UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

SCHEDULE 14A

(Rule 14a–101)

INFORMATION REQUIRED IN CONSENT STATEMENT

SCHEDULE 14A INFORMATION

Consent Statement Pursuant to Section 14(a) of the Securities Exchange Act of 1934

Filed by the Registrant ¨ Filed by a Party other than the Registrant x

Check the appropriate box:

| ¨ | Preliminary Consent Statement | |

| ¨ | Confidential, for Use of the Commission Only (as permitted by Rule 14a-6(e)(2)) | |

| ¨ | Definitive Consent Statement | |

| x | Definitive Additional Materials | |

| ¨ | Soliciting Material Under Rule 14a-12 | |

PUMA BIOTECHNOLOGY, INC.

(Name of Registrant as Specified in Its Charter)

FREDRIC N. ESHELMAN, PHARM.D.

JAMES M. DALY

SETH A. RUDNICK, M.D.

KENNETH B. LEE, JR.

(Name of Persons(s) Filing Consent Statement, if Other Than the Registrant)

Payment of Filing Fee (Check the appropriate box):

| x | No fee required. | |||

| ¨ | Fee computed on table below per Exchange Act Rules 14a-6(i)(1) and 0-11. | |||

| (1) | Title of each class of securities to which transaction applies:

| |||

| (2) | Aggregate number of securities to which transaction applies:

| |||

| (3) | Per unit price or other underlying value of transaction computed pursuant to Exchange Act Rule 0-11 (set forth the amount on which the filing fee is calculated and state how it was determined):

| |||

| (4) | Proposed maximum aggregate value of transaction:

| |||

| (5) | Total fee paid:

| |||

| ¨ | Fee paid previously with preliminary materials: | |||

| ¨ | Check box if any part of the fee is offset as provided by Exchange Act Rule 0-11(a)(2) and identify the filing for which the offsetting fee was paid previously. Identify the previous filing by registration statement number, or the form or schedule and the date of its filing. | |||

| (1) | Amount previously paid:

| |||

| (2) | Form, Schedule or Registration Statement No.:

| |||

| (3) | Filing Party:

| |||

| (4) | Date Filed:

| |||

FREDRIC N. ESHELMAN

January 4, 2016

Dear Fellow Puma Investors,

I am writing to you, on my own behalf and on behalf of my fellow board slate nominees, to ask for your support in adding four additional members to the current five-member board of Puma Biotechnology Inc. (the “Company”). The current management and board have presided over share price erosion resulting in the loss of thousands/millions of dollars by individual shareholders, and purportedly up to a billion dollars by institutional firms. None of us should tolerate this any longer. Shareholders deserve better.

In our view board enhancement is needed to address several issues:

Lack of Transparency: The current CEO/Chairman, with apparent board acquiescence, has run the Company with a lack of transparency and refusal to respond to legitimate and legal shareholder inquiries.

Misleading Statements: The Company has repeatedly made misleading statements that were subsequently refuted by actual data. This has seriously eroded share price and resulted in huge destruction of shareholder value.

No Evidence of Launch Preparation: The Company claims to be submitting an NDA in Q1 ’16 for use in the adjuvant setting for breast cancer. We have heard nothing about regulatory (e.g., pre-NDA meeting with FDA), manufacturing or commercial activities to support an early Q1 ’17 launch (in the event that the drug is approvable).

Lack of Specific Plans: Ongoing and likely required clinical studies will cost significantly above current cash resources. Analysts’ estimates for equity raises to get to cash flow positive would indicate dilution of $5-10 per share at current prices, with no specific plans for meeting these needs discussed.

Current Board is Unprepared to Deal With Near-term Challenges: Near-term data reveals are mostly complete and the operational and regulatory path forward significantly more complex. The Company will need to develop, and be prepared to execute on, detailed strategies for the commercialization of neratinib. Thus, the task now becomes careful and comprehensive coordination of many activities, and continuous evaluation of strategic options, all of which requires significant time and review by board members.

Please see our updated investor presentation, which is enclosed as an attachment to this letter, in support of our proposals to enlarge the Company’s board from five to nine members and elect myself and three other highly qualified director nominees as directors of the Company.

We are disappointed that ISS and Glass Lewis, while fundamentally acknowledging many of our concerns, concluded that change is not necessary at this time. However, Proxy Mosaic has endorsed our proposal and validated our view that “[t]he Board’s stewardship failures have been directly linked to the Company’s recent devaluation and narrowing prospects.” Proxy Mosaic’s report underscores the fact that “there is a very real danger that [neratinib’s] commercial potential will not be realized due to the Board’s mismanagement… The timing of Dr. Eshelman’s campaign could not be better.” Further, Proxy Mosaic affirmed that “the additional directors would have a strong positive effect on overall oversight and accountability, neither of which appear to be particularly valuable commodities for the current Board.”

The Company is at an extremely important point, with regulatory, financing and commercial issues all of critical importance. Our proposal to bring more talent and experience to the board will enhance Puma’s ability to successfully navigate to successful outcomes. We are committed to doing the hard work necessary to restore value for shareholders and potentially benefit patients, rather than simply selling our shares and moving on. I am spending several millions of my own money to try to make this right for all of us.

We are asking that you support our consent solicitation to add very experienced and credentialed nominees to the current board. There is no down side to adding four directors who will provide the Company with the tactical know-how and breadth of experience to address the challenges above.

We would very much appreciate your support.

Sincerely,

/s/ Fredric N. Eshelman

Enclosure: Updated Investor Presentation

Additional Information and Certain Disclosures

Dr. Eshelman is the beneficial owner of 150,000 shares of common stock of the Company, representing approximately .5% of the Company’s outstanding shares, based upon the 32,435,748 shares of common stock reported by the Company to be outstanding as of November 2, 2015 in its Quarterly Report on Form 10-Q filed with the Securities and Exchange Commission (the “SEC”) on November 9, 2015.

Dr. Fredric N. Eshelman, James M. Daly, Dr. Seth A. Rudnick and Kenneth B. Lee, Jr. (collectively, the “Participants”) have filed a definitive consent statement and accompanying form of consent card with the SEC to be used in the connection with the solicitation of consents (the “Consent Solicitation”) from the stockholders of Puma to increase the size of the Company’s board of directors from five to nine members and elect four new directors. Stockholders of the Company should read the definitive consent statement and other documents related to the Consent Solicitation because they contain important information, including additional information related to the Participants and a description of their director or indirect interests by security holdings. The definitive consent statement and accompanying consent card have been furnished to some or all of the Company’s stockholders and are, along with other relevant documents, available at no charge on the internet at www.okapivote.com/pumabiotechnology or on the SEC’s website at http://www.sec.gov/. In addition, Okapi Partners LLC, Dr. Eshelman’s consent solicitor, will provide copies of the definitive consent statement and accompanying consent card without charge upon request by calling (877) 869-0171 or by emailing info@okapipartners.com.

Investor Inquiries:

Okapi Partners LLC

Bruce Goldfarb / Pat McHugh / Lydia Mulyk

(212) 297-0720 or (877) 869-0171

info@okapipartners.com

Media Inquiries:

Finsbury

Kal Goldberg/ Chuck Nathan / Chris Ryall

(646) 805-2000

kal.goldberg@finsbury.com

charles.nathan@finsbury.com

chris.ryall@finsbury.com

PUMA BIOTECHNOLOGY, INC. CONSENT SOLICITATION Information for Investors January 2016 |

Certain Disclosures 2 DR. FREDRIC N. ESHELMAN (“DR. ESHELMAN”) DOES NOT ASSUME RESPONSIBILITY FOR INVESTMENT DECISIONS. THIS PRESENTATION DOES NOT RECOMMEND THE PURCHASE OR SALE OF ANY SECURITY. UNDER NO CIRCUMSTANCES IS THIS PRESENTATION TO BE USED OR CONSIDERED AS AN OFFER TO SELL OR A SOLICITATION OF AN OFFER TO BUY ANY SECURITY. IT IS POSSIBLE THAT THERE WILL BE DEVELOPMENTS IN THE FUTURE THAT CAUSE ONE OR MORE OF THE PARTICIPANTS FROM TIME TO TIME TO SELL ALL OR A PORTION OF THEIR SHARES IN OPEN MARKET TRANSACTIONS OR OTHERWISE “INCLUDING VIA SHORT SALES), BUY ADDITIONAL SHARES (IN OPEN MARKET OR PRIVATELY NEGOTIATED TRANSACTIONS OR OTHERWISE) OR TRADE IN OPTIONS, PUTS, CALLS OR OTHER DERIVATIVE INSTRUMENTS RELATING TO SUCH SHARES. DR. ESHELMAN RESERVES THE RIGHT TO CHANGE ANY OF HIS OPINIONS EXPRESSED HEREIN AT ANY TIME AS HE DEEMS APPROPRIATE. DR. ESHELMAN DISCLAIMS ANY OBLIGATION TO UPDATE THE INFORMATION CONTAINED HEREIN. CERTAIN DATA AND INFORMATION USED IN THE ACCOMPANYING ANALYSES CONTAINED HEREIN HAS BEEN OBTAINED FROM SOURCES THAT DR. ESHELMAN BELIEVES TO BE RELIABLE, IS SUBJECT TO CHANGE WITHOUT NOTICE, IS NOT GUARANTEED TO BE ACCURATE, AND MAY NOT CONTAIN ALL MATERIAL INFORMATION CONCERNING THE SECURITIES WHICH MAY BE THE SUBJECT OF THE ANALYSES. DR. ESHELMAN HAS NOT SOUGHT OR OBTAINED CONSENT FROM ANY THIRD PARTY TO USE ANY STATEMENTS OR INFORMATION INDICATED IN THIS PRESENTATION AS HAVING BEEN OBTAINED OR DERIVED FROM STATEMENTS MADE OR PUBLISHED BY THIRD PARTIES. ANY SUCH STATEMENTS OR INFORMATION SHOULD NOT BE VIEWED AS INDICATING THE SUPPORT OF SUCH THIRD PARTY FOR THE VIEWS EXPRESSED HEREIN. DR. ESHELMAN MAY HAVE RELIED UPON CERTAIN QUANTITATIVE AND QUALITATIVE ASSUMPTIONS WHEN PREPARING THE ANALYSES HEREIN WHICH MAY NOT BE ARTICULATED AS PART OF SUCH ANALYSES. THE REALIZATION OF THE ASSUMPTIONS ON WHICH SUCH ANALYSES WERE BASED IS SUBJECT TO SIGNIFICANT UNCERTAINTIES, VARIABILITIES AND CONTINGENCIES AND MAY CHANGE MATERIALLY IN RESPONSE TO SMALL CHANGES IN THE ELEMENTS THAT COMPRISE THE ASSUMPTIONS, INCLUDING THE INTERACTION OF SUCH ELEMENTS. FURTHERMORE, THE ASSUMPTIONS ON WHICH THE ANALYSES WERE BASED MAY BE NECESSARILY ARBITRARY, MAY BE MADE AS OF THE DATE OF THE ANALYSES, DO NOT NECESSARILY REFLECT HISTORICAL EXPERIENCE WITH RESPECT TO SECURITIES SIMILAR TO THOSE THAT MAY BE CONTAINED IN THE ANALYSES, AND DO NOT CONSTITUTE A PRECISE PREDICTION AS TO FUTURE EVENTS. BECAUSE OF THE UNCERTAINTIES AND SUBJECTIVE JUDGMENTS INHERENT IN SELECTING THE ASSUMPTIONS ON WHICH THE ANALYSES WERE BASED AND BECAUSE FUTURE EVENTS AND CIRCUMSTANCES CANNOT BE PREDICTED, THE ACTUAL RESULTS REALIZED MAY DIFFER MATERIALLY FROM THOSE PROJECTED IN THE ANALYSES. NOTHING INCLUDED IN THESE ANALYSES CONSTITUTES ANY REPRESENTATION OR WARRANTY BY DR. ESHELMAN AS TO FUTURE PERFORMANCE. NO REPRESENTATION OR WARRANTY IS MADE BY DR. ESHELMAN AS TO THE REASONABLENESS, ACCURACY OR SUFFICIENCY OF THE ASSUMPTIONS ON WHICH THE ANALYSES WERE BASED OR AS TO ANY OTHER FINANCIAL INFORMATION THAT IS CONTAINED IN THE ANALYSES, INCLUDING THE ASSUMPTIONS ON WHICH THEY WERE BASED. DR. ESHELMAN SHALL NOT BE LIABLE FOR EITHER (I) ANY ERRORS OR OMISSIONS MADE IN DISSEMINATING THE DATA OR ANALYSES CONTAINED HEREIN OR (II) DAMAGES (INCIDENTAL, CONSEQUENTIAL OR OTHERWISE) WHICH MAY ARISE FROM YOUR OR ANY OTHER PARTY’S USE OF THE DATA OR ANALYSES CONTAINED HEREIN. THE INFORMATION THAT IS CONTAINED HEREIN SHOULD NOT BE CONSTRUED AS FINANCIAL, LEGAL, INVESTMENT, TAX, OR OTHER ADVICE. YOU ULTIMATELY MUST RELY UPON YOUR OWN EXAMINATION AND THAT OF YOUR PROFESSIONAL ADVISORS, INCLUDING LEGAL COUNSEL AND ACCOUNTANTS AS TO THE LEGAL, ECONOMIC, TAX, REGULATORY, OR ACCOUNTING TREATMENT, SUITABILITY, AND OTHER ASPECTS OF THE ANALYSES HEREIN. ON NOVEMBER 18, 2015, DR. ESHELMAN, JAMES M. DALY, SETH A. RUDNICK AND KENNETH B. LEE, JR. (TOGETHER WITH DR. ESHELMAN, THE "PARTICIPANTS") FILED A DEFINITIVE CONSENT STATEMENT AND ACCOMPANYING FORM OF CONSENT CARD WITH THE SECURITIES AND EXCHANGE COMMISSION (THE “SEC”) ON SCHEDULE 14A TO BE USED IN CONNECTION WITH THE SOLICITATION OF CONSENTS (THE “CONSENT SOLICITATION”) FROM THE STOCKHOLDERS OF PUMA BIOTECHNOLOGY, INC. (THE "COMPANY") TO INCREASE THE SIZE OF THE COMPANY’S BOARD OF DIRECTORS FROM FIVE TO NINE MEMBERS AND ELECT FOUR NEW DIRECTORS. ALL STOCKHOLDERS OF THE COMPANY ARE ADVISED TO READ THE DEFINITIVE CONSENT STATEMENT AND OTHER DOCUMENTS RELATED TO THE CONSENT SOLICITATION BY THE PARTICIPANTS BECAUSE THEY CONTAIN IMPORTANT INFORMATION, INCLUDING ADDITIONAL INFORMATION RELATED TO THE PARTICIPANTS AND A DESCRIPTION OF THEIR DIRECT OR INDIRECT INTERESTS BY SECURITY HOLDINGS. THE DEFINITIVE CONSENT STATEMENT AND ACCOMPANYING CONSENT CARD HAVE BEEN FURNISHED TO SOME OR ALL OF THE COMPANY'S STOCKHOLDERS AND ARE, ALONG WITH OTHER RELEVANT DOCUMENTS, AVAILABLE AT NO CHARGE ON THE INTERNET AT WWW.OKAPIVOTE.COM/PUMABIOTECHNOLOGY OR ON THE SEC'S WEBSITE AT HTTP://WWW.SEC.GOV/. IN ADDITION, OKAPI PARTNERS LLC, DR. ESHELMAN'S CONSENT SOLICITOR, WILL PROVIDE COPIES OF THE DEFINITIVE CONSENT STATEMENT AND ACCOMPANYING CONSENT CARD WITHOUT CHARGE UPON REQUEST BY CALLING (877) 869-0171 OR BY EMAILING INFO@OKAPIPARTNERS.COM. |

Bottom Line: Accountability for Management 3 Management actions have resulted in individual stockholders losing millions of dollars, and institutional losses of up to a $1 billion. Stockholders should hold management accountable. “Management Team’s Business Execution Talent Less Than Oustanding … there is the long list of issues associated with neratinib in the extended adjuvant setting from the erroneous trial design, to the several global amendments (first altering the ExteNET follow- up from 5 years to 2 years and then reinstating the follow-up back to 5 years), and the misguided attempt to pursue approval in the extended adjuvant setting ahead of the metastatic setting. Moreover, there are the significant delays between times data readouts are announced to be reported and when they are actually reported, the numerous half-truths hidden in the transcripts of the public conference calls with analysts, and the constant management allusions that PBYI will eventually be sold at a substantial premium as was the case with Cougar Biotechnology, a company previously owned and sold for a significant profit by Alan Auerbach, the CEO of PBYI. Overall, these events are representative of a management team that appears inexperienced and driven by hubris. Their conduct has undoubtedly compromised the interests of the company’s shareholders.” -P. Arora, Seamist Capital, reported in Seeking Alpha. |

Proxy Mosaic Supports Our Campaign Leading proxy advisory firm Proxy Mosaic has come out in support of our approach to restoring stockholder value: 4 “[T]he Company’s focus on three-year relative performance ignores the net effect of recent comments issued by management, which caused the market to substantially raise its expectations for Puma, only to reverse course when the Company’s statements proved to be optimistic.” (p. 13) “The true value in Dr. Eshelman’s nominees is that they possess the range of skills necessary to oversee any of the strategies that the Company could employ going forward” (p. 16) “The Board’s stewardship failures have been directly linked to the Company’s recent devaluation and narrowing prospects… there is a very real danger that its commercial potential will not be realized due to the Board’s mismanagement… The timing of Dr. Eshelman’s campaign could not be better…” (p. 27) “[T]he additional directors would have a strongly positive effect on overall oversight and accountability, neither of which appear to be particularly valuable commodities for the current Board.” (p. 27) “We recommend shareholders return the WHITE consent card.” (p. 28) |

Reaction to ISS and Glass Lewis The recent recommendations by ISS and Glass Lewis also validated many of our concerns: 5 “[T]he dissident’s assertion that Puma’s board composition is still not optimal may hold some truth.” (ISS, page 3) “[I]nvestors may be appropriately concerned about the company’s recent trajectory.” (ISS, page 13) “Share price returns over the past year has been significantly worse than that of its peers… the recent significant decline in the Company’s share price is hardly ideal.” (Glass Lewis, page 9-10) “[W]e agree with the Dissident, at least to some extent, that the Company could do a better job of setting more realistic expectations for its clinical trials.” (Glass Lewis, page 10) However, we disagree with the view that change is not “necessarily warranted at this time" and “is not prudent at this stage” – at this critical juncture, Puma needs an infusion of expertise. |

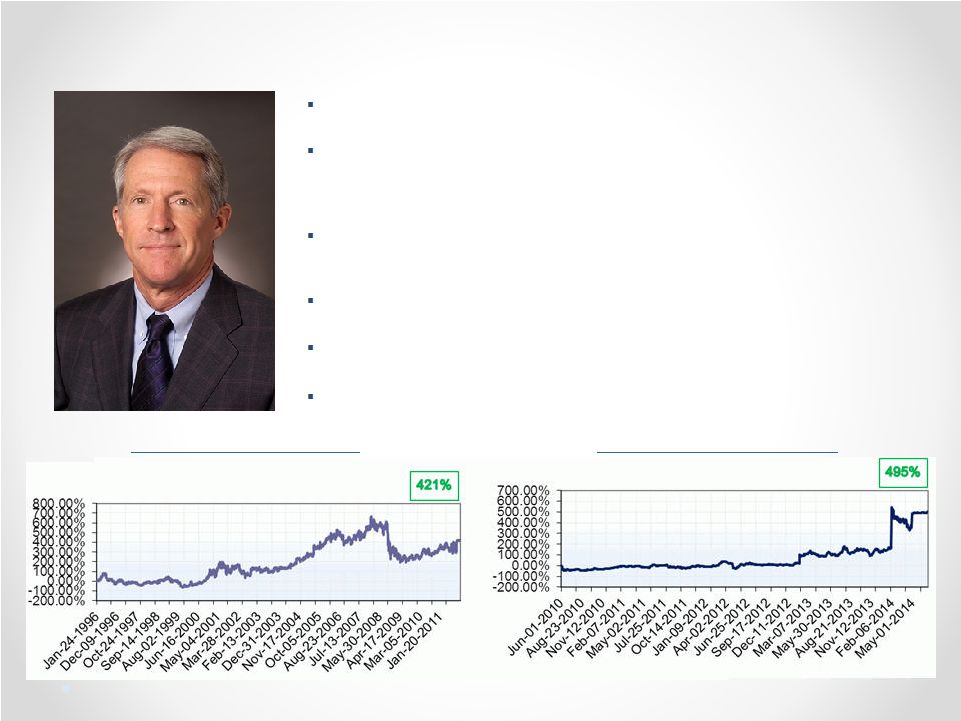

Founder of Eshelman Ventures, LLC, an investment company primarily focused on healthcare companies. Non-Executive Chairman of The Medicines Company, a global biopharmaceutical company focused on saving lives, alleviating suffering and contributing to the economics of healthcare by focusing on the leading acute and intensive care hospitals worldwide. Founder and former CEO and Executive Chairman of Pharmaceutical Product Development, Inc. (“PPDI”), a global contract pharmaceutical research organization. Founding Chairman of Furiex Pharmaceuticals, Inc. (“Furiex”), a company that licensed and rapidly developed new medicines. Former director and Senior Vice President, Development of Glaxo, Inc., predecessor to GlaxoSmithKline plc. Education: Pharm.D., University of Cincinnati; B.S., UNC-Chapel Hill. Fredric N. Eshelman, Pharm.D. 6 PPDI: Total Shareholder Return Furiex: Total Shareholder Return |

Background Of Investment 7 • Between May 18, 2015 and June 4, 2015, I purchased a total of 150,000 shares of Puma’s common stock. • Between October 22, 2015 and November 3, 2015, I acquired options to purchase 150,000 shares of Puma’s common stock. • Currently, I am the beneficial owner of 150,000 shares, representing approximately .5% of Puma’s common stock, after the options expired worthless on December 18, 2015. • Meanwhile, over the last two years, current directors and officers have collectively engaged in net aggregate sales of stock valued at a total of approximately $18,761,916.57. 1. Source: Transactions listed in Participant Transaction Chart on page 44 of the Company’s Definitive Consent Revocation Statement. filed on December 10, 2015. Calculations based on closing price for the date of sale listed. 1 |

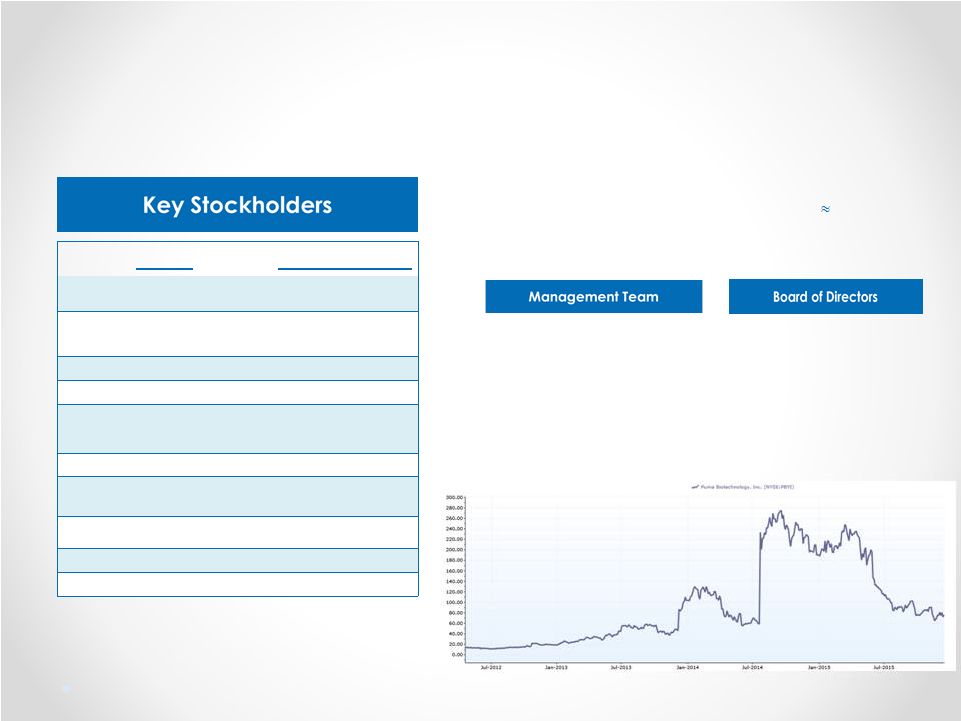

Company Overview Puma Biotechnology, Inc. (NYSE: PBYI) (“Puma” or the “Company”), a Delaware corporation and development stage biopharmaceutical company, focuses on the acquisition, development and commercialization of products for the treatment of various forms of cancer. 8 Name % Outstanding Adage Capital Management LP 17.5% Fidelity Management & Research Co. 14.9% Alan H. Auerbach 12.5%* The Vanguard Group, Inc. 5.5% Capital Research & Management Co. (Global Investors) 5.4% T. Rowe Price Associates, Inc. 5.3% Grantham, Mayo, Van Otterloo & Co. LLC 5.2% Orbimed Advisors LLC 3.7% Franklin Advisers, Inc. 3.0% Frank Zavrl 2.8% • Alan H. Auerbach – CEO and President • Richard Bryce – SVP, Clinical Research and Development • Charles R. Eyler – SVP, Finance and Administration and Treasurer • Alan H. Auerbach – Chairman • Jay M. Moyes • Adrian M. Senderowicz • Troy E. Wilson • Frank E. Zavrl • Headquarters: Los Angeles, CA • Full-time Employees (12/31/14): 120 • • Closing price (12/22/15): $73.72 per share * Excludes 2,116,250 shares exercisable pursuant to anti-dilutive warrant and options to purchase 399,999 shares exercisable within 60 days of April 17, 2015. Sources: Capital IQ; SEC Filings; Bloomberg; NASDAQ. Amounts as of September 30, 2015 unless otherwise indicated. Calculation of percentage outstanding assumes 32,435,748 shares outstanding as of November 2, 2015, as reported in Form 10-Q filed on November 9, 2015. |

Single Drug Candidate Neratinib/PB272 (oral): treatment of breast cancer patients and exploratory studies in other tumors. • Puma presented three-year data from the ExteNET trial of neratinib on December 11, 2015 at the San Antonio Breast Cancer Symposium (“SABCS”). • The two-year data from the ExteNET trial will form the basis of the Company’s new drug application (“NDA”) which, according to management, will be filed with the FDA in Q1’ 2016, according to management. NDA filings are an onerous and complicated process that require significant expertise and experience. • Previous data releases from the ExteNET trial have been the main driver of Puma’s stock value, and the latest data release was no exception. This data will be analyzed in more detail to follow. Company Overview 9 Source: SEC filings Source: Puma website. |

Why Am I Soliciting Consents? 10 Board and management practices are reducing stockholder value. • Stock price underperformance relative to the biotechnology industry and the Company’s closest peers over the most recent six-month and one-year periods. Stockholders have been whipsawed in both directions by management; we have seen significant stock volatility over the last six to nine months. • History of mismanaging market expectations, including making problematic statements and not meeting announced targets or milestones relating to clinical trials. • Stockholder unfriendly executive compensation practices. • Board and management unresponsive and not transparent - my requests for Company documents, including board minutes, through 220 demands under Delaware Corporate Law, were denied after repeated requests. I had to file suit in Delaware to obtain requested stockholder information that is readily available to companies and that I am entitled to as a shareholder. Nominees would add unique expertise and bring a more stockholder-friendly perspective. • Highly qualified and experienced slate of nominees will add value to the board without replacing current directors. • Improved oversight of management in executing Puma’s value proposition and in navigating assets through the regulatory process. • Initiatives to improve transparency for Puma’s investors. • Major near-term clinical data events are over. Now it is a story of regulatory and commercial expertise and experience, which our slate will provide. |

Consent Solicitation Overview 11 |

Consent Solicitation Goals • Increase the size of Puma’s board from five to nine directors. • Elect four highly qualified and experienced directors. • No incumbent directors will be replaced. • The Nominees will each add unique expertise and experience to ensure a successful strategy for navigating the development and regulatory process, and ultimately, a strategy for bringing valuable drugs to market. 12 |

Consent Solicitation Proposals • Proposal 1: Repeal Amendments to the Bylaws o Adoption of Proposal 1 will ensure that the current board cannot (i) prevent or impair the stockholders’ ability to add the Nominees to the Board or (ii) limit the Nominees’ ability to take actions in the best interests of the Company and its stockholders, if elected. • Proposal 2: Removal of Directors o Adoption of Proposal 2 will remove any additional directors appointed after September 9, 2015 and prior to the effectiveness of Proposal 2, but will not remove any current directors. • Proposal 3: Increase the Size of the Board o Adoption of Proposal 3 will increase the size of Puma’s board from five to nine directors. • Proposal 4: Election of the Nominees o Adoption of Proposal 4 will elect the Nominees to serve as directors of the Company. o Stockholders may consent to the election of all or some of the Nominees. 13 |

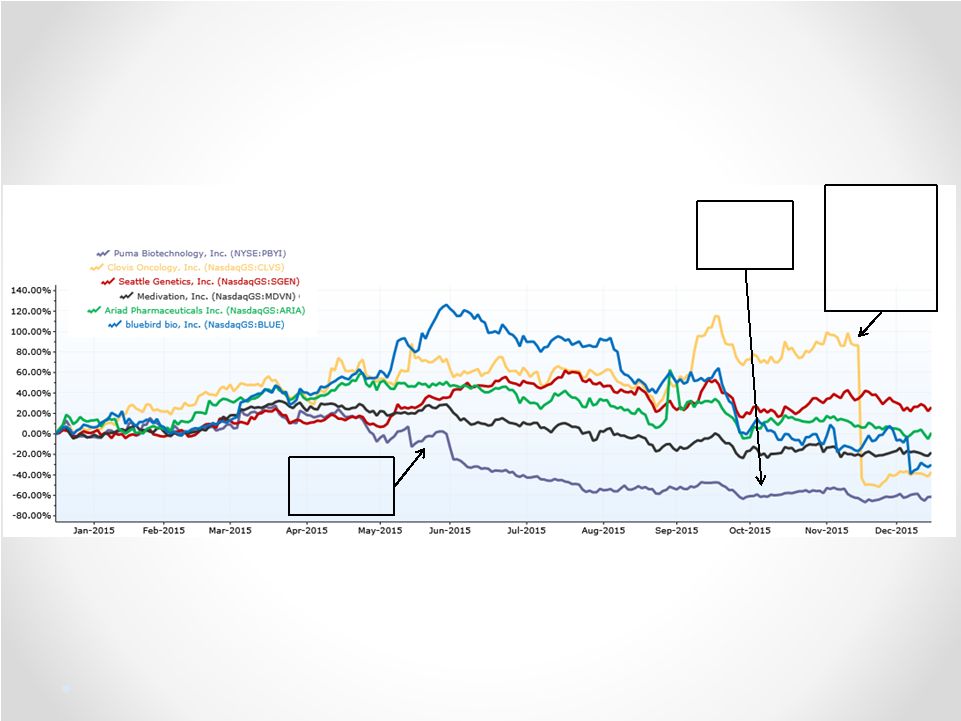

Dramatic Stock Price Underperformance Puma shares have significantly underperformed the S&P 500 and NYSE Arca Biotechnology Index. 14 Source: Capital IQ While the Company has performed generally in line with peers since its IPO in 2012 and outperformed last year due to management description of forthcoming trial results and heightened expectations, since disappointing data was released in June 2015 at the at the American Society of Clinical Oncology (“ASCO”) annual meeting, the Company has underperformed and we believe that value will continue to be destroyed if there is no change in the status quo. Preliminary Consent Solicitation Filed Dr. Eshelman Initial Investment Initial 220 Demand |

Dramatic Stock Price Underperformance Puma has also significantly underperformed its closest peer companies. 15 Source: Capital IQ Sharp fall in Clovis stock due to prematurely announcing drug responses which, subsequently, were not confirmed. Preliminary Consent Statement Filed Dr. Eshelman Initial Investment |

16 History of Problematic Statements: Background ExteNET Trial Description • Started by Pfizer Inc. in April 2009. • Enrolled 2,840 patients in 41 countries. • Double-blind, placebo-controlled, Phase III trial of neratinib vs. placebo after adjuvant treatment with trastuzumab (“Herceptin”) in women with early stage HER2+ breast cancer. • After one year of adjuvant treatment with Herceptin, patients were randomized 1:1 to receive extended adjuvant therapy with neratinib or placebo for one year. • Patients were then followed for recurrent disease, ductal carcinoma in situ or death for a period of two years after randomization into ExteNET, or three years since the initial start of Herceptin. Primary Trial in Support of Q1’16 NDA |

History of Problematic Statements: Optimistic Statements by Puma 17 “The results of the trial demonstrated that treatment with neratinib resulted in a 33% improvement in disease free survival versus placebo.” – Puma Press Release, July 22, 2014 “We saw a 33% improvement in invasive disease-free survival.” - Puma Conference call, May 7, 2015 “Most importantly, a number of those subgroups are extremely differentiating from the other HER2 agents that are commercially available.” “So, I think there is certainly the opportunity for the drug to be used in all patients directly after treatment in year one with Herceptin.” –Puma Conference Call, July 22, 2014 Analysts’ high expectations followed: Beginning on July 22, 2014, and continuing until as late as May 7, 2015, Puma claimed that the ExteNET data would show that neratinib significantly improves results in breast cancer patients over a placebo. We spoke to Puma about the upcoming abstracts… In addition to what is already known, the abstract from the ph3 ExteNET trial will include the actual 2yr DFS values, and key subset analyses that will show neratinib forms well in populations typically challenging for Perjeta and Kadcyla. - UBS, May 4, 2015 “We see upside potential at ASCO, where we think ExteNET data will show well.” - UBS, May 5 2015 Given prior comments from PBYI, investors had expectation of at least a 3% absolute benefit, and perhaps a benefit as high as 4-5%. - Cowen and Company, May 13, 2015 We continue to expect the ExteNET data in Chicago to show the 3+% difference between the two arms… We see a low probability of any negative data surprises…” - RBC Capital Markets, May 11 2015 |

History of Problematic Statements: Impact On Puma’s Stock Price • July 22, 2014 closing price: $59.03. Following market close the Company issued a press release and held a conference call announcing two-year results from the ExteNET trial. • July 23, 2014 closing price: $233.43. • Stock reached its historical high of $270.83 per share on September 12, 2014. 18 “Puma Biotechnology Inc. soared after the company yesterday reported positive trial results for its breast cancer drug… Puma shares almost quadrupled…” -Bloomberg, July 23, 2014 Source: Capital IQ Jul. 22 Release of Positive ExteNET Results Jul. 23 closing price- $233.43 Sept. 12 All-time High June 1 ASCO Presentation |

History of Problematic Statements: Clinical Trial Data Inconsistent With Expectations 19 “[T]he absolute magnitude of difference in DFS was ‘trivial.’ Neratanib’s use is likely to be limited to a small subset…” Cowen and Company, May 21, 2015 Between May 13, 2015 and June 1, 2015, Puma released additional ExteNET data, which was presented at the ASCO annual meeting. The newly released ExteNET data did not meet analyst’s high expectations. “[T]he point estimate at the 2yr landmark is below the 3pp delta set by investors… One can debate the expectation management… We recognize anger about expectations coming in.” “Most investors and oncologists had approximated the minimum delta between the two arms to be about 3% in order to achieve meaningful clinical significance. On its face, the 2.3% IDFS difference falls below expectations… it is not surprising why the stock is down 25%...” RBC Capital Markets, May 14, 2015 UBS, May 13, 2015 |

20 While the Company continued to tout the success of the ExteNET trial at the June 2015 ASCO meeting, significant portions of the analyst, investor, and medical communities saw the data and clearly disagreed. Puma’s stock price plummeted. History of Problematic Statements: Clinical Trial Data Inconsistent With Expectations We believe that the market reacted primarily to management’s failure to provide a clear explanation of what investors could expect from the ExteNET data. With the release of the three-year data, the Company had an opportunity to learn from its past mistakes. It could have pursued a more transparent and realistic approach to managing expectations about the data. Instead, the current management chose to confuse the situation. ASCO Presentation “[W]e view the sell off as more of a reaction to falling short of misguided expectations rather than a fatal flaw in neratinib’s clinical profile. The absolute treatment benefit over placebo (2.3%) was materially below where management had implied when topline data were first released in July 2014.” -J.P. Morgan, August 27, 2015 |

All of These Statements Cannot Be True 21 Q: “And you noted that the FDA is not going to ask for any more data from ExteNET. But you’re now essentially a year since you actually hit the two-year. So a year from now you’re going to be the two-year, so you’re going to be—“ A: “… [A]s we mentioned on the call when we did for announcing the ExteNET data, the curves are continuing to separate. So that obviously would strengthen the data set.” -12/2/2014 Conference Call Q: “And then on to San Antonio, you mentioned the three-year analysis. Do you plan to show just the three-year curves or should we look for data to go further out than 3 years?” A: I would ideally like to be able to show Kaplan-Meier curve that don't just truncate at 36 months. How much more, I don't know the answer to you yet because the data is still blinded. We have not unblinded it yet, so I don't know the answer to that yet. Clearly, the key is going to be what the number of patient at risk is. If it's just that the cut we took, we didn't get a lot of patients out further than if you're down to 50 patients or something toward the 40-, 42-month period that that would be obviously something of concern. I don't think that's going to happen. I think we should be able to show somewhere in between 36 months and 48 months. I just can't give you any exact numbers right now. -11/30/2015 Conference Call Q: “Alan, in terms of the 2-year disease-free survival endpoint, if you don’t need further data, why was the protocol restored and the mandate to improve 5-year results?...” A: “[W]hen we were first giving guidance in what we expected the trial results to show… What we said that well, we expect the curves to be separating, but we don’t think they’d be statistically significant by two years. So they were meant—because we anticipated that the two-year would show a trend, but the five-year would actually be what would be statistically significant. Obviously, we are pleased that the curve separated enough to be positive at the two-year. But it was originally restored because we thought the curves would be trending by two years, but not near positive.” - 6/2/15 Conference call Q: “[C]an you give us a sense as to whether the separation is widening over time or how would you describe the curve separation?” A: “…If we look at curves going out beyond [two years]… it looks like the curves are continuing to separate... [I]f you look at curves in the Herceptin adjuvant trials, so the HERA study, the BCIRG study, et cetera, the absolute difference in disease-free survival increases as you go out year-over- year... So, for instance, in the BCIRG trial, the DFS difference was 6% at two years, then 7% at three years, then 8% at four years, et cetera, et cetera. We’re seeing the same preliminary trend in the ExteNET trial where the curves appear to be continuing to separate as you go out year- over-year, and the absolute DFS difference is increasing year-over-year as well.” - 7/22/201414 Conference Call Mr. Auerbach made numerous statements before December 2015 about the ExteNET data, including claims that the DFS curves were separating beyond the two-year data. Yet, less than two weeks before the three year data was presented, Auerbach claimed that he could not tell investors what data would be presented at SABCS, as the data was still blinded. When did Puma see the DFS data for years 3-5? If the data was blinded, what was the basis for Auerbach’s previous statements? If the statements were based on the data, why did Puma claim that it was blinded and avoid being transparent with investors? |

December 11, 2015: Another Missed Opportunity 22 The actual two and three-year results differed materially from guidance given by management prior to release. While the stock price has rebounded, share prices are still down more than 60% over the last five quarters, erasing billions of dollars in stockholder value. 2015 SABCS has done nothing to improve the Puma’s position or solve any of its problems. When the three-year ExteNET data was finally released, the curves did not separate. DFS results in all indications decreased from Year 2 to Year 3, other than HER2+/HR+ results, which were not meaningful. *Subsequently changed to 2.5% based on additional data. 12/11/2015 SABCS: Stock drops as much as 22%, closing down almost 6% Year 2 Year 3 Indication Absolute Difference in DFS Absolute Difference in DFS Primary 2.3%* 2.1% Centrally Read HER2+ 4.1% 2.2% HER2+/HR+ 4.2% 4.3% Centrally Read HER2+ and HR+ 8.6% 6.4% The market has spoken loudly about its lack of confidence in current management. |

History of Problematic Statements: Regulatory Plan and Cancer Indication 23 Source: Capital IQ “Yes, we are still planning to file the NDA for the ExteNET Study in the first half of 2015.” - Alan Auerbach, Conference Call, November 13, 2014 “Since the Company’s initial NDA filing will now be for the extended adjuvant HER2-positive early stage breast cancer indication… Puma intends to delay its proposed timeline for filing the NDA until the first quarter of 2016.” - Puma Press Release, December 2, 2014 ExteNET is not an aberration - management has a history of mismanaging market expectations. • For example, Puma stated on several occasions, including as late as November 13, 2014, that it would file an NDA for neratinib during the first quarter of 2015. • Less than three weeks later, on December 2, 2014, Puma pushed the projected date of its NDA filing to the first quarter of 2016. 12% Decline • Puma may claim that the delay was due to the FDA’s requirement that the Company file carcinogenicity data, and that it had no control. • We believe that the company should have known that this data would be required because filing for a long-term indication always requires this data. • We believe that Puma mismanaged the regulatory process. |

History of Problematic Statements: Other Trials 24 The Company held a conference call on December 23, 2013 to discuss HER2 mutation trials. • We have tried to locate the transcript but have been unable to do so. As far as we can tell, the transcript seems to be missing and unavailable. However, according to reports written by at least two analysts about the call: • With respect to the refractory NSCLC trial, Mr. Auerbach stated that response rates in both arms of the trial were in the 40-49% range. • Data released on September 9, 2014 was not consistent with the earlier statement (N=27). NERAT NERAT + TORISEL Partial Response 0 3 (21%) Stable Disease 7 (54%) 11 (79%) Clinical benefit 4 (31%) 9 (64%) |

History of Problematic Statements: Public Disclosures & Drug Development Process 25 Clinical Trials • Equivocating on the extent of data to be presented in December 2015 on ExteNET and other trials. Public Filings • In its S-1/A filed on October 17, 2012, the Company outlined its business strategy: S-1/A Strategy Current Status An Investigational New Drug Application (“IND”) would be filed for the IV form of neratinib in 2013. The Company has not filed an IND for the IV form of neratinib. The Company would in-license additional compounds. The Company has not licensed any additional compounds. ExteNET trial would be wound down. Important data from the ExteNET trial was only released in December 2015. Compound PB357 would be evaluated for further development in 2013. 2013 10-K: “We are evaluating PB357 and considering options relative to its development in 2013.” 2014 10-K: “We are evaluating PB357 and considering options relative to its development in 2014.” 2015 10-K: “We are evaluating PB357 and considering options relative to its development in 2015.” |

Failure to Address Key Issues: Tolerability Profile Crucial Issue • If two or three patients out of every ten are affected, neratinib has a major problem. • With approximately 2% DFS, MDs must treat 50 patients to benefit one, while treating just three patients will impair the quality of life in one. • Failure to significantly reduce grade 3 diarrhea or perceived diminished DFS benefit over time will result in a major reduction in addressable population. Severe diarrhea was evident with neratinib even in the early PFE data. • Why didn’t Puma incorporate protocol amendments much earlier for grade 3 diarrhea prophylaxis? Why haven’t trials looking at these issues been more rigorous? • On December 11, 2015, Puma released interim results from an open label trial in BC adjuvant patients with varying treatment duration. Of the 72 patients in the trial, only 50 were evaluable (approximately 30% were unevaluable). The loperamide dosage was changed mid study. • The overall results of 16% grade 3 diarrhea were then compared to a table showing a variety of drugs/combinations for more serious indications, not adjuvant, and then attempting to draw comparative conclusions. • This is voodoo science and will not hold up in regulatory or commercial situations. o Stockholders were also unimpressed – Puma’s stock price did not even recover to its level from the previous week . Inconsistent Results • In the NSABP FB-7 trial, three of the four arms that utilized the prophylaxis had significantly higher rates (30%, 35% and 23%). The patients in the cohort of the SUMMIT basket trial presented at SABCS also had a higher rate (35%). 26 Can stockholders rely on current management to handle this issue from either a regulatory or comercial standpoint? |

M&A Speculation 27 There has been speculation regarding M&A for quite some time. Analysts have also commented: Cowen 5/5/15: “..[F]uture stock performance appears increasingly dependent on M&A, an outcome we have little visibility on.” “Puma management has acknowledged that a sale of the company may be the optimal way to maximize shareholder value and allow neratinib to realize its full potential…In our view, Puma is likely to generate significant acquisition interest...” “[O]ur optimism for an M&A exit is somewhat tempered by the fact that [Puma] has been investigating a potential sale for several months...” UBS 5/4/15: “We reiterate our Buy rating and see Puma as a prime acquisition candidate.” Interestingly, right around the early May timeframe, the SVP of BD left the Company. UBS 5/20/15: “Will Puma be acquired? We have felt that there isn’t a rush to acquire until the calendar flips to 2016 so that it’s dilutive only for one year and carc/filing is de-risked. That said, one reason to move sooner rather than later is to execute on the long-duration trials to max out the tail potential. CVRs may be acceptable to reflect upside sales optionality.” However, a company must always be run under the assumption that there may never be an M&A offer that fully reflects value and is in the best interest of shareholders. |

Stockholder Discontent 28 “Auerbach and Eyler received nearly $22.3 million in salary and incentive-based annual compensation in 2014 alone, all materially enhanced as a result of deceiving the investing public...” -Stockholder Consolidated Complaint, October 16, 2015 • A stockholder class action complaint was filed on June 3, 2015 in the U.S. District Court for the Central District of California against Puma, Alan Auerbach and Charles Eyler. • In the complaint, the stockholder plaintiffs alleged violations of federal securities laws, including claims under Sections 10(b) and 20(a) of the Exchange Act, stemming from Defendants’ allegedly problematic statements and failure to disclose material adverse facts regarding the results of the ExteNET trial and the efficacy of neratinib. • The plaintiffs allege that the defendants, including Auerbach and Eyler, “engaged in a scheme to deceive investors and the market and a course of conduct that artificially inflated the price of Puma stock and operated as a fraud or deceit on Class Period purchasers of Puma stock by misrepresenting and omitting material information about neratinib…” • The outcome of the stockholder litigation is currently pending. The Company’s problematic statements have already led some stockholders to take legal action. |

Stockholder Unfriendly Executive Compensation 29 • Compensation is excessive and not aligned with stockholder interests. • No formula based incentive plan (noted by ISS and Glass Lewis). • Equity plan is dilutive. See Appendix A for more details |

Failure to Respond to 220 Demand Puma’s current board and management are not sufficiently committed to transparent disclosure or responsive to legitimate stockholder concerns. • In July 2015, I exercised my right as a stockholder under DGCL Section 220 to request copies of the Company’s board minutes. o My request was narrowly tailored for the purpose of enabling me to analyze and value my ownership stake. o The Company engaged in a pattern of delays and requested additional time to respond. o Eventually, the Company claimed that it is under no obligation to comply based on its belief that I did not have a legal basis for the request. o I strongly disagree with their position and I provided a valid purpose for the requested materials. • On October 29, 2015 and concurrent with the launch of this consent solicitation, I delivered a second request to inspect the Company’s stockholder lists pursuant to DGCL Section 220. o Initially, the Company provided limited information purportedly in satisfaction of the request, and only committed to provide all of the legally required documents after I filed suit in the Delaware Courts. 30 The Company’s response reflect the board’s lack of transparency and an unwillingness to respond to the legitimate concerns of stockholders. |

Value Proposition |

Value Proposition And Caveats 32 Potential Value • Depending on how various indications for use are valued commercially, and the assigned probability of technical and regulatory success, Puma shares may yet offer investors a value proposition. • However, we do not see any path back to previous prices (>$250) and unlikely that much over $100 per share is attainable. This view is shared in recent analysts’ reports with the exception of one who appears to be close with management. M&A rumors have swirled around the Company as far back as 2013. • As recently as 14 December 2015, RBC said that “We view an acquisition by a big biopharma as the most likely outcome. ” In the same report, they cut their price target from $285 to $103. • In August 2015 JPM said, “….we believe there are too many cards left to be unturned for a suitor to pull the trigger right now.” While some of the cards were revealed at the SABCS, generally investors were disappointed and the stock fell again. • Since management has a history of making misleading and problematic statements not backed up by actual data, any company having a look at Puma would undoubtedly conduct rigorous and lengthy due diligence. Even then it is improbable that any binding offer would be made ahead of FDA and EMEA submissions, as well as waiting to be sure that regulatory authorities would actually file the Applications. It is just too tight to rely on M&A as a strategy with a Q1 ’16 NDA submission and a potential launch early Q1 ’17. Therefore, massive regulatory, manufacturing and commercial efforts must be underway now to meet the proposed launch date. |

Extended Adjuvant Claim Puma says it will submit a US NDA Q1 ’16 for use of neratinib in the extended adjuvant setting based on the results of the ExteNET Trial. They indicate that FDA will evaluate the NDA based on two-year DFS as the protocol primary endpoint. Recently, however, management did waffle about not having heard from FDA about the possibility of needing five-year data. We have concerns about the viability of this plan: Trial Design: There are many issues associated with the trial: Several protocol changes High dropout/censoring rates, 40% occurrence of Grade 3 diarrhea, Potential unblinding of the trial due to the huge incidence of severe diarrhea in the treatment arm. 33 Small Treatment Effect: • As shown previously, the DFS at 3 years was down vs. 2-year rates in every subgroup except HR+ (no central read of HER2), and even there the rate change was immaterial (4.2% to 4.3%). No effect was seen in the HR- group. • Many physicians have indicated that the small overall treatment effect at the expense of a high rate of severe diarrhea would not make them inclined to use the drug routinely. |

Extended Adjuvant Claim 34 Much of the residual value still resides in the adjuvant claim, so a rocky road here would change the valuation outlook substantially. Approvability Questions: Management has ballyhooed the DFS effect in the HR+ subgroup, but this was not predefined as the primary endpoint, and thus is unlikely to result in an approval without additional work. • Even if one were optimistic and accepted the likelihood of getting the HR+ claim, this cuts into the overall population in the adjuvant setting, without even considering competitive threats like Perjeta and ONT 380. • JPM was also skeptical about the approval process: “[A]pproval is not a shoe-in by any stretch. We expect the risk-benefit profile will be highly scrutinized by the Agency, especially given the well known GI toxicities.” JP Morgan, Dec. 2015 “We don’t expect the review process to be smooth sailing for neratinib, as we anticipate that it could come under heavy scrutiny” – JP Morgan, Aug. 2015 Lack of Regulatory Preparation: We have heard nothing about a pre-NDA meeting with FDA with respect to the application. A request must be submitted 60 days prior to the meeting, and briefing data must go in 30 days prior to the meeting. So if Puma wants to submit an NDA in Q1 ’16, this request should have already been made in order to provide adequate time to react/modify following the meeting and prior to submission. |

Other Claims for Use The Company’s original strategy was to make metastatic breast cancer the first submitted application. While some information has been released here, there is no body of data that we are aware of that would imply a submission for this indication in the near future. There have also been some off-the-cuff remarks about the possibility of submitting for a neoadjuvant claim. However, recently released data in this setting was disappointing, and RBC removed neoadjuvant from their valuation model. Two years ago the Company said, “Puma’s company goal is clearly to move neratinib into Phase III in the neoadjuvant setting.” (12/4/13) We do not know where this stands. Likewise, other areas such as mutated HER2, CNS metastasis and other solid tumors are supported by very limited data and do not appear to be near-term possibilities. 35 |

Impact of the SABCS Data Release Puma has been spinning the new data as positive due to the increase in DFS for the HER2+, HR+ subset. We have several concerns about this proposed strategy: • Regulatory: The FDA may not allow the Company to use ExteNET subgroup analysis as the basis for an NDA approval because it was not the pre-selected primary endpoint. • Market Share: Even in the best case scenario, the HER2+, HR+ centrally confirmed subset is not large enough to support the type of sales that would be necessary to justify the Company’s current market cap. If the approval is limited to a series of small subsets, it will be very difficult for a small company like Puma to execute a commercialization plan. • Sales: Building a sales force a serious challenge that could create significant operating losses in the future. • Partnerships: Any attempt to commercialize via partnership will likely harm the Company economically. • M&A: It seems unlikely that there will be any acquirers for Puma until the regulatory situation has been clarified. 36 Puma’s options are becoming more limited and more expensive. High risk from the standpoint of probability of technical and regulatory success, thereby requiring a thoughtful, objective, reality based strategy going forward. |

Overall Position • Here is what JP Morgan had to say in two recent reports (August and December 2015): o “[T]he spotlight will now shift to progress with regulators.” o “[N]eratinib’s commercial prowess remains a major question mark, if it even gets that far.” o “Even if approved, reversing sentiment on neratinib could be a Herculean task.” o “Therefore we believe that Puma faces a daunting task to shift the negative perception of its lead product.” • We agree with all of these statements. As pointed out before, there is no evidence of a comprehensive plan to get the drug approved and positioned correctly, have all of the manufacturing issues dealt with and launch stocks available, and do the upfront commercial work necessary to be ready to launch the drug. • Relying on M&A at an acceptable valuation in the immediate future is a huge gamble, and if it does not happen shareholders will once again be left holding the bag. • Now, more than ever, the Company needs an infusion of highly experienced board members in all aspects of technical/regulatory, commercial, M&A and finance. 37 Shareholders deserve a better shot at restoration and enhancement of value. |

Our Plan to Improve Transparency The Nominees will work with management to improve transparency and manage street and investor expectations, specifically by providing greater clarity with respect to the following issues: • Confirm Q1 ’16 NDA for extended adjuvant and possible neoadjuvant indication. • Address carcinogenicity data if problematic. • Events triggering payments of $187 million milestones due to PFE; cash flow to support R&D going forward, and potential needs for additional financing. • Refine and disclose regulatory and other plans in place in response to ExteNET results, other claims, etc. • Correct any previous problematic statements and improve expectations provided by management going forward. • Make management (as appropriate) other than CEO available on conference calls, meetings, etc. • Give complete outline of ongoing/planned studies, with firm reporting times. • Give complete report of all trial results (or topline at least) ready but heretofore unreleased (Pfizer and Puma). • Show how all of the above line up with commercial expectations and valuations for various indications. • Update on Perjeta and other competitive threats. • PR with oncology community in order to promote better understanding of drug effects and prevention/management of side effects. • Disclose firm, detailed business plan and value enhancing strategy. 38 In this uncertain environment, transparency is especially important for investors. Unfortunately, Puma has lacked transparency in the past. We seek to increase transparency and achieve full value for stockholders. |

Business Initiatives Nominees Plan to Pursue The Nominees have outlined a set of business initiatives that address the following areas that they have identified as critical to their oversight function and a value-maximizing strategy: 39 • While it is difficult to know precisely what actions should be taken without full data access, it is quite clear that an overall comprehensive plan must be adopted and executed expeditiously. • Unfortunately, the current board has not been fully transparent, and has not engaged in public discussion of important issues including: integrating/launching commercial planning, manufacturing/finishing launch stocks of drug, looking at cash flow to support this activity. • The current board has given no indication that such comprehensive planning/implementation has been done. The Nominees are committed to helping Puma develop a comprehensive plan. 1. Regulatory, Clinical and R&D Plan 2. Commercial/Competitive Situation, Label Indications and Valuations, Marketing and Sales Plan Preparatory Activities 3. Manufacturing Considerations 4. Finance and Business Development 5. Investor Relations and Corporate Communications 6. Governance, Management Evaluation, Board Self-Study |

Minority Slate of Highly Qualified Nominees 40 |

Highly Qualified Slate of Nominees The Nominees have the experience and expertise to help guide Puma down the complicated path to a successful launch of neratinib: 41 Dr. Eshelman invested in Puma, undertook this consent solicitation, and assembled an outstanding nominee slate because he believes in the opportunity neratinib presents and is committed to bringing this valuable drug to the market, with the ultimate goal of improving cancer care for patients. • Highly qualified with excellent, relevant track records and significant experience, comparing favorably with current directors. • Proven commitment to enhancing stockholder value and to patient care. • Addition of four new directors brings breadth and depth to the current board of directors. • No incumbent directors will be removed. • Each of the Nominees is independent of Dr. Eshelman and will fulfill their fiduciary duties to act in the best interest of all Company stockholders. |

Optimal Board Size: Nine is Fine Of 31 peer companies identified by either ISS, Capital IQ, or Bloomberg: • Seven peers have boards with nine directors. • Notably, CEO Alan Auerbach sits on the board of Radius Health Inc., which has nine members. Radius Health’s market cap and product pipeline are similar to Puma’s. • 13 peer boards have nine or more members. • NONE of Puma’s peers has a board with fewer than six members. 42 ISS: “A board of between nine and 12 members is considered ideal.” Glass Lewis: “[F]ive directors is almost always a minimum for an effective and properly functioning board.” (2015 Puma Biotechnology Proxy Paper) Council of Institutional Investors Corporate Governance Policies: “[A] board should have no fewer than five and no more than 15 members.” Puma’s current board would have you believe that a five member board “is appropriate for effectively governing the Company” and that the board’s current size “provides for efficient decision-making.” Puma’s claims contradict best practices and industry norms: Best Practices Industry Norms Numerous companies, including Fortune 500 companies, have boards with nine directors: United Natural Foods Inc., Windstream Holdings, Inc., Dr. Pepper Snapple Group, Inc., Lennar Corporation, Laboratory Corp of America Holdings, Cliffs Natural Resources, PulteGroup Inc, Graybar Electric Company Inc. Wynn Resorts, Limited, St. Jude Medical, Inc., Asbury Automotive Group, Big Lots, Inc., Tractor Supply Company, Insight Enterprises Inc., Quintiles Transnational Holdings Inc., Joy Global Inc., Lorillard, Inc., Sanmina, First American Financial Corporation, Avery Dennison Corporation, Allergan Inc., Omnicare Inc., Dick’s Sporting Goods, NCR Corporation, Waste Management, Inc., PPG Industries Inc., Marathon Oil Corporation, Casey’s General Stores, Inc., Agilent Technologies Inc., Symantec Corporation, HollyFrontier Corporation, PBF Energy Inc., Kohl’s Corporation, AbbVie Inc, Vertex Pharmaceuticals Incorporated, Clovis Oncology, Inc., Tesoro Corporation, ARIAD Pharmaceuticals, Inc., Dynavax Technologies Corporation, Lexicon Pharmaceuticals, Inc., Seattle Genetics, Inc., Tesaro, Inc., World Fuel Services Corporation, INTL FCStone Inc., Best Buy Co. Inc, Reliance Steel & Aluminum Co., Stryker Corporation, Cognizant Technology Solutions, Ball Corporation, Broadcom Corporation, CenterPoint Energy, Franklin Resources, Inc., Oaktree Capital Group LLC, Jarden Corporation, Mohawk Industries, Inc., UGI Corporation, The Pantry, Inc., Tyson Foods Inc., Jabil Circuit, Inc., AutoNation Inc., Lear Corporation, Automatic Data Processing Inc., Liberty Interactive Corporation, Ameriprise Financial, Inc., Centene Corporation, Huntsman Corporation, Devon Energy Corporation, Publix Super Markets, Inc., Tech Data Corporation, RiteAid Corporation, National Oilwell Varco, Inc., Xerox Corporation, Arrow Electronics, Gentherm Inc., Cree, Inc Belden Inc., Eastgroup Properties Inc., La-Z-Boy Inc., Amphenol Corporation, CVR Energy Corp, International Bancshares Corp. 1-800-Flowers.com Inc. |

Current Board’s Lack Of Experience Puma claims that the current board members “posses a well diversified range of experience” and the current board “has the experience necessary to guide the Company through the next stages of its development.” • The current board has limited public company corporate governance and oversight experience: o The current board has collectively only served on 6 public boards other than Puma. • Of these companies, the five that remain public have a current combined market cap of $3.21 billion, 1 only slightly larger than Puma itself, of which Radius Health, Inc. accounts for $2.63 billion. Their average market cap was only $642.9M. • Mr. Wilson serves on the board of Zosano, Inc. which since becoming public in 2015 is down approximately 75%. • The stock price of Radius Health, Inc., where Mr. Auerbach is a director, fell 11% after the company delayed an NDA filing for “work health balance,” and was down 23% from its peak in July 2015. The Nominees are far more experienced than the current board: • The four Nominees have served on at least 20 public company boards – more than 3x the five current board members. • The four Nominees have served as Chairman or Lead Director on at least 10 public and private company boards – 10x the five current board members. • The four Nominees have at least 110 years of combined relevant industry experience in the pharmaceutical and biotechnology industry as officers and directors – nearly double the five current board members’ purported 60 years of experience. 43 1. All calculations as of November 24, 2015. |

Nominee Experience 44 Puma claims that the Nominees “provide no additional experience or expertise.” In fact, the Nominees will add extensive expertise that the current board lacks: Drug Development and Regulatory Current Board Nominees Auerbach’s experience at Cougar was limited to an in-licensed drug - early development was completed by PFE; Cougar was sold before any NDA filing. Three Nominees have extensive development experience: • Dr. Seth A. Rudnick was responsible for the development and approval of two significant biologicals - alpha interferon and erythopoietin, at Schering Plough/Biogen and Johnson & Johnson, respectively. • Dr. Eshelman has supervised drug development and approvals in many therapeutic areas. • Mr. James M. Daly worked closely on clinical development, regulatory, and oncology pipeline strategy at both Amgen Inc. and Incyte Corporation. M&A Current Board Nominees No one on the current board has M&A experience other than Auerbach, who was involved in the sale of Cougar for $1.1B. Three Nominees have played key roles in large strategic transactions: • Dr. Eshelman’s previous companies combined have sold for approximately $5 billion- more than 5x the value of Auerbach’s previous transaction that Puma touted in its Revocation Statement. • Mr. Kenneth B. Lee, Jr. served as a director for three companies that were sold in transactions with a combined value of approximately $7.8B, and served on the Transaction Committee and Audit Committee of Pozen Inc. during its acquisition of Tribute Pharmaceuticals Canada Inc. o Lee also founded the Center for Strategic Transactions at Ernst & Young LLP. • Mr. Daly played a key role in Amgen’s acquisitions of Micromet and BioVex, both oncology products. Oncology Current Board Nominees The current board members have limited oncology background. All Nominees have significant oncology experience: • Dr. Rudnick is a medical oncologist and completed an oncology fellowship at Yale University. • Daly served as head of Amgen’s oncology business. He oversaw the successful launches of five oncology products and played a key role in two oncology product acquisitions. • Dr. Eshelman has served on the boards of numerous companies that developed oncology products. • Mr. Lee served on the board of an oncology company, OSI Pharmaceuticals, Inc., that had a marketed product and was acquired by Astellas Pharma, Inc. |

Nominee Experience 45 Investment Current Board Nominees Only one current board member has significant investment experience. Three Nominees have significant investment experience focused on breakthrough and early stage companies, at funds with a venture capital model. • Dr. Eshelman: Founder of Eshelman Ventures LLC., a fund managing investments in numerous healthcare companies. • Dr. Rudnick: 15 years of investment experience. Venture Partner at Canaan Partners, led investments in several breakthrough companies, including CombinatoRX, Esperion, Genaiisance Pharmaceuticals and Pozen. • Mr. Lee: General Partner of Hatteras BioCapital Fund., L.P., where he managed portfolios valued at over $200M. Accounting Current Board Nominees No current board members have accounting experience except for Jay M. Moyes, who spent 12 years at KPMG LLP. Mr. Lee spent 28 years at Ernst & Young LLP. • Titles included: Managing Director of Health Sciences Investment Banking Group & Co-Chairman of International Life Sciences Practice. • Strong understanding of GAP and GAAP as applied to life sciences. • Unique experience structuring transactions at ALZA Corporation. Marketing Current Board Nominees No current board members have significant marketing experience. Mr. Daly was responsible for marketing in his role as Chief Commercial Officer at Incyte and during his time at Amgen, where he served as SVP North America Commercial Operations and SVP Global Marketing and Commercial Development. • During Daly’s tenure at Incyte, annual oncology sales increased from $130M to $600M per year, and during his tenure as head of the oncology business at Amgen sales increased from $1B to $4B. |

CAREER HIGHLIGHTS Age: 66 Founder of Eshelman Ventures, LLC, an investment company primarily focused on healthcare companies. Non-Executive Chairman of The Medicines Company, a global biopharmaceutical company focused on saving lives, alleviating suffering and contributing to the economics of healthcare by focusing on the leading acute and intensive care hospitals worldwide Founded and served as CEO and Executive Chairman of Pharmaceutical Product Development, Inc., a global contract pharmaceutical research organization. In 2008, PPD was selected by Forbes for its Platinum 400 list of the best big companies in America and as best-managed company in health care equipment and services. PPD was sold to a private equity consortium for $3.9 billion in December 2011. Served as Founding Chairman and largest shareholder of Furiex Pharmaceuticals, Inc., which licensed and rapidly developed new medicines. Furiex was separated from PPD in a tax-free spin-off in June 2010 and sold to Forest Labs/Actavis for $1.1 billion in July 2014. Served as Senior Vice President, Development of Glaxo, Inc., predecessor to GlaxoSmithKline plc, as well as in various management positions with Beecham Laboratories and Boehringer Mannheim Pharmaceuticals. Served on the executive committee of the Medical Foundation of North Carolina and the Board of Trustees for UNC-Wilmington. In 2011, Dr. Eshelman was appointed by the North Carolina General Assembly to serve on the Board of Governors for the state's multi-campus university system as well as the North Carolina Biotechnology Center. In addition, he chairs the board of visitors for the School of Pharmacy at UNC-Chapel Hill, which was named the UNC Eshelman School of Pharmacy in recognition of his many contributions to the school and the profession. Awards received by Dr. Eshelman include the Davie and Distinguished Service Awards from UNC and Outstanding Alumnus from both the UNC and University of Cincinnati schools of pharmacy, as well as the North Carolina Entrepreneur Hall of Fame Award. FREDRIC N. ESHELMAN, PHARM.D. 46 NOMINEE EDUCATION Received Pharm.D. from the University of Cincinnati, and completed a residency at Cincinnati General Hospital and a B.S. in pharmacy from UNC- Chapel Hill. Dr. Eshelman is a graduate of the Owner/President Management program at Harvard Business School. |

CAREER HIGHLIGHTS Age: 53 Mr. Daly served as Executive Vice President and Chief Commercial Officer at Incyte Corporation, a biopharmaceutical company, from October 2012 until June 2015. Mr. Daly has served as one of Chimerix Inc’s directors since 2014. Prior to joining Incyte, Mr. Daly served as Senior Vice President of North America Commercial Operations and Global Marketing/Commercial Development at Amgen Inc., a global pharmaceutical company, where he was employed from January 2002 to December 2011. Prior to his employment with Amgen, Mr. Daly was Senior Vice President and General Manager of the Respiratory/Anti-infective business unit at GlaxoSmithKline, where he was employed from June 1985 to December 2001. JAMES M. DALY 47 NOMINEE EDUCATION Received a B.S. and an M.B.A. degree from the University of Buffalo, The State University of New York. |

CAREER HIGHLIGHTS Age: 66 Dr. Seth Rudnick has been venture partner and previously general partner at Canaan Partners, a venture capital firm, since 1998, from which he is now retired. Formerly, Dr. Rudnick was the Chief Executive Officer and Chairman of CytoTherapeutics Inc., a company developing stem cell-based therapies. He helped found and served as the Head of Research and Development for Ortho Biotech, a division of Johnson & Johnson focusing on cancer and chronic illnesses. Dr. Rudnick currently serves on the boards of directors of the following privately held biotechnology companies: Envisia Therapeutics, LQ3 Therapeutics, Meryx Pharmaceuticals, for which he serves as Chairman, Liquidia Technologies, Inc., for which he serves as Chairman, and G1 Therapeutics, for which he serves as Executive Chairman. Dr. Rudnick also served on the board of Square 1, a public company until its October 2015 acquisition by Pacific Western Bank. Currently Dr. Rudnick is a Clinical Adjunct Professor of Medicine at University of North Carolina, Chapel Hill. SETH A. RUDNICK, M.D. 48 NOMINEE EDUCATION Received M.D. from the University of Virginia. Completed a residency at Washington University Barnes Hospital and a fellowship in medical oncology at Yale University. Holds a B.A. in history from the University of Pennsylvania. |

CAREER HIGHLIGHTS Age: 67 Managing member of Hatteras BioCapital, LLC and the general partner of Hatteras BioCapital Fund, L.P., a venture capital fund focusing on life sciences companies. Mr. Lee most recently served as managing director of the firm’s Health Sciences Corporate Finance Group. Currently, Mr. Lee serves on the boards of directors of the following publicly held biotechnology companies: Biocryst Pharmaceuticals, Inc. and Pozen Inc., for which he serves as Lead Director, Chairman of the compensation committee and as a member of the audit committee. Mr. Lee also serves on the boards of directors of two private companies, Clinverse, Inc., and Clinipace Worldwide Inc., for which he serves as Chairman, and is a co-founder of the National Conference on Biotechnology Venture. Between 2002 and 2013, Mr. Lee served on the Boards of several public companies: Maxygen, Inc.; OSI Pharmaceuticals, Inc.; CV Therapeutics, Inc.; Abgenix, Inc. and Inspire Pharmaceuticals, Inc. Mr. Lee was formerly national director of the life science practice at Ernst and Young LLP, where he advised biotechnology and pharmaceutical companies throughout the world on a wide range of financial and strategic planning issues. KENNETH B. LEE, JR. 49 NOMINEE EDUCATION Received a B.A. in from Lenoir-Rhyne College and an M.B.A. from the University of North Carolina at Chapel Hill. |

Contact 50 Legal Inquiries: Cadwalader, Wickersham & Taft LLP Richard Brand (212) 504-5757 richard.brand@cwt.com Investor Inquiries: Okapi Partners LLC Bruce Goldfarb/ Pat McHugh/ Lydia Mulyk (212) 297-0720 or (877) 869-0171 info@okapipartners.com Media Inquiries: Finsbury Kal Goldberg/ Chuck Nathan / Chris Ryall (646) 805-2000 kal.goldberg@finsbury.com charles.nathan@finsbury.com chris.ryall@finsbury.com |

Appendix A Executive Compensation 51 |

History of Problematic Statements: Soaring Stock Price & Effect On Executive Compensation While the stock price was high between July 2014 and June 2015, Chairman, President and CEO Alan Auerbach and SVP Finance and Administration and Treasurer Charles Eyler were each rewarded with generous cash and stock bonuses for 2014. 52 In its Proxy statement, filed in April 2015, the Company justified its 2014 executive compensation program on the following factors: • Price of the common stock increased approximately 1,302% between the Company’s initial OTC listing in April 2012 and the end of its 2014 fiscal year. • Price of the common stock increased approximately 83% during the Company’s 2014 fiscal year. • Positive ExteNET results announced by the Company in July 2014. Eyler: • $117,610 cash bonus • Options to purchase 31,500 shares • Total Value: $4,499,559 Auerbach: • $300,000 cash bonus • Options to purchase150,000 shares • Total Value: $17,797,606 Sources: SEC Filings. |

Stockholder Unfriendly Executive Compensation The Company’s overall executive compensation program is excessive, is not aligned with shareholder interests, and does not reflect best practices. Puma’s executive and director compensation levels are excessive. • Alan Auerbach’s total annual compensation for 2014 was almost 8x the ISS peer group median and included an outsized equity award equal to more than 26x his base salary. • Puma’s outside directors each received compensation in excess of $1.175 million for 2014. Failure to implement formula-based incentive plans with objective metrics and goals. • Puma has a discretionary executive cash bonus program and does not use any performance-vesting equity awards for its executives. • Both ISS and Glass Lewis have identified Puma’s executive compensation program as not being linked to performance and concerns with the structure of long-term incentive pay. 53 |

Stockholder Unfriendly Executive Compensation Executive compensation practices that are not consistent with best practices and investor expectations. • Puma only provides its stockholders with an opportunity to vote on its executive compensation program once every three years (triennial say-on-pay). In 2014, only 15.4% of Russell 3000 companies provided triennial votes. • Puma discloses no clawback, anti-hedging or anti-pledging policies. • CEO Auerbach has 280G gross-up protection. Puma’s equity incentive plan is dilutive and expensive. • More than 1/3 of Puma’s stockholders voted against the 2015 and 2014 equity plan proposals to approve additional shares to increase plan capacity. • According to Glass Lewis, the total potential dilution from the plan is 31.97%, while peer average total dilution is 20.41% and the peer median is 18.67%, and the three-year burn rate is more than 2x the peer median rate (5.64% v. 2.80%). ISS calculated the one-year 2014 burn rate at 6.62%. • Glass Lewis calculated the projected annual cost of the plan per employee at more than 22x the peer average, with an annual per employee cost of over $2.5 million. 1. Source: Towers Watson. 54 Puma’s compensation practices reflect a board that is not responsive to shareholder concerns. 1 |