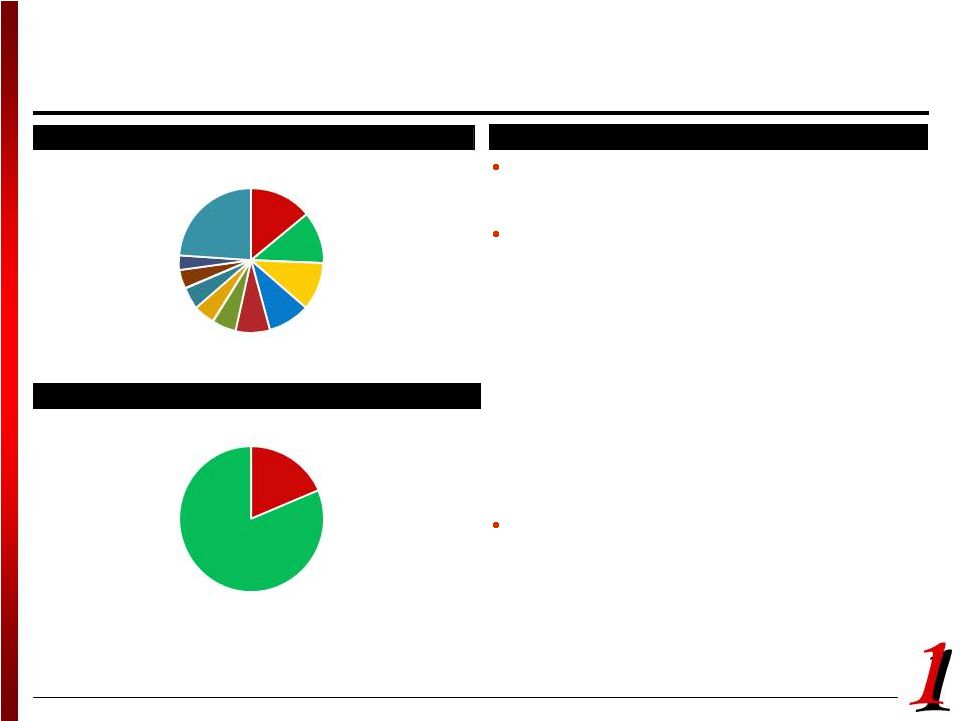

14 Brazil – Future Consolidation Source: ANFAVEA 1. Others include Honda, Iveco, Nissan, Volvo, and Agrate The auto dealerships market is experiencing a transformation, in which monetized players are well-positioned for market consolidation Alternatively, many smaller groups are considering a potential sale due to the following: – Lack of interest to fund and monetize the business in order to adhere to OEM standards – Attractive valuations – Accelerating consolidation movement and size considerations in a sector that will be dominated by larger dealership groups – Opportunity for and willingness of OEMs to rationalize the dealership base The groups are characterized by geographic concentrations – Very few can be considered to have a national presence – Main players have associated themselves with auto assemblers as “exclusive distributors” Group 1 Automotive, Inc. Market Commentary # Dealerships: 3,264 Fiat 14% Ford 11% VW 11% Others 23% Renault 5% Mitsubishi 5% Toyota Mercedes-Benz 5% GM 10% Hyundai 5% Peugeot / Citroen 8% Dealership Breakdown by OEM (2011) (1) Top 15 19% Remaining 81% Number of Dealerships in Hands of Leading Groups (2010) 3% |

15 Group 1 Automotive, Inc. Brazil Economic Outlook Source: ANFAVEA and CIA World Factbook World GDP $1,345 $1,990 $5,862 $0 $3,000 $6,000 $9,000 2000 2010 2030 (US$ in billions) Brazil GDP Evolution 20 38 145 250 262 802 22 43 152 276 289 797 0 300 600 900 India China Brazil Mexico Russia U.S. 2009 2010 Vehicle Ownership in Brazil USA 19% China 14% Japan 6% Others 45% Germany 4% India 6% Russia 3% Brazil 3% China 30% USA 21% India 7% Japan 6% Russia 5% Germany 4% Others 21% Brazil 6% (Cars per 1,000 Inhabitants) World Ranking #9 #8 #4 2030 2011 |

16 Group 1 Automotive, Inc. Brazil vs. U.S. Market Comparison Smaller dealership facilities – Urban locations common – Less outdoor display for new and used vehicles Finance & Insurance is lower – DMV registration process prevents same-day deliveries Lower overall investment in facilities – Typically leased, shorter terms common More volatility in sales rate based on government tax incentives Less sophisticated reporting and management processes Used vehicles have seller warranty by law – restricts type and quality of used vehicles sold by franchised dealers Training and process support Extended warranties and certified pre-owned not common, but increasing Leverage GPI’s proprietary and effective reporting systems to drive operational efficiencies Expanded balance sheet to carry more used car inventory Key Market Differences… …Create Opportunities for Group 1 |

UAB Overview |

18 Group 1 Automotive, Inc. UAB Overview Founded in 1999 Strong, well-respected management team took control in 2005 Management active on dealer councils for all key brands in portfolio 18 Dealerships / 21 Franchises – aligned with brands that are expected to grow market share in Brazil – 4 BMW; 2 MINI; 2 Toyota; 3 Renault; 4 Nissan; 3 Peugeot; 2 Land Rover; 1 Jaguar – 5 Collision Centers Estimated FY2012 new vehicle unit sales ~16,500 No significant capital expenditures required – Major facility improvement program executed during last two years |

UAB Market Overview Sao Paulo Parana Sao Paulo Locations Sao Paulo Sao Jose dos Campos Santo Andre Sao Caetano do Sul Sao Bernardo do Campo Parana Locations Curitiba Londrina Cascavel Located in 2 of the 3 largest sales markets in Brazil – In major cities in the states of Sao Paulo and Parana Group 1 Automotive, Inc. 19 |

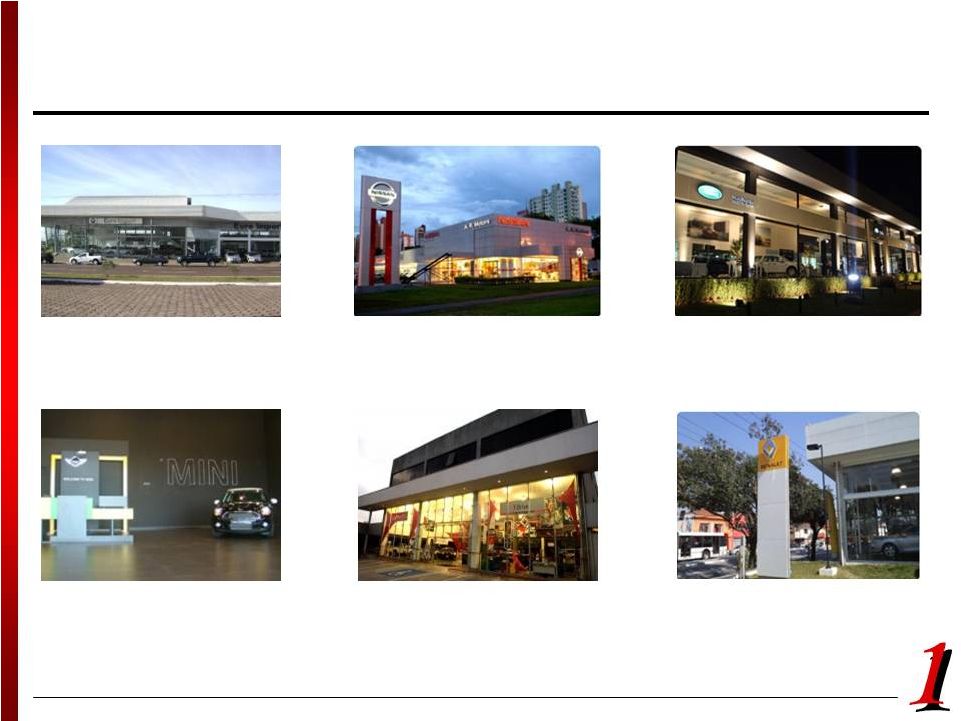

20 Group 1 Automotive, Inc. UAB Dealerships BMW Cascavel Land Rover Curitiba MINI Londrina Nissan Parque Renault Joso Dias Toyota Tatuape |

21 Group 1 Automotive, Inc. Attractive Brand Mix Source: ANFAVEA and UAB UAB brands are well-positioned for growth – One of the largest dealer groups in Nissan and Peugeot – Top-5 dealer group in BMW, MINI and Land Rover – Top-10 dealer group in Toyota and Renault 34% 4% 30% 7% 17% 3% 10% 3% 5% 1% 4% 82% 0% 20% 40% 60% 80% 100% UAB Industry % Mix Nissan Renault Peugeot Toyota BMW / MINI Other UAB vs. Industry New Vehicle Unit Sales 2012E Renault 18% Nissan 28% Peugeot 10% Land Rover 15% Toyota 14% BMW / MINI 15% New Vehicle Brand Mix (2012E Revenues) |

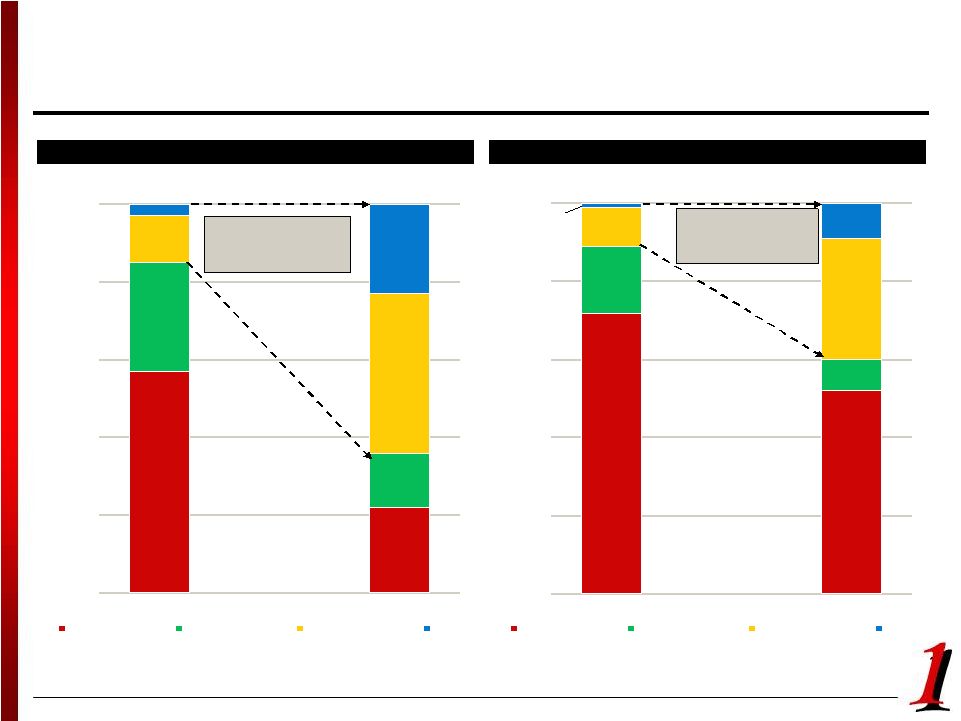

22 Group 1 Automotive, Inc. Business Mix Comparison Source: UAB 57% 22% 28% 14% 12% 3% 23% 41% 0% 20% 40% 60% 80% 100% Revenues Gross Profit % Mix New Vehicles Used Vehicles Parts & Service F&I Group 1 Auto (YTD 9/30/2012) UAB (2012E) 15% of Revenues Generate 64% of Gross Profit 72% 52% 17% 8% 10% 9% 31% 1% 0% 20% 40% 60% 80% 100% Revenues Gross Profit % Mix New Vehicles Used Vehicles Parts & Service F&I 11% of Revenues Generate 40% of Gross Profit |

23 Pro Forma Business Mix Source: UAB Note: Analysis assumes 11/1/2012 Brazilian Central Bank closing exchange rate of 1.00 USD = 2.0312 BRL 1. Group 1 data is LTM 09/30/2012 and UAB data is FY2012E Revenue by Segment (1) New Vehicle Revenue by Brand (1) Group 1 Pro Forma UAB Group 1 Pro Forma UAB = = + + New Vehicle Sales 57% Used Vehicle Sales 28% Parts & Services 12% Finance & Insurance 3% New Vehicle Sales 72% Used Vehicle Sales 17% Parts & Services 10% Finance & Insurance 1% New Vehicle Sales 58% Used Vehicle Sales 27% Parts & Services 12% Finance & Insurance 3% Toyota / Scion / Lexus 29% BMW / MINI 14% Other 48% Nissan / Infiniti 9% Toyota / Scion / Lexus 26% BMW / MINI 15% Other 48% Nissan / Infiniti 11% Nissan / Infiniti 28% BMW / MINI 15% Toyota / Scion / Lexus 14% Other 43% Group 1 Automotive, Inc. |

Summary |

25 What GPI Brings To The Table Capital and floorplan capacity Used vehicle retail sales expertise Parts & service efficiencies Improved finance & insurance processes Advanced technologies Shared best practices Sales and service training Management team with international experience Group 1 Automotive, Inc. |

26 Group 1 Automotive, Inc. Acquisition Timing January 25, 2013 – Form 8-k filed – Slide deck posted to website – Conference call held January – February 2013 – Manufacturer approvals obtained Targeted deal closing on February 28, 2013 January 24, 2013 – Press release issued |

27 Group 1 Automotive, Inc. Conclusion Significant growth opportunities Best-in-class dealership group in the market Highly successful local management team will continue to run business Gives GPI established growth platform Capital, systems expertise, manufacturer relations support from GPI should help drive growth and operational efficiencies Deal should be accretive from day 1 – FY2013 ~US$0.03 to US$0.05 EPCS Expect continued organic growth and expansion in U.S., U.K. and Brazil |

Visit: www.Group1Auto.com CORE VALUES Integrity – we conduct ourselves with the highest level of ethics both personally and professionally when we sell to and perform service for our customers without compromising our honesty Transparency – we promote open and honest communication between each other and our customers Professionalism – we set our standards high so that we can exceed expectations and strive for perfection in everything we do Teamwork – we put the interest of the group first, before our individual interests, as we know that success only comes when we work together |

Appendix |

30 Group 1 Automotive, Inc. Operating Management Team - Corporate Earl J. Hesterberg – President and Chief Executive Officer and Director (April 2005) 35+ Years Industry Experience Manufacturer and Automotive Retailing Experience: Ford Motor Company; Ford of Europe; Gulf States Toyota; Nissan Motor Corporation in U.S.A.; Nissan Europe John C. Rickel – Senior Vice President and Chief Financial Officer (December 2005) 25+ Years Industry Experience Manufacturer and Automotive Retailing Experience: Ford Motor Company; Ford Europe Darryl M. Burman – Vice President and General Counsel (December 2006) 20+ Years Industry Experience Automotive-related Experience: Mergers and Acquisitions; Corporate Finance; Employment and Securities Law – Epstein Becker Green Wickliff & Hall, P.C.; Fant & Burman, L.L.P. Peter C. DeLongchamps – Vice President, Financial Services and Manufacturer Relations (January 2006) 30+ Years Industry Experience Manufacturer and Automotive Retailing Experience: General Motors Corporation; BMW of North America; Advantage BMW in Houston Wade D. Hubbard – Vice President, Fixed Operations (May 2006) 35 Years Industry Experience Automotive Industry Experience: Gulf States Toyota; BMW North America; DaimlerChrysler Corp./Mercedes-Benz; Nissan Motor Corporation USA; Ford Motor Company Mark Iuppenlatz – Vice President, Corporate Development (January 2010) 15 Years Industry Experience Automotive-related Experience: Corporate and Real Estate Development; Construction -Sonic Automotive; REIT J. Brooks O’Hara – Vice President, Human Resources (February 2000) 30+ Years Industry Experience Automotive Industry Experience: Gulf States Toyota |

31 Group 1 Automotive, Inc. Operating Management Team - Field Frank Grese Jr. – Regional Vice President, West Region (January 2006) – 35+ Years Industry Experience – Manufacturer and Automotive Retailing Experience: Ford Motor Company; Nissan Motor Corporation in U.S.A.; AutoNation; Van Tuyl Daryl Kenningham – Regional Vice President, East Region (July 2011) – 20+ Years Industry Experience – Manufacturer and Automotive Retailing Experience: Gulf States Toyota; Nissan Motor Corporation; Ascent Automotive Ian Twinley – Vice President, U.K. Operations – 30+ Years Industry Experience – Manufacturer and Automotive Retailing Experience: John Grose Group; Ford Motor Company Lincoln da Cunha Pereira – Regional Vice President, Brazil – See next slide |

32 Group 1 Automotive, Inc. UAB / Operations Lincoln da Cunha Pereira, 52. Chairman of UAB’s board of directors since October 2007 and legal representative of a public auto group from 1999 to 2005. He incorporated Atrium Telecomunicações in 1999, and entered into an association agreement with JP Morgan Partners, GE Equity and Advent International funds, which was acquired by Grupo Telefônica in December 2004. He began his activities at Cunha Pereira Advogados, where since 1995 he specialized in the management and administration of athletes’ and race car drivers’ careers. He previously worked for Opportunity Asset Management and was the managing director responsible in Brazil for Barclays de Zoete Wedd, the international investment bank of Barclays Group, and has worked for over 10 years at Midland Bank Group (currently HSBC) in different areas, as well as at Banco Bamerindus do Brazil. He is currently the vice-president of the Trade Association of São Paulo (Associação Comercial de São Paulo). He has a Law degree from the Faculdade de Direito do Largo de São Francisco, USP. |